asean agri bites-march 2011 tushar-newagri-bites | asean tanuj shori / ken arieff wong nomura 3 23...

TRANSCRIPT

23 March 2011 Nomura 1

Any authors named on this report are research analysts unless otherwise indicated. See the important disclosures and analyst certifications on pages 61 to 65.

Agri-Bites | A S E A N CONSUMER RELATED/AGRI RELATED

Tanuj Shori +65 6433 6981 [email protected]

Ken Arieff Wong +60 3 2027 6895 [email protected]

Ploenjai Jirajarus (Capital Nomura Securities)

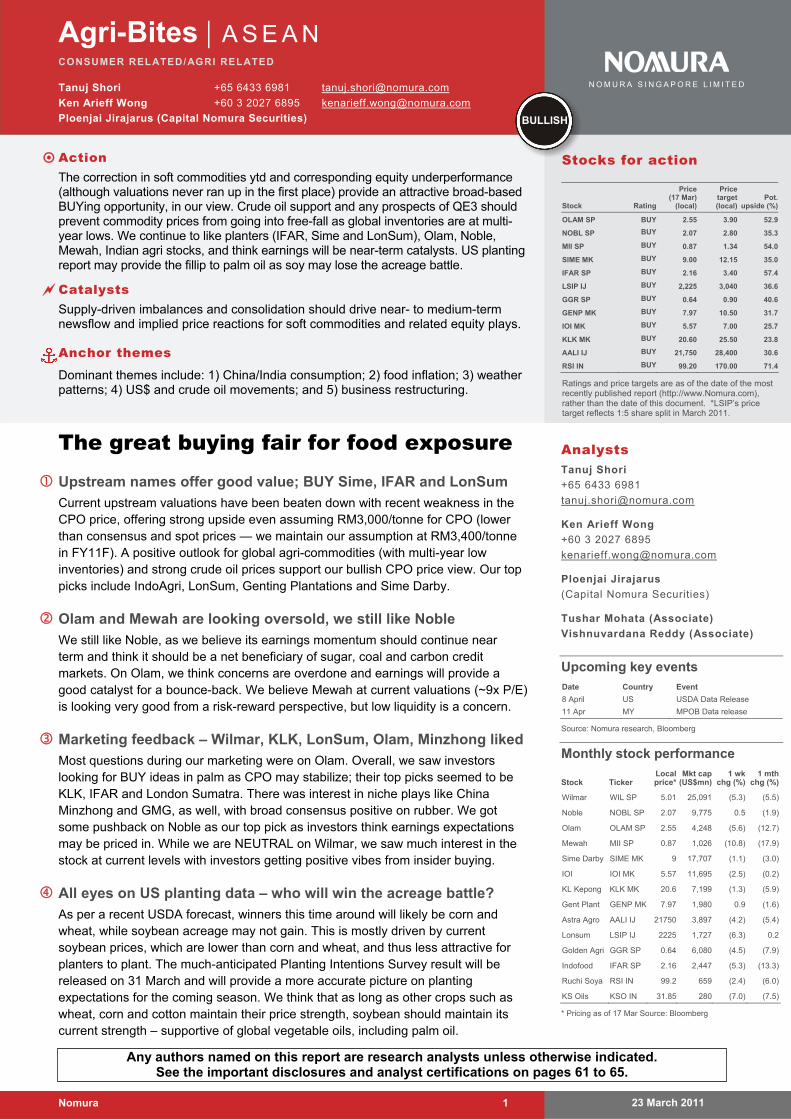

Action

The correction in soft commodities ytd and corresponding equity underperformance (although valuations never ran up in the first place) provide an attractive broad-based BUYing opportunity, in our view. Crude oil support and any prospects of QE3 should prevent commodity prices from going into free-fall as global inventories are at multi-year lows. We continue to like planters (IFAR, Sime and LonSum), Olam, Noble, Mewah, Indian agri stocks, and think earnings will be near-term catalysts. US planting report may provide the fillip to palm oil as soy may lose the acreage battle.

Catalysts

Supply-driven imbalances and consolidation should drive near- to medium-term newsflow and implied price reactions for soft commodities and related equity plays.

Anchor themes

Dominant themes include: 1) China/India consumption; 2) food inflation; 3) weather patterns; 4) US$ and crude oil movements; and 5) business restructuring.

The great buying fair for food exposure Upstream names offer good value; BUY Sime, IFAR and LonSum

Current upstream valuations have been beaten down with recent weakness in the CPO price, offering strong upside even assuming RM3,000/tonne for CPO (lower than consensus and spot prices — we maintain our assumption at RM3,400/tonne in FY11F). A positive outlook for global agri-commodities (with multi-year low inventories) and strong crude oil prices support our bullish CPO price view. Our top picks include IndoAgri, LonSum, Genting Plantations and Sime Darby.

Olam and Mewah are looking oversold, we still like Noble

We still like Noble, as we believe its earnings momentum should continue near term and think it should be a net beneficiary of sugar, coal and carbon credit markets. On Olam, we think concerns are overdone and earnings will provide a good catalyst for a bounce-back. We believe Mewah at current valuations (~9x P/E) is looking very good from a risk-reward perspective, but low liquidity is a concern.

Marketing feedback – Wilmar, KLK, LonSum, Olam, Minzhong liked

Most questions during our marketing were on Olam. Overall, we saw investors looking for BUY ideas in palm as CPO may stabilize; their top picks seemed to be KLK, IFAR and London Sumatra. There was interest in niche plays like China Minzhong and GMG, as well, with broad consensus positive on rubber. We got some pushback on Noble as our top pick as investors think earnings expectations may be priced in. While we are NEUTRAL on Wilmar, we saw much interest in the stock at current levels with investors getting positive vibes from insider buying.

All eyes on US planting data – who will win the acreage battle?

As per a recent USDA forecast, winners this time around will likely be corn and wheat, while soybean acreage may not gain. This is mostly driven by current soybean prices, which are lower than corn and wheat, and thus less attractive for planters to plant. The much-anticipated Planting Intentions Survey result will be released on 31 March and will provide a more accurate picture on planting expectations for the coming season. We think that as long as other crops such as wheat, corn and cotton maintain their price strength, soybean should maintain its current strength – supportive of global vegetable oils, including palm oil.

N O M U R A S I N G A P O R E L I M I T E D

Stocks for action

BULLISH

Stock Rating

Price (17 Mar)

(local)

Price target(local)

Pot.upside (%)

OLAM SP BUY 2.55 3.90 52.9

NOBL SP BUY 2.07 2.80 35.3

MII SP BUY 0.87 1.34 54.0

SIME MK BUY 9.00 12.15 35.0

IFAR SP BUY 2.16 3.40 57.4

LSIP IJ BUY 2,225 3,040 36.6

GGR SP BUY 0.64 0.90 40.6

GENP MK BUY 7.97 10.50 31.7

IOI MK BUY 5.57 7.00 25.7

KLK MK BUY 20.60 25.50 23.8

AALI IJ BUY 21,750 28,400 30.6

RSI IN BUY 99.20 170.00 71.4

Ratings and price targets are as of the date of the most recently published report (http://www.Nomura.com), rather than the date of this document. *LSIP’s price target reflects 1:5 share split in March 2011.

Analysts Tanuj Shori

+65 6433 6981

Ken Arieff Wong

+60 3 2027 6895

Ploenjai Jirajarus

(Capital Nomura Securities)

Tushar Mohata (Associate)

Vishnuvardana Reddy (Associate)

Upcoming key events Date Country Event

8 April US USDA Data Release

11 Apr MY MPOB Data release

Source: Nomura research, Bloomberg

Monthly stock performance

Stock Ticker Local price*

Mkt cap (US$mn)

1 wk chg (%)

1 mth chg (%)

Wilmar WIL SP 5.01 25,091 (5.3) (5.5)

Noble NOBL SP 2.07 9,775 0.5 (1.9)

Olam OLAM SP 2.55 4,248 (5.6) (12.7)

Mewah MII SP 0.87 1,026 (10.8) (17.9)

Sime Darby SIME MK 9 17,707 (1.1) (3.0)

IOI IOI MK 5.57 11,695 (2.5) (0.2)

KL Kepong KLK MK 20.6 7,199 (1.3) (5.9)

Gent Plant GENP MK 7.97 1,980 0.9 (1.6)

Astra Agro AALI IJ 21750 3,897 (4.2) (5.4)

Lonsum LSIP IJ 2225 1,727 (6.3) 0.2

Golden Agri GGR SP 0.64 6,080 (4.5) (7.9)

Indofood IFAR SP 2.16 2,447 (5.3) (13.3)

Ruchi Soya RSI IN 99.2 659 (2.4) (6.0)

KS Oils KSO IN 31.85 280 (7.0) (7.5)

* Pricing as of 17 Mar Source: Bloomberg

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 2

Contents

Nomura ASEAN Soft Commodity Team 4

The great buying fair 5 In line with commodities, equities have underperformed as well… 6 CPO price has corrected 14% from its peak, but equities punished further – unwarranted in our view 6 CPO price assumption maintained 7 CPO discount to soybean oil comes off, lending some comfort 8 All eyes on US spring planting season; USDA expects little change in hectarage for soybean, with most gains in to be made in corn and wheat 8 Impact of Japanese earthquake on agri-commodities 9 Long positions of “managed money” in soy oil futures withdraws as risk appetite withdraws 10

Stocks: what we like and what we don’t 12 Upstream planters severely punished – offer ‘deep value’ 12 Midstream: we continue to like Noble, Olam and Mewah, but are cautious on Wilmar 12 We also like Indian edible oil players – Ruchi Soya and KS Oils 13 Thai Food & Agri: CNS prefers food processors CPF and GFPT on global demand for high-quality processed foods and benefit from soft commodity price drop 13

Other data points for the month 14 Malaysian February palm oil data — production and exports down, prices fairly reflect inventory levels 14 China soybean crushing margins fell in February, US margins almost at parity 14 Palm oil industry refining margins spike 15 Major news flow for the month 16

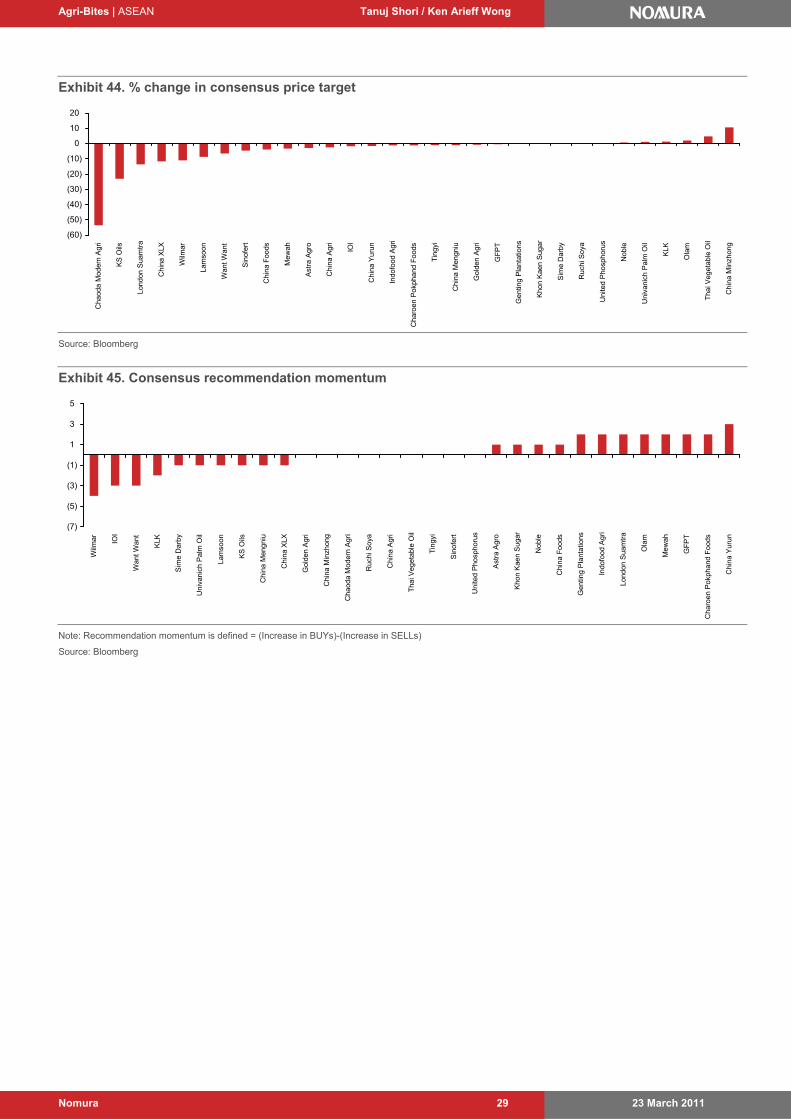

Round-up of Feb-March 2011 17 Last month’s commodity price performance: negative 17 Stock performance generally negative, agri inputs and midstream lead fall 17 Consensus downgrades occur on price correction, profit taking 17

Valuation snapshot 18

Valuation charts 24

The ups and downs 26 Last month’s commodity price performance: negative 26 Stock performance generally negative, agri inputs and midstream lead fall 27 YTD 2011 recap: generally negative returns by agri stocks 27 Consensus downgrades occur due to price correction, profit taking 28

Ears to the ground 30 Important events/news flow summary 30 Company news flow summary 32 Highlights of our published research 33

