are employee stock options liabilities or equity? · are employee stock options liabilities or ......

TRANSCRIPT

Are Employee Stock Options Liabilities or Equity?

Mary E. Barth Stanford University

Leslie D. Hodder Indiana University

Stephen R. Stubben The University of North Carolina at Chapel Hill

October 2011

We wish to thank Patrick Hopkins, Jim Wahlen, Michael Kirschenheiter, Stephen Penman, and workshop participants at The Wharton School of the University of Pennsylvania, Florida International University, Harvard University, Oklahoma University, Singapore Management University, and Brigham Young University for helpful discussions and comments. Leslie Hodder gratefully acknowledges financial support from Ernst and Young, LLC.

Are Employee Stock Options Liabilities or Equity?

Abstract

This study seeks to determine whether employee stock options have characteristics of liabilities

or equity, which is an open financial reporting question. As predicted, we find that common

equity risk and expected return are negatively associated with the extent to which a firm has

outstanding employee stock options, which is inconsistent with the options having characteristics

of liabilities. We also find that the association is less negative for firms that reprice options and

firms that have longer-term options, which indicates that some employee stock options have

characteristics that make them more similar to debt. In addition, we find that the sensitivity of

employee stock option value to changes in asset value mirrors that of common equity value and

is opposite to that of debt value. The evidence also reveals that, unlike liabilities, employee

stock options have substantially higher risk and expected return than common equity. Our

findings are not consistent with classifying employee stock options as liabilities for financial

reporting purposes; rather, the options act as a second type of equity. Our analyses and findings

suggest a classification scheme for claims against the firm—namely, classify as liabilities

(equity) claims that increase (decrease) common equity risk and expected return.

1

Are Employee Stock Options Liabilities or Equity?

I. INTRODUCTION

We address whether employee stock options have characteristics of liabilities or of

equity. In particular, we seek to understand the relation between employee stock options and the

risk of and expected return on common equity. This understanding is important in assessing the

role of employee stock options in the capital structure of the firm, and is relevant to the debate

about whether employee stock options should be classified as liabilities or equity for financial

reporting purposes. Our tests focus on the signs of the associations between the risk of and

expected return on the firm’s common equity and the extent to which a firm has outstanding

employee stock options. Finance theory predicts that leverage increases the risk of and expected

return on common equity. Thus, if the associations between employee stock options and

common equity risk and return are positive, we infer that employee stock options have

characteristics of liabilities. If the associations are negative, we infer the opposite. We find that

the extent to which a firm has outstanding employee stock options is significantly negatively

related to both common equity risk and the expected return on common equity, which is

inconsistent with employee stock options having characteristics of liabilities.

Our study is relevant to the current financial reporting debate about what characteristics

should distinguish liabilities and equity for financial reporting purposes. Thus far, the Financial

Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB)

have been unable to develop a clear principle that distinguishes liabilities from equity for

financial reporting. There is no debate about whether existing common stock should be

classified as equity and straight debt should be classified as liabilities. However, equity for

financial reporting need not be limited to existing common equity. The debate is about whether

2

financial instruments embodying other types of claims against the firm’s assets should be

classified as other types of equity or as liabilities and, if so, what characteristics of those

instruments are relevant to determining the classification.

The FASB’s current Conceptual Framework defines equity as the residual of assets minus

liabilities, where liabilities are present obligations, the settlement of which requires a transfer of

the firm’s assets. However, this characterization of liabilities is subject to criticism because

determining whether a present obligation exists is subjective, and because the form of settlement

is subject to structuring. For these reasons, a growing body of literature and the FASB’s

Preliminary Views on how to account for financial instruments with characteristics of equity

advocate classifying all claims other than common stock as liabilities. This is referred to as the

“basic ownership” approach because it would classify only basic ownership instruments, i.e.,

common stock, as equity and classify all other claims as liabilities. Under the basic ownership

approach, most preferred stock and contingent claims—including employee stock options—

would be classified as liabilities, unless they are specifically exempted from the approach. In

part because of this, there has been resistance to adopting the basic ownership approach. We

inform this debate by showing that the relation between a financial claim and the risk of and

expected return on existing common equity—for which there is no financial reporting

classification debate— can be used to distinguish liabilities from equity.

Our predictions and tests are based on warrant pricing theory. Although the value of

employee stock options is commonly estimated using option pricing models, employee stock

options are warrants. For our study, a key difference between warrants and options is that the

two types of instruments differ with respect to the entity responsible for their settlement. In

particular, whereas warrants are claims against and settled by the firm, options on a firm’s shares

3

are claims against other entities that wrote options on a firm’s shares. Because warrants are

issued and settled by the firm, the issuance of warrants—e.g., employee stock options—should

affect the risk of and expected return on all existing equity claims. Theory predicts that the

issuance of warrants decreases the expected risk of and return on the firm’s common equity,

which is consistent with employee stock options de-levering the firm’s common equity, not

levering it as do liabilities. This is not true of options on the firm’s shares written by other

entities, which have no effect on the firm’s capital structure.

Although finance theory outlines the implications of employee stock options for common

equity risk and expected return, empirical tests of these implications are absent from the

literature. We fill this void by testing the relations between common equity risk and expected

return and the extent to which the firm has employee stock options outstanding. First, we test

whether common equity risk is positively or negatively associated with the extent to which a

firm has employee options outstanding. We use two measures of common equity risk—realized

common equity volatility and common equity volatility implied by the prices of a firm’s traded

options. Following prior research, our tests include controls for leverage, credit risk, firm size,

earnings, change in earnings, and analyst forecasts of earnings growth. In addition, because

riskier firms might issue more options and because options can provide incentives for risk-

taking, we also include controls for a firm’s propensity to issue options and for subsequent risky

investment. Second, we test whether the expected return on common equity is positively or

negatively associated with the extent to which a firm has employee options outstanding. Our

measure of expected return is an estimate of expected cost of capital based on the Fama-French

and momentum factors. Following prior literature, our expected return tests include controls for

4

leverage, firm size, equity book-to-market ratio, beta, momentum, analyst forecasts of earnings

growth, and dispersion in analyst forecasts.

We find that common equity risk is significantly negatively associated with the extent to

which the firm has outstanding employee stock options, using both measures of equity risk. Also

consistent with finance theory, we find that the relation between employee stock options and the

risk of common equity is significantly less negative for firms with longer option terms and for

firms that reprice options. These findings indicate that options with these attributes affect

common equity more like debt than options without these attributes. For firms with longer-term

options, the relation between employee stock options and common equity risk is significantly

negative, which indicates that these options have characteristics of equity and, thus, are only

somewhat more like debt than shorter-term options. However, for firms that reprice options, the

relation between options and common equity risk is not negative, which indicates that these

options do not have characteristics of equity. These findings reveal that employee stock options

can have terms that negate the equity-like characteristics of warrants.

We also find that the expected return on common equity is significantly negatively

associated with the extent to which the firm has outstanding employee stock options. These

findings support the predictions of finance theory and indicate that employee stock options de-

lever a firm’s common equity, not lever it. Therefore, our findings suggest it would be

inappropriate to classify employee stock options as liabilities for financial reporting purposes.

We next provide evidence on the sensitivity to changes in the value of the firm’s assets of

the value of employee stock options, the value of debt, and the value of common equity. Finance

theory predicts that debt and equity values respond differently to changes in asset value. In

particular, theory predicts that the elasticity of debt value to changes in asset value is concave,

5

whereas that of common equity value is convex. Thus, as the value of a firm’s assets exceeds the

value of its debt by a larger margin, the sensitivity of debt value to changes in asset value

approaches zero and the sensitivity of equity value to changes in asset value approaches one. To

assess the elasticity of employee stock option values, we use a recently developed warrant

pricing model. Our empirical tests reveal that the sensitivity of employee stock option values to

changes in asset value is convex, similar to that of common equity value. In contrast but

consistent with theory, our empirical tests show that the sensitivity of liability values to changes

in asset value is concave. These findings confirm the inferences from our primary tests that

employee stock options share the risk and return characteristics of common equity, but do not

share these characteristics of liabilities.

We use our estimates of expected common equity return and parameter estimates from

the warrant pricing model to estimate the expected return on employee stock options. We find

that the expected return on options averages approximately 70% more than the expected return

on common equity. These findings indicate that employee stock options are substantially more

risky than non-option equity, which also is inconsistent with the options sharing the

characteristics of liabilities.

