apple corporation sample accounts receivable subsidiary ledger total due acme $ 10,000 baxter 50,000...

TRANSCRIPT

Apple Corporation Sample Accounts Receivable

Subsidiary Ledger Total Due

Acme $ 10,000Baxter 50,000Jones 15,000Martin 20,000Smith 5,000

$100,000 Gross Accounts

ReceivableLO1

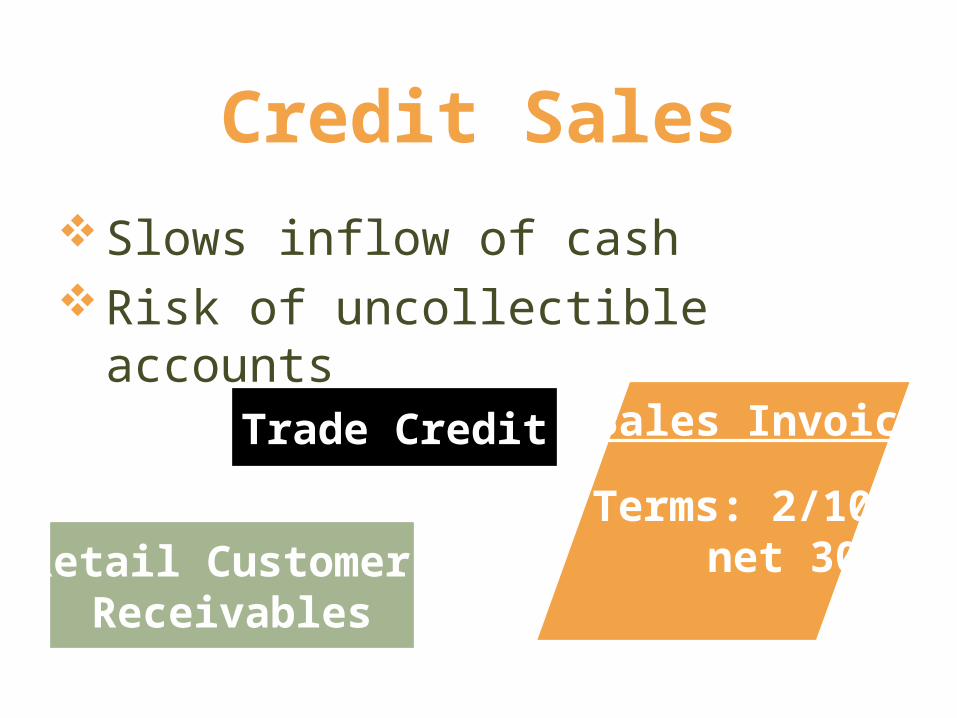

Credit SalesSlows inflow of cashRisk of uncollectible accounts

Trade Credit

Retail Customer Receivables

Terms: 2/10, net 30

Sales Invoice

Accounting for Bad Debts:Direct Write-off Method

Journal entry to record write-off in period determinedto be uncollectible:

Bad Debts Expense XXXAccounts Receivable—Dexter XXX

Period of sale Future period chargedwith expense of bad debtwrite-off

Accounting for Bad Debts: Allowance Method

Period of saleEstimated bad debt expense (and allowance account) recorded in the same period

Accounting for Bad Debts:Allowance Method

Journal entry to record estimated bad debtexpense in period of sale:

Bad Debts Expense XXXAllowance for Doubtful Accounts XXX

I estimate...

Partial Balance Sheet

Accounts receivable $xxx,xxxLess: Allowance for doubtful accounts xxxxNet accounts receivable $XXX,XXX

Balance Sheet Presentation – Allowance Method

Accounting for Bad Debts:Allowance Method

Journal entry to record bad debt write-off inperiod determined uncollectible:

Allowance for Doubtful Accounts XXXAccounts Receivable—Dexter XXX

Bankrupt

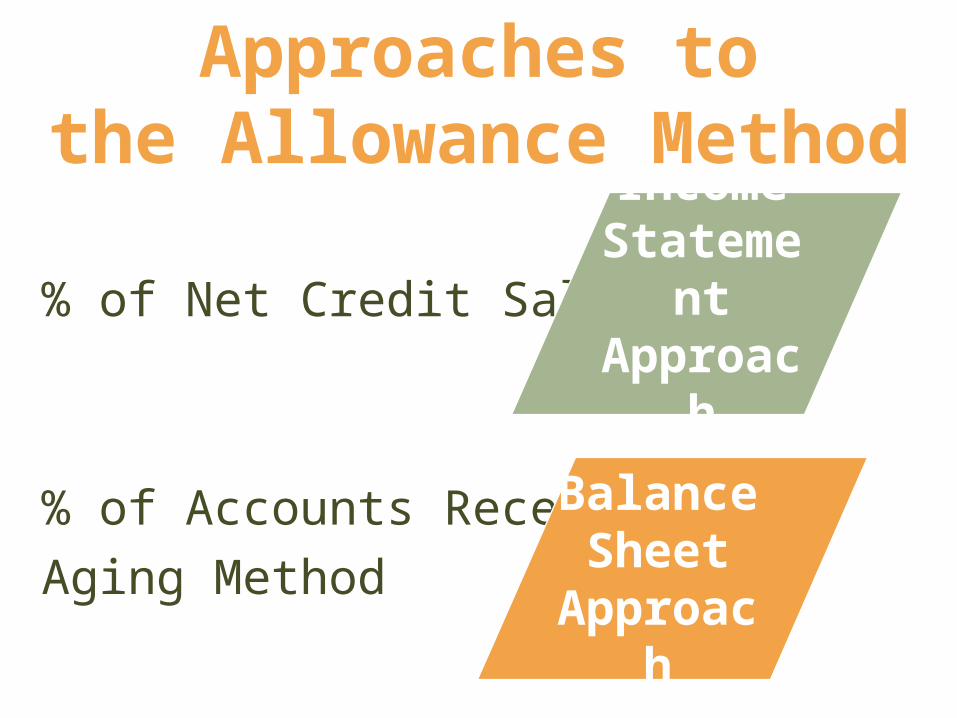

Approaches tothe Allowance Method

% of Net Credit Sales

% of Accounts Receivable Aging Method

Income Statement Approach

Balance Sheet

Approach

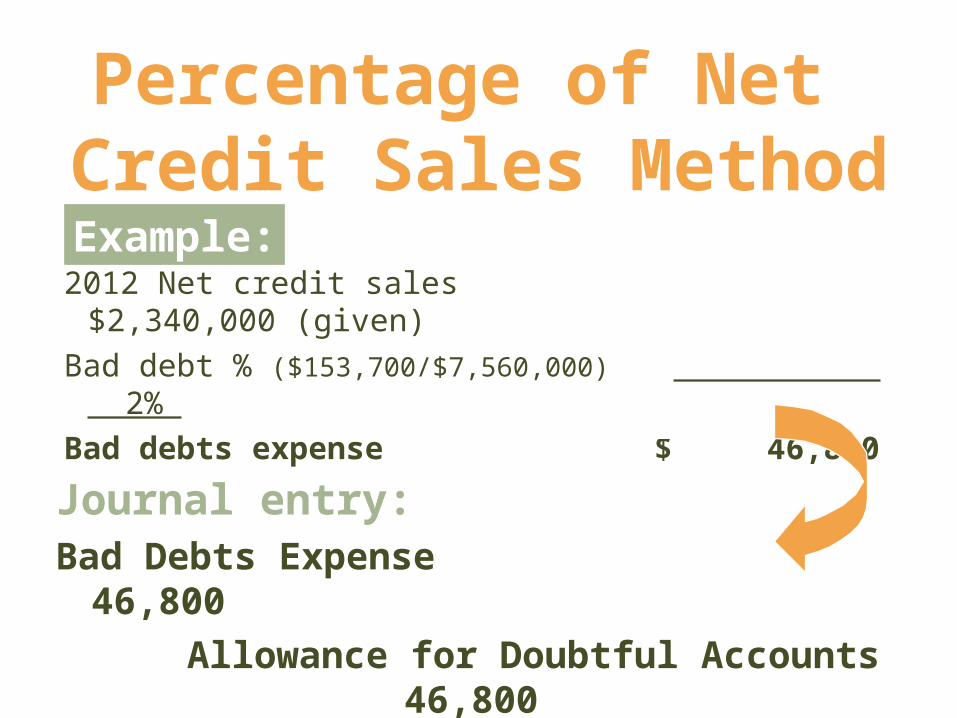

Example:

Percentage of Net Credit Sales Method

Assume prior years’ net credit sales and bad debtexpense is as follows:

Year Net Credit Sales Bad Debts2007 $1,250,000 $ 26,4002008 1,340,000 29,3502009 1,200,000 23,1002010 1,650,000 32,1502011 2,120,000 42,700

$7,560,000 $153,700

Percentage of Net Credit Sales Method

2012 Net credit sales $2,340,000 (given)Bad debt % ($153,700/$7,560,000) 2% Bad debts expense $ 46,800

Example:

Journal entry:Bad Debts Expense 46,800 Allowance for Doubtful Accounts 46,800

Example:

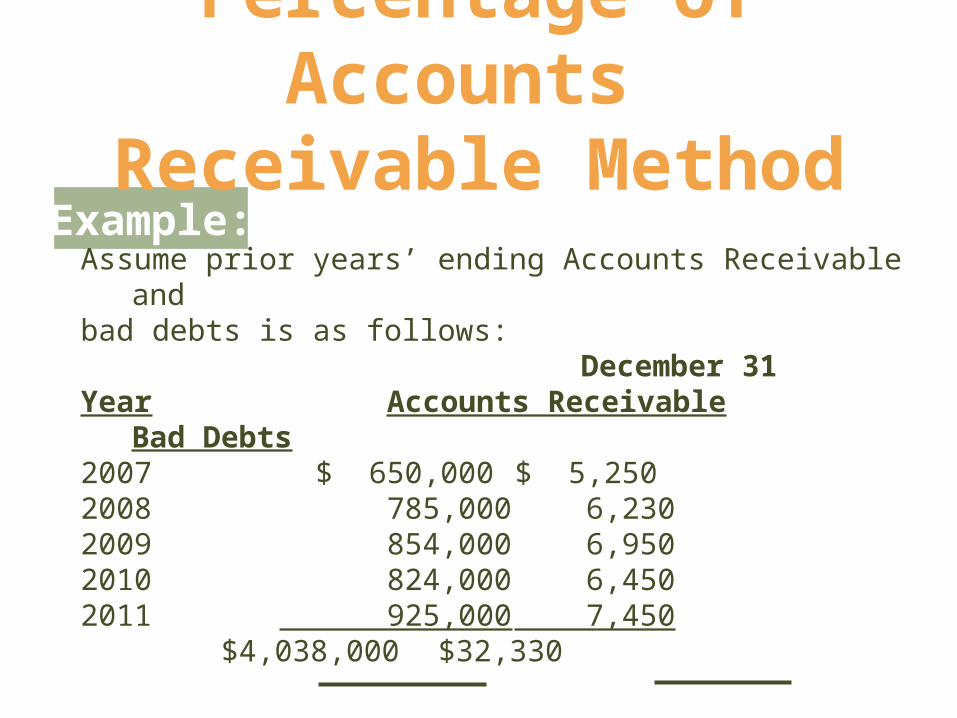

Percentage of Accounts Receivable Method

Assume prior years’ ending Accounts Receivable andbad debts is as follows: December 31Year Accounts Receivable Bad Debts2007 $ 650,000 $ 5,2502008 785,000 6,2302009 854,000 6,9502010 824,000 6,4502011 925,000 7,450

$4,038,000 $32,330

Percentage of Accounts Receivable Method

$32,330 / $4,038,000 = 0.8% ratio of bad debts to the ending accounts receivable

December 31, 2012 Accounts Receivable $865,000

× 0.8% Credit balance required in Allowance account after adjustment $6,920

Example:

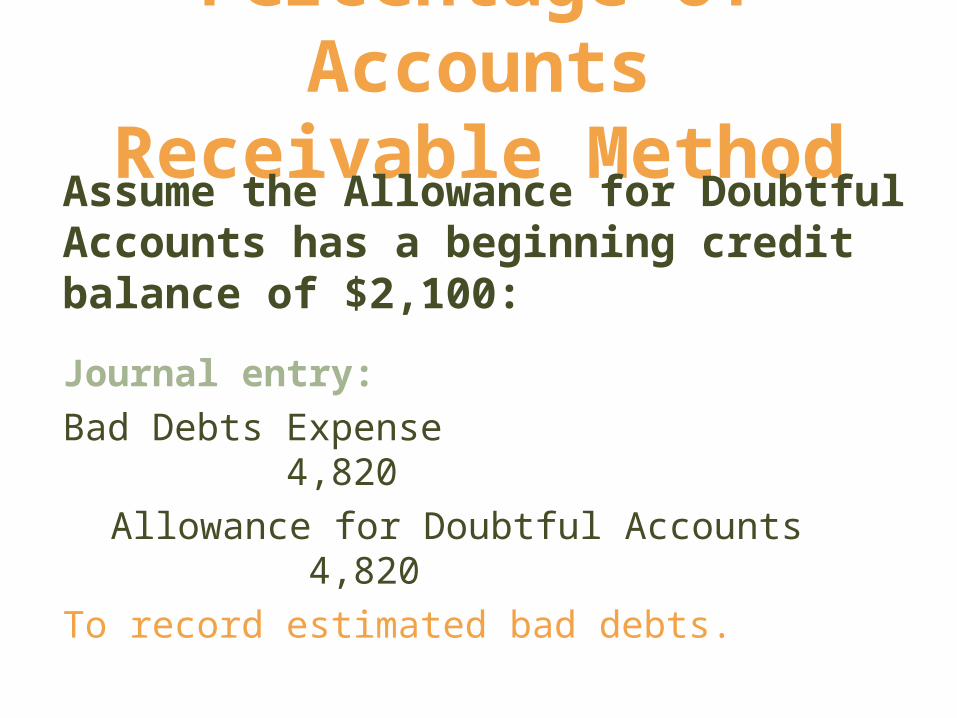

Percentage of Accounts Receivable Method

Assume the Allowance for Doubtful Accounts has a beginning credit balance of $2,100:

Credit balance required in allowance account after adjustment $ 6,920 Less: Credit balance in allowance account before adjustment 2,100Amount for bad debt expense entry $ 4,820

Percentage of AccountsReceivable Method

Assume the Allowance for Doubtful Accounts has a beginning credit balance of $2,100:

Journal entry:Bad Debts Expense 4,820

Allowance for Doubtful Accounts 4,820To record estimated bad debts.