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 3

Commodity snippets 34

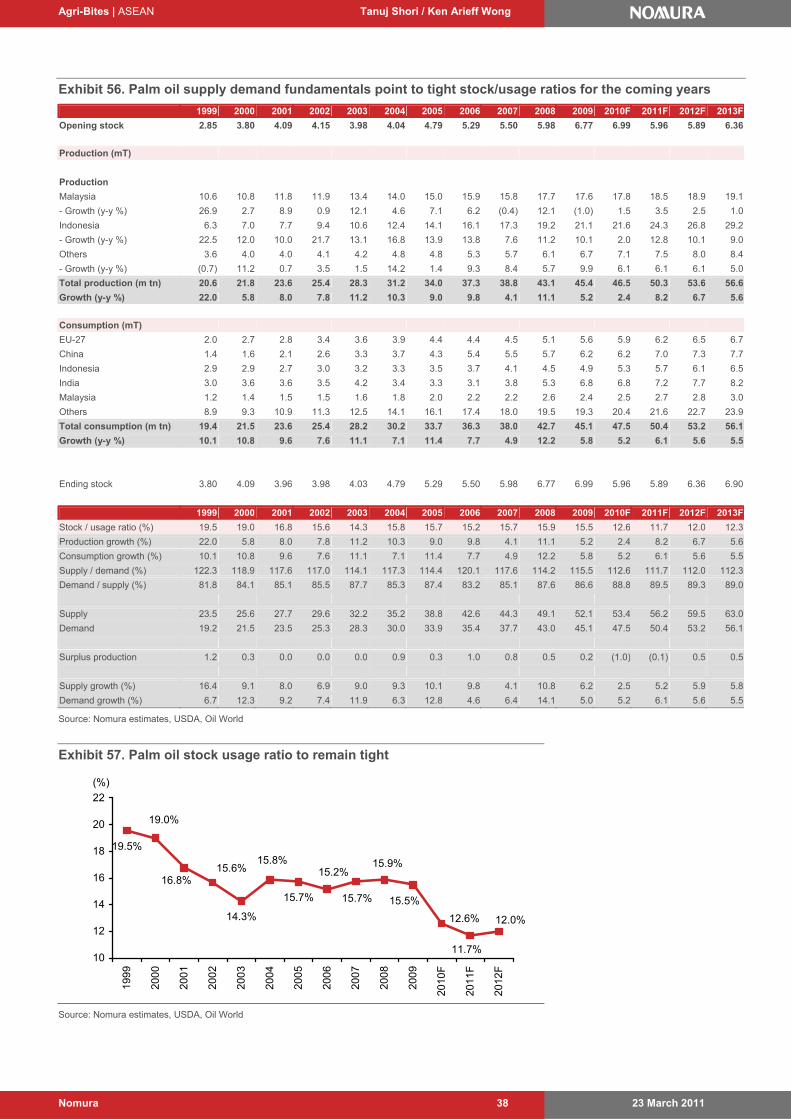

Palm oil 35 What you need to know for the month of March 35

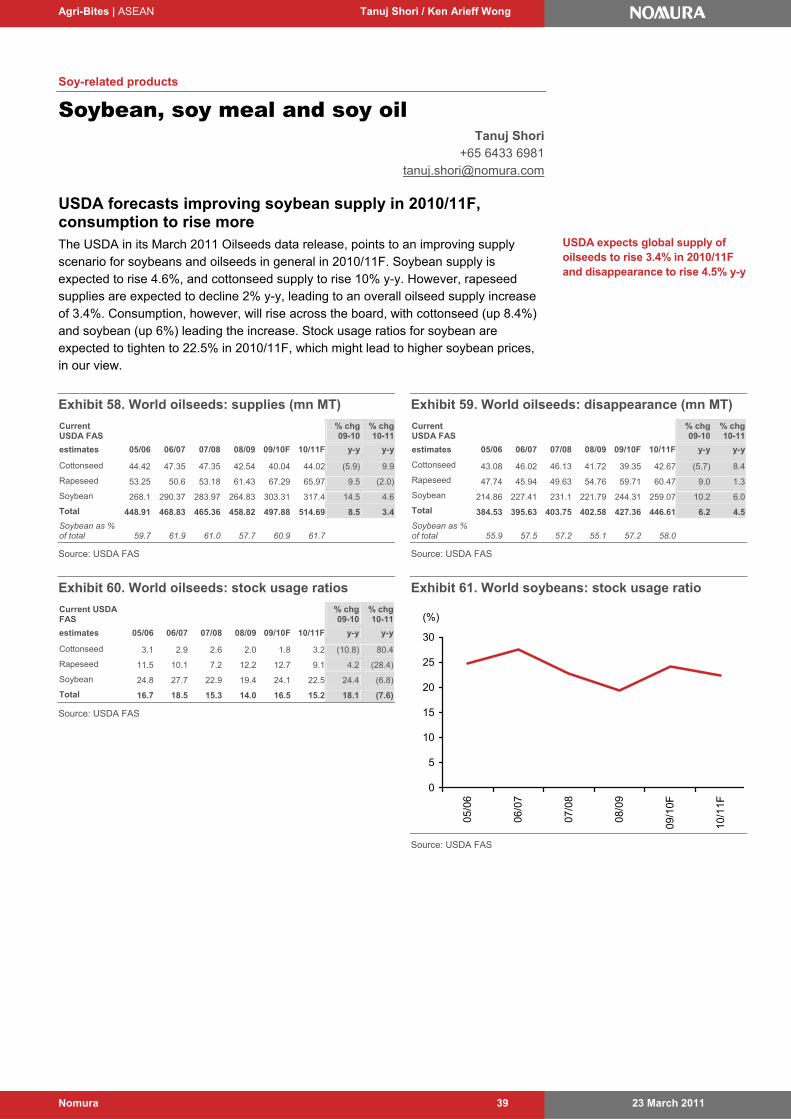

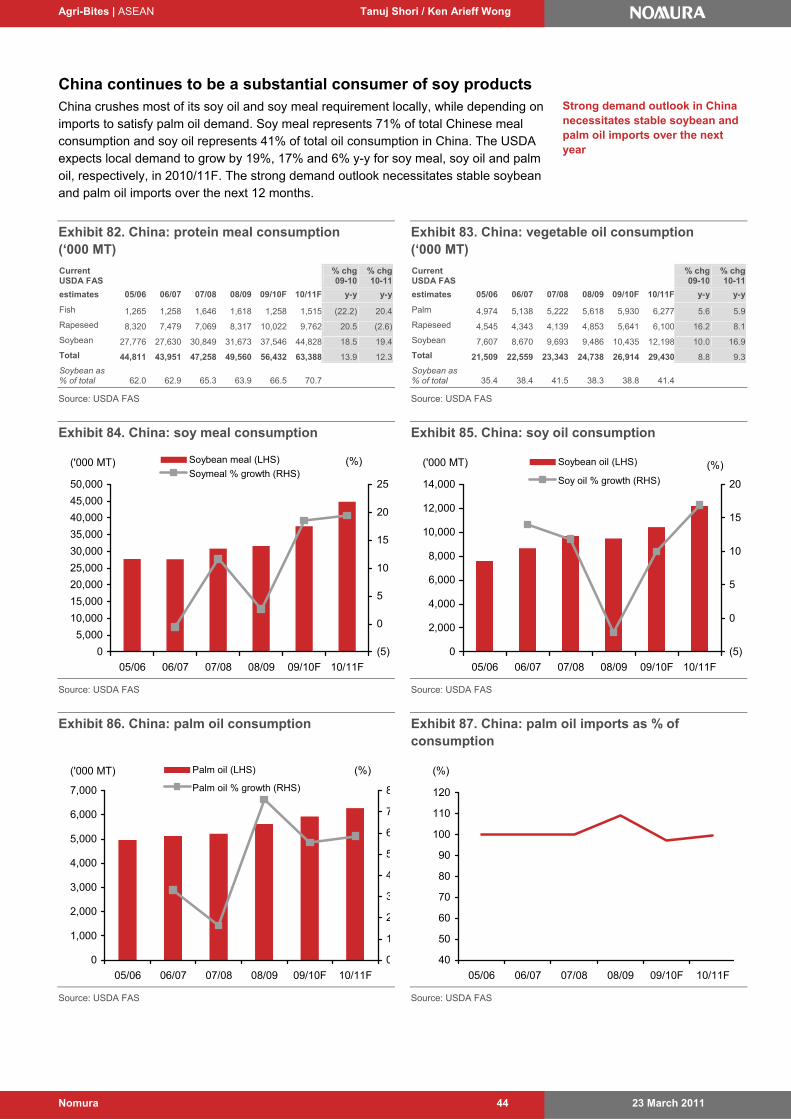

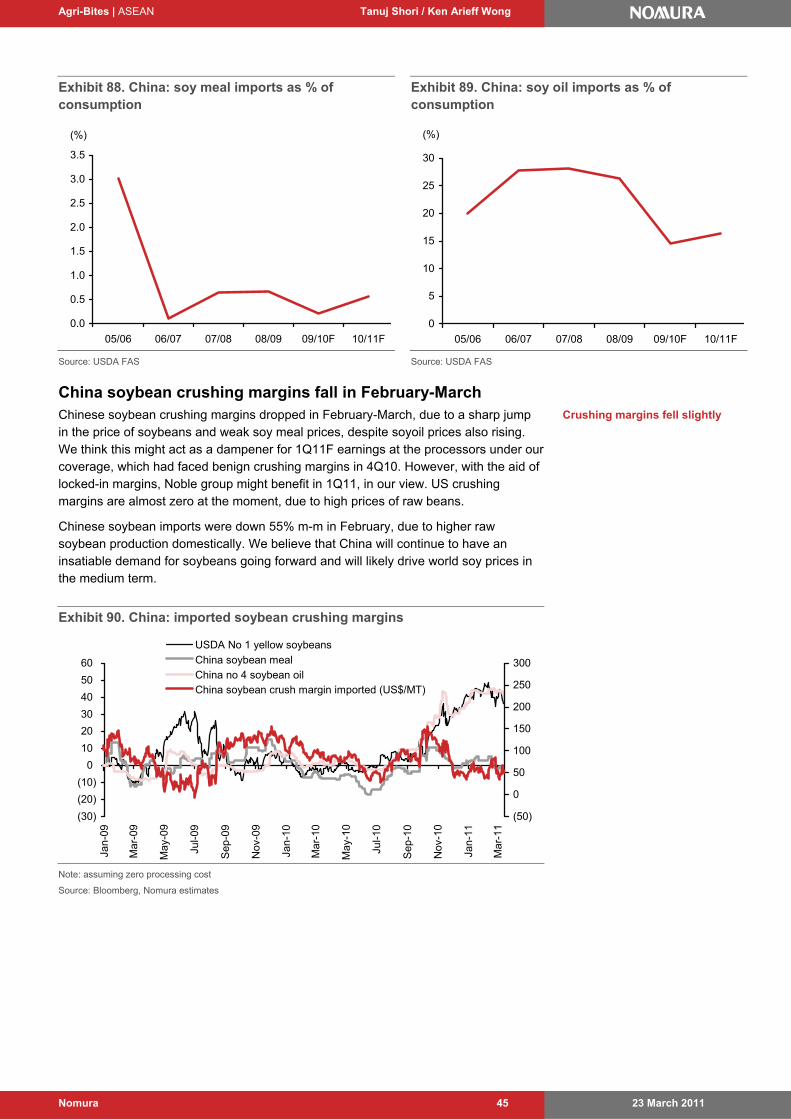

Soybean, soy meal and soy oil 39 USDA forecasts improving soybean supply in 2010/11F, consumption to rise more 39 World protein meal supply to grow in tandem with disappearance; vegetable oil disappearance to outpace supply growth 40 World soybean production to fall slightly in 2010/11F 41 Brazil and US to capture share of Argentine soybean exports in 2010/11F 42 Soybean consumption to grow at 8.1% in 2010/11F; same as 09/10F 42 China continues to be a substantial consumer of soy products 44 China soybean crushing margins fall in February-March 45

Sugar 47 ISO further cuts sugar surplus forecast for 2010/11F on Australian floods and China weather 47 Thai sugar export volume and price up in Jan-11 47 World sugar prices fell m-m in March 2011 due to expected sugar surplus from India 48

Grains — rice, wheat and corn 49 Grain stock usage ratios to tighten in for wheat and corn while improving for rice in 2010/11F 49 World rice price continues to be weak y-y and m-m in Mar-11 50 Thai rice export volume up in Jan 11 51 Wheat exports in major producing regions to drop in 2009/10F and 2010/11F 51 US corn production to fall, but offset by gains in China 52

Rubber 53 Global natural rubber to grow 4.6% in 2011F and 3.8% in 2012F 53 Thai rubber export volume down but export price up in Jan 11 53 Future rubber price down m-m on worry about car industry in China and the impact from the earthquake in Japan 53

Appendix 1: crop calendar 55

Appendix 2: monthly weather update 56

Valuation methodologies 57 Risks to our investment view 58

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 4

Nomura ASEAN Soft Commodity Team

Tanuj SHORI ASEAN Commodity Supply Chain +65 6433 6981 [email protected]

Ken Arieff WONG ASEAN Plantations +60 3 2027 6895 [email protected]

Ploenjai JIRAJARUS Capital Nomura Securities +662 638 5772 [email protected]

Tushar MOHATA +91 22 6723 4042 [email protected]

Vishnuvardana REDDY +91 22 3053 2847 [email protected]

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 5

What’s in this issue of our Agri-Bites

The great buying fair After a strong 2H10, we have so far seen a weak 2011, with agri-commodity prices and stocks both having corrected considerably year to date. Amongst soft-commodities, tea, wheat, rubber and sugar have seen the worst falls in thus far in 2011, whereas a very few — like cotton and cocoa — have bucked the trend and are up year to date.

Exhibit 1. Commodity performance – YTD 2011

(30)

(20)

(10)

0

10

20

30

40

Tea

US

Whe

at

Rub

ber

Su

gar

US

Ric

e

US

Soy

Mea

l

Mal

aysi

aC

PO

US

Soy

bean

Can

ola

Oil

Ref

ined

Pa

lm O

ilU

SS

oybe

anO

ilC

hina

Soy

Mea

l

Tha

iland

Ric

eC

hina

Rap

esee

dO

il

Alm

onds

Chi

naS

oybe

anO

il Cor

n

Chi

naS

oybe

an

Su

nflo

wer

Oil

Coc

oa

Cot

ton

(%)

Source: Bloomberg

This has been in contrast to the gains seen in hard commodities such as crude oil and coal. We see this divergence stemming from two things:

Withdrawal of speculative funds from agri-commodities, as risk appetite deflates

Fears of a demand slowdown for agri-commodities from MENA countries (geo-political concerns), as well as impact from the recent events in Japan.

Hard commodities on the other hand have seen a revival in prices stemming from fears of supply disruption (mainly for crude oil).

To an extent, we find the withdrawal of speculative funds unsurprising (we have acknowledged the increasing amount of long positions in our past notes), and we think that agri-prices could stabilise at current levels for the near term assuming that there are no new major developments from a global supply/demand perspective.

The good part in our view is, global agri-demand is relatively inelastic, and any concerns on demand are usually more infrastructure driven — eg, trade and ports cut-off (bottlenecks).

Positive catalysts for agri-commodities:

Stability leading to improved sentiment and demand outlook for agri-commodities.

