annual report - nbs.rs · integrated supervision of the financial system. in 2004 the national bank...

TRANSCRIPT

NATIONAL BANK OF SERBIA

Annual Report2003

Ekonomski pregled

NATIONAL BANK OF SERBIA

Annual Report2003

Governor�s Statement

The National Bank of Serbia has commenced the year of 2004, theyear of its 120th anniversary, with the high credibility of a trustful

institution persistently devoted to its legal commitments, as defined by thenew Law on the National Bank of Serbia, to preserve price stability andensure efficiency of the overall financial system.

By the measures of monetary policy undertaken in 2003, the NationalBank of Serbia supported the efforts towards accomplishing the keyobjectives of economic policy, above all the last year�s rate of inflation being7.8 per cent against the projected 9 per cent. The foreign exchange marketand the dinar exchange rate remained stable, net purchases in exchangeoperations reached nearly EUR 1.2 billion, considerable increase wasreported in foreign currency and dinar savings, bank privatization processwas initiated, and the development project was launched for the nationalDinaCard which should attract about a million cardholders by the end of theyear.

One of the most extensive financial projects was completed in earlyJanuary 2003, when payment operations were shifted from the Clearing andSettlement Bureau to commercial banks, and the RTGS and clearing systemof the National Bank of Serbia was launched. The number of orderschanneled through this system reached 104 million (or a daily average of343,289 orders) totaling CSD 7,114 billion (or CSD 23.6 billion per day),and the National Bank of Serbia was highly appraised by internationalinstitutions for the work done, particularly by the IMF.

Banking supervision systems were further developed in 2003. The focusof supervision was shifted from legal requirements in the operation of banksto the risks to which they are exposed and to risk management, as well as tothe timely taken corrective measures.

Government deposits, which were withdrawn from commercial banksand placed with the National Bank of Serbia in 2003, added to the centralbank�s more extensive control of monetary flows. This in turn contributed tothe macroeconomic stability, as a significant portion of money originatingfrom foreign capital inflows in 2003 could be sterilized.

The National Bank of Serbia will further support this year�s objectivesof development and economic policies by upgrading market mechanismstowards the implementation of monetary policy, and it has already startedorganizing auction sale of its own bills in the primary market at the variableinterest rate. In 2004 the National Bank of Serbia also intends to start

developing repurchase operations, thus contributing to the growth of bondand money market, and encouraging the demand for government securities.By stimulating direct interbank trading, the central bank plans to graduallyreduce the extent of its interventions in the foreign exchange market, and toallow most of the trading to be done between commercial banks.

After the capital requirement was set to be met by banks until the end of2003, in 2004 the National Bank of Serbia will particularly be committed tothe full application of the CAMEL bank ranking system, along with thecreation of early warning systems to respond to identified risks in thebanking sector. In 2004 the National Bank of Serbia will continue its efforts towards thetransparency of the banking sector and, guided by this objective, it haspublished its first report containing the information on ownership, balancesheet and income statement of banks for 2003. According to the newInsurance Law, this year the National Bank of Serbia will also take over thesupervision in the insurance activity, as the first step leading to theintegrated supervision of the financial system.

In 2004 the National Bank of Serbia plans to issue a new 500-dinarbanknote in addition to the current denominations. Furthermore, the Mintwill be involved in manufacturing excise stamps, and developing the newpassport and Personalization Center. A special collection ofcommemorative coins will be prepared for the 200th anniversary of the FirstSerbian Uprising and the 120th anniversary of the National Bank of Serbia.

In every country undergoing transition, central banks have a key role inbuilding up a sound background for the accelerated development ofeconomy. The National Bank of Serbia is fully aware of this role and it willnot only support, but also lead the reform processes to help Serbia bridgethe gap of several decades which have kept the country away from theEuropean Union.

Governor of the National Bank of Serbia

Radovan Jela{i}

5

Annual Report 2003

CONTENTS

ORGANIZATIONAL STRUCTURE OF THE NATIONAL BANK OF SERBIA 7

MACROECONOMIC DEVELOPMENTS 11

ACTIVITIES OF THE NATIONAL BANK 25

MONETARY POLICY 27

EXCHANGE RATE OF THE DINAR

AND FOREIGN CURRENCY RESERVES 47

ISSUE OF BANKNOTES AND COINS 59

BALANCE OF PAYMENTS 63

EXTERNAL RELATIONS 73

BANKING SECTOR AND BANK SUPERVISION 85

PAYMENT OPERATIONS 101

LEGAL AND REGULATORY ACTIVITIES 105

INTERNAL AUDIT 109

ORGANIZATIONAL AND PERSONNEL CHANGES 113

INFORMATION TECHNOLOGY 119

ANNUAL STATEMENT OF ACCOUNT 123

Annual Report 2003

7

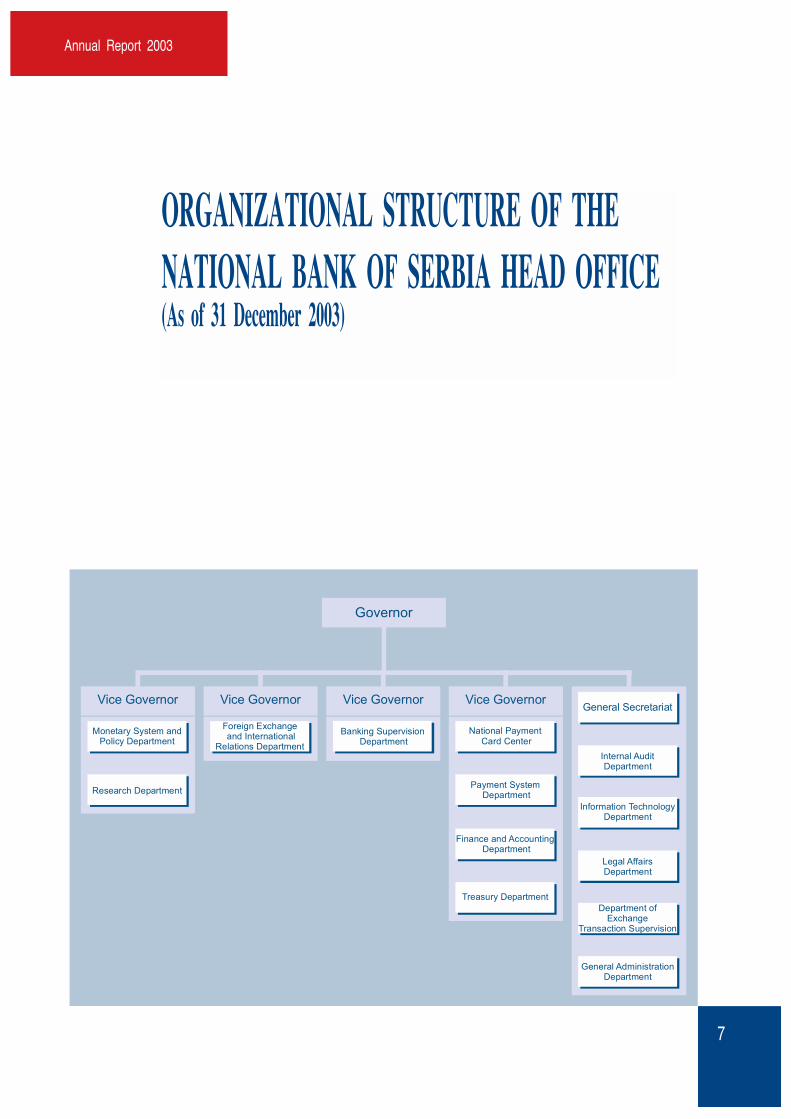

ORGANIZATIONAL STRUCTURE OF THE

NATIONAL BANK OF SERBIA HEAD OFFICE (As of 31 December 2003)

Finance and Accounting Department

Treasury Department

Banking Supervision Department

Foreign Exchange and International

Relations Department

Vice Governor

Monetary System and Policy Department

Research Department

Information Technology Department

Legal Affairs Department

General Secretariat

Internal Audit Department

National Payment Card Center

Payment System Department

Department of Exchange

Transaction Supervision

General Administration Department

Vice Governor Vice Governor Vice Governor

Governor

Annual Report 2003

9

Monetary System and Policy Department

Banking Supervision Department

General Secretariat

Internal Audit Department

Research Department

Information Technology Department

National Payment Card Center

Legal Affairs Department

Payment System Department

Department of Exchange Transactions Supervision

Finance and Accounting Department

Treasury Department

General Administration Department

Registers and Forced Collection Department

Finance and Accounting Division

General Administration Division

Ekspoziture Palilula

Ekspoziture Vozdovac

Ekspoziture Novi Beograd

Ekspoziture Pancevo

Ekspoziture Sabac

Ekspoziture Pozarevac

Ekspoziture Smederevo

Monetary Department

Foreign Exchange Department

Division for On-Site Supervision of Exchange Transactions

Analyses Division

Finance and Accounting Division

Vault Cash Operations Division

General Administration Division

Ekspoziture Novi Sad

Ekspoziture Sombor

EkspozitureSremska Mitrovica

Ekspoziture Vrsac

Ekspoziture Zrenjanin

Ekspoziture Kikinda

Foreign Exchange Division

Solvency and Forced Collection Division

Division for On-Site Supervision of Exchange Transactions

Vault Cash Operations Division

Finance and Accounting Division

General Administration Division

Ekspoziture Zajecar

Ekspoziture Vranje

Ekspoziture Prokuplje

Ekspoziture Pirot

Ekspoziture Leskovac

Ekspoziture Jagodina

Ekspoziture Krusevac

Ekspoziture Kraljevo

Ekspoziture Novi Pazar

Ekspoziture Leposavic

Ekspoziture Valjevo

Ekspoziture Prijepolje

Ekspoziture Loznica

Ekspoziture Cacak

Pre-Press Department

Banknote Printing Department

Mint

Securities Printing Department

Maintenance and Power Supply Department

Marketing Department

Development Center

Quality Center

Financial Department

Legal-Administrative Department

Foreign Exchange and International Relations Department

Ekspoziture Subotica

Ekspoziture Becej

Ekspoziture Senta

Ekspoziture Vrbas

Ekspoziture Stari grad

Specialized InstitutionM a i n O r g a n i z a t i o n a l U n i t s

Foreign Exchange Division

Solvency and Forced Collection Division

Division for On-Site Supervision of Exchange Transactions

Vault Cash Operations Division

Finance and Accounting Division

General Administration Division

Foreign Exchange Division

Solvency and Forced Collection Division

Division for On-Site Supervision of Exchange Transactions

Vault Cash Operations Division

Finance and Accounting Division

General Administration Division

ORGANIZATIONAL STRUCTURE OF THE NATIONAL BANK OF SERBIA(As of 31 December 2003)

11

Annual Report 2003

MACROECONOMIC DEVELOPMENTS

OVERVIEW OF MACROECONOMIC DEVELOPMENTS 12PRICE MOVEMENTS 13ECONOMIC ACTIVITY AND EMPLOYMENT 16

ECONOMIC ACTIVITY 16EMPLOYMENT 19

DOMESTIC DEMAND AND PUBLIC SECTOR 21EARNINGS 21INVESTMENT ACTIVITY 22TRADE TURNOVER 23

Annual Report 2003Macroeconomic Developments

Overview of Macroeconomic Developments

Serbia's economic growth did not reach the projected rate in 2003, althougha moderate improvement of the economic activity reported close to the end of theyear has been even more pronounced in the first quarter of 2004. Besides trade andservices, the economic growth in 2003 was basically generated by constructionindustry, as well as by telecommunications, and has additionally been supported byprocessing industry in the first quarter of 2004. The estimates are that the secondhalf of 2004 will see a substantial impetus given by agricultural production relyingon the positive effects of the planned increase in the agrarian budget for 2004.

