annual report 2014 - 2015 - estia health · annual report 2014 - 2015. we make time to listen...

TRANSCRIPT

Annual Report 2014 - 2015

We make time to listen because we care.

Chairman’s Message 4

CEO’s Message 7

Key Highlights 11

Operating and Financial Review 14

Board of Directors 20

Executive Team 22

Corporate Governance 25

Shareholder Information 31

Financial Report 32

Glossary 109

Our Estia Code 114

CONTENTS

3Left: Ian and Leila, Estia Health CoolarooCover: Shelley and Pat, Estia Health Coolaroo

We do our best to make a difference every day.

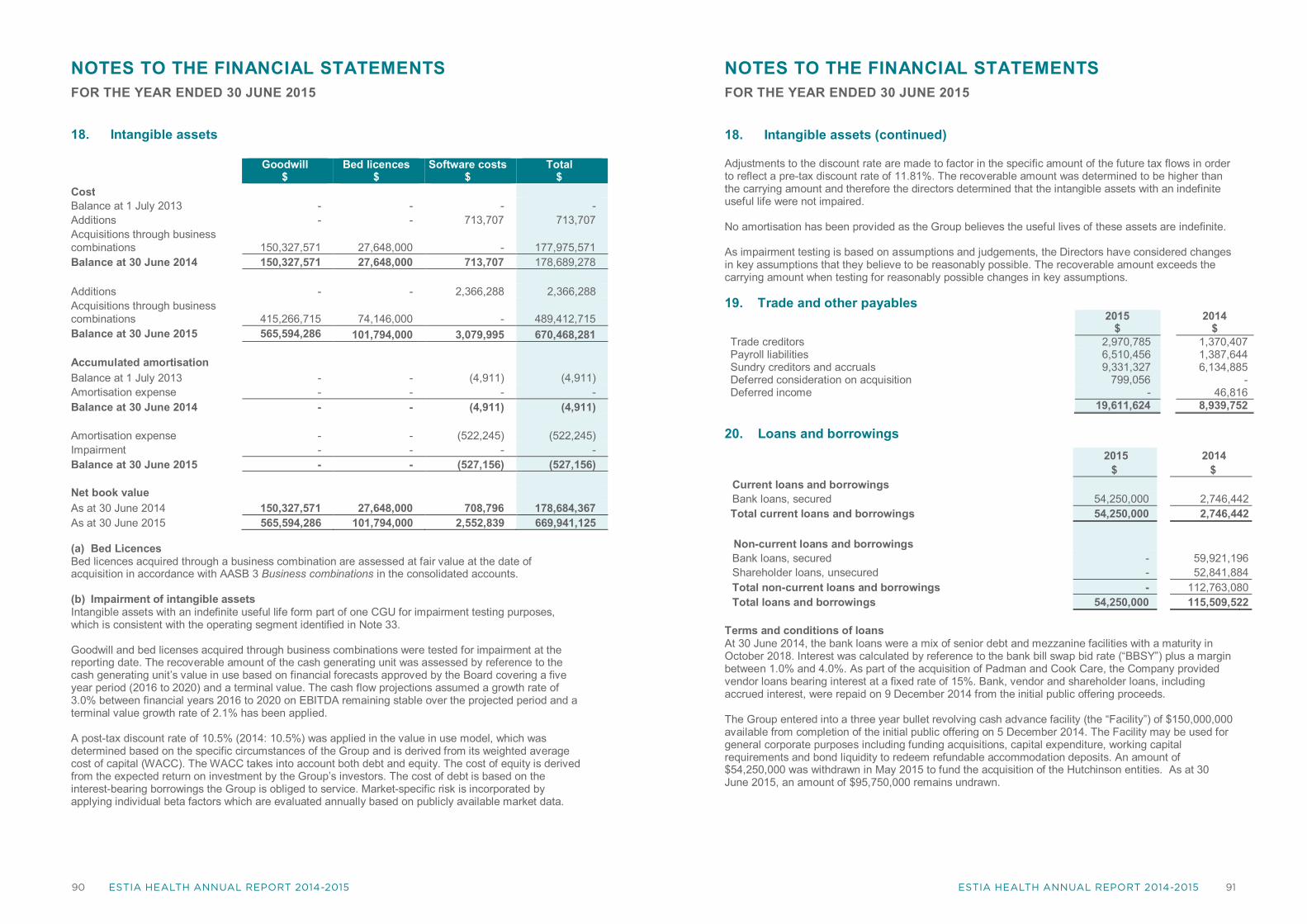

CHAIRMAN’S MESSAGE

It is a pleasure to present to Estia Health shareholders the company’s full-year annual report, our first since debuting on the Australian Securities Exchange on 5 December 2014.

Since the public listing of Estia Health, the company continues to provide consistent, quality levels of care, maintaining a philosophy and way of doing business which will always be at the core of Estia’s operations.

LOOKING AHEADIt is genuinely exciting to be part of a newly formed business that has so much potential in a market that is only going to grow, due to the ageing demographics of Australia’s population and the expected demand for quality aged care facilities.

The aged care sector touches the lives of millions of Australians and the Commonwealth Government’s commitment to older people who need care is demonstrated through the Living Longer, Living Better aged care reforms. As the strong demand for specialised healthcare services increases, Estia is extremely well positioned. We are unique in the market in that 94% of our beds are much sought after single rooms. We have robust systems and networks of facilities already in place to accelerate integration for new acquisitions and manage significant expected growth.

Already, we are a much larger group than initially outlined in the company’s Prospectus. An additional 12 facilities with a total of 1,124 operational places have been acquired since the acquisition of Padman Health Care and Cook Care, taking our total number of operational places to 4,441, as at 12 August 2015.

The company’s medium term plan is to grow the business to 10,000 places by 2020 through acquisition and organic growth. We have a dedicated and skilled workforce of more than 4,700 who have the talent, energy and enthusiasm to reach this goal. As Chairman of a

young company in a fast growing and competitive industry, I look forward to reporting back to shareholders on our progress.

FINANCIAL HIGHLIGHTSWe have experienced a successful first 7 months since listing, and we generated $44.6 million pro forma net profit after tax exceeding our key financial metrics for the financial year ended 30 June 2015.

The Board is pleased to have declared a maiden fully franked dividend of 13.6 cents per share for the financial year ended 30 June 2015, payable on 26 October 2015.

THE BOARD

Your Board is fully committed to the success of Estia Health and to ensuring that business is conducted within the highest standards of corporate governance. We recognise the importance of governance, ethical and social matters, even more so in an industry where the highest quality of resident care goes to the very heart of our existence.

We welcome shareholder questions in writing in advance of our Annual General Meeting on 22 September 2015. I would like to thank all of our people for their daily dedication to providing invaluable care services to the loved ones of so many Australian families.

Pat Grier, Chairman

4 Right: Liu, Estia Health Coolaroo

CEO’S MESSAGE

Undoubtedly, 2014-15 has been an extremely productive period for Estia Health. The highlight was the public listing of the company in December 2014, when we welcomed a number of new investors as shareholders. Since this time, we have acquired a number of new facilities as we progress confidently towards our ambition of reaching 10,000 beds by 2020.

As of 30 June 2015, we have a total of 48 facilities and 4,010 operational places. 94% of these places are single rooms, the most important factor by some margin when it comes to choosing aged care as evidenced through our independent research. As a result, demand for places grew from 92.4% in August 2014 through to 93.6% occupancy level at year end.

Our rapid growth continues: at the time of print, our footprint had increased to 54 facilities and 4,441 operational places.

We are proud to come together as one Estia family. Our ambition is to become ‘the family you choose’.

7

We are one family where everyone belongs.

Left: Enid with Chiko the dog, Estia Health Coolaroo

CEO’S MESSAGE cont.

payment options and location, nearly three quarters of all people surveyed said the #1 decision making factor is access to a single room. With our proportion of single rooms at 94% we have one of the highest quality portfolios in the industry that provides sustainable earnings for the medium term.

In February 2015, we appointed Mark Brandon as Chief Quality Officer on a fixed term contract. Previously CEO of the Australian Government’s Aged Care Standards and Accreditation Agency, Mark is an internationally recognised leader in strategy, quality, accreditation, government relations and organisational transformation. He is busy developing a next generation Quality Management System which will be rolled out across the Estia’s group networks in 2016 to ensure we maintain industry-leading quality standards across the group.

The Government’s Aged Care Funding Instrument (“ACFI”) subsidy for aged care residents was $173 per operating bed day at the year end, an increase of 10.9% over the previous twelve months. Australian Government subsidies also include primary supplements for specific additional support services such as administration of oxygen or enteral feeding. At the year end, 96.5% of all Estia’s residents were receiving high care subsidies.

This funding will continue to underpin Estia’s future revenues as we grow and increase our service offering. Commensurate with this growth is our expanded pool of investable capital through new Refundable Accommodation Deposit (RAD) payments.

STRONG GROWTH MOMENTUMSeveral of the facilities acquired over the past seven months provided opportunities for enhancing quality standards and occupancy levels. These operational improvements are an important component of our strategy of growing both by organic means and through acquisitions.

In reaching our target of 10,000 operated places we will continue to improve and expand our existing facilities. In markets where this ‘brownfield’ expansion is not able to meet strong demand for aged care services and where suitable acquisitions are not available, we will look to develop entirely new ‘greenfield’ facilities. In June, we entered a strategic partnership with Living Choice Australia to develop in excess of 500 additional aged care beds by the end of FY2019. The first two of these developments will be on the Sunshine Coast at Maroochydore and Twin Waters.

This organic growth will be supplemented by further acquisitions which meet our criteria of high standard, single room facilities in attractive locations where we are able to generate value through integration into our networks and systems.

Since the financial year end we have appointed Steven Boggiano as Director of Strategy. Steven is a specialist in mergers and acquisitions with considerable experience and contacts in the Australian health and aged care sector. He will play a vital role in helping us to identify and execute these acquisitions. These may include further standalone facilities or medium to large groups of facilities, as well as strategic alliances with other aged care providers.

LEADERSHIPAs mentioned, we appointed Mark Brandon as Chief Quality Officer in February and Steven Boggiano as Director of Strategy in July. Peter Hamilton, a highly experienced international property and development executive also joined us, appointed to the position of Director of Development in May. These new key appointments will be instrumental in delivering our growth plans and enhancing the quality of the Estia portfolio.

On behalf of the Board, I would like to thank all Estia’s people for their hard work and dedication in helping the company to reach such great heights over the past twelve months.

OUTLOOKThe dynamics of the Australian aged care industry are extremely compelling and the strength of our portfolio puts us in a commanding position to capitalise on new opportunities.

We are confident that we have the right people and systems in place to successfully execute our growth plans, improve returns and create value for our shareholders. I look forward to reporting on our further progress in the year ahead.

Paul Gregersen, CEO

INCREASING CONSUMER CHOICEWhilst it has been a busy year for Estia, at the same time our services and operations are being shaped by the Living Longer, Living Better reforms of 1 July 2014. Today the profile of our residents more commonly reflects a specialised healthcare model. Admission at end of life, with shorter stays and increasing utilisation of Refundable Accommodation Deposits and Combination Payment options to assist with the payment of their stay.

Within this changing market place, and growth in new accommodation payment options, we see the impact of these consumer decisions upon our operating surplus, and an increase in cash receipts. As evidenced by the independent research we commissioned this year, our strong operational performance reflects our substantial single room configuration and operational efficiency as we support increased choice and access to accommodation payments and services for our consumers.

OPERATIONAL OVERVIEWEstia Health was formed on 31 July 2014 through the merger of three residential aged care businesses to create one of the largest private providers of aged care services in Australia. Since then we have expanded our presence in Victoria, South Australia, New South Wales and Queensland, the most populous states, with the acquisition of 12 facilities totalling 1,124 operational places.

The newly acquired facilities have all been successfully integrated into our ten networks with new national IT systems. This incorporates the finance, management information, human resources, time and attendance and clinical care functions in a single, centralised system to deliver efficiency improvements and enhance operational controls.

