annual report - mauritian eagle insurance

TRANSCRIPT

AN

NU

AL

RE

PO

RT

Our VisionTo be the preferred insurance specialist that goes beyond boundaries to create value.

Our MissionWe passionately provide comprehensive, customised and state of the art insurance solutions through innovation and operational excellence.

Company DetailsHead offi ce1st Floor, IBL House, Caudan, Port Louis, Mauritius.Tel: (230) 203 2200 - Fax: (230) 203 2299Email: [email protected]: www.mauritianeagle.com

AuditorsDeloitte, Ebène, Mauritius

Consulting actuaries• Towers Watson SA (Proprietary) Limited, South Africa • QED Actuaries & Consultants (Pty) Limited, South Africa

Bankers• The Mauritius Commercial Bank Limited• The Hong Kong and Shanghai Banking Corporation• Barclays Bank Plc• State Bank of Mauritius• Afrasia Bank Limited

Registrar and transfer offi ceMCB Registry and Securities, Raymond Lamusse Building, 9-11 Sir William Newton Street, Port Louis, Mauritius.

Registered offi ceIBL House, Caudan, Port Louis, Mauritius.

SecretarySimon-Pierre Rey, B.A (Hons) Econ., A.C.A.

Directors’ Profi les

Directors of Subsidiaries

Managers’ Profi les

Managers of Subsidiaries

Notice of Annual Meeting

Chairman’s and Managing Director’s Report

Corporate Governance Report

Statement of Directors’ Responsibilities

Certifi cate from the Company Secretary

Premium and Profi tability Charts

Report of the Auditors to the Shareholders

Statements of Financial Position

Statements of Comprehensive Income

Statements of Changes in Equity

Statements of Cash Flows

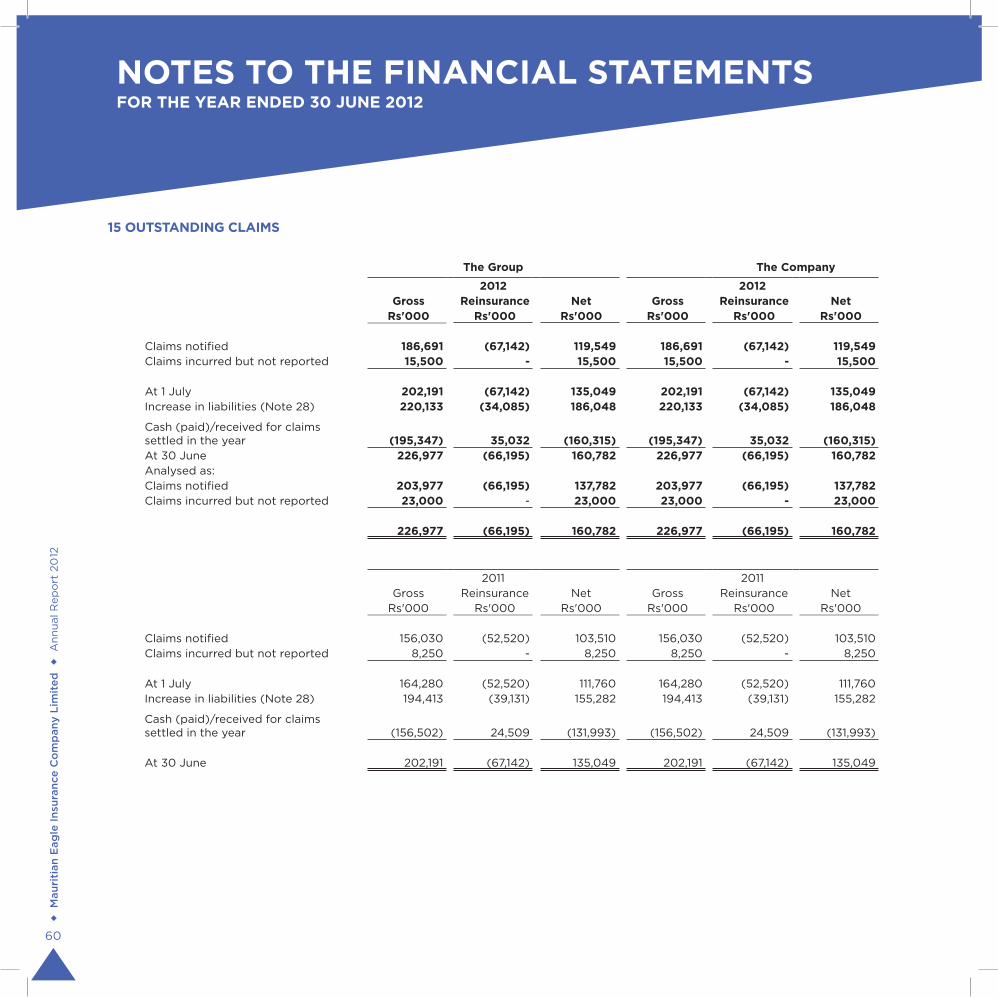

Notes to the Financial Statements

4

7

8

11

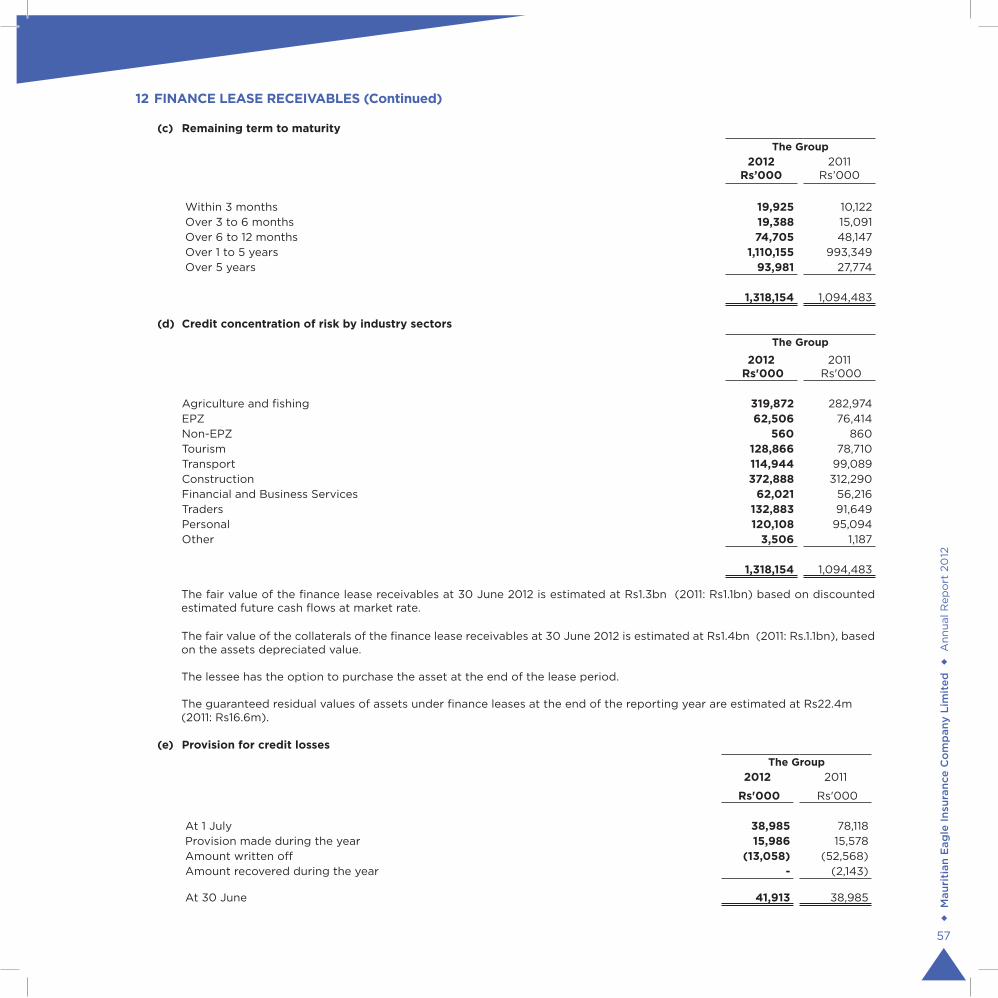

12

13

15

26

27

28

29

30

31

32

33

34

CONTENTS

Nicolas MAIGROTNon-Executive Chairman

Mr Maigrot was appointed Non-Executive Chairman of Mauritian Eagle Insurance on 18th January 2011. He holds a BSc in Management Sciences from the London School of Economics. Mr Maigrot is the Chief Executive and Director of Ireland Blyth Limited.

Gilbert ITHIER, LL. B. Hons, BarristerIndependent Non-Executive Director

Me Ithier was appointed as Independent Non-Executive Director on 15th November 2005. Me Ithier has been practicing as a barrister before all the courts of Mauritius since 1979, specialising mostly in civil, commercial, company, insurance and property matters.

André CHUNG SHUI, FCAManaging Director

Appointed Managing Director of Mauritian Eagle Insurance Company Limited on 1st of July 2011, Mr Chung Shui is a Fellow of the Institute of Chartered Accountants in England & Wales and is a Graduate of the London School of Economics. Before joining the Group, he was with the Happy World Group. He is a Director of the Stock Exchange of Mauritius Limited.

