appraisal report - s3.amazonaws.com · appraisal report industrial showroom ... table of contents...

TRANSCRIPT

PREPARED BY:

TALBOTT VALUATION ADVISORY SERVICES

3379 PEACHTREE ROAD, NE SUITE 555 ATLANTA, GEORGIA 30326

APPRAISAL REPORT

INDUSTRIAL SHOWROOM BUILDING '''''''''' '''''''''''''''''''''''''''' '''''''''''' WESTERVILLE, OHIO 43081 FILE NO. 16074 EFFECTIVE DATE: SEPTEMBER 10, 2016 PREPARED FOR: '''''''' '''''''''' ''''''''''''''' '''''''''''''' ''''''''''''''''''' ''''''''''' ''''''''' '''''''''''''''''''' ''''''''''''''''''' ''''''' '''''''''' ''''''''''''' ''''''''''''' '''''''''''''''''''''' ''''''''''''' AND ''''''' '''''''''''' '''''''''''''''''' ''''''''''''''''''''''''''''''''''''' LOAN NAME: '''''''''''''''''''''''' '''''''''''''''''' DMS NUMBER: ''''''''

TALBOTT VALUATION ADVISORY SERVICES

3379 PEACHTREE ROAD, NE SUITE 555 ATLANTA, GEORGIA 30326 September 14, 2016 ''''''' '''''''''' ''''''''''''' '''''''''''' ''''''''''''''''' ''''''''''' '''''''''' '''''''''''''''''''' ''''''''''''''' ''''''' ''''''''''' '''''''''''' '''''''''''' ''''''''''''''''''' '''''''''''' and ''''''' ''''''''''' ''''''''''''''''' '''''''''''''''''''''''''''' Re: Industrial Showroom Building ''''''''' ''''''''''''''''''' ''''''''' Westerville, Ohio 43081 Loan Name: '''''''''''''''''' '''''''''''''' DMS Number: ''''''''' TVAS File Number: 16074 Dear ''''''' '''''''''''': In accordance with your request, we have completed an appraisal of the above-referenced property. The purpose of the appraisal is to develop an opinion of the market value “as-is” of the fee simple interest in the subject property, subject to certain definitions, assumptions and limiting conditions as set forth in the accompanying report. The subject property was inspected on September 10, 2016, the effective date of this report. The client for this assignment is identified as '''''''''''' '''''''''''''''' '''''''''. The intended users of this report are '''''''''''' '''''''''''''''' ''''''''' and the '''''''' ''''''''''' '''''''''''''''' ''''''''''''''''''''''''''''', and the intended use is for loan underwriting and/or credit decisions. The appraisal is intended to conform with the Uniform Standards of Professional Appraisal Practice (USPAP), the Code of Professional Ethics and Standards of Professional Appraisal Practice of the Appraisal Institute, applicable state appraisal regulations, and the appraisal guidelines of our client. The appraisal is also prepared in accordance with the appraisal regulations issued in connection with the Financial Institutions Reform, Recovery and Enforcement Act (FIRREA). The following appraisal presents the most relevant data gathered in our investigation, details of

the processes utilized, and the interpretation and reconciliation of our analysis leading to the

opinion of value.

'''''''' '''''''''''' '''''''''''' '''''''''''''''' ''''''''' September 14, 2016 Page 2 The subject property consists of one legal parcel containing 87,120 square feet and is improved with a 13,125-square-foot structural steel-framed industrial showroom building constructed in 1995. The building is currently owner-occupied dba '''''''''''''''''''' ''''' '''''''''''''' ''''''''''''''. Based on the examination and analysis, it is our opinion that the market value “as is” of the fee simple interest in the subject property, subject to certain definitions, assumptions and limiting conditions as set forth in the accompanying report, as of September 10, 2016, was:

EIGHT HUNDRED FIFTY-FIVE THOUSAND DOLLARS

$855,000

If you have any questions or comments, please contact the undersigned. Thank you for the opportunity to be of service. Respectfully Submitted,

J. Carl Talbott, III Certified General Real Estate Appraiser Ohio Temporary License No. ACGT. 2016004619 Telephone: (404) 479-9887 Email: [email protected]

TVAS SUBJECT PHOTOGRAPHS

'''''''''''''''''''''' ''''''''' Facing Northeast

'''''''''''''''''''' ''''''''' Facing Southwest

TVAS SUBJECT PHOTOGRAPHS

Southeastern (Front) and Southwestern (Side) Elevations

Southeastern (Front) Elevation

TVAS SUBJECT PHOTOGRAPHS

Northeastern (Side) and Northwestern (Rear) Elevations

Southwestern (Side) and Northwestern (Rear) Elevations

TVAS SUBJECT PHOTOGRAPHS

Showroom/Retail Area

Executive Office

TVAS SUBJECT PHOTOGRAPHS

Office

Employee Breakroom

TVAS SUBJECT PHOTOGRAPHS

Warehouse Interior

Warehouse Interior

TALBOTT VALUATION ADVISORY SERVICES

Table of Contents

EXECUTIVE SUMMARY .................................................................................................................................. 1

Property Identification .............................................................................................................................. 1

Property History ........................................................................................................................................ 1

Site Characteristics .................................................................................................................................... 1

Improvements ........................................................................................................................................... 2

Highest and Best Use ................................................................................................................................ 2

Valuation ................................................................................................................................................... 2

Conditions of the Assignment ................................................................................................................... 3

Pro Forma Data ......................................................................................................................................... 3

Value Conclusions ..................................................................................................................................... 3

SCOPE OF WORK ........................................................................................................................................... 4

Report Criteria........................................................................................................................................... 4

Property History ........................................................................................................................................ 5

Data Sources ............................................................................................................................................. 5

Valuation Approaches ............................................................................................................................... 5

Definition of Values ................................................................................................................................... 6

Exposure/Marketing Time ........................................................................................................................ 6

Competency Statement ............................................................................................................................ 8

AREA ANALYSIS ............................................................................................................................................. 9

NEIGHBOHOOD ANALYSIS........................................................................................................................... 12

Overview ................................................................................................................................................. 12

Access and Linkages ................................................................................................................................ 13

Population ............................................................................................................................................... 13

Households ............................................................................................................................................. 14

Housing ................................................................................................................................................... 14

Income .................................................................................................................................................... 15

Employment ............................................................................................................................................ 15

Retail/Entertainment .............................................................................................................................. 18

Conclusion ............................................................................................................................................... 19

MARKET ANALYIS ........................................................................................................................................ 20

Columbus Industrial Market Overview ................................................................................................... 20

Leasing Activity and Trends .................................................................................................................... 20

Sales Activity ........................................................................................................................................... 21

TALBOTT VALUATION ADVISORY SERVICES

Industry Data and Forecast ..................................................................................................................... 21

Q2 2016 Columbus Industrial Statistics .................................................................................................. 22

Westerville Industrial Submarket ........................................................................................................... 23

Market Outlook ....................................................................................................................................... 23

SITE DESCRIPTION ....................................................................................................................................... 24

Physical Characteristics ........................................................................................................................... 24

Utilities .................................................................................................................................................... 24

Legal Information .................................................................................................................................... 25

Surrounding Arterials .............................................................................................................................. 26

Parcel Map .............................................................................................................................................. 26

Survey...................................................................................................................................................... 27

Flood Zone Map ...................................................................................................................................... 28

IMPROVEMENTS DESCRIPTION ................................................................................................................... 29

General Description ................................................................................................................................ 29

Construction Details ................................................................................................................................ 30

Interior Elements .................................................................................................................................... 30

Mechanical Systems ................................................................................................................................ 30

Special Improvements ............................................................................................................................ 31

Quality and Condition ............................................................................................................................. 31

Improvements Sketch ............................................................................................................................. 32

ZONING ....................................................................................................................................................... 33

Zoning Summary ..................................................................................................................................... 33

Zoning Map ............................................................................................................................................. 34

REAL ESTATE TAXES AND ASSESSMENT ...................................................................................................... 35

Introduction ............................................................................................................................................ 35

Current Property Tax Liability ................................................................................................................. 35

HIGHEST AND BEST USE .............................................................................................................................. 36

Introduction ............................................................................................................................................ 36

Highest and Best Use as Vacant .............................................................................................................. 36

Highest and Best Use as Improved ......................................................................................................... 37

Most Likely Buyer .................................................................................................................................... 38

VALUATION PROCESS .................................................................................................................................. 39

Methodology ........................................................................................................................................... 39

Cost Approach ......................................................................................................................................... 39

Sales Comparison Approach ................................................................................................................... 39

TALBOTT VALUATION ADVISORY SERVICES

Income Capitalization Approach ............................................................................................................. 39

Summary ................................................................................................................................................. 40

SALES COMPARISON APPROACH ................................................................................................................ 41

Summary of Comparable Improved Sales Data ...................................................................................... 41

Comparable Improved Sales Map ........................................................................................................... 44

Comparable Improved Sales Adjustment Grid ....................................................................................... 46

Comparable Improved Sales Analysis ..................................................................................................... 47

Value Conclusion ..................................................................................................................................... 51

INCOME CAPITALIZATION APPROACH ........................................................................................................ 52

Summary of Comparable Rental Data .................................................................................................... 52

Comparable Rentals Map ........................................................................................................................ 55

Comparable Rentals Adjustment Grid .................................................................................................... 56

Comparable Rentals Analysis .................................................................................................................. 57

Market Rent Conclusion.......................................................................................................................... 59

Potential Gross Income ........................................................................................................................... 59

Analysis of Expenses ............................................................................................................................... 59

Mortgage-Equity Capitalization .............................................................................................................. 61

Debt Service Coverage Ratio Technique ................................................................................................. 62

Broker Interview ..................................................................................................................................... 62

Summary of Capitalization Rate Sales .................................................................................................... 63

Capitalization Rate Conclusion ............................................................................................................... 64

Value Conclusion ..................................................................................................................................... 64

