apartment market

DESCRIPTION

market jenTRANSCRIPT

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 120

Summary of Analysis ofDevelopment of Certain Real

Estate Market Segments in 2012

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 220

Content1 Apartment market 3

Apartment market in riga 3

Apartments in standard-type houses in Riga housing estates 3

Apartments in the central part of Riga 4Te Old own 4

Apartment market in the vicinity of Riga 5Apartments in newly built houses 5

Summary of the apartment market 7

Single-family private houses 8

Single-family private houses in Riga 8

2 Private houses 8Single-family private houses in the vicinity of Riga 9

Land market 10

Land for private building in Riga 10

Land for private building in the vicinity of Riga 10

3 Lan 983089983088Land for commercial development (office buildings shopping centres apartment houses etc) 11

Land for agricultural needs 13Office space 15

Retail space 15

4 Market of non-residential properties 15Industrial and warehousing space 16

5 Real estate market in Latvian regions 17

6 Authors 19

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 3203Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

APARTMENTS IN STANDARD-TYPEHOUSES IN RIGA HOUSING ESTATES

During 2012 standard-type apartment prices in generalhave increased he prices increased by an average of 2he price increase was mainly observed in the first quarterof 2012 but in May of this year the prices reached theirhighest position ndash 595 EURmsup2 During the remaining threequarters of the year the prices have remained stable onlyminor fluctuat ions have taken place

It shows that the total activity in the apartment market in

2012 has increasedAfter the apartment price reduction throughout the

year which was observed in 2011 in the beginning of 2012there was a price rise he largest price increase in 2012was observed in March ndash by 07 In other months bothnegative and positive price movements were observed

At the end of 2012 the average value of one msup2 in thehousing estates of Riga was 595 EURmsup2

he highest growth of the average price of 1 sqm ofan apartment in the housing estates of Riga in 2012 wasobserved at Jugla ndash +5 he lowest price changes wereobserved at Zolitūde ndash +06 However the only negativeprice changes in 2012 were observed at Bolderāja wherethe prices fell by an average of 08

APARTMENT MARKET IN RIGA

In 2012 there have been certain changes in theapartment market of Riga however the changes have notbeen so significant as in previous years Price increase in therange of 2 ndash 8 has been observed in almost all apartmentsegments of Riga But in the vicinity of Riga the price levelhas remained unchanged in many locations and in someplaces the prices have even decreased

The following price changes have taken place in theapartment market of Riga in 2012

bull pthe prices of apartments located in the central part ofRiga have increased he prices have increased by 3 ndash 8on average in the central part of Riga he lowest priceincrease was discovered in the Old own and the peripheralpart of the city centre he highest price increase wasobserved in respect of apartments in renovated and newbuildings and apartments located in the Silent Centre andthe boulevard ring

bull practically no price change was observed in respect ofapartments located in wooden buildings An exception is theMaskavas suburb where the price of apartments located inwooden buildings has decreased by 5 on average

bull prices of standard-type apartments located in housingestates have increased by 2 on average he mostsignificant price change in 2012 was observed at Juglawhere the prices have increased by 5 Compared withJune 2007 when the highest price of one square metre ndash1620 EURmsup2 ndash was registered the prices were by 63lower at the end of 2012 If compared with the lowest priceever registered (September 2009 ndash 487 EURmsup2 on average)the prices are grown by 22

bull In the vicinity of Riga the apartment prices havedecreased in certain locations he price decrease has notbeen homogenous ndash it was 1 ndash 3 in 2012 he largest pricedrop was observed at Kauguri Jūrmala where the pricesdecreased by 35 on average during the year

In 2012 people more carefully selected apartmentproperties to be purchased hey took into account also suchfactors as house management and whether the undividedshare in the ground under the house where the apartment wassituated was in ownership

Thus a growing interest isseen for apartments in new orrenovated buildings not only fromthe part of foreigners who mostlyacquire property for obtaining aresidence permit

but also from the par t of local population which explains thelargest increase in prices of apartments in these buildings

1 A

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 4204Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

1 A

bull lack of quality housing in the central part of Riga Alongwith increasing customer requirements interest in theapartments with good location and good condition of thepremises has increased in 2012 Living in the centre of Rigahas several advantages ndash many significant objects are withina walking distance infrastructure development proximity ofsocially significant facilities prestige of residence and otherfactors

Changes of apartmentprices in the central part of Rigahave never been as apparent as inthe housing estates of RigaIn the central part there is a lot of apartments of variousquality levels with many factors influencing the valuesuch as location existence of utilities architecture of thebuilding traff ic intensity etc

After the significant price growth observed in the centralpart of Riga in 2011 the prices tended to stabilize already atthe end of 2011 he price growth observed in 2012 is to beassessed as low and the prices tend to stabilize

THE OLD TOWN

Price level of apartments in the Old own has slightly

increased in 2012 At the end of 2012 apartment prices inthe Old own started from 1500 EURmsup2 Most expensivetransactions recorded were associated with apartmentsin renovated and new buildings in 2012 and as in 2011 insome cases exceeded the amount of 4000 EURmsup2 hehighest amount of transaction per 1 msup2 was observed in thesummer of 2012 in Jēkaba Street where an apartment of17 msup2 in a non-renovated house was sold for 6400 EURmsup2he average transaction price of apartments in the Old ownin 2012 was 1400 ndash 3300 EURmsup2 he highest prices arefor apartments in an exclusive location in renovated or newbuildings with high quality finishing Supply price reached6500 EURmsup2 here are practically no simple apartmentsbeing offered for sale in the Old own the housing market

due to the demand focuses directly on the high-qualityapartments in good condition of the premises

he price increase concerned both medium-quality andhigh-quality apartments in the Old own and was 3 ndash 5in average he increase is explained by the exclusivity ofthe location factor and its key role in the purchase of anapartment

Buyers of homes in the Old Town may be divided in severalcategories

bull foreign nationals who purchase apartments with goodlocation to obtain a residence permit for business travelpurposes or to spend their vacations

bull Latvian residents whose primary residence is in anelite residential area and who purchase such apartments asreplacement housing for a long term

APARTMENTS IN THE CENTRAL PARTOF RIGA

In 2012 the housing market main trend was the sameas in 2011 ndash a stable and increased demand for high-qualityapartments with good location here is still lack of high-quality apartments located in the central part of Riga andbeing sold at a price corresponding to the market conditionsApartments are of ten either not complying with customerrequirements in terms of quality or the price is prohibitivelyhigh and inappropriate In the central part of Riga therewas observed a growth of prices just for good qualityapartments ndash apartments with quality interior decorationgood location in the centre of Riga good location in thebuilding as well as with all the necessary engineeringsystems In the Rigarsquos best locations such as the Old ownCentre and the Silent Centre the apartment prices increasedby 3 ndash 8 in 2012 he price increase is typical mainly forhigh-quality apartments in renovated and new buildingsIn general the prices increased by up to 5 in the centralpart of Riga he prices of apartments being offered arenot lower than 1100 EURmsup2 in the Silent Centre and from1500 EURmsup2 in the Old own he following factors havecaused the price growth and increase of market activity inthe centre of Riga

bull amendments to the immigration tax law adopted in2010 which created possibility to obtain residence permitin the case of purchase of properties in Riga and also inother places in Latvia herefore also in 2012 high-qualityand expensive apartments in the centre of Riga which costin excess of 100 000 LVL which is necessary for obtaining

a residence permit were still demanded Most attractiveapartments for obtaining residence permit were apartmentsin renovated or new buildings because such apartments areeasier to hire out at a later moment

bull investment in real estate is still a very popular and safeform of investment hus people prefer high quality andgood real estates ndash apartments in the central part of Rigathe value of which is less subject to market fluctuationsAcquisition of an apartment in the city centre will always bea less risky investment object

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 5205Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

1 A

APARTMENTS IN NEWLY BUILT HOUSES

In the first three quarters of 2010 there were built 1531apartments and compared to the first three quarters of2009 the decrease was 56 In the first three quarters of2011 there were built 1754 apartments and compared tothe first three quarters of 2010 the increase was 15 Butin the first three quarters of 2012 there were built 1560apartments and compared to the first three quarters of2011 there was a decrease of 11 his change is explainedby the fact that in 2011 new apartment building projectsgradually emerged in the market and many projects underconstruction were completed herefore it should be notedthat in 2012 the number of the commissioned apartmentbuilding projects was less than in the preceding year