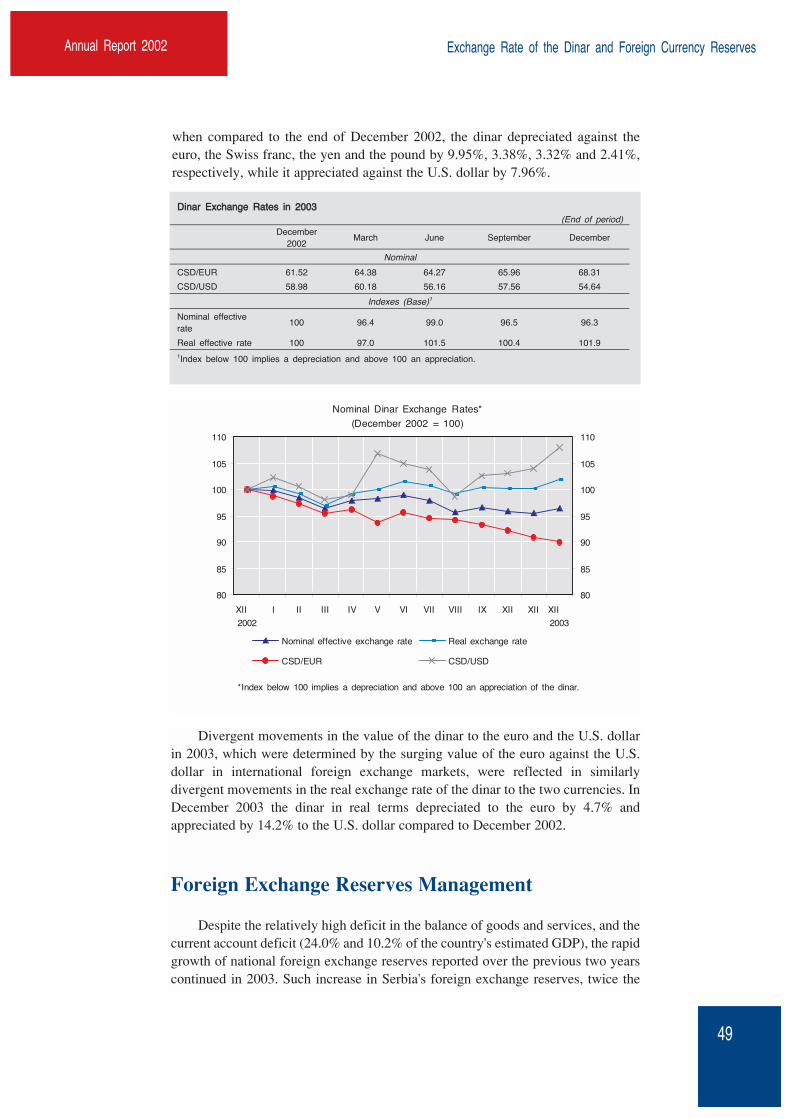

Variations in the exchange rate of the dinar in 2003, within the limits ofmanaged floating, were marked by a highly stable real effective exchange rate anda moderately depreciated nominal effective exchange rate of the dinar. The stabilityof its real effective rate indicated that in 2003 the international pricecompetitiveness of local businesses maintained the same level in the areadetermined by the external value of national currency. As estimated, no changes inthe dinar exchange rate regime are expected in 2004 and the achieved stability willbe preserved.

Last year's interest rates reflected a moderately declining trend, although theyare still relatively high due to the high demand for loans. Interest rates offered inthe market vary to a great extent and are still determined by the investment andpolitical risk, inadequate legal framework capable of protecting creditors in theevent of any disputes, by lacking efficiency of the banking sector, as well as by theunresolved issue of the London Club creditors. High interest rates are among thefactors limiting a more expansive financing of production.

The area with the most limited progress in the past period, though extremelyimportant for a more rapid development, relates to the creation of adequateconditions for market competition. This segment of the economic policy still lacksa number of laws which have not been enacted yet, no new institutions have beenestablished to prevent the monopolistic market behavior of businesses, while theexisting institutions have not been restructured.

In order to achieve the growth of investment, as the driving force of thesustainable growth in the medium and long term, the increase in domestic savingsshould also be encouraged in addition to direct foreign investments. More intensivedirect foreign investments are extremely important for Serbia as, contrary to externalborrowing, they provide for new technology and for lacking capital which, combinedwith the business oriented management, generate direct effects in terms of increasedproductivity. Parallel to the strengthening of public trust in banks, it is important todevelop the non-banking sector, e.g. insurance companies and institutional investors.

12

Annual Report 2003 Macroeconomic Developments

13

To create a favorable investment climate, it is necessary to enact and enforcethe laws providing for legal safety of potential investors and simultaneouslyensuring the efficiency of courts and the compliance with the respective rights andcontracts, whereby the investment risk would be mitigated.

Taking into account the international economic environment, Serbia'sprospects appear to be brighter than in the same period of 2003. The factors bywhich Serbia's economy is encouraged or its balance of payments improved are theeconomic recovery in the EU countries, low interest rates, and the declining valueof the U.S. dollar. Last year's less favorable effects related to the rising oil prices(partly reflecting the depreciation of the U.S. dollar) which made oil import muchmore expensive, with the same trends continuing in 2004.

Price Movements

With respect to the measures taken in the area of monetary and fiscal policies,the year of 2003 saw a considerably reduced rate of inflation in the Republic ofSerbia, which was even below the projected level. According to the data reportedby the official statistics, the rate of inflation measured by retail prices was 7.8%(from December to December) relative to the projected 9%. The suppressedinflation was also supported by delayed adjustments of some of the administrativelyregulated prices, as well as the depreciated value of the dollar with positive effectson the prices of oil and gas which are Serbia's significant imports. The slowed-downinflation was further contributed to by the reduced customs and tax rates in tradewith Montenegro. In structural terms and in comparison to the previous year,inflation was undoubtedly decelerated by relatively slowed-down rise in industrialproducer prices (4.6% from December to December) and in agricultural producerprices in the first three quarters of 2003 (3.2%).

The increase in inflation reported in 2003 was influenced by the real rise inwages and labor unit costs, and to a smaller degree by variations in the exchangerate of the dinar, while the suppressing effects resulted from the high exports ofgoods and services, partly reduced taxes and customs duties, vigorous monetaryrestrictions, enhanced market competition and a number of other factors.

Broken down by groups of products and services, a relatively more rapid risein prices was reported with drinks (6.1%) and tobacco (9.1%), industrial non-foodstuffs and services (6.9%).

Core inflation was considerably below the overall inflation and was reportedat 5.4% as the prices of goods and services subject to market conditions rose moreslowly than those of products and services to which the price disparity adjustmentswere applied. Price disparity adjustments fall within the competence of governmentauthorities, either on the level of the Republic or of local government (for utilities,transport and other public services).

The current rate of core inflation approaches the level reported in 12 euro zonecountries and 25 EU countries. Even so, Serbia's inflation in 2003 was still much higherthan the average one reported in the euro zone countries (2.1%). Compared to each of thecountries which joined the European Union on 1 May 2004, last year's higher rate ofinflation was only recorded by Slovakia (9.3%). In Hungary, for example, it reached5.6%. In 2003 the prices of products and public services subject to disparity adjustmentsrose by 10.5%, which affected the overall inflation and its higher rate compared to coreinflation.

Annual Report 2003Macroeconomic Developments

14

Core and Overall Inflation in the Republic of Serbia(December 2002 = 100)

99

101

103

105

107

109

XII2002

I II III IV V VI 2003

VII VIII IX X XI XII

Core inflation Overall inflation

Due to price disparity adjustments applied to utilities, municipal and otherpublic services, in 2003 the prices of services increased much more rapidly (11.1%)than those of goods (6.6%) measured in December relative to December 2002.Similar movements were reported both in 2001 and 2002, and resulted in the rise inprices of services by as much as 37.3% and prices of goods by 15,6% in the pastthree years, against the general retail price growth of 20.3%, all based on the yearlyaverage.

CCoorree aanndd OOvveerraallll IInnffllaattiioonn iinn tthhee RReeppuubblliicc ooff SSeerrbbiiaa (Retail price growth rates in %)

Dec 2001 Dec 2000

Dec 2002 Dec 2001

Dec 2003 Dec 2002

Overall retail price growth 40.7 14.8 7.8

Price growth in sectors with disparities

Energy

57.7 24.6 9.2

Of which: Electricity 150.1 52.4 16.5 Drugs 74.1 -6.4 -0.6 Bread and wheat flour 92.3 0.8 20.2 Utility services 155.0 70.6 16.1 Transport 57.3 39.8 8.2 PTT 143.6 13.0 1.4

One-off effect of the changes in the tax system 5.0* - -

Core inflation 18.4 6.0 5.4

Source: NBS-RD and RSO. *The effect of tax increase is estimated to be 5 percentage points of the overall retail price growth.

Consequently, the general price level accelerated to a certain extent relative tothe first three quarters. Measured by retail prices, inflation rose by 2% in the lastquarter against 1.7 - 1.9% reported in the first nine months. The rise in pricesreported in the last quarter was not caused by price disparity adjustments, but bygrowing prices of agricultural and food products, increased wages in real terms, andpartly by the so-called psychological inflation - inflation expectations relating to theproblems in forming the Government and the Parliament in late 2003.

Annual Report 2003 Macroeconomic Developments

15

The cost of living rose by 8.1% in 2003, while the prices of services and goodsincreased by 16.9% and 6.7%, respectively.

Similar to retail prices, the cost of living rose more rapidly in the last quarterthan producer prices, due to the growing prices of services and foodstuffs (causedby droughts and floods in 2003). As reported by the official statistics, the cost ofliving increased by 3.2% in the last three months, within which the increase in pricesof services was by 3.5%.