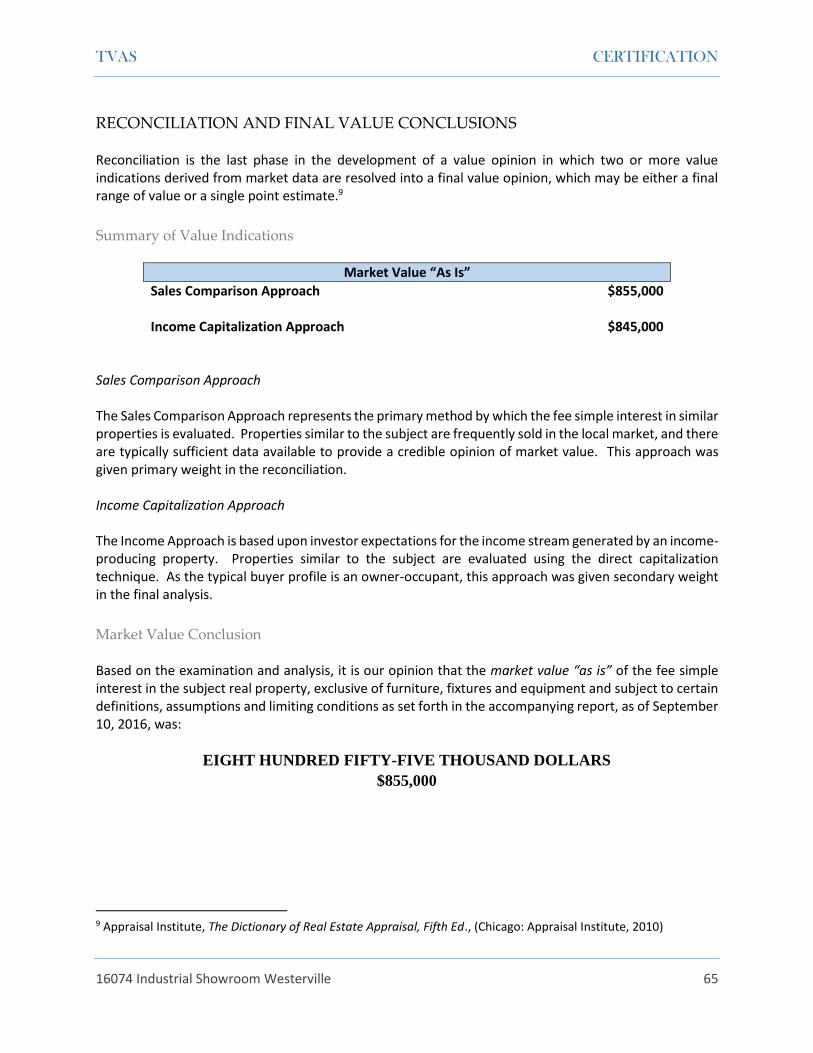

RECONCILIATION AND FINAL VALUE CONCLUSIONS .................................................................................. 65

Summary of Value Indications ................................................................................................................ 65

Market Value Conclusion ........................................................................................................................ 65

CERTIFICATION ............................................................................................................................................ 66

ADDENDA .................................................................................................................................................... 67

Assumptions and Limiting Conditions ..................................................................................................... 67

Qualifications of the Appraiser ............................................................................................................... 69

Engagement Letter .................................................................................................................................. 70

Insurable Value ....................................................................................................................................... 80

Terms and Definitions ............................................................................................................................. 81

TVAS EXECUTIVE SUMMARY

16074 Industrial Showroom Westerville 1

EXECUTIVE SUMMARY

Property Identification

TVAS File No. 16074 Property Type Industrial Showroom Building

Property Address ''''''''' ''''''''''''''''''' ''''''''''

Westerville, Ohio 43081 Parcel Number(s) ''''''''''''''''''''''''''''

Property History

Current Owner(s) '''''''''' '''''' ''''''''''' Previous Market Sale January 12, 1995 Previous Sale Price $125,000 Other Sales – Past Three Years None noted Property Status Owner-occupied

Site Characteristics

Total Land Area 2.0 Acres 87,120 SF Site Shape Mostly rectangular Topography Level Soils Appear adequate to support existing improvements Current Zoning L-M, Limited Manufacturing District

H-35, 35-Foot Height District Utilities All available Easements/Encroachments None noted Street(s) Access Exposure '''''''''''''''''''' ''''''''' Direct Good

TVAS EXECUTIVE SUMMARY

16074 Industrial Showroom Westerville 2

Improvements

Gross Building Area (SF) 13,125 Year Built 1995 Construction Class S, Structural Steel-Frame Effective Age 10 years Remaining Economic Life 30 years Rentable Area (SF) 13,125 Tenancy Single Occupancy Owner-occupied Grade-Level Loading 7 Dock-High Loading 2 Eave Height 14 Feet Finished Office Ratio 16.2% Coverage Ratio 15.1%

Highest and Best Use

Highest and Best Use as Vacant Commercial Use Highest and Best Use as Improved Continued Use of Existing Improvements

Valuation

Value Type Market Value “As-Is” Insurable Value

Property Rights Appraised Fee Simple Exposure/Marketing Time 6-9 months

TVAS EXECUTIVE SUMMARY

16074 Industrial Showroom Westerville 3

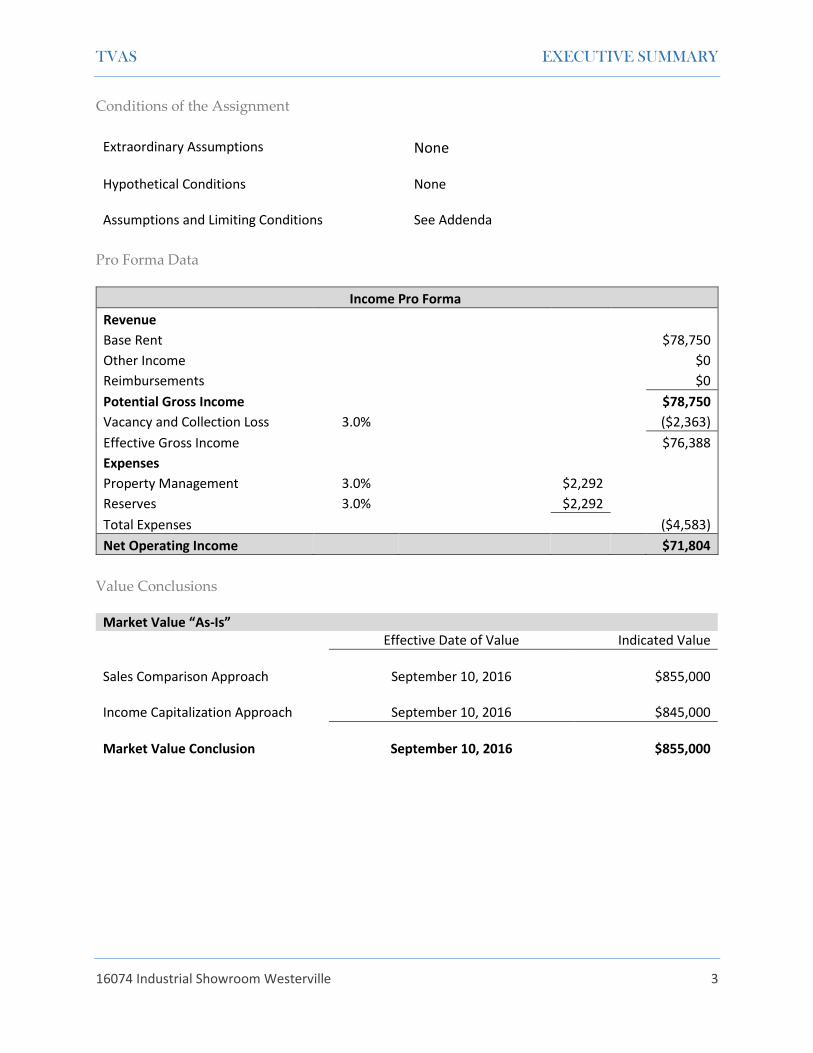

Conditions of the Assignment

Extraordinary Assumptions None Hypothetical Conditions None Assumptions and Limiting Conditions See Addenda

Pro Forma Data

Income Pro Forma

Revenue

Base Rent $78,750

Other Income $0

Reimbursements $0

Potential Gross Income $78,750

Vacancy and Collection Loss 3.0% ($2,363)

Effective Gross Income $76,388

Expenses

Property Management 3.0% $2,292

Reserves 3.0% $2,292

Total Expenses ($4,583)

Net Operating Income $71,804

Value Conclusions

Market Value “As-Is” Effective Date of Value Indicated Value

Sales Comparison Approach September 10, 2016 $855,000 Income Capitalization Approach September 10, 2016 $845,000

Market Value Conclusion September 10, 2016 $855,000

TVAS SCOPE OF WORK

16074 Industrial Showroom Westerville 4

SCOPE OF WORK

Report Criteria

Report Format Appraisal Report Purpose of the Appraisal Estimate Market Value as defined by the Board of

Governors of the Federal Reserve System, in accordance with Title XI of FIRREA (1989)

Intended Use To aid in loan underwriting in connection with

the acquisition, disposition and/or refinancing of the subject property

Client '''''''''''' ''''''''''''''' ''''''''' Intended User(s) The Intended Users are ''''''''''' '''''''''''''''''' '''''''''

and the '''''' '''''''''' '''''''''''''''''' ''''''''''''''''''''''''''''. '''''''''''' ''''''''''''''''' '''''''''' and its respective affiliates (collectively "'''''''''''''''") together with its successors, assigns and transferees with respect to its interests in the subject financing and/or any party to whom '''''''''''''''' has pledged its interest in the subject financing may use and rely upon this Report in connection with the making of a mortgage loan. Further, '''''''''''''''' may furnish this report to third parties involved in evaluating or auditing the subject financing, provided that no such parties may use or rely upon any such information unless the same have succeeded to ''''''''''''''''s interest in connection therewith. Finally, in compliance with banking regulations and internal policy, '''''''''''''''' may provide a copy of this Report to prospective borrowers on a non- reliance basis for informational purposes only.

Property Rights Appraised Fee Simple Date of Report September 14, 2016 Date of Inspection September 10, 2016 Date(s) of Value September 10, 2016

TVAS SCOPE OF WORK

16074 Industrial Showroom Westerville 5

Property Contact - Name ''''''''''' ''''''''''''' Property Contact – Phone '''''''''' ''''''''''''''''''' Inspection Details The appraiser was provided access to all interior

areas within the subject’s improvements.

