annual report - royal ihc · 2017-04-13 · royal ihc | annual report 2015 3 key figures 2011-2015...

TRANSCRIPT

Annual Report2015

Royal IHC | Annual Report 2015 3

Key figures 2011-2015

New orders 826.7 582.9 1,767.1 678.7 1,056.9Revenue 1,161.3 1,214.7 984.5 894.9 1,049.8Order portfolio as at 31 December 834.7 1,165.5 1,743.1 963.6 1,178.8Profit for the period 27.9 124.0 56.3 36.9 103.2Profit for the period attributable to owners of the Company 29.1 123.0 54.4 34.7 100.9EBITDA 84.8 191.9 108.0 83.9 161.4Group equity 305.4 295.7 315.4 370.4 371.6Total assets 1,100.2 1,189.3 1,083.8 832.3 934.5Group equity/total assets 28% 25% 29% 45% 40%Group equity/capital employed 64% 60% 65% 76% 82%Average number of employees (head count) 3,434 3,263 3,224 3,239 3,109

Amounts in millions of euros, unless stated otherwise 2015 2014 2013 2012 2011

Contents 3 Company profile 3 Key figures 2011-2015 4 Report of the Supervisory Board6 Report of the Board of Management12 Abbreviated financial information 201515 Notes to the abbreviated financial information18 Independent auditor’s report

Supervisory BoardJ.C. ten Cate, ChairmanC.J. de BruinC. KorevaarB.H.C. de Bruin-van EijckJ.H.N.M. van der Horst

Board of ManagementA. Roelse, CEO D.A.A.J.A.G. Vander Heyde, CFOA.M. van Noort, COO

DirectorsA.A. den BoonM.P. HakkertA. KlijnsoonW.J. KruijtJ.A. Westerbeek

© 2016, IHC Merwede Holding B.V.

Company profile

Royal IHC: innovative solutions for maritime service providers

In an ever-changing political and economic landscape, Royal IHC enables its customers to execute complex projects from sea level to ocean floor in the most challenging of maritime environments. We are a reliable supplier of innovative and efficient equipment, vessels and services for the offshore, dredging and wet mining markets.

With a history steeped in Dutch shipbuilding since the mid-17th Century, we have in-depth knowledge and expertise of engineering and manufacturing high-performance integrated vessels and equipment, and providing sustainable services. From our head office in The Netherlands and with 3,000 employees working from sites and offices on a global basis, we are able to ensure a local presence and support on every continent.

Dredging operators, oil and gas corporations, offshore contractors, mining houses and government authorities all over the world benefit from IHC’s high-quality solutions and services. With our commitment to technological innovation, in which sustainability and safety are key, we strive to continuously meet the specific needs of each customer in a rapidly evolving world.

All shares of IHC Merwede Holding B.V. are held by IHC B.V. Shareholders of IHC B.V. are as follows: Parkland N.V.: 62.10%, Stichting Administratiekantoor Management en Personeel IHC: 27.89%, Rabo Capital B.V.: 10.01%. Shareholders are committed to IHC in the long-term.

4 Royal IHC | Annual Report 2015 Royal IHC | Annual Report 2015 5

Report of the Supervisory Board

Introduction

As expected, we witnessed a perfect storm in 2015. Falling crude oil prices and China’s economic rebalancing with lower demand for minerals and energy, together with regional instability in the Middle East, led to a hard landing for the BRIC and other upcoming economies. In Europe, growth remains fragile in spite of the ECB quantitative easing policy. This economic climate had a dramatic effect on the entire offshore market. Capital expenditure (capex) programmes were stopped, and operational cost-cutting programmes started up, which had a direct impact on the demand for new equipment and services coming into the market. As a result of the interconnection between the offshore and dredging markets, the latter also saw the number of projects coming to the market drying up.

Being hit in both of its core markets resulted in an order intake of €827 million for Royal IHC in 2015. Order backlog decreased from €1,166 million in 2014 to €835 million in 2015.

The continuing depressed outlook for the offshore and dredging markets, together with a decreasing number of orders, led to the acceleration of the IHC 2020 strategy, which was announced in mid-June 2015. All shipbuilding activities will be concentrated in Kinderdijk and Krimpen aan den IJssel, while IHC IQIP will move to Sliedrecht. The lower order pipeline and declining number of new orders necessitated an increase in efficiency and a readjustment of building capacity in The Netherlands – with the announcement of 487 job losses.

In October 2015, Mr. Alexander van Noort was appointed COO, completing the Board of Management.

Supervision

The Supervisory Board convened seven times (five plenary and two by conference call), with the Board of Management in attendance. In August 2015, a two-day session of the Supervisory Board meeting was entirely dedicated to in-depth, constructive discussions regarding the strategy and downsizing of the Group.

In advance of regular board meetings, the Supervisory Board also met five times without the Board of Management to cover topics such as remuneration, management succession and internal auditing. The remuneration committee and the audit committee each met two times.

The Supervisory Board performed an internal evaluation, as it has been functioning in the same composition since the shareholder change in 2013. The main conclusions shared by all members of the Board are that it is a stable composition and that internal collaboration is considered positive. The same is the case for collaboration with the Board of Directors, as well as the sharing of information.

The Supervisory Board received all relevant documents and information pertaining to the subjects discussed from the Board of Management. This allowed it to form an independent and fair opinion on the Group’s overall activities.

Business presentations were held by the respective directors before the Supervisory Board to elaborate on internationalisation and building capacity abroad, safety and quality, dredging and offshore market developments, and on IHC IQIP.

Alternating members of the Board attended some of the meetings between the Works Council and the Board of Management.

Main topics

Deteriorating economic and market conditions forced the Supervisory Board to maintain a clear focus on sales and the order book. Many discussions were spent and concerns were formulated regarding market approach, prospects and new orders. In order to remain competitive in our rapidly changing markets, acceleration of the IHC 2020 strategic plan was agreed. Increasing efficiency, managing the production and organisation costs, reducing the number of slipways in The Netherlands, and downsizing the temporary and fixed workforce became necessary to prepare Royal IHC for the difficult times ahead. The decision to reduce the workforce was announced in June, and ongoing discussions with the Works’ Council and trade unions took place. By the end of December, a social plan was agreed with the trade unions that will support employees that have to leave the company. The agreement contains royal benefits, both financially and in terms of employability. As expected, the Board of Directors came to a full agreement with the Works’ Council at the beginning of 2016, after which the downsizing process can actually start.