Prices and Cost of Living in the Republic of Serbia

0

20

40

60

80

100

120

140

160

1995 1996 1997 1998 1999 2000 2001 2002 2003

Retail prices Cost of living Industrial producer prices

Industrial producer prices recorded a very moderate (both current andaverage) growth of 4.6% in 2003, or even lower than core inflation. In the twoprevious years these prices rose by 6.1% (in 2002) and 29.1% (in 2001). In all thethree preceding years industrial producer prices increased at a lower rate than retailprices and consequently had a stabilizing effect on the general price level and costof living. Broken down by quarters, producer prices recorded a moderate growth inthe first two quarters, surged in the third by 2.2%, and increased by 1.4% in the lastquarter. When taken by purpose, the highest increase by 6.3% was reported withpersonal goods, the effective demand for which being most pronounced. On theother hand, investment goods and intermediate goods prices recorded a lowergrowth, by 2.4% and 2.9%, respectively. Prices in extractive industry rose by 3.3%in last December relative to December 2002, while a 3.4% increase was reported inprocessing industry. In the processing sector the above average increase wasrecorded by the prices of foodstuffs, drinks and tobacco (6.9%), basic metalproduction (5.5%), and the prices in the publishing sector (11%). A considerabledrop in prices was reported in oil derivatives production (6.6%), wood processingand wood products (2.7%) and in cellulose, paper and paper processing (1.2%).Prices in electric power, gas and water production sector rose by 15%, as the resultof price disparity adjustments and, broken down by industrial sectors, this was thehighest reported increase.

Agricultural producer prices rose by 11.0% in 2003 relative to 2002(measured from December to December), although the increase largely related to theperiod close to the end of the year. Such movements in agricultural producer prices

Annual Report 2003Macroeconomic Developments

16

primarily resulted from adverse weather conditions and less extensively sown areas.Due to the reduced domestic supply, and after a 1% decrease in the first quarter, theprices rose in the second quarter. The upward trends in agricultural producer priceswere most pronounced in the fourth quarter, which saw an increase by more than9%. The average growth of these prices in 2003 exceeded the level reported in 2002by no more than 0.5%, which partly resulted from the lower statistical base in 2002,when agricultural producer prices fell by as much as 3% relative to 2001.

The highest current price growth (measured from December to December) wasreported with potatoes (127.7%), wheat (70.1%), corn (61.4%), and milk and dairyproducts (14.2%). A drop in prices was recorded by alcoholic drinks (24.7%), aswell as vegetables, cattle (beef cattle and swine), poultry and eggs.

As estimated by the NBS Research Center, the upward trend in agriculturalproducer prices will continue until the next harvest in mid-2004 and affect themovements in retail prices and the cost of living.

Economic Activity and Employment

Economic Activity

Industrial production, as opposed to the 1.7% growth in 2002, fell by 3% in2003. This resulted in adverse effects on the growth of the GDP, on exports andforeign trade deficit, as well as on the inflow of fiscal revenues from production. Therecorded fall in processing industry was 4.6%. The drop in production wasundoubtedly contributed to by the poor motivation in socially- and state-ownedcompanies relating to the expected privatization, which was accompanied by slowadjustment to the considerably increased competition in the domestic market(created by imported goods). Moreover, part of the production in the new privatesector was not fully covered by the official statistics, although this sector had notsufficiently accelerated its activity either, considering the initial adjusting steps andslow repositioning in the lost foreign markets.

Social Product and Industrial Output(Index 2001 = 100)

80

90

100

110

120

130

1995 1996 1997 1998 1999 2000 2001 2002 2003

80

90

100

110

120

130

Social product Industrial output

Annual Report 2003 Macroeconomic Developments

17

The growth in production was reported with four industrial branchesaccounting for 38% of industry: electric power, gas and water, coal production, andthe production and processing of chemicals. Other industries recorded a lower orhigher drop in production. The increase in stocks of finished products was alsoreported, due to the growing competition in the domestic market of industrialproducts resulting from extensive imports. In particular, considerable imports wererecorded with consumer goods and consequently resulted in growing stocks offinished products in this segment of domestic production.

GGrroowwtthh RRaatteess ooff RReeaall SSoocciiaall PPrroodduucctt aanndd IInndduussttrriiaall OOuuttppuutt

iinn tthhee RReeppuubblliicc ooff SSeerrbbiiaa ((11998899 −22000033))

Year Social Product (In %)

Industrial Output (In %)

1989 1.3 1.0 1990 -7.7 -12.0 1991 -11.7 -18.0 1992 -28.1 -23.0 1993 -30.4 -37.0 1994 2.6 2.0 1995 5.7 4.0 1996 4.7 6.0 1997 7.4 10.0 1998 2.4 3.9 1999 -22.8 -25.6 2000 5.7 11.4 2001 5.7 0.1 2002 3.3 1.7 2003 1.5* -3.0

Source: RSO *GDP growth for 2003 estimated by RSO.

In 2003, the restructuring of industrial companies continued, but there were stillmany large companies which had to be restructured. The process of privatizationwas considerably intensified and more than 1,000 socially- and state-ownedcompanies were privatized.

Taking into account the declining industrial activity in 2003, newmacroeconomic measures were to be set in action for encouraging the sustainablegrowth of industrial and the overall economic activity. In particular, it was importantto attract and stimulate new domestic and foreign investments. The investmentactivity would be strengthened by the effective use of the proceeds resulting fromthe privatization process, and particularly by foreign direct investments,concessions, etc., as well as by the development of SMEs in the new private sector.

The new investment and technology cycle was to be supported by projects inthe area of transport and economic infrastructure (as forms of public works). Inparticular, it was imperative to encourage housing construction and constructionactivity in general, with the aim of enhancing employment, and avoiding any socialturmoil and delays in economic reforms, including all positive dispersive effects. Inthis context, simpler procedures in obtaining building permits was one of thepriorities, as the way to encourage employment of all the domestic resources(building material, chemical, metal and electrical industry, creation of new jobs,etc.). Furthermore, it was important to adopt the strategies of industrial andeconomic development of the Republic of Serbia, particularly export and foreigntrade strategies.

Annual Report 2003Macroeconomic Developments

Agricultural production was much lower in 2003 than in 2002. This wasundoubtedly the result of severe droughts, in addition to the lower sowing rates, theunresolved financing model for primary agricultural production, the purchase ofmarket surpluses, and other problems associated with agriculture. The preliminaryestimates were that the agricultural output reported in 2003 might be byapproximately 6% lower than in 2002. The drop in the output of some basic fieldcrops was 27% (wheat), 24% (corn), 30% (potatoes), 47% (tobacco), etc. Thedomestic supply of agricultural products decreased, both in terms of output andassortment, in the area of farming, fruit growing and cattle raising, with adverseeffects on the general price level, cost of living and the Republic's trade balance.

Nevertheless, the domestic market was adequately supplied with agriculturalindustrial products, due to purchased and stored products, transitory stocks ofprimary agricultural products, and to imports. Agricultural production is expectedto improve with the 2004 crops, with respect to the anticipated more favorableweather and other conditions of relevance to agriculture.

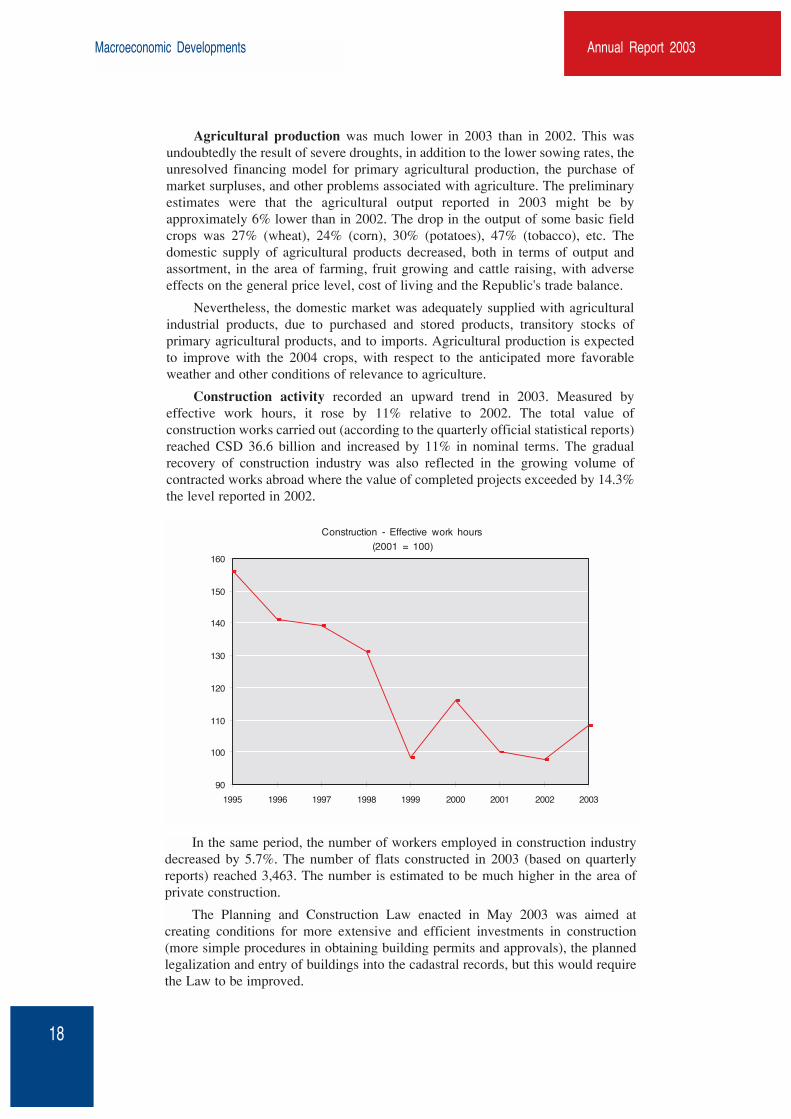

Construction activity recorded an upward trend in 2003. Measured byeffective work hours, it rose by 11% relative to 2002. The total value ofconstruction works carried out (according to the quarterly official statistical reports)reached CSD 36.6 billion and increased by 11% in nominal terms. The gradualrecovery of construction industry was also reflected in the growing volume ofcontracted works abroad where the value of completed projects exceeded by 14.3%the level reported in 2002.

18

Construction - Effective work hours

(2001 = 100)

90

100

110

120

130

140

150

160

1995 1996 1997 1998 1999 2000 2001 2002 2003

In the same period, the number of workers employed in construction industrydecreased by 5.7%. The number of flats constructed in 2003 (based on quarterlyreports) reached 3,463. The number is estimated to be much higher in the area ofprivate construction.

The Planning and Construction Law enacted in May 2003 was aimed atcreating conditions for more extensive and efficient investments in construction(more simple procedures in obtaining building permits and approvals), the plannedlegalization and entry of buildings into the cadastral records, but this would requirethe Law to be improved.

Annual Report 2003 Macroeconomic Developments

19

In the course of 2003, the updating of cadastral records continued in theRepublic of Serbia, with approximately 50% of its territory included in the cadastralrecords until the end of the year. With the expected loan to be provided by the WorldBank, some 98% of Serbia's territory should be covered by the cadastral recordsuntil the end of 2008. This is an important prerequisite for the development ofeconomy, lending, privatization, and foreign investment.

