annual report 2016 - handelsbankenfile/shyp_annual_report_2016.pdf · the level of investment in...

TRANSCRIPT

Annual Report

2016

– a Handelsbanken company

IV STADSHYPOTEK | ANNUAL REPORT 2016

Highlights of the year

Income totalled SEK 12,415 million (11,779).

Operating profit increased by SEK 650 million to SEK 11,366 million (10,716).

Net loan losses totalled SEK -2 million (2).

Profit after tax amounted to SEK 8,857 million (8,322).

Loans to the public grew by 6 per cent, or SEK 68 billion, to SEK 1,151 billion (1,083).

Expenses before loan losses decreased by SEK 18 million and amounted to SEK -1,047 million (-1,065).

PUBLICATION DATE FOR INTERIM REPORTJanuary–June 18 July 2017

11

THE CHIEF EXECUTIVE’S COMMENTS 2

ADMINISTRATION REPORT

Five-year overview 4

Organisation, sustainability and employees 5

Corporate governance report 7

Lending 10

Funding 12

Performance and financial position 14

FINANCIAL REPORTS

Income statement and Statement of comprehensive income 16

Balance sheet 17

Statement of changes in equity 18

Cash flow statement 19

Notes 20

SIGNATURES OF THE BOARD AND THE CHIEF EXECUTIVE 54

AUDITOR’S REPORT 55

STADSHYPOTEK’S BOND TABLES 58

CALCULATION OF KEY FIGURES 59

DEFINITIONS 60

FACTS ABOUT THE COMPANY 61

Contents

The pages in the Annual Report which are part of the administration report are marked separately.

Stadshypotek AB (publ) Corporate identity number: 556459-6715 Registered office: Stockholm www.stadshypotek.se

This Annual Report is also available in Swedish.

2 STADSHYPOTEK | ANNUAL REPORT 2016

THE CHIEF EXECUTIVE'S COMMENTS

THE PAST YEARIn 2016, the Swedish property market has remained in focus, mainly owing to rising prop-erty prices and the housing shortage. The basic explanation for high housing prices in Sweden is that demand is outstripping supply. Although the level of investment in construction projects has been high in recent years, there is still a con-siderable housing shortage, particularly in major cities. The sharp rise in Sweden’s population in recent years has added to the problem, and will continue to do so. The buoyant demand for properties, coupled with continuing price increases, meant another year of strong growth for the Swedish mortgage market in 2016.

Over time, this substantial growth in mort-gages has also led to a rapid increase in house-hold debt ratios in recent years. Meanwhile, the payment capacity of Swedish households has remained strong, as the result of high increases in real wage levels, low inflation, low interest rates and earlier tax cuts. In addition, household savings ratios are generally high, both from a historical perspective and by international stan-dards. According to Handelsbanken’s current forecast, interest rates are expected to remain at historically low levels until the spring of 2018.

The amortisation requirement introduced in Sweden as of 1 June 2016 appears to have only had a marginal effect on the housing market in macroeconomic terms. It is, however, difficult to judge whether this will subdue the demand for properties – and accordingly price trends – to a greater extent in the longer term. A healthy rate of repayment is good, both for society in general and for individual households. It creates a buffer that helps households cope with a possible decline in property prices.

BOOSTING CONSUMER PROTECTION IN THE MORTGAGE MARKETOn 1 January 2017, the EU’s Mortgage Credit Directive was implemented in Swedish legisla-tion. This has generated a considerable amount of work in 2016 in order to make the necessary adjustments to comply with the requirements. The purpose of the Directive is to create a more open and efficient credit market for mortgage loans within the EU, thus further reinforcing protection for consumers and safeguarding financial stability in the market. In Sweden, there have also been calls to promote a healthy cul-ture of amortisation, regardless of loan-to-value (LTV) ratio, and to adopt a more open approach with regards to information about interest rates. Moreover, all bank employees who work with mortgage loans are to be required to sit an exam organised by SwedSec in order to obtain a licence.

The changes that will be most noticeable to customers are those concerning new mort-gages. In future, customers will receive specific information about an offering and its terms and conditions in the form of a fact sheet and a doc-ument that summarises the Bank’s offering with details of matters such as the interest rate fixing periods chosen, the interest rate offered and the loan amount. Customers will also receive a pro-posal for an individual amortisation plan, regard-less of the property’s loan-to-value ratio, which demonstrates how amortisation affects debt levels and the cost of interest from a long-term perspective.

MARKET FUNDINGThe market has been characterised by falling interest rates and the continuing buying of bonds by both the European Central Bank (ECB) and the Swedish Riksbank. However, since the US elections, interest rates have risen and we have also witnessed an interest rate hike

by the Federal Reserve. In 2016, Stadshypotek continued to enjoy good access to market fund-ing. The Swedish market for covered bonds remained our most important source of funding, with Stadshypotek making issues of around SEK 112 billion. We have also been active in the international capital market, completing three euro transactions. These included our first issue using the Finnish cover pool as collateral. There was considerable interest in this and we issued EUR 500 million for 10 years at a rate of 0.13 per cent. This means that Stadshypotek now has three active pools for covered bonds: in Sweden, Norway and Finland. The last two of these are used to finance Stadshypotek’s oper-ations in the countries concerned. During the year, we also received a preliminary AAA rating for a Danish pool for covered bonds.

CUSTOMER SATISFACTIONIn the 2016 survey carried out by Swedish Quality Index (SKI), Handelsbanken once again had the most satisfied mortgage loan customers of all the major banks. For property finance in the corporate market, Handels-banken received a very high rating. For both the private and corporate markets, we received high ratings regarding the Bank’s image. This suggests, among other things, that there is a clear perception that we care about our cus-tomers and that it is easy to have a mortgage with us. A personal meeting with our expert advisers offers considerable added value and this obviously applies equally to private cus-tomers and corporate customers alike. I am very pleased to see that we once again received a high rating this year. Throughout 2016, we continued to develop our offering to mortgage loan customers, resulting in customer benefits in the form of personal meetings at branches and the range of digital services offered.

The Chief Executive’s commentsThe growth rate for mortgage loans in Sweden remained high throughout 2016, albeit slightly lower than the previous year. Stadshypotek grew in line with the market, at a rate of around 7.5 per cent, and was thus able to defend its market position in Sweden. The rate of growth in the corporate market in Sweden dropped to around 4 per cent in 2016, compared to around 7 per cent in 2015. Stadshypotek’s volumes for the corporate market in Sweden rose marginally in 2016. In other countries where Stadshypotek has branches – Denmark, Norway and Finland – growth in lending varied.

STADSHYPOTEK | ANNUAL REPORT 2016 3

THE CHIEF EXECUTIVE'S COMMENTS

FINANCIAL PERFORMANCE IN 2016 During the year, our operating profit increased by 6.1 per cent, or SEK 650 million, to SEK 11,366 million. This increase was primarily attributable to net interest income in Sweden and mainly the result of higher lending volumes to the private market. The profit at our Danish branch increased by 27 per cent to SEK 320 million, as the result of higher lending volumes to the private market. At our branches in Norway and Finland, profits declined as the result of shrinking margins. Our expenses decreased by SEK 18 million to SEK 1,047 million, mainly due to a lower level of compensation paid to Handels-banken for the services performed by its branch operations on behalf of Stadshypotek.

CREDIT RISKS REMAIN LOW Stadshypotek’s net loan losses for the year totalled SEK 2 million, compared to the previous year, when recoveries exceeded new loan losses and the net amount recovered totalled SEK 2 million.

Stadshypotek’s lending operations are inte-grated with Handelsbanken’s operations and its lending is carried out via the Bank’s branch network. Handelsbanken’s decentralised ways of working, combined with reliable knowledge of local market conditions and proximity to the customer, regardless of where Stads hypotek/Handelsbanken is operating, are factors which continue to contribute positively to the low level of credit risk. Of all credit exposures at Stads-hypotek at the year-end, 99 per cent were to customers with an estimated repayment cap acity categorised as normal or better than normal. The proportion of impaired loans was very low, at 0.01 per cent. In summary, Stads-hypotek’s credit portfolio remains strong.