Although the Supervisory Board is satisfied with the results, it would like to express its concern regarding the lack of speed as well as the arduous nature of the entire process. Negotiations took nearly nine months. This time could have been spent making the necessary adjustments within the organisation.

Another main topic for 2015 was safety, health, environment and quality. The untimely death of an IHC employee has highlighted the absolute importance of this. The Supervisory Board will continue paying close attention to these issues in 2016. The same goes for HR matters such as succession planning and talent management, as these are vital to the continuity of the company.

To better serve our customers, the internationalisation plan and the search for building capacity abroad were both accelerated. Local regulations restricting access to markets, lower production costs, local-for-local strategies and closer proximity to the customer all drive the internationalisation plan. Nevertheless, our headquarters in The Netherlands will remain Royal IHC’s knowledge centre. At the end of 2015, Royal IHC acquired Fraser Hydraulic Power, based in Newcastle-upon-Tyne, UK, and a 50% share of Robbins Technology Group, based in Brisbane, Australia. These acquisitions strengthen the foothold of Royal IHC in these two countries, and are visible steps towards the internationalisation strategy for 2020.

The Supervisory Board also closely monitored the One IHC programme, which aims to bring all business units under a single ICT/ERP system. During the last quarter, the first roll-out was successfully implemented at IHC Vremac Cylinders.

A fast-changing economic climate, demanding markets and increasing legislation also required Royal IHC to take further steps towards good governance, compliance and CSR programmes. During its meetings, the Supervisory Board has debated these subjects and carefully monitors comprehensive compliance and good governance – to the benefit of all Royal IHC stakeholders.

Financial results

The Supervisory Board of IHC Merwede Holding B.V. hereby presents the Annual Report 2015. This incorporates the financial statements for the year as prepared by the Board of Management. The financial statements were audited and discussed with KPMG Accountants N.V. (KPMG). They issued an unqualified independent auditor’s report on the 2015 financial statements.

The financial statements were approved by the Supervisory Board on 6 April 2016. The result attributable to the shareholders of the company for 2015 is €29.1 million, down from €123.0 million in 2014. Taking into account one-off expenditures, such as provisions for reorganisation and

impairments, the net result is €52.4 million in 2015, compared to €106.6 million in 2014.

The balance sheet totals €1.100 million, with Group equity standing at €305 million.

The Board of Management proposes a dividend of €14.5 million to the shareholder IHC B.V., while adding the remainder of the net profit to other reserves. This has been approved by the Supervisory Board.

Preview for 2016

Amid volatile markets, rapidly changing economic conditions, geopolitical unrest and high uncertainties regarding global growth, 2016 will no doubt be a challenging year for Royal IHC. A deteriorating order book and fierce price competition for new orders are forcing us to continue accelerating the implementation of our strategy. In order to remain an industry leader, Royal IHC must become more international, more efficient, more agile and more client oriented. 2016 will be a pivotal year in the achievement of these goals.

Conclusion

Never waste a good crisis. 2015 was without doubt a difficult year for Royal IHC, and while the financial figures remain sound – driven by the late cyclical order book and good project execution – the future looks challenging due to the ongoing turmoil in our core markets. Nevertheless, by accelerating the implementation of the IHC 2020 strategy, focusing on internationalisation, and executing the One IHC programme, the foundations are in place to prepare IHC for the future.

The Supervisory Board wishes to express its appreciation to all IHC employees. In difficult circumstances they remained calm and continued to fulfill their tasks. This demonstrates that our workforce is our strongest asset and best guarantee for the successful future of Royal IHC.

Sliedrecht, 6 April 2016

The Supervisory BoardJ.C. ten Cate, ChairmanC.J. de BruinC. KorevaarB.H.C. de Bruin-van EijckJ.H.N.M. van der Horst

6 Royal IHC | Annual Report 2015 Royal IHC | Annual Report 2015 7

Although cash is abundant in the world economy, from a business perspective these times require IHC to be prudent in terms of outgoing cash flow, limiting us to a restricted scope for acquisitions. At the start of 2015, IHC integrated SAS Offshore, Alphen aan den Rijn (including SAS do Brasil), active in offshore deck equipment, in conjunction with a 70% share in its owner, Brastec (Brazil), which supplies machines for the production of flexible pipe. The end of 2015 saw the conclusion of the acquisition of the UK-based offshore rental equipment company Fraser Hydraulic Power, and the 50% merger with Robbins Technology Group (RTG) of Australia, a FEED company specialising in mineral sands mining plants. All of these acquisitions fitted IHC’s strategy of becoming less dependent on large capex new builds.

Financial

Revenue and result developmentRevenues during the year decreased by 4.4% to €1,161.3 million (2014: €1,214.7 million). External costs decreased by 1.8% to €755.1 million (2014: €769.2 million). These expenses amounted to 65.0% of revenue, which is an increase of 1.7% compared to 2014 (63.3%). Employee costs increased by 7.1% to €297.6 million (2014: €277.8 million). Expressed as a percentage of revenue, employee costs increased from 22.9% in 2014 to 25.6% in 2015.

The average cost per employee amounted to €65,134, an increase of 2.2% compared to 2014. Depreciation and impairment of property, plant and equipment decreased from €32.8 million in 2014 to €31.3 million in 2015. Amortisation and impairment of intangible assets increased from €10.9 million in 2014 to €16.5 million in 2015, due to increased amortisations caused by recent additions and impairments of development costs, goodwill and other intangibles.

The result from operating activities, plus the depreciation and impairment of property, plant and equipment, and amortisation and impairment of intangible assets (EBITDA) was €84.8 million (€191.9 million in 2014). This is a decrease of 55.8% compared to the previous year due to: - a decrease in margins, as the markets the Group operates

in are becoming more and more competitive- one-off results included in the results of last year due to

the sale of Group companies- a provision for restructuring which is included in the results

of the current year.

