annual report - j. lauritzen a/sstatic.j-l.com/imce/jlar2014_lowres.pdf · this annual report...

TRANSCRIPT

www.j-lauritzen.com

2014Annual Report

CONTENT · ANNUAL REPORT 20142

OVERVIEWIntroduction by Chairman and CEO 3About Us 4Highlights 2014 6Group Key Figures 8Outlook 2015 10

BUSINESSLauritzen Bulkers 11Lauritzen Kosan 16Other Businesses 21People, Relations and Systems 22Finance 24

GOVERNANCECorporate Governance 26Risk Management 27Corporate Responsibility 29Board of Directors 30Management 32

FINANCIALS Financial review 34Consolidated financial statements 36Parent company financial statements 67Management statement 89Independent Auditors’ Report 90List of Group Companies 91

Table of Contents

DISCLAIMERThis Annual Report contains forward-looking statements about J. Lauritzen’s future financial position. Such statements are subject to risks and uncertainties as various factors, many of which are beyond the control of J. Lauritzen, may cause actual developments and actual results to differ materially from expectations contained in the Annual Report. Accordingly, forward-looking statements should not be relied upon as a prediction of actual results.

OVERVIEW · ANNUAL REPORT 2014 3

Early 2014, an undercurrent of optimism existed in the shipping markets in general and amongst members of the dry-cargo community in particu-lar. The reality of the past year has proved this op-timism misplaced, and 2014 turned out to be con-siderably more difficult and challenging for us than expected.

The net results for 2014 were USD (166)m com-pared to USD (285)m in 2013. The results were in line with our most recent expectations but consi-derably below our expectations at the beginning of the year. The results were heavily impacted by impairment and provisions totalling USD (161)m. While the results were unsatisfactory in financial terms, we regard them as an outcome consistent with a very difficult year.

It is part of our strategy to diversify the revenue base and value creation opportunities by spread-ing business activities and investment interests across different market segments. The exit from the product tanker segment in 2013-14, the sales of our shuttle tankers and two of our capesize bulk carriers in 2014 have changed the risk profile of our revenue base. We maintain some diversifica-tion by operating two distinctly different business activities while our investment in Axis Offshore provides a further diversification to our value cre-ation opportunities.

In our view, our value creation will to an increasing extent have to be driven by our ability to combine

acumen, operational excellence and talent to transform relations, insight and knowledge into shared value to our owner and to our clients.

The global shipping industry faces cost-intensive challenges imposed on our industry by regulators and authorities. We support well considered en-vironmental regulation and call for their effective enforcement when economic incentives for non-compliance are obvious.

We have little doubt that we are facing a 2015 where it is very difficult indeed to find any credit-able reasons for our markets to improve conside-rably. The gas carrier earnings will continue to be impacted by slow global economic growth, dry bulk suffers from severe oversupply and offshore activities are hampered by low oil prices.

Low energy prices may provide the beginning of an upturn as households all over the world feel the increased spending power and start consuming. It is, however, unlikely for this to have an impact short-term, and we believe that our three business areas will be faced with a year of hard work and little financial reward.

Bent ØstergaardChairman of the Board Jan Kastrup-NielsenPresident and CEO

Introduction by Chairman and CEO

OVERVIEW · ANNUAL REPORT 20144

About Us J. Lauritzen has served the maritime trade world-wide for more than 130 years and has been en-gaged in a range of different segments of the shipping industry. Today, we are a global provider of marine transportation of dry bulk cargoes, pe-trochemicals and liquefied petroleum gases. In addition we have investments in the offshore ser-vice sector.

Our businessLauritzen Bulkers controls a modern fleet of more than 100 primarily handysize and supramax dry bulk carriers. The handysize operation is our main business activity and is based on a large homoge-neous fleet of owned, part-owned and long-term time-chartered vessels, vessels committed by partners as well as a substantial number of short-term time-chartered vessels.

Lauritzen Kosan specialises in carriage of petro-chemicals and liquefied petroleum gases - a seg-ment of the shipping industry characterised by technically complex requirements from regulators and clients. Lauritzen Kosan controls a fleet of 39 semi-refrigerated, fully-pressurized and ethylene gas carriers.

In addition to our two main business areas, we have business interests in the offshore service sector through our part-ownership of Axis Off-shore Ltd., provider of high specification accom-modation units servicing the offshore oil and gas industry.

Lauritzen Bulkers

Lauritzen Kosan

Invested capital per business unit, year-end 2014

Lauritzen Bulkers

Lauritzen Kosan

Revenue per business unit, 2014

J. Lauritzen at a glance

• Founded in 1884, Denmark• Owned by the Lauritzen Foundation. The

Lauritzen Foundation is a self-governing in-stitution regulated by the Danish Act on Commercial Foundations. Through its char-ter, the Foundation is committed to promote and develop the Danish shipping industry in general and support humanitarian work.

• Operating world-wide with headquarters in Copenhagen, Denmark

• Overseas offices in Singapore, China, the Philippines, the United States, Switzerland and Spain

• 5,759 port calls in 104 countries during 2014• 213 employees ashore• 20 nationalities with a gender distribution of

37% female and 63% male• 798 seafarers on board owned vessels

OVERVIEW · ANNUAL REPORT 2014 5

Who we areWe consider ourselves a value-driven organisa-tion with Accountability, Respect, Competence, Enthusiasm, Entrepreneurship and Team Spirit representing the essence of who and what we are. Our attitudes, decisions and actions always reflect our values.

Our value creation is anchored in the ability of our people to build and manage relations with our clients and hereby understand and fulfil effi-ciently many different types of transportation re-quirements.

Our aim is to be considered always approach-able, always accountable and always looking to-wards shared value creation.

We can only achieve this by attracting and devel-oping high-calibre talented people, who anchor themselves in our tradition for open communica-tion, in combination with our organisational structure and tools, and who are empowered to develop our business.

We believe that part of a quality service is to con-duct business in a responsible manner creating benefits broadly while being open, fair and hon-est in all our activities.

Lauritzen Kosan

Lauritzen Bulkers

0% 20% 40% 60% 80% 100%

Africa Asia Oceania Europe North America South America

Business strategyDuring 2013-14 we made wide-ranging adjust-ments to our business portfolio, and this has al-lowed us to devote our full attention to the devel-opment of Lauritzen Bulkers and Lauritzen Kosan. The strategies of Lauritzen Bulkers and Lauritzen Kosan share the objective of creating value to our owner and clients by being reliable and trustwor-thy providers of marine transportation services on a global scale. Our two business units operate in two distinctly different segments of the shipping industry, and their respective business models dif-fer, yet, they share the following strategic attri-butes:

• Build and manage long-term relations with clients and stakeholders

• Create insight via building critical mass in selected segments

• Embrace complexity, leverage skills and competencies

• Select and invest in talent

Geographic distribution of imports, 2014

OVERVIEW · ANNUAL REPORT 20146

Highlights 2014

2014 turned out to be considerably more difficult and challenging than we anticipated. After a somewhat disappointing first half of 2014 in terms of global economic growth and world trade, some improvement was expected in the second half of the year. However, as the year progressed, our market forecasts were repeatedly revised down-wards, and the cautious optimism we expressed mid-year for the markets beyond Q3 had to be ad-justed.

J. Lauritzen’s net results for 2014 were USD (165.7)m compared to USD (284.6)m in 2013. The results were in line with our most recent expecta-tions but considerably below our expectations, not only at the beginning of the year but also at the presentation of the results for the first half year of 2014. The results were unsatisfactory in financial terms but an outcome consistent with a very diffi-cult year.

The results for 2014 were heavily impacted by special items net totalling USD (118.9)m, in particular due to impairment losses and provisions. In 2013, special items net totalled USD (136.1)m also mainly related to impairment losses. Furthermore, net results for 2014 included USD 18.7m profit from discontinued operations com-pared to USD (47.8)m in 2013.

On a comparable basis, excluding special items and profit from discontinued operations, the net results for 2014 were USD (65.6)m compared to USD (100.7)m for 2013.

At year-end 2014, the solvency ratio amounted to 47% (2013: 39%) and cash and undrawn commit-ted credit facilities stood at USD 284m (USD 154m). Net debt amounted to USD 268m equal to 37% of broker values (in 2013 USD 631m and 62%, respectively).

The business environmentThe global economy experienced an uneven de-velopment during 2014, with recovery to acceler-ated growth in the US, slowdown in China, deteri-oration of the growth outlook for the emerging economies and increased risk of recession in Eu-rope.

2014 turned out to be another year of headwind in terms of transforming global economic growth into global trade. Declining commodity prices during the year reduced the incentive to have much in storage to the detriment of seaborne trade. Thus, the anticipated market improvement for dry bulk carriers and smaller gas carriers in the second half of 2014 did not materialise.