Property History According to tax records, the subject property is currently owned by '''''''''''' '''''' '''''''''''. The subject property is presently owner-occupied dba ''''''''''''''''' ''''' '''''''''''''' '''''''''''''. We are not aware of any transactions regarding ownership during the three years preceding the preparation of this report. We are not aware of any agreement for sale or option currently in existence concerning the subject property.

Data Sources

Site To Do Business (STDB) Costar COMPS LoopNet U.S. Bureau of Labor Statistics Government Officials Ohio Department of Labor Moody’s Economy.com Institute of Real Estate Management Marshall Valuation Services Local brokers

Valuation Approaches

Approaches Utilized Approaches Omitted

Sales Comparison *Cost Approach

Income Capitalization Approach

*The cost approach was excluded from this appraisal because of the age of the improvements and the inherent difficulty in accurately quantifying depreciation for this type of asset.

TVAS SCOPE OF WORK

16074 Industrial Showroom Westerville 6

Definition of Values Market value is defined as: the most probable price that a property would bring in a competitive and open market under all conditions requisite to a fair sale, the buyer and seller each acting prudently and knowledgeably, and assuming the price is not affected by undue stimulus. Implicit in this definition is the consummation of a sale as of a specified date and the passing of title from seller to buyer under conditions whereby:

• Buyer and seller are typically motivated;

• Both parties are well informed or well advised, and acting in what they consider to be their own best interests;

• A reasonable time is allowed for exposure in the open market;

• Payment is made in terms of cash in U.S. dollars or in terms of financial arrangements comparable thereto; and

• The price represents the normal consideration for the property sold unaffected by special or creative financing or sales concessions granted by anyone associated with the sale.1

Insurable Value is defined as: the value used by insurance companies as the basis for insurance. Often

considered to be replacement or reproduction cost plus allowances for debris removal or demolition less

deterioration and non-insurable items. Sometimes cash value or market value, but often entirely a cost

concept.2

Exposure/Marketing Time Exposure time is the estimated time a property would have been offered to the market at a price equivalent to market value prior to sale on the effective date of valuation. Marketing time is the period of time necessary to sell the subject property interest at its estimated market value after the effective date of valuation. Marketing periods for transactions involving comparable properties can provide a reasonable proxy for determining an appropriate exposure time for the subject. We reviewed sales of similar properties to determine an appropriate exposure time for the subject property. We also reviewed other sales data reported by Costar within the subject’s market. The Westerville industrial submarket is relatively small comprising about 1.6% of the metro inventory. It is second-ranked in terms of both asking rents ($7.83) and vacancy rates (0.7%) versus the overall Columbus market. There have been only two sales in the past three years comprising approximately 40,000 square feet.

1 Federal Register, Vol. 55, 165, Friday, August 24, 1990, Rules and Regulations, 12 CFR Part 34.42(F) 2 Marshall & Swift/Boeckh, Marshall Valuation Service, (Los Angeles: Marshall & Swift/Boeckh, 2010), Sec. 3, Pg. 2.

TVAS SCOPE OF WORK

16074 Industrial Showroom Westerville 7

According to CoStar Group3, the Columbus MSA is projected to add jobs at a rate of 2.9% per year which is similar to recent historical growth as shown in the following chart.

As there is no evidence to suggest that forecasted market conditions will differ significantly from market conditions experienced within the last year, our estimate for exposure time is considered a reasonable proxy for the subject’s marketing time. Based on our analysis, we conclude the subject property to have a marketing time and exposure time between 6 and 9 months.

3 Columbus Economic Overview 3Q 2016

TVAS SCOPE OF WORK

16074 Industrial Showroom Westerville 8

Competency Statement

The Competency Provision of the Uniform Standards of Professional Appraisal Practice, promulgated by the Appraisal Foundation and required as part of the Financial Institutions Reform, Recovery, and Enforcement Act, states that: Prior to entering an agreement to perform any assignment, an appraiser must properly identify the property to be appraised and have the knowledge and experience that will be required to complete the assignment competently or alternatively: Disclose the lack of knowledge and/or experience to the client before accepting the assignment; Take all appropriate steps necessary to complete the assignment competently; and Describe the lack of knowledge and/or experience and the steps taken to complete the assignment competently in the report. The appraisers affirm that they have the knowledge and experience to competently complete the assignment in accordance with the competency provision in USPAP.

TVAS AREA ANALYSIS

16074 Industrial Showroom Westerville 9

AREA ANALYSIS The subject property is located within the city limits of Columbus in Franklin County, Ohio just south of the city of Westerville and approximately nine miles northeast of the central business district of Columbus. Franklin County is one of ten counties considered as part of the Columbus, OH Metropolitan Statistical Area. As of the 2015 census, the Columbus, OH MSA had a population of 2,021,632. Area Map

TVAS AREA ANALYSIS

16074 Industrial Showroom Westerville 10

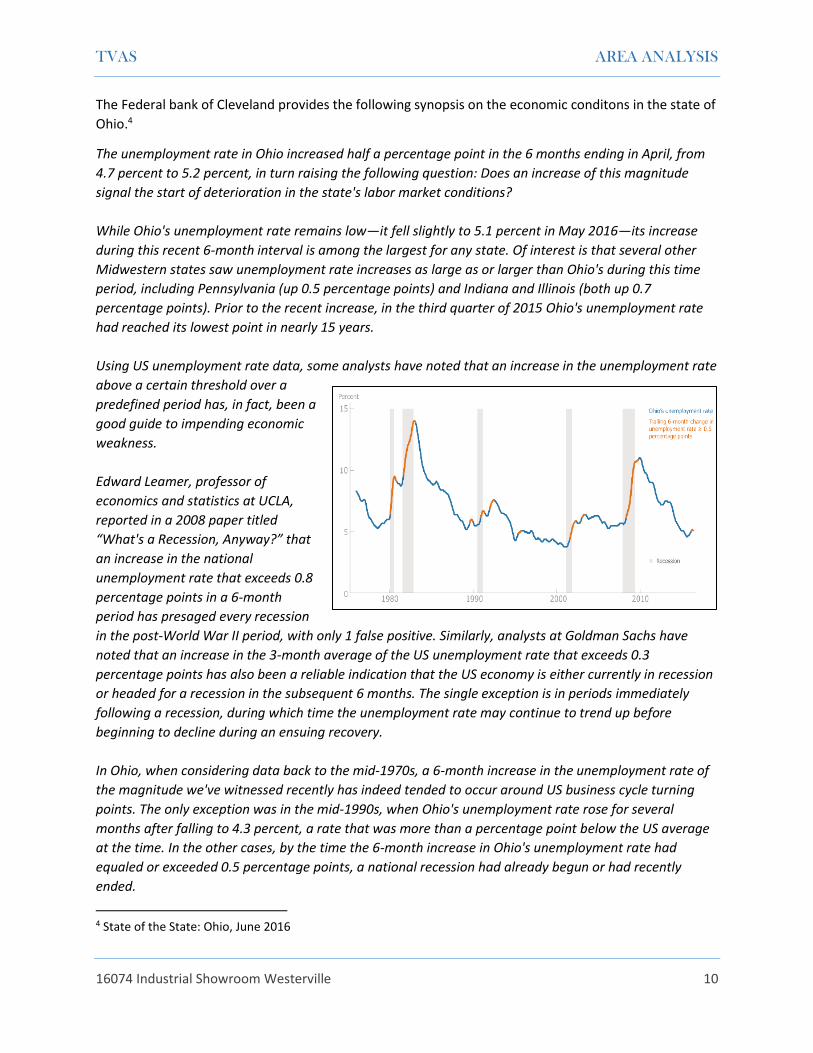

The Federal bank of Cleveland provides the following synopsis on the economic conditons in the state of

Ohio.4

The unemployment rate in Ohio increased half a percentage point in the 6 months ending in April, from

4.7 percent to 5.2 percent, in turn raising the following question: Does an increase of this magnitude

signal the start of deterioration in the state's labor market conditions?

While Ohio's unemployment rate remains low—it fell slightly to 5.1 percent in May 2016—its increase

during this recent 6-month interval is among the largest for any state. Of interest is that several other

Midwestern states saw unemployment rate increases as large as or larger than Ohio's during this time

period, including Pennsylvania (up 0.5 percentage points) and Indiana and Illinois (both up 0.7

percentage points). Prior to the recent increase, in the third quarter of 2015 Ohio's unemployment rate

had reached its lowest point in nearly 15 years.

Using US unemployment rate data, some analysts have noted that an increase in the unemployment rate

above a certain threshold over a

predefined period has, in fact, been a

good guide to impending economic

weakness.

Edward Leamer, professor of

economics and statistics at UCLA,

reported in a 2008 paper titled

“What's a Recession, Anyway?” that

an increase in the national

unemployment rate that exceeds 0.8

percentage points in a 6-month

period has presaged every recession

in the post-World War II period, with only 1 false positive. Similarly, analysts at Goldman Sachs have

noted that an increase in the 3-month average of the US unemployment rate that exceeds 0.3

percentage points has also been a reliable indication that the US economy is either currently in recession

or headed for a recession in the subsequent 6 months. The single exception is in periods immediately

following a recession, during which time the unemployment rate may continue to trend up before

beginning to decline during an ensuing recovery.

In Ohio, when considering data back to the mid-1970s, a 6-month increase in the unemployment rate of

the magnitude we've witnessed recently has indeed tended to occur around US business cycle turning

points. The only exception was in the mid-1990s, when Ohio's unemployment rate rose for several

months after falling to 4.3 percent, a rate that was more than a percentage point below the US average

at the time. In the other cases, by the time the 6-month increase in Ohio's unemployment rate had

equaled or exceeded 0.5 percentage points, a national recession had already begun or had recently

ended.

4 State of the State: Ohio, June 2016

TVAS AREA ANALYSIS

16074 Industrial Showroom Westerville 11

The national unemployment rate continues to decline, and other indicators continue to point to ongoing

growth. In addition, it's important to be cautious in interpreting the recent increase in Ohio's

unemployment rate because of the annual revision process that often changes these data in significant

ways.