Also in 2012 like in 2011 the supply of apar tments in newprojects consisted mainly of projects seized by banks within

which there are offered apartments not sold by developersof multi-apartment projects of largeconstruction companies such asMerks YIT NCC Hanner etc aswell as of individual apartments inprojects of recent years

However while in 2011 the banksand their subsidiaries still thoughtwhat to do with the new housingfacility portfolio hoping that aninterest in the purchase thereof couldbe shown by potential investors whowould purchase projects as a wholebut when these expectations werenot met in 2012 we see that theproportion of new projects seizedby banks has grown significantly inthe supply structure and that thoseprojects are being offered for sale inthe form of separate housing unitshe largest number of apartmentswithin new housing projects isoffered by Ektornet a subsidiary of

Swedbank who is offering severalcompetitive facilities both in terms of location and price Acustomer can choose from a variety of renovated differentsize apartments mostly in and around Riga Ektornet bycarrying out an intensive marketing campaign in 2012 hasbeen able to attract a wide range of stakeholders whichis demonstrated by the rapid growth in the number oftransactions

Also subsidiaries of other banks have taken a numberof measures to promote sale of the seized facilities andimprove the market recognisability here are created newbrands such as Reverta ( Parex banka ) Pillar ( Trasform ABLV ) Company websites are being developed andimproved more attention is paid to the customerservice both by involving larger real estate companies ascooperation partners in sale of properties and by creatinginternal sales teams

If the main competitive advantage of bank subsidiariesis the price and the varied offer then in terms of qualityand safety the biggest competitors are large developercompanies that have proved themselves in the market

bull buyers placing their free funds and considering suchapartments to be safe investment objects such apartmentsare usually hired out after purchase

APARTMENT MARKET IN THE VICINITYOF RIGA

Demand for apartments in the vicinity of Riga is mainlyformed by

bull People who work in Riga but for financial reasonsare looking for an opportunity to buy a cheaper apartmentoutside of Riga

bull Locals who are looking for a new residence forthemselves in well-known surroundings

bull People for whom it is a conscious choice to live outsidethe capital city and for whom the financial arguments arenot playing the main role

In contrast to the small priceincrease in the housing estates ofRiga the average price level hasdecreased outside of Riga

The pricedrop in the vicinity ofRiga was not evenhe largest price drop in 2012 wasregistered in Jūrmala Kauguri wherethe prices have decreased by 35(in 2011 ndash -88) But the lowestprice drop was registered in Ogre ndash13 (in 2011 ndash -43)

In Salaspils the prices havedecreased by 31 (in 2011 ndash -73)he price difference betweenSalaspils and Riga housing estates has increased again ndashup to 26 (in 2008 ndash10 in 2009 ndash 20 in 2010 ndash 16)But in Ogre at the end of 2012 the apartment prices werealready by 41 lower than in Riga (at the end of 2011 ndash by

39 at the end of 2010 ndash by 30) he price difference hasgrown also in Jūrmala Kauguri where at the end of 2010the prices were by 25 lower but at the end of 2011 theprices were already by 38 lower than in Riga housingestates At the end of 2012 the apartment prices in Kauguriwere already by 44 lower than in Riga housing estateshus the gap between the prices has increased possibly upto a maximum and this trend should not continue in 2013

Price level of an apartment in satisfactory technicalcondition in a standard-type house in the vicinity of Rigaat the end of 2012 ranged from 360 to 560 EURmsup2depending on the location availability of infrastructure aswell as the distance to Riga A higher apartment price levelis in some locations in the vicinity of Riga such as ĀdažiBaloži Carnikava and also Ķekava where the standard-typeapartment prices are ranging from 500 EURmsup2

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 6206Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

1 A

If in the new housing projects located in the city centrethe customers purchased the apartments paying moreattention to the location of the building and the amenities

provided and were willing to sacrifice quite a large amountdespite the fact that decoration and interior fitting-outworks were not completed and had to be carried out inthe economy class segment the target audience had clearlystrengthened their demand to have a completely finishedapartment his was evidenced by a rapid increase in thenumber of transactions with completed new projects andvery little interest in the facili ties where the internal finishingwork had to be carried out by the owners themselvesdespite the fact that such facilities were offered at a lowerprice herefore those bank subsidiaries who renovatedcompleted improved the seized projects and offered forsale finished apartments with full interior decorat ions are tobe considered progressive and forward-looking

All of the above factorsdetermine the price level in thesegment of new projectsIn the new projects offered by banks the price per squaremetre of apartment in Riga housing estates ranges from900 to 1300 EUR depending on location finishing quality

level and other factors In the Riga district the competitiveprice ranges from 700 to 1000 per square metre hebanksrsquo housing portfolio contains also new projects in theRiga city centre Jūrmala and other demanded places with ahigher price level but they were not of fered for sale in 2012Most likely an increase of prices for this price category isexpected in the nearby future when the sale could be moresuccessful

A new apartment building construction costs in 2012had risen to an average of 800 ndash 1000 EURmsup2 In order toensure the profitability of the construction in the case whenfully finished and completed apartments are offered in thehousing market developers must sell the apartments ata price not less than 1100 ndash 1300 EURmsup2 of living spaceConsequently the major developers such as YIT and Merksoffered newly built apartments in the housing estates atthe price of 1300 ndash 1900 per msup2 he price range for 1 sqm

In particular we can highlight such companies as YI andMerks which in spite of the fact that their price level ishigher than the prices offered by banks for equivalentfacilities have achieved very good results both in terms offacilities offered and the number of transactions

High demand for new dwellings in the central part of Rigawas a characteristic feature of this year

Foreigners are themain target audience for suchfacilities they purchase propertiesfor obtaining a residence permit

in LatviaOne of the most demanded projects in the reporting year

was the project at Antonijas Street 16a where most of the60 apartments offered have been sold Also apartments atMartas Street 7 were highly demanded several transactionshave been concluded also in respect of the project PetitParis in Melngalvja Street in spite of the high price level in allthese projects

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 7207Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

1 A

of apartment located in a new project situated in the citycentre was from 1800 to 3000 EUR in 2012

In cases where apartments located in newly built houses

are sold in the secondary market their prices are oftenhigher because the buildings are fully populated and thedemand for such housing is relatively high