OVERVIEW · ANNUAL REPORT 2014 7

Falling crude oil prices in the second half of the year led to reduced bunker prices and reduced the incentive to slowsteam, effectively increasing the supply of carrying capacity.

Main events in 2014During 2014, we succeeded in executing signifi-cant adjustments to our business portfolio, in-cluding the exit from the product tanker and shut-tle tanker segments.

The completion of these adjustments allowed us to devote our full attention to the development of Lauritzen Bulkers and Lauritzen Kosan.

A range of initiatives and adjustments were initi-ated in Lauritzen Bulkers with a view to increasing the value creation from transforming a significant number of shipping transactions into knowledge and market insight that enable Lauritzen Bulkers to take additional but time-limited shipping risk and hereby generate additional earnings from spot trading activities.

At Lauritzen Kosan, efforts were made to strength-en the business model, which is rooted in the abil-ity to, repeatedly, deliver reliable performance in a niche market surrounded by complex require-ments.

In order to simplify the legal structure of the J. Lauritzen Group, the decision was taken to merge subsidiary group companies with the parent com-pany in Denmark and Singapore, respectively. Lauritzen Bulkers and Lauritzen Kosan remain the trading names of our business activities.

During 2014, Lauritzen Bulkers and Lauritzen Ko-san controlled a combined average fleet of 147 vessels compared to 155 vessels in 2013. At year-end 2014, we owned 19 bulk carriers (average age of 4.6 years) and 22 gas carriers (average age of 9.8 years).

Our newbuilding programme consists of four su-pramax and two handysize dry bulk carriers. Two additional handysize dry bulk carriers have been ordered in a joint venture. The newbuildings are expected to be delivered through 2016-18.

Axis Offshore, our joint venture in the Accommo-dation and Support Vessel (ASV) segment, has two high-specification semi-submersible ASVs under construction with expected delivery in 2015 and 2016.

Assets and solvencyTotal invested capital was USD 836m at year-end 2014, down from USD 1,225m at year-end 2013.

The total book value of vessels amounted to USD 773.0m, down USD 248.1m on 2013 due to the sale of assets, impairment losses and deprecia-tion. Brokers’ valuations of vessels were on aver-age down 9% on 2013.

OVERVIEW · ANNUAL REPORT 20148

USDm 2014 2013 2012 2011 2010

Income statementRevenue 443 501 558 587 665Time-charter equivalent income (TCE) 351 352 388 520 588Operating income before depreciation (EBITDA) and special items 15 7 17 126 192EBITDA accounted for as discontinued operations 16 48 55 N/A N/AProfit/(loss) on sale of vessels and other assets 14 (8) 2 8 (12)Depreciation (56) (63) (75) (91) (75)Share of profit in joint ventures (1) (6) (8) 5 11Operating income (EBIT) before special items (28) (70) (64) 48 115Special items, net (119) (136) (200) (25) 82Financial items, net (40) (31) (41) (69) (56)Profit/(loss) from continuing operations before tax (187) (237) (305) (46) 141Profit/(loss) from discontinued operations 19 (48) (43) N/A N/AThe J. Lauritzen Group's share of profit/(loss) (166) (285) (350) (46) 131

Balance sheetNon current assets 952 1,185 1,931 2,361 2,062Total assets 1,208 1,877 2,315 2,682 2,411J. Lauritzen's share of equity 573 740 852 1,199 1,239Non-current liabilities 424 754 1,297 1,311 967Invested capital * 836 1,225 1,469 2,344 2,049Net interest bearing debt (NIBD) * 268 631 685 1,160 840

Cash flows and financial ressourcesCash flow from operating activities 60 (20) 34 86 164Cash flow from investment activities 553 28 (108) (330) (325)- hereof investments in vessels, machinery and equipm. (43) (118) (190) (438) (538)Cash flow from financing activities (572) (126) 107 323 142Changes for the year in cash and cash equivalents 41 (118) 33 79 (19)Financial ressources at the end of the year 284 154 268 292 202

Key figures and financial ratios Average number of employees * 1,064 1,125 1,167 1,300 1,148 Total number of ship days * 53,515 56,736 59,156 55,115 54,385 DKK exchange rate year-end 612 541 566 575 561 Average DKK exchange rate 562 562 580 536 563

Profit margin (6.1)% (12.7)% (10.0)% 7.4% 15.6%NIBD/EBITDA * 17.5 86.2 39.4 9.2 4.4Solvency ratio 47% 39% 37% 45% 52%Return on equity (ROE) (25.3)% (35.8)% (34.1)% (3.8)% 11.1%Return on invested capital (ROIC) * (14.3)% (15.3)% (17.1)% 1.1% 10.2%

* Continuing operations only in 2012-2014

Group Key Figures

In 2013, J. Lauritzen decided to discontinue its operations in Lauritzen Offshore - Shuttle tankers and Lauritzen Tankers and thus these activities

have been accounted for as discontinued operations for the periods 2012-2014. Comparison figures for 2010-2011 have not been represented.

The key figures have been calculated as follows:

Profit margin: Operating income before special items excl. Share of profit in joint ventures x 100 / Revenue

Solvency ratio: Total equity, year-end x 100 / Total equity and liabilities, year-end

Return on equity: J. Lauritzen’s share of profit/(loss) x 100 / J. Lauritzen’s average share of equity

Invested capital: Total assets less cash, securities, non operational assets and non interest-bearing current liabilities

Return on invested capital: Operating income after special items x 100 / Average invested capital

Net interest bearing debt (NIBD): Interest-bearing liabilities, less subordinated loan, interest-bearing assets and cash

NIBD/EBITDA: NIBD / Operating income before depreciation and special items

OVERVIEW · ANNUAL REPORT 2014 9

Capital structure USDm

Revenue USDm

Selected key figures USDm

Cash flow from operations and financial resources USDm

-400

-300

-200

-100

0

100

200

2010 2011 2012 2013 2014

EBITDA EBIT

Result for the year Special items, net

0

200

400

600

800

2010 2011 2012 2013 2014

Lauritzen Bulkers Lauritzen Kosan Other Discontinued oper.

0

500

1,000

1,500

2,000

2,500

3,000

2010 2011 2012 2013 2014

Total equity Non-current liab. Current liab.

-50

0

50

100

150

200

250

300

2010 2011 2012 2013 2014

Cash flow from operating activities Financial resources

OVERVIEW · ANNUAL REPORT 201410

Outlook 2015Global economic activity is expected to increase slightly in 2015 primarily due to solid growth in the US, whereas the European area is struggling to avoid recession. The contribution to global growth from China and from emerging economies is ex-pected to decrease. China’s economy is gradually changing from investment driven growth towards consumption driven growth. We see this as a risk for further decrease of Chinese import growth of raw materials to the detriment of demand for dry bulk shipping.

The current low oil prices are, however, expected to turn out to be a stimulus to global growth, and the availability of low priced LPG in combination with the US recovery is e.g. expected to support demand for gas carriers.

Increases in protectionist measures and sanctions that reflect ongoing geopolitical conflicts repre-sent a threat to global trade and marine transpor-tation. The existing Indonesian mineral export ban and the Chinese coal import restrictions are ex-pected to continue to have a negative impact on demand for dry bulk shipping.

Tonnage supply is expected to grow slightly stronger than demand growth in 2015, and net fleet growth is expected to further increase in the coming years due to significant ordering in 2013 and 2014. The incentive to slowsteam has been reduced with the current low bunker oil prices ef-fectively causing an additional increase in carry-ing capacity.

Based on the above, we expect market conditions and the overall business environment in 2015 to remain as challenging as in 2014.

EBITDA before special items for 2015 is expected to be within the range USD (20)m-30m, compared to USD 15m in 2014.

Net results are expected to be USD (70)m-(20)m, up compared to USD (166)m in 2014 where spe-cial items net had an impact of USD (119)m on the net results.

Currency and interest rate fluctuations as well as effects from the sale of assets, if any, may impact the result.

BUSINESS · ANNUAL REPORT 2014 11

Lauritzen Bulkers

2014 2013

Revenue 311.5 319.5

Time-charter equivalent income 248.8 238.6

EBITDA before special items 6.4 (12.1)

Depreciation (29.5) (36.9)

Profit/(loss) on sale of vessels etc. 13.4 (10.7)

Share of profits in joint ventures (3.9) (11.9)

Operating income before special items (13.6) (71.6)

Special items, net (118.9) (136.1)

Operating income after special items (132.5) (207.7)

Ship-days 39,118 40,895

Key figures USDm

0

20

40

60

80

100

120

0

20

40

60

80

100

2010 2011 2012 2013 2014 Handysize Supramax

Capesize Total (RHS)

Agricultural products

Construction materials

Metals

Energy

Minerals

Activity (average no. of ships)

Cargo mix, 2014

Operating income from our dry bulk activities be-fore depreciation (EBITDA) and special items amounted to USD 6.4m in 2014 which was up compared to USD (12.1)m in 2013. The activity level, measured by performed ship-days, declined by 4% compared to 2013.

