annual report 2015 1925 20years15 - agostini … ar 15.pdf · annual report 2015 2 the cover about...

TRANSCRIPT

19252015Years

ANNUAL REPORT 2015

AN

NU

AL

REP

OR

T 20

15

1

Contents

About the Cover 2

Notice of Meeting 3

Milestones of our 90 Years 4

Companies owned by Agostini’s 6

Alliances for Growth: Companies owned by Caribbean Distribution Partners 10

Overview of Product Categories of our Companies 19

Board of Directors 20

Corporate Governance 22

Chairman’s Remarks 26

Management Discussion & Analysis 28

Report of the Directors 33

Corporate Information 34

Independent Auditor’s Report 35

Consolidated Statement of Financial Position 36

Consolidated Income Statement 38

Consolidated Statement of Comprehensive Income 39

Consolidated Statement of Changes In Equity 40

Consolidated Statement of Cash Flows 41

Notes to the Consolidated Financial Statements 42

Directors’ & Senior Officers’ Interest & 10 Largest Shareholders 79

Honouring Long Service / Company of the Year 80

Proxy Form 81

Management Proxy Circular 82

All figures in this report are quoted in TT$. The exchange rate was US$1.00=TT$6.3733 as at 30 September 2015.

AN

NU

AL

REP

OR

T 20

15

2

the CoverAbout

In 2015, Agostini’s Limited celebrated its 90th anniversary since commencement of its activities in 1925. The Group has never been stronger, with assets of $1.5 billion, sales of $1.7 billion and profits of $80.6 million, employing 1,890 persons and operating in six countries.

Registered Office: 18 Victoria Avenue,

P.O. Box 191, Port of Spain, Trinidad, West Indies

Phone: (868) 623-4871Fax: (868) 623-1966

www.agostinislimited.com

19252015Years

ANNUAL REPORT 2015

AN

NU

AL

REP

OR

T 20

15

3

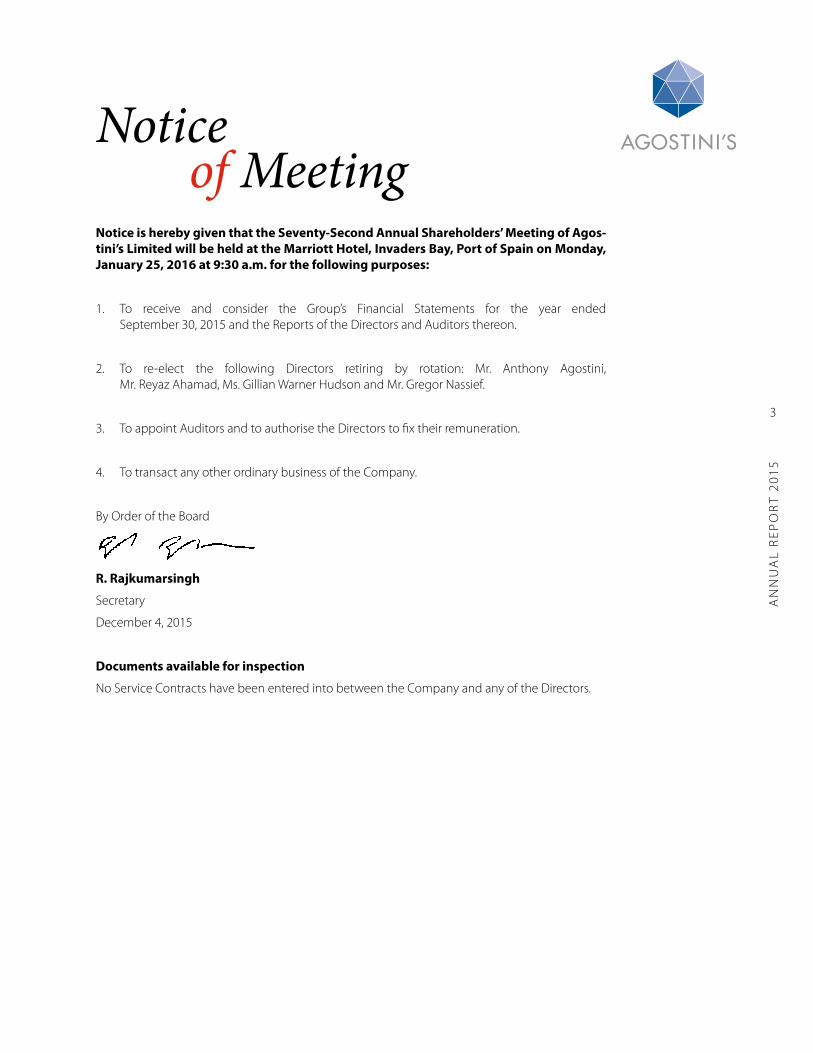

of MeetingNotice

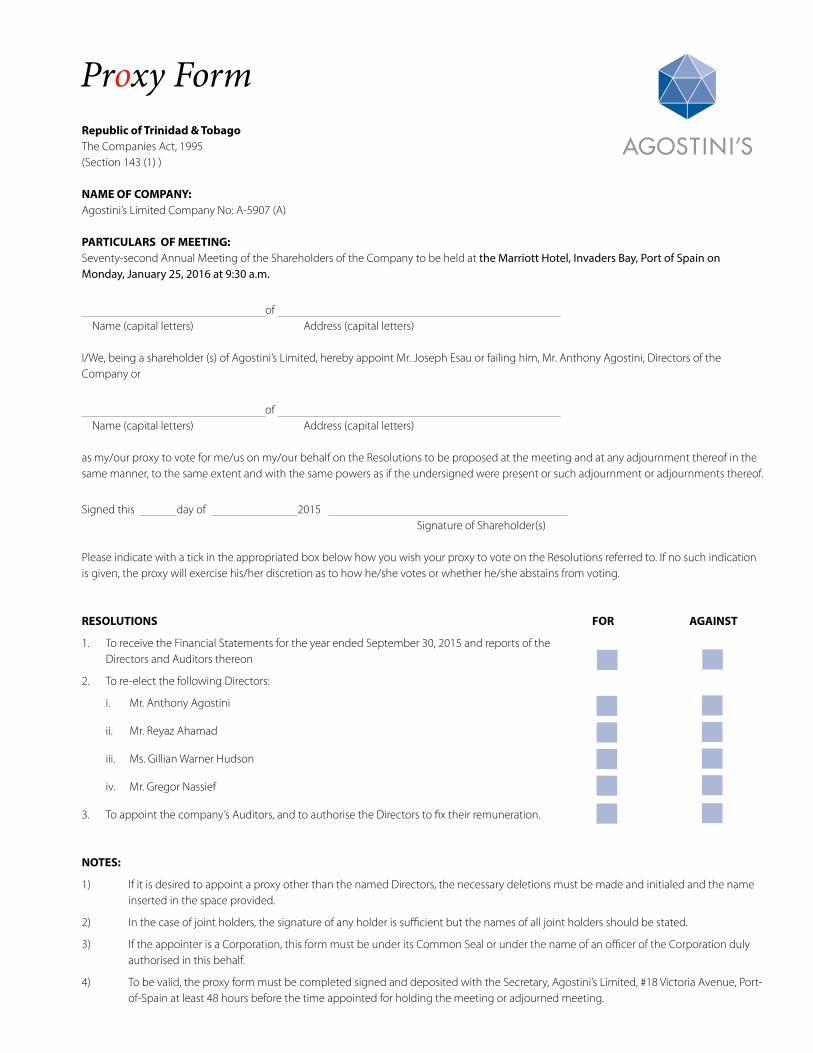

Notice is hereby given that the Seventy-Second Annual Shareholders’ Meeting of Agos-tini’s Limited will be held at the Marriott Hotel, Invaders Bay, Port of Spain on Monday, January 25, 2016 at 9:30 a.m. for the following purposes:

1. To receive and consider the Group’s Financial Statements for the year ended September 30, 2015 and the Reports of the Directors and Auditors thereon.

2. To re-elect the following Directors retiring by rotation: Mr. Anthony Agostini, Mr. Reyaz Ahamad, Ms. Gillian Warner Hudson and Mr. Gregor Nassief.

3. To appoint Auditors and to authorise the Directors to fix their remuneration.

4. To transact any other ordinary business of the Company.

By Order of the Board

R. Rajkumarsingh

Secretary

December 4, 2015

Documents available for inspection

No Service Contracts have been entered into between the Company and any of the Directors.

4

Annual Report 2013

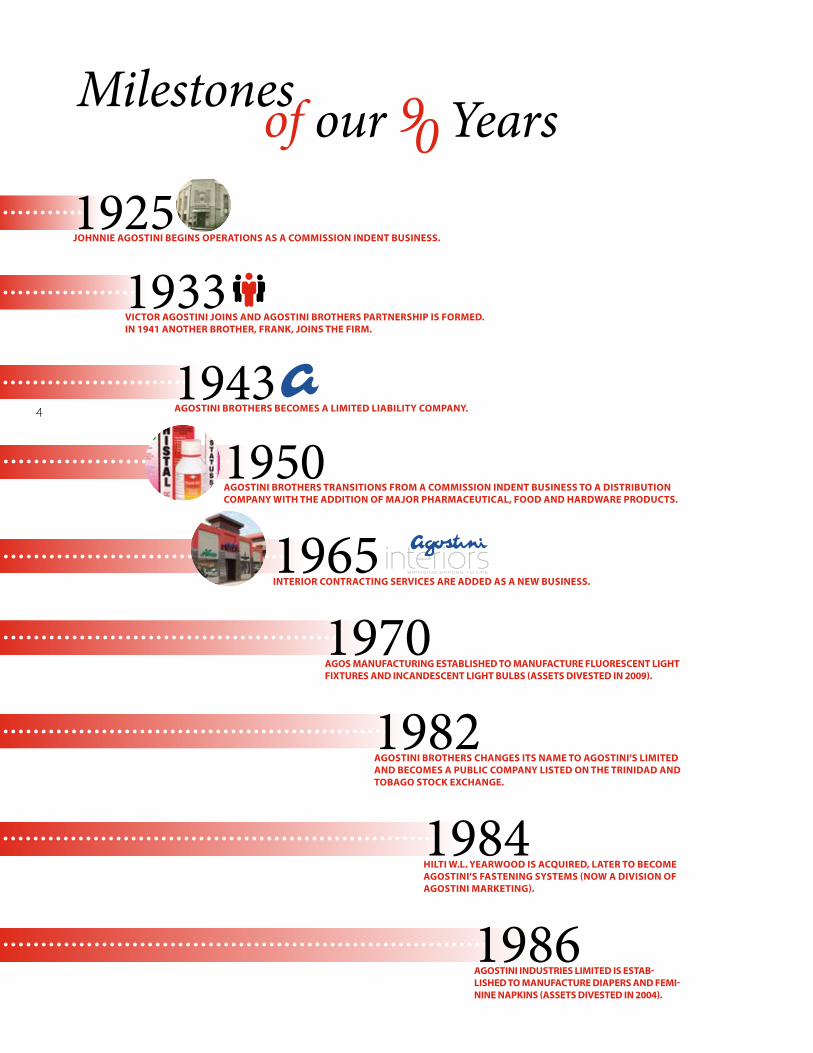

Milestonesof our 90 Years

1925JOHNNIE AGOSTINI BEGINS OPERATIONS AS A COMMISSION INDENT BUSINESS.

1933VICTOR AGOSTINI JOINS AND AGOSTINI BROTHERS PARTNERSHIP IS FORMED. IN 1941 ANOTHER BROTHER, FRANK, JOINS THE FIRM.

1943AGOSTINI BROTHERS BECOMES A LIMITED LIABILITY COMPANY.

1950AGOSTINI BROTHERS TRANSITIONS FROM A COMMISSION INDENT BUSINESS TO A DISTRIBUTION COMPANY WITH THE ADDITION OF MAJOR PHARMACEUTICAL, FOOD AND HARDWARE PRODUCTS.

1965INTERIOR CONTRACTING SERVICES ARE ADDED AS A NEW BUSINESS.

1970AGOS MANUFACTURING ESTABLISHED TO MANUFACTURE FLUORESCENT LIGHT FIXTURES AND INCANDESCENT LIGHT BULBS (ASSETS DIVESTED IN 2009).