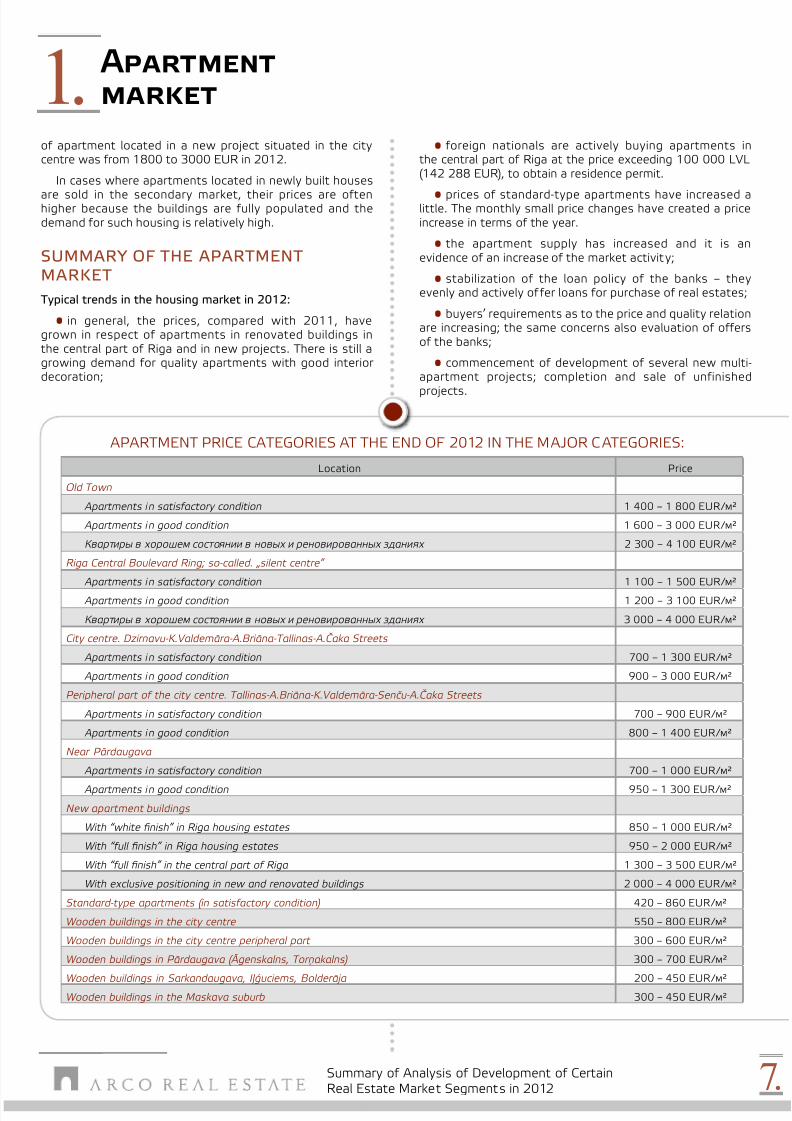

SUMMARY OF THE APARTMENTMARKET

Typical trends in the housing market in 2012

bull in general the prices compared with 2011 havegrown in respect of apartments in renovated buildings inthe central part of Riga and in new projects here is still agrowing demand for quality apartments with good interiordecoration

APARMEN PRICE CAEGORIES A HE END OF 2012 IN HE MAJOR CAEGORIES

Location Price

Old Town

Apartments in satisfactory condition 1 400 ndash 1 800 EURмsup2

Apartments in good condition 1 600 ndash 3 000 EURмsup2

Квартиры в хорошем состоянии в новых и реновированных зданиях 2 300 ndash 4 100 EURмsup2

Riga Central Boulevard Ring so-called bdquosilent centrerdquo

Apartments in satisfactory condition 1 100 ndash 1 500 EURмsup2

Apartments in good condition 1 200 ndash 3 100 EURмsup2

Квартиры в хорошем состоянии в новых и реновированных зданиях 3 000 ndash 4 000 EURмsup2

City centre Dzirnavu-KValdemāra-ABriāna-Tallinas-AČaka Streets

Apartments in satisfactory condition 700 ndash 1 300 EURмsup2

Apartments in good condition 900 ndash 3 000 EURмsup2

Peripheral part of the city centre Tallinas-ABriāna-KValdemāra-Senču-AČaka Streets

Apartments in satisfactory condition 700 ndash 900 EURмsup2

Apartments in good condition 800 ndash 1 400 EURмsup2

Near Pārdaugava

Apartments in satisfactory condition 700 ndash 1 000 EURмsup2

Apartments in good condition 950 ndash 1 300 EURмsup2

New apartment buildings

With ldquowhite finishrdquo in Riga housing estates 850 ndash 1 000 EURмsup2

With ldquofull finishrdquo in Riga housing estates 950 ndash 2 000 EURмsup2

With ldquofull finishrdquo in the central part of Riga 1 300 ndash 3 500 EURмsup2

With exclusive positioning in new and renovated buildings 2 000 ndash 4 000 EURмsup2

Standard-type apartments (in satisfactory condition) 420 ndash 860 EURмsup2

Wooden buildings in the city centre 550 ndash 800 EURмsup2

Wooden buildings in the city centre peripheral part 300 ndash 600 EURмsup2

Wooden buildings in Pārdaugava (Āgenskalns Torņakalns) 300 ndash 700 EURмsup2

Wooden buildings in Sarkandaugava Iļģuciems Bolderāja 200 ndash 450 EURмsup2Wooden buildings in the Maskava suburb 300 ndash 450 EURмsup2

bull foreign nationals are actively buying apartments inthe central par t of Riga at the price exceeding 100 000 LVL(142 288 EUR) to obtain a residence permit

bull prices of standard-type apartments have increased alittle he monthly small price changes have created a priceincrease in terms of the year

bull the apartment supply has increased and it is anevidence of an increase of the market activity

bull stabilization of the loan policy of the banks ndash theyevenly and actively offer loans for purchase of real estates

bull buyersrsquo requirements as to the price and quality relationare increasing the same concerns also evaluation of offersof the banks

bull commencement of development of several new multi-apartment projects completion and sale of unfinished

projects

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 8208Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

bull there is still lack of sufficient funding support fromcredit institutions in the private house segment whichwould allow construction of new contemporary privatehouses with optimum space and low running costs Banksare still very cautions when granting loans for purchase ofprivate houses and liquidity risks are carefully evaluatedFurther development of the market will largely depend onthe loan policy of the banks

Development ofnew residential villages andconstruction of new homes forsale in 2012 was very inactiveNew private houses were mostly being built for own needswith adequate living space quality of finish and engineeringsystems

At the end of 2012 the costs of new private costs wereincreased Data of the Central Statistical Bureau showedthat in October 2012 the total construction costs hadincreased by 59 compared with October 2011 he mostsignificant increase concerned wages and salaries (+163)as well as mechanism maintenance and operational costs(+113) Prices of building materials during this perioddecreased by 1

SINGLE-FAMILY PRIVATE HOUSES INRIGA

he prices in the private house segment in Riga slightlydecreased in 2012 he prices decreased by 3 ndash 5

aking into consideration the fact that the constructionof new buildings in Riga is geographically limited andconstruction volumes in 2012 were still small the limitedsupply of new private houses allows sellers to keep prices ata suff iciently high level here are a limited number of people

SINGLE-FAMILY PRIVATE HOUSES

In 2012 the private house segment was not one of themost active segments in the real estate market hereare bought and sold primarily qualitative properties atreasonable and normal market prices At the end of 2012the greatest demand was for new private houses withoptimum space area (150 ndash 200 square meters) as well aswith land area ranging from 1000 msup2

The most important features of the private house marketsegment in 2012

bull in 2012 the average prices of private houses slightlydecreased both in Riga and its closest vicinity In Rigathe price drop was 3 ndash 5 but in the vicinity of Riga theprices decreased by 3 on average aking into account theinsignificant price changes the private house market shouldbe considered as stable

bull demand is mainly for houses erected in the last twodecades with fully completed interior decoration ready tomove in as well as with at least satisfactory infrastructureavailable hus the highest demand for private homesremained near Riga in district centres or near them withthe optimum building and land area In this segment of themarket the supply is minimal and mostly it does not meetthe peoplersquos ability to pay At the same time the prices forsuch private houses have increased as opposed to the totalprivate house segment he greatest interest remains in theprivate houses within the price range of up to 200 000 EURPrivate house above euro 200 000 must be located in Riga orhave an excellent location or close to the water to be of

minimum interestbull minimum interest is in private houses with area of

above 200 msup2 unfinished with limited engineering systemsand restricted access

bull lack of good quality supply Market supply consistsmainly of houses with large non-useful space as well ashouses erected in the period from 2005 to 2007 of lowquality hese are houses that are mostly traded below costwhile interest in them is low

2P

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 9209Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

2P

The demand in the

vicinity of Riga is for small andmedium-sized private houses withan area of 200 msup2 and the landarea of up to 2000 msup2he average sales price of such a private house (withcomplete interior decoration) is from 100000 to 200000EUR depending on the location engineering systemspublic transport access building materials used and interiordecoration Buyers who need bank financing actively showinterest in private homes that now are owned by subsidiariesof banks as more favourable loan conditions are offered inrespect of such properties At the end of 2012 the offerprice in certain cases exceeded 300 000 EUR however suchhigh prices are not considered appropriate for the currentmarket and actually no transactions are closed at suchprices he exception is exclusive buildings with high qualityinterior decoration or a good location c lose to water bodies

he average price level in the most important privatehouse categories in the vicinity of Riga (except SaulkrastiJūrmala Sigulda) at the end of 2012

bull summer houses and garden houses in gardeningsocieties ndash 15 000ndash40 000 EUR

bull residential houses in gardening societies ndash 30 000ndash

110 000 EURbull private houses built in preceding years in the vicinity of

Riga (outside gardening societies) ndash 40 000ndash120 000 EUR(lowest price level concerns private houses with partialamenities in bad technical condition)

bull new private houses outside villages ndash 80 000ndash200 000 EUR

bull private houses in new and well-developed villages ndash100 000ndash250 000 EUR

who could buy this type of housing as the price level isrelatively high At the same time the prices of private homesbuilt in the last century in Riga decreased in 2012 hisapplies primarily to non-renovated houses with a large areaas well as high operating costs he price reduction is dueto the increase of the real estate tax and other operatingexpenditures so that maintenance and operation of suchhouses is becoming more and more expensive

he highest prices of private houses located in Riga areobserved in such areas as Mežaparks (up to 2 000 000 EUR)Vecāķi (up to 540 000) and eika (up to 450 000 EUR) Butthe relatively cheapest private house areas are DārzciemsPļavnieki Purvciems as well as Jugla Zolitūde andZiepniekkalns he lowest prices of private houses are inDārziņi as well as in Suži and Jaunciems