The results for 2014 were negatively impacted by special items net totalling USD (118.9)m which comprised impairment losses and provisions to-talling USD (161.0)m, revenue from the sale of a counterparty claim relating to STX Pan Ocean and other settlements totalling USD 31.7m as well as a profit of USD 10.4m from sale of vessels also as a consequence of the STX Pan Ocean default. For comparison, the results for 2013 were impacted by special items net totalling USD (136.1)m main-ly related to impairment losses.

Operating income after special items amounted to USD (132.5)m compared to USD (207.7)m in 2013.

Measured by time-charter equivalent income, the total income in 2014 amounted to USD 248.8m, with USD 9,012/day in the handysize segment, USD 9,958/day in the supramax segment and USD 29,518/day in the capesize segment. The spot trading activity contributed with USD 8.4m, net.

During 2014, we worked on a range of initiatives and organisational adjustments to focus our busi-ness activities and to improve our ability to gener-ate value in fluctuating markets, in particular from spot trading activities.

Market conditions turned out to be considerably more difficult in 2014 than expected, and we ex-pect the business environment to remain chal-lenging throughout 2015.

ACTIVITY IN 2014In 2014, the total number of ship-days performed reached 39,118 corresponding to 107 vessels on average, compared to 40,895 ship-days with 112 vessels on average in 2013. Spot ship-days amounted to 10,311 compared to 8,897 in 2013 due to increased focus on the spot trading activi-ty.

Measured by the number of fixtures, which amounted to 1,098 in 2014, the activity in 2014 was on par with 2013. Our client base totalled more than 250 clients.

0

10,000

20,000

30,000

40,000

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2010-01 2011-01 2012-01 2013-01 2014-01 2015-01

Average of the 4 T/C Routes for Baltic Capesize Index - LHS Average of the 6 T/C Routes for Baltic Supramax Index - RHS Average of the 6 T/C Routes for the Baltic Handysize Index - RHS

Spot market rates since 2010 in time-charter equivalent USD/day

Source: Own analysis based on data from clarkson research services

BUSINESS · ANNUAL REPORT 201412

GLOBAL MARKET DEVELOPMENTSThe dry bulk markets started 2014 with expect-ation of a recovery in the second part of 2014. Fol-lowing the trough related to the Chinese New Year, the expected seasonal uptick in Q2 did, how-ever, not materialise due to a combination of ne-gative events, including the effects of the mineral export ban imposed by Indonesia. This and the slowdown in Chinese coal imports dented the ex-pected rate improvements in the latter part of Q3 and into Q4. Despite overall robust demand growth (approximately 6%) that actually exceed-ed nominal supply growth (approximately 5%) freight rates were disappointing. The decreasing bunker prices in H2 reduced the incentive to slow-steam, and this effectively increased the supply of carrying capacity in addition to the nominal sup-ply growth.

The annual spot market average (on time-charter equivalent basis, as reported by Clarkson Re-search Services) was down 6% in the handysize segment, down 4% in the supramax segment and down 2% in the capesize segment compared to 2013.

STRATEGY AND BUSINESS MODELA strong presence in the handysize bulk carrier segment is the hallmark of Lauritzen Bulkers’ strategy.

The objective is to deliver competitive and reliable transportation services to our clients while gener-ating earnings to our owner exceeding market lev-els.

The dry bulk market is generally characterised by solid demand, fragmentation among carriers, strong price competition and fluctuating capacity

utilisation. This allows us ample possibilities to provide dry bulk shipping services on the basis of a large homogeneous fleet consisting of a core of owned, part-owned and long-term time-chartered vessels, vessels committed by partners and a sub-stantial volume of shorter term time-chartered vessels.

Our business model in handysize is rooted in our ability to transform a significant number of ship-ping transactions into knowledge and market in-sight. We have a strategic goal to employ a similar approach in the neighbouring supramax segment as this will allow us more opportunity to leverage our business model.

To achieve this we pay special attention to:• Positioning: Remain a preferred carrier by

having strong client focus and providing first-class dry bulk shipping services

• Performance: Optimise fleet utilisation in order to minimise ballasting days

• Processes: Always look to improve and trim processes to reduce costs and ensure scalability

• Spot trading: Leverage our knowledge and take additional time-limited shipping risk, i.e. additional positions in cargo, periods or ship-days, and thereby generating additional earnings

In addition to our presence in the handysize and supramax bulk carrier segments, we have a limit-ed presence in the capesize segment with two owned vessels long-term employed to a reliable counterparty. We do not wish to take new active shipping risk in this segment and our focus is strictly to act as shipowners under existing long-term charters.

BUSINESS · ANNUAL REPORT 2014 13

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

100%

Capesize Supramax Handysize

2015 2014

Business risk managementFluctuations in freight rates is the primary risk fac-tor associated with our business model. With a business strategy focusing on the handysize and supramax segments, the majority of our business is concluded in the spot and shorter term period market and market volatility is thus reflected in our earnings. The existence of market volatility is, however, also supportive for our strategy to earn margins from our spot trading activities.

Based on our outlook for handysize and supramax dry bulk carriers, the contract coverage for 2015 in relation to our committed fleet in handysize is approximately at the same level as early 2014, whereas coverage for our committed supramax fleet has increased, to some extent due to a de-crease in the fleet size. In the capesize segment, the relatively high coverage reflects our aim only to have vessels employed on longer term con-tracts.

Other important risk factors associated with our business model are access to tonnage, credit risk related to counterparties and fleet portfolio man-agement. We manage risk in relation to these fac-tors in the following way:• Tonnage: Securing and rejuvenating the

controlled fleet with focus on size and fuel efficiency. Obtaining flexibility in charter parties in terms of trading, period and purchase options

• Counterparties: Careful scrutiny of counter-parties, including i.a. their trading history, prior to concluding longer term contracts within predefined limits

• Fleet portfolio management: Balancing the needs for control, flexibility and commitment by having a core fleet of owned, part-owned and longer-term time-chartered vessels, vessels committed by partners as well as short-term chartered vessels enabling our spot trading activity

Coverage at the beginning of the year

BUSINESS · ANNUAL REPORT 201414

Core fleet and vessels committed by poolpartners at year-end 2014

2015 2016 2017 2018

Owned

Handysize 2

Supramax 2 1 1

Part-owned

Handysize 2

Supramax

Chartered

Handysize 3 6 3

Supramax 1 1

Total 4 9 8 1

Handysize 3 6 7

Supramax 1 3 1 1

Deliveries of newbuildings

Handy-size

Supra-max

Cape-size

Total New-buildings

Owned 17 0 2 19 6

Part-owned 10 0 0 10 2

T/C in 25 10 2 37 14

Pool, etc. 11 0 0 11 0

Total 63 10 4 77 22

FLEETIn 2014, our core fleet averaged 57 vessels (un-changed from 2013). Vessels committed by pool partners averaged 22 (down from 30 in 2013). At year-end 2014, our core fleet and vessels commit-ted by pool partners comprised 63 handysize, ten supramax and four capesize bulk carriers.

Two supramax vessels, sold in 2013, were deli-vered to new owners, and a further two were sold and delivered during 2014. Two capesize vessels were also sold and delivered to their new owners in 2014, reflecting our strategy to exit this seg-ment as an active player. A total of 16 long-term time-chartered vessels were delivered to the core fleet while ten vessels were redelivered to owners during 2014.

Four scheduled dry dockings were completed in 2014. Unscheduled off-hire for our owned fleet came to 0.47% of available ship-days in 2014 (0.57% in 2013).

At year-end 2014, the average age of the owned fleet was 4.6 years (3.3 years at year-end 2013).

The newbuilding programme includes six owned vessels and a further two vessels ordered by a joint-venture formed together with Sincere Indus-trial Corporation with scheduled delivery in 2016-18. Various tonnage providers are expected to de-liver a further 14 newbuildings on long-term time-charter to us.

PERFORMANCEWe work with our processes and organisation to ensure our competitiveness in a cost-focused market, where we see reliability, quality and glo-bal presence as a way to deliver value.

Increasing vessel performanceOur technical department implemented Vessel Energy Renovation Plans (VERP) on four vessels during 2014 (three vessels in 2013). VERP is a fleet performance catalogue that covers the opti-misation of auxiliary machine consumption, in-cluding pumps, fans and air conditioning, plus ad-ditional initiatives for technical and operational optimisation.