Percentage of AccountsReceivable Method

The net realizable value of accounts receivable would be determined as follows:

Accounts receivable $xxx,xxxLess: Allowance for doubtful account 6,920

Net realizable value $xxx,xxx

Aging Method Estimated Percent Estimated Amount

Category Amount Uncollectible Uncollectible Current $ 85,600 1% $ 856Past due: 1–30 days 31,200 4% 1,248 31–60 days 24,500 10% 2,450 61–90 days 18,000 30% 5,400 90+ days 9,200 50% 4,600 Totals $168,500 $14,554

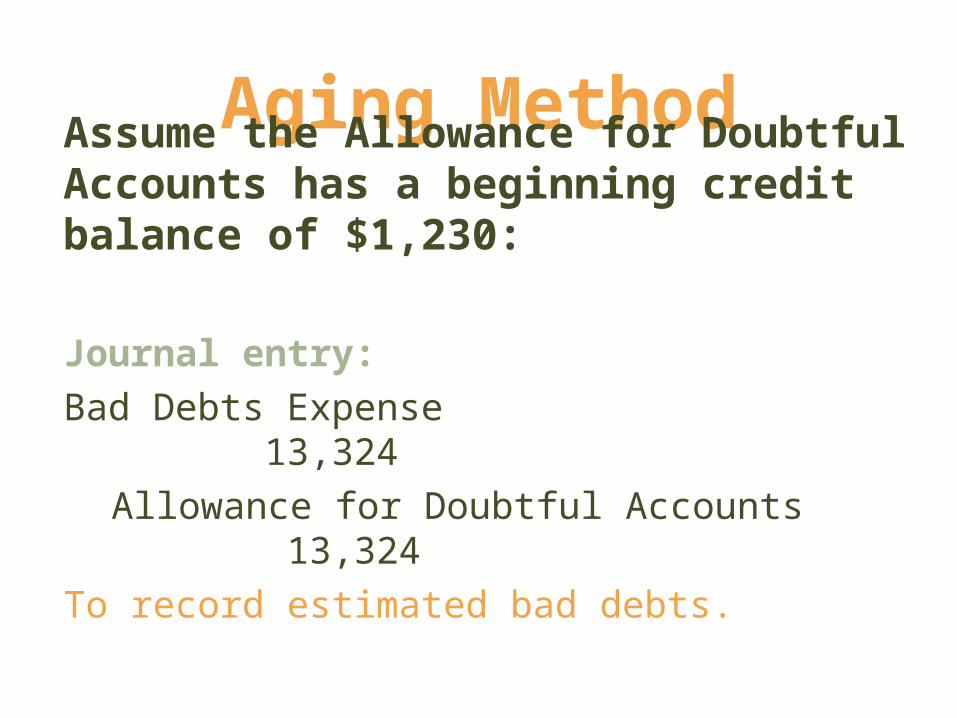

Aging MethodAssume the Allowance for Doubtful Accounts has a beginning credit balance of $1,230:

Credit balance required in allowance account after adjustment $14,554 Less: Credit balance in allowance account before adjustment (1,230)Amount for bad debt expense entry $13,324

Aging MethodAssume the Allowance for Doubtful Accounts has a beginning credit balance of $1,230:

Journal entry:Bad Debts Expense 13,324

Allowance for Doubtful Accounts 13,324To record estimated bad debts.

Aging MethodThe net realizable value of accounts receivable would be determined as follows:

Accounts receivable $xxx,xxxLess: Allowance for doubtful account 14,554

Net realizable value $xxx,xxx

Accounts Receivable Turnover

Net Credit SalesAverage Accounts Receivable

Indicates how quickly a company is collecting (i.e., turning over) its receivables

LO2

Accounts Receivable Turnover Too fast may mean: credit policies too stringent; may be losing sales

Too slow may mean: credit department not operating effectively; dissatisfied customers

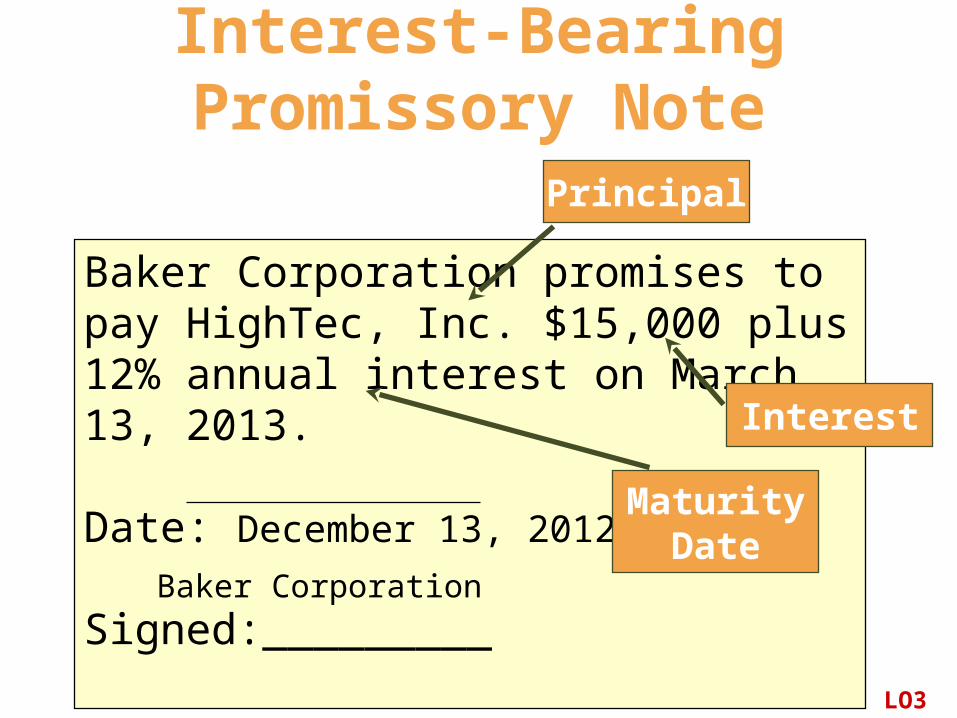

Baker Corporation promises to pay HighTec, Inc. $15,000 plus 12% annual interest on March 13, 2013.