A good example of such change is the most recent annual revision to the 2015 data. Initially, the

unemployment rate for June was estimated to be 5.2 percent, but it was subsequently revised down to

4.8 percent, a 0.4 percentage point change. Similarly, the initial estimate for October was reported to be

4.4 percent, but was subsequently revised up to 4.7 percent, a 0.3 percentage point change. Clearly,

revisions—which can change several years' worth of data—could eliminate the recent increase in the

state's unemployment rate.

There is a far more benign interpretation of the recent increase in Ohio's unemployment rate: It could be

the result of more people entering the labor force because they believe their likelihood of securing jobs

has improved. Indeed, after remaining relatively flat for several years at about 5.7 million workers,

Ohio's labor force has increased—and sharply. Over the 6-month periods ending in April and May, the

state's labor force grew by 2.3 percent and 2.4 percent, respectively, the largest increases in any 6-month

period since the mid-1970s.

However, these recent increases seem surprisingly large, and they therefore may not survive later

revisions. If there are downward revisions to the recent labor force estimates without meaningful

revisions to the estimates of employment, these numbers could cause a downward revision to the

unemployment rate, thereby moderating or erasing recent increases.

While increases in the unemployment rate can be a good predictor of economic conditions to come, it's

too early to conclude that a downturn is imminent. Indeed, many other indicators, including anecdotal

reports from our District contacts, continue to point to ongoing moderate growth in the economy.

Summary Ohio's unemployment rate has increased more than that of many other states during a recent

6-month span, something that could signal a turn in the business cycle; however, most indicators

continue to point to ongoing growth.

TVAS NEIGHBORHOOD ANALYSIS

16074 Industrial Showroom Westerville 12

NEIGHBOHOOD ANALYSIS A neighborhood is defined as a grouping of complimentary land uses affected by similar operations of the social, economic, governmental, and environmental forces that influence property values. Therefore, it is necessary to evaluate the dynamics of these forces within the defined neighborhood to understand their effect on the projected value of a real estate property. For purposes of our analysis, the subject neighborhood is defined as the area within a ten-minute drive of the subject property. Neighborhood Map

Overview The subject property is located on the northwest side of ''''''''''''''''''''''' '''''''''' about three-quarters of a mile south of Interstate 270 within the city limits of Columbus, Ohio. The area is comprised of commercial development on the main arterials with residential developments located on the secondary roads. '''''''''''''''''''' ''''''''', aka '''''''''' '''''''''' '''''''''' ''', is a major north–south highway which traverses from Cincinnati to Cleveland by way of Columbus. It is the second longest state route in Ohio and a major transportion route near the subject having traffic counts between 15,000 and 20,000 vehicles per day.

TVAS NEIGHBORHOOD ANALYSIS

16074 Industrial Showroom Westerville 13

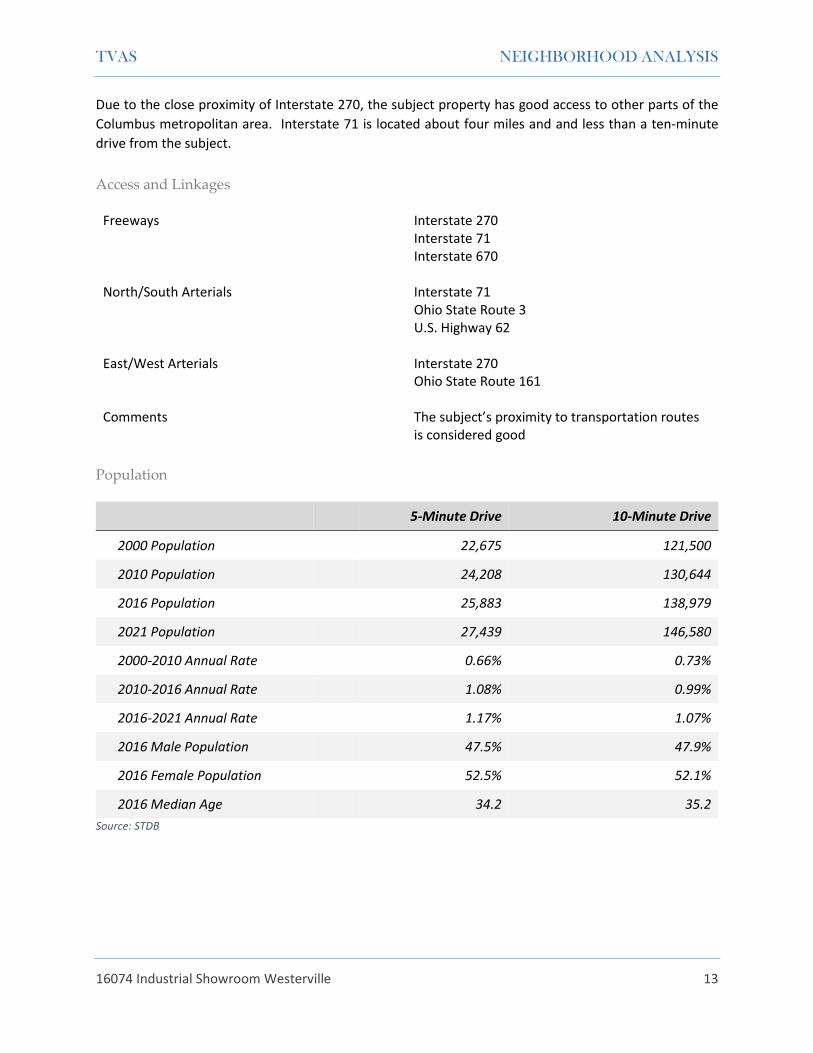

Due to the close proximity of Interstate 270, the subject property has good access to other parts of the

Columbus metropolitan area. Interstate 71 is located about four miles and and less than a ten-minute

drive from the subject.

Access and Linkages

Freeways Interstate 270 Interstate 71 Interstate 670

North/South Arterials Interstate 71

Ohio State Route 3 U.S. Highway 62

East/West Arterials Interstate 270

Ohio State Route 161 Comments The subject’s proximity to transportation routes

is considered good

Population

5-Minute Drive 10-Minute Drive

2000 Population 22,675 121,500

2010 Population 24,208 130,644

2016 Population 25,883 138,979

2021 Population 27,439 146,580

2000-2010 Annual Rate 0.66% 0.73%

2010-2016 Annual Rate 1.08% 0.99%

2016-2021 Annual Rate 1.17% 1.07%

2016 Male Population 47.5% 47.9%

2016 Female Population 52.5% 52.1%

2016 Median Age 34.2 35.2

Source: STDB

TVAS NEIGHBORHOOD ANALYSIS

16074 Industrial Showroom Westerville 14

Households

5-Minute Drive 10-Minute Drive

2000 Households 9,457 50,179

2010 Households 9,809 53,705

2016 Total Households 10,408 56,953

2021 Total Households 11,008 60,069

2000-2010 Annual Rate 0.37% 0.68%

2010-2016 Annual Rate 0.95% 0.94%

2016-2021 Annual Rate 1.13% 1.07%

2016 Average Household Size 2.46 2.40

Source: STDB

Housing

5-Minute Drive 10-Minute Drive

2016 Total Housing Units 11,252 62,247

2016 Owner Occupied Housing Units 5,027 28,932

2016 Renter Occupied Housing Units 5,381 28,021

2016 Vacant Housing Units 844 5,294

2021 Total Housing Units 11,905 65,655

2021 Owner Occupied Housing Units 5,305 30,576

2021 Renter Occupied Housing Units 5,703 29,493

2021 Vacant Housing Units 897 5,586

Currently, 46.5% of the 62,247 housing units in the area are owner occupied; 45.0%, renter occupied; and 8.5% are vacant. Currently, in the U.S., 55.4% of the housing units in the area are owner occupied; 32.9% are renter occupied; and 11.7% are vacant. Median home value in the area is $157,071, compared to a median home value of $198,891 for the U.S. In five years, median value is projected to change by 2.36% annually to $176,511.