Ulrica Stolt Kirkegaard Stockholm, February 2017

ADMINISTRATION REPORT

4 STADSHYPOTEK | ANNUAL REPORT 2016

Key figures 2016 2015 2014 2013 2012

Profit before loan losses, SEK m 11,368 10,714 8,719 8,118 7,907

Loan losses/recoveries, SEK m -2 2 22 -22 -21

Operating profit, SEK m 11,366 10,716 8,741 8,096 7,886

Total assets, SEK m 1,187,525 1,116,431 1,058,857 984,659 925,961

Equity, SEK m 33,018 32,616 32,368 26,723 25,940

Return on equity, % 24.4 24.2 20.9 20.3 19.6

C/I ratio before loan losses, % 8.4 9.0 14.9 14.5 3.5

C/I ratio after loan losses, % 8.4 9.0 14.6 14.7 3.8

Net interest margin, % 1.07 1.08 1.00 0.99 0.89

Loan loss ratio, % 0.00 -0.00 -0.00 0.00 0.00

Reserve ratio for impaired loans, % 31.2 29.6 24.4 17.0 35.4

Proportion of impaired loans, % 0.01 0.01 0.01 0.02 0.01

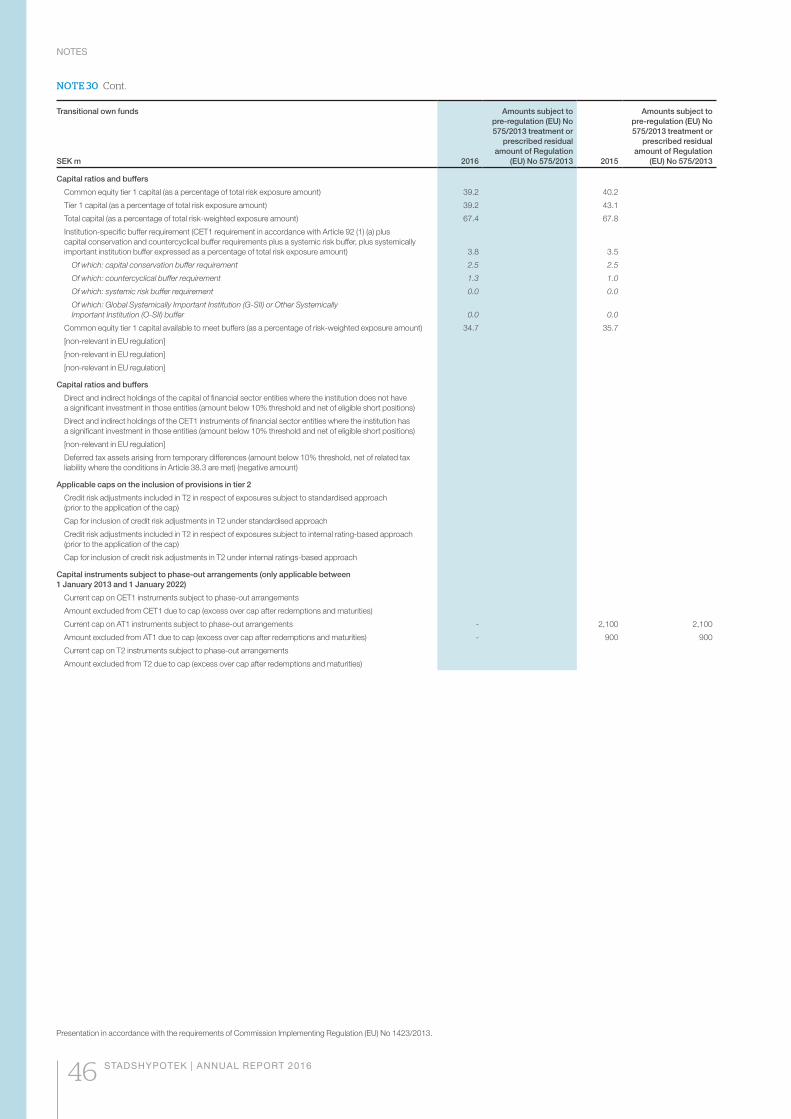

Total capital ratio, %1 67.4 67.8 67.1 62.3 56.9

Tier 1 ratio, % 1 39.2 43.1 42.4 41.2 40.6

Common equity tier 1 ratio, % 39.2 40.2 39.0

Return on total assets, % 0.77 0.76 0.66 0.66 0.64

Average number of employees 78 77 72 69 45

1 Capital ratio and tier 1 ratio according to Basel II up to and including 2013.

Five-year overview

Income statementsSEK m 2016 2015 2014 2013 2012

Interest income 20,295 21,884 26,946 29,023 32,163

Interest expense -7,933 -10,128 -16,706 -19,592 -24,111

Net interest income 12,362 11,756 10,240 9,431 8,052

Net fee and commission income -29 -6 -7 -5 -7

Net gains/losses on financial transactions 82 29 7 70 150

Total income 12,415 11,779 10,240 9,496 8,195

Expenses -1,047 -1,065 -1,521 -1,378 -288

Profit before loan losses 11,368 10,714 8,719 8,118 7,907

Loan losses -2 2 22 -22 -21

Operating profit 11,366 10,716 8,741 8,096 7,886

Taxes -2,509 -2,394 -1,968 -1,805 -2,085

Profit for the year 8,857 8,322 6,773 6,291 5,801

Balance sheetsSEK m, 31 December 2016 2015 2014 2013 2012

Assets

Loans to credit institutions 12,027 10,516 10,148 7,966 5,758

Loans to the public 1,150,611 1,082,659 1,018,533 955,251 891,200

Value change of interest-hedged item in portfolio hedge 35 28 70 96 5,271

Derivative instruments 22,746 20,514 24,960 15,235 20,708

Other assets 2,106 2,714 5,146 6,111 3,024

Total assets 1,187,525 1,116,431 1,058,857 984,659 925,961

Liabilities and equity

Due to credit institutions 497,110 472,238 405,074 337,097 286,294

Issued securities 612,787 568,416 579,485 572,746 565,865

Derivative instruments 4,429 4,145 4,063 8,186 11,988

Other liabilities 18,481 18,316 17,167 18,707 19,174

Subordinated liabilities 21,700 20,700 20,700 21,200 16,700

Equity 33,018 32,616 32,368 26,723 25,940

Total liabilities and equity 1,187,525 1,116,431 1,058,857 984,659 925,961

For definitions and calculation of key figures, see pages 59 and 60.

ADMINISTRATION REPORT

STADSHYPOTEK | ANNUAL REPORT 2016 5

Organisation, sustainability and employeesStadshypotek AB (publ), corporate identity number 556459-6715, is a public credit market company authorised to conduct operations under the Swedish Banking and Financing Business Act. Its core business comprises the financing of residential property and also office and commercial buildings. Since 1997, the company has been a wholly owned subsidiary of Svenska Handelsbanken AB (publ), corporate identity number 502007-7862.

ORGANISATIONStadshypotek AB is responsible for Handels-banken’s mortgage business in Sweden, Denmark, Finland and Norway. In Sweden, the business comprises the financing of residential property and also office and commercial build-ings. The business operations of Stadshypotek’s branches in Denmark, Finland and Norway focus primarily on the financing of residential property.

INTEGRATION WITH HANDELSBANKENThe business operations of Stadshypotek are highly decentralised. The basic principle is that the organisation and working practices are cen-tred around Handelsbanken’s branch offices, which are responsible for all the business of individual customers. One consequence of this approach is that Stadshypotek’s lending opera-tions in Sweden are run via Handelsbanken’s Swedish branch operations, while the lending operations at Stadshypotek’s branches in Denmark, Finland and Norway are run via Handelsbanken’s branch operations in each of the respective countries. Stadshypotek’s treasury function is integrated with Handels-banken’s Treasury Department. A collaboration agreement regulates the overall relationship between the parties and individual outsourcing agreements specify the services which Handels banken is to perform on behalf of Stadshypotek. Handelsbanken’s decentralised method of working has been successfully applied since Handelsbanken’s acquisition of the company in 1997.

SUSTAINABILITYSustainability is completely integrated into Stads-hypotek’s corporate culture and working methods, and the principles are established in the Sustain-ability policy and Policy for ethical standards which are decided by Stadshypotek’s Board.

International initiatives and guidelines with the common aim of encouraging and facilitating cor-porate sustainability must guide Stadshypotek’s work in this field.

Such initiatives and guidelines include the UN Global Compact, the OECD Guidelines for

Multinational Enterprises, the UN Environment Programme Finance Initiative (UNEP FI), the UN Principles for Responsible Investment (PRI), the UN Guiding Principles on Business and Human Rights and the International Labour Organiza-tion’s core conventions.

EnvironmentAccording to Stadshypotek, integrating environ-mental aspects into operations is a basic premise of long-term value creation. Thus environmental efforts are a natural part of operations, with the company taking responsibility for contributing to long-term sustainable development and seeking to minimise its environmental impact.

Stadshypotek must strive to minimise its indi-rect impact on the environment, for example through its lending and investment. This can be achieved with long-term sustainable business decisions in which environmental factors are taken into consideration.

PERSONNELIn 2016, the average number of employees at Stadshypotek was 78 (77). Of these, 46 per cent (47) were women and 54 per cent (53) were men. Stadshypotek’s branches in Finland and Norway have no employees. They buy all services from Handelsbanken’s branch in each of the respective countries. At Stadshypotek’s branch in Denmark, three people work part-time and, in addition, administrative services are purchased from Handelsbanken’s branch in Denmark. The heads of Handelsbanken’s regional banks in Denmark, Finland and Norway also represent Stadshypotek’s branches in each of the respective countries.