The overall volume of transport services, according to the statistical data, fellby 0.9% in 2003 relative to 2002. Viewed by different transport branches, landtransport recorded a 10.4% decrease including an increase by 5.5% both in railwayand pipeline transport, and a drop by 29% in road transport. The physical volume ofriver transport fell by 30% and, and increased by 14.2% with air transport. The latterwas also the highest growth reported by a transport industry, followed by PTTservices and telecommunications (13.8%). The overall passenger transport fell by2.4%, as opposed to freight transport which rose by 6.5%.

In 2003 considerable allocations were made for the reconstruction anddevelopment of this branch of economy. Investment in the reconstruction of the1,000 km long road network was approximately EUR 300 million, Telecom Serbiainvested EUR 250 million in further telecommunications network development, andthe project "Belgrade Airport - Gate of Serbia", with the total cost of EUR 22million, was launched close to the end of the year.

With respect to the extensive investments planned in the area of transportinfrastructure, the coming period is expected to see a considerably intensifiedtransport activity and improved services, which would support the recovery of theentire economy.

Tourist activity measured by the total number of overnights fell by 7.2% in2003 relative to 2002. The number of overnights reported for foreign guestsincreased by 7.2% against an 8.9% drop with domestic guests. The total number ofarrivals decreased by 9.6%, where the number of arrivals rose by 8.7% with foreignguests, and fell by 12.6% with domestic guests.

Last year's number of incoming tourists was 1.2 million, with 6.7 millionreported overnights. In 2003, the privatization was completed for 52 companiesinvolved in tourist and catering industry. Last year's foreign exchange inflowresulting from tourism reached USD 150 million, or 115% over the level reported in2002. Tourist activity is expected to grow further in the coming period.

Employment

In 2003 the employment rate continued to show downward trends reported inthe previous years, as the economic activity was lower than projected, while the newprivate sector was unable to absorb the redundancies. As estimated by the StatisticsOffice of the Republic of Serbia, the number of the employed was 2,019.8 thousandin late 2003, or 0.9% less than a year ago. The number of the unemployed rose by4.5% in the same period and reached 944.9 thousand.

The estimates show that the gray economy absorbs nearly one third of theemployed, while the total number of unregistered workers is estimated at 600-800thousand. The labor inspectors discovered 48.9 thousand unregistered workers in2003 (relative to 18.6 thousand in 2002). Some three fourths of those discoveredwere duly employed after the inspection.

Annual Report 2003Macroeconomic Developments

20

Employment and Unemployment(Annual average, in thousands)

0

500

1,000

1,500

2,000

2,500

1995 1996 1997 1998 1999 2000 2001 2002 2003

0

500

1,000

1,500

2,000

2,500

Number of employed Number of unemployed

On the other hand, the fictitious employment still poses a major problem. Asreported by the Statistics Office of the Republic of Serbia, over 12% of theemployed were not paid wages in December 2003, which speaks of serious problemsin the area of employment and the state of the economy. Although the number ofnewly employed by the private sector in 2003 exceeded by 40% the level reportedin the previous year, this is apparently far from being sufficient to make up for thedrop in employment resulting from the restructured state- and socially-ownedcompanies.

The new Law on Employment and Unemployment Insurance enacted in Julyprimarily focused on the reform of the employment office, with the emphasis on amore active involvement by the unemployed, subventions for self-employment andemployment of people over 50 years of age, increased fines for any employers withunregistered workers, etc. In addition to subventions, for the purpose of encouragingself-employment, which should be an important generator of employment in thecoming period, the opening of business centers in Serbia was initiated in 2003 toprovide education and professional help for the unemployed interested in launchingtheir own businesses.

However, simpler (and less expensive) procedures for establishing SMEs, aswell as for overcoming obstacles and creating adequate conditions (above all, interms of the legal framework) for foreign direct investments, are still the basicdirections to be focused on by the government in order to enhance employment.

Annual Report 2003 Macroeconomic Developments

21

Domestic Demand and Public Sector

In 2003 the consolidated public expenditures in the Republic of Serbia, aspreliminary reported by the government, accounted for 45.5% of the GDP, with thefiscal deficit equal to 3.5% of the GDP, which is somewhat above the fiscal deficitof the EU countries and other leading industrial western countries. The fiscal deficitreported in the OECD countries generally ranges from 2.5-3.5% of the GDP, i.e.1.5-2.0% in the European Union, approximately 5% in the U.S.A., andapproximately 6% in Japan. Serbia's objective is to have its fiscal deficit reducedbelow 3% of the GDP, as one of the requirements for the association to theEuropean Union in compliance with the Maastricht Criteria.

As reported by the Public Payments Agency, gross allocated revenuesincluding the social insurance revenues reached CSD 555.3 billion in 2003, i.e. innominal terms 9.5% above or in real terms 2% less than in 2002. Allocated taxesand other public revenues accounted for CSD 411.3 billion and increased by 8.7%in nominal terms. Social insurance revenues reached CSD 144.0 billion with thenominal growth of 11.9% relative to 2002.

Further improvements of the fiscal system and new statutory solutions arebeing prepared towards the harmonization with the fiscal systems of the EuropeanUnion. Most of all this refers to the Value Added Tax Law, the fiscalization in tradeand other businesses, and to other regulations to make the fiscal system moreefficient and help suppress illegal trade in goods and services.

Earnings

In spite of the increase reported in the past three years, wages in the republicof Serbia are still lower than in the majority of the European countries, excluding anumber of the East European transition countries. This is the reason why, ifmeasured by the level of wages, Serbia's economy is still much more competitivecompared to most of the countries in Europe. Therefore, labor unit costs arerelatively low and competitive, despite the growth reported in the period 2001-2003.

Wages considerably increased in 2003 both in nominal and real terms. InDecember 2003, the average net wage in the Republic of Serbia was CSD 14,528(EUR 123) and exceeded the level reported in December 2002 by 25.7%, or by16.2% in real terms. Compared to 2002, the average net wage increased by 24.9%and 13.7% in nominal and real terms, respectively. It should be noted, however, thatwages are not regularly paid to every eighth employed worker.

It is apparent that 2003 saw a continued trend of more rapidly growing wagescompared to productivity. However, the percentage of savings relative to the GDPis still low, whereas it should be taken into account that a further increase inhousehold savings and in the overall domestic savings is an important preconditionfor the economic growth in medium and long term. Although production may beencouraged by higher wages or by domestic demand in short term, experience hasshown that in Serbia this mainly results in increasing imports, i.e. in foreign tradedeficit.

The positive effect of the rise in wages is undeniably the enhanced standard ofthe employed, which measured by the minimum consumer basket improved by15.6% in 2003.

Annual Report 2003Macroeconomic Developments

22

Wages paid in 2003 again varied to a higher or lower degree depending both onregions and on industries. Viewed by municipalities, the highest average net wagewas reported in Beocin, and the lowest in Dimitrovgrad. Broken down by industry,the highest wage of CSD 29,272 was earned in tobacco industry, and the lowest ofCSD 2,169 in textile and leather industry.

Average Real Wage Growth in the Republic of Serbia (Index, 2001 = 100)

70

80

90

100

110

120

130

140

1995 1996 1997 1998 1999 2000 2001 2002 2003

Investment Activity

The investment activity in 2003 was somewhat more favorable than in 2002 (inthe area of transport infrastructure, partly in construction industry, etc.), but theestimates are that it is still considerably below the requirements of accelerateddevelopment of Serbia's economy, with respect to the fact that the technical andtechnological lag equals 3-4 technological cycles.

Parallel to the insufficient investment activity, a significant real increase inpersonal and public consumption reported in 2003 was unfavorable in terms ofdevelopment and Serbia's future economic growth. In 2003 the growth of Serbia'seconomy was below the sustainable level and below the level causing employmentto increase and all the internal and external payments to be duly settled.

The estimates are that the total investments in fixed assets ranged around 16%of the GDP, while the sustainable development would require the investment rate toreach or even exceed 20% of the GDP in the shortest possible period. In the mediumand long term, the investment rate should go up by 25% of the GDP, or from timeto time even above that level. It would, therefore, be necessary to increase theinvestment from both domestic and foreign sources, to the extent that they couldreach an annual level of at least USD 3.5-4 billion. Such investment in fixed assetswould provide for the reconstruction and development of transport and economicinfrastructure, and for the recovery of housing and other construction, and ofSerbia's entire real sector. Particular efforts should be made to attract foreigninvestors on permanent basis (FDI, concessionary and BOT investment, jointventures, etc.), as well as to improve the credit and investment rating of the Republicof Serbia, and Serbia and Montenegro which is still at a low level.

Annual Report 2003 Macroeconomic Developments

23

Trade Turnover

The turnover in retail trade in 2003 increased by 12% in real terms relativeto 2002, and by no more than 3% in wholesale trade. Under the circumstances ofprice stability, the real increase in wages and purchasing power resulted in thegrowing turnover compared to the previous year.

Although the value added tax was not imposed in 2003, intensive activitieswere undertaken in the process of introducing electronic cash registers with fiscalmemory. The use of cash registers will have suppressing effects on the grayeconomy, with fiscal obligations and actual retail trade turnover properly recorded,in addition to the supported recovery of the domestic electronic industry and theencouraged cashless payment system, whereby trade will be brought in compliancewith the European standards.

Turnover in Trade and Transport (Index, 2001 = 100)

50

70

90

110

130

1995 1996 1997 1998 1999 2000 2001 2002 2003

Transport

60

80

100

120

140

160

Trade

Freight transport (in km) Physical volume of retail trade

Many socially-owned companies trading in goods and services were privatizedin 2003. This is one of the prerequisites for productive competition, which will inturn result in improved quality of services and in reduced retail prices of goods.