1982AGOSTINI BROTHERS CHANGES ITS NAME TO AGOSTINI’S LIMITED AND BECOMES A PUBLIC COMPANY LISTED ON THE TRINIDAD AND TOBAGO STOCK EXCHANGE.

1984HILTI W.L. YEARWOOD IS ACQUIRED, LATER TO BECOME AGOSTINI’S FASTENING SYSTEMS (NOW A DIVISION OF AGOSTINI MARKETING).

1986AGOSTINI INDUSTRIES LIMITED IS ESTAB-LISHED TO MANUFACTURE DIAPERS AND FEMI-NINE NAPKINS (ASSETS DIVESTED IN 2004).

5

Caribbean Distribution Partners Limited

1993GORDON GRANT TRADING, A DISTRIBUTION COMPANY SPECIALISING IN PHARMACEUTICAL DISTRIBUTION, IS ACQUIRED. AGOSTINI MARKET-

ING’S PHARMACEUTICAL LINES ARE MERGED INTO THIS COMPANY, WHICH IS RENAMED AGOSTINI PHARMACEUTICAL LIMITED.

1995AGOSTINI’S ACQUIRES A MAJORITY SHAREHOLDING IN ROSCO SALES LIMITED,

AN OILFIELD SUPPLY COMPANY FOUNDED IN 1950.

2000AGOSTINI INDUSTRIES: THE GROUP EXPANDS INTO LOW-COST HOUSING AND TOWNHOUSE CONSTRUCTION, AND

CONSTRUCTS 30 TOWNHOUSES AND OVER 300 LOWCOST SINGLE FAMILY HOMES (ASSETS DIVESTED IN 2010).

2000PETROAVANCE TRINIDAD LIMITED, AN OILFIELD SUPPLY COMPANY, IS ACQUIRED AND MERGED WITH ROSCO SALES TO

BECOME ROSCO PETROAVANCE LIMITED.

2008HAND ARNOLD TRINIDAD LIMITED, A LARGE DIVERSIFIED CONSUMER PRODUCTS DISTRIBU-

TOR ESTABLISHED IN 1920, IS ACQUIRED. IN JULY 2015, IT BECOMES PART OF CARIBBEAN DISTRIBUTION PARTNERS LIMITED.

2010VICTOR E. MOUTTET LIMITED ACQUIRES A CONTROLLING INTEREST IN AGOSTINI’S

LIMITED WITH ITS SALE OF SMITH ROBERTSON & CO. LIMITED, A MAJOR PHARMACEUTICAL DISTRIBUTOR FOUNDED IN 1894, AND THE ACQUISITION

OF SUPERPHARM LIMITED, A MAJOR RETAIL PHARMACY CHAIN, WHICH BEGAN OPERATIONS IN 2005.

2011IN JULY 2011, AGOSTINI PHARMACEUTICAL IS AMALGAMATED INTO

SMITH ROBERTSON & COMPANY LIMITED.

2012AGOSTINI’S LIMITED RE-BRANDED

“EVERY BUSINESS A BENCHMARK”

2015CARIBBEAN DISTRIBUTION PARTNERS LTD.

JOINT VENTURE WITH GODDARD ENTERPRISES

AN

NU

AL

REP

OR

T 20

15

6

Smith Robertson & Company Limited

J. Cumming & Co. was established in Trinidad in the 1830’s. In 1894 when two Scotsmen, Adam Smith and William Robertson, decided to form a partnership. Mr. Robertson had been employed by J. Cumming & Co and purchased the company and changed its name to Smith Robertson. In 1929 the company was registered as a limited liability company. In the early years Smith Robertson was in the indent business and represented many lines from Canada, the USA and insurance coverage from London. It also offered Champagne and Brandy from France.

In 1929 Mr. Eddie Barcant became a director of the company and would later buy out the owners of the day and bring in his two sons, David and Geoffrey.

Over the years, many agencies were added in the pharmaceutical and personal care areas.

In 1938 Wyeth, previously American Home Products and more recently purchased by Pfizer, was their first pharmaceutical line. In 1956 the Revlon line of Cosmetics and Toiletries joined their offerings. Other early Pharma lines carried by the company were Ayerst, ICI, Smith Kline & French and Lederle.

In the mid 1980’s, Geigy (now Novartis), Medimpex, Beiersdorf (Nivea), ICI (which became Zeneca then AstraZeneca) and Abbott were added.

In 1998, when Smith Robertson was bought by Victor E.

C.E. Mouttet - ChairmanR.A. Farah - CEO/DirectorI. Maharaj - DirectorM. Stagg - DirectorN.R. Ramjohn - Finance Director/SecretaryA.J. Agostini - Non-Exec Director

Mouttet Limited, all of the pharmaceutical lines handled by their distribution company, VEMCO Limited were transferred into Smith Robertson and it became the largest distributor of pharmaceuticals in Trinidad and Tobago. VEMCO had itself been in the pharmaceutical business for several years and in the 1990’s had managed such agencies as Aventis (now Sanofi Aventis), Pharmacia & Upjohn (since bought over by Pfzier) and Carlilse Laboratories. After the merger, new lines were acquired such as Bayer Schering, Glaxo Smith Kline, Merck Sharp & Dohme and Johnson & Johnson.

Agostini’s had also operated a Pharmaceutical division for more than fifty years, and had spun it off into a focused Pharmaceutical distribution company ten years earlier. It had also acquired and merged into it Hand Arnold Pharmaceutical that had represented Pfizer among other lines. Smith Robertson was acquired by Agostini’s in August 2010 and shortly thereafter Agostini Pharmaceutical Limited, which was then distributing Pharmaceutical lines for over sixty years, such as Roche, Wyeth, Eli lilly and Ciba (now Novartis) was absorbed into Smith Robertson and Company Limited.

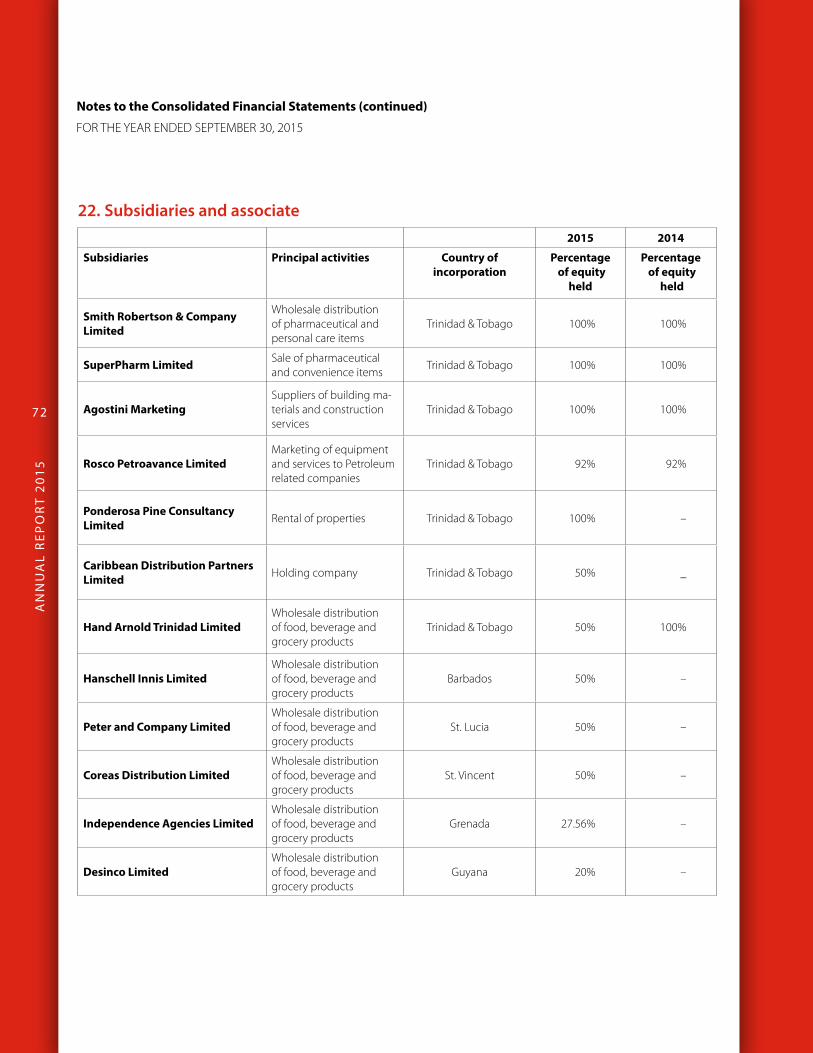

Companies 100% owned by Agostini’s:

Trinidad & Tobago

AN

NU

AL

REP

OR

T 20

15

7

Companies 100% owned by Agostini’s (cont'd):

Agostini Marketing

Agostini Marketing started as the trading arm of Agostini's Limited. Its roots go back to the company's beginning in 1925, when Johnnie Agostini, whose forefathers came from Corsica in 1794, began a commission indent business. The early lines that Johnnie Agostini handled were men's socks, flour, Soya beans and pickled meats. In 1933 he was joined by his brother Albert Victor Agostini and a partnership was registered as Agostini Brothers.

Eight years later, their youngest brother, Frank "Sonny" Agostini joined the firm and in 1943 Agostini Brothers became a limited liability company. Nearly forty years after, in 1982, the company became a publicly listed company quoted on the Trinidad and Tobago Stock Exchange. At that time the "Brothers" was dropped from the name and the company became know as "Agostini's Limited".

During the last ninety years, the company has been involved in many aspects of business here in Trinidad. In 1933 an Insurance Division was formed and later in 1938 when George Farah joined the company, the division was expanded to handle all classes of Insurance. Later this division would be divested. In the late 1930's the company diversified from an indent type of business into the distribution arena. The early products included "Carlings" beer, "Arrow" shirts and "Standard" brand condensed milk.

In the 1950's, the Company continued adding to the list of products it distributed, with the addition of

A.J. Agostini - ChairmanA.B. Pashley - CEO / DirectorC.G. Bernard - DirectorR.A. Rodriguez - DirectorG.M. Agostini - Non-Exec DirectorT.K. Austin - Non-Exec DirectorR.A. Farah - Non-Exec Director

pharmaceutical lines from Hoffman La Roche, Wyeth Ayerst and Ciba Geigy. Later, Eli Lilly, A. H. Robins, Sanofi Aventis, Leo Pharma and Bayer would be added. The pharmaceutical division is now part of Smith Robertson.

In the 1960's our hardware section grew with the addition of plywood and a range of carpets, floorings, partitions and Armstrong flooring and ceilings. Interior contracting services became a natural addition to our offerings around this same time and continues to be a major part of the company's service offering.

In 1984 the Company acquired Hilti W. L. Yearwood Limited, a company that exclusively marketed the industrial range of Hilti products. This company now operates as the Abfast division of Agostini Marketing and now also markets Explosives, Sig and Ruger small arms and a range of ammunition.

In 1993 the company began its printery supplies division, offering a wide range of paper, imaging products and signage supplies.

Over the past few years the company has further expanded its distribution business with the addition of several hardware lines, Fursys demountable partitions and entered the retail arena with three decorative lighting stores that dual as retail Pratt & Lambert paint outlets.

Trinidad & Tobago

AN

NU

AL

REP

OR

T 20

15

8

SuperPharm Limited

Retail pharmacy and convenience store

The year was 2005, and the very first SuperPharm opened in Westmoorings.

The story of SuperPharm starts with the desire by enterprising local entrepreneurs to push the industry forward, and to do that in a simple but revolutionary manner put the needs of customers first. This meant being available and open when it is convenient for our customers, as opposed to when it's convenient for us.

The initial investors, went through a lengthy and detailed process with US-based consultants in the areas of store design, layout, brand strategy and product selection. Consultation brought up many questions. The main one was, what should SuperPharm be to customers? As the process continued everyone came to understand that to be valuable to a community, the stores had to be about convenience.

SuperPharm was designed to take that focus to a whole new level in Trinidad. Extended opening hours weren't enough, the stores would also be open on holidays, and on those days the hours would not be limited. SuperPharm is open until 11 pm, 7 days a week, 364 days a year. Only closing on Christmas Day.

Locations were carefully selected to ensure that they were convenient for the communities in which they operated. Parking was given priority.