Continued strength in crude oil prices supporting biofuel demand in the US.

Spring planting intentions which could spur prices further in the fight for acreage.

Negative catalysts for agri-commodities:

Further geopolitical concerns damaging sentiment and global demand outlook.

Withdrawal of ‘Quantitative Easing II’ liquidity in the US (likely by end-June 2011) driving prices lower

Stronger production in 2H11 of palm oil, as well as higher-than-expected planting intentions for a specific crop (eg, soybeans).

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 6

In line with commodities, equities have underperformed as well… In-line with weak commodity performance in 2011, equities have been weak since the beginning of the year, as well. However, a key difference in our view is that equities never had re-rated as strongly as commodities had in the first place. Indeed, almost all of the stocks under our coverage — from Singapore midstream names (down 10% ytd vs index down 8%) to upstream planters (Malaysian names down 1% vs index down 1%, Indonesian names down 18% vs index down 6%) — are down ytd. (Please see page 26 for a list of stock P/Es.)

Exhibit 2. Sectoral performance YTD

(30)

(25)

(20)

(15)

(10)

(5)

0

5

10

1-J

an

8-J

an

15-J

an

22-J

an

29-J

an

5-F

eb

12-F

eb

19-F

eb

26-F

eb

5-M

ar

12-M

ar

Singapore Commodity SCM Malaysian Planters

Indonesian Planters Indian Agri

Thai Agri

(%)

Source: Bloomberg

Exhibit 3. Soft commodity stocks: recent performance

Company Closing price 7-month high High attained on

Fall from highs (%)

Target Price Upside (%) EPS CAGR (CY10-12F)

(%)

P/E (CY11F)

P/E (CY12F)

Wilmar 5.02 6.88 9-Nov-10 (27.0) 5.60 11.6 22.0 17.2 14.9

Noble 2.04 2.34 16-Jan-11 (12.8) 2.80 37.3 26.6 13.7 11.9

Olam 2.58 3.38 9-Nov-10 (23.7) 3.90 51.2 20.2 16.5 13.9

Mewah 0.87 1.20 18-Jan-11 (27.5) 1.34 54.0 6.5 9.5 8.1

Sime Darby 9.01 9.46 4-Jan-11 (4.8) 12.15 34.9 40.6 14.4 12.9

IOI 5.78 6.05 4-Jan-11 (4.5) 7.00 21.1 17.3 16.0 14.2

KLK 20.64 22.86 20-Jan-11 (9.7) 25.50 23.5 24.5 15.4 12.9

Genting Plant 8.00 9.03 4-Jan-11 (11.4) 10.50 31.3 23.9 13.7 12.2

Golden Agri 0.64 0.82 3-Jan-11 (22.0) 0.90 40.6 28.1 11.0 9.9

Indo Agri 2.12 2.95 4-Jan-11 (28.1) 3.40 60.4 36.7 10.0 9.3

London Sumatra 2,225 2,570 2-Jan-11 (13.4) 3,040 36.6 26.8 11.2 10.5

Astra Agro 22,100 27,100 9-Dec-10 (18.5) 28,400 28.5 33.0 12.4 11.0

Note: As on 18-March-2011

Source: Bloomberg, Nomura estimates

CPO price has corrected 14% from its peak, but equities punished further – unwarranted in our view Palm oil prices have corrected by 14.2% from the recent peak of RM3,930/tonne in mid-February. This withdrawal coincided largely with weakness seen in other agri-commodities, including vegetable oils (soy), oilseeds and meals, grains and rubber.

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 7

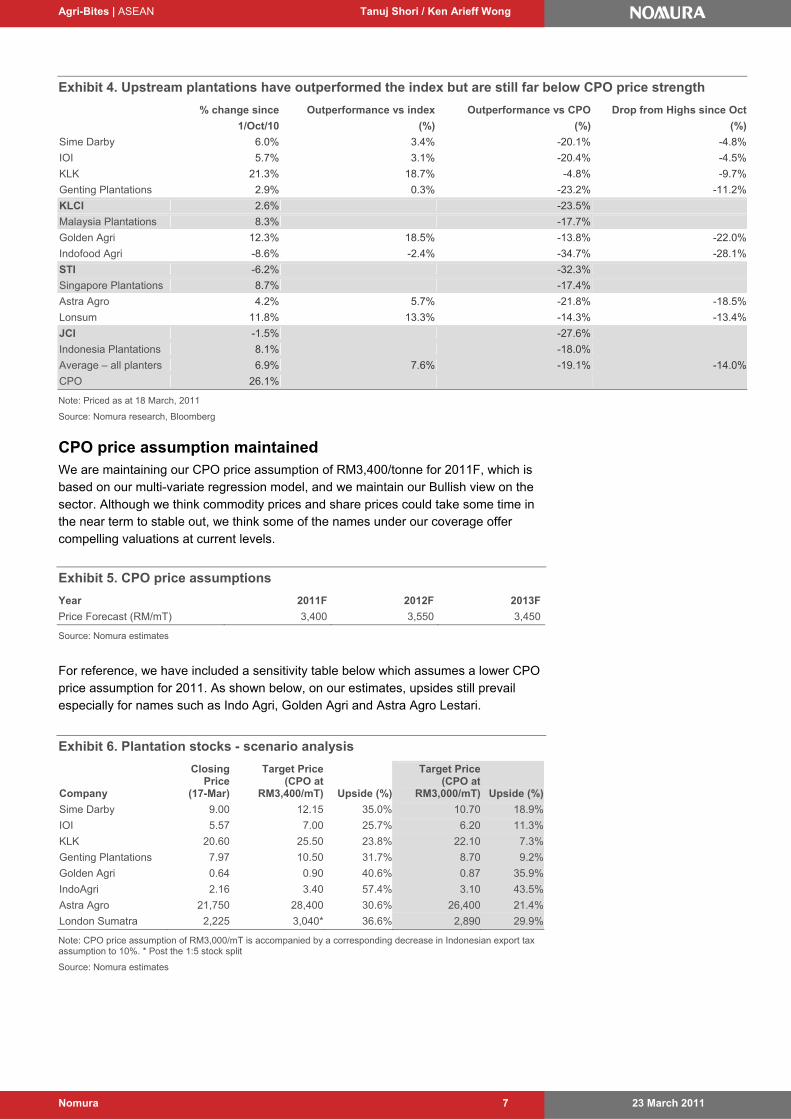

Exhibit 4. Upstream plantations have outperformed the index but are still far below CPO price strength

% change since Outperformance vs index Outperformance vs CPO Drop from Highs since Oct

1/Oct/10 (%) (%) (%)

Sime Darby 6.0% 3.4% -20.1% -4.8%

IOI 5.7% 3.1% -20.4% -4.5%

KLK 21.3% 18.7% -4.8% -9.7%

Genting Plantations 2.9% 0.3% -23.2% -11.2%

KLCI 2.6% -23.5%

Malaysia Plantations 8.3% -17.7%

Golden Agri 12.3% 18.5% -13.8% -22.0%

Indofood Agri -8.6% -2.4% -34.7% -28.1%

STI -6.2% -32.3%

Singapore Plantations 8.7% -17.4%

Astra Agro 4.2% 5.7% -21.8% -18.5%

Lonsum 11.8% 13.3% -14.3% -13.4%

JCI -1.5% -27.6%

Indonesia Plantations 8.1% -18.0%

Average – all planters 6.9% 7.6% -19.1% -14.0%

CPO 26.1% Note: Priced as at 18 March, 2011

Source: Nomura research, Bloomberg

CPO price assumption maintained We are maintaining our CPO price assumption of RM3,400/tonne for 2011F, which is based on our multi-variate regression model, and we maintain our Bullish view on the sector. Although we think commodity prices and share prices could take some time in the near term to stable out, we think some of the names under our coverage offer compelling valuations at current levels.

Exhibit 5. CPO price assumptions

Year 2011F 2012F 2013F

Price Forecast (RM/mT) 3,400 3,550 3,450

Source: Nomura estimates

For reference, we have included a sensitivity table below which assumes a lower CPO price assumption for 2011. As shown below, on our estimates, upsides still prevail especially for names such as Indo Agri, Golden Agri and Astra Agro Lestari.

Exhibit 6. Plantation stocks - scenario analysis

Company

Closing Price

(17-Mar)

Target Price (CPO at

RM3,400/mT) Upside (%)

Target Price (CPO at

RM3,000/mT) Upside (%)

Sime Darby 9.00 12.15 35.0% 10.70 18.9%

IOI 5.57 7.00 25.7% 6.20 11.3%

KLK 20.60 25.50 23.8% 22.10 7.3%

Genting Plantations 7.97 10.50 31.7% 8.70 9.2%

Golden Agri 0.64 0.90 40.6% 0.87 35.9%

IndoAgri 2.16 3.40 57.4% 3.10 43.5%

Astra Agro 21,750 28,400 30.6% 26,400 21.4%

London Sumatra 2,225 3,040* 36.6% 2,890 29.9%

Note: CPO price assumption of RM3,000/mT is accompanied by a corresponding decrease in Indonesian export tax assumption to 10%. * Post the 1:5 stock split

Source: Nomura estimates

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 8

CPO discount to soybean oil comes off, lending some comfort Following the recent correction in the CPO price, the CPO price discount to soy oil has widened to around ~10% from previous tightness of ~5%. This, we think, leaves some room for CPO prices to stabilise (and possibly trend upwards slightly), as palm oil should be able to maintain its price competitiveness.

Exhibit 7. CPO price widens discount to 10-15% vs soybean oil and rapeseed

-25%

-20%

-15%

-10%

-5%

0%

1-J

an-1

0

22-J

an-1

0

12-F

eb-1

0

5-M

ar-1

0

26-M

ar-1

0

16-A

pr-1

0

7-M

ay-1

0

28-M

ay-1

0

18-J

un-1

0

9-Ju

l-10

30-J

ul-1

0

20-A

ug-1

0

10-S

ep-1

0

1-O

ct-1

0

22-O

ct-1

0

12-N

ov-1

0

3-D

ec-1

0

24-D

ec-1

0

14-J

an-1

1

4-F

eb-1

1

25-F

eb-1

1

18-M

ar-1

1

Palm Oil Disc to Rape Oil Palm Oil Disc to Soy Oil

Source: Bloomberg

All eyes on US spring planting season; USDA expects little change in hectarage for soybean, with most gains in to be made in corn and wheat The U.S. Department of Agriculture (USDA) recently disclosed its expectations for acreage (USDA forecasts – not based on a survey). The winners this time around according the results will likely be corn (+4% y-y) to 92mn acres and wheat at 57mn acres (+6% y-y), although soybean acreage looks to remain unchanged at 78mn acres (+1%). This is mostly driven by current soybean prices, which are lower than corn and wheat, and therefore less attractive for planters to plant. The much-anticipated Planting Intentions Survey result will be released on 31 March and will provide a more accurate picture on the plantings expectations for the coming season.

Additionally, in its 2011 Agri Outlook, the USDA believes that the three main factors shaping 2011 will be tight supplies of corn and soybeans, the small supply cushion for corn and soybeans in the event of adverse weather and the expected strong exports of corn, wheat and soybean.

We think that as long as other crops such as wheat, corn and cotton maintain their price strength, soybean should maintain its current strength – supportive of global vegetable oils, including palm oil.

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 9

Exhibit 8. USDA: Acreage forecast

79.2 78.3 93.5 86.0 86.5 88.2 92.0

64.2 75.5 64.7 75.7 77.5 77.4 78.0

75.1 57.3 60.5 63.2 59.2 53.6 57.0

42.3 32.3 29.1 28.2 25.9 26.0 28.1

34.536.0 36.8 34.6 33.7 31.4 31.9

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

1996 …. 2006 2007 2008 2009 2010 2011F

Corn Soybeans Wheat Other Feed Grains, Rice & Cotton CRP(mn acre)

Source: USDA Agricultural Outlook Forum

Exhibit 9. Soy-corn ratio (below average)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Sep

-98

Sep

-99

Sep

-00

Sep

-01

Sep

-02

Sep

-03

Sep

-04

Sep

-05

Sep

-06

Sep

-07

Sep

-08

Sep

-09

Sep

-10

Soy to corn ratio Average=2.65

Source: Nomura, Bloomberg

Exhibit 10. Soy-cotton ratio (below average)

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

Sep

-98

Sep

-99

Sep

-00

Sep

-01

Sep

-02

Sep

-03

Sep

-04

Sep

-05

Sep

-06

Sep

-07

Sep

-08

Sep

-09

Sep

-10

Soy to cotton ratio Average=0.22

Source: Nomura, Bloomberg

Impact of Japanese earthquake on agri-commodities We think the recent earthquake and tsunami in Japan could have a meaningful impact on the world trade and prices of various agri-commodities. The situation is currently unfolding, and it is uncertain how much of the port capacity or agricultural land has been affected. However any prolonged disruption to trade flow / agricultural production in Japan could impact prices, in our view. Japan is predominantly an importer and a net consumer of soft commodities. In our view, the commodities most likely to face downward pressure in prices given import delays might be corn, rapeseed, cottonseed and soymeal, given Japan’s large share of world imports in these commodities. However, we also flag that since this questions supply of food, disruption, if any, should be minimal, in our view.

Regarding supplies, the most obvious impact would be on rice, given that one of the biggest agricultural products in Japan is rice. Estimates for crop damage to rice have varied, with some estimates (USDA economists) saying the impacted area accounts for 6-10% of rice production in Japan with others putting estimates as high as 26%. Plantings for rice take place end of April to late June, with harvesting in September. This leads us to believe any impact will likely be seen in the next planting/harvesting season – and more from salt water poisoning (as rice is not as tolerant as wheat and barley to salt).

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 10

Exhibit 11. Japan as % of world commodities supply demand

Production Imports Exports Consumption

Grains

Rice, Milled 1.7 2.4 0.7 1.9

Wheat 0.1 4.1 0.2 0.9

Corn n.m. 17.8 n.m. 2.0

Oilseeds

Oilseed, Copra n.m. n.m. n.m. n.m.

Oilseed, Cottonseed n.m. 20.1 n.m. 0.3

Oilseed, Peanut 0.1 5.7 n.m. 0.4

Oilseed, Rapeseed n.m. 21.5 n.m. 3.8

Oilseed, Soybean 0.1 3.9 n.m. 1.6

Protein Meals

Meal, Copra n.m. 2.4 n.m. 1.0

Meal Cottonseed 0.1 1.5 n.m. 0.1

Meal,Fish 7.1 12.4 0.3 13.0

Meal,Peanut n.m. n.m. n.m. n.m.