25

Annual Report 2003

ACTIVITIES OF THE NATIONAL BANK

MONETARY POLICY 27EXCHANGE RATE OF THE DINARAND FOREIGN CURRENCY RESERVES 47ISSUE OF BANKNOTES AND COINS 59BALANCE OF PAYMENTS 63EXTERNAL RELATIONS 73BANKING SECTOR AND BANK SUPERVISION 85PAYMENT TRANSACTIONS 101LEGAL AND REGULATORY ACTIVITIES 105INTERNAL AUDIT 109ORGANIZATIONAL AND PERSONNEL CHANGES 113INFORMATION TECHNOLOGY 119 ANNUAL STATEMENT OF ACCOUNT 123

Annual Report 2003

27

MONETARY POLICY

MONETARY POLICY OBJECTIVES AND TARGETS 28MOVEMENTS IN KEY MONETARY AGGREGATES 29

RESERVE MONEY 29MONEY SUPPLY M1 31MONEY SUPPLY M2 31MONEY SUPPLY M3 32MONEY CREATION 33

MONETARY POLICY INSTRUMENTS 35RESERVE REQUIREMENTS 35CREDIT FACILITIES 38DEPOSIT FACILITIES 38INTEREST RATES 39MINIMUM CREDIT RATING REQUIREMENTS 39

CREDITS TO THE GOVERNMENT 40ACTIVITIES IN THE PRIMARY SECURITIES MARKET 41PLANNED NBS ACTIVITIES IN THE MONEY MARKET IN 2004 43ACTIVITIES RELATING TO FROZEN FOREIGN CURRENCYSAVINGS 43

Annual Report 2003Monetary Policy

28

Monetary Policy Objectives and Targets

In 2003 the principal objectives of monetary policy were not significantlydifferent from those prevailing in the two previous years. The key objective againfocused on a further slow-down of inflation and a maintained macroeconomicstability. However, taking into account the assumption that the year of 2003 was tosee a considerably decelerated growth of money demand and that, under theexisting circumstances, the remonetization in economy had largely been completed,the rates of growth of the key monetary aggregates were set at much lower levelsand mainly adjusted to the nominal growth of the GDP. In this context, a strictmonetary policy was pursued in 2003.

With respect to the measures taken within the monetary policy, as well as toother macroeconomic efforts, the 2003 inflation in the Republic of Serbia wasfurther slowed down, with the preserved stability of the financial system. A strictmonetary policy of the NBS and its interventions in the open money and short-termsecurities market, as well as in the domestic foreign exchange market, reduced theinflation to the lowest level in the past nine years of 7.8% measured from Decemberto December. In the same period, core inflation was considerably below the overallinflation and was reported at 5.4% for products and services with prices setaccording to market conditions.

In 2004 the monetary policy will primarily focus on its key objective - pricestability. With respect to encouraging results in the area of disinflation, as well asto economic trends expected in the first quarter of 2004, the NBS reduced thediscount rate to the current 8.5%. The rate of inflation in 2004, as projected, shouldremain below 8.5% at annual level. The NBS will also be actively involved increating systemic and regulatory solutions so as to support increased competitionand improved efficiency of financial intermediation in the banking system.

The estimates are that no considerable changes should be expected in theconditions in which the monetary policy will be implemented in 2004, and that itshould remain firm in order to reach the targets set for this year. In this respect, theforecasts point to a relatively modest growth of key monetary aggregates, at therates which should be slightly above the rate of the nominal GDP growth. For thepurpose of achieving quantitative objectives of monetary policy, the NBS willfurther focus on strengthening and enhancing market instruments of monetaryregulation, which should contribute to the development of the financial market.Improvements should also be seen in open market operations in securities, primarilythrough repurchase transactions in the government securities, along with theintended upgrading of operations in the foreign exchange market aimed at making

Annual Report 2003 Monetary Policy

29

it more liberalized, less segmented and more integrated. This would result in arelatively smaller number of interventions by the NBS and in a greater involvementof banks in foreign exchange market transactions.

In addition to the enhanced monetary policy instruments and the developmentof money and capital market, it is necessary to create an institutional framework forthe insurance of deposits.

Movements in Key Monetary Aggregates

Reserve Money

The overall reserve money increased by approximately 14% in 2003. Theincrease predominantly related to bank foreign currency deposits with the NBS,while the dinar reserve money recorded a marginal increase. Within the latter, adrop was reported with currency in circulation against an increase in bank dinarreserves. Bank reserves reflected an increase in required dinar reserves, and adecrease in the excess reserves of banks. Growing foreign currency bank depositswith the NBS mostly resulted from increased allocations of banks based on foreigncurrency savings, and partly from those based on required foreign currencyreserves. Within the overall reserve money, a slight increase was also reported withdeposits by the local government and other financial organizations.

The reviewed trends in the reserve money creation point to the more significantincrease in the NBS net foreign position, mainly due to the growing foreignexchange reserves which had partly increased with respect to the credit facilitiesprovided by the IMF, though with a neutral effect on the net foreign assets (NFA).The increase in the NFA mostly resulted from the growth in the government andbank foreign currency deposits with the NBS. In 2003, the process of privatizationgenerated considerable foreign currency proceeds for the government whichdeposited the currency with the NBS. Consequently, this resulted in the increase inthe NBS foreign exchange reserves, i.e. the NFA. A portion of foreign currency wassold to the NBS by the government, and it used the dinars resulting from thesetransactions to settle its debts, which in turn caused the reserve money to grow. Theremaining portion of foreign currency still held by the government in its accountswith the NBS has not yet made any effects on the reserve money.

The NBS net domestic assets (NDA) recorded a rather significant decrease in2003, yet nearly half of it related to the rise in the government foreign currencydeposits with the NBS. This had no effects on reserve money, but on the increasein the NFA. The government dinar deposits with the NBS also rose to aconsiderable extent, which in turn resulted in the reduction of reserve money, as theincrease was largely created by transfers of deposits from banks to the NBS.Finally, a decrease in the NDA, as well as in reserve money, partly resulted fromthe reduced NBS credits to the government and other sectors, and lower borrowingsof banks from the NBS. The reduction in credits to the government and othersectors were mainly the result of adjustments applied to such credits after the bookswere finally reconciled for 2003.

Annual Report 2003Monetary Policy

30

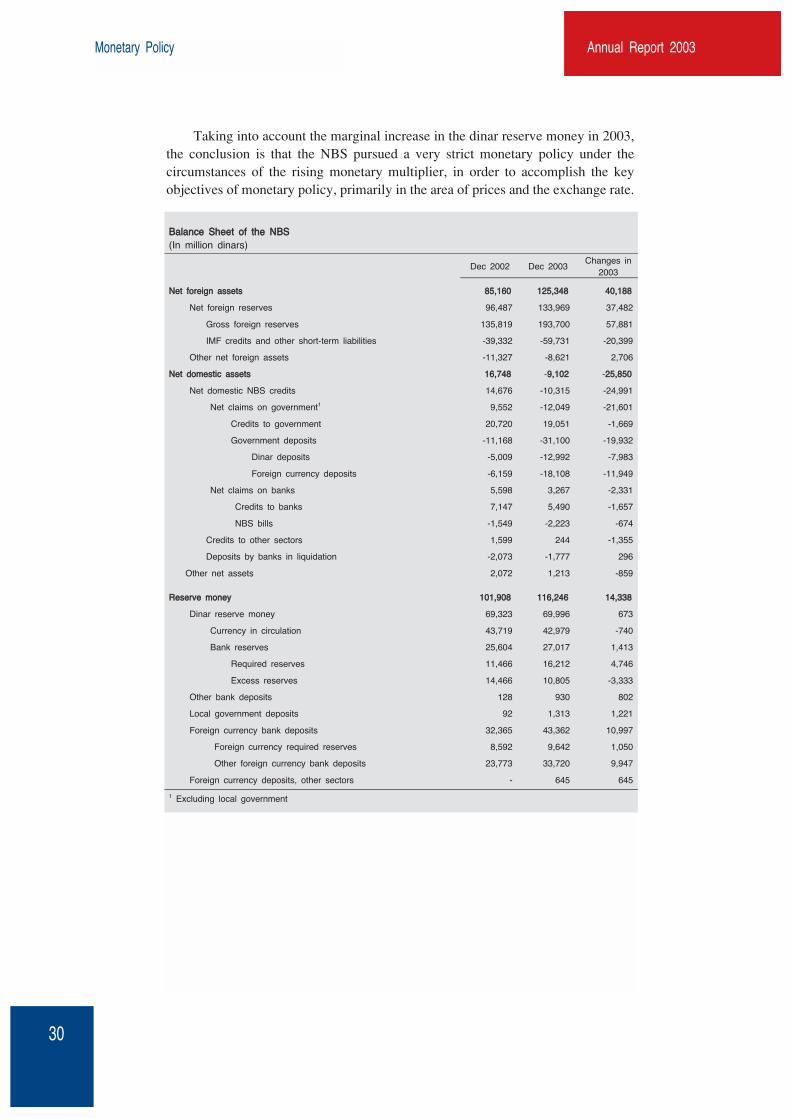

Taking into account the marginal increase in the dinar reserve money in 2003,the conclusion is that the NBS pursued a very strict monetary policy under thecircumstances of the rising monetary multiplier, in order to accomplish the keyobjectives of monetary policy, primarily in the area of prices and the exchange rate.

BBaallaannccee SShheeeett ooff tthhee NNBBSS (In million dinars)

Dec 2002 Dec 2003 Changes in

2003

NNeett ffoorreeiiggnn aasssseettss 8855,,116600 112255,,334488 4400,,118888

Net foreign reserves 96,487 133,969 37,482

Gross foreign reserves 135,819 193,700 57,881

IMF credits and other short-term liabilities -39,332 -59,731 -20,399

Other net foreign assets -11,327 -8,621 2,706

NNeett ddoommeessttiicc aasssseettss 1166,,774488 -99,,110022 -2255,,885500

Net domestic NBS credits 14,676 -10,315 -24,991

Net claims on government1 9,552 -12,049 -21,601

Credits to government 20,720 19,051 -1,669

Government deposits -11,168 -31,100 -19,932

Dinar deposits -5,009 -12,992 -7,983

Foreign currency deposits -6,159 -18,108 -11,949

Net claims on banks 5,598 3,267 -2,331

Credits to banks 7,147 5,490 -1,657

NBS bills -1,549 -2,223 -674

Credits to other sectors 1,599 244 -1,355

Deposits by banks in liquidation -2,073 -1,777 296

Other net assets 2,072 1,213 -859

RReesseerrvvee mmoonneeyy 110011,,990088 111166,,224466 1144,,333388

Dinar reserve money 69,323 69,996 673

Currency in circulation 43,719 42,979 -740

Bank reserves 25,604 27,017 1,413

Required reserves 11,466 16,212 4,746

Excess reserves 14,466 10,805 -3,333

Other bank deposits 128 930 802

Local government deposits 92 1,313 1,221

Foreign currency bank deposits 32,365 43,362 10,997

Foreign currency required reserves 8,592 9,642 1,050

Other foreign currency bank deposits 23,773 33,720 9,947

Foreign currency deposits, other sectors - 645 645

1 Excluding local government

Annual Report 2003 Monetary Policy

31

Money Supply M1

The increase in the money supply M1 continued in 2003, though it was muchless intensive than in the previous years with respect to the more moderate growthof money demand. M1 rose by CSD 11,216 million or 11.9% relative to the end of2002, and reached CSD 105,212 million by the end of December or EUR 1,540million at the rate of exchange applicable close to the end of 2003. Deflated by theretail price index, M1 in real terms rose by 3.8% relative to 2002 (40.5%).

The coverage of the money supply by the NBS foreign exchange reserves was184.4% at the end of 2003 and significantly increased in comparison to the end of2002, as the foreign exchange reserves rose more rapidly than M1.