Robert IP MIN WAN, FCAIndependent Non-Executive Director

Mr Ip Min Wan was appointed as Independent Non-Executive Director on 13th June 2008. He was a Senior Audit Manager of Deloitte & Touche LLP in London before returning to Mauritius. He has a wide experience in the audit of the banking sector amongst others.

DIRECTORS’ PROFILES

Mau

riti

an E

agle

Insu

ranc

e C

om

pan

y Li

mit

ed

Ann

ual R

epo

rt 2

012

4

Subhash LALLAH, BarristerIndependent Non-Executive Director

Me Lallah was appointed as Independent Non-Executive Director on 29th March 2005. Former Chairman of the National Transport Corporation and Member of the Board of Governors of the Mauritius Broadcasting Corporation, he is the legal advisor of a number of companies and corporations.

Gaetan LAN HUN KUEN, FCANon-Executive Director

Mr Lan was appointed as Non-Executive Director on 1st January 2005 and before that he was the Chief Executive of Mauritian Eagle Insurance Company Limited. Mr Lan is the Chairman of the Stock Exchange of Mauritius Ltd, Director of Central Depository & Settlement Co Ltd and Ireland Blyth Limited. He has been with the IBL Group since 1977 and is currently the Chief Finance Offi cer of the Group.

John Edward O’NEILL, BCom (Hons), Chartered Accountant Non-Executive Director

Mr O’Neill has been appointed on 27th September 2012 and has over 16 years of extensive auditing experience within the fi nancial services sector with specialised knowledge in retail and stock broking, treasury, corporate and investment banking and securities trading. Mr O’Neill is currently the Chief Executive Offi cer of Zurich South Africa.

Alain MALLIATE, FCII, ACISExecutive Director

Mr Malliaté was appointed as Executive Director on 30th March 2004. He has been with the Company since August 1985 and is in charge of the Fire and Accident and Claims Departments of Mauritian Eagle Insurance.

Simon-Pierre REY, BA (Hons), ACANon-Executive Director

Mr Rey was appointed as Non-Executive Director on 3rd August 1989 and is also the Company Secretary since December 1996. He is currently the Chief Operating Offi cer in charge of Corporate Services of Ireland Blyth Limited.

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

5

DIRECTORS OF SUBSIDIARIES

Philip VENPIN, BSc Executive DirectorMauritian Eagle Life Company Limited

Joined Mauritian Eagle Insurance Company Limited in 1991 as Marketing manager, Mr Venpin who holds a bachelor degree in Actuarial science from the University of Toronto currently heads the Life and Pensions department. His areas of expertise are business and product development. Mr Venpin is a member of the Insurance Institute of Mauritius.

Yves MEYEPA Executive DirectorMauritian Eagle Leasing Company Limited

Mr Meyepa worked for more than 20 years in the IBL Group before joining Mauritian Eagle Leasing Company Limited at its incorporation as Executive Manager. He was appointed Executive Director in September 2005. His areas of responsibility include the management of day-to-day activities and liaison with regulatory authorities.

Natasha WONG CHUNG KI, FCCA, MBAExecutive DirectorMauritian Eagle Leasing Company Limited

Appointed Executive Director in September 2005, after having held offi ce in the audit department of Kemp Chatteris Deloitte and accounting department of DTOS Ltd, Mrs Wong Chung Ki’s areas of responsibility include the establishment of policies and procedures and monitoring of the fi nancial aff airs of the company.

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

7

Pierre AH SOON, ACCAFinance Manager

Joined in 2004, Pierre’s area of expertise is audit in which he has more than 5 years experience in an off shore company. He is actually responsible for the activities of the Finance department and is the Money Laundering Reporting Offi cer of the Company.

Bruno CHAN SIP SIONG, BSc (Hons)Manager, IT Department

Joined in 1995, Bruno has been working in the IT fi eld for more than 15 years including 10 in the insurance industry. Bruno is responsible for the day-to-day operations of IT Services department and end-user support. His other areas of responsibility also include the maintenance of insurance application systems.

José ARSENIUS, CISA, CISM Senior Manager, IT Department

Joined in 1994, with more than 20 years experience in the IT sector, José is the head of the IT Services department. He is responsible for all corporate management & information systems such as Information Security, Quality, Business Continuity and IT Service. He is both a Chartered IT and a Certifi ed Information Security Professional.

Vikash MUNGLA, BA (Hons)Reinsurance Manager

Joined in 2003 after more than 5 years with a world leading reinsurer, Vikash leads the Reinsurance department, including the underwriting of Global insurance policies. His main area of expertise is Reinsurance Analytics with specialization in dynamic fi nancial analysis and treaty structuring.

Winson CHAN CHIN WAH, ACII, Chartered Insurer Manager, Marine Department

Joined in 2004, with a vast experience in the general insurance industry, Winson leads the Marine department. He is a Chartered Insurer and a member of the Insurance Institute of Mauritius.

MANAGERS’ PROFILES

Mau

riti

an E

agle

Insu

ranc

e C

om

pan

y Li

mit

ed

Ann

ual R

epo

rt 2

012

8

Stéphanie PALLAMY, ACII, Chartered InsurerManager, Motor Department

Joined in 2005, Stéphanie has been working in the insurance industry for more than 10 years and is currently responsible for the operations of the Motor department. She is a Chartered Insurer and a council member of the Insurance Institute of Mauritius.

Jean Mario TYPHIS, ACII Senior Manager, Fire and Accident Department

Joined in 1987 as Reinsurance manager after more than 13 years in the reinsurance industry. His responsibilities subsequently moved to the underwriting and development of the Fire and Accident department which embraces fi re, accident, liability and engineering classes of insurance. Mario is a Chartered Insurer and is a member of the Insurance Institute of Mauritius.

Joëlle GRENOUILLE, BSc Human Resources Manager

Joined in 2011, Joëlle is responsible of the HR requirements of the Financial Services sector. Her responsibilities include recruitment, coaching, training, career development and counselling. Joëlle is the co-ordinator of the CSR Program of the Financial Services sector.

Gilbert PETITE Senior Manager, Claims Department

Joined in 1999, with more than 35 years experience in the insurance industry, Gilbert is conversant with both English and French insurance procedures. He actually manages the day-to-day operations of Claims department which processes motor, fi re and engineering claims. He is a member of the Insurance Institute of Mauritius.

Jean Claude TSANG YAN SANG, MCIM, MBA Senior Manager, Sales and Marketing Department

Joined in 2004, Jean Claude has worked in the insurance industry for the past 15 years. His area of expertise includes marketing analysis and planning. He is currently responsible for the Sales and Marketing department. Jean Claude is a member of the Chartered Institute of Marketing and of the Insurance Institute of Mauritius.

Allen LEUNG YOON SIUNG, Cert CII Manager, Fire and Accident Department

Joined in April 2012 with more than 20 years of experience in the insurance industry, Allen is responsible for the underwriting of fi re, accident, liability and engineering classes of insurance. He is a member of the Insurance Institute of Mauritius.

Mau

riti

an E

agle

Insu

ranc

e C

om

pan

y Li

mit

ed

Ann

ual R

epo

rt 2

012

9

MANAGERS OF SUBSIDIARIES

Guyto DEVALET, ACII Technical ManagerMauritian Eagle Life Company Limited

Joined the company in 2006 and has cumulated up to now more than 23 years experience in the fi eld of Life Insurance in diff erent positions. Guyto’s present area of responsibility in the Life & Pension Department includes technical aspects such as underwriting, group life, reinsurance and calculations.

Soobiraj KHAITOO, ACCA, MBA Operations ManagerMauritian Eagle Leasing Company Limited

Appointed Operations Manager in January 2009, after having held the post of accountant in diff erent departments within IBL since year 2000. Soobiraj’s responsibility include administration of the leasing department, client relationships and business development.

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

11

Notice is hereby given that the thirty-seventh Annual Meeting of the Shareholders of the Company will be held at the offi ces of the Company, 1st Floor, IBL House, Caudan, Port Louis on Friday 7th December 2012 at 14.00 hours to transact the following business :

Ordinary Resolutions • To adopt the minutes of proceedings of the annual meeting held on 1st December 2011.

• To receive and adopt the Group’s and Company’s fi nancial statements for the year ended 30 June 2012 and the Directors’ and Auditors’ reports thereon.

• To re-appoint Messrs Deloitte as Auditors for the ensuing year and to authorise the Board of Directors to fi x their remuneration.

• To appoint Mr John Edward O’Neill as Director.

• To re-elect as Directors to hold offi ce until the next Annual Meeting by way of separate resolutions the following persons:

- Mr André Chung Shui - Mr Robert Ip Min Wan - Me Gilbert Ithier - Me Subhash Lallah - Mr Gaetan Lan Hun Kuen - Mr Nicolas Maigrot - Mr Alain Malliaté - Mr Simon-Pierre Rey

By Order of the BoardSimon-Pierre ReySecretaryPort Louis, Mauritius

21 November 2012

A member entitled to attend and vote at the meeting may appoint any person, whether a member or not, to attend and vote in his stead. Proxy forms

must be lodged at the registered offi ce of the company not less than twenty-four hours before the meeting. A proxy form is included in the Annual Report

and is also available at the Registered Offi ce of the Company.