Meal, Rapeseed 3.8 1.6 n.m. 3.9

Meal,Soybean 1.2 4.0 n.m. 2.5

Vegetable oils

Oil,Coconut n.m. 2.2 n.m. 1.3

Oil, Cottonseed 0.1 4.2 n.m. 0.2

Oil, Palm n.m. 1.7 n.m. 1.3

Oil, Palm Kernel n.m. 3.4 n.m. 1.6

Oil, Peanut n.m. 0.6 n.m. n.m.

Oil, Rapeseed 4.0 0.3 n.m. 4.1

Oil, Soybean 1.2 0.3 n.m. 1.3

Oil, Sunflowerseed n.m. 0.8 n.m. 0.3

Others

Coffee, Green n.m. 7.4 n.m. 5.7

Cotton n.m. 0.8 n.m. 0.3

Sugar, Centrifugal 0.7 3.1 n.m. n.m.

Note: 2009/10 crop year. n.m. implies very low or not meaningful

Source: USDA FAS

Long positions of “managed money” in soy oil futures withdraws as risk appetite withdraws Based on our review of CFTC data, US CBOT soy oil futures held by managed money (eg, portfolio funds and not hedgers and traders) have fallen 22% from their peak – close to early-October levels. This was in line with the overall weakness in commodities, as risk appetite declined with geopolitical concerns and fears of slower global demand stemming from Japan’s natural disasters.

Though we actually find it comforting that some speculative liquidity has left the market, we still think the risk remains whereby commodity prices could recede very quickly with a turn in sentiment. In the near term, we think that liquidity should remain supported so long as QE II liquidity remains intact (ie, to last through 1H11) and fundamentals for the sector (which in the case of palm oil are currently driven by tight supplies) remain supportive.

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 11

Exhibit 12. CFTC data – Increasing managed money positions demonstrate speculation declining

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,0005

-Jan

-10

19-J

an-1

02

-Feb

-10

16-F

eb-1

02

-Mar

-10

16-M

ar-1

030

-Mar

-10

13-A

pr-1

027

-Apr

-10

11-M

ay-1

025

-May

-10

8-J

un-1

022

-Jun

-10

6-Ju

l-10

20-

Jul-1

03

-Aug

-10

17-A

ug-1

031

-Aug

-10

14-S

ep-1

028

-Sep

-10

12-O

ct-1

026

-Oct

-10

9-N

ov-1

023

-Nov

-10

7-D

ec-1

021

-Dec

-10

4-J

an-1

118

-Jan

-11

1-F

eb-1

115

-Feb

-11

1-M

ar-1

1

30

35

40

45

50

55

60

65Managed Money Long Positions (LHS)

Managed Money Short Positions (LHS)

CBOT Soy Oil Prices (RHS)

Source: Commodity Futures Trading Commission

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 12

Our stock calls

Stocks: what we like and what we don’t This section summarises our stock action points for the month.

Upstream planters severely punished – offer ‘deep value’ We still believe that CPO prices will be supported at least through 1H11 and believe that the market has taken too negative a view on CPO upstream plays – having punished names like IndoAgri and Golden Agri, down 22-27% from the peaks. Revisiting our CPO price assumption, even at an assumption of RM3,000/tonne (below consensus view of RM3,100/tonne (based on a Reuters published poll), these names offer good value and upside.

BUY London Sumatra, Indo Agri and Golden Agri, after the recent sell-down. Sensitivities show that they are still compelling BUYs, even with a lower CPO price assumption of RM3,000/tonne. We also like Sime Darby on a positive outlook for all its divisions (apart from oil & gas). We like IndoFood Agri for its strong CPO production growth, coupled with higher leverage to CPO prices (being purer plantation plays), while London Sumatra offers good leverage to CPO prices, as well as exposure to the Indonesian market (where our strategist Wilianto Ie is positive) at compelling valuations (cheapest within our upstream palm oil coverage). Golden Agri is the most liquid CPO name in our coverage, with pure leverage to CPO prices. Sime Darby, in our view, also offers a strong re-rating story given its recent lag (relative to CPO price strength), while low-hanging fruit presents potentially easy wins in terms of earnings upside. Further, Sime Darby’s large market weighting and high liquidity could increasingly be used as a proxy for improving sentiment on Malaysia, especially given a relatively low foreign shareholding of ~15%.

Midstream: we continue to like Noble, Olam and Mewah, but are cautious on Wilmar Noble: Among the midstream space, we like Noble, as we think that the current commodity price upcycle, along with strong performance in agri, energy and locked margins in FY11F should ensure a good FY11 for the company. The company also stands to benefit from high coal prices due to Australian floods, as its mines in NSW are relatively insulated from the floods. It should also be a net beneficiary of any rising coal prices due to higher Japanese demand post the earthquake.

We like Olam, as its asset strategy continues to surprise positively and it is trading at extremely attractive valuations post the recent correction on export incentives. Its recent investments in Africa, such as the Gabon fertiliser project and the sugar refinery in Nigeria, if executed well, could act as a substantial boost to the bottom line, in our view. In its recent NDR with us, Olam reiterated the recent uptick in its growth guidance helped by faster-than-expected contributions of various assets, such as almonds, tomato processing and wheat milling. Moreover, NZFSU and PureCircle can turn around in ~2 years, according to management, which could present potential upside surprise.

Although we think there is inherent dilution risk (to fund expansion), we believe the recent correction is overdone and presents buying opportunity. It is now trading at 16.5x CY11 P/E, de-rating from peak of ~21x CY1 P/E, and at all-time low discounting the time during financial crisis

However, we remain NEUTRAL on Wilmar, as we expect a shrinking valuation premium due to non-core investments in property and weak earnings to continue in 1QFY11. We think that the stock should remain rangebound in the near term on the back of a lack of catalysts. During our recent marketing, we saw a great deal of interest in the stock at current levels, with investors getting positive vibes from recent insider buying.

BUY Indo Agri, Golden Agri and LonSum for good leverage to CPO prices; we also have a BUY on Sime Darby on possible restructuring improvements

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 13

We also like recently cited Mewah for its leadership in West Africa pack oil, scale in palm refining, cheap valuation compared to peers and likely high capex intensity post listing, but low liquidity remains a concern.

We also like Indian edible oil players – Ruchi Soya and KS Oils We also like Indian edible oil players Ruchi Soya and KS Oils and think that they will benefit from the rising per capita edible oil consumption in India, a larger percentage of branded sales, increasing capacity utilisation through incremental consolidation in the industry, greater economies of scale and upstream participation. We shift our preference to Ruchi Soya as a strong soybean crop in 4Q CY10–1Q CY11 will likely boost the company’s margins and volume, resulting in a positive earnings surprise, in our view.

Thai Food & Agri: CNS prefers food processors CPF and GFPT on global demand for high-quality processed foods and benefit from soft commodity price drop Regarding Thai agricultural and food companies, Capital Nomura Securities analyst Ploenjai Jirajarus maintains a Neutral rating for the sector. She this month prefers food processors with high-quality products — names like CPF and GFPT. The tense politic situation in the Middle East, high crude price and the Japan earthquake have given rise to worries of global economic uncertainty and therefore, led to a fall in soft commodity price. Thus, CNS’ analyst prefers CPF and GFPT because they are beneficiaries of rising demand for high-quality processed foods for export. Moreover, a slowdown in soft commodities — eg, soybean and corn — will also lower feed costs.

CNS feels that CPF and GFPT are likely to see upward revision in consensus earnings estimates thanks to higher-than-expected demand for processed chicken products exported to Japan and the Middle East. Moreover, the slowdown in global soybean price should ease their feed costs.

CNS also likes TVO as because expected rising export volume for processed chicken products will increase demand for Thailand animal farming and feed mills, and TVO should then be able to sell more soybean meal as a result. Although a fall in soybean and soybean meal prices might be negative to TVO, CNS believes rising demand for both soybean meal and soybean oil will raise production utilisation and, therefore, reduce fix cost per unit.

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 14

Other data points for the month

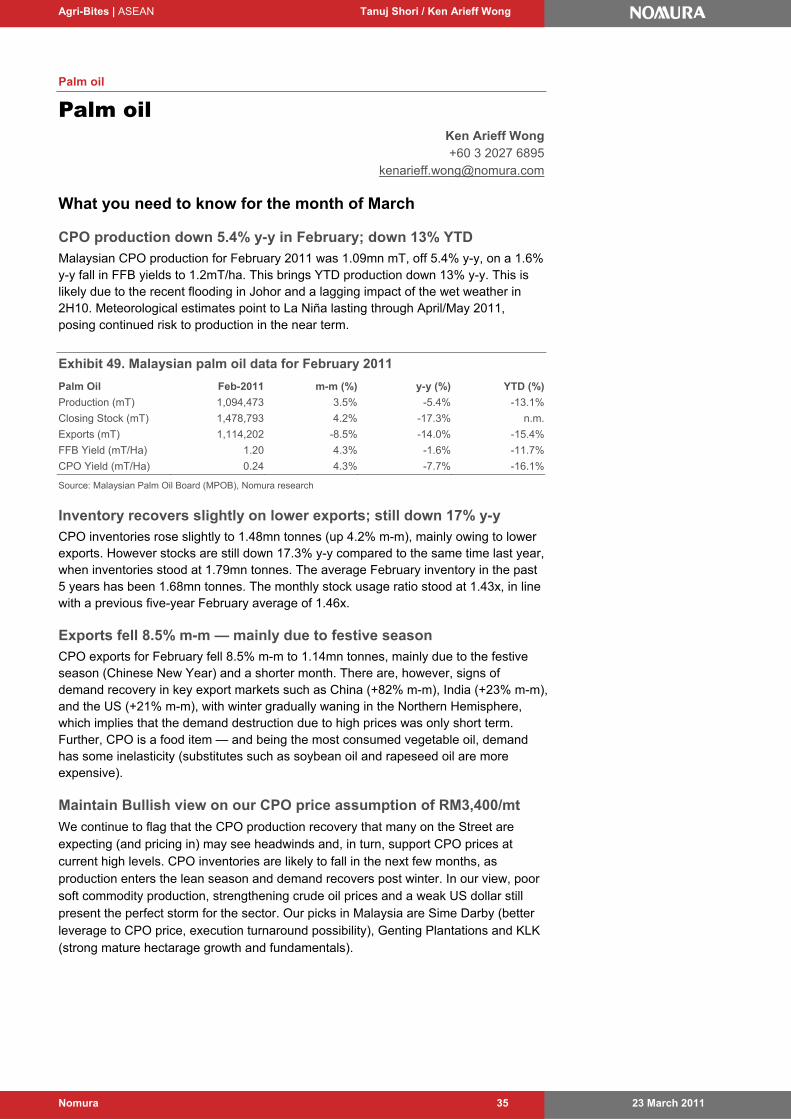

Other data points for the month Malaysian February palm oil data — production and exports down, prices fairly reflect inventory levels Malaysian CPO production for the month saw the lowest February reading in the last three years at 1.09mn mT (-5% y-y), though exports fell a sharper 8.5% m-m, partly on the back of the shorter month in February and festive holidays. This brought inventories to 1.5mn tonnes, closer to 2007 levels.

We continue to flag that the CPO production recovery that many people on the Street are expecting (and pricing in) may see headwinds, in our view, and in turn, support CPO prices at current high levels. CPO inventories are likely to fall in the next few months, we believe, as production enters the lean season and demand recovers post winter. In our view, poor soft commodity production, strengthening crude oil prices and a weak US dollar continue to create the perfect storm for the sector.

Exhibit 13. Malaysian palm oil data for February 2011

Palm Oil Feb-2011 m-m (%) y-y (%) YTD (%)

Production (mT) 1,094,473 3.5% -5.4% -13.1%

Closing Stock (mT) 1,478,793 4.2% -17.3% n.m.