SINGLE-FAMILY PRIVATE HOUSES INTHE VICINITY OF RIGA

he prices remained stable in the market of privatehouses of the vicinity of Riga in 2012 In the municipalitiesoutside the municipality centres there is still quite a largeprice stagnation and negative price fluctuations in someplaces he prices have slightly decreased also for goodquality private houses with area of up to 200 msup2 located inthe municipality centres So the private house prices in thevicinity of Riga have decreased in general by 3 on average

he supply of private houses in the vicinity of Riga stillis relatively large he largest supply of private houses inthe Riga district is in Ķekava Mārupe Carnikava and Babītemunicipalities he number of houses offered is in the rangefrom 170 to 270 in each municipality

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 102010Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

and most probably given the small land area which is typicalfor Dārziņi have reached the lower limit value

LAND FOR PRIVATE BUILDING IN THE VICINITY OF RIGA

In 2012 in the vicinity of Riga the demand for land forprivate building was still low ndash transactions were relativelyinfrequent mainly with high quality land with good accessopportunities and available utilities hanks to this marketof high-quality land plots the average price of 1 msup2 landin 2012 slightly increased by an average of 4 Howeverdue to the fall in prices in 2011 (-7) the prices of land forprivate building continue to be at the level of the end of2010beginning of 2011 In general reluctance of banksas to granting loans for land purchase and constructionof new buildings as well as the large supply of land forprivate building kept the price level low enough o a largeextent in this market situation the most important factoris how beneficial the real estate price is It is practicallyimpossible to sell land that is not completely developedand that is parcelled and that is not completely connectedto engineering systems Similarly any interest in well-developed land located in the new residential villages builtin the preceding years far from the city or municipalitycentres has not practically been observed

Among the areas located in the vicinity of Riga andresearched by ARCO REAL ESTATE the highest prices atthe end of 2012 remained to exist in the neighbourhoodof the Little and the Big Baltezers Lake in Mārupe Babīteand Garkalne municipalities he lowest prices of land plots

intended for private building existed in Olaine municipality inSalaspils and its neighbourhood

LAND MARKET

According to the State Land Service data transactionswith land plots are being closed but the number oftransactions compared to previous years is still assessedas low In 2012 for the third consecutive year this segmentof the market has stagnated Most notably the stagnationwas observed in residential land market ransactions in2012 were closed only in respect of high-quality buildingsites with good access possibilities and connected to orwith availability of all the required utilities Often such landplots are purchased without bank financing Also in theagricultural and forestry land market transactions are closedmostly in respect of high-value assets

Low demand and lackof activity is largely due to therestrictions imposed by creditinstitutions as to granting loansfor land propertiesbecause such properties have high liquidity risk hesolvency rate of population has improved slightly but thereis lack of direct bank financing support without which landacquisition is not available for most of the potential buyersBecause of minimal interest and demand land prices are

very uneven Prices of 1 msup2 of adjacent parcels can vary byas much as several times both in the of fer and in registeredtransactions

LAND FOR PRIVATE BUILDING IN RIGA

Prices of land plots intended for private building in Rigagrew only slightly in 2010 ndash by 5 but in 2011 practicallyno changes were observed and the average price of 1 msup2of land increased slightly ndash within the range of 2 In 2012the prices of land plots intended for private building in Rigaslightly decreased hey dropped an average of 2 so it canbe assumed that since the beginning of 2011 the privatebuilding land prices in Riga have not changed he slight

price decrease was caused by lack of interest and demandIn Riga there is a relatively low number of offers causedby shortage of free land in addition the land that can bepurchased in Riga is mainly intended for multi-apartmentor commercial buildings rather than construction of privatehouses

he highest prices have still remained in Mežaparks andVecāķi In Vecāķi there are still offered land plots of up to150 EURmsup2 and in Mežaparks ndash of up to 400 EURmsup2 forland in an exclusive location hese high prices have beencaused by the lack of alternatives to such places in Rigaas well as the fact that there are not so many free landplots and the number of such plots is still decreasing Butthe lowest prices in Riga at the end of 2012 were observedin Dārziņi where the price of land plots for private building(550 ndash 1000msup2) practically has not changed in the last twoyears he prices have remained at the level of 20 ndash 30 euro msup2

3L

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 112011Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

3L

commercial land in Riga in general has slightly increased ndash by anaverage of 5 to 7 At the same time in the suburbs of Rigain areas with low demand in the current market situation forlarge land areas with significant burdens and lack of utilitiesthe level of prices tends to decrease

Apartment building developers stillare interested in relatively smallparcels of land with building areaof up to 5000 square metreswith good location and availableinfrastructure

Although the volume of construction has grown for thesecond consecutive year ndash in Q3 2012 relative to the sameperiod of the previous year the construction growth was83 (in the 3rd quarter of 2011 the growth was 196relative to the previous yearrsquos corresponding period) it has notcontributed to growth of activity in the land segment Whilein the first three quarters of 2012 the volume of residentialbuildings constructed has increased by 142 compared tothe same period in 2011 it has been mostly on the accountof completion and putting into operation of buildings partiallybuilt in the pre-crisis period

here still exist supply of land plots with developedand approved apartment house projects but usually thissupply consists of projects developed in the preceding yearsthat do not correspond to the current market and demandrequirements

here is practically no demand for larger plots of land thatcan be parcelled creating residential building villages Marketvalue of created parcels in the current market situation doesnot cover the total cost of the development which includesconstruction of access roads and laying of engineeringsystems Semi-developed land is still available for purchaseat well below the prime cost of investment in developmentSupply of land plots intended for private building in thevicinity of Riga far exceeds the demand hus these largerland plots which were previously mainly divided into smallerplots are currently either divided into 1 ndash 3 larger buildingplots or if possible change the zoning to other type of use

Taking into account the minimum demand the price of landplots with area from 1 to 10 ha located in the vicinity ofRiga is as follows

bull with developed parcellation project engineeringsystem projects close to existing buildings and location ofconnection to utilities adjacent to existing projects Pricesin this category at the end of 2012 15 ndash 8 EURmsup2

bull land plots with possible parcellation with poorlydeveloped infrastructure and unmanaged environment withpossibility to connect to engineering systems Prices in thiscategory at the end of 2012 1 ndash 5 EURmsup2

bull land plots intended for parcellation withoutengineering systems and access roads ndash 01 ndash 15 EURmsup2

LAND FOR COMMERCIAL DEVELOPMENT(OFFICE BUILDINGS SHOPPING

CENTRES APARTMENT HOUSES ETC)Land for commercial use was one of the most stagnatingmarket segments in 2012 ransactions are still very rareand demand is low Demand has grown only for land in thecentral part of Riga with an excellent location therefore theprice level in 2012 of such land plots has increased more thanin the preceding years Consequently the average price for

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 122012Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

3L

In Salaspils the price of commercial development landranged from 2 to 15 EURmsup2 but in Ādaži the price ofcommercial development land ranged from 3 to 20 EURmsup2On average the price of commercial development land in theRiga district ranged from 15 to 25 EURmsup2