C.E. Mouttet - ChairmanG. Maharaj - Managing DirectorM. Gonsalves Suite - DirectorJ.M.Aboud - Non-Exec DirectorA.J.Agostini - Non-Exec DirectorL.M. Mackenzie - Non-Exec DirectorJ.J.Rahael - Non-Exec DirectorN. M. Fung - CFO / Company Secretary

Another important aspect of convenience was putting together a large variety of products, to be much more than a pharmacy. The comparison of SuperPharm to big box US-based pharmacies like Walgreens and CVS is not unfounded, the similarity is by deliberate design.

SuperPharm Westmoorings had an impact on everyone who walked through the doors on opening day, and also on everyone who discovered the final aspect of convenience, the drive-thru window.

The Agostini Group was happy to acquire SuperPharm in 2010 and to continue building the brand by adding stores in several additional locations.

Today we have eight stores strategically located in Westmoorings, Valsayn, Chaguanas, Maraval, Gulf View, Trincity, Marabella and Diego Martin. Our ninth store is currently under construction in Mausica and scheduled to be opened at the end of 2016.

Many people can’t remember what they did before Superpharm came into their area, transforming the way they shopped and contributing to their well being.

Additional stores are in the process of being planned as we know there are many other communities that would welcome a well stocked and convenient pharmacy and convenience store in their neighbourhood.

Trinidad & Tobago

Companies 100% owned by Agostini’s (cont'd):

AN

NU

AL

REP

OR

T 20

15

9

Rosco Petroavance Limited

Rosco Petroavance Limited (RPL), formerly English Drilling Equipment Company Limited (Edeco), was founded by Mr. Elgen Scott on 21 April 1951. Mr. Scott realised the potential of forming a business around importation & distribution of oilfield equipment and associated supplies. Edeco was very successful and grew rapidly to become a leading supplier, representing many quality manufacturers. Years later Edeco was sold and the company’s name was changed to Rosco Sales Limited.

In 1995 Rosco Sales Limited was purchased by Agostini’s Ltd [80%] together with Mr. Walter Bernard [20%] and Rosco became a subsidiary of the Agostini’s. Always looking to expand, Rosco acquired Petroavance Trinidad Limited in 2000. In 2009 both companies were merged, and the Company’s name was changed to Rosco Petroavance Limited.

Over the years, Rosco Petroavance Ltd has been able to grow and diversify into other sectors, doubling their sales over the last five years, while maintaining their dedication to excellent customer service and support. To match the range of diverse product offerings they market and service, they changed the operating structure of the business as they

A.J. Agostini - ChairmanWalter Bernard - Deputy ChairmanWayne Bernard - CEO/DirectorJ.P. Rostant - DirectorC.G. Bernard - Non-Exec DirectorR.A. Rodriguez - Non-Exec DirectorV. Balroop - CFO/Company Secretary

recognised that each product category required specialised personnel, equipment and management. They currently operate under six divisions, managed by individuals with long experience in their fields. These divisions are: Oil Well [Harbison Fischer, National Oilwell Varco, Stren, Echometer], Rig Spares [Oil States, Rexroth, Braden Paccar, Martin Sprocket], Valves [Forum Energy, PBV, DSI, Balon, Quadrant, Mueller, GE], Hydraulics [Effer Cranes, Eaton Hydraulics, OMFB, Spx Powerteam, Char Lynn, Jurop, Permco], Safety [Capital Safety, DBI/SALA, protector, Mecanix, Dickies, Amot, Charlwyn, Roda Deco] and Service.

All their products are sold through sole distributorship channels. Rosco Petroavance Ltd has the capacity and capabilities to continue to be a major player in the Oil & Gas, Petrochemical, Process, Construction and Marine Industries in which they presently operate. In 2016 they will launch their seventh division, Mobil Lubricants.

With dedication to quality, as shown by their recent re-certification from STOW, Rosco has become a company known for its quality employees supporting quality products and quality service.

Trinidad & Tobago

Companies 92% owned by Agostini’s:

AN

NU

AL

REP

OR

T 20

15

10

AN

NU

AL

REP

OR

T 20

15

10 Alliances

AN

NU

AL

REP

OR

T 20

15

11

for GrowthIn July 2015, Agostini’s Limited formed an alliance with Goddard Enterprises Limited to form a jointly-owned company, Caribbean Distribution Partners Limited.Into this company were transferred the two groups’ fast-moving consumer goods companies.

& =Caribbean Distribution Partners Limited

AN

NU

AL

RE

PO

RT

20

15

11

AN

NU

AL

REP

OR

T 20

15

12

CARIBBEAN DISTRIBUTION PARTNERS LIMITED

Partnering for Growth in the Region.

Our group, together with the Goddard Enterprises Ltd group of Barbados, entered into a partnership arrange-ment in July 2015, in order to use our combined strengths in FMCG towards creating a powerful distribution net-work in the Caribbean region.

As a result we have transferred the six FMCG distribution companies in the two groups into a 50/50 owned joint venture company named Caribbean Distribution Partners Limited [CDP].

The six companies:-

1. Hand Arnold Trinidad Limited, a 95 year-old Trinidad-based distribution company.

2. Hanschell Inniss Limited, which has been operating in Barbados for the past 131 years.

Caribbean Distribution Partners Limited(a 50/50 JV between Agostini’s Limited and Goddard Enterprises Limited)

Caribbean Distribution Partners Limited

C.E. Mouttet - ChairmanA.J. Agostini - DirectorA. Ali - DirectorC. A. Herbert - DirectorW. P. Putnam - DirectorR. Rajkumarsingh - DirectorT.D. Shuffler - CEO

3. Coreas Distribution Limited of St. Vincent, which is over 170 years old.

4. Peter & Company Ltd, a 131 year-old distribution company in St. Lucia.

5. Independence Agencies Limited, a 42 year-old Gre-nadian distribution company. CDP presently owns a 55.12% stake in this company.

6. Desinco Limited, a Guyanese distribution company with its roots formed in 1980. CDP presently owns a 40% stake in this company.

We expect that with this focus and strong distribution network, our group owned brands and those that we represent on behalf of our international partners, will see growth in the coming years, that will further position us to be the partner of choice, in the Caribbean region.

Trinidad & Tobago

Barbados

Guyana

Grenada

St Vincent

St Lucia

AN

NU

AL

REP

OR

T 20

15

13

HAND ARNOLD TRINIDAD LIMITED

Hand Arnold was founded in 1920 by two pioneering Canadians, John Hand and his friend Arnold then operat-ing out of Bermuda. They started as commission agents with Canadian products which included Heinz, Red Rose Salmon and Harvest Queen and Five Roses Flours from ‘The Lake of the Woods Milling Co.’ in Quebec.

Another early product was Klim powdered milk which was invented by the Canada Milk Company with whom Hand Arnold traded. In 1928. Bordens bought the Klim Brand which was later sold to Nestles.

Other products carried by the company also included Portland Cement, Kings Beer from Canada, Salt fish, Salt beef, Pig tail, Onions, Potatoes, Cheese, Butter, New Zea-land meat, Harvest Queen flour and Cigarettes from Brit-ish American Tobacco Company. Selling Life Insurance for Sun Life of Canada was also a line of business at that time.

By 1945 Messrs. Hand and Arnold had died, and their widows sold the branches to their respective managers. Arthur Hale, the manager in Trinidad, bought the Trini-dad branch and the new company was locally registered as Hand Arnold (Trinidad) Limited (HAL). Osmond Hale joined his father in the company in 1946 and his brother Peter came on board in 1960. Later Osmond’s son John Hale, became Managing Director.

By 1962 products sold in Pharmacies such as Plough Cop-pertone and the Jergens range were added. In 1967 Hand Arnold was relocated to Wrightson Road. In 1970 HAL

was computerised. The company ventured into cosmetic manufacturing in the early 1970’s after the negative list was introduced when they manufactured Jergens and Brylcreem under license. In the 1980’s a larger 70,000 sq ft warehouse facility was built in El Socorro. In 1990 the company faced its darkest period when during the at-tempted coup its warehouse was looted and plundered to the tune of $12m. A huge amount in those days. Had it not been for the tremendous support given by the company’s many suppliers who extended terms of up to a year to allow the company time to rebuild, it may not have survived at that time.

In 1992 the company moved into their newly constructed office building in their warehouse compound and in 1994 acquired Alfred Telfer and Company, a Pharmaceutical dis-tribution company marketing Pfizer and other products.

The company started selling Housewares in 1994, opened the Wines & Spirits department in 1997, added Kelloggs cereals in 1998, started with the high volume bulk New Zealand cheese category in 2002 and added the Anchor brand of cheese and butter in 2007. They actually were the largest local toy distributor and re-exporter for the period 1997 to 2005.

The Agostini’s group acquired the company in 2008 and brought it into the Caribbean Distribution Partners joint venture in July 2015.

A.J. Agostini - ChairmanS.A. Gunness-Balkissoon - CEO/DirectorS.K. Malzar - Finance Director/Company SecretaryS.J. Montano - DirectorA.Ali - Non Exec DirectorL.M. Mackenzie - Non-Exec DirectorR. Rajkumarsingh - Non-Exec DirectorT. D. Shuffler - Non Exec Director

100% owned by Caribbean Distribution Partners (a 50/50 JV between Agostini’s Limited and Goddard Enterprises Limited) (continued)

Trinidad & Tobago

AN

NU

AL

REP

OR

T 20

15

14

PETER & COMPANY LIMITED

124 Years of Service

In 1879 William Peter established a private coaling com-pany to provide mineral coal for merchant ships plying the Caribbean and South American waters. The venture flourished under his dynamic direction. By the turn of the century, Peter & Company was the “leading coal mer-chant in the West Indies”. William Peter, died in 1933, leav-ing the Company to his two sons Gregor and Allan. With the replacement of coal with oil as fuel for the shipping industry, the company was inevitably sailing into the dol-drums. William Peter’s great granddaughter Lilia together with her husband William Eaton struggled to maintain the business. Fortunately, Lilia’s friendship with Jeanette Goddard, a niece of the then Managing Director of the well known Barbados firm, would provide for the survival of Peter & Co. Ltd., when in 1961 of J. N Goddard & Sons of Barbados acquired majority shares in the company.

In January 2015, Peter & Company purchased ANSA McAl’s 1/3 shareholding stake in Bryden & Partners (St. Lucia) Ltd., a sister food & beverage company under the M&C Group of Companies banner, which is also owned by Goddard Enterprises Ltd. (GEL). The remaining shares in Brydens were purchased by Peter & Company (PCL) in June 2015 from M&C Ltd and the company divested its interests in all its non"food & beverage" operations and properties to focus on it fast moving consumer goods division.

In July 2015, Caribbean Distribution Partners Ltd. (a joint venture between Agostini Ltd. and GEL), purchased 100% of the shares of Peter & Company Ltd. and the company merged its Brydens and PCL food & beverage operations into a single legal entity trading as Peter & Company Dis-tribution Ltd.

T. D. Shuffler - ChairmanR. L. Leonard - CEO / DirectorA. J. Agostini - DirectorA. Ali - Non Exec DirectorC. O. Boxill - CFO / Company Secretary

100% owned by Caribbean Distribution Partners (a 50/50 JV between Agostini’s Limited and Goddard Enterprises Limited)

St. Lucia

AN

NU

AL

REP

OR

T 20

15

15

HANSCHELL INNISS LIMITED

Hanschell & Company was founded in 1884 by Mr. Valdemar Hanschell. He was of Danish descent and came to Barbados from the Virgin Islands, continuing his trade in ship brokerage and eventually adding ship chandlery to his services. Cockspur Rum was also founded in 1884 as a Hanschell brand and with this addition, the company traded successfully into the twentieth century led by his sons.

During the 1930’s Mr. G. A Larsen, then Attorney to the company and also from Denmark, joined the business and the company changed its name to Hanschell, Larsen & Co. Ltd. The company continued through most of the early part of the century focused on ship chandlery and branching out into the local liquor market with Cockspur and Best Matured Rums as well as imported spirits.

The company Hanschell Inniss Limited as we know it today was formed in 1970 through the merging of J. H. Inniss & Son Ltd. and Hanschell Larsen & Co. Ltd.. J. H. Inniss & Son Ltd was the importing arm of a merchant company, which developed its agency business as a result of being appointed as the agents for world renown brands such as Mars and Kellogg’s. The combined company Hanschell Inniss Limited continued its operations in ship chandlery while expanding its market share in servicing the hotel sector and well as selling FMCG products to the retail sector.