The remainder of the paper proceeds as follows. Section II discusses the background for

our inquiry and related research, and Section III outlines our research design. Section IV

describes our data and presents our findings relating to equity risk and expected return. Section

V presents evidence on how the values of debt, employee stock options, and non-option equity

respond to changes in asset value, and estimates of the expected return on employee stock

options. Section VI summarizes and concludes.

6

II. BACKGROUND AND RELATED RESEARCH

Capital structure effects of employee stock options

Although the value of employee stock options is commonly estimated using option

pricing models, the terms of employee stock options differ from those of traditional options as

specified in these models. Employee stock options are warrants that firms issue to employees as

compensation for services. Warrants are call options on the firm’s assets, not on its existing

common equity. Warrants have a fixed strike price and maturity and are settled on exercise

when the warrant holder conveys the strike price to the firm and the firm issues additional shares

of stock to the warrant holder. Warrant exercise increases the firm’s cash and, because warrant

holders only exercise warrants when they are in the money, dilutes its existing common equity.

In contrast, options are written and exercised outside of the firm. Thus, option exercise does not

affect the firm’s assets, liabilities, or equity. In addition, whereas options can be traded,

employees cannot sell or otherwise transfer employee stock options. Each of these differences

can cause option values and employee stock option, i.e., warrant, values to diverge.1

That the exercise of employee stock options modifies the capital structure of the firm is

obvious. Option exercise causes the firm to issue new shares of common stock and to receive the

strike price in cash, thereby increasing both the number of common shares outstanding and the

total assets of the firm. Less obvious are the capital structure modifications that occur when the

firm issues the options. Finance theory shows that issuing warrants increases the expected value

In addition,

warrants have implications for capital structure that options do not.

1 Li and Wong (2005) estimates that the value of employee stock options is overstated by 6% when option pricing models are used. In section V, we also find that employee stock option value estimates are overstated when option pricing models are used, although our mean overstatement is larger—50%, i.e., 4% of market value of common equity compared to 6%. The difference in overstatement estimates may be attributable to sample period or estimation method. The Li and Wong (2005) sample period is 1996 through 2001, whereas ours is 2004 through 2009, which likely includes years of greater equity volatility that affects option values. Our estimation method differs from that in Li and Wong (2005) in that we jointly estimate the volatilities and values of employee stock options and common equity.

7

of the firm’s assets and decreases the expected risk of and return on the firm’s equity (e.g., Daves

and Ehrhardt 2007). This occurs for three reasons. First, employees pay for the options with

their services, leaving additional cash in the firm that can be used for other purposes.2

Because our interest is in determining whether employee stock options have

characteristics of liabilities, our tests focus on the third capital structure effect. In particular, if

employee stock options are associated with lower risk of and expected return on common equity,

then we infer that the options do not have characteristics of liabilities.

Second,

the expected exercise price of the options is anticipated by the firm and its claimants from the

date the firm issues the options. Therefore, the expected value of the firm’s assets increases with

the number of employee stock options issued; employee stock options are an additional,

potentially dilutive claim against this larger expected asset base. Third, the issuance of employee

stock options decreases the expected risk of, and thus the expected return on, existing common

equity. A decrease in common equity risk and expected return is consistent with the options

having a de-levering effect on the firm’s common equity. Intuitively, this is what would occur if

the firm sold a fraction of its risky assets at current value and invested the proceeds in a riskless

bond. When the firm receives the bond proceeds at maturity, it will purchase additional risky

assets at their value at that time. In this way, equity holders are insulated from asset risk between

the options’ issue date and exercise date.

Liabilities and equity in financial reporting

Although liabilities and equity are distinct financial statement elements, there is a lack of

consensus among accountants as to whether and how to draw a line between liabilities and 2 Option compensation procures labor resources that are provided over the vesting service period. This is a key factor in the FASB’s decision to require the grant-date value of options to be recognized as an expense over the vesting period. In addition, options affect the incentives of employees. We focus on the direct capital structure effects of options, rather than on the incentive effects. However, our tests include controls for possible risk-taking incentive effects.

8

equity, and which type of claim is embodied in employee stock options. Achieving consensus on

the distinction between liabilities and equity—and, thus, determining which claims of the firm

are classified in which category—is crucial for the current financial reporting model. The

identification of liabilities is important for assessing solvency. In addition, the distinction

between liabilities and equity has a direct subsequent effect on net income—after initial

recognition, changes in the recognized amounts of liabilities are recognized in comprehensive

income but corresponding changes in equity are not.3

Early accounting theorists present conflicting views of liabilities and equity. Sprague

(1907) advances a proprietary theory of the firm in which the separation of liabilities from equity

is necessary to assess solvency and determine profitability. In contrast, Paton (1962) suggests

that debt and equity claims are inherently indistinguishable because all claimants participate to

some extent in the risks and rewards of the firm. Assuming the profitability of operations is

unaffected by financing decisions, Paton (1962) reasons that the classification of claims into debt

and equity is arbitrary and largely irrelevant as long as operating profit, which excludes all

capital financing costs, is separately identified. The current financial reporting model is more

For example, if employee stock options

were classified as liabilities, then changes in the value of the options are candidates for

recognition as expenses. If they are classified as equity, then changes in their values are not

candidates for expense recognition. Without a clear distinction between the two claims

classifications, perhaps the most fundamental financial reporting amount—earnings—is ill-

defined.

3 Debt capital maintenance costs are recognized in comprehensive income as interest expense. Changes in the recognized amounts of liabilities that result in expense recognition include, but are not limited to, accretion of issue discount, amortization of issue premium, remeasurement to fair value, and settlement or cancellation at amounts that differ from recognized liability amounts at the time of settlement. Because current accounting theory and concepts provide that equity capital maintenance costs are not recognized as expenses, similar or corresponding equity events do not result in expense recognition.

9

consistent with the former view; liabilities are separately defined and net income reflects the cost

of debt capital, but not the cost of equity capital.

However, the lack of consensus about characteristics that distinguish liabilities and equity

is reflected in current accounting standards relating to financial instruments, which include over

60 pieces of literature that have been called “inconsistent…(and) difficult to understand and

apply” (FASB 2007, iii). The FASB’s current Conceptual Framework defines liabilities as

probable future sacrifices of the firm’s assets arising from a present obligation (FASB 1985,

para. 35). This definition rests primarily on two factors: the existence of a present obligation and

the requirement to transfer the firm’s assets in settlement. However, this definition of liabilities

is subject to criticism because determining whether a present obligation exists is subjective, and

because the form of settlement is subject to structuring. For these reasons, a growing body of

literature advocates changing the definition of liabilities to include all claims other than common

stock (e.g., Kirschenheiter et al. 2004; Ohlson and Penman 2005).

In a move toward this definition, the FASB released Preliminary Views: Financial

Instruments with Characteristics of Equity (“Preliminary Views,” FASB 2007) to solicit

comments on its proposal that a basic ownership approach to equity classification would improve

financial reporting. The Preliminary Views notes that distinguishing liabilities from equity by

applying the current definition of liabilities is subjective, particularly to complex instruments

with contingent settlement outcomes. For example, under current requirements, a written call

option is classified as a liability if it must be settled with cash, but is classified as equity if it can

be settled with shares. In contrast to current Generally Accepted Accounting Principles (GAAP),

the basic ownership approach would classify as equity only common stock, i.e., there would be

only one type of equity. As a result, preferred stock, options, and other contingent claims would

10

be classified as liabilities under the FASB’s proposed basic ownership approach, rather than as

different types of equity.

The basic ownership approach arguably is less subjective and easier to apply than the

current definition of liabilities because it obviates the need (1) to identify the essential

characteristics of liabilities and (2) to determine whether particular instruments have such

characteristics. Under the basic ownership approach, liabilities comprise any claim that is not

the basic ownership interest, irrespective of whether the claim embodies a present obligation.

However, defining equity as only basic ownership interests means that liabilities would be the

residual category for claims against the firm’s assets. This is in contrast to the current definition

of equity as the residual of assets minus liabilities, and could lead to a classification system that

fails to reflect appropriately those characteristics of non-basic ownership claims that affect the

risk of and expected return on the basic ownership interests.

Consistent with these concerns, critics of the basic ownership approach to equity

classification believe that classifying as liabilities both present obligations and non-obligating

financing instruments would result in a heterogeneous class of liabilities and “an artificially

narrow set of equities that will decrease the usefulness of the balance sheet, both for assessing a

firm’s solvency, and for valuing its residual claims” (FASAC, 2001, page 388).4

4 Consistent with this view, Terando et al. (2007) presents empirical evidence that market participants differentially value share puts based on their solvency characteristics.