Order bookOn 31 December 2015, the value of the order book amounted to €834.7 million – 28.3% lower than on 31 December 2014 (€1,165.5 million). Based on the decreasing order book, the

Group expects that the permanent production capacity will not be fully utilised in 2016. Sales in 2015 amounted to €826.7 million, an increase of €243.8 million compared to 2014.

Cash flowThe following represents the cash flow in the past two years:

Working capitalWorking capital amounting to -€45.2 million, as of 31 December 2015, is more negative than the previous year (-€6.8 million). Such fluctuations are inherent to the character of the company, as work in progress is financed either on a milestone payment schedule by the customer or by an agreed payment schedule with the bank consortium. Depending on the agreed payment schedule with the customer and the stage of completion of the projects under construction, the amount due to or due from customers, or the amount of trade receivables, may differ substantially.

InvestmentsInvestments in property, plant and equipment during 2015 can be specified as follows:

Investments in property, plant and equipment are directly related to the current business. Investments in rental equipment is related to the rental fleet of IHC IQIP.

Report of the Board of Management

Introduction

The world as a whole experienced continuous volatility in 2015. All aspects of society, the environment, the economy and politics were in a constant state of flux. The onset of a downward trend for the world economy in 2014 was accelerated in 2015. El Niño not only had a strong effect on the world’s climate, but also seemed to effect its economy. ‘Disruption’ was the key word for 2015. Disruptive changes in energy, climate, migration and consumption were the main drivers for demanding disruptive solutions to the problems facing mankind. For IHC, which develops solutions for harvesting worldwide maritime resources, almost all of these issues had a major impact – one way or the other – on developing business.

Market developments

The main factor that characterised our market in 2015 was the drop in oil prices. World markets experienced a downturn in consumer spending, creating the need to uphold financial stability by injecting large amounts of cash into the system. Interest rates were down to a minimum and sometimes even in the negative. Resource demand declined – whether for energy, base materials or rare earths – resulting in an unstable and insecure outlook for investment. Offshore capex investments for deeper water and complex operations dried up completely, and the focus shifted to opex for finding ways to reduce cost levels.

‘Spending’ became a dirty word in 2015; downsizing and outright ‘survival mode’ is the name of game. Mining, specifically wet mining, has also been hit by the same cocktail of poisons: low demand compared to supply, and trying to salvage as many sunken costs as possible. The dredging market is in a replacement cycle for assets that are technically and/or economically written off – a buyer’s market with the time and appetite for finding the lowest price with unconventional partners and combinations. Renewables remained vibrant and show further potential in a world hungry for clean energy. However, government regulation, approval procedures and subsidy programmes have a tendency to slow down new projects coming to market.

In addition, the trickle down from the offshore slump makes price pressures in the renewables sector felt.

Company developments

Due to the steep capex investment decline in the offshore

industry, 2015 became a transitional year. The order book was still dominated by the pipelaying series, of which the last vessels were launched at the end of the year. The backlog for the dredging market was still suffering from the new-build bonanza in the first half of the decade. Next to a consistently stable demand for the standard cutter suction dredger range and some state-owned counter-cyclic projects, the focus of the big four contractors was on detailing a replacement programme for the older generation of dredging equipment. Offshore markets being dead, IHC was delighted to secure orders for many of the new dredging vessels coming to the market, with half of those being the two new series of standard hopper dredgers. The Motion Control & Automation group of companies had a steady year, with a lot of work and good results. All other equipment suppliers and capacity units struggled with order intake and price levels. For the wind energy industry, IHC had to cope with a slowdown of investment programmes and, for equipment supply in general, a heavy price competition from competitors trying to retain market share. Bucking the trend was the success of IHC Fundex Equipment, which came as the result of a solid development programme for bigger piling equipment and the step-by-step comeback of the building industry.

The strategy programme, IHC 2020 – with the five building blocks: customer focus, cost reduction, innovation, employer of choice and internationalisation – was intensified in combination with a plan to reduce the permanent workforce by 15%. These measures were put forward proactively in order to respond to the dramatic downturn in the offshore and oil and gas industries, and the expectation of a long period of negotiation with the Works Council and trade unions. For both programmes, the transformation from planning and discussions into actually doing things required constant pressure from the management. Agreement on the terms for individual severance has been reached with the trade unions and also an agreement with the Works Council has been reached.

The prelude to the IHC 2020 strategy, the ONE IHC programme, is now well into the its execution phase following the integrated implementation at IHC Vremac Cylinders. Apart from minor issues and some intensive care solutions, the changeover was successful, breaking ground for the follow-up at headquarters. The lessons learned demonstrated the vulnerability of milestone achievement to having a correct and complete Product Data set.

SHEQ and CSR initiatives were actively pursued. Safety awareness during all working procedures must be raised to the next level, as was very regretfully highlighted by an incident that resulted in the death of an employee.

In millions of euros: 2015 2014Net cash flow from:

Operating activities (excluding changes in working capital) 85.2 157.1

Changes in working capital -17.4 -107.4

Investing activities -29.9 -14.5Financing activities 1.3 -111.1

Net increase / decrease in cash and cash equivalents 39.2 -75.9

In millions of euros:

Land, docks, slipways, dry docks, business premises, floating equipment 1.2

Plant and machinery 3.9

Rental equipment and other operating fixed assets 23.9

Other items 9.138.1

Usage of the project working capital is limited to fund working capital for certain designated vessels and the maturity date is linked to the expected delivery date of the relevant vessel. The borrowings are repaid and the facility (partly) cancelled pro rata with the delivery of the relevant vessels. The cancelled amount will become available again as ‘uncommitted accordion facility’ and can be subsequently reinstated. In 2015, the Group has agreed to extend most of the above mentioned facilities by one year with one additional annual extension option left. These facilities are provided by a consortium of financial institutions consisting of ABN AMRO, DBS Bank Ltd, Delta Lloyd, Deutsche Bank, ING Bank, Rabobank and the Royal Bank of Scotland. In the context of this credit agreement, most of the immovable property has been mortgaged and certain inventories, receivables, bank balances, other movable property and current assets have been pledged to the lenders. The commitments to the financial covenants have been met in full as at 31 December2015.