Staff developmentThe decentralised way of working adopted by the parent company Handelsbanken also applies to the employees at Stadshypotek. The Handelsbanken Group’s strength is derived from the combined expertise of its employees. The most important source of increased profes-sionalism is learning in your daily work, where all employees are responsible for constant

development – their own and that of the opera-tions. All employees participate in their own unit’s business planning every year. After that, individual competency mapping, planning dialogues and performance reviews are carried out, linking business goals with the goals of individual employees. Each employee then puts together an action plan setting out the goals to be attained and the conditions necessary for this. Based on the action plan and follow-ups, all employees then have a salary dialogue review with their line manager at the end of the year.

Stadshypotek is part of the Handelsbanken Group’s internal labour market. The strong cor-porate culture and the Handelsbanken Group’s values are crucial to the success of operations, so internal recruitment is important. Internal mobility spreads the working methods, exchange of experience and corporate culture throughout the Handelsbanken Group. Employ-ees with many years’ experience and extensive knowledge acquired from different parts of the Handelsbanken Group make a vital contribution to the Group having satisfied customers. Stads-hypotek’s need for employees in various posi-tions is primarily met through internal recruit-ment within the Handelsbanken Group. Managers must be exemplary ambassadors for the Bank’s corporate culture, which explains why most managers are recruited internally.

Gender equality and diversityWork to promote gender equality, diversity and an inclusive corporate culture is a fundamental part of the Handelsbanken Group’s core values. At Stadshypotek, women and men must have the same opportunities to develop. Regardless of background, the staff have their own charac-teristics and strengths and their own way of expressing themselves as individuals. No type of discrimination is allowed at Stadshypotek. Stadshypotek works continuously for gender equality and diversity, which is vital for being able to attract and retain competent employees. A prioritised element of the work related to equality is increasing awareness of how social and cultural norms affect us in our daily lives.

ADMINISTRATION REPORT

6 STADSHYPOTEK | ANNUAL REPORT 2016

Work environment and healthThe overall, long-term goal of work environment efforts is for the employees to enjoy good health, to develop on a personal level and to function in an optimal way. Many different factors influence this goal. A work environment survey is carried out at least once a year by managers, together with work environment representatives and employees, covering the physical and the psychosocial working environment as well as gender equality, diversity and an inclusive corporate culture. The results form the basis of a work environment plan which is integrated with the unit’s business plan and in this way becomes a natural part of how the operation develops. Stadshypotek also follows up the sickness absence rate figures, as well as reported incidents.

OKTOGONEN – THE HANDELSBANKEN GROUP’S PROFIT-SHARING SCHEMEStadshypotek’s employees are covered by the Handelsbanken Group’s profit-sharing scheme. Allocations to the profit-sharing scheme are subject to the Handelsbanken Group achieving its goal of better profitability than the average of peer banks in its home markets. All employees receive an equal part of the allocated amount, regardless of their position or duties. Payments can start to be made in the year the holder reaches the age of 60.

ADMINISTRATION REPORT

STADSHYPOTEK | ANNUAL REPORT 2016 7

Corporate governance report

The shareholders ultimately make the decisions about Stadshypotek’s governance. At the annual general meeting, the shareholders appoint the Board and the auditors. The Board is responsible to the owners for the company’s organisation and management of the company’s affairs, and it appoints a Chief Executive to run the company’s operating activities. The auditors examine the financial reporting, among other matters, and submit an auditor's report.

BOARD AND CHIEF EXECUTIVEThe Board is to continuously assess the com-pany’s financial situation and ensure that Stads-hypotek is organised such that the accounting records, management of funds and other aspects of the company’s financial circum-stances are satisfactorily controlled. The Board establishes policies and instructions on how this should be done and establishes rules of procedure for the Board and also instructions for the Chief Executive.

The fundamental rules regarding the allocation of responsibilities among the Board, the Chair-man and the Chief Executive are manifested in the Board’s rules of procedure, as well as in its instructions to the Chief Executive.

Chairman of the BoardThe Board’s rules of procedure state that the Chairman shall ensure that the Board carries out its work efficiently and that it fulfils its duties. This involves organising and managing the Board’s work and creating the best possible conditions for this work. The Chairman must also ensure that the Board members continually update and expand their knowledge of Stads-hypotek, and that new members receive an appropriate introduction and training. The Chairman must be available to the Chief Execu-tive as an advisor and discussion partner, but must also prepare the Board’s evaluation of the Chief Executive's work. In addition, the Chair-man is responsible for ensuring that the Board’s work is evaluated annually. The Chairman is also responsible for contacts with the owner on ownership matters and for conveying points of view from the owner to the Board.

Board membersThe members of the Board have broad and extensive experience of banking and finance, and several members have worked on Stads-hypotek’s Board for a long time and are very familiar with the company’s operations.

During the year, the Board convened 17 times, of which nine times by correspondence.

At the annual general meeting on 14 March 2016, Stefan Nilsson was elected as a new Board member, while Yonnie Bergqvist, Michael Green, Olof Lindstrand, Ulrica Stolt Kirkegaard

and Michael Bertorp were re-elected as mem-bers until the annual general meeting has been held in 2017. After Yonnie Bergqvist asked to be relieved of his duties as Board member and Chairman on 7 November, the Board elected Stefan Nilsson as new Chairman at the Board meeting held on 11 November 2016. Monica Morén was appointed employee representative by the Financial Sector Union of Sweden.

For information on certain terms of employ-ment for executive officers and on loans to Board members and executive officers, see note 6 on page 33.

COMPANY MANAGEMENT• Ulrica Stolt Kirkegaard, Chief Executive,

employed since 2014• Heléne Boström, Finance, employed

since 2006• Christer Ericsson, Systems Development,

employed since 2006• Heléne Grönberg, Business Development

and Market, Sweden, employed since 2012• Mattias Lidgren, Funding, employed

at Handelsbanken• Yvonne Orre, Credits, employed since 2007 • Ulrika Söderberg, Legal Affairs, employed

since 2015• Lolou Sörenson, HR, employed at

Handelsbanken• Pär Tysk, Branches, Covered Bonds and

Global Product Owner, employed since 2014• Johan Nordström, Property Valuations,

employed 2016.

AUDITORSAt the annual general meeting in 2016, KPMG AB were appointed auditors of Stadshypotek AB until the annual general meeting in 2017. The chief auditor is Anders Bäckström, autho-rised public accountant, Stockholm.

FRAMEWORK FOR CONTROLInternal control for operations Responsibility for internal control has been dele-gated from the Chief Executive to department managers and branch managers who are respon-sible for internal control within their respective units. This responsibility means that the appropri-ate instructions and procedures for the operation

must be in place, and compliance with these procedures must be monitored regularly. The responsibility for internal control is thus an integral part of managerial responsibility at Stadshypotek.

Internal AuditInternal audit operations at Stadshypotek are managed by Group Audit at Handelsbanken in accordance with the collaboration agreement and outsourcing agreements between Stads-hypotek and Handelsbanken. Internal Audit’s assignments are based on an internal auditing policy established by the Board. Each year, the Board determines a plan for the work of the Internal Audit function. Internal Audit must inde-pendently examine Stadshypotek’s operations and reporting and also evaluate and examine the business operation’s processes for risk management, internal governance and control to establish how satisfactory they are. The con-clusions of internal audits, the actions to be taken and their status are reported to the Board.

Compliance The Compliance function must ensure that laws, regulations and internal rules, as well as accepted business practices and standards, are complied with in the operations conducted by Stadshypotek. The function must also assist in drawing up internal rules and provide informa-tion about new and amended rules for opera-tions. The Head of Compliance submits regular reports regarding material observations to the Chief Executive. In addition, the Chief Executive receives a quarterly compliance report and twice a year, a compliance report is submitted to the Board.

Risk ControlRisk Control is responsible for identifying, mea-suring, analysing and reporting all material risks in the business. Risk Control is also responsible for ensuring that the application of measuring methods used for calculating risk utilisation, in accordance with the applicable internal and external regulations, are fit for purpose and accurate. Moreover, Risk Control is responsible for ensuring that the models applied are regu-larly evaluated and that the results of the evaluation are documented.

ADMINISTRATION REPORT

8 STADSHYPOTEK | ANNUAL REPORT 2016

The Head of Risk Control informs the Chief Executive and the Head of Group Risk Control at Handelsbanken of any material observations that could be deemed to involve risk or of any comments from public authorities.

The Head of Risk Control submits a monthly risk report to the Chief Executive and the Head of Group Risk Control at Handelsbanken. These reports are presented to the Board on a quar-terly basis by the Head of Risk Control.

REMUNERATION PRINCIPLESThe principles for Stadshypotek’s system of remuneration are established in a remuneration policy decided by the Board.

Stadshypotek has a long-term view of its staff’s employment. Remuneration varies over an employee’s period of employment with Stads hypotek and good efforts must always be rewarded. The total level of remuneration should help improve Stadshypotek’s competitive posi-tion and profitability so that the company is able to attract, retain and develop skilled employees

and establish a healthy management succes-sion structure.

Stadshypotek has a low risk tolerance in general. This approach is reflected in the com-pany’s view of remuneration. Stadshypotek considers that fixed remuneration contributes to healthy operations and all employees of Stads hypotek therefore only receive a fixed remuneration. There are no exceptions to this principle of a fixed salary.