During the year we commissioned independent market research that identified that room configuration is the most important factor for residents and families in choosing aged care by some margin. Ahead of quality of environment,

At 94%single rooms, we meet consumer needs today and for the medium term future given that single rooms are the

#1choice driver

8 9

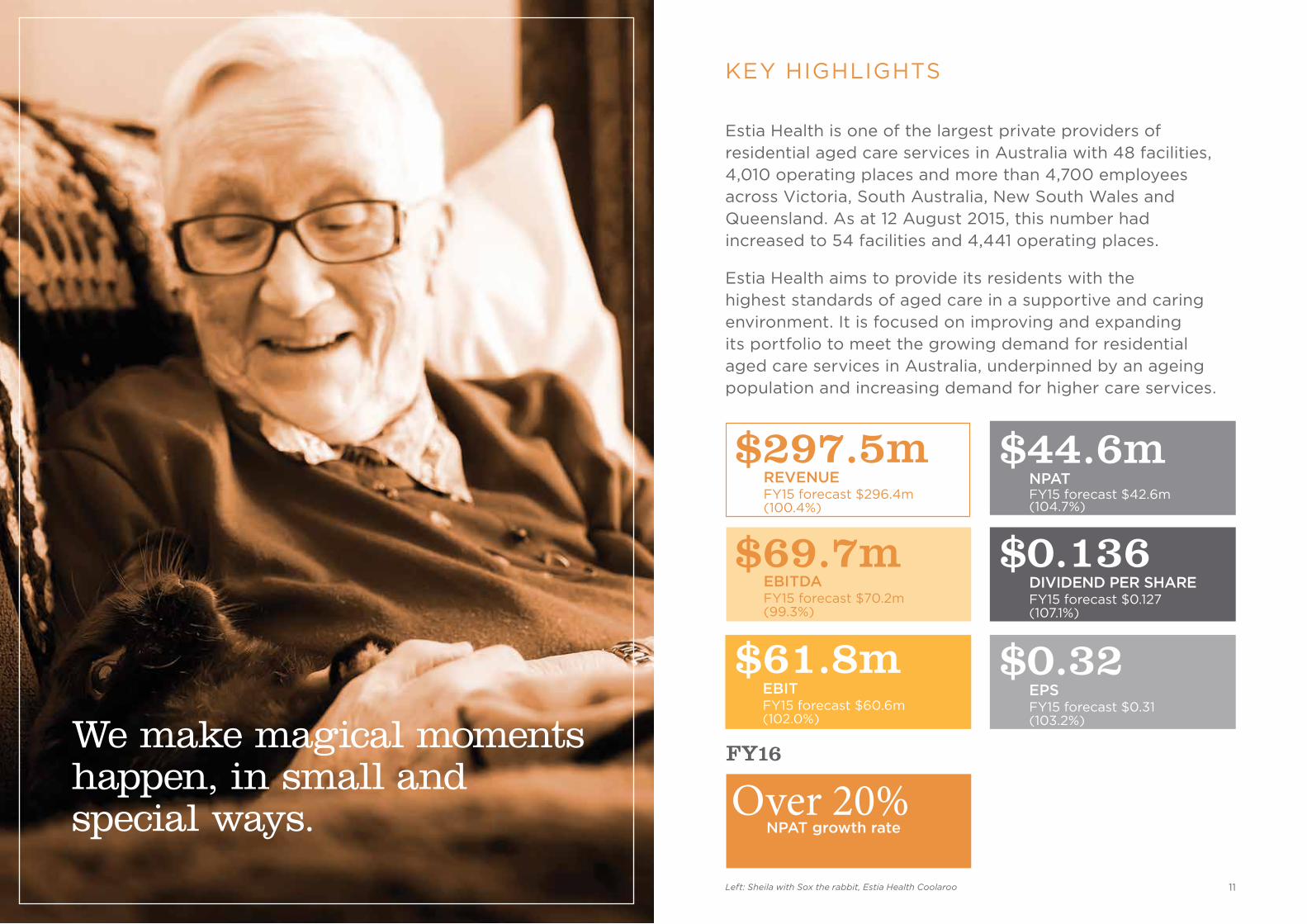

$297.5mREVENUEFY15 forecast $296.4m (100.4%)

$69.7mEBITDAFY15 forecast $70.2m (99.3%)

$61.8mEBITFY15 forecast $60.6m (102.0%)

$44.6mNPATFY15 forecast $42.6m (104.7%)

$0.136DIVIDEND PER SHAREFY15 forecast $0.127 (107.1%)

$0.32EPSFY15 forecast $0.31 (103.2%)

Over 20%NPAT growth rate

FY16

KEY HIGHLIGHTS

Estia Health is one of the largest private providers of residential aged care services in Australia with 48 facilities, 4,010 operating places and more than 4,700 employees across Victoria, South Australia, New South Wales and Queensland. As at 12 August 2015, this number had increased to 54 facilities and 4,441 operating places.

Estia Health aims to provide its residents with the highest standards of aged care in a supportive and caring environment. It is focused on improving and expanding its portfolio to meet the growing demand for residential aged care services in Australia, underpinned by an ageing population and increasing demand for higher care services.

11Left: Sheila with Sox the rabbit, Estia Health Coolaroo

We make magical moments happen, in small and special ways.

SA14 facilities1,133 places

VIC19 facilities1,541 places

NSW10 facilities898 places

QLD5 facilities438 places

AS AT 30 JUNE 2015

No. of Facilities

No. of Operational Places48 4,010

KEY HIGHLIGHTS cont.

GROWTH STRATEGY

GROWTH STRATEGY cont.

SINGLE SITES: 500 – 1,000 places per annum

GROUP: 1+ medium/large sized group in period

GREENFIELD: 500 – 1,000 places in period

BROWNFIELD: 300+ places in period

ORGANIC

ACQUISITION

Operating place per Prospectus 3,613

New acquisitions above Prospectus (CY15) 921

Closure of nursing home wing at Mudgeeraba for redevelopment June 2015 (55)

Offline places (26)

Places under redevelopment at Craigmore (12)

Forecast operating places October 2015 4,441

FY16 Acquisitions

49 KEYSBOROUGH 60 places July 15

50 BENDIGO 73 places Sept 15

51 KEILOR 60 places Sept 15

52 ACQUISITION 1 70 places Sept 15

53 BANNOCKBURN 120 places Oct 15

54 ACQUISITION 2 48 places Oct 15

431 places

TOTAL OF 4,441 OPERATIONAL PLACES

1312

Estia Health aims to reach

10,000 places

by FY2020through a combination of acquisitions and organic growth.

OPERATING AND FINANCIAL REVIEW

OVERVIEW OF THE GROUPEstia Health is one of the largest providers of residential aged care services in Australia with a portfolio of 48 facilities and 4,010 operating places (as at 30 June 2015) from which it provides residents with high quality clinical care services, daily living services, accommodation services and extra services. With facilities across Victoria, South Australia, New South Wales and Queensland, the company is predominantly focused on self-funded residents in metropolitan areas with above average socio-economic backgrounds.

Estia’s facilities are supported by a variety of functions (Finance & Commercial, Risk & Quality, Strategy & Development and People & Communications) both at the facility level and through a range of centralised national, state and regional functions. These functions enable each facility to focus on providing better quality care and operating more places efficiently. It also enables Estia to better manage operational risks and its financial performance as well as achieve its growth strategy.

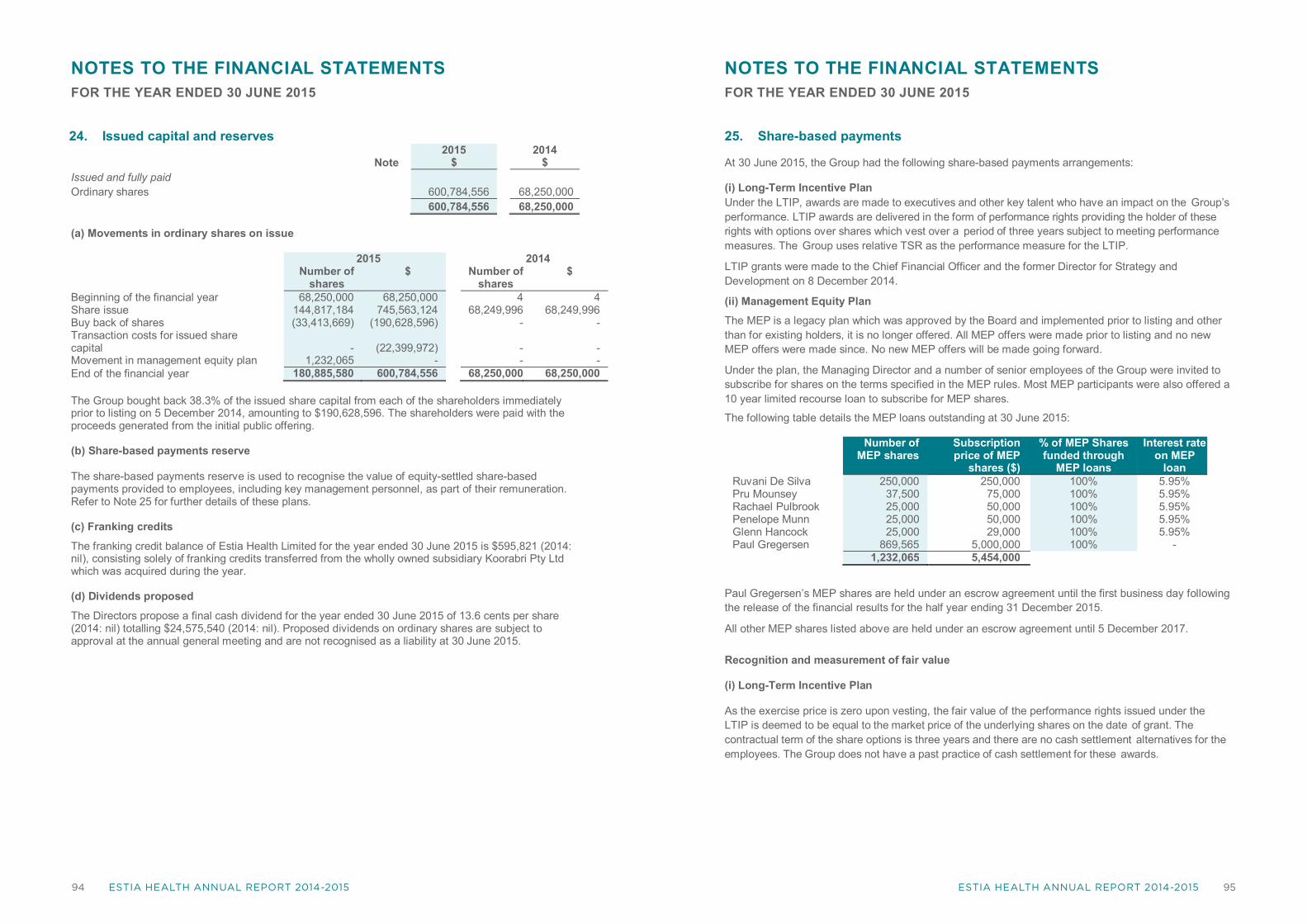

PRINCIPAL ACTIVITIESSignificant changes in the state of affairs On 5 December 2014 the Company successfully listed on the Australian Securities Exchange. A total of 126,087,759 shares were issued in the float with total gross proceeds of $725,004,614.

On 9 December 2014 the proceeds raised from the listing were used to repay in full the funding provided under existing senior debt and mezzanine facilities, vendor and shareholder loans.

SERVICE OFFERINGEstia provides consistent, high levels of clinical care services and offers a wide range of services to its residents. Estia also provides additional amenities to its residents.

The company provides the following services:

– Clinical care services: Estia provides 24-hour nursing care, personal care, wound management, administering pharmaceuticals, physiotherapy and occupational therapy, and arranging on-site visits from external medical practitioners.

– Daily living services: At each of its facilities, Estia provides residents with a range of daily living services such as laundry, meals, recreational activities, emotional support and cleaning.

– Accommodation services: Estia provides its residents with modern, high quality accommodation services.

– Extra services: Estia provides extra services to residents in Dedicated Extra Service places, and additional optional services to residents that do not hold a Dedicated Extra Service place.

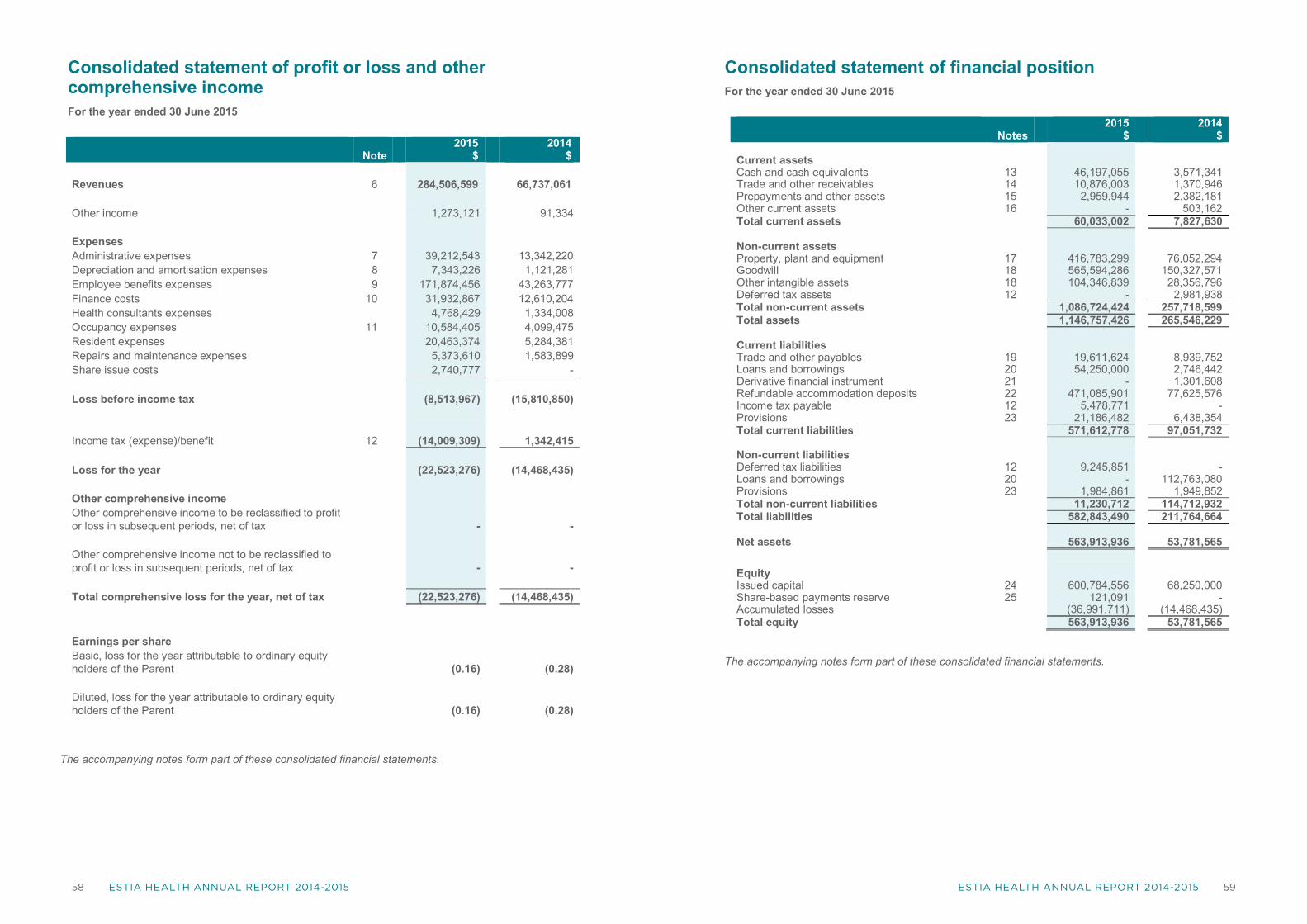

FINANCIAL PERFORMANCEEstia’s pro forma net profit after tax of $44.6 million exceeded pro forma forecast by $2.0 million or 4.7%.

