apidc – venture capital limited -...

TRANSCRIPT

133

4. APIDC – VENTURE CAPITAL LIMITED AND

ENTREPRENEURSHIP DEVELOPMENT OF

ANDHRA PRADESH

4.1 APIDC – VENTURE CAPITAL LIMITED AND

ENTREPRENEURSHIP DEVELOPMENT OF ANDHRA

PRADESH

Andhra Pradesh Industrial Development Corporation (APIDC) promoted

APIDC–Venture Capital Limited (VCL) on 29th

August 1989. The approval of

the Government of India to commence operations was accorded in April 1990.

APIDC-VCL was privatized in 1994 and Dynam ventures (East) Pvt. Ltd, has

been awarded control of APIDC-VCL after a competitive selection process.

Thus it has become a subsidiary of Dynam Venture (East) Pvt. Ltd., a firm

promoted by professionals with a wealth of experience in entrepreneurship,

consulting, equity investments, technology development, etc.

The company acts as manager and trustee to the APIDC Venture Capital

Fund (VCF), 1990. It is the first state level Venture Capital Fund in India to be

managed by owner-managers with strong entrepreneurial skills. The fund

manager’s strength is their understanding of what conceiving and building a

business or enterprise is all about, having gone through the process

themselves.

Initially it was incorporated with an authorized capital of Rs.2 million,

out of which Rs. 0.2755 million was paid-up capital in 1989. The paid up

capital was raised to the level of authorized capital of Rs. 2 million during

1991-92.

The company managers the venture fund of Rs. 135 million. The

authorized corpus capital of the fund is Rs. 135 million out of which Rs.41.35

134

million is paid-up, which forms the corpus of the fund known as ‘ APIDC

Venture Capital Fund – 1990’. The fund resources come from the World

Bank, the Industrial Development Bank of India (IDBI), the Andhra Pradesh

Industrial Development Corporation (APIDC), Small Industrial Development

Bank of India (SIDBI), Andhra Bank, Indian Overseas Bank (IOB) and NRIs

etc.

APIDC-VCL is the first of series of venture capital funds that will invest

in companies in Southern & Western India, with a focus on the state of

Andhra Pradesh. It will invest across several business sectors, with projections

that seek to exploit key differentials (in market potential, technology,

operations, and return on capital) between India and industrialized world.

Generally it will invest in start-up as well as expansion type of projects.

APIDC has been encouraging technology based ventures in the state of

Andhra Pradesh particularly those started by first generation technocrat-

entrepreneurs, through equity participation and by canalizing IDBI’s seed

capital assistance to entrepreneurs. However the main objectives of the fund

are:

1. To promote high technology and assist entrepreneurs to take up

ventures involving high risk.

2. To generate the highest long-term capital gains for its investors,

who view their investments as ‘patience’ money and

3. To make its commitment to the enterprises it assist beyond mere

funding i.e. assisting and adding values to them in every way it

can.

135

4.2 INVESTMENT STRATEGY AND SIZE

APIDC-VCL will invest in companies with the ability to build unique

competitive advantages that others will find difficult to emulate. It will add

value to portfolio companies through support in activities external to the

company, being a responsive facilitator of the entrepreneurial process.

APIDC-VCL is mandated to restrict its investment to Rs. 200 lakhs per

round of investment. However, it has successfully syndicated large

investments with other venture capital/private equity funds. This funding will

be in the form of equity or quasi-equity investment. Hence the company uses

equity shares, redeemable preference shares, convertible debt and conditional

loan as instruments for its venture capital finance.

4.3 DEAL GENERATION AND INVESTMENT DECISION-

MAKING STEPS

VCL deal generation strategy will practice a relatively higher level of

quality deals than a general promotional approach, and will generate sufficient

deals to invest the monies raised by it. Their focused approach to canvassing

entrepreneurs will be more efficient in finding qualified entrepreneurs and

project ideas that meet their criteria of ‘Key differentials’. VCL has set up a

flow of investment opportunities with its existing network in India and with

it’s associated in the USA. VCL also pans to promote through focused

seminars, a public relations campaign to institutions and industry associations,

to heighten the awareness of its activities.

136

VCL has set up a responsive system of receiving the investment proposals,

evaluating them and communication to the promoters/entrepreneurs. This is

basically a four-step process.

1. The submission of a full-fledged business plan with all supporting

evidence

2. A full blown presentation by the management team

3. Final completion of the due diligence

4. Negotiation of the terms of investment

The promoters/entrepreneurs are made fully aware of these steps and at

each stage they are informed whether the process has moved forward or the

proposal is being rejected.

4.4 DUE DILIGENCE AND CRITERIA FOR

INVESTMENT

VCL will evaluate each deal against the started ‘investment strategy’,

and whether the returns meet the target rates, and whether the risks can be

contained and are appropriate, prior to proceeding further. Specifically, VCL

will evaluate:

1. The quality of the management team

2. The match with their strategy of ‘Key differentials’ resulting in a

strong competitive edge for the company;

3. The size and growth rate of the market

4. Potential for high profitability while protecting the downside;

5. Types of risk and their management; and

6. The ability to disinvest with high capital gains and the congruence of

these objectives with the management teams.

137

4.5 MONITORING AND VALUE ADDITION

VCL, in line with its pro-active strategy of value-addition, follows and

active mode of monitoring and value addition. Specifically, VCL in

collaboration with the investee company sets up milestones that lead up to the

eventual disinvestments from the investee company. These milestones are then

monitored actively, and the invested company is urged to adopt a reporting

system that facilitates the monitoring of the progress versus the milestones. At

least one member from VCL will typically serve on the Board of Directors of

the company on the average of once in a week, and will install a reporting

system that evaluates progress of the investee company versus the milestone

every month government connectivity to add value to the process of enterprise

building.

4.6 THRUST AREAS

The new Equity Policy of the company proposes to give a special

impetus to Industrial Development. The company has identified the following

for special focus for investment.

1. Food & Agro processing except traditional industries.

2. Petroleum and Petro-chemicals.

3. Chemicals & Fertilizers.

4. Engineering & Automotives.

5. Minerals based industries.

6. Information Technology.

7. 100% Export Oriented Units.

8. Biotechnology.

9. Renewable sources of Energy.

138

10. Energy Saving Devices, Appliances, etc.

11. Energy Efficient and Waste Reduction Technologies and Processes.

12. Pollution Control Equipment and Devices.

13. Waste Utilization and Recycling.

4.7 BIOTECH INVESTMENT

APIDC-Venture capital has put investments of $1.62 million (Rs.

