argentas: the future of money · argentas • argentashas a realistic project that creates a...

TRANSCRIPT

Argentas18 June 2018 © Argentas I Confidential1

Argentas: The Future of MoneyApril 2018

Argentas

• Where will global finance go? Global finance will go crypto, and there is no way back• Bank accounts as we know them will disappear, replaced by the blockchain• Banks as we know them today will also vanish and morph into blockchain network

interfaces – blockchain will record transactions and hold ‘account balances’• Bank services will become dapps, decentralized network applications• Enabled by the distributed ledger technologies (DLT), first time ever, truly global,

instant and virtually free payments are possible, all taking place in the blockchain• DLTs have first time ever made possible to create a truly global open financial

architecture and system – without any central authority or control• No one has so far created a ‘perfect’ solution, despite of many good projects

18 June 2018 © Argentas I Confidential2

The opportunity

Argentas

• Argentas has a realistic project that creates a powerful platform to transition global payments and ‘centralized’ banking into the decentralized world of blockchain

• The project is not only to create the right blockchain but the interfaces and model bridge entities to facilitate smooth movement and transition between traditional and crypto economies, boosting the growth of the crypto economy

• Argentas decentralizes banking and payments and gives power back to the people• The network will become the ‘de-central bank of crypto’, which will generate

immense value to its users in terms of money, time and effort saved• Global finance will be made democratic first time: universal access will be given to

all, and the bank will truly be in the pocket of every user: true financial inclusion

18 June 2018 © Argentas I Confidential3

Why Argentas?

Argentas18 June 2018 © Argentas I Confidential4

Where does the network value come from?Migration from old to new will inevitably happen like in many industries before

VisaMarket cap

USD 275B

MasterCardMarket cap

USD 180B

AmexMarket capUSD 80B

SWIFTDaily tx volume

At least USD 5 trillion

BANKSGlobal market cap

Trillions of dollars (e.g. 70 biggest ca. USD 6 trillion)

Crypto

DLT / Blockchain

space

Migration of value:The total global

market cap of banks (largest ones ca. USD

400B) is several trillion dollars, 3 key card

schemes USD 500B+, and SWIFT processes trillions of dollars of payments every day.

Most financial transactions will be

digital and decentralized, and

Argentas is well positioned to capture

this migration of value.

Argentas18 June 2018 © Argentas I Confidential5

How we do it?Argentas DLT network “HydraNet” description

Speed (low latency): Fast transaction confirmation times of 2-5 seconds (base case), w/objective instant (< 1 second)

Tx throughput (scalability): Targeting at least 50-60 thousand tx per second (vs. Visa), but research on “lightning network” (no viable commercial application exists yet) as secondary payment channel to enable up to millions of tx per second

No mining: Consensus-based tx validation (based on a variation of ‘Byzantine Generals’ Agreement), no proof-of work (PoW) / proof-of-stake (PoS), consumes much less computing power, much more environmentally friendly

Low transaction cost: Lack of mining consumes much less computing power, causing much less network congestion and capacity problems, which enables much lower costs

Decentralized control, transparency and flexible trust: Anyone free to access and participate the network and choose who to trust –anyone equal, enabling complete financial inclusion

Safety and security: The security should not only rest on “normal” digital signatures and hash families (base case) but eventually be quantum resistant (for which more research is needed).

Easy, convenient, intuitive user interfaces: User interfaces – e.g. the native the wallet, are simple and easy to use, intuitively facilitating buy, sell, store and transfer of value and use of any available app.