In addition to above mentioned credit facilities, the Group has the following other credit facilities:

(i) a €60 million guarantee facility with NV Nationale Borg-Maatschappij of which €51.9 million was outstanding at 31 December 2015;

(ii) a €16.2 million term loan provided by a vendor finance provider in the form of a 5-year annuity on a quarterly basis;

(iii) €13.0 million outstanding under a lease facility provided by a leasing company to finance (part of) the rental assets of the group in the form of a 5-year annuity on a quarterly basis;

(iv) a €10 million revolving credit facility of which €3.3 million was outstanding at 31 December 2015;

(v) €9.0 million outstanding loans of Brastec Technologies SA. Guarantees have been given by a fund related to a minority shareholder for an amount of €4.7 million.

Research & DevelopmentInnovation, as one of the building blocks of IHC 2020, is crucial to answer tomorrow’s market demands and is focused on innovative output that sells. IHC annually spends approximately 3% of its revenue on innovation and has a specialist in-house R&D institute, IHC MTI. The focus is to deliver the most efficient vessels, equipment and services for the specialist maritime industry.

Risk management

Amidst worsening market conditions, the company’s risk profile needs close monitoring and a pro-active approach. With margins under more pressure and contract specifics becoming less favourable, the need for appropriate and effective risk management becomes even more clear.2015 saw a focus on the risk management in projects, resulting in an improved management overview of exposure, mitigation progress, process adherence, and contingencies for all active projects.

Risk management – for both threats and opportunities – is completed via a process of risk identification, assessment, planning adequate responses and implementing effective monitoring. This process adheres to Management of Risk®, ISO31000:2009 and ISO9001:2015.

The Board of Management has overall responsibility for the risk management and control framework within the company. The Chief Financial Officer acts as formal representative of this responsibility and is advised by the Corporate Risk Manager and other related staff functions, aided by information from a dedicated software system. The adequacy and effectiveness of the framework are regularly reviewed.

Project risksThe products that IHC delivers to its customers are managed predominantly on a project basis. The IHC Project Management methodology has Risk Management as one of its most prominent controls. Project Risk Logs are maintained in a centralised database and monitored by overarching Project Management, Business Control and Risk Management functions.The focus remains on the reduction of the variation in project results by proactive identification of significant technical, commercial and contractual risks, and finding timely, effective responses to reduce threats and enhance opportunities.All major contracts are reported to and discussed with the Executive Committee and important milestones to a larger audience of internal stakeholders. Work in progress is insured for damage.

Market risksWith the further development of the IHC Services organisation and subsequent opportunities, different types of risk enter the risk profile. Risk management attention has been applied where needed and will continue to follow the development closely from a risk management perspective.

8 Royal IHC | Annual Report 2015 Royal IHC | Annual Report 2015 9

Report of the Board of Management

Balance sheet ratiosThe condensed balance sheet as at 31 December is:

Group equity increased by €9.7 million. This increase is the balance of the profit for the 2015 financial year (€27.9 million) less the distributed dividend (totaling €34.5 million), a positive movement in the hedging reserve (€13.8 million after tax) related to hedge accounting on outstanding contracts and changes following amended fair values and currency differences (€2.5 million). The solvency ratio as at 31 December 2015 was 27.8%, an increase of 2.9% compared to 31 December 2014. The current ratio as at year end 2015 was 1.2, which is the same as at year end 2014.

FinancingIn 2015, the Group has refinanced a bilateral term loan by increasing its €1,500,000,000 credit facilities to €1,535,000,000. This is divided as follows:

Amount Maturity date Amortisation Type Drawn per 31-12-2015

Bank guarantees 900,000 30 May 2019 Not applicable Committed 534,822

Project working capital 135,000 30 May 2016 Delivery vessel Committed 120,000

Project working capital 48,800 30 June 2017 Delivery vessel Committed -

Project working capital 39,000 31 Dec 2017 Delivery vessel Committed -

Revolving credit facility 50,000 30 May 2019 Bullet Committed -

Term debt 85,000 30 May 2019 Bullet Committed 85,000

Accordion facility 277,200 30 May 2019 Not applicable Uncommitted -

1,535,000 739,822

In millions of euros:31 Dec

201531 Dec

2014 Difference

Non-current assets 336.0 350.1 -14.1

Working capital (excluding cash and cash equivalents)

-45.2 -6.8 -38.4

Cash and cash equivalents 188.0 149.2 38.8

Net assets 478.8 492.5 -13.7

Non-current liabilities 173.4 196.8 -23.4

Group equity 305.4 295.7 9.7

Financing 478.8 492.5 -13.7

10 Royal IHC | Annual Report 2015 Royal IHC | Annual Report 2015 11

Report of the Board of Management

2015 marked the seventh consecutive year of downturn in global shipbuilding and a deep crisis in Offshore Oil & Gas Industry. IHC, being a third-tier Original Equipment Manufacturer in the chain, saw the order intake decreasing due to lack of capex investment from O&G companies and downstream contractors. Also, with negative news coming from China and Iran re-entering the world economy as an oil supplier these, and other, dynamics are expected to prolong the low crude price from 2015 well into 2016. Overall, vessel prices are still at rock bottom, but the cost of production has continued to increase, affecting sector margins. Globally, only a small number of shipbuilding orders are being placed, and these are primarily granted to dominant yards that possess superior brand, technology and financial strength.

Contract risksIHC has a strict acceptance policy for political and payment risks. In principle, these are covered by credit insurance or a letter of credit, except in the case of existing customers with an excellent credit rating. IHC is also in continuous dialogue with export credit agencies to look for tailor-made solutions to mitigate political and payment risks.

Interest rate and currency riskAll currency risks are managed in accordance with the company’s strict hedging policy. This is reviewed and updated annually.The company follows a policy of ensuring that its exposure to changes in interest rates on loans and borrowings is on a fixed-rate basis. This is done by entering into interest rate swaps for almost all loans and borrowings.

Credit riskThe company has established a credit policy under which each customer’s creditworthiness is analysed before the company’s standard payment and delivery terms and conditions are offered. If deemed necessary based on the creditworthiness analysis, credit risks are covered by obtaining payment security, such as bank guarantees, (confirmed) letters of credit, advance payments, parent company guarantees and/or credit risk insurance.