Estia’s statutory loss after tax of $22.5 million for the year ended 30 June 2015 was $16.8 million (294.7%) above Prospectus forecast. A summary pro forma and statutory income statement in line with the Estia’s Prospectus lodged 3 December 2014 is reflected in the following tables:

Summary of pro forma income statement($ million)

Actual2 2015

Forecast1 2015

Total revenue 297.5 296.4EBITDA3 69.7 70.2

EBIT4 61.8 60.6

NPAT 44.6 42.6

EPS (cents) 32.2 30.8

Summary of statutory income statement($ million)

Actual

2015Forecast1

2015

Total revenue 284.5 283.9EBITDA3 30.8 35.6

EBIT4 23.4 26.6

NPAT (22.5) (5.7)

EPS (cents) (16.3) (4.0)

1 Pro Forma Forecast Financial Information is consistent with the information disclosed in the Prospectus lodged 3 December 2014.2 Pro Forma Actual has been prepared consistent with the assumptions set out in the Prospectus lodged 3 December 2014.3 Earnings before Interest, Tax, Depreciation and Amortisation (“EBITDA”) has been prepared consistent with the assumptions set out in the Prospectus lodged 3 December 2014.4 Earnings before Interest and Tax (‘EBIT”) has been prepared consistent with the assumptions set out in the Prospectus lodged 3 December 2014.

EARNINGS PER SHARE

The Group’s pro forma earnings per share (EPS) in FY15 were 32.2 cents (FY15 forecast: 30.8 cents). EPS in the current period was impacted by the issue of new shares from the entitlement offer equity raising undertaken in 2014.

FINANCIAL PERFORMANCE OVERVIEWThe Group uses earnings before interest, income tax expense, depreciation and amortisation (EBITDA) in combination with other financial measures to evaluate the Group’s operating performance. The Company believes that EBITDA is a relevant and useful financial measure used by management to measure the Company’s operating performance. EBITDA reflects the profit for the year prior to including the effect of net finance costs, income taxes, depreciation and amortisation. Depreciation and amortisation are calculated in accordance with AASB 116: “Property, Plant and Equipment” and AASB 138: “Intangible Assets”, respectively.

Adjusting for acquisition transaction costs incurred in purchasing the Padman and Cook Care Groups and additional facilities, the Estia Health Group achieved an EBITDA for the year ended 30 June 2015 of $61,501,183. This includes several other non-recurring expenses incurred as part of those acquisitions and restructure of the Group.

Estia Health’s FY2015 Pro Forma NPAT was $44.6m. Pro Forma EBIT of $61.8m and Revenue of $297.5m were led by total occupancy levels increasing to 93.6% in June 2015, and 96.5% of residents receiving higher care subsidies. Occupancy levels for FY2015 were at 93.6%, above 89.3% in FY2014.

Estia also performed strongly on two other key operating metrics with Aged Care Funding Instruments (ACFI) subsidies increasing to $172.81 per day in June 2015, and $170.42 for FY2015, and average equivalent new RAD of $343,683, above FY2015 forecast of $238,000.

Estia maintained an industry leading figure of 94% single beds across the Company’s portfolio of 48 homes with 4,010 operational places.

Post the acquisition of Padman Health Care and Cook Care, during the year, Estia completed 12 acquisitions, adding a total 1,124 operational available places, 550 more places than forecast in the prospectus.

In addition to the strong financial result, the Estia Health Group maintained accreditations at all of its facilities and invested in capital works to improve the standard of each facility operated by the Group.

Future strategic initiatives for the Estia Health Group include the following:

– Continued growth through acquisitions, brownfield and greenfield developments and partnering with suitable organisations to provide aged care services;

– Maintaining and enhancing the skills and expertise of Estia Health Group’s employees to enhance the services provided to residents; and

– Introducing uniform procedures, software systems and infrastructure across the Estia Health Group to underpin the continued growth of the Group and to enhance the financial performance of the Group.

GROWTH STRATEGY Estia aspires to reach 10,000 operating places by the end of FY2020. Estia intends to supplement organic growth with acquisitions, brownfield developments, corporate partnerships and greenfield developments.

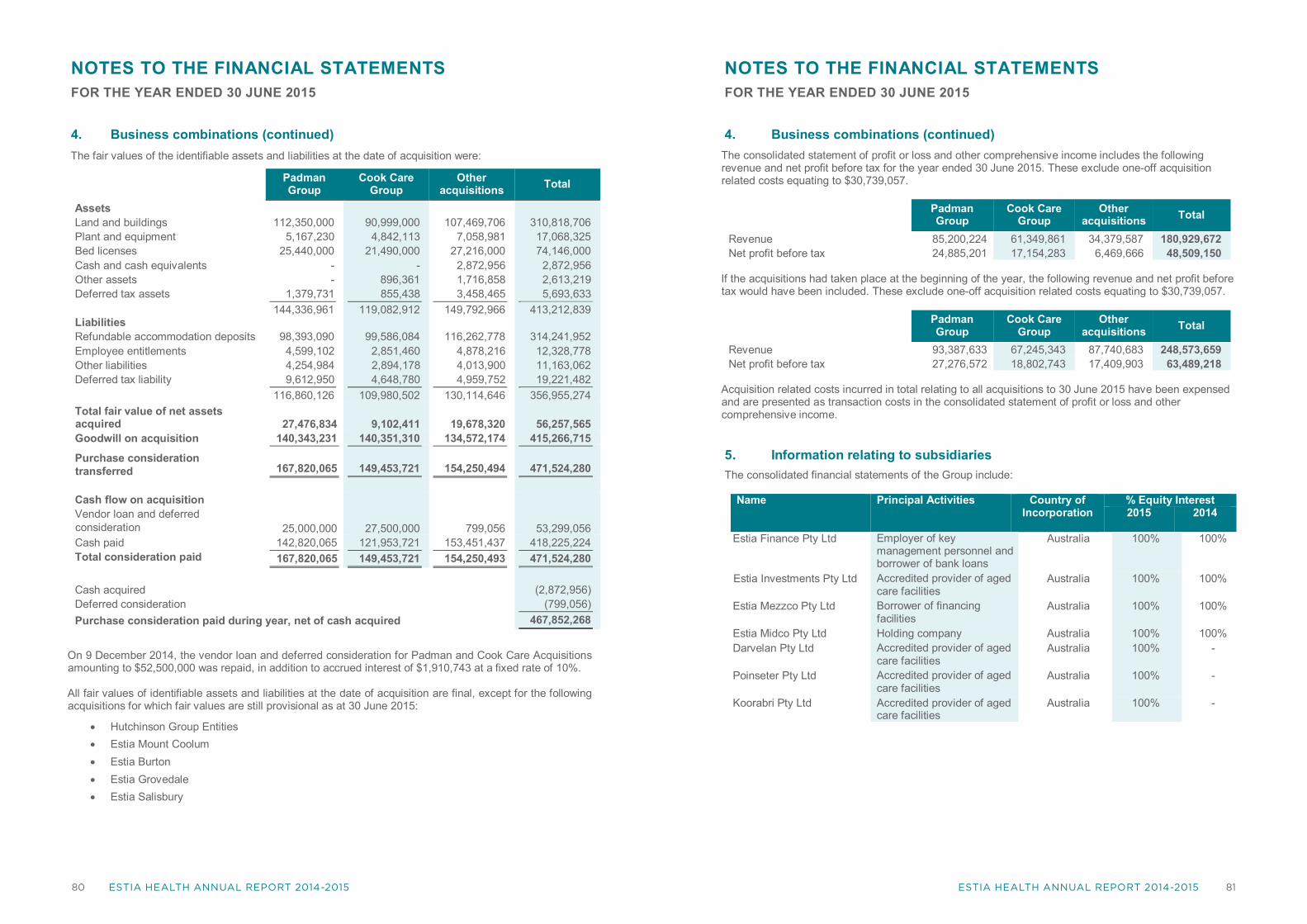

Acquisitions During the year the Estia Health Group successfully acquired the Padman and Cook Care Group operations as at 31 July 2014, operating in South Australia, New South Wales and Queensland. Since the formation of the company on 31 July 2014, Estia acquired the following facilities:

– Freehold of another Victorian-based facility on 29 September 2014;

– Two facilities in Victoria and one in New South Wales on 1 October, 2014;

– Two facilities in Victoria and one in South Australia on 1 December 2014;

– One facility in Victoria on 1 February 2015;

– One facility in South Australia on 1 April 2015;

– Three facilities in New South Wales on 6 May, 2015; and

– One facility in Queensland on 1 June 2015.

Since their acquisition, Estia has been focused on implementing operational improvements to increase occupancy levels, improve resident care needs and enhance operating efficiencies.

Estia aims to grow its operating places by 500 – 1,000 per annum through single site acquisitions. This may also be supplemented by the acquisition of a medium or large sized group operator.

Brownfield Developments Estia also aims to expand the number of its facilities to meet growing demand for residential aged care services through brownfield developments. Estia has an active brownfield development program where there is the potential to increase earnings from existing facilities, increase the overall level of RAD funding and provide attractive returns on capital.

14 15

OPERATING AND FINANCIAL REVIEW cont.

Estia aims to increase its operating places by more than 300 through brownfield developments by FY2020.

Greenfield Developments Where brownfield expansion is unable to meet the growing demand for services and acquisitions are not available or do not meet Estia’s requirements, Estia may consider the development of new greenfield facilities. Estia has entered into strategic alliances and corporate partnerships with developers of residential aged care facilities to grow the number of places it operates.

On 25 June 2015, Estia entered into a strategic partnership with Living Choice to build 500 residential aged care places by end FY2019, beginning with two facilities on the Sunshine Coast in Maroochydore and Twin Waters.

Estia aims to increase its operating places by 500 – 1,000 through greenfield developments by FY2020.

KEY BUSINESS RISKS Changes to regulatory frameworkThe Australian aged care industry is highly regulated and subject to change. The way that the industry is regulated and funded by the Australian Government has a fundamental influence on Estia’s business model. Funding from the Australian Government contributed approximately 70% of Estia’s revenues in FY2015.

Estia is a member of the Aged Care Guild (the ‘Guild’) which represents for-profit aged care providers in Australia. The Guild meets with the Department of Social Services three times a year and is proactive in addressing issues that would impact the current industry business model.

Refundable accommodation bonds/RADsEstia is exposed to risks associated with the repayment of accommodation bonds and RADs. If a larger than expected number of bond/RAD paying residents were to leave Estia’s aged care facilities, Estia would be required to repay a large sum of accommodation bonds/RADs. Estia is also exposed to risks that may adversely affect the future value of Estia’s total accommodation bonds/RADs.

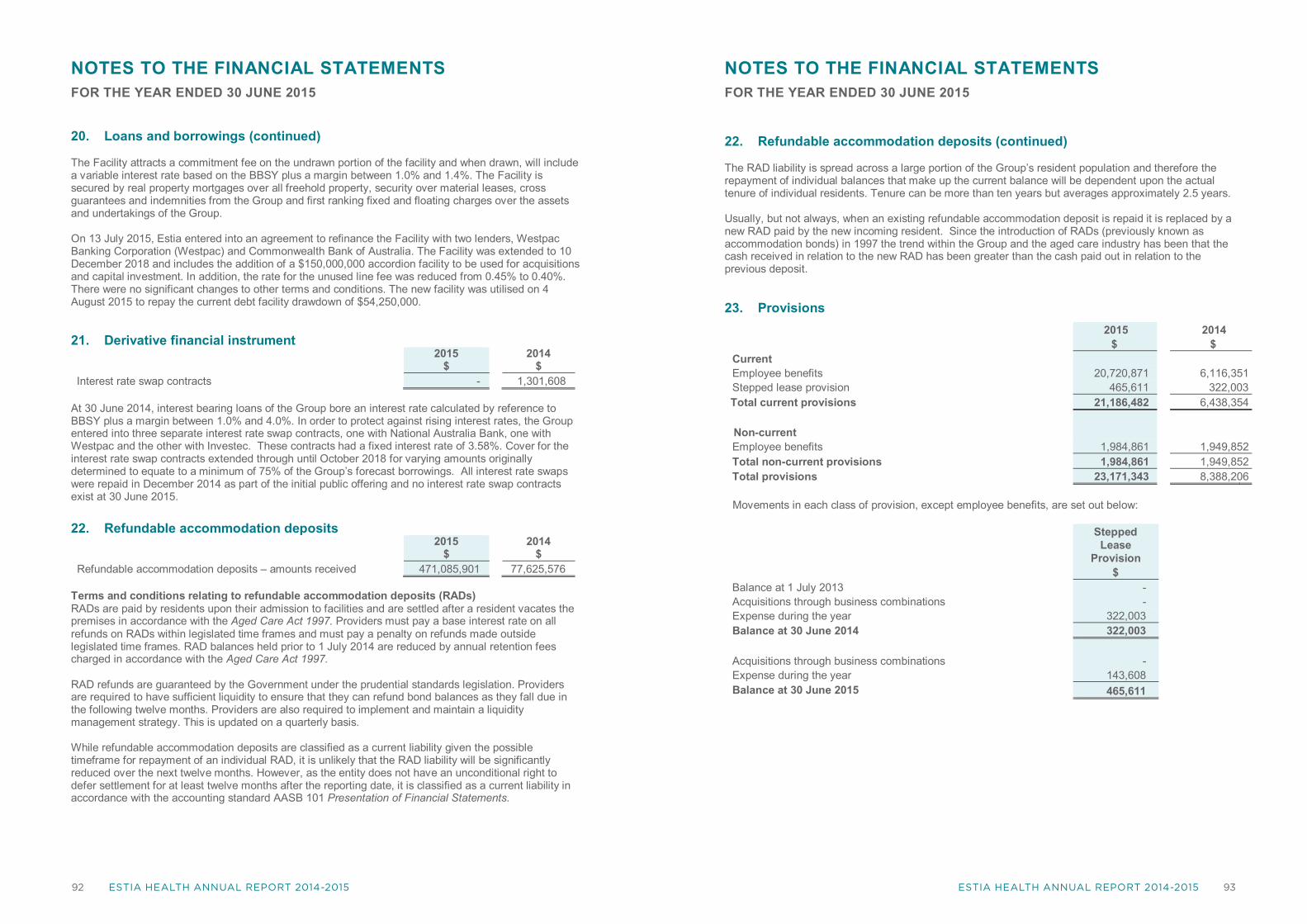

Estia has a Liquidity Management Strategy to ensure RADs are paid when due, which includes a $20,000,000 debt facility available for working capital requirements centred on refunding RADs.

