are 2 incomes necessary? common misconception – 2 incomes are necessary to live on in today’s...

TRANSCRIPT

Are 2 incomes necessary?

Common misconception – 2 incomes are necessary to live on in today’s society

On average, a 2nd income needs to be $25,000 a year to break even assuming $500 a month in day care costs and

increased expenses for commuting, meals out, dry cleaning, clothing, and etc.

2nd income calculator (linked on webCT – Pearls of Wisdom):

http://moneycentral.msn.com/investor/calcs/n_spwk/main.asp

• This site says: You might be surprised at how little extra income your family gets when both spouses work. To determine whether it's worthwhile,

What does it cost to work?

Opportunity cost Out-of-pocket costs

Day care or care for a dependent relative Taxes Retirement plans Union or professional dues Office collections Added household expenses Health insurance Transportation Clothing and personal care Meals & coffee breaks at work Others?

Parental Investments in Children

Extensive marginal investment - expanding a household’s investment in children by having an additional child, holding other resource allocations constant.

Intensive marginal investment - expanding a household’s investment in children by devoting more resources to the children in the household, holding numbers constant.

Watch “William Tell Overture”

Trends in U.S. Fertility Over Time

Kids are fun!

Today, Intensive Investments in Children Take Many Forms... Direct money expenditures designed

to enhance their human capital (e.g., food, clothing, braces)

Expenditures of time and energy directed at enhancing their human capital (e.g., child care time, helping with homework, coaching soccer)

Total Direct Expenditures on One Child, 0-17 (USDA, 2006– Study based on Husband/Wife hhs with 2 children-- Highest Income Group; Middle Inc Grp; Lowest Inc Grp)

$190,050

$260,700

$381,050

$0 $100,000 $200,000 $300,000 $400,000 $500,000

Total $Expenditures

HighestMiddleLowest

http://www.cnpp.usda.gov/Publications/CRC/crc2006.pdf

Adjustments for different numbers of children...

These estimates are for the younger child of a 2 child family.

Costs are 24% higher for families with one child. Costs are 23% less per child for families with 3+

children

THESE ADJUSTMENTS REFLECT ECONOMIES OF SCALE!

These expenditure estimates do not account for...

Post-secondary education expenditures Investments in children made by other family

members outside of the immediate household Government expenditures on children Opportunity costs of these investments Time-related investments in children

Implications...

Family sizes have fallen over the past 60 years, while direct or primary child care time has increased.

This implies a huge increase in investments in children at the intensive margin.

But, is direct child care time, the only investment time?

Saving For a Child’s Education

Is it possible?

How can I/we do it?

Estimate Cost

Current estimates are about $100,000 for 4 years of education in 18 years for public schools, and $200,000 for privateAssumes 5% annual inflation

• Realistic?

How to finance?

Bottom line START NOW! Only have 18 years, so an aggressive

stance is vital Take advantage of investing with tax

breaks

Financing Alternatives

Roth IRACan withdraw earnings tax-free, if have

held account for 5 yearsCan use money in your Roth for yourself,

your spouse, your child, or your grandchildDownside?

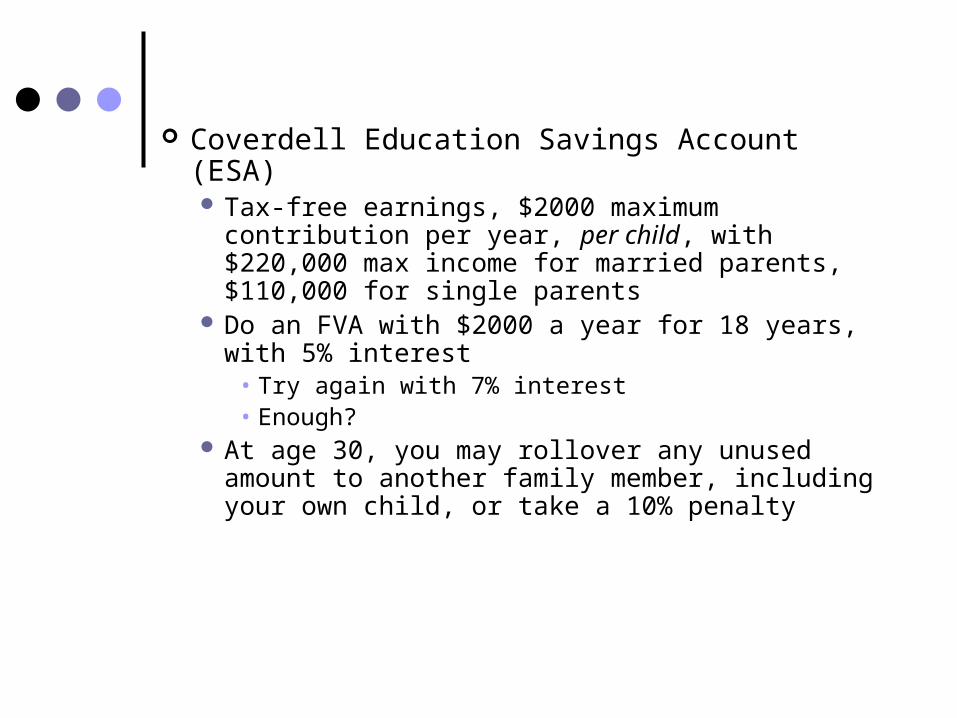

Coverdell Education Savings Account (ESA) Tax-free earnings, $2000 maximum

contribution per year, per child, with $220,000 max income for married parents, $110,000 for single parents

Do an FVA with $2000 a year for 18 years, with 5% interest

• Try again with 7% interest• Enough?

At age 30, you may rollover any unused amount to another family member, including your own child, or take a 10% penalty

State 529 plans (or state college saving plans)Contributions are tax-deferred, and when used

to finance education, are taxed at student’s tax rate

• New law: Tax-free if withdrawn before 2010If money is not used for college expenses,

penalties are up to 15% of the earnings, or 1% of the total balance

Utah’s plan info available at www.uesp.org or by calling 800-418-2551

Upromise.com

Series EE government savings bondsInterest is tax-free if used to pay for

college• Have to buy the bond in your name, not

your child’s• Full deduction up to income of $81,100

for joint filers• Parent must be at least 24 years old at

time of purchase

Invest in your child’s nameUnder age 14:

• $750 a year in interest income is earned tax-free

• Next $750 in earned interest is taxed at child’s tax rate (10%)

• Over $1500 is taxed at parent’s rate

Over 14:• Income up to $5250 = 10%• Income up to $27,050 = 15%