Vessel Energy Renovation Plans have been implemented on seven vessels over the last

two years realising fuel-savings of approximately 7%

A performance desk was established during 2014 to strengthen our efforts within energy-efficiency and increasing fleet performance. This new func-tion is establishing a Key Performance Indicator system for all performance-related data as a tool to streamline efficiency and at the same time stimulate a performance-oriented culture.

Operational excellenceDuring 2014, our operations department began utilising the Optimum Ship Routing (OSR) plat-form provided by WNI Weathernews Internation-al, enabling us to work in an even more structured way with day-to-day performance analysis, pro-jected fuel consumption and routing recommen-dations.

Note: Not including vessels with a charter duration of less than 12 months

BUSINESS · ANNUAL REPORT 2014 15

Our RightShip risk profile To benchmark our efforts to ensure low-risk op-erations, we utilise RightShip’s database, the Ship Vetting Information System (SVIS) to rate our owned vessels. The SVIS data provide evalu-ation of vessels based on factors such as flag and class performance, technical manager perfor-mance, yard profile, casualty history, terminal re-ports and age.

The average risk rating of the owned fleet was unchanged and satisfactory at 4.9 on the Right-Ship vetting scale (with 5.0 as the best rating) at year-end 2014. The rating supports our ambition to remain a preferred carrier.

PEOPLETo ensure quality operations at all organisational levels ashore and at sea, we rely on employees with the right sets of skills and ethical mindset.

Transforming the organisationDuring the year we continued our shift towards a more client-oriented business model. The transi-tion has allowed us to attract new talent to open positions and at the same time protect the know-ledge and know-how already present. To support the organisational transformation we have initiated projects facilitating interaction across the organisation as we wish to foster and stimulate a feedback culture. In 2014, a project dedicated to further streamlining our processes and increasing our operational performance also allowed us to work in a more cross-functional manner.

Building on our relationsIn 2014, we continued to focus on building and managing relations with clients, trading houses, shipyards, technical managers and crews.

As part of our strategy to move closer to our clients,

we opened a new office in Geneva, Switzerland

Newbuildings for our own account are all being built at Japanese shipyards or at Japanese co-owned shipyards. Likewise, newbuildings for de-livery in 2015-17 on structured charter deals are solely being built at Japanese shipyards. Many of these shipyards and the trading houses involved have been our partners for decades, and in 2014 we strengthened our relationship activities as Japanese tonnage suppliers are essential for our tonnage strategy.

Technical management, including crewing for our owned fleet, is performed by New Century Over-seas Management Inc., Manila, and Synergy Ma-ritime Pte., Singapore providing safe, cost-effect-ive and reliable vessel operations controlled and supervised by our in-house technical department.

As part of our ambition to get closer to the crews onboard our owned vessels, we are conducting regular officer seminars with support from our technical managers.

OUTLOOK FOR 2015We expect demand growth for transportation of dry bulk commodities to be on par with or slightly lower than in 2014.

Fleet growth of bulk carriers is expected to in-crease compared to 2014, albeit only marginally. The decrease in bunker oil prices is, however, ef-fectively causing an additional increase in the car-rying capacity as the incentive to slowsteam has decreased. The dry bulk markets are already struggling with oversupply, and further capacity increases are negative for the market balance.

With demand and supply growth expected to al-most equal out each other in 2015, only marginal-ly improved markets are expected for 2015 com-pared to 2014.

In 2015, we expect to employ 90 handysize and 25 supramax vessels on average.

Note: Not including vessels with a charter duration of less than 12 months

BUSINESS · ANNUAL REPORT 201416

Lauritzen Kosan

0

10

20

30

40

50

0

5

10

15

20

25

2010 2011 2012 2013 2014

Semi-refrigerated Ethylene Fully-pressurised (F/P) Total (RHS)

LPG

Propylene

Butadiene

Ethylene Other

Activity (average no. of ships)

2014 2013

Revenue 131.8 180.8

Time-charter equivalent income 102.3 112.5

EBITDA before special items 17.9 28.1Depreciation (26.5) (26.5)

Profit/(loss) on sale of vessels etc. - 1.3

Share of profits in joint ventures 1.3 0.8

Operating income before special items (7.3) 3.6Special items, net - -

Operating income after special items (7.3) 3.6Ship-days 14,397 15,841

Cargo mix, 2014 Key figures USDm

EBITDA before special items from our gas carrier activities amounted to USD 17.9m in 2014 com-pared to USD 28.1m in 2013. Challenging market conditions for smaller semi-refrigerated gas carri-ers and a decrease in activity level, measured by ship-days down 9% compared to 2013, were the main contributing factors.

Operating income amounted to USD (7.3)m com-pared to USD 3.6m in 2013.

Measured as time-charter equivalent income, the total income in 2014 amounted to USD 102.3m, with notable differences between vessel types and sizes, ranging from USD 6,971/day for the fully-pressurised carriers, USD 9,883/day for the semi-refrigerated carriers to USD 14.436/day for the ethylene carriers.

During 2014, we made efforts to strengthen our business with focus on improving performance while building closer relations to existing clients and potential new business partners. One out-come from the activities was the agreement with Odfjell Gas to have two of their ethylene gas carri-ers join our ethylene gas carrier pool.

Market conditions turned out to be considerably more difficult in 2014 than anticipated, and we ex-pect the business environment to remain chal-lenging in 2015.

ACTIVITY IN 2014In 2014, the total number of ship-days performed reached 14,397 corresponding to 39 vessels on average, compared to 15,841 ship-days with 43 vessels on average in 2013. We maintained a strong presence in the Atlantic basin with transat-lantic cargo contracts as well as an increasing number of LPG exports from the US.

Our client base, representing some of the world’s largest oil majors and energy traders, totals some 90 clients, and the top 10 clients accounted for half of the 2014 revenues. The vast majority are repeating clients.

BUSINESS · ANNUAL REPORT 2014 17

0

100

200

300

400

500

600

700

2010-01 2011-01 2012-01 2013-01 2014-01

F/P (3,500 cbm., trading east of Suez) F/P (3,500 cbm., trading west of Suez)

Semi-refrigerated (6,500 cbm) Ethylene (10,000 cbm)

Spot market rates since 2010 in time-charter equivalent 1,000 USD/month

Source: Own analysis based on data from Fearnley’s

GLOBAL MARKET DEVELOPMENTSAfter some improvement in the market balance during the first part of 2014, a set-back was seen during the second half. Economic and geopolitical factors contributed to disappointing overall de-mand growth for smaller gas carriers in 2014. An-other factor that put a strain on the market was a number of unscheduled turnarounds in the petro-chemical industry which reduced availability of products for exports.

STRATEGY AND BUSINESS MODELLauritzen Kosan specialises in safe and efficient carriage of petrochemicals and liquefied petroleum gases on a global basis - a segment of the shipping industry characterised by technically complex re-quirements from regulators and clients.

The strategy is based on our brand and rooted in years of solid operational performance. We strive to remain a leading, reliable, high quality provider of safe and flexible transportation to our clients and in this way generate value to our owner.

We control and operate smaller semi-refrigerated, ethylene and fully-pressurised gas carriers in the 3-10,000 cbm segment serving the petrochemical companies, oil majors and traders. The underlying

long-term drivers of demand for smaller gas carri-ers are the global consumption of plastics and li-quefied petroleum gases (for fuel and heating pur-poses as well as petrochemical feedstock). In the shorter term, the demand for transportation is fluc-tuating with production cycles in the refinery and petrochemical industry.

The reliability of our performance has earned us the trust of our

many repeating clients

Our business model is based on our ability to main-tain reliability and embrace complexity:

• Maintain reliability: Continuous focus on im-provements through education and training, innovation and careful implementation of pro-cedures to ensure our reliability as service pro-vider to our clients

• Embrace complexity: Strong collaboration be-tween the commercial departments and our in-house technical department to ensure that we meet the strictest health, safety and envi-ronmental standards and stringent require-ments from clients and authorities

BUSINESS · ANNUAL REPORT 201418

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

100%

Fully-pressurised Semi-refrigerated Ethylene

2015 2014

Business risk managementVessel employment and fluctuating freight rates are key risk factors associated with our business model. Cargo contracts that are renewed annually form the majority of our business. The contract coverage at the beginning of 2015 is slightly lower for our fully-pressurised gas carriers but slightly higher for our semi-refrigerated gas carriers and ethylene carriers compared to last year. The changes reflect market conditions as well as a change in committed days.