Exports (mT) 1,114,202 -8.5% -14.0% -15.4%

FFB Yield (mT/Ha) 1.20 4.3% -1.6% -11.7%

CPO Yield (mT/Ha) 0.24 4.3% -7.7% -16.1%

Source: Malaysian Palm Oil Board (MPOB), Nomura research

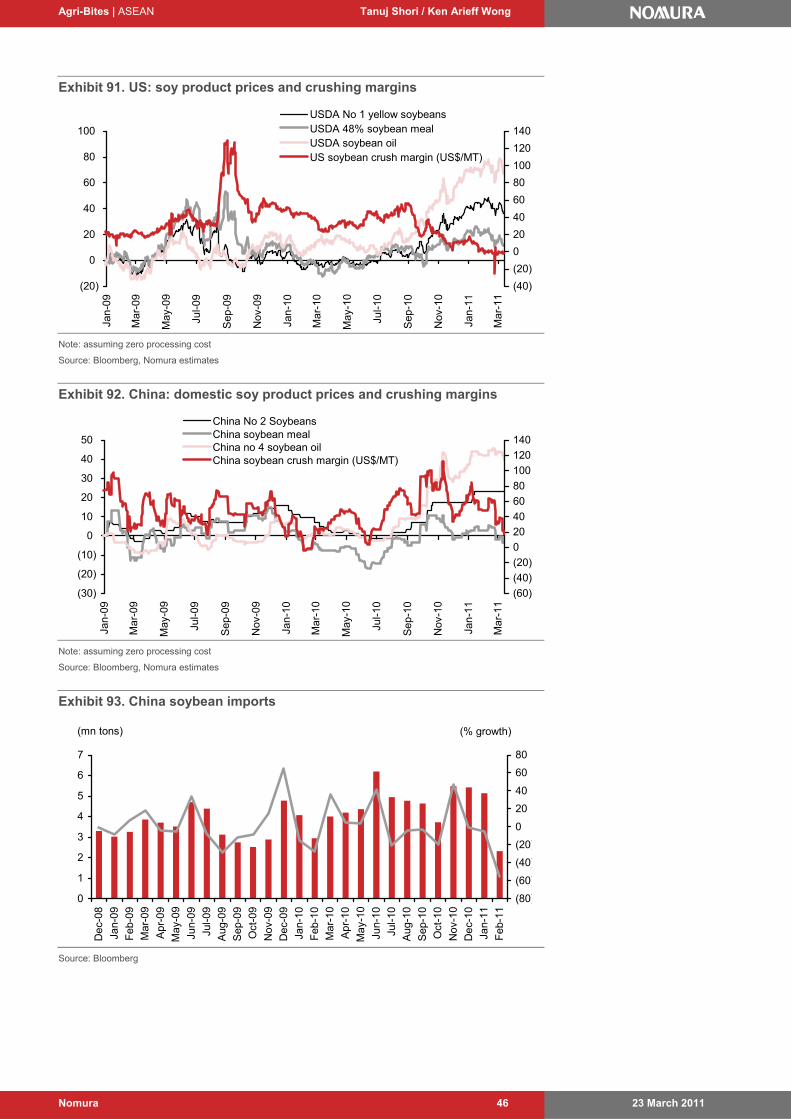

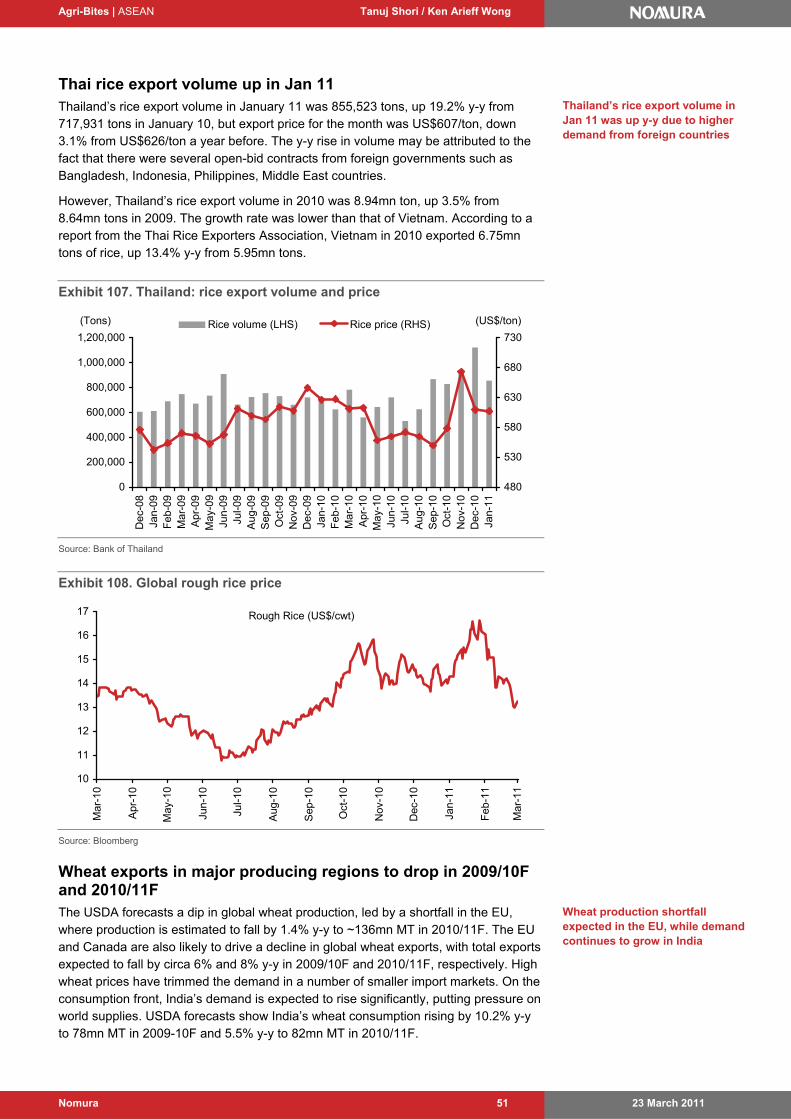

China soybean crushing margins fell in February, US margins almost at parity Chinese soybean crushing margins dropped in February-March due to a sharp jump in the price of soybeans and weak soymeal prices, despite soyoil prices also rising. We think this might act as a dampener for 1Q11F earnings at the processors under our coverage, which had faced benign crushing margins in 4Q10. However, with the aid of locked-in margins, Noble group might benefit in 1Q11, in our view. US crushing margins are almost zero at the moment, due to high prices of raw beans.

Chinese soybean imports were down 55% m-m in February, due to higher raw soybean production domestically. We believe that China will continue to have an insatiable demand for soybeans going forward and will likely drive world soy prices in the medium term.

Exhibit 14. Soybean crushing margins

(40)(20)

020406080

100120140160180

Jun

-09

Jul-0

9

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Jan

-10

Feb

-10

Ma

r-10

Apr

-10

May

-10

Jun

-10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Jan

-11

Feb

-11

Ma

r-11

US soybean crush margin (US$/MT)

China soybean crush margin (US$/MT)

China soybean crush margin imported (US$/MT)

Note: Assuming zero processing cost; Source: Bloomberg, Nomura estimates

Crushing margins fell slightly

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 15

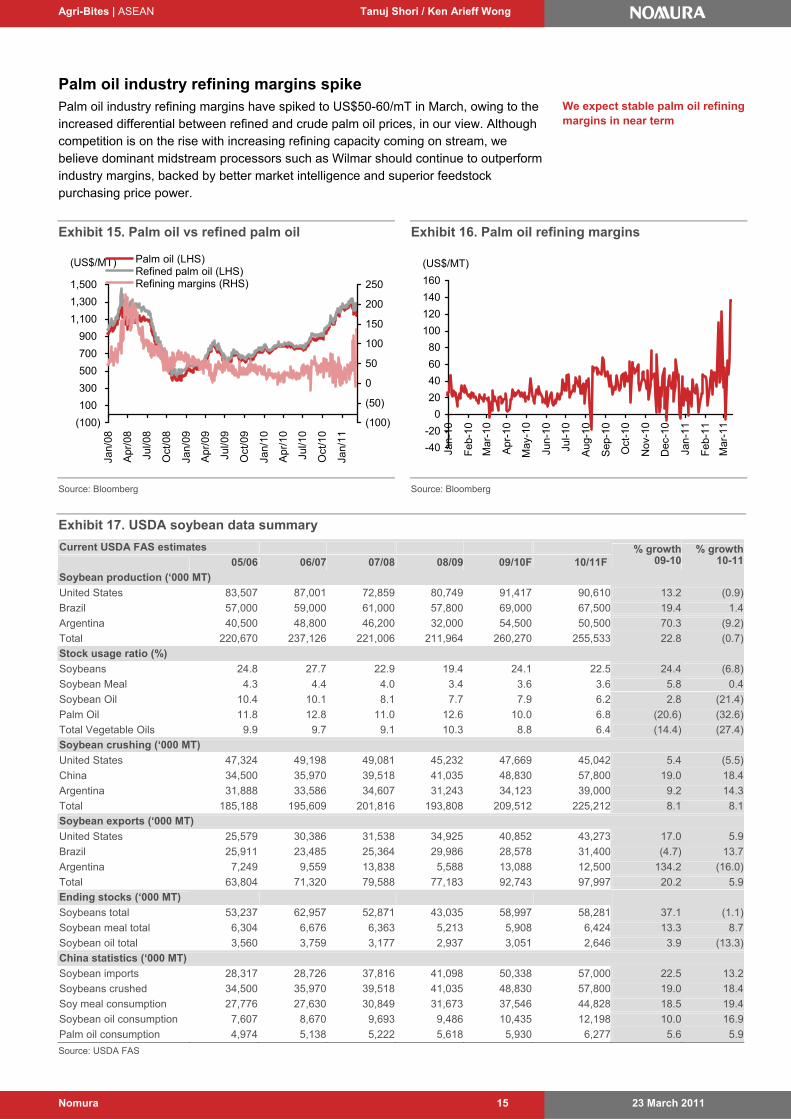

Palm oil industry refining margins spike Palm oil industry refining margins have spiked to US$50-60/mT in March, owing to the increased differential between refined and crude palm oil prices, in our view. Although competition is on the rise with increasing refining capacity coming on stream, we believe dominant midstream processors such as Wilmar should continue to outperform industry margins, backed by better market intelligence and superior feedstock purchasing price power.

Exhibit 15. Palm oil vs refined palm oil

(100)

100

300

500

700

900

1,100

1,300

1,500

Jan/

08

Apr

/08

Jul/0

8

Oct

/08

Jan/

09

Apr

/09

Jul/0

9

Oct

/09

Jan/

10

Apr

/10

Jul/1

0

Oct

/10

Jan/

11

(US$/MT)

(100)

(50)

0

50

100

150

200

250

Palm oil (LHS)Refined palm oil (LHS)Refining margins (RHS)

Source: Bloomberg

Exhibit 16. Palm oil refining margins

-40

-20

0

20

40

60

80

100

120

140

160

Jan-

10

Feb

-10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

(US$/MT)

Source: Bloomberg

Exhibit 17. USDA soybean data summary

Current USDA FAS estimates

05/06 06/07 07/08 08/09 09/10F 10/11F % growth

09-10% growth

10-11

Soybean production (‘000 MT)

United States 83,507 87,001 72,859 80,749 91,417 90,610 13.2 (0.9)

Brazil 57,000 59,000 61,000 57,800 69,000 67,500 19.4 1.4

Argentina 40,500 48,800 46,200 32,000 54,500 50,500 70.3 (9.2)

Total 220,670 237,126 221,006 211,964 260,270 255,533 22.8 (0.7)

Stock usage ratio (%)

Soybeans 24.8 27.7 22.9 19.4 24.1 22.5 24.4 (6.8)

Soybean Meal 4.3 4.4 4.0 3.4 3.6 3.6 5.8 0.4

Soybean Oil 10.4 10.1 8.1 7.7 7.9 6.2 2.8 (21.4)

Palm Oil 11.8 12.8 11.0 12.6 10.0 6.8 (20.6) (32.6)

Total Vegetable Oils 9.9 9.7 9.1 10.3 8.8 6.4 (14.4) (27.4)

Soybean crushing (‘000 MT)

United States 47,324 49,198 49,081 45,232 47,669 45,042 5.4 (5.5)

China 34,500 35,970 39,518 41,035 48,830 57,800 19.0 18.4

Argentina 31,888 33,586 34,607 31,243 34,123 39,000 9.2 14.3

Total 185,188 195,609 201,816 193,808 209,512 225,212 8.1 8.1

Soybean exports (‘000 MT)

United States 25,579 30,386 31,538 34,925 40,852 43,273 17.0 5.9

Brazil 25,911 23,485 25,364 29,986 28,578 31,400 (4.7) 13.7

Argentina 7,249 9,559 13,838 5,588 13,088 12,500 134.2 (16.0)

Total 63,804 71,320 79,588 77,183 92,743 97,997 20.2 5.9

Ending stocks (‘000 MT)

Soybeans total 53,237 62,957 52,871 43,035 58,997 58,281 37.1 (1.1)

Soybean meal total 6,304 6,676 6,363 5,213 5,908 6,424 13.3 8.7

Soybean oil total 3,560 3,759 3,177 2,937 3,051 2,646 3.9 (13.3)

China statistics (‘000 MT)

Soybean imports 28,317 28,726 37,816 41,098 50,338 57,000 22.5 13.2

Soybeans crushed 34,500 35,970 39,518 41,035 48,830 57,800 19.0 18.4

Soy meal consumption 27,776 27,630 30,849 31,673 37,546 44,828 18.5 19.4

Soybean oil consumption 7,607 8,670 9,693 9,486 10,435 12,198 10.0 16.9

Palm oil consumption 4,974 5,138 5,222 5,618 5,930 6,277 5.6 5.9

Source: USDA FAS

We expect stable palm oil refining margins in near term

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 16

Major news flow for the month

Exhibit 18. Major news flow

Noble Raises US$500mn in new equity

Noble Group raised US$500mn in new equity in a share placement, with CIC investing pro-rata stake. (Source: Company filing)

Nomura comment: We believe Noble’s intention to maintain investment-grade ratings has led to this capital raising, esp after recent sugar asset acquisitions. We continue to expect strong near-term performance led by a positive macro environment.

Sime Darby sued by Oil & Gas services company for US$178mn – Sime management says claim has 'no basis whatsoever in law'

The press reported that Sime is being sued by Emirates International Energy Services (EMAS) for ~US$178mn. EMAS (a consultant to Sime Darby Engineering–SDE) has accused SDE of backing out of project tenders to help other foreign companies win the tenders, and claims that it had lost expected revenues due to SDE’s withdrawals. (Source: The National, 14 Feb)

Nomura comment: Sime’s mgmt views EMAS’ claims as ‘baseless allegations,' according to the report. Based on our understanding, we do not think it warrants any provision for contingent liability.

Olam to Boost Financial Commodity Unit With ‘Half Dozen Funds’

Olam International Ltd., among the world’s three biggest suppliers of rice and cotton, plans to expand a pilot fund that invests in commodities more than fourfold and add about six new investment vehicles. Using its market knowledge as supplier of more than 20 raw materials, the Singapore-based trader will grow its Ektimo Commodity Relative Value Fund LP to $250 million from $60 million currently, Olam Chief Executive Officer Sunny Verghese said in an interview. “Tailor-made” commodity funds will follow, he said. (Source: Bloomberg)

Sime Hasn’t Signed Agreement to Invest in Oil Palm in Cameroon

Sime Darby Bhd. hasn’t signed any agreement to invest in an oil palm plantation in Cameroon, the Malaysian company said in a statement. “The company does from time to time explore investment opportunities relating to its core businesses as part of the continuous expansion plan of the group,” Sime said. (Source: Company filing)

Ruchi Group lines up $150mn for overseas expansion

In tune with Indian corporates looking abroad to source their raw material needs abroad, Indore-based Ruchi Group plans to grow oil palm in Cambodia. The group has signed a memorandum of understanding with Phnom Penh for this and, initially, oil palm will be cultivated in 20,000 hectares, a company official said. Ruchi Group plans a total investment of $150 million in the next three years to expand globally, while in the country, it plans to spend Rs 80-100 crore for expansion. In Ethiopia, Ruchi has cultivated soyabean on a pilot basis and the result has been good. It plans commercial cultivation of soyabean on 25,000 hectares there. During the pilot project, the yield was two tonnes a hectare. (Source: BusinessLine)

KLK drops plans to issue US$300mn bonds

KUALA Lumpur Kepong Bhd (KLK) has dropped plans to issue US$300 million (RM912 million) bonds based on the company's current financial condition. KLK feels it no longer requires the planned US$300 million, five-year unsecured guaranteed exchangeable bonds with an over- allotment option to increase the issue by US$100 million (RM304 million). (Source: Bloomberg).