For production needs the customers prefer to purchaseland with utilities or in close proximity to utilities One of themost significant factors is the possibility to make connectionto the utilities and the possible capacity of the utilities in theparticular location Another significant factor is condition ofaccess roads as well as whether the location is strategicallyadvantageous and has good access possibilities he mostdemanded land area for this purpose is 1 ndash 3 ha Customersare interested mainly in land located in Ķekava OlaineMārupe Ādaži and other areas in the vicinity of Riga

In 2012 unlike the previous three years themanufacturing business activity increased and thereforean increased interest in land plots suitable for building ofindustrial facilities was observed hus in 2012 shouldbe viewed as a turning point as to increase of interestand demand he demand is based on non-complianceof industrial space available on the market with therequirements which are often specif ic as well as the limitedsupply and low quality of industrial space ndash lack of adequatecapacity of the utilities bad interior decoration andopportunities of utilization It is expected that continueddemand for industrial space will result in an increaseddemand for land with utilities One of the most importantconditions for purchase of such land plots is availability ofelectrical power as well as capacity expansion options Noless important is the time period for possible increase ofpower capacity it should not exceed 6 months

In the territory of Riga City the lowest prices are aroundMaskavas Street and in Rumbula ndash starting from 20 EURmsup2But around Riga there are available land plots with areaof up to 10 000 msup2 with available utilities at the price of8 EURmsup2 Supply price of the land in many cases exceedsthe demand price At the same time in 2012 there wereregistered several transactions with industrial developmentland at the price of 5 ndash 8 EURmsup2

The main condition for a commercially advantageous landplot is its location

bull faccedilade of the building overlooking main streets and

their intersectionsbull nearby intensive traffic and large pedestr ian flows

bull next to newly built business centres

bull locations with easy access

bull good visibility places

bull locations with important public facilities and similartype buildings

Most suitable and

popular areas for commercialdevelopment are areas of KrastaMaskavas KUlmaņa gatveSkanstes Mūkusalas Krustpilsand Granīta Streets

he prices of land plots suitable for multi-storey buildingsin Riga housing estates ranged from 30 to 130 EURmsup2except eika where land plot prices achieved 150 EURmsup2But in the central part of Riga this price is from 100 to

1200 EURmsup2In the vicinity of Riga the prices of land suitable for

commercial development remained in 2012 at the previouslevel without any significant changes he highest pricesof land for commercial development still were observed inMārupe he supply contains land plots with larger areas(1 ndash 5 ha) at the price of 3 ndash 25 EURmsup2 and the price maybe even up to 45 EURmsup2 However no transactions havebeen closed at these prices ransactions usually are closedwithin the range of 2 ndash 10 EURmsup2 sale prices of land plotswith area below 1 ha are up to 25 EURmsup2 In the area of theAirport bdquoRigardquo the price level of land offered has remained tobe high ndash 15 ndash 90 EURmsup2

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 132013Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

3L

In 2012 farmland prices

tended to remain at the currentlevel or even to grow in certainlocations

Agricultural land prices are rising because of severalfactors First of all the supply contains a few goodcultivated and fertile land plots because in the courseof the years that have passed since the moment whenthe agricultural land came under private ownership (in theearly years of independence of Latvia) there have becomeapparent persons who want to farm and who have keptthe land in their ownership and developed agriculture aswell as those who wanted to sell such land and who havealready done it For the second ndash if such land appears on themarket the competition between farmers and the desire tobuy is so fierce that between the seller and the buyer thereis held an informal auction For the third farmersrsquo interestin agricultural land adjacent to the land already owned orthe land that has been leased and maintained by him is sogreat that if the owner of the land is ready to sell the payeris willing to pay a high price For the fourth in the resultof agricultural modernization more and more farms areincreasingly expanding their farm area otherwise farmingbecomes uneconomic For the fifth land acquisition alsoprovides additional income from public assistance programsgrants single area payments excise-free fuel

Land prices for manufacturing and warehousing needs inRiga and its surroundings

bull land for manufacturing needs in Riga ndash 20 ndash 60 EURmsup2

here are also cheaper land plots starting from 10 EURmsup2 ndash thisprice level is typical only for land plots with large area problemsof usage bad configuration difficulties with connection tothe utilities and located in Riga suburbs ndash Šķirotava Bolderājaetc he highest prices of up to 60 EURmsup2 were observed forland plots located in the area of Maskavas Ganību dambis andKatlakalna Streets

bull land for manufacturing needs around Riga ndash 1 ndash 15 EURmsup2depending on access possibilities availability of utilities distanceto Riga and other factors

LAND FOR AGRICULTURAL NEEDS

hroughout the territory of Latvia this is still one of themost active segments of the market High demand fromthe part of foreign citizens is still remaining as well as theoverall demand for agricultural land has remained at a highlevel Supply of land with a sufficiently large area (from50 ha) at a price that corresponds to the current marketsituation is very low Investors are mostly interested inland plots of at least 100 hectares If they are divided theyshould be located close to one another Demand price foragricultural land from 50 ha and more ranges from 430 to2000 euroha while average selling prices are from 800 to3500 euroha ranging mainly depending on size locationfertility and moisture levels Agricultural land prices mayexceed the average price when they are placed next to largefarm estates In this case there can also be a small area ofland which the owner can sell to the large farms at a veryadvantageous price

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 142014Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

3L

Another reason for

the price increase that should bementioned is the state supportto agricultural land acquisitionand loans taken for this purposethat was adopted in the springof 2012 Tus this factor hasstimulated the demand increase

A large part of land plots owned by foreign nationalsare managed by local farmers renting the land or evencultivating the land without paying compensation to theowner he owners are interested in maintenance of the landand compliance thereof with the agricultural land status

here is also a large demand for rental of agricultural landLease transactions in Latvia are closed mainly at the rentlevel of 60 ndash 85 euroha per year On the Zemgale flatland therent amounts to 140 EURha However rental of agriculturalland in Latvia is still considered risky because the leasecontract periods are too short and the risk of losing thewell-developed land by the lessee is assessed as high

It is expected that in 2013 the real estate tax (RE) forthe agricultural land will increase due to the increase of thecadastral value In Latvian regions the difference betweenagricultural land cadastral value and market value is stillhighndash about 35 on average

Key factors in the acquisition of agricultural land as well asthe main driving factors of price are as follows

bull agricultural land fertility and drainage

bull land area in one land plot

bull access possibilities

bull overall economical development level of the district andthe district centre

bull distance to Riga or district centre as well as accessibilityof Riga or district centre

bull size of continuous land plot

he highest prices of agricultural land in 2012 wereobserved in Zemgale and Kurzeme regions wheretransaction amounts reached 3 700 EURha and in certaincases the prices were even higher the lowest prices were

observed in Latgale ndash even as low as 430 EURha

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 152015Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

Decrease of vacant

office areas is observed in thehigh-demand office segments inthe Class A and Class B officebuildingsAt the same time minimal demand still exists for largeand morally outdated office areas Unless a possibility ofrenovation of such premises is found improving energyefficiency and dividing such premises in smaller lease unitsit is difficult to expect growth in demand for such premisesin the coming years

RETAIL SPACE

In 2012 as the economy improved and the purchasingpower slightly increased positive trends were observed alsoin the retail space market Along with the growth of costof living and average wage both the retail turnover and thelevel of consumer prices has increased According to theinformation of the CSB ( Central Statistical Bureau ) startingfrom September 2010 the consumer prices began to growin comparison with the relevant period of the precedingyear Also in 2012 the consumer prices compared with theprevious year has only increased

Retail trade turnover is one of the most importantcharacteristics that affect retail space sphere affectingboth the demand for commercial space and the market rentlevels According to the Central Statistical Bureau ( CSB ) inthe first three quarters of 2012 the turnover indicators ofthe Latvian retail companies have exceeded the indicators ofthe relevant period of the previous year

In 2012 due to general improvement in the consumersentiment as well as the increasing number of foreigntourists the number of vacant retail premises hasdecreased he highest demand for retail space is in the Oldown Audēju Kaļķu Vaļņu Skārņu and Šķūņu Street and inthe so-called ldquoNear Centrerdquo ndashsections of ērbatas BaronaElizabetes Dzirnavu Blaumaņa Antonijas Streets with themost intense traff ic he number of vacant retail premises inthe Old own number has decreased to 3 ndash 4 while in thecentral part of Rig it has decreased to approximately 6 ndash 8