Occupancy levels may fallEstia’s occupancy levels may fall below expectations as a result of factors such as increased competition in the residential aged care industry, specific issues arising at any of Estia’s facilities which adversely impact its

reputation and/or perceptions of the quality of clinical care provided, any trend towards home and community care, a deterioration in general economic and housing market conditions, or a decline in referrals from hospitals and other referral sources.

Estia aims to be the first choice in residential aged care for consumers. Estia’s Client Relations Team proactively builds strong relationships with local referral teams and monitors competitors, working with a dedicated Property Team to drive capital improvements to maintain a strong competitive position. Estia holds a strong portfolio with 94% single rooms, which remains the number one choice for consumers.

Reputational damage

Estia’s reputation could be adversely impacted if it, or the aged care sector generally, suffers from any adverse publicity. Any such adverse publicity could result in existing residents transferring away from Estia’s facilities to competitor aged care facilities or reduce Estia’s ability to attract new residents to its facilities, both of which could adversely impact Estia’s financial performance and position and future prospects.

Estia maintains robust systems and stringent quality control across all facilities to minimise risks that may result in adverse publicity. Through the establishment of regional networks, Estia has implemented strong support systems between facilities to address any potential adverse events at any one home.

AcquisitionsEstia has acquired a number of aged care facilities as part of its growth strategy. At the time each aged care facility was acquired, Estia conducted due diligence enquiries. Notwithstanding this due diligence, it is possible that one or more material issues or liabilities may not have been identified, or are of an amount that is greater than expected. Such issues or liabilities could adversely affect Estia’s financial performance and position and future prospects.

Estia engages independent financial and legal advisors to assist with due diligence on the acquisition of three or more facilities as well as conducting thorough due diligence on smaller single entity facilities internally. Financial projections in modelling acquisitions are benchmarked against existing Estia facilities.

Growth strategy Estia’s ability to meet its growth targets is dependent on its ability to identify and acquire suitable facilities. In particular, the success of Estia’s acquisition strategy will be dependent on a number of factors, including:

– the level of RADs held by Estia to fund such acquisitions;

– the availability of debt and equity funding and the suitability of the terms of such funding;

– the availability of suitable facilities at an acceptable price to Estia; and

– the number and resources of any of Estia’s competitors bidding for any target acquisition.

Estia’s ability to meet its growth targets is also dependent on its ability to identify existing sites on which to develop or expand new brownfield facilities or acquire attractive sites on which to develop new greenfield facilities. Given Estia’s strategy to operate in metropolitan areas of major Australian capital cities, there is no assurance that Estia will be able to develop new brownfields sites or secure new greenfield sites, on favourable economic terms or at all.

Estia has a balanced strategy for growth which includes acquisitions, brownfield and greenfield developments. Estia works with various agents to identify acquisitions. In addition, Estia has entered into a partnership for turnkey greenfield developments in Queensland and seeks to identify further partnerships to cover other eastern Australia states.

Loss of key personnelEstia relies on a high quality management team with significant aged care industry experience. The loss of key personnel could undermine Estia’s ability to operate its facilities and its business to the current standard, and to effectively comply with regulations. This may, in turn, result in a reduction in demand for Estia’s aged care services from new and existing residents and could adversely impact Estia’s financial performance and position and future prospects.

To attract and maintain key personnel, leaders are incentivised through short term incentives based on financial and non financial metrics.

Shortage of skilled employeesEstia’s business depends on a specialised health and aged care workforce. There is a risk that Estia may not be able to retain or expand a workforce that is appropriately skilled and trained to meet the existing or future demands of residents at its facilities and/or a risk that a shortage of employees leads to upward wage pressure which may adversely affect Estia’s business, financial performance and position and future prospects.

A Graduate Nursing Program to recruit and develop highly talented nursing staff will roll out in January 2016. In addition, ongoing training is provided to ensure employees maintain up to date knowledge to care for residents in Estia homes.

Availability of funding Estia may require funding or working capital in the future in order to pursue its growth strategy. Given the nature of Estia’s revenue profile and the potentially capital intensive nature of its business, there is no assurance that any such additional capital or funding will be available on favourable terms or at all and that Estia will be able to comply with the terms of such facilities. If adequate funds are not available, Estia may not be able to achieve its growth targets or respond to competitive pressures.

A new debt facility was agreed in July 2015 resulting in an extension to December 2018 and the addition of an accordion facility of $150,000,000 for capital investments and acquisitions. In total, Estia’s debt facility for funding growth is $280,000,000.

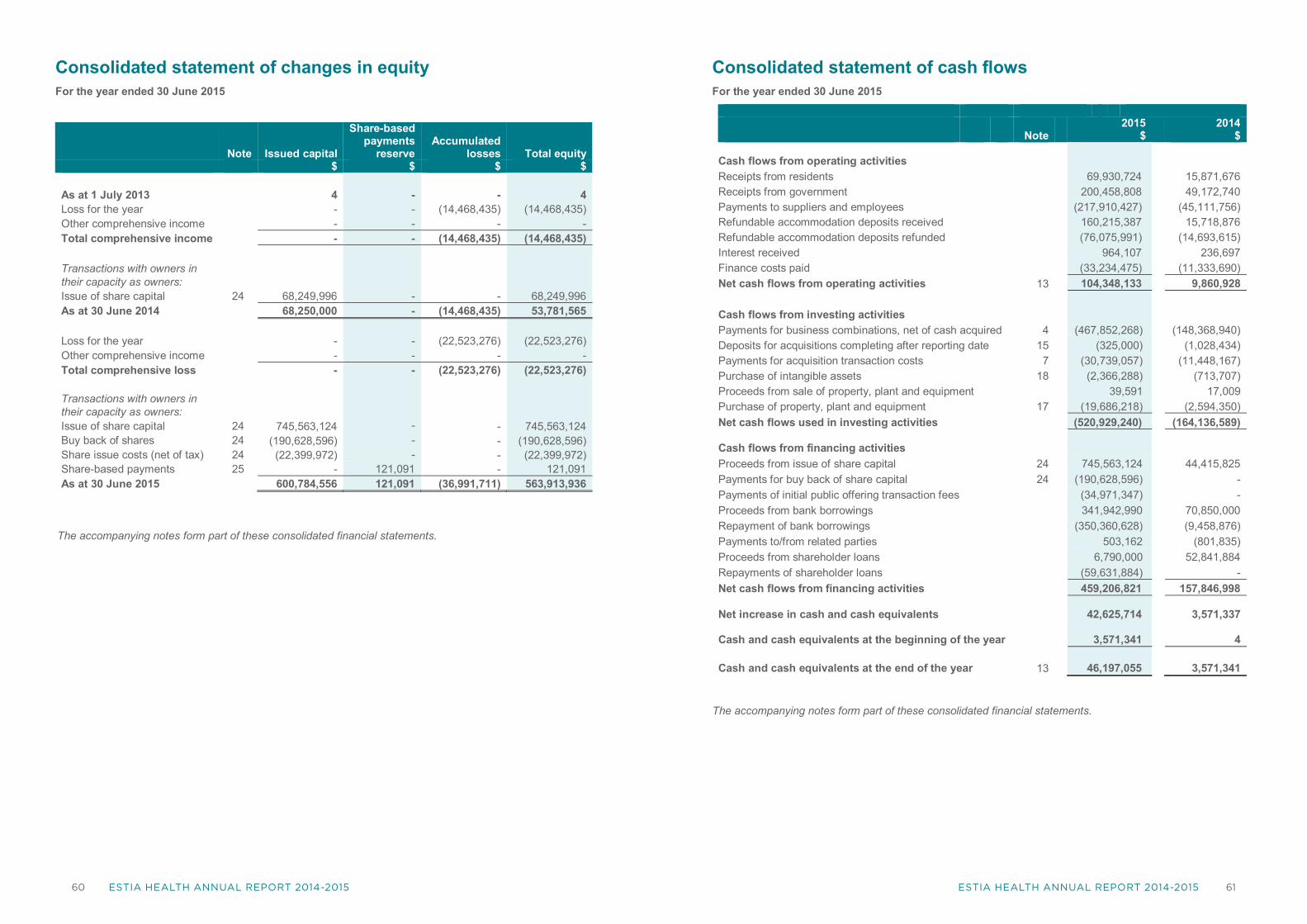

FINANCIAL POSITION At 30 June 2015, Estia’s net assets were $563.9 million, up 948.51% from 30 June 2014. The increase in net assets was primarily attributable to the following:

– acquisition of Padman, Cook Care and Hutchinson aged care groups

– acquisition of 9 individual aged care facilities

– equity raised in December 2014 of $725 million (gross).

A summary balance sheet is presented below.

Summary balance sheet ($ million)

30 June 2015

Actual

30 June 2014

Pro forma

Current assets 60.0 90.8

Non current assets 1086.7 797.0

Total assets 1146.8 887.8

Current liabilities 571.6 296.2

Non current liabilities

11.2 14.5

Total liabilities 582.8 310.7

Net assets 563.9 577.1

Estia’s principal sources of funds are cash flows from operations, refundable accommodation deposits and debt facilities. The cash position and available working capital facility is expected to provide sufficient liquidity to meet Estia’s currently anticipated cash requirements.

1716

OPERATING AND FINANCIAL REVIEW cont.

On 4 November 2014 the Company entered into a banking facility amounting to $150,000,000. These facilities have a maturity date of December 2017 and interest is calculated at BBSY plus a margin ranging from 1.0% to 1.4%. On 4 August 2015, the company refinanced the banking facility with two major lenders and i) extended the term to December 2018, ii) added a $150,000,000 accordion facility and iii) reduced the unused line fees from a rate of 0.45% to 0.40%. The new banking facilities will be used to fund acquisitions, capital expenditure and working capital.

Debt funding is utilised from time to time to finance acquisition of residential aged care businesses whilst seeking to maintain gearing within prudent levels.

The gearing ratio is calculated as a percentage of Net Debt/Total Equity. Net Debt is the total financial liabilities (including accommodation bonds / RADS) less cash on hand. Total Equity is as presented on the statement of financial position. For more information on capital management, see Note 29 of the financial statements.

RADs provide Estia with capital funding to support growth through capital investment in existing and new facilities as well as through acquisitions. RADs have contributed $88.5 million to net cash flows, $55.3 million in excess of forecast. Both an increase in the average accommodation price and an increase in the RAD penetration have contributed to the strong net RAD receipts.

A summary pro forma cash flow as at 30 June 2015 is presented below.

Summary of pro forma cash flow ($ million)

Actual2

2015Forecast1

2015

Net accommodation bonds / Refundable accommodation deposits

88.5 32.7

Other operating cash flows

62.0 66.6

Net cash flow from operations

150.5 99.3

Net cash flow from investing activities

(172.9) (99.6)

Net cash flow from financing activities

35.9 (18.0)

Net cash flows 13.5 (18.3)

A summary statutory cash flow as at 30 June 2015 is presented below.

Summary of statutory cash flow ($ million)

Actual

2015Forecast3

2015

Net accommodation bonds / Refundable accommodation deposits

84.1 32.7

Other operating cash flows

20.2 42.1

Net cash flow from operations

104.3 74.8

Net cash flow from investing activities

(520.9) (419.0)

Net cash flow from financing activities

459.2 386.6

Net cash flows 42.6 42.4

1. Pro Forma Forecast Financial Information is consistent with the information disclosed in the Prospectus lodged 3 December 2014. 2. Pro Forma Actual have been prepared consistent with the basis set out in the Prospectus lodged 3 December 2014.3. Statutory Forecast Financial Information is consistent with the information disclosed in the Prospectus lodged 3 December 2014.

DIVIDEND REINVESTMENT PLAN (DRP) On 15 July 2015, Estia introduced a DRP. The DRP was introduced after a period of significant company growth, to allow all shareholders participants to reinvest their dividends into acquiring additional Estia shares without incurring any brokerage or handling costs. To elect to participate in the Company’s DRP shareholders can use the online share registry facility or contact the share registry, Link Market Services. Please refer to estiahealth.com.au/investor-centre for the plan booklet and forms.

DIVIDENDSA final dividend of 13.6 cents per share (2014: nil) or $24,575,540 (2014: nil) is recommended for payment on ordinary shares. The tax rate at which recommended dividends will be franked is 30%. Estia’s Dividend Reinvestment Plan will apply to the dividend.