Compliance, utilisation and fleet portfolio man-agement are other important risk factors associ-ated with our business model. We manage risk in relation to these risk factors in the following way:

• Compliance: In a business with complex re-quirements from regulators and clients, lack of compliance can have detrimental impact on our daily business and on our long-term business relations. In all aspects of our business we thus have strict focus on complying with requirements to be able to trade for any client anywhere

• Utilisation: A significant part of our business is concluded as cargo contracts (COAs) and we strive to balance the need to provide ton-nage to meet contract requirements with additional employment from time-char-ter and spot contracts in order to maximise fleet utilisation

• Fleet portfolio management: Tonnage char-tering, part-ownership (joint ventures), pool- partnership and sale and purchase of vessels are core elements of our fleet portfo-lio management. The limited size of the market for smaller gas carriers, however, restricts the availability of tonnage for char-tering and likewise limits sales & purchase turnover

Coverage at the beginning of the year

BUSINESS · ANNUAL REPORT 2014 19

Semi-refrigerated Ethylene Fully-pressurised Total New-buildings

Owned 6 6 10 22 0

Part-owned 0 3 0 3 0

B/B in 6 0 0 6 0

T/C in 0 0 2 2 0

Pool, etc. 6 4 0 10 0

Total 18 13 12 43 0

Vetting PerformanceThe 27 gas carriers that are technically managed in-house were inspected 124 times by oil majors during 2014. During the year, we focussed par-ticularly on improving performance under the Oil Companies International Marine Forum’s (OCIMF) Ship Inspection Report Programme (SIRE).

Our target for SIRE inspections in 2014 (4.5 observations per vetting inspection) was met with an average of 4.1 observations per vetting inspection. Crew-related observations accounted for an average of 1.5 of the total observations. The last 2.6 observations related to office and vessel construction and design observations. Vetting performance is a reflection of the safety performance of our company. Our focus continues to be on strengthening the safety culture of our people onboard the vessels and in the offices. A reduction in the number of vetting observations will not only reduce the commercial implications originating from the vetting regime, but it will also contribute to creating safer operations of our vessels.

FLEETThe total operated fleet consists of owned, part-owned and chartered tonnage as well as vessels in commercial management (pool). In total, the com-bined average carrying capacity was 220,004 cbm in 2014 (224,737 cbm in 2013). At the end of 2014, the average age of the owned fleet was 9.8 years (9.3 years at year-end 2013).

On average, we operated a total fleet of 39 vessels in 2014. The average operated fleet of semi-refrig-erated gas carriers totalled 17 vessels (down one from 2013). We extended the bareboat charter on four vessels and now operate a modern fleet of smaller semi-refrigerated vessels following our sale of older tonnage and redelivery of older bare-boat-chartered vessels. The operated fleet of fully-pressurised gas carriers decreased to 12 vessels in 2014. The fleet of ethylene gas carriers decreased in 2014 to 11 vessels.

In 2014, we conducted eight scheduled drydock-ings (14 in 2013). Unscheduled off-hire came to 1.6% of available vessel days in 2014 (1.9% in 2013).

PERFORMANCEThe ever-changing regulatory agenda is setting an increasingly demanding scene for ship manage-ment in terms of both complexity and costs. How-ever, we see increased complexity as an opportun-ity. Working proactively with regulators and increased demands are embedded in our business model. We continuously monitor new demands and we prepare and invest to meet future demands from regulators and clients always focusing on competitive ship management and pushing the boundaries of best practice.

Improving energy-efficiencyOur performance management department moni-tors, develops and implements energy-efficiency initiatives as part of our REJUICE programme, a systematic approach to assessing and achieving fuel-savings.

Since 2012, our energy-efficiency related to trans-port work has improved by more than 15% across our owned fleet. Our initial focus has been to de-velop a solid data platform for ongoing monitoring and evaluation of performance. Enhanced data collection through auto-logging and KPI tracking has been added to the traditional daily reports to form the basis for an automated reporting system that provides us with a reliable and current over-view of the performance of our fleet.

In 2014, focus on optimising trim and ballasting, as well as limiting hull and propeller fouling, contrib-uted with approximately 6% fuel savings. Looking into 2015, further improvements are expected as we introduce enhanced weather routing and initia-tives to increase crew awareness on energy-effi-ciency. The implementation of an enhanced KPI structure will support and motivate energy-effi-ciency efforts onboard our owned vessels.

Core fleet and vessels committed by pool partners at year-end 2014

BUSINESS · ANNUAL REPORT 201420

PEOPLETo ensure quality operations at all organisational levels ashore and at sea, we rely on employees with the right sets of skills and ethical mindset.

Strengthening the organisationWe continued the organisational changes initiated in 2013 resulting in closer collaboration between our commercial, operational and technical depart-ments. These changes provided us with the ability to better understand and meet clients’ expecta-tions.

Supporting the organisational transformation, ad-ditional focus was on facilitating knowledge shar-ing and empowerment of our employees with the objective of ensuring competitive ship manage-ment.

During the year, our technical organisation was ex-panded in Manila, the Phillipines.

Focus on our safety cultureSafeguarding our people, the environment and our clients’ cargoes is the crux of our health and safety efforts and improving the safety culture for all em-ployees is always on top of our agenda.

All crew members are introduced to Lauritzen Ko-san at a Safety Culture Awareness course and on the basis of this our senior officers are enrolled in the Lauritzen Kosan Leadership and Management course, empowering leaders on board our vessels with our management culture and tools.

Lost Time Injury Frequency was 0.5 in 2014

While the human element is one of many factors we work with, we also include IT and business in-telligence as part of our efforts. In 2014, we contin-ued to work with identifying trends and patterns to improve our performance. Combining our experi-enced seafarers, our company culture and IT tools form the basis of our strategic work to create value and increase safety performance.

Long-term relationsAn open dialogue and face-to-face meetings are an important part of the way we build trust and devel-op our business relationships. Identification and insight of our clients’ priorities enable us to im-prove our services as well as create a solid basis for future investments and new tonnage.

Our competitiveness and service are demonstrated by the fact that many clients have had their con-tracts with us for more than 15 years.

OUTLOOK FOR 2015In 2015, we will continue to pursue our strategy of leveraging both our brand and technical manage-ment platform to build long-term relations with our existing as well as potential new clients. In addi-tion, we will continue to work to optimise the com-position of our fleet, both through pool arrange-ments as well as through the evaluation of existing time charters.

In 2015, we anticipate a slight improvement of the market balance. Supply is projected to grow by ap-proximately 6% with especially fully-pressurised as well as larger semi-refrigerated tonnage continu-ing to flow into the market. Demand growth is ex-pected to grow slightly faster, assuming a stabilisa-tion of energy and petrochemical prices, and a reduction of maintenance and outage of refining and petrochemical plants.

Rate improvements are only expected to a limited extent in 2015 and any case, it will be a recovery from low levels, particularly for the smallest size gas carriers.

We expect to employ 36 vessels on average in 2015. The decrease of the operated fleet is a result of redelivery of the bareboat-chartered vessels and fewer pool vessels.

BUSINESS · ANNUAL REPORT 2014 21

Other BusinessesIn addition to our main business activities in the dry bulk and gas segments, we have investments in the offshore service sector and a minor sharehold-ing in the product tanker segment. These invest-ments have originated as part of our own business activities.

Axis OffshoreWe hold 34% of the shares (50% of the voting rights) in Axis Offshore Pte. Ltd.

Axis Offshore was formed in 2012 as a joint ven-ture together with the Norwegian equity fund HitecVision, based on our existing business in the Accommodation and Support Vessel (ASV) seg-ment and our monohull ASV, the Dan Swift. In ad-dition to the Dan Swift, Axis Offshore has two high-specification semi-submersible ASVs under construction at the Cosco Qidong Offshore ship-yard in China. The newbuildings are expected to be delivered in 2015-16.

Our outstanding capital commitment to Axis Off-shore amounts to up to USD 67m to be injected in connection with the delivery of the two newbuild-ings. The actual amount to be injected depends on the financing structure of Axis Offshore.

Hafnia TankersWe hold 5.6% of the shares in Hafnia Tankers Ltd. The shares were acquired in connection with the sale of our fleet of product tankers to Hafnia Tank-

ers during 2013-14. Hafnia Tankers is a shipping company focused on ownership and chartering of tonnage in the product tanker segment.

Discontinued activitiesIn August 2013, the strategic decision was taken to exit the product tanker segment, cf. above and in October 2013 we sold our fleet of ten owned MR product tankers to Hafnia Tankers. The last of our owned product tankers was delivered to the new owner in Q1 of 2014.

Lauritzen Tankers contributed USD 2.8m to the 2014 results included as profit from discontinued operations.

In early January 2014, we announced that we had accepted an offer to sell Lauritzen Offshore’s fleet of three shuttletankers to Knutsen NYK Off-shore Tankers (KNOT). The vessels were deli-vered during Q2 and Q3 of 2014. The operational activities in Lauritzen Offshore Services were ter-minated simultaneously with the delivery of the vessels.