NOTICE OF ANNUAL MEETING

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

12

Overall resultsThe Group posted a turnover of Rs1,420.1m (LY: Rs1,256.0m), representing an increase of 13.1% over the corresponding period. Profi t before tax (PBT) increased signifi cantly to reach Rs98.2m (LY: Rs45.9m), last year’s fi gure included major provisions for impairment of trade receivables at the Leasing subsidiary.

Earnings per share stood at Rs10.40 (LY: Rs7.16) and Net Asset per share was Rs67.81 (LY: Rs63.62).

Short term insuranceThe Company generated improved turnover and profi tability. Gross insurance premiums increased by 12.7% to reach a total of Rs739.3m. All departments posted growth, with the Engineering department recording the largest increase at 96.6%. Net claims incurred were relatively stable at 54.3% (LY: 54.7%). Reinsurance costs went down to 46.8% of Gross premiums (LY: 47.9%). There were no major increases in the reinsurance rates during the year despite the major catastrophes which occurred during 2011. Underwriting profi ts as a percentage of net earned premiums improved to 17.1% (LY: 16.6%).

PBT amounted to Rs92.9m (LY: Rs75.9m), an increase of 22.5%.

Long term insuranceThe life fund stood at Rs 597.5m (LY: Rs 515.6m) on 30th June 2012.

Gross premiums went down to Rs 184.8m (LY: Rs208.8m), a decrease of 11.5%. However, last year’s turnover was exceptionally boosted by Rs91.7m, with some of the clients renewing their interest in the same product and other unit-linked products. No profi t was recognised by the life operations as recommended by the actuaries (LY: PBT of Rs11.2m).

Associate in SeychellesH Savy Insurance, an entity where we hold 20% of the issued share capital, performed reasonably during the year. We have consolidated Rs 5.9m (LY: Rs6.4m) within the year’s results. We received dividends amounting to Rs1.1m (LY: Rs2.8m) during the year.

LeasingThe department was in a marginal profi t position with a PBT of Rs0.4m (LY: loss of Rs44.8m) for the year. The leasing portfolio stood at Rs 1.56bn (LY: Rs 1.30bn) at the end of the year.

DividendsAn interim dividend of Rs1.10 (LY: Rs1.00) was paid during the year. The directors recommend that a fi nal dividend of Rs 1.30 (LY: 1.10) be paid to the shareholders.

Activities under CSRThe Group has been very active with many projects, a summary of these projects is included in the Corporate Governance Report on page 15.

DirectorsMessrs Gavin Munnoch and Dylan Garnett resigned from the Board with eff ect from 20th May and 31st May 2012 respectively. We thank them for their contributions to the deliberations of the Board.

ProspectsCompetition remains fi erce in the short term insurance sector. As competitors continue to fi ght for market share, premium rates remain under pressure and in some cases are being pushed below economic levels. This is not a healthy situation for the sector.

We will endeavour to maximise the use of our reinsurance treaties for the various risks that we are underwriting. Underwriting profi ts will continue to be our priority as we move forward.

AppreciationOur appreciation goes to the management and staff of the company for their contributions and commitment. Mr Mike Henry, Manager in the Fire & Accident department, retired during the year on grounds of ill-health, we thank him for his important contribution over the years. The management team witnessed the arrival of Mr Allen Leung in the Fire & Accident department. Lastly, we are grateful to our fellow directors for their involvement on the Board and the various committees.

CHAIRMAN’S AND MANAGING DIRECTOR’S REPORT

Nicolas Maigrot Chairman

Andre Chung ShuiManaging Director

Mau

riti

an E

agle

Insu

ranc

e C

om

pan

y Li

mit

ed

Ann

ual R

epo

rt 2

012

13

CORPORATE INFORMATION AND HISTORY

Mauritian Eagle Insurance Company Limited (“MEI”) was incorporated in 1973 and admitted on the Offi cial List of the Stock Exchange of Mauritius in 1993. MEI operates in both the domestic and commercial markets and is engaged in short-term insurance business. As from 1 January 2011, the activities of the long-term business of MEI were transferred to Mauritian Eagle Life Company Limited (“MEL”), a wholly-owned subsidiary of the Company. Mauritian Eagle Leasing Company Limited (“MELCO”), another subsidiary of MEI, provides deposit taking services and leasing facilities, both fi nance and operating leases.

Major Milestones2012 MEI awarded ISO 20000 IT Service Management Certifi cation

2010 Establishment of MEL as a separate entity

2007 MEI awarded ISO 27001:2005 Certifi cation

2005 MEI increased its stake to 20% in H.Savy Insurance Company Limited

2004 MEI obtained QM 9004 Certifi cation MEI participated in NQA Level 2 MEI celebrated its 30 years (1974-2004)

2003 MEI received Quality Commitment Award MEI obtained ISO 9001:2000 Certifi cation Second Branch Offi ce in Rodrigues

2002 Launching of Mauritian Eagle’s corporate website First Branch Offi ce in Centre de Flacq

2001 Establishment of MELCO

1998 Moving into new premises at Caudan

1996 MEI acquired a 15% stake in H.Savy Insurance Company Limited

1994 MEI celebrated its 20 years

1993 MEI listed on the Stock Exchange of Mauritius 1991 Launching of Life Assurance Policies & Pension Plans

1974 ME Insurance starts operation

CORPORATEGOVERNANCEREPORT

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

15

CORPORATE GOVERNANCE STATEMENTS

The Board, management and staff of the Group fully support and are committed to best practices of business integrity, transparency and professionalism.

We strive to ensure that all the activities of the Group are conducted in such a way as to satisfy the characteristics of good Corporate Governance, namely, • Discipline – behaviour that is universally recognised and accepted as correct and proper;• Transparency – ease with which an outsider is able to make meaningful analysis of the Company’s actions, its economic fundamentals

and the non-financial aspects pertinent to the business;• Independence – the extent to which mechanisms have been put in place to avoid or manage conflicts; • Accountability – the existence of effective mechanisms to ensure accountability; • Responsibility – the implementation of processes that allow for corrective actions and acting responsibly towards all stakeholders;• Fairness – the existence of systems within the Company that allow balancing of competing interests; and • Social responsibility – being aware of and responding to social issues and to place a high priority on ethical standards.

The Group is committed to high standards of corporate governance with the Board being accountable to the shareholders for good governance. The Board of Directors recognises that the Report on Corporate Governance (the Code) is regarded as best practice and therefore uses its best endeavours to ensure compliance with the provisions set out in the Code.

The Group has established a corporate governance system involving the Board of Directors, Board Committees, Management, Internal and External Auditors, Industry Best Practices as well as established policies and procedures across all operations. This ensures that the business and affairs of the Group are managed according to the highest standards of corporate governance and in the best interest of all its stakeholders.

GROUP STRUCTURE

GML Investissement Limitée(48.29%)

Zurich Insurance Company South Africa Limited

(15%)

Mauritian Eagle Life Company Limited

(100%)

Mauritian Eagle Insurance Company Limited

Public(27.23%)

Ireland Blyth Limited(60%)

H. Savy Insurance Company Limited –Seychelles

(20%)

Other Shareholders(24.48%)

Other Shareholders(25%)

Mauritian Eagle Leasing Company Limited

(51%)

CORPORATE GOVERNANCE REPORT

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

16

BOARD OF DIRECTORS

The Board bears the responsibility of organizing and directing the affairs of the Group in a manner that is in the best interest of shareholders and other stakeholders. It is primarily responsible for, amongst other things, the review and adoption of strategic plans, the overview of business performance, adoption of appropriate risk management systems and the establishment of proper internal control systems.

It is also responsible for continually reviewing the activities, practices and trends of the Group so that these are in conformity with legal and regulatory requirements. The Board retains full and effective control over MEI and its subsidiaries, delegating the day-to-day running and operational issues to the Managing Director and his management team.

CompositionThe Board, under the recommendation of the Nomination Committee, is responsible for the appointment of directors who are selected on the basis of their integrity, skill, acumen and experience to make sound judgements relevant to the business of the Company. The Board includes two executive directors, three independent non-executive directors and five non-executive directors. The Company complies with Section 30 (2) of the Insurance Acts 2005 which states that an insurance company’s Board of directors should be composed of no less than 7 natural persons of which 30% should be independent non-executive directors. The independent non-executive directors bring a wealth of experience and expertise to the Board and are free from any business or other relationships which would affect their eligibility to exercise independent judgement.

The Code of Corporate Governance provides for directors to be elected or re-elected every year at the annual meeting of shareholders.

The composition of the Board for the year under review was as follows:Nicolas MAIGROT Non-Executive Chairperson André CHUNG SHUI Managing Director Appointed on 1st July 2011Alain MALLIATE Executive DirectorRobert IP MIN WAN Independent Non- Executive DirectorGilbert ITHIER Independent Non-Executive DirectorSubhash LALLAH Independent Non-Executive DirectorGaetan LAN HUN KUEN Non-Executive DirectorGavin MUNNOCH Non-Executive Director Resigned on 20th May 2012Simon-Pierre REY Non-Executive DirectorDylan GARNETT Non-Executive Director Resigned on 31st May 2012John Edward O’NEILL Non-Executive Director Appointed on 27th September 2012

Changes in directorship

• Mr André CHUNG SHUI was appointed on 1st July 2011• Mr Gavin MUNNOCH resigned on 20th May 2012• Mr Dylan GARNETT resigned on 31st May 2012• Mr John Edward O’NEILL has been appointed on 27th September 2012

New directors have been informed of their duties and responsibilities by way of an induction.