Liquidity riskThe company’s approach to managing liquidity is to ensure that it will always have sufficient liquidity to meet its liabilities when due without incurring unacceptable losses or risking damage to the company’s reputation.

Human resources

In 2015, we have concentrated on several HR-related subjects:• the introduction of our performance management method• employer of choice becoming one of the strategic building

blocks of IHC 2020• the announced reduction of the company workforce by

almost 500 employees.

By introducing performance management, our employees now hold at least two conversations with their manager each year. At the start of the year, an employee’s goals are agreed and at the end of the year a follow-up meeting is held to discuss what has been achieved. So far, we have employed a so-called ‘paper’ version, but in 2016 we will introduce an electronic version that will make reporting much easier.

In 2015, we also launched an employee survey in order to measure employee satisfaction and to compare ourselves with other companies in The Netherlands and within our branch. We conducted this survey in the framework of employer of choice. In addition to the internal survey, we also conducted an external survey with companies who are already employer of choice.

The outcome of the internal survey has been presented at a departmental level and, in dedicated meetings together with the employees of the department, improvement plans have been made. The main topics were: communication, role abstruseness and leadership. Young IHC formed three so-called ‘Challenge Teams’ with the following subjects: talent development, image and leadership. They presented their results to the Board of Management, which has translated some of their ideas into policy. Three working groups were formed by the HR department, with the following subjects: strategic personnel planning, leadership and the modernisation of labour terms. Plans were subsequently drawn up with action points that will be implemented in the coming years, with representatives of Young IHC participating in the working groups. The first meeting addressing the subject of leadership has been arranged for 1 December, and in 2016 several training sessions will be held.

Unfortunately, in June we had to announce our intended downsizing of the company. The trade unions were informed, and advice was sought from the Works Council. At the end of the year, we were able to agree a social plan with the trade unions.

IHC has taken note of the law requiring a more balanced representation of men and women on the Board of Management. Under this law, at least 30% of the positions

must be held by women and 30% must be held by men. When making future nominations and appointments, the Board of Management will take into account the statutory requirements for a balanced representation of men and women.

Corporate Social Responsibility

IHC is aware of the social and environmental impact of its activities, and its capacity to minimise the impact of its equipment and vessels during their entire life cycle. A solid CSR strategy contributes to the company’s overall corporate objectives and enables IHC to meet the increasing expectations of internal and external stakeholders for taking responsibility and communicating transparently regarding the results.

IHC’s CSR strategyIn 2015, IHC further embedded its CSR strategy into the organisation by incorporating CSR within the Safety, Health, Environment and Quality (SHEQ) department. The establishment of an advisory board comprising representatives from a wide variety of internal departments supports the implementation of the corporate CSR policy and the realisation of its objectives. This organisational change contributes to the integration of CSR in the day-to-day business of the company.

IHC’s CSR strategy is about sustainable entrepreneurship, social responsibility and environmental accountability. Supply chain management, health and safety, sustainable product development and the carbon footprint are a few examples of topics identified as being important to the organisation. IHC reports its non-financial results annually according to the guidelines of the Global Reporting Initiative.

IHC Merwede FoundationIHC contributes to local communities through the IHC Merwede Foundation. In 2015, a project was initiated to offer children working in the shipbreaking yards in Bangladesh a better future by providing education in cooperation with World Vision. In South Africa, the knowledge and passion of IHC employees was demonstrated during the annual dry-docking and renovation period of the AFRICA MERCY, the world’s largest floating hospital operated by Mercy Ships.

ComplianceCompliance with national and international legislation is of the utmost importance for IHC. To achieve this, several regulations are in place including a code of conduct, anti-corruption regulations and a whistleblower policy. Compliance is closely monitored.

The future

For the foreseeable future, we do not expect the direction our markets have taken to revert back to the way they were a couple of years ago. As the average temperature increases as a result of climate change, the current situation is the new norm. High volatility, overcapacity in terms of assets and suppliers, and a craving for initiatives to reduce costs are the main elements to set the compass by.

The IHC 2020 strategy, conceived in 2014, was a timely response to the first signs of cracks in the mould. The direction of the plan was – and still is – right on the mark. However, speed is of the essence if IHC is to outclass the competition. Idle hope based on volatile countercurrents runs the risk of structurally neglecting the strong undertow. This crisis can only be turned into a good crisis if it is not wasted due to lack of change.

The Board of Management will continue to challenge the organisation to adapt to the new reality, giving IHC employees the freedom to experiment in light of a market demand for new solutions. Outside-in instead of inside-out, technology-driven coming second to customer-driven, and lean processes creating space for innovative ideas. The task that has been set is to make IHC stronger through cooperation and leadership – in every dimension. As a people company, strong teams with standardised tools and practices working in a safe environment are prerequisites for sharpening the competitive edge of our customers.

In general, the conclusion can be drawn that in a turbulent business environment, IHC was successful in keeping afloat on a healthy balance sheet, backed by a relatively good net result and order intake. Having crossed the first part of the river towards better conditions on the other shore, the Board of Management – including our new COO – is ready to battle the next round of strong waves and current.

Sliedrecht, 6 April 2016

Board of ManagementA. Roelse, CEOD.A.A.J.A.G Vander Heyde, CFOA.M. van Noort, COO

12 Royal IHC | Annual Report 2015 Royal IHC | Annual Report 2015 13

Abbreviated financial information 2015

In thousands of euros 2015 2014Revenue 1,161,347 1,214,701Other income 3,517 25,381Operating income 1,164,864 1,240,082

External costs 755,094 769,161Employee expenses 297,563 277,845Depreciation and impairment of property, plant and equipment 31,286 32,797Amortisation and impairment of intangible assets 16,527 10,862Other expenses 27,382 1,192Operating expenses 1,127,582 1,091,857

Result from operating activities 37,012 148,225

Finance income 7,135 4,845Finance expenses -7,339 -5,296Net finance income -204 -451

Share of profit of equity accounted investees (net of income tax) -1,021 501Profit before income tax 35,787 148,275

Income tax expense -7,852 -24,287Profit for the period 27,935 123,988

Profit attributable to:Owners of the Company 29,138 123,025Non-controlling interests -1,203 963Profit for the period 27,935 123,988