8.1crore) in three US-Indian biotech companies. In the first batch of

funding from its recent Biotech Venture Fund, it has put in $5,40,000

each in Bioserve Biotechnologies, Genomik Design Pharma and Silico

Insights. The investment through the APIDC-Venture Capital has

attracted tremendous response from several banks and insurance

companies. So, it planned with a corpus of Rs. 150 crore, and has closed

commitments for Rs 40 crore, including contributions from GIC, LIC,

Andhra Bank and the AP Government. The fund has picked start-up and

early-stage businesses such as healthcare, drug discovery, agriculture,

dairy etc. The portfolio of investments made by APIDC Venture Capital

Ltd is clearly demonstrated in table.

Table 4.1

VENTURE UNITS ASSISTED BY APIDC-VCL

Sl.

No

Name of

the

company

Amount

Sanct-

ioned

(Rs.lakh

s)

BUSINESS

COMPETITIVE

STRENGTH

1 Suyog

Chemicals

Pvt. Ltd.,

Nagpur

60.00 Specialty chemicals

with applications in

mining, paper, sugar,

effluent treatment etc.

Xanthates, acrylic

polymers, Phthalates

1. Indigenous developed

continuous process

technology for

Xanthates competitive

batch process, giving

rise to better yields and

139

and other chemicals lower cost of

production.

2. Innovative

management team.

2 Kakatiya

Electronics

Pvt. Ltd.,

Hyderabad

5.90 Provide innovative

products based on

Infrared sensors in

Automotive industry.

Indigeneously

developed Auto dippers

for LCVs & Cars for the

first time in the country.

3 Gland

Pharma

Limited,

Hyderabad.

150.00 Pharma company with

focus on small volume

parenterals

(injectibles). Moving

from a contract

manufacturing

company to direct

marketing capitalizing

its strengths in

institutional sales and

SVPs.

Collaboration from

Vetters Injekt, Germany,

one of the best contract

manufacturing

companies in the World,

for prefilled syringes for

the first time in the

country.

4 Srinisons

Cables

Limited,

Chennai

50.00 Providing wiring

harnesses for

automotive and white

goods industry.

One of the two

integrated wiring

harness manufacturers

in the country and only

Indian company.

5 Trendex

Retail

Informatics

Pvt. Ltd.,

Hyderabad

9.04 Providing information

data base to FMCG

sector.

Development of 100 %

reliable data base of

retail outlets for various

cities.

6 Ocean

Sparkle

Ltd.,

Hyderabad.

250.05 Providing OEM

services for ports, ship

to shore cargo

transport, etc.

Excellent management

team with hands on

shipping experience.

Established virtual

monopoly in managing

private sector corporate

ports and moving into

Govt. managed ports

like Goa, Ennore, etc.

7 Nucon

Zander

(India) Pvt.

Ltd.,

Hyderabad

48.48 Manufacture of high

efficiency, air/gas

filters and dryers

German collaboration

for Manufacture of high

pressure filter elements

in the pneumatic

applications. One of the

top two companies in

the country.

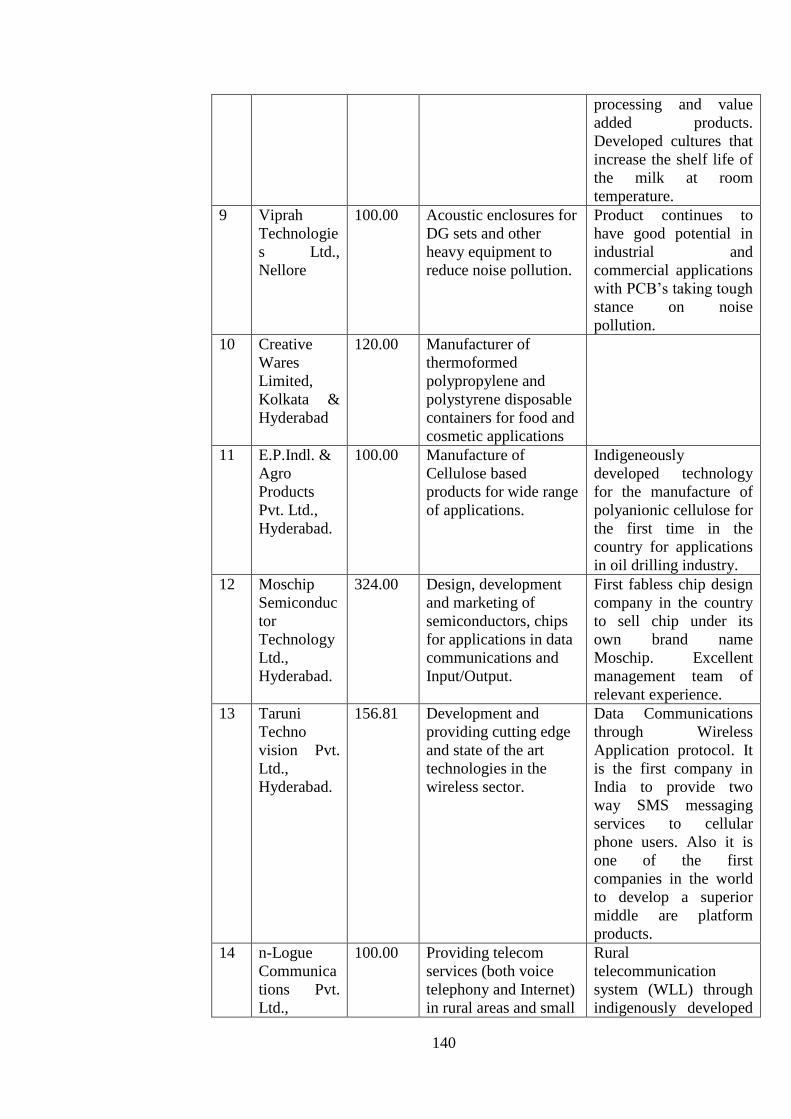

8 Dodla Dairy

Ltd.,

Nellore

170.40 Procuting and

processing milk, and

manufacture of value

added products.

Collaboration with

IMAC USA, one of the

top three dairy

technology companies

in the US, for milk

140

processing and value

added products.

Developed cultures that

increase the shelf life of

the milk at room

temperature.

9 Viprah

Technologie

s Ltd.,

Nellore

100.00 Acoustic enclosures for

DG sets and other

heavy equipment to

reduce noise pollution.

Product continues to

have good potential in

industrial and

commercial applications

with PCB’s taking tough

stance on noise

pollution.

10 Creative

Wares

Limited,

Kolkata &

Hyderabad

120.00 Manufacturer of

thermoformed

polypropylene and

polystyrene disposable

containers for food and

cosmetic applications

11 E.P.Indl. &

Agro

Products

Pvt. Ltd.,

Hyderabad.