Often the interior decoration condition of retail premisesdoes not meet the tenantsrsquo needs Necessary improvementof the interior decoration which not infrequently requiresinvolvement of designer services requires a sizeableinvestment of funds frequently up to 150 EURmsup2 Insuch cases tenants are often willing to enter into a leaseagreement for a period of up to 5 years to compensatethe investments In particular when it is important for arestaurant and bar owner to find a suitable place and thespace condition does not play an important rope For a retail

space with good location and of adequate configurationtenants are often willing to pay a rent which is by 20 ndash 30higher than the average rent his is typical for street

OFFICE SPACE

Improvement of competitiveness of the Latvian economyand increase of economic sentiment index in 2012 isreflected in the office space rental market Area of vacantspace in 2012 continued to decrease and rents are graduallyincreasing Change of rent level in different office spacesegments is very different While the rent for high-qualityoffice space with an area of 250 msup2 increased by 25 thenin turn the rent for medium or large office area with an areaof over 250 square metres rents have increased only byslightly more than 5 In 2012 just due to insufficiency oflarge multinational companies as tenants the lease off icespace owners had still to be cautious As a result new officebuildings are practically not built with a few exceptions ndashthe ldquo Jupiter Centrerdquo office building in Skanstes Street wasconstructed in 2012 and the construction works are stillcontinuing in the high-rise multi-functional building Z-Towers in Pārdaugava and in the new SRS centre in ČiekurkalnsStability of the office space market exists only in the Rigacity centre in the small office space market as well as innew office centres with good car parking possibilitiesOne of the key indicators of a successful office lease areais where the office building is capable of providing one carparking space per 50 msup2 lease area At the same time inthe central part of Riga only few office buildings are ableto provide one car parking space per 200 square metersPartially this inconvenience is compensated by the proximityof public transport and the city institutions to the leasedspace

4M -

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 162016Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

4M -

Due to the continued development of manufacturingcompanies most prospective as to renovation are heated orinsulated premises with a ceiling height of 6 ndash 10 m and thepossibility of installing a hoist

he most demanded locations of industrial premisesare in the proximity of the Riga ring road which providesfor more convenient and faster logistics than for examplein the proximity of the city centre he most demandedindustrial premises are those located around KrustpilsGranīta Katlakalna and Bauskas Streets

Industrial space rents have gone up in 2012 by up to 15in the most demanded industrial space segment ndash high-quality space in new buildings At the same time the rentincrease for large areas of over 3000 square metres orpremises in poor technical condition has not pract ically beenobserved

Vacant areas of industrial space for rent do not exceed15 of the total area and in the most demanded industrialspace buildings the vacant areas do not exceed 5 of thetotal area

Availability of a vacant space close to the facility is animportant factor for potential buyers of premises since mostcompanies who are willing to invest in space acquisition areplanning a space increase by at least 50 in the next 3 ndash 5years

It is expected that also in the coming 2 ndash 3 years a largepart of the supply in the industrial space sale market willbe made by premises of companies having had financialdifficulties during the preceding years and being sold in an

auction or by subsidiaries of banks Purchase of such a spaceis limited because in connection with speculative spaceacquisition transactions banks are not willingly grantingloans for purchase of such premises Premises that aretoo large for the market capacity or that are of insufficientquality or that are situated in a not advantageous locationare often being sold below their forced sale value whichusually corresponds to 60 ndash 70 of the market value of theproperty

sections in the Old own with the most intensive touristflow he greatest demand in 2012 was from the partof owners of the ldquomono-brandrdquo international brands andrestaurants he most active search time for rental spaceis spring and early summer when the cost burden caused bythe heating season is over

An increase of the retailspace rent in 2012 was observedin all street sections with themost intensive pedestrian flow inRigaWhile in street sections with low pedestrian flow wheretypical tenants therefore are tenants of low solvency therewas in many cases observed a rent decline by 5 ndash 10 onaverage in comparison with 2011

INDUSTRIAL AND WAREHOUSING SPACE

Compared with 2011 when industrial space rental marketwas unstable and when it was characterized by a relativelylarge percentage of vacant space in 2012 the situationhas changed he demand for new high-quality facilitieshas significantly increased Demand growth is based onthe growth of the export business capacities or transfer of

manufacturing closer to Riga he changes in the marketsituation have resulted in a lack of newly built industrialpremises both for rent and for sale

One of the most important aspects faced byentrepreneurs in search of manufacturing space is the lackof electrical power An increase of the required capacityusually requires not only additional investments but alsoconsiderable time resources

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 172017Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

he number of transactions has increased in theapartment segment but the prices have fallen in manyplaces Lot of apartments with a forced sale value havebeen launched in the market and those apartments aresold through auctions by ZTI and bank-related companieshe intense competition among sellers results in reductionof the offer price thus undermining the overall price level inthe housing market he apartment rental market becamemuch more active in 2012 his trend is linked to the locallabour force moving from disadvantaged rural communitiesto cities or parishes where there is availability of work

Office and retail space rental market segment in 2012

in the Latvian regions did not show any signs of activity ndashno significant change has occurred Many retail servicefacilities came into possession of insolvency administratorsbailiffs or bank subsidiaries which regularly put on salesuch properties At the same time there are relatively fewvacant premises for adequate rent in commercial buildingsand houses with space for rent Higher rents are for space inshopping centres with high pedestrian traffic as well as inproperties with very advantageous location Slightly lower

In general there are two stable and growing ndash in termsof the price ndash market segments in the Latvian regions ndashagricultural land and single-family residential houses

he increase in the agricultural land has been caused byvarious factors but the key factor has been the low supplyof fertile land of relevant size

The second segmentwhich experienced growth thisyear was the segment of singlefamily houses and country estates

with the directly attributable landplot of up to 10 hectareshe number of transactions has been a relatively high

however in most cases with properties that are were inpoor or satisfactory condition When buying such a propertythe buyer acquires ownership rights at a relatively low priceand the property is likely to have been bought by usingthe buyerrsquos own funds thus saving on account of bankingpayments ndash credit interest commissions But renovationand improvement of the home the buyer mostly carries outby his own resources investing his available funds in longterm or through a consumer loan

At the same time in the market segment of vacant landplots for private building and commercial development thecustomer activ ity was very low in 2012 although the priceswere low Credit institutions are rarely f inancing purchase ofland plots intended for building Due to relatively low landprices the owners whose ownership of the building andthe land beneath it was shared became more active hesetransactions were conducted in order to arrange singleownership

5R

L

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 182018Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

5R

L

The overall real estate market trends in Latvian regions in2012

bull most stable real estate market segments with price

grow ndash agricultural land and single-family housesbull number of transactions with apartments has increased

but prices are dropped in many places

bull the segment of land intended for building and thesegment of non-residential space are still without any signsof activity

bull the highest market activity was observed in Q2 and Q3

bull in underdeveloped municipalities and parishes the mainreal estate market object was agricultural and forestry land

rents are for space in second and third floors of commercialproperties Rent for of fice (administrative) space in industrialbuildings usually does not differ from the industrial spacerent and usually in the lease contracts there is set auniform rent amount for the whole space area Marketexpertsrsquo opinion about the industrial space market segmentrecovery and constantly growing demand is attributable toRiga and Riga region but not to the Latvian regions hecurrent demand for warehouse manufacturing facilitiesin the regions is specific Also Soviet-time specializedfacilities and industrial complexes appear in the market butthey sometimes do not meet the contemporary customerdemands

Due to the shortage of

industrial and warehouse spacewhile investors currently are not interested in thedevelopment of new industrial parks due to relatively lowrents customers are evaluating their possibilities to buildrelevant industrial facilities which meet their needs

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 192019Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

6 A

Agita eile Real estate valuation | JelgavaPhone +371 2939 4315

E-mail agitateilearcoreallv

Ilze ApeineCertified valuator | CēsisPhone +371 2837 7166E-mail ilzeapeinearcoreallv

Guna KlimonaReal estate valuation | GulbenePhone +371 2645 7883E-mail gunaklimonaarcoreallv

