annual report – year to 31 january 2021 - martin currie

TRANSCRIPT

Registered in Scotland, no SC192761 www.martincurrieglobal.com

MARTIN CURRIE GLOBAL PORTFOLIO TRUST PLC

Annual report – year to 31 January 2021

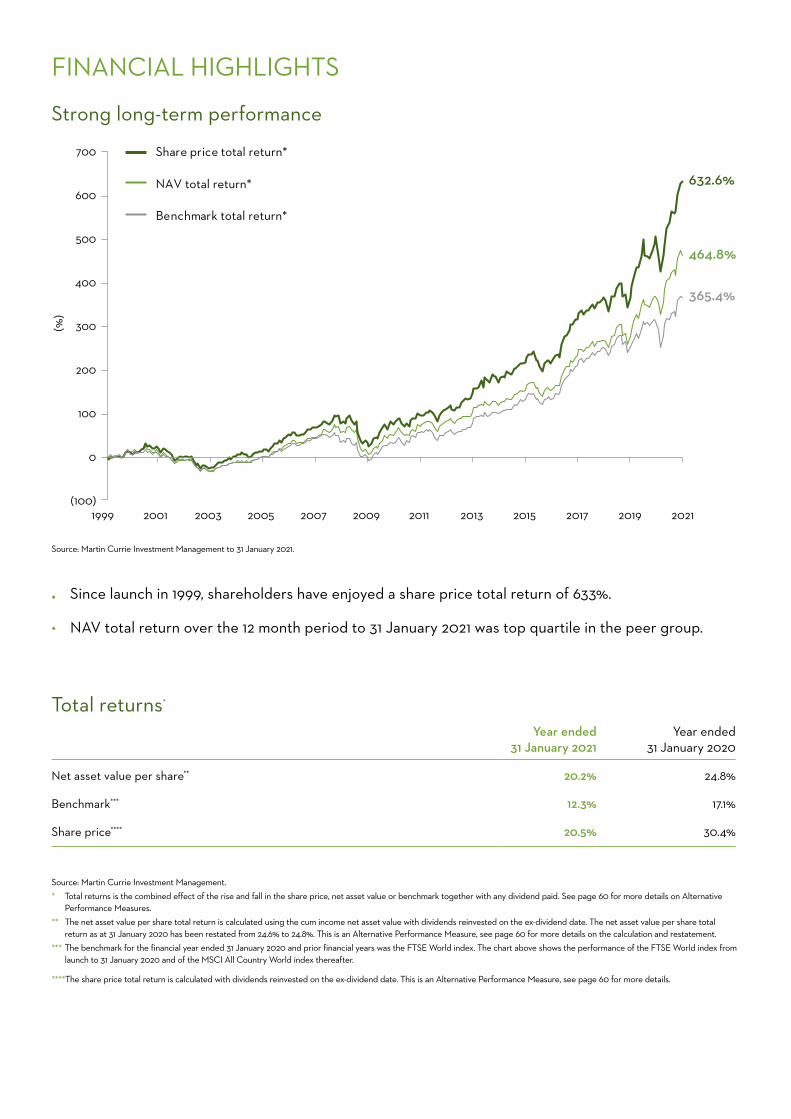

FINANCIAL HIGHLIGHTS

Strong long-term performance

• Since launch in 1999, shareholders have enjoyed a share price total return of 633%.

• NAV total return over the 12 month period to 31 January 2021 was top quartile in the peer group.

Total returns*

Year ended 31 January 2021

Year ended 31 January 2020

Net asset value per share** 20.2% 24.8%

Benchmark*** 12.3% 17.1%

Share price**** 20.5% 30.4%

Source: Martin Currie Investment Management.* Total returns is the combined effect of the rise and fall in the share price, net asset value or benchmark together with any dividend paid. See page 60 for more details on Alternative

Performance Measures.** The net asset value per share total return is calculated using the cum income net asset value with dividends reinvested on the ex-dividend date. The net asset value per share total

return as at 31 January 2020 has been restated from 24.6% to 24.8%. This is an Alternative Performance Measure, see page 60 for more details on the calculation and restatement.*** The benchmark for the financial year ended 31 January 2020 and prior financial years was the FTSE World index. The chart above shows the performance of the FTSE World index from

launch to 31 January 2020 and of the MSCI All Country World index thereafter.

**** The share price total return is calculated with dividends reinvested on the ex-dividend date. This is an Alternative Performance Measure, see page 60 for more details.

Source: Martin Currie Investment Management to 31 January 2021.

1999 2001

(%)

300

400

700

600

500

200

100

0

(100)

Share price total return*

632.6%

464.8%

365.4%

NAV total return*

Benchmark total return*

2003 2005 2007 2009 2011 2013 2015 2017 2019 2021

OverviewChairman’s statement 2

Manager’s review 5

Portfolio summary 10

Portfolio holdings 11

Strategic report 13

Board of directors 19

GovernanceReport of the directors 20

Corporate governance statement 27

Audit committee report 32

Directors’ remuneration statement 34

Financial reviewIndependent auditors’ report 36

Statement of comprehensive income 41

Statement of financial position 42

Statement of changes in equity 43

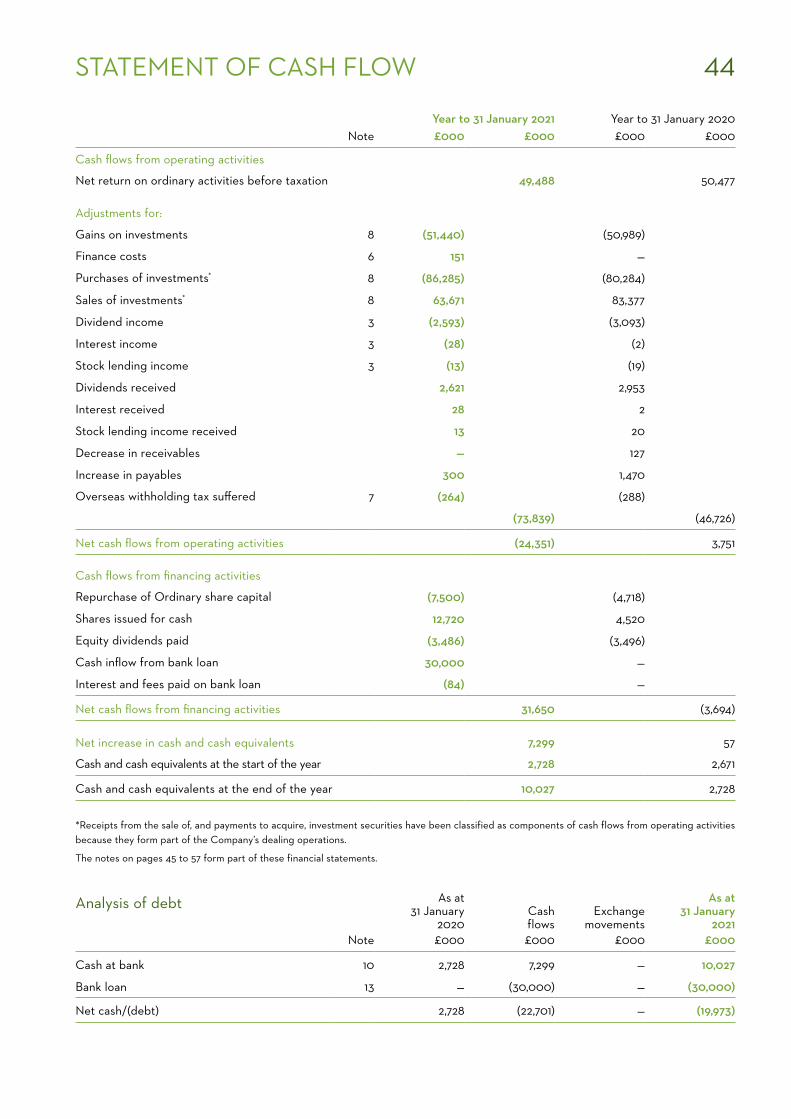

Statement of cash flow 44

Notes to the financial statements 45

Investor information

Directors and advisers 58

Stock lending disclosure 59

Alternative performance measures 60

Glossary of terms 62

Shareholder information 64

Ways to invest in the Company 65

Notice of annual general meeting 66

1ABOUT MARTIN CURRIE GLOBAL PORTFOLIO TRUST

A global strategy for long-term growthMartin Currie Global Portfolio Trust plc (‘the Company’) offers investors access to a diversified portfolio of between 25 and 40 of the world’s leading companies. It invests in global equities for long-term growth and has a strong track record of delivering capital and income growth above inflation.

Objective and PolicyThe objective is to produce long-term returns in excess of the total return from the MSCI All Country World index.

The investment policy is:

• Investing in predominantly blue chip equities with market capitalisation in excess of $3 billion.

• Investing predominantly in quality growth companies with superior share price appreciation potential based on attractive ROIC (return on invested capital), balance sheet strength and Environmental, Social and Corporate Governance ('ESG') credentials.

• A high conviction portfolio typically with 25-40 stocks, with a view to holding stocks over a long time horizon.

• Debt may be used to enhance returns to shareholders.

Proven management teamYour Board has appointed Edinburgh based Martin Currie Fund Management Limited as its Alternative Investment Fund Manager (‘AIFM’), which in turn has appointed Martin Currie Investment Management Limited (the ‘investment manager’ or the ‘manager’, who together with the AIFM, 'Martin Currie') to manage the portfolio. Under the leadership of portfolio manager, Zehrid Osmani, a specialist team analyses the world’s

stocks to find the very best ideas. Zehrid is supported by a wider team of 43 investment professionals who meet over 900 companies every year.

Managed discount The Company manages its discount to ensure that the Company’s share price trades at, or around, NAV in normal market conditions.

Total returnAll returns shown are total returns.

Capital structureAs at 31 January 2021, 84,759,499 Ordinary shares of 5p were in issue, each entitled to one vote and a further 13,916,408 shares were held in Treasury, with no entitlement to vote.

Dividends paidJanuary, April, July and October.