100.00 Manufacture of

Cellulose based

products for wide range

of applications.

Indigeneously

developed technology

for the manufacture of

polyanionic cellulose for

the first time in the

country for applications

in oil drilling industry.

12 Moschip

Semiconduc

tor

Technology

Ltd.,

Hyderabad.

324.00 Design, development

and marketing of

semiconductors, chips

for applications in data

communications and

Input/Output.

First fabless chip design

company in the country

to sell chip under its

own brand name

Moschip. Excellent

management team of

relevant experience.

13 Taruni

Techno

vision Pvt.

Ltd.,

Hyderabad.

156.81 Development and

providing cutting edge

and state of the art

technologies in the

wireless sector.

Data Communications

through Wireless

Application protocol. It

is the first company in

India to provide two

way SMS messaging

services to cellular

phone users. Also it is

one of the first

companies in the world

to develop a superior

middle are platform

products.

14 n-Logue

Communica

tions Pvt.

Ltd.,

100.00 Providing telecom

services (both voice

telephony and Internet)

in rural areas and small

Rural

telecommunication

system (WLL) through

indigenously developed

141

Hyderabad. towns based on WILL

technology.

Cordect technology

facilitating usage of

internet and telephony

on the same line at the

same time.

15 CxK

Networks,

Hyderabad.

50.00 Providing researched

content to corporate

sector.

Excellent management

team.

16 Indus

Technology

Pvt. Ltd.,

Chennai &

Singapore

100.00 A Computer Machine

Vision Solutions

company, providing

high-end machine

vision solutions to

customers in the

manufacturing

industry.

Collaboration with IIT,

Madras & TeNet group

and has sound domain

knowledge and expertise

in the technology and

business of machine

vision. It has delivered a

variety of solutions to

several leading

companies in the field of

semiconductor

manufacturing, both in

the front-end and the

back-end areas of

operation.

17 Triad

Fleetcontrol

India Pvt.

Ltd.,

Singapore.

50.00 Providing automated

Fuel and Fleet

Management System

(FMS) (CRM

technology tool) to

fleet managers of large

fleet transport

organizations.

Technical collaboration

with Rose man Engg.,

one of the world leaders

for automated fuel and

fleet management

systems.

18 Vibromech

Engineers &

Services

Ltd.,

Chennai.

125.00 Manufacture of

Vibration Dampers,

Lube Oil Pumps and

Air Cylinders

Assemblies.

Company has significant

advantages in

technology; cost of

manufacture and cost of

design, over the

developed market

vendors, who are the

only current competitors

for the large auto majors

around the world.

19 Foursoft

Ltd.

100.00 Logistics

Source: Annual reports of APIDC-VCL

It is evident from Table 4.1 that the portfolio of investments of APIDC-

Venture Capital Ltd. It has invested Rs.365.85 lakhs in Computers and

Software, Rs.60 lakhs in Chemicals, Rs.329.90 lakhs in Electronics, Rs.150

142

lakhs in Pharma, Rs.425.05 lakhs in Services, Rs.170.40 lakhs in Milk, Rs.100

lakhs in Agro, Rs.150 lakhs in Communications, Rs.50 lakhs in Cables,

Rs.168.48 lakhs in Manufacturing and Rs.100 lakhs in Logistics.

Hence, the major investments of APIDC-Venture Capital Ltd were

attracted by Services, Electronics and IT industry. However, it is very clear

from the table that APIDC-Venture Capital Ltd has invested its money to the

extent of 68.42 percent in Andhra Pradesh.

Financial performance of APIDC is also very considerable and

significant when compared to other venture capital funds as the IRR of

APIDC-VCL is very high due to its portfolio of undertakings in which it has

the investments.

Hence, the summarized financial results of APIDC-Venture Capital

Fund for the year of 2005-06 and 2013-14 and a percentage change in the total

performance are given through table 4.2. From table 4.2 it can be seen that the

financial performance of APIDC-VCL. The gross income of the organization

increased by 88.61 percent whereas expenditure was decreased by 7.18

percent. The gross profit of the organization was Rs.2.027 lakhs during 2005-

06 against to 32.491 lakhs in 2013-14. Hence, the profitability position of the

organization was multiplied over the years at 106.24 growth.