Andris LakušsReal estate valuation | DaugavpilsPhone +371 2837 9051E-mail andrislakussarcoreallv

Kristiāna KārkliņaMarketing project managerPhone +371 2926 6379E-mail kristianakarklinaarcoreallv

Māris LaukalējsMember of the Board Head of valuation department Nr 1

Phone +371 2923 0073E-mail marislaukalejsarcoreallv

Ieva JansoneMember of the Board Head of residential departmentPhone +371 2911 4811E-mail ievajansonearcoreallv

Guntis KanenbergsHead of commercial departmentPhone +371 2863 2211E-mail guntiskanenbergsarcoreallv

Līva JaunozolaHead of rent departmentPhone +371 2642 4119E-mail livajaunozolaarcoreallv

Jānis DzedulisReal estate valuation | Riga

Phone +371 2835 5271E-mail janisdzedulisarcoreallv

Oļesja BogodistajaHead of International DepartmentPhone +371 2868 8666E-mail olesjabogodistajaarcoreallv

Jana SemerikovaSaulkrasti Branch managerPhone +371 2836 6397

E-mail janasemerikovaarcoreallv

Ineta Zīberga Consultant | Saulkrasti BranchPhone +371 2860 0918E-mail inetazibergaarcoreallv

Kaspars RogaConsultant | Saulkrasti BranchPhone +371 2616 7468E-mail kasparsrogaarcoreallv

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 2020

ARCO REAL ESTATE

Brivibas street 39 Riga LV-1010

Phone +371 6736 5555Fax +371 6728 4423

E-mail rigaarcoreallv

httpwwwarcoreallv

httpwwwdraugiemlvarcoreal

httptwittercomArcoRealEstate

httpwwwfacebookcomARCOREALESAE

copy ARCO REAL ESTATE 2013

Quoting or republishing

appropriate coordination with

Ltd ldquoARCO REAL REAL ESAErdquo mandatory

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 220

Content1 Apartment market 3

Apartment market in riga 3

Apartments in standard-type houses in Riga housing estates 3

Apartments in the central part of Riga 4Te Old own 4

Apartment market in the vicinity of Riga 5Apartments in newly built houses 5

Summary of the apartment market 7

Single-family private houses 8

Single-family private houses in Riga 8

2 Private houses 8Single-family private houses in the vicinity of Riga 9

Land market 10

Land for private building in Riga 10

Land for private building in the vicinity of Riga 10

3 Lan 983089983088Land for commercial development (office buildings shopping centres apartment houses etc) 11

Land for agricultural needs 13Office space 15

Retail space 15

4 Market of non-residential properties 15Industrial and warehousing space 16

5 Real estate market in Latvian regions 17

6 Authors 19

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 3203Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

APARTMENTS IN STANDARD-TYPEHOUSES IN RIGA HOUSING ESTATES

During 2012 standard-type apartment prices in generalhave increased he prices increased by an average of 2he price increase was mainly observed in the first quarterof 2012 but in May of this year the prices reached theirhighest position ndash 595 EURmsup2 During the remaining threequarters of the year the prices have remained stable onlyminor fluctuat ions have taken place

It shows that the total activity in the apartment market in

2012 has increasedAfter the apartment price reduction throughout the

year which was observed in 2011 in the beginning of 2012there was a price rise he largest price increase in 2012was observed in March ndash by 07 In other months bothnegative and positive price movements were observed

At the end of 2012 the average value of one msup2 in thehousing estates of Riga was 595 EURmsup2

he highest growth of the average price of 1 sqm ofan apartment in the housing estates of Riga in 2012 wasobserved at Jugla ndash +5 he lowest price changes wereobserved at Zolitūde ndash +06 However the only negativeprice changes in 2012 were observed at Bolderāja wherethe prices fell by an average of 08

APARTMENT MARKET IN RIGA

In 2012 there have been certain changes in theapartment market of Riga however the changes have notbeen so significant as in previous years Price increase in therange of 2 ndash 8 has been observed in almost all apartmentsegments of Riga But in the vicinity of Riga the price levelhas remained unchanged in many locations and in someplaces the prices have even decreased

The following price changes have taken place in theapartment market of Riga in 2012

bull pthe prices of apartments located in the central part ofRiga have increased he prices have increased by 3 ndash 8on average in the central part of Riga he lowest priceincrease was discovered in the Old own and the peripheralpart of the city centre he highest price increase wasobserved in respect of apartments in renovated and newbuildings and apartments located in the Silent Centre andthe boulevard ring

bull practically no price change was observed in respect ofapartments located in wooden buildings An exception is theMaskavas suburb where the price of apartments located inwooden buildings has decreased by 5 on average

bull prices of standard-type apartments located in housingestates have increased by 2 on average he mostsignificant price change in 2012 was observed at Juglawhere the prices have increased by 5 Compared withJune 2007 when the highest price of one square metre ndash1620 EURmsup2 ndash was registered the prices were by 63lower at the end of 2012 If compared with the lowest priceever registered (September 2009 ndash 487 EURmsup2 on average)the prices are grown by 22

bull In the vicinity of Riga the apartment prices havedecreased in certain locations he price decrease has notbeen homogenous ndash it was 1 ndash 3 in 2012 he largest pricedrop was observed at Kauguri Jūrmala where the pricesdecreased by 35 on average during the year

In 2012 people more carefully selected apartmentproperties to be purchased hey took into account also suchfactors as house management and whether the undividedshare in the ground under the house where the apartment wassituated was in ownership

Thus a growing interest isseen for apartments in new orrenovated buildings not only fromthe part of foreigners who mostlyacquire property for obtaining aresidence permit

but also from the par t of local population which explains thelargest increase in prices of apartments in these buildings

1 A

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 4204Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

1 A

bull lack of quality housing in the central part of Riga Alongwith increasing customer requirements interest in theapartments with good location and good condition of thepremises has increased in 2012 Living in the centre of Rigahas several advantages ndash many significant objects are withina walking distance infrastructure development proximity ofsocially significant facilities prestige of residence and otherfactors

Changes of apartmentprices in the central part of Rigahave never been as apparent as inthe housing estates of RigaIn the central part there is a lot of apartments of variousquality levels with many factors influencing the valuesuch as location existence of utilities architecture of thebuilding traff ic intensity etc

After the significant price growth observed in the centralpart of Riga in 2011 the prices tended to stabilize already atthe end of 2011 he price growth observed in 2012 is to beassessed as low and the prices tend to stabilize

THE OLD TOWN

Price level of apartments in the Old own has slightly

increased in 2012 At the end of 2012 apartment prices inthe Old own started from 1500 EURmsup2 Most expensivetransactions recorded were associated with apartmentsin renovated and new buildings in 2012 and as in 2011 insome cases exceeded the amount of 4000 EURmsup2 hehighest amount of transaction per 1 msup2 was observed in thesummer of 2012 in Jēkaba Street where an apartment of17 msup2 in a non-renovated house was sold for 6400 EURmsup2he average transaction price of apartments in the Old ownin 2012 was 1400 ndash 3300 EURmsup2 he highest prices arefor apartments in an exclusive location in renovated or newbuildings with high quality finishing Supply price reached6500 EURmsup2 here are practically no simple apartmentsbeing offered for sale in the Old own the housing market

due to the demand focuses directly on the high-qualityapartments in good condition of the premises

he price increase concerned both medium-quality andhigh-quality apartments in the Old own and was 3 ndash 5in average he increase is explained by the exclusivity ofthe location factor and its key role in the purchase of anapartment

Buyers of homes in the Old Town may be divided in severalcategories

bull foreign nationals who purchase apartments with goodlocation to obtain a residence permit for business travelpurposes or to spend their vacations

bull Latvian residents whose primary residence is in anelite residential area and who purchase such apartments asreplacement housing for a long term

