arqiva broadcast parent limited and arqiva group … broadcast parent limited and arqiva group...

TRANSCRIPT

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited

1

Arqiva Broadcast Parent Limited and

Arqiva Group Parent Limited

Financial Report Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited

2

CONTENTS

Page

FORWARD LOOKING STATEMENTS ................................................................................................... 3

INDUSTRY AND MARKET INFORMATION ........................................................................................... 4

DESCRIPTION OF BUSINESS .............................................................................................................. 5

FINANCIAL RESULTS AND RECENT DEVELOPMENTS .................................................................... 6

EXECUTIVE SUMMARY ........................................................................................................................ 7

Financial Overview ............................................................................................................................. 7

Recent Developments since 30 June 2014 ....................................................................................... 7

Financial Results for the three months ended 30 September 2014 ................................................ 10

Profit and Loss ................................................................................................................................. 10

Capital expenditure .......................................................................................................................... 17

Net cash flows .................................................................................................................................. 18

Contractual Obligations and Commitments ..................................................................................... 22

Critical Accounting Policies ................................................................................................................... 25

Appendix ............................................................................................................................................... 28

Description of Certain Income Statement Line Items ...................................................................... 28

Note Regarding EBITDA and Reconciliation of EBITDA to Net Cash Inflow From Operating Activities ........................................................................................................................................... 31

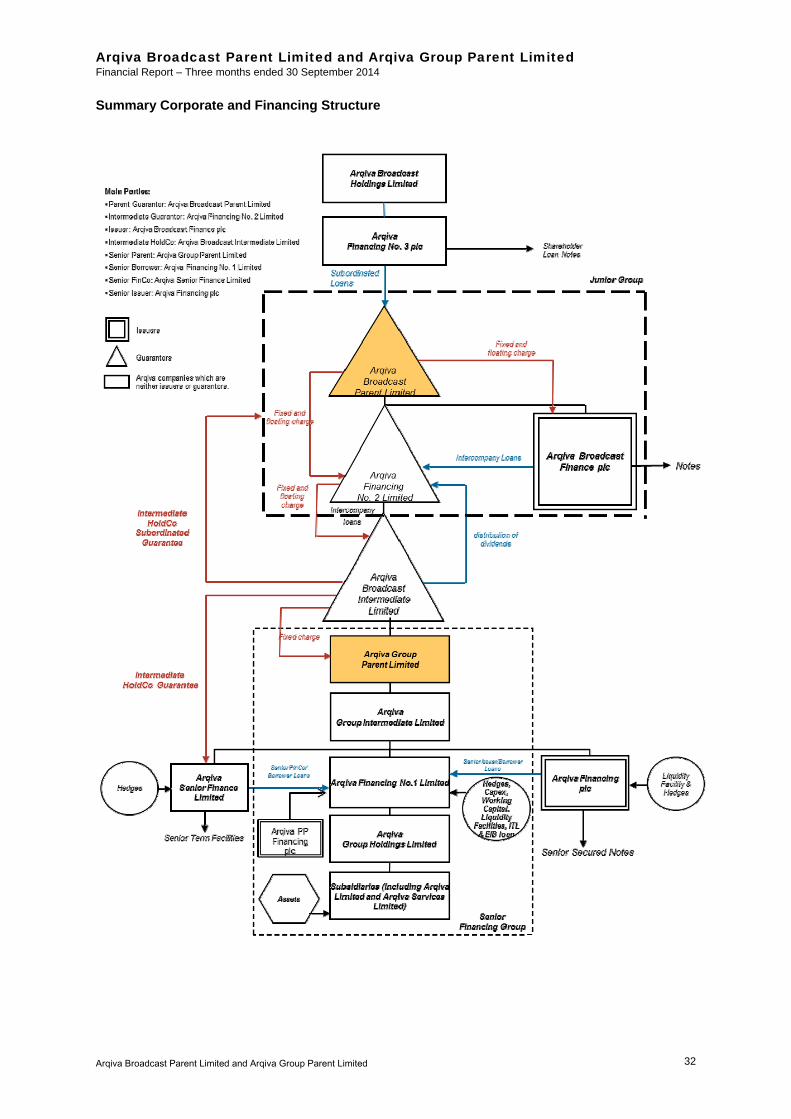

Summary Corporate and Financing Structure ................................................................................. 32

CONDENSED CONSOLIDATED FINANCIAL STATEMENTS FOR THE THREE MONTHS ENDED 30 SEPTEMBER 2014 OF ABPL AND AGPL ...................................................................................... 33

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 3

THIS FINANCIAL REPORT IS NOT AN OFFER OR SOLICITATION OF AN OFFER TO BUY OR SELL SECURITIES. IT IS SOLELY FOR INFORMATION PURPOSES ONLY. THIS FINANCIAL REPORT DOES NOT CONTAIN ALL OF THE INFORMATION THAT IS MATERIAL TO A PROSPECTIVE INVESTOR.

This document is not a prospectus for any securities or transaction. Investors should only subscribe for any securities on the basis of information in a relevant prospectus and not on the basis of any information provided herein. This document does not disclose all the risks and other significant issues related to an investment in any securities/transaction. Prior to transacting, potential investors should ensure that they fully understand the terms of any securities/transaction and any applicable risks.

This Financial Report has been prepared pursuant to Condition 4.5 of the Junior Notes (£600m of notes issued by Arqiva Broadcast Finance plc) and pursuant to Paragraph 5.1 and Paragraph 5.4 of Schedule 2 of the CTA and certain information reporting covenants of the Notes. The date of this Financial Report is 24 November 2014. Unless otherwise defined herein, capitalised terms have the meanings given in the final offering prospectus for the multicurrency programme for the issuance of Senior Notes dated 21 February 2013. This Financial Report has been prepared by the Group (Arqiva Broadcast Parent Limited, Arqiva Group Parent Limited and their subsidiaries) and may be amended and supplemented and may not be relied upon for the purposes of entering into any transaction. Although the Group has taken all reasonable care to ensure that the information herein is accurate and correct, neither of the Group, nor any of its respective directors, officers, employees, shareholders, affiliates, agents, advisers, other representatives (collectively, Representatives) makes any additional representation, warranty or undertaking, express or implied, as to the fairness, accuracy, completeness or correctness of the information or the opinions contained herein or any other material discussed in the Financial Report.

The financial information set forth in this Financial Report has been subjected to rounding adjustments for ease of presentation. Accordingly, in certain instances, the sum of the numbers in a column or a row in tables may not conform exactly to the total figure given for that column or row. Percentage figures included in this Financial Report have not been calculated on the basis of rounded figures but have been calculated on the basis of such amounts prior to rounding.

The views reflected herein are solely those of the Group and are subject to change without notice. All estimates, projections, valuations and statistical analyses are provided to assist the recipient in the evaluation of the matters described herein and may be based on subjective assessments and assumptions and may use one among alternative methodologies that produce different results and to the extent that they are based on historical information, they should not be relied upon as an accurate prediction of future performance. Certain analysis is presented herein and is intended solely for purposes of indicating a range of outcomes that may result from changes in market parameters. It is not intended to suggest that any outcome is more likely than another, and it does not include all possible outcomes or the range of possible outcomes, one of which may be that the investment value declines to zero. FORWARD LOOKING STATEMENTS

This Financial Report contains various forward-looking statements regarding events and trends that are subject to risks and uncertainties that could cause the actual results and financial position of the Group to differ materially from the information presented herein. When used in this Financial Report, the words “estimate”, “project”, “intend”, “anticipate”, “believe”, “expect”, “should” and similar expressions, as they relate to the Group, are intended to identify such forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. Save as otherwise required by any rules or regulations, the Group does not undertake any obligations publicly to release the result of any revisions to these forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

The risks and uncertainties referred to above include:

actions or decisions by governmental and regulatory bodies, or changes in the regulatory framework in which the Group operates, which may impact the ability of the Group to carry on its businesses;

changes or advances in technology, and availability of resources such as spectrum, necessary to use new or existing technology, or customer and consumer preferences regarding technology;

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 4

the performance of the markets in the UK, the EU and the wider region in which the Group operates;

the ability of the Group to realise the benefits it expects from existing and future projects and investments it is undertaking or plans to or may undertake;

the ability of the Group to develop, expand and maintain its telecommunications infrastructure;

the ability of the Group to obtain external financing or maintain sufficient capital to fund its existing and future investments and projects;

the Group’s dependency on only a limited number of key customers for a large percentage of its revenue; and

expectations as to revenues not under contract.

INDUSTRY AND MARKET INFORMATION

This Financial Report may include market share and industry data which the Group obtained from industry publications and surveys, industry reports prepared by consultants, internal data and customer feedback. None of the third party sources has made any representation, express or implied, and has not accepted any responsibility, with respect to the accuracy or completeness of any of the information contained in this Financial Report.

These third party sources generally state that the information they contain has been obtained from sources believed to be reliable. However, these third party sources also state that the accuracy and completeness of such information is not guaranteed and that the projections they contain are based on significant assumptions. As the Group does not have access to all of the facts and assumptions underlying such market data, statistical information and economic indicators contained in these third party sources, the Group is unable to verify such information and cannot guarantee its accuracy, fairness or completeness. Similarly, internal surveys, industry forecasts and market research have not been independently verified.

In addition, certain information in this Financial Report may not be based on published data obtained from independent third parties or extrapolations thereof but on information and statements reflecting the Group’s best estimates based upon information obtained from trade and business organisations and associations, consultants, and other contacts within the industries in which the Group operates, as well as information published by the Group’s competitors. Such information is based on the following: (i) in respect of the Group’s market position, information obtained from trade and business organisations and associations and other contacts within the industries in which the Group operates, and (ii) in respect of industry trends, the Group’s senior management team’s business experience and experience in the industry and the markets in which the Group operates. The Group cannot assure you that any of the assumptions that it has made in compiling this data are accurate or correctly reflect the Group’s position in its markets.

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 5

DESCRIPTION OF BUSINESS

The Group is the UK’s national provider of essential terrestrial television and radio broadcast infrastructure as well as a key provider of communications services to major distributors of media and wireless voice and data services in the UK. The Group’s core tower business (comprising terrestrial broadcast and wireless site share infrastructure) generates predictable operating profits (which management estimates constituted circa two-thirds of the Group’s gross profits for the year ended 30 June 2014), supported by strong market positions, diverse revenue streams, long-life assets and a significant proportion of revenues coming from long term contracts.

The Group has the following key competitive positions:

regulated position as the sole UK national provider of network access (NA) and managed transmission services (MTS) for terrestrial television broadcasting, the most popular television broadcast platform in the UK. The Group owns and operates all television transmission towers used for digital terrestrial television (DTT) broadcasting in the UK and has long-term contracts with public service broadcaster (PSB) customers (who depend on the Group to meet the obligations under their licences to extend coverage to 98.5% of the UK population) as well as commercial broadcasters. The Group upgraded the UK’s DTT network through the £600m digital switchover (DSO), which it completed within budget and on schedule in October 2012;

market leader for commercial spectrum used for transmission of digital terrestrial television (DTT), owning two of the three commercial SD Multiplexes (out of a total of six existing DTT Multiplexes covering both SD and HD) plus two new High Definition (HD) capable DTT (DVB-T2) Multiplexes (recently awarded for additional HD/SD services on Freeview in the DVB-T2 format – i.e. Freeview HD compatible sets). DTT video streams in the UK are more valuable to broadcasters than either satellite and cable video streams, due to DTT’s more extensive viewer coverage and more limited supply of commercial channels as compared to approximately 250 channels on cable and 500 on satellite;

ownership for over 90% of the radio transmission towers for terrestrial broadcasting in the UK and operator of the sole, existing national commercial digital radio Multiplex and, as at 30 September 2014, 26 of the 59 local radio Multiplexes;

largest independent (non-MNO) portfolio of wireless tower sites in the UK, which are licensed to national Mobile Network Operators (MNOs) and other wireless network operators. The Group has approximately 25% of the total active licensed wireless tower site market and, the Group believes, approximately four times the active licensed wireless tower sites of the next largest independent operator as at 30 September 2014. It holds a strong and difficult-to-replicate position in rural and suburban areas where cost, economies of scale, planning permission restrictions and regulations that limit a landlord's ability to terminate the leases for the Group's sites provide barriers to entry for competitors;

sole provider for smart metering communication services in Northern England and Scotland to provide a network to connect smart meters to DCC Systems (Data and Communications Company, a body licensed by statute) for approximately 9.3 million homes. Building on the recent success securing the smart metering communication services contract, Arqiva has also established a Smart Metering M2M (machine to machine) business division to address opportunities in the smart metering and grid, and machine-to-machine market. In April 2014 Arqiva announced the signature of a partnership deal with SIGFOX, a leading international Internet of Things business, and has begun the construction of the UK’s first national low-power, low-bandwidth Internet of Things (IoT) network using SIGFOX technology;

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 6

largest owner of independent satellite uplink infrastructure and satellite distribution services in the UK in terms of the number of channels uplinked for UK Direct-to-Home (DTH) satellite broadcast that serves as an alternative for customers who do not wish to use BSkyB's uplinking services or who choose to use Arqiva as an uplink provider to their own UK DTH satellite capacity. The Group has over 40% market share in terms of the number of transponders accessed from their uplink infrastructure as at 30 September 2014;

one of the largest providers of WiFi in the UK with circa 26,000 deployed access points, and provision of WiFi services in 35 airports and 10 London boroughs; and

a significant proportion of revenue from long-term contracts with automatic RPI-linked increases.

FINANCIAL RESULTS AND RECENT DEVELOPMENTS

The following discussion of the Group’s financial condition and results of operations should be read in conjunction with the Group’s audited consolidated financial statements for the year ended 30 June 2014 and the Group’s unaudited condensed consolidated financial statements for the three months ended 30 September 2014 and the related notes to those consolidated financial statements.

Some of the statements contained below, including those concerning future revenues, costs, capital expenditures, acquisitions and financial condition, may contain forward-looking statements. As such statements involve inherent uncertainties, actual results may differ materially from the results expressed in or implied by such forward-looking statements. A discussion of such uncertainties is provided under “Forward Looking Statements.”

Where the financial results for both Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited are identical, the financial tables and commentaries have been presented in this report only once and should be viewed as referring to both groups. Where the financial results are different, the financial tables include a break to separate the results and separate commentaries have been provided under the appropriate sub-headings.

Results of operations for the prior year or the recent period are not necessarily indicative of the result to be expected for any future period. Some of the performance indicators and ratios reported herein, such as EBITDA, are not financial measures defined in accordance with IFRS, or UK GAAP and, as such, may be calculated by other companies using different methodologies and having different results. Therefore, these performance indicators and ratios are not directly comparable to similar figures and ratios reported by other companies.

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 7

EXECUTIVE SUMMARY

The Financial Overview and Recent Developments discussed in this section relate to both Arqiva Broadcast Parent Limited (‘ABPL’) and Arqiva Group Parent Limited (‘AGPL’), together the ‘Group’. The trading results of the two consolidation groups are identical but with different financing structures. Commentary relates to both ABPL (including senior and junior debt) and AGPL (senior debt only) unless specified otherwise. Items discussed in the Financial Results section from page 11 onwards which relate to both ABPL and AGPL have been shaded for ease of reference. Financial Overview

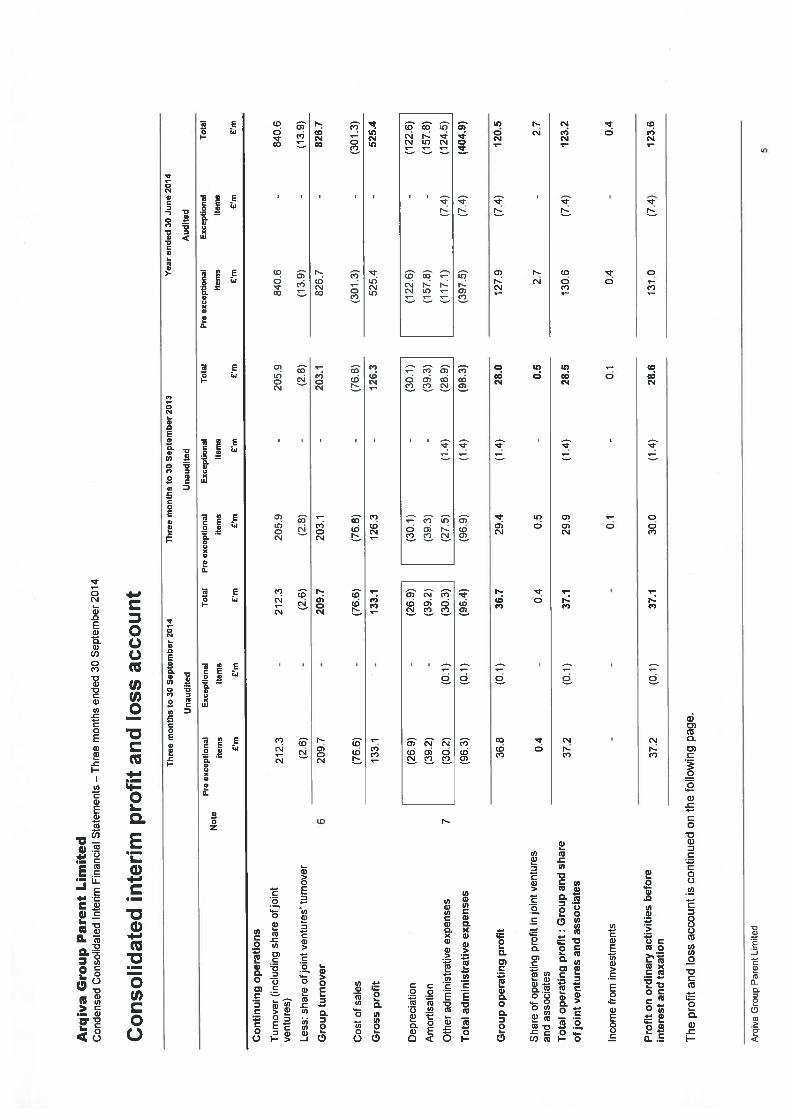

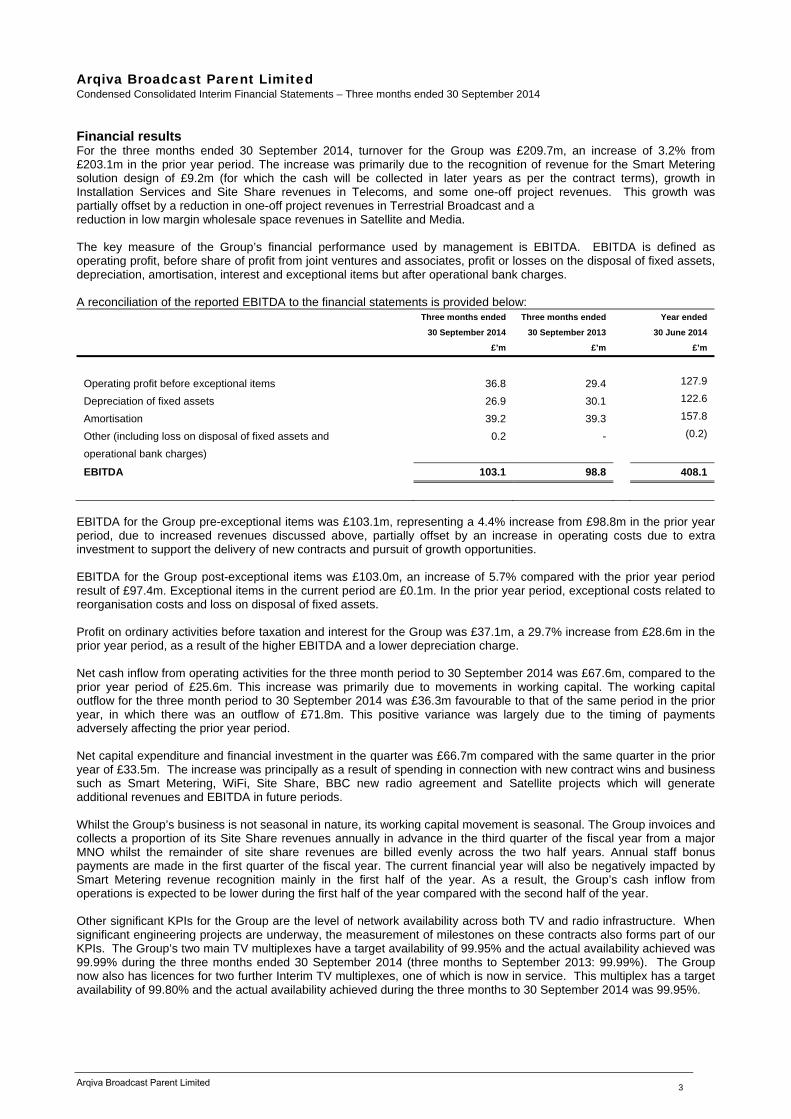

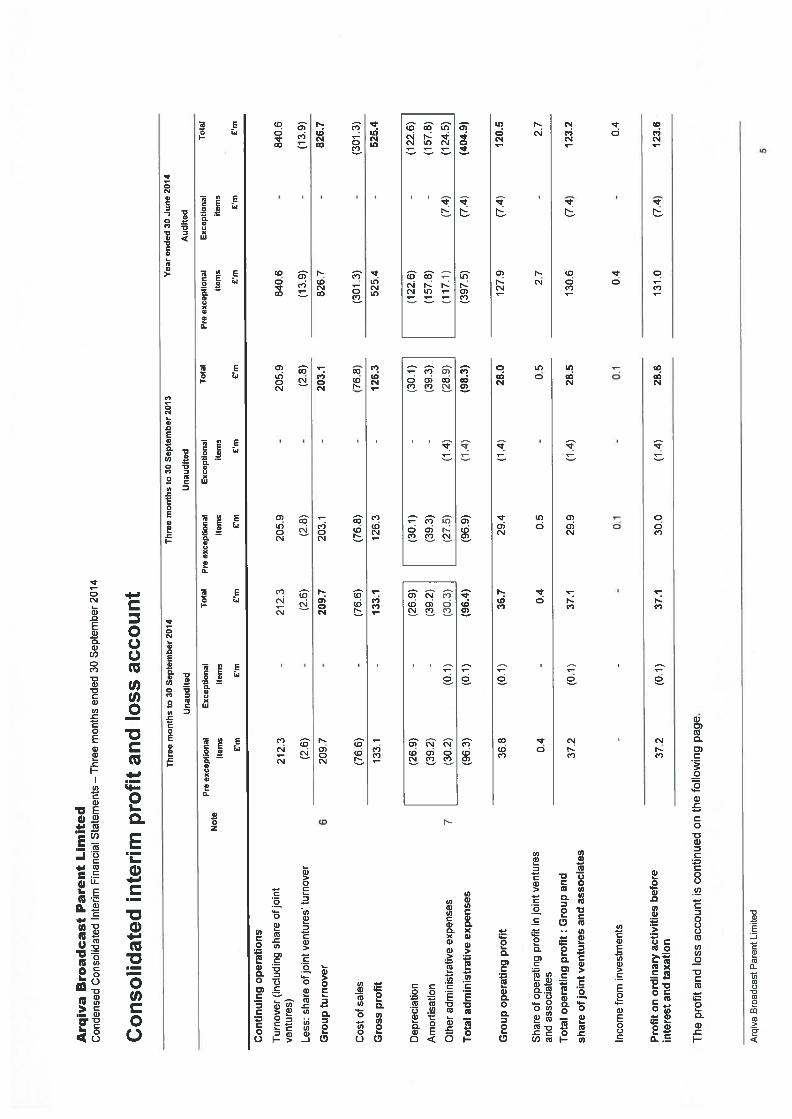

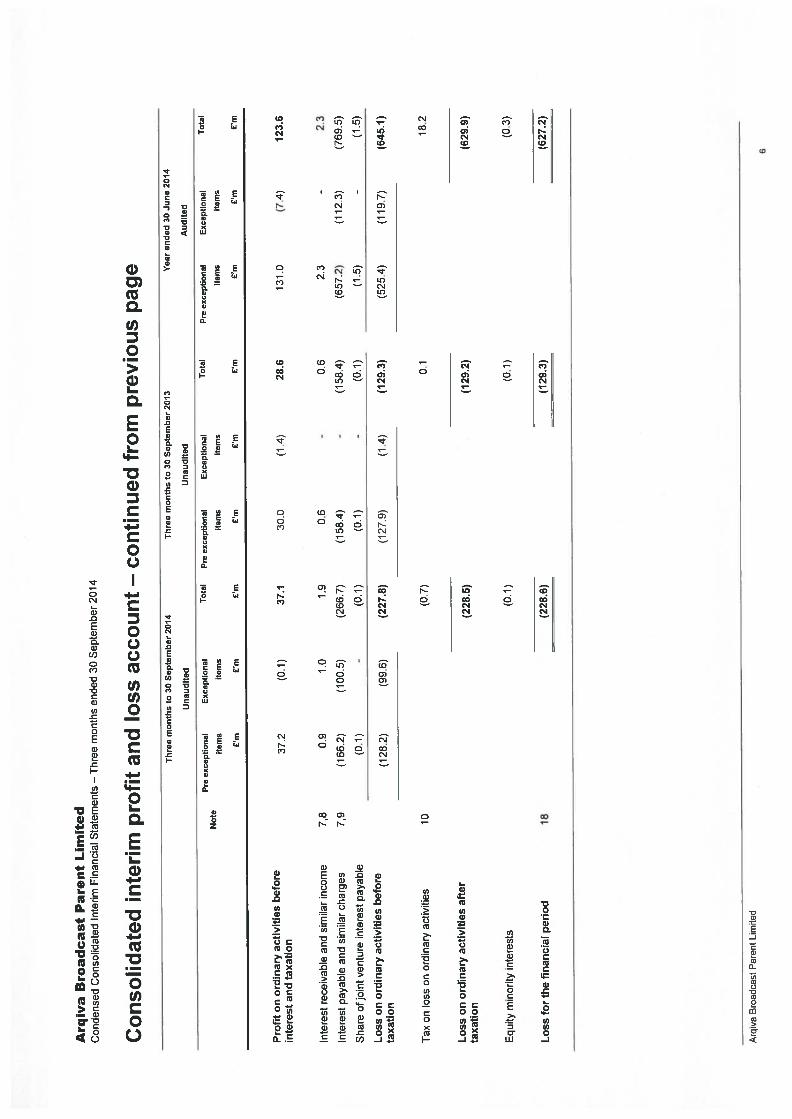

For the three months ended 30 September 2014, turnover for the Group was £209.7m, an increase of 3.2% from £203.1m in the prior year period. The increase was primarily due to the recognition of revenue for the Smart Metering solution design of £9.2m (for which the cash will be collected in later years as per the contract terms), growth in Installation Services and Site Share revenues in Telecoms, and some one-off project revenues. This growth was partially offset by a reduction in one-off project revenues in Terrestrial Broadcast and a reduction in low margin wholesale space revenues in Satellite and Media. EBITDA for the Group pre-exceptional items was £103.1m, representing a 4.4% increase from £98.8m in the prior year period, due to increased revenues discussed above, partially offset by an increase in operating costs due to extra investment to support the delivery of new contracts and pursuit of growth opportunities. EBITDA for the Group post-exceptional items was £103.0m, an increase of 5.7% compared with the prior year period result of £97.4m. Exceptional items in the current period are £0.1m. In the prior year, exceptional costs of £1.4m related to reorganisation costs and loss on disposal of fixed assets. Profit on ordinary activities before taxation and interest for the Group was £37.1m, a 29.7% increase from £28.6m in the prior year period, as a result of the higher EBITDA and a lower depreciation charge. Net cash inflow from operating activities for the three month period to 30 September 2014 was £67.6m, compared to the prior year period of £25.6m. This increase was primarily due to movements in working capital. The working capital outflow for the three month period to 30 September 2014 was £36.3m favourable to that of the same period in the prior year, in which there was an outflow of £71.8m. This positive variance was largely due to the timing of payments adversely affecting the prior year period. Net capital expenditure and financial investment in the quarter was £66.7m compared with the same quarter in the prior year of £33.5m. The increase was principally as a result of spending in connection with new contract wins and business such as Smart Metering, WiFi, Site Share, BBC new radio agreement and Satellite projects which will generate additional revenues and EBITDA in future periods.

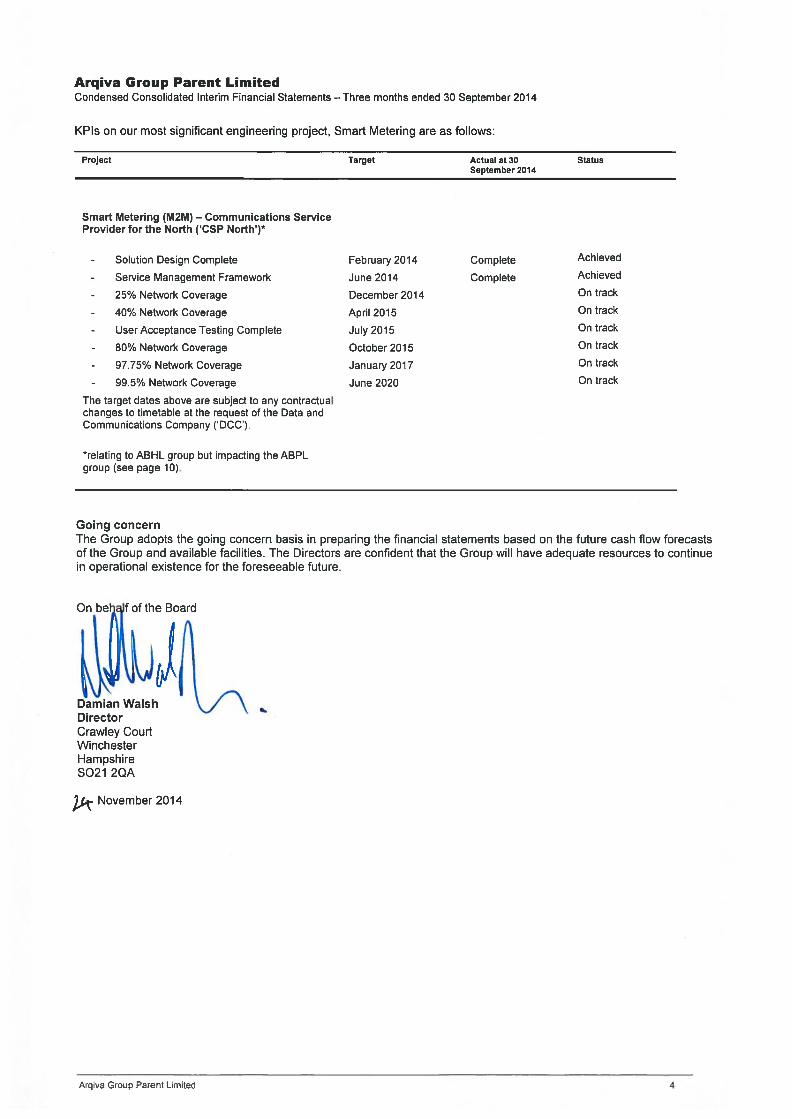

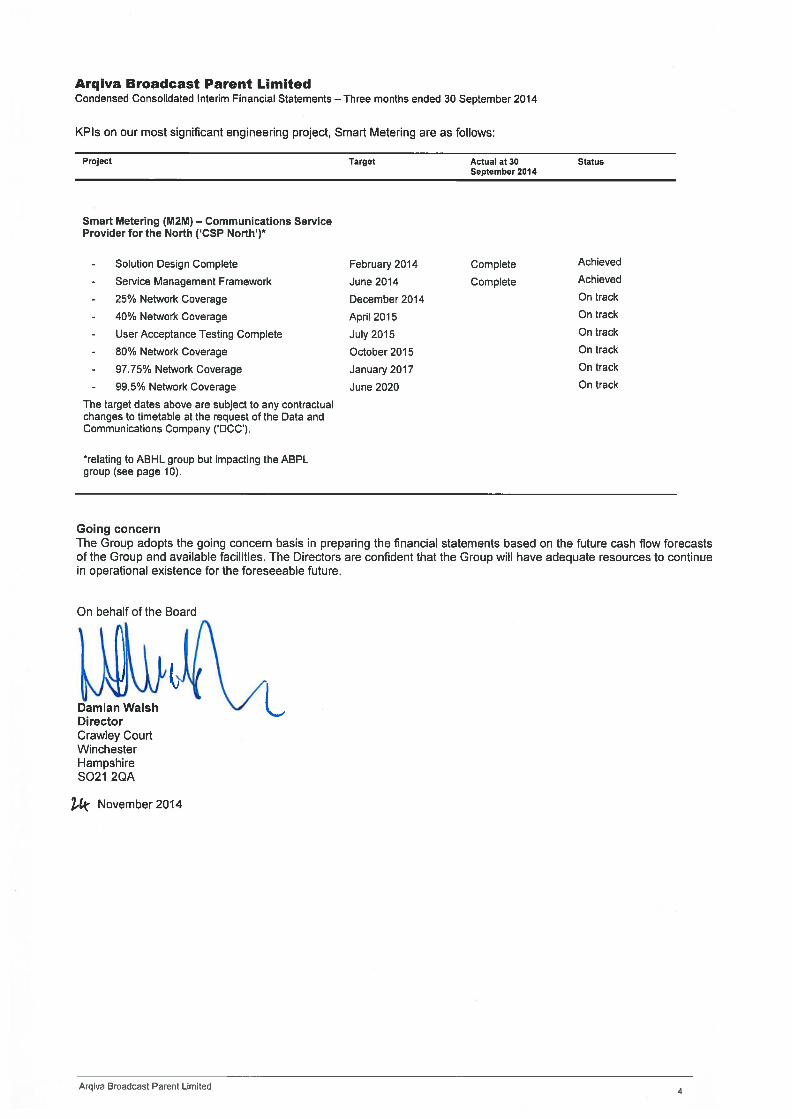

Recent Developments since 30 June 2014 Smart metering rollout progress

In September 2013, Arqiva signed a 15-year contract with the Data and Communications Company (the DCC, a body licensed by statute) to provide communications infrastructure to connect smart meters to DCC Systems for approximately 9.3 million homes and small businesses in Scotland and northern England.

In the twelve months since the award of the contract, Arqiva has consistently met all of its contracted milestones on time. Work is underway to establish the communications network with 139 of the total radio sites already acquired to date and ready for equipment installation. In the three months ended 30 September 2014 the Group recognised £9.2m revenues relating to project management services provided by Arqiva Limited, within the WBS financing group, to Arqiva Smart Metering Limited (ASML) including revenues in relation to progress towards the completion of the design and development milestone, as part of the construction of the network infrastructure.

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 8

Arqiva has also established its two data centres, with equipment installed, powered up and accepted. The implementation achievements to date enable Arqiva to start testing its solution. Our next coverage milestone of 25% population coverage by the end of calendar year 2014 remains on track.

4G rollout

The four main MNOs are all increasing their 4G network capability. Arqiva in turn is being contracted to carry out a large volume of antenna and feeder upgrade projects for our customers. As a result Arqiva will report a significant increase in Installation Services revenue this year and next year compared to the year ended 30 June 2014.

Mobile infrastructure project update

The Mobile Infrastructure Project (MIP) is a strategic programme funded by the Government with the ultimate goal of providing service to areas without any mobile coverage services (‘not-spots’). In May 2013, Arqiva was awarded the contract for the project by the Department of Culture and Media and Sport (DCMS) to provide mobile network planning and deployment services to build infrastructure (cellular and backhaul transmission) which the Mobile Network Operators (MNO) will utilise. The DCMS intends to invest up to £150m to improve mobile coverage. Initial work on the programme has taken longer than anticipated due to the external challenges of bringing coverage to such rural and remote areas. The main challenges were difficulties in getting backhaul into the MNOs’ networks and identifying not spot areas that should be covered under the project. The build part of the programme is now ramping up very fast and the Group expects over 100 sites to be at an advanced stage of build and completion by the end of the current financial year. 700 MHz spectrum usage update

The DTT platform currently uses spectrum in the 470-790MHz bands. In May 2014, Ofcom published a consultation on the future use of the 700 MHz band along for mobile data use with a discussion document on Free To View TV. Arqiva submitted its response to Ofcom’s consultation at the end of August 2014 and also provided a joint response with Digital UK shareholders including the Public Service Broadcasters. The response highlights the requirement to protect the DTT platform and 600 MHz spectrum for TV use. In September 2014 the Group also contracted with Ofcom to undertake a capability assessment to identify the work required to modify the existing DTT network infrastructure to meet the requirements for the 700MHz Clearance. From this assessment, the Group will provide Ofcom with the output reports during the current financial year detailing the technical requirements and costs for the programme. This information will then be used to develop the final plans for the 700 MHz Clearance programme.

BBC new radio agreement (NRA) update

The Group has been progressing with the delivery of the programme under the BBC New Radio Agreement (NRA). We successfully transitioned the analogue and digital radio services to the new service and reporting levels required by the NRA in October 2013. Since then we have been upgrading the analogue network as well as building out the Phase 4 BBC National DAB network. As at 1 October 2014, Arqiva had put 48 new transmitters on air increasing the BBC’s UK DAB network coverage from 93% to 95%. By the time the project is completed in December 2015, the BBC national DAB network will reach 97% of the population via a total of 392 transmitters. Second national DAB multiplex

In July 2014 Ofcom launched a process to offer a second national commercial multiplex. The Group intends to bid for the licence, as part of a joint venture with Bauer and UTV. Separately, as part of the requirement for the new national DAB multiplex, the Group has also provided a Reference Offer for Network Access and Managed Transmission Services, which has been made available to all bidders. The submission date for licence bids has been extended by Ofcom to the end of January 2015 with a decision expected in Spring 2015.

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 9

Financing developments

During July 2014, the Group completed a new 15-year amortising, floating rate US Private Placement debt issue raising £300.0m which has been used to pay down the 5-year term bank facility, leaving only £353.5m outstanding from original bank term loans of £1,586.0m taken out as part of the February 2013 refinancing. At the same time, the Group restructured Interest Rate Swaps (IRS) with a £300m nominal value to match exactly the amount outstanding on the new amortising US Private Placement. As part of the restructure, the IRS in ASF (Arqiva Senior Finance Limited) were terminated which resulted in a Mark-to-Market termination payment of £100.5m. This has been reported as exceptional financing expenses in the ABPL and AGPL accounts. The termination payment was entirely funded by the £100.5m premium received from entering into a replacement IRS in AF1 (Arqiva Financing No. 1 Limited).

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 10

Financial Results for the three months ended 30 September 2014

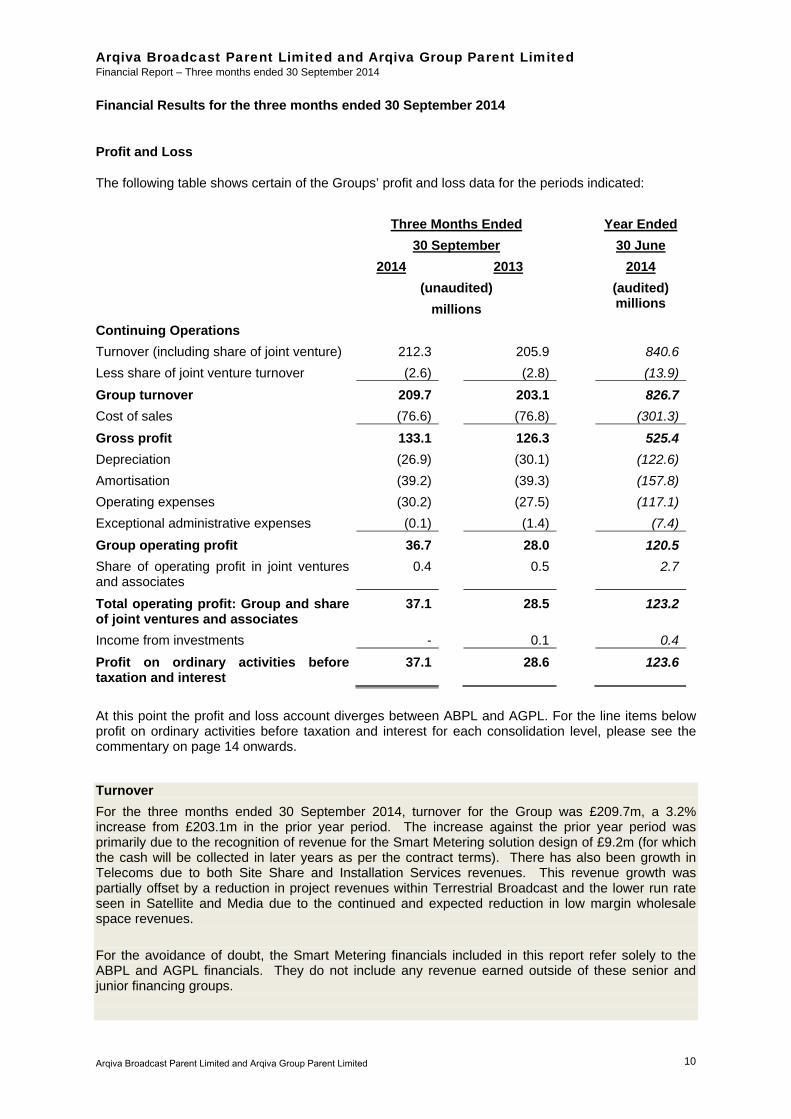

Profit and Loss

The following table shows certain of the Groups’ profit and loss data for the periods indicated:

Three Months Ended

30 September

Year Ended

30 June

2014 2013 2014

(unaudited)

millions

(audited) millions

Continuing Operations

Turnover (including share of joint venture) 212.3 205.9 840.6

Less share of joint venture turnover (2.6) (2.8) (13.9)

Group turnover 209.7 203.1 826.7

Cost of sales (76.6) (76.8) (301.3)

Gross profit 133.1 126.3 525.4

Depreciation (26.9) (30.1) (122.6)

Amortisation (39.2) (39.3) (157.8)

Operating expenses (30.2) (27.5) (117.1)

Exceptional administrative expenses (0.1) (1.4) (7.4)

Group operating profit 36.7 28.0 120.5

Share of operating profit in joint ventures and associates

0.4 0.5 2.7

Total operating profit: Group and share of joint ventures and associates

37.1 28.5 123.2

Income from investments - 0.1 0.4

Profit on ordinary activities before taxation and interest

37.1 28.6 123.6

At this point the profit and loss account diverges between ABPL and AGPL. For the line items below profit on ordinary activities before taxation and interest for each consolidation level, please see the commentary on page 14 onwards.

Turnover

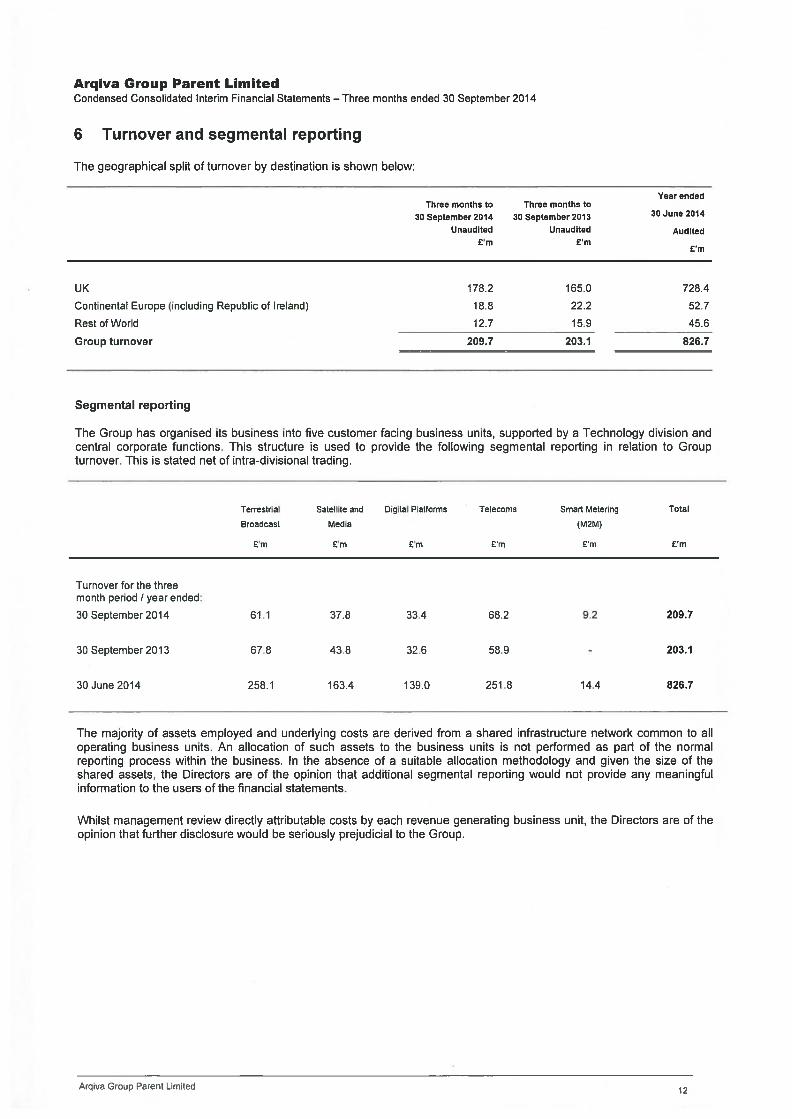

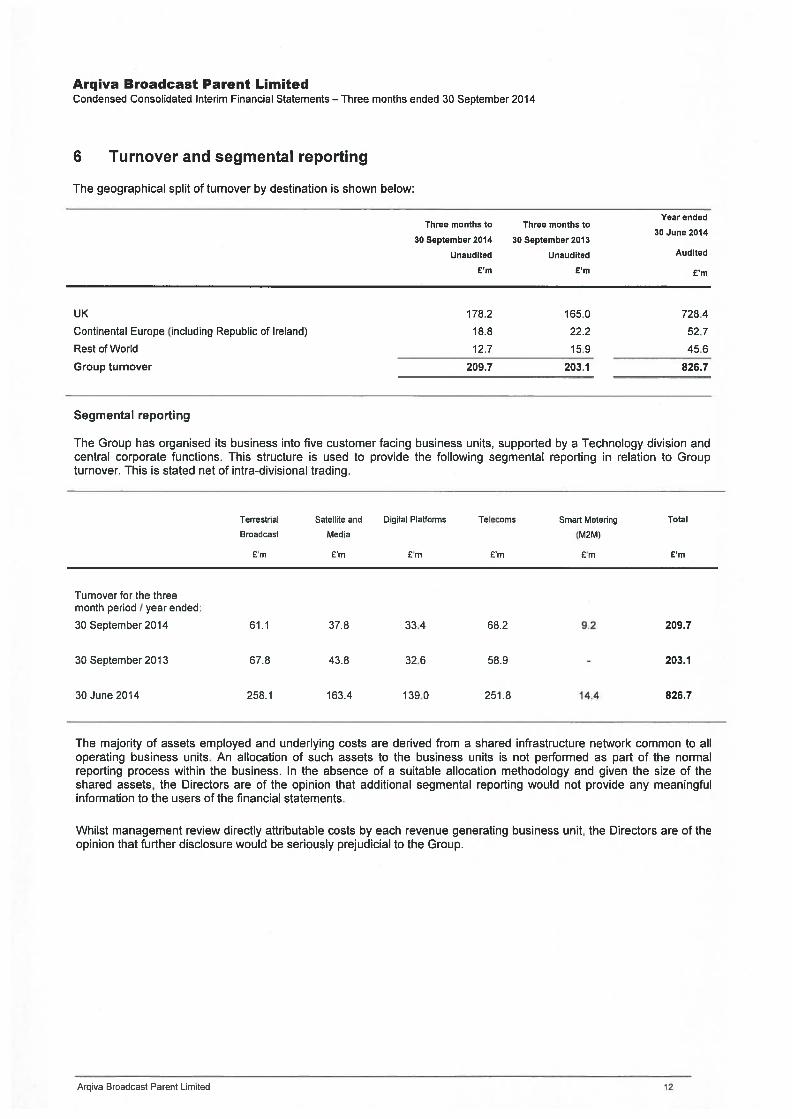

For the three months ended 30 September 2014, turnover for the Group was £209.7m, a 3.2% increase from £203.1m in the prior year period. The increase against the prior year period was primarily due to the recognition of revenue for the Smart Metering solution design of £9.2m (for which the cash will be collected in later years as per the contract terms). There has also been growth in Telecoms due to both Site Share and Installation Services revenues. This revenue growth was partially offset by a reduction in project revenues within Terrestrial Broadcast and the lower run rate seen in Satellite and Media due to the continued and expected reduction in low margin wholesale space revenues.

For the avoidance of doubt, the Smart Metering financials included in this report refer solely to the ABPL and AGPL financials. They do not include any revenue earned outside of these senior and junior financing groups.

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 11

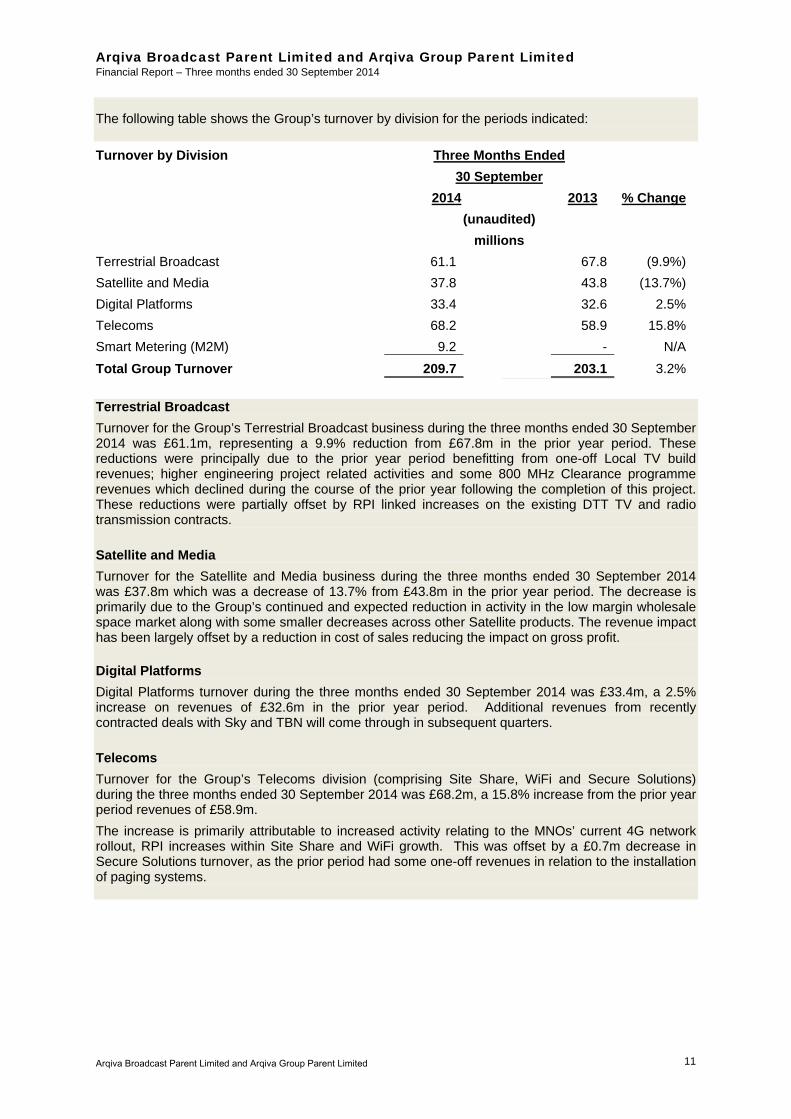

The following table shows the Group’s turnover by division for the periods indicated:

Turnover by Division Three Months Ended

30 September

2014 2013 % Change

(unaudited)

millions

Terrestrial Broadcast 61.1 67.8 (9.9%)

Satellite and Media 37.8 43.8 (13.7%)

Digital Platforms 33.4 32.6 2.5%

Telecoms 68.2 58.9 15.8%

Smart Metering (M2M) 9.2 - N/A

Total Group Turnover 209.7 203.1 3.2%

Terrestrial Broadcast

Turnover for the Group’s Terrestrial Broadcast business during the three months ended 30 September 2014 was £61.1m, representing a 9.9% reduction from £67.8m in the prior year period. These reductions were principally due to the prior year period benefitting from one-off Local TV build revenues; higher engineering project related activities and some 800 MHz Clearance programme revenues which declined during the course of the prior year following the completion of this project. These reductions were partially offset by RPI linked increases on the existing DTT TV and radio transmission contracts.

Satellite and Media

Turnover for the Satellite and Media business during the three months ended 30 September 2014 was £37.8m which was a decrease of 13.7% from £43.8m in the prior year period. The decrease is primarily due to the Group’s continued and expected reduction in activity in the low margin wholesale space market along with some smaller decreases across other Satellite products. The revenue impact has been largely offset by a reduction in cost of sales reducing the impact on gross profit.

Digital Platforms

Digital Platforms turnover during the three months ended 30 September 2014 was £33.4m, a 2.5% increase on revenues of £32.6m in the prior year period. Additional revenues from recently contracted deals with Sky and TBN will come through in subsequent quarters.

Telecoms

Turnover for the Group’s Telecoms division (comprising Site Share, WiFi and Secure Solutions) during the three months ended 30 September 2014 was £68.2m, a 15.8% increase from the prior year period revenues of £58.9m.

The increase is primarily attributable to increased activity relating to the MNOs’ current 4G network rollout, RPI increases within Site Share and WiFi growth. This was offset by a £0.7m decrease in Secure Solutions turnover, as the prior period had some one-off revenues in relation to the installation of paging systems.

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 12

Smart Metering (M2M)

Revenues for the three months ended 30 September 2014 of £9.2m (2013: £nil) represent project management services provided by Arqiva Limited, within the WBS financing group, to ASML including revenues in relation to progress towards completion of the design and development milestone, as part of the construction of the network infrastructure.

Cost of Sales

For the three months ended 30 September 2014, cost of sales for the Group was £76.6m, in line with £76.8m in the prior year period. In the current period, cost of sales has not increased at the same rate as turnover primarily due to the recognition of the Smart Metering project management services which have a minimal cost of sale. Increases seen in Telecoms costs of sales reflect the higher revenue generation, and have been partially offset by savings seen in satellite capacity costs following reduced revenues within Satellite and Media.

Gross profit

For the three months ended 30 September 2014, gross profit for the Group was £133.1m, representing a 5.4% increase from £126.3m in the prior year period. This is primarily attributable to the recognition of the Smart Metering project management revenue, partially offset by the reduction in gross profit within Terrestrial Broadcast.

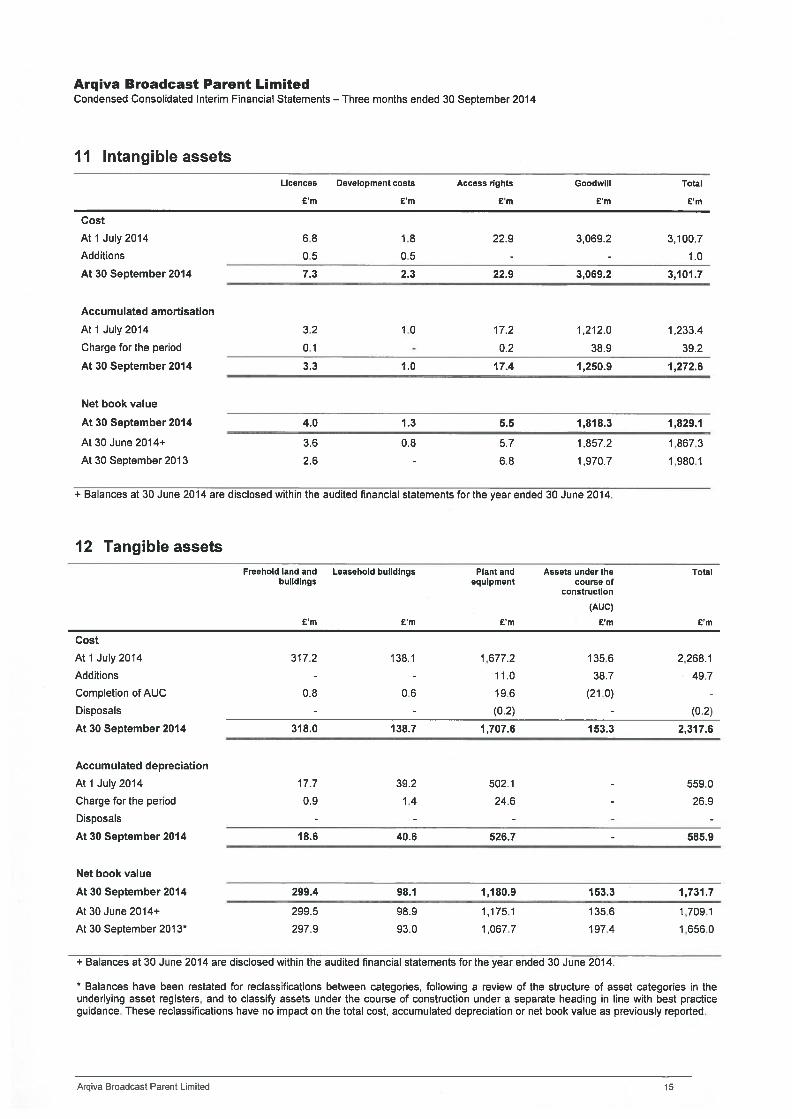

Depreciation

Depreciation for the Group during the three months ended 30 September 2014 was £26.9m, representing a 10.6% decrease from £30.1m in the prior year period. The decrease is due to a number of one-off charges in the prior period in relation to DSO and other major projects.

Amortisation

Amortisation for the Group during the three months ended 30 September 2014 was £39.2m, in line with the prior year period figure of £39.3m.

Operating expenses

Operating expenses for the Group during the three months ended 30 September 2014 excluding exceptional items were £30.2m, 9.8% higher than the prior year period costs of £27.5m due to extra investment in headcount required to resource growth initiatives and one-off items in the prior year.

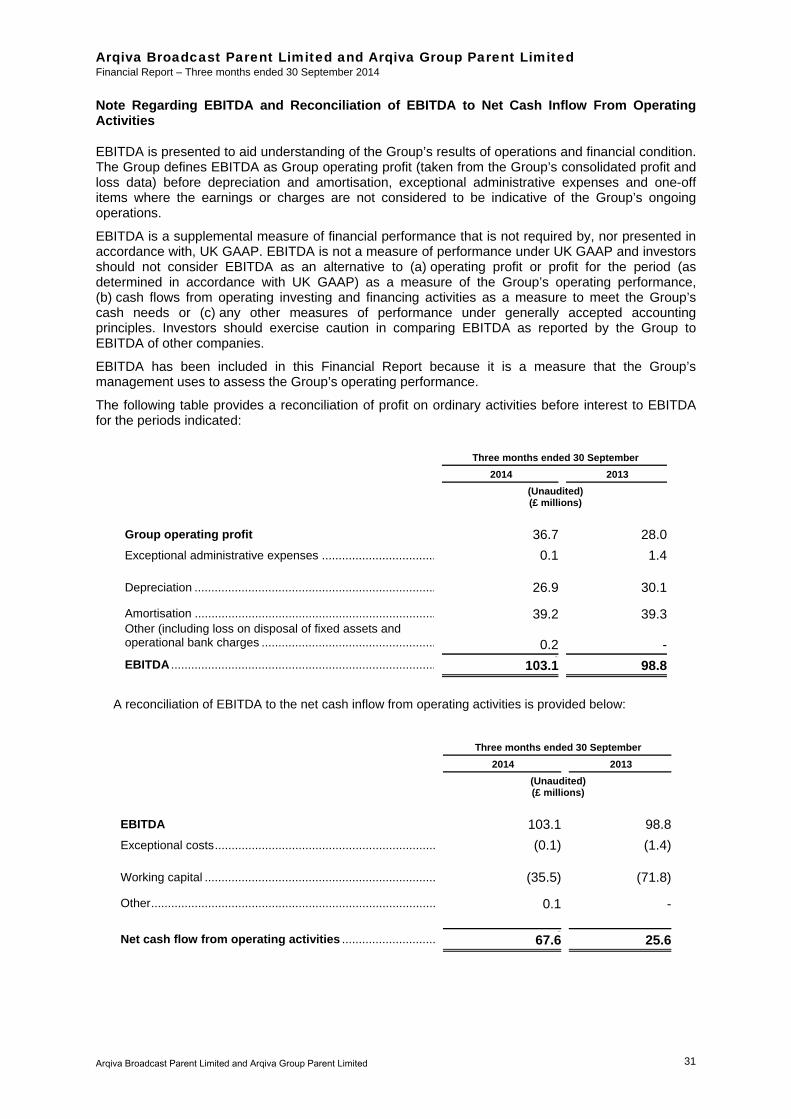

EBITDA

For the three months ended 30 September 2014, EBITDA pre-exceptional costs for the Group was £103.1m, representing a 4.4% increase from £98.8m in the prior year period, explained by the increase in gross profit partially offset by increased operating costs as the Group gears up to deliver new contracts and business opportunities.

EBITDA for the Group post-exceptional items was £103.0m for the three months ended 30 September 2014, an increase of 5.7% compared with the prior year period result of £97.4m. Exceptional items of £1.4m in the prior year primarily related to reorganisation costs and loss on disposal of fixed assets which have not recurred in the current year.

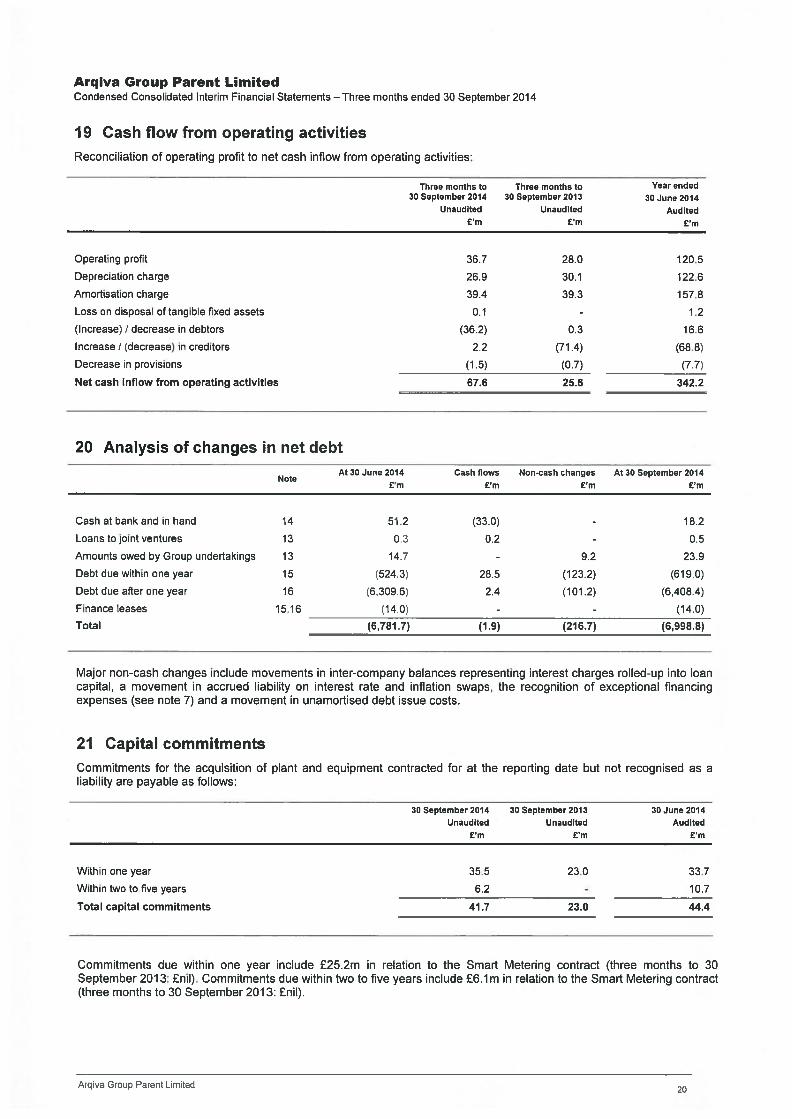

For reconciliation of Group operating profit to EBITDA, see “Note Regarding EBITDA and Reconciliation from EBITDA to Net Operating Cash Inflow From Operating Activities” in the Appendix.

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 13

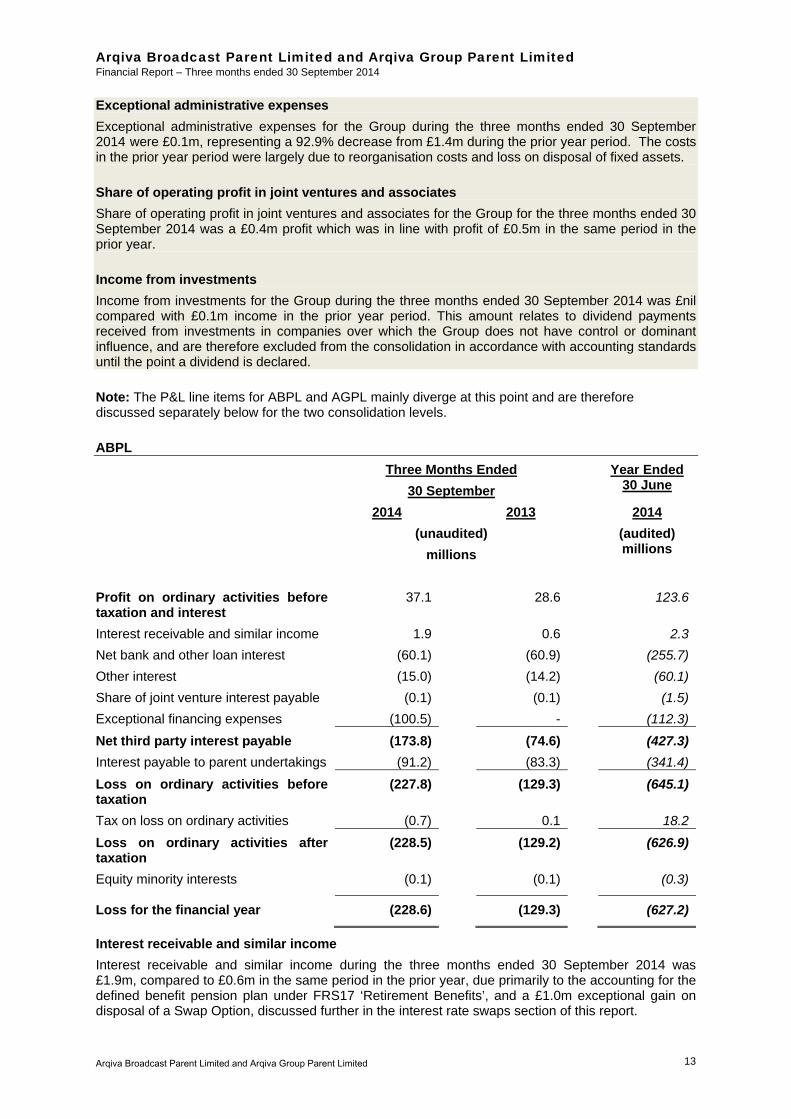

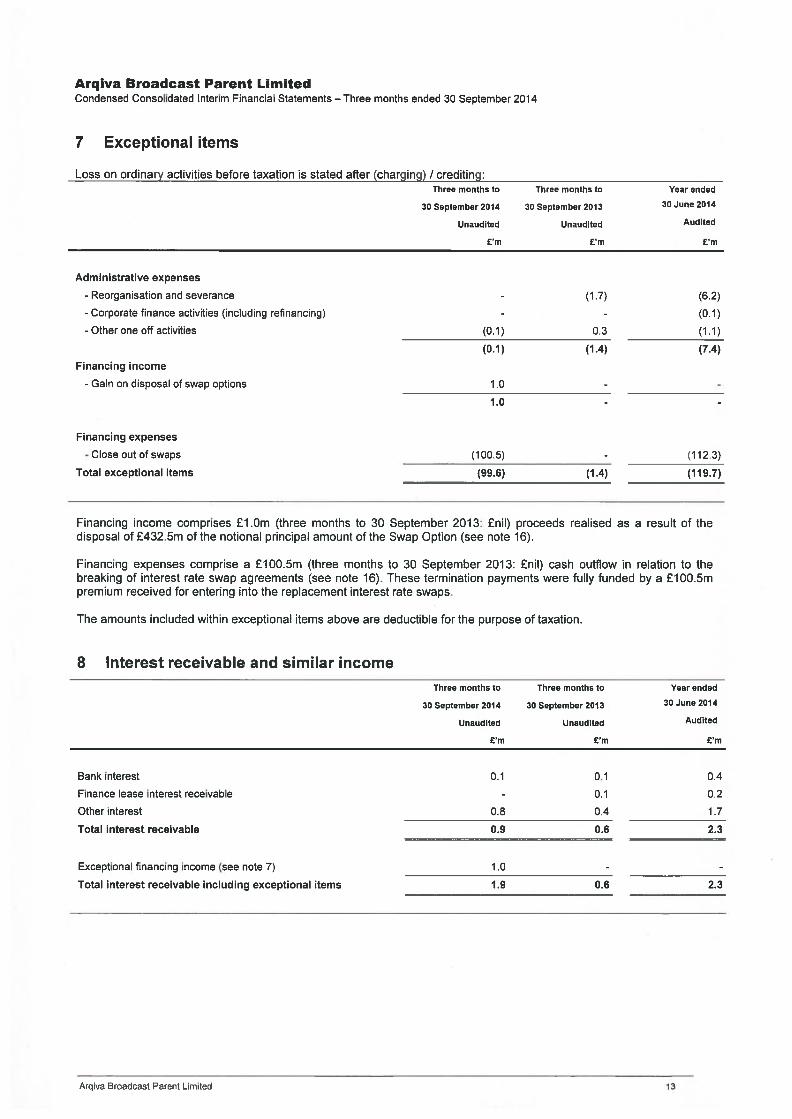

Exceptional administrative expenses

Exceptional administrative expenses for the Group during the three months ended 30 September 2014 were £0.1m, representing a 92.9% decrease from £1.4m during the prior year period. The costs in the prior year period were largely due to reorganisation costs and loss on disposal of fixed assets.

Share of operating profit in joint ventures and associates

Share of operating profit in joint ventures and associates for the Group for the three months ended 30 September 2014 was a £0.4m profit which was in line with profit of £0.5m in the same period in the prior year.

Income from investments

Income from investments for the Group during the three months ended 30 September 2014 was £nil compared with £0.1m income in the prior year period. This amount relates to dividend payments received from investments in companies over which the Group does not have control or dominant influence, and are therefore excluded from the consolidation in accordance with accounting standards until the point a dividend is declared.

Note: The P&L line items for ABPL and AGPL mainly diverge at this point and are therefore discussed separately below for the two consolidation levels.

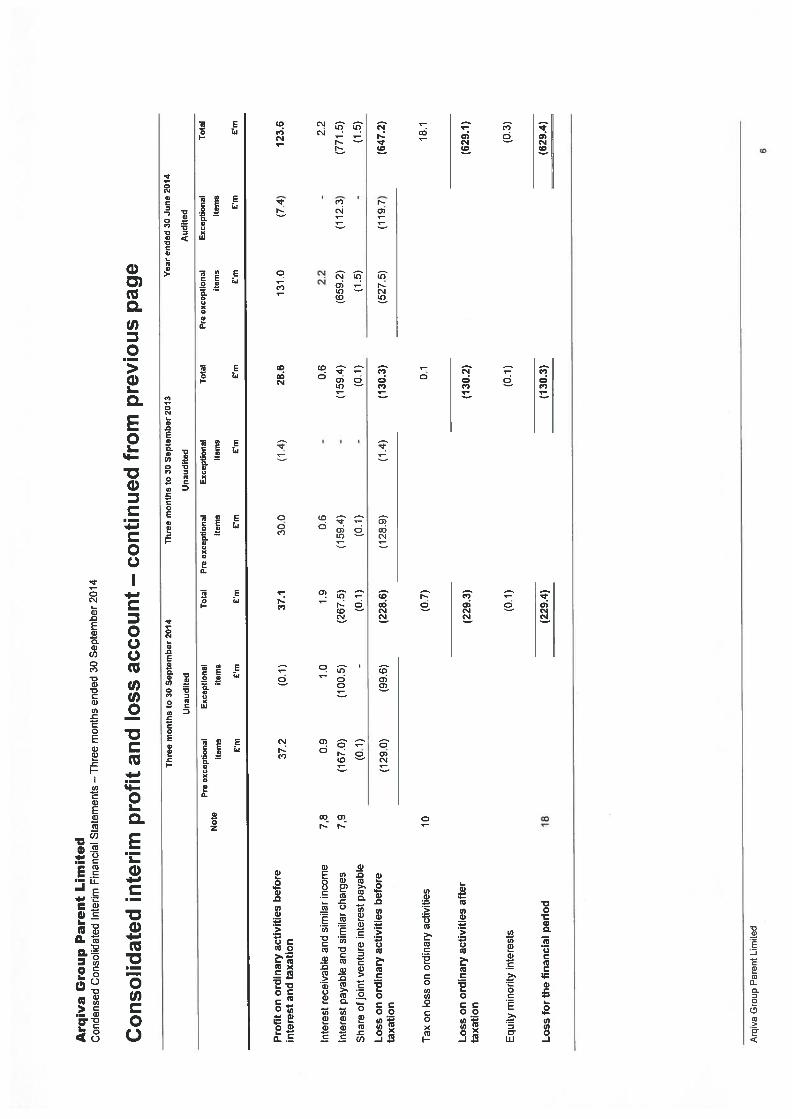

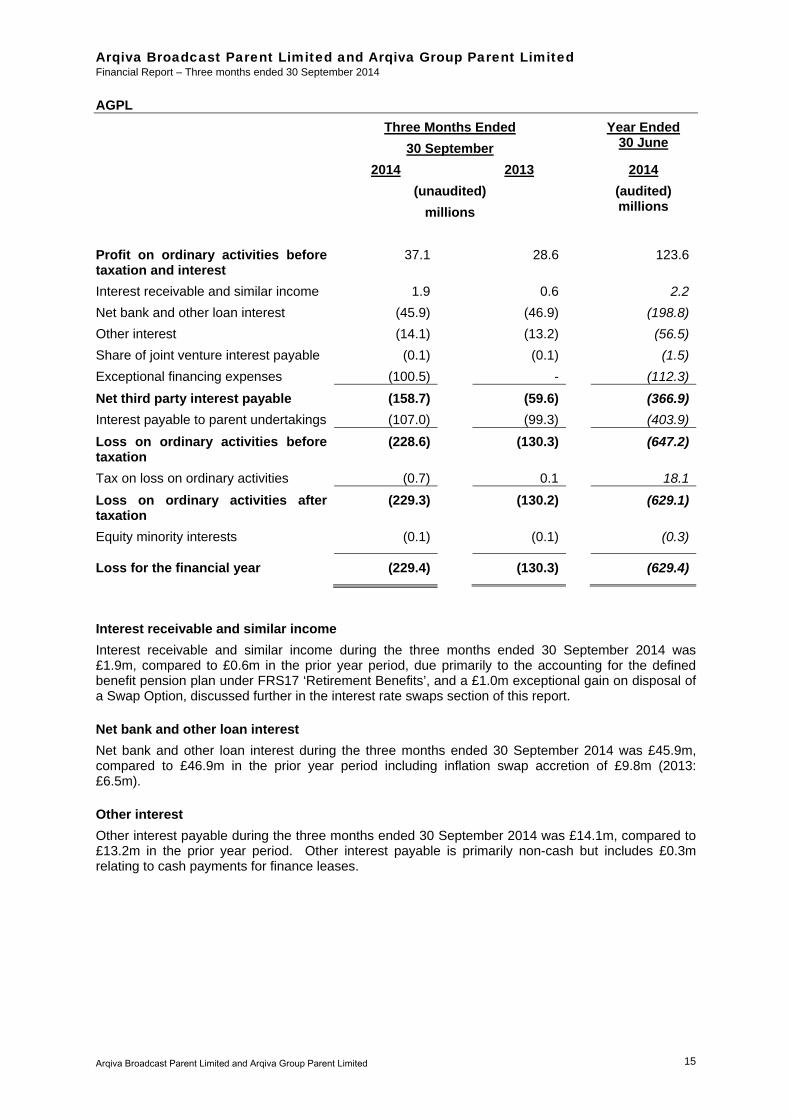

ABPL

Three Months Ended

30 September

Year Ended 30 June

2014 2013 2014

(unaudited)

millions

(audited) millions

Profit on ordinary activities before taxation and interest

37.1 28.6 123.6

Interest receivable and similar income 1.9 0.6 2.3

Net bank and other loan interest (60.1) (60.9) (255.7)

Other interest (15.0) (14.2) (60.1)

Share of joint venture interest payable (0.1) (0.1) (1.5)

Exceptional financing expenses (100.5) - (112.3)

Net third party interest payable (173.8) (74.6) (427.3)

Interest payable to parent undertakings (91.2) (83.3) (341.4)

Loss on ordinary activities before taxation

(227.8) (129.3) (645.1)

Tax on loss on ordinary activities (0.7) 0.1 18.2

Loss on ordinary activities after taxation

(228.5) (129.2) (626.9)

Equity minority interests (0.1) (0.1) (0.3)

Loss for the financial year (228.6) (129.3) (627.2)

Interest receivable and similar income

Interest receivable and similar income during the three months ended 30 September 2014 was £1.9m, compared to £0.6m in the same period in the prior year, due primarily to the accounting for the defined benefit pension plan under FRS17 ‘Retirement Benefits’, and a £1.0m exceptional gain on disposal of a Swap Option, discussed further in the interest rate swaps section of this report.

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 14

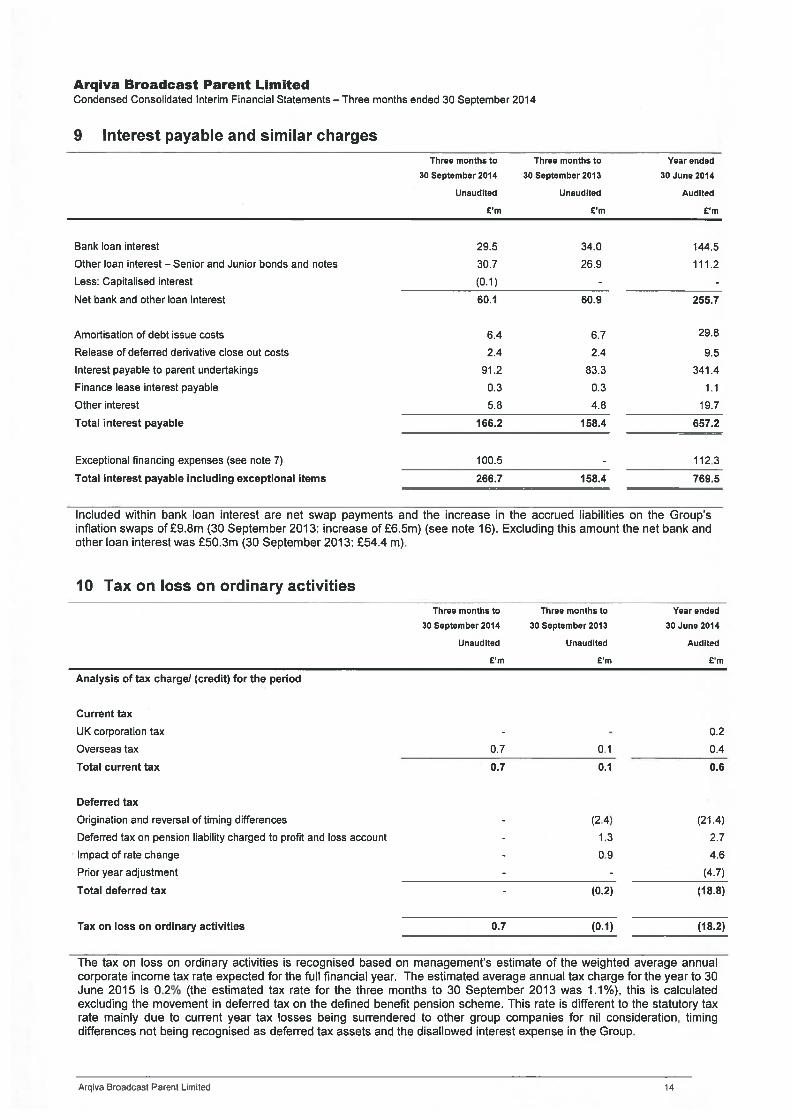

Net bank and other loan interest

Net bank and other loan interest for the Group during the three months ended 30 September 2014 was £60.1m compared to £60.9m in the prior year period including inflation swap accretion of £9.8m (2013: £6.5m).

Other interest

Other interest payable for the Group during the three months ended 30 September 2014 was £15.0m, compared to £14.2m in the prior year period. Other interest payable is primarily non-cash but includes £0.3m relating to cash payments for finance leases.

Share of joint venture interest payable

Share of joint venture interest payable for the Group during the three months ended 30 September 2014 was £0.1m (2013: £0.1m).

Exceptional financing costs

During July 2014, the Group restructured certain derivative financial instruments, when £300.0m of the 5 year term debt was refinanced by a US Private Placement floating rate debt issue. This exceptional cost of £100.5m was incurred in relation to the breaking of IRS agreements. The termination payments were fully funded by a £100.5m premium received for entering into the replacement IRS.

Interest payable to parent undertakings

Interest payable to parent undertakings for the Group during the three months ended 30 September 2014 was £91.2m, compared to £83.3m in the prior year period. This increase was due to the increase in the principal amount of subordinated intercompany loans.

Tax on loss on ordinary activities

Tax on loss on ordinary activities during the three months ended 30 September 2014 was a £0.7m charge, compared to a £0.1m credit in the prior year period, primarily due to an increased overseas tax charge.

Equity minority interests

For the three months ended 30 September 2014, the equity minority interest not attributable to the Group was £0.1m in line with £0.1m in the prior year period. This relates to the share of Now Digital (East Midlands) Limited and South West Digital Radio Limited that is not owned by the Group.

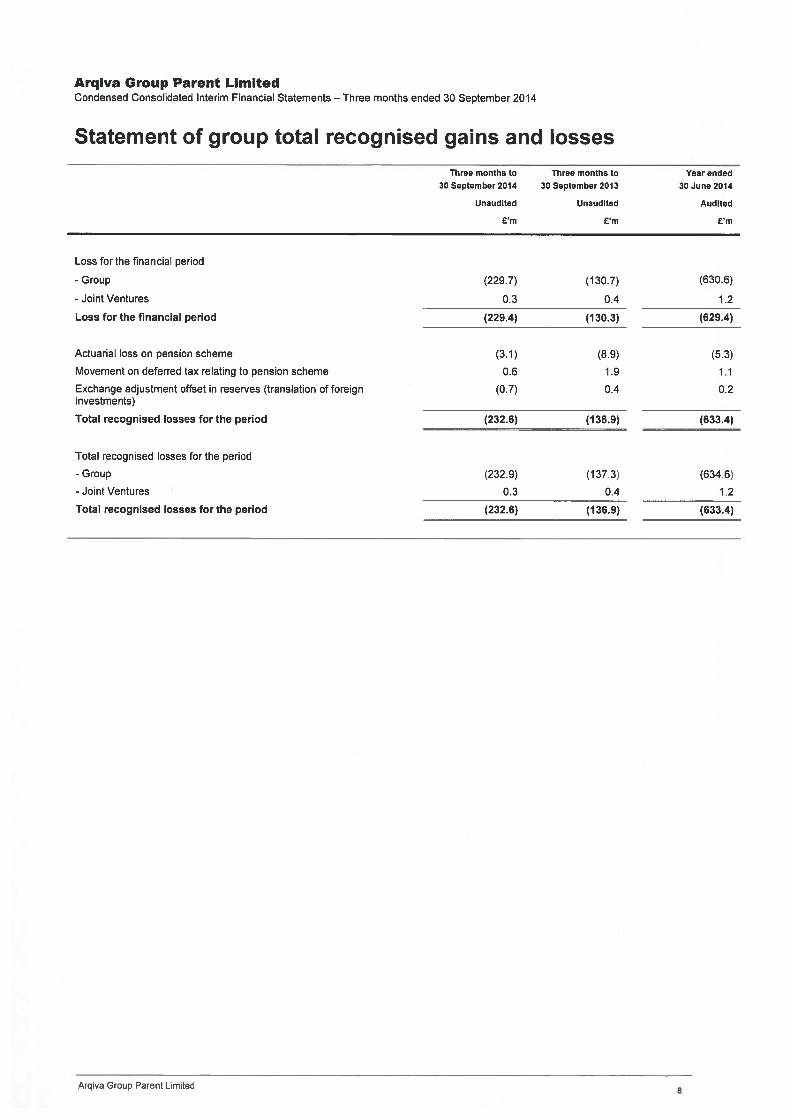

Loss for the financial period

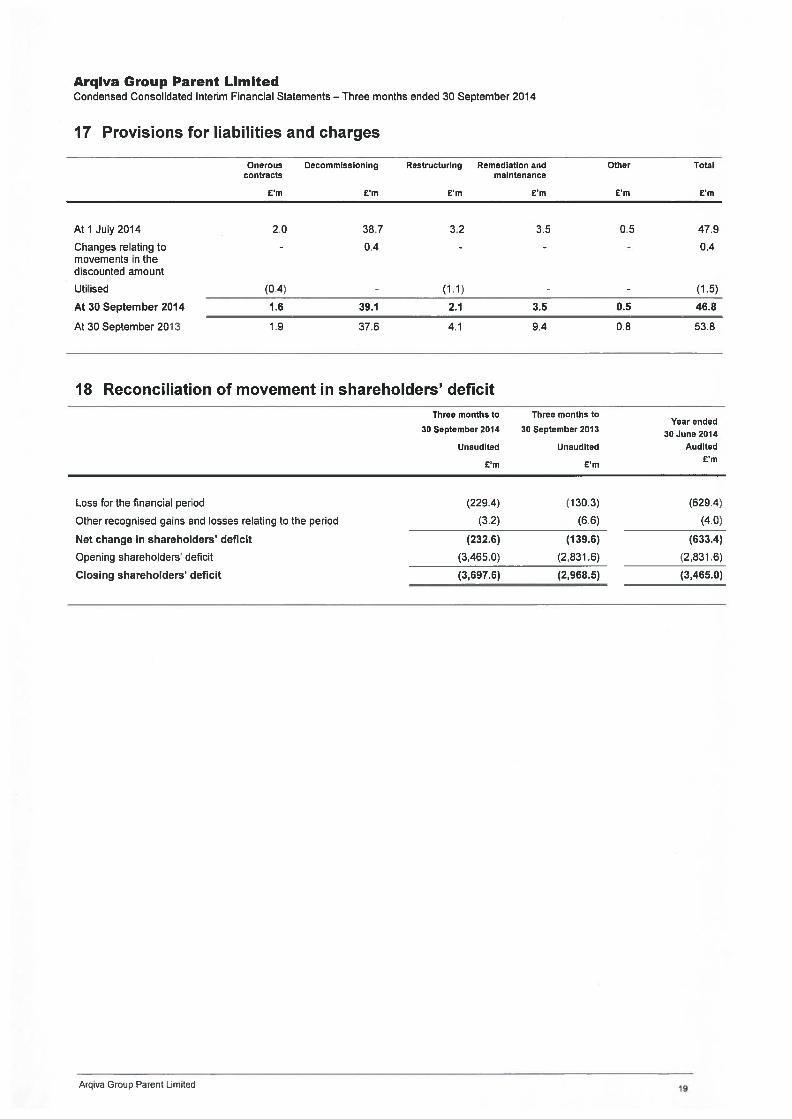

Loss for the three months ended 30 September 2014 was £228.6m, compared to a £129.3m loss in the prior year period. This movement was primarily due to the £100.5m exceptional financing expense incurred in relation to the breaking of interest rate swaps which was fully funded by a £100.5m premium receipt for entering into the replacement interest rate swaps.

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 15

AGPL

Three Months Ended

30 September

Year Ended 30 June

2014 2013 2014

(unaudited)

millions

(audited) millions

Profit on ordinary activities before taxation and interest

37.1 28.6 123.6

Interest receivable and similar income 1.9 0.6 2.2

Net bank and other loan interest (45.9) (46.9) (198.8)

Other interest (14.1) (13.2) (56.5)

Share of joint venture interest payable (0.1) (0.1) (1.5)

Exceptional financing expenses (100.5) - (112.3)

Net third party interest payable (158.7) (59.6) (366.9)

Interest payable to parent undertakings (107.0) (99.3) (403.9)

Loss on ordinary activities before taxation

(228.6) (130.3) (647.2)

Tax on loss on ordinary activities (0.7) 0.1 18.1

Loss on ordinary activities after taxation

(229.3) (130.2) (629.1)

Equity minority interests (0.1) (0.1) (0.3)

Loss for the financial year (229.4) (130.3) (629.4)

Interest receivable and similar income

Interest receivable and similar income during the three months ended 30 September 2014 was £1.9m, compared to £0.6m in the prior year period, due primarily to the accounting for the defined benefit pension plan under FRS17 ‘Retirement Benefits’, and a £1.0m exceptional gain on disposal of a Swap Option, discussed further in the interest rate swaps section of this report.

Net bank and other loan interest

Net bank and other loan interest during the three months ended 30 September 2014 was £45.9m, compared to £46.9m in the prior year period including inflation swap accretion of £9.8m (2013: £6.5m).

Other interest

Other interest payable during the three months ended 30 September 2014 was £14.1m, compared to £13.2m in the prior year period. Other interest payable is primarily non-cash but includes £0.3m relating to cash payments for finance leases.

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 16

Share of joint venture interest payable

Share of joint venture interest payable for the Group during the three months ended 30 September 2014 was £0.1m, comparable to the £0.1m payable in the prior year period.

Exceptional financing costs

During July 2014, the Group restructured certain derivative financial instruments, when £300.0m of the 5 year term debt was refinanced by a US Private Placement floating rate debt issue. This exceptional cost comprises £100.5m incurred in relation to the breaking of IRS agreements. The termination payments were fully funded by a £100.5m premium received for entering into the replacement IRS.

Interest payable to parent undertakings

Interest payable to parent undertakings for the Group during the three months ended 30 September 2014 was £107.0m, compared to £99.3m in the prior year period. This increase is due primarily to an increase in the principal amount of intercompany loans owed by the Group. £78.5m of the £107.0m charge was non-cash. £28.5m was settled in cash in the period and used to pay interest on the £600.0m junior bonds.

Tax on loss on ordinary activities

Tax on loss on ordinary activities during the three months ended 30 September 2014 was a £0.7m charge, compared to a £0.1m credit in the prior year period, primarily due to an increased overseas tax charge.

Equity minority interests

For the three months ended 30 September 2014, the equity minority interest not attributable to the Group was £0.1m, compared to £0.1m in the prior year period. This relates to the share of Now Digital (East Midlands) Limited and South West Digital Radio Limited that is not owned by the Group.

Loss for the financial period

Loss for the three months ended 30 September 2014 was £229.4m, compared to a £130.3m loss in the prior year period. This movement was primarily due to the £100.5m exceptional financing expense incurred in relation to the breaking of interest rate swaps which was fully funded by a £100.5m premium receipt for entering into the replacement interest rate swaps.

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 17

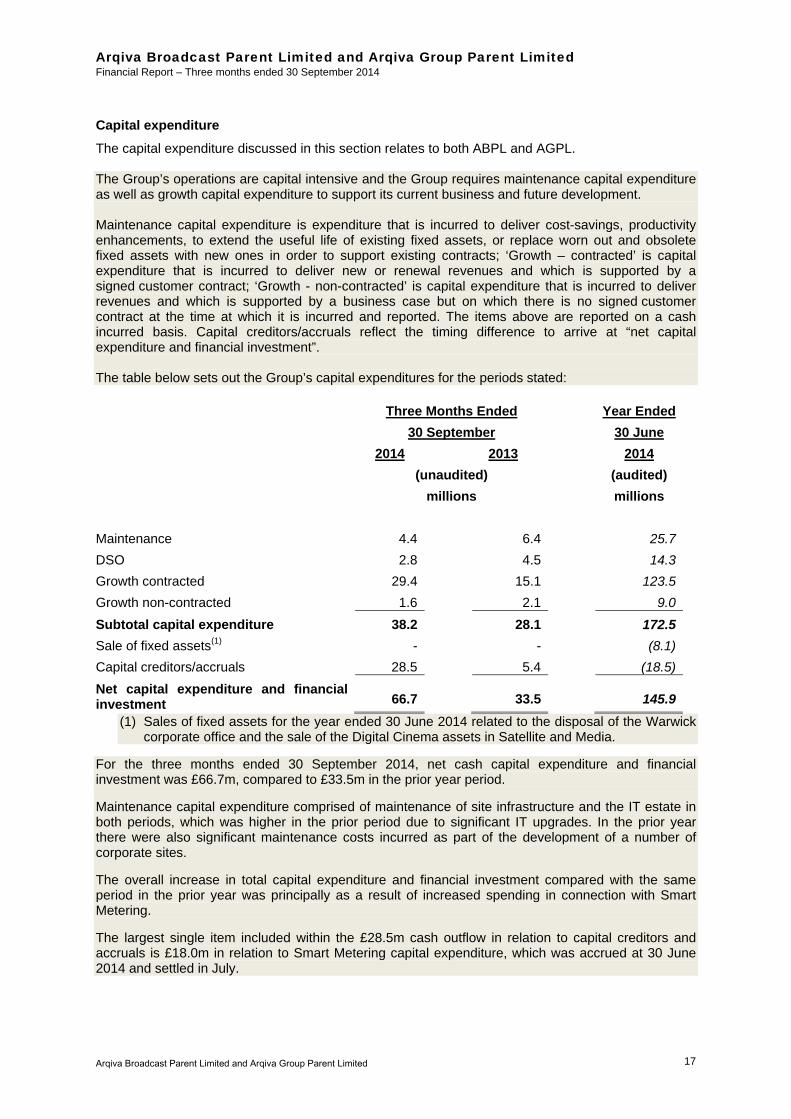

Capital expenditure

The capital expenditure discussed in this section relates to both ABPL and AGPL. The Group’s operations are capital intensive and the Group requires maintenance capital expenditure as well as growth capital expenditure to support its current business and future development. Maintenance capital expenditure is expenditure that is incurred to deliver cost-savings, productivity enhancements, to extend the useful life of existing fixed assets, or replace worn out and obsolete fixed assets with new ones in order to support existing contracts; ‘Growth – contracted’ is capital expenditure that is incurred to deliver new or renewal revenues and which is supported by a signed customer contract; ‘Growth - non-contracted’ is capital expenditure that is incurred to deliver revenues and which is supported by a business case but on which there is no signed customer contract at the time at which it is incurred and reported. The items above are reported on a cash incurred basis. Capital creditors/accruals reflect the timing difference to arrive at “net capital expenditure and financial investment”. The table below sets out the Group’s capital expenditures for the periods stated:

Three Months Ended

30 September

Year Ended

30 June

2014 2013 2014

(unaudited)

millions

(audited)

millions

Maintenance 4.4 6.4 25.7

DSO 2.8 4.5 14.3

Growth contracted 29.4 15.1 123.5

Growth non-contracted 1.6 2.1 9.0

Subtotal capital expenditure 38.2 28.1 172.5

Sale of fixed assets(1) - - (8.1)

Capital creditors/accruals 28.5 5.4 (18.5)

Net capital expenditure and financial investment 66.7 33.5 145.9

(1) Sales of fixed assets for the year ended 30 June 2014 related to the disposal of the Warwick corporate office and the sale of the Digital Cinema assets in Satellite and Media.

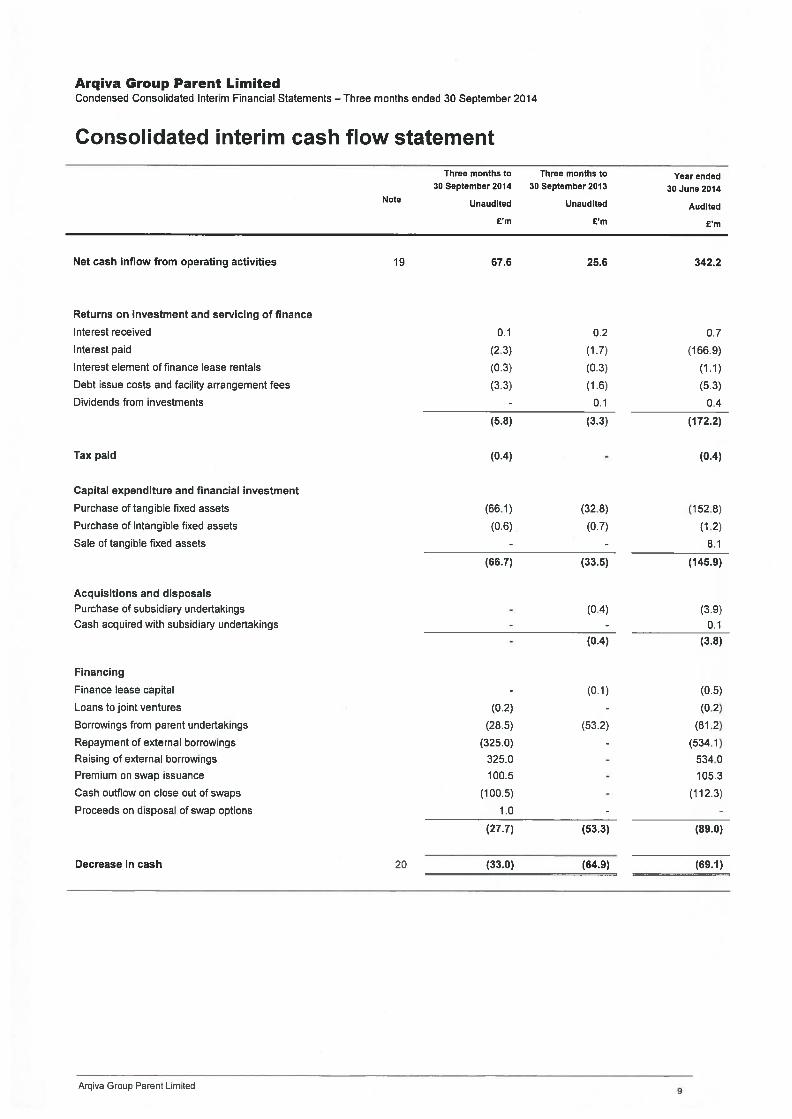

For the three months ended 30 September 2014, net cash capital expenditure and financial investment was £66.7m, compared to £33.5m in the prior year period.

Maintenance capital expenditure comprised of maintenance of site infrastructure and the IT estate in both periods, which was higher in the prior period due to significant IT upgrades. In the prior year there were also significant maintenance costs incurred as part of the development of a number of corporate sites.

The overall increase in total capital expenditure and financial investment compared with the same period in the prior year was principally as a result of increased spending in connection with Smart Metering.

The largest single item included within the £28.5m cash outflow in relation to capital creditors and accruals is £18.0m in relation to Smart Metering capital expenditure, which was accrued at 30 June 2014 and settled in July.

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 18

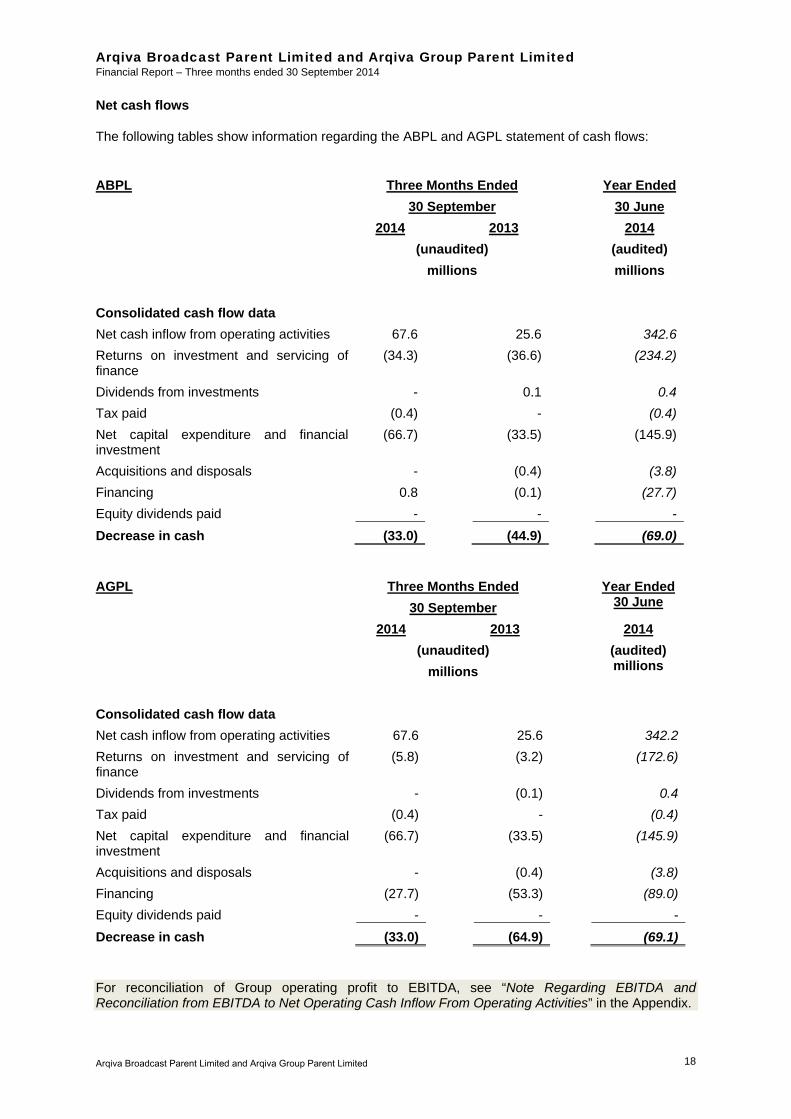

Net cash flows

The following tables show information regarding the ABPL and AGPL statement of cash flows:

ABPL Three Months Ended

30 September

Year Ended

30 June

2014 2013 2014

(unaudited)

millions

(audited)

millions

Consolidated cash flow data

Net cash inflow from operating activities 67.6 25.6 342.6

Returns on investment and servicing of finance

(34.3) (36.6) (234.2)

Dividends from investments - 0.1 0.4

Tax paid (0.4) - (0.4)

Net capital expenditure and financial investment

(66.7) (33.5) (145.9)

Acquisitions and disposals - (0.4) (3.8)

Financing 0.8 (0.1) (27.7)

Equity dividends paid - - -

Decrease in cash (33.0) (44.9) (69.0)

AGPL Three Months Ended

30 September

Year Ended 30 June

2014 2013 2014

(unaudited)

millions

(audited) millions

Consolidated cash flow data

Net cash inflow from operating activities 67.6 25.6 342.2

Returns on investment and servicing of finance

(5.8) (3.2) (172.6)

Dividends from investments - (0.1) 0.4

Tax paid (0.4) - (0.4)

Net capital expenditure and financial investment

(66.7) (33.5) (145.9)

Acquisitions and disposals - (0.4) (3.8)

Financing (27.7) (53.3) (89.0)

Equity dividends paid - - -

Decrease in cash (33.0) (64.9) (69.1)

For reconciliation of Group operating profit to EBITDA, see “Note Regarding EBITDA and Reconciliation from EBITDA to Net Operating Cash Inflow From Operating Activities” in the Appendix.

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 19

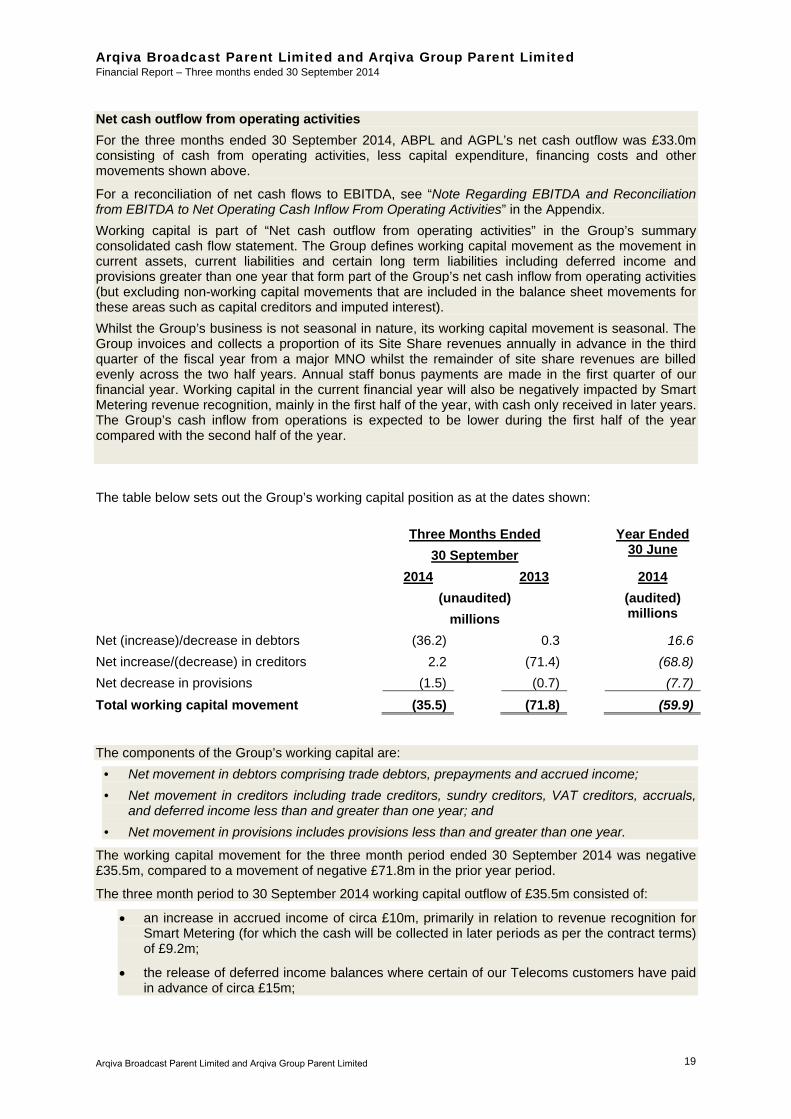

Net cash outflow from operating activities

For the three months ended 30 September 2014, ABPL and AGPL’s net cash outflow was £33.0m consisting of cash from operating activities, less capital expenditure, financing costs and other movements shown above.

For a reconciliation of net cash flows to EBITDA, see “Note Regarding EBITDA and Reconciliation from EBITDA to Net Operating Cash Inflow From Operating Activities” in the Appendix.

Working capital is part of “Net cash outflow from operating activities” in the Group’s summary consolidated cash flow statement. The Group defines working capital movement as the movement in current assets, current liabilities and certain long term liabilities including deferred income and provisions greater than one year that form part of the Group’s net cash inflow from operating activities (but excluding non-working capital movements that are included in the balance sheet movements for these areas such as capital creditors and imputed interest).

Whilst the Group’s business is not seasonal in nature, its working capital movement is seasonal. The Group invoices and collects a proportion of its Site Share revenues annually in advance in the third quarter of the fiscal year from a major MNO whilst the remainder of site share revenues are billed evenly across the two half years. Annual staff bonus payments are made in the first quarter of our financial year. Working capital in the current financial year will also be negatively impacted by Smart Metering revenue recognition, mainly in the first half of the year, with cash only received in later years. The Group’s cash inflow from operations is expected to be lower during the first half of the year compared with the second half of the year.

The table below sets out the Group’s working capital position as at the dates shown:

Three Months Ended

30 September

Year Ended 30 June

2014 2013 2014

(unaudited)

millions

(audited) millions

Net (increase)/decrease in debtors (36.2) 0.3 16.6

Net increase/(decrease) in creditors 2.2 (71.4) (68.8)

Net decrease in provisions (1.5) (0.7) (7.7)

Total working capital movement (35.5) (71.8) (59.9) The components of the Group’s working capital are:

• Net movement in debtors comprising trade debtors, prepayments and accrued income;

• Net movement in creditors including trade creditors, sundry creditors, VAT creditors, accruals, and deferred income less than and greater than one year; and

• Net movement in provisions includes provisions less than and greater than one year.

The working capital movement for the three month period ended 30 September 2014 was negative £35.5m, compared to a movement of negative £71.8m in the prior year period.

The three month period to 30 September 2014 working capital outflow of £35.5m consisted of:

an increase in accrued income of circa £10m, primarily in relation to revenue recognition for Smart Metering (for which the cash will be collected in later periods as per the contract terms) of £9.2m;

the release of deferred income balances where certain of our Telecoms customers have paid in advance of circa £15m;

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 20

the unwinding of the accrual for the annual bonus and long term incentive plan payment of circa £10m made in September 2014; and

other timing differences.

Dividends from investments

During the three months ended 30 September 2014 the Group received a dividend of £nil (2013: £0.1m) from MXR Holdings Limited, a company which owns and operates several regional digital radio Multiplexes within the UK, and a dividend from YouView TV Limited, a joint venture, of £nil (2013: £nil).

Tax paid

For the three months ended 30 September 2014 the Group’s tax paid was £0.4m (2013: £nil).

Acquisitions and disposals

For the three months ended 30 September 2014, the cash outflow from the Group’s acquisitions and disposals was £nil (2013: £0.4m).

Equity dividends paid

For the three months ended 30 September 2014, the Group’s equity dividends paid were £nil (2013: £nil).

Note: The Consolidated cashflow line items diverge at some points and therefore are discussed separately below for the two consolidation levels.

ABPL line items:

Returns on investment and servicing of finance

For the three months ended 30 September 2014, the Group’s returns on investment and servicing of finance was an outflow of £34.3m (2013: outflow of £36.6m), consisting of £0.1m in interest received, less £30.8m in interest paid to external sources, less debt issue costs of £3.3m and less £0.3m from the interest element of finance lease rentals.

Financing

For the three months ended 30 September 2014, the Group’s net financing inflow was £0.8m (2013: outflow of £0.1m). This included a premium on swap issuance of £100.5m, offset entirely by a cash outflow on close out of these swaps of £100.5m, a raising and subsequent total repayment of £325.0m of external borrowings, a small inflow of proceeds on disposal of a Swap Option of £1.0m offset by outflows of £0.2m to joint ventures. The disposal of the Swap Option is discussed further in the interest rate swaps section of this report.

Net cash flow from financing differs to the interest and financing expenses within the profit and loss account due primarily to non-cash charges in the profit and loss account in respect of the amortisation of debt issue costs, imputed interest, accretion liabilities and movements in the amount of accrued interest balances.

Decrease in cash

For the three months ended 30 September 2014 the ABPL Group’s decrease in net cash was £33.0m (2013: £44.9m) due to the above factors.

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 21

AGPL line items:

Returns on investment and servicing of finance

For the three months ended 30 September 2014, the Group’s returns on investment and servicing of finance was an outflow of £5.8m (2013: outflow of £3.2m), consisting of £0.1m in interest received, less £2.3m in interest paid to external sources, less £3.3m debt issue costs, and less £0.3m from the interest element of finance lease rentals.

Financing

For the three months ended 30 September 2014, the Group’s net financing outflow was £27.7m (2013: outflow of £53.3m). This included a premium on swap issuance of £100.5m, offset entirely by a cash outflow on close out of these swaps of £100.5m, a small inflow of proceeds on disposal of a Swap Option of £1.0m, offset by outflows of £0.2m to joint ventures and £28.5m repayment of borrowings from parent undertakings, paid to the ABPL group. This outflow was a permitted payment under the terms of the senior financing and was used to settle interest due on the £600.0m junior notes.

Net cash flow from financing differs to the interest and financing expenses within the profit and loss account due primarily to non-cash charges in the profit and loss account in respect of the amortisation of debt issue costs, imputed interest, accretion liabilities and movements in the amount of accrued interest balances.

Decrease in cash

For the three months ended 30 September 2014 the Group’s decrease in net cash was £33.0m (2013: £44.9m) due to the above factors.

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 22

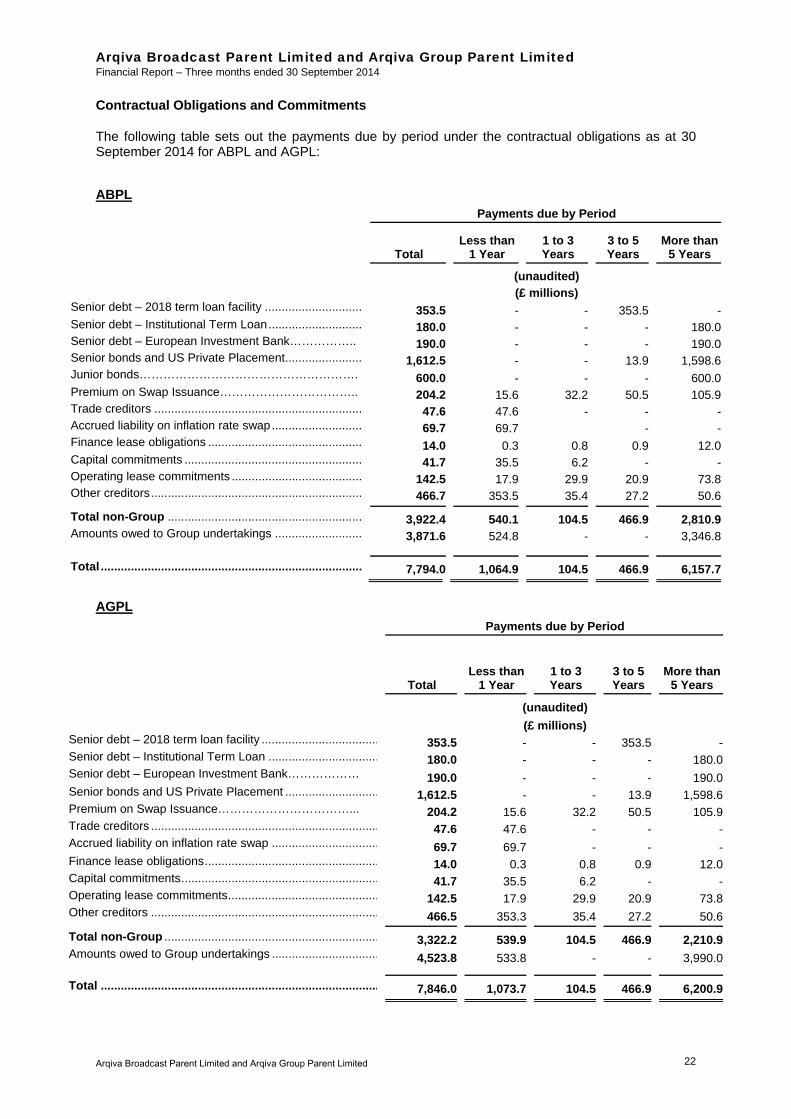

Contractual Obligations and Commitments

The following table sets out the payments due by period under the contractual obligations as at 30 September 2014 for ABPL and AGPL: ABPL

Payments due by Period

Total

Less than1 Year

1 to 3 Years

3 to 5 Years

More than5 Years

(unaudited)

(£ millions) Senior debt – 2018 term loan facility ............................. 353.5 - - 353.5 -Senior debt – Institutional Term Loan ............................ 180.0 - - - 180.0Senior debt – European Investment Bank…………….. 190.0 - - - 190.0Senior bonds and US Private Placement....................... 1,612.5 - - 13.9 1,598.6Junior bonds………………………………………………. 600.0 - - - 600.0Premium on Swap Issuance…………………………….. 204.2 15.6 32.2 50.5 105.9Trade creditors .............................................................. 47.6 47.6 - - -Accrued liability on inflation rate swap ........................... 69.7 69.7 - -Finance lease obligations .............................................. 14.0 0.3 0.8 0.9 12.0Capital commitments ..................................................... 41.7 35.5 6.2 - -Operating lease commitments ....................................... 142.5 17.9 29.9 20.9 73.8Other creditors ............................................................... 466.7 353.5 35.4 27.2 50.6

Total non-Group .......................................................... 3,922.4 540.1 104.5 466.9 2,810.9Amounts owed to Group undertakings .......................... 3,871.6 524.8 - - 3,346.8

Total .............................................................................. 7,794.0 1,064.9 104.5 466.9 6,157.7

AGPL

Payments due by Period

Total

Less than1 Year

1 to 3 Years

3 to 5 Years

More than5 Years

(unaudited)

(£ millions) Senior debt – 2018 term loan facility ................................... 353.5 - - 353.5 -Senior debt – Institutional Term Loan ................................. 180.0 - - - 180.0Senior debt – European Investment Bank……………… 190.0 - - - 190.0Senior bonds and US Private Placement ............................ 1,612.5 - - 13.9 1,598.6Premium on Swap Issuance……………………………... 204.2 15.6 32.2 50.5 105.9Trade creditors .................................................................... 47.6 47.6 - - -Accrued liability on inflation rate swap ................................ 69.7 69.7 - - -Finance lease obligations .................................................... 14.0 0.3 0.8 0.9 12.0Capital commitments ........................................................... 41.7 35.5 6.2 - -Operating lease commitments ............................................. 142.5 17.9 29.9 20.9 73.8Other creditors .................................................................... 466.5 353.3 35.4 27.2 50.6

Total non-Group ................................................................ 3,322.2 539.9 104.5 466.9 2,210.9Amounts owed to Group undertakings ................................ 4,523.8 533.8 - - 3,990.0 Total ................................................................................... 7,846.0 1,073.7 104.5 466.9 6,200.9

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 23

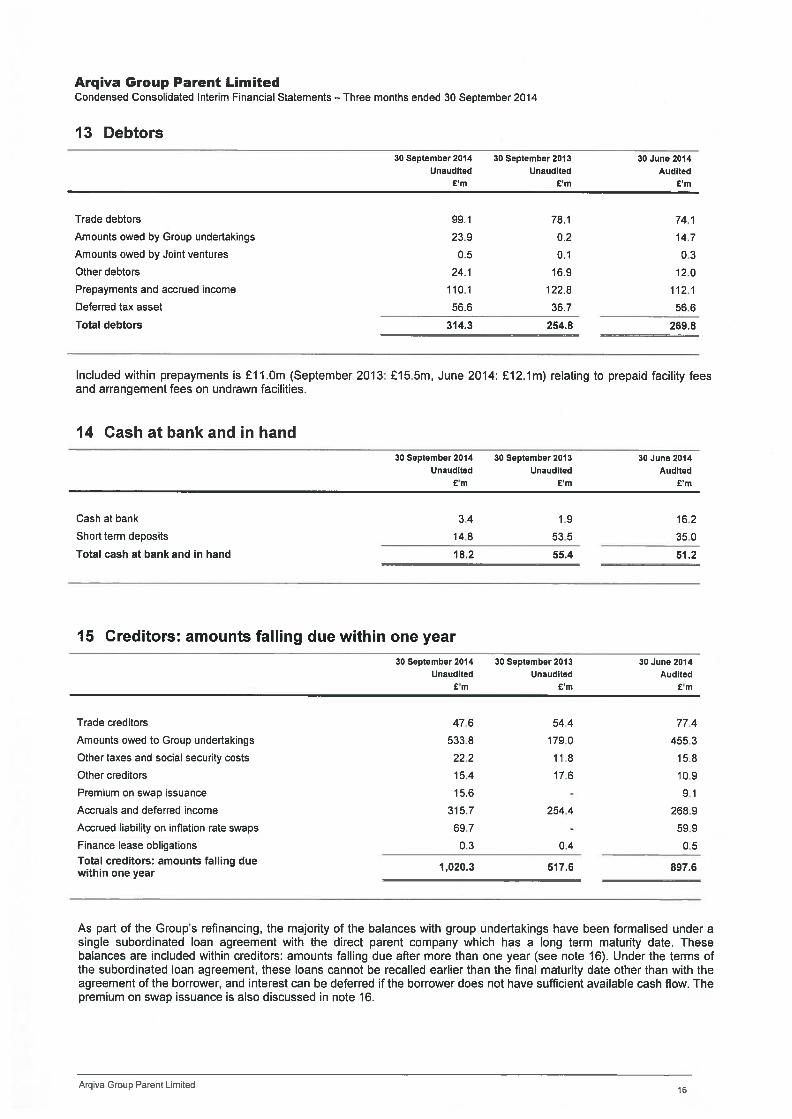

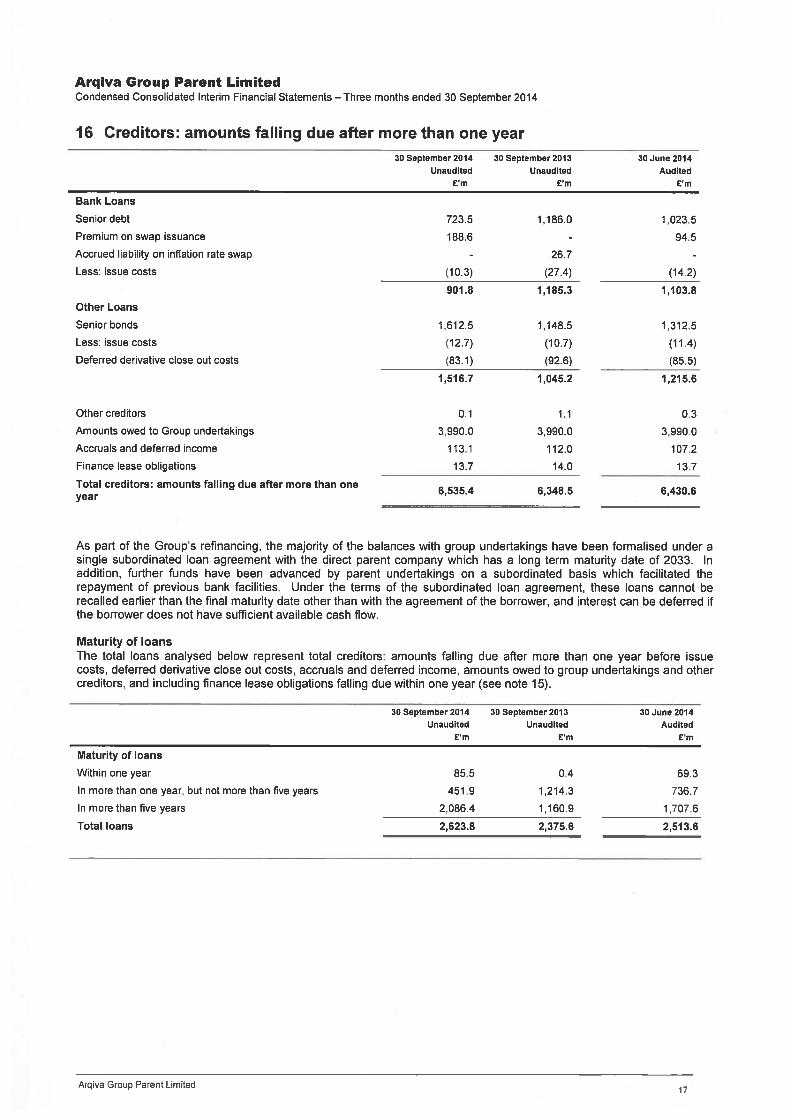

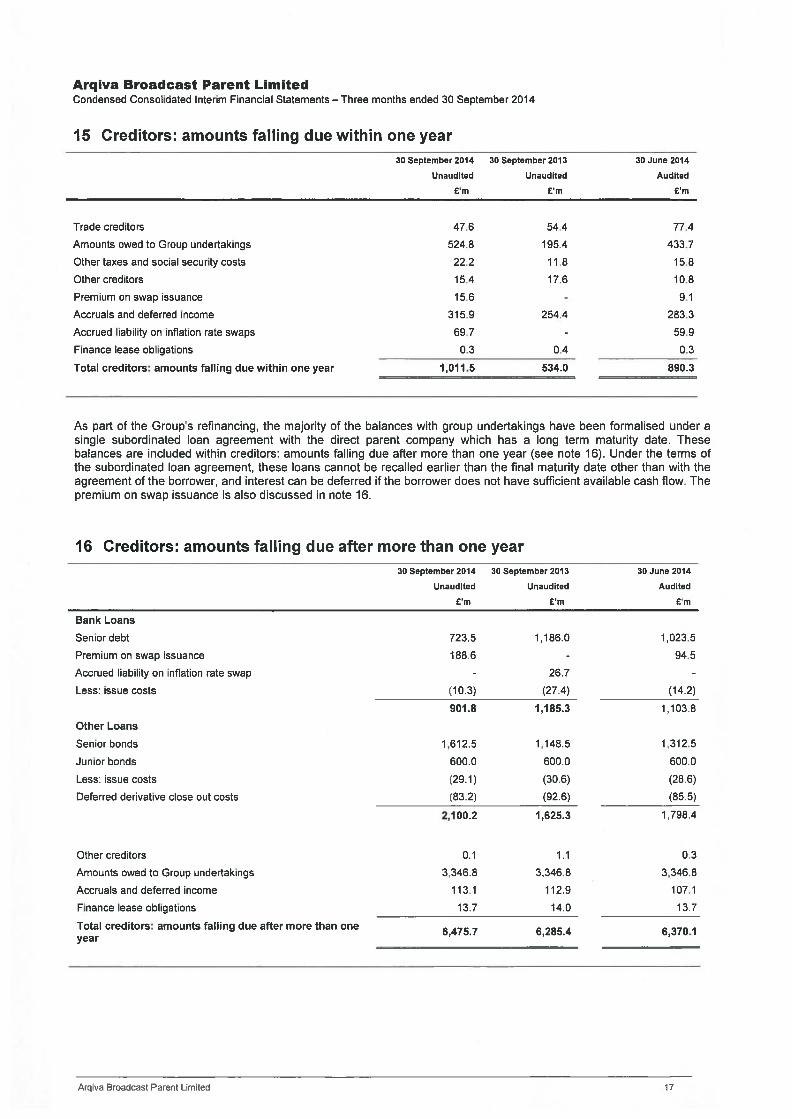

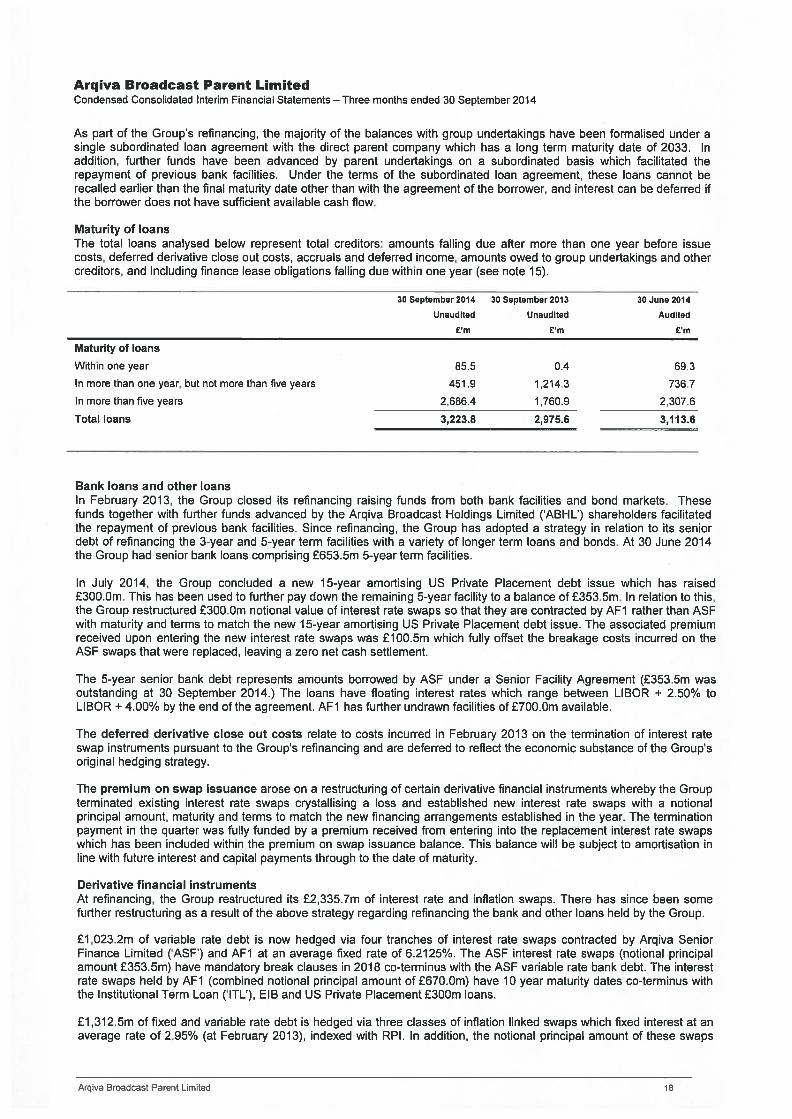

As part of the Group’s refinancing, the majority of the balances with group undertakings have been formalised under a single subordinated loan agreement with the direct parent company which has a long term maturity date of 2033. Under the terms of the subordinated loan agreement, these loans cannot be recalled earlier than the final maturity date other than with the agreement of the borrower, and interest can be deferred if the borrower does not have sufficient available cash flow.

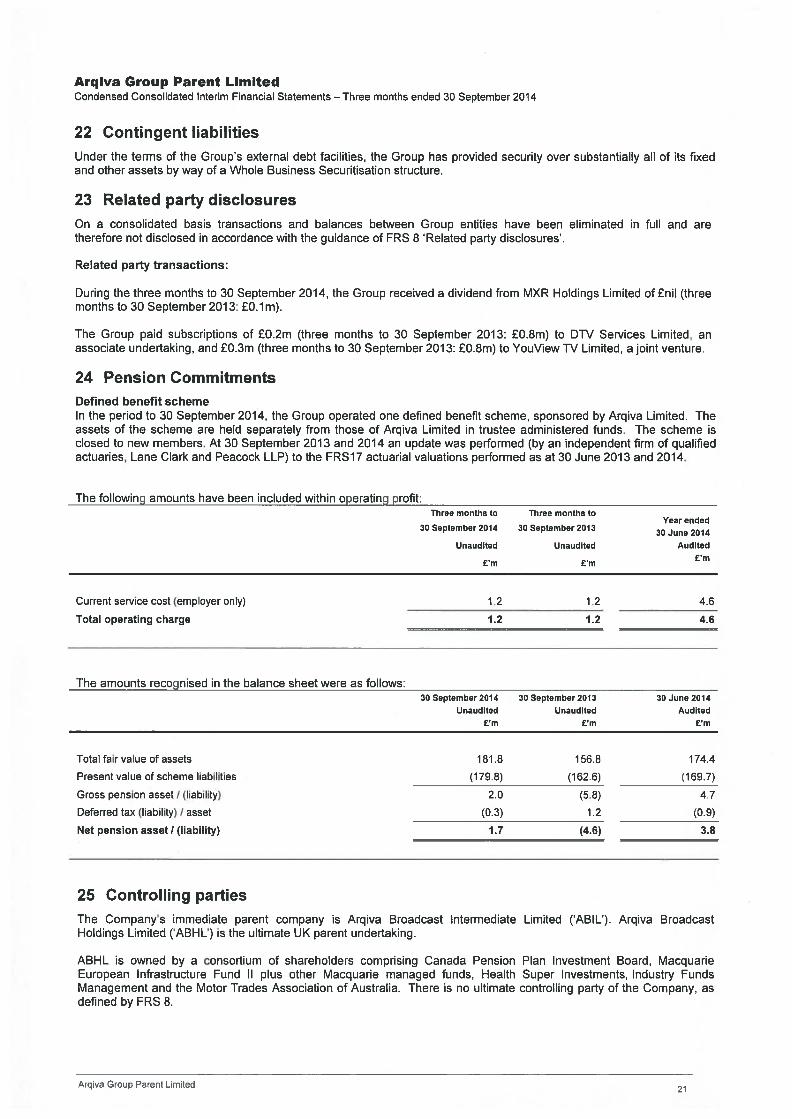

Contingent Liabilities

Under the terms of the Group’s external debt facilities, it has provided security over substantially all of its fixed and other assets by way of a Whole Business Securitisation structure.

Financing During July 2014, the Group completed a US Private Placement floating rate debt issue of £300.0m, with a final expected maturity of 15 years and a weighted average life of 11.5 years. The proceeds of this loan were utilised to repay a portion of the 5-year term bank facility. As at 30 September 2014 the outstanding balance on the 5-year term bank facility was £353.5m.

Off-Balance Sheet Arrangements

The Group does not, and has not used off-balance sheet special purpose vehicles or similar financing arrangements on an historical basis. In addition, the Group has not had and does not have off-balance sheet arrangements with any of its affiliates.

The Group uses Interest Rate Swaps (‘IRS’), Inflation Linked Swaps (‘ILS’) and cross-currency swaps to reduce its exposure to fluctuations in variable interest rates on its debt and currency movements on its US dollar debt. Receipts, payments and accreting liabilities on interest rate and inflation swaps are recognised on an accruals basis, over the life of the instrument. Changes in the fair value of such derivatives are not required to be recognised under UK GAAP, but are instead disclosed in the notes. Amounts received and paid under the swaps are shown at net value under financing costs, where they are part of the same legal agreement and settled at net value in practice. Accreting liabilities on ILS are recognised on an accruals basis. The Group also utilises forward purchase contracts to hedge certain foreign currency transactions. The changes in the fair value of such derivatives are not recognised, and the gain or loss on settlement is taken to the profit and loss account. Inflation linked swaps (ILS)

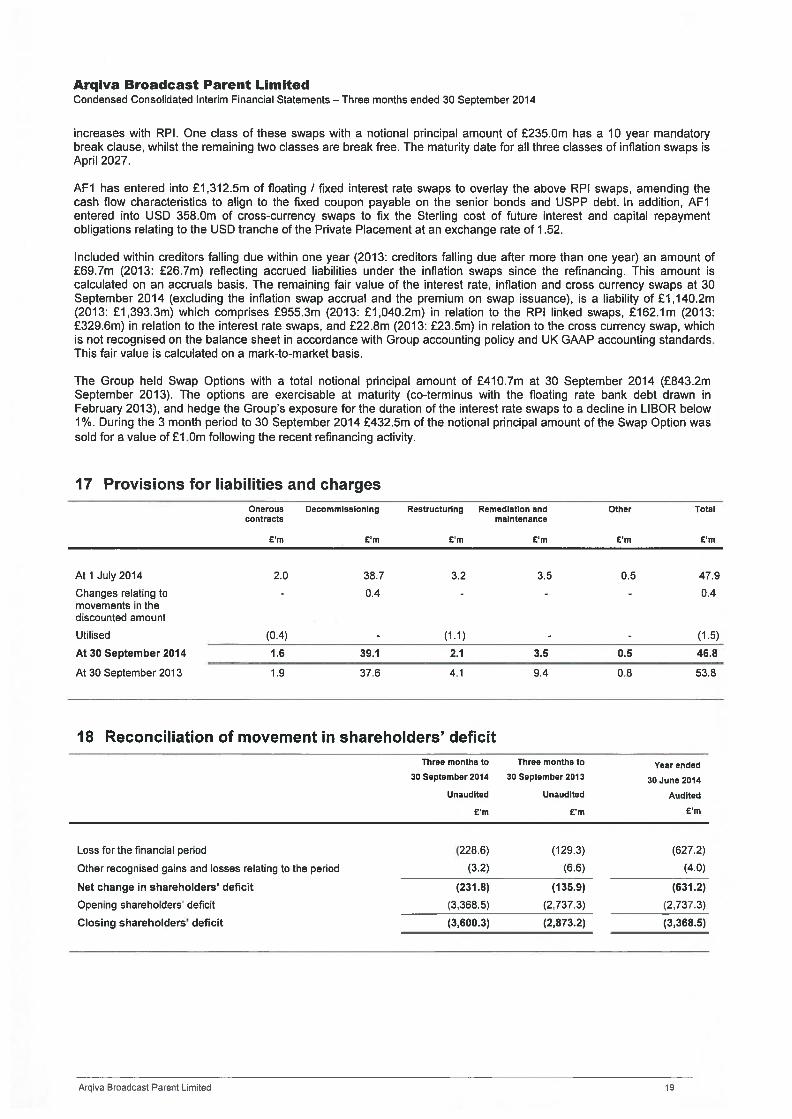

£1,312.5m of fixed rate debt is hedged via three classes of ILS which either directly or via overlay swaps, fix interest at an average rate of 2.95% (at February 2013), indexed with RPI. In addition, the principal amount of these swaps increases with RPI. One class of these swaps with a nominal value of £235.0m has a 10 year mandatory break clause, whilst the remaining two classes are break-free.

The maturity date for all three classes of ILS is April 2027. The accretion of £69.7m at September 2014 will be settled in cash at 30 June 2015 together with the further accretion to that date.

Interest rate swaps (IRS)

£1,023.2m of variable rate debt is now hedged via four tranches of interest rate swaps contracted by ASF and AF1 at an average fixed rate of 6.2125%. The ASF interest rate swaps (nominal value £353.5m) have mandatory break clauses in 2018 co-terminus with the ASF variable rate bank debt. The interest rate swaps held by AF1 (combined nominal values of £670.0m) have maturity dates co-terminus with the Institutional Term Loan (‘ITL’), EIB and US Private Placement £300m loans.

A premium on swap issuance of £205.7m (September 2013: £nil) is recorded within creditors. During the 2014 financial year, the Group paid total termination costs of £112.6m and received a total premium of £105.6m for entering into replacement IRS in the Borrower, following the termination of existing equivalent swaps in ASFL reflecting the refinancing of the underlying debt in ASFL. These transactions resulted in a cash cost of £7.0m during the year ended 30 June 2014.

In July 2014, on raising of the US Private Placement floating rate loan of £300.0m, an additional premium of £100.5m was received by AF1 for entering into replacement IRS and used to fund the whole mark-to-market payment of £100.5m due by ASF at termination of the equivalent IRS. As at 30 September 2014, the outstanding premium amount after amortisation of £0.4m was £205.7m.

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 24

The restructure of the swaps and transfer from ASF to AF1 has resulted in a charge to the profit and loss account, owing to the fact that the termination payment of the relevant ASF (Finco) hedges has been recognised immediately, whereas the premium received for entering into the new IRS in AF1 has been recorded on the balance sheet and will be amortised over the 11.5 year weighted average life of the new IRS.

The fair value of the interest rate, inflation and cross currency swaps at 30 September 2014 (excluding the inflation swap accrual and the premium on swap issuance), is a liability of £1,117.4m which comprises £955.3m in relation to the RPI linked swaps, £162.1m in relation to the interest rate swaps, and £22.8m in relation to the cross currency swap (2013: total £1,393.3m). This fair value calculated on a Mark-to-Market basis is not recognised on the balance sheet in accordance with Group accounting policy and UK GAAP accounting standards.

The Group held Swap Options with a total notional principal amount of £410.7m at 30 September 2014 (£843.2m September 2013). The options are exercisable at maturity (co-terminus with the floating rate bank debt drawn in February 2013) on 29th February 2016 and 28th February 2018, and hedge the Group’s exposure for the duration of the interest rate swaps to a decline in LIBOR below 1%. During the 3 month period to 30 September 2014 £432.5m of the notional principal amount of the Swap Option was sold for a value of £1.0m to match the IRS exposure after the recent refinancing.

Cross Currency Swaps

AF1 has entered into USD 358.0m of cross-currency swaps to fix the Sterling cost of future interest and capital repayment obligations relating to the USD tranche of the Private Placement at an exchange rate of 1.52.

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 25

CRITICAL ACCOUNTING POLICIES

Turnover

Turnover, which is stated net of value added tax, includes the value of charges made for transmission services, distribution services, products, facilities leasing, external network services to national and international telecommunication operators, other contracts, rents from properties and charges made under site sharing agreements.

Turnover is recognised as services are provided. Cash received or invoices raised in advance is taken to deferred income and recognised as turnover when service is provided. Where consideration received in advance is discounted reflecting a significant financing component it is reflected within turnover and interest payable and similar charges. During the three month period ended 30 September 2014 £1.8m of revenue and £2.0m of interest expense was recognised as a result of the time value of money.

Turnover recognised in advance of cash received or invoices raised is taken to accrued income.

Profit is recognised on long-term contracts, if the final outcome can be assessed with reasonable certainty, by including in the profit and loss account turnover and related costs as contract activity progresses. Turnover is calculated by reference to the value of work performed as a proportion of the total contract value.

Derivative financial instruments

The Group uses interest rate swaps to reduce its exposure to fluctuations in variable interest rates on its debt and inflation swaps to reduce its exposure to inflation on revenue contracts. Receipts, payments and accreting liabilities on interest rate and inflation swaps are recognised on an accruals basis, over the life of the instrument. Deferred derivative close out costs are also recognised within other interest which relate to costs incurred in February 2013 on the termination of interest rate swap instruments pursuant to the Group's refinancing and are deferred to reflect the economic substance of the Group’s original hedging strategy. Changes in the fair value of such derivatives, however, are not recognised. Amounts received and paid under interest rate and inflation swaps are shown net under financing costs, where they are part of the same legal agreement and settled net in practice. The Group utilises forward foreign exchange contracts to hedge the value of certain foreign currency transactions. In addition, the Group utilises cross currency swaps to hedge the principal and interest payments due under the USD tranche of the Private Placement against variations in foreign exchange and interest rates. The changes in the fair value of such derivatives are not recognised, and the gain or loss on settlement is taken to the profit and loss account. During the three month period to 30 September 2014 the Group received premium receipts of £100.5m for entering into replacement interest rate swaps upon further refinancing, the treatment for which is discussed elsewhere in this report.

Leasing Commitments

Assets held under finance leases, which are leases where substantially all the risks and rewards of ownership of the asset have passed to the Group, are capitalised in the balance sheet and depreciated over their useful economic lives or the lease term, if shorter.

The capital elements of future lease obligations are recorded as liabilities, while the interest elements are charged to the profit and loss account over the period of the lease to produce a constant rate of charge on the balance of capital repayments outstanding.

Operating lease payments for assets leased from third parties are charged to the profit and loss account on a straight line basis over the period of the lease.

Equipment leased to customers under finance leases is deemed to be sold at normal selling price and this value is taken to turnover at the inception of the lease. Debtors under finance leases represent outstanding amounts due under these agreements, less finance charges allocated to future periods. Finance lease interest is recognised over the primary period of the lease so as to produce a constant rate of return on the net cash investments.

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 26

Recent and Prospective Changes in Accounting Policies

To the best of the Group’s knowledge, there are no accounting standards applicable to it that will require a prospective change in any of its accounting policies during the current or following financial year as at June 2014. Management are considering the future of UK Generally Accepted Accounting Practise (UK GAAP), or possible conversion to International Financial Reporting Standards (IFRS). The changes resulting from this would apply to the Group from the 30 June 2016 year end. Given this change, management are considering the updated IFRS Accounting Standard recently released on IFRS 15 “Revenue from Customer Contracts” and monitoring the latest news in relation to the expected final Standard on IAS 17 “Leases”.

Basis of Preparation

The condensed consolidated interim financial statements, and the annual audited financial statements, have been prepared in accordance with the Companies Act 2006 and applicable UK accounting standards under the historical cost convention. In order to show a true and fair view, the Group’s policy in respect of merger accounting departs from the requirements of the Companies Act 2006. Details of the departures are given in the annual financial statements.

Basis of Consolidation

The consolidated financial statements incorporate the assets and liabilities of all entities controlled by the Company, as at 30 September 2014, and the results of all controlled entities for the period then ended.

Businesses acquired, previously held externally to the Group, are accounted for as acquisitions with effect from the date control passes. Those disposed of are accounted for up until the date of disposal. Intra group profits have been eliminated. Undertakings, other than subsidiary undertakings, in which the Group has an investment representing not less than 20% of the voting rights and over which it exerts significant influence are treated as associated undertakings. Associates are accounted for using the equity method of accounting in accordance with FRS 9 ‘Associates and joint ventures’. Joint ventures are accounted for using the gross equity method. The consolidated financial statements include the appropriate share of those undertakings’ results and reserves.

Pensions

Defined benefit schemes are funded, with the assets of the scheme held separately from those of the Group, in separate trustee administered funds. Pension scheme assets are measured at fair value and liabilities are measured on an actuarial basis using the projected unit method and discounted at a rate equivalent to the current rate of return on a high quality corporate bond of equivalent currency and terms to the scheme liabilities.

Any defined benefit asset or liability is presented separately on the face of the balance sheet and net of deferred tax.

Since 30 June 2010, there has been a single defined benefit pensions arrangement operating, with Arqiva Limited as the sponsor. On this basis the disclosure for the schemes has been combined. The assets of the scheme are held separately from those of Arqiva Limited in trustee-administered funds.

The triennial valuation of the Group’s defined benefit pension obligations as at 30 June 2011, for actuarial funding purposes, had resulted in an assessed deficit of £17.4m. Gross plan liabilities at the valuation date were £130.5m compared to gross plan assets of £113.1m. Arqiva Limited agreed with the trustees to make deficit recovery payments into the Plan totalling £15.5m after taking into account payments already made under the previous recovery plan subsequent to the date of the valuation. A final amount of £4.1m payable under this recovery plan is due in July 2015. A further triennial valuation is due as at 30 June 2014 and will be prepared by the Group’s actuaries in the current financial year.

For defined contribution schemes, the amount charged to the profit and loss account in respect of pension costs and other post-retirement benefits is the contribution payable in the year. Differences between contributions payable for the year and contributions actually paid are shown as either accruals or prepayments in the balance sheet.

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited Financial Report – Three months ended 30 September 2014

Arqiva Broadcast Parent Limited and Arqiva Group Parent Limited 27

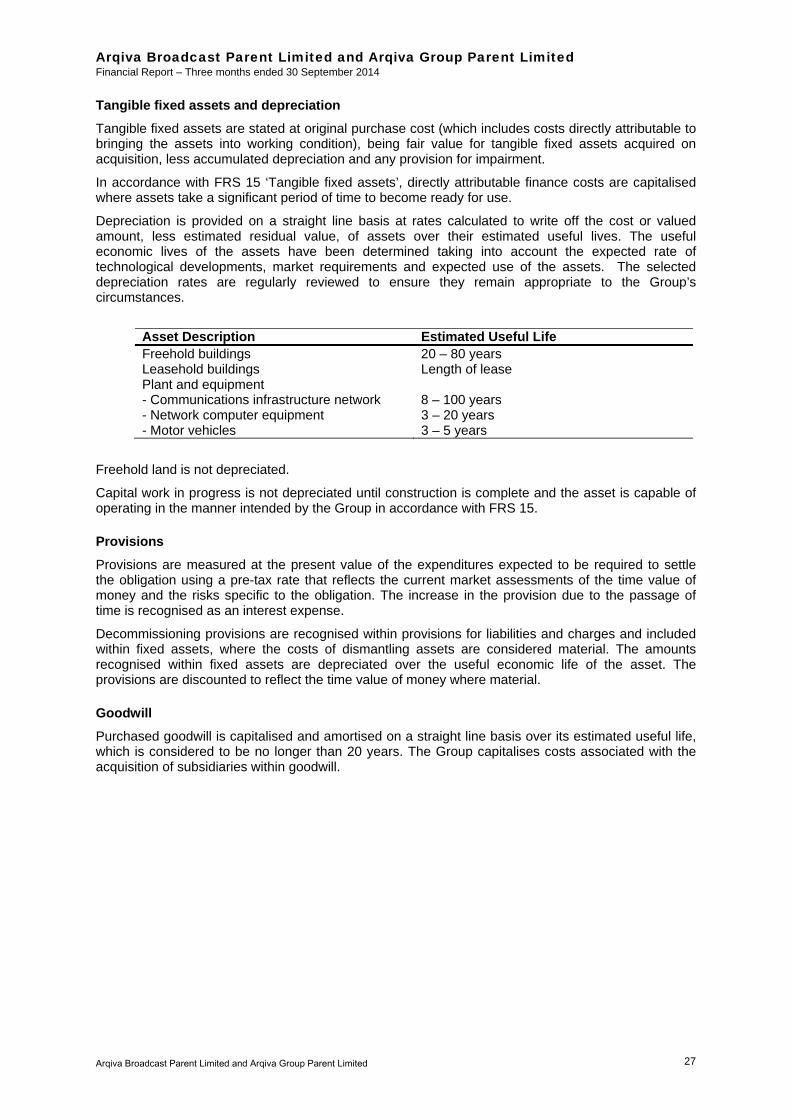

Tangible fixed assets and depreciation

Tangible fixed assets are stated at original purchase cost (which includes costs directly attributable to bringing the assets into working condition), being fair value for tangible fixed assets acquired on acquisition, less accumulated depreciation and any provision for impairment.

In accordance with FRS 15 ‘Tangible fixed assets’, directly attributable finance costs are capitalised where assets take a significant period of time to become ready for use.

Depreciation is provided on a straight line basis at rates calculated to write off the cost or valued amount, less estimated residual value, of assets over their estimated useful lives. The useful economic lives of the assets have been determined taking into account the expected rate of technological developments, market requirements and expected use of the assets. The selected depreciation rates are regularly reviewed to ensure they remain appropriate to the Group’s circumstances.

Asset Description Estimated Useful Life Freehold buildings 20 – 80 years Leasehold buildings Length of lease Plant and equipment - Communications infrastructure network 8 – 100 years - Network computer equipment 3 – 20 years - Motor vehicles 3 – 5 years

Freehold land is not depreciated.

Capital work in progress is not depreciated until construction is complete and the asset is capable of operating in the manner intended by the Group in accordance with FRS 15.

Provisions