143

Table-4.2

FINANCIAL PERFORMANCE OF APIDC-

VENTURE CAPITAL LTD

Particulars 2005-06 2013-14 % increase

/ decrease

Gross Income 4.502 39.525 88.61

Expenditure 6.529 7.034 7.18

Gross Profit 2.027 32.491 106.24

Increase (Diminution) in value of

current investments

- - -

Doubtful Debts - - -

Bad debts written off - - -

Loans written off` - - -

Profit after Tax (PAT) / (Loss) 2.027 32.491 106.24

Balance as per last year 72.599 40.108 81.01

Surplus carried to Balance Sheet 70.573 72.599

2.79

Surplus in unrealized Investment

Reserve

292.409 178.426 63.88

Gross Profit on disinvestments - 77.04 100.00

Gross Loss on disinvestment and

w/ offs

- 43.12 100.00

Net Profit on sale of shares - 33.92 100.00 Source: Annual report of APIDC-VCL

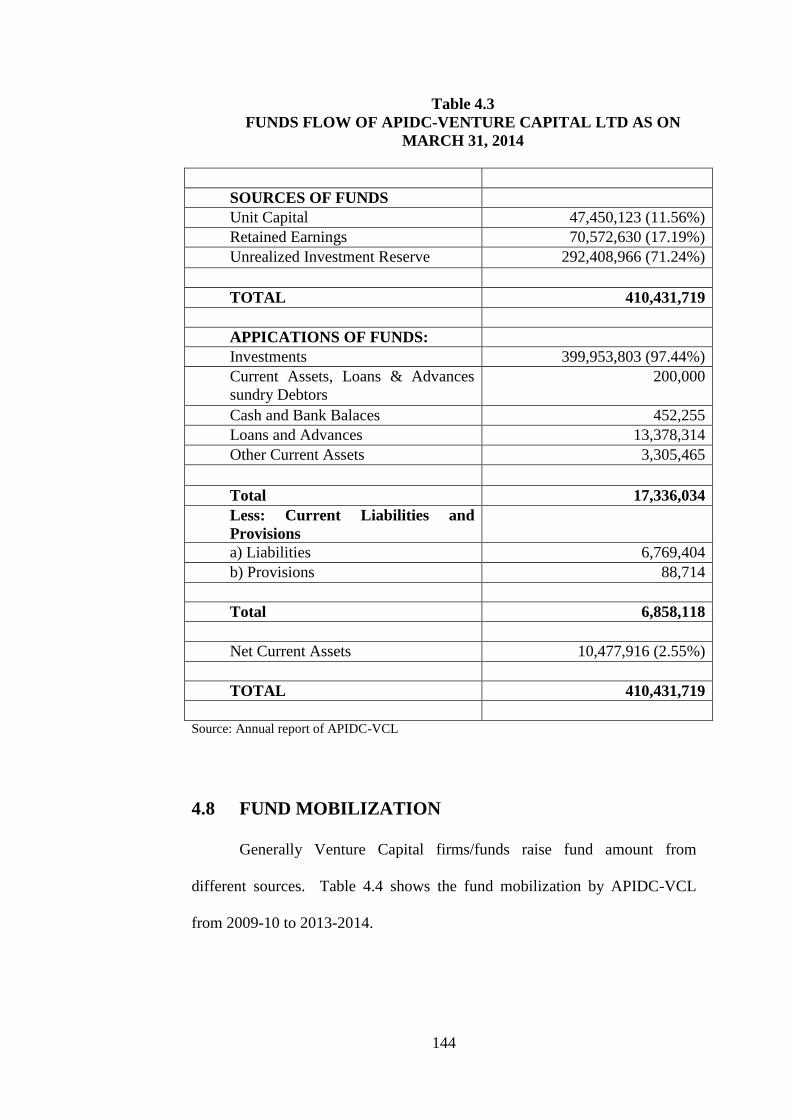

From Table 4.3, it is evident that the sources of funds for APIDC-

Venture Capital Ltd are Unit capital 11.56 percent, Retained earnings 17.19

percent, and Unrealized investment reserve 71.24 percent. On the other hand,

the deployment of the funds was made to investments at 97.44 percent and Net

Current Assets 2.55 percent.

144

Table 4.3

FUNDS FLOW OF APIDC-VENTURE CAPITAL LTD AS ON

MARCH 31, 2014

SOURCES OF FUNDS

Unit Capital 47,450,123 (11.56%)

Retained Earnings 70,572,630 (17.19%)

Unrealized Investment Reserve 292,408,966 (71.24%)

TOTAL 410,431,719

APPICATIONS OF FUNDS:

Investments 399,953,803 (97.44%)

Current Assets, Loans & Advances

sundry Debtors

200,000

Cash and Bank Balaces 452,255

Loans and Advances 13,378,314

Other Current Assets 3,305,465

Total 17,336,034

Less: Current Liabilities and

Provisions

a) Liabilities 6,769,404

b) Provisions 88,714

Total 6,858,118

Net Current Assets 10,477,916 (2.55%)

TOTAL 410,431,719

Source: Annual report of APIDC-VCL

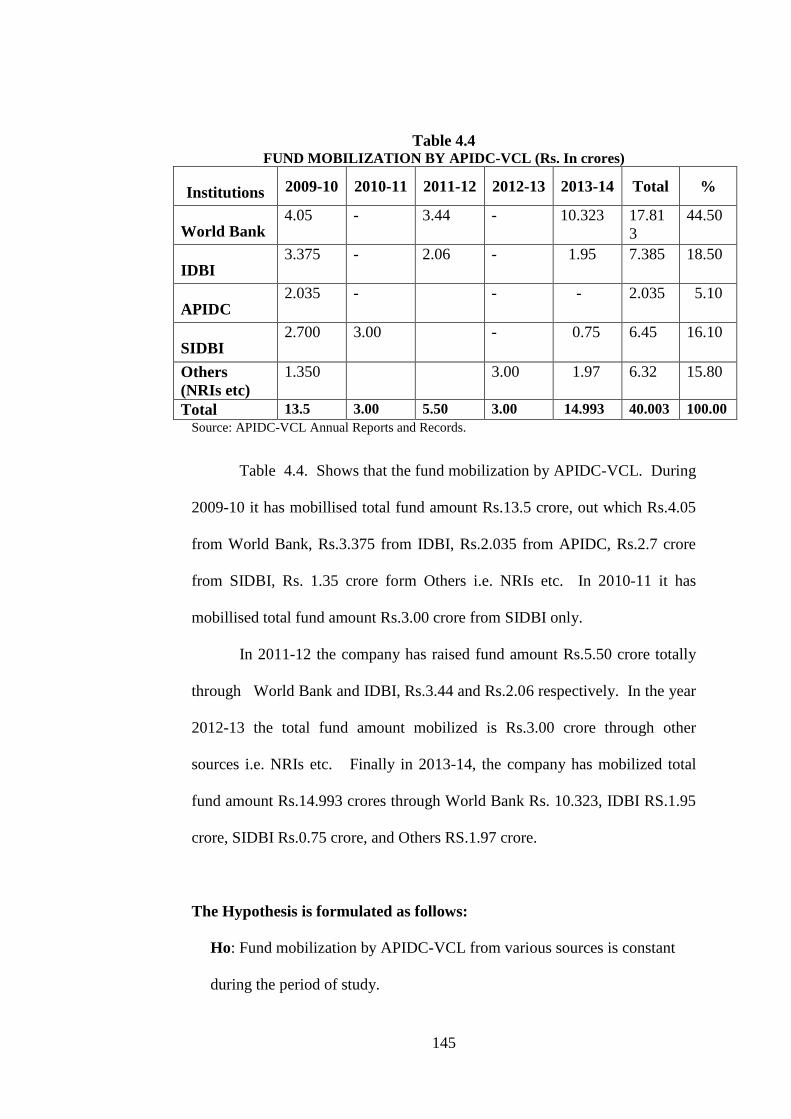

4.8 FUND MOBILIZATION

Generally Venture Capital firms/funds raise fund amount from

different sources. Table 4.4 shows the fund mobilization by APIDC-VCL

from 2009-10 to 2013-2014.

145

Table 4.4 FUND MOBILIZATION BY APIDC-VCL (Rs. In crores)

Institutions 2009-10 2010-11 2011-12 2012-13 2013-14 Total %

World Bank 4.05 - 3.44 - 10.323 17.81

3

44.50

IDBI 3.375 - 2.06 - 1.95 7.385 18.50

APIDC 2.035 - - - 2.035 5.10

SIDBI 2.700 3.00 - 0.75 6.45 16.10

Others

(NRIs etc)

1.350 3.00 1.97 6.32 15.80

Total 13.5 3.00 5.50 3.00 14.993 40.003 100.00

Source: APIDC-VCL Annual Reports and Records.