In 1973 Goddard’s agreed to buy out the main shareholders in Hanschell Inniss and combined it with an

existing Goddard subsidiary which already represented several food and spirits lines. Investment in what was then an ultra-modern facility at the current location at Kensington allowed the company to expand further and this included the birth of the EVE brand of hamburgers and hot dogs from its own meat processing plant (which would later become Hipac Limited) and later the launch of the Farmers Choice brand as well. Further growth was derived through the acquisition of Atkinson & Wolfe, a leading distributor of meats and fish and supplier company to the hospitality trade. Simeon Hunte & Son Ltd. with a range of agencies complementary to the Hanschell brands was also acquired.

In 1992 a joint venture company with International Distillers & Vintners (IDV), part of the Grand Metropolitan Group of the UK was formed, ID Caribbean (Distribution) Limited was formed to handle the distribution and marketing of all IDV brands and the Hanschell Inniss brands of rum and locally produced spirits throughout the Caribbean. ID Caribbean was subsequently merged with Hanschell Inniss Limited resulting in a Wines & Spirits division being formed in each of the distribution companies in the Goddard’s group.

Today Hanschell Inniss is a leading FMCG distributor in Barbados and as of July 2015, became one of the companies in the Caribbean Distribution Partners joint venture.

100% owned by Caribbean Distribution Partners (a 50/50 JV between Agostini’s Limited and Goddard Enterprises Limited) (continued)

T. D. Shuffler - ChairmanA.J. Agostini - Non Exec DirectorA. Ali - Non Exec DirectorR. Rajkumarsingh - Non Exec DirectorT. Greaves - CFO

Barbados

AN

NU

AL

REP

OR

T 20

15

16

100% owned by Caribbean Distribution Partners (a 50/50 JV between Agostini’s Limited and Goddard Enterprises Limited)

COREA’S DISTRIBUTION LIMITED

The history of Coreas Distribution Ltd, which was separat-ed from Coreas Hazells Inc. in July 2015, to become part of the Goddard’s and Agostini’s joint venture, Caribbean Dis-tribution Partners Ltd, is a complex one as it has evolved from the amalgamation of several companies over the past 170 years.

Its earliest roots go back to Hazells Limited which was established in St. Vincent in 1845 and is the oldest reg-istered company in St. Vincent, with wholesale food and liquor being two of its departments that are relevant to the company today. This company was acquired by God-dard’s in 1981.

Before that, in 1962, Goddard Enterprises Limited ac-quired United Traders Limited, a privately owned com-pany which traded in hardware (Hardware Department), food (Supermarket), motor vehicles (Automotive Depart-ment) and a Department Store.

In 1963 Goddard’s purchased another privately owned company called Corea and Co Limited with similar trad-ing practices to the above and included other activities.

Later, in 1968, another private company was purchased – Gerry Palmer Limited. In 1973, H.D. Dear Ltd – a company that held lands at Cane Hall and several agencies includ-

ing B.A.T (British American Tobacco) – was also purchased.

In 1985, Goddard acquired 53.59% of the shares in W.B. Hutchinson & Co (St. Vincent) Limited and in 1990 all the remaining shares were acquired. WBH had a Food Distri-bution Department among others.

In February 2002, Coreas Trading Limited took over the trading activities of W.B. Hutchinson (St. V) Ltd. In June 2002, Corea’s Trading Ltd and Hazells Ltd amalgamated under the name – Coreas Hazells Inc. In July 2003, Coreas Hazells Inc and Goddard Enterprises (ST. V) Ltd amalgam-ated under the name – Coreas Hazells Inc.

Coreas Distribution Limited

T. D. Shuffler - ChairmanJ. J. Forde - CEO / DirectorA. J. Agostini - Non Exec DirectorW. P. Putnam - Non Exec DirectorR. Rajkumarsingh - Non Exec DirectorC. D. James - CFO / Company Secretary

Main Office / Warehouse

Secondary Warehouse

St. Vincent

AN

NU

AL

REP

OR

T 20

15

17

INDEPENDENCE AGENCIES LIMITED

Independence Agencies Limited was established in October 1973 by C.K. Ralph Sylvester. The company consisted of C.K. Sylvester as Managing Director, his son Ken, and Richard Smith who operated a sales van.

Some of the first suppliers that the Company represented were Akafa, who supplied DANO powdered milk, British American Tobacco, Becks and Orangeboom beer from Holland, Mc Callum’s whisky from the UK and matches from Swedish Match. The company also imported rice, flour and sugar in bulk from Canada, USA and Guyana respectively.

By 1985, the company relocated to a larger location with more warehouse space and chill room facilities to allow for storage of bigger brands like Anchor cheese and butter from New Zealand and Alaska condensed milk from Holland. In 1988, the Empire cinema building was purchased and renovated to be the new location of the Head Office and warehouse. Brian Sylvester, a younger son of the founder joined the company then as a new addition to the management team.

In 1994 another building was purchased in Grand Anse, which was renovated and CK’s Super Valu Cash and Carry was opened the following year. By the end of 1995 the company purchased another portion of land on the Maurice Bishop Highway and constructed a warehouse building.

In 2000, the company was approached by Goddard’s Enterprises of Barbados. The shareholders at that time agreed to sell 51% of the shares to Goddard’s.

In September 2004, the Head Office in St. George’s was destroyed by Hurricane Ivan and the entire operation had to be relocated into the C.K.’s Super Valu Building. Within two years a new Head Office was opened on the Maurice Bishop Highway. Today, Independence Agencies is one of the leading distributors in Grenada with one of the widest ranges of world-renowned brands.

Goddard’s had acquired another 4% taking their holding to 55.12% by the time IAL was brought into the Caribbean Distribution Partners joint venture in July 2015.

55.12% owned by Caribbean Distribution Partners (a 50/50 JV between Agostini’s Limited and Goddard Enterprises Limited) (continued)

T. D. Shuffler - ChairmanK.P. Sylvester - CEO / DirectorC. B. Sylvester - DirectorA. J. Agostini - Non Exec DirectorR. Rajkumarsingh - Non Exec DirectorK.A. Joseph - CFO / Company Secretary

Grenada

AN

NU

AL

REP

OR

T 20

15

18

DESINCO TRADING LIMITED

By 1980. consumer goods had become increasingly scarce and virtually unavailable in Guyana. With the country at a crossroads, severe constrains and restriction on imports were imposed by the government of the day.

Frank DeAbreu (a life insurance salesman) garnered together his meagre resources and began “suitcase trading” in small quantities of items that were in short supply, such as cricket balls and Jamaican Ambi and Lander products.

Six years later, as consumer demand grew for better quality products, DeAbreu began importing from Lever Brothers West Indies Limited, Nabisco Incorporated and Sterling Drugs Limited. He imported such products as Breeze detergent, Dot toilet cleaner, Royal icing sugar, Royal gelatin, Fresco drink mix, Panadol and several others.

40% owned by Caribbean Distribution Partners (a 50/50 JV between Agostini’s Limited and Goddard Enterprises Limited)

By 1990, DeAbreu’s investment capital became severely strained, which resulted in him teaming up with Bhagwan Singh to form DeSinco Trading Limited (i.e. a partnership of DeAbreu & Singh). The following year the partnership ended and DeAbreu acquired sole ownership.

By 1993, Desinco had four employees and was well on the way to realizsing the company’s dream and vision of “Being the best distributor of quality consumer’s goods in Guyana”.

Desinco continued to grow and maintain strong brand presence and in January 2015 welcomed Agostini’s Ltd as their new partner, selling them a 40% stake in the business.

In July 2015, Desinco Limited became part of the Caribbean Distribution Partners joint venture.

DeSinco

F. D. DeAbreu - ChairmanD. P. DeAbreu - DirectorA. P. DeAbreu - DirectorA.J. Agostini - Non Exec DirectorC. E. Mouttet - Non Exec DirectorR. Rajkumarsingh - Non Exec DirectorG. T. DeLisle - CFO/ Company Secretary

Guyana

AN

NU

AL

REP

OR

T 20

15

19

AN

NU

AL

REP

OR

T 20

15

19

Pharma-ceutical

Per-sonal Care

Food-stuff

House-hold Beer Wines Spirits To-

baccoIndus-

trialOil-field

Hard-ware

Con-tract-

ing

Nutri-tionals

• • •

• • • • • • • •

• • •• •

• • •

• • • • • •Coreas Distribution Limited • • • • • • • • •

• • • • • • • •

• • • • • • •DeSinco • •

Overview of Product Categories of our Companies

AN

NU

AL

REP

OR

T 20

15

20

Boardof Directors

Christian MouttetNon-Executive DirectorCEO / Director of Victor E. Mouttet LtdChairman of Prestige Holdings Ltd Director since 2010Chairman of the Corporate Gover-nance and Nomination Committee and Member of the Human Resources & Compensation Committee

Anthony J. AgostiniManaging Director of Agostini’s LtdDirector of Caribbean Finance Company LtdDirector since 1990

Joseph EsauChairman of Agostini’s LtdDirector of Prestige Holdings Ltd, Grace Kennedy Ltd and UWI Arthur Lok Jack Graduate School of BusinessDirector since 2004Member of the Human Resourc-es & Compensation Committee and Corporate Governance and Nomination Committee

Gregor NassiefNon-Executive Independent DirectorCEO of Cerca TechnologyDirector/Owner of Secret Bay (Dominica)Executive Chairman of Fort Young Hotel (Dominica)President of the Dominica Hotel & Tourism AssociationDirector since 2012

Barry A. DavisNon-Executive Indepen-dent DirectorFinancial Controller of Atlantic LNG Company of Trinidad & TobagoDirector since 2007Chairman of the Audit & Risk Committee and Member of the Corporate Governance and Nomina-tion Committee

AN

NU

AL

REP

OR

T 20

15

21

E. Gillian Warner-HudsonNon-Executive Indepen-dent DirectorManagement ConsultantDirector since 2009Member of the Human Resources & Compensa-tion Committee and Audit & Risk Committee

Reyaz W. Ahamad Non-Executive Director Chairman of Caribbean Finance Company Ltd Director of Southern Sales & Service Co Ltd and Trinidad and Tobago Chamber of Industry and CommerceDirector since 1996Committees: Chairman of Human Resources & Com-pensation Committee

Rajesh RajkumarsinghChief Financial Officer & Company Secretary of Agostini’s LtdDirector of First Citizens Bank Ltd.Company Secretary since 2014

Lisa M. MackenzieNon-Executive DirectorFinance Director of Access & Security Solutions Ltd.Director of Scotiabank Trinidad & Tobago Ltd and Scotialife Trinidad & Tobago LtdDirector since 2004

Amalia L. MaharajNon-Executive Independent DirectorPartner of Pollonais, Blanc, De la Bastide & JacelonDirector of Heroes Founda-tionDirector since 2011Member of the Audit & Risk Committee

Roger A. FarahNon-Executive Director CEO/Director of Smith Rob-ertson & Company LtdDirector of Vemco LtdDirector since 2010

AN

NU

AL

REP

OR

T 20

15

22Board ReportThe board of the company had four quarterly board meetings, one special board meeting to discuss the formation of Caribbean Distribution Partners Ltd and a strategic review / Plans and Budget meeting.

The average number of attendees at board meetings were 9.8 out of 10.

Board Committee Mandates & CommitteesCorporate Governance & Nomination Committee

The Committee makes appropriate recommenda-tions to the board based on the following:-

To monitor best practices for governance worldwide and review the Company’s governance practices to ensure they continue to exemplify appropriately high standards of corporate governance.

To recommend to the Board for consideration and adoption :

• The membership and mandates of Board Committees.

• The size and composition of the Board.

• Suitable candidates for nomination as Non- Executive Directors.

• Appointments to the Boards of Subsidiary, Affiliate and Associate Companies.

• The communication process between the Board and Management.

• Approval of the appointments of Executives to the Boards of companies outside the Agostini’s Limited Group.

To establish/review policies and procedures with respect to transactions between the Company, its subsidiaries and affiliates and Related Parties, Executive Officers and Directors.

To establish/monitor an appropriate Code of Conduct for the Company, its Executives, Managers and Employees and consider and deal with all matters of an ethical nature involving Executives and Non-Executive Directors.

To review as required and at least every two (2) years, the mandates and composition of Board committees.

To review the performance of Directors at least every two (2) years, by no later than August 31 of the review year.