Date: December 13, 2012

Signed:_________

Interest-Bearing Promissory Note

Baker Corporation

MaturityDate

Principal

Interest

LO3

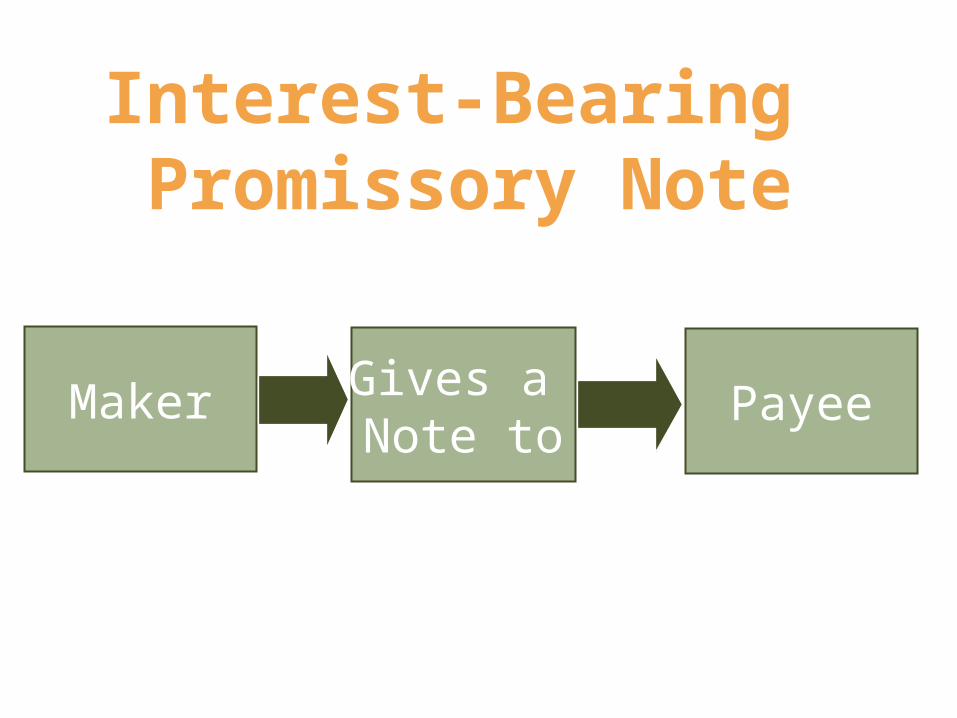

Interest-Bearing Promissory Note

Maker Gives a Note to

Payee

Receipt of Interest-Bearing Promissory Note

Journal entry to record the receipt of the noteon December 13, 2012:

Notes Receivable 15,000 Sales Revenue 15,000

Interest-Bearing Promissory Note

Adjusting entry to record interest on Dec. 31, 2012:Interest Receivable 90

Interest Revenue 90* *Interest = $15,000 × 12% × 18/360

Interest-Bearing Promissory Note

Journal entry to record the collection of the note on March 13, 2013:Cash 15,450

Notes Receivable 15,000Interest Revenue 360*

Interest Receivable 90*15,000 × 12% × 72/360

Accelerating the Cash Inflow from Sales

Credit card salesDiscounting notes receivable

LO4

Credit Card Sales

Competitive necessityCredit card company:

• Charges fee• Assumes risk of nonpayment

Discounting Notes ReceivableSell note prior to maturity date for cashReceive less than face value (i.e.,