Remuneration for work performed is set indi-vidually for each employee. Remuneration is paid in the form of a fixed salary, customary salary benefits and a pension provision. Salaries are established locally and are based on factors known in advance: the nature and level of diffi-culty of the work, competencies, performance and results achieved, leadership (for managers who are responsible for the career development of employees), and supply and demand on the market, as well as performance as an ambassa-dor for Stadshypotek’s business culture.

Stadshypotek’s view is that fixed remuneration does not lead to behaviour that gives rise to an increased risk level.

INTERNAL CONTROL REGARDING FINANCIAL REPORTINGThe control environment described above in this corporate governance report is fundamental to Stadshypotek’s internal control of financial reporting.

Risk assessment is another part of the inter-nal control process and comprises identification and management of the risks that may affect financial reporting, as well as the control activi-ties aimed at preventing, detecting and correct-ing deviations.

Risk assessmentThe annual self-evaluations carried out at all departments are an essential part of Stads-hypotek’s risk assessment. Risks related to financial reporting are part of this overall analysis.

NameStefan Nilsson, Chairman

Ulrica Stolt Kirkegaard, Board member

Michael Bertorp, Board member

Education B.A. Business Administration Uppsala UniversityAMP – Harvard

M.A. EconomicsB.A. Business Administration

Law graduate

Year of birth 1957 1968 1949

Other assignments Chairman • Handelsbanken Liv AB• Handelsbanken Fastigheter AB• Handelsbanken Regional Bank The NetherlandsVice Chairman • Handelsbanken Regional Bank Denmark• Handelsbanken Regional Bank Finland• Handelsbanken Regional Bank Norway

Chairman• Setra Group AB Board member • Xact Kapitalförvaltning AB • Idevall & Partners Fonder AB• Maderna Corporate Services AB

Background • Handelsbanken Senior Management 1997– 2006, 2013 –

• 2013 – 2016 Regional Bank Eastern Sweden

• 2008 – 2013 Handelsbanken USA

• 2006 – 2007 Handelsbanken International

• 2002 – 2006 Handelsbanken Pension & Life

• 1997– 2002 Regional Bank Northern Sweden

• 1992 –1997 Regional Bank Central Sweden

• 1988 –1992 Handelsbanken Capital Markets

• Chief Executive Stadshypotek since 2014• 2014 –

Handelsbanken Senior Management• 2014 –

Stadshypotek• 2006 – 2014

Handelsbanken Regional Bank Stockholm• 1998 – 2006

Handelsbanken Markets• 1994 – 1998

Handelsbanken Regional Bank Central Sweden

• 2006 – Legal consultancy business

• 1986 – 2006 SCA

• 1985 – 1986 Sunds Defibrator AB

• 1984 – 1985 SCA

• 1982 – 1984 Ministry of Justice

• 1972 – 1982 Swedish courts

Employed at Handelsbanken since 1980 Employed at Handelsbanken since 1994

Board meeting attendance

11/17 17/17 17/17

ADMINISTRATION REPORT

STADSHYPOTEK | ANNUAL REPORT 2016 9

In a self-evaluation, the employee defines the events that constitute potential risks to the operation and then estimates the probability and consequences of each risk. An action plan is then developed based on the self-evaluation.

Control activitiesVarious control activities are incorporated in the financial reporting process. Reported amounts and analyses of income statements and balance sheets are reconciled and checked regularly within the finance and accounting department.

Heads of finance and accounting at branches are responsible for ensuring that the control activ-ities in the financial reporting for their respective units are fit for purpose; in other words, that they are designed to prevent, detect and correct errors and deviations, and are in compliance with internal guidelines and instructions. At each quarterly closing of accounts, the branches certify that the prescribed periodic checks and reconciliation of accounts have been carried out.

MonitoringInternal Audit, Compliance, Risk Control and the finance and accounting department monitor compliance with internal policies, instructions and other policy documents. The policy estab-lished by the Board for internal audit states that it must examine internal governance and control.

SHAREHOLDERS AND SHAREHOLDERS’ MEETINGRights of shareholders Stadshypotek AB is a wholly owned subsidiary of Svenska Handelsbanken AB (publ). Stads-hypotek’s Articles of Association contain no limitations with regard to the number of votes each shareholder may represent at a share-holders’ meeting.

Every year, a shareholders’ meeting is held which is an annual general meeting where Stads hypotek’s shareholders decide on matters that include the following:• which individuals should be appointed as

members of the Board of the company

• who should be appointed as the company’s auditors

• determining fees to Board members and auditors

• adopting the income statement and balance sheet

• appropriation of profits• whether the Board and Chief Executive are

to be discharged from liability for the past financial year.

The shareholders at a shareholders’ meeting also make decisions regarding possible amend-ments to the company’s Articles of Association.

NameOlof Lindstrand, Board member

Michael Green,Board member

Monica Morén, Employee representative

Education Law graduate Economics programme upper secondary schoolBusiness AdministrationEconomicsLegal studiesContract law and Company law

Upper secondary school

Year of birth 1949 1966 1958

Other assignments Chairman• Xact Kapitalförvaltning ABBoard member• AB Handel och Industri• Ecster AB

Chairman• Handelsbanken InternationalBoard member• Handelsbanken Liv AB• Handelsbanken Fonder AB• Ecster AB• AB Handel och Industri• EFN AB• Swedish-American Chamber of Commerce,

New York (SACC N.Y.)• Financial Competence Centre in Gothenburg• Handelsbanken Regional Bank

Northern Great Britain • Handelsbanken Regional Bank

Southern Great Britain• Handelsbanken Regional Bank

Central Great Britain • Handelsbanken Regional Bank

South West Great Britain• Handelsbanken Regional Bank

North East Great Britain

Board member• Handelsbanken Regional Bank

Central SwedenDeputy Board member• Handelsbanken's Pension Fund• Handelsbanken’s Pension Foundation• Handelsbanken’s Staff Foundation

Background • 2006 – 2011 EVP Handelsbanken

• 2011 – 2015 Handelsbanken Senior Management

• 2005 – 2011 Handelsbanken Central Credit Department

• 2002 – 2005 Handelsbanken Capital Markets

• 2000 – 2002 Handelsbanken Markets

• 1996 – 2000 Handelsbanken Central Development Department

• 1992 – 1996 Handelsbanken Central Credit Department

• 1985 – 1992 Handelsbanken Regional Bank Stockholm City

• 1977 – 1985 Swartlings law firm

• 1974 – 1977 Swedish courts

• EVP Handelsbanken since 2008• 2008 –

Handelsbanken Senior Management• 2015 –2016

Handelsbanken Sweden• 2011 – 2015

Handelsbanken Capital Markets• 2008 – 2011

Handelsbanken Regional Bank Western Sweden

• 2006 – 2007 Handelsbanken USA

• 1994 – 2005 Handelsbanken Regional Bank Western Sweden

• 1986 – 1994 Götabanken

• 1977 – Handelsbanken Regional Bank Central Sweden

Employed at Handelsbanken since 1985 Employed at Handelsbanken since 1994 Employed at Handelsbanken since 1977

Board meeting attendance

17/17 11/17 11/17

ADMINISTRATION REPORT

10 STADSHYPOTEK | ANNUAL REPORT 2016

LendingSTADSHYPOTEK’S ROLE IN HANDELSBANKENIn the Swedish operations of the Handels-banken Group, mortgage finance is conducted principally via Stadshypotek. At Stadshypotek’s branches in Denmark, Finland and Norway, business operations focus primarily on financing residential property. Lending takes place through Handelsbanken’s branch network in the country concerned. As a result of the decen-tralised method of working within the Handels-banken Group, the branches have been dele-gated responsibility for marketing, contact with customers, pricing and processing all mortgage loans. Handelsbanken thus acts as an agent for Stadshypotek, with responsibility for ensuring that credit assessment and collateral valuations are carried out in accordance with the guide-lines approved by Stadshypotek’s Board.

MORTGAGE MARKET IN SWEDENIn 2016, the Swedish mortgage market was characterised by a continued demand for mort-gage loans. Table 1 on page 11 shows mort-gage lending to households with single-family housing or housing co-operative apartments as collateral at year-end and the year-on-year change, as reported by Statistics Sweden.

According to Mäklarstatistik (estate agent statistics), single-family house prices rose by 9 per cent (12) for Sweden as a whole in 2016. Prices of housing co-operative apartments rose by an average of 7 per cent (16) for Sweden as a whole. Continued migration to metropolitan areas, with their limited supply of housing, led to rising prices in these areas. However, the rate of increase in prices has been lower than in previous years in all metropolitan areas. Table 2 on page 11 shows price increases in the Greater Stockholm, Greater Gothenburg and Greater Malmö areas.

CORPORATE MARKET IN SWEDEN The market for lending secured by mortgages to non-financial companies grew by 3.7 per cent during the year, compared with 7.4 per cent in 2015. The lower rate of market growth in percentage terms was entirely attributable to commercial properties. Table 3 on page 11 shows lending secured by mortgages to Swedish non-financial companies as reported by Statistics Sweden, both at year-end and the year-on-year change.