To establish/monitor an appropriate procedure governing the trading in the Company’s securities by Directors and Officers.

To address any matter of Corporate Governance as delegated by the Board from time to time and to report to the Board on same.

Reporting of Committee Resolutions

The Committee shall report its resolutions by way of recommendations to the full Board for consideration and adoption at the next meeting of the Board following such meeting of the Committee.

This committee met twice during the year.

Corporate Governance & Nomination Committee

Christian Mouttet (Chairman)Joseph EsauBarry Davis

CorporateGovernance

AN

NU

AL

REP

OR

T 20

15

23Audit & Risk Committee

This Committee is responsible for :-

Financial Reporting

To review, and challenge where necessary, the actions and judgments of management, in relation to the Company’s financial statements, operating and financial review, interim reports, preliminary announcements and related formal statements before submission to, and approval by, the Board, and before clearance by auditors. Particular attention should be paid to:

• Critical accounting policies and practices, the consistency of their application and any changes in them.

• Decisions requiring a significant element of judgement.

• The extent to which the financial statements are affected by any unusual transactions in the year and how they are disclosed.

• The clarity of disclosures.

• Significant adjustments resulting from the audit.

• The going concern assumption.

• Compliance with accounting standards.

• Compliance with stock exchange and other legal requirements.

• The review of the annual financial statements of the pension funds and tri-annual actuarial valuations.

• To consider other topics, as defined by the Board.

Internal Audit

To monitor and review the effectiveness of the Company’s Internal Audit function in the context of the Company’s overall risk management system.

To approve the appointment of the external provider or head of internal audit.

To consider and approve the scope of the internal audit and ensure it has adequate resources and appropriate access to information to enable it to perform its function effectively and in accordance with the relevant professional standards. The Committee shall also ensure the function has adequate standing and is free from management or other restrictions.

To review and assess the annual internal audit plan.

To review promptly all reports on the Company from the internal auditor.

To review and monitor management’s responsiveness to the findings and recommendations of the internal auditor.

External Audit

To oversee the Company’s relations with the external auditor.

To consider, and make recommendations on the appointment, reappointment and removal of the external auditor.

To approve the terms of engagement and the remuneration to be paid to the external auditor in respect of audit services provided.

To assess the qualification, expertise and resources, effectiveness and independence of the external auditors annually. Steps to consider include;

The Company is in compliance with the Trinidad & Tobago Corporate

Governance Code.

AN

NU

AL

REP

OR

T 20

15

24

Seeking reassurance that the auditors and their staff have no family, financial, employment, investment or business relationship with the company (other than in the normal course of business).

Seeking from the Audit firm, on an annual basis, information about policies and processes for maintaining independence and monitoring compliance with relevant requirements.

Monitoring the external audit firm’s compliance with applicable ethical guidance.

To discuss with the external auditor, before the audit commences, the annual audit plan including the nature and scope of the audit and appropriate levels of materiality.

To review with the external auditors, the findings of their work, including any major issues that arose during the course of the audit and have subsequently been resolved and those issues that have been left unresolved; key accounting and audit judgements, levels of errors identified during the audit, obtaining explanations from management and, where necessary the external auditors, as to why certain errors might remain unadjusted;

To assess, at the end of the audit cycle, the effectiveness of the audit process by:

Reviewing whether the auditor has met the agreed audit plan and understanding the reasons for any changes, including changes in perceived audit risks and the work undertaken by the external auditors to address those risks.

Consideration of the robustness and perceptiveness of the auditors in their handling of the key accounting and audit judgements identified and in responding to questions from the audit committee, and in their commentary, where appropriate, on the systems of internal control.

Obtaining feedback about the conduct of the audit from key people involved.

To review and monitor the content of the external auditor’s management letter, in order to assess whether it is based on a good understanding of the company’s business and establish whether recommendations have been acted upon and, if not, the reasons why they have not been acted upon;

To develop and recommend to the board the company’s policy in relation to the provision of non-audit services by

the auditor and ensure that the provision of such services does not impair the external auditor’s independence or objectivity.

Internal Control

To review the effectiveness of the Company’s procedures for whistleblowing and for detecting fraud;

To review management’s reports of the effectiveness of the systems for internal financial control and financial reporting;

To review the statement in the annual report and accounts on the company’s internal controls and risk management framework;

To monitor the integrity of the company’s internal financial controls;

To assess the effectiveness of the systems established by management to identify, manage and monitor both financial and non financial risks,

Risk

To consider any matters relating to the identification, assessment, monitoring and management of risks associated with the operations of the Group, that it determines to be appropriate and any other matters referred to it by the Board.

To consider, and make recommendations to the Board in connection with, the compliance by the Group with its Risk Appetite Statement.

To report to the Board on any material changes to the risk profile of the Group.

To monitor and refer to the Board any instances involving material breaches or potential breaches of the Group’s Risk Appetite Statement.

To review the annual insurance coverage and ensure all insurable risks are adequately covered.

The Audit & Risk Committee met four times during the year.

Audit & Risk Committee

Barry Davis (Chairman)Gillian Warner Hudson

Amalia Maharaj

Corporate Governance (continued)

AN

NU

AL

REP

OR

T 20

15

25

Human Resources, Compensationand Stock Options Committee

This Committee is responsible for all matters relating to the compensation policies of the Group. It reviews, approves or recommends to the Board of Directors suitable Compensation Policies, the compensation structure and programmes, and Stock Option grants to Senior Management.

The Committee’s primary responsibilities are as follows:-

To review and approve (if previously delegated by the Board) or recommend to the Board of Directors, for adoption, as appropriate, all Human Resource and Compensation Policies of the Agostini’s Limited Group.

To review and recommend to the Board for approval, the compensation structure and incentive programmes for the Group Managing Director and other Executives. The Group Managing Director may also consult with the Committee regarding the compensation structure and programmes for Managers, whose compensation will be determined by the Group Managing Director, consistent with the guidelines set by the Committee.

To propose, within the guidelines set out in the Company’s compensation structure, for approval for the Board, annual Stock Option/ESOP grants under the Company’s Long Term Incentive Plan, and Annual Bonus and other Incentive Based awards to Executives and other qualifying employees.

To review the compensation paid to Non-Executive Directors and recommend appropriate adjustments from time to time.

To review and approve management succession plans for Executive Officers.

To review with the Group Managing Director and to recommend to the Board, appointments of all officers at or above the level of General Manager throughout the Agostini’s Limited Group.

To monitor the Executive Medical Examination Policy and process, including the approval of the physician.

To address any matters of Human Resources or Compensation as delegated by the Board from time to time and to report to the Board on same.

Reporting of Committee Resolutions

The Committee shall report its resolutions by way of recommendations to the full Board for consideration and adoption at the next meeting of the Board following such meeting of the Committee.

This Committee met once during the year.

HR, Compensation & Stock Options Committee

Reyaz Ahamad (Chairman)

Joseph Esau

Christian Mouttet

Barry Davis

AN

NU

AL

REP

OR

T 20

15

26

AN

NU

AL

RE

PO

RT

20

15

26

Industrial and Construction

Agostini Marketing, our building products and contracting services business, achieved record results.

Rosco Petroavance, our oilfield, industrial and hydraulic products business, had a very challenging year, and recorded substantially lower profit due to the steep fall in oil and gas prices that affected their main customer base. They have recently completed a new and expanded office and warehouse facility, and will be launching the ExxonMobil lubricants product line in January 2016; we expect this to support the currently depressed energy segment of the business.

Fast Moving Consumer Goods [FMCG]

Last July we entered into a joint venture with Goddard Enterprises Ltd of Barbados, forming Caribbean Distribution Partners Ltd [CDP], which now holds the FMCG businesses of both groups.

Hand Arnold Trinidad Limited, Hanschell Inniss Limited of Barbados and Peter & Company Limited of St Lucia all had a challenging year, and performed below expectations. Coreas Distribution Limited of St Vincent, Independence Agencies Limited of Grenada [55.12%] and Desinco Limited of Guyana [40%], recorded good results.

CDP will be investing heavily in infrastructure and systems to modernize the operations and to accommodate new lines that the synergies of the two Groups will deliver, and we are positive about the future of this JV.

CONSOLIDATED RESULTSAND FINANCIAL POSITION

Group sales and profit attributable to shareholders for the year ended September 30, 2015 amounted to $ 1.71 billion and $ 80.6 million, compared with $1.36 billion and $79.9 million in the previous year, respectively. Earnings per share was $1.37 compared with $1.36 in 2014. Included in these results are $9.3m in non-recurring costs associated with the HDC arbitration, refinancing penalties and expenses related to our investment in the region, all previously reported on in previous quarters.

Our year-end debt to equity ratio remains strong at 23:77 after funding an additional $90 million investment in the Joint Venture with Goddard Enterprises Limited.

OPERATIONS REVIEW AND SEGMENT ANALYSIS

Pharmaceutical & Personal Care

Smith Robertson, our Pharmaceutical and Personal Care distribution Company, again produced strong results, and continues to be a significant contributor to the Group’s performance.

SuperPharm, with eight locations, also had an excellent year that saw record results in sales and profit. Our planned Mausica store, which is part of a property being developed by the landowner, has been progressing very slowly but we are hoping for a late 2016 opening.

Chairman’sRemarks

JOSEPH P. ESAU

AN

NU

AL

REP

OR

T 20

15

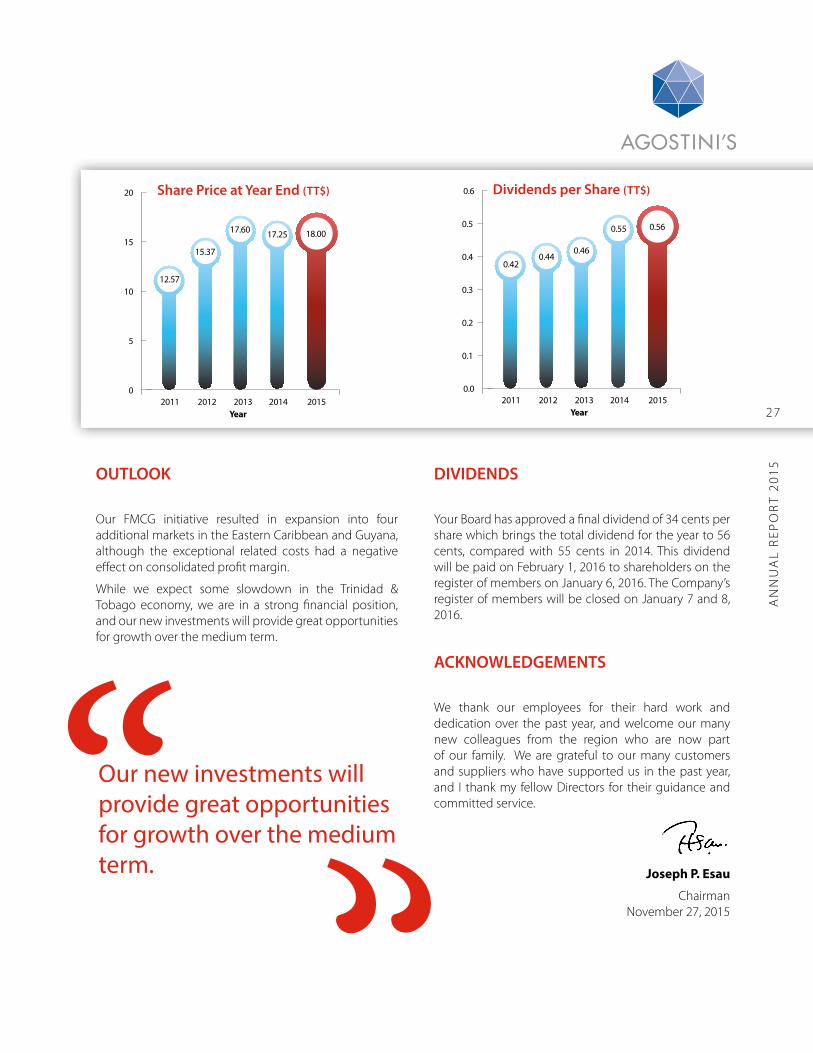

2727

0.0

0.1

0.2

0.3

0.4

0.5

0.6

Year2011 2012 2013 2014 2015

0.440.42

0.55

0.46

0.56

Our new investments will provide great opportunities for growth over the medium term.

