apec oil and gas security newsletter -...

TRANSCRIPT

APEC Oil and Gas

Security Newsletter

Your Organization June 2015 Issue No.4

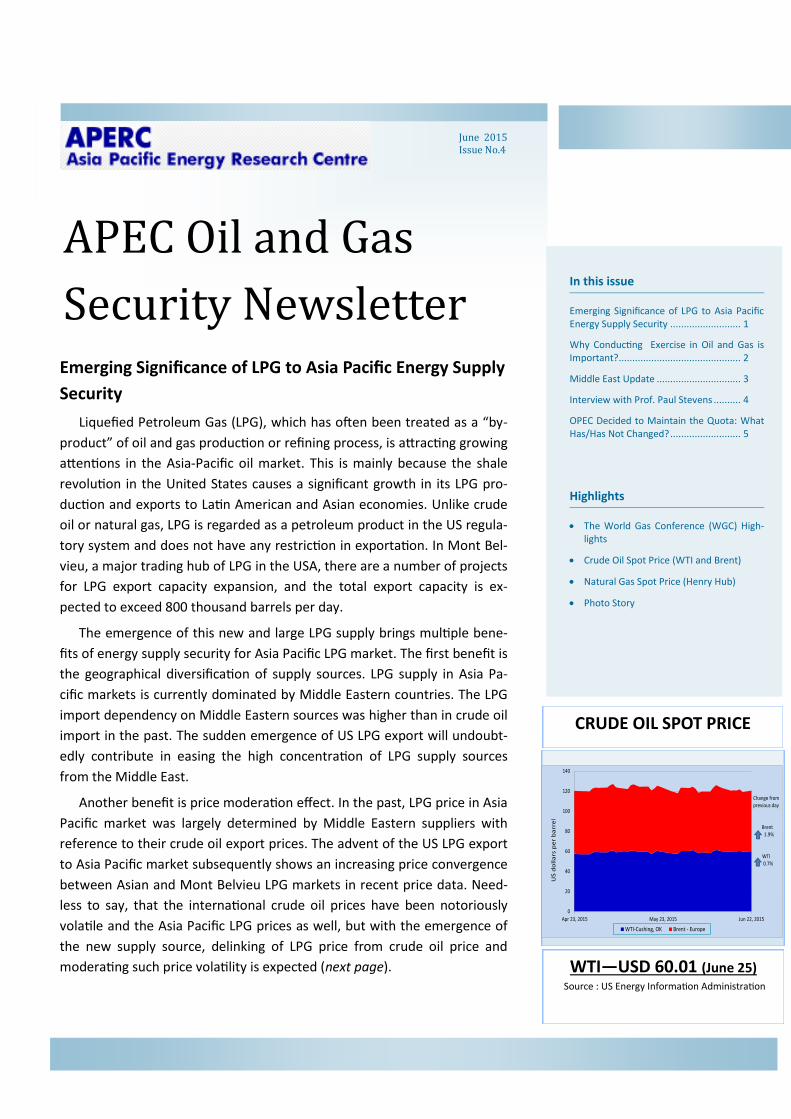

CRUDE OIL SPOT PRICE

WTI—USD 60.01 (June 25) Source : US Energy Information Administration

In this issue

Emerging Significance of LPG to Asia Pacific Energy Supply Security .......................... 1

Why Conducting Exercise in Oil and Gas is Important? ............................................. 2

Middle East Update ............................... 3

Interview with Prof. Paul Stevens .......... 4

OPEC Decided to Maintain the Quota: What Has/Has Not Changed? .......................... 5

Highlights

The World Gas Conference (WGC) High-lights

Crude Oil Spot Price (WTI and Brent)

Natural Gas Spot Price (Henry Hub)

Photo Story

Emerging Significance of LPG to Asia Pacific Energy Supply

Security

Liquefied Petroleum Gas (LPG), which has often been treated as a “by-

product” of oil and gas production or refining process, is attracting growing

attentions in the Asia-Pacific oil market. This is mainly because the shale

revolution in the United States causes a significant growth in its LPG pro-

duction and exports to Latin American and Asian economies. Unlike crude

oil or natural gas, LPG is regarded as a petroleum product in the US regula-

tory system and does not have any restriction in exportation. In Mont Bel-

vieu, a major trading hub of LPG in the USA, there are a number of projects

for LPG export capacity expansion, and the total export capacity is ex-

pected to exceed 800 thousand barrels per day.

The emergence of this new and large LPG supply brings multiple bene-

fits of energy supply security for Asia Pacific LPG market. The first benefit is

the geographical diversification of supply sources. LPG supply in Asia Pa-

cific markets is currently dominated by Middle Eastern countries. The LPG

import dependency on Middle Eastern sources was higher than in crude oil

import in the past. The sudden emergence of US LPG export will undoubt-

edly contribute in easing the high concentration of LPG supply sources

from the Middle East.