Independent Non-Executive

33%

Executive22%

Non-Executive45%

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

17

BOARD OF DIRECTORS (continued)

Directors’ attendance at Board Meetings

Mauritian Eagle Life Company Limited The directors of MEL are as follows:Gaetan LAN HUN KUEN Non-Executive Chairman Philip VENPIN Executive Director Robert IP MIN WAN Independent Non- Executive Director Gilbert ITHIER Independent Non-Executive Director Subhash LALLAH Independent Non-Executive Director Gavin MUNNOCH Non-Executive Director Resigned on 20th May 2012André CHUNG SHUI Non-Executive Director Appointed on 1st July 2011

Board attendance of Mauritian Eagle Life Company Limited

Directors Board Meetings27 Sep 2011 7 Nov 2011 13 Feb 2012 7 May 2012

Nicolas Maigrot

André Chung Shui (Appointed on 1st July 2011)

Alain Malliaté apologies

Robert Ip Min Wan

Gilbert Ithier

Subhash Lallah

Gaetan Lan Hun Kuen

Gavin Munnoch (Resigned on 20th May 2012) apologies apologies apologies

Simon-Pierre Rey

Dylan Garnett (Resigned on 31st May 2012) apologies apologies

Directors Board Meetings27 Sep 2011 27 Mar 2012

Gaetan Lan Hun Kuen

Philip Venpin

Robert Ip Min Wan

Gilbert Ithier

Subhash Lallah

Gavin Munnoch (Resigned on 20th May 2012)

André Chung Shui (Appointed on 1st July 2011)

CORPORATE GOVERNANCE REPORT

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

18

Directors Board Meetings27 Sep 2011 7 Nov 2011 13 Feb 2012 7 May 2012

Nicolas Maigrot

Yves Méyépa

Natasha Wong Chung Ki

Antoine Domingue apologies

Robert Ip Min Wan

Gilbert Ithier

Subhash Lallah

Gaetan Lan Hun Kuen

Simon-Pierre Rey apologies

André Chung Shui (Appointed on 1st July 2011)

Mauritian Eagle Leasing Company Limited The directors of MELCO are:Nicolas MAIGROT Non-Executive Chairperson Yves MEYEPA Executive DirectorNatasha WONG CHUNG KI Executive DirectorAntoine DOMINGUE Independent DirectorRobert IP MIN WAN Independent DirectorGilbert ITHIER Independent DirectorSubhash LALLAH Independent DirectorGaëtan LAN HUN KUEN Non Executive DirectorSimon-Pierre REY Non Executive DirectorAndré CHUNG SHUI Non-Executive Director Appointed on 1st July 2011

Attendance at Board Meetings of Mauritian Eagle Leasing Company Limited

COMMITTEES OF THE BOARD OF DIRECTORS The Board fulfills its proper governance responsibilities through various Committees. Each Board Committee has formal written terms of reference in line with the Mauritian Code of Corporate Governance and international best practices that are reviewed on an annual basis. The directors confirm that the committees have functioned in accordance with these terms of reference during the year under review.

Two Committees deal with audit, risk, corporate governance and nomination issues.

Audit and Risk CommitteeThe Audit and Risk Committee is appointed by the Board of MEI and is chaired by an independent non-executive director, and comprises of at least two members who are non-executive directors. For the year under review, the Committee consisted of three directors, namely, Messrs.

Robert IP MIN WAN Independent Non-Executive DirectorGaetan LAN HUN KUEN Non-Executive Director and Simon Pierre REY Non-Executive Director

Its principal function is to oversee the financial reporting process. The activities of the Audit Committee includes regular reviews and monitoring of the effectiveness of MEI’s financial reporting and internal control policies and risk management systems, the effectiveness of the internal audit function, the independence of the external audit process and assessment of the external auditor’s performance, the remuneration of external auditors and to ensure compliance with laws and regulations relevant to financial reporting and with our internal code of business conduct. The Committee meets as frequently as it deems necessary prior to the Board’s review of the annual financial statements and profit announcements.

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

19

COMMITTEES OF THE BOARD OF DIRECTORS (continued)

Attendance to the Audit and Risk Committee for year under review was as follows:

Committee members Committee Meetings29 July 2011 22 Sep 2011 3 Nov 2011 2 Feb 2012 2 May 2012

Robert Ip Min Wan

Gaetan Lan Hun Kuen apologies

Simon-Pierre Rey apologies apologies

The presence of internal and external auditors and management team was requested whenever necessary. The internal audit function is entrusted to Ernst & Young who have been given unrestricted access to the records, management and employees of the group. The Board confirms that there have been no significant issues that have affected the proper functioning of the internal control systems during the year under review which could have impacted on the financial statements.

Risk Management

The Audit and Risk Committee is also responsible for reviewing the effectiveness of the risk strategy of MEI, for establishing and maintaining a strong risk control environment and for the monitoring of the risk management process. It ensures that appropriate structures, procedures and systems are in place to mitigate all risks. Risk assessment activities were carried out during the year under review and the risks discussed and identified. A Risk management process was implemented to minimize the impact of identified risks which have been categorised as follows:

• Insurance Risk MEI’s insurance activities are primarily concerned with the pricing, acceptance and management of risks from customers and also

include reinsurance risks. The claims department closely monitors claims developments whilst treaty purchases are analysed to ensure that the level of cover is aligned with the company’s strategy and objectives.

• Operational Risk Operational risks can have significant negative impact on the company’s financial position. These are fraud risks, reputational risks,

material damage, business continuity risks and disaster recovery, change management and human resources risks. In line with the requirement of the ISO standard which requires the identification of an operational area which is accessible to all stakeholders in case the company needs to rapidly operate after a disaster, a Business Continuity Management System has been implemented and tested during the year under review.

• Regulatory and Environment Risk These include regulatory risks and industry risks which can result in increased pressures and significantly affect the company’s ability

to conduct business.

• IT Risk These are the risks that hardware and software used are exposing the company to losses. MEI is certified ISO 27001-2005 Security

Management System Certification since February 2007.

CORPORATE GOVERNANCE REPORT

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

20

Corporate Governance CommitteeThe Corporate Governance Committee is appointed by the Board and the majority of which is composed of non-executive directors. The current committee consists of five members with the Chairman being an independent non-executive director and four other members, two of whom are non-executive directors.

The current Committee is composed of Messrs. Subhash LALLAH Independent Non-Executive DirectorGaetan LAN HUN KUEN Non-Executive DirectorSimon-Pierre REY Non-Executive DirectorAndre CHUNG SHUI Managing Director andAlain MALLIATE Executive Director

Attendance of Corporate Governance Committee for year under review was as follows:

The main functions of the Corporate Governance Committee is to provide guidance to the Board on aspects of corporate governance and for recommending the adoption of policies and best practices as appropriate for the Group. The Committee meets at least twice a year and on an ad-hoc basis.

Remuneration PhilosophyThe Board has entrusted the Corporate Governance Committee the responsibility for the nomination and remuneration of Directors by taking into consideration the market conditions, benchmarking in the industry and the Group’s results.

The Group strongly believes that the achievements and merits of high performing employees should be recognized and rewarded. The Human Resources department is delegated the responsibility of determining managers’ and employees’ remunerations and benefits. This is reviewed annually after taking into consideration market conditions and practices as well as the performances and responsibilities of the employees.

Internal ControlThe directors have the overall responsibility for maintaining a sound and effective system of internal controls. The system of internal controls has been designed to provide the Directors with reasonable assurance that assets of the Group are safeguarded, that transactions are authorised and properly recorded, that material misstatements or losses are either prevented or detected within a reasonable time and that the risks of failures in operational systems are being managed.

Dividend PolicyDividends are declared and paid half yearly. Subject to internal cash flow requirements and the need for future capital investments, it is MEI’s policy to declare dividends out of profits available for distribution in accordance with the Companies Act 2001 and International Financial Reporting Standards; the balance being transferred to reserves. For the year under review, a dividend of Rs 17,599,994 was paid (2011: Rs 15,999,996).

SHAREHOLDERS’ CALENDAR

Release of first quarter results November 2012 Payment of final dividend December 2012 Annual meeting of shareholders December 2012 Release of second quarter results and declaration of interim dividend February 2013 Payment of interim dividend April 2013 Release of third quarter results May 2013 Release of financial year end results and declaration of final dividend September 2013

Committee members Committee Meetings22 Sep 2011 2 Feb 2012

Subhash Lallah

Gaetan Lan Hun Kuen apologies

Simon-Pierre Rey apologies

Andre Chung Shui

Alain Malliaté

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

21

OTHER STATUTORY DISCLOSURES

Directorship of other listed companiesIncluded in Directors’ profile

Common DirectorsThe common directors of MEI and its subsidiaries are as follows:

The directors’ remuneration is disclosed by category in view of the confidentiality and sensitivity of the information.

The directors’ remuneration has also been disclosed under note 38 for related party transactions.