APARTMENTS IN THE CENTRAL PARTOF RIGA

In 2012 the housing market main trend was the sameas in 2011 ndash a stable and increased demand for high-qualityapartments with good location here is still lack of high-quality apartments located in the central part of Riga andbeing sold at a price corresponding to the market conditionsApartments are of ten either not complying with customerrequirements in terms of quality or the price is prohibitivelyhigh and inappropriate In the central part of Riga therewas observed a growth of prices just for good qualityapartments ndash apartments with quality interior decorationgood location in the centre of Riga good location in thebuilding as well as with all the necessary engineeringsystems In the Rigarsquos best locations such as the Old ownCentre and the Silent Centre the apartment prices increasedby 3 ndash 8 in 2012 he price increase is typical mainly forhigh-quality apartments in renovated and new buildingsIn general the prices increased by up to 5 in the centralpart of Riga he prices of apartments being offered arenot lower than 1100 EURmsup2 in the Silent Centre and from1500 EURmsup2 in the Old own he following factors havecaused the price growth and increase of market activity inthe centre of Riga

bull amendments to the immigration tax law adopted in2010 which created possibility to obtain residence permitin the case of purchase of properties in Riga and also inother places in Latvia herefore also in 2012 high-qualityand expensive apartments in the centre of Riga which costin excess of 100 000 LVL which is necessary for obtaining

a residence permit were still demanded Most attractiveapartments for obtaining residence permit were apartmentsin renovated or new buildings because such apartments areeasier to hire out at a later moment

bull investment in real estate is still a very popular and safeform of investment hus people prefer high quality andgood real estates ndash apartments in the central part of Rigathe value of which is less subject to market fluctuationsAcquisition of an apartment in the city centre will always bea less risky investment object

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 5205Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

1 A

APARTMENTS IN NEWLY BUILT HOUSES

In the first three quarters of 2010 there were built 1531apartments and compared to the first three quarters of2009 the decrease was 56 In the first three quarters of2011 there were built 1754 apartments and compared tothe first three quarters of 2010 the increase was 15 Butin the first three quarters of 2012 there were built 1560apartments and compared to the first three quarters of2011 there was a decrease of 11 his change is explainedby the fact that in 2011 new apartment building projectsgradually emerged in the market and many projects underconstruction were completed herefore it should be notedthat in 2012 the number of the commissioned apartmentbuilding projects was less than in the preceding year

Also in 2012 like in 2011 the supply of apar tments in newprojects consisted mainly of projects seized by banks within

which there are offered apartments not sold by developersof multi-apartment projects of largeconstruction companies such asMerks YIT NCC Hanner etc aswell as of individual apartments inprojects of recent years

However while in 2011 the banksand their subsidiaries still thoughtwhat to do with the new housingfacility portfolio hoping that aninterest in the purchase thereof couldbe shown by potential investors whowould purchase projects as a wholebut when these expectations werenot met in 2012 we see that theproportion of new projects seizedby banks has grown significantly inthe supply structure and that thoseprojects are being offered for sale inthe form of separate housing unitshe largest number of apartmentswithin new housing projects isoffered by Ektornet a subsidiary of

Swedbank who is offering severalcompetitive facilities both in terms of location and price Acustomer can choose from a variety of renovated differentsize apartments mostly in and around Riga Ektornet bycarrying out an intensive marketing campaign in 2012 hasbeen able to attract a wide range of stakeholders whichis demonstrated by the rapid growth in the number oftransactions

Also subsidiaries of other banks have taken a numberof measures to promote sale of the seized facilities andimprove the market recognisability here are created newbrands such as Reverta ( Parex banka ) Pillar ( Trasform ABLV ) Company websites are being developed andimproved more attention is paid to the customerservice both by involving larger real estate companies ascooperation partners in sale of properties and by creatinginternal sales teams

If the main competitive advantage of bank subsidiariesis the price and the varied offer then in terms of qualityand safety the biggest competitors are large developercompanies that have proved themselves in the market

bull buyers placing their free funds and considering suchapartments to be safe investment objects such apartmentsare usually hired out after purchase

APARTMENT MARKET IN THE VICINITYOF RIGA

Demand for apartments in the vicinity of Riga is mainlyformed by

bull People who work in Riga but for financial reasonsare looking for an opportunity to buy a cheaper apartmentoutside of Riga

bull Locals who are looking for a new residence forthemselves in well-known surroundings

bull People for whom it is a conscious choice to live outsidethe capital city and for whom the financial arguments arenot playing the main role

In contrast to the small priceincrease in the housing estates ofRiga the average price level hasdecreased outside of Riga

The pricedrop in the vicinity ofRiga was not evenhe largest price drop in 2012 wasregistered in Jūrmala Kauguri wherethe prices have decreased by 35(in 2011 ndash -88) But the lowestprice drop was registered in Ogre ndash13 (in 2011 ndash -43)

In Salaspils the prices havedecreased by 31 (in 2011 ndash -73)he price difference betweenSalaspils and Riga housing estates has increased again ndashup to 26 (in 2008 ndash10 in 2009 ndash 20 in 2010 ndash 16)But in Ogre at the end of 2012 the apartment prices werealready by 41 lower than in Riga (at the end of 2011 ndash by

39 at the end of 2010 ndash by 30) he price difference hasgrown also in Jūrmala Kauguri where at the end of 2010the prices were by 25 lower but at the end of 2011 theprices were already by 38 lower than in Riga housingestates At the end of 2012 the apartment prices in Kauguriwere already by 44 lower than in Riga housing estateshus the gap between the prices has increased possibly upto a maximum and this trend should not continue in 2013

Price level of an apartment in satisfactory technicalcondition in a standard-type house in the vicinity of Rigaat the end of 2012 ranged from 360 to 560 EURmsup2depending on the location availability of infrastructure aswell as the distance to Riga A higher apartment price levelis in some locations in the vicinity of Riga such as ĀdažiBaloži Carnikava and also Ķekava where the standard-typeapartment prices are ranging from 500 EURmsup2

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 6206Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

1 A

If in the new housing projects located in the city centrethe customers purchased the apartments paying moreattention to the location of the building and the amenities

provided and were willing to sacrifice quite a large amountdespite the fact that decoration and interior fitting-outworks were not completed and had to be carried out inthe economy class segment the target audience had clearlystrengthened their demand to have a completely finishedapartment his was evidenced by a rapid increase in thenumber of transactions with completed new projects andvery little interest in the facili ties where the internal finishingwork had to be carried out by the owners themselvesdespite the fact that such facilities were offered at a lowerprice herefore those bank subsidiaries who renovatedcompleted improved the seized projects and offered forsale finished apartments with full interior decorat ions are tobe considered progressive and forward-looking

All of the above factorsdetermine the price level in thesegment of new projectsIn the new projects offered by banks the price per squaremetre of apartment in Riga housing estates ranges from900 to 1300 EUR depending on location finishing quality

level and other factors In the Riga district the competitiveprice ranges from 700 to 1000 per square metre hebanksrsquo housing portfolio contains also new projects in theRiga city centre Jūrmala and other demanded places with ahigher price level but they were not of fered for sale in 2012Most likely an increase of prices for this price category isexpected in the nearby future when the sale could be moresuccessful

A new apartment building construction costs in 2012had risen to an average of 800 ndash 1000 EURmsup2 In order toensure the profitability of the construction in the case whenfully finished and completed apartments are offered in thehousing market developers must sell the apartments ata price not less than 1100 ndash 1300 EURmsup2 of living spaceConsequently the major developers such as YIT and Merksoffered newly built apartments in the housing estates atthe price of 1300 ndash 1900 per msup2 he price range for 1 sqm

In particular we can highlight such companies as YI andMerks which in spite of the fact that their price level ishigher than the prices offered by banks for equivalentfacilities have achieved very good results both in terms offacilities offered and the number of transactions

High demand for new dwellings in the central part of Rigawas a characteristic feature of this year

Foreigners are themain target audience for suchfacilities they purchase propertiesfor obtaining a residence permit

in LatviaOne of the most demanded projects in the reporting year

was the project at Antonijas Street 16a where most of the60 apartments offered have been sold Also apartments atMartas Street 7 were highly demanded several transactionshave been concluded also in respect of the project PetitParis in Melngalvja Street in spite of the high price level in allthese projects

7172019 Apartment Market

httpslidepdfcomreaderfullapartment-market 7207Summary of Analysis of Development of Certain

Real Estate Market Segments in 2012

1 A

of apartment located in a new project situated in the citycentre was from 1800 to 3000 EUR in 2012

In cases where apartments located in newly built houses