These critics

believe that the decision-usefulness of liability and equity classification derives from defining

and identifying liabilities, not from defining and identifying the most basic ownership interest.

This need to identify liabilities is consistent with the theoretical finance literature that

models risk of and expected return on common equity as a function of financial leverage

(Hamada 1969; Rubinstein 1973). The importance of leverage is demonstrated by the model in

11

Robichek and Myers (1966), among others, which shows that leverage can have a negative effect

on common equity value when bankruptcy is possible, or when leverage affects future

investment and growth. These studies conceptualize liabilities in terms of unavoidable

obligations to surrender firm assets in particular states of the world, and suggest that

distinguishing obligations from other claims is important for financial statement analysis and

assessing the risk and value of common equity.

The possibility that financing constraints and bankruptcy costs can affect the value of

equity is inconsistent with Paton’s (1962) view of the entity, which is based largely on the

premise that operating and financing decisions are independent and that financing decisions are

irrelevant for valuation of the firm. We posit that if finance theory is empirically descriptive,

then reporting liabilities separately from equity and disaggregating claims using a classification

scheme based on their identifiable risk and return characteristics should be useful to investors for

valuing common equity and for assessing its risk and expected return.

With regard to classification, several studies view employee stock options as more akin to

liabilities than to equity (e.g., Clark 1993; Balsam 1994; Hull and White 2003; Kirschenheiter et

al. 2004; Maines et al. 2004; Ohlson and Penman 2005; Sacho and Oberholster 2005; Landsman

et al. 2006). Some of these studies contend that the current financial reporting conceptual

framework requires options to be classified as liabilities because options reflect claims of

potential owners rather than existing owners (e.g., Clark 1993). Others contend that the issuance

of options creates a conditional obligation to issue common stock for less than its market value in

some potential future states of the world, that these conditional obligations are sufficiently

“present” to meet the definition of a liability, and that value estimates derived from valuation

12

models are the most appropriate measures of these obligations at any reporting date

(Kirschenheiter 2004; Ohlson and Penman 2005).

However, the more prevalent rationale for classifying employee stock options as

liabilities is the perspective that the exercise of options results in a “windfall gain” to option

holders that the firm should recognize as an expense. Because changes in the value of equity are

not recognized in net income, this perspective suggests that recognition in net income of changes

in option value subsequent to the grant date requires the options to be classified as liabilities.

Inferring liability or equity classification from desired effects on net income would be a new

approach to determining financial statement element classification.5 Hull and White (2003)

takes this perspective to an extreme and expresses the view that liability or equity classification

is entirely irrelevant for employee stock options, but that “proper accounting” requires expense

recognition of changes in the option value subsequent to grant.6

Little extant empirical research attempts to identify the characteristics of employee stock

options that are relevant for determining the appropriate classification of the options in the

statement of financial position. Li and Wong (2005) and Landsman et al. (2006) document that

employee stock options must be considered when using a residual income model to estimate the

value of common equity. This is because net income accrues for the combined benefit of

employee stock option holders and common equity holders, and failure to account for the

fraction of income accruing for the benefit of option holders causes the residual income model to

overstate the estimated value of equity. Li and Wong (2005) approaches the problem by using

total residual income to estimate the combined value of employee stock options and common

5 For example, preferred stock is classified as equity. Preferred dividends are recognized as an expense in determining net income available to common equity holders, but not in determining net income. 6 Exercise date value of employee stock options is frequently accepted as the “real cost” of compensation. For example, Core, Guay, and Larcker (2008) finds that negative press coverage about potentially excessive executive compensation focuses more on the proceeds from option exercises than on grant-date values.

13

equity and then subtracting the option value estimated from a warrant pricing model to derive an

estimate of common equity value.

Landsman et al. (2006) evaluates the relative explanatory power of alternative “pro-

forma” methods of accounting for employee stock options, and finds that subtracting option

value from total residual income over the term of the options increases the cross-sectional

explanatory power of the residual income model for common equity value.7

Although both Li and Wong (2005) and Landsman et al. (2006) document the importance

of separately considering employee stock option value when valuing common equity, neither

directly addresses the classification of employee stock options as liabilities or equity based on

the relation between the options and the risk and return characteristics of common equity.

Similar to Kirschenheiter et al. (2004), Landsman et al. (2006) infers liability classification from

the apparent need to account for the value of employee stock options when valuing common

equity. In contrast, we posit that classification in the statement of financial position should

derive from capital structure effects, including risk and return.

Landsman et al.

(2006) concludes that employee stock options should be classified as liabilities and changes in

option value each period should be included in net income. However, as Aboody (2006) points

out, the residual income model cannot be used to assess the efficacy of alternative methods of

accounting because if the residual income model is applied correctly, one should always be able

to recover the value of common equity. Thus, Landsman et al. (2006) can be viewed as a

comparison of hypothetical valuation errors that would occur if investors failed in specified ways

to correctly incorporate available information when applying the residual income model.

8

7 Subtracting estimated option value from total residual income implicitly assumes that the estimated option value equals the expected present value of residual income accruing to option holders.

8 That the residual income model is equivocal with respect to liability or equity classification can be illustrated by considering a firm with common equity and traded warrants. For residual income to explain the current value of the

14

We contribute to the debate about the appropriate classification of employee stock

options by identifying empirically those characteristics that differentiate liabilities from common

equity. We show that employee stock options are negatively associated with common equity risk

and the expected return on common equity. That is, we show that the effects of employee stock

options on common equity risk and expected return are opposite to those of debt—debt is

positively associated with common equity risk and expected return. These findings suggest that

options should not be classified as liabilities.

Relation between warrants and equity risk and return

Modigliani and Miller (1958) shows that in the absence of taxes and transaction costs,

although total firm value is independent of leverage, the cost of equity varies positively with the

debt-to-equity ratio. That is, Modigliani and Miller (1958) shows that a firm’s equity risk

increases when it issues debt, and the expected return on equity reflects a risk premium

commensurate with this increased risk. Extending the work of Modigliani and Miller (1958,

1963), Hamada (1972) empirically shows that, in the cross-section, realized equity returns are

increasing in leverage.9

However, the theoretical effects of contingent claims on common equity risk and return

are not as straightforward as are the effects of straight debt. Ingersoll (1977) models the value of

convertible debt as a combination of the values of straight debt and a warrant with an exercise

price equal to the amount of implied straight debt. One implication of Ingersoll’s (1977) model

is that the net effect of convertible debt on common equity risk is a product of two countervailing

warrants without error, the value of common equity must be deducted from residual income. However, we do not view this implying that common equity should be classified as a liability when a firm has traded warrants. 9 More recent studies testing the relation between leverage and equity returns report contradictory results. For example, Penman et al. (2007) finds that leverage is negatively related to realized equity returns and Korteweg (2004) finds that equity factor loadings decrease after equity-for-debt exchanges. Empirical deviations from Modigliani and Miller (1958) are collectively referred to as the “leverage puzzle”.

15

forces: common equity risk increases with the implied amount of straight debt and decreases

with the implied amount of the warrant. Galai and Schneller (1978) extends Ingersoll (1977) and

develops a structural model for separately pricing warrants on levered common equity.

Consistent with Ingersoll’s (1977) analysis, Galai and Schneller’s (1978) model predicts that the

issuance of warrants decreases the risk of and expected return on the firm’s common equity.

Consistent with Modigliani and Miller’s (1958) result for debt, warrant valuation models assume

that the issuance of warrants does not result in a change to common equity value (Ukhov 2004;

Daves and Ehrhardt 2007). Because warrants are settled by the firm receiving cash and issuing

stock, the issuance of warrants at their current value is equivalent to the contingent sale of a

fraction of the firm at its current value in return for a riskless receivable.10

Appendix A presents a numerical example to illustrate the implications of this theoretical

literature. Intuitively, common equity risk decreases as warrants outstanding increase because by

issuing warrants the firm effectively sells a portion of the upside asset return potential for its

current value.