Cost effectiveFor the period 1 February 2020 to 31 January 2021, the investment management fee was charged at 0.4% per annum on the ex-income NAV of the Company, calculated and payable quarterly. A performance fee was also payable as detailed on page 21. With effect from 1 February 2021, the performance fee arrangement was discontinued, and the investment management fee is charged at 0.5% per annum on the first £300 million of the Company's ex-income NAV and at 0.35% on the ex-income NAV in excess of £300 million, calculated and payable quarterly.

The ongoing charges (excluding performance fee) for the year ended 31 January 2021 were 0.58% of average net assets. See page 60 for more details of Alternative Performance Measures.

CONTENTS

This is my first annual report as Chairman of the Company and I would like to start by thanking my predecessor, Neil Gaskell. Neil has expertly guided the Board while overseeing significant growth throughout his nine year tenure as a Director and Chairman and leaves the Company in excellent shape. I am delighted to be taking on the role of Chairman at this exciting time in the Company's evolution.

Investment performanceThe financial year ended 31 January 2021 has included one of the most

turbulent periods in peacetime in the modern era. At the end of January this year the news media reminded us how “normal” the world was a year ago, just before the extent of the Covid-19 pandemic became apparent. When it did, stock markets immediately became very volatile and fell sharply in March 2020 as many countries imposed various restrictions due to the pandemic. The subsequent stock market recovery has proven to be resilient and over the period under review your Company’s net asset value (NAV) total return was +20.2% with a share price total return of +20.5%, both of which compare well with a benchmark total return of +12.3%. This level of return could be labelled “strong” in any year, but in the circumstances it was exceptional.

Investment returns over the longer term have also been strong. Zehrid Osmani became the lead portfolio manager in the third quarter of 2018 and has built on the previous track record. Over three years the NAV total return was +52.2% (compared with a benchmark total return of +32.7%), over five years was +120.8% (benchmark +99.7%) and over ten years was +228.2% (benchmark +199.3%).

Income and dividends Revenue earnings per share for the period amounted to 1.97 pence, a reduction of 22% compared with the last financial year. The Company has paid three interim dividends of 0.9 pence per share and intends to pay a fourth interim dividend of 1.5 pence per share on 30 April 2021 to shareholders on the register on 9 April 2021. The total dividends with respect to the year to 31 January 2021 will be 4.2 pence per share, maintaining the same level of dividend as the previous year.

This means that dividends for the year will not be covered by net revenue earnings. The Company has substantial distributable reserves which can be used alongside current year net revenue earnings to permit the payment of the dividends already paid and the planned fourth interim dividend. The Board recognises the importance of dividends to many shareholders and our distributable reserves provide

us with the flexibility to maintain the dividend while not compromising our portfolio manager’s investment approach. The primary focus of the portfolio manager remains on capital growth and is not constrained by any income target.

Environmental Social and Corporate Governance (ESG)Martin Currie is a leading proponent of ESG as an essential element of the investment management process and the Board fully supports our manager’s approach. Active engagement not only helps to improve the investee managements’ behaviours but also supports the performance of the portfolio by deepening the investment manager’s understanding of companies.

Martin Currie has retained its triple A+ rating for Strategy and Governance, Incorporation and Active Ownership, the three categories in the United Nations Principles for Responsible Investment ('UNPRI') rating which places it among the very best of investment managers. Further, Morningstar, the investment research adviser, has awarded your Company not only a five-star rating for its performance, but the maximum ‘Five Globes’ for sustainability, the only investment trust in the AIC Global sector to have achieved this accolade and placing it in the top 2% of the over 6,700 funds around the world categorised by Morningstar as Global Equity Large Cap. Martin Currie recently published an electronic magazine 'Trust in Sustainability'. I encourage you to download a copy of this. Up to date details of current ESG initiatives are available on our website at martincurrieglobal.com.

OperationsAs well as impacting our investment portfolio, the Covid-19 pandemic has had a profound effect on the way that our investment manager and other suppliers operate. While professional service companies all have disaster recovery plans, these were generally based on an assumption that individuals may not be able to access their workplace for a few days. In practice the entire industry has been largely working from home for a year. The Board took a close interest in ensuring that we could maintain business as usual and I am pleased to report that all of our suppliers were able to continue to operate effectively under the restrictions which were brought in to control the spread of the pandemic. The Board would like to record its thanks to all involved.

2CHAIRMAN’S STATEMENT

Share issuance and buybacksAs detailed above, the Company has performed well and is experiencing significant increased demand for its shares from a wide range of investors. We continue to operate a ‘zero discount’ policy with the objective of providing shareholders, in normal market conditions, with assurance that the share price is in continuing alignment with the prevailing NAV per share and liquidity so that investors can buy or sell as many shares as they wish at a price which is not significantly different from the NAV. This involves the Company both buying back shares (which are then held in Treasury) and reissuing shares from Treasury or issuing new shares.

In February 2021 we reached a point where almost all of the Directors’ authority to issue shares on a non-preemptive basis granted at the Annual General Meeting (AGM) in July 2020 had been utilised. At a General Meeting on 10 March 2021 shareholders gave the Directors increased authority to issue up to 15% of the Company’s issued equity share capital as at 12 February 2021 on a non-preemptive basis. This renewed and increased authority expires at this year’s AGM.

At this year’s AGM we will again request that shareholders grant authority both to issue and to buy back shares so that we can continue with our established ‘zero discount’ policy as well as meet increasing new demand. Shares will only be issued at a price above the prevailing NAV per share and when the Board considers issuing shares to be in the best interests of existing shareholders. Similarly, shares will only be bought back at a discount and when in the best interests of existing shareholders. Further details of the authorities sought are set out on pages 24 and 25.

Our management companyThe acquisition of Legg Mason by Franklin Resources Inc. was announced during the financial year and completed on 31 July 2020. While most of our support functions have been integrated into the broader Franklin Templeton organisation, with the associated advantages of scale, the Board has been assured that Martin Currie will maintain its autonomy as an affiliate and its investment philosophy and processes will remain unchanged.

Management feesThe strong performance which I describe above resulted in Martin Currie earning a performance fee of £2,819,000 for the period to 31 January 2021.

Looking forward, we announced in January a simplified fee structure which includes the removal of the performance fee element. The new structure consists solely of a two-tiered management fee. The first tier applies a fee of 0.5% per annum to the first £300 million of the Company’s NAV (excluding income); the second applies a reduced fee of 0.35% per annum to NAV (excluding income) exceeding £300 million.

This is a positive step and the Board is confident that the new structure will maintain a competitive ongoing charge and contribute to increasing shareholder value.

Gearing introducedWe announced on 23 November 2020 that the Company had entered into an unsecured sterling term loan facility agreement with The Royal Bank of Scotland International Limited which was fully drawn the next day at a fixed interest rate of 1.181% for a three year term. At the time of drawing, the loan represented approximately 10% of the then NAV and at the 31 January 2021 year end, the loan represented 9.9% of NAV. While recognising that the use of the loan may increase volatility, the Board is confident in the ability of the investment manager to take advantage of this facility and deliver investment returns over the long term in excess of the cost of this debt.

The BoardAs described above, Neil Gaskell was the Chairman of the Company during the year under review and stepped down from that role on 1 February 2021.

As a result of my taking the Chair, Gary Le Sueur has taken on the role of Senior Independent Director and Christopher Metcalfe has taken over the chairmanship of the marketing and communications committee.

Neil Gaskell will not stand for re-election at this year’s AGM. The Board has decided that after Neil steps down from the Board it will continue to operate with four Directors for the time being. We will, however, keep this under regular review.

OutlookAt the time of writing many parts of the world remain affected by the Covid-19 pandemic with restrictions on movement, companies particularly in the entertainment and travel sectors unable to operate and a high proportion of the working population unable to go to their normal place of work. The development of effective vaccines provides hope that the world may return to some semblance of normality in the near future and this has been reflected in upward movements in stock market valuations. Recovery from the economic impact caused by the pandemic will not be uniform, many businesses will be damaged either permanently or will take a long time to recover and governments have incurred substantial debts in an attempt to limit economic damage. In the Board’s view, as the long-term effects unfold over time, an investment approach which focuses on a limited number of holdings researched in great depth and promising excellent growth prospects provides, we believe, an effective way to invest for the future.

Our ambition remains to grow the Company and Martin Currie, along with its parent company Franklin Resources Inc., has committed to a sales and marketing strategy with the aim of maintaining and increasing demand for the Company's shares.

3

4

Gillian WatsonChairman

20 April 2021

CHAIRMAN’S STATEMENT

Our ability to grow the Company is driven by our focus on a combination of strong investment performance, market leading ESG credentials and effective marketing. Recent performance has been recognised by increased demand for the shares which resulted in our holding an additional meeting in March 2021 to request shareholders’ approval to issue further shares on a non-preemptive basis. The Board believes that the Company is well placed to continue to deliver attractive investment returns and that this should enable us to grow the size of the Company over time.

Annual General MeetingOur AGM this year will be held at 12:30 on Wednesday 9th June in Edinburgh. Full details are in the Notice of Annual General Meeting on page 66. At the date of this report, Covid-19 restrictions remain in place which may prevent shareholders from attending the AGM in person. We have made arrangements for shareholders to submit any questions to the AGM on their proxy forms and a written response will be posted on the Company's website following the AGM. We will continue to monitor developments and if there are any changes to the AGM arrangements we will notify shareholders, post information on our website and

also announce this via a Regulatory Information Service as soon as possible. In the circumstances, shareholders are strongly advised to submit a proxy form in advance of the meeting so that your votes are registered, whether or not you intend to attend the meeting in person. If you do plan to attend in person, please check our website in the days before the meeting.

Keep in touchThe Company’s website at www.martincurrieglobal.com is a comprehensive source of information and includes regular portfolio manager updates and outlook videos, monthly performance factsheets and independent research reports. I recommend that you subscribe for regular email updates that will keep you abreast of the news on your Company.

I thank you for your continued support. Please contact me if you have any questions regarding your Company by email at: [email protected].

5

The year to the end of January 2021 was an exceptional year: the Covid-19 pandemic led to a deep global recession and the fastest fall and recovery in equity markets seen in decades. In such uncertain and challenging conditions, the Company managed to perform strongly, adding another year of outperformance to its track record. For the year ahead, we are optimistic about the outlook for equities, but cognisant of several key risks.