Directors’ remuneration and benefitsEmoluments paid by MEI and related corporations to directors of MEI is set out in the table below:

Directors Mauritian Eagle Insurance

Company Limited

Mauritian Eagle Leasing Company

Limited

Mauritian Eagle Life Company

LimitedAndré Chung Shui (Appointed on 1st July 2011) Director Director Director

Antoine Domingue - Director -

Dylan Garnett (Resigned on 31st May 2012) Director - -

Robert Ip Min Wan Director Director Director

Gilbert Ithier Director Director Director

Subhash Lallah Director Director Director

Gaetan Lan Hun Kuen Director Director Chairman

Alain Malliaté Director - -

Nicolas Maigrot Chairman Chairman -

Yves Méyépa - Director -

Gavin Munnoch (Resigned on 20th May 2012) Director - Director

Simon-Pierre Rey Director Director -

Philip Venpin - - Director

Natasha Wong Chung Ki - Director -

The Group The Company Related Corporations

2012Rs’000

2011Rs’000

2012Rs’000

2011Rs’000

2012Rs’000

2011Rs’000

Full-Time 16,480 17,159 8,828 11,090 - -

Part-Time 1,653 905 483 395 41,381 43,882

18,133 18,064 9,311 11,485 41,381 43,882

CORPORATE GOVERNANCE REPORT

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

22

Directors’ Service ContractsThere are no service contracts between MEI and its directors.

Directors’ Share InterestsNone of the directors have a direct or indirect share in the equity of MEI or its subsidiaries.

Share DealingsMembers of the Board have been informed that they should not deal in MEI’s shares during the 30 calendar days preceding publication of results, and prior to the declaration of dividends, or any major event affecting the company that might influence its share price. Members have also been advised to declare to MEI all transactions conducted by them outside the periods mentioned.

Significant ContractsNo contracts of significance existed during the year under review between MEI or one of its subsidiaries and any director or controlling shareholder of MEI, either directly or indirectly.

Substantial ShareholdingThe directors have been advised that the following persons or entities (excluding directors) held 5% or more of the nominal value of the share capital of MEI.

N.B. The above number of shareholders is indicative, due to consolidation of multi portfolios for reporting purposes. The total number of active shareholders as at 30 June 2012 was 614.

ConstitutionThe constitution of MEI does not provide any ownership restriction or pre-emption rights. It is in conformity with the Companies Act 2001 and the Mauritius Stock Exchange Listing Rules.

Auditor’s fees

Messrs. Deloitte, who has accepted to continue in office, will be proposed for re-appointment at the Annual Meeting.

Shareholding ProfileOwnership of ordinary share capital by size of shareholding as at 30 June 2012 was as follows:

Shareholders holding more than 5% of the shares Number of ordinary shares %Ireland Blyth Limited 4,800,000 60.00%

Zurich Insurance Company South Africa Limited 1,200,000 15.00%

Size of Shareholding Number of shareholders Number of Shares Owned % Holding1 - 100 shares 169 7,339 0.09%

101 - 200 shares 54 9,220 0.12%

201 - 300 shares 46 13,643 0.17%

301 - 500 shares 34 14,367 0.18%

501 - 1000 shares 89 64,372 0.80%

Above 1000 shares 184 7,891,057 98.64%

576 7,999,998 100.00%

The Group The Company

Fees paid to Deloitte for:2012

Rs’0002011

Rs’0002012

Rs’0002011

Rs’000

Audit fees 488 404 230 222

Tax services 10 15 - -

Advisory services - 760 - 471

498 1,179 230 693

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

23

OTHER STATUTORY DISCLOSURES (continued)

Share price information and performance

Year ended 30-Jun-12

Year ended 30-Jun-11

6 months ended 30-Jun-10

Year ended 31-Dec-09

Year ended 31-Dec-08

Market Price (Rs) 70.00 80.00 62.00 65.00 45.50

Earnings Per Share (Rs) 10.40 7.34 3.33 4.30 6.99

Dividend per share (Rs) 2.40 2.10 1.00 1.83 1.83

Price Earnings ratio (times) 6.73 10.90 18.62 15.12 24.86

Net Assets value per share (Rs) 67.81 63.62 55.17 51.22 42.55

Dividend yield (%) 3.43 2.63 3.23 2.82 4.02

Relationship with shareholdersThe Board is committed to properly understand the information needs of all shareholders and other stakeholders of MEI. It ensures that lines of communication are kept open to communicate all matters affecting MEI to its shareholders.

Anti-Money LaunderingIn line with the requirements of the Financial Intelligence and Anti-Money Laundering Act 2002 and the Regulations 2003, control procedures and internal policies are regularly reviewed and staff training is done at least twice yearly.

Safety, Health and Environmental PracticesHealth and safety policies adopted have ensured satisfactory compliance with the appropriate legislation and ruling standards. No injuries at work were recorded. The Group adheres to the IBL Group’s health and safety and environmental policies.

Code of EthicsThe Group is committed to the highest standards of integrity and ethical conduct with all its stakeholders.

Social ResponsibilityThe Group has kept working towards the advancement and welfare of its employees and the socio-economic development of the island. In line with the Group’s corporate social responsibility policy to help underprivileged children, numerous activities have been organised and staff have been encouraged to participate; these include amongst others:

• Sweat shirts were offered to needy children of Vuillemin Voluntary Association at Cite Sainte Catherine, Saint Pierre;• In addition to providing musical instruments for children aged 6-17 years, school materials were also provided to Groupe Zenfants

Innocents at Quatre Bornes;• Tables and chairs were provided to Fraternité Nord-Sud, an organisation promoting the education of children who have not completed

the Certificate of Primary Education exams;• Books and furniture were offered to Association des Amis de Don Bosco for the setting up of an educational room for children aged

5 to 15;• A Christmas tree and gifts were offered to needy children of The Thalassemia Society; and• At the request of Commission Solidarite et Justice, an offspring of Caritas Ile Maurice, a Christmas carol for 140 children and an

educational outing for 60 children were organised. A summer camp was also set up at Senlis-Sur-Mer, Riambel for youngsters aged 14 to 15.

CORPORATE GOVERNANCE REPORT

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

24

Promoting human resource developmentThe Group endeavours to maintain a high standard of professionalism with continuous training. The employees regularly attend training and refresher courses and are also encouraged to pursue further studies by taking advantage of the employee study scheme which provides funding to employees wishing to obtain professional qualifications in insurance and accounting.

The year under review saw an increased demand from employees of the Group for sponsorship of their studies as part of the training scheme. This demonstrates an increased awareness about the need of obtaining a professional qualification in a fast growing sector.

Carbon Reduction ReportingAs part of its ongoing programme to help protect the environment and within the context of the GML “Think Green” initiative, the IBL Group has set up a committee composed of representatives of different clusters, to promote the values of both IBL Environment and GML Think Green Charters. The Charter aims to:

• promote an environment culture by recognising environmental achievement as one of the main core values;• create a sense of awareness among employees to be more proactive rather than reactive in all activities with regards to the

environment;• endeavour to comply with relevant environmental regulations and standards;• adopt good practices by optimising all non-renewable resources and encouraging best waste management;• evaluate the objectives fixed for energy saving and resources management and a continuous assessment of good practices adopted; and• act responsibly towards the environment by committing to sustainable development of the Group for the benefit of the society,

shareholders and other stakeholders.

The direct impact on climate change will be reduced with the Group’s commitment to manage carbon reduction by focusing on the areas such as:

• controlling air conditioning;• switching off of lights in areas where not required after office hours;• installing passive infra-red lighting in certain common areas;• monitoring the purchase of low energy consumption equipments;• intensive use of emails to reduce the use of papers;• turning off the computers when going out for lunch; and• paperless office and recto/verso document printing if required.

Donations

The Group The Company

2012Rs’000

2011Rs’000

2012Rs’000

2011Rs’000

Charitable donations 145 38 7 38

Corporate social responsibility contribution 1,212 1,031 855 901

1,357 1,069 862 939

The Group did not make any contribution to political parties during the year under review.

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

25

STATEMENT OF DIRECTORS’ RESPONSIBILITIES

The directors acknowledge their responsibilities to prepare the fi nancial statements that fairly present the state of aff airs of the Group and the Company as at the end of the fi nancial year and the results of its operations and cashfl ows for that period in accordance with International Financial Reporting Standards and in compliance with the requirements of the Mauritius Companies Act 2001 and the Financial Reporting Act 2004. In preparing each of the Group and Company fi nancial statements the Directors have: • selected appropriate accounting policies supported by reasonable and prudent judgements and estimates and then applied them

consistently; • adhere to applicable accounting standards or, if there has been any departure in the interest of fair presentaton, this must not only

be disclosed and explained but quantifi ed; and

• prepared the fi nancial statements on a going concern basis.

The Directors are responsible for:

• the maintenance of adequate accounting records which disclose with reasonable accuracy at any time the fi nancial position of the Company.

• the set up of an eff ective system of internal controls and risk management; and • safeguarding the assets of the Company and hence for taking reasonable steps for the prevention and detection of fraud and other

irregularities. The external auditors are responsible for reporting on whether the fi nancial statements are fairly presented.

Signed on behalf of the Board of Directors

DIRECTOR DIRECTOR

26 September 2012

DIRECTOR

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

26

CERTIFICATE FROM THE COMPANY SECRETARY

In terms of Section 166(d) of the Companies Act 2001, I certify that to the best of my knowledge and belief, the Company has fi led with the Registrar of Companies all such returns as are required of the Company under the Companies Act.