11 This transfer truncates both tails of the return distribution for common equity,

thereby reducing the variance of its return. As Figure 1 in Appendix A shows, assuming there is

no uncertainty, the issuance of warrants is identical to a stock subscription, and neither the value

of nor the expected return on existing equity changes. However, as Figure 2 in Appendix A

shows, in the more realistic case of uncertainty, although the value of existing common equity

does not change when a firm issues warrants, the risk of and expected return on existing common

equity both decrease.12

10 By focusing our tests on common equity risk and expected return, we implicitly assume that the Modigliani and Miller (1958) capital structure irrelevance proposition holds, at least on average.

That is, the issuance of warrants de-levers common equity.

11 In the example, this value is $9.00. 12 The deductibility of employee stock option intrinsic value for tax purposes can provide tax benefits relative to other types of financing. As with debt tax shields, these stock option tax benefits potentially further reduce the cost of financing with options. We leave to future research the analysis of the relation between employee stock option tax benefits and the value of and expected return on common equity.

16

Empirical estimation of Galai and Schneller’s (1978) model parameters requires

knowledge of the value of the firm’s assets and the variance of the assets’ return, both of which

are unobservable. Largely as a result of the identification problem this lack of observability

poses, the empirical validity of Galai and Schneller’s (1978) pricing model remains an open

question (e.g., Noreen and Wolfson 1981; Galai 1989). As a solution to the identification

problem, Ukhov (2004) develops an algorithm using only observable inputs for pricing warrants

on levered common equity and for determining the variance of the warrants’ return. The Ukhov

(2004) algorithm can be solved numerically, and provides a mechanism for computing the price

and the variance of each of class of claims for a firm with a complex capital structure. More

recently, as Appendix B explains, Daves and Ehrhardt (2007) shows how to compute the

expected return on various capital structure components using observable data. We use the

Daves and Ehrhardt (2007) methodology to compute the value of and expected return on

employee stock options in Section V.

Despite the theoretical basis for expecting that warrants de-lever common equity, the

association between warrants and the risk of and expected return on common equity have not

been established empirically. The theoretical models are based on assumptions, which may not

be descriptively valid, particularly for employee stock options. For example, employee stock

options frequently are issued to insiders who may have the ability to influence the firm to amend

their option contracts after issuance. Such implicit contractual terms may create contracts that do

not meet the definition of a warrant. Repricing the options is an example of such an option

contract amendment because repricing negates the fixed strike price feature of a warrant. In

addition, the warrant models assume markets are complete, and the inability of employees to sell

their options is a form of market incompleteness with unclear implications for the models’

17

predictions. Moreover, distributional assumptions underlying the models’ predictions might not

be descriptive (Galai 1989). Therefore, testing the predictions of the models is necessary if the

theoretical effects of warrants on common equity are to be used as a basis for their financial

statement classification.13

We contribute to this literature by testing the predictions of the warrant valuation models

as they relate to employee stock options. That is, in contrast to debt, employee stock options are

predicted to be negatively associated with the risk of and expected return on common equity.

We also provide evidence on how changes in the values of employee stock options and common

equity correspond to changes in the firm’s asset value, and on the magnitude of the expected

returns on these two types of claims. Consistent with the models’ predictions, we find that as the

firm’s distance to default increases, the sensitivities of common equity and employee stock

option values to changes in asset value increases, and the sensitivity of debt value to changes in

asset value decreases. That is, common equity and employee stock option values are convex in

asset value, and liability values are concave. We also find that the expected return on employee

stock options is on average 70% greater than the expected return on common equity, which is

inconsistent with employee stock options being a claim against a firm’s assets with higher

priority than common equity.

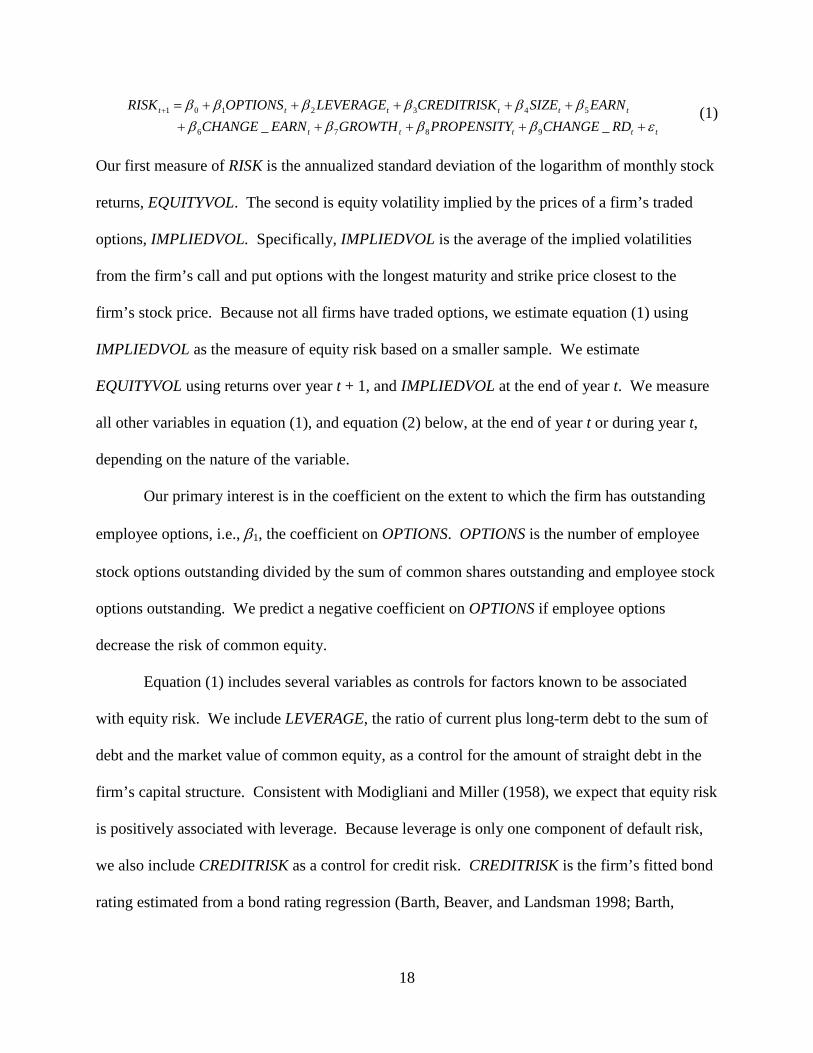

III. RESEARCH DESIGN Common equity risk

We first test whether common equity risk is negatively associated with the extent of

outstanding employee stock options, as predicted by finance theory. To do so, we estimate

equation (1), using two measures of equity risk, RISK. 13 For example, evidence from empirical validation of the Black-Scholes (1973) option pricing model indicates that the model is generally descriptive. However, market prices frequently deviate from those predicted by the model (see Mayhew 1995 for discussion). In general, the model does not perform well for options that are far out of the money.

18

ttttt

tttttt

RDCHANGEPROPENSITYGROWTHEARNCHANGEEARNSIZECREDITRISKLEVERAGEOPTIONSRISK

εββββββββββ

++++++++++=+

__ 9876

5432101 (1)

Our first measure of RISK is the annualized standard deviation of the logarithm of monthly stock

returns, EQUITYVOL. The second is equity volatility implied by the prices of a firm’s traded

options, IMPLIEDVOL. Specifically, IMPLIEDVOL is the average of the implied volatilities

from the firm’s call and put options with the longest maturity and strike price closest to the

firm’s stock price. Because not all firms have traded options, we estimate equation (1) using

IMPLIEDVOL as the measure of equity risk based on a smaller sample. We estimate

EQUITYVOL using returns over year t + 1, and IMPLIEDVOL at the end of year t. We measure

all other variables in equation (1), and equation (2) below, at the end of year t or during year t,

depending on the nature of the variable.

Our primary interest is in the coefficient on the extent to which the firm has outstanding

employee options, i.e., β1, the coefficient on OPTIONS. OPTIONS is the number of employee

stock options outstanding divided by the sum of common shares outstanding and employee stock

options outstanding. We predict a negative coefficient on OPTIONS if employee options

decrease the risk of common equity.