Year to the end of January 2021 in review

Unprecedented pandemic crisis, human resilience and mobilisation have been the highlights: the year to the end of January 2021 was exceptional in many ways

The pandemic crisis brought a deep global recession as a result of the forced lockdowns in most regions in the first half of the year. Stock markets responded with the fastest bear market since the second world war in the space of a few weeks in March. There were initial fears of a liquidity crisis (leading companies to reduce or cancel dividend payments and to secure credit lines) but this was averted by decisive and sizeable coordinated fiscal and monetary support. As a result, during a few weeks in April share prices rebounded with what was the fastest bull market since the second world war. Pledges of fiscal support by governments continued to increase, now equating to c.15% of GDP in aggregate across the world. This contributed to pushing equity markets higher throughout the summer.

On the geopolitical front, China-US tensions were de-emphasised during the pandemic crisis. The Biden victory in the US presidential election in the final quarter of the year led to more optimism in the market. Specifically, the belief is that the US approach to dealing with China will be more diplomatic and more constructive. Strongly positive vaccine results in November and December provided further optimism, pushing equity markets towards all-time highs on the hopes of a closer ending to the pandemic crisis at some point in 2021. This also triggered a much anticipated rotation away from ‘Growth’ into ‘Value’ areas of equity markets given the sizeable valuation spread that had opened prior to that and which we comment on further below.

At the company level, earnings downgrades were sizeable in the first half of 2020 as expectations were rebased to take account of the recession and reached a low point in the second quarter of 2020. Thereafter there was a shift in momentum with improved results in the third quarter. This

provided further support for equity markets later in the year.

Corporates, in general, reacted well through the crisis, managing their cost bases but also taking more ethical actions. The crisis put more emphasis on sustainability for corporates and households along with responsible corporate citizenship, leading many companies to pursue more sustainable growth strategies going forward. Finally, this crisis has shown that online platforms can be powerful disruptors, but also invaluable tools for both corporates and consumers in ensuring continuity in activity and in providing access to goods and services.

Changes to the portfolio As the pandemic crisis was unfolding in March, we reviewed all of our forecasts for all companies held, working on a scenario of a severe recession, a gradual recovery rather than a V-shaped one and with no return to previous activity levels projected until some point in 2022. We also stress-tested each company’s balance sheet and assessed its liquidity risks. That assessment was extended to the key suppliers and customers of all of the companies in which we were invested. It was probably the busiest period in our careers. We also tested our convictions on all of the holdings held in the portfolio to ensure that we retained confidence in the business models, in what was a rapidly changing environment.

During the year, we added some new holdings that increased our exposure to robotics and automation, with the purchase of Ansys in the first half of the year, which we funded through selling out of Spirax Sarco after a period of strong share price performance. We also increased our exposure to the structural growth opportunity that we foresee in the genomics space, with the purchase of world leader Illumina. We continued to build a position following its purchase of Grail which gives it an additional strong positioning in the liquid biopsy segment. Additionally, we further strengthened our exposure in the healthcare segment with the purchase of Veeva Systems which is at the forefront of bringing tailored software to drug development and commercialisation. It operates in a segment with high barriers to entry, unfulfilled demand and where the potential for growth is strong over the long term.

Towards the end of the year, we purchased Kingspan after the share price weakened, in order to increase exposure to the mid-term opportunities related to infrastructure spending and to green building initiatives that we believe provide strong long-term structural growth potential. Finally, we also purchased Wuxi Biologics, a healthcare bioprocessing company that should benefit from the shift to increasingly complex drug development and production favouring providers of tools for life science.

MANAGER’S REVIEW

6

2021/22 outlook for the Company

Macro outlook – certainty in recovery, uncertainty in magnitude of recovery

Given the severe recession that we experienced in 2020, the sizeable fiscal stimuli being pledged to kick-start economies and the more optimistic outlook post the vaccination news, it is highly likely that 2021 will be a year of strong rebound. The magnitude of this rebound is the key question.

2021 is also likely to be a peculiar year where we are faced with sluggish activity early on before economies start to fully re-open as vaccination programmes ramp up. This means that activity may remain muted in the first quarter of the year, followed by a sharp rebound beyond that, depending on the speed of the roll out of vaccinations. In our view, the key questions to focus on are how long will markets rely on the hope of an upcoming recovery if that recovery takes longer to come and what will the reaction be if it is not as strong as expected? Economic leading indicators are, for the time being, moving in the right direction and showing gradual improvements in manufacturing and stabilisation in services, which is encouraging.

Monetary and fiscal policies provide support – inflation is where the risk could lie

Fiscal support pledged throughout the world in 2020 to tackle the recession brought by the pandemic crisis has been sizeable. There will potentially be a further increase in fiscal support in 2021, and notably, in the United States, President Biden signed a huge £1.9 trillion stimulus package into law in March 2021 and has announced a sizeable investment in infrastructure over the next eight years. This support should help the recovery in economic activity in 2021 and beyond.

At the same time, monetary policy support should continue, with key central banks signalling that interest rates will remain on hold at historically low levels for extended periods of time. Central banks are apparently targeting higher levels of inflation, but it may be the case that inflationary pressures, which should temporarily increase this year helped by the low base effect and as a result of potential supply/demand friction as economies reopen fully, might not be sustained beyond this year. This is due to the many underlying deflationary pressures that we foresee, notably from technological advances. Limited wage inflation and the deterioration in labour markets arising from the pandemic crisis might also dampen price rises in some parts of the economy for the time being.

We are also cognisant of the trend for corporates to near-shore or on-shore more of their production and to shorten their supply chains as a result of the realisation that these are vulnerable to disruption. We believe that this might take time to implement and could lead to more investment in robotics and automation, which in itself could help to contain labour costs.

Economic growth in 2021 should result in strong earnings growth as recovery comes through

Given the macroeconomic picture, 2021 will see a strong rebound in corporate earnings. Consensus estimates point to a growth of +25% in year-on-year (‘YoY’) earnings in 2021 for the MSCI World index, with substantial variation by region as summed up in the table below.

Consensus Earnings Growth YoY 2020E 2021E

MSCI World -16% 25%

S&P 500 (US larger companies) -14% 24%

MSCI EU index (Europe) -25% 33%

FTSE 350 (UK) -44% 51%

Nasdaq (US growth companies) -10% 40%

MSCI Asia Pacific ex-Japan -5% 26%

Topix (Japan) -29% 32%

Source: Bloomberg and FactSet. Estimates as at 12 February 2021.

As for economic forecasts, earnings growth expectations may be inaccurate. We believe that it might well be more useful to look at the two-year growth outlook as a way both to navigate a wide forecast range and to smooth out 2021, which will show explosive growth in large part driven by the effect of such a weak 2020. Our forecasts assume that 2022 will be the year in the course of which earnings will normalise, albeit not immediately back to previous trend levels for some geographical areas such as Europe.

Equity market valuations – less supportive versus history but still supportive versus bond yields

Equity markets have performed strongly since the lows of March 2020. Valuation levels on a stand-alone price to earnings ratio look demanding compared with historic levels but we believe that, given such an unusual period in terms of earnings collapse and rebound in 2020 and 2021 respectively, investors should take account of where we are in the economic cycle. On that basis, European and Global equity valuations remain supportive, while the US equity market is closer to its historic highs.

Equity valuations in general remain attractive in terms of the earnings yields that they offer compared to bond yields. This is likely to remain the main supportive argument for an ongoing high rating of equity markets, given that interest rates are likely to remain low for extended periods of time.

MANAGER’S REVIEW

7

Market focus on sustainability trends will continue to increase and likely accelerate

The nature of the 2020 recession triggered by the pandemic crisis has put more emphasis on sustainability and responsible corporate citizenship with the opportunity to tackle some of the necessary structural reforms as economies are rebuilt. Investors have increased their focus on assessing Environmental, Social and Governance (“ESG”) criteria and we expect this to continue to gain momentum in 2021. Regulation is further driving the focus on ESG. Carbon intensity assessments and a drive to decarbonise economies by policy makers is adding to the momentum. President Biden has taken the US back into the Paris Agreement which will be material in aligning all major economies globally towards significantly reducing carbon emissions.

Given our long-established expertise in ESG and our proprietary innovative ESG risk assessment framework, we believe that the Company is very well positioned to benefit from the growing focus on sustainability. We manage a portfolio of companies with strong governance and a leading approach to managing environmental and social risks, with good overall sustainability potential.

Style rotation could remain a key debate in this supportive cyclical growth environment

With 2021 having the potential to be such a strong year of economic recovery and significant earnings rebound, market commentators are suggesting that the ‘Value’ style and smaller companies could lead the market higher. This could be further amplified by the very wide difference between the market valuations of ‘Value’ compared with ‘Growth’ stocks.

As long-term investors we find the debate around style rotation to be too short-term a consideration and prone to uncertainty. Our focus remains on finding companies with superior growth and return profiles and therefore strong earnings power over the long term, with compounding cash flow characteristics underestimated by the market. If we prove accurate in finding these sustainable quality growth stocks, we believe that they should perform well over the long term, irrespective of short-term market environments.