Lauritzen Offshore contributed USD 15.9m to the 2014 results included as profit from discontinued operations.

BUSINESS · ANNUAL REPORT 201422

People, Relations and Systems Our people, tools and systems enable us to build and manage our relations with stakeholders effi-ciently. Attracting and developing talented em-ployees is essential to us, as competent and moti-vated employees are an important foundation towards fulfilling our goals.

Ensuring employee developmentIn 2014, we amended our appraisal system by launching the Employee Development Dialogue (EDD). EDD is a tool assisting us in the implemen-tation of our business strategies by setting ambi-tious goals for each employee and linking individ-ual goals with individual development activities and business strategy. The new system supports our focus on stimulating a performance-oriented feedback culture. The system is aimed at our en-tire land-based organisation. As part of the imple-mentation of EDD, we have conducted mandato-ry workshop sessions both at the Copenhagen office and the Singapore office covering 95% of management being trained in the new approach. Almost all our land-based employees have attend-ed sessions introducing the EDD.

A new IT-platform for all human resource (HR) matters was introduced in 2014 to streamline and ensure more accurate and accessible HR data across the organisation.

Internal talent pipelineIt is important that we develop relationships with talents early in their careers and that we recognise our responsibility to develop these new talents.

In line with our recruitment strategy, we have tak-en steps to develop our internal talent pipeline by increasing the number of trainees. In 2014, new trainees joined us in Copenhagen, Singapore and Stamford, USA. At year-end, 6% of our land-based workforce was trainees.

In addition to trainees, we also welcome young talents conducting shorter internships in our of-fices. In Singapore, two interns were taken on-board as part of our commitment to the Global In-ternship Award, an initiative taken by the Maritime and Port Authority of Singapore as part of their ongoing efforts to promote maritime careers amongst the young talent pool in Singapore.

DiversityWe define diversity in terms of cultural width, ex-tensive experience, new inspiration and gender. Diversity is an important and natural prerequisite for innovation and development of our business.

We employ 20 different nationalities across our offices.

2014 was a year with influx of new graduates from universities as well as experienced shipping employees bringing experience from other parts of the industry.

In 2013, a policy for diversity management, in-cluding equal gender composition of all manage-ment levels, was approved by the Board of Direc-tors. Our target is that the overall gender distribution of employees shall be matched at management levels. The distribution of females and males in managerial positions of our shore-based organisation was 26% and 74% in 2014. We aim to reach the goal of 31% and 69% by De-cember 2015. The corresponding distribution be-tween females and males within the organisation as a whole remained stable at 37% and 63%.

Our aim to increase the number of females in managerial positions has led us to put further em-phasis on initiatives focusing on recruitment, staff development, measurement and benchmarking that may strengthen a more equal gender distri-bution amongst managers in 2015.

Executive Management has an equal gender dis-tribution.

At year-end 2014, the Board of Directors consist-ed of nine members, six elected by the general meeting and three by the employees.

With six board members elected by the annual general meeting, the diversity profile of the Board of Directors was 17% female with 34% coming from outside Denmark compared to 20% female and 40% coming from outside Denmark at year-end 2013. Our objective is to have two female board members by 2017 elected at the annual general meeting.

Employee developmentThe retention rate for shore-based personnel was 83% and remained at the same level as last year. Retirements, organisational changes, including the termination of our product and shuttle tanker operations affected the turnover of staff in 2014.

At year-end our total headcount was 1,011 com-pared to 1,108 in 2013.

BUSINESS · ANNUAL REPORT 2014 23

0

200

400

600

800

1,000

2013 2014

Seafarers Head office Overseas offices

2013 2014

Total workforce 2013-2014

The average age of shore-based personnel in-creased to 42.3 years (40.6 in 2013). The average length of service with J. Lauritzen increased slightly to 8.8 years (8.4 in 2013).

SeafarersAt Lauritzen Bulkers, ship management and crew-ing is outsourced to external service providers. Our in-house technical department controls and supervises the external managers to ensure safe, efficient operations and alignment of expecta-tions.

An essential part of Lauritzen Kosan’s services de-pends on crew performance, and all officers are selected carefully together with external crew managers. Technical management of the owned fleet is conducted in-house or by associated com-panies.

Irrespective of the technical management set-up, both business units conduct officer seminars to communicate specific topics and provide dia-logue and discussions between the shore and sea sides of our operations.

Strengthened global presenceThrough our offices in Singapore, China, USA, Spain, the Philippines, Switzerland and our head-quarters in Copenhagen, we are in close contact with our clients, brokers, tonnage providers and other stakeholders.

In 2014, our Singapore and Manila offices grew in terms of number of staff. The increased number of employees serving our clients in the Eastern Hem-isphere implied that both offices moved to new and larger facilities during the year.

A new office opened in Geneva in January 2015 providing proximity to our growing number of Swiss-based clients.

Networks for solutions and new insightsWe see network participation as a way of engag-ing and building leverage related to issues and challenges relevant to us and our industry. We participate in the following networks and commit-tees:

• The Danish Shipowners’ Association • The Danish Committee on Corporate

Governance• International Chamber of Shipping• BIMCO• The Baltic Exchange• Danish Society for Education and Business• The Trident Alliance• The Maritime Anti-Corruption Network• IMPA ACT• UN Global Compact

Our systemsInformation Technology (IT) systems are critical for the conduct of our business. Our IT infrastruc-ture and application management is outsourced to a third party provider, while our internal IT or-ganisation has the authority, capabilities and ca-pacity to manage the relationship in order to en-sure the desired quality and availability of the IT services.

Following a review of the existing set-up, a tender for renewal of the operation and maintenance of our systems was conducted during 2014, and to-wards the end of 2014 the transition to a new ser-vice provider was completed. During the year, we launched a new IT strategy plan with the objective of securing compliance with our business strate-gy based on a stable platform.

Building business intelligence

We regard superior knowledge as key to in-creasing performance and decided to establish a central Business Intelligence (BI) unit in 2014.

The BI function will help us transform internal and external data into meaningful and useful information for business analysis and thereby support improved decision making and provide basis for the development of new service offer-ings to our clients.

BUSINESS · ANNUAL REPORT 201424

Finance and Investor RelationsIt is a key objective for us to have access to diver-sified financial resources to finance our fleet of owned and part-owned vessels.

The owned fleet is financed with a mix of debt in-struments (bank facilities and issued bonds) and own funds. At year-end 2014, bank facilities ac-counted for 75% of the long-term debt with the remainder sourced from corporate bonds (net of own holdings).

Bank facilitiesThe bank facilities are provided by Scandinavian and international banks, financial institutions and in some cases supported by export credit agen-cies (ECAs).

The bank facilities are composed of amortising loan facilities (term loans) and revolving credit fa-cilities (long-term rights to draw liquidity on-de-mand). ECA-backed term loans are fully amortis-ing whereas other term loans typically are repaid as bullet loans at maturity which usually requires refinancing. Revolving credit facilities reduce the need to hold excess liquidity and are used to opti-mise our funding position and lower the net fi-nancing costs.

Facilities are obtained by J. Lauritzen A/S (the pa-rent company) or our subsidiary J. Lauritzen Sin-gapore Pte. Ltd., depending on vessel ownership, and are provided on the basis of collateral security including a mortgage on the vessels.

Corporate bondsWe currently have two corporate bonds outstand-ing. The first bond was issued in 2010 and the sec-ond in 2012. Both were issued with a five-year tenor and are listed on the Oslo Stock Exchange. To reduce the amount of relatively expensive debt, a nominal NOK 29m in the 2017-maturing bond and a nominal NOK 37.5m in the 2015-maturing bond were repurchased in 2014. In 2013, a nomi-nal NOK 259m was repurchased in the 2015-ma-turing bond.

Refinancing of maturing debtDuring 2014 we refinanced USD 226m (corres-ponding to 73%) of bank facilities originally scheduled to mature in 2015-17. This refinancing was provided by banks from the existing group of lenders after a tender process. The refinancing in-creased the share of revolving credit facilities. The remaining refinancing of bank facilities amounts to a total USD 83m during 2016-17.

A total of USD 71m, net (NOK 441m, net) of the bond debt will mature in May 2015.

Financing of newbuilding programmeOur newbuilding programme, comprising six owned dry bulk carriers, is scheduled to be deli-vered between 2016 and 2018. A committed post-delivery bank facility for up to USD 109m (65% loan to market value at delivery) covering all six vessels has been secured.

Financing of newbuildings to be part-owned via joint ventures will be raised directly in the joint venture entities.