Equation (1) includes several variables as controls for factors known to be associated

with equity risk. We include LEVERAGE, the ratio of current plus long-term debt to the sum of

debt and the market value of common equity, as a control for the amount of straight debt in the

firm’s capital structure. Consistent with Modigliani and Miller (1958), we expect that equity risk

is positively associated with leverage. Because leverage is only one component of default risk,

we also include CREDITRISK as a control for credit risk. CREDITRISK is the firm’s fitted bond

rating estimated from a bond rating regression (Barth, Beaver, and Landsman 1998; Barth,

19

Hodder, and Stubben 2008).14 Specifically, we estimate the relation between a firm’s credit

rating and financial statement variables, i.e., assets, return on assets, leverage, and indicator

variables for whether a firm pays dividends, has subordinated debt, and reports negative

earnings, for the subsample of firms with credit ratings.15

Prior research finds a negative relation between firm size and equity risk (Pastor and

Veronesi 2003). Thus, we include in equation (1) SIZE, which is the natural logarithm of the

market value of equity, and expect it has a negative association with equity risk. Hanlon,

Rajgopal, and Shevlin (2004) finds that operating performance is negatively associated with

equity volatility in the cross-section. Thus, we include in equation (1) earnings, EARN, and

change in earnings, CHANGE_EARN, as controls for operating performance. EARN is annual

income before extraordinary items divided by total assets, and CHANGE_EARN is the change in

EARN from year t – 1 to year t. We expect EARN is negatively associated with equity risk. We

do not predict the sign of the association for CHANGE_EARN; CHANGE_EARN may reflect

operating performance that is negatively associated with equity risk or short-term growth that is

positively associated with equity risk.

We then apply the estimated

coefficients from this relation to the financial statements amounts of the sample firms to obtain

fitted values for credit risk. We expect that credit risk is positively associated with equity risk.

Because higher long-term growth typically is associated with higher risk and can provide

opportunities for managers to profit from equity-based compensation, we include GROWTH, the

last consensus long-term earnings growth forecast, in equation (1) as a control for growth. In

addition, Core and Guay (2001) finds that firms with more growth opportunities grant options

14 Our tabulated findings are based on estimating the bond rating regression pooling observations over time. Estimating the regression separately year by year does not alter our inferences. 15 During our sample period, recognition of stock-based compensation expense became mandatory. Thus, to mitigate the potential for confounded coefficient estimates, we calculate return on assets using net income before stock-based compensation expense.

20

more frequently, suggesting GROWTH is likely to be positively correlated with OPTIONS.

Thus, failure to include a control for growth could bias the coefficient on OPTIONS. We expect

GROWTH is positively associated with equity risk.

Firms select whether to issue employee stock options, and there is evidence that firms

with greater operating risk and more growth opportunities are more likely to issue options.

Although we include GROWTH as a control for firms’ propensity to issue options, and SIZE and

CHANGE_EARN can reflect operating risk, there could be other factors associated with

OPTIONS and RISK that are not captured by these variables. Thus, we include in equation (1)

PROPENSITY as a control for firms’ propensity to issue options. We measure PROPENSITY

based on Core and Guay (2001). In particular, we estimate year by year the relation between

OPTIONS and the natural logarithm of the sum of market value of equity and book value of debt,

the natural logarithm of the number of employees, equity volatility, the book-to-market ratio,

research and development expense divided by total assets, and industry effects.16

Finally, options can provide incentives for managers to increase the risk of the firm’s

assets (DeFusco et al. 1990; Rajgopal and Shevlin 2002; Williams and Rao 2006).

PROPENSITY

is the predicted value from this relation. We expect a firm’s propensity to issue options is

positively associated with equity risk.

17

16 The relation in Core and Guay (2001) also includes segment information as measures of total diversification and geographic diversification. Because requiring the use of segment information dramatically reduces our sample size, we do not use segment information when constructing our propensity measure. However, untabulated analyses reveal that a propensity measure that includes segment information is 99% correlated with our propensity measure. Not surprisingly given this high correlation, our inferences are unchanged when we estimate equation (1) using the alternative propensity measure and the subsample of firms with available segment data.

As a control

for subsequent risky investment, we include in equation (1) CHANGE_RD (Coles et al. 2006).

17 Lambert, Larcker, and Verrecchia (1991) shows analytically that options can, for particular parameter values, decrease risk-taking incentives. Although the expected value of option payoffs increases with asset volatility, options are risky assets, and risk-averse, undiversified executives can become more risk-averse if options are a large component of compensation (Carpenter 2000). Thus, the association between options and risk-taking is situational.

21

CHANGE_RD is the year t + 1 research and development expense divided by total assets minus

year t’s research and development expense divided by total assets. We expect that an increase in

risky investment is positively associated with equity risk.

Expected return on common equity

We next test whether the expected return on common equity is negatively associated with

the extent of outstanding employee stock options, also as predicted by finance theory. To do so,

we estimate equation (2).

ttt

ttttttt

DISPERSIONGROWTHMOMBETABMSIZELEVERAGEOPTIONSECC

εβββββββββ

+++++++++=

87

6543210 (2)

ECC is the expected cost of common equity at the end of year t. Our estimate of ECC is based

on the Fama and French (1993) three-factor model supplemented with the momentum factor,

time-varying factor loadings, risk-free interest rates, and risk premiums. We calculate ECC

following Barth, Konchitchki, and Landsman (2010) by first estimating factor betas for each firm

using five-year rolling windows, updated annually, and then using these estimated betas, along

with expected factor returns based on historical averages, to estimate ECC. As with equation (1),

our primary interest is in the coefficient on OPTIONS, β1. We predict it is negative.

Equation (2) also includes as control variables proxies for factors commonly associated

with expected returns. As with equation (1), we include LEVERAGE in equation (2) and expect

a positive association between leverage and expected equity cost of capital. Based on prior

empirical studies, we also expect the cost of equity capital to be negatively associated with firm

size, SIZE, and to be positively associated with the firm’s equity book-to-market ratio, BM, and

stock return beta, BETA (e.g., Fama and French 1993). BM is the natural logarithm of the book

value of equity divided by the market value of equity. BETA is the coefficient on the market

22

return from firm-specific estimation of the relation between a firm’s monthly returns and the

market return, using five-year rolling windows.18

Jegadeesh and Titman (1993) examines price momentum and finds that past winners earn

substantially higher returns than past losers. Thus, we include price momentum, MOM, in

equation (2) and expect it has a positive association with expected equity cost of capital. MOM

is the firm’s raw return over the first ten months of year t. Beaver, Kettler, and Scholes (1970)

posits that high growth firms are more profitable because abnormal profits erode over time as a

result of competition. Thus, we include GROWTH in equation (2) and expect a positive

association between growth and expected equity cost of capital. Finally, because information

risk is positively associated with cost of equity capital (Botosan and Plumlee 2005), we include

DISPERSION in equation (2). DISPERSION is the coefficient of variation of year t earnings

forecasts outstanding in June of year t. We predict a positive association between analyst

forecast dispersion and expected equity cost of capital.

IV. DATA AND FINDINGS FOR EQUITY RISK AND EXPECTED RETURN

Data and descriptive statistics

We base our tests on a sample of U.S. firms over the period 2004 to 2009. Our sample

begins in 2004 because this is the first year employee stock option data are available on

Compustat for a broad set of firms. We obtain stock prices and returns from CRSP and analyst

forecasts from I/B/E/S. We calculate implied equity volatility using data from Optionmetrics

and the approach in Bartov, Mohanram, and Nissim (2007). We estimate equations (1) and (2)

using the pooled cross-sectional sample and base reported t-statistics on standard errors clustered

18 BETA is a proxy for systematic risk and options can increase systematic risk, idiosyncratic risk, or both. Market beta also is theoretically related to leverage. Our including BETA in equation (2) in addition to LEVERAGE is consistent with prior research examining the determinants of ECC. Excluding BETA from equation (2) has no effect on our inferences.

23

by firm and year to mitigate intertemporal and cross-sectional correlation of residuals (Gow,

Ormazabal, and Taylor 2010). We estimate several versions of equations (1) and (2) using

different combinations of the explanatory variables. We do so in part because lack of data

reduces the number of observations available for some variables.

Table 1, Panel A, presents descriptive statistics for each variable we use in our analyses.

Regarding our measures of equity risk and expected return, Panel A reveals that realized equity

volatility, EQUITYVOL, averages 47%, and implied volatility, IMPLIEDVOL, averages 45%.

Panel A also reveals that the mean of expected equity cost of capital, ECC, is 13%. Panel A

reveals that the mean of OPTIONS is 0.08, which indicates that the average ratio of options

outstanding to the total of common equity shares and option outstanding is 8%. This is slightly

larger than the 6.4% reported by Core and Guay (2001) over an earlier sample period and is

consistent with the use of options increasing over time.19

Regarding the control variables, Panel A reveals that the mean of LEVERAGE is 21% of

the sum of the market value of equity and debt. This ratio is consistent with the findings of

Barth, Hodder, and Stubben (2008).