Source: STDB

TVAS NEIGHBORHOOD ANALYSIS

16074 Industrial Showroom Westerville 15

Income

5-Minute Drive 10-Minute Drive

2016 Median Household Income $52,115 $52,952

2021 Median Household Income $58,738 $60,638

2016-2021 Annual Rate 2.42% 2.75%

2016 Average Household Income $63,380 $70,399

2021 Average Household Income $70,329 $77,578

2016-2021 Annual Rate 2.10% 1.96%

2016 Per Capita Income $25,637 $28,987

2021 Per Capita Income $28,358 $31,898

2016-2021 Annual Rate 2.04% 1.93%

Source: STDB

Employment

Business Data 5-Minute Drive 10-Minute Drive

Total Businesses: 1,134 6,001

Total Employees: 16,095 95,763

Total Residential Population: 25,883 138,979

Employee/Residential Population Ratio: 0.62:1 0.69:1

Source: STDB

TVAS NEIGHBORHOOD ANALYSIS

16074 Industrial Showroom Westerville 16

Neighborhood Employment Businesses Employees

Number Percent Number Percent

Agriculture, Forestry, Fishing & Hunting 2 0.0% 6 0.0%

Mining 2 0.0% 77 0.1%

Utilities 5 0.1% 215 0.2%

Construction 361 6.0% 3,553 3.7%

Manufacturing 149 2.5% 3,489 3.6%

Wholesale Trade 154 2.6% 1,908 2.0%

Retail Trade 931 15.5% 17,174 17.9%

Motor Vehicle & Parts Dealers 118 2.0% 1,460 1.5%

Furniture & Home Furnishings Stores 52 0.9% 684 0.7%

Electronics & Appliance Stores 75 1.2% 913 1.0%

Bldg. Material & Garden Equipment & Supplies Dealers 47 0.8% 840 0.9%

Food & Beverage Stores 105 1.7% 2,706 2.8%

Health & Personal Care Stores 81 1.3% 1,117 1.2%

Gasoline Stations 31 0.5% 140 0.1%

Clothing & Clothing Accessories Stores 169 2.8% 4,078 4.3%

Sport Goods, Hobby, Book, & Music Stores 62 1.0% 855 0.9%

General Merchandise Stores 36 0.6% 2,550 2.7%

Miscellaneous Store Retailers 134 2.2% 1,194 1.2%

Non-store Retailers 20 0.3% 636 0.7%

Transportation & Warehousing 76 1.3% 1,644 1.7%

Information 125 2.1% 2,260 2.4%

Finance & Insurance 606 10.1% 5,543 5.8%

Central Bank/Credit Intermediation & Related Activities 318 5.3% 2,146 2.2%

Securities, Commodity Contracts & Other Related Activities 89 1.5% 628 0.7%

Insurance Carriers & Related Activities 199 3.3% 2,769 2.9%

Real Estate, Rental & Leasing 425 7.1% 2,611 2.7%

Professional, Scientific & Tech Services 599 10.0% 7,870 8.2%

TVAS NEIGHBORHOOD ANALYSIS

16074 Industrial Showroom Westerville 17

Legal Services 109 1.8% 702 0.7%

Management of Companies & Enterprises 1 0.0% 5 0.0%

Administrative & Support & Waste Management & Remediation 276 4.6% 4,426 4.6%

Educational Services 155 2.6% 14,322 15.0%

Health Care & Social Assistance 691 11.5% 12,654 13.2%

Arts, Entertainment & Recreation 84 1.4% 1,209 1.3%

Accommodation & Food Services 418 7.0% 9,999 10.4%

Accommodation 46 0.8% 1,505 1.6%

Food Services & Drinking Places 372 6.2% 8,495 8.9%

Other Services (except Public Administration) 657 10.9% 4,572 4.8%

Automotive Repair & Maintenance 105 1.7% 755 0.8%

Public Administration 67 1.1% 1,872 2.0%

Unclassified Establishments 216 3.6% 352 0.4%

Totals 6,001 100.0% 95,763 100.0%

Source: STDB

TVAS NEIGHBORHOOD ANALYSIS

16074 Industrial Showroom Westerville 18

Retail/Entertainment

Major Shopping Centers Distance Opened GLA SF

Columbus Square 0.82 SW 1980 534,808

Highway 161 & Cleveland Avenue

80 Stores; Anchors: Columbus Square

Bowling, Ohio Thrift Store, Applicance Smart

Northland Plaza 0.96 SW 1988 210,036

Cleveland Avenue & E. Dublin-Granville Road

24 Stores; Anchors: None

Westerville Plaza 1.33 NE 1974 226,957

Huber Village Blvd & S. State Street

10 Stores; Anchors: Kohl’s, Macy’s, OfficeMax

Easton Square 2.32 SE 1994 613,706

Morse Rd & Stelzer Rd

24 Stores; Anchors: WalMart Supercenter,

Sam’s Club, Best Buy

Northtowne Centre 2.45 SW 1969 206,750

Morse Rd & Northtowne Blvd

12 Stores; Anchors: Old Time Pottery, Aldi

Morse Centre 2.56 SW 1979 235,589

Morse Rd & Northtowne Blvd

33 Stores; Anchors: Big Lots, Guitar Center

Easton Market 2.72 SE 1998 502,111

Easton Way & Morse Crossing

34 Stores; Anchors: Dick’s Sporting Goods,

Bed Bath & Beyond

Easton Town Center 2.88 SE 1999 1,500,000

Interstate 270 & Morse Rd

260 Stores; Anchors: Costco, Macy’s,

Nordstrom, Dick’s Sporting Goods

Source: STDB

TVAS NEIGHBORHOOD ANALYSIS

16074 Industrial Showroom Westerville 19

Conclusion The demographic data indicate that the subject neighborhood is in the growth stage of the economic life cycle with moderate forecasted population and job growth. Overall, there is a large residential and employment pool within five miles of the subject. The location of the neighborhood is benefited by good local and regional accessibility and is well-served by good transportation linkages and support services. In summary, economic and demographic factors point toward a stable environment for the neighborhood in the near future. Over the long term, the prospects for stable growth remain intact with moderate prospects for net appreciation in real estate values.

TVAS MARKET ANALYSIS

16074 Industrial Showroom Westerville 20

MARKET ANALYIS

Columbus Industrial Market Overview5

The industrial market is growing. A surprising thought considering all the headlines that promise to

reshape the economic landscape; notably Great Britain opting to leave the EU and the looming

presidential election, yet industrial tenants and landlords continue to show confidence in Central Ohio.

During the second quarter of 2016, the region saw 440,487 square feet of net absorption, constituting

the 13th consecutive quarter of growth. Absorption numbers are up 8.7 percent year-over year reducing

the overall vacancy rate to 6.1 percent– a 30 basis point reduction from the second quarter of 2015.

Advances in technology and e-commerce are shaping consumer shopping preferences, and warehousing

companies are taking notice. Now tenants look to improve their logistics capabilities by moving into

modern bulk space near transportation hubs. In Central Ohio, this kind of space is leasing rapidly. Major

deals this quarter include XPO Logistics who leased 151,200 square feet at 4000 Creekside Pkwy in

Lockbourne and Coty LCD who leased 144, 236 square

feet at 147-163 Heritage Dr. in Etna.

Rising occupier demand and ever tightening market

conditions have led to an influx of construction

activity in the region. Central Ohio now has over 3.5

million square feet in the pipeline, marking the fifth

consecutive quarter of construction levels over 3

million square feet. Amazon has positioned

themselves on the forefront of this wave of

investment. The e-commerce giant will deliver two fulfillment centers to Central Ohio in 2016: one in

Etna Township and the other at the Rickenbacker Global Logistics Park in Obetz.

Leasing Activity and Trends

At the close of the second quarter, the Central Ohio industrial market signed 1.3 million square feet of

new or expanded leases, a 36 percent decrease compared to the second quarter of 2015. The Southeast

submarket showed the most demand this quarter with 486,551 square feet of leasing activity followed

by the East submarket with 177,121 square feet.

Occupier demand for quality warehouse space continues to place pressure on rental rates and reduce

availabilities. Particulary this quarter, the amount of new deals between 50,000 and 150,000 square feet

have diminished the supply of quality mid-sized warehouse space available in the market. As a result,

5 Colliers International Columbus Industrial Report Q2 2016

TVAS MARKET ANALYSIS

16074 Industrial Showroom Westerville 21

landlords are charging higher rent prices and offering less concessions to existing tenants. Moving

forward, we can expect this trend to continue until new speculative developments add supply and ease

inventory tension.

Sales Activity On the sales side, approximately 14 industrial buildings over 20,000 square feet sold during the second quarter for a total of $30,653,000, an average price per square foot of $24.18. The largest sale came from the Trident Capital who acquired the 218,000-square-foot bulk warehouse at 6150 Huntley Road for $6.4 million or $29.35 per square foot.

Industry Data and Forecast There is much speculation among investors and market experts about how the U.S. economy will perform throughout the second half of 2016, especially in lieu of worldwide current events. So far economic fundamentals are showing mixed reviews. Over the past year 2.8 million jobs were added in the U.S., and yet the overall economy plateaued; GDP recorded a sluggish 1.1 growth rate over Q1 2016– a possible result of decreased exports due to volatile markets overseas. Nevertheless, the U.S. industrial market lingers in its growth phase. According to the most recent addition of the U.S. industrial Outlook report from Colliers International, all but 12 of the 70 markets covered in the report recorded positive net absorption reducing the national vacancy rate to 6.3 percent–the lowest rate in a decade. Back home, Central Ohio continues to expand and outpace markets in Ohio and the nation. Job growth is a great indicator of this. Over the past year Central Ohio has added 20,541 which helped reduce the overall unemployment rate to 3.8 percent– well below the U.S. rate now at 5.1 percent. Looking forward, we can expect the Central Ohio industrial market to attract both occupier and investor demand as more industrial tenants view the region as a stable, growth market.

TVAS MARKET ANALYSIS

16074 Industrial Showroom Westerville 22

Q2 2016 Columbus Industrial Statistics

TVAS MARKET ANALYSIS

16074 Industrial Showroom Westerville 23

Westerville Industrial Submarket6

The Westerville industrial submarket is relatively small comprising about 1.6% of the metro inventory. It is currently second-ranked in terms of both asking rents ($7.83) and vacancy rates (0.7%) versus the overall Columbus market.

Source: CoStar

Market Outlook According to CoStar, net absorption is projected to keep pace with deliveries over the next two years as shown in the following chart.

6 CoStar Westerville Industrial Report 2Q 2016

TVAS SITE DESCRIPTION

16074 Industrial Showroom Westerville 24

SITE DESCRIPTION

Physical Characteristics

Location '''''''''' '''''''''''''''''''' ''''''''''' Westerville, Ohio 43081 The subject is located on the northwest side of ''''''''''''''''''' ''''''''''' ¾ of a mile south of Interstate 270. The subject is under the jurisdiction of the city of Columbus but has a Westerville address.

Total Land Area 2.0 Acres 87,120 SF Site Shape Mostly rectangular Topography Level Surplus/Excess Land None noted Soil Conditions We were not provided a soil report for review.

The soils that comprise the subject site appear to be of adequate support and permeability to support the existing and/or proposed structure(s). We did not observe any evidence to the contrary during our physical inspection of the property.

Environmental Considerations We are not aware of any known source of

pollution or environmental hazards noted in the area. As no gross evidence of contamination was observed, this report assumes that the site is free of contaminants. The opinion of value in this report is contingent upon no environmental hazards on or around the subject site. A Phase I environmental evaluation is suggested to verify these assumptions.

Utilities

Water Available Sewer Available Electricity Available Gas Available

TVAS SITE DESCRIPTION

16074 Industrial Showroom Westerville 25

Legal Information

Parcel Number(s) '''''''''''''''''''''''''' Current Owner ''''''''''' '''''' ''''''''''' Current Zoning L-M, Limited Manufacturing District

H-35, 35-Foot Height District City of Columbus*

*Zoning Comments According to the the city of Columbus GIS site,

the subject parcel is zoned L-M, Limited Manufacturing District. However, we could not find this particular designation in the city’s zoning ordinance. It appears the L-M designation has been retired. Our attempts to verify the subject property’s zoning were unsuccessful.

