annual report2013 - dawood family takaful limited · 2016-12-05 · this refers to participation of...

TRANSCRIPT

ANNUAL

Partner for life

REPORT2013

Salamti

Financial Protection & Savings Growth

* Avail Income tax relief on paid contributions.

Sum Cover.

Net PIA value accumulated atthe time of death.

In the Event of Death

Net PIA Value accumulated atthe time of Maturity.

Distributable surplus from theWaqf Fund, if any.

Maturity Benefits

Sukoon

Endowment for Retirement

* Avail Income tax relief on paid contributions.

Sum Cover.

Net PIA value accumulated atthe time of death.

In the Event of Death

Sum Cover.

Net PIA Value accumulated atthe time of Maturity.

Distributable surplus from theWaqf Fund, if any.

Maturity Benefits

Samar

Child Education & Marriage Plan

* Avail Income tax relief on paid contributions.

Plan Contribution Benefit.

Family Income Benefit.

Sum Cover, in case ofaccidental Death.

In the Event of Death

Net PIA Value available atMaturity.

Distributable surplus from theWaqf Fund, if any.

Maturity Benefits

Sahulat

After 15 years

After 16 years

After 17 years

After 18 years

After 19 years+

Loyalty Reward

From 11th Year

Special Reward

@ 10th year

@ 15th year

@ 20th year

Every 5 years

3 Choose Term

3 Choose Amount

Financial Protection & Savings Growth

* Avail Income tax relief on paid contributions.

Sum Cover.

Higher of early maturity sumcover or PIA.

Distributable surplus from theWaqf Fund, if any.

In the Event of Death

Higher of early maturity sumcover or PIA.

Distributable surplus from theWaqf Fund, if any.

Early Maturity Benefits

Salary Saving

Salary Savings Plan

* Avail Income tax relief on paid contributions.

Sum Cover.

Net PIA value accumulated atthe time of death

In the Event of Death

Net PIA value accumulated atthe time of Maturity.

Distributable surplus from theWaqf Fund, if any.

Maturity Benefits

Single Contribution

Financial Protection & Savings Growth

* Avail Income tax relief on paid contributions.

Sum Cover.

Net PIA value accumulated atthe time of death.

Distributable surplus from theWaqf Fund, if any.

In the Event of Death

Net PIA value accumulated atthe time of Maturity.

Distributable surplus from theWaqf Fund, if any.

Maturity Benefits

‘Silah’

Participants of the meetingof the Senior management

with the Regional and Senior Branch Managersheld in January 2014

This refers to participation of Takaful on group basis where the participant is a bona-fide legal entitiy (e.g.

companies, organizations etc.) representing its members whose lives are being covered. The term of coverage

is limited to one year only and subject to renewal.

The contrifbution paid by the participant is fully allocated into the Waqf fund as Tabarru’ (donation) from which

payment of defined benefits will be made in case of death/disablement of any member. Unlike Individual Takaful

plans it carries no cash value.

The distinctive features are affordable contribution per person and minimal underwriting for members. Optional

riders are also available for coverage enhancements.

Group Term

This plan is normally availed by an employer for the protection of its employees or by an organization for the

benefits of its members in the event of death. The amount of sum covered per person is determined either

according to categories of employment / membership or it may be leveled across the board.

Group Credit

This product protects a financial institution on the facilities provided to its customers. In the event of death or

disability of a customer, the financial institution will be indemnified on the amount of outstanding balance (including

profit) without the hassle of recovery from deceased family.

Gorup Accident

This product has been developed to provide economical coverage to participants where the scope of cover is

only accidental death / disablement. Under this cover if any person covered dies due to accidental means within

ninety (90) days of such accident and sustained injuries are solely and independently caused by external, violent

and purely accidental means, compensation will be paid to the participant for benefit of his/her beneficiaries.

GROUP TAKAFUL PLANS

Page No.

Vision and Mission Statements 01

Core Values 02

Corporate Information 03

Directors’ Report to the Shareholders 05

Shariah Audit Report 10

Auditors’ Report to the Members 11

Financial Statements 13

Statement of Directors 61

Certificate of Appointed Actuary 62

Pattern of Shareholding 63

Notice of Annual General Meeting 65

Proxy Form

CONTENTS

VisionThe Company will strive to become

the Takaful partner of choice in

Pakistan catering to the financial

protection, long term savings,

retirement and financial planning

needs of individuals, businesses

and the public sector, in full

conformity with Shariah principles.

Mission To be recognized as a reputable,

profitable, Shariah driven Family

Takaful operator offering innovative

financial solutions to its clients

through best in class talent,

technology and distribution power.

01

Core ValuesOur values transcend throughout the entire organization. These principleswill guide us to succeed in our business and will serve us well aheadinto the future, from day-to-day business operation to product developmentand customer service.

Islamic Values

We are establishing a fully moral and ethical Company whose peopleare strong in religious values and live by the highest ethical standards.

Our Company

We are building a Team that takes personal responsibility for the deliveryof our services and promises to our participants and business partners.We shall consciously seek to develop our staff and consultants in theirchosen careers and install in them a sense of pride and ownership in theCompany.

Financial Strength

We strive to earn the confidence of our participants by building areputation for fair and prompt claims services and ensuring the financialstability of the Company. We believe that these form the foundation oftheir security.

Customer – centric

We believe that by being pro-active and meeting the changing needs ofour participants through value-added products and services, we willmeet the aspirations of all stakeholders.

Quality Culture

We believe in doing the right things right the first time and every time.Quality and continuous improvements shall be the key drivers in all ourmanagement processes.

02

Board of Directors

Mr. Muhammad Rizwan-ul-Haque ChairmanMr. Rizwan Ahmed Farid Chief Executive OfficerMr. Syed Ishtiaq Hussain DirectorMr. Tahir Mehmood DirectorMr. Muhammad Munir DirectorMr. Muhammad Salah-ud-din Arif Director

Shariah Supervisory Board

Professor Mufti Munib-ur-Rehman ChairmanMufti Syed Zahid Siraj MemberMufti Syed Sabir Hussain Member

Audit Committee

Mr. Muhammad Munir ChairmanMr. Tahir Mehmood MemberMr. Syed Ishtiaq Hussain MemberMr. Fahad Alam Secretary

Investment Committee

Mr. Muhammad Rizwan-ul-Haque ChairmanMr. Tahir Mehmood MemberMr. Muhammad Salah-ud-din Arif MemberMr. Rizwan Ahmed Farid MemberMr. Ghazanfar ul Islam MemberMr. Syed Muhammad Salman MemberMr. Fahad Alam Secretary

Chief Financial Officer Mr. Ghazanfar ul Islam

Company Secretary Mr. Fahad Alam

Statutory Auditors Ernst & Young Ford Rhodes Sidat Hyder & CoChartered Accountants

Internal Auditors BDO Ebrahim & CoChartered Accountants

Appointed Actuary Mr. Shujat Siddiqui, MA, FIA, FPSAAkhtar & Hassan (Pvt.) Limited

Legal Advisor Nishtar & ZafarAdvocates and Legal Consultants

Share Registrar FD Registrar Services (SMC-Pvt) Limited1705, 17th Floor, Saima Trade Towers – A,I.I. Chundrigar RoadKarachi – 74000

Corporate Information

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 03

As on December 31, 2013

Bankers

Silk Bank Limited, Emaan Islamic BankingSoneri Bank Limited, Islamic BankingBurj Bank LimitedDubai Islamic Bank LimitedAl Baraka Bank (Pakistan) LimitedMeezan Bank LimitedBank Al-Falah LimitedUBL Ameen Islamic BankingFaysal Bank Limited Barkat Islamic BankingHabib Bank Limited, Islamic BankingBank Al Habib Limited, Islamic BankingHabib Metropolitan Bank Limited, Islamic Banking

Registered and Head Office 17th Floor, Saima Trade Towers – AI.I. Chundrigar RoadKarachi – 74000

Website www.dawoodtakaful.com

Management Committee

Mr. Rizwan Ahmed Farid Chief Executive OfficerMr. Ghazanfar ul Islam Chief Financial OfficerDr. Bakht Jamal Shaikh Chief Operating OfficerMr. Nasir Mahmood Head of Marketing – IndividualMr. Muhammad Asif Haq Head of Information TechnologyMr. Fahad Alam Company Secretary and VP FinanceMr. Masta Khan AVP – Group Marketing Mr. Syed Muhammad Salman AVP – ActuarialMr. Muhammad Khalid AVP – AdministrationMr. Tasawar Ali Manager TrainingMs. Sakina Qamar Manager Operations

Underwriting Committee

Mr. Rizwan Ahmed Farid ChairmanDr. Bakht Jamal Shaikh MemberMr. Ghazanfar ul Islam MemberMr. Syed Muhammad Salman MemberMs. Sakina Qamar Secretary

Claim Settlement Committee

Mr. Rizwan Ahmed Farid ChairmanMr. Ghazanfar ul Islam MemberDr. Bakht Jamal Shaikh MemberMr. Syed Muhammad Salman MemberMr. Muhammad Rafique Secretary

Re-takaful Committee

Mr. Rizwan Ahmed Farid ChairmanDr. Bakht Jamal Shaikh MemberMr. Ghazanfar ul Islam MemberAppointed Actuary MemberMr. Syed Muhammad Salman Secretary

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 04

DIRECTORS’ REPORT TO THE SHAREHOLDERS

Dear Shareholders,

The Directors of your company are pleased to present to you the 7th Annual Report of the Company for theyear ended 31st December 2013. By the grace of Allah the performance of the year was marked with manyimprovements.