20

Panel B of Table 1 presents the Pearson correlations between the variables. Most of the

correlations are as expected. For example, the correlation between EQUITYVOL and

IMPLIEDVOL is large and positive (Pearson Corr. = 0.60; Spearman Corr. = 0.70). In addition,

The means of earnings, EARN, and change in earnings,

CHANGE_EARN, are negative, but the medians are not. The mean (median) of EARN is –16%

(1%) and of CHANGE_EARN is –1% (0%). The left skewness of earnings is consistent with

prior research (e.g., Ball, Sadka, and Sadka 2009).

19 Because Core and Guay (2001) reports options divided by common shares, for ease of comparison, we convert the ratio in Core and Guay (2001) to the ratio we use. 20 Barth, Hodder and Stubben (2008) measures leverage as the ratio of debt to total assets. Our inferences are invariant to using this alternative measure of leverage.

24

consistent with theory, both measures of risk are positively correlated with CREDITRISK and

GROWTH (Pearson Corr. = 0.36 and 0.45 for CREDITRISK; 0.19 and 0.24 for GROWTH), and

negatively correlated with SIZE (Corr. = –0.36 and –0.56), EARN (Corr. = –0.36 and –0.37), and

CHANGE_EARN (Corr. = –0.11 and –0.06), consistent with the findings of Hanlon, Rajgopal,

and Shevlin (2004). Also as expected, PROPENSITY is positively correlated with EQUITYVOL

and IMPLIEDVOL (Corr. = 0.15 and 0.18). Although the univariate correlations generally are

supportive of our predictions, we base our inferences on the multivariate relations specified by

equations (1) and (2).

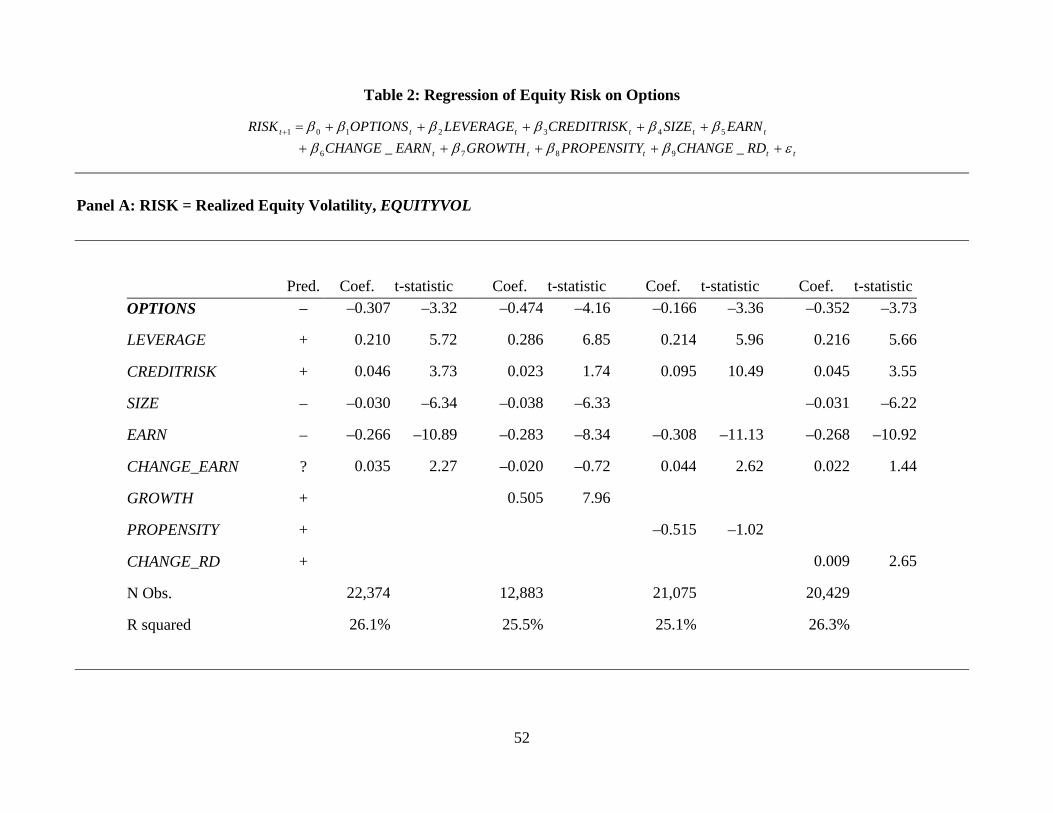

Findings: Employee stock options and equity risk

Table 2, Panel A, presents regression summary statistics from estimating four versions of

equation (1). Consistent with our prediction the coefficient on OPTIONS is significantly

negative in all specifications, with t-statistics of –3.32, –4.16, –3.36, and –3.73. That is, the

extent to which a firm has outstanding employee stock options is significantly negatively

associated with equity risk, as measured by realized equity volatility. Panel A also reveals that

leverage is significantly positively associated with equity volatility in all specifications (t = 5.72,

6.85, 5.96, and 5.66). Finding a significant positive association between leverage and equity

volatility coupled with finding a significant negative association between employee stock options

and equity volatility indicates that employee stock options de-lever the firm’s equity, as

predicted.

Regarding the other control variables, Panel A reveals, as expected, that CREDITRISK is

positively associated with equity risk in all versions, although the association is only marginally

significant in the version that includes GROWTH (t = 3.73, 1.74, 10.49, and 3.55). Also as

expected, SIZE is significantly negatively associated with equity volatility (t = –6.34, –6.33, and

25

–6.22). In all specifications, earnings, EARN, is significantly negatively associated with equity

volatility, consistent with the findings of Hanlon, Rajgopal, and Shevlin (2004) (t = –10.89, –

8.34, –11.13, and –10.92). The coefficient on change in earnings, CHANGE_EARN, is

significantly positive in two of the specifications (t = 2.27, –0.72, 2.62, and 1.44). The sign of

the coefficient on CHANGE_EARN is sensitive to the inclusion of GROWTH, which suggests

that CHANGE_EARN also is a proxy for growth. Consistent with growth reflecting greater risk,

GROWTH is significantly positively associated with equity volatility (t = 7.96). The coefficient

on future risk taking, represented by CHANGE_RD, is also significantly positive (t = 2.65).

Panel A also reveals that PROPENSITY is not significantly associated with equity volatility,

incremental to the other variables (t = –1.02).21

Table 2, Panel B, presents regression summary statistics from estimating equation (1)

with implied volatility, IMPLIEDVOL, as the measure of equity risk. Panel B reveals inferences

identical to those revealed by Panel A with respect to the relation between equity risk and

employee stock options. In particular, the coefficient on OPTIONS is significantly negative in

all four specifications of equation (1), with t-statistics ranging from –4.53 to –4.85.

Regarding the control variables, Panel B reveals that, as expected, SIZE and EARN are

consistently negatively associated with implied volatility, with t-statistics ranging from –7.93 to

–9.22. LEVERAGE is significant in all specifications (t = 2.43, 4.24, 2.87 and 2.44). However,

the significance of CREDITRISK depends on the inclusion of SIZE. When SIZE is included in

the equation the coefficients on CREDITRISK are not significantly different from zero; the t-

21 Table 1, Panel B, reveals that PROPENSITY is positively correlated with EQUITYVOL (Corr. = 0.15) and with OPTIONS (Corr. = 0.53). This suggests that the association between PROPENSITY and EQUITYVOL is subsumed by other variables in the estimation equation. Consistent with this conjecture, untabulated findings from estimating equation (1) with only PROPENSITY and OPTIONS as explanatory variables reveal that PROPENSITY is significantly positively associated with EQUITYVOL, and OPTIONS is significantly negatively associated with EQUITYVOL. Untabulated findings using IMPLIEDVOL as the dependent variable reveal the same inferences as the untabulated findings using EQUITYVOL.

26

statistics are all less than or equal to 0.66 in absolute value. When SIZE is not included, the

coefficient on CREDITRISK is significantly positive, as expected (t = 10.62). Also as expected,

the coefficient on GROWTH is significantly positive (t = 8.55) and those on CHANGE_EARN

are significantly positive, except when GROWTH is included in the equation (t =2.49, 0.30, 2.94,

and 2.22). The other control variables are not significantly associated with implied volatility.