Money Supply (M1)(Cumulative growth rates)

90

95

100

105

110

115

XII I II III IV V VI 2003

VII VIII IX X XI XII

90

95

100

105

110

115

Retail prices Money supply (M1) Real money supply

Certain changes were recorded in terms of the money supply composition.Currency in circulation decreased against the increase in the deposit money, withconsequently reduced percentage of currency in circulation within the overallmoney supply, from 46.5% to 40.8% at the end of 2002 and 2003, respectively.

Broken down by sectors, the highest increase by CSD 9,195 million or 28.1%was reported in the real sector, as opposed to the much more moderate growth inother sectors and in households. In terms of available monetary assets, real sectorwas in a relatively better position in 2003.

Money Supply M2

The monetary aggregate M2, which in addition to M1 includes time and otherdinar deposits and securities, increased by CSD 13,663 million or 12.3% in 2003,and reached CSD 124,824 million at the end of the year.

A slightly higher growth rate reported in M2 relative to M1 was the result of amore rapid increase in savings and time dinar deposits with commercial banks.

Annual Report 2003Monetary Policy

Money Supply M3

The monetary aggregate M3 stood at CSD 244,811 million at the end of 2003,and increased by CSD 52,213 million or 27,1% compared to December 2002. Aconsiderably higher growth of M3 relative to M2 and M1 resulted from the surgingforeign currency deposits with commercial banks, primarily household foreigncurrency savings, although the increase was partly created by variations in theexchange rate of the dinar. Viewed by sectors, households recorded the highestnominal growth within M3. Monetary assets held by this sector rose by CSD 25,032or 24.8% relative to December 2002, mostly due to the growing new foreigncurrency savings, while the real sector recorded an increase by CSD 24,219 millionor 31.7%.

32

NBS Forex Reserves(Cumulative changes in million U.S. dollars)

-200

200

600

1,000

1,400

1,800

2,200

2,600

3,000

3,400

XII2002

I II III IV V VI2003

VII VIII IX X XI XII

-200

200

600

1,000

1,400

1,800

2,200

2,600

3,000

3,400

Forex reserve inflow

Sales in the Interbank foreign exchange market

Forex reserves

Money Supply Coverage by Total Forex Reserves(In million dinars, end of period)

020,00040,00060,00080,000

100,000120,000140,000160,000180,000200,000220,000240,000260,000

XII2002

I II III IV V VI 2003

VII VIII IX X XI XII

Money supply Total forex reserves

Annual Report 2003 Monetary Policy

33

As for the M3 composition, at the end of the year M1 accounted for 43.0%,time dinar deposits for 8.0%, and foreign currency deposits for 49.0%. Thecoverage of M3 by the NBS foreign exchange reserves was reported at 79.2% at theend of 2003 (against 69.8% at the end of 2002).

Money Creation

The increase in the money supply M1 reported in 2003 was mostly influencedby bank corporate and retail lending, government spending of foreign currencydeposits resulting from the privatization process and as for M3, by a high growth ofdeposits with banks. However, based on the information reported in financialstatements it appears that the major portion of the money supply was created as theresult of the increased NFA of the banking sector, primarily the growth of the NBSforeign exchange reserves. On the other hand, if the movements in the moneysupply creation are analyzed in more detail, the conclusion is that the increase in theNBS foreign exchange reserves, with the effects based on the IMF credits excluded,resulted from the growing government foreign currency deposits with the NBS andforeign currency deposits with banks. Movements in the reserve money creationshow that part of the government foreign currency deposits spent by it in 2003, hadan increasing effect on foreign exchange reserves and the money supply, while theother part still held in accounts with the NBS had no effects on the money supply.

Moreover, a high increase in foreign currency deposits with banks resulted inthe growing foreign exchange reserves. If the effects based on changes in thegovernment foreign currency deposits and those held with banks are excluded fromthe NFA, it is apparent that withdrawals were reported as the result of direct foreigntransactions of the banking sector, which may be related to much higherinternational payments associated with relatively high imports compared to theforeign exchange inflow based on exports.

The NDA of the banking sector rose by CSD 14,582 million. The claims ongovernment fell by CSD 10,187 million, as opposed to the increase in bank lending,mostly to corporate and retail borrowers. The reduced net claims on the governmentpartly resulted from the decrease in loans provided to the government, and to alarger extent from growing government deposits with the banking sector. On theother hand, banks bought government bonds based on frozen foreign currencysavings and created money amounting to CSD 3,308 million.

Corporate and retail loans rose by CSD 16,124 million. However, their realgrowth and the resulting money creation were much more extensive, since the loansconsiderably decreased against the reported provisions. As provided by the newChart of Accounts for banks and with the applicable International AccountingStandards, at the end of 2003 banks were required to create provisions for theirloans and investments to the debit of previously allocated provisions underliabilities and, consequently, reported considerably reduced net receivables basedon disbursed loans. The net amount of dinar corporate loans reported by banksincreased by CSD 17,379 million and, with the provisions excluded, the increaseamounted to CSD 29,799 million. In addition to the growth of CSD 12,623 millionreported with retail lending, the real increase in the aggregate dinar corporate and

Annual Report 2003Monetary Policy

34

retail lending reached CSD 42,422 million or 48%. Net foreign currency loans fellby CSD 13,951 million, mainly due to considerably higher provisions.

Furthermore, the reported money creation based on other net assets of thebanking sector stood at CSD 5,337 million, but it largely resulted from the reducedprovisions under liabilities to which subsequently allocated loan provisions andmajor losses of banks were charged.

MMoonneettaarryy SSuurrvveeyy (In million dinars)

Dec 2002 Dec 2003 Changes in

2003

NNeett ffoorreeiiggnn aasssseettss 111144,,664422 115522,,227733 3377,,663311

NBS net foreign assets 85,160 125,348 40,188

Bank net foreign assets 29,482 26,925 -2,557

NNeett ddoommeessttiicc aasssseettss ooff bbaannkkiinngg sseeccttoorr 7777,,995566 9922,,553388 1144,,558822

Net domestic credits 151,415 160,660 9,245

Net claims on government -7,761 -17,948 -10,187

Credits to government 23,580 21,846 -1,734

Dinar 22,904 21,726 -1,178

Foreign currency 676 120 -556

Government deposits -31,341 -39,794 -8,453

Dinar -15,508 -17,830 -2,322

Foreign currency -15,833 -21,964 -6,131

Credits to other resident sectors 157,587 173,711 16,124

Credits to other financial organizations 632 392 -240

Credits to real sector 136,421 139,849 3,428

Dinar 71,532 88,911 17,379

Foreign currency 64,889 50,938 -13,951

Credits to households 16,020 28,643 12,623

Credits to local government 593 1,403 810

Credits to other sectors 3,921 3,424 -497

Purchased frozen foreign currency savings bonds 1,589 4,897 3,308

Other net assets -73,459 -68,122 5,337

MMoonneeyy ssuuppppllyy MM33 119922,,559988 224444,,881111 5522,,221133

Money supply M2 111,161 124,824 13,663

Money supply M1 93,996 105,212 11,216

Currency in circulation 43,719 42,979 -740

Transaction deposits 50,277 62,233 11,956

Dinars savings and time deposits 17,165 19,612 2,447

Foreign currency deposits 81,437 119,987 38,550

Annual Report 2003 Monetary Policy

35

Monetary Policy Instruments

In 2003 the NBS continued the process of improving the mechanisms ofmonetary regulation commenced in 2001. The new Law on the National Bank ofSerbia enacted in July 2003 explicitly restricted the application of direct monetaryregulation methods. Furthermore, the Law does not allow the government andbanks to permanently borrow from the NBS, including the precisely definedrestrictions on short-term borrowing for the purpose of resolving liquidityproblems.

In the course of 2003, the NBS further pursued applying the bank requiredreserve model, whereby the required reserves are calculated against the dinar andforeign currency deposits, in addition to the average daily balance of allocatedreserve maintained in the accounting period. In line with movements in the liquidityof banks, several adjustments were applied to the required reserve ratio in thecourse of the year.

With respect to its commitment to rely on indirect instruments of monetaryregulation in implementing the objectives of monetary policy, at the beginning ofthe last quarter the NBS started trading its bills in independently organized andcompleted auctions using its auction platform - the RTGS technologicalinfrastructure. The new electronic trading system, as expected, made the purchaseof the NBS bills more attractive to banks.

With the decision on credit facilities issued in early 2003, the NBS created anadditional option made available to banks providing for sufficient liquidity in theirpayment transactions performed in compliance with the law. The use of depositfacilities created one more option for banks to employ their excess liquidity.

Credit rating requirements applicable to banks were tightened in 2003, as wellas the sanctions in case of non-compliance. The application of this policy resultedin the improved financial discipline of banks and most of them complied with theminimum credit rating requirements.

With the new Law on Payment Transactions enacted in early 2003, paymentoperations were shifted to commercial banks. The process was effectivelycompleted and the initial difficulties were resolved as they occurred. Banks hadconsiderable liquid assets available in the first months to facilitate paymenttransactions.

In early 2003, in line with the inflation trends, the NBS discount rate had beenreduced from 9.5% to 9% per annum, and remained unchanged until the end of theyear.

Reserve Requirements

In 2003 the NBS pursued an active policy relating to bank required reservesand the ratio was subject to relatively frequent changes, depending on the liquidityof banks. The required reserve model was further applied whereby the calculationis based on the dinar and foreign currency deposits, and the average daily balance

Annual Report 2003Monetary Policy

of allocated reserves maintained within the accounting period from the 11th day ofthe current month until the 10th day of the following month.

In the first months of the year, in January and February, the required reserveratio was 20%. However, with respect to the considerably improved liquidity ofbanks, the NBS increased the required reserve ratio from 20% to 23% on 10 March.The measure was aimed at neutralizing the effects of the excess liquidity of banksresulting from significantly increased government deposits. In the meantime, theNBS and the Republic of Serbia agreed on the planned withdrawal of governmentdeposits from banks and their transfer to deposits with the NBS, whichconsequently resulted in a further reduction of the required reserve ratio to 22% on10 April, and to 20% on 10 May.

As in early July the liquidity of banks fell below the average level reported inthe first six months of 2003, for the purpose of improving the banks' liquidity andlending potential, the NBS reduced the required reserve ratio from 20% to 18% andkept it unchanged until the end of the year.

36

With respect to allocated dinar required reserves, there were two distinctiveperiods: January-June when the average required reserves allocated by banks werebelow the calculated level, and July-December when the average allocationsexceeded the calculated required reserves.

In the first six months, due to the liquidity problems faced by some banks, thepercentage of allocated dinar required reserves ranged from 89.3% to 99.8%relative to the calculated level. With the improved liquidity of banks in the secondhalf of the year, the average dinar required reserves allocated by banks exceeded thecalculated level.

On the other hand, banks faced no problem with foreign exchange requiredreserves, and the average allocations on account of foreign exchange requiredreserves were above the calculated level throughout the year (as shown in RequiredReserves above).