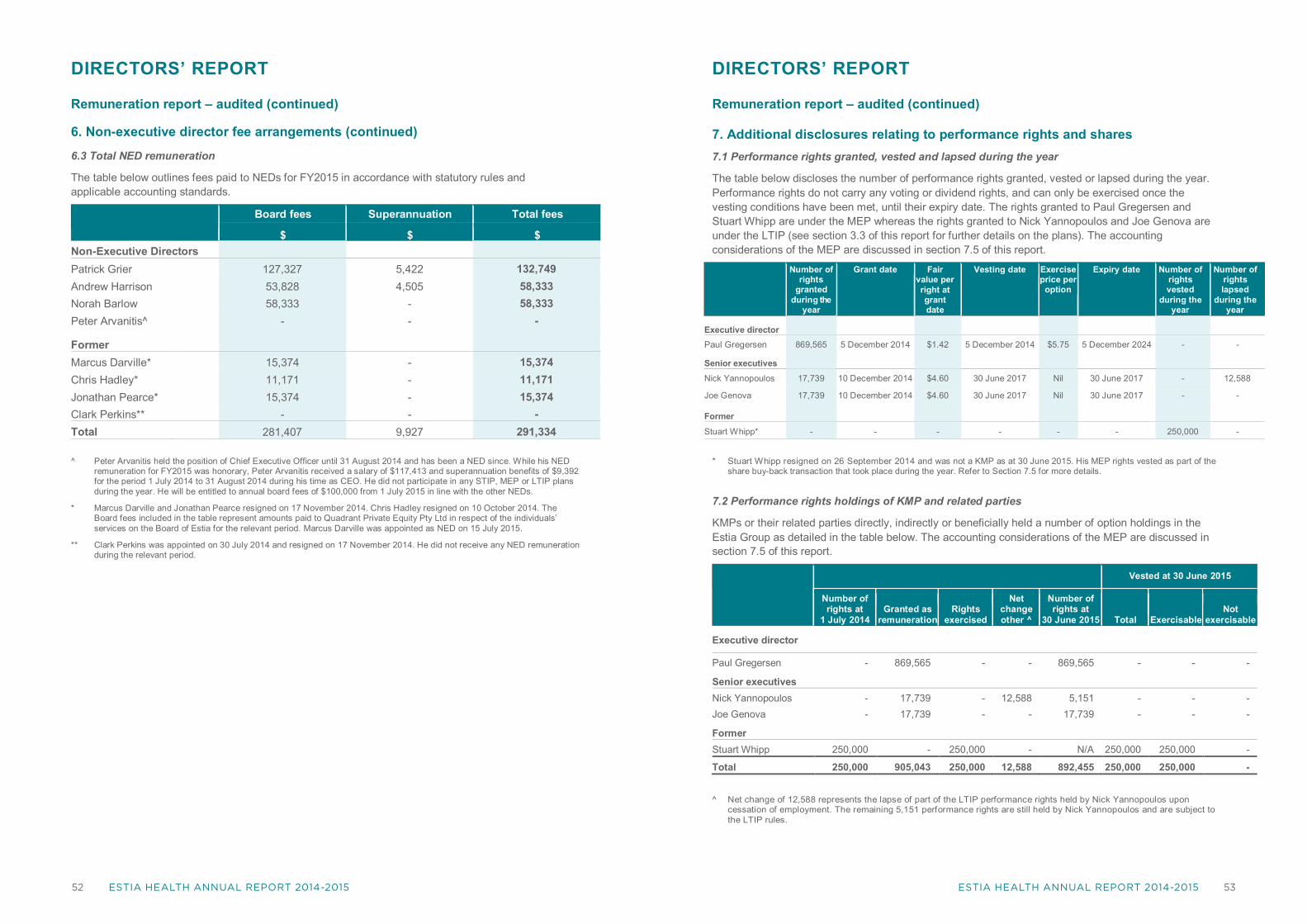

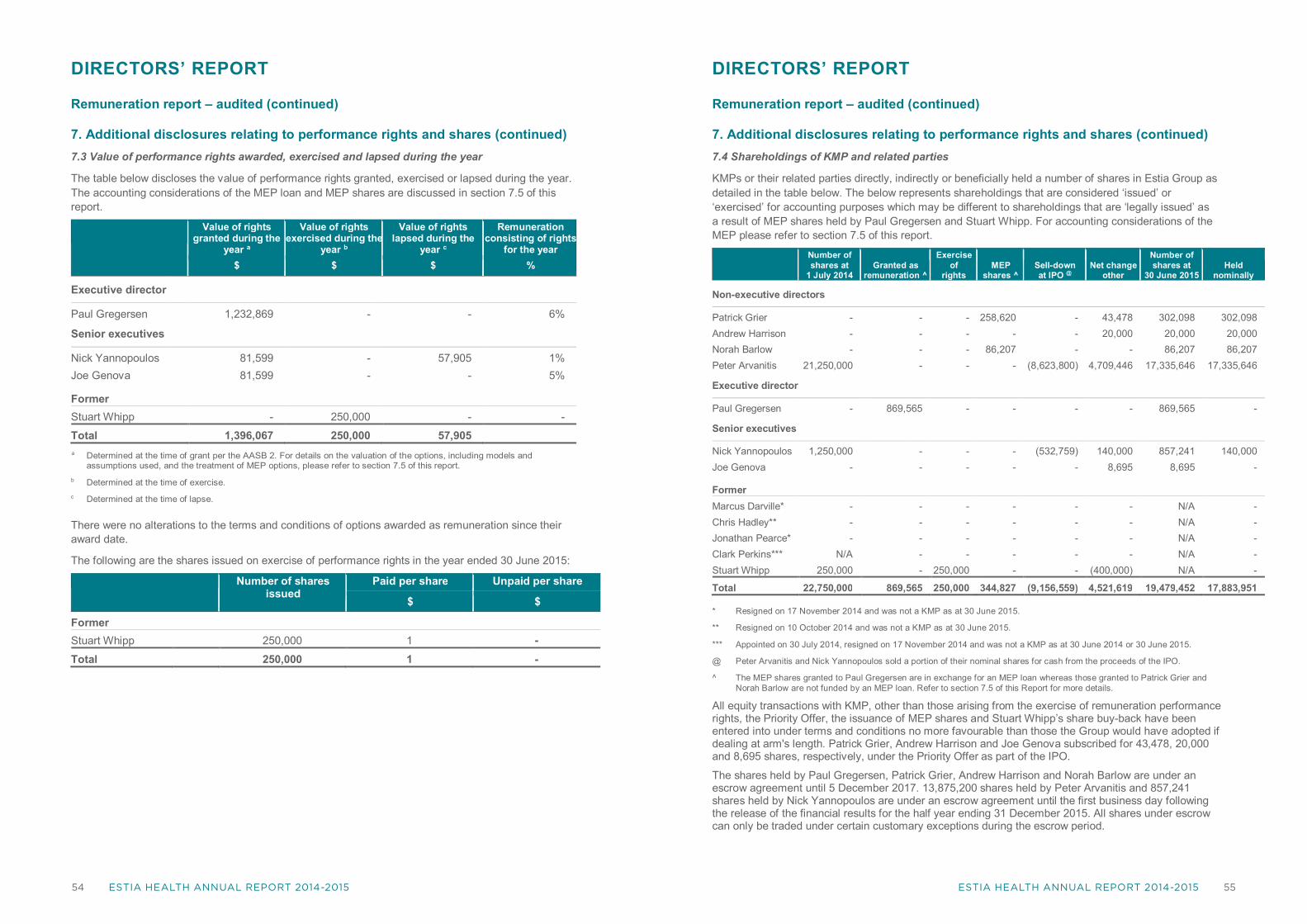

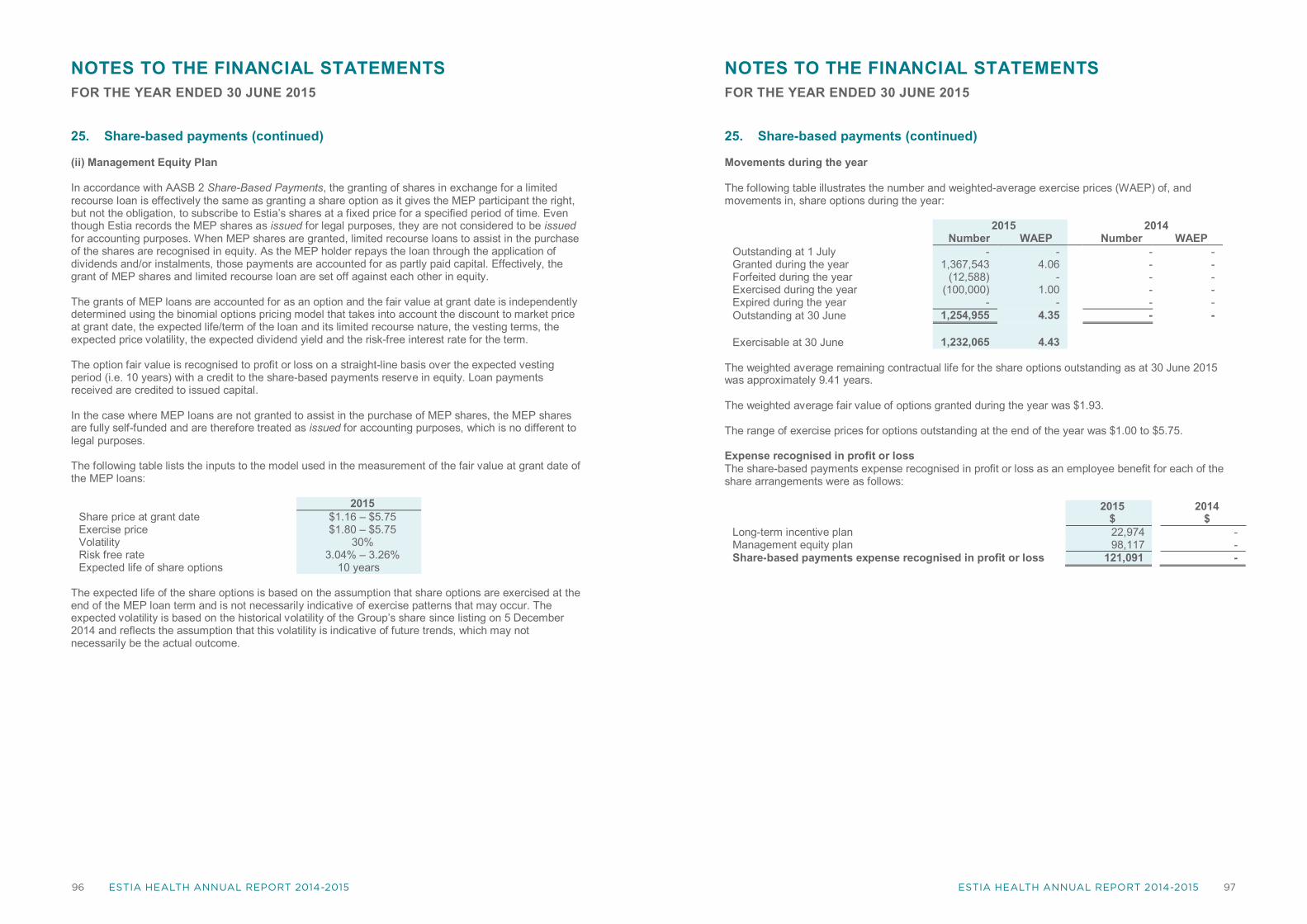

PERFORMANCE RIGHTSAt the date of this report, there were 22,890 performance rights under the Long Term Incentive Plan that are yet to vest. Refer to the Remuneration Report and Note 25 of the financial statements for further details of any rights outstanding as at 30 June 2015.

SIGNIFICANT EVENTS AFTER THE REPORTING DATEOn 13 July 2015, Estia entered into an agreement to refinance its existing debt facility to improve the ability to fund future growth. As part of the refinancing, Estia reduced the number of participants in the syndicated debt facility to include Westpac Banking Corporation and Commonwealth Bank of Australia. The amendments to the existing debt facility include an extension to 10 December 2018, a reduction in the unused line fee from 0.45% to 0.40% and the addition of a revolving $150,000,000 accordion facility. The refinancing became effective 4 August 2015.

In July 2015:

– Estia acquired a 60 bed facility in Keysborough, Victoria

– a strategic partnership agreement was entered into with developers to build four residential aged facilities which will add 500 places over 18 months to June 2017 with an option to build a further 500 places

– Estia entered into agreements to purchase two residential aged care facilities (133 places) in Victoria to be completed in September 2015 and one residential aged care facility (120 places) in regional Victoria to be completed in October 2015.

In August 2015, Estia entered into agreements to purchase:

- a 70 bed facility in metropolitan Melbourne, to be completed in September 2015

- a 48 bed facility in metropolitan Melbourne, to be completed in October 2015.

Other than those mentioned, no matters or circumstances have arisen since the end of the reporting period which significantly affected or may significantly affect the operations of the Group, the results of those operations, or the state of affairs of the Group in future financial years.

OUTLOOK Estia expects to generate over 20% NPAT growth against current year pro forma NPAT as the full earnings potential of acquisitions completed during FY15 begin to be realised and growth through further acquisitions in FY16 continues. Coupled with NPAT growth will be continued growth in cash from net RAD receipts and incremental growth on accommodation pricing for new residents. The continued positive cash flows will provide capital to fund FY16 acquisitions and will contribute to the achievement of long term returns greater than 15% on net capital employed.

The Board and Executive team are confident in delivering further growth through both acquisitions and organic development to achieve Estia’s vision of 10,000 beds by 2020.

19Right: Erna and Ann-Mari, Estia Health Coolaroo18

PATRICK GRIER, AM

Non-executive Director and Chairman, BSc; AO

Patrick was MD and CEO of Ramsay Health Care Limited for 14 years. Under his leadership, Patrick grew the Ramsay group from 7 hospitals to an ASX listed organisation operating over 100 hospitals in Australia and overseas, with an annual turnover of almost $3 billion and employing 25,000 people. He remains on the board of Ramsay as a non-executive director. Prior to this role, he was with Hospital Corporation Australia.

Patrick also served as both President and Chairman of the Australian Private Hospitals Association for over 10 years. In 2010, he was awarded the Order of Australia for his leadership and contribution to the Australian health care sector. He was previously the Chairman of the Opal Aged Care group and Chairman of the Australian Healthcare Workforce Institute. Patrick is a member of the Skin Cancer Network Advisory Board.