Table 4.4. Shows that the fund mobilization by APIDC-VCL. During

2009-10 it has mobillised total fund amount Rs.13.5 crore, out which Rs.4.05

from World Bank, Rs.3.375 from IDBI, Rs.2.035 from APIDC, Rs.2.7 crore

from SIDBI, Rs. 1.35 crore form Others i.e. NRIs etc. In 2010-11 it has

mobillised total fund amount Rs.3.00 crore from SIDBI only.

In 2011-12 the company has raised fund amount Rs.5.50 crore totally

through World Bank and IDBI, Rs.3.44 and Rs.2.06 respectively. In the year

2012-13 the total fund amount mobilized is Rs.3.00 crore through other

sources i.e. NRIs etc. Finally in 2013-14, the company has mobilized total

fund amount Rs.14.993 crores through World Bank Rs. 10.323, IDBI RS.1.95

crore, SIDBI Rs.0.75 crore, and Others RS.1.97 crore.

The Hypothesis is formulated as follows:

Ho: Fund mobilization by APIDC-VCL from various sources is constant

during the period of study.

146

Test

Used

Degree of

Freedom

Level of

Significance

Calculated

Value

Table

Value

Result

Chi-

square 16 5 35.42 26.296 Rejected

It shows that the fund mobilization by APIDC-VCL from various

sources is not constant over the study period.

4.9 FUND MOBILIZED TO COMMITMENT

APIDC-VCL has the commitment for fund mobilization from World

Bank, Andhra Bank, IDBI, SIDBI, NRIs and others. Table 4.5 shows the

percentage of fund mobilized to commitment.

Table 4.5 PERCENTAGE OF FUND MOBILIZED TO COMMITMENT

(Rs. In crores)

Year Name of

Institution

Fund

Mobilized Commitment

% of

Mobilization

to

commitment

2008-09 Andhra Bank 1.00 1.50 66.66

2009-10 NRIs 1.657 5.00 33.14

2010-11 NRIs 0.313 5.00 6.26

2011-12

World Bank 5.52 11.52 47.93

IDBI 0.65 3.00 21.66

SIDBI 0.75 3.00 25.00

2012-13 World Bank 4.00 11.52 34.72

2013-14 World Bank

Own Funds

0.80

0.45

11.52

2.25

6.94

20.45

Total 15.14 54.31 27.87

Source: APIDC-VCL Annual Reports

From table 4.5 it can be seen that during the year 2010-11 APIDC-

VCL has mobililsed fund amount Rs. 31.3 lacks from NRI”S out of the

committed fund amount of Rs 5 crores. This stands at 6.26%. In the year

‘2007-08’ the firm has mobilized fund amount Rs. 6.92 crore from World

147

Bank(WB), IDBI, SIDBI at 5.52crores, 0.65 crores and .75 crores

respectively. This year it has mobilized the fund amount out of the

commitment at 47.93 %, 21.66% and 25% from WB, IDBI ,SIDBI

respectively.

In the year 2012-13 APIDC_VCL has mobilised Rs 4 crore at 34.72%

from the committed amount of Rs 11.52 crore from World Bank. During the

year 2013-2014 Rs 1.25 crore amount was mobilised from World Bank and

own funds. In this year they received .0.80 crores from World Bank which is

6.91% of its committed amount of Rs 11.52 crore and also received 0.45 crore

from own funds which amount to 20.45 % of their committed amount of Rs

2.25 crores.

It is inferred that the total fund committed is not fully mobilized by the

APSIDC-VCL from the sources so far as it is slowly moving towards taking

up the new ventures to promote with the principles of risk and return and

sustainability with greater success.

4.10 DISTRIBUTION OF DISBURSEMENT

Finance companies generally disburse the total amount of sanctions

periodically or by installments. It depends on the requirements of investee

firms. Table 4.6 shows the distribution of disbursement of APIDC-VCL.

Table 4.6 APIDC-VCL’S DISTRIBUTION OF DISBURSEMENT

Year No. of

Projects

Equity

(Rs. In crs.)

Loan

(Rs. In crs.)

Total

(Rs. In crs.)

%

2009-10 3 - .60 .60 3.8

2010-11 3 3.25 - 3.25

96.2 2011-12 4 4.30 - 4.30

2012-13 3 4.50 - 4.50

2013-14 4 3.00 - 3.00

Total 17 15.05 .60 15.65 100 Source: APIDC-VCL Annual Reports and Records.

148

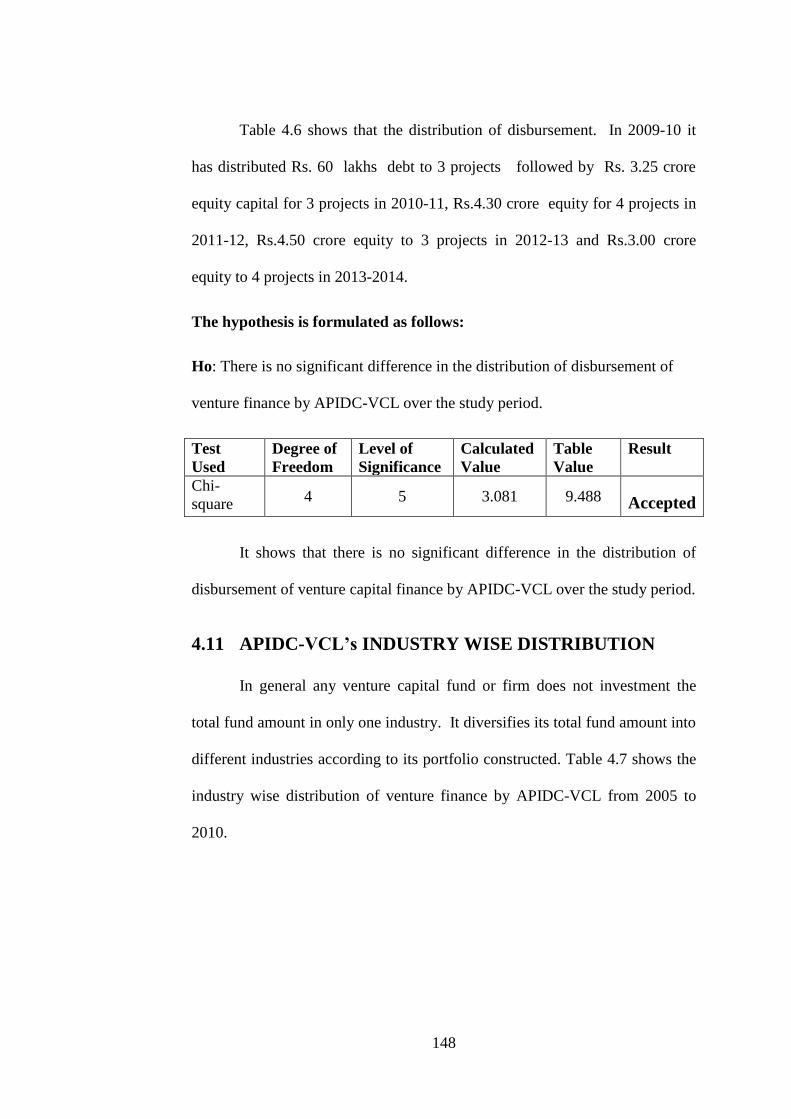

Table 4.6 shows that the distribution of disbursement. In 2009-10 it

has distributed Rs. 60 lakhs debt to 3 projects followed by Rs. 3.25 crore

equity capital for 3 projects in 2010-11, Rs.4.30 crore equity for 4 projects in

2011-12, Rs.4.50 crore equity to 3 projects in 2012-13 and Rs.3.00 crore

equity to 4 projects in 2013-2014.