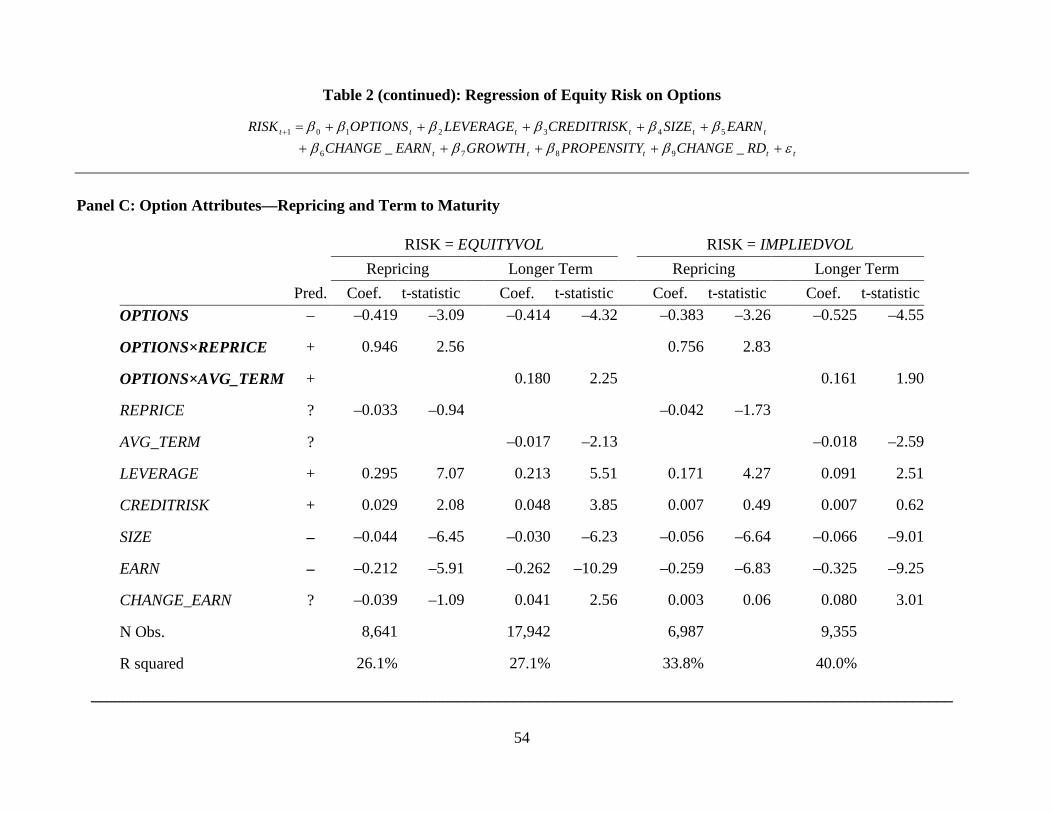

Relation across option attributes

The potential for managers to increase the certainty of option payouts by reducing the

strike price of the options, and the long term of employee stock options relative to other warrants

are two characteristics that distinguish employee stock options from other warrants and that

potentially invalidate the theoretical models upon which we base our predictions. Specifically,

the role of OPTIONS in a firm’s capital structure should be more similar to liabilities and less

similar to equity when 1) the options pose greater risk to the common equity holders because the

option strike price is lowered, thereby making option payouts more certain, or 2) the options are

longer term and therefore have less of a de-levering effect on common equity (Schultz and

Trautmann 1994). Thus, to provide additional support for our primary findings and inferences,

we investigate whether the relation between RISK and OPTIONS varies predictably with these

attributes of the employee stock options.

To examine the effects of increased certainty of option payouts associated with expected

strike price reductions, we examine the association between option repricing and the relation

between RISK and OPTIONS. Repricing is the practice of resetting the strike price on a stock

option contract, typically after the stock price declines. We collect repricing data from

ExecuComp and Equilar, and we set an indicator variable, REPRICE, equal to one in the year a

27

firm reprices options for at least one executive, and zero otherwise.22

Warrant value is most sensitive to asset value changes for near-maturity, in-the-money

warrants; therefore, warrant volatility increases as time to maturity decreases. Because asset

volatility is a weighted average of warrant volatility and common equity volatility, for any given

level of asset volatility, common equity volatility decreases as warrant volatility increases. This

implies that common equity volatility should decrease as the time to maturity of employee stock

options decreases. To examine the effects of longer option terms on the relation between RISK

and OPTIONS, we set an indicator variable, AVG_TERM, equal to one if the average term of

options outstanding is above the sample median, and zero otherwise. We estimate the average

life remaining for outstanding options using each firm’s disclosed expected life of newly granted

options. Following Landsman et al. (2006), we assume that the average life for all options

outstanding equals one-half of the expected life of newly granted options. Because longer-term

options have less effect on the risk of and expected return on common equity, we predict a

positive coefficient on the interaction of AVG_TERM and OPTIONS.

Because we expect that the

relation between employee stock options and common equity risk is less negative when firms

have a tendency to reprice options, we predict a positive coefficient on the interaction of

REPRICE and OPTIONS.

Table 2, Panel C, presents the findings. The first four columns present findings from

using realized volatility, EQUITYVOL, as the risk measure, and the last four columns present

findings using implied volatility, IMPLIEDVOL. Consistent with predictions, the findings

relating to repricing in Panel C reveal that the relation between OPTIONS and RISK is

22 This analysis is based on firms covered by ExecuComp, i.e., current and former members of the S&P 1500 plus some requests by clients of S&P. Equilar identifies some repricing firms that ExecuComp does not. Thus, we use both sources to identify repricing firms to increase the power of our tests. Using only ExecuComp to identify repricing firms does not alter our inferences.

28

significantly less negative for firms that reprice options (t = 2.56 and 2.83 for EQUITYVOL and

IMPLIEDVOL). In addition, untabulated findings reveal that the total coefficient on OPTIONS

for firms that reprice options, i.e., the sum of the coefficients on OPTIONS and

OPTIONS×REPRICE, is not significantly different from zero (t = 1.44 and 1.46 for

EQUITYVOL and IMPLIEDVOL). These findings suggest that option repricing changes the

characteristics of employee stock options such that the options no longer have characteristics of

equity.

Relating to longer option terms, Panel C also reveals, as predicted, that the relation

between OPTIONS and RISK is muted when the remaining average employee stock option term

to maturity is above the sample median. The positive coefficient on the interaction variable,

OPTIONS×AVG_TERM, indicates that the relation is significantly less negative for both risk

proxies (t = 2.25 and 1.90 for EQUITYVOL and IMPLIEDVOL). However, untabulated findings

reveal that the total coefficient on OPTIONS for firms with longer-term options, i.e., the sum of

the coefficients on OPTIONS and OPTIONS×AVG_TERM, is significantly negative for both risk

proxies (t = –2.05 and –4.24 for EQUITYVOL and IMPLIEDVOL). These findings suggest that

although longer-term employee stock options have characteristics somewhat less similar to

warrants than shorter-term options, they do not have characteristics of liabilities.

Taken together, the results in Table 2, Panel C, are consistent with the predictions of

theory: employee stock options with contractual terms closer to true warrants exhibit stronger

negative associations with equity risk.

Robustness checks

We conduct four additional tests to check the robustness of our inferences. Untabulated

findings from all robustness checks support the inferences we obtain from the tabulated findings.

29

First, because there are few established models of the determinants of equity volatility,

our empirical specification of equation (1) is necessarily ad hoc. Thus, to investigate the

robustness of our inferences, we include in equation (1)—both with EQUITYVOL and with

IMPLIEDVOL as the dependent variable—several additional variables shown by prior research

to be associated with common equity risk or return. Specifically, we include the equity book-to-

market ratio, momentum, analyst forecast dispersion, the inverse of price per share, and firm age

as additional explanatory variables. The untabulated findings reveal that although the

significance of the association between common equity risk and some of control variables,

including CHANGE_EARN, differs when these additional variables are included in the

estimating equation, the association between common equity risk and OPTIONS is consistently

significantly negative.

Second, because our results could be unduly influenced by the unusually high market

volatility in 2008, we re-estimate our equations excluding observations from 2008. Third, as an

alternative control for the propensity to issue options, we include option grants in the preceding

year. Fourth, we test whether results are sensitive to our measuring OPTIONS as the percentage

of dilution, i.e., the number of options outstanding relative to the total of numbers of common

shares and options outstanding. In particular, we measure OPTIONS as their estimated value,

rather than as the percentage dilution.