PAUL GREGERSEN

Managing Director and CEO, BEng (Hons); MBA (Distinction) and graduate of Wharton Business School’s Advanced Management Programme

Paul holds extensive experience and knowledge in the health care and financial services sectors. He has delivered outstanding performance in a variety of leadership roles around the globe, with particular expertise in the funding and provision of private health care.

Paul was MD of Bupa Aged Care Services Australia for five years and has over 24 years of general management experience, including roles across the United Kingdom, Singapore, Australia and China. Through his position as the inaugural chair of The Aged Care Guild, Paul advised the Australian Government on the Living Longer, Living Better aged care reforms in Australia. In 2012, the Cabinet of the Australian Government appointed Paul as an independent expert for the Aged Care Financing Authority to assist in the reform of Australia’s aged care system.

PETER ARVANITIS

Non-executive Director

Peter is the founder and former CEO of Estia. Peter founded Estia as Lasting Changes in 2005, having identified a need for improving the quality and consistency of residential aged care in Australia, both at the corporate and facility level. Under Peter’s leadership, Estia expanded successfully from its first aged care home to 39 facilities. As CEO, Peter led the acquisition of Padman, Cook Care and 17 individual facilities.

Prior to Estia, Peter had successfully founded, operated and disposed of a number of businesses in transport, agriculture, residential and commercial property.

NORAH BARLOW

Non-executive Director, BCA; ACA; ONZM

Norah has an extensive background in business leadership and management, strategy, corporate finance, governance, tax and accounting. Formerly the CEO of Summerset New Zealand, she remains on the board as a non-executive director and is director across a number of organisations.

A member of the National Advisory Council on the Employment of Women and the National Taskforce on Allied Health Workers governance committee, she was President of the Retirement Villages Association (NZ) for seven years and made an Officer of the New Zealand Order of Merit for services to business in 2014.

ANDREW HARRISON

Non-executive Director, BEc; MBA; CA

Andrew is an experienced company director and corporate adviser. He is currently a non-executive director of Burson Group Limited. He has previously held executive and non-executive directorships with public, private and private equity owned companies, including as CFO of Seven Group Holdings, Group Finance Director of Landis + Gyr. and CFO and a director of Alesco.

Andrew was previously a Senior Manager at Ernst & Young (Sydney and London) and Gresham Partners Limited, and an Associate at Chase Manhattan Bank (New York).

MARCUS DARVILLE

Non-executive Dircector, MA (Hons), MBA

Marcus has over 20 years of private equity experience starting in the UK with NatWest Ventures (now Bridgepoint). He joined AMP in 1994 as Joint Head of Private Equity where he completed several major buyouts including Tasman Building Products.

Marcus joined Quadrant Private Equity in March 2006 and is a member of the Quadrant Investment Committee, a Director of Quadrant investees Super A-Mart/Barbeques Galore, Estia Health and ICON Cancer Care.

BOARD OF DIRECTORS

2120

STEVEN BOGGIANO

Strategy Director

Steven is a highly experienced executive with an extensive track record in banking, private equity and mergers and acquisitions. Steven was Managing Director and Head of Asia for Healthcare, Consumer, Retail & Real Estate at Barclays Investment Bank, Australia. He played an integral role in the formation of Estia Health including advising the company on the initial acquisition of Estia Health by Quadrant Private Equity and the subsequent acquisition of the Cook Care Group.

As Strategy Director, Steven’s role is to apply his considerable mergers and acquisitions experience to help deliver Estia’s ambitious expansion and growth agenda.

PAUL GREGERSEN

Managing Director and Chief Executive Officer

Paul holds extensive experience and knowledge in the health care and financial services sectors. He has delivered outstanding performance in a variety of leadership roles around the globe, with particular expertise in the funding and provision of private health care.

Formerly MD of Bupa Care Services, Paul has over 24 years of general management experience, including roles across the United Kingdom, Singapore, Australia and China. He has successfully developed and delivered propositions in health funding, primary care, hospitals and aged care to deliver superior performance.

KATE SELLICK

People and Communications Director

Formerly the HR and Corporate Affairs Director at Bupa Care Services from 2007 to 2012, Kate also completed a number of strategic consulting roles during 2013 and 2014 at Opal, Uniting Care Ageing and Pulse Health, prior to joining Estia Health in October 2014.

Kate has 20 years HR experience across a range of government, not for profit and private industries including from start up to global in education, defence, telecoms, retail, health, aged care and disability.

As People and Communications Director, Kate is integral to the growth, connectivity and interrelationships of Estia’s talented people, residents, families, volunteers and communities.

JOE GENOVA

Chief Financial Officer

Previously Director of Finance at Bupa Care Services and Director of Health, Ageing and Human Services sector at KPMG, with over 20 years of experience in management, finance and leadership roles in Australia and Canada.

Joe plays an important role in shaping the strategy and growth of Estia Health, bringing a wealth of residential aged care and financial management experience to the executive team. He has an integral role in development of new systems and processes and oversight of Estia’s mergers and acquisition activities of behalf of the Group.

PETER HAMILTON

Development Director

Previously, Peter was GM Property and Capital Works at HammondCare for 7 years, where he led all capital works projects, including the refurbishment and upgrade of existing residential aged care facilities and hospitals. He has 35 years’ experience in a range of executive management roles in aged care, construction and finance sectors across Australia, the UK and South Africa.

As Development Director, Peter will lead facility redevelopments and best-practice design principles across our homes, and assist in land acquisition and plan next-phase and future redevelopment priorities for the Group.

MARK BRANDON

Chief Quality Officer

Mark is an internationally recognised thought leader and expert on strategy, health and aged care quality and accreditation, government relations and organisation transformation. Mark held the CEO position at the Australian government’s Aged Care Standards and Accreditation Agency from 2002 to 2013.

Mark was awarded an Order of Australia (OAM) Medal in June 2015, in recognition of his contribution to health and aged standards.

Mark’s pivotal role is to guide the group to embed a next generation Quality Management System to deliver excellence in care, and enhance service quality for our residents and families.

EXECUTIVE TEAM

2322

CORPORATE GOVERNANCE

The Board is responsible for the overall corporate governance of Estia. The Board monitors the operational and financial position and performance of Estia and oversees its business strategy, including approving the strategic goals of Estia and considering and approving an annual business plan, including a budget.

The Board is committed to maximising performance, generating appropriate levels of shareholder value and financial return, and sustaining the growth and success of Estia. In conducting Estia’s business with these objectives, the Board seeks to ensure that Estia is properly managed to protect and enhance shareholder interests, and that Estia, its Directors, officers and personnel operate in an appropriate environment of corporate governance.

Accordingly, the Board has created a framework for managing Estia, including adopting relevant internal controls, risk management processes and corporate governance policies and practices which it believes are appropriate for Estia’s business and which are designed to promote the responsible management and conduct of Estia.

25

We challenge ourselves and inspire others.

Left: Melissa and Heather, Estia Health Yarra Valley

CORPORATE GOVERNANCE cont.

THE BOARD OF DIRECTORSThe Board of Directors comprises five non-executive Directors (three of whom are independent, including the Chairman), and one executive Director, being the Managing Director and CEO.

The board charter adopted by the Board sets out guidelines and thresholds of materiality for the purpose of determining independence of Directors in accordance with the ASX Recommendations, and has adopted a definition of independence that is based on the ASX Corporate Governance Principles and Recommendations (3rd Edition).

BOARD CHARTER The Board Charter sets out:

– the roles and responsibilities of the Board including to provide overall strategic guidance for Estia and effective oversight of management, oversight of Estia’s financial and capital management, management and review of Estia’s compliance with its disclosure obligations and the disclosure and communication policy, promotion of effective engagement with security holders, oversight of policies between Estia and other stakeholders, ethical and responsible decision making along with compliance and risk management;

– the role and responsibilities of the Chairman and company secretary;

– the delegations of authority of the Board to both committees of the Board, the CEO and other management of Estia;

– the membership of the Board, including in relation to the Board’s composition and size and the process of selection and re-election of Directors, independence of Directors and conduct of individual Directors;

– Board process, including how the Board meets; and

– the Board’s performance evaluation processes, including in respect of its own performance, and the performance of the Board committees, individual Directors and senior executives.

BOARD COMMITTEESThe Board may from time to time establish appropriate committees to assist in the discharge of its responsibilities. The Board has established the Audit and Risk Committee and the Nomination and Remuneration Committee.

The role of the Audit and Risk Committee is to assist the Board in carrying out its accounting,

auditing and financial reporting responsibilities including oversight of:

– the integrity of Estia’s external financial reporting and financial statements;

– the appointment, remuneration, independence and competence of Estia’s external auditors;

– the performance of the internal and external audit function and review of their audits;

– the effectiveness of Estia’s system of risk management and internal controls; and

– Estia’s systems and procedures for compliance with applicable legal regulatory requirements.

The role of the Nomination and Remuneration Committee is to assist and advise the Board on the following nomination related matters:

– appointment and re-election of directors;

– induction and continuing professional development programs for directors;

– development and implementation of processes for evaluating the performance of the Board, its committees and directors;

– processes for recruiting new directors (including evaluation of skills, independence and experience);

– the appointment and re-election of directors; and

– succession planning for the Board, the Chief Executive Officer and other senior executives, to ensure that the Board is of a size and composition conducive to making appropriate decisions, with the benefit of a variety of perspectives and skills and in the best interests of Estia as a whole.

The Nomination and Remuneration Committee also assists and advises the Board on remuneration policies and practices for the Board, the CEO, the CFO, other senior executives and other persons whose activities, individually or collectively, affect the financial soundness of Estia. In accordance with the ASX Recommendations, the Audit and Risk Committee and the Nomination and Remuneration Committee each comprise at least three non-executive directors (a majority of whom are independent), and an independent chair who is not the Chairman of the Board. The Audit and Risk Committee comprises Andrew Harrison (Chair), Patrick Grier and Norah Barlow. The Nomination and Remuneration Committee comprises Norah Barlow (Chair), Patrick Grier and Peter Arvanitis. Other committees may be established by the Board as and when required to consider other matters of special importance.

SKILLS Skills, experience and expertise of the Board is set out below: – Strategy – Accounting and financial reporting – Risk and compliance oversight – Organisational culture and leadership – Government relations / political advisory – Corporate governance – Aged care management – Broad health sector experience – Listed company experience

– Global business operational experience.

DIVERSITY POLICY The Board has adopted a diversity policy which sets out Estia’s commitment to diversity and inclusion in the workplace at all levels. The diversity policy provides a framework to achieve Estia’s diversity goals and commitment to creating a diverse work environment where everyone is treated fairly and with respect and where everyone feels responsible for the reputation and performance of Estia.

DISCLOSURE AND COMMUNICATION POLICY The Board has adopted a written policy, which establishes procedures which are aimed at ensuring that Directors and management are aware of and fulfill their obligations in relation to the timely disclosure of material price-sensitive information. Under the disclosure and communication policy, the Board is responsible for managing Estia’s compliance with its continuous disclosure obligations.

SECURITIES TRADING POLICYThe Board has adopted a securities trading policy which sets out the restrictions that apply to dealing with shares including “prohibited periods”, during which certain designated persons are generally not permitted to deal with shares along with a procedure under which certain persons are required to submit prior notification and obtain written confirmation prior to dealing in shares outside the prohibited periods.

CODE OF CONDUCT In addition, many governance elements are contained in the Constitution. Estia’s code of conduct sets out the values, commitments, ethical standards and policies of Estia and outlines the standards of conduct expected of Estia’s business and people in a range of circumstances. In particular, the code requires awareness of, and compliance with, Estia’s other policies

and procedures. Details of Estia’s key policies and practices and the charters for the Board and each of its committees are available at estiahealth.com.au

VOTING RIGHTSShareholders (whether residents or non-residents of Australia) may vote at a meeting of shareholders in person, directly or by proxy, attorney or representative, depending on whether the shareholder is an individual or a company.

Subject to any rights or restrictions attaching to our shares, on a show of hands each shareholder present in person or by proxy, attorney or representative has one vote and, on a poll, has one vote for each fully paid share held. Presently, we have only one class of fully paid ordinary shares and these do not have any voting restrictions. If shares are not fully paid, on a poll the number of votes attaching to the shares is pro-rated accordingly.

SUSTAINABILITY Sustainability forms part of our everyday activities, and is a major driver of our acquisition and growth strategy to achieve operational efficiency and economic sustainability. Sustainability is achieved through meeting the needs of our residents and by each and every one of our facilities becoming an accepted part of their local communities.

Since the merger of the three residential aged care businesses on 31 July 2014, Estia has focused on the integration of these three operations and subsequent acquisitions.

Meeting both the care and social inclusion needs of our residents is important. Our residents are supported to remain involved in their local communities through varied programs including intergenerational activities, playgroups and school groups, gender specific programs targeted at male residents, and social networking tools including Skype, Facebook and emails.

Both social and economic sustainability will benefit enormously by future practices aimed at environmental sustainability as this will target our environmental footprint as we grow.

Estia is committed to being an active and valued member of its local communities. Part of our integration involves being environmentally sustainable, making as small an environmental footprint as we can, whilst still providing the exceptional levels of care our residents expect. Environmental sustainability can encompass many things, and as we enter our second year, we will focus on understanding those environmental issues that are important to Estia and our relationship with our communities.

2726

CORPORATE GOVERNANCE cont.

ESTIA HEALTH PURPOSE AND VALUESEstia Health’s purpose is to be one family, where everyone belongs. This reflects Estia’s intent to build inclusive and diverse workplaces where everyone is treated equally.

Estia Health’s purpose is supported by its values statement called the Estia Code. The Estia Code is our five behaviours that guide our employees in the delivery of care and services for residents, families, local communities and each other.