Simon-Pierre ReyCompany Secretary

26 September 2012

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

27

PREMIUM AND PROFITABILITY CHARTS

General Business- Breakdown by category

Transportation 14%

Engineering 5%

Fire & Allied 29%

Motor 27%

Group Turnover

2008

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

Rs.000

Rs.000

2009 2010(6 months)

2011 2012

Profitability before and after Tax

Before Tax After Tax

Management Expense ratio

2008

10,000

20,000

30,000

40,000

50,000

Per

cent

age

of

Turn

over

60,000

70,000

80,000

90,000

2009 2010(6 months)

2011 20122008 2009 2010

(6 months)

11%

12%

14%

78,3

24

1,420

,09

4

1,256

,015

1,06

0,8

94

541,8

34

1,122

,00

6

92,

925

75,8

51

32,6

8740

,772

56,8

06 66

,58

7

27,9

94

30,3

12

49

,833

15%

11%

2011 2012

Accident 25%

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

28

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

29

INDEPENDENT AUDITOR’S REPORT TO THE SHAREHOLDERSOF MAURITIAN EAGLE INSURANCE COMPANY LIMITED

This report is made solely to the company’s shareholders, as a body, in accordance with section 205 of the Mauritius Companies Act 2001. Our audit work has been undertaken so that we might state to the company’s shareholders those matters we are required to state to them in an auditor’s report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the company and the company’s shareholders as a body, for our audit work, for this report, or for the opinions we have formed.

Report on the Financial Statements

We have audited the financial statements of Mauritian Eagle Insurance Company Limited (“the company”) and its subsidiaries (collectively referred as “the group”) on pages 30 to 97 which comprise the statements of financial position as at 30 June 2012 and the statements of comprehensive income, statements of changes in equity and statements of cash flows for the year then ended and a summary of significant accounting policies and other explanatory information.

Directors’ responsibilities for the financial statements The directors are responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards and in compliance with the requirements of the Mauritius Companies Act 2001 and the Financial Reporting Act 2004. They are also responsible for such internal control as they determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s responsibilityOur responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

OpinionIn our opinion, the financial statements on pages 30 to 97 give a true and fair view of the financial position of the group and company as at 30 June 2012, and of their financial performance and cash flows for the year then ended in accordance with International Financial Reporting Standards and comply with the requirements of the Mauritius Companies Act 2001 and the Financial Reporting Act 2004.

Report on other legal requirementsIn accordance with the requirements of the Mauritius Companies Act 2001, we report as follows:

• wehavenorelationshipwith,orinterestsin,thecompanyanditssubsidiariesotherthaninourcapacitiesasauditorandtaxadvisor;• wehaveobtainedallinformationandexplanationsthatwehaverequired;and• inouropinion,properaccountingrecordshavebeenkeptbythecompanyasfarasappearsfromourexaminationofthoserecords.

The Financial Reporting Act 2004The directors are responsible for preparing the Corporate Governance Report and making the disclosures required by Section 8.4 of the Corporate Governance of Mauritius (“Code”). Our responsibility is to report on these disclosures.

In our opinion, the disclosures in the Corporate Governance Report are consistent with the requirements of the Code.

Insurance Act 2005

The financial statements have been prepared in the manner and meet the requirements specified by the Financial Services Commission.

7th Floor, Raffles Tower19 CybercityEbèneMauritius

DeloitteChartered Accountants

26 September 2012

L. Yeung Sik Yuen, ACALicensed by FRC

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

30

STATEMENTS OF FINANCIAL POSITION AS AT 30 JUNE 2012

The Group The Company2012 2011 2012 2011

Notes Rs'000 Rs'000 Rs'000 Rs'000(Restated)

ASSETSNon-current assetsProperty, plant and equipment 5 589,559 445,909 76,114 78,996 Intangible assets 6 11,028 11,362 2,476 3,692 Investment in subsidiaries 7 - - 127,000 127,000 Investment in associate 8 25,961 19,758 6,313 6,313 Statutory and other deposits 9 2,500 6,500 2,500 6,500 Financial assets 10 492,350 397,825 178,738 145,321 Mortgage and other loans 11 105,165 105,681 - - Finance lease receivables 12 934,970 790,521 - -

2,161,533 1,777,556 393,141 367,822 Current assetsStatutory and other deposits 9 6,500 9,500 6,500 9,500 Mortgage and other loans 11 17,108 16,741 - - Finance lease receivables 12 341,271 264,977 - - Trade and other receivables 13 280,105 259,710 146,356 147,810 Amounts due from group companies 14 272,953 261,492 195,150 184,348 Claims recoverable from reinsurers 15 66,195 67,142 66,195 67,142 Bank and cash balances 33 523,705 383,868 230,172 115,586

1,507,837 1,263,430 644,373 524,386

Total assets 3,669,370 3,040,986 1,037,514 892,208

EQUITY AND LIABILITIESCapital and reserves Stated capital 16 80,000 80,000 80,000 80,000 Reserves 452,350 417,445 424,032 369,868 Equity attributable to owners of the company 532,350 497,445 504,032 449,868 Non-controlling interests 99,305 99,273 - -

Total equity 631,655 596,718 504,032 449,868

Other reserves 17 2,346 2,334 - -

Insurance fundsGeneral insurance fund 18 217,784 167,088 217,784 167,088 Life insurance fund 19 597,511 515,586 - -

815,295 682,674 217,784 167,088 Non-current liabilitiesLoans 20 35,737 45,076 - - Deposits from customers 21 683,331 543,999 - - Deferred tax liabilities 22 11,980 11,581 3,657 3,617

731,048 600,656 3,657 3,617 Current liabilitiesTrade and other payables 23 209,822 114,006 79,228 66,833 Amounts due to immediate holding company 24 - 294 - - Loans 20 43,124 - - - Gross outstanding claims 15 226,977 202,191 226,977 202,191 Deposits from customers 21 1,003,267 839,502 - - Current tax liabilities 25(i) 5,836 2,611 5,836 2,611

1,489,026 1,158,604 312,041 271,635

Total equity and liabilities 3,669,370 3,040,986 1,037,514 892,208

Approved by the Board of Directors and authorised for issue on 26 September 2012

DIRECTOR DIRECTOR

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

31

STATEMENTS OF COMPREHENSIVE INCOMEFOR THE YEAR ENDED 30 JUNE 2012

The Group The Company 2012 2011 2012 2011

Notes Rs'000 Rs'000 Rs'000 Rs'000

Gross insurance premiums 923,881 864,875 739,345 656,157 Gross lease rental income 496,213 391,140 - -

1,420,094 1,256,015 739,345 656,157

Reinsurance premiums ceded (375,792) (330,127) (346,214) (314,228)Capital element of finance lease rental income (261,325) (197,337) - -

(637,117) (527,464) (346,214) (314,228)

Net Revenue 782,977 728,551 393,131 341,929 Investment income 26 67,463 61,522 30,712 22,558 Commission income 57,356 61,027 53,604 54,077 Other income 27 34,887 13,762 4,168 6,710

942,683 864,862 481,615 425,274 Benefits and ExpensesNet benefits and claims 28 (258,204) (395,918) (186,048) (155,282)Commission payable (87,414) (79,028) (67,735) (60,066)Administrative expenses 29 (244,074) (232,031) (84,211) (76,131)

(589,692) (706,977) (337,994) (291,479)

Profit from operations 352,991 157,885 143,621 133,795

(Release to)/transfer from: General insurance fund 18 (50,696) (57,944) (50,696) (57,944)Life insurance fund 19 (81,925) 69,717 - -

(132,621) 11,773 (50,696) (57,944)

220,370 169,658 92,925 75,851 Finance costs 30 (128,111) (130,151) - -

92,259 39,507 92,925 75,851 Share of profits of associate 8 5,940 6,367 - -

Profit before taxation 98,199 45,874 92,925 75,851 Income tax expense 25(ii) (14,960) (8,840) (14,601) (9,264)

Profit after taxation 83,239 37,034 78,324 66,587

Transfer to statutory reserve fund 17 (12) - - -

Profit for the year 83,227 37,034 78,324 66,587

Other comprehensive incomeNet (loss)/gain arising on revaluation of available-for-sale financial assets during the year

10 (19,137) 23,684 (1,274) 15,052

Reclassification adjustment relating to the transfer of life operations - - - (13,241)Reclassification adjustments relating to available-for-sale financial assets disposed of in the year (12,918) 1,116 (5,286) 1,414 Exchange difference arising from translation of associate operations 1,365 (2,096) - - Other comprehensive (loss)/income for the year (30,690) 22,704 (6,560) 3,225

TOTAL COMPREHENSIVE INCOME FOR THE YEAR 52,537 59,738 71,764 69,812

Profit/(loss) attributable to: Owners of the company 83,195 58,756 78,324 66,587 Non-controlling interests 32 (21,722) - -

83,227 37,034 78,324 66,587

Total comprehensive income/(loss) attributable to:Owners of the company 52,505 81,460 71,764 69,812 Non-controlling interests 32 (21,722) - -

52,537 59,738 71,764 69,812

EARNINGS PER SHARE 31 10.40 7.34 Rs

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

32

STATEMENTS OF CHANGES IN EQUITY FOR THE YEAR ENDED 30 JUNE 2012

Foreign Attributablecurrency to owners

Property Investments translation of the Non Total Stated revaluation revaluation reserve Retained company controlling equity Capital reserve reserve (Restated) earnings (Restated) interests (Restated)