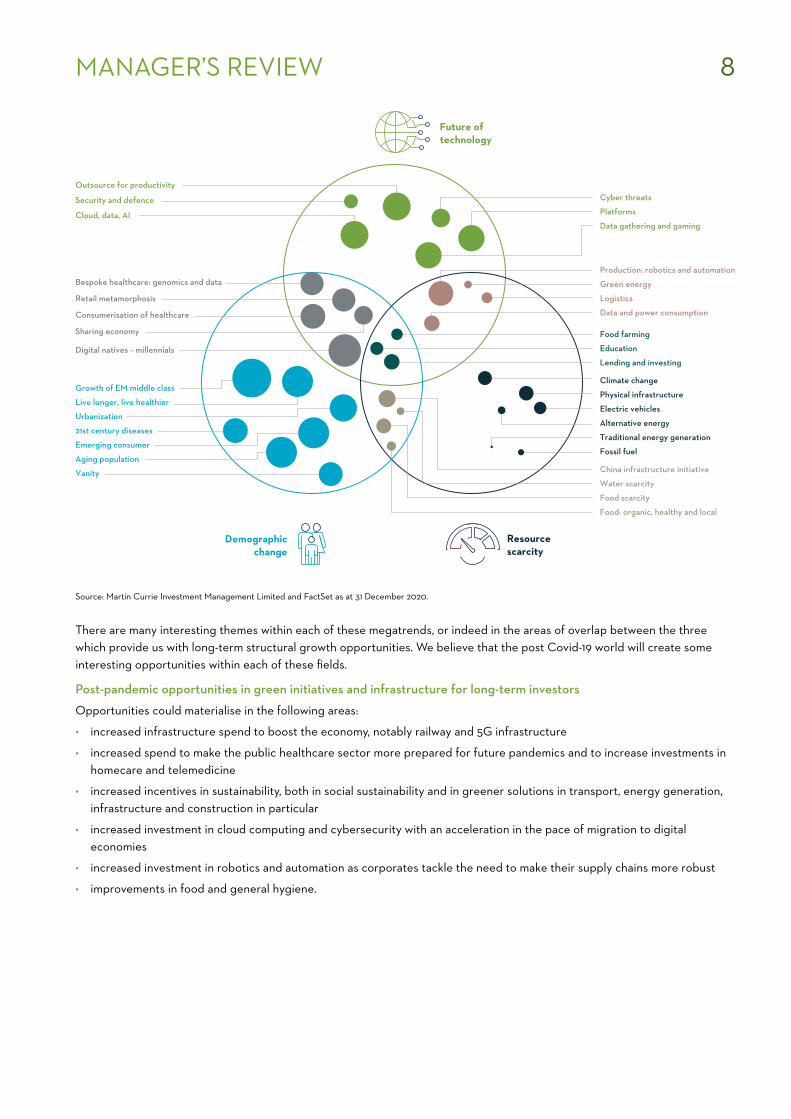

Long-term opportunities across our three megatrends

Looking ahead, it will be critical to focus on investing in companies with sustainable business models that have strong pricing power. Pricing power is particularly important if we remain in a period of low inflation and will be critical to protecting margins should we move into a period of rising inflation.

Our approach is to invest in sustainable business models that:

• have strong leadership positions

• operate in industries with high barriers to entry

• have strong pricing power

• demonstrate low disruption risk

• offer attractive structural growth prospects

• generate high returns

• have compounding characteristics and solid balance sheets

• maintain strong corporate governance and sustainability profiles.

We continue to invest guided by the Company's Investment Policy and using our thematic megatrends framework, focusing on the three trends that we have identified and which are (i) Demographic Change (ii) Future of Technology and (iii) Resource Scarcity. We assess our portfolio exposures to the megatrends and to the themes within those megatrends, as shown in the diagram overleaf.

8

Outsource for productivity

Security and defence

Cloud, data, AI

China infrastructure initiative

Water scarcity

Food scarcity

Food: organic, healthy and local

Production: robotics and automation

Green energy

Logistics

Data and power consumption

Future oftechnology

Demographicchange

Resourcescarcity

Bespoke healthcare: genomics and data

Retail metamorphosis

Consumerisation of healthcare

Sharing economy

Digital natives – millennials

Growth of EM middle class

Live longer, live healthier

Urbanization

21st century diseases

Emerging consumer

Aging population

Vanity

Climate change

Physical infrastructure

Electric vehicles

Alternative energy

Traditional energy generation

Fossil fuel

Food farming

Education

Lending and investing

Cyber threats

Platforms

Data gathering and gaming

Source: Martin Currie Investment Management Limited and FactSet as at 31 December 2020.

There are many interesting themes within each of these megatrends, or indeed in the areas of overlap between the three which provide us with long-term structural growth opportunities. We believe that the post Covid-19 world will create some interesting opportunities within each of these fields.

Post-pandemic opportunities in green initiatives and infrastructure for long-term investors

Opportunities could materialise in the following areas:

• increased infrastructure spend to boost the economy, notably railway and 5G infrastructure

• increased spend to make the public healthcare sector more prepared for future pandemics and to increase investments in homecare and telemedicine

• increased incentives in sustainability, both in social sustainability and in greener solutions in transport, energy generation, infrastructure and construction in particular

• increased investment in cloud computing and cybersecurity with an acceleration in the pace of migration to digital economies

• increased investment in robotics and automation as corporates tackle the need to make their supply chains more robust

• improvements in food and general hygiene.

MANAGER’S REVIEW

9

Zehrid OsmaniPortfolio Manager, Martin Currie Global Portfolio Trust plc Head of Global Long Term Unconstrained Equities, Martin Currie

20 April 2021

Risks for 2021 – a year of lower tail risks and more predictability, but with the potential risk of bubbles forming

In managing the portfolio we are keenly aware of the following key risks to our projections:

• Geopolitical risks will remain omnipresent, notably the China-US and China-rest of the world tensions. The unpredictability and therefore volatility risk related to this aspect has, however, significantly reduced in our view, with the US presidency shifting to an administration which will follow a more diplomatic approach in terms of interactions.

• Brexit risk remains relevant to watch – a deal was struck late last year, which is beneficial to both the UK and the EU, but there is more work to be done given that the deal only covers goods. Services will need to be tackled and the increased trade frictions that Brexit has brought could also cause issues.

• Forecast risk in economic and corporate earnings projections globally remains high, but with economies on a path towards a sharp rebound from the lows of 2020, earnings momentum should remain supportive and continue to improve.

• Pandemic relapse risk with the possibility of further waves of infection remaining high as we write. The more significant risk to highlight is the event of a mutating virus that leads to a less efficacious mass vaccination programme and a higher risk of prolonged pandemic crisis.

• Risk of bubbles in asset prices is potentially the most relevant risk to consider in 2021 and beyond. Current supportive monetary policies, with interest rates remaining low for extended periods of time, could lead to increased risk taking in the search for yield, which could lead to excess valuations.

• Increased indebtedness as a result of sizeable fiscal spending pledges across the globe has the potential to damage future growth. Higher indebtedness typically leads to subsequent periods of lower growth as debt is repaid and also increases the risk of higher taxation for both households and corporates.

• Risk of rising rates expectations The final risk worth highlighting is whether we are in a period of market euphoria based on the uncomfortable conflicting assumption that inflationary pressures will be picking up but interest rates will remain low for extended periods of time. We would expect, if inflationary pressures start building, that interest rates trend higher which could weigh on financial market sentiment.

Overall, and in conclusion, as we look at the year ahead, we believe that it will be a year based on a lower risk of unexpected events and more optimism. This will be a positive and much needed contrast to what was an exceptional and highly unpredictable year in 2020. We will be watching out for the pace of deployment of fiscal stimuli into the real economies and for any signs of meaningful inflationary trends picking up. As we write, we believe that the Company is well positioned for the mid and long-term opportunities that we highlight, as the portfolio contains some exciting businesses which are forecast to generate a strong mix of structural growth and attractive returns across a range of sectors. We will continue to ensure that we offer exposure to investments in which we have strong conviction and that we manage diversification efficiently across the various measures on which we focus.

10

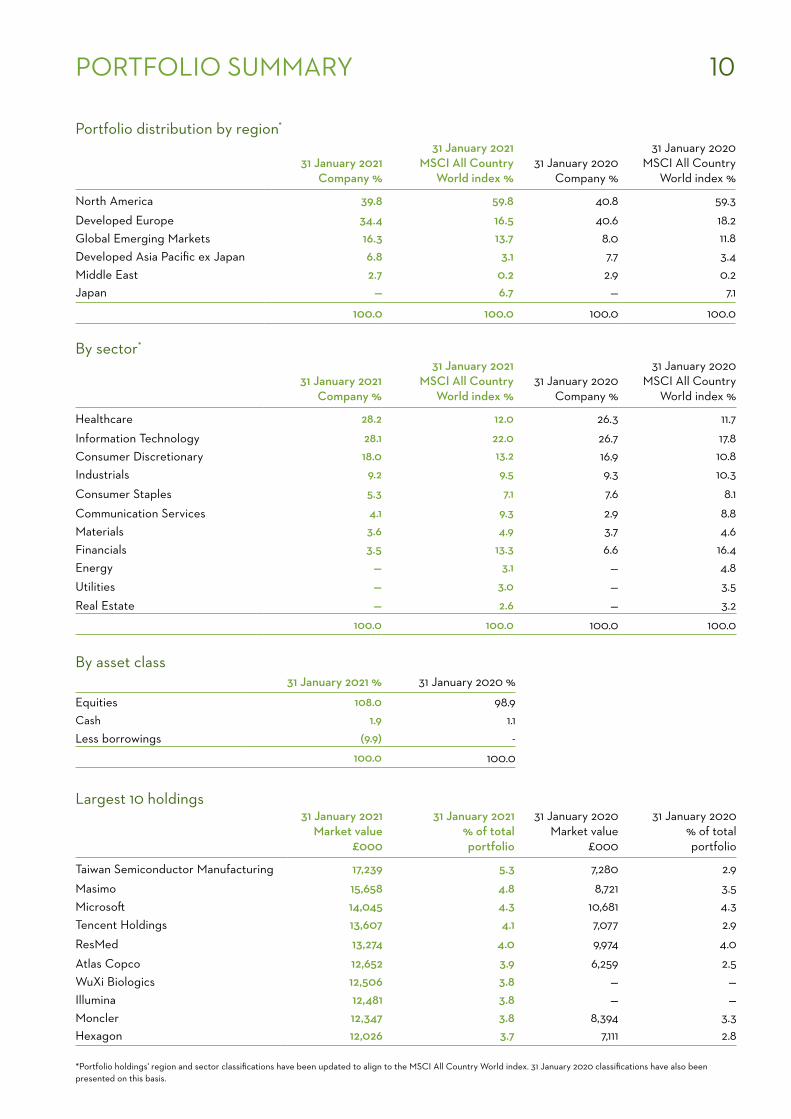

By asset class

31 January 2021 % 31 January 2020 %

Equities 108.0 98.9 Cash 1.9 1.1

Less borrowings (9.9) - 100.0 100.0

PORTFOLIO SUMMARY

Portfolio distribution by region*

31 January 2021 Company %

31 January 2021 MSCI All Country

World index %31 January 2020

Company %

31 January 2020 MSCI All Country

World index %

North America 39.8 59.8 40.8 59.3

Developed Europe 34.4 16.5 40.6 18.2 Global Emerging Markets 16.3 13.7 8.0 11.8 Developed Asia Pacific ex Japan 6.8 3.1 7.7 3.4 Middle East 2.7 0.2 2.9 0.2 Japan — 6.7 — 7.1