Another benefit is price moderation effect. In the past, LPG price in Asia

Pacific market was largely determined by Middle Eastern suppliers with

reference to their crude oil export prices. The advent of the US LPG export

to Asia Pacific market subsequently shows an increasing price convergence

between Asian and Mont Belvieu LPG markets in recent price data. Need-

less to say, that the international crude oil prices have been notoriously

volatile and the Asia Pacific LPG prices as well, but with the emergence of

the new supply source, delinking of LPG price from crude oil price and

moderating such price volatility is expected (next page).

0

20

40

60

80

100

120

140

Apr 23, 2015 May 23, 2015 Jun 22, 2015

WTI-Cushing, OK Brent - Europe

Change from previous day

Brent1.9%

WTI 0.7%

US

do

lla

rs p

er

ba

rre

l

2

Emerging Significance …..

There are of course challenges to realize such benefits. Importation

and distribution infrastructures need to be developed. The relative

price of LPG against other energy sources such as coal also has to be

competitive. Yet, rooms for LPG demand growth are immense in Asia

Pacific region and this emerging opportunity to improve energy supply

security should be fully utilized.

NATURAL GAS SPOT PRICE

Why Conducting Exercise in Oil and Gas is Important?

There are a number of factors that could trigger threats to an

economy’s oil or gas infrastructure facilities. It could either caused by

natural calamities in the economy or from outside influences particu-

larly if the economy has supply dependency on oil and gas exporting

countries like the Middle East. In addition, uncertainty of oil or gas

chokepoint due to war or terrorism may also pose a threat in oil and

gas supply to the economy.

Depending on the scale of incident, extent of the damage or the

time required for repairing the facilities, this would create oil or gas

supply disruptions in the economy. These could lead to serious cross-

sectoral problem cascading to infrastructure system failures since oil

and gas are important fuels in the energy sector (e.g. transport and

electricity sectors). Worst-case-scenario, it will cause a regional or

national security threat to the economy for a short period of time or

longer if not addressed immediately.

Readiness, performance, and capacity of the system (e.g. policies,

plans, procedures, and communication protocols) including personnel

of the organization that would have a function of addressing certain

energy crisis and/or emergency must always be strengthened. This is

to ensure effective implementation of measures and the response and

recovery strategies as well during the real emergency situation. The

key to achieve the best performance and capacity of the system and

personnel in handling the disruptions of oil and gas supply is by con-

ducting regular exercise on oil and gas emergency.

Exercise is the process used for training, assessment and practice

to improve performance and capacity in an organization through a

simulated situation where the system and personnel should respond

to so that their decision or action can be evaluated. Specifically, exer-

cises can be used for the following:

“ ..…could then trigger

to more serious cross-

sectoral issue, cascading

to infrastructure system

failures.”

Henry Hub—USD 2.79 (June 25) Source : US Energy Information Administration

3

Map of Saudi Arabia

Map of Saudi Arabia

Saudi Arabia has 16% of the world's proved oil reserves, is

the largest exporter of total petroleum liquids in the world,

and maintains the world's largest crude oil production ca-

pacity.

Source :Country Analysis Brief: Saudi Arabia

US-Energy Information Administration (EIA)

Validating and testing the system covering the oil and gas

fields (e.g., policies, plans, procedures, institutional struc-

tures, information and communication technologies);

Training of personnel regarding their respective roles and

responsibilities to improve performance and capacity in

dealing with oil and gas supply disruptions;

Improving institutional frameworks for better inter-

organizational coordination and communication in dealing

with oil and gas supply disruptions;

Identifying gaps in resources to effectively dispense

measures/programs when addressing supply disruptions;

Identifying opportunities to improve the system and person-

nel, and

Improvising to find the best solution and strategy to address

oil and gas supply disruptions.

“... means that IS has the

ability of carrying out violent

attacks even in areas under

strict surveillance.”

Middle East Update—Terrorist Attacks in Saudi

Arabia

Two Shia Mosques in the Eastern Province of Saudi Arabia

were attacked by suicide bombers in separate incidents in May.

The twin suicide attacks, targeting Friday prayer gatherings, re-

sulted to at least 29 deaths. The Islamic State (IS), a terrorist

organization based in Iraq and Syria, claimed responsibility for

both crimes in statements posted on social media. The two inci-

dents only showed that the IS has already penetrated into one

of the world largest oil producing countries, which also means

that IS has the ability of carrying out violent attacks even in are-

as under strict surveillance.