RReeqquuiirreedd RReesseerrvveess 1100 JJaannuuaarryy 22000033 - 1100 JJaannuuaarryy 22000044 (In million dinars)

Dinar required reserves Foreign exchange required reserves Accounting

period Base Calculated Allocated average

Difference (3-2)

Base Calculated Allocated average

Difference (7-6)

Difference (8+4)

1 2 3 4 5 6 7 8 9 11/1 � 10/2

80,617.2 16,123.4 14,869.8 -1,253.6 36,883.5 7,376.7 8,528.0 1,151.3 -102.3 11/2 � 10/3

85,777.4 17,155.5 15,722.6 -1,432.9 37,366.2 7,473.2 7,757.7 284.5 -1,148.4 11/3 � 10/4

90,860.4 20,897.9 18,669.2 -2,228.7 38,384.9 8,828.5 8,877.6 49.1 -2,179.6 11/4 � 10/5

83,227.2 18,310.0 17,584.8 -725.2 39,278.7 8,641.3 8,693.3 52.0 -673.2 11/5 � 10/6

83,497.2 16,699.4 16,662.0 -37.4 39,955.3 7,991.1 8,123.7 132.6 95.2 11/6 � 10/7

83,199.2 16,639.8 16,725.9 86.1 40,980.7 8,196.1 8,322.9 126.8 212.9 11/7 - 10/8

81,885.8 14,739.4 14,886.3 146.9 42,694.2 7,685.0 7,809.0 124.0 270.9 11/8 - 10/9

81,183.6 14,613.1 14,733.2 120.1 42,338.5 7,620.9 7,699.2 78.3 198.4 11/9 - 10/10

84,529.7 15,215.3 15,492.8 277.5 43,730.6 7,871.5 7,939.5 68.0 345.5 11/10 - 10/11

86,601.6 15,588.3 15,597.6 9.3. 45,440.1 8,179.2 8,219.8 40.6 49.9 11/11 - 10/12

87,423.4 15,736.2 15,784.5 48.3 50,233.7 9,042.1 9,047.3 5.2 53.5 11/12/2003/- - 10/1/2004 87,011.1 15,662.0 16,389.2 727.2 52,791.3 9,502.4 9,561.8 59.4 786.6

Annual Report 2003 Monetary Policy

37

In 2004 the NBS intends to modify the required reserve instrument to theeffect that:

• Giro accounts of banks and their required reserve accounts arecombined

Pursuant to the applicable Decision on Required Reserves Held with theNational Bank of Serbia, banks are obliged to have their required reserves allocatedto a special account. With respect to the applied method of average required reserveallocations, and the fact that the funds are available to banks to be freely used withinthe accounting period, depending on the level of their liquidity, it is believed thatthere is no need for dinar required reserves to be kept in special accounts. It is,therefore, planned to have these funds and those maintained on bank giro accountscombined, thus avoiding unnecessary orders for the purpose of transfers fromrequired reserve accounts to giro accounts and vice versa.

The previous obligation to have dinar required reserves allocated to specialaccounts had been provided by the Law on the National Bank of Yugoslavia, whileit was not specified by the new Law on the National Bank of Serbia.

• Foreign exchange required reserves are allocated in the euros and theU.S. dollars

As provided by the Decision, foreign exchange required reserves may beallocated by banks in different currencies. In 2003, the average composition ofallocated foreign exchange reserves was as follows: EUR 56.0%; JPY 25.9%; USD13.8%; and CHF 4.3%.

Calculated and Allocated Dinar and Foreign Exchange Required Reserves from 10 january 2003 do 10 january 2004

(In million dinars)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,000

11/1 -

- 10/2

11/2 -

- 10/3

11/3 -

- 10/4

11/4 -

- 10/5

11/5 -

- 10/6

11/6 -

- 10/7

11/7 -

- 10/8

11/8 -

- 10/9

11/9 -

- 10/10

11/10 -

- 10/11

11/11 -

- 10/12

11/12 -

- 10/1

Calculated dinar RRs

Average allocated dinar RRs

Calculated foreign exchange RRs

Average allocated foreign exchange RRs

Monetary Policy

38

Annual Report 2002

As revealed by estimates and analyses conducted by the NBS, there is no needto have foreign exchange required reserves allocated in several different currencies.A new decision has consequently been issued for foreign exchange requiredreserves to be allocated only in the euros and the U.S. dollars, with respect to highyields generated by these currencies compared to the Swiss franc and the Japaneseyen.

Credit Facilities

After the new Law on Payment Transactions became effective on 1 January2003, payment operations were taken over by commercial banks. With adequatelymaintained current liquidity being the prerequisite for the normal functioning of thepayment system, by its decision on credit facilities issued at the beginning of theyear the NBS, as an active participant in the payment system, created an additionaloption available to banks for the purpose of providing sufficient liquidity for theirpayment transactions.

Credit facilities are provided through allowed bank account overdrafts, i.e. asort of intraday facilities available to banks within the time needed to complete theirpayment transactions.

Overdrafts are interest-free and any defaults in repayment of used funds aresecured by loans for the purpose of daily liquidity against the pledged NBS bills.

With respect to the relatively adequate liquidity in 2003, loans for the purposeof daily liquidity were used by no more than three banks. The maximum borrowingamounted to CSD 400 million.

The applicable credit facility model is subject to the collateral solely in theform of the NBS bills and it functions as a standard loan approved by the NBS.

The credit facility model is planned to be modified next year to provide for:

• Government bills to be included as collateral

With the government bills included as collateral, the NBS would contribute tothe development of securities market which is one of its priorities, on the one hand,and it would additionally encourage the purchase of the government bills, on theother.

• Less complex proceduresIn order to make the current procedures simpler and reduce the time needed for

all the formal and legal issues relating to collateralized loans, the idea is to use thesecurities trading electronic platform for accepting requests of banks and reduce thetime required to obtain liquid funds.

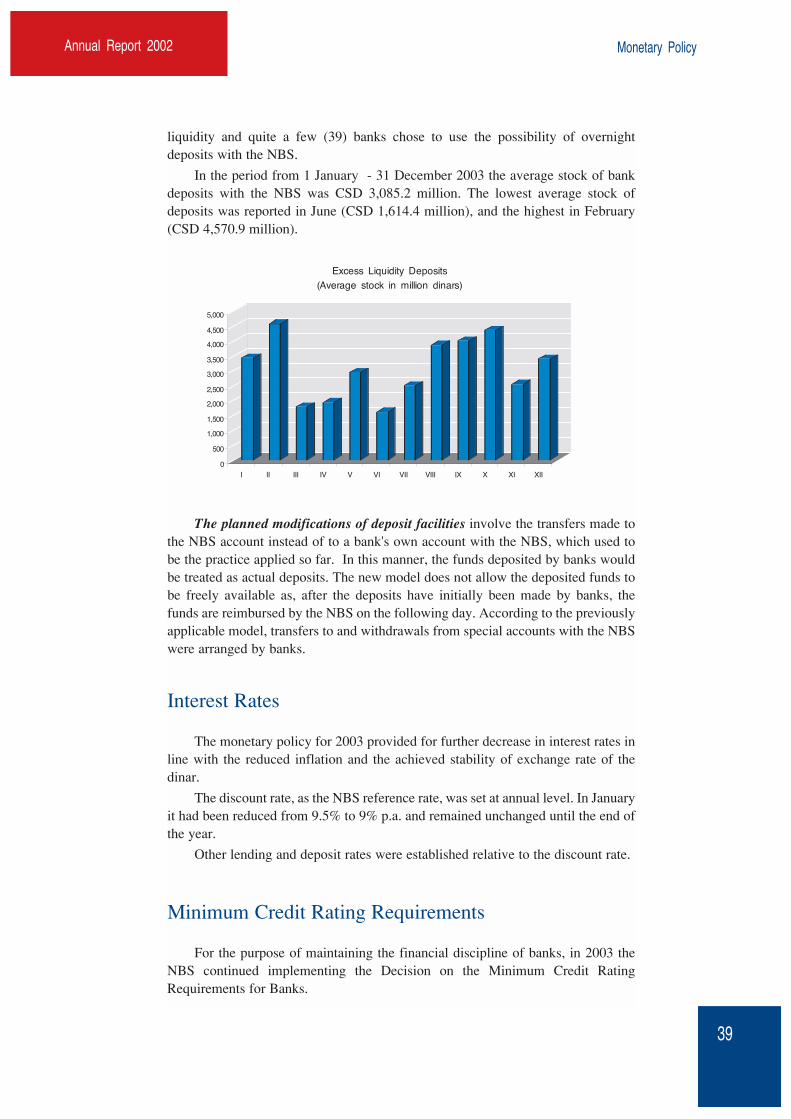

Deposit Facilities

With deposit facilities applicable throughout 2003, banks could place anyexcess liquidity in deposits with the NBS against the respective interest paid.

These facilities created an additional option for banks to employ any excess

39

liquidity and quite a few (39) banks chose to use the possibility of overnightdeposits with the NBS.

In the period from 1 January - 31 December 2003 the average stock of bankdeposits with the NBS was CSD 3,085.2 million. The lowest average stock ofdeposits was reported in June (CSD 1,614.4 million), and the highest in February(CSD 4,570.9 million).

The planned modifications of deposit facilities involve the transfers made tothe NBS account instead of to a bank's own account with the NBS, which used tobe the practice applied so far. In this manner, the funds deposited by banks wouldbe treated as actual deposits. The new model does not allow the deposited funds tobe freely available as, after the deposits have initially been made by banks, thefunds are reimbursed by the NBS on the following day. According to the previouslyapplicable model, transfers to and withdrawals from special accounts with the NBSwere arranged by banks.

Interest Rates

The monetary policy for 2003 provided for further decrease in interest rates inline with the reduced inflation and the achieved stability of exchange rate of thedinar.

The discount rate, as the NBS reference rate, was set at annual level. In Januaryit had been reduced from 9.5% to 9% p.a. and remained unchanged until the end ofthe year.

Other lending and deposit rates were established relative to the discount rate.

Minimum Credit Rating Requirements

For the purpose of maintaining the financial discipline of banks, in 2003 theNBS continued implementing the Decision on the Minimum Credit RatingRequirements for Banks.

Annual Report 2002 Monetary Policy

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

I II III IV V VI VII VIII IX X XI XII

Excess Liquidity Deposits(Average stock in million dinars)

Annual Report 2003Monetary Policy

40

The Decision effective as of 1 January 2003 was adjusted to the provisions ofthe Law on the Settlement of Public Debt of the FR of Yugoslavia Arising fromPersonal Foreign Currency Savings and the Law on Payment Transactions. As thepublic debt of the FR of Yugoslavia based on personal foreign currency savings hadbecome the debt of the Republic of Serbia and the Republic of Montenegro, bankswere no longer required to allocate1 15% of the debt resulting from personal foreigncurrency savings and, consequently, any outstanding liabilities of a bank under thepublic debt could not be treated as its non-compliance with the minimum creditrating requirements. Moreover, with payment transactions shifted to banks, bankswere made more responsible for their liquidity and it was no longer necessary toapply the provision whereby a criterion for non-compliance with the minimumcredit rating requirements related to a bank's failure to act upon orders received2 .