Outstanding debt and commitment at year-end in USDm

Repayment profile of outstanding debt in USDm

Note: Existing facilities and commitments. Bond debt at hedged value less holdings of own bonds. Numbers may change subsequently

0

50

100

150

200

250

2015 2016 2017 2018 2019 > 2019

Repayment Bullet bank loans Bullet bonds Undrawn revolving credits

0

100

200

300

400

500

600

2014 2015 2016 2017 2018 2019Term loans Term loans ECA backedRevolving credits (drawn) Bonds unsecuredUndrawn revolving credits

Note: Existing facilities and commitments. Bond debt at hedged value less holdings of own bonds. Numbers may change subsequently

BUSINESS · ANNUAL REPORT 2014 25

CovenantsOur bank facilities include customary covenants: • Security maintenance: A requirement to

maintain a minimum value of the collateral security (e.g. a ratio between the fair value of the security and the outstanding debt in the particular facility) of typically 125%

• Financial covenants: A value-adjusted con-solidated solvency ratio of minimum 30%, consolidated liquidity of minimum USD 50m and consolidated working capital ratio (ratio between current assets and current liabilities) to be higher than 1

The corporate bonds have financial covenants re-quiring a consolidated solvency ratio of minimum 30% and a consolidated liquidity of minimum USD 50m. Prospectuses for the bonds are avail-able on http://www.j-l.com/about/investor-rela-tions

Throughout 2014, we complied with all coven-ants.

INVESTOR RELATIONSDue to the listing of corporate bonds on the Oslo Stock Exchange, we have since 2010 kept an on-going dialogue with current and potential inves-tors, analysts and other market professionals, providing them with easy and equal access to in-formation. Maintaining close relations with the investor community is important to us.

We want to provide timely, precise and relevant information about our business, results and ex-pectations and other matters that affect the per-ception and assessment of the securities we is-sue. It is our objective that the market price of the securities we issue fairly reflects our expected fi-nancial performance and our ability to repay our debt obligations as they fall due.

Stock Exchange Announcements 2014 The following Stock Exchange announcements were released in calendar 2014 via Oslo Stock Ex-change.

Announcement No. 1:Sale of three shuttle tankers

Announcement No. 2:Financial report for 2013

Announcement No. 3:New member of the Board of Directors

Announcement No. 4: Sale of counterparty claim

Announcement No. 5 :Interim financial report - first quarter 2014

Announcement No. 6:J. Lauritzen contemplates intra-group merger

Announcement No. 7:J. Lauritzen contemplates intra-group merger - update

Announcement No. 8:Interim financial report for the first half of 2014

Announcement No. 9:Interim financial report - third quarter 2014 Announcement No. 10:Write-downs and provisions

GOVERNANCE · ANNUAL REPORT 201426

Our corporate governance efforts are conducted in accordance with the “Recommendations for Corporate Governance” made by the Danish Committee on Corporate Governance and Section 107b of the Danish Financial Statements Act.

MANAGEMENT STRUCTUREIn accordance with the Danish Companies Act, we have a two-tier management structure con-sisting of two separate bodies: the Board of Direc-tors and the Executive Management. The Board of Directors is the central, supreme governing body. Day-to-day management is conducted by the Ex-ecutive Management in line with the rules and procedures laid down by the Board of Directors.

Board of DirectorsThe core task of the Board of Directors is to ensure that J. Lauritzen has a business strategy and ap-propriate capital structure, just as the Board must ensure the sound organisation of the activities of the company. In addition, focus is on risk manage-ment and internal control as well as ensuring that budgets and estimates are drawn up and ap-proved and that monthly and quarterly reports are submitted.

In 2014, the Board met six times, including a strat-egy seminar. Between meetings, recommenda-tions were submitted to the Board for written re-solution seven times.

The Board of Directors is supported by two per-manent committees: The Audit Committee and the Nomination and Remuneration Committee. The Audit Committee held five meetings and the Nomination and Remuneration Committee held two meetings in 2014.

At the general meeting in April 2014, five mem-bers were re-elected and Mr. Jesper Lok, (CEO, Falck Emergency as of January 2015) was elected as new member of the Board of Directors. At year-end 2014, the Board of Directors consisted of nine members, six elected by the general meeting and three by the employees.

With six board members elected at the annual general meeting, the diversity profile of the Board of Directors was 17% female with 34% coming from outside Denmark compared to 20% female and 40% coming from outside Denmark at year-end 2013. Our objective is to have two female board members by 2017.

The average length of board members’ service was eight years.

Corporate Governance

Lauritzen Foundation J. Lauritzen A/S was founded in 1884 and has been engaged in ocean transport for more than 130 years. The Lauritzen Foundation was estab-lished in 1945, and since then, it has been in full control of J. Lauritzen. The Lauritzen Foundation is a commercial foundation and is as such a self-governing institution under Danish law and is re-gulated by the Danish Act on Commercial Founda-tions. The Foundation is also subject to supervision by the Danish Ministry of Justice and the Danish Ministry of Business and Growth.

Through its charter, the Foundation is committed to promoting and developing the Danish shipping industry in general and supporting humanitarian work. Its policy is also to ensure flexible capital structures of the companies it owns.

In addition to its ownership of J. Lauritzen and its controlling interest in DFDS A/S (42.8% holding), the Lauritzen Foundation has holdings via wholly-owned LF Investment ApS in oil analysis, measu-ring equipment, software, healthcare products, biotechnology and real estate sectors.

The Lauritzen Foundation supports our goal of having a well-balanced financial structure, taking into consideration J. Lauritzen’s continued exist-ence and development.

Executive ManagementThe Executive Management is appointed by the Board of Directors and consists of Jan Kastrup-Nielsen, President & CEO and Birgit Aagaard-Svendsen, Executive Vice President & CFO. Day-to-day management is conducted by the Executive Management. An Executive Group functions as the coordinating forum for the day-to-day management and includes the Executive Management, Business Unit presidents and the heads of Corporate Control, Treasury and Corpo-rate Human Resources.

Additional informationPlease visit our corporate website for additional information on our Board Committees’ Terms of Reference, competence profiles of Board mem-bers and Principles of Remuneration at http://www.j-l.com/about/corporate-governance

Our statutory report on Corporate Governance 2014 is available at http://static.j-l.com/imce/jl_answer_cguk_2014.pdf

GOVERNANCE · ANNUAL REPORT 2014 27

Risk ManagementRisk Management is an integral part of our cor-porate governance and our policies on handling risk are approved by the Board of Directors.

RISK APPETITE AND TOLERANCESJ. Lauritzen enjoys strong brand recognition and it is vital to protect our reputation as an accountable quality shipowner and operator with high stand-ards in all aspects of safety and corporate gover-nance.

We create value by taking calculated business risk. We want to minimise our exposure to finan-cial risk and aim to keep a certain credit risk pro-file, defined by e.g. key financial indicators, sup-porting J. Lauritzen as being a solid and trustworthy business partner. Our risk tolerance related to operational issues such as fleet man-agement and safety is in principle zero.

BUSINESS RISKBusiness risk relates primarily to volatility in freight rates and asset values.

Our earnings generation benefits from the diversi-fication of our business portfolio which spans across distinctively different areas of maritime transportation as well as the presence in different vessel segments within the business units. Volati-lity in our earnings is further reduced via a delibe-rate combination of open and covered ship-days (including use of Forward Freight Agreements, FFAs).

The business strategies for the individual business units, including policies for contract coverage by vessel segments and overall limits for off-balance sheet exposure (such as chartered tonnage), are approved by the Board of Directors and reporting on these are an integral part of our internal report-ing routines. Please see the chapters about our business units for detailed information on their re-spective business models, contract coverage and management of their specific business risk.

Fluctuations in asset values affect our balance sheet, financial covenants and the minimum val-ue clauses in our loan agreements. Risk relating to fleet and asset values is managed by having a di-versified fleet comprising owned, part-owned as well as pool and time-chartered vessels with dif-ferent durations, optional periods and purchase options. Cash generation and profitability is mon-itored vessel-by-vessel.

2014 saw vessel values decline, and USD 1.2m in cash has been provided as additional security af-

ter year-end 2014 in one loan facility to comply with security covenants due to the decrease in vessel values. Should vessel values decrease by 10% during 2015 compared to the December 2014 valuations, nil would be required by year-end 2015 as additional security for the existing bank facilities.

FINANCIAL RISKCredit riskContracts for longer term business entail a poten-tial counterparty credit risk. To minimise the risk of entering into agreements with anyone who does not have the ability or willingness to honour their part of agreed terms, we perform a thorough credit assessment prior to concluding longer term contracts. This assessment includes i.a. the cli-ent’s credit rating and financial statements as well as recent trading history, payment performance and reputation. Larger contracts are approved by the Board of Directors. Please see note 4.5 in the accounts for further details.