100.0 100.0 100.0 100.0

By sector*

31 January 2021 Company %

31 January 2021 MSCI All Country

World index %31 January 2020

Company %

31 January 2020 MSCI All Country

World index %

Healthcare 28.2 12.0 26.3 11.7

Information Technology 28.1 22.0 26.7 17.8 Consumer Discretionary 18.0 13.2 16.9 10.8 Industrials 9.2 9.5 9.3 10.3

Consumer Staples 5.3 7.1 7.6 8.1

Communication Services 4.1 9.3 2.9 8.8 Materials 3.6 4.9 3.7 4.6 Financials 3.5 13.3 6.6 16.4 Energy — 3.1 — 4.8 Utilities — 3.0 — 3.5 Real Estate — 2.6 — 3.2

100.0 100.0 100.0 100.0

Largest 10 holdings 31 January 2021

Market value £000

31 January 2021 % of total portfolio

31 January 2020 Market value

£000

31 January 2020 % of total portfolio

Taiwan Semiconductor Manufacturing 17,239 5.3 7,280 2.9

Masimo 15,658 4.8 8,721 3.5Microsoft 14,045 4.3 10,681 4.3Tencent Holdings 13,607 4.1 7,077 2.9

ResMed 13,274 4.0 9,974 4.0

Atlas Copco 12,652 3.9 6,259 2.5WuXi Biologics 12,506 3.8 — —Illumina 12,481 3.8 — —Moncler 12,347 3.8 8,394 3.3Hexagon 12,026 3.7 7,111 2.8

*Portfolio holdings' region and sector classifications have been updated to align to the MSCI All Country World index. 31 January 2020 classifications have also been presented on this basis.

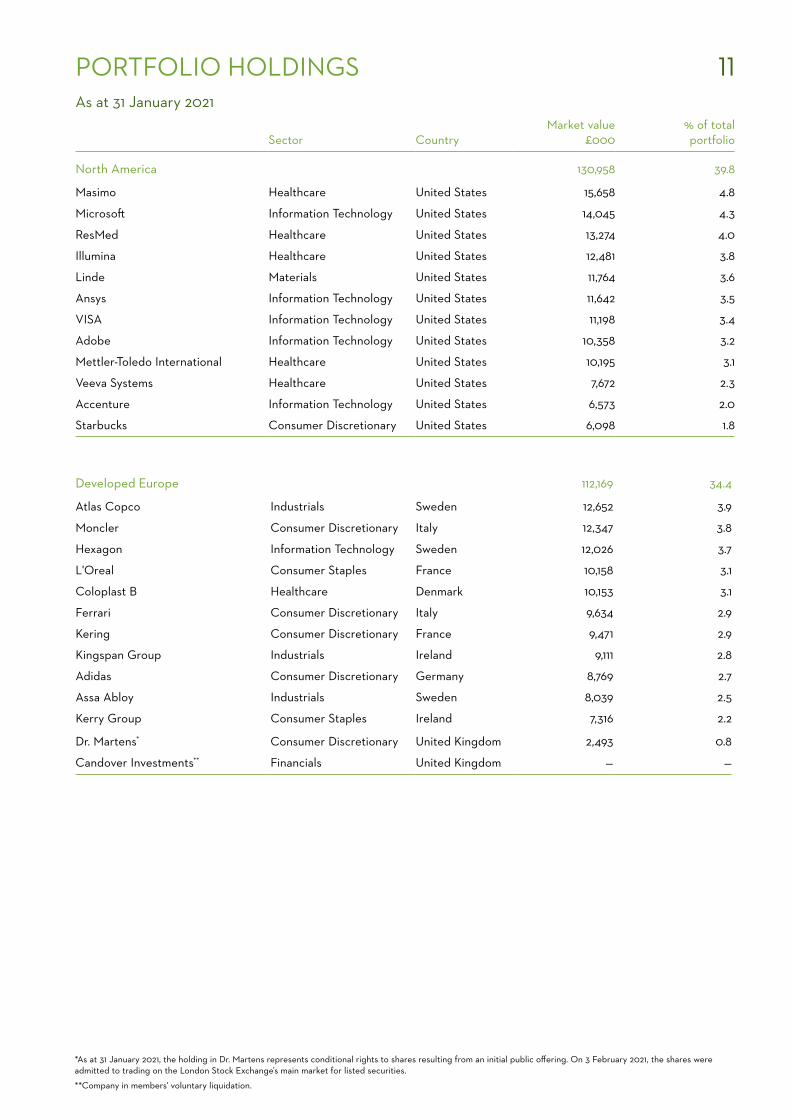

11

Sector CountryMarket value

£000% of total portfolio

North America 130,958 39.8

Masimo Healthcare United States 15,658 4.8

Microsoft Information Technology United States 14,045 4.3

ResMed Healthcare United States 13,274 4.0

Illumina Healthcare United States 12,481 3.8

Linde Materials United States 11,764 3.6

Ansys Information Technology United States 11,642 3.5

VISA Information Technology United States 11,198 3.4

Adobe Information Technology United States 10,358 3.2

Mettler-Toledo International Healthcare United States 10,195 3.1

Veeva Systems Healthcare United States 7,672 2.3

Accenture Information Technology United States 6,573 2.0

Starbucks Consumer Discretionary United States 6,098 1.8

PORTFOLIO HOLDINGS

Developed Europe 112,169 34.4

Atlas Copco Industrials Sweden 12,652 3.9

Moncler Consumer Discretionary Italy 12,347 3.8

Hexagon Information Technology Sweden 12,026 3.7

L'Oreal Consumer Staples France 10,158 3.1

Coloplast B Healthcare Denmark 10,153 3.1

Ferrari Consumer Discretionary Italy 9,634 2.9

Kering Consumer Discretionary France 9,471 2.9

Kingspan Group Industrials Ireland 9,111 2.8

Adidas Consumer Discretionary Germany 8,769 2.7

Assa Abloy Industrials Sweden 8,039 2.5

Kerry Group Consumer Staples Ireland 7,316 2.2

Dr. Martens* Consumer Discretionary United Kingdom 2,493 0.8

Candover Investments** Financials United Kingdom — —

*As at 31 January 2021, the holding in Dr. Martens represents conditional rights to shares resulting from an initial public offering. On 3 February 2021, the shares were admitted to trading on the London Stock Exchange’s main market for listed securities.

**Company in members' voluntary liquidation.

As at 31 January 2021

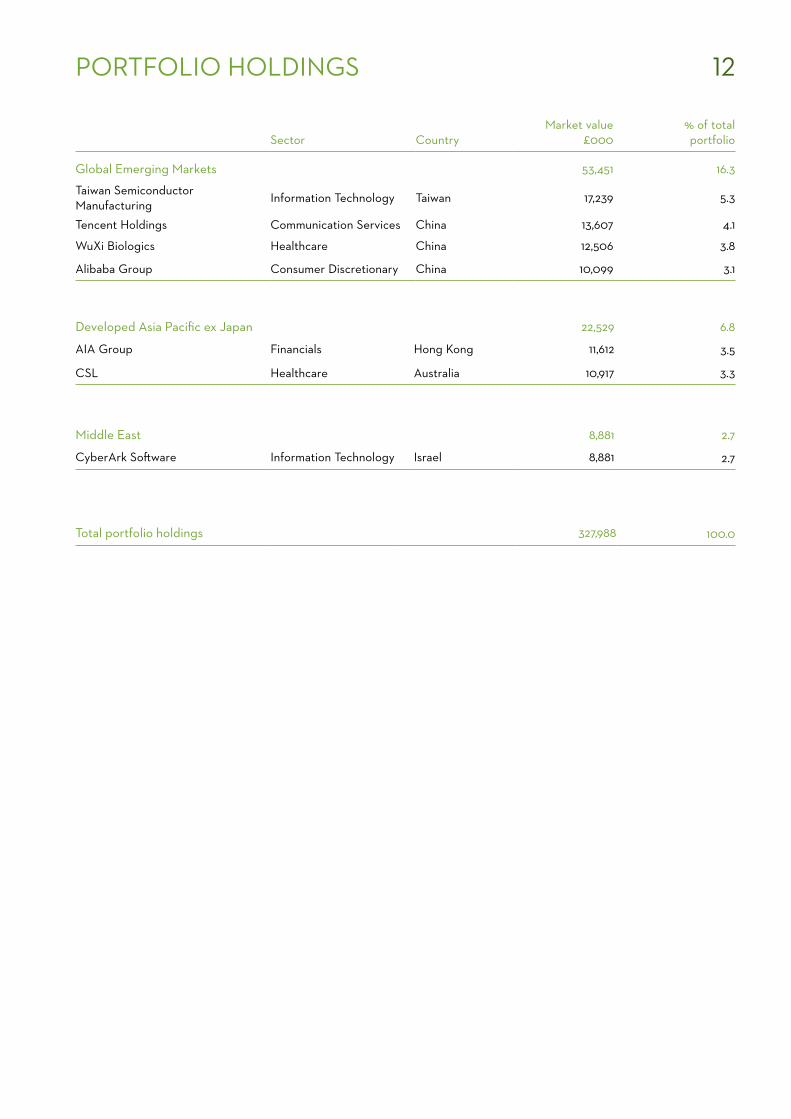

12

Total portfolio holdings 327,988 100.0

Sector CountryMarket value

£000% of total portfolio

Global Emerging Markets 53,451 16.3

Taiwan Semiconductor Manufacturing Information Technology Taiwan 17,239 5.3

Tencent Holdings Communication Services China 13,607 4.1

WuXi Biologics Healthcare China 12,506 3.8

Alibaba Group Consumer Discretionary China 10,099 3.1

Middle East 8,881 2.7

CyberArk Software Information Technology Israel 8,881 2.7

Developed Asia Pacific ex Japan 22,529 6.8

AIA Group Financials Hong Kong 11,612 3.5

CSL Healthcare Australia 10,917 3.3

PORTFOLIO HOLDINGS

13

Business modelThe investment objective and policy of the Company are detailed on page 1.