Consolidated income statement

In thousands of euros 31 Dec 2015 31 Dec 2014AssetsProperty, plant and equipment 217,640 214,042Investment property 9,360 9,518Intangible assets and goodwill 95,020 99,654Investments in equity accounted investees 5,113 2,829Deferred tax assets 1,800 3,620Other non-current financial assets 7,043 20,471Non-current assets 335,976 350,134

Inventories 117,453 104,161Due from customers for work in progress 243,744 326,290Trade and other receivables 213,494 258,512Current tax receivables 1,504 985Cash and cash equivalents 188,003 149,212Current assets 764,198 839,160

Total assets 1,100,174 1,189,294

Group equityShare capital 250 250Share premium reserve 68,136 68,136Reserves 206,670 129,725Unappropriated result 29,138 96,025Total equity attributable to equity holders of the Company 304,194 294,136Non-controlling interests 1,166 1,585Total Group equity 305,360 295,721

LiabilitiesLoans and borrowings 114,756 88,779Derivatives 3,287 30,655Deferred tax liabilities 41,855 51,703Provisions 8,113 16,637Other liabilities 5,396 9,065Total non-current liabilities 173,407 196,839

Trade and other payables 352,669 374,457Due to customers for work in progress 82,607 159,210Current portion of loans and borrowings 131,915 128,652Current tax liabilities 2,649 12,379Provisions 51,567 22,036Total current liabilities 621,407 696,734Total liabilities 794,814 893,573

Total Group equity and liabilities 1,100,174 1,189,294

Consolidated balance sheet(Before appropriation of result)

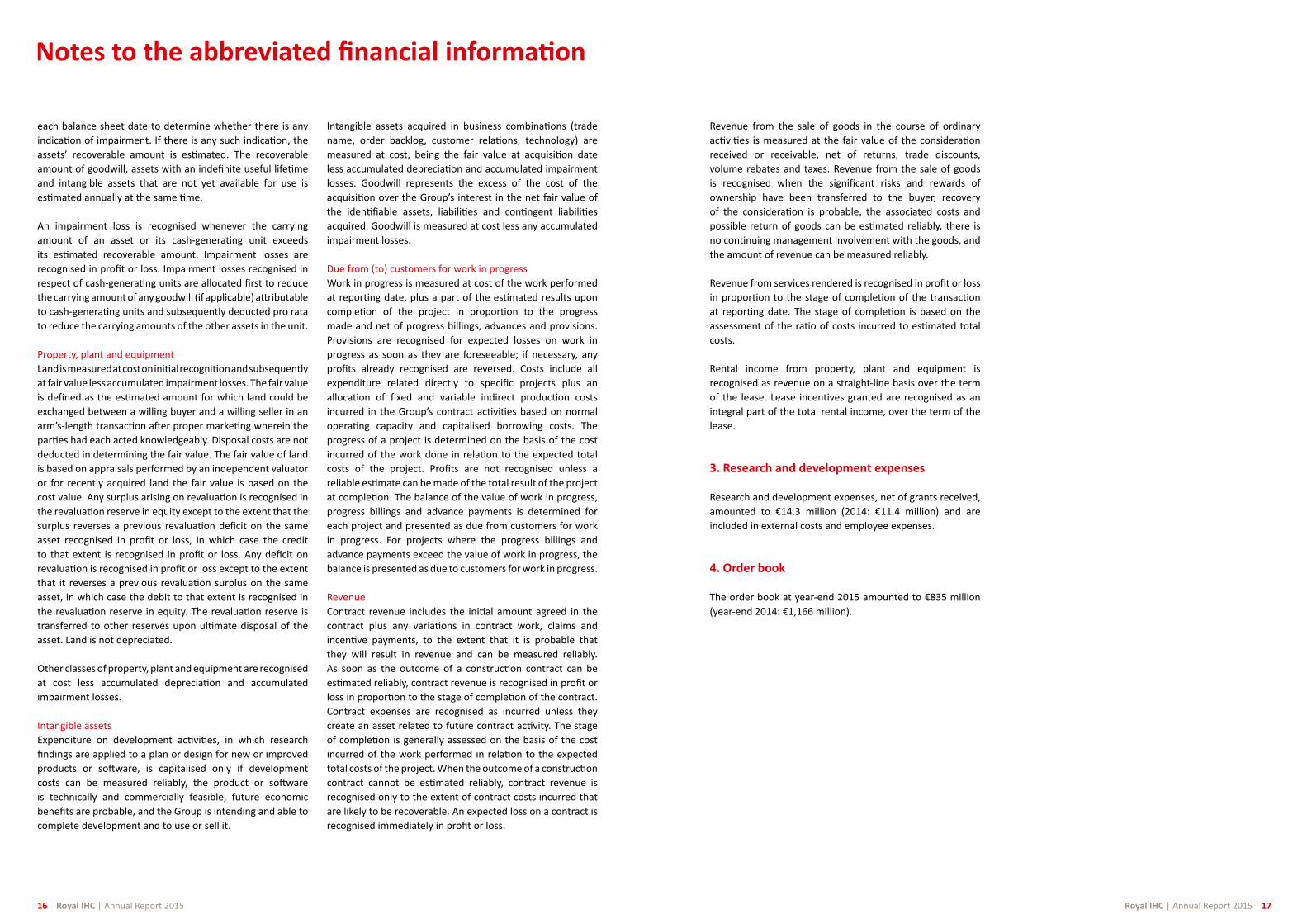

In thousands of euros 2015 2014Profit for the period 27,935 123,988Adjustments for:Depreciation, amortisation and impairment expenses 47,813 43,659Revaluation of land 64 -243Loss/(gain) on sale of property, plant and equipment 90 -124Loss/(gain) on investment property - -393Share of result of equity accounted investees 1,021 -501Gain on sale of participations - -21,633Net finance income 204 451Income tax expense 7,852 24,287Changes in provisions 20,906 -3,548

105,885 165,943

Interest (paid) / received -1,923 -595Income tax paid -18,710 -8,264Net cash flow from operating activities (excluding changes in working capital) 85,252 157,084