The Estia Code is:

1. Always approachable – we take time to listen because we care.

2. My daily best – we do our best to make a difference every day.

3. Creating happiness – we make magical moments happen in small and special ways.

4. Pushing our limits – we challenge ourselves and inspire others.

5. See something, say something – we pay attention and are quick to act.

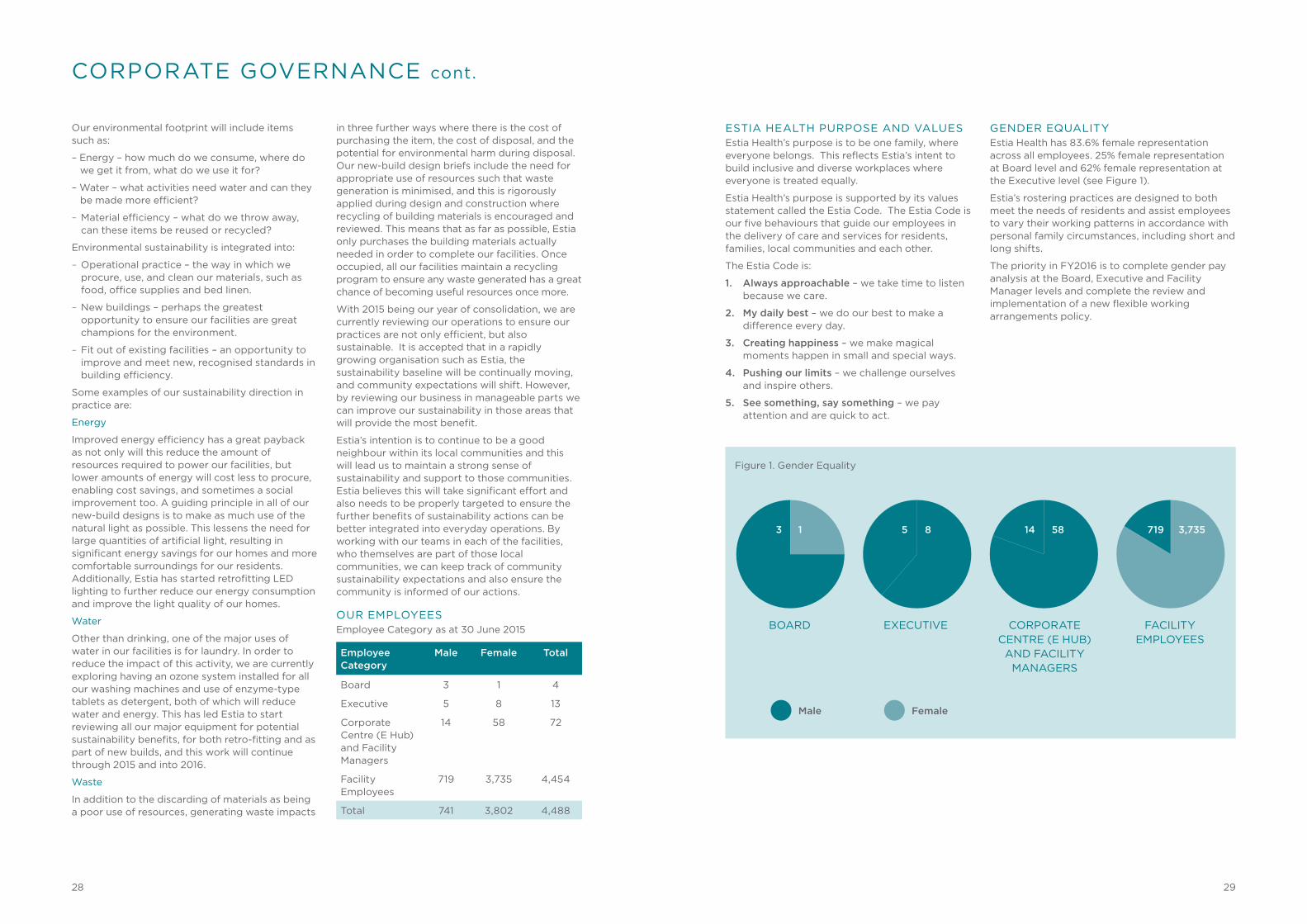

GENDER EQUALITYEstia Health has 83.6% female representation across all employees. 25% female representation at Board level and 62% female representation at the Executive level (see Figure 1).

Estia’s rostering practices are designed to both meet the needs of residents and assist employees to vary their working patterns in accordance with personal family circumstances, including short and long shifts.

The priority in FY2016 is to complete gender pay analysis at the Board, Executive and Facility Manager levels and complete the review and implementation of a new flexible working arrangements policy.

Our environmental footprint will include items such as:

– Energy – how much do we consume, where do we get it from, what do we use it for?

– Water – what activities need water and can they be made more efficient?

– Material efficiency – what do we throw away, can these items be reused or recycled?

Environmental sustainability is integrated into:

– Operational practice – the way in which we procure, use, and clean our materials, such as food, office supplies and bed linen.

– New buildings – perhaps the greatest opportunity to ensure our facilities are great champions for the environment.

– Fit out of existing facilities – an opportunity to improve and meet new, recognised standards in building efficiency.

Some examples of our sustainability direction in practice are:

Energy

Improved energy efficiency has a great payback as not only will this reduce the amount of resources required to power our facilities, but lower amounts of energy will cost less to procure, enabling cost savings, and sometimes a social improvement too. A guiding principle in all of our new-build designs is to make as much use of the natural light as possible. This lessens the need for large quantities of artificial light, resulting in significant energy savings for our homes and more comfortable surroundings for our residents. Additionally, Estia has started retrofitting LED lighting to further reduce our energy consumption and improve the light quality of our homes.

Water

Other than drinking, one of the major uses of water in our facilities is for laundry. In order to reduce the impact of this activity, we are currently exploring having an ozone system installed for all our washing machines and use of enzyme-type tablets as detergent, both of which will reduce water and energy. This has led Estia to start reviewing all our major equipment for potential sustainability benefits, for both retro-fitting and as part of new builds, and this work will continue through 2015 and into 2016.

Waste

In addition to the discarding of materials as being a poor use of resources, generating waste impacts

in three further ways where there is the cost of purchasing the item, the cost of disposal, and the potential for environmental harm during disposal. Our new-build design briefs include the need for appropriate use of resources such that waste generation is minimised, and this is rigorously applied during design and construction where recycling of building materials is encouraged and reviewed. This means that as far as possible, Estia only purchases the building materials actually needed in order to complete our facilities. Once occupied, all our facilities maintain a recycling program to ensure any waste generated has a great chance of becoming useful resources once more.

With 2015 being our year of consolidation, we are currently reviewing our operations to ensure our practices are not only efficient, but also sustainable. It is accepted that in a rapidly growing organisation such as Estia, the sustainability baseline will be continually moving, and community expectations will shift. However, by reviewing our business in manageable parts we can improve our sustainability in those areas that will provide the most benefit.

Estia’s intention is to continue to be a good neighbour within its local communities and this will lead us to maintain a strong sense of sustainability and support to those communities. Estia believes this will take significant effort and also needs to be properly targeted to ensure the further benefits of sustainability actions can be better integrated into everyday operations. By working with our teams in each of the facilities, who themselves are part of those local communities, we can keep track of community sustainability expectations and also ensure the community is informed of our actions.

OUR EMPLOYEESEmployee Category as at 30 June 2015

Employee Category

Male Female Total

Board 3 1 4

Executive 5 8 13

Corporate Centre (E Hub) and Facility Managers

14 58 72

Facility Employees

719 3,735 4,454

Total 741 3,802 4,488

Figure 1. Gender Equality

BOARD EXECUTIVE CORPORATE CENTRE (E HUB)

AND FACILITY MANAGERS

FACILITY EMPLOYEES

13 5 14 7198 58 3,735

Male Female

28 29

SHAREHOLDER INFORMATION

Distribution of shares

Range No. of shareholders

% Securities %

100,001 and Over 66 1.60 155,489,489 85.96

10,001 to 100,000 581 14.08 13,320,522 7.36

5,001 to 10,000 776 18.81 5,723,791 3.16

1,001 to 5,000 2,081 50.44 5,980,485 3.31

1 to 1,000 622 15.08 371,293 0.21

Total 4,126 100.00 180,885,580 100.00

Twenty largest shareholders

Name Shares held % of issued shares

HSBC CUSTODY NOMINEES (AUSTRALIA) LIMITED 20,197,935 11.17

J P MORGAN NOMINEES AUSTRALIA LIMITED 19,145,387 10.58

NATIONAL NOMINEES LIMITED 14,419,172 7.97

AGED SERVICES VICTORIA PTY LTD 13,876,200 7.67

CITICORP NOMINEES PTY LIMITED 12,037,017 6.65

QUADRANT PRIVATE EQUITY NO. 3, LP 11,388,507 6.30

QUADRANT PRIVATE EQUITY NO. 3D PTY LIMITED 11,076,291 6.12

MCF 4 LIMITED 7,551,488 4.17

QUADRANT PRIVATE EQUITY NO. 3C PTY LIMITED 6,167,200 3.41

UBS WEALTH MANAGEMENT AUSTRALIA NOMINEES PTY LTD 4,094,971 2.26

BNP PARIBAS NOMS (NZ) LTD 4,068,745 2.25

BNP PARIBAS NOMS PTY LTD 2,961,425 1.64

MR PETER ARVANITIS & MRS ARETI ARVANITIS 2,813,100 1.56

CUSTODIAL SERVICES LIMITED 2,249,386 1.24

HSBC CUSTODY NOMINEES (AUSTRALIA) LIMITED - A/C 3 2,023,367 1.12

HSBC CUSTODY NOMINEES (AUSTRALIA) LIMITED - A/C 2 1,708,296 0.94

QUADRANT PRIVATE EQUITY NO. 3A PTY LIMITED 1,653,334 0.91

CARPE DIEM ASSET MANAGEMENT PTY LTD 1,173,913 0.65

MR VINCENT MICHAEL O'SULLIVAN 1,151,000 0.64

AVANTEOS INVESTMENTS LIMITED 1,060,294 0.59

Total for top 20 shareholders 140,817,028 77.85

FOR THE YEAR ENDED 30 JUNE 2015

30 31

We pay attention and are quick to act.

Left: Donald and Rosario, Estia Health Yarra Valley

For information on shareholder voting rights, please refer to page 27.

Annual Report 2014 - 2015

Annual Financial Report FOR THE YEAR ENDED 30 JUNE 2015 ESTIA HEALTH LIMITED ABN 37 160 986 201

33ESTIA HEALTH ANNUAL REPORT 2014-2015 33

FINANCIAL REPORT

Estia Health Annual Report 2014-2015 33

Estia Health LimitedABN 37 160 986 201

Contents to financial report

Corporate information 34

Directors’ report 35

Auditor’s independence declaration 57

Consolidated statement of profit or loss and other comprehensive income 58

Consolidated statement of financial position 59

Consolidated statement of changes in equity 60

Consolidated statement of cash flows 61

Notes to the financial statements 62

Directors’ declaration 106

Auditor’s report 107

34 ESTIA HEALTH ANNUAL REPORT 2014-2015 35ESTIA HEALTH ANNUAL REPORT 2014-2015

CORPORATE INFORMATION

Estia Health Annual Report 2014-2015 34

ABN 37 160 986 201

DirectorsPaul Gregersen (Managing Director) Appointed 17 November 2014Patrick Grier (Non-executive Chairman) Appointed 17 November 2014Andrew Harrison (Non-executive Director) Appointed 17 November 2014Norah Barlow (Non-executive Director) Appointed 17 November 2014Peter Arvanitis (Non-executive Director)*Marcus Darville (Non-executive Director) Resigned 17 November 2014, re-appointed 15 July 2015Chris Hadley (Non-executive Director) Resigned 10 October 2014Clark Perkins (Non-executive Director) Appointed 30 July 2014, resigned 17 November 2014Jonathan Pearce (Non-executive Director) Resigned 17 November 2014Nick Yannopoulos (Executive Director) Resigned 17 November 2014

* Peter Arvanitis was Chief Executive Officer until 31 August 2014

Company SecretarySuzy Watson Appointed 5 December 2014Nick Yannopoulos Appointed 26 September 2014, resigned 5 December 2014Stuart Whipp Resigned 26 September 2014

Registered office357 Camberwell RoadCamberwell VIC 3124

Principal place of business357 Camberwell RoadCamberwell VIC 3124

SolicitorsKing & Wood MallesonsGovernor Phillip Tower1 Farrer PlaceSydney NSW 2000

BankersWestpac Banking Corporation275 Kent StreetSydney NSW 2000

AuditorsErnst & Young8 Exhibition StreetMelbourne VIC 3000

DIRECTORS’ REPORT

Estia Health Annual Report 2014-2015 35

Your directors submit their report for the yearended 30 June 2015.

DirectorsThe names and details of the Group’s directors inoffice during the financial year and until the date ofthis report are as follows. Directors were in officefor the entire period unless otherwise stated. Moredetail on the current directors can be found onpages 20 and 21 of this Annual Report.

Paul Gregersen (Managing Director)Paul joined Estia on 1 August 2014 as ChiefExecutive Officer and was then appointed as aManaging Director on 17 November 2014.

Paul holds a Bachelor in Engineering from theUniversity of Wales, a Master in BusinessAdministration from the University of Bradford andis also a graduate of the Wharton BusinessSchool’s Advanced Management Programme.

Patrick GrierPatrick was appointed to the board in November2014 as Chairman and independent non-executive director.

Patrick holds a Bachelor of Science and aDiploma in Education from Capetown University.

Patrick has also been a director of Ramsay HealthCare Limited since 25 June 1997 and PrimeMedia Group Limited between 6 June 2008 and20 November 2014.

Andrew HarrisonAndrew was appointed to the Board in November2014 as an independent non-executive director.