This report provides shareholders with details of the Company’s business model and strategy as well as the principal and emerging risks and challenges that it faces.

The Company has no employees and outsources its entire operational infrastructure to third-party organisations. In particular, the Board appoints and oversees an independent AIFM, which, in turn, appoints an investment manager to manage the investment portfolio. The Board sets the Company’s strategy, decides the appropriate financial policies to manage the assets and liabilities of the Company, ensures compliance with tax, legal and regulatory requirements and reports regularly to shareholders on the Company’s performance.

The Directors do not envisage any change to this model in the foreseeable future.

For more information on investment trusts in general please visit www.theaic.co.uk.

Purpose, values and strategy Purpose

To deliver a sustainable long-term total return to shareholders by investing in a global equity portfolio of high quality companies actively managed on the Company’s behalf by its investment manager.

Values

Independence: to act independently in the interests of shareholders.

Sustainability: to ensure that the companies in which the Company invests are supportive of good environmental, social and governance practices and that its investment manager encourages continuous improvement in these areas.

Transparency: to report transparently and accurately to shareholders on the condition, performance and prospects of the Company.

Culture

The Board considers that its culture of openness of debate combined with strong governance and the benefits of a diverse Board are central to delivering against its purpose, values and strategies that are discussed in this report. The Board monitors and reviews its culture as part of its annual evaluation process and monitors the culture within the investment manager to ensure that it is closely aligned with that of the Company. During the year, the Board received a presentation from the investment manager on developments in its organisational culture and its alignment to that of the Company.

Gender Diversity

Following Neil Gaskell's retirement, the Board will comprise four non-executive Directors of whom two are women and two are men.

Environmental, Social and Governance (ESG)

The Company and investment manager believe that good ESG practices are a fundamental component of a high quality company. A review of ESG practices will typically include shareholder rights, accounting standards, remuneration, board structure, supply chain, data protection, pollution/hazardous waste policies, water usage and climate change policies. The investment manager’s ESG analysis may influence key financial assumptions such as cost of capital, revenues or costs and thus the estimate of a company’s intrinsic value. These are discussed in greater detail on page 7. A poor governance, environmental or social track record for a company can indicate wider sustainability issues and could lessen the attractiveness of the investment.

ESG issues are integral to the Company’s investment philosophy, and the approach taken by the investment manager has been rewarded with the highest possible rating (A+) from the UNPRI across its three key criteria and is a ‘tier 1‘ signatory of the UK Stewardship Code 2012 issued by the UK Financial Reporting Council (FRC).

StrategiesInvestment

In order to achieve its investment objective, the Company has adopted a distinctive philosophy in implementing its investment policy. This clearly focuses on using the investment manager’s ability to combine investment performance with socially responsible investment. This is done through their leading global research capabilities in identifying high-quality companies that will benefit from exposure to growth megatrends worldwide and their leading performance in engaging with these companies on ESG issues.

The Company invests predominantly in blue chip equities with a market capitalisation in excess of $3 billion and selects quality growth companies which are market leaders in their industries with superior share price appreciation potential based on attractive return on invested capital (ROIC), balance sheet strength and ESG credentials as described above.

The resulting diversified portfolio of between 25 and 40 international quoted companies as listed on pages 10 to 12 is actively managed and concentrated, focusing on high conviction stocks selected on the basis of detailed research analysis. This active portfolio management policy will inevitably involve some periods when the Company’s portfolio outperforms or underperforms the Company’s benchmark.

The Board does not impose any limits on the investment manager’s discretion to select individual stocks. The investment manager ensures that investment risk is dominated by the high conviction stocks in the portfolio within the guidelines set by the Board and that the combination of stocks held does not lead to unintended reliance on a particular macroeconomic factor (for example, a higher oil price or lower interest rates).

STRATEGIC REPORT

14

Current asset allocation and actual holdings are discussed in the Manager’s review on page 5 and details are contained in the portfolio summary and portfolio holdings on pages 10 to 12.

Risk management

Risk management is largely focused on managing investment risk in accordance with the investment policy guidelines set by the Board. Following the appointment of an external AIFM as detailed in the Report of the directors on page 20, the AIFM is required under the AIFM Regulations to establish a permanent and independent risk management function and implement a comprehensive and effective risk management policy covering the risks associated with the management of the Company’s portfolio. Subject to the oversight of the Board, the AIFM has established risk parameters with the investment manager within which the portfolio is managed. The AIFM monitors the relevant risk parameters, including leverage, and periodically assesses the portfolio’s sensitivity to key risks.

At each Board meeting, the Board reviews the relevant risk metrics presented by the investment manager to ensure that there is sufficient but not excessive risk being taken within the portfolio.

The wider corporate risks relate mainly to the challenges of managing the Company in an increasingly regulated and competitive market place. These risks are each actively managed using the mitigation measures which the Board has put in place and which are discussed on page 17 of this report.

Marketing

The marketing strategy seeks to expand the shareholder base through increased engagement with key audiences, using the most appropriate promotional techniques. Deepening demand for the Company’s shares should enable growth over time in the number of shares in issue, improve the efficiency of the Company and increase liquidity in its shares.

This is supported by a commitment to provide clear, transparent and regular communication to shareholders delivered primarily through the Franklin Templeton UK Distribution team and the Company’s website which contains information relating to performance, outlook and significant developments as they occur as well as interviews with the portfolio manager, Zehrid Osmani. In addition, the Company utilises marketing tools such as advertising, social media, public relations and research. The portfolio manager also meets regularly with existing and potential institutional shareholders, including private wealth managers.

Financial

The Company's main financial strategic goals are:

• the management of shareholder capital;

• the use of gearing; and

• the management of the risks to the assets and liabilities of the Company.

The Board’s principal aim for the management of shareholder capital is the achievement of long-term total return. Growth should incorporate both the investment manager’s investment performance and the issuance of shares when sufficient demand exists to do this without diluting the value of existing shareholder capital. However, the Board has also maintained or increased dividends each year since the Company’s launch in 1999 and remains committed to delivering a strong long-term total return performance on shareholder capital.

The Company operates a ‘zero discount’ policy with the objective of providing shareholders, in normal market conditions, with assurance that the Company’s share price is in continuing alignment with the prevailing net asset value per share (“NAV”) and liquidity so that investors can buy or sell as many shares as they wish at a price which is not significantly different from the NAV. This involves the Company both buying back shares and reissuing shares from Treasury or issuing new shares. Shares bought back as part of this policy are held in Treasury and reissued when demand exists which the market cannot supply.

Discount is an Alternative Performance Measure, see page 60 for more details.

On 23 November 2020, the Company entered into an unsecured three year £30 million sterling term loan facility agreement with The Royal Bank of Scotland International Limited.

The facility was drawn down in full on 24 November 2020 at a fixed interest rate of 1.181% and for a fixed term of three years. The Company has no other borrowings. The Company’s gearing position was 10.2% (being the debt:equity ratio) at the time of draw down.

The Board imposes borrowing limits to ensure that gearing levels are appropriate and reviews these on a regular basis. Current guidelines state that the total borrowings will not exceed 20% of the net assets of the Company at the time of drawdown. The Board monitors the Company’s gearing closely and takes a prudent approach.

Gearing is an Alternative Performance Measure, see page 60 for more details.

The Company does not currently use derivatives for the purpose of mitigating investment risk, although the investment manager may hedge an excessive concentration of currency risk into sterling should this situation arise. Risk management is discussed further on page 16.

The Board is committed to its policy of keeping shareholders regularly informed about the Company’s performance and, in particular, giving an objective and transparent report on the underlying investment performance of the investment manager. The formal annual and half-yearly financial statements provide a comprehensive review of the overall position, compliant with best practice as recommended by the Financial Reporting Council.

STRATEGIC REPORT

15

Principal developments and future prospects

The Board’s main focus is the achievement of a competitive total annual return. The future of the Company is dependent upon the success of the investment strategy in light of economic factors and developments in equity markets. The outlook and future prospects for the Company are discussed in both the Chairman’s statement on page 3 and in the Manager’s review on pages 5 to 9. In particular, the continuing impact of Covid-19 is discussed on pages 2, 3 and 9.

The Board continues to monitor the impact of the UK's departure from the European Union and to assess the potential consequences for the Company’s future activities. The Board does not believe that these uncertainties are material for the Company.

Duty to promote the success of the Company

The Company is required to provide a statement which describes how the Directors have had regard to the matters set out in Section 172 of the Companies Act 2006 (the "Section 172 matters") when performing their duty to promote the success of the Company, including:

• The likely consequences of any decision in the long term;

• The interests of the Company’s employees;

• The need to foster the Company’s business relationships with suppliers, customers, and others;

• The impact of the Company’s operations on the community and the environment;

• The desirability of the Company maintaining a reputation for high standards of business conduct; and

• The need to act fairly as between members of the Company.

The Board is focused on promoting the long-term success of the Company and regularly reviews the Company’s long-term strategic objectives, including consideration of the impact of the investment manager’s actions on the marketability and reputation of the Company and the likely impact on the Company’s stakeholders of the Company’s principal strategies.

The main stakeholders in the Company are its shareholders, its lender and a number of external third-party suppliers who provide investment management, company secretarial, depositary, custodial, banking, registry and legal services along with the wider community in which the Company operates.

The Company, as an investment trust, does not have any employees and its customers are also its shareholders. The primary purpose of the Company is to deliver long-term returns for shareholders from a portfolio of investments. Continued shareholder support and engagement are critical to the existence of the Company and the delivery

of its long-term strategy. The Board and the investment manager recognise the importance of engaging with shareholders on a regular basis in order to maintain a high level of transparency and accountability and to inform the Company’s decision making and future strategy.

Alongside shareholders’ equity, the Company has, since November 2020, been partly funded by debt. The Company’s debt is subject to contractual terms and restrictions. The Company has a procedure in place to report regularly to its lender on compliance with debt terms.