OUTLOOK

Our FMCG initiative resulted in expansion into four additional markets in the Eastern Caribbean and Guyana, although the exceptional related costs had a negative effect on consolidated profit margin.

While we expect some slowdown in the Trinidad & Tobago economy, we are in a strong financial position, and our new investments will provide great opportunities for growth over the medium term.

DIVIDENDS

Your Board has approved a final dividend of 34 cents per share which brings the total dividend for the year to 56 cents, compared with 55 cents in 2014. This dividend will be paid on February 1, 2016 to shareholders on the register of members on January 6, 2016. The Company’s register of members will be closed on January 7 and 8, 2016.

ACKNOWLEDGEMENTS

We thank our employees for their hard work and dedication over the past year, and welcome our many new colleagues from the region who are now part of our family. We are grateful to our many customers and suppliers who have supported us in the past year, and I thank my fellow Directors for their guidance and committed service.

Joseph P. Esau

ChairmanNovember 27, 2015

Dividends per Share (TT$)Share Price at Year End (TT$)

0

5

10

15

20

Year2011 2012 2013 2014 2015

15.37

12.57

17.2517.60 18.00

AN

NU

AL

REP

OR

T 20

15

28

FINANCIAL HIGHLIGHTS 2015 2014 % Increase $’000 $’000 Gross Sales 1,811,788 1,410,639 28.44 Sales to Third Parties 1,706,617 1,359,383 25.54 Operating Profit 124,273 123,696 0.47 Profit before Tax 113,839 107,145 6.25 Profit for the Year 82,175 80,546 2.02 Profit attritutable to Shareholders 80,576 79,932 0.81 Stock Units In Issue ('000) 58,704 58,704 - Earnings per Share $1.37 $1.36 0.74 Total Dividends 32,874 32,287 1.82 Total Assets 1,513,617 955,373 58.43 Stockholder's Equity 747,358 555,305 34.59

Management Discussion

& Analysis

ANTHONY AGOSTINI

Agostini’s expands regionally in its 90th anniversary year.

The group’s 90th year of operation in 2015 was a trans-formational one. On January 1, 2015 we acquired a 40% shareholding in Desinco Limited in Guyana, our first in-vestment outside of Trinidad and Tobago in the Fast-Mov-ing Consumer Goods (FMCG) area. This was followed by our acquisition of Facey Trading Limited in Barbados in February. During this period we were also in discussions with Goddard Enterprises Limited, a Barbados-based con-glomerate, to pool our FMCG resources in the region. This arrangement was concluded on July 1, 2015, when we entered into a 50/50 joint venture with Goddard’s, form-ing Caribbean Distribution Partners Limited (CDP). We transferred our holdings in Hand Arnold Trinidad Limited of Trinidad and Tobago, Desinco Limited of Guyana and Facey Trading Limited of Barbados into CDP and God-dard’s transferred their holdings in Hanschell Inniss Lim-

ited of Barbados, Peter & Company Limited of St. Lucia, Coreas Distribution Limited of St. Vincent, all of which they owned 100%, and also their 55.12% holding in In-dependence Agencies Limited of Grenada into the joint venture.

In August we closed Facey Trading and moved their significant lines into Hanschell Inniss. This platform across six Caribbean territories has provided us with an excellent opportunity to leverage our group’s own brands, those owned by Goddard Enterprises and other imported brands, where we could offer our unique marketing and distribution expertise and a wider range of international brands. The first international addition to our distribution network has been the Campbell’s line, which covers Campbell’s soups, V8 juices, Pepperidge Farm cookies and Prego.

AN

NU

AL

RE

PO

RT

20

15

28

29

The sales of the group grew by 25% to $1.7 billion and profit before taxation also grew by 6% to $113 million. This resulted in our profit after tax being just above the prior year’s at $80.6 million. Contributing factors to prof-its being close to the prior year’s were higher tax rates in the region, penalties paid on our debt restructuring, which were not allowable for tax purposes, one-off legal and other expenses related to our investment in our re-gional joint venture and one-off legal and arbitration fees incurred in our matter with the Housing Development Corporation (HDC). The decision on the latter is expected in the near future. We have fully provided for the mon-ies owed to us and for the expected legal and arbitration fees.

PHARMACEUTICAL AND PERSONAL CARE DISTRIBUTION

Our pharmaceutical distribution company, Smith Robert-son, recorded another strong performance in 2015. This subsidiary continues to be the leading supplier of both prescription and over-the counter (OTC) pharmaceuticals to the government and the private sectors. In addition to Pharmaceuticals, the company also has a significant port-folio of Personal Care Brands, for which the company re-ceived awards during the past year from two major Health & Beauty Care Suppliers in recognition of its performance and distribution of their products. Smith Robertson con-tinues to serve market needs at a superior level through the provision of quality products within an efficient dis-tribution framework.

RETAIL

SuperPharm opened its eighth big box outlet in Diego Martin in November 2014 and has been well received by the residents of the area. This additional outlet assisted in the achievement of another record year for sales and profit. The building of our store at Mausica, Arima, which is being constructed by the property owner, continues to face setbacks. We believe progress will be made in 2016 and look forward to the opening in late 2016. We con-tinue to look for suitable sites to expand our footprint in areas we do not currently serve.

AN

NU

AL

REP

OR

T 20

15

29

0

500

1,000

1,500

2,000

Year2011 2012 2013 2014 2015

1,2941,2561,3591,313

1,707

Turnover (TT$ million)

0

30

60

90

120

150

Year2011 2012 2013 2014 2015

99101

123

104

124

Operating Profit (TT$ million)

AN

NU

AL

REP

OR

T 20

15

30

MD&A (continued)

FAST MOVING CONSUMER GOODS (FMCG)

With our joint venture company CDP, we expect that our learnings and synergies in the FMCG sector, together with the transfer of the distribution of the two group brands into the various companies, will allow for growth and success going forward.

The subsidiaries of CDP are:-

Hand Arnold Trinidad Limited -100%

Hand Arnold had a challenging year with commodity prices falling and margins being squeezed as a result. With pricing now stabilised and the Goddard lines of Bop and Beep being distributed by Hand Arnold from January 2016, we can expect much improved results in the year ahead.

Hanschell Inniss Limited - 100%

Hanschell Inniss had a difficult year as they struggled with the implementation of a new IT platform and a sluggish Barbados economy. With the new lines we added from the Facey Trading acquisition and the transfer of the Swiss lines from January 2016, we can expect a quick turn-around. A new distribution facility to cater for Hanschell's expanded business is under consideration.

Peter & Company Limited - 100%

The amalgamation of Bryden & Partners with Peter & Company is nearing completion. The expanded offices and warehousing facility at Cul de Sac should be com-pleted by the company's third quarter. The full benefits of this merger will be more evident when this is completed. We can therefore expect better results from this company in 2016.

Coreas Distribution Limited - 100%

Coreas had a good year but suffered a setback when their "Food Mart" in the heart of downtown Kingstown was de-stroyed by fire in August 2015. Rebuilding at the same site is about to commence. An expanded distribution facility at Diamond is being planned.

Independence Agencies Limited - 55.12%

Independence Agencies had a good year in spite of the challenges facing the Grenadian economy. An expansion to their warehouse facility will commence in early 2016.

Desinco Limited - 40%

Desinco had an excellent nine months and substantially expanded its product offering during the year. With sev-eral additional lines coming on stream in early 2016, we can expect their growth to continue.

Agostini Marketing had a record year in 2015, driven by a wide number of interior contracting contracts and by sales of building materials being more robust than in the recent past.

AN

NU

AL

REP

OR

T 20

15

3131

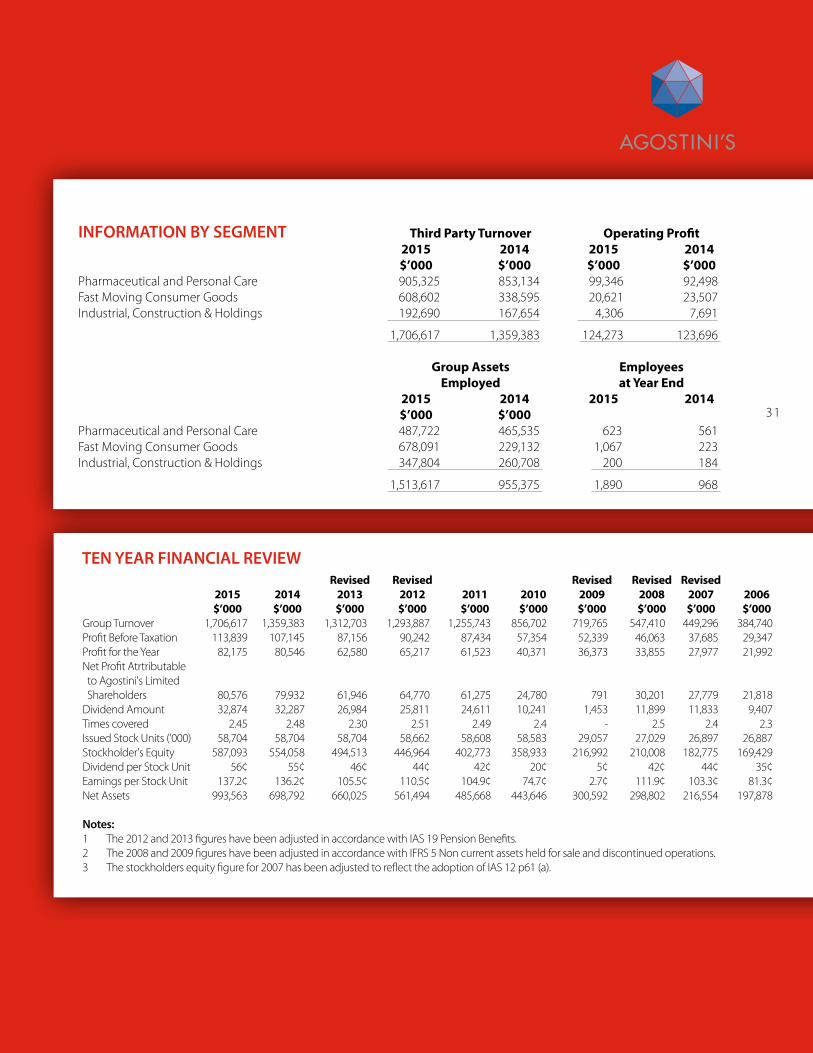

TEN YEAR FINANCIAL REVIEW Revised Revised Revised Revised Revised 2015 2014 2013 2012 2011 2010 2009 2008 2007 2006 $’000 $’000 $’000 $’000 $’000 $’000 $’000 $’000 $’000 $’000Group Turnover 1,706,617 1,359,383 1,312,703 1,293,887 1,255,743 856,702 719,765 547,410 449,296 384,740 Profit Before Taxation 113,839 107,145 87,156 90,242 87,434 57,354 52,339 46,063 37,685 29,347 Profit for the Year 82,175 80,546 62,580 65,217 61,523 40,371 36,373 33,855 27,977 21,992 Net Profit Atrtributable to Agostini's Limited Shareholders 80,576 79,932 61,946 64,770 61,275 24,780 791 30,201 27,779 21,818 Dividend Amount 32,874 32,287 26,984 25,811 24,611 10,241 1,453 11,899 11,833 9,407 Times covered 2.45 2.48 2.30 2.51 2.49 2.4 - 2.5 2.4 2.3 Issued Stock Units ('000) 58,704 58,704 58,704 58,662 58,608 58,583 29,057 27,029 26,897 26,887 Stockholder's Equity 587,093 554,058 494,513 446,964 402,773 358,933 216,992 210,008 182,775 169,429 Dividend per Stock Unit 56¢ 55¢ 46¢ 44¢ 42¢ 20¢ 5¢ 42¢ 44¢ 35¢ Earnings per Stock Unit 137.2¢ 136.2¢ 105.5¢ 110.5¢ 104.9¢ 74.7¢ 2.7¢ 111.9¢ 103.3¢ 81.3¢ Net Assets 993,563 698,792 660,025 561,494 485,668 443,646 300,592 298,802 216,554 197,878 Notes: 1 The 2012 and 2013 figures have been adjusted in accordance with IAS 19 Pension Benefits.2 The 2008 and 2009 figures have been adjusted in accordance with IFRS 5 Non current assets held for sale and discontinued operations.3 The stockholders equity figure for 2007 has been adjusted to reflect the adoption of IAS 12 p61 (a).