Economic overview

The year 2013 was the election year marked by political uncertainty. Economy of the country continues tostruggle due to power shortages and law and order situation. Even after considerable time taking charge noclear economic direction has been given by the government which perhaps due to the fact that its attentiondiverted to more dire concerns of maintaining peace and control terrorism. Continuous depreciation of PakRupee against US Dollar from Pak Rs 97.08 to Pak Rs 108.58 during the year had a direct impact on the savingpropensity towards family Takaful business. State Bank’s Annual Report (on the state of economy) 2013 recordsNational GDP growth of 3.6% and continuous decline in the investment to GDP ratio since 2007.

Market overview

Our country still lacks awareness of Life insurance/Family Takaful and therefore we have low insurance penetrationwith Takaful share even lower nevertheless with passage of time we are witnessing improvements and overallvolume of Insurance/Takaful is increasing year by year owing to efforts of the market players by expandingbranch networks, training staff and spreading public awareness. As a predominantly Islamic country Takafulconcept is well receive by the masses hence in growth rate Shariah Compliant Family Takaful companies areoutperforming the conventional companies.

BUSINESS PERFORMANCE

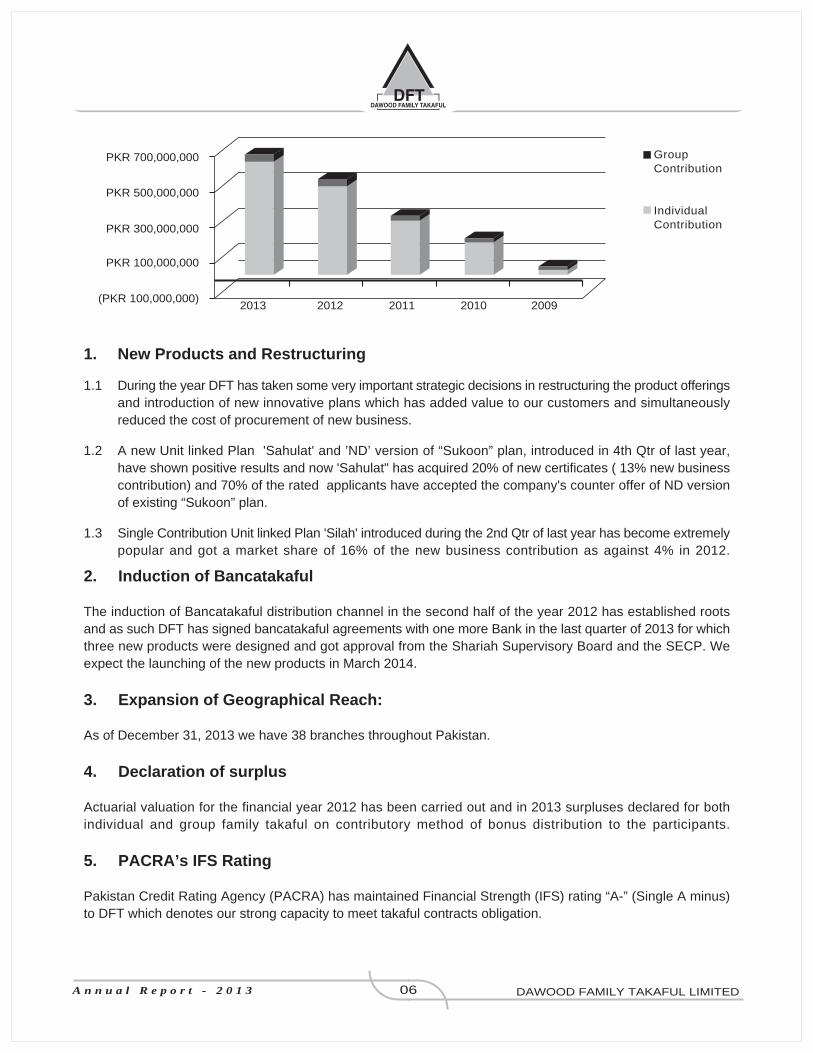

Due to aforesaid market conditions the Company unable to meet its business targets but still able to achievea sizable growth of 27.25% over last year despite the above challenges and national trends. Gross contributionearned, during last five years is as follows,

2013 2012 2011 2010 2009

---------------------------------------------Rupees----------------------------------------------

Individual Takaful 630,844,716 485,832,201 298,721,386 180,202,774 29,453,906

Group Takaful 35,199,190 37,547,633 27,532,529 23,449,969 20,369,003

Total 666,043,906 523,379,834 326,253,915 203,625,743 49,822,909

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 05

1. New Products and Restructuring

1.1 During the year DFT has taken some very important strategic decisions in restructuring the product offeringsand introduction of new innovative plans which has added value to our customers and simultaneouslyreduced the cost of procurement of new business.

1.2 A new Unit linked Plan 'Sahulat' and ’ND’ version of “Sukoon” plan, introduced in 4th Qtr of last year,have shown positive results and now 'Sahulat" has acquired 20% of new certificates ( 13% new businesscontribution) and 70% of the rated applicants have accepted the company's counter offer of ND versionof existing “Sukoon” plan.

1.3 Single Contribution Unit linked Plan 'Silah' introduced during the 2nd Qtr of last year has become extremelypopular and got a market share of 16% of the new business contribution as against 4% in 2012.

2. Induction of Bancatakaful

The induction of Bancatakaful distribution channel in the second half of the year 2012 has established rootsand as such DFT has signed bancatakaful agreements with one more Bank in the last quarter of 2013 for whichthree new products were designed and got approval from the Shariah Supervisory Board and the SECP. Weexpect the launching of the new products in March 2014.

3. Expansion of Geographical Reach:

As of December 31, 2013 we have 38 branches throughout Pakistan.

4. Declaration of surplus

Actuarial valuation for the financial year 2012 has been carried out and in 2013 surpluses declared for bothindividual and group family takaful on contributory method of bonus distribution to the participants.

5. PACRA’s IFS Rating

Pakistan Credit Rating Agency (PACRA) has maintained Financial Strength (IFS) rating “A-” (Single A minus)to DFT which denotes our strong capacity to meet takaful contracts obligation.

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 06

2012 2011 2010 2009

PKR 700,000,000

PKR 500,000,000

PKR 300,000,000

PKR 100,000,000

(PKR 100,000,000)

GroupContribution

IndividualContribution

2013

6. Training

6.1 Senior management has facilitated several sessions on Underwriting and Claims Settlement across ourbranch network in 2013.

6.2 Training & Development Department arranged and delivered 54 training sessions. These trainings includedthe mandatory required Foundation training sessions, as well as Advance Level Consultant Developmentsessions and Managerial Development Program sessions – conducted across the three regions of IndividualMarketing branch network in Pakistan.

7. Information Technology

During 2013 the DFTL IT team successfully developed and rolled out the Group Takaful Operational Software.It has also undertaken the in-house development of Individual Takaful Software.

8. Re-takaful arrangements

To enhance the customers confidence and to secure the risk of takaful arrangements DFT has renegotiatedcomprehensive re-takaful arrangements with best international re-takaful companies “Munich Re-takaful” and“Hannover Re-takaful”, having strong credit rating “AA-“(Double A minus) and “A+” (Single A plus) respectively.

9. Claim settlements

DFT strive to be most efficient in claims processing, during the year 2013 DFT has successfully paid total claimsof Rs. 34 million.

FINANCIAL PERFORMANCE

2013 2012 ---------------- Rupees -------------------

Takaful Income 305,433,992 244,820,911

Investment income 29,911,826 41,428,854

Gain on redemption/sale of investments 2,022,800 23,687,700

Other income 1,963,901 493,980

Total Income 339,332,519 310,431,445

Management expenses 235,320,355 226,726,588

Commission expense 173,031,116 147,648,565

Total Expenses (408,351,471) (374,375,153)

Loss before tax (69,018,952) (63,943,708)

Taxation 21,237,219 20,950,300

Loss after tax (47,781,733) (42,993,408)

During the year the Company has earned Rs.305 millions from Takaful operations a 25% growth over last year.While commission expense to Takaful income ratio has improved from 60% to 56.6%, the investment incomehas gone down mainly due to principal redemption of Sukuks portfolio. The net loss after tax have increased

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 07

by Rs.4.7 million, however if we examine the last year performance Company had earned Rs. 23.7 million asgain on sale/redemption of investment which were nonrecurring events, if minus this impact we could see theimprovement of around Rs. 17 million during the year 2013. As stated in the earlier reports these are plannedlosses part of Family Takaful Company life cycle, your Company is in growth phase and poised to achieve break-even in near future.

RELATED PARTY TRANSACTIONS

All related party transactions during the year have been executed on an arm’s length basis. All such transactionshave been approved by the Board of Directors in their meeting.

INTERNAL CONTROL AND AUDIT FUNCTION

The Board is responsible for the effective implementation of sound internal controls systems including compliancewith the control procedures. The Audit Committee is assisted by the Internal Audit function which is outsourcedto a reputable Chartered Accountants firm which review both adequacy and operational effectiveness of theinternal controls.