Flood Zone A Zone: Areas with a 1% annual chance of

flooding and a 26% chance of flooding over the life of a 30‐year mortgage. Because detailed analyses are not performed for such areas; no depths or base flood elevations are shown within these zones. In communities that participate in the NFIP, mandatory flood insurance purchase requirements apply to this zone.

Flood Map FEMA Flood Insurance Rate Map, Community

Panel 39049C0183K dated June 17, 2008 Wetlands/Watershed None noted Easements/Encroachments A 25-foot sanitary sewer easement traverses

through the northern quarter of the parcel and a 25-foot sewer and drainage easement traverses along the rear property line. We are not aware of any other easements or encroachments which would adversely affect the utilization of the site.

Preliminary Title Report An authoritative report of title was not provided

for review.

TVAS SITE DESCRIPTION

16074 Industrial Showroom Westerville 26

Surrounding Arterials

''''''''''''''''''''' ''''''''''

Access/Exposure Type of Street Primary No. of Lanes 2 with median turn lane Frontage 349.91 feet Access Direct No. of Curb Cuts 1 Improvements Curbs No Gutters No Sidewalks Yes Street Lighting Yes Median Yes Street Parking No

Parcel Map

TVAS SITE DESCRIPTION

16074 Industrial Showroom Westerville 27

Survey

TVAS SITE DESCRIPTION

16074 Industrial Showroom Westerville 28

Flood Zone Map

TVAS IMPROVEMENTS DESCRIPTION

16074 Industrial Showroom Westerville 29

IMPROVEMENTS DESCRIPTION

General Description

Property Type Industrial – Showroom Gross Building Area (SF) 13,125 Rentable Area (SF) 13,125 Finished Showroom/Office Area (SF) 2,125 Finished Ratio 16.2% Occupancy Owner-occupied Year Built 1995 No. of Buildings 1 No. of Stories 1 Construction Class Class S, Structural Steel-Frame Construction Quality Average Floor Area Ratio 0.151 Coverage Ratio 15.1% Parking Type Surface Parking Spaces 17 Parking Ratio 1.29 spaces/1,000 SF Loading: Grade-Level 7 (12 ft. height x 11 ft. width) Dock-high 2 (10 ft. height x 10 ft. width) Eave Height 14 feet

TVAS IMPROVEMENTS DESCRIPTION

16074 Industrial Showroom Westerville 30

Construction Details

Foundation Poured concrete slab Construction Structural steel-framed Exterior Walls Modular metal panels Roof Gable with metal standing seam. The appraiser

was not provided access to the roof.

Windows Anodized aluminum frame Entry Doors Glass storefront and metal Ventilation Appears adequate Insulation Appears adequate

Interior Elements

Interior Layout Warehouse area, finished showroom/office space, and three service bays

Walls Metal panels with insulation

Wood-frame drywall partitioning Lighting Fluorescent Restrooms Two, two-fixture

Mechanical Systems

Heating Gas FWA Cooling Package Units Electrical 3-Phase, 480/277 volts, 1200 amps Plumbing Standard piping and hot water systems assumed

TVAS IMPROVEMENTS DESCRIPTION

16074 Industrial Showroom Westerville 31

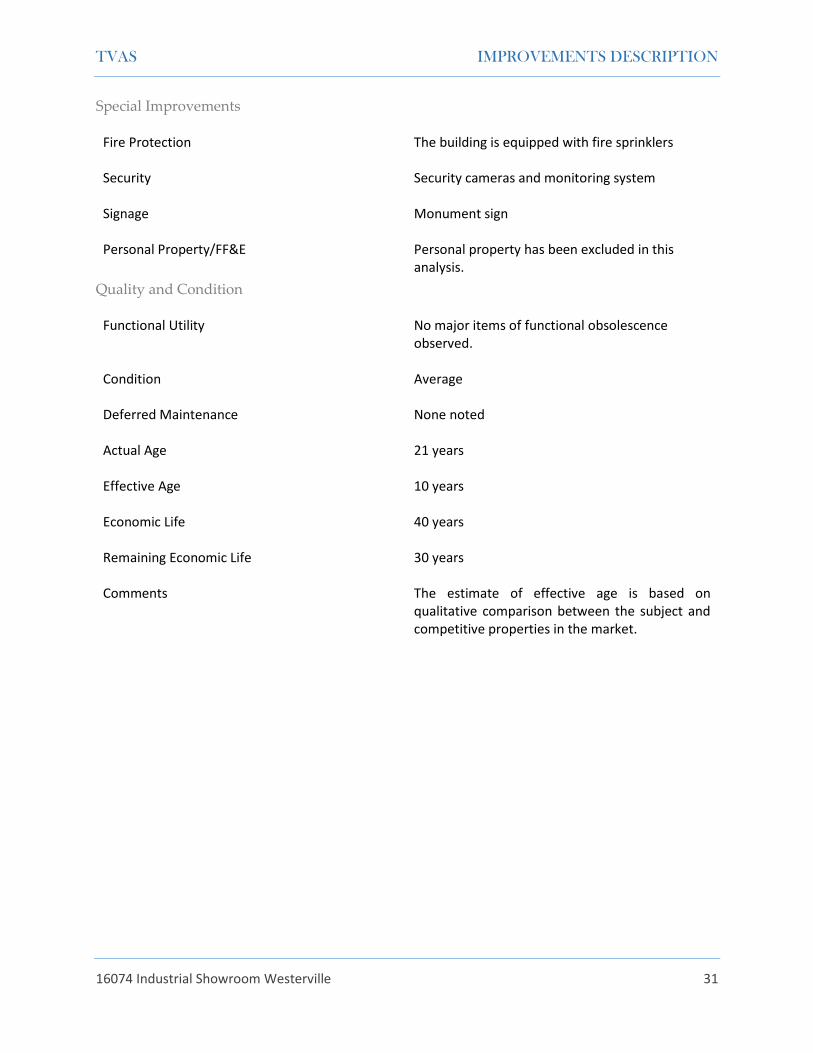

Special Improvements

Fire Protection The building is equipped with fire sprinklers Security Security cameras and monitoring system Signage Monument sign Personal Property/FF&E Personal property has been excluded in this

analysis.

Quality and Condition

Functional Utility No major items of functional obsolescence observed.

Condition Average Deferred Maintenance None noted Actual Age 21 years Effective Age 10 years Economic Life 40 years Remaining Economic Life 30 years Comments The estimate of effective age is based on

qualitative comparison between the subject and competitive properties in the market.

TVAS IMPROVEMENTS DESCRIPTION

16074 Industrial Showroom Westerville 32

Improvements Sketch

TVAS ZONING

16074 Industrial Showroom Westerville 33

ZONING

Zoning Summary

Zoning Jurisdiction City of Columbus Zoning Designation L-M, Limited Manufacturing District

H-35, 35-Foot Height District* *Comments According to the the city of Columbus GIS site,

the subject parcel is zoned L-M, Limited Manufacturing District. However, we could not find this particular designation in the city’s zoning ordinance. It appears the L-M designation has been retired. Our attempts to verify the subject property’s zoning were unsuccessful.

Legally Conforming? Assumed to be legally conforming Zoning Change Likely? No

TVAS ZONING

16074 Industrial Showroom Westerville 34

Zoning Map

TVAS REAL ESTATE TAXES AND ASSESSMENT

16074 Industrial Showroom Westerville 35

REAL ESTATE TAXES AND ASSESSMENT

Introduction In Ohio all real property types similar to the subject are required to be assessed at 35% of the fair market value unless otherwise specified by law. Property is assessed at the county level by the Auditor’s Office. Ohio law requires counties to revalue all real property every six years with an update at the three year midpoint as ordered by the Tax Commissioner of the State of Ohio. Franklin County is scheduled for a reappraisal in 2017.

Current Property Tax Liability The subject property is under the tax jurisdiction of Columbus, Ohio. The 2015 millage rate for properties

located in Columbus was $80.798968 per $1,000 of assessed value. The millage rate for 2016 has not

been determined. The following table summarizes the 2015 property tax liability for the subject property.

Parcel No. ''''''''''''''''''''''''''

Tax Year 2015

Tax-Appraised Value: Land Value $155,300

Improvement Value $419,700

Total Tax-Appraised Value $575,000

Times 35% Assessment 0.35

Assessed Value $201,260

Times Current Millage Rate 0.080798968

Total Property Taxes $16,261.60

According to the Franklin County Treasurer, the 2015 taxes for the subject property have been paid as of

the effective date of this report.

TVAS HIGHEST AND BEST USE

16074 Industrial Showroom Westerville 36

HIGHEST AND BEST USE

Introduction Highest and best use is defined as the reasonably probable and legal use of vacant land or an improved property.7 The four criteria the highest and best use must meet are:

◻ Legal Permissibility – a property use that is either currently allowed or most probably allowable under zoning codes, building codes, environmental regulations, and other applicable laws and regulations that govern land use;

◻ Physical Possibility – the land must be able to accommodate the size and shape of the ideal improvement;

◻ Financial Feasibility – the ability of a property to generate sufficient income to support the

use for which it was designed; and

◻ Maximum Productivity – the selected land use must yield the highest value of the possible uses.

Highest and Best Use as Vacant Legally Permissible The zoning regulations in effect at the time of the appraisal determine the legal permissibility of a potential use of the subject site. As described in the Zoning Section of this report, the subject parcel is zoned L-M, Limited Manufacturing District. However, we could not find this particular designation in the city’s zoning ordinance. It appears the L-M designation has been retired. Our attempts to verify the subject property’s zoning were unsuccessful. Based on the existing code, a number of commercial uses would be permitted in a “limited manufacturing” type of designation. Additionally, given the character of the area and the location of the subject within the district, a change in zoning is considered improbable. Physically Possible The physical possibility of a use is dictated by the size, shape, topography, availability of utilities, and any other physical aspects of the site. The subject property consists of a legal tax parcel containing 2.0 acres or 87,120 square feet. The site is mostly rectangular in shape and level with the street grade. The subject site has frontage along ''''''''''''''''''''' ''''''''''' with good exposure. All utilities are available to the site. A 25-foot sanitary sewer easement traverses through the northern quarter of the parcel and a 25-foot sewer

7 Appraisal Institute, The Dictionary of Real Estate Appraisal, Fifth Ed., (Chicago: Appraisal Institute, 2002)

TVAS HIGHEST AND BEST USE

16074 Industrial Showroom Westerville 37

and drainage easement traverses along the rear property line. The physical characteristics are considered adequate to accommodate most types of permitted development. Financially Feasible and Maximally Productive Financially feasible uses are those uses that can generate an income or return greater than or equal to the costs of development. Of the uses that are permitted, possible, and financially feasible, the one that will result in the maximum value for the property is considered the highest and best use. Conclusion We considered the legal issues related to zoning and legal restrictions. We also analyzed the physical characteristics of the site to determine what legal uses would be possible, and considered the financial feasibility of these uses to determine the use that is maximally productive. Considering the subject site’s physical characteristics and location, as well as the state of the local market, it is our opinion that the Highest and Best Use of the subject site as vacant is commercial use developed in accordance with the predominant supply and demand characteristics of the local market.