The hypothesis is formulated as follows:

Ho: There is no significant difference in the distribution of disbursement of

venture finance by APIDC-VCL over the study period.

Test

Used

Degree of

Freedom

Level of

Significance

Calculated

Value

Table

Value

Result

Chi-

square 4 5 3.081 9.488 Accepted

It shows that there is no significant difference in the distribution of

disbursement of venture capital finance by APIDC-VCL over the study period.

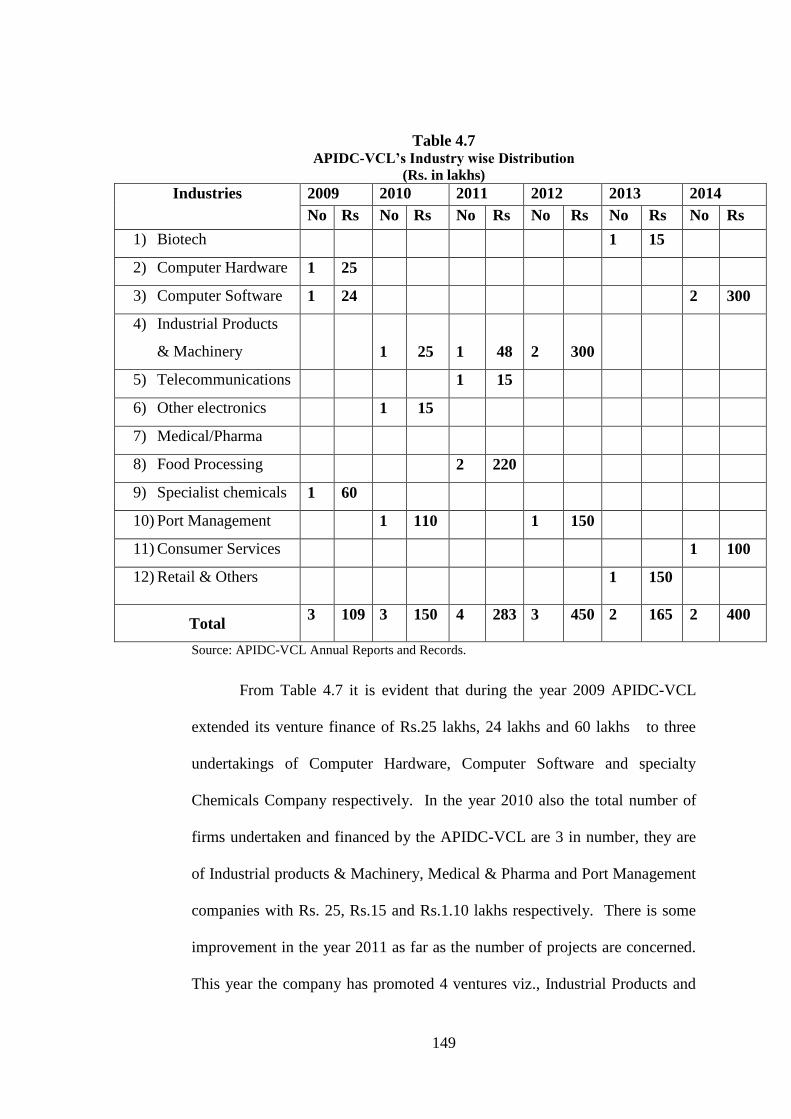

4.11 APIDC-VCL’s INDUSTRY WISE DISTRIBUTION

In general any venture capital fund or firm does not investment the

total fund amount in only one industry. It diversifies its total fund amount into

different industries according to its portfolio constructed. Table 4.7 shows the

industry wise distribution of venture finance by APIDC-VCL from 2005 to

2010.

149

Table 4.7 APIDC-VCL’s Industry wise Distribution

(Rs. in lakhs)

Industries 2009 2010 2011 2012 2013 2014

No Rs No Rs No Rs No Rs No Rs No Rs

1) Biotech 1 15

2) Computer Hardware 1 25

3) Computer Software 1 24 2 300

4) Industrial Products

& Machinery

1

25

1

48

2

300

5) Telecommunications 1 15

6) Other electronics 1 15

7) Medical/Pharma

8) Food Processing 2 220

9) Specialist chemicals 1 60

10) Port Management 1 110 1 150

11) Consumer Services 1 100

12) Retail & Others

1 150

Total 3 109 3 150 4 283 3 450

2 165 2 400

Source: APIDC-VCL Annual Reports and Records.

From Table 4.7 it is evident that during the year 2009 APIDC-VCL

extended its venture finance of Rs.25 lakhs, 24 lakhs and 60 lakhs to three

undertakings of Computer Hardware, Computer Software and specialty

Chemicals Company respectively. In the year 2010 also the total number of

firms undertaken and financed by the APIDC-VCL are 3 in number, they are

of Industrial products & Machinery, Medical & Pharma and Port Management

companies with Rs. 25, Rs.15 and Rs.1.10 lakhs respectively. There is some

improvement in the year 2011 as far as the number of projects are concerned.

This year the company has promoted 4 ventures viz., Industrial Products and

150

machinery, Tele communication and Food Processing with Rs.48, Rs.15, and

Rs.2.20 lakhs respectively.

During 2012 the company has promoted 3 units out of which 2 are

related to Industrial products and machinery and the remaining one is related

to port management with Rs.300 lakhs and 150 lakhs respectively.

In 2013 it has promoted 2 projects of Biotech and retail and other

industries with Rs.15 lakhs and 150 lakhs respectively. Hence during the year

2014 the company has promoted two projects – one in computer software and

the other one in consumer services with Rs.300 lakhs and Rs.100 lakhs

respectively.

