apm® : the new amcc phenomenal products, explosive growth

TRANSCRIPT

1 © AppliedMicro Proprietary & Confidential © AppliedMicro 2013 Proprietary & Confidential

APM® : The new AMCC Phenomenal Products, Explosive Growth

May 2013

Jefferies 2013 Global Technology Media & Telecom

2 © AppliedMicro Proprietary & Confidential © AppliedMicro 2013 Proprietary & Confidential

Safe Harbor Forward Looking Statements During the course of this presentation, we will discuss our anticipated future financial performance and make other forward-looking statements, including “street estimates” that are comprised of reported analyst estimates compiled by the Company. Actual results may differ materially from these statements due to a number of risks and uncertainties, including, but not limited to customer demand for our products, the successful and timely development of new products, internal and external manufacturing execution, the business of the Company’s major customers and macro economic conditions. For a more detailed discussion of these and other factors, we refer you to our SEC filings.

Regulation G Reconciliation During the course of this presentation, we may refer to historical and forward-looking non-GAAP financial measures. A reconciliation of historical non-GAAP financial measures with the most directly comparable GAAP financial measures can be found on our web site at http://www.amcc.com in the “Investor Relations” section. We have not provided a reconciliation of

forward-looking non-GAAP financial measures due to the difficulty in forecasting and quantifying the amounts that would be required to be included in the comparable GAAP measure that are dependent upon future market conditions and valuations.

THIS PRESENTATION DOES NOT CONSTITUE AN OFFER TO SELL OR A SOLICITATION OF AN OFFER TO BUY ANY SHARES OR OTHER SECURITIES OF THE COMPANY IN ANY JURISDICTION. WHILE THE INFORMATION PRESENTED IS BELIEVED TO BE ACCURATE AND COMPLETE AS OF THE DATE OF THIS PRESENTATION, NO WARRANTIES OF ANY KIND, EITHER EXPRESS OR IMPLIED, ARE MADE. ALL MATERIALS PRESENTED IN THIS PRESENTATION ARE THE PROPERTY OF THE COMPANY AND ARE PROECTED BY U.S. AND INTERNAIONAL COPYRIGHT, TRADEMARK AND OTHER APPLICABLE LAWS. APPPLIED MICRO, APM, ARMING THE CLOUD, SERVER ON A CHIP, CLOUD SERVER AND X-GENE ARE REGISTERED TRADEMARKS OR TRADEMARKS OF APPLIED MICRO CIRCUITS CORPORATION.

3 © AppliedMicro Proprietary & Confidential © AppliedMicro 2013 Proprietary & Confidential

October 2011: APM is “Arming the Cloud ”

Revolutionary Cloud Product Portfolio

From Fiber to Backplane

Disruptive Computing

World’s first ARM 64-bit Server on a Chip

Total Addressable Market Expands to $7.3B

The Capability Is In Our DNA

TM

3

4 © AppliedMicro Proprietary & Confidential

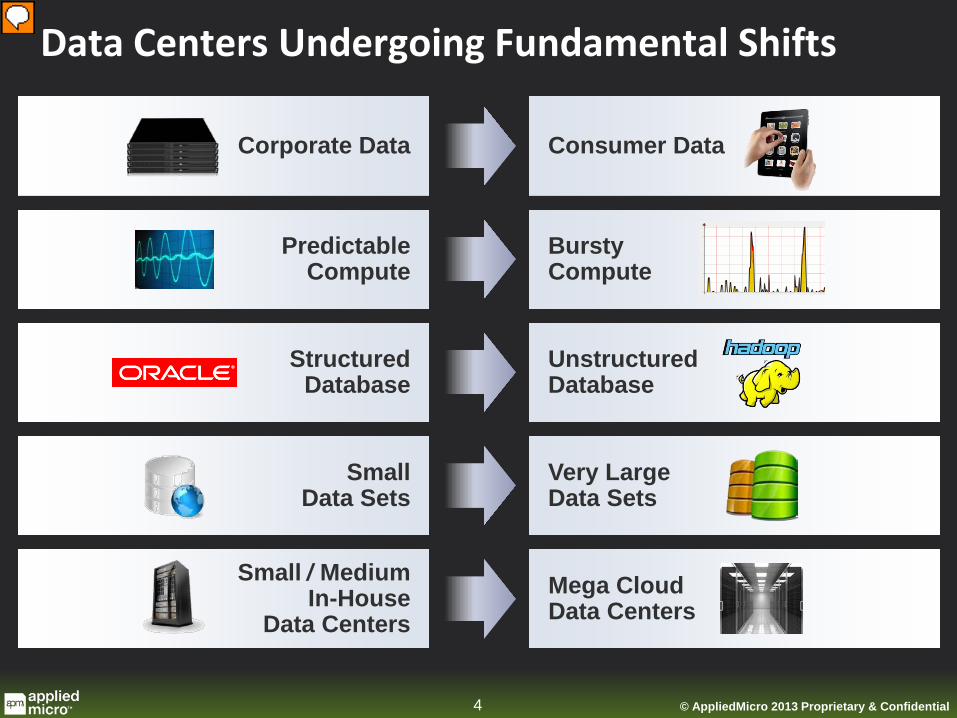

Small Data Sets

Very Large Data Sets

Data Centers Undergoing Fundamental Shifts

Consumer Data Corporate Data

Predictable Compute

Bursty Compute

Structured Database

Unstructured Database

Mega Cloud Data Centers

Small / Medium In-House

Data Centers

© AppliedMicro 2013 Proprietary & Confidential 4

5 © AppliedMicro Proprietary & Confidential

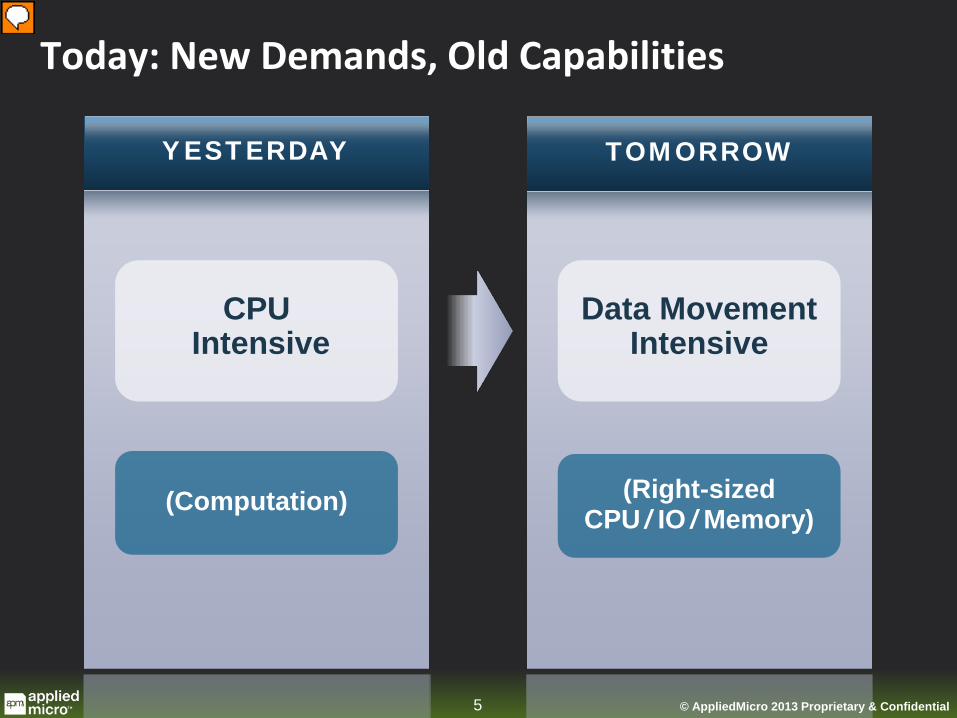

Today: New Demands, Old Capabilities

CPU Intensive

YESTERDAY TOMORROW

(Computation)

(Right-sized CPU / IO / Memory)

Data Movement Intensive

© AppliedMicro 2013 Proprietary & Confidential 5

6 © AppliedMicro Proprietary & Confidential

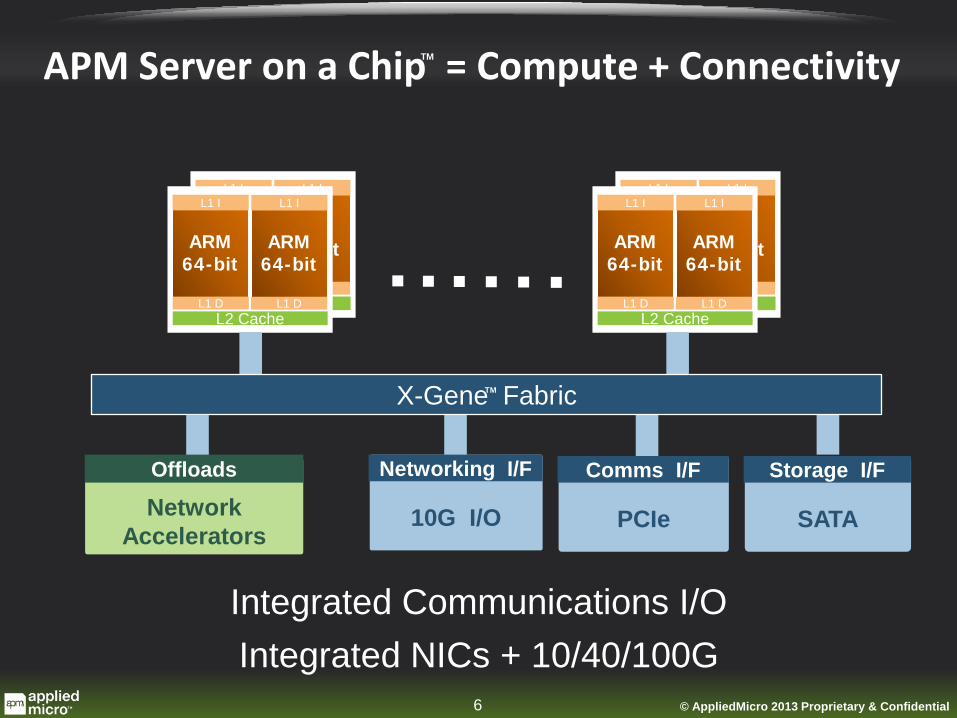

L2 Cache

ARM 64-bit

L1 D

L1 I

ARM 64-bit

L1 D

L1 I

L2 Cache

ARM 64-bit

L1 D

L1 I

ARM 64-bit

L1 D

L1 I

L2 Cache

ARM 64-bit

L1 D

L1 I

ARM 64-bit

L1 D

L1 I

L2 Cache

ARM 64-bit

L1 D

L1 I

ARM 64-bit

L1 D

L1 I

SATA

Storage I/F

PCIe

Comms I/F

10G I/O

Networking I/F

Integrated NICs + 10/40/100G Integrated Communications I/O

X-Gene Fabric

Network

Accelerators

Offloads

APM Server on a Chip = Compute + Connectivity

© AppliedMicro 2013 Proprietary & Confidential

TM

TM

6

7 © AppliedMicro Proprietary & Confidential © AppliedMicro 2013 Proprietary & Confidential

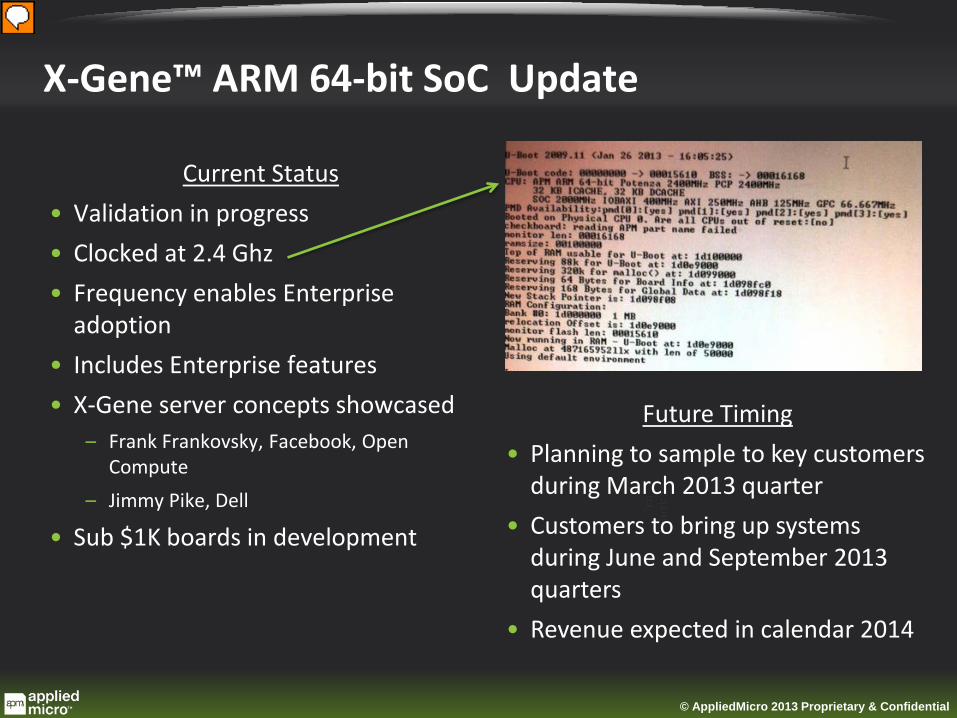

X-Gene™ ARM 64-bit SoC Update

Current Status • Validation in progress • Clocked at 2.4 Ghz • Frequency enables Enterprise

adoption • Includes Enterprise features • X-Gene server concepts showcased

– Frank Frankovsky, Facebook, Open Compute

– Jimmy Pike, Dell

• Sub $1K boards in development

Future Timing • Planning to sample to key customers

during March 2013 quarter • Customers to bring up systems

during June and September 2013 quarters

• Revenue expected in calendar 2014

8 © AppliedMicro Proprietary & Confidential © AppliedMicro 2013 Proprietary & Confidential

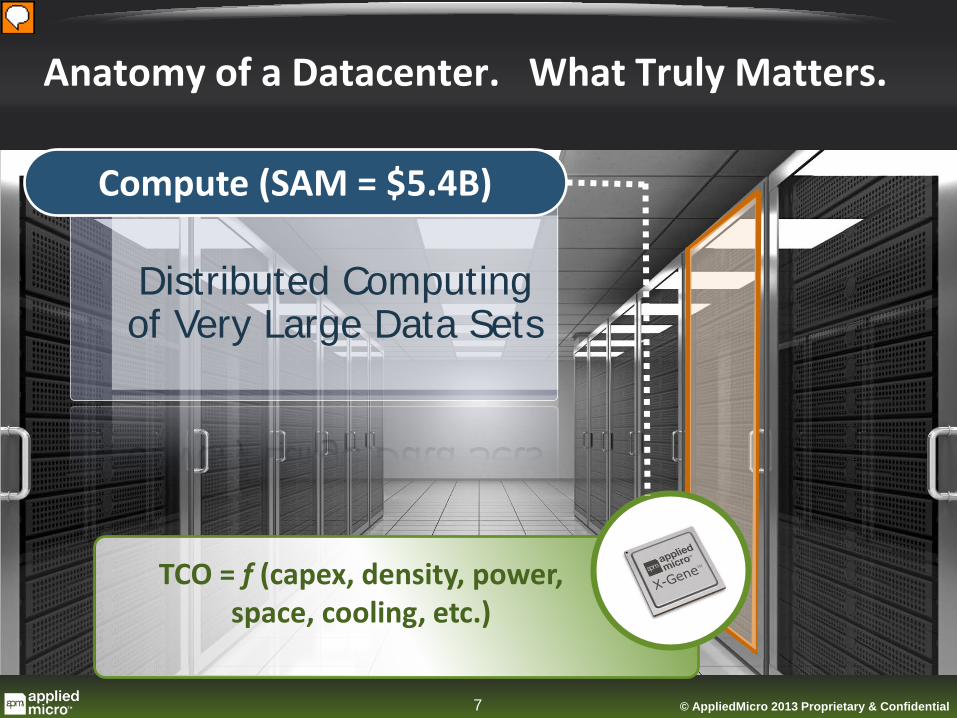

Anatomy of a Datacenter. What Truly Matters.

Compute (SAM = $5.4B)

Distributed Computing of Very Large Data Sets

TCO = f (capex, density, power, space, cooling, etc.)

7

9 © AppliedMicro Proprietary & Confidential © AppliedMicro 2013 Proprietary & Confidential

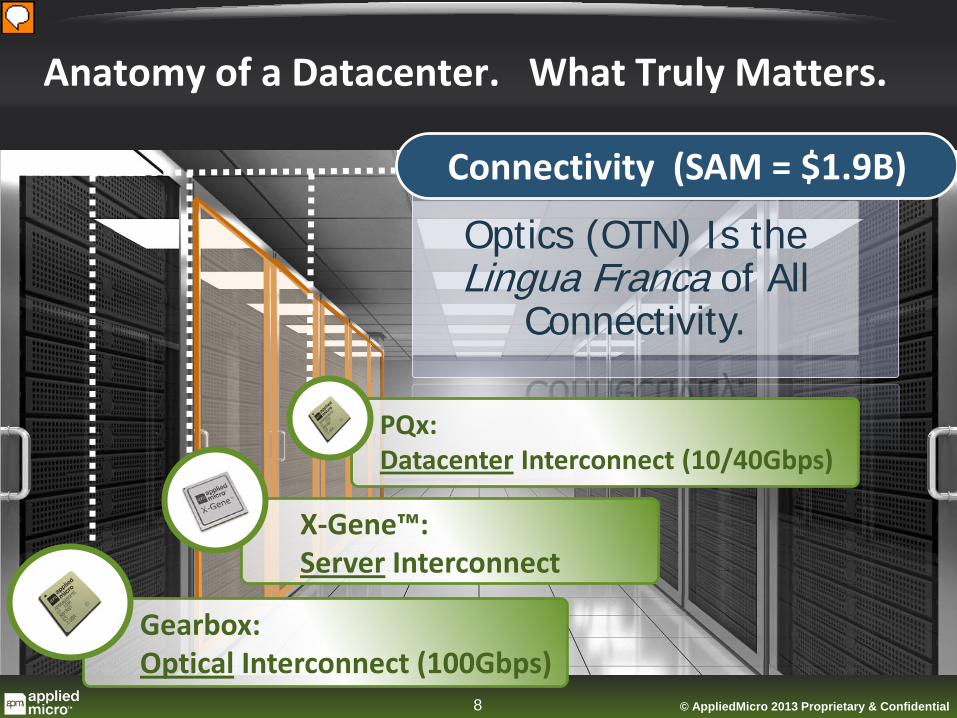

Anatomy of a Datacenter. What Truly Matters.

Connectivity (SAM = $1.9B)

Optics (OTN) Is the Lingua Franca of All

Connectivity.

Gearbox: Optical Interconnect (100Gbps)

PQx: Datacenter Interconnect (10/40Gbps)

X-Gene™: Server Interconnect

8

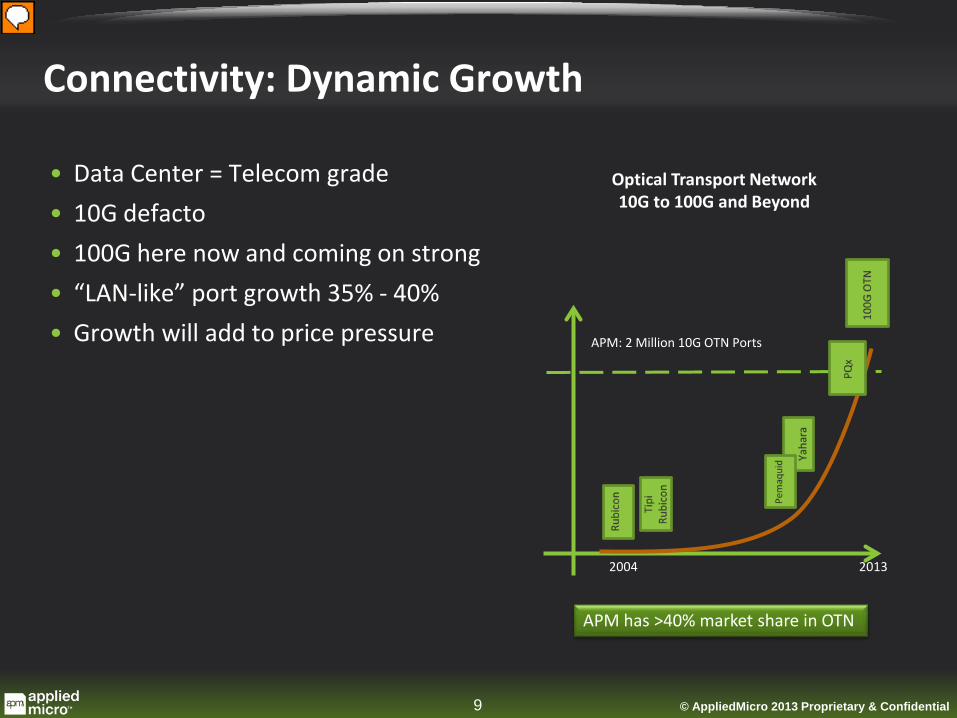

10 © AppliedMicro Proprietary & Confidential © AppliedMicro 2013 Proprietary & Confidential

Connectivity: Dynamic Growth

• Data Center = Telecom grade • 10G defacto • 100G here now and coming on strong • “LAN-like” port growth 35% - 40% • Growth will add to price pressure APM: 2 Million 10G OTN Ports

2004 2013

Optical Transport Network 10G to 100G and Beyond

APM has >40% market share in OTN

9

11 © AppliedMicro Proprietary & Confidential

*new

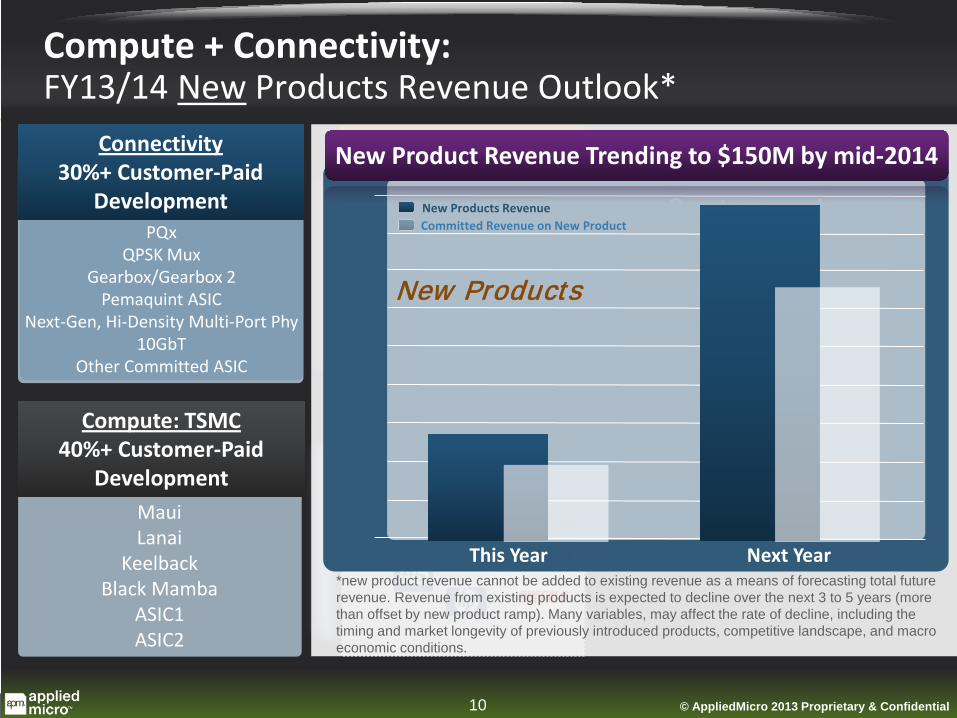

Compute + Connectivity: FY13/14 New Products Revenue Outlook*

Connectivity 30%+ Customer-Paid

Development

Compute: TSMC 40%+ Customer-Paid

Development

Market Leaders

This Year Next Year

New Products Revenue Committed Revenue on New Product

New Products

PQx QPSK Mux

Gearbox/Gearbox 2 Pemaquint ASIC

Next-Gen, Hi-Density Multi-Port Phy 10GbT

Other Committed ASIC

Maui Lanai

Keelback Black Mamba

ASIC1 ASIC2

New Product Revenue Trending to $150M by mid-2014

*new product revenue cannot be added to existing revenue as a means of forecasting total future revenue. Revenue from existing products is expected to decline over the next 3 to 5 years (more than offset by new product ramp). Many variables, may affect the rate of decline, including the timing and market longevity of previously introduced products, competitive landscape, and macro economic conditions.

10 © AppliedMicro 2013 Proprietary & Confidential

12 © AppliedMicro Proprietary & Confidential

Financial Details

April 2013 CFO Report

11 © AppliedMicro 2013 Proprietary & Confidential

13 © AppliedMicro Proprietary & Confidential

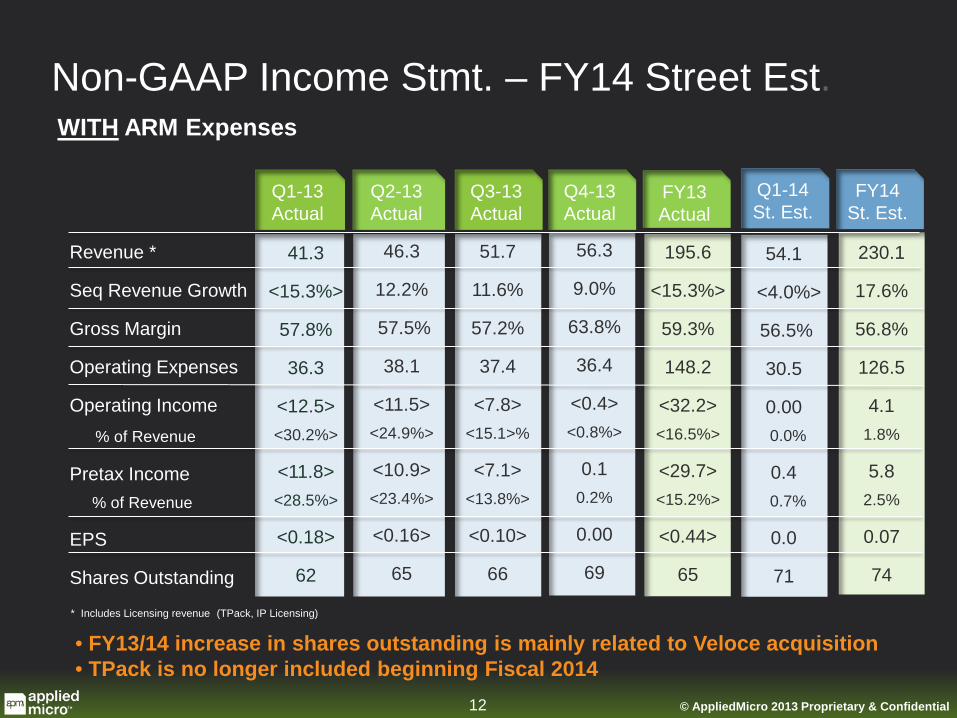

Non-GAAP Income Stmt. – FY14 Street Est.

• FY13/14 increase in shares outstanding is mainly related to Veloce acquisition • TPack is no longer included beginning Fiscal 2014

* Includes Licensing revenue (TPack, IP Licensing)

Revenue *

Seq Revenue Growth

Gross Margin

Operating Expenses

Operating Income % of Revenue

Pretax Income % of Revenue

EPS

Shares Outstanding

Q1-13 Actual

FY14 St. Est.

54.1

<4.0%>

56.5%

30.5

0.00 0.0%

0.4 0.7%

0.0

71

WITH ARM Expenses

41.3

<15.3%>

57.8%

36.3

<12.5> <30.2%>

<11.8> <28.5%>

<0.18>

62

46.3

12.2%

57.5%

38.1

<11.5> <24.9%>

<10.9> <23.4%>

<0.16>

65

51.7

11.6%

57.2%

37.4

<7.8> <15.1>%

<7.1> <13.8%>

<0.10>

66

195.6

<15.3%>

59.3%

148.2

<32.2> <16.5%>

<29.7> <15.2%>

<0.44>

65

Q2-13 Actual

Q3-13 Actual

Q4-13 Actual

Q1-14 St. Est.

12 © AppliedMicro 2013 Proprietary & Confidential

195.3

<15.4%>

58.1%

146.3

<32.9> <16.8%>

<30.3> <15.5%>

<0.45>

65

FY13 Actual

230.1

17.6%

56.8%

126.5

4.1 1.8%

5.8 2.5%

0.07

74

56.3

9.0%

63.8%

36.4

<0.4> <0.8%>

0.1 0.2%

0.00

69

14 © AppliedMicro Proprietary & Confidential

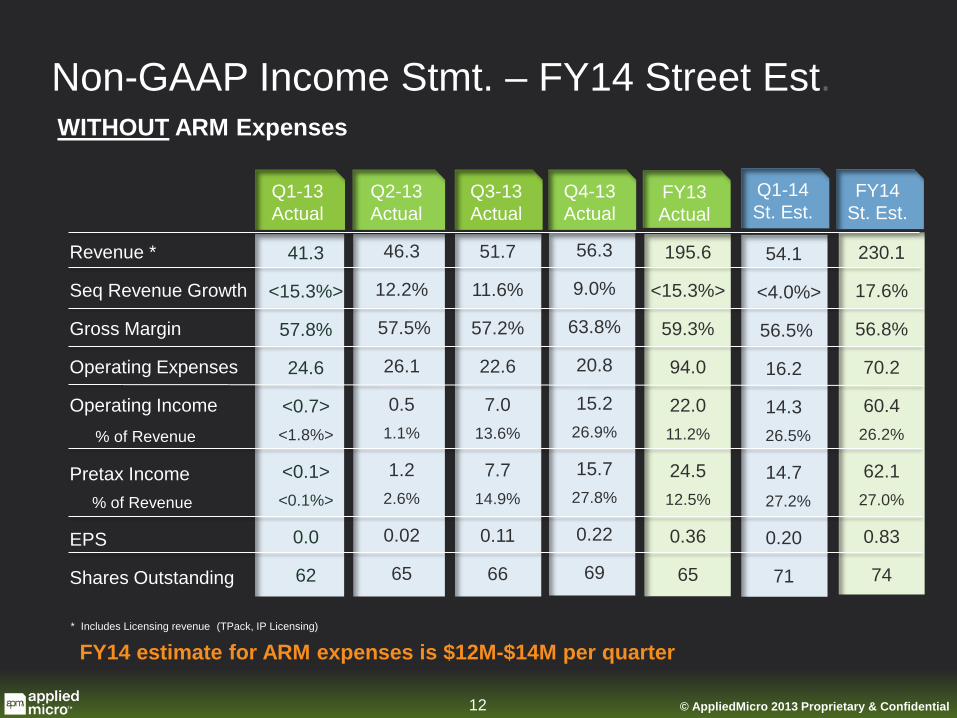

Non-GAAP Income Stmt. – FY14 Street Est.

* Includes Licensing revenue (TPack, IP Licensing)

Revenue *

Seq Revenue Growth

Gross Margin

Operating Expenses

Operating Income % of Revenue

Pretax Income % of Revenue

EPS

Shares Outstanding

Q1-13 Actual

FY14 St. Est.

54.1

<4.0%>

56.5%

16.2

14.3 26.5%

14.7 27.2%

0.20

71

WITHOUT ARM Expenses

41.3

<15.3%>

57.8%

24.6

<0.7> <1.8%>

<0.1> <0.1%>

0.0

62

46.3

12.2%

57.5%

26.1

0.5 1.1%

1.2 2.6%

0.02

65

51.7

11.6%

57.2%

22.6

7.0 13.6%

7.7 14.9%

0.11

66

195.6

<15.3%>

59.3%

94.0

22.0 11.2%

24.5 12.5%

0.36

65

Q2-13 Actual

Q3-13 Actual

Q4-13 Actual

Q1-14 St. Est.

12 © AppliedMicro 2013 Proprietary & Confidential

195.3

<15.4%>

58.1%

146.3

<32.9> <16.8%>

<30.3> <15.5%>

<0.45>

65

FY13 Actual

230.1

17.6%

56.8%

70.2

60.4 26.2%

62.1 27.0%

0.83

74

56.3

9.0%

63.8%

20.8

15.2 26.9%

15.7 27.8%

0.22

69

FY14 estimate for ARM expenses is $12M-$14M per quarter

15 © AppliedMicro Proprietary & Confidential

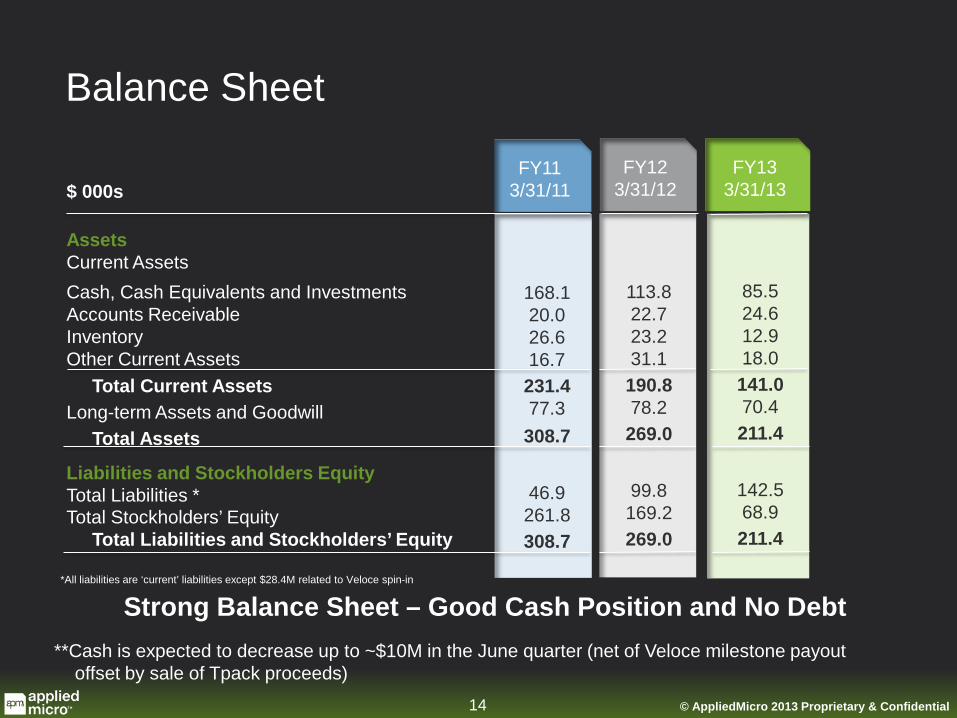

Assets Current Assets Cash, Cash Equivalents and Investments Accounts Receivable Inventory Other Current Assets Total Current Assets Long-term Assets and Goodwill Total Assets

Liabilities and Stockholders Equity Total Liabilities * Total Stockholders’ Equity Total Liabilities and Stockholders’ Equity

*All liabilities are ‘current’ liabilities except $28.4M related to Veloce spin-in

$ 000s

Balance Sheet

Strong Balance Sheet – Good Cash Position and No Debt

FY13 3/31/13

FY11 3/31/11

85.5 24.6 12.9 18.0 141.0 70.4 211.4

142.5 68.9 211.4

FY12 3/31/12

168.1 20.0 26.6 16.7 231.4 77.3 308.7

46.9 261.8 308.7

113.8 22.7 23.2 31.1 190.8 78.2 269.0

99.8 169.2 269.0

**Cash is expected to decrease up to ~$10M in the June quarter (net of Veloce milestone payout offset by sale of Tpack proceeds) 14 © AppliedMicro 2013 Proprietary & Confidential