As a self-claimed Sunni radical organization, IS has been tar-

geting Shia population in the Middle East, because it considers

them apostates rejecting Sunni beliefs. Besides, it is also calling

for the Arabian Peninsula to be cleansed of Shia and Saudi Ara-

bia has a certain number of Shia minorities especially in the

Eastern Province. This is where main oil fields and petroleum-

related facilities are concentrated.

On June 3, Saudi Ministry of Interior issued a wanted list of

16 suspects in connection with the recent terrorist attacks,

offering a reward of 5 million Saudi Riyals for information lead-

ing to their arrests. The suspects are all Saudi nationals.

4

Interview with Prof. Paul Stevens

Prof. Paul was a panel discussant during the IEEJ 50th /APERC 20th Pre-

Anniversary Joint Symposium held in Tokyo last 11th June 2015. His presentation was

on “Oil prices and the economic impact for the UK” which touched upon oil prices

prospects and other factors. In conclusion, he mentioned that low prices will serious-

ly inhibit investment in North Sea oil production.

Following was APERC’s Interview with Prof. Stevens:

APERC—I understand you have been with the academe since 1973 and alter-

nately serve as consultant both in the private and government companies,

especially in the field of oil and energy, would you describe briefly how do

you manage?

Prof. Stevens—There is considerable overlap between being an academic

and a consultant given the practical nature of oil and gas. Thus my consul-

tancy work helped inform both my academic work (teaching and research)

and vice versa.

APERC—As a professor which area did you enjoy teaching most?

Prof. Stevens—The issues relating to energy policy because of their practical

application and the fact that there were no “correct” answers to the ques-

tions. Thus the material made for interesting discussions with the students.

APERC—As a consultant, have you been sought advice in addressing oil and

gas supply security issues? If yes, do you mind mentioning which country

and in what particular issue or what were the cause of the threat?

Prof. Stevens—Many different countries, that ranged from OECD countries

to emerging market economies all over the world. The issues included do-

mestic energy pricing; how to improve energy efficiency; polices to attract

upstream investment; how to avoid resource curse and manage oil revenues

effectively; managing price volatility; and many other topics.

APERC—In 2009 you received an OPEC Award in recognition of your out-

standing work in the field of oil and energy research, which research was

this?

Prof. Stevens—It was not for any specific piece of research. Rather it was

for a general contribution to research into the oil industry over many years

APERC—In your studies and researches were these cases of supply security

issues due to global oil and gas markets volatility, natural calamities, or geo-

political instability, among others? How did you address the supply (or po-

tential) disruption? Please explain briefly.

Prof. Stevens—It is not possible to generalize about these issues because

each case tended to be different. The only commonality is that in most cas-

es security of supply concerns are best dealt with by ensuring diversity of

supply, both in terms of types of energy and their geographic sources.

Prof. Paul Stevens is a distinguished fellow at

Chatham House, the Royal Institute of International

Affairs, in London. He was educated as an economist

and as a specialist on the Middle East at Cambridge

and the School of Oriental and African Studies be-

tween 1973 and 1979. From 1979 to 1993 he taught

at the American University of Beirut in Lebanon,

interspersed with two years as an oil consultant at

the University of Surrey. Between 1993 and 2008 he

was professor of Petroleum Policy and Economics at

the Centre for Energy, Petroleum and Mineral Law

and Policy at the University of Dundee, Scotland, a

chair created by BP. He is now professor emeritus at

the University of Dundee and a visiting professor at

University College London (Australia). He has pub-

lished extensively on energy economics, the interna-

tional petroleum industry, economic development

issues and the political economy of the Gulf. He also

works as a consultant for many companies and gov-

ernments. In March 2009 he was presented with the

OPEC Award in recognition of his outstanding work

in the field of oil and energy research.

(http://www.chathamhouse.org/about-us/

directory/70680#sthash.TnZH2Sbd.dpuf )

“...in the APEC region,

importers tend to be

more risk averse than in

Europe.”

5

APERC—As a Researcher based in Europe what is the major difference in ener-

gy security issues between Europe and the APEC region?

Prof. Stevens—There are many similarities given both regions are dependent

upon energy imports. However, an important difference is that in the APEC

region, importers tend to be more risk averse than in Europe. This means they

are willing to pay more for secure supplies, which gives rise to the so-called

“Asian Premium” both in oil and gas prices into Asia. “...risk in the OPEC

market share being

threatened again by

unconventional crude

oil.”

Photo and Photo Story

OPEC Headquarters in Vienna, Austria

Photo from Wikimedia Commons

OPEC is a permanent intergovernmental or-

ganization of 12 oil-exporting developing na-

tions that coordinates and unifies the petrole-

um policies of its Member Countries.

Source: http://www.opec.org/opec_web/en/

OPEC Decided to Maintain the Quota: What Has/Has Not

Changed?