Transaction volumes for commercial proper-ties remained high in 2016. Rents for offices and

commercial premises remained stable during the year. In more attractive market locations, vacancy rates were low. As rental properties, modern office premises generally hold greater appeal than less modern premises, and this is also reflected in the level of rents and vacancies. The required rate of return on residential proper-ties remained low during the year.

MORTGAGE MARKETS IN DENMARK, FINLAND AND NORWAYIn all countries where Stadshypotek has branches, mortgage markets continued to grow in 2016, and housing prices rose. The increase in mortgage lending to households was largest in Norway, where the annual percentage increase was 6.8 per cent. The increase in housing prices was also highest in Norway, with an annual increase of 12.8 per cent. Tables 4 and 5 on page 11 show mortgage lending to households and the trend in housing prices in each country.

BOOSTING CONSUMER PROTECTION IN THE MORTGAGE MARKETOn 1 January 2017, the EU’s Mortgage Credit Directive came into effect. The purpose of the Directive is to create a more open and efficient credit market for mortgage loans within the EU, thus contributing to better protection for con-sumers and safeguarding financial stability in the market. In Sweden, requirements are also being introduced to:• promote a healthy amortisation culture,

which means that all customers will have an individual mortgage amortisation plan, regardless of the loan-to-value ratio.

• increase transparency regarding interest rates when making offers to customers.

For customers, one result of the Directive is new documentation when applying for a mortgage loan. The aim of this is to clarify the loan offer and make it easier for customers to compare different banks’ offers. The individual amortisa-tion plan is intended to show how debt and the cost of interest decrease over time if the cus-tomer chooses a higher level of amortisation than that required by the Swedish Financial Supervisory Authority.

AMORTISATION REQUIREMENTOn 1 June 2016, the Swedish Financial Super-visory Authority’s regulations on amortisation of mortgage loans came into effect. The aim of the

amortisation requirement is to establish a more robust amortisation culture in society and promote balance in the personal finances of individual households.

The amortisation requirement means that, for new mortgage loans with a loan-to-value ratio of 50–70 per cent of the market value, at least 1 per cent of the total amount borrowed must be amortised each year. Mortgage loans with a loan-to-value ratio of more than 70 per cent of the market value must be amortised annually by at least 2 per cent of the total amount of the loan.

Households will amortise based on the new amortisation requirement. Households with a loan-to-value ratio of 50–70 per cent of their home’s market value will experience the biggest change in their amortisation plan.

STADSHYPOTEK’S LENDINGIn 2016, Stadshypotek’s lending volume in Sweden rose by SEK 46.6 billion (57.6). Loans to the private market increased by SEK 46.3 bil-lion (46.9), while loans to the corporate market grew by SEK 0.3 billion (10.7). At year-end, Stadshypotek’s loans to the public in Sweden were SEK 983.3 billion (936.7). Some 68 per cent – SEK 670.7 billion – of Stadshypotek’s loans to the public are to the private market.

The Handelsbanken Group’s market share for loans to Swedish households secured by mortgages on single-family housing or housing co-operative apartments was 22.9 per cent (23.0) at the end of December. According to Statistics Sweden’s statistics, the market com-prises total lending to Swedish households with single-family homes or co-operative apartments as collateral. The market share therefore also includes Handelsbanken’s lending to Swedish households with collateral in single-family hous-ing or co-operative apartments.

At year-end, loans to the public by Stads-hypotek’s branch in Norway totalled NOK 75.4 billion (69.7), with the private market accounting for NOK 58.2 billion (54.0) and the corporate market for NOK 17.2 billion (15.8). Loans to the public by Stadshypotek’s branch in Denmark totalled DKK 28.7 billion (24.0) at year-end, all of which were loans to the private market. At year-end, loans to the public by Stadshypotek’s branch in Finland totalled EUR 5.3 billion (5.3), with the private market accounting for EUR 2.3 billion (2.3) and the corporate market account-ing for EUR 3.0 billion (3.0).

ADMINISTRATION REPORT

STADSHYPOTEK | ANNUAL REPORT 2016 11

Table 4. Mortgage markets in Denmark, Finland and Norway

Mortgage lending to households 1

2016 2015 Change Change, %

Denmark 2, DKK bn 1,506 1,470 36 2.4

Finland 3, EUR bn 94 92 2 2.2

Norway 4, NOK bn 2,524 2,364 160 6.8

Table 3. Corporate market in Sweden

Lending to non-financial companies, SEK bn 31 December

Type of collateral 2016 2015 Change, SEK bn Change, %

Property 952 918 34 3.7

of which multi-family dwellings 674 633 41 6.5

of which housing co- operative associations 416 388 28 7.2

Table 5. Mortgage markets in Denmark, Finland and Norway

Price change 5, % 2016 2015

Denmark 4

– Single-family housing 3.6 5.2

– Owner-occupied apartments 6.9 11.5

Finland 2 3.1 -0.3

Norway 6 12.8 5.0

1 Sources: Denmark – Association of Danish Mortgage Banks, Finland – Bank of Finland, Norway – Statistics Norway2 At 30 September3 At 30 November4 At 31 October5 Sources: Denmark – Statistics Denmark, Finland – Statistics Finland, Norway – Eiendomsverdi6 At 31 December

Table 1. Mortgage market in Sweden

Mortgage lending to households, SEK bn 31 December

Type of collateral 2016 2015 Change, SEK bn Change, %

Single-family housing as collateral 2,001 1,890 111 5.9

Housing co-operative apartment as collateral 901 806 95 11.8

Total 2,902 2,696 206 7.6

Table 2. Mortgage market in Sweden

Price change, % 2016 2015

Single-family housing

Greater Stockholm 6 17

Greater Gothenburg 11 14

Greater Malmö 8 12

Housing co-operative apartments

Greater Stockholm 6 18

Greater Gothenburg 12 18

Greater Malmö 14 12

ADMINISTRATION REPORT

12 STADSHYPOTEK | ANNUAL REPORT 2016

FundingStadshypotek’s treasury function is integrated with Handelsbanken’s Treasury Department. This organisational structure offers the best conditions for using the funding source and instrument offering the lowest funding cost each time funding is carried out. An integrated treasury department has also made it possible to make efficient use of the Handelsbanken Group’s liquidity.

FUNDING INSTRUMENTSStadshypotek raises funds mainly on the Swedish money market and capital market and through the parent company. Foreign markets are also used for the purposes of diversification. The primary source of funding is bonds in Sweden.

Covered bonds are issued in the company’s own name and primarily within the framework of a benchmark loan system aimed at the Swedish institutional market. This means that only a small number of separate bonds are issued, with respective final maturity dates set at intervals of about nine months. Concentrating large volumes into a small number of loans in this manner achieves good market liquidity. At year-end, Stadshypotek had eight outstanding benchmark loans which mature between 2017 and 2022. Stadshypotek’s bonds are arranged by five market makers. The same programme is also used for issues in Norwegian kronor.

International issues of covered bonds are done mainly within a Euro Medium Term Covered Note (EMTCN) programme. The total facility amount of this programme is EUR 20 bil-lion. Issues under this programme are arranged according to agreements signed with 21 banks.

In addition, Stadshypotek has a US Medium Term Covered Bond programme for issues in the US. The total facility amount of this pro-gramme is USD 15 billion. Stadshypotek has reached sales agreements with 13 banks as part of the programme.

Stadshypotek also has a programme for issues in Australia (AMTCN) aimed at Australian and Asian investors.

In addition to the above, Stadshypotek has commercial paper programmes in Sweden and Europe. The ceiling for the Swedish commercial paper programme is SEK 90 billion. The ceiling for the European programme is EUR 4 billion.

Covered bondsCovered bonds are issued on an ongoing basis, by permission of the Swedish Financial Super-visory Authority, under the Covered Bonds (Issuance) Act (2003:1223). Covered bonds are bonds with priority rights to Stadshypotek’s assets (the cover pool assets). These assets

consist of credits and their associated collateral pursuant to the Swedish legislation for such bonds.

Stadshypotek has previously established covered bond pools in Sweden and Norway. In 2016, a cover pool was established in Finland, and the first issue was collateralised by assets in the Finnish pool. All pools have been given the highest possible rating by Moody’s: Aaa. A pre-liminary rating was also issued in respect of the Danish operations. The cover pools consist of collateral as per the legislation mentioned above and include a safety buffer (over collateral, or OC) that exceeds the statutory requirements by a good margin.

The unutilised facilities under the cover pools, including the Danish branch, corresponded to 66 per cent of the nominal debts at 31 Decem-ber 2016. Information about the assets in the cover pools is provided in the tables on page 13.

INTEREST RATE TRENDS The annual average for both long and short Swedish bond yields continued to fall in 2016 compared with 2015. Short bond yields had already turned negative in 2015, and in 2016, longer bond yields, up to five years, also dropped below zero. Early in the year, the Riksbank cut the repo rate again, this time to -0.5 per cent, and continued to buy government bonds.