MEETINGS OF THE BOARD

During the year four meetings of the Board of Directors have been held. The number of meeting attended byeach director is as follows,

Name of Directors AttendanceMr. Muhammad Rizwan-ul Haque 4 out of 4Mr. Tahir Mehmood 4 out of 4Mr. Rizwan Ahmed Farid 4 out of 4Mr. Muhammad Munir 4 out of 4Mr. Syed Ishtiaq Hussain 3 out of 4Mr. Muhammad Salah-ud-din Arif 1 out of 1

EXTERNAL AUDITORS

Ernst & Young Ford Rhodes Sidat Hyder & Co. Chartered Accountants are willing to continue and proposedto be appointed as Auditors of the Company for the year ending 2014 by the Board of Directors on recommendationof the Audit Committee.

PATTERN OF SHAREHOLDING

A statement showing the pattern of shareholding is attached with this report.

EVENTS AFTER BALANCE SHEET DATE

There have been no material changes since December 31, 2013 to date of this report and the Company hasnot entered into any material commitment during this period which would adversely affect the financial positionof the Company.

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 08

EARNINGS PER SHARE

The loss per share of the Company for the year 2013 is Rs.0.64 (2012: Rs.0.57) per ordinary share of Rs. 10each.

ACKNOWLEDGEMENT

We wish to recognize and acknowledge valuable support of our Directors, employee and clients.

On behalf of the Board

Rizwan Ahmed FaridChief Executive Office

Karachi, February 24, 2014

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 09

D A W O O D F A M I L Y T A K A F U L L I M I T E D

1701-A, Saima Trade Towers, I.I. Chundrigar Road, Karachi-74000UAN: 111-DFT-786 (111-338-786) Fax: (92-21) 3227-7188

www.dawoodtakaful.com

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 10

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 11

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 12

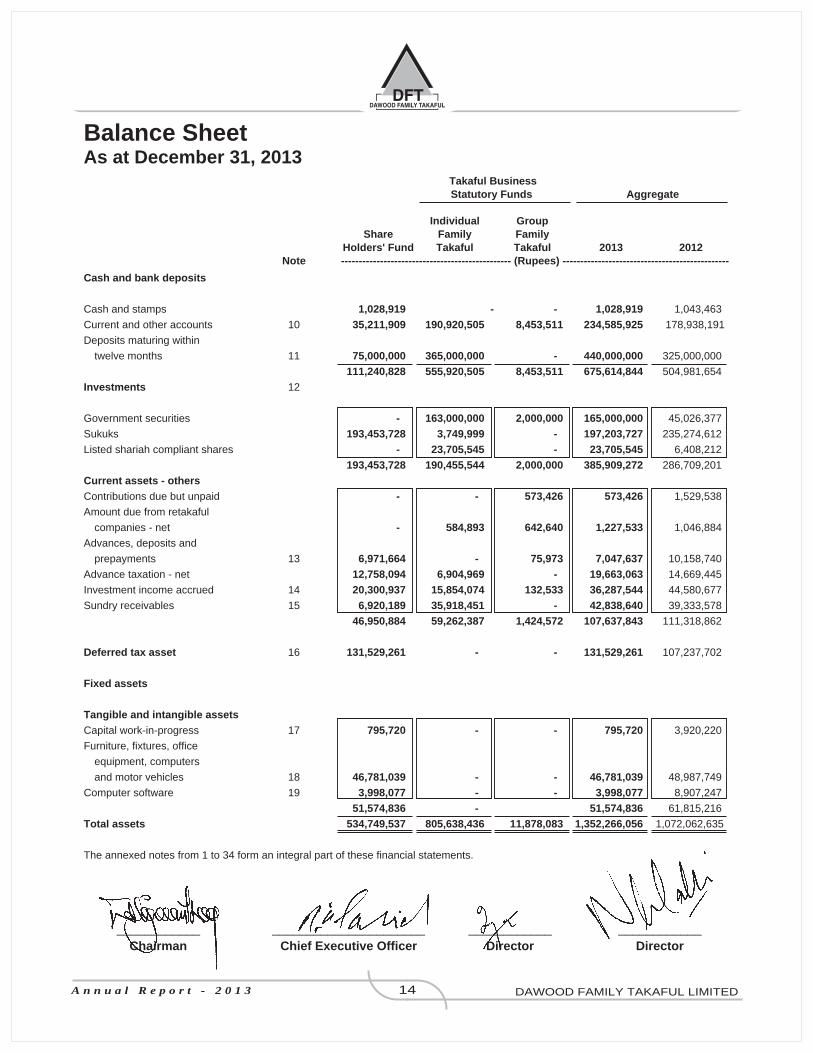

Authorised share capital

80,000,000 (2012: 80,000,000)

Ordinary shares of Rs.10 each 800,000,000 - - 800,000,000 800,000,000

Issued, subscribed and

paid-up share capital 6 750,000,000 - - 750,000,000 750,000,000

Accumulated deficit (278,304,852) - - (278,304,852) (230,523,119)

Contribution to takaful

business statutory funds (90,000) - - (90,000) (5,090,000)

Net shareholders' equity 471,605,148 - - 471,605,148 514,386,881

Balance of Takaful

Business Statutory Funds

Cede money - waqf - - 100,000 100,000 100,000

Participant Investment Fund 7 - 516,764,078 - 516,764,078 312,878,034

Participant Takaful Fund - 209,896,737 7,287,187 217,183,924 119,995,465

- 726,660,815 7,387,187 734,048,002 432,973,499

Creditors and accruals

Outstanding claims - 6,519,084 3,636,250 10,155,334 10,042,469

Contributions received in advance - 35,312,225 - 35,312,225 23,166,316

Amount due to agents 37,366,770 - - 37,366,770 31,786,572

Other creditors and accruals 8 25,777,619 37,146,312 854,646 63,778,577 59,706,898

63,144,389 78,977,621 4,490,896 146,612,906 124,702,255

Total liabilities 63,144,389 805,638,436 11,878,083 880,660,908 557,675,754

Total equity and liabilities 534,749,537 805,638,436 11,878,083 1,352,266,056 1,072,062,635

Contingencies and commitments 9

The annexed notes from 1 to 34 form an integral part of these financial statements.

Balance SheetAs at December 31, 2013

Takaful BusinessStatutory Funds Aggregate

Individual GroupShare Family Family

Holders' Fund Takaful Takaful 2013 2012Note ------------------------------------------------ (Rupees) -----------------------------------------------

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 13

____________ ______________________ ____________ ____________Chairman Chief Executive Officer Director Director

Balance SheetAs at December 31, 2013

Cash and bank deposits

Cash and stamps 1,028,919 - - 1,028,919 1,043,463

Current and other accounts 10 35,211,909 190,920,505 8,453,511 234,585,925 178,938,191

Deposits maturing within

twelve months 11 75,000,000 365,000,000 - 440,000,000 325,000,000

111,240,828 555,920,505 8,453,511 675,614,844 504,981,654

Investments 12

Government securities - 163,000,000 2,000,000 165,000,000 45,026,377

Sukuks 193,453,728 3,749,999 - 197,203,727 235,274,612

Listed shariah compliant shares - 23,705,545 - 23,705,545 6,408,212

193,453,728 190,455,544 2,000,000 385,909,272 286,709,201

Current assets - others

Contributions due but unpaid - - 573,426 573,426 1,529,538

Amount due from retakaful

companies - net - 584,893 642,640 1,227,533 1,046,884

Advances, deposits and

prepayments 13 6,971,664 - 75,973 7,047,637 10,158,740

Advance taxation - net 12,758,094 6,904,969 - 19,663,063 14,669,445

Investment income accrued 14 20,300,937 15,854,074 132,533 36,287,544 44,580,677

Sundry receivables 15 6,920,189 35,918,451 - 42,838,640 39,333,578

46,950,884 59,262,387 1,424,572 107,637,843 111,318,862

Deferred tax asset 16 131,529,261 - - 131,529,261 107,237,702

Fixed assets

Tangible and intangible assets

Capital work-in-progress 17 795,720 - - 795,720 3,920,220

Furniture, fixtures, office

equipment, computers

and motor vehicles 18 46,781,039 - - 46,781,039 48,987,749

Computer software 19 3,998,077 - - 3,998,077 8,907,247

51,574,836 - 51,574,836 61,815,216

Total assets 534,749,537 805,638,436 11,878,083 1,352,266,056 1,072,062,635

The annexed notes from 1 to 34 form an integral part of these financial statements.

Takaful BusinessStatutory Funds Aggregate

Individual GroupShare Family Family

Holders' Fund Takaful Takaful 2013 2012Note ------------------------------------------------ (Rupees) -----------------------------------------------

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 14

____________ ______________________ ____________ ____________Chairman Chief Executive Officer Director Director

2013 2012Note ----------------- (Rupees) -----------------

Takaful operator feeWakala fee 285,027,025 230,431,740Mudarib share 1,979,103 1,350,167Tharawat fee 5,867,048 3,335,248Bid offer share 12,560,816 9,703,756Total takaful operator fee 305,433,992 244,820,911

Investment income not attributable to Takaful Business Statutory Funds

Income from non-trading investmentProfit on investment in sukuk 17,784,572 25,810,933Profit on term deposits 9,050,907 10,469,316Profit on saving accounts 3,076,347 5,151,733Total income from non-trading investment 29,911,826 41,431,982

Gain on redemption of investments 2,022,800 15,865,032Gain / (loss) on sale of investments - 7,822,668Total investment income 31,934,626 65,119,682

Investment related expenses - (3,128)Net investment income 31,934,626 65,116,554

Other income 20 1,963,901 493,980Total income 339,332,519 310,431,445

Less: Expenses not attributable toTakaful Business Statutory Funds

Management expenses 21 (235,320,355) (226,726,588)Commission expense (173,031,116) (147,648,565)Total expenditure (408,351,471) (374,375,153)Loss before tax (69,018,952) (63,943,708)

Taxation 22 21,237,219 20,950,300Loss after tax (47,781,733) (42,993,408)

Loss per share 23 (0.64) (0.57)

The annexed notes from 1 to 34 form an integral part of these financial statements.

Profit and Loss AccountFor the year ended December 31, 2013

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 15

____________ ______________________ ____________ ____________Chairman Chief Executive Officer Director Director

2013 2012 ----------------- (Rupees) -----------------

Loss after tax for the year (47,781,733) (42,993,408)

Other comprehensive income

Items of other comprehensive income not to be reclassifiedto profit and loss account in subsequent periods - -

Total comprehensive loss for the year (47,781,733) (42,993,408)

The annexed notes from 1 to 34 form an integral part of these financial statements.

Statement of Comprehensive IncomeFor the year ended December 31, 2013

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 16

____________ ______________________ ____________ ____________Chairman Chief Executive Officer Director Director

Reserves Issued, Capital

subscribed contributionsand paid-up Accumulated to Takaful Net

share capital deficit Business reserves Total---------------------------------------------------- (Rupees) ----------------------------------------------------

Statement of Changes in EquityFor the year ended December 31, 2013

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 17

Balance as at January 01, 2012 750,000,000 (187,529,711) (10,090,000) (197,619,711) 552,380,289

Changes in equity 2012

Transactions directly related toowner's equity

Capital redemption from participantinvestment fund - Islamic Income Fund - - 5,000,000 5,000,000 5,000,000

Total comprehensive incomefor the year

Loss for the year - (42,993,408) - (42,993,408) (42,993,408)

Other comprehensive income - - - - - - (42,993,408) - (42,993,408) (42,993,408)

Balance as at December 31, 2012 750,000,000 (230,523,119) (5,090,000) (235,613,119) 514,386,881

Balance as at January 01, 2013 750,000,000 (230,523,119) (5,090,000) (235,613,119) 514,386,881

Changes in equity 2013

Transactions directly related toowner's equity

Capital redemption from participantinvestment fund - Islamic Aggressive Fund - - 5,000,000 5,000,000 5,000,000

Total comprehensive incomefor the year

Loss for the year - (47,781,733) - (47,781,733) (47,781,733)

Other comprehensive Income - - - - - - (47,781,733) - (47,781,733) (47,781,733)

Balance as at December 31, 2013 750,000,000 (278,304,852) (90,000) (278,394,852) 471,605,148

The annexed notes from 1 to 34 form an integral part of these financial statements.

____________ ______________________ ____________ ____________Chairman Chief Executive Officer Director Director

Takaful BusinessStatutory Funds Aggregate

GroupShare Holders' Individual Family

Fund Family Takaful Takaful 2013 2012 ------------------------------------------------------------ (Rupees) -------------------------------------------------------------

Statement of Cash FlowsFor the year ended December 31, 2013

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 18

Operating cash flows

Cash flow from takaful activitiesContributions received - 638,890,680 36,155,302 675,045,982 532,008,754Surrender / withdrawal paid - (68,807,366) - (68,807,366) (37,365,773)Claims paid - (7,891,343) (25,674,811) (33,566,154) (28,882,083)Retakaful paid - (7,360,117) (4,969,988) (12,330,105) (13,537,043)Wakala fee 292,881,827 (287,139,588) (5,742,239) - -Mudarib fee 2,620,717 (1,811,976) (808,741) - -Tharawat fee 5,903,057 (5,903,057) - - -Bid offer liability 5,563,235 (5,563,235) - - -Commission paid to agents (167,450,919) - - (167,450,919) (137,859,063)Net cash flows from takaful activities 139,517,917 254,413,998 (1,040,477) 392,891,438 314,364,792

Other operating cash flows

Income tax paid 4,965,691 (6,904,969) - (1,939,278) (4,765,628)General management expenses paid (216,434,075) (37,356) - (216,471,431) (210,690,469)Other operating payments (703,835) (4,376,908) (131,209) (5,211,952) (1,332,974)Other operating receipts 4,099,946 - - 4,099,946 1,032,798Sundry receivables - - - - 1,508,708Advances, deposits and prepayments 3,111,103 - - 3,111,103 (1,832,957)Net cash flows from other operating activities (204,961,170) (11,319,233) (131,209) (216,411,612) (216,080,522)

Net cash flows from / (used in) all operating activities (65,443,253) 243,094,765 (1,171,686) 176,479,826 98,284,270

Investment activities

Profit on investment received 42,454,096 41,781,512 818,044 85,053,652 53,262,448Proceeds from disposal of units of mutual fund - - - - 50,982,120Receipt against maturity of short-term musharika - 250,000,000 - 250,000,000 50,000,000Payment against short-term musharika - (365,000,000) - (365,000,000) (260,000,000)Payment against purchase of listed

shariah compliant shares - (17,549,851) - (17,549,851) (2,675,980)Receipts against sale of listed shariah compliant shares - 5,790,344 - 5,790,344 2,507,654Dividend received from listed shariah compliant shares - 360,532 - 360,532 244,468Redemption of sukuks 38,070,885 45,000,000 - 83,070,885 57,628,861Payment against purchase of sukuks - (163,000,000) (2,000,000) (165,000,000) -Proceeds from disposal of fixed assets 1,754,503 - - 1,754,503 381,499Payment against fixed capital expenditure (6,349,552) - - (6,349,552) (7,856,364)Net cash flows from / (used in) investing activities 75,929,932 (202,617,463) (1,181,956) (127,869,487) (55,525,294)

Financing activitiesCapital contribution from shareholders fund - - - - -Capital contribution redeemed from PIF fund 7,022,800 - - 7,022,800 7,401,950Net cash flows from financing activities 7,022,800 - - 7,022,800 7,401,950Net cash flows from / (used in) all activities 17,509,479 40,477,302 (2,353,642) 55,633,139 50,160,926Cash and cash equivalents at the beginning of the year 18,731,349 150,443,203 10,807,153 179,981,705 129,820,728Cash and cash equivalents at the end of the year 36,240,828 190,920,505 8,453,511 235,614,844 179,981,654

Cash and cash equivalentsCash and stamps 1,028,919 - - 1,028,919 1,043,463Current and other accounts 35,211,909 190,920,505 8,453,511 234,585,925 178,938,191

36,240,828 190,920,505 8,453,511 235,614,844 179,981,654

The annexed notes from 1 to 34 form an integral part of these financial statements.

____________ ______________________ ____________ ____________Chairman Chief Executive Officer Director Director

Takaful BusinessStatutory Funds Aggregate

GroupIndividual Family

Family Takaful Takaful 2013 2012

Note --------------------------------------------- (Rupees) ---------------------------------------------

Revenue AccountFor the year ended December 31, 2013

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 19

Income

Contribution net off retakaful 361,781,750 12,083,984 373,865,734 291,226,992

Investment income 13,464,876 613,405 14,078,281 9,402,698

Net risk contribution/ANF contribution 3,646,231 - 3,646,231 1,587,317

Surplus from retakaful operator 4,984,070 262,859 5,246,929 2,435,638

Total net income 383,876,927 12,960,248 396,837,175 304,652,645

Less: Claims and expenditures

Claims net off retakaful recoveries 3,334,375 6,505,521 9,839,896 8,637,444

Wakala fee 280,356,092 5,388,945 285,745,037 230,160,685

Mudarib fee 1,549,720 429,383 1,979,103 1,350,167

Waqf direct expenses 245,781 1,500 247,281 355,756

Total claims and expenditures 285,485,968 12,325,349 297,811,317 240,504,052

Excess of income over expenditure 98,390,959 634,899 99,025,858 64,148,593

Technical reserve at the beginning of the year 93,578,466 3,654,078 97,232,544 47,585,707

Less: Technical reserve at the end of the year 24 176,079,873 4,642,038 180,721,911 97,232,544

Surplus before distribution 15,889,552 (353,061) 15,536,491 14,501,756

Net movement in technical reserves 82,501,407 987,960 83,489,367 49,646,837

Surplus distribution (1,699,691) (137,708) (1,837,399) (381,819)

Balance of Takaful Business Statutory Fund

at the beginning of the year 113,205,469 6,789,996 119,995,465 56,228,691

Balance of Takaful Business Statutory

Fund at the end of the year 209,896,737 7,287,187 217,183,924 119,995,465

The annexed notes from 1 to 34 form an integral part of these financial statements.

____________ ______________________ ____________ ____________Chairman Chief Executive Officer Director Director

Takaful Business Statutory Funds Aggregate

Individual GroupFamily Takaful Family Takaful 2013 2012

------------------------------------------------ (Rupees) ------------------------------------------------

Statement of ContributionsFor the year ended December 31, 2013

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 20

Gross contributions

Regular contributions on individual policies

- first year 280,379,820 - 280,379,820 237,954,902

- second year 142,770,363 - 142,770,363 107,213,330

- subsequent years 140,591,852 - 140,591,852 63,640,698

Top up contributions 20,593,402 - 20,593,402 43,817,364

Single contribution on individual policies 46,509,279 - 46,509,279 33,205,907

Group policies without cash values - 35,199,190 35,199,190 37,547,633

Total gross contributions 630,844,716 35,199,190 666,043,906 523,379,834

Gross contributions allocated as follows:

Participants' Investment Fund (PIF)

Regular contributions on individual policies 230,059,262 - 230,059,262 149,187,609

Top up contributions on individual policies 20,593,402 - 20,593,402 43,817,364

Total contributions allocated to PIF 250,652,664 - 250,652,664 193,004,973

Participants' Takaful Fund (PTF)

Regular contributions on individual policies 380,192,052 - 380,192,052 292,827,228

Group policies without cash values - 35,199,190 35,199,190 37,547,633

Total gross contributions allocated to PTF 380,192,052 35,199,190 415,391,242 330,374,861

Less: Retakaful contributions ceded

Regular individual policies (18,410,302) - (18,410,302) (13,229,846)

Group policies without cash values - (23,115,206) (23,115,206) (24,330,706)

Total retakaful ceded (18,410,302) (23,115,206) (41,525,508) (37,560,552)

Net risk contributed to PTF 361,781,750 12,083,984 373,865,734 292,814,309

Contributions allocation to shareholders' fund

Regular individual policies 280,356,092 - 280,356,092 223,810,708

Group policies without cash values - 5,388,945 5,388,945 6,349,977

Total contributions allocated to shareholders' fund 280,356,092 5,388,945 285,745,037 230,160,685

Net risk contributed to PTF 81,425,658 6,695,039 88,120,697 62,653,624

The annexed notes from 1 to 34 form an integral part of these financial statements.

____________ ______________________ ____________ ____________Chairman Chief Executive Officer Director Director

Takaful BusinessStatutory Funds Aggregate

Individual GroupFamily Takaful Family Takaful 2013 2012

-------------------------------------------------- (Rupees) -------------------------------------------------

Statement of ClaimsFor the year ended December 31, 2013

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 21

Gross claims

- by death 8,872,737 21,850,558 30,723,295 28,831,955

- by event other than death 730,221 2,515,503 3,245,724 2,058,501

Total gross claims 9,602,958 24,366,061 33,969,019 30,890,456

Less: Retakaful recoveries (6,268,583) (17,860,540) (24,129,123) (22,253,012)

Net claims 3,334,375 6,505,521 9,839,896 8,637,444

The annexed notes from 1 to 34 form an integral part of these financial statements.

____________ ______________________ ____________ ____________Chairman Chief Executive Officer Director Director

Takaful BusinessStatutory Funds Aggregate

Individual GroupFamily Takaful Family Takaful 2013 2012

-------------------------------------------------- (Rupees) -------------------------------------------------

Statement of ExpensesFor the year ended December 31, 2013

Wakala fee 280,356,092 5,388,945 285,745,037 230,160,685

Mudarib share 1,549,720 429,383 1,979,103 1,350,167

Waqf direct expenses 245,781 1,500 247,281 355,756

282,151,593 5,819,828 287,971,421 231,866,608

The annexed notes from 1 to 34 form an integral part of these financial statements.

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 22

____________ ______________________ ____________ ____________Chairman Chief Executive Officer Director Director

Takaful BusinessStatutory Funds Aggregate

Individual GroupFamily Takaful Family Takaful 2013 2012

-------------------------------------------------- (Rupees) -------------------------------------------------

Statement of Investment IncomeFor the year ended December 31, 2013

Income from non-trading

investments

Return on sukuks 2,031,488 139,062 2,170,550 891,449

Return on term deposits 6,876,082 - 6,876,082 966,263

Return on saving accounts 4,583,683 474,343 5,058,026 7,607,576

Amortisation of premium

on sukuks (26,377) - (26,377) (62,590)

Net investment income 13,464,876 613,405 14,078,281 9,402,698

The annexed notes from 1 to 34 form an integral part of these financial statements.

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 23

____________ ______________________ ____________ ____________Chairman Chief Executive Officer Director Director

1. STATUS AND NATURE OF BUSINESS

Dawood Family Takaful Limited (the Company or DFTL) was incorporated in Pakistan as an unquoted public limited company onMay 04, 2007 under the Companies Ordinance, 1984. The Company received the certificate of registration on May 16, 2008 underSection 6 of the Insurance Ordinance, 2000. The registered office of the Company is situated at 1701-A, Saima Trade Towers, I. I.Chundrigar Road, Karachi. The principal business activity of the Company is to undertake family takaful business in accordancewith the Insurance Ordinance 2000, Securities and Exchange Commission (Insurance) Rules, 2002 and Takaful Rules, 2005.

To carry out the family takaful business, the Company has established the Takaful Business Statutory Fund with effect from December,01 2008 as per Rule 8 of the Takaful Rules, 2005 and Section 15 of the Insurance Ordinance, 2000. The Takaful Business StatutoryFund has the following components in accordance with the Waqf-Wakala Model adopted by the Company.

i) Participant Takaful Fund (PTF i.e. DFTL Waqf): The Company has formed a Waqf on 30 May 2008 to manage the risk relatedcontributions and payment of Takaful benefits. The Waqf shall support the following:

a) Group Family Takaful Business (both term and credit takaful).

b) Risk related contributions of Individual Takaful Products (mortality and morbidity charges) including supplementary ridercontributions.

ii) Participant Investment Fund (PIF): Investment component of the participants contributions are managed in PIF which representsthe aggregate of the individual Participant’s Investment Accounts (PIA).The Company has established three sub-investmentfunds under PIF, with cede money, having different investment objectives. During the year, the Company has withdrawn cedemoney from Islamic Aggressive Fund as per the written advice of the appointed actuary.

Name of sub-funds Effective dates

a) Islamic Income Fund December 01, 2008

b) Islamic Balanced Fund December 01, 2008

c) Islamic Aggressive Fund April 29, 2011

As per Section 21 of the Insurance Ordinance, 2000 capital contribution to a statutory fund is distributable back to the shareholders’fund subject to the written advice of the appointed actuary.

2. STATEMENT OF COMPLIANCE

These financial statements have been prepared in accordance with approved accounting standards as applicable in Pakistan.Approved accounting standards comprise of such International Financial Reporting Standards (IFRSs) issued by the InternationalAccounting Standards Board and Islamic Financial Accounting Standards issued by the Institute of Chartered Accountants of Pakistanas are notified under the Companies Ordinance, 1984, provisions of and directives issued under the Companies Ordinance, 1984,Insurance Ordinance, 2000, Securities and Exchange Commission (Insurance) Rules, 2002 and Takaful Rules, 2005. In case therequirements differ with the standards, the provisions or directives of the Companies Ordinance, 1984, Insurance Ordinance, 2000,Securities and Exchange Commission (Insurance) Rules, 2002 and Takaful Rules, 2005 shall prevail.

During 2012, the Securities and Exchange Commission of Pakistan (SECP) notified Takaful Rules, 2012 on July 16, 2012. TheCompany along with other takaful operators filed a constitutional petition in the Honorable High Court of Sindh (the Court) challengingthe said rules on various grounds. The Court vide its order dated August 01, 2012 has directed all parties to maintain status quo.The matter is currently pending with the Court. Accordingly, these financial statements have been prepared in compliance with theTakaful Rules, 2005.

3. BASIS OF PREPARATION

These financial statements have been prepared on the format of financial statements issued by SECP through Securities andExchange Commission (Insurance) Rules, 2002 with appropriate modifications based on the advice of the Shariah Board of theCompany.

Notes to the Financial StatementsFor the year ended December 31, 2013

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 24

3.1 Basis of measurement

These financial statements have been prepared on the basis of historical cost convention, except for certain investments which arecarried at fair value.

3.2 Functional and presentation currency

These financial statements are presented in Pak Rupees which is also the Company's functional currency.

3.3 Use of estimates and judgments

The preparation of financial statements in conformity with approved accounting standards requires management to make judgments,estimates and assumptions that effect the application of policies and reported amount of assets and liabilities, income and expenses.These estimates and associated assumptions are based on historical experience and various other factors that are believed to bereasonable under the circumstances, the result of which form the basis of making the judgments about the carrying values of assetsand liabilities that are not readily apparent from other sources.

Actual results may differ from these estimates. The estimates and underlying assumptions are reviewed on an ongoing basis.Revisions to accounting estimates are recognised in the period in which the estimate is revised, if the revision affects only the periodof the revision and future period if the revision affects both current and future periods.

The areas involving a higher degree of judgment or complexity, or areas where assumptions and estimates are significant to thefinancial statements or judgments were exercised in application of accounting policies, are as follows:

a) Technical reserves

Technical reserves required to be setup in the Participants Takaful Fund as determined by the appointed actuary of the TakafulOperator. Technical reserves may consist of any or combination of the following reserves:

Group Family Takaful Individual Family Takaful

i) unearned contribution reserves i) net technical reserve

ii) incurred but not reported reserves ii) incurred but not reported reserves

iii) contribution deficiency reserves iii) contribution deficiency reserves

iv) contingency reserves iv) contingency reserves

v) reserve for qard-e-hasna v) reserve for qard-e-hasna

vi) surplus equalisation reserve vi) surplus equalisation reserve

vii) provision for outstanding claimsexceeding 12 months

b) Waqf participants’ liabilities

Waqf participants’ liabilities are calculated by the appointed actuary using appropriate discount rate and mortality assumptions.Actual investment returns and mortality charge is, by its nature, expected to be different from estimates.

Changes in the above would affect the technical reserve balance at the year end.

c) Claims

Calculation for claims incurred but not reported (IBNR) is made on the assumption that the claim lag pattern will follow the historicaltrend experience.

Notes to the Financial StatementsFor the year ended December 31, 2013

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 25

d) Fixed assets

The Company reviews the rate of depreciation, useful life and value of assets for possible impairment on an annual basis. Anychange in the estimates in future years might affect the carrying amounts of respective items of fixed assets with a correspondingeffect on the depreciation charge and impairment.

e) Deferred taxation

In recognising the deferred tax assets the management has carried out detailed review of projections of taxable profit for foreseeablefuture based upon information considered to be most reliable in the circumstances.

f) Impairment of available-for-sale investments

The Company recognises that available-for-sale investments are impaired when there has been a significant or prolonged declinein the fair value below the cost. In making this judgment the Company consider various market factors including projected profit rateand capital market performance.

4. STANDARDS, INTERPRETATIONS AND AMENDMENTS TO APPROVED ACCOUNTING STANDARDS THAT ARE NOT YETEFFECTIVE

The following revised standards, amendments and interpretations with respect to the approved accounting standards as applicablein Pakistan would be effective from the dates mentioned below against the respective standard or interpretation:

Effective date (annual periodsBeginning

Standard or Interpretation on or after)

IAS 32 – Offsetting Financial Assets and Financial liabilities – (Amendment) January 01, 2014

IAS 36 – Recoverable Amount for Non-Financial Assets – (Amendment) January 01, 2014

IAS 39 – Novation of Derivatives and Continuation of Hedge Accounting – (Amendment) January 01, 2014

IFRIC 21 – Levies January 01, 2014

The Company expects that the adoption of the above revision, amendments and interpretation of the standards will not affect theCompany's financial statements in the period of initial application.

In addition to the above, the following new standards have been issued by IASB which are yet to be notified by the SECP for thepurpose of applicability in Pakistan.

IASB Effective date (annual periodsbeginning

Standard on or after)

IFRS 9 - Financial Instruments: Classification and Measurement January 01, 2015

IFRS 10 - Consolidated Financial Statements January 01, 2013

IFRS 11 - Joint Arrangements January 01, 2013

IFRS 12 - Disclosure of Interests in Other Entities January 01, 2013

IFRS 13 - Fair Value Measurement January 01, 2013

Notes to the Financial StatementsFor the year ended December 31, 2013

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 26

5. SIGNIFICANT ACCOUNTING POLICIES

The accounting policies adopted in the preparation of these financial statements are consistent with those of the previous financialyear except as described below in note 5.1.

5.1 New and amended standards and interpretations

The Company has adopted the following amendments to IFRSs which became effective during the current year:

IAS 1 – Presentation of Financial Statements – Presentation of items of other comprehensive income (Amendment)

IAS 19 – Employee Benefits – (Revised)

IFRS 7 – Financial Instruments: Disclosures – (Amendments)

– Amendments enhancing disclosures about offsetting of financial assets and financial liabilities

IFRIC 20 – Stripping Costs in the Production Phase of a Surface Mine

Improvements to Accounting Standards Issued by the IASB

IAS 1 – Presentation of Financial Statements - Clarification of the requirements for comparative information

IAS 16 – Property, Plant and Equipment – Clarification of Servicing Equipment

IAS 32 – Financial Instruments: Presentation – Tax Effects of Distribution to Holders of Equity Instruments

IAS 34 – Interim Financial Reporting – Interim Financial Reporting and Segment Information for Total Assets and Liabilities

The adoption of the above amendments did not have any effect on the financial statements.

5.2 Takaful contracts

The takaful contracts are based on the principles of Wakala Waqf Model. Takaful is a programme based on shariah compliant,approved concept founded on the principles of mutual cooperation, solidarity and brotherhood.

The Company maintains Takaful Business Statutory Funds for all classes of family takaful business. Assets, liabilities, revenuesand expenses are recorded in respective funds, if referable or, on the basis of actuarial advice if not referable. Other assets, liabilities,revenues and expenses are allocated to shareholders' fund.

Technical reserves included in the Takaful business statutory funds are determined based on appointed actuary’s valuation conductedat the balance sheet date, in accordance with section 50 of the Insurance Ordinance, 2000.

The obligation of Waqf for Waqf participants' liabilities is limited to the amount available in the waqf fund. In the event where thereis insufficient funds in waqf to meet their current payments less receipts, the deficit is funded by way of an interest free loan (Qard-e-Hasna) from the Shareholders' fund to the statutory fund (Takaful Business Statutory Funds). The amount of Qard-e-Hasna isrefundable to the shareholders' fund in event of the surplus balance in the statutory funds.

Principal actuarial assumptions used in computing technical reserves are:

a) the liability in respect of Group Family Takaful Business and riders of all types was set using the unearned premium method.Due provision was made for claims incurred but not reported (IBNR) and contingencies over the term of coverage.

Notes to the Financial StatementsFor the year ended December 31, 2013

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 27

b) the liability was calculated by summing up individual mathematical reserves for the policies. The mathematical reserves as atthe valuation date were calculated individually.

Group Takaful

The group family takaful contracts are issued typically on yearly renewable term basis (YRT). The Company offers group term lifeand group credit plans to its clients. For one or more of the takaful contracts following risks may be covered:

- Death due to any cause- Accidental Death Benefit- Accidental Permanent Total Disability (PTD-A)- Accidental Permanent Partial Disability (PPD-A)- Accidental Temporary Disability (TTD-A)- Natural Disability- Accidental Hospitalisation (AH) - Reimbursement of hospital expense due to accident with limits- Accidental Medical Expense Reimbursement (AMER) - Reimbursement of medical expense due to accident with limits- Critical Illness (CI)

Individual Takaful Contracts – unit linked

The Company offers Unit Linked Takaful Plans which provide Shariah compliant financial protection and investment vehicle toindividual participants. These plans carry cash value. The death benefit design is based on Constant Sum at Risk approach i.e. thesum cover is paid in addition to the cash value. The plans offer investment choices to the customer to direct their investment relatedcontributions based on their risk / return objectives. No investment guarantees are offered. The investment risk is borne by theparticipants.

The following riders are offered by the Company which can be added to the basic Unit Linked Takaful Plans.

Type of Contract Benefit Type

Accidental Death Benefit (ADB) Lump SumAccidental Death and Disability Benefit (ADDB) Lump SumFamily Income Benefit (FIB) AnnuityAdditional Takaful Benefit (ATB) Lump SumFuneral Expense Benefit (FEB) Lump SumTotal & Permanent Disability (TPD) Lump SumWaiver of Contribution (WOC) AnnuityFamily Protection Benefit (FPB) Lump SumCritical Illness (CI) Lump SumShareek-e-Zindagi Takaful Benefit (STB) Lump Sum

5.3 Technical reserve

Provision for outstanding claims including claims incurred but not reported (IBNR)

A liability for outstanding claims is recognised in respect of all claims incurred at the balance sheet date which represents theestimates of the claims intimated or assessed before the end of the accounting year and measured at the undiscounted value ofexpected future payments. Provision for outstanding claims include amounts in relation to unpaid reported claims, claims incurredbut not reported (IBNR) and expected claims settlement costs.

Provision for IBNR is made for the cost of settling claims incurred but not reported at the balance sheet date at a value determinedby the appointed actuary which takes into account the expected future patterns of claims and the claims of current period reportedsubsequent to the balance sheet date in Group Family Takaful. For Individual Family Takaful, a provision is made in respect of IBNRas a percentage of annual mortality costs.

Retakaful recoveries against outstanding claims and salvage recoveries are recognised as assets and measured at the amountexpected to be received.

Notes to the Financial StatementsFor the year ended December 31, 2013

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 28

Contribution deficiency reserve

The Company is required as per Takaful Rules, 2005 to maintain a provision in respect of contribution deficiency for the class of businesswhere the unearned contribution reserve is not adequate to meet the expected future liability, after retakaful claims and other supplementaryexpenses expected to be incurred after the balance sheet date in respect of the unexpired policies in that class of business at thebalance sheet date. The movement in the contribution deficiency reserve is recorded as an expense / income in the revenue account.

No provision has been made as the unearned contribution reserve for each class of business as at the year end is adequate to meetthe expected future liability after retakaful from claims and other expenses, expected to be incurred after the balance sheet date inrespect of policies in force at balance sheet date as per the advice of appointed actuary.

5.4 Commission

Commission expense incurred in obtaining and recording policies is deferred and recognised as an expense in accordance withthe pattern of recognition of contribution revenue.

5.5 Provision for claims

A liability for outstanding claims is recognised in respect of all claims incurred up to the balance sheet date and includes expected settlementcost, except for accident and health claims which are recognised as soon as reliable estimates of the claims amount can be made.

Claims where intimation of the event giving rise to the claim is received or in respect of investment linked business when the policyceases to participate in the earnings of the statutory funds are reported as claims in the revenue account. The liability for claimsincurred but not reported at the year end is determined by the appointed actuary and are included in technical reserves.

Claims recoveries receivable from the retakaful operator are recognised at the same time as the claim which gave rise to the rightof recovery and are measured at the amount expected to be recovered.

5.6 Retakaful

These contracts entered into by the Company with retakaful operator under which the Waqf cedes takaful risks assumed duringnormal course of its business and according to which the Waqf is compensated for losses on contracts issued byit are classified as retakaful contracts held.

Retakaful contribution

Retakaful contributions is recorded at the time the retakaful is ceded. Surplus from retakaful operator is recognised in the revenueaccount.

Retakaful assets and liabilities

Retakaful assets represent balances due from retakaful operator. Recoverable amounts are estimated in a manner consistent withthe outstanding claims provision and are in accordance with the retakaful treaties.

Retakaful liabilities represent balances due to retakaful companies. Amounts payable are calculated in a manner consistent withthe associated retakaful treaties.

Retakaful assets are not offset against related takaful liabilities. Income or expenses from retakaful contract are not offset againstexpenses or income from related takaful assets as required by Insurance Ordinance, 2000.

Retakaful assets or liabilities are derecognised when the contractual rights are extinguished or expired.

Impairment of retakaful assets

An impairment review of retakaful assets is performed at each balance sheet date. If there is an objective evidence exists that theasset is impaired, the Company reduces the carrying amount of the retakaful asset to its recoverable amount and recognises thatimpairment loss in the revenue account.

Retakaful expense is recognised as a liability in accordance with the pattern of recognition of related contribution.

Notes to the Financial StatementsFor the year ended December 31, 2013

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 29

5.7 Business segment

A business segment is a group of assets and operations engaged in providing products or services that are subject to risks andreturns that are different from those of other business segments. The Company accounts for segment reporting using the classesor sub classes of business (Takaful Business Statutory Funds) as specified under the Insurance Ordinance, 2000 and Securitiesand Exchange Commission (Insurance) Rules, 2002 as the primary reporting format.

The Company has two primary business segments for reporting purposes; Individual Family Takaful (Unit linked), Group FamilyTakaful:

a) The Individual Family Takaful (unit linked) segment provides family takaful coverage to individuals under unit based policiesissued by the Company.

b) The Group Family Takaful business segment provides family takaful coverage to member of business enterprises, corporateentities and common interest groups under group family takaful schemes issued by the Company.

5.8 Investments

Investments are being categorised as follows:

5.8.1 Available-for-sale (AFS)

Investments which are intended to be held for an undefined period of time but may be sold in response to the need for liquidity,changes in profit rates, equity prices or exchange rates are classified as available-for-sale.

Quoted

Subsequent to initial recognition at cost, quoted investments are stated at the lower of cost or market value (market value on anindividual investment basis being taken as lower if the fall is other than temporary) in accordance with the requirements of the SEC(Insurance) Rules, 2002. The Company uses stock exchange quotations at the balance sheet date to determine the market value.

Available-for-sale investments relating to the units assigned to policies of investment linked business are subsequently measuredat their fair values and difference taken to respective revenue account.

Unquoted

Unquoted investments are recorded at cost less impairment, if any.

5.8.2 Financial instruments at fair value through profit or loss

An instrument is classified at fair value through profit or loss if it is held-for-trading or is designated as such upon initial recognition.Financial instruments are designated at fair value through profit or loss if the Company manages such investments and makespurchase and sale decisions based on their fair value in accordance with the Company's documented risk management or investmentstrategy. Financial assets which are acquired principally for the purpose of generating profit from short-term price fluctuation or arepart of the portfolio in which there is recent actual pattern of short-term profit taking are classified as held-for-trading or a derivative.

Upon initial recognition, attributable transaction cost is recognised in profit and loss account when incurred. Financial instrumentsat fair value through profit or loss are measured at fair value, and changes therein are recognised in profit and loss account.

5.8.3 Date of recognition

All purchases and sales of investments that require delivery within the time frame established by regulations or market conventionare recognised at the trade date. Trade date is the date on which the Company commits to purchase or sell the investments.

5.8.4 Derecognition

All investments are derecognised when the rights to receive cash flows from the investments have expired or have been transferredand the Company has transferred substantially all risks and rewards of ownership.

Notes to the Financial StatementsFor the year ended December 31, 2013

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 30

5.9 Revenue recognition

Group Family Takaful contributions are recognised when due. A provision for unearned contribution is included in the technicalreserves.

First year Individual Family Takaful contributions are recognised once the related policies have been issued and the contributionsreceived. Renewal contributions are recognised upon receipt provided the policy is still in force. Single contributions recognised oncethe related policies are issued against the receipts of contribution.

Return on bank deposits and income on Islamic investment products is recorded on a time proportion basis taking into account theeffective yield on such investments.

Gain / loss on sale of AFS investment are included in profit and loss account in the period of sale.

Dividend income is recognised when right to receive such dividend is established.

Takaful operator fee (Wakala Fee) is recognised once the contribution is recognised in the books. The Company acts as Wakeelof the Waqf Fund. As such the Company is entitled for the wakala fee for the management of Takaful operation under Waqf Fundto meet its general and administrative expenses. For group, it is recognised over the period of policy and in case of individual takaful,it is recognised on the initiation of the policy as it represents cost of acquiring the policy. Mudarib fee is recognised on the basis ofshare of the investment profit of the Waqf.

Tharawat fee is recognised on time proportion basis on the net asset value of the participant investment Fund.

5.10 Waqf participants' liabilities

Waqf Participants' liabilities are stated at a value determined by the appointed actuary through an actuarial valuation carried outas at each balance sheet date. No valuation basis has been prescribed by the Commission under Sub-Section (5) of Section 50 ofthe Ordinance. Hence, in pursuance of Sub-Rule (2) of Rule 20 of the Insurance Rules, 2002, the valuation was carried out on theminimum valuation basis prescribed by the relevant rules made under the repealed Act.

5.11 Qard-e-Hasna

When the PTF including reserves are insufficient to meet the current payments less receipt the deficit, is funded by way of interestfree loan (qard-e-hasna) from the shareholder's fund.

5.12 Staff retirement benefits - Defined Contribution Plan

The Company operates a defined contribution plan for all permanent employees. Monthly contributions to the fund are made in accordancewith the employment rules by the employee and the Company. Contributions made to this fund are recognised as an expense.

5.13 Leave encashment

Liability in respect of provision for leave encashment is accounted for in the year in which these are earned on the basis of actuarialvaluation carried out using the Projected Unit Credit Method. Actuarial gain or losses if any, are recognised immediately.

5.14 Fixed assets and depreciation

Tangible

These are stated at cost less accumulated depreciation and impairment loss, if any. Depreciation is charged over the estimateduseful life of the asset on a systematic basis to income applying the straight line method, using the following rates:

Rates of Depreciation

Furniture and fixtures 10%Office equipments 10%Vehicles 20%Computer equipments 33%Leasehold Improvements 10%

Notes to the Financial StatementsFor the year ended December 31, 2013

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 31

Depreciation on additions is charged from the month in which the asset is available for use where as no depreciation is chargedfrom the month the asset is disposed off.

Subsequent cost are included in the assets' carrying amount or recognised as a separate asset, as appropriate, only when it ispossible that the future economic benefits associated with the items will flow to the Company and the cost of the item can bemeasured reliably. Maintenance and normal repairs are charged to profit and loss account currently.

An item of tangible asset is derecognised upon disposal or when no future economic benefits are expected from its use or disposal.Any gain or loss arising on derecognition of the asset (calculated as the difference between the net disposal proceeds and thecarrying amount of the asset) is included in the profit and loss in the year the asset is derecognised.

Intangible

These are stated at cost less accumulated amortisation and impairment loss, if any. Amortisation is charged over the estimateduseful life of the asset on a systematic basis to income applying the straight line method at the rates specified in note 20 to thefinancial statements.

Amortisation on additions is charged from the month in which the asset is acquired or capitalised whereas no amortisation is chargedfrom the month the asset is disposed off.

Capital work-in-progress

Capital work-in-progress is stated at cost less any impairment in value. It consists of advances made to suppliers in respect oftangible and intangible assets.

5.15 Ijarah

Ijarah rentals are recognised as an expense on accrual basis as and when the rentals become due.

5.16 Taxation

Current

Provision for current taxation is based on taxable income at the rates enacted or substantively enacted at the balance sheet dateafter taking into account available tax credits and rebates, if any.

Deferred

Deferred tax is accounted for using the balance sheet liability method in respect of all temporary differences at the balance sheetdate between the tax bases and carrying amounts of assets and liabilities for financial reporting purposes. Deferred tax liabilitiesare generally recognised for all taxable temporary differences and deferred tax assets are recognised to the extent that it is probablethat taxable profits will be available against which the deductible temporary differences, unused tax losses and tax credits can beutilised.

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply to the period when the asset is realisedor the liability is settled, based on the tax rates (and tax laws) that have been enacted or substantively enacted at the balance sheetdate. Deferred tax is charged or credited in the profit and loss account, except in the case of items credited or charged to equity inwhich case it is included in equity.

5.17 Financial instruments

Financial assets and financial liabilities other than those arising out of takaful contracts are recognised at the time when the Companybecomes a party to the contractual provisions of the instrument. At the time of initial recognition, financial assets and liabilities aremeasured at fair values which is the cost of consideration given or received for it. Financial assets are derecognised when thecontractual right to future cash flows from the asset expire or is transferred along with the risk and reward of the asset. Financialliabilities are derecognised when obligation specified in the contract is discharged, cancelled or expired. Any gain or loss onderecognition of the financial asset and liabilities are recognised in the profit and loss account of the current period.

Notes to the Financial StatementsFor the year ended December 31, 2013

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 32

5.18 Off setting the financial assets and liabilities

Financial assets and liabilities are only offset and the net amount is reported in the financial statements when the Company has alegally enforceable right to set off the recognised amounts and it intends either to settle on the net basis or to realise the asset andsettle the liability simultaneously.

5.19 Foreign currency translations

Foreign currency transactions are translated into Pak Rupees (functional currency) using the exchange rates prevailing at the dateof the transactions. Monetary assets and liabilities in foreign currencies are translated into Pak Rupees using the rate of exchangeruling at the balance sheet date. Exchange differences, if any, are transferred to profit and loss account.

5.20 Cash and cash equivalents

For the purpose of cash flow statement, cash and cash equivalents consist of cash and stamps in hand, balances with banks, short-term deposits maturing within three months of the year end, highly liquid short-term investments that are convertible to known amountof cash and are subject to insignificant risk of change in value.

5.21 Dividend and appropriation of reserves

Dividend and appropriation to reserves except appropriations required by the law or determined by actuary or allowed by InsuranceOrdinance, 2000 are recognised in the year in which these are approved.

5.22 Impairment

The carrying amount of assets (other than deferred tax asset) are reviewed at each balance sheet date to determine whether thereis any indication of impairment of any asset or group of assets. If such indication exists, the recoverable amount of the asset isestimated. An impairment loss is recognised whenever the carrying amount of an asset exceeds its recoverable amount. Impairmentlosses are recognised in profit and loss account / revenue account as appropriate.

5.23 Creditors and accruals

Liabilities for creditors and other amounts payable are carried at cost which is fair value of the consideration to be paid in future forgoods and / or services received, whether or not billed to the Company.

5.24 Provisions

Provisions are recognised when the Company has a present legal or constructive obligation as a result of past events, it is probablethat an out flow of resources embodying economic benefits will be required to settle the obligation and a reliable estimate of theamount can be made. Provisions are reviewed at each balance sheet date and adjusted to reflect the current best estimate.

5.25 Earnings per share

Earnings per share are calculated by dividing the profit / (loss) after tax attributable to Ordinary shareholders for the year by theweighted average number of shares outstanding during the year.

6. ISSUED SUBSCRIBED AND PAID-UP SHARE CAPITAL

2013 2012 2013 2012 (Number of shares) ---------- (Rupees) ----------

Ordinary shares of Rs.10 75,000,000 75,000,000 each fully paid in cash 750,000,000 750,000,000

Notes to the Financial StatementsFor the year ended December 31, 2013

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 33

Notes to the Financial StatementsFor the year ended December 31, 2013

7. PARTICIPANTS' INVESTMENT FUND

Opening balance 312,878,034 148,839,955

Allocated contributions 250,652,664 193,004,974

Withdrawals / refunds (62,910,759) (38,129,487)

Net risk contribution / ANF contribution (3,646,231) (1,587,317)

496,973,708 302,128,125

Investment income

Profit on Government Securities 11,439,003 6,464,534

Return on bank balances 12,631,168 12,078,209

Return on shariah compliant placements 8,700,242 3,677,540

Gain on disposal of listed Ordinary shares 965,419 248,737

Unrealised gain on revaluation of listed Ordinary shares 4,153,051 1,080,826

Dividend income 360,532 243,418

38,249,415 23,793,264

Expenditure

Bid offer expenses (12,560,816) (9,703,756)

Tharawat fee (on net assets related to participants) (5,867,048) (3,335,248)

Brokerage fee and other charges (31,181) (4,351)

(18,459,045) (13,043,355)

Net surplus for the year 19,790,370 10,749,909

Closing balance 516,764,078 312,878,034

Net asset value per units:

Income Fund

Units 413,265 333,686

Net asset value per unit 159.618 148.160

Balanced Fund

Units 2,504,849 1,622,142

Net asset value per unit 162.681 151.050

Aggressive Fund

Units 305,345 159,281

Net asset value per unit 141.831 115.609

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 34

2013 2012 ------------ (Rupees) ----------

Notes to the Financial StatementsFor the year ended December 31, 2013

DAWOOD FAMILY TAKAFUL LIMITEDA n n u a l R e p o r t - 2 0 1 3 35

8. OTHER CREDITORS AND ACCRUALS

Takaful Business Statutory Funds AggregateShare Holders' Individual Group Family

Fund Family Takaful Takaful 2013 2012Note

Wakala fee payable toshareholders' fund - - - - 11,236,736

Mudarib share payable toshareholders' fund - 609,697 98,856 708,553 1,350,167

Unearned wakala fee 2,772,259 - - 2,772,259 2,239,806Tharawat fee payable to

shareholders' fund - 84,961 - 84,961 120,970Payable to participant investment fund - 33,784,746 - 33,784,746 21,161,644Bid offer liability - 1,713,839 - 1,713,839 1,410,026Interfund payable 1,187,290 - 630,478 1,817,768 2,244,467Payable to suppliers 299,606 - - 299,606 1,062,168Salary payable 7,003,240 - - 7,003,240 4,498,331Provident fund payable 1,038,677 - - 1,038,677 2,663EOBI payable 249,080 - - 249,080 46,560Provision for bonus - - - - 193,307Provision for leave encashment 4,708,814 - - 4,708,814 4,646,585Accrued expenses 3,368,156 - - 3,368,156 3,020,449Audit fee payable 425,000 - - 425,000 400,000Consultancy fee payable 541,500 - - 541,500 596,500Withholding tax payable 1,463,444 - - 1,463,444 390,418Rent payable 117,575 - - 117,575 16,000Surplus distribution payable - 492,048 125,312 617,360 381,819Workers' welfare fund payable 648,593 - - 648,593 648,593Stale cheques payable 1,874,385 44,082 - 1,918,467 1,022,617Payable in respect of

purchase of shares 8.1 - 416,939 - 416,939 115,470Other payables 80,000 - - 80,000 2,901,602

25,777,619 37,146,312 854,646 63,778,577 59,706,898

8.1 These represent payable in respect of purchase of shares to Dawood Equities Limited, a related party.

9. CONTINGENCIES AND COMMITMENTS2013 2012

Ijarah lease rentals

Not later than one year 4,299,297 4,595,652Later than one year and not later than five years 5,083,560 7,008,525

9,382,857 11,604,177

10. CURRENT AND OTHER ACCOUNTSTakaful Business Statutory Funds Aggregate

Share holders' Individual Group FamilyFund Family Takaful Takaful 2013 2012

Note

Current accounts 2,624 7,254,228 - 7,256,852 14,826,324Saving accounts 10.1 35,209,285 164,990,042 - 200,199,327 150,234,122

Participant Takaful FundSaving accounts 10.1 - 18,676,235 8,453,511 27,129,746 13,877,745

35,211,909 190,920,505 8,453,511 234,585,925 178,938,191

10.1

11. DEPOSITS MATURING WITHIN TWELVE MONTHS

Takaful Business Statutory Funds AggregateShare Holders' Individual Group Family

Fund Family Takaful Takaful 2013 2012Note

Term deposits with islamic banks /islamic banking operations 11.1 & 11.2 75,000,000 365,000,000 - 440,000,000 325,000,000

75,000,000 365,000,000 - 440,000,000 325,000,000

------------------------------------------ (Rupees) ------------------------------------------

------------------------------------------ (Rupees) ------------------------------------------

------------------------------------------ (Rupees) ------------------------------------------

---------- (Rupees) ----------

These represent bank deposits maintained with Islamic banking operations of commercial banks under profit and loss sharing basis carryingprofit rates ranging from 5% to 9.20% (2012: 6% to 9%) per annum.

Notes to the Financial StatementsFor the year ended December 31, 2013

11.1

11.2

12. INVESTMENTS

Aggregate

2013 2012Note

Available-for-sale investments

Government securities 12.1 - 163,000,000 2,000,000 165,000,000 45,026,377Sukuks 12.2 193,453,728 3,749,999 - 197,203,727 235,274,612

193,453,728 166,749,999 2,000,000 362,203,727 280,300,989Held-for-trading investmentsListed shariah compliant shares 12.3 - 23,705,545 - 23,705,545 6,408,212

193,453,728 190,455,544 2,000,000 385,909,272 286,709,201

12.1 Government securities

Government of PakistanIjara sukuks 12.1.1 - 163,000,000 2,000,000 165,000,000 45,026,377

- 163,000,000 2,000,000 165,000,000 45,026,377

12.1.1

Aggregate

2013 201212.2 Sukuks Note 2013 2012