Source: Various media reports, company announcements, Nomura research

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 17

Recap for the last month

Round-up of Feb-March 2011 Here we summarise key developments from last month.

Last month’s commodity price performance: negative Commodity price performance was generally negative over the past month, due to concerns over the impact of events in Japan and expectations of supply recovery capping prices. Prices of oils such as CPO (-14.1% m-m), refined palm oil (-11.1% m-m), US soybean (-10.6% m-m), US wheat (-26.6% m-m) and rubber (-25.2% m-m) were lower. We witnessed a secular downtick in commodity prices across the board. The S&P GSCI Agri Index was down 12.3% last month.

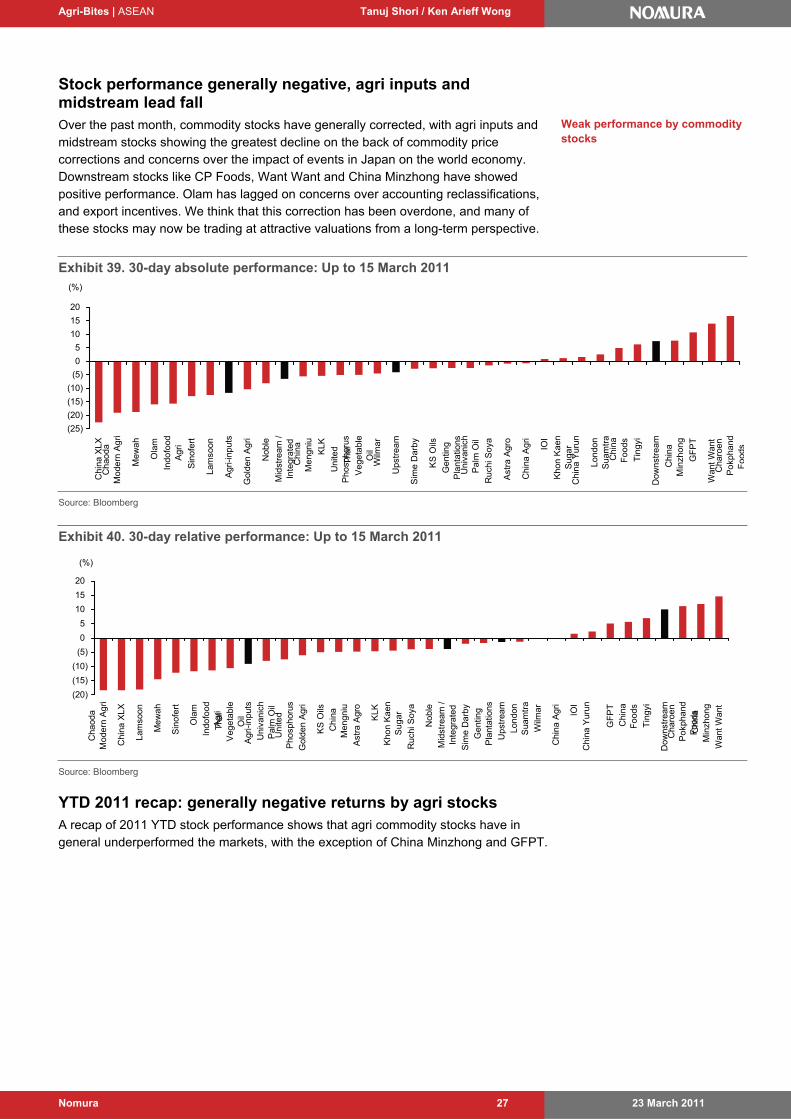

Stock performance generally negative, agri inputs and midstream lead fall Over the past month, commodity stocks have generally corrected, with agri inputs and midstream stocks showing the greatest fall, on the back of commodity price corrections and concerns on the impact of the Japanese earthquake on the world economy. Downstream stocks like CP Foods, Want Want and China Minzhong have showed positive performance. Olam has lagged on concerns over export incentives and accounting reclassifications. We think that this correction has been overdone, and many of these stocks may now be trading at attractive valuations from a long-term perspective.

Review of stock performance

Exhibit 19. Top- and bottom-five performers over last month

Top five Bottom five

Name Absolute (%) Relative (%) Name Absolute (%) Relative (%)

CP Foods 16.8 11.2 China XLX (22.6) (18.3)

Want Want 13.9 14.6 Chaoda Modern (19.0) (18.3)

GFPT 10.7 5.1 Mewah (18.7) (14.5)

China Minzhong 7.7 11.9 Olam (15.9) (11.7)

Tingyi 6.3 7.0 Indofood Agri (15.6) (11.3)

Source: Bloomberg, Nomura research

Consensus downgrades occur on price correction, profit taking Overall, the Street cut earnings estimates and price targets for many agri companies, pointing to a weaker environment ahead (consensus source: Bloomberg). Wilmar also saw its consensus earnings and PT cut owing to continued weak results. Conversely, Noble’s recommendation spread was upped due to bullish 4Q10 momentum.

Commodity price performance was generally negative over the past month

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 18

Valuation

Valuation snapshot

Exhibit 20. Valuations

Name CountryNomura rating

Market cap (US$mn)

Closing price

CY10F CY11F CY12F CY10F CY11F CY12F CY10F CY11F CY12FPEG (CY11

P/E vs CY10-12F CAGR)

CY10F CY11F CY12F

UPSTREAMPalm OilSime Darby (SIME MK) Malaysia BUY 17,797 9.01 25.6 14.4 12.9 2.5 2.3 2.2 13.2 8.3 7.6 0.4 2.0 3.7 4.3IOI (IOI MK) Malaysia BUY 12,185 5.78 19.5 16.0 14.2 3.3 3.0 2.7 12.4 10.9 9.7 0.9 2.1 2.4 2.8KLK (KLK MK) Malaysia BUY 7,242 20.64 20.1 15.4 12.9 3.6 3.3 3.0 12.5 9.8 8.3 0.6 3.1 3.9 4.6Genting Plantations (GENP MK) Malaysia BUY 1,995 8.00 18.7 13.7 12.2 2.1 1.8 1.6 12.2 9.2 8.0 0.6 1.1 1.7 1.9 Boustead Holdings (BOUS MK) Malaysia N.R. 1,663 5.38 13.2 8.8 8.1 1.3 1.5 1.6 12.2 8.6 7.6 0.3 5.8 8.0 8.3 Hap Seng Plantations (HAPL MK) Malaysia N.R. 736 2.80 13.5 9.7 9.8 1.3 1.2 1.1 9.4 6.8 6.9 0.5 4.9 6.1 5.9 Kulim (KUL MK) Malaysia N.R. 1,410 3.40 18.1 12.5 12.2 1.2 1.1 1.0 6.9 5.2 5.1 0.6 1.2 1.6 1.7 IJM Plantations (IJMP MK) Malaysia N.R. 766 2.91 17.5 14.5 13.6 1.8 1.7 1.6 10.8 9.0 8.7 1.1 2.8 3.3 3.6 Malaysia palm oil average 18.3 13.1 12.0 2.1 2.0 1.9 11.2 8.5 7.7 0.6 2.9 3.8 4.1 Golden Agri (GGR SP) Singapore BUY 6,103 0.64 16.3 11.0 9.9 1.0 0.9 0.8 10.3 7.4 6.5 0.4 1.2 1.8 2.0Indofood Agri (IFAR SP) Singapore BUY 2,411 2.12 17.4 10.0 9.3 1.8 1.5 1.3 8.3 5.3 4.6 0.3 0.0 0.0 0.0First Resources (FR SP) Singapore N.R. 1,442 1.25 12.8 10.3 9.1 2.1 1.8 1.5 8.1 6.4 5.8 0.6 1.5 2.3 2.9 Kencana Agri (KAGR SP) Indonesia N.R. 361 0.40 45.0 16.6 10.5 1.6 1.7 1.4 22.4 10.5 7.3 0.2 0.6 1.9 2.9 Singapore palm oil average 22.9 11.9 9.7 1.6 1.5 1.3 12.2 7.4 6.0 0.3 0.8 1.5 1.9 Astra Agro (AALI IJ) Indonesia BUY 3,973 22,100 19.4 12.4 11.0 5.0 4.4 3.9 12.0 8.1 7.0 0.4 3.1 5.2 5.9London Sumatra (LSIP IJ) Indonesia BUY 1,733 2,225 16.9 11.2 10.5 3.5 3.0 2.6 10.4 7.4 6.8 0.4 2.4 4.0 4.8Sampoerna Agro (SGRO IJ) Indonesia N.R. 610 2,825 14.0 11.7 10.9 2.6 2.2 2.0 na na na 0.9 1.8 2.5 2.7 Bakrie Sumatera (UNSP IJ) Indonesia N.R. 542 350 16.2 9.6 7.3 0.6 0.6 0.5 na na na 0.2 1.0 1.6 2.8 Indonesia palm oil average 16.6 11.2 9.9 2.9 2.5 2.2 11.2 7.7 6.9 0.5 2.1 3.3 4.0 Univanich Palm Oil (UVAN TB) Thailand BUY 247 79.50 12.3 8.4 7.4 3.4 2.8 2.5 7.8 5.4 4.8 0.3 5.9 8.7 9.8 Palm Oil Average 18.6 12.1 10.7 2.3 2.0 1.8 11.2 7.9 7.0 0.5 2.4 3.5 3.9 - Others (rubber, sugar, etc)Khon Kaen Sugar (KSL TB) Thailand BUY 665 13.00 71.1 21.5 18.2 2.4 2.0 1.9 20.8 15.7 15.5 0.2 0.8 1.2 1.4 Lamsoon (LST TB) Thailand BUY 112 4.14 12.5 7.9 7.0 1.5 1.4 1.3 9.2 6.1 5.6 0.2 4.6 7.2 8.2 China Minzhong (MINZ SP) China N.R. 688 1.60 10.5 8.1 6.2 2.0 1.5 1.2 5.9 4.3 3.3 0.3 na 0.2 0.3 Chaoda Modern Agri (682 HK) Hong Kong REDUCE 1,756 4.10 2.9 2.5 na 0.5 0.5 na 1.9 1.5 na na 2.0 2.6 naGMG Global (GGL SP) Singapore N.R. 814 0.27 19.3 8.4 6.1 na na na 10.7 4.6 3.3 0.1 1.5 3.0 4.1 Bisi Intl (BISI IJ) Indonesia N.R. 479 1,400.00 23.0 16.0 12.1 3.5 3.0 2.5 15.6 11.9 9.1 0.4 na 0.7 1.2 UPSTREAM AVERAGE 19.8 11.8 10.5 2.2 2.0 1.8 11.1 7.7 7.1 0.4 2.4 3.2 3.7 MIDSTREAM / INTEGRATEDWilmar (WIL SP) Singapore NEUTRAL 25,238 5.02 22.1 17.2 14.9 2.1 1.9 1.8 19.1 14.3 13.4 0.8 1.4 1.5 1.7Noble (NOBL SP) Hong Kong BUY 9,670 2.04 19.0 13.7 11.9 2.4 2.1 1.9 13.3 9.7 8.9 0.5 1.4 1.6 2.2Olam (OLAM SP) Singapore BUY 4,314 2.58 20.0 16.5 13.9 2.8 2.5 2.2 13.1 11.2 10.4 0.8 1.6 1.7 2.1Mewah (MII SP) Singapore BUY 1,030 0.87 9.2 9.5 8.1 1.8 1.7 1.4 8.8 7.6 6.3 1.5 2.5 na naSingapore Average 17.6 14.2 12.2 2.3 2.1 1.8 13.5 10.7 9.7 0.9 1.7 1.6 2.0 Itochu (8001 JP) Japan BUY 15,657 799.00 6.8 5.8 5.6 1.1 1.0 0.8 10.2 8.2 7.8 0.5 2.6 3.1 3.2 Mitstui (8031 JP) Japan BUY 31,074 1,374.00 8.1 6.2 5.8 1.1 1.0 0.9 9.5 7.9 7.7 0.4 2.8 3.7 3.9 Marubeni (8002 JP) Japan NEUTRAL 12,076 562 7.8 6.6 6.3 1.3 1.2 1.0 11.5 9.9 9.4 0.6 2.0 2.3 2.5 Mitsubishi (8058 JP) Japan BUY 44,566 2,124 8.5 7.3 7.1 1.3 1.2 1.1 12.4 9.8 9.8 0.7 2.7 3.1 3.2 Sumitomo (8053 JP) Japan BUY 16,885 1,092 7.1 6.2 5.8 0.9 0.8 0.7 11.7 9.9 9.4 0.6 3.1 3.9 4.3 Japan traders average 7.7 6.4 6.1 1.1 1.0 0.9 11.0 9.1 8.8 0.6 2.6 3.2 3.4 Ruchi Soya (RSI IN) India BUY 665 100.00 14.3 11.8 9.4 1.7 1.6 1.3 7.4 6.2 5.1 0.5 0.8 1.0 1.2 KS Oils (KSO IN) India BUY 273 31.05 6.6 5.8 4.7 0.9 0.8 0.6 4.1 3.6 3.0 0.3 0.8 0.9 1.1 China Agri (606 HK) Hong Kong BUY 4,136 7.99 12.3 9.1 7.3 1.8 1.5 1.2 14.8 10.2 8.1 0.3 2.1 3.0 3.8 ADM (ADM US) United States N.R. 22,280 34.96 11.2 10.1 9.8 1.4 1.3 1.2 9.4 8.6 8.2 1.5 1.7 1.8 1.8 Bunge (BG US) United States N.R. 9,839 67.00 17.8 11.5 10.3 0.9 0.8 0.8 10.2 8.2 7.7 0.4 1.3 1.3 1.4 Petra Foods Ltd (PETRA SP) Singapore N.R. 720 1.50 18.2 14.1 12.1 2.5 2.2 2.0 13.0 10.9 9.4 0.6 2.3 2.9 3.1 Graincorp (GNC AU) Australia N.R. 1,465 7.41 14.3 10.7 11.0 1.1 1.1 1.0 7.5 5.9 6.1 0.8 3.9 4.7 4.7 Sri-Trang Agro Industry (STA TB) Thailand NEUTRAL 1,109 26.25 6.8 8.5 8.0 2.5 2.5 2.0 na na na (1.1) na na naKernel Hdg (KER PW) Ukraine N.R. 2,049 80.50 11.2 9.2 8.7 3.0 2.3 1.9 10.2 8.2 7.6 0.7 0.0 0.4 1.0 Cosan (CSAN3 BZ) Brazil N.R. 6,084 24.95 14.5 14.4 13.4 1.9 1.7 1.6 7.4 7.3 7.8 3.8 1.7 2.1 2.8 Thai Vegetable Oil (TVO TB) Thailand BUY 689 27.25 14.0 11.2 10.0 3.5 3.0 2.7 13.0 9.5 8.5 0.6 5.0 6.2 7.0 MIDSTREAM AVERAGE 12.5 10.3 9.2 1.8 1.6 1.4 10.9 8.8 8.1 0.7 2.1 2.5 2.8 DOWNSTREAM / F&BChina Foods (506 HK) Hong Kong REDUCE 1,743 4.87 28.6 20.3 15.2 2.4 2.2 2.0 15.0 11.8 9.5 0.5 1.2 1.6 2.3 Want Want (151 HK) China BUY 10,721 6.33 29.0 21.9 16.9 10.7 9.1 7.7 22.4 16.4 12.2 0.7 2.7 3.7 4.8 Tingyi (322 HK) China BUY 13,479 18.82 34.5 24.1 20.1 6.9 6.0 5.0 15.1 11.8 9.4 0.8 1.7 2.1 2.5 China Mengniu (2319 HK) Hong Kong BUY 4,478 20.10 24.2 16.4 12.5 3.1 2.7 2.3 12.5 8.7 6.9 0.4 0.9 1.4 1.8 China Yurun (1068 HK) China BUY 5,164 22.20 15.9 11.7 9.0 2.9 2.4 2.0 18.7 12.3 8.8 0.4 1.6 2.2 2.8 Indofood Sukses Makmur (INDF IJ) Indonesia N.R. 4,861 4,850.00 15.2 13.2 11.7 3.2 2.8 2.4 na na na 0.9 2.0 2.5 3.0 GFPT (GFPT TB) Thailand BUY 364 8.80 9.2 8.3 7.5 2.0 1.7 1.5 7.0 6.2 6.4 0.8 3.1 3.5 3.9 Charoen Pokphand Foods (CPF TB) Thailand NEUTRAL 6,132 24.70 12.6 11.9 11.4 3.1 2.7 2.5 12.0 11.3 11.2 2.2 4.0 5.1 5.3 DOWNSTREAM AVERAGE 21.2 16.0 13.0 4.3 3.7 3.2 14.7 11.2 9.2 0.8 1.7 2.2 2.6 AGRI-INPUTSSinofert (297 HK) Hong Kong REDUCE 3,330 3.70 22.2 14.8 11.5 1.7 1.5 1.4 21.0 11.6 9.6 0.4 0.6 1.0 1.3 United Phosphorus (UNTP IN) India BUY 1,390 136.00 10.8 9.3 8.2 1.8 1.6 1.4 6.5 5.8 5.3 0.6 2.0 3.3 4.8 China XLX (CXLX SP) China N.R. 299 0.38 9.8 10.0 8.7 1.2 1.1 1.0 7.9 6.7 5.7 1.7 2.5 2.2 2.6 AGRI INPUTS AVERAGE 14.3 11.4 9.5 1.5 1.4 1.3 11.8 8.0 6.8 0.9 1.7 2.2 2.9

P/B EV/EBITDA Div yld (%)P/E

Note: NR = Not rated, UR = Under review, Pricing as of 18 Mar; Ratings and price targets are as of the date of the most recently published report (http://www.Nomura.com), rather than the date of this document.

Source: Nomura estimates for companies under coverage, Thai covered company estimates provided by Capital Nomura Securities, Bloomberg estimates for others.

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 19

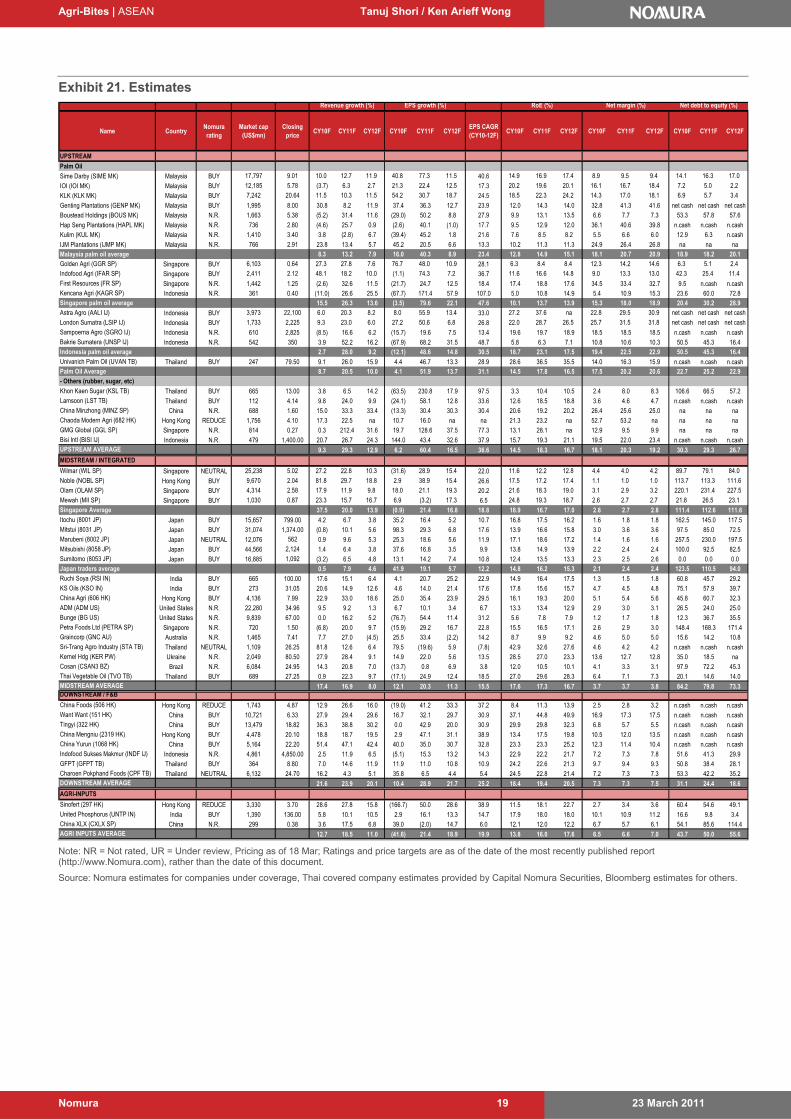

Exhibit 21. Estimates

Name CountryNomura rating

Market cap (US$mn)

Closing price

CY10F CY11F CY12F CY10F CY11F CY12FEPS CAGR (CY10-12F)

CY10F CY11F CY12F CY10F CY11F CY12F CY10F CY11F CY12F

UPSTREAM

Palm Oil

Sime Darby (SIME MK) Malaysia BUY 17,797 9.01 10.0 12.7 11.9 40.8 77.3 11.5 40.6 14.9 16.9 17.4 8.9 9.5 9.4 14.1 16.3 17.0

IOI (IOI MK) Malaysia BUY 12,185 5.78 (3.7) 6.3 2.7 21.3 22.4 12.5 17.3 20.2 19.6 20.1 16.1 16.7 18.4 7.2 5.0 2.2

KLK (KLK MK) Malaysia BUY 7,242 20.64 11.5 10.3 11.5 54.2 30.7 18.7 24.5 18.5 22.3 24.2 14.3 17.0 18.1 6.9 5.7 3.4

Genting Plantations (GENP MK) Malaysia BUY 1,995 8.00 30.8 8.2 11.9 37.4 36.3 12.7 23.9 12.0 14.3 14.0 32.8 41.3 41.6 net cash net cash net cashBoustead Holdings (BOUS MK) Malaysia N.R. 1,663 5.38 (5.2) 31.4 11.6 (29.0) 50.2 8.8 27.9 9.9 13.1 13.5 6.6 7.7 7.3 53.3 57.8 57.6

Hap Seng Plantations (HAPL MK) Malaysia N.R. 736 2.80 (4.6) 25.7 0.9 (2.6) 40.1 (1.0) 17.7 9.5 12.9 12.0 36.1 40.6 39.8 n.cash n.cash n.cashKulim (KUL MK) Malaysia N.R. 1,410 3.40 3.8 (2.8) 6.7 (39.4) 45.2 1.8 21.6 7.6 8.5 8.2 5.5 6.6 6.0 12.9 6.3 n.cash

IJM Plantations (IJMP MK) Malaysia N.R. 766 2.91 23.8 13.4 5.7 45.2 20.5 6.6 13.3 10.2 11.3 11.3 24.9 26.4 26.8 na na naMalaysia palm oil average 8.3 13.2 7.9 16.0 40.3 8.9 23.4 12.8 14.9 15.1 18.1 20.7 20.9 18.9 18.2 20.1 Golden Agri (GGR SP) Singapore BUY 6,103 0.64 27.3 27.8 7.6 76.7 48.0 10.9 28.1 6.3 8.4 8.4 12.3 14.2 14.6 6.3 5.1 2.4Indofood Agri (IFAR SP) Singapore BUY 2,411 2.12 48.1 18.2 10.0 (1.1) 74.3 7.2 36.7 11.6 16.6 14.8 9.0 13.3 13.0 42.3 25.4 11.4

First Resources (FR SP) Singapore N.R. 1,442 1.25 (2.6) 32.6 11.5 (21.7) 24.7 12.5 18.4 17.4 18.8 17.6 34.5 33.4 32.7 9.5 n.cash n.cashKencana Agri (KAGR SP) Indonesia N.R. 361 0.40 (11.0) 26.6 25.5 (67.7) 171.4 57.9 107.0 5.0 10.8 14.9 5.4 10.9 15.3 23.6 60.0 72.8 Singapore palm oil average 15.5 26.3 13.6 (3.5) 79.6 22.1 47.6 10.1 13.7 13.9 15.3 18.0 18.9 20.4 30.2 28.9 Astra Agro (AALI IJ) Indonesia BUY 3,973 22,100 6.0 20.3 8.2 8.0 55.9 13.4 33.0 27.2 37.6 na 22.8 29.5 30.9 net cash net cash net cash

London Sumatra (LSIP IJ) Indonesia BUY 1,733 2,225 9.3 23.0 6.0 27.2 50.6 6.8 26.8 22.0 28.7 26.5 25.7 31.5 31.8 net cash net cash net cashSampoerna Agro (SGRO IJ) Indonesia N.R. 610 2,825 (8.5) 16.6 6.2 (15.7) 19.6 7.5 13.4 19.6 19.7 18.9 18.5 18.5 18.5 n.cash n.cash n.cashBakrie Sumatera (UNSP IJ) Indonesia N.R. 542 350 3.9 52.2 16.2 (67.9) 68.2 31.5 48.7 5.8 6.3 7.1 10.8 10.6 10.3 50.5 45.3 16.4 Indonesia palm oil average 2.7 28.0 9.2 (12.1) 48.6 14.8 30.5 18.7 23.1 17.5 19.4 22.5 22.9 50.5 45.3 16.4 Univanich Palm Oil (UVAN TB) Thailand BUY 247 79.50 9.1 26.0 15.9 4.4 46.7 13.3 28.9 28.6 36.5 35.5 14.0 16.3 15.9 n.cash n.cash n.cashPalm Oil Average 8.7 20.5 10.0 4.1 51.9 13.7 31.1 14.5 17.8 16.5 17.5 20.2 20.6 22.7 25.2 22.9 - Others (rubber, sugar, etc)

Khon Kaen Sugar (KSL TB) Thailand BUY 665 13.00 3.8 6.5 14.2 (63.5) 230.8 17.9 97.5 3.3 10.4 10.5 2.4 8.0 8.3 106.6 66.5 57.2 Lamsoon (LST TB) Thailand BUY 112 4.14 9.8 24.0 9.9 (24.1) 58.1 12.8 33.6 12.6 18.5 18.8 3.6 4.6 4.7 n.cash n.cash n.cashChina Minzhong (MINZ SP) China N.R. 688 1.60 15.0 33.3 33.4 (13.3) 30.4 30.3 30.4 20.6 19.2 20.2 26.4 25.6 25.0 na na naChaoda Modern Agri (682 HK) Hong Kong REDUCE 1,756 4.10 17.3 22.5 na 10.7 16.0 na na 21.3 23.2 na 52.7 53.2 na na na naGMG Global (GGL SP) Singapore N.R. 814 0.27 0.3 212.4 31.6 19.7 128.6 37.5 77.3 13.1 28.1 na 12.9 9.5 9.9 na na naBisi Intl (BISI IJ) Indonesia N.R. 479 1,400.00 20.7 26.7 24.3 144.0 43.4 32.6 37.9 15.7 19.3 21.1 19.5 22.0 23.4 n.cash n.cash n.cashUPSTREAM AVERAGE 9.3 29.3 12.9 6.2 60.4 16.5 36.6 14.5 18.3 16.7 18.1 20.3 19.2 30.3 29.3 26.7

MIDSTREAM / INTEGRATED

Wilmar (WIL SP) Singapore NEUTRAL 25,238 5.02 27.2 22.8 10.3 (31.6) 28.9 15.4 22.0 11.6 12.2 12.8 4.4 4.0 4.2 89.7 79.1 84.0

Noble (NOBL SP) Hong Kong BUY 9,670 2.04 81.8 29.7 18.8 2.9 38.9 15.4 26.6 17.5 17.2 17.4 1.1 1.0 1.0 113.7 113.3 111.6Olam (OLAM SP) Singapore BUY 4,314 2.58 17.9 11.9 9.8 18.0 21.1 19.3 20.2 21.6 18.3 19.0 3.1 2.9 3.2 220.1 231.4 227.5