The management engagement committee is tasked with reviewing the performance of the investment manager and the audit committee receives reports from and reviews the service, quality and value for money provided by other third-party suppliers.

The investment manager is tasked with maintaining a constructive relationship with such other third-party suppliers, on behalf of the Company. It is the Board’s policy that all payments due to suppliers will be made in full and on time.

The Board is responsible for setting the strategic priorities of the Company along with monitoring its corporate governance and risk and controls. It is also responsible for monitoring the investment performance and marketing activities undertaken by the investment manager on its behalf.

The Board is committed to maintaining and demonstrating high standards of corporate governance and the Company’s corporate governance statement is set out on pages 27 to 31 and, together with the compliance statement on page 27, details how the Company maintains high standards of business conduct.

The Company works closely with the investment manager to develop and monitor its investment strategy and activities, not only to achieve its investment objective, but also to deliver the Company’s values of Independence, Sustainability and Transparency, which are discussed further on page 13. The Board also expects good governance standards to be maintained at the companies in which the Company is invested and reviews the engagement and voting activities which are undertaken by the investment manager. Further details of the ESG engagement during the year are discussed in the Chairman’s statement on page 2 with the Company’s purpose, values and strategy outlined on page 13. The ESG strategy followed by the Company and the investment manager is detailed on page 7.

16

During the year, the Board took a number of key decisions which required the Directors to have regard to the Section 172 matters referred to above:

• As detailed in previous annual reports, the Board has kept the possibility of gearing under active consideration and, following an assessment of the market outlook and the cost of debt, the Board decided during the year that it is now in the best interests of the Company that it has a modest level of structural gearing consistent with the gearing policy. Further information on the nature and level of the Company’s gearing is set out on page 60.

• Further to the decision to employ gearing, the Board appointed Martin Currie Fund Management Limited as the Company's external AIFM and State Street Trustees Limited as depositary in accordance with the AIFM Regulations. Further information on the appointment of an external AIFM and depositary is set out in the Report of the directors on pages 20 and 21, respectively.

• Following a review during the year, the Board agreed a new fee structure with the AIFM and investment manager that it believes will contribute to a stable and competitive ongoing charge, which will increase shareholder value as the net asset value grows. Further information on the changes to the management and performance fees is set out in the Report of the directors on page 21.

• In line with the succession plan indicated in the half-yearly financial report, it was decided that Neil Gaskell would step down as Chairman of the Board to be succeeded by Gillian Watson as Chairman on 1 February 2021. Further information on the composition of the Board is set out in the Corporate governance report on page 28.

• The Board continued to monitor the operation of the 'zero discount' policy, which it believes helps to give all shareholders assurance of continuing alignment between NAV and the share price together with liquidity. Shortly after the financial year end, on 9 February 2021 and in light of increased demand for the Company’s shares, the Board announced that it would seek permission from shareholders to renew and increase the authority to issue shares. Further authority was granted at a General Meeting on 10 March 2021. See page 57 for details.

The Board receives regular reports from the investment manager on shareholder engagement, with the investment manager tasked with maintaining regular and open dialogue with larger shareholders. Directors, primarily through the Chairman, also meet regularly with major shareholders to understand their views and to help inform the Board’s decision making process. The Company maintains an award-winning website which hosts copies of the annual and half-yearly reports along with factsheets and other relevant materials. Shareholders are, where possible, also invited to attend the AGM at which they have the opportunity to speak directly with Directors.

At the date of this report, Covid-19 restrictions remain in place which may prevent shareholders from attending the AGM to be held on 9 June 2021. To ensure that shareholders still have an opportunity to engage with the Board, shareholders will be able to submit questions to the AGM on their proxy forms. Responses to any questions received and the minutes of the meeting will be published on the Company's website. Further information regarding the Company’s AGM arrangements is set out in the Report of the directors on page 24 and the Notice of annual general meeting on page 66.

Principal and emerging risks and uncertainties

Risk and mitigation

The Company’s business model is longstanding and resilient to most of the short-term operational uncertainties that it faces. The Board believes that these are effectively mitigated by the internal controls established by the Board and by the AIFM and their combined oversight of the investment manager, as described in the table below. Its principal risks and uncertainties are therefore largely long-term and driven by the inherent uncertainties of investing in global equity markets.

Operational and management risks are regularly monitored by the AIFM and additionally by the Board at Board meetings and the Board’s planned mitigation measures for the principal and emerging risks are described below. As part of its annual strategy meeting, the Board carries out a robust assessment of the principal and emerging risks facing the Company, including those that would threaten its business model, future performance, solvency or liquidity.

As part of its assessment, the Board recognised that gearing was a new risk to the Company. Further details are set out below.

Gearing risk

As set out on page 14, the Company entered¬into an unsecured term loan facility agreement during the year. Whilst the use of borrowings should enhance the NAV total return where the return on the Company’s underlying assets is rising and exceeds the cost of borrowing, it will have the opposite effect where the underlying return is falling, further reducing the NAV total return. As a result, the use of borrowings by the Company may increase the volatility of the NAV. To mitigate against the gearing risk, the Board has set a limit on total borrowings and monitors the Company’s gearing closely. While the risks associated with gearing are new to the Company, the Board believes that such risks are mitigated and that gearing can enhance returns to shareholders over the long term. The Board does not consider that the gearing represents a principal risk to the Company.

STRATEGIC REPORT

17

Risk Mitigation

Pandemic risk In 2020 Covid-19 delivered an abrupt, exogenous shock to the global economy of considerable magnitude, the after effects of which continue. The Company was exposed to falling equity markets and market volatility, while the operational resilience of service providers to the Company could have been reduced.

The Board receives regular reporting on the ability of Martin Currie and other key service providers to operate in the working environment created by Covid-19. Business continuity plans were invoked last year and continue to operate satisfactorily, with operational resilience preserved. The investment manager continues to monitor the portfolio and the income deriving from it in light of the potential risks arising from the pandemic. Further information on Covid-19 is set out in the Chairman’s statement on pages 2 and 3, and in the Manager’s review on page 9.

Sustained investment underperformance

The Board monitors the implementation and results of the investment process with the portfolio manager, who attends all Board meetings and reviews data that shows statistical measures of the Company’s risk profile. Should investment underperformance be sustained despite the mitigation measures taken by the investment manager, the Board would assess the cause and take appropriate action to manage this risk.

Material decline in market capitalisation of the Company

The Board recognises that the ‘zero discount’ policy allows new shareholders to purchase shares and current shareholders to sell their shares at close to NAV, in normal market conditions. Although this level of liquidity encourages investment in the Company, it could also increase the risk of a material decline in the size of the Company. The Board monitors the performance and pace of buybacks and the Company's shareholder profile. The Board believes that good long-term performance will increase demand for the Company's shares and, subject to overall market stability, permit the market capitalisation of the Company to increase.

Loss of s1158-9 tax status

Loss of s1158-9 tax status would have serious consequences for the attractiveness of the Company’s shares. The Board considers that, given the regular oversight of this risk by the audit committee, the AIFM and the investment manager, the likelihood of this risk occurring is minimal. The audit committee regularly reviews the eligibility conditions and the Company’s compliance against each, including the minimum dividend requirements and shareholder composition for close company status.

Following the ongoing assessment of the principal and emerging risks facing the Company, and its current position, the Board is confident that the Company will be able to continue in operation and meet its liabilities as they fall due. The Board believes that the processes of internal control that the Company has adopted and oversight by Martin Currie continue to be effective.

As a consequence of the Board's annual review of risks, the Board has identified the following principal risks to the Company:

18

1. Net asset value performance relative to benchmark

The Board assessed the net asset value total return compared to the benchmark. It is measured on a financial year basis and assessed over a rolling three year period. For the year ended 31 January 2021 the benchmark was the total return of the MSCI All Country World index. Prior to 1 February 2020 the benchmark was the total return of the FTSE All-World index.

The KPI was achieved for the period. The return of the Company was 52.17% and the benchmark 32.74% for the three years to 31 January 2021.

2. Performance against the Company’s peers

The Board monitors the share price total return performance versus all competitor funds within the AIC Global sector over a rolling three year period.

The share price total return for the Company was 56.73% over the three years to 31 January 2021 which ranked 4th out of 15. The share price total return of the Company ranked 3rd out of 15 in the AIC Global sector for the financial year ended 31 January 2021.

3. Ongoing charges

The Board monitors ongoing charges on a regular basis to ensure that it meets its target by maintaining cost discipline and its focus on value adding activities. The ongoing charges figure excludes the performance fee. The KPI was met for the year at 0.58%.

Gillian WatsonChairman 20 April 2021

Key Performance Indicators and Performance

The Board uses certain key performance indicators (‘KPIs’) to monitor and assess its performance in achieving the Company’s objectives.