After the United Kingdom voted to leave the European Union in the referendum held in June, bond yields and stock prices suffered more declines. However, investors decided that, as happened before, increased risks would also mean increased stimulus from central banks, mainly the Bank of England in this case. Thus stock markets recovered quickly. Surprisingly robust economic statistics in the wake of the referendum led to bond yields also rising in the autumn.

Since the US presidential election, markets have concentrated on the prospects of a more expansionary fiscal policy. Fiscal stimulus in the US is expected to create a stronger platform for interest rate hikes by the Federal Reserve and a greater need for funding for the US government. In combination, these factors pushed US bond yields up at the end of the year.

While the Federal Reserve raised its rate for the second time in this cycle, the ECB signalled that purchases of bonds would continue throughout 2017, and the Riksbank has sig-nalled that purchases of government bonds will continue in the first half of 2017. However, further stimulus from central banks in Europe limited the impact of the rise in US rates on European bond yields.

As with interest rates in general, yields on mort-gage bonds declined in 2016. However, this trend was interrupted after the US election in November, when yields on Swedish mortgage bonds rose in line with yields in the US and else-where. Despite this late rally, mortgage bond yields declined substantially in 2016.

FUNDING The integration of Stadshypotek’s Treasury func-tion with Handelsbanken’s Treasury department ensures efficient management of the Handels-banken Group’s liquidity and market funding. Among other things, Handelsbanken’s liquidity surplus is used to finance funding at Stads-hypotek. Liquidity is transferred on a daily basis in the form of overnight loans and lending trans-actions from Handelsbanken to Stadshypotek that involve maturities of up to around one year. In addition, long-term funding in Handels-banken’s name on the international capital market can be passed on to Stadshypotek.

With the aim of reducing liquidity risk, short-term funding is augmented by long-term fund-ing, which is adjusted using swap agreements so that the interest fixing period matches the maturity of lending. Thus, Stadshypotek has good diversification of its funding with respect to both geographical markets and maturity.

Lending with long-term rate fixing has mainly been financed in Stadshypotek’s own name in Sweden through the issue of covered bonds. Stadshypotek also has international long-term funding in its own name through international funding programmes.

Stadshypotek uses swap agreements to reduce interest rate and currency risks in con-nection with funding. The use of derivatives increases flexibility in connection with the funding. Thus, funding can be carried out when market conditions are favourable, without exposing the company to interest rate and currency risks.

At the end of the year, interest rate swap agreements in which fixed interest is received totalled SEK 232.2 billion (208.9), while interest rate swap agreements paying fixed interest amounted to SEK 25.0 billion (11.5). The issued volume of bonds from Stadshypotek’s bench-mark series during the year was SEK 112.7 bil-lion (112.8). During the year, a nominal volume totalling SEK 82.7 billion (115.3) matured or was repurchased. The carrying amount of the out-standing benchmark loans was SEK 408.1 billion (385.6) at year-end.

Sales of bonds from the EMTCN programme totalled the equivalent of approximately EUR 2.75 billion (1.25). The outstanding volume at year-end was the equivalent of around EUR 11.0 billion (9.1).

ADMINISTRATION REPORT

STADSHYPOTEK | ANNUAL REPORT 2016 13

At 31 December 2016, the cover pool assets, categorised by type of collateral, were as follows:

Type of collateral Sweden Norway Denmark Finland Total

Public 10,526 16,256 26,782

Single-family housing 400,843 41,284 23,500 9,672 475,299

Second homes 20,102 1,710 2,686 935 25,433

Rental properties 214,706 16,090 9,639 240,435

Housing co-operative apartments, units 191,416 4,474 11 195,901

Owner-occupied apartments 10,423 4,140 14,563

Housing company shares – apartments 595 6,663 7,258

Housing company shares – houses 4,224 4,224

Commercial/Offices 35,273 99 35,372

Agricultural 28,989 535 14 27 29,565

Residential farms 16 486 502

Other 1,007 46 1,053

Total 902,862 75,226 30,826 47,473 1,056,387

Stadshypotek’s funding31 DecemberSEK bn

2016 2015

Carryingamount

Share, %

Carryingamount

Share, % Change

Funding from the parent company 518.8 45.9 493.0 46.4 25.8

of which subordinated liabilities 21.7 - 20.7 - 1.0

Commercial paper - - - -

Covered bonds, SEK 443.0 39.1 421.1 39.7 21.9

of which repos 0.0 - 0.3 - -0.3

Covered bonds, other currencies 169.8 15.0 146.4 13.8 23.4

Commercial paper – ECP - - 0.9 0.1 -0.9

Total 1,131.6 100.0 1,061.4 100.0 70.2

In Norway, a total of NOK 10.2 billion (1.5) was issued. The outstanding volume at year-end was NOK 27.0 billion (17.0).

No issues were made under the US or Australian programmes during the year. The outstanding volumes at year-end were USD 3.75 billion (3.75) and AUD 750 million (750) respectively.

At year-end, there was no outstanding volume in the European commercial paper programme (preceding year SEK 0.9 billion).

Stadshypotek’s total funding at year-end was SEK 1,131.6 billion (1,061.4), of which SEK 518.8 billion (493.0) came from Handels-banken. The breakdown of funding by instru-ment is shown in the table below.

RATINGSIn 2016, Fitch upgraded Stadshypotek’s long-term rating, from AA- to AA. Other ratings remained unchanged during the year.

StadshypotekCovered

bonds Long-term Short-term

Moody’s Aaa - P-1

Standard & Poor’s AA- A-1+

Fitch AA F1+

Average loan-to-value ratio of the cover pools31 December% 2016 2015

Swedish pool 49.97 53.57

Norwegian pool 53.63 56.68

Finnish pool 48.72 -

Lending volumes available in cover pools31 DecemberSEK m

Assets pooled Assets utilised

2016 2015 2016 2015

Swedish pool 902,862 859,400 626,458 600,024

Norwegian pool 75,226 62,264 31,270 17,701

Finnish pool 47,473 - 5,192 -

ADMINISTRATION REPORT

14 STADSHYPOTEK | ANNUAL REPORT 2016

Performance and financial positionFINANCIAL PERFORMANCEStadshypotek’s operating profit for the year was SEK 11,366 million (10,716), an increase of SEK 650 million, or 6.1 per cent, compared to the previous year.

OPERATING INCOMEIncome totalled SEK 12,415 million (11,779), up 5.4 per cent on the figure for 2015. Of this income, SEK 598 million (875) was attributable to the branch in Norway, SEK 385 million (426) to the branch in Finland and SEK 345 million (276) to the branch in Denmark.

Net interest income grew by SEK 606 million, or 5.2 per cent, to SEK 12,362 million (11,756). Of the net interest income, SEK 577 million (875) was attributable to the branch in Norway, SEK 377 million (417) to the branch in Finland and SEK 345 million (276) to the branch in Denmark. Excluding the branches, net interest income thus increased by SEK 875 million. This increase was primarily due to higher lend-ing volumes to the private market in Sweden. The decrease in net interest income at the Norwegian branch was attributable to weaker margins for both the private market and corpo-rate market, although this was offset slightly by an increase in lending volumes. The decrease in net interest income at the Finnish branch was a result of weaker margins, while net interest income at the Danish branch increased due to an increase in lending volumes to the private market. Net gains/losses on financial transac-tions increased, to SEK 82 million (29).

EXPENSES AND LOAN LOSSESExpenses decreased by SEK 18 million, or 1.7 per cent, to SEK -1,047 million (-1,065), of which SEK -58 million (-59) was attributable to the branch in Norway, SEK -36 million (-34) to the branch in Finland and SEK -23 million (-24) to the branch in Denmark. Staff costs rose by SEK -5 million, or 5.6 per cent, compared to 2015 due to an increase in the number of employees and annual salary increases. Other administrative expenses decreased by SEK 16 million, or 1.7 per cent, mainly due to a lower level of sales compensation paid to the parent company for the services performed by the branch operations on behalf of Stadshypotek related to the sale and administration of mort-gage loans. Development costs for IT systems were also lower compared to the previous year.

Net loan losses totalled SEK -2 million (2).

TAXES AND NET PROFIT FOR THE YEARAfter taxes of SEK -2,509 million (-2,394), profit for the year after tax was SEK 8,857 million (8,322).

PROFITABILITYThe profit corresponded to a return on equity of 24.4 per cent (24.2).

For a five-year overview of income state-ments and balance sheets, and for key financial figures and ratios, see page 4.

OTHER COMPREHENSIVE INCOMEOther comprehensive income consists primarily of the effective portion of the change in the fair value of interest rate swaps and cross-currency interest rate swaps used as hedging instru-ments in cash flow hedging. Cash flow hedges are applied to manage exposures to variations in cash flows relating to changes in the variable interest rates on lending and funding. Cash flow hedging is also used to hedge currency risk in future cash flows relating to funding in foreign currencies. Lending and funding are measured at amortised cost, whereas the derivatives that hedge these items are recognised at market value. Over time, the market values of the derivatives reach zero as each individual hedge reaches maturity, but this entails volatility in other comprehensive income during the term of the hedge. In 2016, changes in the value of hedge derivatives in cash flow hedges equalled SEK -984 million (-542) after tax. These value changes derive primarily from changes in the discount rates for the relevant currencies as well as the time factor that reduces the market value of a derivative to zero as its maturity date approaches.