INFORMATION BY SEGMENT Third Party Turnover Operating Profit 2015 2014 2015 2014 $’000 $’000 $’000 $’000Pharmaceutical and Personal Care 905,325 853,134 99,346 92,498Fast Moving Consumer Goods 608,602 338,595 20,621 23,507 Industrial, Construction & Holdings 192,690 167,654 4,306 7,691

1,706,617 1,359,383 124,273 123,696 Group Assets Employees Employed at Year End 2015 2014 2015 2014 $’000 $’000Pharmaceutical and Personal Care 487,722 465,535 623 561Fast Moving Consumer Goods 678,091 229,132 1,067 223 Industrial, Construction & Holdings 347,804 260,708 200 184

1,513,617 955,375 1,890 968

AN

NU

AL

REP

OR

T 20

15

32

MD&A (continued)

INDUSTRIAL & CONSTRUCTION PRODUCTS & SERVICESCONSTRUCTION

Agostini Marketing had a record year in 2015. This was driven by a wide number of interior contracting contracts and by sales of building materials being more robust than in the recent past.

ENERGY & INDUSTRIAL PRODUCTS & SERVICES

Rosco Petroavance’s performance suffered as they serve the oil and gas sector, which was depressed by low en-ergy prices. Their profit fell short of prior year as a result. Construction of the company’s new office and warehouse building has just been completed and is providing much needed additional space for storage and service activities. Rosco has been successful in securing the ExxonMobil lu-bricant distributorship and will launch the range in 2016. This should be a significant addition to their business in the years ahead.

PROPERTY RATIONALISATIONDuring the year we purchased the Kimberly Clark proper-ty on Chootoo Road. SuperPharm's office and warehouse will be moving there in the second quarter 2016. Surplus warehouse space has been rented.

Our Nelson Street property is for rent and sale. We pres-ently have 30% rented and another 30% to be finalised shortly, with the final available area attracting some inter-est.

CORPORATE SOCIAL RESPONSIBILITYDuring the year, the group donated to numerous chari-ties and worthy causes as a means of giving back to those less fortunate in our community. We have registered a Foundation and await its approval by the tax authorities, so that we can put it into full operation.

Anthony Agostini

Managing DirectorDecember 4, 2015

AN

NU

AL

REP

OR

T 20

15

33

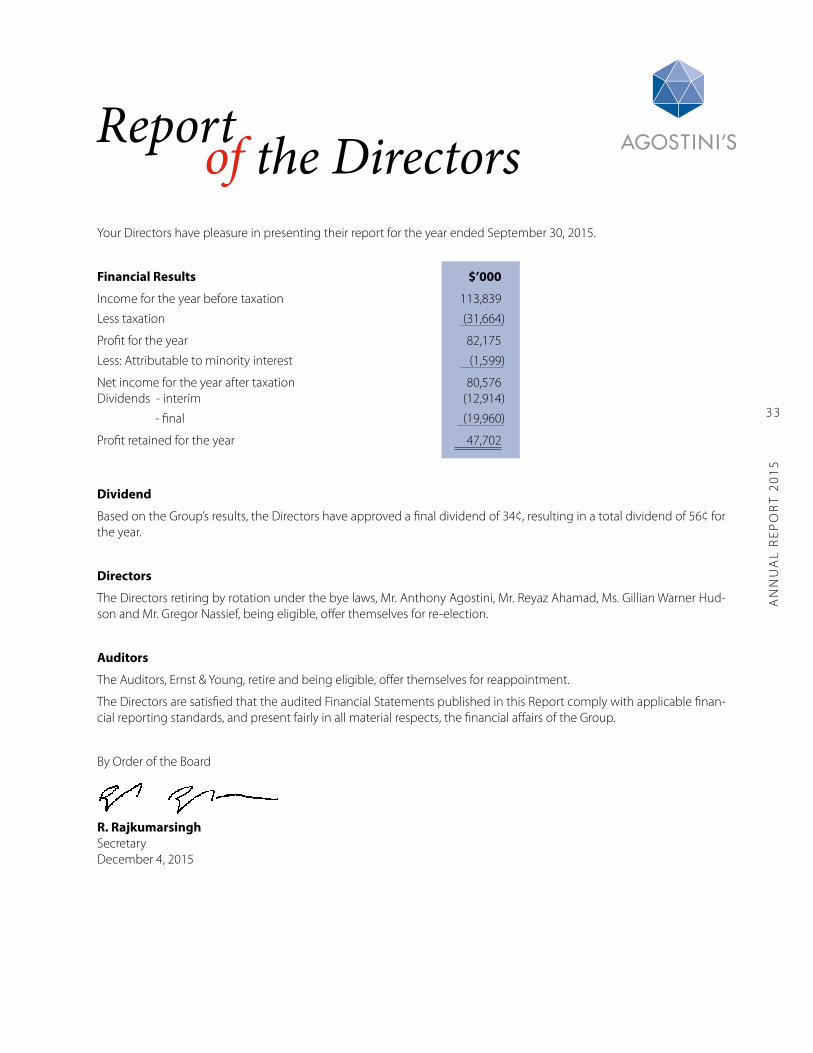

Your Directors have pleasure in presenting their report for the year ended September 30, 2015.

Financial Results $’000

Income for the year before taxation 113,839

Less taxation (31,664)

Profit for the year 82,175

Less: Attributable to minority interest (1,599)

Net income for the year after taxation 80,576 Dividends - interim (12,914)

- final (19,960)

Profit retained for the year 47,702

Dividend

Based on the Group’s results, the Directors have approved a final dividend of 34¢, resulting in a total dividend of 56¢ for the year.

Directors

The Directors retiring by rotation under the bye laws, Mr. Anthony Agostini, Mr. Reyaz Ahamad, Ms. Gillian Warner Hud-son and Mr. Gregor Nassief, being eligible, offer themselves for re-election.

Auditors

The Auditors, Ernst & Young, retire and being eligible, offer themselves for reappointment.

The Directors are satisfied that the audited Financial Statements published in this Report comply with applicable finan-cial reporting standards, and present fairly in all material respects, the financial affairs of the Group.

By Order of the Board

R. RajkumarsinghSecretaryDecember 4, 2015

Reportof the Directors

AN

NU

AL

REP

OR

T 20

15

34

Secretary and Registered Office:R. Rajkumarsingh

18 Victoria Avenue

Port of Spain

Registrars:RBC Trust (Trinidad and Tobago) Limited

8th Floor, 55 Independence Square

Port of Spain

Attorneys-at-Law:Pollonais, Blanc, De la Bastide & Jacelon

17 Pembroke Street

Port of Spain

Auditors: Ernst & Young

5&7 Sweet Briar Road

St. Clair

CorporateInformation

Bankers: Scotiabank Trinidad & Tobago Limited

ScotiaCentre

Corner Park & Richmond Streets

Port of Spain

Republic Bank Limited

59 Independence Square

Port of Spain

First Citizens Bank Limited

9 Queen’s Park East

Port of Spain

AN

NU

AL

RE

PO

RT

20

15

35

To the Shareholders of Agostini’s Limited

Report on the consolidated financial statements

We have audited the accompanying consolidated financial statements of Agostini’s Limited and its subsidiaries (the Group) which comprise the consolidated statement of financial position as of 30 September 2015 and the consolidated income statement, consolidated statement of comprehensive income, consolidated statement of changes in equity and con-solidated statement of cash flows for the year then ended and a summary of significant accounting policies and other explanatory information.

Management’s responsibility for the financial statements

Management is responsible for the preparation and the fair presentation of these consolidated financial statements in accordance with International Financial Reporting Standards, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assess-ments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appro-priateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the consolidated financial statements present fairly, in all material respects the financial position of the Group as of 30 September 2015, and its financial performance and its cash flows for the year then ended in accordance with International Financial Reporting Standards.

Port of SpainTRINIDADNovember 27, 2015

Independent Auditor’sReport

AN

NU

AL

RE

PO

RT

20

15

36

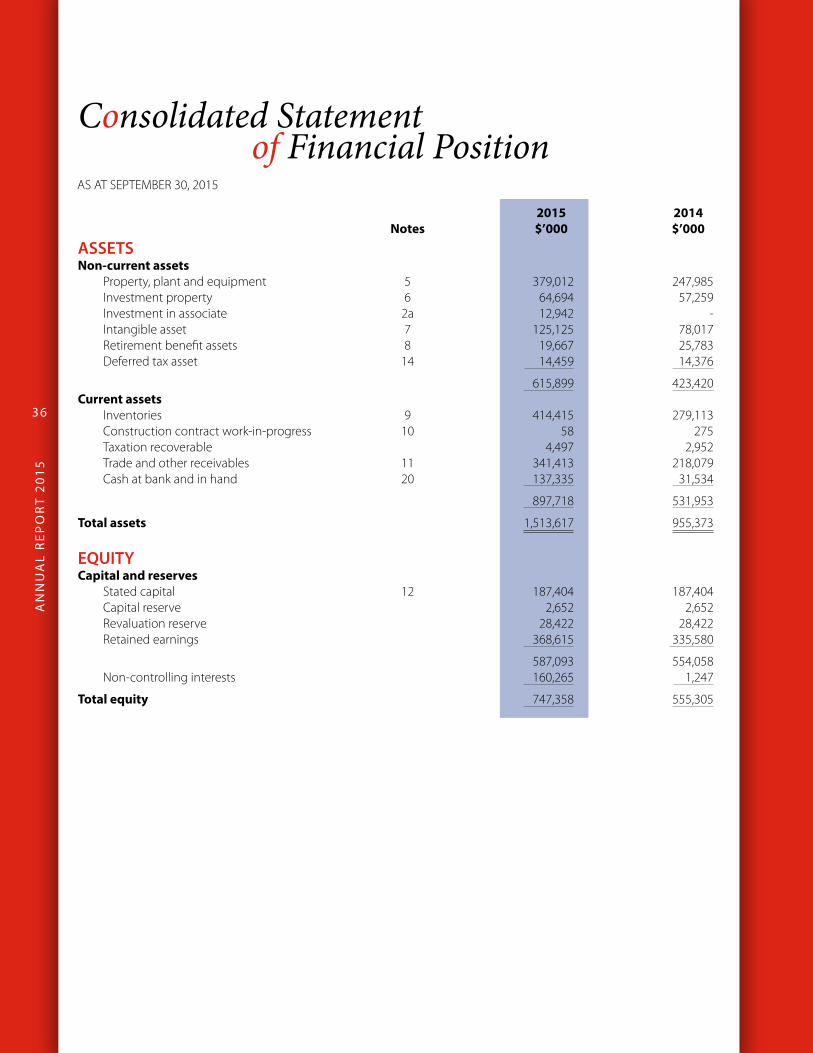

Consolidated Statementof Financial Position

2015 2014 Notes $’000 $’000

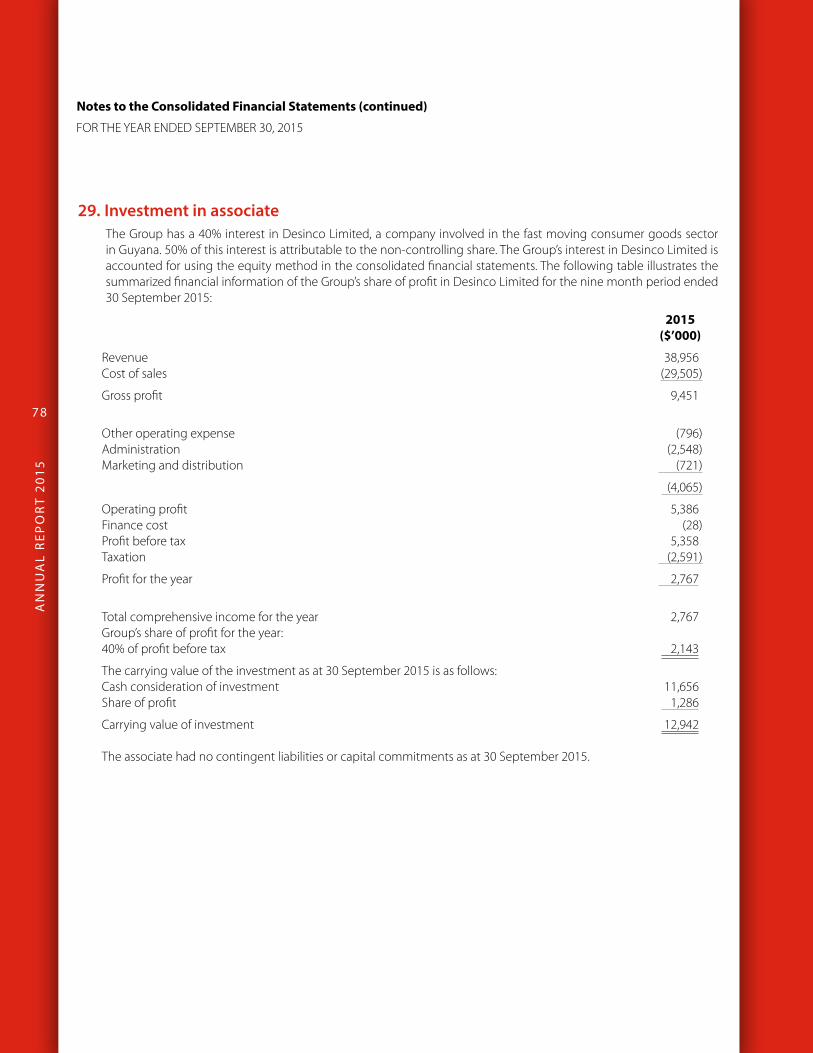

ASSETSNon-current assets Property, plant and equipment 5 379,012 247,985 Investment property 6 64,694 57,259 Investment in associate 2a 12,942 - Intangible asset 7 125,125 78,017 Retirement benefit assets 8 19,667 25,783 Deferred tax asset 14 14,459 14,376