The Organization of Petroleum Exporting Countries (OPEC) Conference

was held last 5 June 2015. While some member countries have requested

production cutbacks even before the Conference has started to maintain

crude oil prices at an optimum level, others expressed intentions to increase

their respective national production. Nevertheless, by having the leadership

of Saudi Arabia and other GCC countries, OPEC’s policy on production quota

was left unchanged at 30 million barrels per day.

While final decision made was always the same as the previous confer-

ences, there are several differences in terms of the circumstances and back-

ground.

The first difference is on the expectation by market players on produc-

tion. The decision to postpone the production cutback made at the 2014

Conference came as a surprise to the market players who were expecting for

a reduction that time. Then this year, OPEC decided to maintain the produc-

tion quotas just as how the market would be expecting it.

The second difference is on the oil demand forecasts. When the Confer-

ence was held last year, the global oil demand forecast for 2015 was project-

ed to be declining, and crude oil price was already at the downward trend.

Due in part to it, OPEC decision to maintain their quota has further resulted

to significant drop of crude oil prices to about $40-per-barrel level early this

year. But then, oil consumption has started to show a recovery before the

2015 Conference. Therefore this time, the OPEC decision was not recognized

as a factor for transaction in the market.

What then was the meaning and effect of the decision for keeping the

production quota the same? The decision is commonly viewed as OPEC’s

strategy to secure their market share. As a result of what has happened after

the 2014 Conference, the number of shale-oil drilling rig in the United States

starts to decrease in order to avoid loss from lower oil price. Also, with the

sign of recovery in global oil demand, the oil market seemed to return to be-

coming OPEC dependent again. (next page)

6

The World Gas Conference (WGC) Highlights

Energy Challenges

The most significant gathering in the global gas industry was

held during the first week of June 2015 in Paris. According to the

organisers - the French Gas Association (AFG) and the Interna-

tional Gas Union (IGU) - 3,700 delegates from 90 countries were

present at the 26th triennial event to exchange views on strate-

gic, commercial, technical, and engineering issues and opportu-

nities in the increasingly globalising gas and LNG markets.

Unlike other major gas industry events during the past cou-

ple of years, the conference did not feature direct exchanges of

blunt views on pricing of LNG and natural gas.

The global gas industry today faces difficulties - lower oil and

gas prices, slower demand growth (than previously expected),

tougher conditions for project development, as well as challeng-

es posed by competition from different energy sources. Re-

flecting the difficult environment and ongoing discussions on

global climate change leading to the UN gathering to be held

later this year in the same city, many of speakers called policy

measures to encourage natural gas to play even more im-

portant roles in the sustainable global energy mix. The gas in-

dustry also acknowledged the need for better communication

with the general public and policy makers about the potential

advantages of natural gas in realising sustainable future for the

planet.

While the discontent against government policies expressed

by the speakers was apparently focused on Europe, one speaker

specifically mentioned Japan as a country where imbalanced

policy measures could hinder growth of natural gas.

Noticeable though in the conference was the relatively low

presence of Asian speakers in the plenary sessions, despite the

fact that the region is expected to have significant growth in gas

demand in the future. There were Asian speakers one each from

Korea and China, but there was no keynote speaker from Japan

for the first time in many decades.

The anticipated significant expansion of LNG liquefaction

capacity in the next couple of years mainly from Australia and

the United States is expected to bring about structural changes

in the global gas markets. The next two big IGU events will be

held in those two countries -'LNG 18' in Perth in 2016 and 27th

WGC in Washington DC in 2018.

_____ 1The conference is held once every three years. The first was held in 1931

in London )

Asia Pacific Energy Research Centre

The Asia Pacific Energy Research Centre (APERC) was established in

July 1996 in Tokyo following the directive of APEC Economic Leaders

in the Osaka Action Agenda. The primary objective of APERC is to

conduct researches to foster understanding among APEC members of

regional energy outlook, market developments and policy.

Fax (+81) 3-5144-8555

Tel (+81) 3-5144-8551

E-mail [email protected]

Contributors for this Edition

Mr. Yoshikazu Kobayashi

Mr. Chrisnawan Anditya

Mr. Shuji Hosaka

Mr. Ichiro Kutani

Mr. Takashi Matsumoto

Mr. Hiroshi Hashimoto

Ms. Elvira Torres Gelindon

Editor-in-Chief

OPEC Decided ...

On the other hand, this may possibly adversely affect

the OPEC member countries. Over supplied and lower

crude oil price market will eventually lead to the contin-

ued pressure on the national finances of oil-producing

countries. If this is the case, even if oil demand increases

in the future, OPEC oil-producing countries might not be

able to invest enough in new field and in responding de-

mand hikes in a timely manner. It will then pose a risk in

the OPEC market share being threatened again by uncon-

ventional crude oil.