Notes Rs'000 Rs'000 Rs'000 Rs'000 Rs'000 Rs'000 Rs'000 Rs'000 THE GROUP

Balance as per previously reported at 1 July 2010 80,000 19,754 11,609 - 330,027 441,390 101,395 542,785

Effect of restatement 8 - - - (9,405) - (9,405) - (9,405)

Balance as restated at 1 July 2010 80,000 19,754 11,609 (9,405) 330,027 431,985 101,395 533,380

Issue of shares - - - - - - 19,600 19,600

Dividends 32 - - - - (16,000) (16,000) - (16,000)

Profit for the year - - - - 58,756 58,756 (21,722) 37,034 Other comprehensive income for the year - - 24,800 (2,096) - 22,704 - 22,704 Total comprehensive income for the year - - 24,800 (2,096) 58,756 81,460 (21,722) 59,738

Balance at 30 June 2011 80,000 19,754 36,409 (11,501) 372,783 497,445 99,273 596,718

Dividends 32 - - - - (17,600) (17,600) - (17,600)Transfer to retained earnings - (1,000) - - 1,000 - - - Profit for the year - - - - 83,195 83,195 32 83,227 Other comprehensive income for the year - - (32,055) 1,365 - (30,690) - (30,690)Total comprehensive income for the year - - (32,055) 1,365 83,195 52,505 32 52,537

Balance at 30 June 2012 80,000 18,754 4,354 (10,136) 439,378 532,350 99,305 631,655

Stated Property Investments Retained Total Notes Capital revaluation revaluation earnings

reserve reserveRs'000 Rs'000 Rs'000 Rs'000 Rs'000

THE COMPANY

Balance at 1 July 2010 80,000 19,754 11,609 284,693 396,056

Dividends 32 - - - (16,000) (16,000)

Profit for the year - - - 66,587 66,587 Other comprehensive income for the year - - 3,225 - 3,225 Total comprehensive income for the year - - 3,225 66,587 69,812

Balance at 30 June 2011 80,000 19,754 14,834 335,280 449,868

Dividends 32 - - - (17,600) (17,600)Transfer to retained earnings - (1,000) - 1,000 - Profit for the year - - - 78,324 78,324 Other comprehensive income for the year - - (6,560) - (6,560)Total comprehensive income for the year - - (6,560) 78,324 71,764

Balance at 30 June 2012 80,000 18,754 8,274 397,004 504,032

The difference in the depreciation based on revalued amount and the cost of the building, net of deferred tax, is transferred from property revaluation reserve to retained earnings.

The difference in the depreciation based on revalued amount and the cost of the building, net of deferred tax, is transferred from property revaluation reserve to retained earnings.

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

33

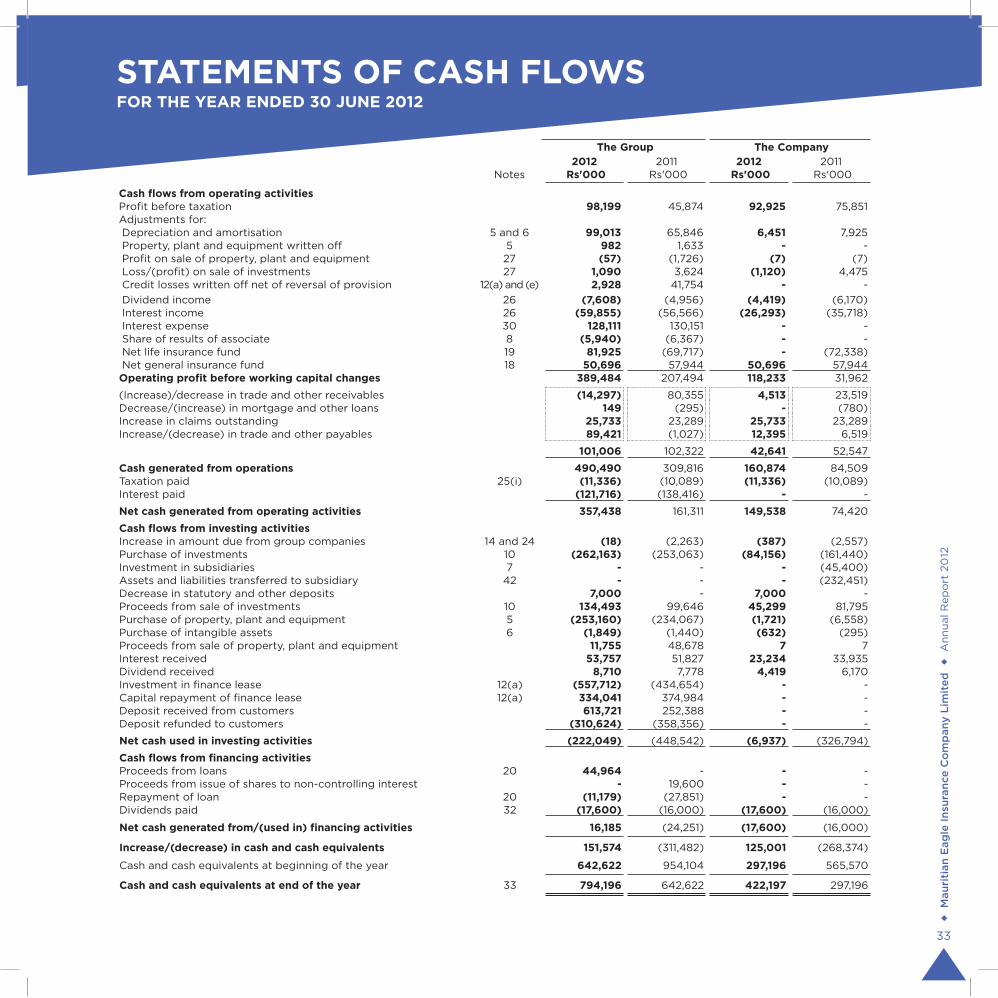

STATEMENTS OF CASH FLOWS FOR THE YEAR ENDED 30 JUNE 2012

The Group The Company2012 2011 2012 2011

Notes Rs'000 Rs'000 Rs'000 Rs'000

Cash flows from operating activitiesProfit before taxation 98,199 45,874 92,925 75,851 Adjustments for: Depreciation and amortisation 5 and 6 99,013 65,846 6,451 7,925 Property, plant and equipment written off 5 982 1,633 - - Profit on sale of property, plant and equipment 27 (57) (1,726) (7) (7) Loss/(profit) on sale of investments 27 1,090 3,624 (1,120) 4,475 Credit losses written off net of reversal of provision 12(a) and (e) 2,928 41,754 - - Dividend income 26 (7,608) (4,956) (4,419) (6,170) Interest income 26 (59,855) (56,566) (26,293) (35,718) Interest expense 30 128,111 130,151 - - Share of results of associate 8 (5,940) (6,367) - - Net life insurance fund 19 81,925 (69,717) - (72,338) Net general insurance fund 18 50,696 57,944 50,696 57,944 Operating profit before working capital changes 389,484 207,494 118,233 31,962

(Increase)/decrease in trade and other receivables (14,297) 80,355 4,513 23,519 Decrease/(increase) in mortgage and other loans 149 (295) - (780)Increase in claims outstanding 25,733 23,289 25,733 23,289 Increase/(decrease) in trade and other payables 89,421 (1,027) 12,395 6,519

101,006 102,322 42,641 52,547

Cash generated from operations 490,490 309,816 160,874 84,509 Taxation paid 25(i) (11,336) (10,089) (11,336) (10,089)Interest paid (121,716) (138,416) - -

Net cash generated from operating activities 357,438 161,311 149,538 74,420

Cash flows from investing activitiesIncrease in amount due from group companies 14 and 24 (18) (2,263) (387) (2,557)Purchase of investments 10 (262,163) (253,063) (84,156) (161,440)Investment in subsidiaries 7 - - - (45,400)Assets and liabilities transferred to subsidiary 42 - - - (232,451)Decrease in statutory and other deposits 7,000 - 7,000 - Proceeds from sale of investments 10 134,493 99,646 45,299 81,795 Purchase of property, plant and equipment 5 (253,160) (234,067) (1,721) (6,558)Purchase of intangible assets 6 (1,849) (1,440) (632) (295)Proceeds from sale of property, plant and equipment 11,755 48,678 7 7 Interest received 53,757 51,827 23,234 33,935 Dividend received 8,710 7,778 4,419 6,170 Investment in finance lease 12(a) (557,712) (434,654) - - Capital repayment of finance lease 12(a) 334,041 374,984 - - Deposit received from customers 613,721 252,388 - - Deposit refunded to customers (310,624) (358,356) - -

Net cash used in investing activities (222,049) (448,542) (6,937) (326,794)

Cash flows from financing activitiesProceeds from loans 20 44,964 - - - Proceeds from issue of shares to non-controlling interest - 19,600 - - Repayment of loan 20 (11,179) (27,851) - - Dividends paid 32 (17,600) (16,000) (17,600) (16,000)

Net cash generated from/(used in) financing activities 16,185 (24,251) (17,600) (16,000)

Increase/(decrease) in cash and cash equivalents 151,574 (311,482) 125,001 (268,374)

Cash and cash equivalents at beginning of the year 642,622 954,104 297,196 565,570

Cash and cash equivalents at end of the year 33 794,196 642,622 422,197 297,196

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

34

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2012

1 GENERAL INFORMATION Mauritian Eagle Insurance Company Limited (the “Company”) is a listed limited liability company incorporated and domiciled in

Mauritius. The Company’s registered office is situated at 5th Floor, IBL House, Caudan, Port Louis and operates at 1st Floor, IBL House, Caudan, Port Louis. The Company, the subsidiaries and associate are collectively referred to as the “Group”.