TOTAL ASSETS AND EQUITYAt 31 December 2016, Stadshypotek’s total assets stood at SEK 1,187,525 million (1,116,431), and equity was SEK 33,018 million (32,616).

GROUP CONTRIBUTIONSA Group contribution of SEK 10,100 million (9,235) has been provided to the parent company, Handelsbanken.

FINANCIAL RISKSFor information about financial risks, see note 2.

RECOMMENDED APPROPRIATION OF PROFITS In accordance with the balance sheet for Stads-hypotek AB, the following profits after deduction for a net paid Group contribution of SEK 7,878 million are at the disposal of the annual general meeting:

Retained earnings SEK 9,329 million

Fair value fund SEK 2,664 million

Profit for the year SEK 8,857 million

Total SEK 20,850 million

The Board proposes that the profits be carried forward to the next year.

When assessing the amount of the Group contribution from the company, account has been taken of the nature of operations, their scope, the consolidation requirement and risk-taking.

The Board’s assessment is that the above appropriation of profits is prudent and well-adapted to the operations as a going concern. Unrealised changes in the value of assets and liabilities at fair value have had a net impact on equity of SEK 3,156 million.

The total capitalisation of Stadshypotek at year-end exceeded the statutory minimum requirement pursuant to Regulation (EU) No 575/2013 and Directive 2013/36/EU and other relevant requirements established by the authorities for the company.

Half-yearly performance 2016 2015 2014

SEK m Jul-Dec Jan-Jun Jul-Dec Jan-Jun Jul-Dec

Interest income 10,153 10,142 10,415 11,469 13,060

Interest expense -3,825 -4,108 -4,527 -5,601 -7,647

Net interest income 6,328 6,034 5,888 5,868 5,413

Net fee and commission income -15 -14 -4 -2 -4

Net gains/losses on financial transactions 39 43 -30 59 -75

Total income 6,352 6,063 5,854 5,925 5,334

Staff costs -46 -48 -47 -42 -44

Other administrative expenses -480 -467 -468 -495 -713

Depreciation and amortisation -3 -3 -6 -7 -7

Total expenses -529 -518 -521 -544 -764

Profit before loan losses 5,823 5,545 5,333 5,381 4,570

Net loan losses -7 5 -1 3 26

Operating profit 5,816 5,550 5,332 5,384 4,596

Financial reports

16 staDsHYpoteK | annUal report 2016

Income statement

SEK m 2016 2015

Interest income 20,295 21,884

Interest expense -7,933 -10,128

Net interest income Note 3 12,362 11,756

Fee and commission income 13 14

Fee and commission expense -42 -20

Net fee and commission income Note 4 -29 -6

Net gains/losses on financial transactions Note 5 82 29

Other income 0 0

Total income 12,415 11,779

Staff costs Note 6 -94 -89

Other administrative expenses Note 7 -947 -963

Depreciation and amortisation of intangible assets and property and equipment Note 14, 15 -6 -13

Total expenses before loan losses -1,047 -1,065

Profit before loan losses 11,368 10,714

Net loan losses Note 8 -2 2

Operating profit 11,366 10,716

Taxes Note 9 -2,509 -2,394

Profit for the year 8,857 8,322

Net earnings per share, before and after dilution, SEK 54,674 51,370

Statement of comprehensive income

SEK m 2016 2015

Profit for the year 8,857 8,322

Other comprehensive income

Items that may subsequently be reclassified to the income statement

Cash flow hedges Note 23 -1,262 -695

Translation differences for the year 407 -329

Taxes on items that may subsequently be reclassified to the income statement

– cash flow hedges Note 23 278 153

Total comprehensive income for the year 8,280 7,451

Financial reports

staDsHYpoteK | annUal report 2016 17

Balance sheet

SEK m, 31 December 2016 2015

ASSETS

Loans to credit institutions Note 10 12,027 10,516

Loans to the public Note 11 1,150,611 1,082,659

Value change of interest-hedged item in portfolio hedge 35 28

Shares and participating interests in Group companies Note 12 0 0

Derivative instruments Note 13 22,746 20,514

Intangible assets Note 14 12 14

Property and equipment Note 15 0 0

Current tax assets - 71

Other assets Note 16 701 1,221

Prepaid expenses and accrued income Note 17 1,393 1,408

Total assets 1,187,525 1,116,431

of which Group claims Note 25 34,849 31,093

LIABILITIES AND EQUITY

Due to credit institutions Note 18 497,110 472,238

Issued securities Note 19 612,787 568,416

Derivative instruments Note 13 4,429 4,145

Current tax liabilities 188 -

Deferred tax liabilities Note 9 735 1,012

Other liabilities Note 20 10,143 9,273

Accrued expenses and deferred income Note 21 7,415 8,031

Subordinated liabilities Note 22 21,700 20,700

Total liabilities 1,154,507 1,083,815

Equity Note 23

Share capital 4,050 4,050

Other funds 10,782 11,347

Retained earnings 9,329 8,897

Profit for the year 8,857 8,322

Total equity 33,018 32,616

Total liabilities and equity 1,187,525 1,116,431

of which Group liabilities Note 25 533,896 506,740

Financial reports

18 staDsHYpoteK | annUal report 2016

Restricted equity Non-restricted equity

SEK m Share

capital 1 Statutory

reserve

Fund for software

developedin-house

Hedgereserve

Translationreserve

Retained earnings Total

Equity at 31 December 2014 4,050 8,106 4,133 -21 16,100 32,368

Profit for the year 8,322 8,322

Other comprehensive income -542 -329 -871

Total comprehensive income for the year -542 -329 8,322 7,451

Group contributions provided -9,235 -9,235

Tax effect on Group contributions 2,032 2,032

Equity at 31 December 2015 4,050 8,106 3,591 -350 17,219 32,616

Profit for the year 8,857 8,857

Other comprehensive income -984 407 -577

Total comprehensive income for the year -984 407 8,857 8,280

Fund for software developed in-house 12 -12 -

Group contributions provided -10,100 -10,100

Tax effect on Group contributions 2,222 2,222

Equity at 31 December 2016 4,050 8,106 12 2,607 57 18,186 33,018

1 Average number of shares, before and after dilution, 162,000.

Statement of changes in equity

Financial reports

staDsHYpoteK | annUal report 2016 19

SEK m 2016 2015

OPERATING ACTIVITIES

Operating profit 11,366 10,716

of which paid-in interest 20,310 22,287

of which paid-out interest -8,267 -10,292

Adjustment for non-cash items in profit/loss:

Loan losses 22 27

Unrealised changes in value 158 466

Depreciation, amortisation and impairment 6 13

Paid income tax -169 -314

Change in the assets and liabilities of operating activities:

Loans to the public -67,974 -64,156

Due to credit institutions 24,872 67,183

Issued securities 44,371 -11,069

Derivative instruments, net -3,110 3,730

Other 0 1,112

Cash flow from operating activities 9,542 7,708

INVESTING ACTIVITIES

Investment in tangible non-current assets 0 0

Disposal of tangible non-current assets - -

Investment in intangible non-current assets -3 -

Cash flow from investing activities -3 0

FINANCING ACTIVITIES

Subordinated loans 1,000 -

Group contribution paid out -9,235 -7,180

Cash flow from financing activities -8,235 -7,180

CASH FLOW FOR THE YEAR 1,304 528

Liquid funds at beginning of year 5,516 5,129

Cash flow from operating activities 9,542 7,708

Cash flow from investing activities -3 0

Cash flow from financing activities -8,235 -7,180

Exchange rate difference on liquid funds 207 -141

Liquid funds at end of year 7,027 5,516

Liquid funds consist of funds available with banks and equivalent institutions, excluding funds on a blocked account.

Liquid funds with banks and equivalent institutions 7,027 5,516

Funds on a blocked account with banks relating to issuance of covered bonds 5,000 5,000

Loans to credit institutions 12,027 10,516

Cash flow statement

notes

20 staDsHYpoteK | annUal report 2016

NotesNOTE 1 Accounting policies

Stadshypotek’s Annual Report is prepared in accordance with the Swedish Annual Accounts Act for Credit Institutions and Securities Compa-nies (1995:1559), the regulations and general guidelines issued by the Swedish Financial Supervisory Authority, FFFS 2008:25, Annual reports in credit institutions and securities com-panies, the Swedish Financial Reporting Board’s recommendation RFR 2 Accounting for legal enti-ties, and statements from the Swedish Financial Reporting Board. In accordance with the Finan-cial Supervisory Authority’s general guidelines, Stadshypotek applies statutory IFRS. This means that the international accounting standards and interpretations of these standards as adopted by the EU have been applied to the extent that is possible within the framework of national laws and directives and the link between accounting and taxation.