Highest and Best Use as Improved The Dictionary of Real Estate Appraisal defines highest and best use of the property as improved as: The use that should be made of a property as it exists. An existing improvement should be renovated or retained as is so long as it continues to contribute to the total market value of the property, or until the return from a new improvement would more than offset the cost of demolishing the existing building and constructing a new one. In analyzing the Highest and Best Use of a property as improved, it is recognized that the improvements should continue to be used until it is financially advantageous to alter physical elements of the structure or to demolish it and build a new one. Legally Permissible As described in the Zoning Section of this report, the subject parcel is zoned L-M, Limited Manufacturing District. However, we could not find this particular designation in the city’s zoning ordinance. It appears the L-M designation has been retired. Our attempts to verify the subject property’s zoning were unsuccessful. The site is improved with an industrial showroom building containing 13,125 square feet of gross building area which was constructed in 1995. It is assumed the improvements are legally conforming. Physically Possible The subject improvements are considered to be in average condition and appear be adequately maintained. There are no apparent major items of functional obsolescence or deferred maintenance. We know of no current or pending municipal actions or covenants that would require a change to the current improvements.

TVAS HIGHEST AND BEST USE

16074 Industrial Showroom Westerville 38

Financially Feasible and Maximally Productive In our opinion, the improvements provide a substantial value contribution to the property as a whole. Therefore, continued use of the existing improvements is financially feasible. The maximally productive use of the subject property as improved is for continued use of the existing improvements.

Most Likely Buyer The most probable buyer of the subject property would be an owner-occupant.

TVAS VALUATION PROCESS

16074 Industrial Showroom Westerville 39

VALUATION PROCESS

Methodology The thee generally accepted approaches to developing an opinion of value are the Cost Approach, the Sales Comparison Approach and Income Capitalization Approach. The applicability of each approach is considered based on the quality of market data and the motivation of market participants. The type and reliability of data and the applicability of each approach is then considered and reconciled into a final value estimate.

Cost Approach The Cost Approach is based on the principle of substitution, where an informed purchaser would pay no more for the subject than the cost to produce a substitute property with equivalent utility. This approach is particularly applicable when the property being appraised involves relatively new improvements which represent the highest and best use of the land or when relatively unique or specialized improvements are located on the site for which market data of comparable properties is difficult to obtain. The Cost Approach is also appropriate when existing improvements are reaching the end of their economic life and/or when the underlying land comprises the majority of the total property value. In these instances, the Cost Approach isolates the largest component of value by developing a full evaluation of the underlying land.

Sales Comparison Approach The Sales Comparison Approach is also based on the principle of substitution. This approach uses a market-based unit of comparison such as price per square foot, price per unit, etc. for analysis of the sales. The strength of this approach is its wide market acceptance among investors who often evaluate comparable properties on a price per unit means of comparison. In this approach, sales of comparable properties are identified and then adjustments are applied to the unit of comparison from an analysis of comparable sales. The adjusted unit of comparison is then used to derive an opinion of value for the subject property.

Income Capitalization Approach The Income Capitalization Approach reflects the subject property’s income-producing capabilities. This approach is based on the assumption that value is created by the expectation of benefits to be derived in the future. The two common valuation techniques associated with the Income Capitalization approach are direct capitalization and discounted cash flow (DCF) analysis.

TVAS VALUATION PROCESS

16074 Industrial Showroom Westerville 40

Summary The Cost Approach was considered but not deemed to be applicable in the valuation of the subject property. The age of the improvements renders an accurate estimate of depreciation difficult to obtain. The Sales Comparison Approach represents the primary method by which the fee simple interest in similar properties is evaluated. As such, this approach was given primary consideration in the reconciliation. In the Income Capitalization Approach, market rent was utilized for the subject’s forecasted operating statement. After estimating gross income, deductions were made for ownership and operational expenses. The resulting net operating income was then converted into an indication of value by means of direct capitalization. As the typical buyer profile for the subject property is an owner-occupant, this approach was given secondary consideration in the reconciliation.

TVAS SALES COMPARISON APPROACH

16074 Industrial Showroom Westerville 41

SALES COMPARISON APPROACH

Summary of Comparable Improved Sales Data

Subject Sale 1 Sale 2 Sale 3 Sale 4 Sale 5 Sale 6

Location Details

Address ''''''''' '''''''''''''''''''' '''''' 6900 Americana Pkwy 5130 Transamerica Dr 1849 Westbelt Dr 4751 Poth Rd 8010 Dove Pkwy 132 Johnson Dr

Westerville Reynoldsburg Columbus Columbus Whitehall Canal Winchester Delaware

Parcel No(s). ''''''''''''''''''''''''''''''' 540-234799-00 560-235123-00 560-210801-00 090-008263-00 428376370 428376390

419-210-01-006-004

Transaction Data

Date of Sale 4/1/2016 8/1/2016 5/3/2016 6/8/2015 3/11/2016 1/22/2016

Sale Price $1,100,000 $525,000 $670,000 $630,000 $650,000 $695,000

Price/SF $63.99 $82.03 $60.91 $55.35 $54.49 $58.19

Grantor Donald S. Trasin Spring Properties, Ltd. Ralph Steven Marcus et al

Trifecta Investments Ltd.

Jack H. Graham Engineered

Material Systems

Grantee Armor & Anchor, LLC Area Endeavors, Ltd. GMD Silver, Inc. Central America Distributors, LLC

380 W Muskegon, LLC

Wolfrum & Cline Realty Investors

Physical Attributes

GBA (SF) 13,125 17,190 6,400 11,000 11,382 11,928 11,944

Year Built 1995 1996 1997 1989 1996 2002 1997

Site Size (SF) 87,120 157,687 47,524 45,694 59,939 177,899 78,582

Finish Ratio 16.2% 16.3% 18.7% 27.0% 16.0% 16.8% 33.0%

Parking Ratio 1.29/1,000 SF 1.63/1,000 SF 2.66/1,000 SF 1.09/1,000 SF 2.11/1,000 SF 3.27/1,000 SF 1.84/1,000 SF

Coverage Ratio 15.1% 10.9% 13.5% 24.0% 19.0% 6.7% 15.2%

Eave Height 14 ft 17 ft 16 ft 20 ft 17 ft 18 ft 18 ft

Loading 7 GL/2 DH 4 GL/0 DH 1 GL/1 DH 1 GL/2 DH 1 GL/1 DH 6 GL/0 DH 1 GL/2 DH

Loading/SF 1,458 4,298 3,200 3,667 5,691 1,988 3,981

Verification

Donald Trasin Seller

(614) 866-6980

Public Record Ryan McGreevy NAI Ohio Equities (614) 629-5282

Daniel Goss Coldwell Banker (614) 889-0808

Public Record Public Record

TVAS SALES COMPARISON APPROACH

16074 Industrial Showroom Westerville 42

Comparable Sale 1

Comparable Sale 2

TVAS SALES COMPARISON APPROACH

16074 Industrial Showroom Westerville 43

Comparable Sale 3

Comparable Sale 4

TVAS SALES COMPARISON APPROACH

16074 Industrial Showroom Westerville 44

Comparable Sale 5

Comparable Sale 6

TVAS SALES COMPARISON APPROACH

16074 Industrial Showroom Westerville 45

Comparable Improved Sales Map

TVAS SALES COMPARISON APPROACH

16074 Industrial Showroom Westerville 46

Comparable Improved Sales Adjustment Grid

Subject Sale 1 Sale 2 Sale 3 Sale 4 Sale 5 Sale 6

Address ''''''''' ''''''''''''''''''''

6900 Americana Pkwy

5130 Transamerica Dr

1849 Westbelt Dr 4751 Poth Rd 8010 Dove Pkwy 132 Johnson Dr

Westerville Reynoldsburg Columbus Columbus Whitehall Canal Winchester Delaware

Sale Price $1,100,000 $525,000 $670,000 $630,000 $650,000 $695,000

Gross Building Area (SF) 13,125 17,190 6,400 11,000 11,382 11,928 11,944

Price/SF $63.99 $82.03 $60.91 $55.35 $54.49 $58.19

Transactional Adjustments

Property Rights Fee Simple Fee Simple Fee Simple Fee Simple Fee Simple Fee Simple

Adjustment 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Adjusted Sale Price/SF $63.99 $82.03 $60.91 $55.35 $54.49 $58.19

Cash Equivalency Assumed Market Assumed Market Assumed Market Assumed Market Assumed Market Assumed Market

Adjustment 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Adjusted Sale Price/SF $63.99 $82.03 $60.91 $55.35 $54.49 $58.19

Conditions of Sale None None None None None None

Adjustment 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Adjusted Sale Price/SF $63.99 $82.03 $60.91 $55.35 $54.49 $58.19

Market Conditions 4/1/2016 8/1/2016 5/3/2016 6/8/2015 3/11/2016 1/22/2016

Adjustment 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Adjusted Sale Price/SF $63.99 $82.03 $60.91 $55.35 $54.49 $58.19

Property Adjustments

Location 0.0% 10.0% 20.0% 15.0% 20.0% 20.0%

GBA (SF) 13,125 6.0% -20.0% -3.0% -2.0% -1.0% -1.0%

Condition/Quality Average -10.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Finish Ratio 16.2% 0.0% 0.0% -3.0% 0.0% 0.0% -6.0%