The Company carries out short term and long term insurance business and with effect from 1 January 2011, the activities of the long-term business were transferred to Mauritian Eagle Life Company Limited, a wholly-owned subsidiary of the Company. Short term insurance comprises of general insurances and covers the following:-

• Accident • Engineering • Fireandalliedperils • Motor • Transportation The activities of the subsidiary companies are disclosed in note 7(c). 2 APPLICATION OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRSs) In the current year, the Group and the Company have applied all of the new and revised Standards and Interpretations issued by the

International Accounting Standards Board (“IASB”) and the International Financial Reporting Interpretations Committee (“IFRIC”) of the IASB that are relevant to its operations and effective for accounting periods beginning on 1 July 2011.

2.1 Standards and Interpretations applied with no effect on financial statements The following relevant new and revised Standards and Interpretations have been adopted in these financial statements. Their

application has not had any significant impact on the presentation and disclosure and on the amounts reported in these financial statements but may impact the accounting for future transactions or arrangements.

IAS 1 Presentation of Financial Statements - Amendments resulting from May 2010 Annual Improvements to IFRSs IAS 24 Related Party Disclosures - Revised definition of related parties IFRS 7 Financial Instruments: Disclosures - Amendments resulting from May 2010 Annual Improvements to IFRSs IFRS 7 Financial Instruments: Disclosures - Amendments enhancing disclosures about transfers of financial assets IFRIC 14 IAS 19 - The limit on a defined benefit asset, minimum funding requirements and their Interaction (November 2009

amendment with respect to voluntary prepaid contributions) 2.2 Standards and Interpretations in issue not yet effective At the date of authorisation of these financial statements, the following Standards and Interpretations were in issue but effective

on annual periods beginning on or after the respective dates as indicated: IAS 1 Presentation of Financial Statements - Amendments to revise the way other comprehensive income is presented

(effective 1 July 2012) IAS 1 Presentation of Financial Statements - Amendments resulting from Annual Improvements 2009-2011 Cycle

(comparative information) (effective 1 January 2013)

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

35

2 APPLICATION OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRSs) (Continued) 2.2 Standards and Interpretations in issue not yet effective (Continued)

IAS 12 Deferred Tax: Income taxes - Limited scope amendments (recovery of underlying assets) IAS 19 Employee Benefits 2011 - Amendments with revised requirements for pensions and other postretirement benefits,

termination benefits and other changes (effective 1 January 2013) IAS 27 Separate Financial Statements (2011) - Original issue (effective 1 January 2013) IAS 28 Investments in Associates and Joint Ventures (2011) - Original issue (effective 1 January 2013) IAS 32 Financial Instruments: Presentation - Amendments relating to the offsetting of assets and liabilities (effective 1

January 2014) IAS 32 Financial Instruments: Presentation - Amendments resulting from Annual Improvements 2009-2011 Cycle (tax effect

of equity distributions) (effective 1 January 2013) IFRS 7 Financial Instruments: Disclosures - Amendments related to the offsetting of assets and liabilities (effective 1 January

2013) IFRS 7 Financial Instruments: Disclosures - Deferral of mandatory effective date of IFRS 9 and amendments to transition

disclosures (effective 1 January 2015) IFRS 9 Financial Instruments - Reissue to include requirements for the classification and measurement of financial liabilities

and incorporate existing derecognition requirements (effective 1 January 2013) IFRS 9 Financial Instruments - Original issue (effective 1 January 2015) IFRS 10 Consolidated Financial Statements - Original issue (effective 1 January 2013) IFRS 10 Consolidated Financial Statements - Amendments to transitional guidance (effective 1 January 2013) IFRS 12 Disclosure of Interests in Other Entities - Original issue (effective 1 January 2013). IFRS 12 Disclosure of Interests in Other Entities - Amendments to transitional guidance (effective 1 January 2013) IFRS 13 Fair Value Measurement - Original issue (effective 1 January 2013)

The directors anticipate that these amendments will be applied in the financial statements for the annual periods beginning on the respective dates as indicated above. The directors have not yet had an opportunity to consider the potential impact of the adoption of these amendments.

3 SIGNIFICANT ACCOUNTING POLICIES

The principal accounting policies adopted by the Group are as follows: 3.01 Basis of preparation The financial statements are prepared under the historical cost convention as modified by the revaluation of land and buildings

and certain available-for-sale investments and in accordance with International Financial Reporting Standards (IFRSs).

3.02 Basis of consolidation The consolidated financial statements include the results of the Company and of its subsidiaries. The results of the subsidiaries

acquired or disposed of during the year are included in the statements of comprehensive income from the date of their acquisition or up to the date of their disposal. Inter-Group transactions and balances are eliminated on consolidation.

Subsidiaries are all entities over which the Company has the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities.

Non-controlling interests in the net assets of the subsidiaries are identified separately from the Group’s equity therein. Non-

controlling interests consist of the amount of those interests at the date of the original business combination and the non-controlling interests of changes in equity since the date of the combination. Losses applicable to the minority in excess of the non-controlling interests’s interest in the subsidiary’s equity are allocated against the interests of the Group except to the extent that the minority has a binding obligation and is able to make an additional investment to cover the losses.

When the Group loses control of a subsidiary, the profit or loss on disposal is calculated as the difference between (i) the aggregate of the fair value of the consideration received and the fair value of any retained interest and (ii) the previous carrying amount of the assets (including goodwill), and liabilities of the subsidiary and any non-controlling interests. Amounts previously recognised in other comprehensive income in relation to the subsidiary are accounted for (i.e. reclassified to profit

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

36

3 SIGNIFICANT ACCOUNTING POLICIES (continued)

3.02 Basis of consolidation (Continued)

or loss or transferred directly to retained earnings) in the same manner as would be required if the relevant assets or liabilities were disposed of. The fair value of any investment retained in the former subsidiary at the date when control is lost is regarded as the fair value on initial recognition for subsequent accounting under IAS 39 Financial Instruments: Recognition and Measurement or, when applicable, the cost on initial recognition of an investment in an associate or jointly controlled entity.

3.03 Property, plant and equipment

Property, plant and equipment are stated at cost or revalued amount less accumulated depreciation and any accumulated impairment losses. Revaluations are performed such that the carrying amount does not differ materially from that which would be determined using fair values at end of the reporting period.

Any revaluation increase arising on the revaluation of such land and buildings is recognised in other comprehensive income and

accumulated in equity, except to the extent that it reverses a revaluation decrease for the same asset previously recognised in profit or loss, in which case the increase is credited to profit or loss to the extent of the decrease previously expensed. A decrease in the carrying amount arising on the revaluation of such land and buildings is recognised in profit or loss to the extent that it exceeds the balance, if any, held in the properties revaluation reserve relating to a previous revaluation of that asset.

An item of property, plant and equipment is derecognised upon disposal or when no future economic benefits are expected to arise from the continued use of the asset. Any gain or loss arising on the disposal or retirement of an item of property, plant and equipment is determined as the difference between the sales proceeds and the carrying amount of the asset and is recognised in profit or loss.

Profit or loss on disposal of property, plant and equipment is determined as the difference between the carrying amount of the

assets and the net disposal proceeds and is accounted for in the statement of comprehensive income. Depreciation on revalued buildings is recognised in profit or loss. On the subsequent sale or retirement of a revalued property,

the attributable revaluation surplus remaining in the properties revaluation reserve is transferred directly to retained earnings. Surplus on the revalued property is transferred annually from property revaluation reserve to retained earning. The amount

transferred is computed on the difference between depreciation based on the revalued amount of the asset and depreciation based on the asset’s original cost.

3.04 Depreciation

No depreciation is provided on land. Depreciation on other property, plant and equipment is calculated to write off the cost or revalued amount of the assets to their estimated residual values on a straight line basis over their expected useful lives as follows:

Building 2.5 % Furniture and equipment 20 % Computer equipment 33.3 % Motor vehicles 6 years Plant and machinery and motor vehicles under operating leases depreciated over the lease terms

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2012

M

auri

tian

Eag

le In

sura

nce

Co

mp

any

Lim

ited

Ann

ual R

epo

rt 2

012

37

3 SIGNIFICANT ACCOUNTING POLICIES (continued)

3.05 Intangible asset and amortisation

Computer software is stated at cost less accumulated amortisation. Amortisation of computer software is calculated to write off its cost on a straight line basis over its estimated useful life of 3 to 6 years.

An intangible asset is derecognised on disposal, or when no future economic benefits are expected from use or disposal. Gains

or losses arising from derecognition of an intangible asset, measured as the difference between the net disposal proceeds and the carrying amount of the asset, are recognised in profit or loss when the asset is derecognised.

3.06 Investment in subsidiaries

In the Company’s financial statements, investment in subsidiaries is stated at cost. The carrying amount is reduced if there is any indication of impairment in value.

3.07 Investment in associate

An associate is an entity over which the Company has significant influence and that is neither a subsidiary nor an interest in a joint venture. Significant influence is the power to participate in the financial and operating policy decision of the investee but is not control or joint control over these policies.