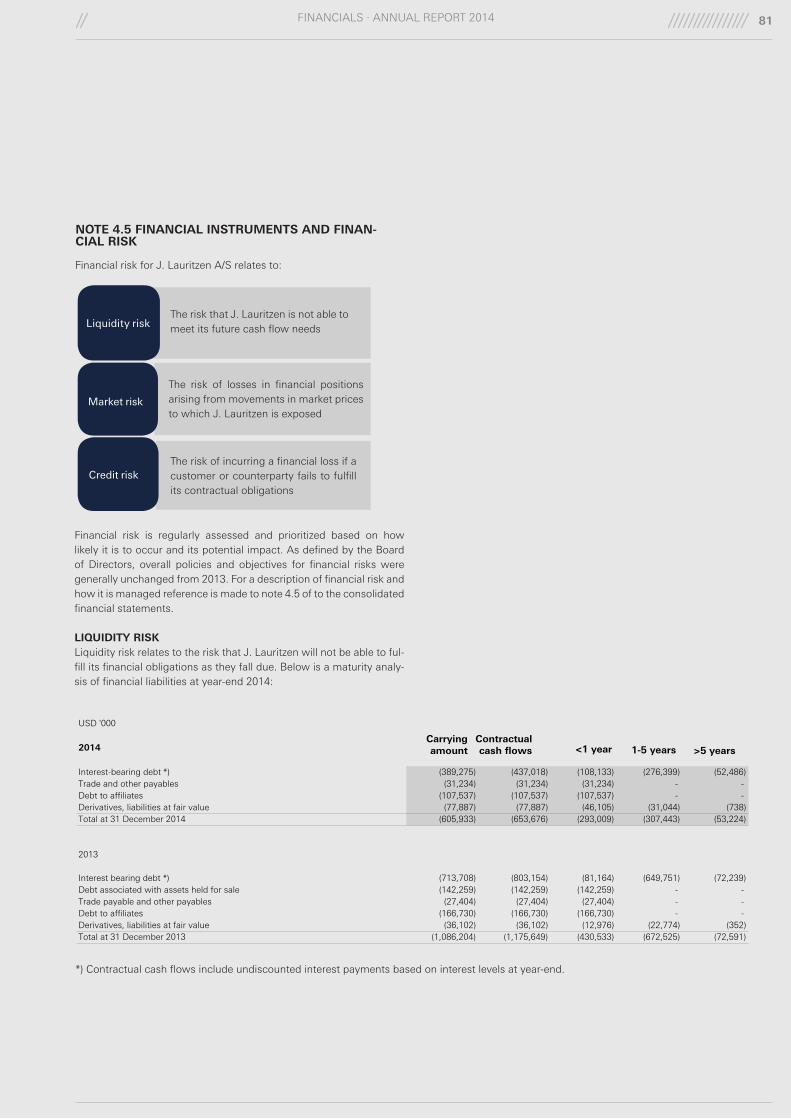

Liquidity riskManaging liquidity risk is essential in a volatile in-dustry like shipping. Liquidity is continuously monitored and assessed based on forecasts for the current year and projections for the subse-quent years. Sensitivity analyses and stress tests are performed regularly. Please see note 4.5 in the accounts for further details. Currency and interest riskCurrency and interest risk relate to currency ex-change rates and interest rates as well as to risk connected with the use of derivative financial in-struments.

Our policy is to use derivative financial instru-ments to hedge currency and interest rate risk. When using derivative financial instruments, our exposure relates to movements in the market val-ue of the derivatives which could cause margin calls affecting our liquidity. To reduce the risk of margin calls we have established credit lines with a number of financial counterparties based on second priority mortgages in our vessels.

For an overview of derivative financial instru-ments, risk related to changes in market values of derivatives, currency exchange rates and interest rates, please refer to notes 4.1 and 4.5 in the ac-counts.

Currency RiskOur operating and reporting currency is USD and thus all amounts are recorded and reported in

GOVERNANCE · ANNUAL REPORT 201428

Ebola outbreakIn March 2014, a serious outbreak of Ebola was seen in West Africa, which turned out to become the largest and most complex outbreak of Ebola in history. No seafarers are yet known to have been infected with Ebola during a call to one of the Ebola-affected countries.

Conducting port calls in West Africa, we have en-sured that all necessary information and precau-tionary instructions have been provided to vessels calling at ports in the affected areas. Recommen-dations from both the International Maritime Or-ganization (IMO) and the World Health Organiza-tion (WHO) advocate that the movement of ships, including the handling of cargo and goods, to and from affected areas, should continue as normal in order to reduce the isolation and economic hard-ship of the affected countries. We fully support these recommendations.

We recognise how vital it is for West Africa’s economy that ship operations are maintained in the area. Lauritzen Bulkers’ primary activities in the region mainly relate to discharge of food products, including grain and wheat.

USD. Currency exposure relates to operational and financial cash flows in other currencies than USD. The most important non-USD operating cost currency is DKK arising mainly from head of-fice costs. Currency risk related to debt in JPY is partially hedged and is fully hedged with regards to debt in NOK.

Interest RiskPart of our loan portfolio is subject to floating in-terest rates. At year-end 2014, all debt was hedged into fixed interest rates. The hedge ratio was 176% when measured by total debt less our cash in hand and deposits at year-end.

BUNKER OIL PRICE RISKBunker oil is a significant cost element but in prin-ciple only a risk in relation to contracted cargo vol-umes not covered by BAF (Bunker Adjustment Factor). Most of the operated fleet is either em-ployed in the spot market, re-let, on time-charter or employed under a Contract of Affreightment (COA) with BAF, and the bunker oil price risk is thus considered limited.

OPERATIONAL RISKOperational risk refers to potential losses resulting from non-compliance, human error and inade-quate systems, accidents, piracy, insufficient in-surance and IT systems. Operational risk is gener-ally managed via detailed operating procedures and ongoing training. The chapters about our business units have specific discussions on topics relating to their operations.

SafetyCasualties from ship operations can have serious consequences and the shipping industry has widely implemented international safety stand-ards. Several clients have additional requirements relating to safety, environmental protection, etc. At J. Lauritzen, we have safety standards in place, complying not only with general safety standards, but also above and beyond client demands.

Operation in high-risk areasRisk related to our crews and clients’ cargo due to piracy or violent crime-related activity in certain parts of the world has our strictest attention. We adhere to recommendations and best manage-ment practices (BMP4) from relevant national and international bodies. The necessity for engaging armed security teams on vessels operating in high-risk regions is assessed on the basis of voy-age-specific risk assessments. This is supported by industry anti-piracy measures aboard, close

monitoring by technical management and by mili-tary sources providing intelligence relevant to our vessels and military escorts. In 2014, Lauritzen Bulkers had 50 transits in high-risk areas whereas Lauritzen Kosan had 32. There were no incidents related to these transits.

InsuranceAn insurance policy is adopted with the aim of re-ducing the financial implications of incidents and casualties. The insurances cover our assets, our chartered and operated fleet, our liabilities and non-marine risk. As a general rule, insurances are always taken out with first class international in-surance companies and are always taken out with a certain financial safety margin to avoid any seri-ous consequential impact of an incident or casua-lty on our financial status.

IT systemsIT is critical, and it is imperative that our IT sys-tems are available round-the-clock and are ac-cessible worldwide. Redundant systems and du-plicate infrastructure are in place, and systems are tested to ensure that they can be restored within pre-defined time limits.

GOVERNANCE · ANNUAL REPORT 2014 29

Corporate ResponsibilityOur corporate responsibility efforts are based on our core values and aligned with internationally recognised principles, such as the voluntary UN Global Compact initiative and the UN Guiding Prin-ciples on Business and Human Rights.

Policy commitmentOur corporate responsibility policy includes com-mitments in relation to human rights, labour rights, protection of the environment, anti-corruption and responsible supply chain management. In 2014, we formalised an overarching policy that sum-marises our global commitments and existing poli-cies.

Focus areasIn 2014, our main corporate responsibility activities were focused on human rights assessment in rela-tion to our offices, the continued implementation of energy-efficiency projects, compliance sessions as part of the implementation of our anti-corrup-tion programme and dialogue with selected suppli-ers as part of the implementation of our supplier code of conduct. Our main achievements and results in 2014 can be summarised as follows:

• Assessment of our potential and actual human rights impacts in relation to our offices

• Continuous implementation of our Energy Efficiency Project enabling a cut in our CO2 emissions

• Founding member of Trident Alliance• Anti-corruption training of approximately

75% of our shore-based personnel in Copenhagen, Singapore, Shanghai and Manila