Andrew holds a Bachelor of Economics from theUniversity of Sydney and a Master of BusinessAdministration from the Wharton School at theUniversity of Pennsylvania, and is a CharteredAccountant.

Norah BarlowNorah was appointed to the Board in November2014 as an independent non-executive director.

Norah holds a Bachelor of Commerce andAdministration from Victoria University and is anAssociate Chartered Accountant.

Norah has also served as a director of IngeniaCommunities Group since 31 March 2014, EvolveEducation Group since 13 November 2014, andSummerset Group Holdings Limited since 26March 2009.

Peter ArvanitisPeter is the founding director and former CEO ofEstia and has been a non-independent non-executive director since 1 September 2014.

Marcus DarvilleMarcus was reappointed as a non-independentnon-executive director in July 2015 after heresigned in November 2014.

Marcus was also a director of Isentia GroupLimited between 14 January 2014 and 9 May2014, Virtus Health Limited between 11 February2008 and 7 October 2014, and Summerset GroupHoldings Limited between 17 April 2009 and 21October 2013.

Chris HadleyChris is the Managing Director of QuadrantPrivate Equity. He is one of the longest servingexecutives in the Australian Private Equityindustry and was one of the founding councilmembers of AVCAL. Chris has led and manageda number of Quadrant investments and has beena director on many investee boards.

Chris is a Chartered Accountant and is a memberof Financial Services International (Australia).

Chris has also been a director of APN OutdoorGroup Limited between 1 May 2012 and 17October 2014, Burson Group Limited between 17October 2011 and 31 March 2014, Isentia GroupLimited between 14 January 2014 and 9 May2015, and Summerset Group Holdings Limitedbetween 17 April 2009 and 21 October 2013.

Chris resigned from the Board in October 2014.

Clark PerkinsClark is the CEO of Mercury Capital and has morethan 25 years’ experience in the investmentbanking, private equity and financial servicesindustry.

Clark holds a Bachelor of Commerce from theUniversity of Auckland.

Clark resigned from the Board in November 2014.

Jonathan PearceJonathan joined Quadrant Private Equity inJanuary 2012 as an Investment Director. Prior tothis Jonathan was a Director ofPricewaterhouseCoopers, where he wasresponsible for advising on private equity andcorporate mergers and acquisitions acrossEurope, the US and Asia.

Jonathan holds a Bachelor of Commerce and is aChartered Accountant.

Jonathan resigned from the Board in November2014.

36 ESTIA HEALTH ANNUAL REPORT 2014-2015 37ESTIA HEALTH ANNUAL REPORT 2014-2015

DIRECTORS’ REPORT

Estia Health Annual Report 2014-2015 36

Nick YannopoulosNick joined Estia Health Group from a backgroundin sales, property and management roles. Nickplayed an integral part in improving anddeveloping new systems and processesthroughout the Group. He also played a major rolein the Group's recent expansion and in particularensuring that all acquisitions have transitionedsmoothly into the Estia Health Group.

Nick resigned from the Board in November 2014and as Company Secretary in December 2014.

Company Secretary

Suzy WatsonSuzy was appointed as Company Secretary andGeneral Counsel in December 2014.

Suzy was previously in-house counsel at BUPA inboth Sydney and the UK. She holds a B.A Hons(Law and Government), an LLM in InternationalEconomic Law (Distinction) and is studying for anLLM (Applied Law) in In-House Practice. Suzy is aqualified Solicitor in England and Wales and inAustralia, a member of the Law Society ofVictoria, a member of the Australian CorporateLawyers Association and a member of theGovernance Institute of Australia.

Dividends

The Directors propose a final cash dividend for theyear ended 30 June 2015 of 13.6 cents per share(2014: nil) totalling $24,575,540 (2014: nil).Proposed dividends on ordinary shares aresubject to approval at the annual general meetingand are not recognised as a liability at 30 June2015.

Principal activities

The principal activities of the Estia Health Groupduring the year ended 30 June 2015 included theoperating and developing of owned and leasedresidential aged care facilities throughoutAustralia.

Operating and financial review

Information on the operations and financialposition for the Group is set out in our Operatingand Financial Review (OFR) from page 14 of thisfinancial report.

Significant changes in the state of affairs

On 5 December 2014 the Group successfullylisted on the Australian Stock Exchange. A total of126,087,759 shares were issued in the float withtotal gross proceeds of $725,004,614.

On 9 December 2014 the proceeds raised fromthe listing were used to repay in full the fundingprovided under existing senior debt andmezzanine facilities, vendor and shareholderloans.

Significant events after the balance dateOn 13 July 2015, Estia refinanced its existing debtfacility to improve the ability to fund future growth.As part of the refinancing, Estia reduced thenumber of participants in the syndicated debtfacility to include Westpac Banking Corporationand Commonwealth Bank of Australia. Theamendments to the existing debt facility include anextension to 10 December 2018, a reduction inthe unused line fee from 0.45% to 0.40% and theaddition of a revolving $150,000,000 accordionfacility. The new facility was utilised on 4 August2015 to repay the existing debt facility drawdownof $54,250,000.In July 2015:

• Estia acquired a 60 bed facility inKeysborough, Victoria;

• a strategic partnership agreement wasentered into with developers to build fourresidential aged facilities which will add500 places over 18 months to June 2017with an option to build a further 500places; and

• Estia entered into agreements topurchase two residential aged carefacilities (133 places) in Victoria to becompleted in September 2015 and oneresidential aged care facility (120 places)in regional Victoria, to be completed inOctober 2015.

In August 2015, Estia entered into an agreementto purchase a 70 bed facility, to be completed inSeptember 2015 and a 48 bed facility to becompleted in October 2015, both in metropolitanMelbourne.

Total committed gross consideration for theseacquisitions is $90,800,000.

Other than those mentioned above, no matters orcircumstances have arisen since the end of thereporting period which significantly affected ormay significantly affect the operations of theGroup, the results of those operations, or the stateof affairs of the Group in future financial years.

DIRECTORS’ REPORT

Estia Health Annual Report 2014-2015 37

Likely developments and expected results

The Group’s growth strategy centres onincreasing the size of its aged care portfoliothrough the acquisition of additional aged carefacilities and the developments of greenfield andbrownfield projects.

Other than the likely developments disclosedabove and elsewhere in this report, no matters orcircumstances have arisen which significantlyaffected or may significantly affect the operationsof the Group, the results of those operations, orthe state of the affairs of the Group in futurefinancial years.

Environmental regulation and performance

The Group is not subject to significantenvironmental legislation under eitherCommonwealth or State legislation.

Indemnification and insurance of directors andofficers

The Group has agreed to indemnify all thedirectors and executive officers for any breach ofenvironmental or discrimination laws by the Groupfor which they may be held personally liable. Theagreement provides for the Group to pay anamount provided that:

(a) The liability does not arise out of conductinvolving a lack of good faith; and

(b) The liability is for costs and expensesincurred by the director or officer in defendingproceedings in which judgement is given intheir favour or in which they are acquitted.

During or since the financial year, the Group haspaid premiums in respect of a contract insuring allthe directors of Estia Health Ltd against legalcosts incurred in defending proceedings forconduct other than:

(a) A wilful breach of duty; or

(b) A contravention of sections 182 or 183 of theCorporations Act 2001, as permitted by section199B of the Corporations Act 2001.

The total amount of insurance contract premiumspaid was $272,500.

Indemnification of auditors

To the extent permitted by law, the Group hasagreed to indemnify its auditors, Ernst & YoungAustralia, as part of the terms of its auditengagement agreement against claims by thirdparties arising from the audit (for an unspecifiedamount). No payment has been made toindemnify Ernst & Young during or since thefinancial year.

Rounding

The amounts contained in this report and in thefinancial report have been rounded to the nearest$1 (where rounding is applicable) and wherenoted ($) under the option available to the Groupunder ASIC CO 98/0100. Estia Health Ltd is anentity to which the class order applies.

Committee membership

As at the date of this report, the Group had aNomination and Remuneration Committeecomprising of Norah Barlow (chairperson), PatrickGrier and Peter Arvanitis, and an Audit and RiskCommittee comprising of Andrew Harrison(chairperson), Norah Barlow (chairperson) andPatrick Grier.

38 ESTIA HEALTH ANNUAL REPORT 2014-2015 39ESTIA HEALTH ANNUAL REPORT 2014-2015

DIRECTORS’ REPORT

Estia Health Annual Report 2014-2015 38

Directors' meetings

The number of meetings of directors (including meetings of committees of directors) held during the yearand the number of meetings attended by each director were as follows:

Directors’meetings

Nomination andremuneration

committee

Audit and riskcommittee

No. of meetings held: 10 2 3

Eligible Attended Eligible Attended Eligible AttendedPaul Gregersen 10 10 - - - -Patrick Grier 10 10 2 2 3 3Andrew Harrison 10 10 - - 3 3Norah Barlow 10 10 2 2 3 3Peter Arvanitis 10 9 2 2 - -Marcus Darville 1 1 - - - -Chris Hadley 1 - - - - -Clark Perkins 1 - - - - -Jonathan Pearce 1 1 - - - -Nick Yannopoulos 1 - - - - -

DIRECTORS’ REPORT

39Estia Health Annual Report 2014-2015

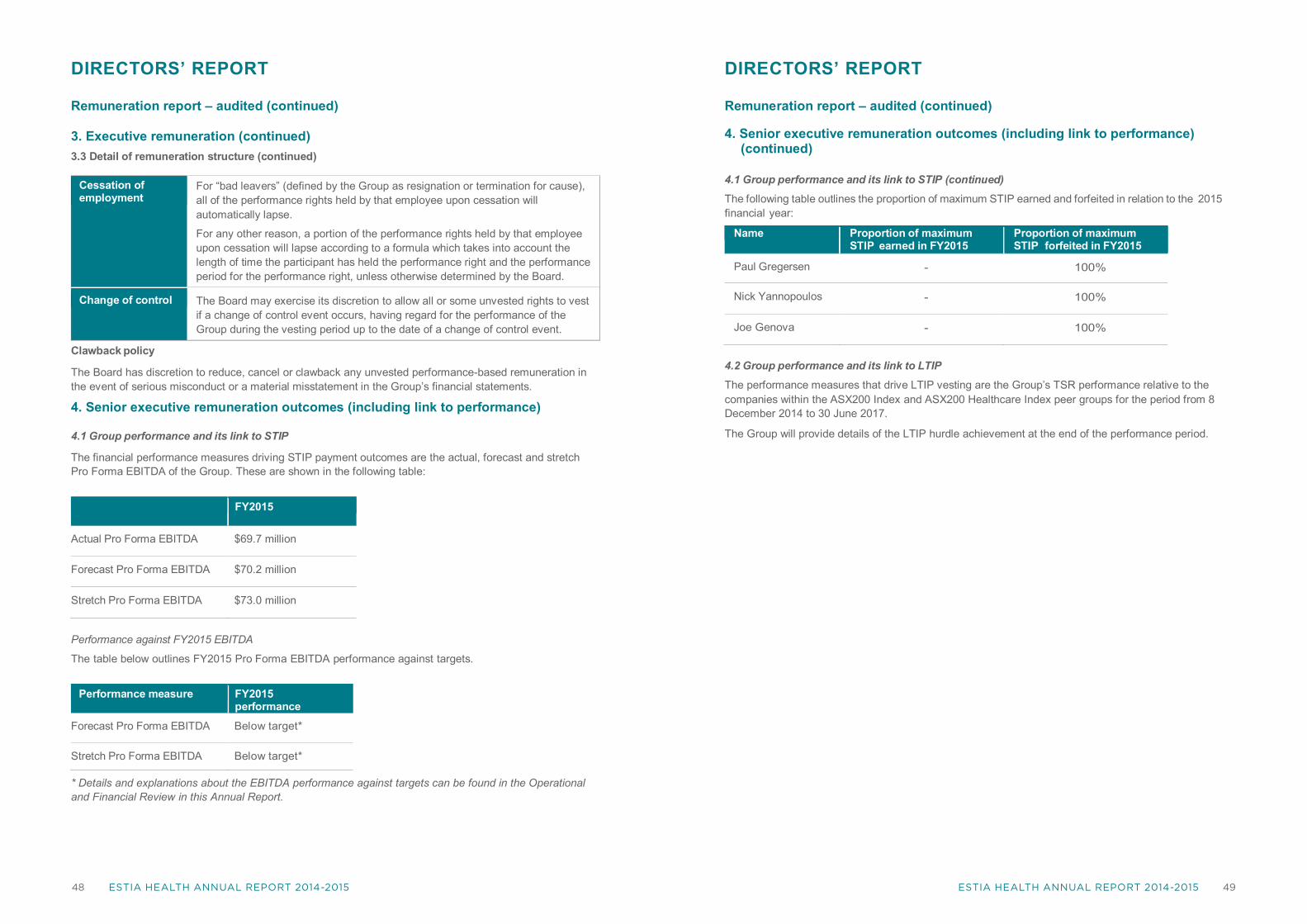

Remuneration report –auditedFY2015 was an exciting year for Estia Health withthe successful listing of the company on theAustralian Securities Exchange on 5 December2014.

The Prospectus lodged on 3 December 2014contained an outline of the remuneration of KeyManagement Personnel (KMP) who have directauthority and responsibility for planning, directingand controlling the activities of Estia. In FY2015,no changes were made to the remunerationframework, however, the Board proposes to makeminor adjustments to the framework in FY2016.

Estia’s remuneration policy is aimed at ensuringthe remuneration outcomes are linked to theGroup’s performance and align the interests ofmanagement with the interests of shareholders.The principles that underpin the remunerationframework support and drive the achievement ofEstia’s business strategy and seek to attract,retain and motivate senior management.

Summary of remuneration framework

In FY2015, the executive remuneration frameworkcomprised a mix of fixed annual remuneration,and short and long-term performance-linkedincentive plans as follows: