aon investment research and insights msci s … investment research and insights msci s announcement...

TRANSCRIPT

Aon Investment Research and Insights

MSCI’s Announcement to Add China A-Shares to its Emerging Markets IndexLooking Beyond the Tiny Percentage

November 2017

Aon HewittRetirement and Investment

2 Name of study or publication

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

China A-Shares, a big market but a tiny weight in the MSCI EM index . . 3

Background of the baby step . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

When A-Shares are fully included . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Implications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

More than the influx of passive money . . . . . . . . . . . . . . . . . . . . . . . . 10

Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Table of contents

About Aon Investment Research and InsightsAon Hewitt’s robust portfolio of ideas, tools and researched solutions support trustees and sponsors to anticipate their future investment requirements.

By beginning to identify investment research and communicate ideas before they are needed we can shorten the implementation times for our clients and act in a timely way when opportunities are correctly priced.

To learn more and to access other research and insights from Aon’s investment experts, visit aonhewitt.com/investment

Aon Hewitt | Retirement and Investment | Research and Insights MSCI’s Announcement to Add China A-Shares to its Emerging Markets Index 3

China A-Shares, a big market but a tiny weight in the MSCI EM index

Introduction

On 20 June 2017, MSCI announced that it will add 222 China A Large Cap shares to the MSCI Emerging Markets (“EM”) Index. When the inclusion is officially launched in June 2018, China A Large Cap shares are expected to account for about 0.73% of the MSCI EM Index.

As the latest note in a series of three1 on the globalisation

of China’s financial markets, this paper explains the

background of the index change, estimates future

changes in the Index composition, and also points out the

potential implications on institutional investors if China

A-Shares claim 17% or more in the MSCI EM Index.

We believe:

• In the near term, the announcement has more

of a symbolic meaning than actual impact.

• However, this tiny index change could potentially

open up a huge opportunity in the future.

• Further inclusion of A-Shares could happen

much sooner than the initial review process.

• The potential influx of institutional money could

reach at least 5.3% of the value of all A-Shares.

• Institutional investors should understand the

implications and adjust accordingly.

Figure 1. Top equity markets by market capitalisation ($Bn) as of 31/3/2017Being the second largest economy in the world, China has expanded its equity markets over the past three decades to a size only ranked after the U.S. by market capitalisation.

However, international investors’

participation in China’s equity

markets has not been proportionate

to its share of the world economy

and of the global capital market,

primarily due to the tight control

of foreign ownership and access

by Chinese authorities. Based on

listing locations and accessibility

to different groups of investors,

China’s equity market is unique in

its regulation and structured with

multiple classes of shares such as

A, B, and H shares, as well as Red

and P chips and overseas listings.

0

$5,000

$10,000

$15,000

$2,0000

$25,000

$30,000

Shan

ghai

, She

nzhe

n &

Hon

g Ko

ng C

omb

ined

Shan

ghai

& S

henz

hen

Com

bin

ed

NYS

E&

Nas

daq

Com

bin

ed

Nor

ther

n Eu

rop

e(N

ASD

AQ N

ord

ic E

xcha

nge)

Aus

tral

ia

Kore

a

Switz

erla

nd

Ger

man

y (D

euts

che

Börs

e)

Ind

ia (

Bom

bay

)

Can

ada

(Tor

onto

)

Chi

na (

Shen

zhen

)

Hon

g Ko

ng

Euro

pe

(NYS

E Eu

rone

xt)

UK

(Lon

don

Sto

ck E

xcha

nge

Gro

up)

Chi

na (

Shan

ghai

)

Jap

an (

Jap

an E

xcha

nge

Gro

up)

U.S

. (N

asd

aq)

U.S

. (N

YSE

Euro

next

)

1 Aon research: Onshore Chinese Bonds Enter the Global Bond Universe, by Lucinda Downing Aon research: All Aboard the Through Train, China A-Shares, by James Jackson

Aon Hewitt | Retirement and Investment | Research and Insights MSCI’s Announcement to Add China A-Shares to its Emerging Markets Index 4

Table 1. Comparison of multiple classes of shares

Table 2. Comparison of A-Shares listings in onshore China markets with other China listings

A-Shares B-Shares H-Shares Red Chips P Chips Overseas Listings

Incorporation location China China China Outside of China

Outside of China

China

Listing location China China Hong Kong Hong Kong Hong Kong U.S./Singapore

Trading currency RMB USD/HKD HKD HKD HKD USD/SGD

Availability to foreign investors

Only under QFII, RQFII, and Stock Connect

Yes Yes Yes Yes Yes

Hong Kong Shanghai Shenzhen Nasdaq NYSE

Main Board

Chi-Next A-Shares B-Shares A-Shares B-Shares Overseas Listings *

Overseas Listings*

No. of listed companies

1,746 287 1,294 51 1,983 49 127 22

No. of listed H-Shares 222 24 N/A N/A N/A N/A N/A N/A

No. of listed Red Chips

152 6 N/A N/A N/A N/A N/A N/A

No. of listed P Chips* 614 N/A N/A N/A N/A N/A N/A N/A

No. of listed securities 10,003 288 1,294 51 1,983 49 127 22

Market capitalisation (billion USD)

$3,623 $34 $4,489 $15 $3,309 $12 $1,056 $71

Floating market capitalisation (billion USD)

N/A N/A $3,764 $15 $2,304 $12 N/A N/A

Total market turnover (million USD)

$10,006 $24,147 $31,058 N/A N/A

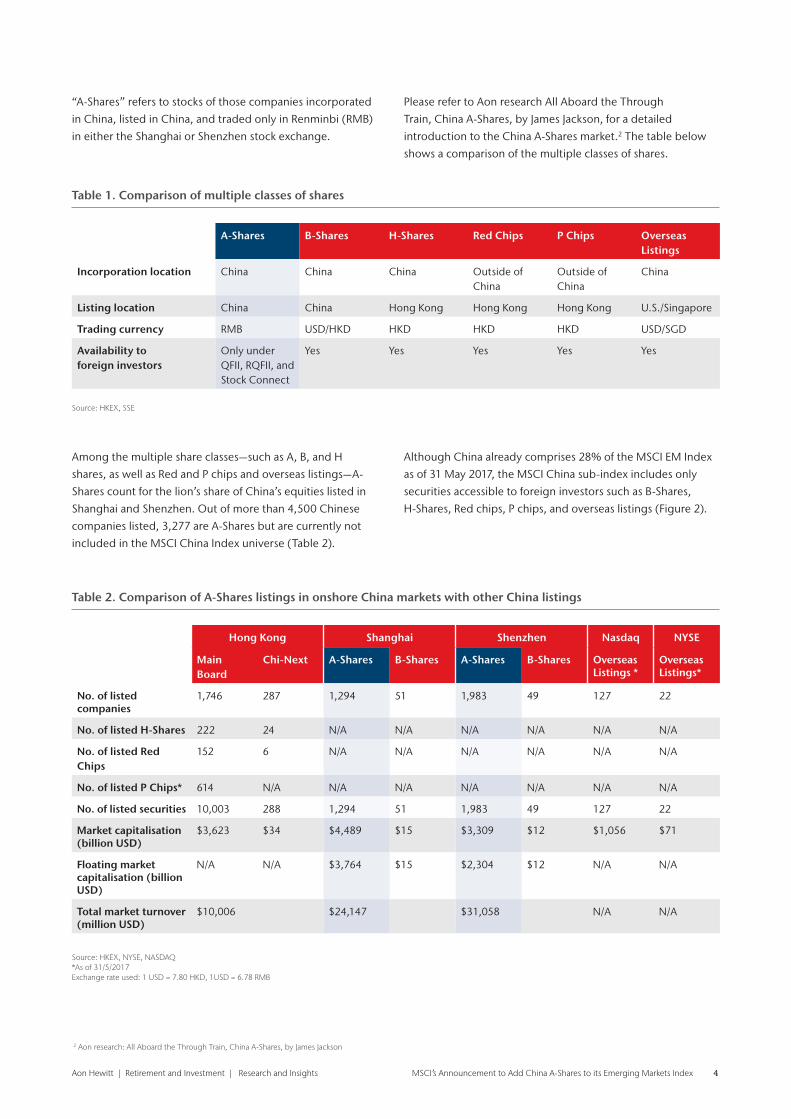

“A-Shares” refers to stocks of those companies incorporated

in China, listed in China, and traded only in Renminbi (RMB)

in either the Shanghai or Shenzhen stock exchange.

Please refer to Aon research All Aboard the Through

Train, China A-Shares, by James Jackson, for a detailed

introduction to the China A-Shares market.2 The table below

shows a comparison of the multiple classes of shares.

Among the multiple share classes—such as A, B, and H

shares, as well as Red and P chips and overseas listings—A-

Shares count for the lion’s share of China’s equities listed in

Shanghai and Shenzhen. Out of more than 4,500 Chinese

companies listed, 3,277 are A-Shares but are currently not

included in the MSCI China Index universe (Table 2).

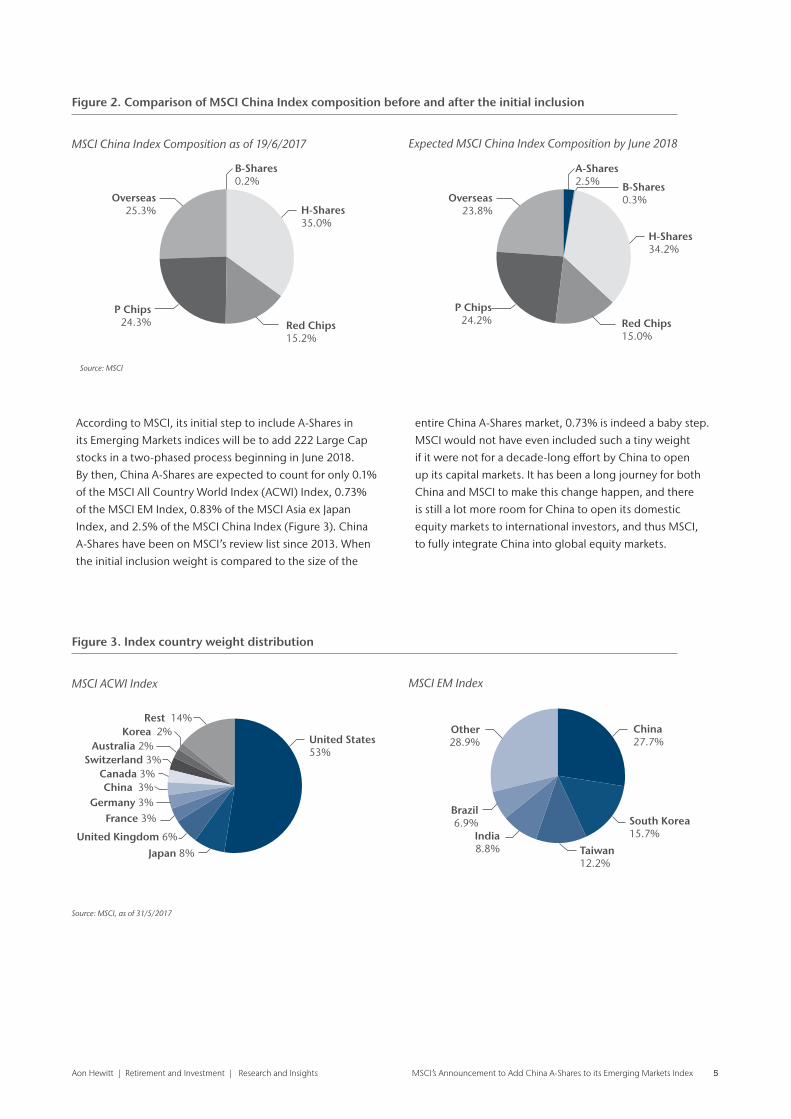

Although China already comprises 28% of the MSCI EM Index

as of 31 May 2017, the MSCI China sub-index includes only

securities accessible to foreign investors such as B-Shares,

H-Shares, Red chips, P chips, and overseas listings (Figure 2).

Source: HKEX, NYSE, NASDAQ*As of 31/5/2017Exchange rate used: 1 USD = 7.80 HKD, 1USD = 6.78 RMB

Source: HKEX, SSE

2 Aon research: All Aboard the Through Train, China A-Shares, by James Jackson

Aon Hewitt | Retirement and Investment | Research and Insights MSCI’s Announcement to Add China A-Shares to its Emerging Markets Index 5

Figure 2. Comparison of MSCI China Index composition before and after the initial inclusion

Figure 3. Index country weight distribution

Expected MSCI China Index Composition by June 2018

MSCI EM Index

MSCI China Index Composition as of 19/6/2017

MSCI ACWI Index

Source: MSCI, as of 31/5/2017

Source: MSCI

According to MSCI, its initial step to include A-Shares in

its Emerging Markets indices will be to add 222 Large Cap

stocks in a two-phased process beginning in June 2018.

By then, China A-Shares are expected to count for only 0.1%

of the MSCI All Country World Index (ACWI) Index, 0.73%

of the MSCI EM Index, 0.83% of the MSCI Asia ex Japan

Index, and 2.5% of the MSCI China Index (Figure 3). China

A-Shares have been on MSCI’s review list since 2013. When

the initial inclusion weight is compared to the size of the

entire China A-Shares market, 0.73% is indeed a baby step.

MSCI would not have even included such a tiny weight

if it were not for a decade-long effort by China to open

up its capital markets. It has been a long journey for both

China and MSCI to make this change happen, and there

is still a lot more room for China to open its domestic

equity markets to international investors, and thus MSCI,

to fully integrate China into global equity markets.

Overseas25.3%

P Chips24.3% Red Chips

15.2%

H-Shares35.0%

B-Shares0.2%

Overseas23.8%

P Chips24.2% Red Chips

15.0%

H-Shares34.2%

B-Shares0.3%

A-Shares2.5%

Rest 14% Korea 2%

Australia 2% Switzerland 3%

Canada 3% China 3%

Germany 3% France 3%

United Kingdom 6%

Japan 8%

United States53%

Other28.9%

Brazil6.9%

India8.8% Taiwan

12.2%

South Korea15.7%

China 27.7%

Aon Hewitt | Retirement and Investment | Research and Insights MSCI’s Announcement to Add China A-Shares to its Emerging Markets Index 6

Background of the baby step

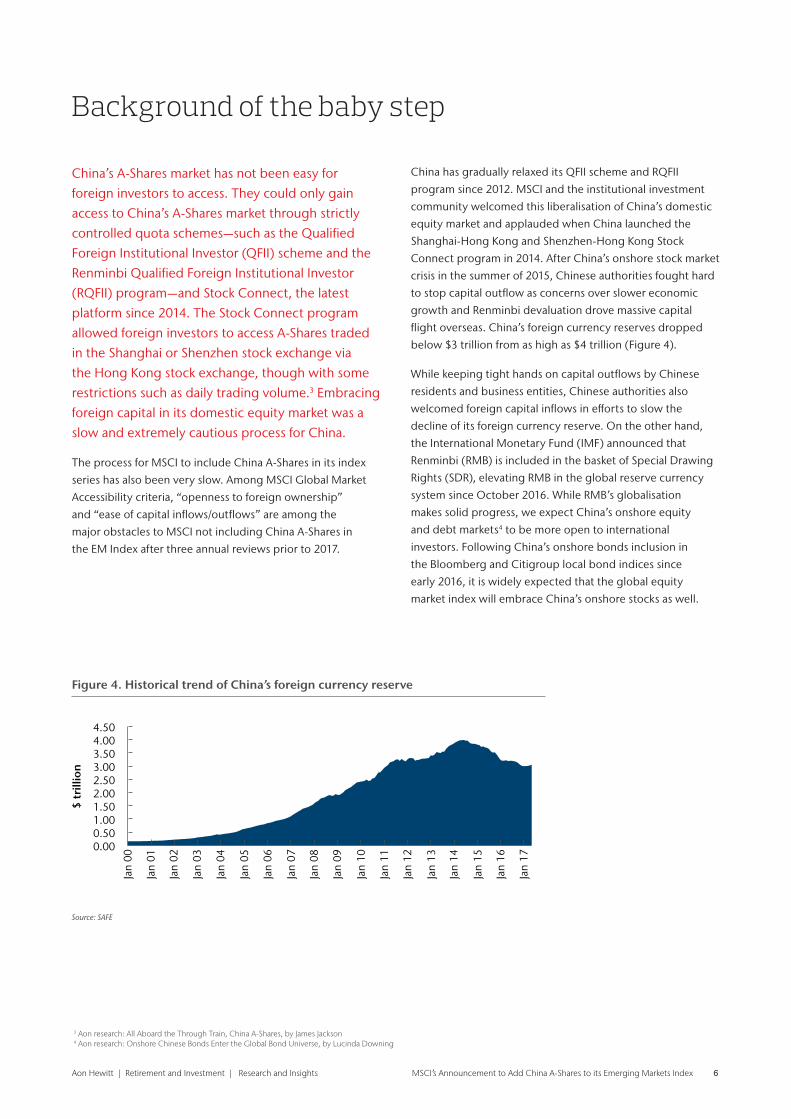

China’s A-Shares market has not been easy for foreign investors to access. They could only gain access to China’s A-Shares market through strictly controlled quota schemes—such as the Qualified Foreign Institutional Investor (QFII) scheme and the Renminbi Qualified Foreign Institutional Investor (RQFII) program—and Stock Connect, the latest platform since 2014. The Stock Connect program allowed foreign investors to access A-Shares traded in the Shanghai or Shenzhen stock exchange via the Hong Kong stock exchange, though with some restrictions such as daily trading volume.3 Embracing foreign capital in its domestic equity market was a slow and extremely cautious process for China.

The process for MSCI to include China A-Shares in its index

series has also been very slow. Among MSCI Global Market

Accessibility criteria, “openness to foreign ownership”

and “ease of capital inflows/outflows” are among the

major obstacles to MSCI not including China A-Shares in

the EM Index after three annual reviews prior to 2017.

China has gradually relaxed its QFII scheme and RQFII

program since 2012. MSCI and the institutional investment

community welcomed this liberalisation of China’s domestic

equity market and applauded when China launched the

Shanghai-Hong Kong and Shenzhen-Hong Kong Stock

Connect program in 2014. After China’s onshore stock market

crisis in the summer of 2015, Chinese authorities fought hard

to stop capital outflow as concerns over slower economic

growth and Renminbi devaluation drove massive capital

flight overseas. China’s foreign currency reserves dropped

below $3 trillion from as high as $4 trillion (Figure 4).

While keeping tight hands on capital outflows by Chinese

residents and business entities, Chinese authorities also

welcomed foreign capital inflows in efforts to slow the

decline of its foreign currency reserve. On the other hand,

the International Monetary Fund (IMF) announced that

Renminbi (RMB) is included in the basket of Special Drawing

Rights (SDR), elevating RMB in the global reserve currency

system since October 2016. While RMB’s globalisation

makes solid progress, we expect China’s onshore equity

and debt markets4 to be more open to international

investors. Following China’s onshore bonds inclusion in

the Bloomberg and Citigroup local bond indices since

early 2016, it is widely expected that the global equity

market index will embrace China’s onshore stocks as well.

Figure 4. Historical trend of China’s foreign currency reserve

0.00

Jan

00

Jan

01

Jan

02

Jan

03

Jan

04

Jan

05

Jan

06

Jan

07

Jan

08

Jan

09

Jan

10

Jan

11

Jan

12

Jan

13

Jan

14

Jan

15

Jan

16

Jan

17

0.501.001.502.002.503.003.504.004.50

$ tr

illio

n

Source: SAFE

3 Aon research: All Aboard the Through Train, China A-Shares, by James Jackson4 Aon research: Onshore Chinese Bonds Enter the Global Bond Universe, by Lucinda Downing

Aon Hewitt | Retirement and Investment | Research and Insights MSCI’s Announcement to Add China A-Shares to its Emerging Markets Index 7

When A-Shares are fully included

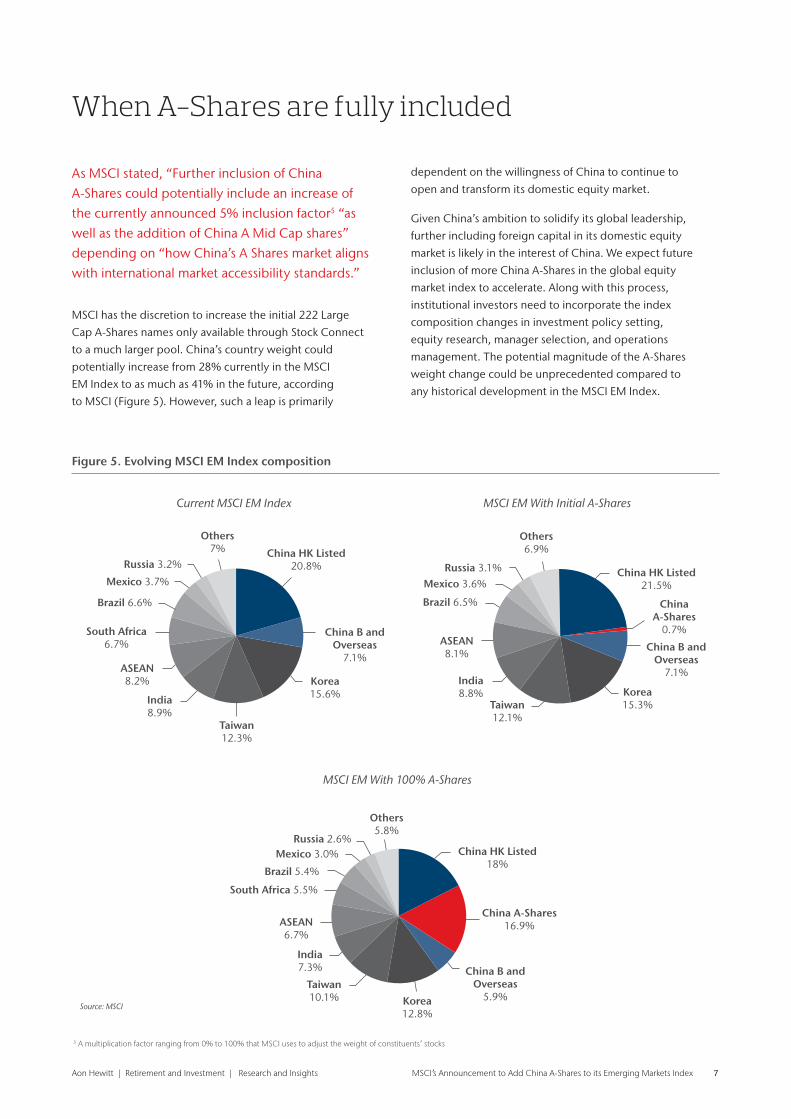

As MSCI stated, “Further inclusion of China A-Shares could potentially include an increase of the currently announced 5% inclusion factor5 “as well as the addition of China A Mid Cap shares” depending on “how China’s A Shares market aligns with international market accessibility standards.”

MSCI has the discretion to increase the initial 222 Large

Cap A-Shares names only available through Stock Connect

to a much larger pool. China’s country weight could

potentially increase from 28% currently in the MSCI

EM Index to as much as 41% in the future, according

to MSCI (Figure 5). However, such a leap is primarily

dependent on the willingness of China to continue to

open and transform its domestic equity market.

Given China’s ambition to solidify its global leadership,

further including foreign capital in its domestic equity

market is likely in the interest of China. We expect future

inclusion of more China A-Shares in the global equity

market index to accelerate. Along with this process,

institutional investors need to incorporate the index

composition changes in investment policy setting,

equity research, manager selection, and operations

management. The potential magnitude of the A-Shares

weight change could be unprecedented compared to

any historical development in the MSCI EM Index.

Figure 5. Evolving MSCI EM Index composition

5 A multiplication factor ranging from 0% to 100% that MSCI uses to adjust the weight of constituents’ stocks

Others7%

Russia 3.2%

Mexico 3.7%

Brazil 6.6%

South Africa6.7%

ASEAN8.2%

India8.9%

Taiwan12.3%

Korea15.6%

China B andOverseas

7.1%

China HK Listed20.8%

Others6.9%

Russia 3.1%Mexico 3.6%

Brazil 6.5%

ASEAN8.1%

India8.8%

Taiwan12.1%

Korea15.3%

China B andOverseas

7.1%

ChinaA-Shares

0.7%

China HK Listed21.5%

Others5.8%

Russia 2.6%Mexico 3.0%

Brazil 5.4%

South Africa 5.5%

ASEAN6.7%

India7.3%

Taiwan10.1% Korea

12.8%

China B andOverseas

5.9%

China A-Shares16.9%

China HK Listed18%

Others7%

Russia 3.2%

Mexico 3.7%

Brazil 6.6%

South Africa6.7%

ASEAN8.2%

India8.9%

Taiwan12.3%

Korea15.6%

China B andOverseas

7.1%

China HK Listed20.8%

Others6.9%

Russia 3.1%Mexico 3.6%

Brazil 6.5%

ASEAN8.1%

India8.8%

Taiwan12.1%

Korea15.3%

China B andOverseas

7.1%

ChinaA-Shares

0.7%

China HK Listed21.5%

Others5.8%

Russia 2.6%Mexico 3.0%

Brazil 5.4%

South Africa 5.5%

ASEAN6.7%

India7.3%

Taiwan10.1% Korea

12.8%

China B andOverseas

5.9%

China A-Shares16.9%

China HK Listed18%

Source: MSCI

Current MSCI EM Index MSCI EM With Initial A-Shares

MSCI EM With 100% A-Shares

Aon Hewitt | Retirement and Investment | Research and Insights MSCI’s Announcement to Add China A-Shares to its Emerging Markets Index 8

If China’s country weight claims 41% in the EM Index, and A-Shares alone count for 17%, as MSCI has illustrated as a future possibility, investors will need to incorporate the A-Shares market risk/return profile in their capital market assumptions for Emerging Markets Equity.

When A-Shares are at a full inclusion stage, we believe

investors need to re-evaluate the capability of their broad

mandate managers in Emerging Markets or Asia markets

and be ready to deploy specialist managers if necessary.

Whether adopting a passive or active strategy, investors

will have to assess their prior experience and exposure

and identify available resources. Certain style and factor

investment managers will need to calibrate their factor

investing approaches for some unique characteristics

of A-Shares. On the operational front, investors need

to embrace different trading and settlement rules.

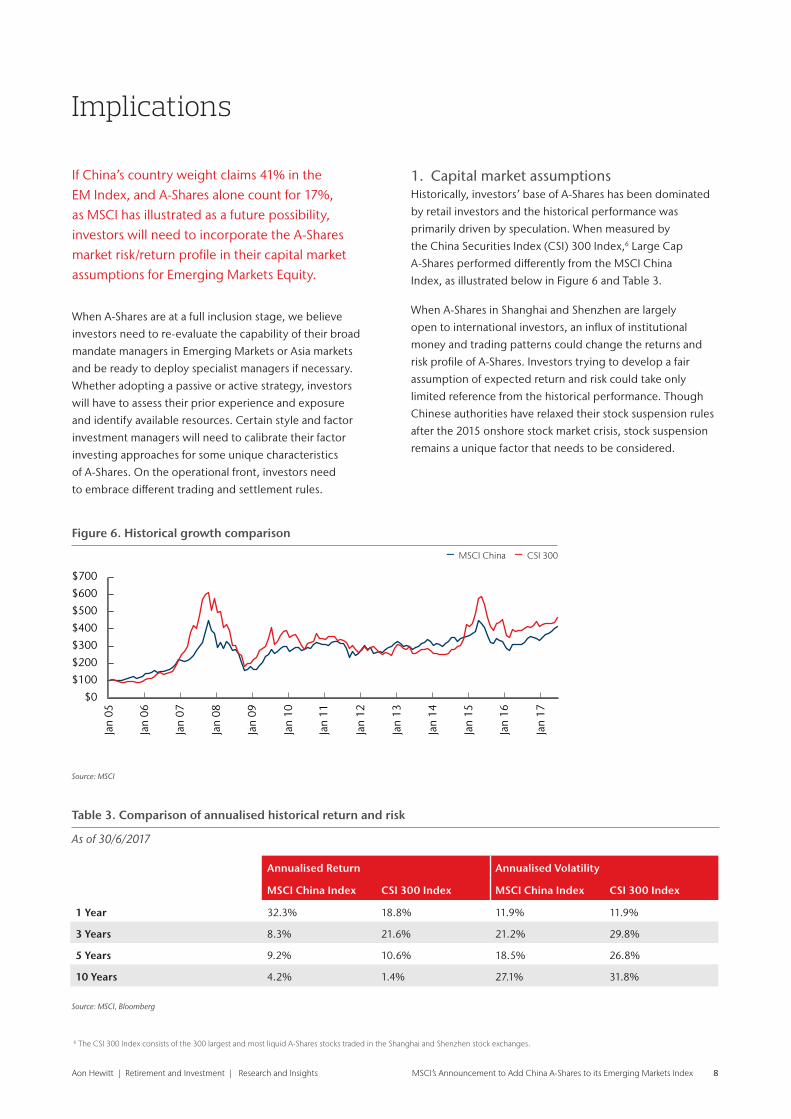

1 . Capital market assumptions Historically, investors’ base of A-Shares has been dominated

by retail investors and the historical performance was

primarily driven by speculation. When measured by

the China Securities Index (CSI) 300 Index,6 Large Cap

A-Shares performed differently from the MSCI China

Index, as illustrated below in Figure 6 and Table 3.

When A-Shares in Shanghai and Shenzhen are largely

open to international investors, an influx of institutional

money and trading patterns could change the returns and

risk profile of A-Shares. Investors trying to develop a fair

assumption of expected return and risk could take only

limited reference from the historical performance. Though

Chinese authorities have relaxed their stock suspension rules

after the 2015 onshore stock market crisis, stock suspension

remains a unique factor that needs to be considered.

Implications

Figure 6. Historical growth comparison

– MSCI China – CSI 300

Table 3. Comparison of annualised historical return and risk

As of 30/6/2017

Annualised Return Annualised Volatility

MSCI China Index CSI 300 Index MSCI China Index CSI 300 Index

1 Year 32.3% 18.8% 11.9% 11.9%

3 Years 8.3% 21.6% 21.2% 29.8%

5 Years 9.2% 10.6% 18.5% 26.8%

10 Years 4.2% 1.4% 27.1% 31.8%

$0

$100

$200

$300

$400

$500

$600

$700

Jan

05

Jan

06

Jan

07

Jan

08

Jan

09

Jan

10

Jan

11

Jan

12

Jan

13

Jan

14

Jan

15

Jan

16

Jan

17

Source: MSCI

Source: MSCI, Bloomberg

6 The CSI 300 Index consists of the 300 largest and most liquid A-Shares stocks traded in the Shanghai and Shenzhen stock exchanges.

Aon Hewitt | Retirement and Investment | Research and Insights MSCI’s Announcement to Add China A-Shares to its Emerging Markets Index 9

2 . Passive vs . active considerations Asset owners need to evaluate whether a passive or

active strategy is the best approach to gain exposure. We

believe investors without prior exposure or experience

with A Shares are better off adopting a passive strategy.

Nevertheless, the challenge is then shifted to managers and

custodian banks, which need to be ready to include 2,000+

companies. Investors already embracing an active strategy

in their Emerging Markets Equity mandate need to realise

that current active Emerging Markets managers will be

challenged with a far broader research base, yet presented

with opportunities of alpha generation. Asset owners need

to check whether their equity fund managers have sufficient

resources to develop insights around the A-Shares market.

3 . Broader mandate or specialist manager We still believe a broader mandate of Emerging Markets

and ACWI Asia would be appropriate at the initial stage of

MSCI EM Index inclusion. However, at a full inclusion stage,

investors must determine whether a broader mandate

manager has sufficient capability to cover the entire

China market. Otherwise, a specialist manager should be

considered. By that time, we suspect that MSCI might roll

out the Emerging Markets ex China Index to pair with the

China Index so that investors have sufficient flexibility to

deploy different strategies. We encourage investors to review

and evaluate their current Global Equity and Emerging

Markets managers in the context of the evolving landscape.

4 . Calibration of style and factor investment approach

We would like to point out some unique China A-Shares

market characteristics for investors who are used to

mature markets in the U.S. and Europe. For example,

many state-owned enterprises (SOEs) are traded at

relatively low price-to-earnings (P/E) ratios compared to

the broader A-Shares. We suggest that traditional value

investors resist comparing SOEs to other value stocks on

the same platform. Due to the unique stock suspension

rule in Shanghai and Shenzhen exchanges, historical

volatility might not accurately reflect a stock’s real risk

level. Low-volatility managers will need to calibrate their

approach to count in the impact of stock suspensions.

High turnover of fund managers7 is common in China.

Therefore, short track records of many funds in A-Shares

are another reality for investors relying on back testing.

5 . Different trading and settlement rulesA-Shares are subject to some unique trading rules, such as

a daily price limit of +/10% and unit of trading quantity.

Most A-Shares are limited to a daily trading price range of

+10% to 10% of the prior day’s closing price. Currently,

trading quantity of A-Shares cannot be any random number

of shares, but has to be in the multiples of 100 shares. In

addition to the trading rule difference, the current settlement

cycle of A-Shares through Stock Connect is also different

from the schedule in the U.S. Securities settle on T and

money on T+1 for A-Shares through Stock Connect, as

compared to securities on T and money on T+3 in the U.S.8

If such a settlement cycle difference remains in the future,

we don’t see it as a risk for managers and brokers. Over the

past few years, working with local brokers, sub-custodian

banks, and clearing houses in China, many institutions have

already handled investing, and custody and accounting

in the China market effectively through Stock Connect.

7 Aon Hewitt Retirement & Investment Blog: “Volatility in China’s Stock Market” by Fei Amy Shang and John Thompson – https://retirementandinvestmentblog.aon.com/BlogHome/Blog/October-2015/Volatility-in-China’s-Stock-Market.aspx

8 http://english.sse.com.cn/investors/shhkconnect/clear/

Aon Hewitt | Retirement and Investment | Research and Insights MSCI’s Announcement to Add China A-Shares to its Emerging Markets Index 10

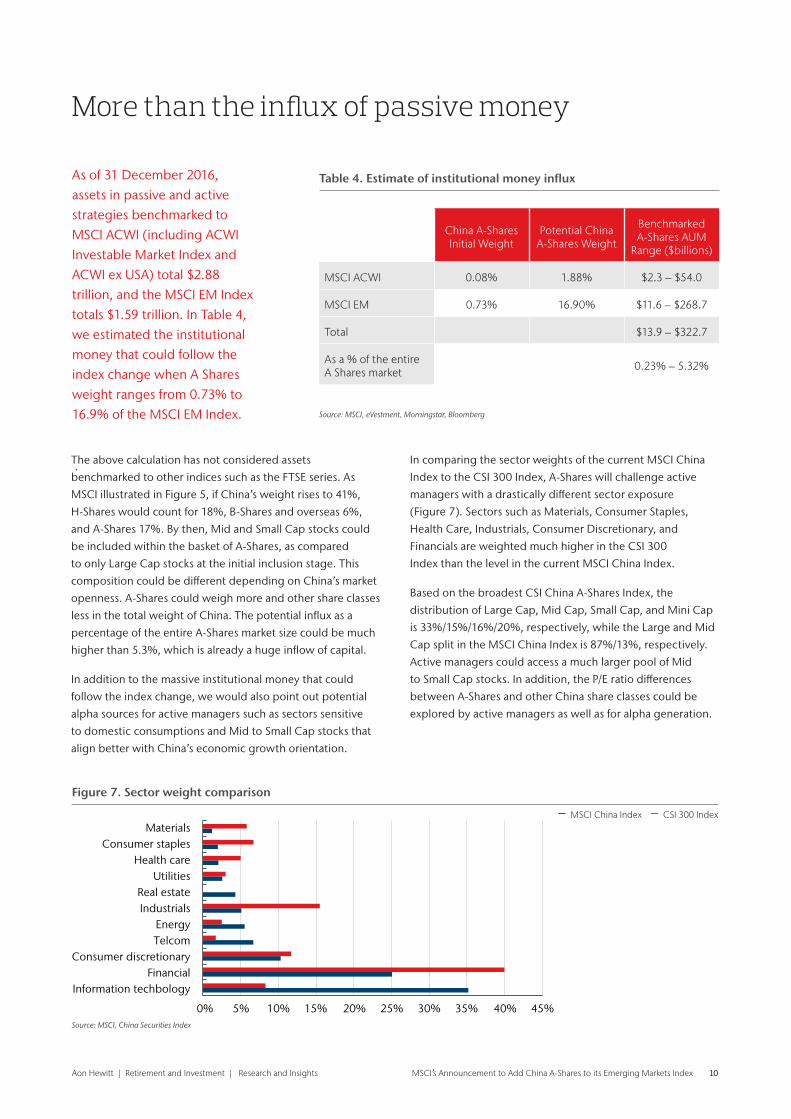

As of 31 December 2016, assets in passive and active strategies benchmarked to MSCI ACWI (including ACWI Investable Market Index and ACWI ex USA) total $2.88 trillion, and the MSCI EM Index totals $1.59 trillion. In Table 4, we estimated the institutional money that could follow the index change when A Shares weight ranges from 0.73% to 16.9% of the MSCI EM Index.

The above calculation has not considered assets

benchmarked to other indices such as the FTSE series. As

MSCI illustrated in Figure 5, if China’s weight rises to 41%,

H-Shares would count for 18%, B-Shares and overseas 6%,

and A-Shares 17%. By then, Mid and Small Cap stocks could

be included within the basket of A-Shares, as compared

to only Large Cap stocks at the initial inclusion stage. This

composition could be different depending on China’s market

openness. A-Shares could weigh more and other share classes

less in the total weight of China. The potential influx as a

percentage of the entire A-Shares market size could be much

higher than 5.3%, which is already a huge inflow of capital.

In addition to the massive institutional money that could

follow the index change, we would also point out potential

alpha sources for active managers such as sectors sensitive

to domestic consumptions and Mid to Small Cap stocks that

align better with China’s economic growth orientation.

In comparing the sector weights of the current MSCI China

Index to the CSI 300 Index, A-Shares will challenge active

managers with a drastically different sector exposure

(Figure 7). Sectors such as Materials, Consumer Staples,

Health Care, Industrials, Consumer Discretionary, and

Financials are weighted much higher in the CSI 300

Index than the level in the current MSCI China Index.

Based on the broadest CSI China A-Shares Index, the

distribution of Large Cap, Mid Cap, Small Cap, and Mini Cap

is 33%/15%/16%/20%, respectively, while the Large and Mid

Cap split in the MSCI China Index is 87%/13%, respectively.

Active managers could access a much larger pool of Mid

to Small Cap stocks. In addition, the P/E ratio differences

between A-Shares and other China share classes could be

explored by active managers as well as for alpha generation.

More than the influx of passive money

Table 4. Estimate of institutional money influx

Source: MSCI, eVestment, Morningstar, Bloomberg

China A-Shares Initial Weight

Potential China A-Shares Weight

Benchmarked A-Shares AUM

Range ($billions)

MSCI ACWI 0.08% 1.88% $2.3 – $54.0

MSCI EM 0.73% 16.90% $11.6 – $268.7

Total $13.9 – $322.7

As a % of the entire A Shares market 0.23% – 5.32%

Figure 7. Sector weight comparison

– MSCI China Index – CSI 300 Index

0%

Information techbologyFinancial

Consumer discretionaryTelcomEnergy

IndustrialsReal estate

UtilitiesHealth care

Consumer staplesMaterials

5% 10% 15% 20% 25% 30% 35% 40% 45%Source: MSCI, China Securities Index

Aon Hewitt | Retirement and Investment | Research and Insights MSCI’s Announcement to Add China A-Shares to its Emerging Markets Index 11

Conclusion

This will account for about 0.73% of

the index

China A Large Cap shares are being

added to the MSCI EM Index

Small change but opens up a large

opportunity

We welcome MSCI’s move to include China A-Shares in the MSCI EM Index, as investors start to access the investment universe of the second largest economy in the world.

In the near term, the announcement has more of a symbolic

meaning than actual impact on market participants. We

encourage investors to look beyond the initial tiny weight

that A-Shares constitute in the MSCI EM Index. We expect

A-Shares to claim higher weight in the EM Index and at a

much faster pace if China further opens up its domestic

equity market. Before A Shares account for a more substantial

weight, we believe that investors should understand the

potential implication of such a change and make adjustments

on investment policy setting, manager selection, investment

approach, and operational management accordingly.

We’re here to empower results

For more information visit

aonhewitt.com/investment or contact your Aon representative.

Aon Hewitt | Retirement and Investment | Research and Insights MSCI’s Announcement to Add China A-Shares to its Emerging Markets Index 12

Contacts

With thanks to our author

Fei Amy Shang, CFASenior Investment ConsultantInvestment Policy Services+1(312) 381 [email protected]

John BelgroveSenior [email protected]+44 (0)20 7086 9021

Kate Charsley [email protected]+44 (0)117 900 4414

Sion ColeSenior Partner and Head of Client [email protected]+44 (0)20 7086 9432Follow me on twitter – @PensionsSion

Tim [email protected]+44 (0)20 7086 0252 Follow me on Twitter @investmenttim

Tim GilesHead of UK Investment [email protected]+44 (0)20 7086 9115

Aon Hewitt empowers organisations and individuals to

secure a better future through innovative retirement,

health, and talent solutions. We advise and design a

wide range of solutions that enable our clients’ success.

Our teams of experts help clients navigate the risks and

opportunities to optimise financial security; redefine

health solutions for greater choice, affordability, and

wellbeing; and achieve sustainable growth by driving

business performance through people performance.

We serve more than 20,000 clients through our 15,000

professionals located in 50 countries around the world.

For more information, please visit aon.com

About Aon Hewitt

About Aon Aon plc (NYSE:AON) is a leading global professional

services firm providing a broad range of risk, retire-

ment and health solutions. Our 50,000 colleagues in

120 countries empower results for clients by using

proprietary data and analytics to deliver insights that

reduce volatility and improve performance.

For further information on our capabilities and to

learn how we empower results for clients, please visit

http://aon.mediaroom.com.

© Aon plc 2017. All rights reserved.This document and any enclosures or attachments are prepared on

the understanding that it is solely for the benefit of the addressee(s).

Unless we provide express prior written consent, no part of this

document should be reproduced, distributed or communicated to

anyone else and, in providing this document, we do not accept or

assume any responsibility for any other purpose or to anyone other

than the addressee(s) of this document.

Notwithstanding the level of skill and care used in conducting due

diligence into any organisation that is the subject of a rating in this

document, it is not always possible to detect the negligence, fraud,

or other misconduct of the organisation being assessed or any

weaknesses in that organisation’s systems and controls or operations.

This document and any due diligence conducted is based upon

information available to us at the date of this document and takes no

account of subsequent developments. In preparing this document we

may have relied upon data supplied to us by third parties (including

those that are the subject of due diligence) and therefore no warranty

or guarantee of accuracy or completeness is provided. We cannot

be held accountable for any error, omission or misrepresentation of

any data provided to us by third parties (including those that are the

subject of due diligence). This document is not intended by us to

form a basis of any decision by any third party to do or omit to do

anything.

Any opinions or assumptions in this document have been derived

by us through a blend of economic theory, historical analysis and/or

other sources. Any opinion or assumption may contain elements of

subjective judgement and are not intended to imply, nor should be

interpreted as conveying, any form of guarantee or assurance by us of

any future performance. Views are derived from our research process

and it should be noted in particular that we can not research legal,

regulatory, administrative or accounting procedures and accordingly

make no warranty and accept no responsibility for consequences

arising from relying on this document in this regard.

Calculations may be derived from our proprietary models in use at

that time. Models may be based on historical analysis of data and

other methodologies and we may have incorporated their subjective

judgement to complement such data as is available. It should be

noted that models may change over time and they should not be

relied upon to capture future uncertainty or events.

Aon Hewitt Limited is authorised and regulated by the

Financial Conduct Authority. Registered in England & Wales.

Registered No: 4396810.

Registered Office:

The Aon Centre

The Leadenhall Building

122 Leadenhall Street

London EC3V 4AN

Copyright © 2017 Aon plc

aon.com