1

2

34

5 6

8

Smart sharding: Research on the possibility not to replicate the whole ledger entirely (as in base case) but portion it across the network through “smart sharding”, lowering network load & increasing overall capacity

7

Argentas18 June 2018 © Argentas I Confidential6

The Argentas EcosystemThe 3 dimensions of the project: network, interfaces & bridge entities and dapps

Phase 1: Network and interfaces & bridge entities Phase 2: Further dapps

1. HydraNet 2. HydraNet interfaces & bridge entities 3. Dapps / “dapp economy” leveraging the power of the network (type examples)

Argentas Ecosystem

Possible lightning layer for secondary payment channels to increase confirmation speed & throughput

HydraNet Core w/nodesRunning Hydra ProtocolDecentralized exchange

WalletNative HydraNet wallet as network interface, for native digital asset and any asset transferred on the network,

dapp store

ExchangeInterface of native decentralized exchange / other

exchanges (crypto & ‘traditional’) interfacing with the network

Bank (and other entities)Banks (incl. the model network bridge banks and any bank interfacing with the network), and other entities

interfacing with the network

Merchant processing

POS, Internet payment order processing

LendingDecentralized loans,

mortgages, SME lending, micro lending

InvestingStocks, bonds, funds,

savings instruments – any asset issued on the net

Venture capitalAccess to venture capital,

venture debt, seed financing

Identity mgmtIDs, authentication based

on the immutability of blockchain record

Credit scoringCredit scoring enabling

lending, based on immutable DLT records

Argentas18 June 2018 © Argentas I Confidential7

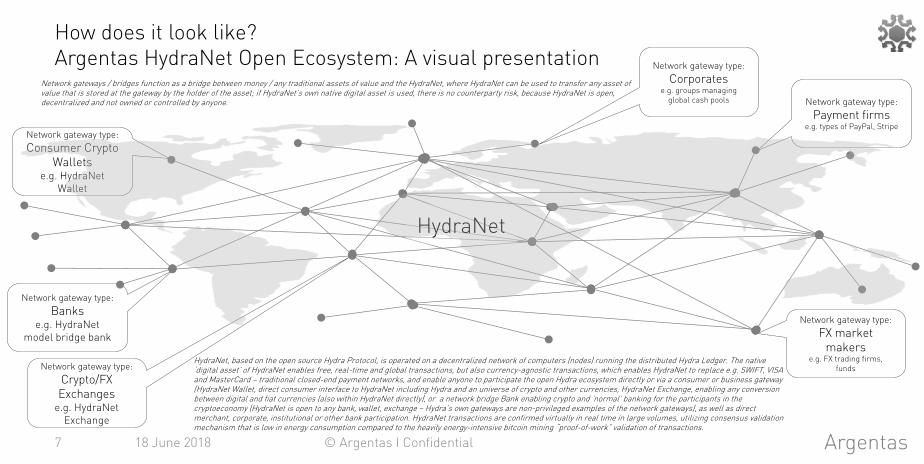

How does it look like?Argentas HydraNet Open Ecosystem: A visual presentation

Network gateway type:

Bankse.g. HydraNet

model bridge bank

Network gateway type:

Consumer Crypto Wallets

e.g. HydraNetWallet

Network gateway type:

Crypto/FX Exchanges

e.g. HydraNetExchange

Network gateway type:

FX market makers

e.g. FX trading firms, funds

Network gateway type:

Payment firmse.g. types of PayPal, Stripe

Network gateway type:

Corporatese.g. groups managing

global cash pools

HydraNet, based on the open source Hydra Protocol, is operated on a decentralized network of computers (nodes) running the distributed Hydra Ledger. The native ‘digital asset’ of HydraNet enables free, real-time and global transactions, but also currency-agnostic transactions, which enables HydraNet to replace e.g. SWIFT, VISA and MasterCard – traditional closed-end payment networks, and enable anyone to participate the open Hydra ecosystem directly or via a consumer or business gateway (HydraNet Wallet, direct consumer interface to HydraNet including Hydra and an universe of crypto and other currencies, HydraNet Exchange, enabling any conversion between digital and fiat currencies (also within HydraNet directly), or a network bridge Bank enabling crypto and ’normal’ banking for the participants in the cryptoeconomy (HydraNet is open to any bank, wallet, exchange – Hydra’s own gateways are non-privileged examples of the network gateways), as well as direct merchant, corporate, institutional or other bank participation. HydraNet transactions are confirmed virtually in real time in large volumes, utilizing consensus validation mechanism that is low in energy consumption compared to the heavily energy-intensive bitcoin mining “proof-of-work” validation of transactions.

Network gateways / bridges function as a bridge between money / any traditional assets of value and the HydraNet, where HydraNet can be used to transfer any asset of value that is stored at the gateway by the holder of the asset; if HydraNet’s own native digital asset is used, there is no counterparty risk, because HydraNet is open, decentralized and not owned or controlled by anyone.

HydraNet

Argentas

• Even if banks and bank accounts as we know them now will eventually disappear and morph into the blockchain, as of today, they can interface with and act as important bridges between the crypto economy and the traditional economy, holding balances of fiat money and other assets that are issued as network credit

• Recent bad treatment of crypto users by traditional banks, blocking access to their payment, card and other services, makes it urgent to create crypto friendly banks

• A bank entity can act as a laboratory for the transition from closed-ledger “centralized” banks to the DLT “decentralized” crypto banking, and dapps replacing banking services on the network, eventually making the network the bank

• Such model bank will run an entirely digital online platform leveraging machine learning / artificial intelligence and minimize human intervention

18 June 2018 © Argentas I Confidential8

The role of a network bridge bankWhy a bank entity adds value for a network that will render banks useless?

Argentas18 June 2018 © Argentas I Confidential9

AXU specification for token distributionPrivate pre-sale and public sale (ICO)

Token symbolAXU

Token nameArgentasExchange

Unit

Total issued1,000,000,000

AXU

(fixed – no more can be issued)

Private presale100,000,000AXU (max)10% of total

Public sale600,000,000

AXU 60% of total

Team & reserve300,000,000

AXU 30% of total

(for further development)

NetworkStellar

(for the token distribution process)

Currency accepted

XLM (lumen)

Private presale starts

8 June 2018 noon

Private presale ends

Latest when hardcap ca. 100M tokens distributed

Offer price1 XLM = 2.5 AXU

(at presale discounted vs. public sale at least by 50%)

Public sale to be announced

Q3/2018at a higher offer price per token

The token issued for the crowdsale is not the same as the native digital asset of HydraNet blockchain that can only be issued when the HydraNet is launched.

Token details

Argentas

Q4/2017-Q1/2018• Initial network

research and development

• Work on team and recruitment, preparation of legal and operating structures

• Preparation of primer, white pape, presentation, website, token distribution, terms & conditions, social media content

18 June 2018 © Argentas I Confidential10

Roadmap

Q2-Q3/2018• Token distribution

(private presale and ICO)

• Release of technical white paper

• Continued recruitment, structures and operational setup Development of HydraNet Protocol

• Development of HydraNetincluding the native digital asset

• Development of the Wallet (native, multiasset) and Exchange (native decentralized + gateway interface) applications

Q1/2019• Launch of the

Minimal Viable Test Network of HydraNet

• Testing and security audits of HydraNet

Q2/2019• Deployment of the

stable version of HydraNet

• Launch of Wallet• Launch of

Exchange • Launch of

application development and creation of HydraNet-based ecosystem

• Development of partnerships and expansion of use cases for HydraNet

Q3-Q4/2019• Launch of

HydraNet bridges (including the optional bridge model Bank that as an operating entity is subject to licensing that may take longer)

• Expansion of gateways and network dappecosystem

2020-• Further

development of a global network of gateways

• Expansion of the HydraNetecosystem through continued direct and third party decentralized application development, partnerships and user volume growth

Roadmap timeline subject to change depending on funding and resources available, progress in the technology development and changes in operating environment

Argentas18 June 2018 © Argentas I Confidential11

The Argentas Project is about fulfilling our missionWe have all what it takes to deliver with success

We are here to make global financial services faster, cheaper, simpler, more convenient, accessible and secure, and to offer it all with style and substance.

“

#1Passion for what

we do – inspired by the opportunity to

truly transform global finance

#2Our deep & wide competence & experience in

banking, payments & other financial

services

#3Technology - our

technological competence and track record in

creating successful Fintech platforms

#4Innovation and

creativity - our ability to create and

innovate and make real entirely new,

pioneering things

#5Style & substance –

our aesthetic capability to create

sleek things of quality that look & feel good

inside out