During the period of the study APIDC-VCL’s Venture Capital is

attracted by Industraial Product and Manufacturing industry followed by

Computer Software industry, Food processing industry, Port Management to

the maximum extent and followed by other industries as shown.

The hypothesis is framed as follows

Ho: The Industrial distribution of number of projects and venture capital

finance by APIDC-VCL is constant over the study period.

Particulars Test

Used

Degree

of

Freedom

Level of

Significance

Calculated

Value

Table

Value

Result

Projects Chi-

square

55 5 77.09 73.3 Rejected

Finance Chi-

square

55 5 5961.762 73.3 Rejected

It shows that the industrial distribution of number of projects and

venture capital finance by APIDC-VCL is significantly different in all the

years of the study period.

151

4.12 FINANCING BY INVESTMENT STAGE

There are broadly five stages of finance under venture capital financing

unlike in traditional finance as Seed stage, Start-Up stage, Later stage, Other

Early stage and Turnaround Financing. Table 4.8 reveals the financing by

investment stage from 2009 to 2014 financial years

Table 4.8

APIDC-VCL’S FINANCING BY INVESTMENT STAGE

(Rs. in lakhs)

Investment

Stage

2009 2010 2011 2012 2013 2014

Rs. No. Rs. No. Rs. No. Rs. No. Rs. No. Rs. No.

Seed Stage 9.04 1 50.0 1 10 1

Start-Up

Stage

5.0 1 0.90 1 50.0 1 130.5 1 140.27 2

Later Stage 35.0 1 163.48 2 260 3 193.0 4 83.8 2

Other Early

Stage

Turnaround

Financing

60.0 1 50.0 1

TOTAL 65.0 2 94.94 4 263.48 4 270 4 323.5 5 224.08 4 Source: APIDC-VCL Annual Reports and Records.

Table 4.8 shows APIDC-VCL’s financing by investment stage is

covered by 5 different stages namely Seed Stage, Start-Up Stage, Later Stage,

Other Early Stage and Turnaround Financing. During the study period it has

financed 3 ventures at seed stage in 2010, 2011 and 2012 by Rs. 9.04,

Rs.50.00 and 10.00 lakhs respectively.

Ventures financed at Start-Up stage were totally 6 as in 2009, 2010,

2011, 2013 and 2014 with the amount of Rs. 50.00 lakhs, Rs.0.9 lakhs, Rs.50

lakhs, Rs.130.5 lakhs and Rs.140.27 lakhs respectively.

On the other hand ventures financed at Later Stage were totally 12 as

one in 2010, two in 2011, three in 2012, four in 2013 and remaining two in

152

2014 with Rs. 35 lakhs, Rs.163.48 lakhs, Rs.260.00 lakhs, Rs.193.00 lakhs

and Rs.83.8 lakhs respectively.

At the stage of Turnaround financing, two ventures were financed

totally as one in 2009 and the remaining one in 2010 with the total

disbursement of Rs. 60 lakhs and Rs.50 lakhs respectively. Hence there were

no ventures at other early stage during the study period.

The hypothesis is framed as follows:

Ho: There is no significant difference in the number of projects and finance

provided to undertakings at different stages of finance by APIDC-VCL

over the period of the study.

Particulars Test

Used

Degree of

Freedom

Level of

Significance

Calculated

Value

Table

Value

Result

Projects Chi-

square

20 5 13.272 31.4 Accepted

Finance Chi-

square

20 5 1288 31.4 Rejected

It shows that there is no significant difference in number of projects

and a significant difference in finance provided by APIDC-VCL at different

stages of finance to investee companies over the study period.

4.13 REGION WISE-DISTRIBUTION

Venture capital firms/funds won’t confine themselves to a particular

geographical area. Because where they can find an opportunity there they can

invest the money. Table 4.8 shows APIDC-VCL’s Region wise projects and

investment distribution.

153

Table 4.9

APIDC-VCL REGION WISE-DISTRIBUTION

(Rs. In millions)

Source: APIDC-VCL Annual Reports and Records.

Table 4.9 shows the region wise distribution of venture capital by

APIDC-VCL during the study period. It has promoted 2 projects with Rs.49

lakhs, 3 projects with Rs.150 lakhs, 4 projects with Rs. 283 lakhs, 2 projects

with Rs.165 lakhs and finally 2 projects with Rs.400 lakhs in 2009, 2010,

2011, 2012.2013 and 2014 respectively in Southern part of India. On the

other hand it has promoted only 1 project in Eastern part of India in 2012 with

Rs.150 lakhs.

In western part of India the company has promoted 1 project with Rs.

60 lakhs in 2009 and 2 projects with Rs.300 lakhs in 2012. However there are

no projects promoted by APIDC-VCL in North India so far.

The Hypothesis is formulated as follows:

Ho: There is no significant difference in the distribution of number of projects

and venture finance provided to investees’ by APIDC-VCL in the four

regions of India.

Region 2009 2010 2011 2012 2013 2014

No. Rs. No. Rs. No. Rs. No. Rs. No. Rs. No. Rs.

South

2

49

3

150

4

283

-

-

2

165

2

400

East - - - - - - 1 150 - - - -

North - - - - - - - - - - - -

West

1

60 -

- -

- 2

300 - - - -

Total 3 109 3 150 4

283 3 450 2 165 2 400

154

Particulars Test

Used

Degree

of

Freedom

Level of

Significance

Calculated

Value

Table

Value

Result

Projects Chi-

square

20 5 13.272 31.4 Accepted

Finance Chi-

square

20 5 1288 31.4 Rejected

This shows that the region wise distribution of projects and finance

provided by APIDC-VCL is very significant in the four regions of India.

