argos retail group - experian plc - home · argos retail group 2 argos retail group •agr mledo...

TRANSCRIPT

Argos Retail Group

2

Argos Retail Group

• ARG model

• Argos Direct model

• Scale advantage

• Future opportunities

3

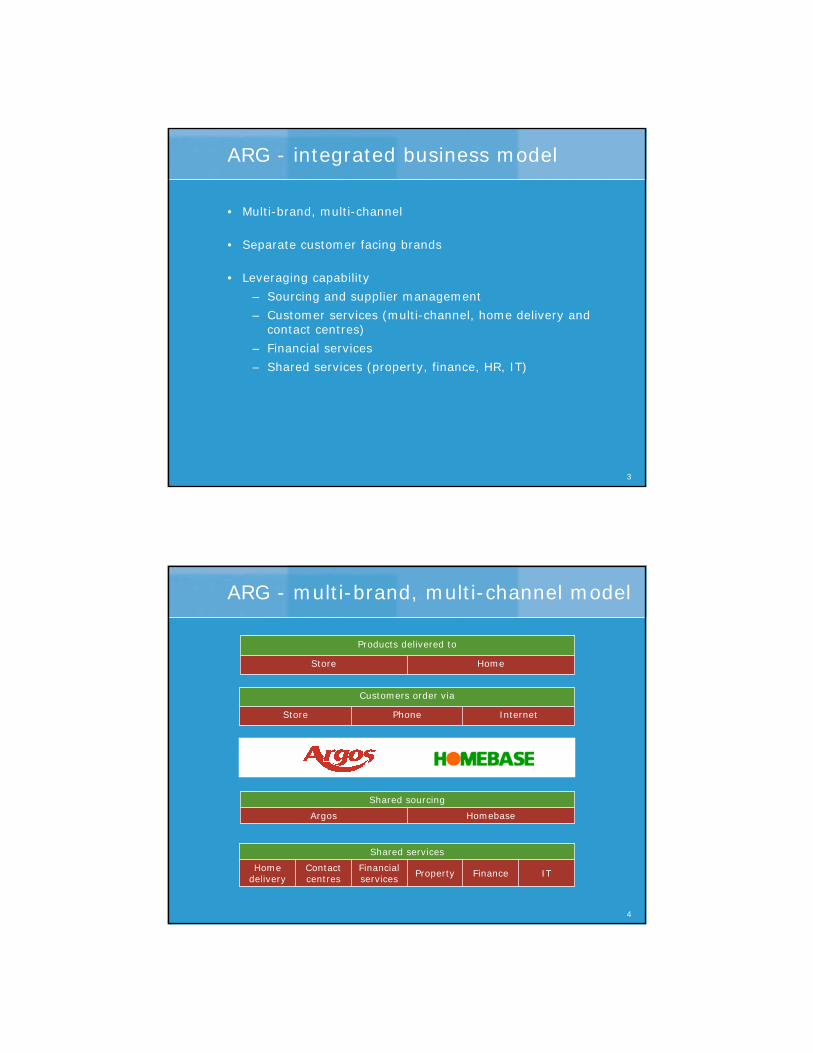

ARG - integrated business model

• Multi-brand, multi-channel

• Separate customer facing brands

• Leveraging capability

– Sourcing and supplier management

– Customer services (multi-channel, home delivery and contact centres)

– Financial services

– Shared services (property, finance, HR, IT)

4

ARG - multi-brand, multi-channel model

ITFinancePropertyFinancial services

Contact centres

Home delivery

Shared services

InternetPhone Store

Customers order via

HomeStore

Products delivered to

HomebaseArgos

Shared sourcing

5

Argos Direct - business model

• Product markets

• Customer proposition

• Competitive advantages

6

Attractive markets

• Large markets

• Fast growing markets

• Fragmented markets

• Requires national home delivery service

• Big ticket market currently challenging

7

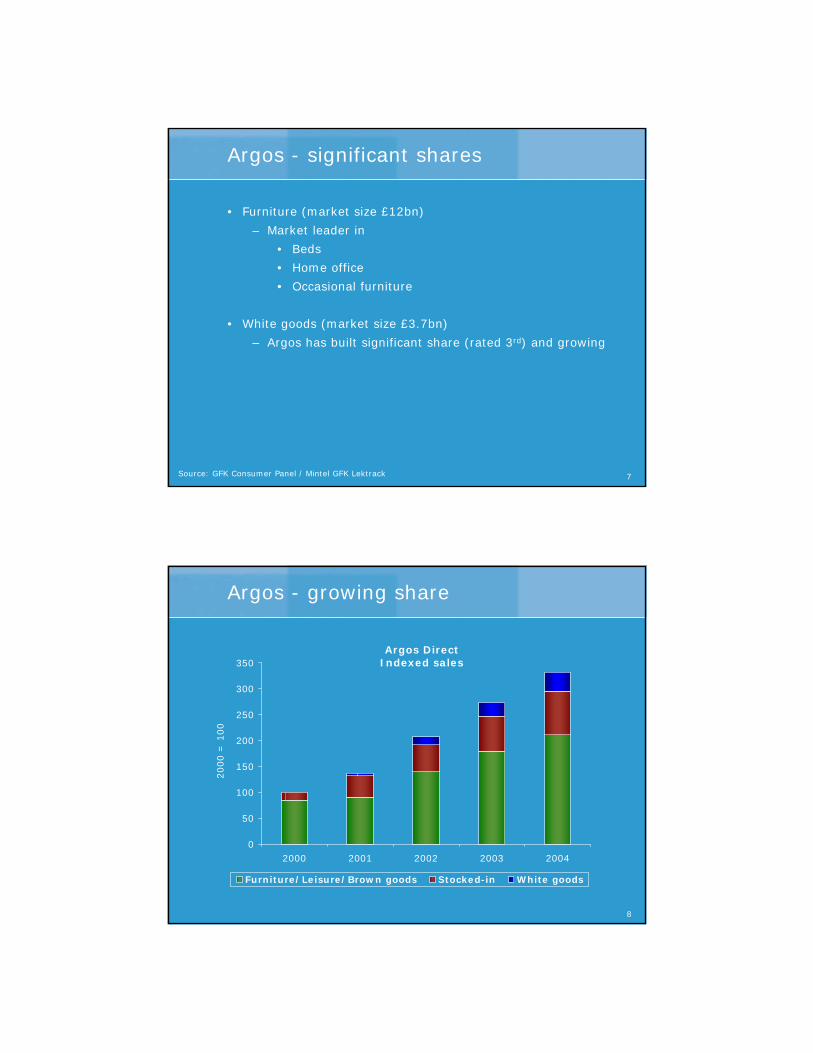

Argos - significant shares

• Furniture (market size £12bn)

– Market leader in

• Beds

• Home office

• Occasional furniture

• White goods (market size £3.7bn)

– Argos has built significant share (rated 3rd) and growing

Source: GFK Consumer Panel / Mintel GFK Lektrack

8

Argos - growing share

0

50

100

150

200

250

300

350

2000 2001 2002 2003 2004

Furniture/Leisure/Brown goods Stocked-in White goods

Argos DirectIndexed sales

2000 =

100

9

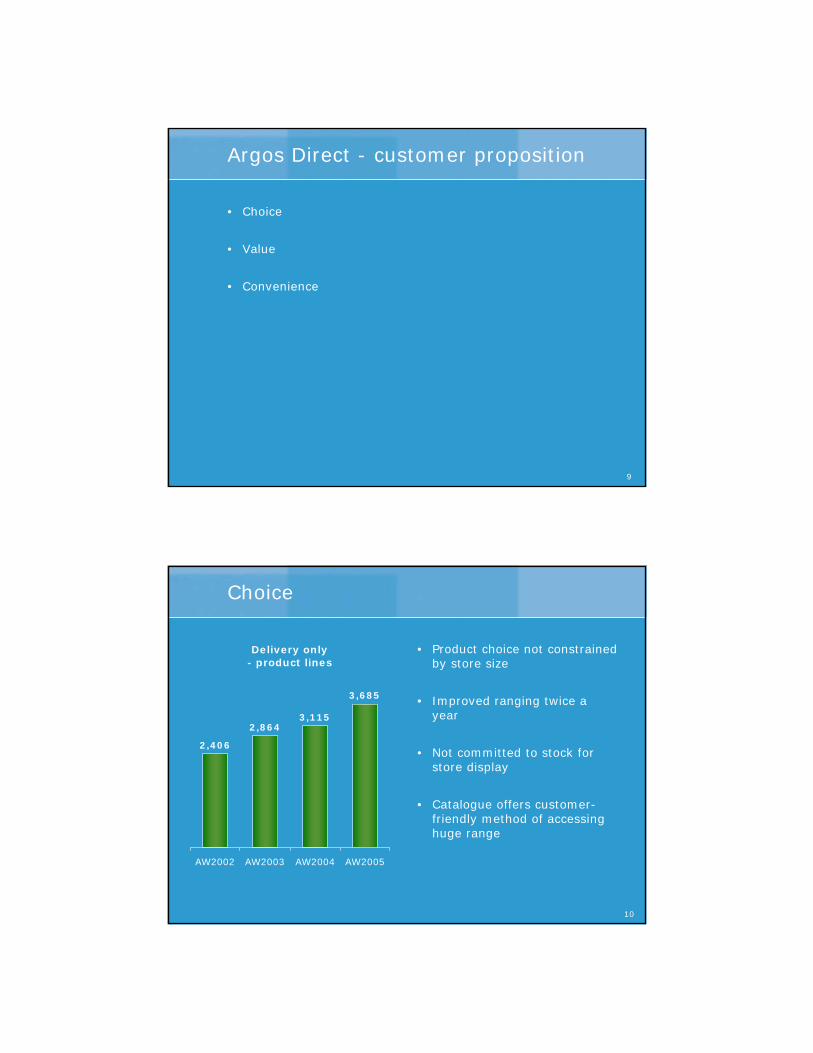

Argos Direct - customer proposition

• Choice

• Value

• Convenience

10

Choice

Delivery only - product lines

2,406

2,8643,115

3,685

AW2002 AW2003 AW2004 AW2005

• Product choice not constrained by store size

• Improved ranging twice a year

• Not committed to stock for store display

• Catalogue offers customer-friendly method of accessing huge range

11

Value

• Market beating deals -“WOW” offers

• Promotional offers

• 16 day money back guarantee

• Direct sourcing and supply chain

• Credit - easy ways to pay

• Great value for new looks

12

Convenience

• Multi-channel proposition

• Delivery within 48 hours for small products and on average 14 days for larger products

• Market-leading home delivery service – am/pm and Saturday

• All products available for delivery to home

13

Competitive advantages

• Large scale national operation

• Sourcing scale

• Cost efficiency

• Attractive economic model

14

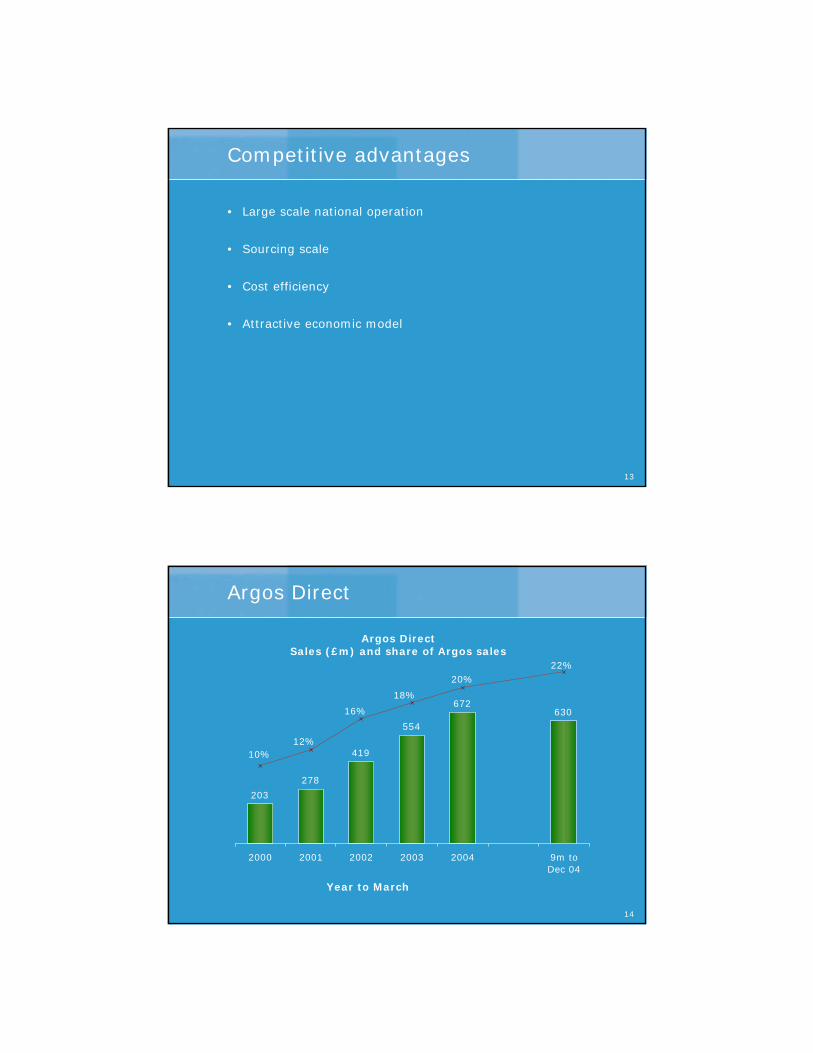

Argos Direct

203

278

419

554

672630

22%20%

18%

16%

12%10%

2000 2001 2002 2003 2004 9m toDec 04

Argos DirectSales (£m) and share of Argos sales

Year to March

15

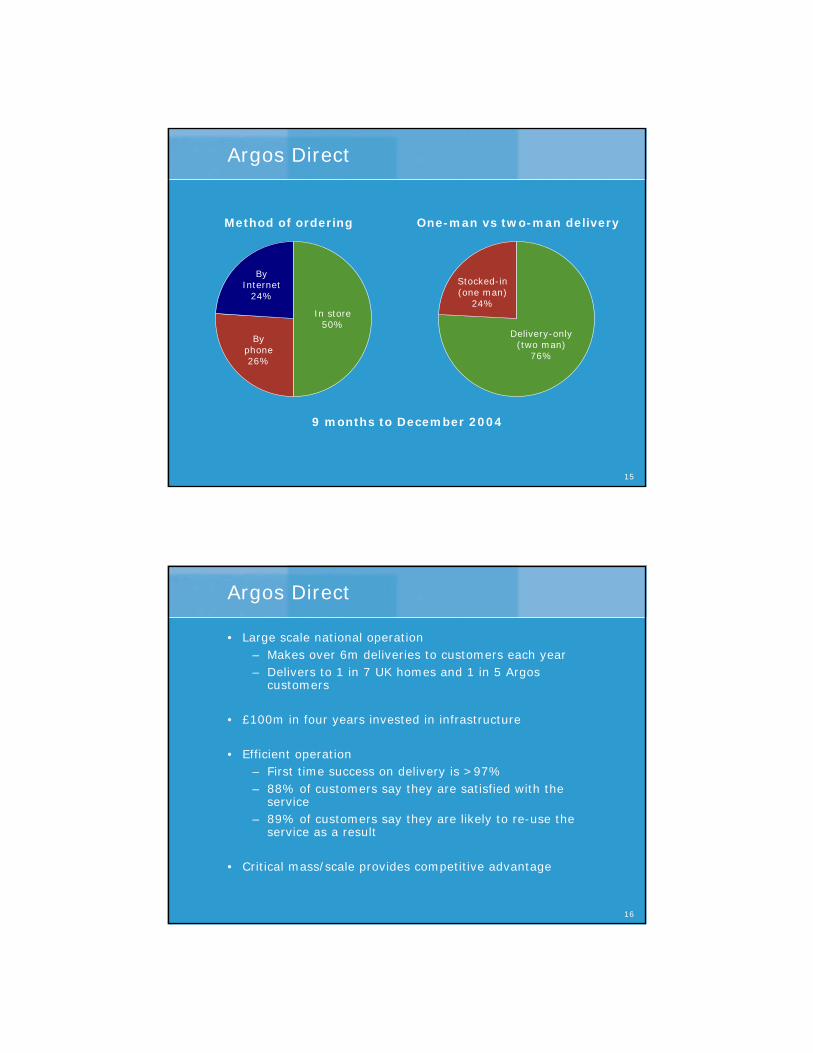

Argos Direct

By phone26%

In store50%

By Internet

24%

Method of ordering

Delivery-only(two man)

76%

Stocked-in(one man)

24%

One-man vs two-man delivery

9 months to December 2004

16

Argos Direct

• Large scale national operation– Makes over 6m deliveries to customers each year– Delivers to 1 in 7 UK homes and 1 in 5 Argos

customers

• £100m in four years invested in infrastructure

• Efficient operation– First time success on delivery is >97%– 88% of customers say they are satisfied with the

service– 89% of customers say they are likely to re-use the

service as a result

• Critical mass/scale provides competitive advantage

17

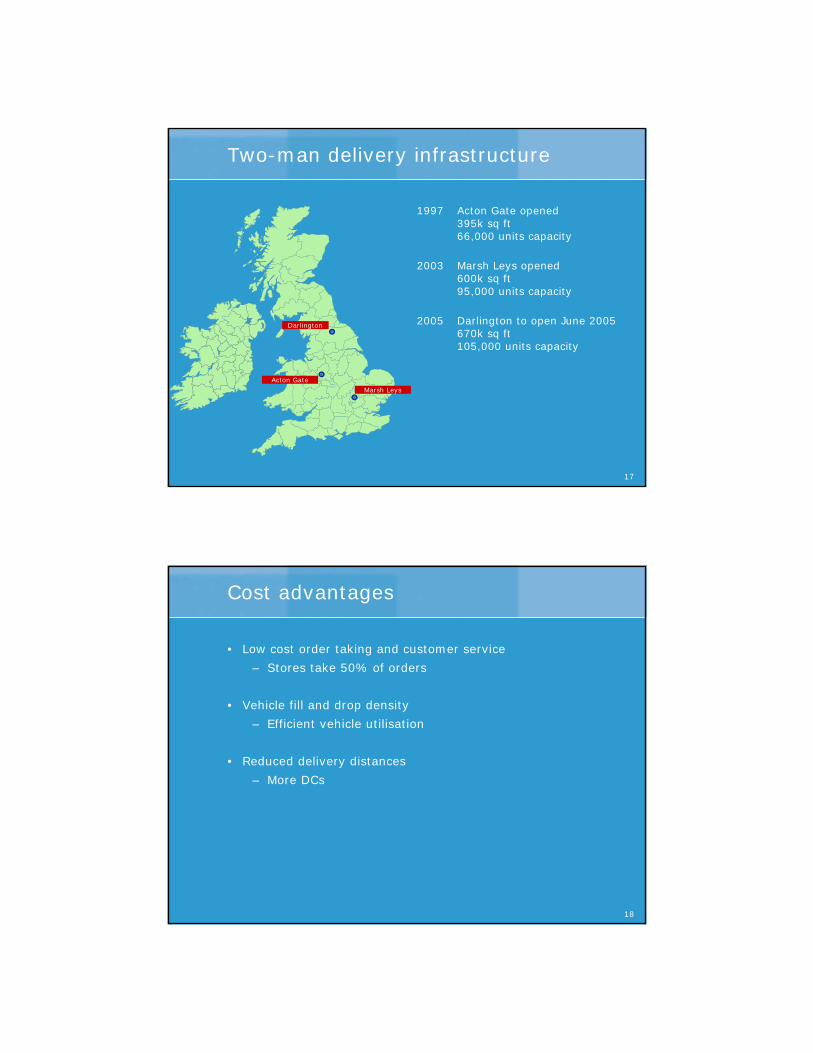

Two-man delivery infrastructure

1997 Acton Gate opened395k sq ft66,000 units capacity

2003 Marsh Leys opened600k sq ft95,000 units capacity

2005 Darlington to open June 2005670k sq ft105,000 units capacity

Darlington

Acton Gate

Marsh Leys

18

Cost advantages

• Low cost order taking and customer service

– Stores take 50% of orders

• Vehicle fill and drop density

– Efficient vehicle utilisation

• Reduced delivery distances

– More DCs

19

Leveraging the infrastructure

• Homebase volume

• National delivery service

• Argos Direct provides over 40% cost saving versus third party carrier

• Argos Direct has proven capabilities

20

• Customers pay 100% in advance of delivery

• Delivery within 14 days

• Stock turn over 25 times

• Average creditor payment is 45 days

Working capital efficiencies

21

Future opportunities

• Improving Argos Direct proposition

– More choice

– Enhancing delivery options

• Leverage infrastructure for Homebase

– Furniture Direct

– Homebase website

– Homebase appliance catalogue trial

– Garden furniture

22

Homebase - growth

• Wider furniture range, great prices, free and fast delivery

• 52 pages

• 770 options

• On website

• Currently in 19 stores

• Leverage Argos product pool and infrastructure

Furniture Direct

23

Homebase - growth

• Launched in February 2005

• 4,000 Internet exclusive lines (Argos product and infrastructure)

• 4,000 Homebase lines (non-transactional) to be added in April

• Leveraging Argos web technologies

• Leveraging product pool and infrastructure

Homebase website

24

Homebase - growth

• Trialling Homebase appliance catalogue from Easter

– 52 pages of Argos products

– On website

– In 20 stores

• Leveraging Argos product pool and infrastructure

White goods

25

Summary

• Argos Direct continues to drive growth in Argos

• Large market opportunity

• Multi-brand approach

• Leveraging single infrastructure

• Scale and economic model providing competitive advantage

26

Marsh Leys - key facts

• 38 acre site

• 656k sq ft warehouse

• 96 loading docks

• 175 lorry parking spaces

• Employs 410 over 3 shifts

• Dispatch c£300m of sales in last 12 months

• Equivalent to 1.9m units

• Dispatch 140,000 components per week (equal to 1,156 delivery vehicles per week)

27

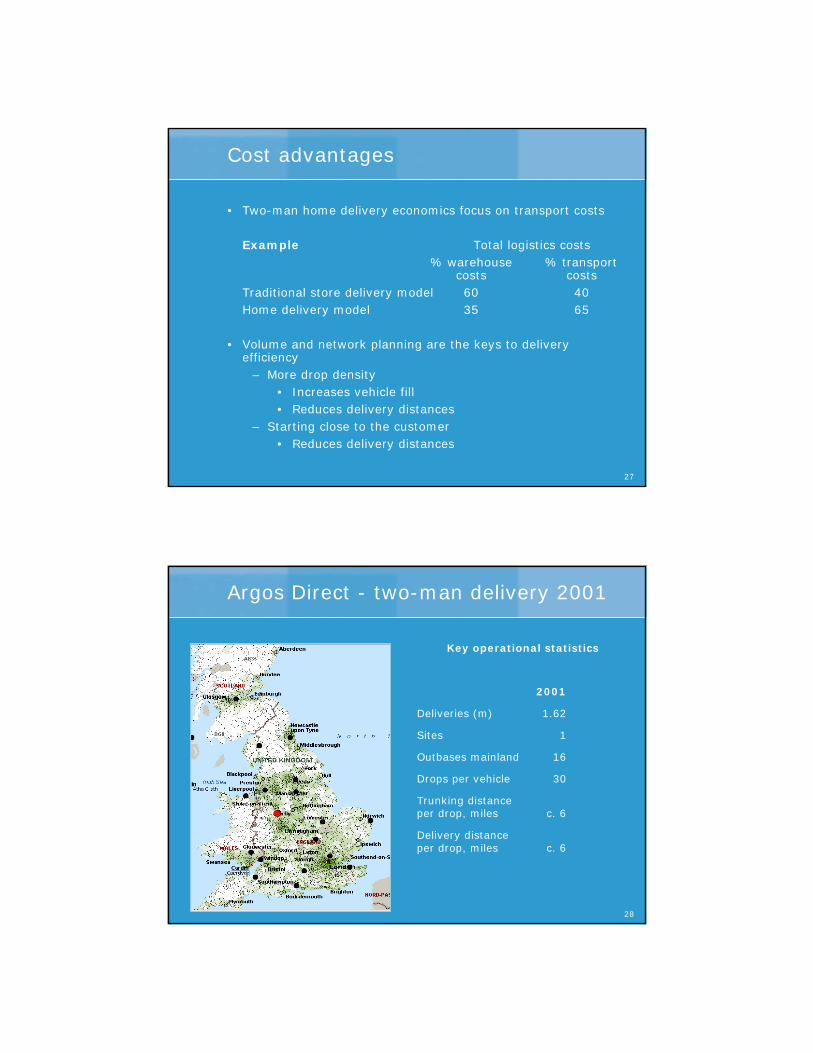

Cost advantages

• Two-man home delivery economics focus on transport costs

Example Total logistics costs% warehouse % transport

costs costsTraditional store delivery model 60 40Home delivery model 35 65

• Volume and network planning are the keys to delivery efficiency

– More drop density• Increases vehicle fill• Reduces delivery distances

– Starting close to the customer• Reduces delivery distances

28

Argos Direct - two-man delivery 2001

Key operational statistics

2001

Deliveries (m) 1.62

Sites 1

Outbases mainland 16

Drops per vehicle 30

Trunking distanceper drop, miles c. 6

Delivery distanceper drop, miles c. 6

29

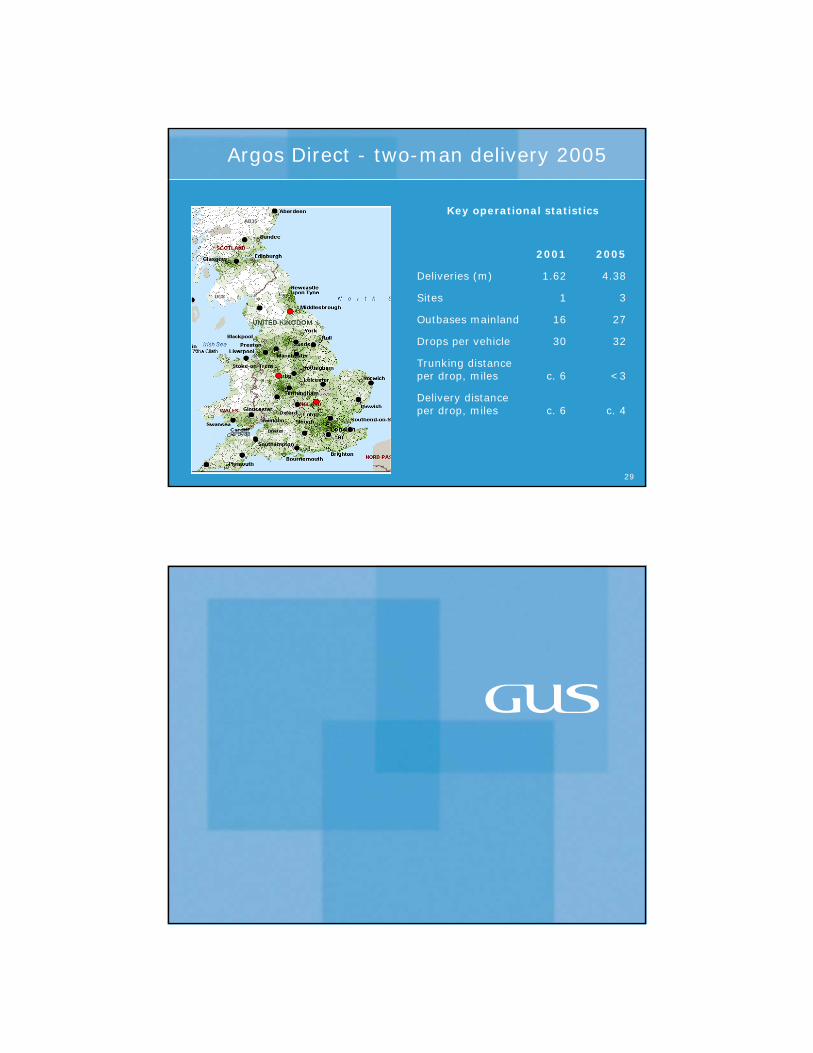

Argos Direct - two-man delivery 2005

2001 2005

Deliveries (m) 1.62 4.38

Sites 1 3

Outbases mainland 16 27

Drops per vehicle 30 32

Trunking distanceper drop, miles c. 6 <3

Delivery distanceper drop, miles c. 6 c. 4

Key operational statistics