Changes in working capital (excluding cash and cash equivalents):- Acquisition of rental fleet -25,207 -18,460- Inventories -11,141 -3,541- Due from customers for work in progress 82,546 -63,059- Trade and other receivables (excluding derivatives and accrued interest) 48,923 -90,125- Due to customers for work in progress -76,603 20,721- Trade and other payables (excluding derivatives and accrued interest) -42,575 15,202- Other changes in working capital 6,601 31,910Changes in working capital -17,456 -107,352

Net cash flow from operating activities 67,796 49,732

Acquisitions of intangible assets and property, plant and equipment -24,526 -28,995Proceeds from divestments of property, plant and equipment 1,655 3,702Acquisition of subsidiaries, net of cash acquired -4,880 -14,397Proceeds from disposals of subsidiaries, net of cash disposed - 23,670Proceeds from disposals of participations in limited partnerships, net of cash disposed 2,029 348Proceeds from disposals of equity accounted investees - 1,100Investments in other non-current financial assets -5,003 -Dividends received 372 154Issue of loans and receivables 497 -34Net cash flow used in investing activities -29,856 -14,452

Acquisition of non-controlling interests - -16,748Capital contribution related to non-controlling interests 639 -Additions to loans and borrowings 112,147 122,808Repayment of loans and borrowings -77,033 -158,330Dividends paid -34,500 -57,000Dividends paid to minority interests - -1,890Net cash flow used in financing activities 1,253 -111,160

Net increase / (decrease) in cash and cash equivalents 39,193 -75,880

Cash and cash equivalents as at 1 January 149,212 223,921Movements in net cash and cash equivalents 39,193 -75,880Effect of exchange rate fluctuations on cash held -402 1,171Cash and cash equivalents as at 31 December 188,003 149,212

Abbreviated financial information 2015Consolidated statement of cash flows

Notes to the abbreviated financial information

1. General

The abbreviated financial information is derived from the financial statements 2015, which are prepared in accordance with the International Financial Reporting Standards (IFRS) and interpretations as adopted by the European Union (EU-IFRS) and with Part 9 of Book 2 of The Netherlands Civil Code. The abbreviated financial information gives the headlines of the financial position of IHC Merwede Holding B.V. and its consolidated subsidiaries (together referred to as the ‘Group’) for the year ended 31 December 2015.

For a better understanding of the Group’s financial position, we emphasise that the abbreviated financial information should be read in conjunction with the unabridged financial statements, from which the abbreviated financial information was derived. An unqualified auditor’s report thereon dated 6 April 2016 was issued by KPMG Accountants N.V. The unabridged financial statements 2015 are available at the Company or at the Chamber of Commerce in Rotterdam.

2. Significant accounting policies

An abbreviation of a selection of the most significant accounting policies is included below. For a full overview of the accounting policies refer to the unabridged financial statements 2015.

Basis of preparationThe consolidated financial statements are presented in euros unless indicated otherwise, the euro being the Group’s functional currency. The consolidated financial statements are based upon historical cost unless stated otherwise.

EstimatesThe preparation of the financial statements in accordance with IFRS requires management to make judgements, estimates and assumptions based on experience and various other factors that can be considered reasonable under the circumstances. Those estimates and assumptions form the basis for judgements about the carrying values of assets and liabilities that are not readily apparent from other sources. Actual outcome may differ from these estimates. The most important judgements in the financial statements concern the assessment of the result of contract work, measurement of warranty provisions, the measurement of recoverable amounts of cash-generating units containing goodwill, recoverability of development costs, valuation of inventories and acquisition of subsidiaries.

Basis of consolidationSubsidiaries are entities controlled by the Group. The Group controls an entity when it is exposed to, or has rights to, variable returns from its involvement with the entity and has the ability to affect those returns through its power over the entity. The financial statements of subsidiaries are included in the consolidated financial statements from the date that control commences until the date that control ceases. The accounting policies of subsidiaries have been aligned with the policies adopted by the Group.

Foreign currenciesThe assets and liabilities of foreign operations that are denominated in foreign currencies, including goodwill and fair value adjustments arising on acquisition, are converted to the euro at exchange rates at the reporting date. The income and expenses of foreign operations are converted to the euro at exchange rates at the date of the transaction. Foreign currency differences are recognised in the currency translation reserve in equity. Exchange rate differences as a result of operational transactions and of the conversion at the end of the reporting period of monetary assets and liabilities denominated in foreign currencies are recognised in profit or loss in the reporting period.

DerivativesThe Group holds derivative financial instruments to decrease its exposure to foreign currency risks and interest rate risks. Derivatives are measured at fair value and changes therein are recognised in the consolidated income statement, unless hedge accounting is applied.

When a derivative is designated as the hedging instrument in a hedge of the variability in cash flows attributable to a particular risk associated with a recognised asset or liability or a highly probable forecast transaction that could affect profit or loss, the effective portion of changes in the fair value of the derivative is recognised in the hedging reserve in equity. When the hedged item is a non-financial asset, the amount accumulated in equity is included in the carrying amount of the asset when the asset is recognised. In other cases the amount accumulated in equity is reclassified to profit or loss in the same period that the hedged item affects profit or loss. The portion of the gain or loss on an instrument used to hedge a net investment in a foreign operation that is determined to be an effective hedge is recognised directly in the currency translation reserve in Group equity.

ImpairmentThe carrying amount of the Group’s assets, excluding inventories, work in progress, deferred tax assets and assets that are classified as held for sale, are reviewed on

Royal IHC | Annual Report 2015 1514 Royal IHC | Annual Report 2015

Royal IHC | Annual Report 2015 17

each balance sheet date to determine whether there is any indication of impairment. If there is any such indication, the assets’ recoverable amount is estimated. The recoverable amount of goodwill, assets with an indefinite useful lifetime and intangible assets that are not yet available for use is estimated annually at the same time.

An impairment loss is recognised whenever the carrying amount of an asset or its cash-generating unit exceeds its estimated recoverable amount. Impairment losses are recognised in profit or loss. Impairment losses recognised in respect of cash-generating units are allocated first to reduce the carrying amount of any goodwill (if applicable) attributable to cash-generating units and subsequently deducted pro rata to reduce the carrying amounts of the other assets in the unit.