Furthermore, in early March one more credit rating requirement was tightened- the average daily balance of the allocated dinar and foreign exchange reserves inthe previous accounting period was set at 100% of the calculated required reserves(previously no less than 80%). However, as the non-allocation of required reserves(equal to the calculated required reserves) was provided by interest policies, theconclusion reached in the very next accounting period was that the strict creditrating requirement might be modified. Therefore, the obligation relating to themaintained average of allocated required reserves was reduced to 90% as of 11April.

According to the Decision on the Minimum Credit Rating Requirements, in theperiod of non-compliance with the minimum credit rating requirements, banks arenot allowed to use any loans from or make any investments with the NBS other thanthose for the purpose of daily liquidity, or to buy the NBS bills in the primary marketor foreign exchange from the NBS, or make any excess liquidity deposits with theNBS. Such rigid sanctions had a positive impact on the financial discipline of banksand most of them complied with the minimum credit rating requirements throughoutthe year.

Continual non-compliance with the credit rating requirements in 2003 mostlyrelated to the banks in the process of rehabilitation, and resulted from overdue debtsto the NBS and the average required reserve allocations below the level provided bythe Decision.

The NBS will continue implementing the Decision in the coming period,including the intended technical adjustments to facilitate its application in practice.

Credits to the Government

To bridge the gap between the revenues and expenditures within the budget ofthe Republic of Serbia, a short-term overdraft facility was made available by theNBS to the budget of the Republic in the period from January to November 2003.The average amount under the short-term credit used by the Republic in 2003 wasabout CSD 2 billion dinars and was duly repaid as agreed.

1These liabilities were replaced by the obligation to issue shares to be held by the member republics.2According to the Decision, the amount of any orders received and not acted upon in the previous daycould not exceed 5% of the aggregate amount of orders issued to the debit of a bank's giro account.

Annual Report 2003 Monetary Policy

41

As for the payments due to the NBS from the government and other directborrowers, which were associated with servicing problems in the past, the NBScontinued to seek solutions for them to be settled. In this context, the consideredpossibilities of long-term settlement included the payments due from the Republicof Serbia, the FR of Yugoslavia, the Directorate for Commodity Reserves of theRepublic of Serbia, and the Public Enterprise Electric Power Supply of Serbia.

As the long-term settlement was not operationally feasible until the end of2003, the NBS started applying short-term debt postponement. Until 30 June 2004debt postponements included the payments due from the Republic of Serbia basedon short-term securities (CSD 17 billion) and from Electric Power Supply of Serbia(CSD 1.9 billion).

Taking into account the total amount of these debts, their scheduled maturities,the time in which they were created, the modified legal status of some of theborrowers, as well as the servicing problems, the NBS plans to cooperate with therelevant authorities of the Republic in 2004 in preparing the adequate systemicsolutions so that the debts may be settled.

Activities in the Primary Securities Market

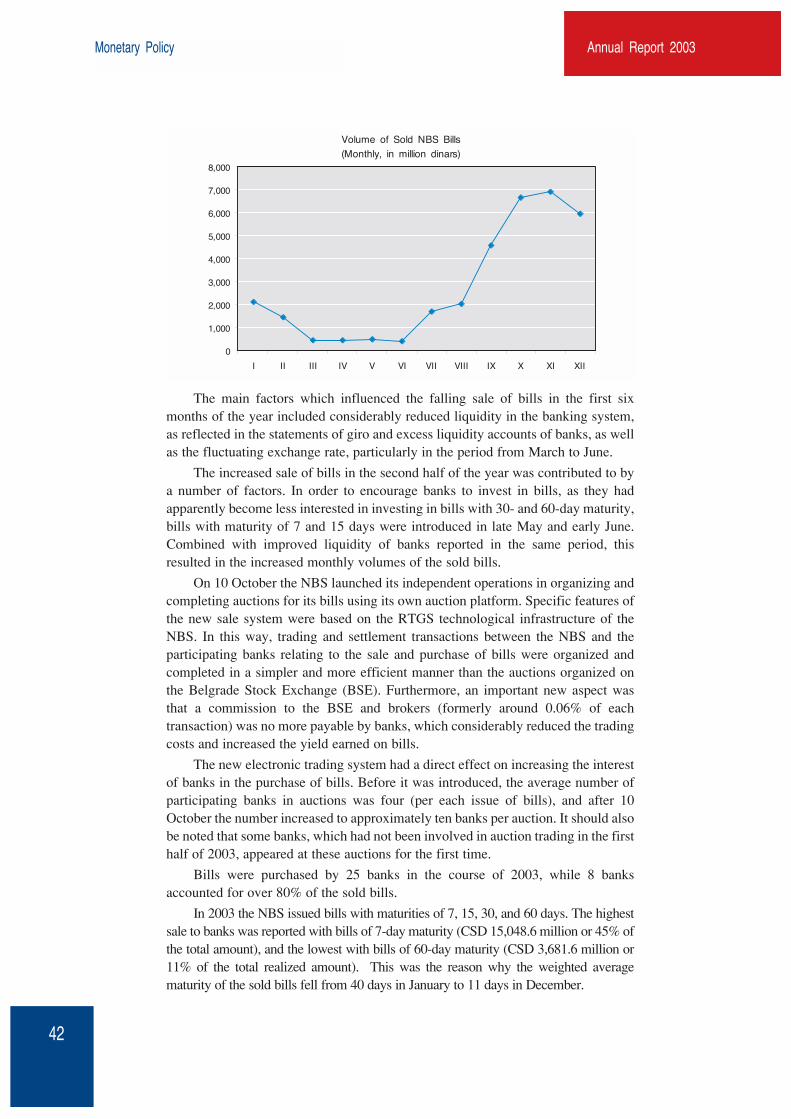

Similar to previous years, for the purpose of reducing the excess liquidity ofbanks in 2003, the form in which the NBS basically intervened in the money marketinvolved the auction sale of its own short-term securities - the NBS bills.

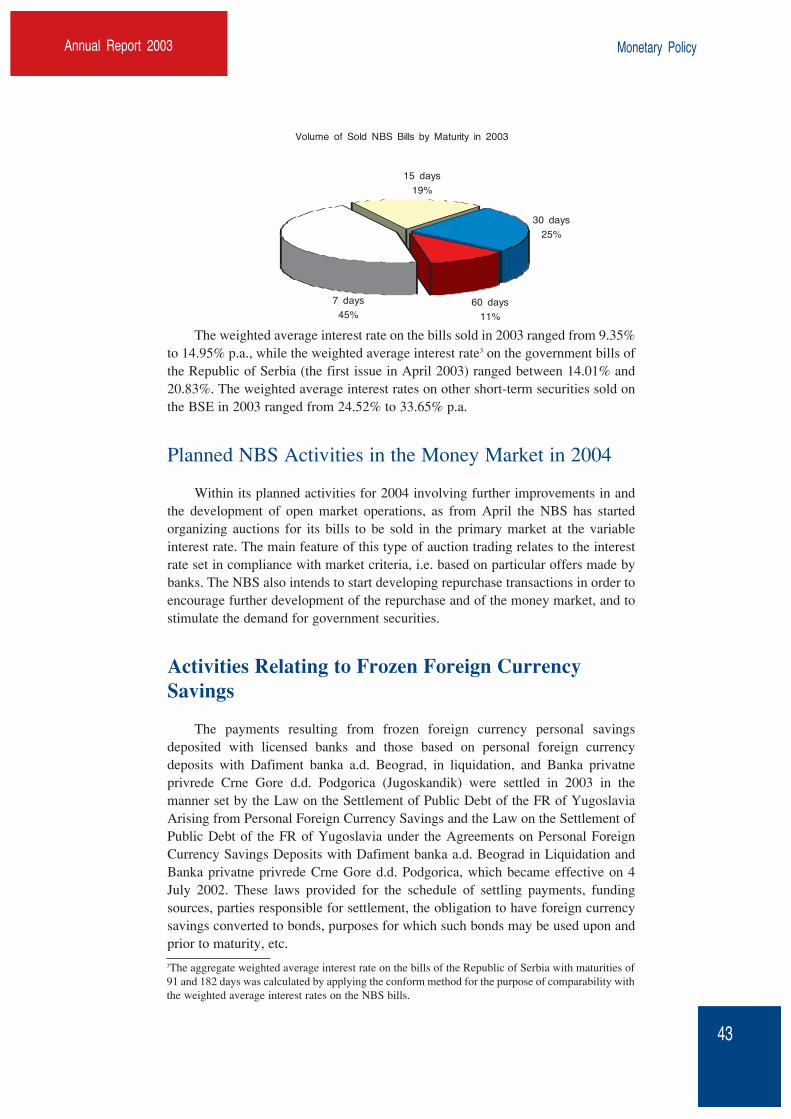

In 2003, the NBS organized 231 auctions for its bills where the discountedamount of sold bills reached CSD 33,354.1 million out of the total issued billsamounting to CSD 88,200.0 million. The NBS also issued bills with maturity of 7,15, 30 and 60 days. In addition to regular auctions, a number of special auctionswere organized, particularly in the third and fourth quarters. The effort made byspecial auctions was aimed at reducing the purchase of foreign currency in theInterbank Foreign Exchange Market.

In the period from January to July, the sale of the NBS bills was continuallyfalling, from CSD 2,123.7 million in January to CSD 414.4 million in July. In theperiod from March to July, monthly volumes of the sold bills ranged between CSD414 and 502 million. The lowest amount in the portfolios of banks was reported on16 and 17 July, i.e. no more than CSD 392.9 million, or CSD 1,155.9 million lessthan on 31 December 2002.

Contrary to the first six months, an increase in the sold bills was reported in thesecond half of the year, particularly in the last quarter. The third quarter alreadypointed to the rising volume of sale, from CSD 1,717.9 million in July to CSD4,578.7 million in September. The highest monthly figures in 2003 were reportedin the last quarter. Banks became increasingly interested in bills in October, whenthe sold bills reached CSD 6,671.5 million and, particularly in November, with therecord amount of CSD 6,918.8 million, since the NBS started selling its bills inNovember 2000. With such favorable trends, bills reported in portfolio of banksstood at CSD 4,981.4 million on 7 November which was the highest amountreported in 2003. The sale declined to a certain extent in December (CSD 5,965.6million) relative to October and November, and the balance of bills in portfolios ofbanks was CSD 2,223.3 million on 31 December 2003.

Annual Report 2003Monetary Policy

The main factors which influenced the falling sale of bills in the first sixmonths of the year included considerably reduced liquidity in the banking system,as reflected in the statements of giro and excess liquidity accounts of banks, as wellas the fluctuating exchange rate, particularly in the period from March to June.