Parking Ratio 1.29/1,000 SF 0.0% -5.0% 0.0% 0.0% -5.0% 0.0%

Coverage Ratio 15.1% 0.0% 0.0% 0.0% 0.0% -5.0% 0.0%

Eave Height 14 ft -3.0% -1.0% -6.0% -3.0% -4.0% -4.0%

Loading 7 GL/2 DH 5.0% 2.0% 2.0% 3.0% 3.0% 2.0%

Net Adjustment -2.0% -14.0% 10.0% 13.0% 8.0% 11.0%

Adjusted Sale Price/SF $62.71 $70.55 $67.00 $62.55 $58.85 $64.59

TVAS SALES COMPARISON APPROACH

16074 Industrial Showroom Westerville 47

Comparable Improved Sales Analysis Property Rights Conveyed All the comparable sales analyzed included a transfer of the fee simple interest and no adjustments were deemed necessary after comparison of the adjusted sales. Financing/Cash Equivalency Data related to mortgage rates for the comparable sale transactions were unavailable, but most appear to have been financed with new conventional loans or purchased all-cash. It is assumed that the financing terms for the comparable sale transactions were market-oriented. No adjustments have been applied under this category. Conditions of Sale Market value of the subject property is based on the premise of an arms-length transaction for properties exposed to the market for a reasonable length of time. All of the comparable sales are believed to be arms-length transactions or sold at market value. Market Conditions According to CoStar Group8, no discernible trend in pricing is evident in the Columbus industrial market as shown in the chart below. According to Ryan McGreevy of NAI Ohio Equities, industrial sale prices have remained stable in the subject’s market area. No adjustments were indicated for changes in market conditions.

Source: CoStar

8 Columbus Economic Overview 3Q 2016

TVAS SALES COMPARISON APPROACH

16074 Industrial Showroom Westerville 48

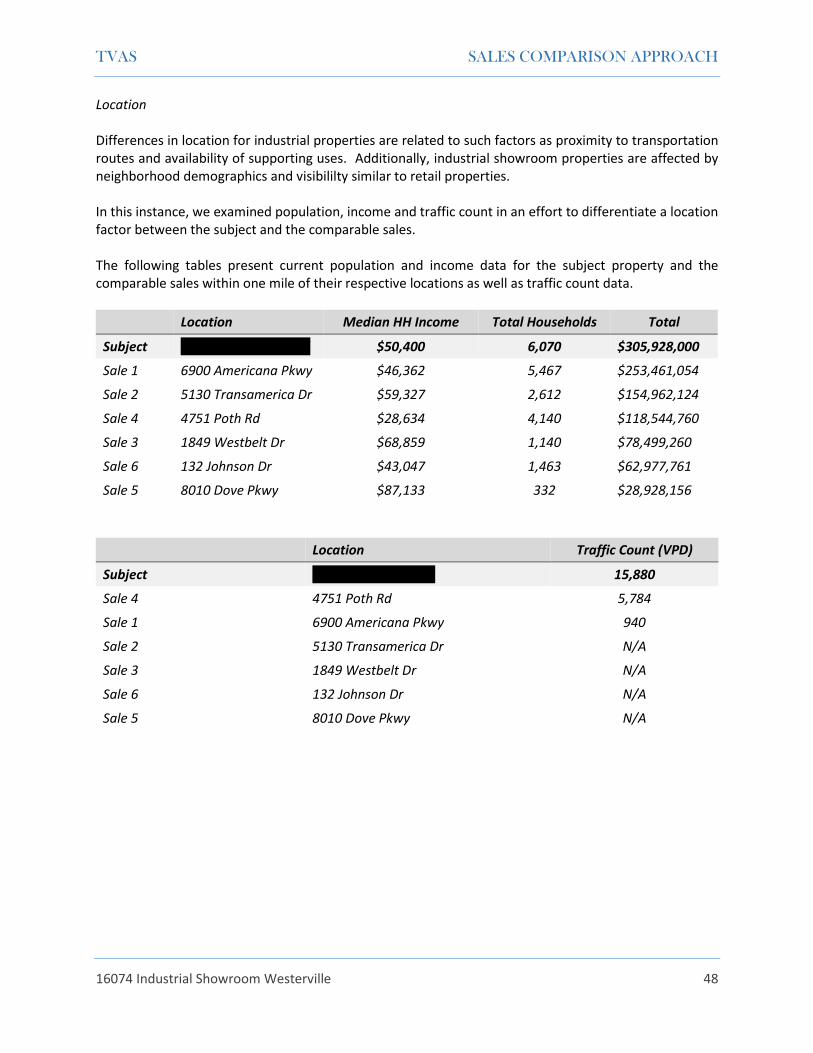

Location Differences in location for industrial properties are related to such factors as proximity to transportation routes and availability of supporting uses. Additionally, industrial showroom properties are affected by neighborhood demographics and visibililty similar to retail properties. In this instance, we examined population, income and traffic count in an effort to differentiate a location factor between the subject and the comparable sales. The following tables present current population and income data for the subject property and the comparable sales within one mile of their respective locations as well as traffic count data.

Location Median HH Income Total Households Total

Subject '''''''''' '''''''''''''''''''''' '''' $50,400 6,070 $305,928,000

Sale 1 6900 Americana Pkwy $46,362 5,467 $253,461,054

Sale 2 5130 Transamerica Dr $59,327 2,612 $154,962,124

Sale 4 4751 Poth Rd $28,634 4,140 $118,544,760

Sale 3 1849 Westbelt Dr $68,859 1,140 $78,499,260

Sale 6 132 Johnson Dr $43,047 1,463 $62,977,761

Sale 5 8010 Dove Pkwy $87,133 332 $28,928,156

Location Traffic Count (VPD)

Subject ''''''''' '''''''''''''''''''' ''''' 15,880

Sale 4 4751 Poth Rd 5,784

Sale 1 6900 Americana Pkwy 940

Sale 2 5130 Transamerica Dr N/A

Sale 3 1849 Westbelt Dr N/A

Sale 6 132 Johnson Dr N/A

Sale 5 8010 Dove Pkwy N/A

TVAS SALES COMPARISON APPROACH

16074 Industrial Showroom Westerville 49

Applied location adjustments are summarized in the following table.

Location Population/Income Traffic Counts Applied

Adjustment

Sale 1 6900 Americana Pkwy 0% 0%* 0%

Sale 2 5130 Transamerica Dr 0% 10% 10%

Sale 4 4751 Poth Rd 10% 5% 15%

Sale 3 1849 Westbelt Dr 10% 10% 20%

Sale 6 132 Johnson Dr 10% 10% 20%

Sale 5 8010 Dove Pkwy 10% 10% 20%

*Although Sale 1 is accessed from a road with a low traffic count, the parcel has good frontage and visibility from Interstate 70. No adjustment for traffic count was deemed necessary.

Building Size Differences in this category are attributable to the concept of economies of scale whereby larger properties would sell for a lower price per unit than smaller properties and vice versa. The following table summarizes the adjustments applied to the comparable sales.

Gross Building Area

(SF) Difference (SF) Applied Adjustment

Sale 1 17,190 4,065 6%

Subject 13,125

Sale 6 11,944 1,181 -1%

Sale 5 11,928 1,197 -1%

Sale 4 11,382 1,743 -2%

Sale 3 11,000 2,125 -3%

Sale 2 6,400 6,725 -20%

Condition/Quality Adjustments under this category account for differences in the estimated effective age of the subject property relative to the comparable data set. Differences in construction, quality and appeal are also considered in this category. The subject property is an industrial showroom building constructed in 1995. The estimated effective ages of all of the comparable sales were sufficiently similar to the effective age of the subject. Adjustments were based on inspection of interior photographs and broker comments when available. A downward adjustment was applied to Comparable 1 based superior construction quality.

TVAS SALES COMPARISON APPROACH

16074 Industrial Showroom Westerville 50

Showroom/Office Ratio The subject building is improved with 2,125 square feet of showroom/office area which equates to a finished ratio of 16.2%. Adjustments for differences in finished ratios are based on a contributory value estimate of $20 per square foot. The adjustments applied under this category are exhibited in the table below.

Comparable Sale 1 2 3 4 5 6

Finished Differential (SF)* -17 -160 -1,188 23 -71 -2,007

Contributory Value $20/SF -$340 $-3,200 -$23,760 $460 -$1,420 $-40,140

Sale Price^ $1,100,000 $525,000 $670,000 $630,000 $650,000 $695,000

Implied Adjustment 0% 0% -3% 0% 0% -6%

Applied Adjustment 0% 0% -3% 0% 0% -6% *Difference between the subject’s finished ratio applied to the comparable and the comparable finished space.

^Adjusted sale price prior to physical adjustments

Parking Ratio

Parking ratios were determined by the number of dedicated parking spaces on asphalt surfaces. Downward adjustments were applied to comparable sales 2 and 5 which have sufficiently higher parking ratios relative to the subject property. All of the other comparable sales were similar to the subject and were not adjusted. Coverage Ratio The subject’s 13,125-square-foot building is situated on a 87,120-square-foot site, resulting in a coverage ratio of 15.1%. A downward adjustment was applied to Comparable Sale 5 due to a superior coverage ratio. We considered location, frontage and orientation of the existing improvements in estimating the contributory value of the excess land. The adjustment applied under this category is exhibited in the table below.

Comparable Sale 5

Estimated Contributory Value of Excess Land $32,000 Sale Price^ $650,000

Implied Adjustment -5% ^Adjusted sale price prior to physical adjustments

TVAS SALES COMPARISON APPROACH

16074 Industrial Showroom Westerville 51

Eave Height The subject building’s minimum clear height was measured to 14 feet. All of the comparable sales have higher clear heights relative to the subject and were adjusted downward. Adjustments were based on our experience utilizing capitalized rent adjustments. In this instance, a rental difference of $0.05 per linear foot of clear height was capitalized at our estimated capitalization rate of 8.5% indicating a contributory value of $0.59 per linear foot. The adjustments applied under this category are exhibited in the table below.

Comparable Sale 1 2 3 4 5 6

Height Differential (Feet) -3 -2 -6 -3 -4 -4