Property, plant and equipmentLand is measured at cost on initial recognition and subsequently at fair value less accumulated impairment losses. The fair value is defined as the estimated amount for which land could be exchanged between a willing buyer and a willing seller in an arm’s-length transaction after proper marketing wherein the parties had each acted knowledgeably. Disposal costs are not deducted in determining the fair value. The fair value of land is based on appraisals performed by an independent valuator or for recently acquired land the fair value is based on the cost value. Any surplus arising on revaluation is recognised in the revaluation reserve in equity except to the extent that the surplus reverses a previous revaluation deficit on the same asset recognised in profit or loss, in which case the credit to that extent is recognised in profit or loss. Any deficit on revaluation is recognised in profit or loss except to the extent that it reverses a previous revaluation surplus on the same asset, in which case the debit to that extent is recognised in the revaluation reserve in equity. The revaluation reserve is transferred to other reserves upon ultimate disposal of the asset. Land is not depreciated.

Other classes of property, plant and equipment are recognised at cost less accumulated depreciation and accumulated impairment losses.

Intangible assetsExpenditure on development activities, in which research findings are applied to a plan or design for new or improved products or software, is capitalised only if development costs can be measured reliably, the product or software is technically and commercially feasible, future economic benefits are probable, and the Group is intending and able to complete development and to use or sell it.

Intangible assets acquired in business combinations (trade name, order backlog, customer relations, technology) are measured at cost, being the fair value at acquisition date less accumulated depreciation and accumulated impairment losses. Goodwill represents the excess of the cost of the acquisition over the Group’s interest in the net fair value of the identifiable assets, liabilities and contingent liabilities acquired. Goodwill is measured at cost less any accumulated impairment losses.

Due from (to) customers for work in progressWork in progress is measured at cost of the work performed at reporting date, plus a part of the estimated results upon completion of the project in proportion to the progress made and net of progress billings, advances and provisions. Provisions are recognised for expected losses on work in progress as soon as they are foreseeable; if necessary, any profits already recognised are reversed. Costs include all expenditure related directly to specific projects plus an allocation of fixed and variable indirect production costs incurred in the Group’s contract activities based on normal operating capacity and capitalised borrowing costs. The progress of a project is determined on the basis of the cost incurred of the work done in relation to the expected total costs of the project. Profits are not recognised unless a reliable estimate can be made of the total result of the project at completion. The balance of the value of work in progress, progress billings and advance payments is determined for each project and presented as due from customers for work in progress. For projects where the progress billings and advance payments exceed the value of work in progress, the balance is presented as due to customers for work in progress.

RevenueContract revenue includes the initial amount agreed in the contract plus any variations in contract work, claims and incentive payments, to the extent that it is probable that they will result in revenue and can be measured reliably. As soon as the outcome of a construction contract can be estimated reliably, contract revenue is recognised in profit or loss in proportion to the stage of completion of the contract. Contract expenses are recognised as incurred unless they create an asset related to future contract activity. The stage of completion is generally assessed on the basis of the cost incurred of the work performed in relation to the expected total costs of the project. When the outcome of a construction contract cannot be estimated reliably, contract revenue is recognised only to the extent of contract costs incurred that are likely to be recoverable. An expected loss on a contract is recognised immediately in profit or loss.

Notes to the abbreviated financial information

Revenue from the sale of goods in the course of ordinary activities is measured at the fair value of the consideration received or receivable, net of returns, trade discounts, volume rebates and taxes. Revenue from the sale of goods is recognised when the significant risks and rewards of ownership have been transferred to the buyer, recovery of the consideration is probable, the associated costs and possible return of goods can be estimated reliably, there is no continuing management involvement with the goods, and the amount of revenue can be measured reliably.

Revenue from services rendered is recognised in profit or loss in proportion to the stage of completion of the transaction at reporting date. The stage of completion is based on the assessment of the ratio of costs incurred to estimated total costs.

Rental income from property, plant and equipment is recognised as revenue on a straight-line basis over the term of the lease. Lease incentives granted are recognised as an integral part of the total rental income, over the term of the lease.

3. Research and development expenses

Research and development expenses, net of grants received, amounted to €14.3 million (2014: €11.4 million) and are included in external costs and employee expenses.

4. Order book

The order book at year-end 2015 amounted to €835 million (year-end 2014: €1,166 million).

16 Royal IHC | Annual Report 2015

To: the Board of Management of IHC Merwede Holding B.V.

The accompanying abbreviated financial information, which comprises the consolidated income statement for the year ended 31 December 2015, the consolidated balance sheet as at 31 December 2015, the consolidated statement of cash flows for the year then ended, and notes, comprising a summary of the significant accounting policies and other explanatory information, are derived from the audited financial statements of IHC Merwede Holding B.V. for the year ended 31 December 2015. We expressed an unqualified audit opinion on those financial statements in our report dated 6 April 2016. Those financial statements do, and the abbreviated financial information does, not reflect the effects of events that occurred subsequent to the date of our report on those financial statements.

The abbreviated financial information does not contain all the disclosures required by the International Financial Reporting Standards as adopted by the European Union and with Part 9 of Book 2 of the Netherlands Civil Code. Reading the abbreviated financial information, therefore, is not a substitute for reading the audited financial statements of IHC Merwede Holding B.V.

Management’s responsibilityManagement is responsible for the preparation of the abbreviated financial information on the basis described in note 1.

Auditor’s responsibilityOur responsibility is to express an opinion on the abbreviated financial information based on our procedures, which were conducted in accordance with Dutch law, including the Dutch Standard on Auditing 810 ‘Engagements to report on summary financial statements’.

OpinionIn our opinion, the abbreviated financial information derived from the audited financial statements of IHC Merwede Holding B.V. for the year ended 31 December 2015 are consistent, in all material respects, with those financial statements, on the basis described in note 1.

Rotterdam, 6 April 2016 KPMG Accountants N.V.J.J. Visser RA

Independent auditor’s report

18 Royal IHC | Annual Report 2015

Royal IHC

P.O. Box 3, 2960 AA KinderdijkSmitweg 6, 2961 AW KinderdijkThe Netherlands

T +31 78 691 09 11