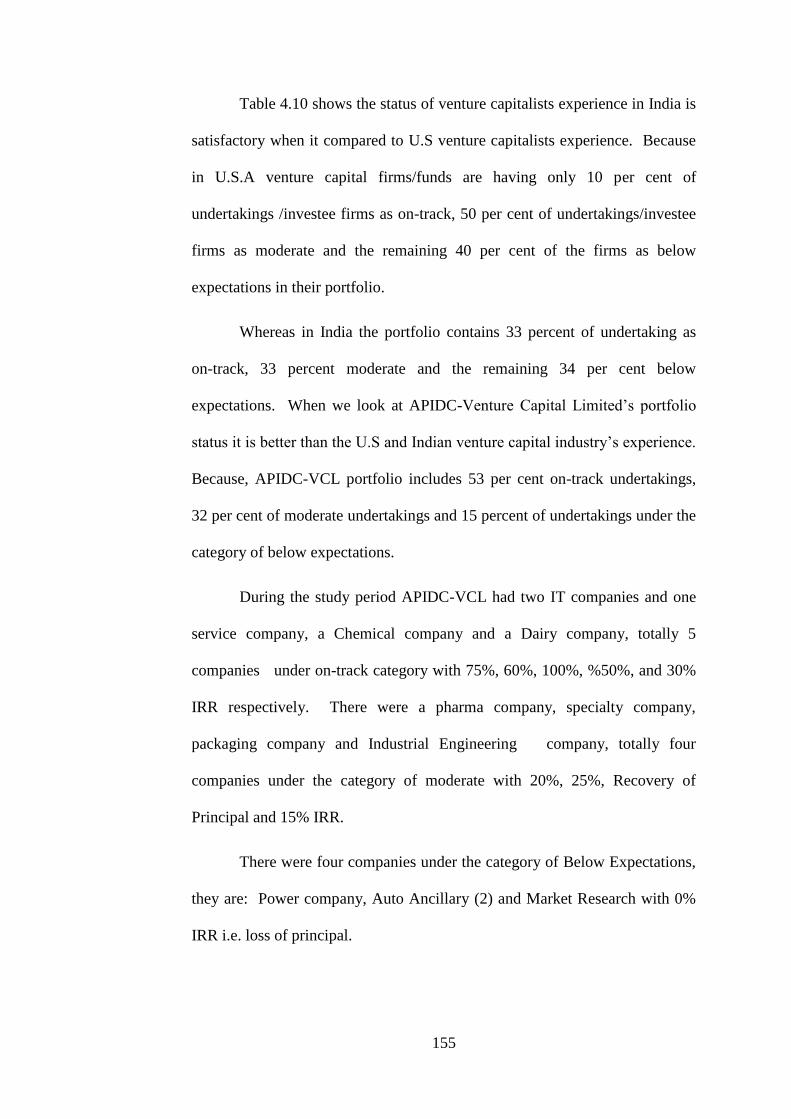

4.14 STATUS OF PORTFOLIO COMPANIES

Portfolio is the combination of financial assets, in general all the

venture capital funds maintain a well-designed portfolio with a good balance

of different industries while performing the investment activity, on which the

success of the company depends. Table 6.8 shows status of APIDC-VCL’s

portfolio companies.

Table 4.10 STATUS OF APIDC-VCL’S PORTFOLIO COMPANIES

ON-TRACK MODERATE

BELOW

EXPECTATIONS

U.S VC’s

Experience

10% 50% 40%

Indian VC’s

Experience

33% 33% 34%

APICC-VCL 53% 32% 15%

COMPANIES OF

APSIDC-VCL (

IRR)

1. IT Company

(75%)

1. Pharma Company

(20%)

1. Power Company ((0%)

(Loss of Principal)

2.Service

Company (60%)

2. Specialty

Company (25%)

2. Auto Ancillary (0%)

(Loss of Principal)

3. IT Company

(100%)

3. Packaging

Company

(Return of Principal)

3. Market Research (0%)

(Loss of Principal)

4. Chemical

Company(50%)

4. Industrial

Engineering (15%)

4. Auto Ancillary (0%)

(Loss of Principal)

5. Dairy

Company

(30%)

Source: APIDC-VCL Annual Reports and Records.

155

Table 4.10 shows the status of venture capitalists experience in India is

satisfactory when it compared to U.S venture capitalists experience. Because

in U.S.A venture capital firms/funds are having only 10 per cent of

undertakings /investee firms as on-track, 50 per cent of undertakings/investee

firms as moderate and the remaining 40 per cent of the firms as below

expectations in their portfolio.

Whereas in India the portfolio contains 33 percent of undertaking as

on-track, 33 percent moderate and the remaining 34 per cent below

expectations. When we look at APIDC-Venture Capital Limited’s portfolio

status it is better than the U.S and Indian venture capital industry’s experience.

Because, APIDC-VCL portfolio includes 53 per cent on-track undertakings,

32 per cent of moderate undertakings and 15 percent of undertakings under the

category of below expectations.

During the study period APIDC-VCL had two IT companies and one

service company, a Chemical company and a Dairy company, totally 5

companies under on-track category with 75%, 60%, 100%, %50%, and 30%

IRR respectively. There were a pharma company, specialty company,

packaging company and Industrial Engineering company, totally four

companies under the category of moderate with 20%, 25%, Recovery of

Principal and 15% IRR.

There were four companies under the category of Below Expectations,

they are: Power company, Auto Ancillary (2) and Market Research with 0%

IRR i.e. loss of principal.

156

4.15 MANAGEMENT FEE

Unlike the traditional financing the venture financing organizations

collect some amount of money from the investee as in the form of

management fee for their managerial services. In fact which stands a

significant part of the total income. Table 4.10 shows the Management fee

collected by APIDC-VCL

Table 4.11

Management Fee

Source: APIDC-VCL Annual Reports

Table 4.11 shows the Management Fee that is earned by APIDC-VCL

through managerial services provided to its investee firms. During the year

2008-09 the company has earned income through management fee

Rs.7, 39,612, which is 94.6 per cent of the total income. In 2009-10 it is 86

per cent, in 2011-12 it is 91.5 per cent, in 2012-13 it is 62.6 per cent, in 2012-

13 it is 52.9 per cent and in 2013-14 it is 52.6 per cent of total income.

4.16 DIVIDEND ON INVESTMENTS

Dividend on investments is the ultimate returns of the company.

Generally when the investee firms commercially succeeds in the market and

generates some profits then they offer dividend to the venture capitalist.

Year (Rs.) % Total Income

2008-09 7,39,612 94.6

2009-10 12,11,276 86.0

2010-11 12,20,970 91.5

2011-12 39,08,475 62.6

2012-13 51,08,475 52.9

2013-14 47,88,000 52.6

157

Table 4.11 shows the dividend received by APIDC-VCL from its investee

companies from 2008-09 to 2013-14.

Table 4.12 DIVIDEND ON INVESTMENTS

(Rs. in lakhs)

Year Dividend in (Rs.in lakhs)

2008-09 -

2009-10 1,60,970

2010-11 4,20,004

2011-12 3,31,667

2012-13 2,55,898

2013-14 25,83,312

Source: APIDC-VCL Annual Reports

The table 4.12 shows the Dividend received by APIDC-VCL on its

investments during the study period. In 2008-09 there is no dividend received

by the company. In 2009-10 Dividend was Rs. 1,60,970, in 2010-11

Rs. 4,20,004, in 2011-12 Rs. 3,31,667, in 2012-13 Rs. 2,55,898 and in

2013-14 Rs. 25,83,312. It is found that as the business operations and number

of undertakings increased to APIDC-VCL the management fee in totally also

increased very significantly.