Findings: Employee stock options and expected return on equity

Table 3 presents regression summary statistics from estimating two versions of equation

(2). Consistent with our findings for equity risk, statistics in Table 3 from both versions reveal

that OPTIONS is negatively associated with the expected equity cost of capital, ECC (t = –2.95

and –4.55). Consistent with the equity volatility findings, the association between ECC and

30

LEVERAGE is positive, although it is only significantly so when we include GROWTH and

DISPERSION in the equation (t = 1.44 and 3.96).

As expected, SIZE is significantly negatively associated with ECC (t = –3.62 and –5.81)

and BETA is significantly positively associated (t = 4.29 and 2.78). BM and DISPERSION are

not significantly associated with ECC (t = –1.55 and –1.28 for BM, and –1.44 for DISPERSION)

and, contrary to expectations, MOM is significantly negatively associated (t = –4.93 and –2.54).

V. SENSITIVITY OF CLAIMS VALUES TO CHANGES IN ASSET VALUES

Finance theory suggests that debt and equity values respond differently to changes in

asset value. In particular, as the value of the firm’s assets exceeds the value of debt by a larger

margin, the sensitivity of debt value to changes in asset value approaches zero and the sensitivity

of equity value to changes in asset value approaches one (Merton, 1974). Therefore, if the

sensitivity to changes in asset value of the value of employee stock options is more similar to

equity than it is to debt, then the sensitivity of option value to changes in asset value should be

closer to one (zero) for firms further from (closer to) debt default. As a test of this relation, we

present evidence on the sensitivity of the change in the value of liabilities, ∆MVL, equity, ∆MVE,

and employee stock options, ∆MVO, to changes in the value of assets, ∆MVA, for firms with

different distances to default on their debt. We also provide evidence on the expected return on

options, RET_OPT.

We base our estimates of option value and expected return on the approach in Daves and

Ehrhardt (2007), as outlined in Appendix B. Daves and Ehrhardt (2007) shows how to compute

capital components’ values and required returns using only market observables. Specifically,

using EQUITYVOL, common shares outstanding, and employee stock option disclosure data

from Compustat, we first simultaneously solve equations (B3) through (B6) in Appendix B to

31

obtain estimates of option value and the partial derivative of option value with respect to share

price. We then input those estimates, combined with share price, ECC, and the risk-free interest

rate, into equation (B6) in the Appendix to obtain an estimate of the return on options,

RET_OPT. To estimate the values of assets and liabilities, we use the procedure described in

Barth, Hodder, and Stubben (2008), which builds on Merton (1974) and Hillegeist et al. (2004).

Given observed equity value and historical stock return volatility, we invert the Merton (1974)

model to estimate the value of assets, which is then used to estimate the value of liabilities.

For purposes of comparison, we also estimate the value of employee stock options using

the Black-Scholes (1973) option pricing formula, based on inputs from the employee stock

option disclosure data from Compustat; namely, average exercise price, expected stock return

volatility, risk-free interest rate, expected dividend yield, and time to maturity. We follow

Landsman et al. (2006) to estimate the average life for options outstanding.

Table 4, Panel A, presents distributional statistics for and Panel B presents correlations

between the variables we construct. We refer to the Daves and Ehrhardt (2007) estimate of the

value of employee stock options as the D-E value, and the Black-Scholes (1973) estimate as the

B-S value, both scaled by market value of common equity. The estimation methods differ most

with respect to their treatment of dilution and leverage.23

23 The Black-Scholes (1973) option pricing model is frequently used by firms to estimate the value of employee options at the grant date (Aboody, Barth, and Kasznik 2006; Landsman et al. 2006). The binomial pricing model is another common method used to estimate option value. As commonly applied, neither of these methods adjusts for the effects of dilution or considers debt in the capital structure. Appendix A shows how the binomial model can be adjusted for dilution and leverage.

How large differences are is an

empirical question. Panel A reveals that the mean B-S value of employee options is 6% of the

market value of common equity and the mean D-E value is 4%. These statistics indicate that the

Black-Scholes (1973) formula results in values of employee stock options that are overstated by

approximately 50% when dilution is ignored. Consistent with the greater risk of employee stock

32

options, the mean expected return on options, RET_OPT, of 22% is substantially higher than the

mean expected equity cost of capital, ECC, of 13%.

Additional descriptive statistics presented in Panel B reveal that B-S value and D-E value

are positively correlated, although not highly (Corr. = 0.14). Panel B also reveals that, contrary

to theory, B-S value is negatively correlated with BETA (Corr. = –0.20). This is not the case for

D-E value, which is positively correlated with BETA (Corr. = 0.17). B-S value is positively

correlated with LEVERAGE (Corr. = 0.08) and D-E value is negatively correlated with

LEVERAGE (Corr. = –0.26). Neither value estimate is highly correlated with equity volatility,

EQUITYVOL.24

Table 5 presents statistics that enable us to assess the sensitivity to changes in asset value

of equity value, liability value, and employee option value as the distance to default increases.

Panel A presents the median ratio of the change in the values of equity, debt, and options to the

change in asset value by distance-to-default quintile. We define distance to default as the excess

of asset market value over liability book value, scaled by the market value of assets. As

expected, Panel A reveals that the unit change in equity value per unit change in asset value

monotonically decreases as the distance to default increases (0.98 for quintile 5 to 0.73 for

quintile 1). Also as expected, Panel A reveals the opposite for debt—that is, the unit change in

debt value per unit change in asset value monotonically increases as the distance to default

increases (–0.02 for quintile 5 to 0.25 for quintile 1). These relations are consistent with Merton

Consistent with theory, the D-E required return on options, RET_OPT, is

positively correlated with BETA (Corr. = 0.12). RET_OPT is positively correlated with

EQUITYVOL by construction. Overall, the statistics in Table 4 indicate that D-E value and

RET_OPT are consistent with the theory from which they are derived.

24 Recall that the value of a warrant is increasing in the volatility of firm assets and decreasing in leverage. Leverage increases the volatility of equity but not necessarily the volatility of assets. Therefore, the value of warrants is not necessarily increasing in the volatility of common equity.

33

(1974), which shows that as the probability of default increases toward certainty, debt holders

become claimants on the firm’s assets and, thus, effectively equity holders.

More importantly for our research question, as predicted, Panel A reveals that the change

in D-E value exhibits a convex pattern that is similar to that of equity value and opposite that of

debt value. Namely, D-E value decreases monotonically in the change in asset value as the

distance to default decreases (0.06 for quintile 5 to 0.01 for quintile 1). To test whether these

patterns are significant, we estimate the relation between each of the value sensitivities and

distance to default. Table 5, Panel B, presents the findings. It reveals that the sensitivity of

common equity value and option value to changes in asset value each is significantly positive (t

= 5.16 for equity value and 8.67 for option value). In contrast, the sensitivity of liability value to

changes in asset value is significantly negative (t = –5.24).

Taken together, the findings in Table 5 provide corroborative evidence that employee

stock options share more in common with equity than with debt. This, too, suggests that options

would be more appropriately classified as equity, not liabilities, for financial reporting purposes.

VI. SUMMARY AND CONCLUDING REMARKS

This study seeks to determine whether employee stock options have characteristics of

liabilities or of equity. We focus our tests on how the options relate to the risk of and expected

return on firms’ common equity. Based on previously untested finance theory we predict that

because employee stock options are warrants issued and settled by the firm, the presence of

employee stock options is associated with both lower risk of and expected return on common

equity. Our evidence supports this prediction. In particular, we find that realized common

equity return volatility, the volatility implied by a firm’s traded options, and expected equity cost

34

of capital all are negatively associated with the extent to which firms have outstanding employee

stock options.

Consistent with the theory upon which our tests are based, we find that the relation

between employee stock options and the risk of common equity is significantly less negative for

firms with longer-term options and for firms that reprice options. These findings indicate that

the relation between common equity and options with these attributes is more like debt than it is

for options without these attributes. For firms with longer-term options, the relation between

employee stock options and common equity risk is muted but significantly negative, which

indicates that these options are only somewhat more like debt in the capital structure than

shorter-term options. However, for firms that reprice options, the relation between options and

common equity risk is positive, which indicates that these options have characteristics of debt,

not equity. These findings reveal that some employee stock options have terms that negate the

equity-like characteristics of warrants.

We also find that the sensitivity of the value of employee stock options to changes in