discounted amount)Can be sold with or without recourse

Reasons Companies Invest in Other Companies

Short-term cash excesses

Long-term investing for future cash needs

Exert influence over investee

Obtain control of investeeLO5

Investment in a CD

Purchase of investment: Short-Term Investments—CD 100,000

Cash 100,000

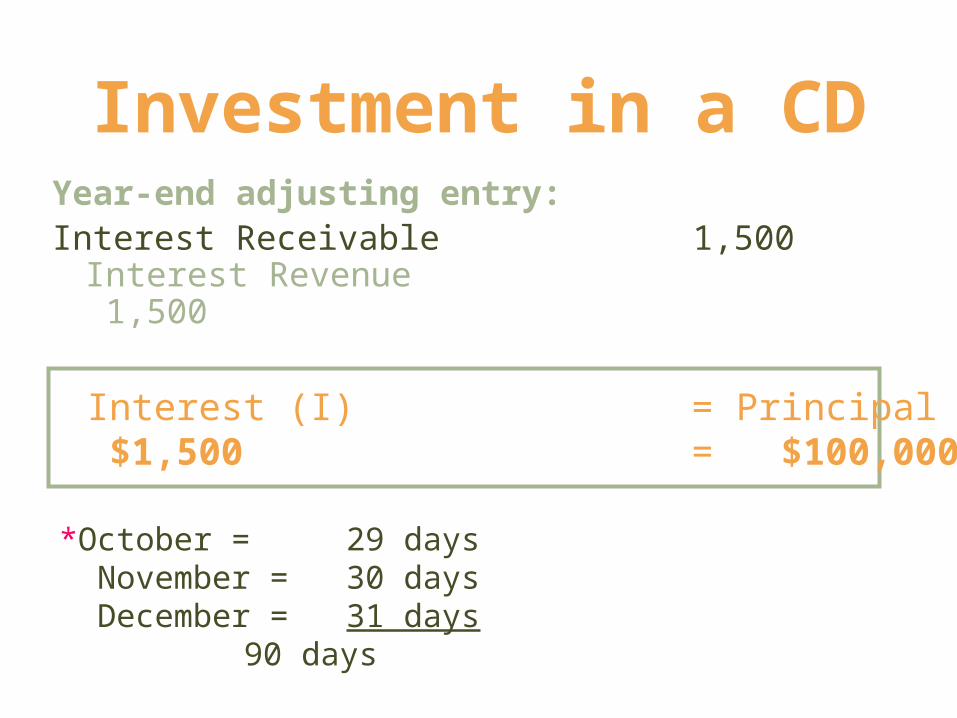

On October 2, 2012, Creston invests $100,000 of excess cash in a 120-day CD. Principal plus interest @ 6% due upon investment maturity.

Example:

Year-end adjusting entry:Interest Receivable 1,500

Interest Revenue 1,500

Investment in a CD

Interest (I) = Principal (P) × Rate (R) × Time (T) $1,500 = $100,000 × 6% × 90*/360

*October = 29 days November = 30 days December = 31 days

90 days

Upon investment maturity:

Cash 102,000Short-Term Investments—CD 100,000Interest Receivable 1,500Interest Revenue* 500