615,899 423,420Current assets Inventories 9 414,415 279,113 Construction contract work-in-progress 10 58 275 Taxation recoverable 4,497 2,952 Trade and other receivables 11 341,413 218,079 Cash at bank and in hand 20 137,335 31,534

897,718 531,953

Total assets 1,513,617 955,373

EQUITYCapital and reserves Stated capital 12 187,404 187,404 Capital reserve 2,652 2,652 Revaluation reserve 28,422 28,422 Retained earnings 368,615 335,580

587,093 554,058 Non-controlling interests 160,265 1,247

Total equity 747,358 555,305

AS AT SEPTEMBER 30, 2015

AN

NU

AL

RE

PO

RT

20

15

37

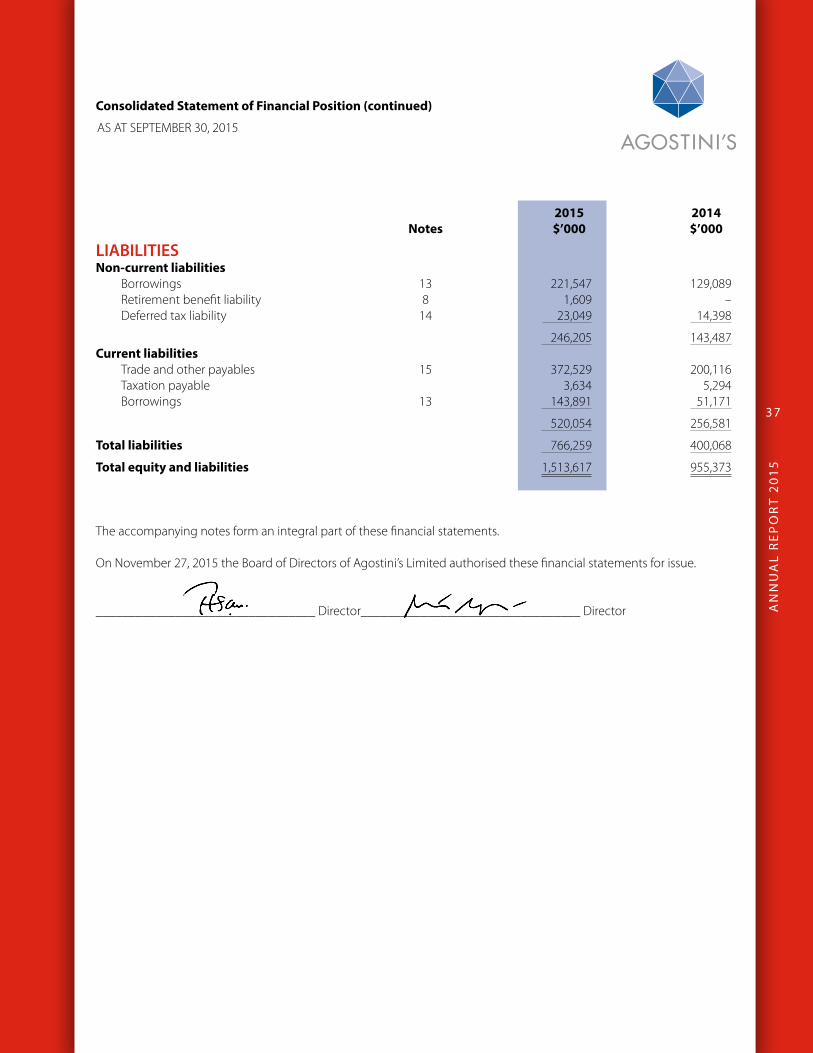

Consolidated Statement of Financial Position (continued)

2015 2014 Notes $’000 $’000

AS AT SEPTEMBER 30, 2015

LIABILITIESNon-current liabilities Borrowings 13 221,547 129,089 Retirement benefit liability 8 1,609 – Deferred tax liability 14 23,049 14,398

246,205 143,487Current liabilities Trade and other payables 15 372,529 200,116 Taxation payable 3,634 5,294 Borrowings 13 143,891 51,171

520,054 256,581

Total liabilities 766,259 400,068

Total equity and liabilities 1,513,617 955,373

The accompanying notes form an integral part of these financial statements.

On November 27, 2015 the Board of Directors of Agostini’s Limited authorised these financial statements for issue.

_________________________________ Director _________________________________ Director

AN

NU

AL

RE

PO

RT

20

15

38

ConsolidatedIncome Statement

2015 2014 Notes $’000 $’000

Turnover 1,706,617 1,359,383

Cost of sales (1,314,052) (1,035,534)

Gross profit 392,565 323,849

Other operating income 31,887 28,080

424,452 351,929

Expenses Other operating (176,425) (132,518) Administration (89,375) (60,661) Marketing and distribution (34,379) (35,054)

(300,179) (228,233)

Operating profit 124,273 123,696Gain on revaluation of investment property 6 - 32Finance costs - net 17 (12,577) (16,583)Share of profit in associate 29 2,143 -

Profit before taxation 113,839 107,145

Taxation 18 (31,664) (26,599)

Profit for the year 82,175 80,546

Attributable to: Owners of the parent 80,576 79,932 Non-controlling interests 1,599 614

82,175 80,546Earnings per share for profit attributable to shareholders $ $ - Basic 19 1.37 1.36

- Diluted 19 1.37 1.36

The accompanying notes form an integral part of these financial statements.

FOR THE YEAR ENDED SEPTEMBER 30, 2015

AN

NU

AL

RE

PO

RT

20

15

39

Consolidated Statementof Comprehensive Income

2015 2014 $’000 $’000

Profit for the year 82,175 80,546

Other comprehensive income not to be reclassified to profit or loss in subsequent period:

(Losses)/gain on defined benefit plans (11,238) 10,485Income tax effect 2,684 (2,621)

(8,554) 7,864Revaluation loss of land and buildings (Note 5) - (100)Income tax effect (Note 14) - 25

Net other comprehensive income not to be reclassified to profit or loss in subsequent periods - (75)

Other comprehensive (loss)/income for the year, net of tax (8,554) 7,789

Total comprehensive income for the year, net of tax 73,621 88,335

Attributable to:Owners of the parent 74,992 87,721Non-controlling interests (1,371) 614

73,621 88,335

The accompanying notes form an integral part of these financial statements.

FOR THE YEAR ENDED SEPTEMBER 30, 2015

AN

NU

AL

RE

PO

RT

20

15

40

Consolidated Statementof Changes in Equity

Attributable to equity holders of the parent

Re- Non Stated Capital valuation Retained controlling capital reserve reserve earnings Total interests Total Notes $’000 $’000 $’000 $’000 $’000 $’000 $’000

Year ended 30 September 2015

Balance at 1 October 2014 187,404 2,652 28,422 335,580 554,058 1,247 555,305Other changes in the composition of the Group – – – (9,670) (9,670) 160,583 150,913Profit for the year – – – 80,576 80,576 1,599 82,175Other comprehensive loss – – – (5,584) (5,584) (2,970) (8,554)

Total comprehensive income – – – 65,322 65,322 160,459 224,534Dividend paid – 2015 (55¢ per share) 26 – – – (32,287) (32,287) (194) (32,481)

Balance at 30 September 2015 187,404 2,652 28,422 368,615 587,093 160,265 747,358

Year ended 30 September 2014

Balance at 1 October 2013 187,404 2,652 28,497 275,960 494,513 1,069 495,582Profit for the year – – – 79,932 79,932 614 80,546Other comprehensive income – – (75) 7,864 7,789 – 7,789

Total comprehensive income – – (75) 87,796 87,721 614 88,335Dividend paid – 2014 (48¢ per share) 26 – – – (28,176) (28,176) (436) (28,612)

Balance at 30 September 2014 187,404 2,652 28,422 335,580 554,058 1,247 555,305

The accompanying notes form an integral part of these financial statements.

FOR THE YEAR ENDED SEPTEMBER 30, 2015

AN

NU

AL

RE

PO

RT

20

15

41

Consolidated Statementof Cash Flows

2015 2014 Notes $’000 $’000Operating activitiesProfit before taxation 113,839 107,145Adjustments for:Depreciation of property, plant and equipment 5 19,128 18,546Amortisation of intangible assets 7 1,148 1,058Gain on sale of plant and equipment (562) (7)Share of profit of associate 29 (2,143) –Net retirement benefit expense 8 1,817 483Gain on revaluation of investment property 6 – (32)Property, plant and equipment write off – 1,567

Operating profit before changes in working capital 133,227 128,760Changes in working capitalDecrease/(increase) in inventories 11,703 (33,145)Decrease/(increase) in work-in-progress 217 (193)Decrease/(increase) in trade and other receivables 76,099 (31,330)(Decrease)/increase in trade and other payables (45,703) 39,123

Net cash flows from operations 175,543 103,215Taxation paid (24,343) (22,997)

Net cash flows from operating activities 151,200 80,218

Investing activitiesPurchase of property, plant and equipment 5 (62,019) (22,654)Purchase of investment property 6 (7,435) –Proceeds from sale of plant and equipment 685 130Purchase of intangible assets 7 (2,000) (51)Purchase of subsidiaries (75,799) –Investment in associate 29 (11,656) –

Net cash flows used in investing activities (158,224) (22,575)

Financing activitiesNet proceeds/(repayment) of loans 96,502 (23,040)Dividends paid 26 (32,287) (28,176)Dividends paid to minority interests (195) (436)

Net cash flows from/(used in) financing activities 64,020 (51,652)

Cash increase during the year 56,996 5,991

Cash and cash equivalents, at 1 October (1,433) (7,424)

Cash and cash equivalents, at 30 September 20 55,563 (1,433)

The accompanying notes form an integral part of these financial statements.

FOR THE YEAR ENDED SEPTEMBER 30, 2015

AN

NU

AL

RE

PO

RT

20

15

42

Notes to theConsolidated Financial Statements

1. General informationThe Company is a limited liability company, incorporated and domiciled in the Republic of Trinidad and Tobago and the address of its registered office is 18 Victoria Avenue, Port of Spain. The Group is principally engaged in trading and distribution and interior building contracting.

The shares of the Parent Company are listed on the Trinidad and Tobago Stock Exchange. The majority shareholder is Victor E. Mouttet Limited (VEML), which owns 50.3% of the shares.

2. Summary of significant accounting policiesThe principal accounting policies applied in the preparation of these consolidated financial statements are set out below. These policies have been consistently applied to all the years presented, unless otherwise stated.

(a) Basis of preparation

The consolidated financial statements of the Group are prepared under the historical cost convention as modified by the revaluation of the land and buildings, investment property and financial investments (Notes 2(e), 2(f ) and 2 (k)). These consolidated financial statements are expressed in Trinidad and Tobago dollars.

The consolidated financial statements provide comparative information in respect of the previous period.

i) Statement of compliance