The parent company, Svenska Handelsbanken AB, prepares consolidated accounts which include Stadshypotek.

Stadshypotek’s subsidiary holdings comprise the dormant company Svenska Intecknings Garanti AB Sigab. In accordance with Chapter 7, Section 7(4) of the Swedish Annual Accounts Act for Credit Institu-tions and Securities Companies, Stadshypotek has not prepared consolidated accounts as its subsidi-ary is of marginal significance.

The presentation currency is Swedish kronor.

ISSUE AND ADOPTION OF ANNUAL REPORTThe Annual Report was approved for issue by the Board and Chief Executive on 7 February 2017 and will be submitted for adoption by the AGM on 28 March 2017.

CHANGED ACCOUNTING POLICIES, ETC.ESMA has published guidelines on disclosures regarding alternative performance measures which should be followed in financial reports pub-lished after 3 July 2016. The guidelines entail an increase in the disclosure of financial ratios that are not defined in IFRS. In accordance with the requirements in the guidelines, the company informs about definitions and reconciliation of alternative performance measures in the Annual Report on pages 59 – 60. In other respects, the accounting policies, classifications and calcula-tion methods applied during the financial year agree in all essential respects with the policies applied in the 2015 Annual Report.

FUTURE REGULATORY CHANGESIFRS 9 Financial Instruments, which is to replace IAS 39 Financial Instruments: Recognition and Measurement, has been adopted for application by the EU. The standard must be applied as of the 2018 financial year. The standard comprises

three areas: classification and measurement, impairment of financial instruments and general hedge accounting. According to the new classifi-cation and measurement rules, financial assets must be classified at fair value through profit or loss, at amortised cost or at fair value through other comprehensive income. The starting point for classification of debt instruments is the com-pany’s business model for managing the financial assets and whether the instrument’s contractual cash flows only contain payments of interest and principal amounts. Equity instruments are to be classified at fair value through profit or loss unless the company at the time of initial recognition opted to present these instruments at fair value through other comprehensive income. This option means that only dividends from these holdings are recognised in the income statement. Other gains and losses due to changes in fair value are not permitted to be reclassified from other comprehensive income to the income statement. The rules for classification of financial liabilities are largely unchanged compared to IAS 39. The main change is that fair value changes due to own credit risk for financial liabili-ties where it has been decided to measure at fair value through profit or loss are presented in other comprehensive income instead of in the income statement. Stadshypotek’s current assessment is that the classification and measurement rules are not expected to have any significant impact on the financial reports. No reclassifications between fair value and amortised cost are expected for the first application period.

As a result of the new regulations on impair-ment, a model is being introduced which is based on expected loan losses and not on incurred loan losses as in the existing model in IAS 39. IFRS 9 states that all assets measured at amortised cost and fair value through other comprehensive income, as well as guarantees and credit commit-ments, must be subject to the impairment testing requirement. The assets whose impairment needs to be tested are split into three stages depending on the degree of credit impairment. Stage 1 comprises assets for which the credit risk has not increased significantly since initial recog-nition. Stage 2 comprises assets for which the credit risk has significantly increased since initial recognition. Stage 3 comprises assets which have been individually valued as impaired loans. In stage 1, provisions are to be recognised corre-sponding to the loss expected to occur within 12 months. In stages 2 and 3, provisions are to be recognised corresponding to the loss expected to occur during the entire remaining maturity of the asset. Forward-looking factors must be taken into account in conjunction with the calculation of these provisions. The provisions must also be

based on a probability-weighted outcome, unlike the current IAS 39 where the provision is based on the most expected outcome. Depending on the factors which are established as defining a significant increase in the credit risk, and how the forward-looking factors are weighted in the calcu-lation of the provisions, these may fluctuate more over time than is the case today.

The new general rules for hedge accounting allow the company’s own risk management to be better reflected in the financial reports and also introduce less detailed rules for how the effective-ness of the hedges is to be assessed.

Stadshypotek is currently analysing the finan-cial effects of IFRS 9 in more detail.

IFRS 15 Revenue from Contracts with Cus-tomers has also been adopted for application in the EU. The standard must be applied as of the 2018 financial year, but can be applied before this. Stadshypotek does not intend to apply the standard ahead of the stipulated date. IFRS 15 introduces a five-step model to establish how and when revenue must be recognised. However, the standard does not apply to financial instruments, insurance contracts or leases. IFRS 15 also con-tains increased disclosure requirement relating to revenue. The current assessment is that the new standard will not have any material impact on Stadshypotek’s financial reports, capital ade-quacy and large exposures.

IFRS 16 Leases has also been published by the IASB. Assuming that IFRS 16 is adopted by the EU, and the date of implementation proposed by the IASB is not changed, this standard will be applied as of the 2019 financial year. The main change due to the new standard is that all lease contracts (with the exception of short-term and minor lease contracts) must be recognised as an asset (right-of-use asset) and as a liability in the lessee’s balance sheet. The lease payment must be reported as depreciation and interest expense. There are also increased disclosure requirements. For lessors, the requirements are largely unchanged. The company is analysing the finan-cial effects of the new standard.

None of the other changes in the accounting regulations issued for application are expected to have a material impact on Stadshypotek’s finan-cial reports, capital adequacy, large exposures or other circumstances according to the applicable operating rules.

SHARES AND PARTICIPATING INTERESTS IN SUBSIDIARIES Shares and participating interests in subsidiaries are measured at cost.

notes

staDsHYpoteK | annUal report 2016 21

RECOGNITION OF LIABILITIES AND ASSETS IN FOREIGN CURRENCY The company’s presentation currency is Swedish kronor. The functional currency for the company’s operations outside Sweden usually differs from the company's presentation currency. The cur-rency used in the economic environment where the operations are primarily conducted is regarded as the functional currency.

Transactions in foreign currency are translated to the functional currency on the transaction date. Monetary items and assets and liabilities at fair value are valued at the functional currency’s spot price at the end of the balance sheet date. Exchange rate differences are recognised in the income statement.

Translation of foreign operations to the Group’s presentation currency When translating the foreign units’ balance sheets and income statements from the functional cur-rency to the company’s presentation currency, the current method has been used. This means that assets and liabilities are translated at the closing day rate. Equity is translated at the rate applicable at the time of investment or earning. The income statement has been translated at the average annual rate. Translation differences are recognised as a component of Other comprehen-sive income and are included in the translation reserve in equity.

RECOGNITION OF ASSETS AND LIABILITIES IN THE BALANCE SHEET An asset is defined as a resource over which there is control as a result of past events and that is expected to provide future economic benefit. Assets are recognised on the balance sheet when it is probable that the future economic benefits related to the asset will accrue to the company and when the value or acquisition cost of the asset can be reliably measured.

Liabilities are the company’s existing obligations which as a result of past events are expected to lead to an outflow of resources from the company. A liability is recognised on the balance sheet when, in order to fulfil an existing obligation, it is probable that the company must surrender a resource with a value that can be reliably measured.

Purchases and sales of money market and capital market instruments on the spot market are recognised on the trade date. The same applies to derivatives. Other financial assets and liabilities are normally recognised on the settlement date.

Financial assets are removed from the balance sheet when the contractual rights to the cash flows originating from the asset expire or when all risks and rewards related to the asset are trans-ferred to another party. A financial liability is removed from the balance sheet when the obliga-tion ceases or is cancelled.

Financial assets and liabilities are set off on the balance sheet if Stadshypotek has a contractual right to set off the recognised amounts and intends to settle the payments simultaneously with a net amount.

Stadshypotek has no framework agreements regarding offsetting, which means that the disclosure requirements in IFRS 7 Financial instruments: Disclosures do not apply.

CLASSIFICATION AND RECOGNITION OF FINANCIAL ASSETS AND LIABILITIESFor the purposes of measurement, in compliance with IAS 39, all financial assets are placed in the following valuation categories:1. loans and receivables2. assets held to maturity3. assets at fair value through profit or loss – held for trading – assets which upon initial recognition were

designated at fair value through profit or loss4. available-for-sale assets.

Financial liabilities are classified as follows:1. liabilities at fair value through profit or loss – liabilities held for trading – liabilities which upon initial recognition were

designated at fair value through profit or loss2. other financial liabilities.

The classification in the balance sheet is indepen-dent of the measurement category. Thus, differ-ent measurement principles may be applied for assets and liabilities carried on the same line on the balance sheet. A classification into measure-ment categories of the financial assets and liabili-ties which are recognised on the balance sheet is shown in note 28.

Stadshypotek’s financial assets and liabilities are categorised in loans and receivables and other financial liabilities respectively. Derivatives that are not formal hedging instruments come under the held-for-trading category. Upon initial recognition, all financial assets and liabilities are designated at fair value. For assets and liabilities at fair value through profit or loss, the transaction costs are recognised in the income statement under Net gains/losses on financial transactions. For other financial instruments, the transaction costs are included in the acquisition value.