Investment in a CD

*Interest earned in January:$100,000 × 6% × 30/360 = $500

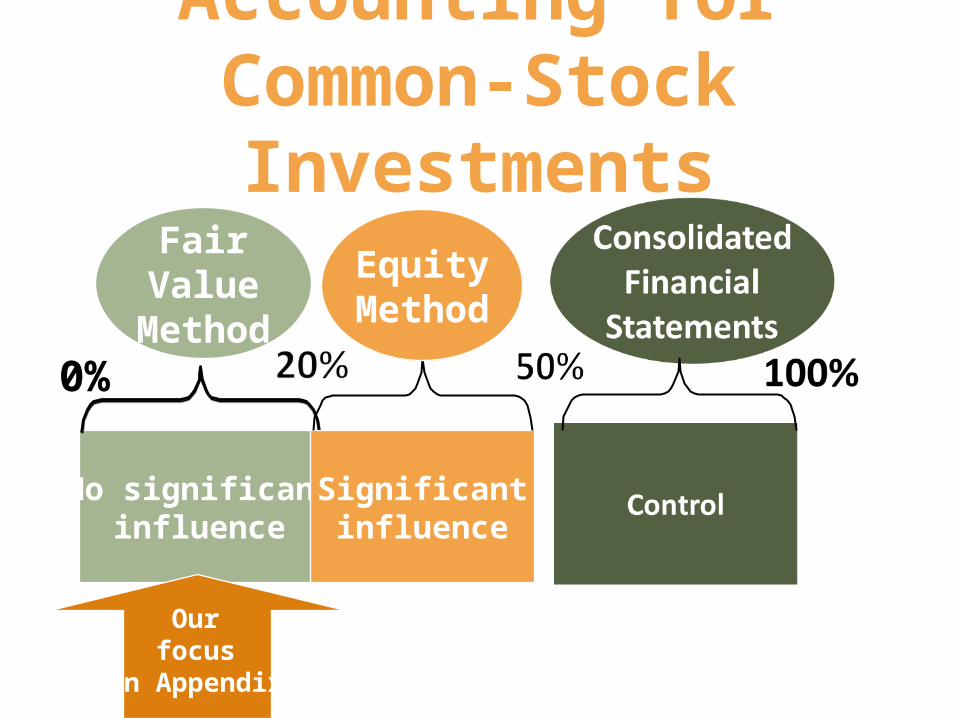

Accounting for Common-Stock Investments

No significantinfluence

0%

FairValue

Method

Significantinfluence

EquityMethod

Ourfocus

in Appendix

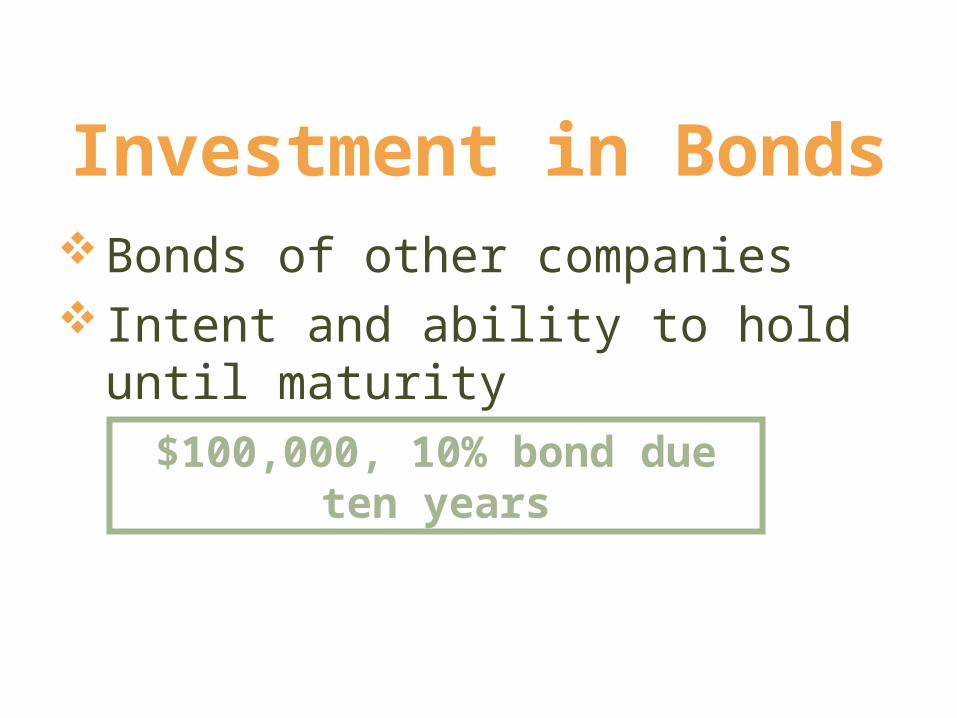

Investment in BondsBonds of other companies Intent and ability to hold until maturity

$100,000, 10% bond due ten years

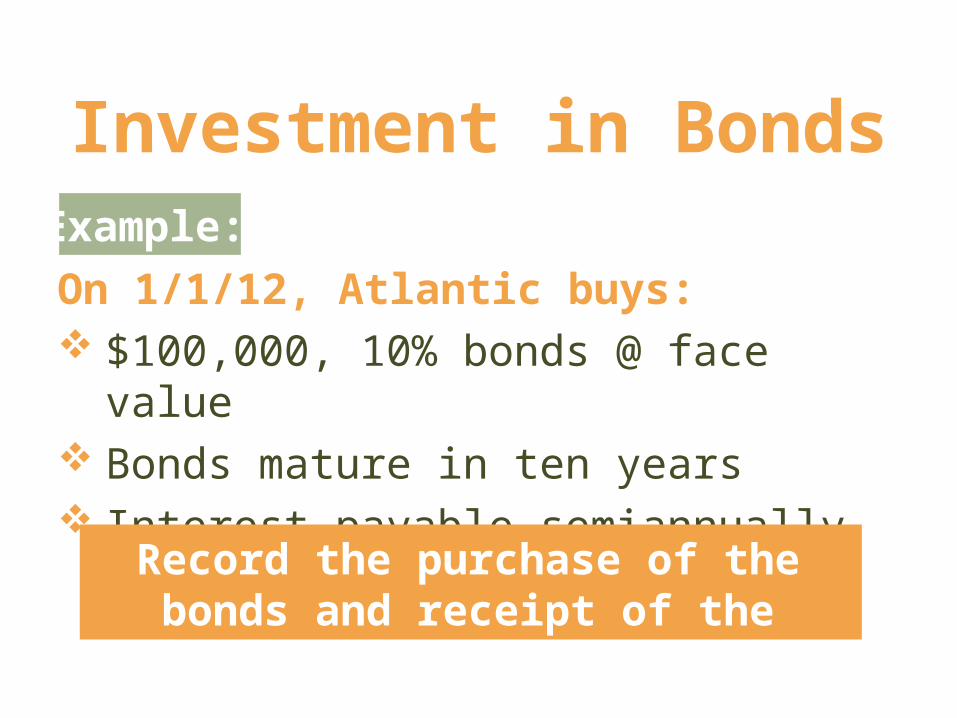

Investment in Bonds

On 1/1/12, Atlantic buys: $100,000, 10% bonds @ face value Bonds mature in ten years Interest payable semiannually

Example:

Record the purchase of the bonds and receipt of the first interest payment

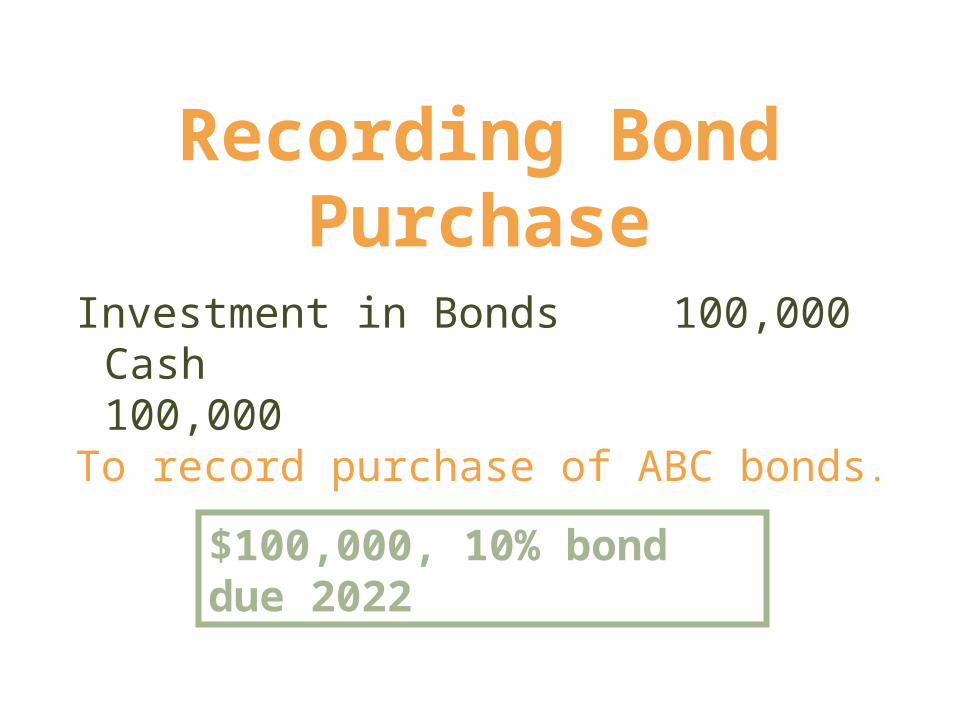

Recording Bond Purchase

Investment in Bonds 100,000Cash100,000

To record purchase of ABC bonds.

$100,000, 10% bond due 2022

Recording Receipt of Interest Payment

6/30/12

Cash ($100,000 × 10% × 1/2) 5,000 Interest Income 5,000

To record interest income on ABC bonds.

Recording Bond Sale7/1/12

Cash 99,000Loss on Sale of Bonds 1,000 Investment in Bonds 100,000

To record sale of ABC bonds.

Investment in Stocks

Stocks of other companiesRecorded at cost, including any

brokerage fees, commissions or other fees paid to acquire the shares

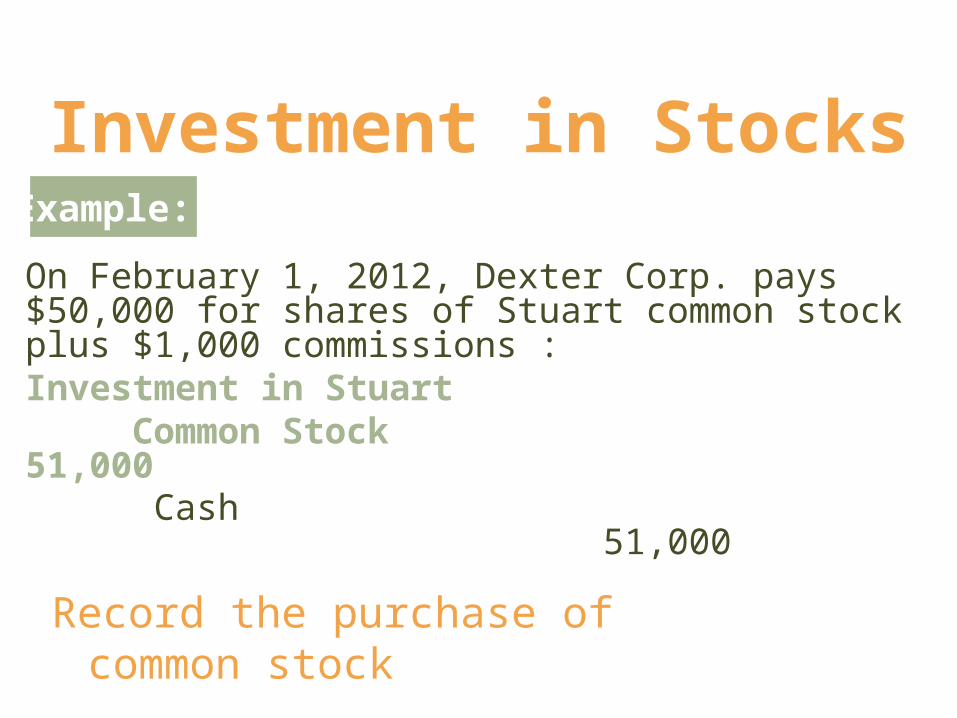

Investment in Stocks

On February 1, 2012, Dexter Corp. pays $50,000 for shares of Stuart common stock plus $1,000 commissions : Investment in Stuart Common Stock 51,000 Cash 51,000

Example:

Record the purchase of common stock

Recording Receipt of DividendsDexter receives $500 cash dividends from Stuart common stock on March 31, 2012:

Cash 500Dividend Income 500

To record the receipt of dividends

Sale of Investment in StocksSale of Investment in Stuart common stock on May 20, 2012 for $53,000:

Cash 53,000 Investment in Stuart Common Stock 51,000 Gain on Sale of Stock 2,000

To record the sale of Stuart common stock.

Operating Activities Net income xxx Increase in accounts receivable – Decrease in accounts receivable + Increase in notes receivable – Decrease in notes receivable +Investing Activities Purchases of held-to-maturity and available-for-sale securities – Sales/maturities of held-to-maturity and available-for-sale securities +Financing Activities

Liquid Assets and the Statement of Cash Flows – Indirect Method

LO6

End of Chapter 7