Summary of KPIs Target 2021 Achieved 2020 Achieved

1. Net asset value performance relative to benchmark (over 3 years)

Outperform 19.43% Yes 8.46% Yes

2. Performance against Company’s peers (over 3 years)

Top third performance 4th out of 15 Yes 7th out of 16 No

3. Ongoing charges Less than 0.70% 0.58% Yes 0.61% Yes

STRATEGIC REPORT

19BOARD OF DIRECTORS

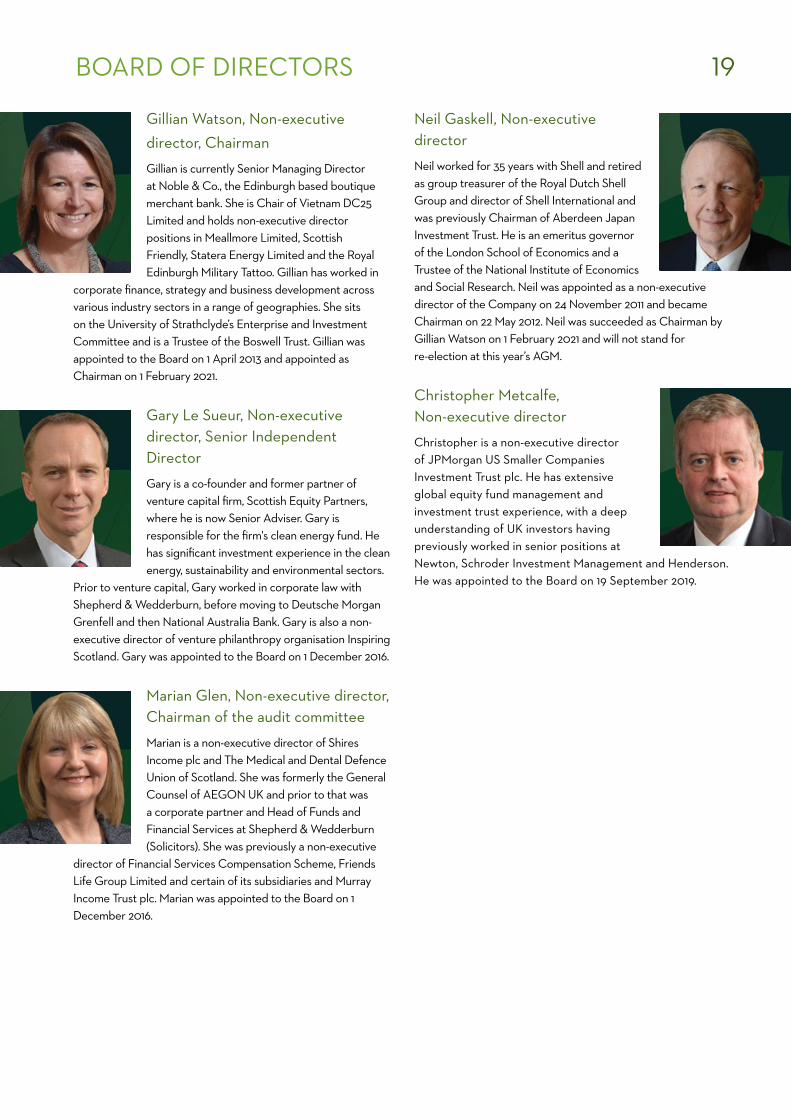

Gillian Watson, Non-executive director, Chairman

Gillian is currently Senior Managing Director at Noble & Co., the Edinburgh based boutique merchant bank. She is Chair of Vietnam DC25 Limited and holds non-executive director positions in Meallmore Limited, Scottish Friendly, Statera Energy Limited and the Royal Edinburgh Military Tattoo. Gillian has worked in

corporate finance, strategy and business development across various industry sectors in a range of geographies. She sits on the University of Strathclyde’s Enterprise and Investment Committee and is a Trustee of the Boswell Trust. Gillian was appointed to the Board on 1 April 2013 and appointed as Chairman on 1 February 2021.

Gary Le Sueur, Non-executive director, Senior Independent Director

Gary is a co-founder and former partner of venture capital firm, Scottish Equity Partners, where he is now Senior Adviser. Gary is responsible for the firm's clean energy fund. He has significant investment experience in the clean energy, sustainability and environmental sectors.

Prior to venture capital, Gary worked in corporate law with Shepherd & Wedderburn, before moving to Deutsche Morgan Grenfell and then National Australia Bank. Gary is also a non-executive director of venture philanthropy organisation Inspiring Scotland. Gary was appointed to the Board on 1 December 2016.

Marian Glen, Non-executive director, Chairman of the audit committee

Marian is a non-executive director of Shires Income plc and The Medical and Dental Defence Union of Scotland. She was formerly the General Counsel of AEGON UK and prior to that was a corporate partner and Head of Funds and Financial Services at Shepherd & Wedderburn (Solicitors). She was previously a non-executive

director of Financial Services Compensation Scheme, Friends Life Group Limited and certain of its subsidiaries and Murray Income Trust plc. Marian was appointed to the Board on 1 December 2016.

Neil Gaskell, Non-executive director

Neil worked for 35 years with Shell and retired as group treasurer of the Royal Dutch Shell Group and director of Shell International and was previously Chairman of Aberdeen Japan Investment Trust. He is an emeritus governor of the London School of Economics and a Trustee of the National Institute of Economics and Social Research. Neil was appointed as a non-executive director of the Company on 24 November 2011 and became Chairman on 22 May 2012. Neil was succeeded as Chairman by Gillian Watson on 1 February 2021 and will not stand for re-election at this year’s AGM.

Christopher Metcalfe, Non-executive director

Christopher is a non-executive director of JPMorgan US Smaller Companies Investment Trust plc. He has extensive global equity fund management and investment trust experience, with a deep understanding of UK investors having previously worked in senior positions at Newton, Schroder Investment Management and Henderson. He was appointed to the Board on 19 September 2019.

20

Status

The Company is registered as a public limited company in Scotland under number SC192761 and is an investment company as defined by Section 833 of the Companies Act 2006. It is a member of the Association of Investment Companies (the ‘AIC’).

The Company has been accepted by HM Revenue & Customs as an investment trust subject to it continuing to meet the relevant eligibility conditions of Section 1158 of the Corporation Tax Act 2010 and the ongoing requirements of Part 2 Chapter 3 Statutory Instrument 2011/2999 for all financial years commencing on or after 1 April 2012.

The Directors are of the opinion that the Company has conducted its affairs for the year ended 31 January 2021 so as to enable it to comply with the ongoing requirements for investment trust status.

Business reviewAppointment of an external AIFM

As detailed in the Chairman’s statement on pages 2 to 4, the Board decided during the year that it was in the best interests of the Company that it has a modest level of structural gearing consistent with the gearing policy. In accordance with the terms of the AIFM Regulations, it was therefore necessary for the Company to appoint an external AIFM as indicated in last year’s annual report.

With effect from 23 November 2020, Martin Currie Fund Management Limited (the 'AIFM'), an associated company of Martin Currie Investment Management Limited (the ‘investment manager’ or the ‘manager’, who together with the AIFM, 'Martin Currie'), was appointed to act as the Company's AIFM pursuant to an alternative investment fund management agreement (the ‘AIFM agreement’) in substitution for, and on materially the same commercial terms as, the Company’s previous investment management agreement with the investment manager. The AIFM has been authorised by the FCA to act as an AIFM.

The AIFM has delegated the function of managing the Company’s investment portfolio to the investment manager, the manager of the Company’s assets since its launch in 1999. There have therefore been no changes to the individuals managing the assets of the Company, nor to the way in which the Company’s assets are invested.

The ultimate parent company of the AIFM is Franklin Resources Inc ('Franklin'). The AIFM has delegated certain administration and support functions to other Franklin entities.

The AIFM and investment manager

Martin Currie is an international equity specialist based in Edinburgh, managing money for a wide range of global clients. Its investment process is focused on selecting stocks through fundamental proprietary research and constructing well balanced high conviction portfolios. The Board closely monitors investment performance and Zehrid Osmani, the portfolio manager, attends each Board meeting to present a detailed update to the Board. The Board uses this opportunity to challenge the portfolio manager on any aspect of the portfolio’s management.

Continued appointment of the AIFM

The Board conducts an annual performance appraisal of the investment manager, and now the AIFM, against a number of criteria, including operational performance, results and investment performance and other contractual considerations.

Following the recent appraisal carried out by the management engagement committee in January 2021, the Board considers that it is in the best interests of shareholders to continue with the appointment of Martin Currie Fund Management Limited as AIFM. The AIFM has delegated investment management to the investment manager and the Board remains content with this arrangement. As part of this year’s appraisal, the Board received an update on the acquisition of Legg Mason by Franklin Resources, which completed in July 2020, and was assured that Martin Currie continues to maintain its autonomy as an affiliate and its investment philosophy and processes remain unchanged.

Main features of the contractual arrangement with the AIFM (the 'AIFM agreement'):

The AIFM agreement contains materially the same commercial terms as the Company’s previous agreement with the investment manager, including:

• Six month notice period.

• Immediate termination if the AIFM ceases to be capable of carrying on investment business.

• In the event that the Company terminates the agreement otherwise than as set out above, the AIFM is entitled to receive compensation equivalent to four times the basic quarterly investment management fee payable.

Notwithstanding the appointment of the AIFM, company secretarial and certain administrative services continue to be provided to the Company by the investment manager pursuant to a separate secretarial services agreement.

REPORT OF THE DIRECTORS

The Directors present their report and the audited financial statements of the Company for the year ended 31 January 2021.

21

Investment management fee and secretarial services fee for the period from 1 February 2020 to 31 January 20211

During the year ended 31 January 2021, Martin Currie was paid an annual investment management fee of 0.4 % (2020: 0.4%) of the ex-income NAV of the Company, calculated and payable quarterly. Martin Currie Investment Management Limited also provides secretarial and administration services to the Company; the annual secretarial fee for the year ended was £55,088 plus VAT (2020: £54,452 plus VAT).

Performance fee for the period 1 February 2020 to 31 January 20211

The AIFM is entitled to a performance fee for the year ended 31 January 2021 should certain criteria be met. The key terms and related definitions of the calculation of the performance fee are summarised below.

• If the cumulative performance over this period is less than or equal to one per cent., then no performance fee is payable.

• If the cumulative performance over this period is greater than one per cent., a performance fee is payable which is based on 12.5 per cent. of the cumulative performance during the period.

• The maximum performance fee payable in respect of the period is one per cent. of the Company’s net asset value (as defined below) as at the last day of the period.

Definitions for performance fee for the year ended 31 January 2021

• 'cumulative performance' means the percentage change in the Company’s cum-income net asset value per share adjusted to include dividends announced by the Company with effect from the date that they are marked ex-dividend during the relevant period and the impact of the reinvestment of such dividends to the financial year end, adjusted for the impact of share buy backs and issues of ordinary shares out of Treasury and any provision for the performance fee, less the percentage change in the total return of the MSCI All Country World index (the Company’s benchmark) over the relevant period.

• ‘net asset value’ means the Company’s total assets (excluding income) less any liabilities it has, before any provision for performance fee and adjusted for the impact of share buy backs and issues of ordinary shares out of Treasury.

The cumulative performance in the year ended 31 January 2021 was 8.81%. As at 31 January 2021 a performance fee of £2,819,000 was payable.

Investment management fee with effect from 1 February 2021 and termination of performance fee1