Mewah (MII SP) Singapore BUY 1,030 0.87 23.3 15.7 16.7 6.9 (3.2) 17.3 6.5 24.8 19.3 18.7 2.6 2.7 2.7 21.8 26.5 23.1Singapore Average 37.5 20.0 13.9 (0.9) 21.4 16.8 18.8 18.9 16.7 17.0 2.8 2.7 2.8 111.4 112.6 111.6 Itochu (8001 JP) Japan BUY 15,657 799.00 4.2 6.7 3.8 35.2 16.4 5.2 10.7 16.8 17.5 16.2 1.6 1.8 1.8 162.5 145.0 117.5 Mitstui (8031 JP) Japan BUY 31,074 1,374.00 (0.8) 10.1 5.6 98.3 29.3 6.8 17.6 13.9 16.6 15.8 3.0 3.6 3.6 97.5 85.0 72.5 Marubeni (8002 JP) Japan NEUTRAL 12,076 562 0.9 9.6 5.3 25.3 18.6 5.6 11.9 17.1 18.6 17.2 1.4 1.6 1.6 257.5 230.0 197.5 Mitsubishi (8058 JP) Japan BUY 44,566 2,124 1.4 6.4 3.8 37.6 16.8 3.5 9.9 13.8 14.9 13.9 2.2 2.4 2.4 100.0 92.5 82.5 Sumitomo (8053 JP) Japan BUY 16,885 1,092 (3.2) 6.5 4.8 13.1 14.2 7.4 10.8 12.4 13.5 13.3 2.3 2.5 2.6 0.0 0.0 0.0 Japan traders average 0.5 7.9 4.6 41.9 19.1 5.7 12.2 14.8 16.2 15.3 2.1 2.4 2.4 123.5 110.5 94.0 Ruchi Soya (RSI IN) India BUY 665 100.00 17.6 15.1 6.4 4.1 20.7 25.2 22.9 14.9 16.4 17.5 1.3 1.5 1.8 60.8 45.7 29.2 KS Oils (KSO IN) India BUY 273 31.05 20.6 14.9 12.6 4.6 14.0 21.4 17.6 17.8 15.6 15.7 4.7 4.5 4.8 75.1 57.9 39.7 China Agri (606 HK) Hong Kong BUY 4,136 7.99 22.9 33.0 18.6 25.0 35.4 23.9 29.5 16.1 19.3 20.0 5.1 5.4 5.6 45.8 60.7 32.3 ADM (ADM US) United States N.R. 22,280 34.96 9.5 9.2 1.3 6.7 10.1 3.4 6.7 13.3 13.4 12.9 2.9 3.0 3.1 26.5 24.0 25.0 Bunge (BG US) United States N.R. 9,839 67.00 0.0 16.2 5.2 (76.7) 54.4 11.4 31.2 5.6 7.8 7.9 1.2 1.7 1.8 12.3 36.7 35.5 Petra Foods Ltd (PETRA SP) Singapore N.R. 720 1.50 (6.8) 20.0 9.7 (15.9) 29.2 16.7 22.8 15.5 16.5 17.1 2.6 2.9 3.0 148.4 168.3 171.4 Graincorp (GNC AU) Australia N.R. 1,465 7.41 7.7 27.0 (4.5) 25.5 33.4 (2.2) 14.2 8.7 9.9 9.2 4.6 5.0 5.0 15.6 14.2 10.8 Sri-Trang Agro Industry (STA TB) Thailand NEUTRAL 1,109 26.25 81.8 12.6 6.4 79.5 (19.6) 5.9 (7.8) 42.9 32.6 27.6 4.6 4.2 4.2 n.cash n.cash n.cashKernel Hdg (KER PW) Ukraine N.R. 2,049 80.50 27.9 28.4 9.1 14.9 22.0 5.6 13.5 28.5 27.0 23.3 13.6 12.7 12.8 35.0 18.5 naCosan (CSAN3 BZ) Brazil N.R. 6,084 24.95 14.3 20.8 7.0 (13.7) 0.8 6.9 3.8 12.0 10.5 10.1 4.1 3.3 3.1 97.9 72.2 45.3 Thai Vegetable Oil (TVO TB) Thailand BUY 689 27.25 0.9 22.3 9.7 (17.1) 24.9 12.4 18.5 27.0 29.6 28.3 6.4 7.1 7.3 20.1 14.6 14.0 MIDSTREAM AVERAGE 17.4 16.9 8.0 12.1 20.3 11.3 15.5 17.6 17.3 16.7 3.7 3.7 3.8 84.2 79.8 73.3 DOWNSTREAM / F&B

China Foods (506 HK) Hong Kong REDUCE 1,743 4.87 12.9 26.6 16.0 (19.0) 41.2 33.3 37.2 8.4 11.3 13.9 2.5 2.8 3.2 n.cash n.cash n.cashWant Want (151 HK) China BUY 10,721 6.33 27.9 29.4 29.6 16.7 32.1 29.7 30.9 37.1 44.8 49.9 16.9 17.3 17.5 n.cash n.cash n.cashTingyi (322 HK) China BUY 13,479 18.82 36.3 38.8 30.2 0.0 42.9 20.0 30.9 29.9 29.8 32.3 6.8 5.7 5.5 n.cash n.cash n.cashChina Mengniu (2319 HK) Hong Kong BUY 4,478 20.10 18.8 18.7 19.5 2.9 47.1 31.1 38.9 13.4 17.5 19.8 10.5 12.0 13.5 n.cash n.cash n.cashChina Yurun (1068 HK) China BUY 5,164 22.20 51.4 47.1 42.4 40.0 35.0 30.7 32.8 23.3 23.3 25.2 12.3 11.4 10.4 n.cash n.cash n.cashIndofood Sukses Makmur (INDF IJ) Indonesia N.R. 4,861 4,850.00 2.5 11.9 6.5 (5.1) 15.3 13.2 14.3 22.9 22.2 21.7 7.2 7.3 7.8 51.6 41.3 29.9 GFPT (GFPT TB) Thailand BUY 364 8.80 7.0 14.6 11.9 11.9 11.0 10.8 10.9 24.2 22.6 21.3 9.7 9.4 9.3 50.8 38.4 28.1 Charoen Pokphand Foods (CPF TB) Thailand NEUTRAL 6,132 24.70 16.2 4.3 5.1 35.8 6.5 4.4 5.4 24.5 22.8 21.4 7.2 7.3 7.3 53.3 42.2 35.2 DOWNSTREAM AVERAGE 21.6 23.9 20.1 10.4 28.9 21.7 25.2 18.4 19.4 20.5 7.3 7.3 7.5 31.1 24.4 18.6

AGRI-INPUTS

Sinofert (297 HK) Hong Kong REDUCE 3,330 3.70 28.6 27.8 15.8 (166.7) 50.0 28.6 38.9 11.5 18.1 22.7 2.7 3.4 3.6 60.4 54.6 49.1 United Phosphorus (UNTP IN) India BUY 1,390 136.00 5.8 10.1 10.5 2.9 16.1 13.3 14.7 17.9 18.0 18.0 10.1 10.9 11.2 16.6 9.8 3.4 China XLX (CXLX SP) China N.R. 299 0.38 3.6 17.5 6.8 39.0 (2.0) 14.7 6.0 12.1 12.0 12.2 6.7 5.7 6.1 54.1 85.6 114.4 AGRI INPUTS AVERAGE 12.7 18.5 11.0 (41.6) 21.4 18.9 19.9 13.8 16.0 17.6 6.5 6.6 7.0 43.7 50.0 55.6

RoE (%) Net debt to equity (%)EPS growth (%) Net margin (%)Revenue growth (%)

Note: NR = Not rated, UR = Under review, Pricing as of 18 Mar; Ratings and price targets are as of the date of the most recently published report (http://www.Nomura.com), rather than the date of this document.

Source: Nomura estimates for companies under coverage, Thai covered company estimates provided by Capital Nomura Securities, Bloomberg estimates for others.

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 20

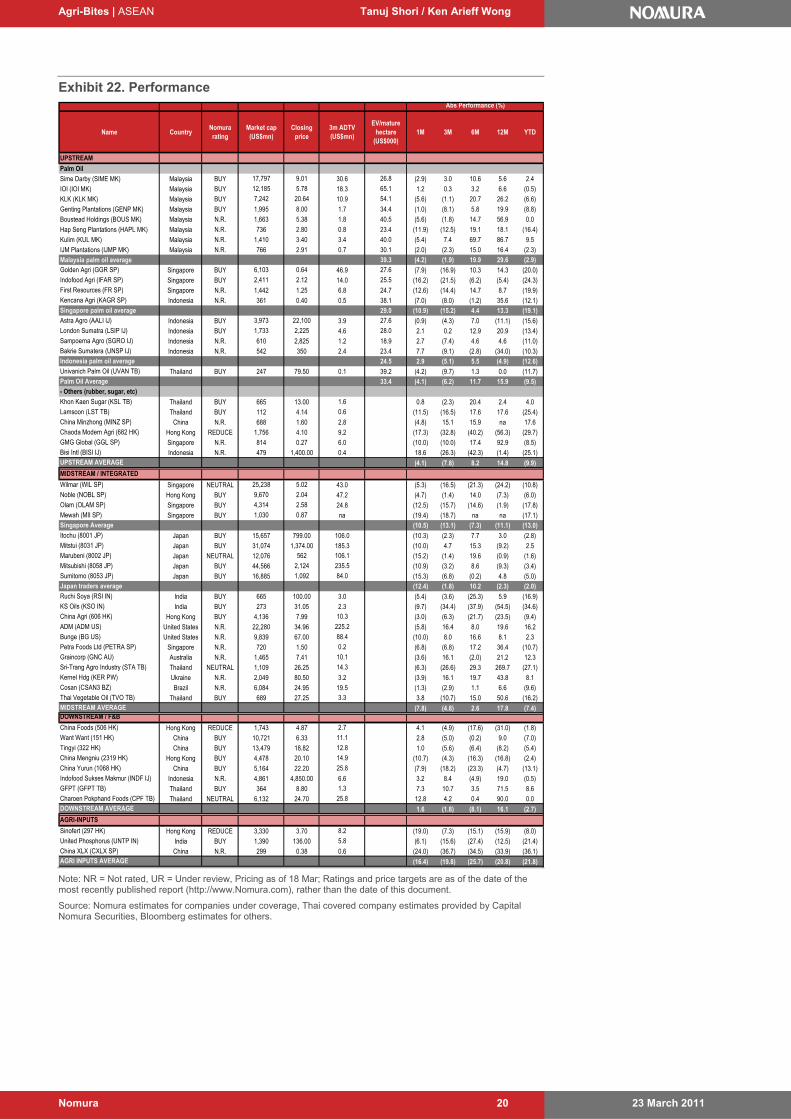

Exhibit 22. Performance

Name CountryNomura rating

Market cap (US$mn)

Closing price

3m ADTV (US$mn)

EV/mature hectare

(US$000)1M 3M 6M 12M YTD

UPSTREAM

Palm Oil

Sime Darby (SIME MK) Malaysia BUY 17,797 9.01 30.6 26.8 (2.9) 3.0 10.6 5.6 2.4 IOI (IOI MK) Malaysia BUY 12,185 5.78 18.3 65.1 1.2 0.3 3.2 6.6 (0.5)KLK (KLK MK) Malaysia BUY 7,242 20.64 10.9 54.1 (5.6) (1.1) 20.7 26.2 (6.6)Genting Plantations (GENP MK) Malaysia BUY 1,995 8.00 1.7 34.4 (1.0) (8.1) 5.8 19.9 (8.8)Boustead Holdings (BOUS MK) Malaysia N.R. 1,663 5.38 1.8 40.5 (5.6) (1.8) 14.7 56.9 0.0

Hap Seng Plantations (HAPL MK) Malaysia N.R. 736 2.80 0.8 23.4 (11.9) (12.5) 19.1 18.1 (16.4)Kulim (KUL MK) Malaysia N.R. 1,410 3.40 3.4 40.0 (5.4) 7.4 69.7 86.7 9.5 IJM Plantations (IJMP MK) Malaysia N.R. 766 2.91 0.7 30.1 (2.0) (2.3) 15.0 16.4 (2.3)Malaysia palm oil average 39.3 (4.2) (1.9) 19.9 29.6 (2.9)Golden Agri (GGR SP) Singapore BUY 6,103 0.64 46.9 27.6 (7.9) (16.9) 10.3 14.3 (20.0)Indofood Agri (IFAR SP) Singapore BUY 2,411 2.12 14.0 25.5 (16.2) (21.5) (6.2) (5.4) (24.3)First Resources (FR SP) Singapore N.R. 1,442 1.25 6.8 24.7 (12.6) (14.4) 14.7 8.7 (19.9)Kencana Agri (KAGR SP) Indonesia N.R. 361 0.40 0.5 38.1 (7.0) (8.0) (1.2) 35.6 (12.1)Singapore palm oil average 29.0 (10.9) (15.2) 4.4 13.3 (19.1)Astra Agro (AALI IJ) Indonesia BUY 3,973 22,100 3.9 27.6 (0.9) (4.3) 7.0 (11.1) (15.6)London Sumatra (LSIP IJ) Indonesia BUY 1,733 2,225 4.6 28.0 2.1 0.2 12.9 20.9 (13.4)Sampoerna Agro (SGRO IJ) Indonesia N.R. 610 2,825 1.2 18.9 2.7 (7.4) 4.6 4.6 (11.0)Bakrie Sumatera (UNSP IJ) Indonesia N.R. 542 350 2.4 23.4 7.7 (9.1) (2.8) (34.0) (10.3)Indonesia palm oil average 24.5 2.9 (5.1) 5.5 (4.9) (12.6)Univanich Palm Oil (UVAN TB) Thailand BUY 247 79.50 0.1 39.2 (4.2) (9.7) 1.3 0.0 (11.7)Palm Oil Average 33.4 (4.1) (6.2) 11.7 15.9 (9.5)- Others (rubber, sugar, etc)

Khon Kaen Sugar (KSL TB) Thailand BUY 665 13.00 1.6 0.8 (2.3) 20.4 2.4 4.0 Lamsoon (LST TB) Thailand BUY 112 4.14 0.6 (11.5) (16.5) 17.6 17.6 (25.4)China Minzhong (MINZ SP) China N.R. 688 1.60 2.8 (4.8) 15.1 15.9 na 17.6 Chaoda Modern Agri (682 HK) Hong Kong REDUCE 1,756 4.10 9.2 (17.3) (32.8) (40.2) (56.3) (29.7)GMG Global (GGL SP) Singapore N.R. 814 0.27 6.0 (10.0) (10.0) 17.4 92.9 (8.5)Bisi Intl (BISI IJ) Indonesia N.R. 479 1,400.00 0.4 18.6 (26.3) (42.3) (1.4) (25.1)UPSTREAM AVERAGE (4.1) (7.8) 8.2 14.8 (9.9)

MIDSTREAM / INTEGRATED

Wilmar (WIL SP) Singapore NEUTRAL 25,238 5.02 43.0 (5.3) (16.5) (21.3) (24.2) (10.8)Noble (NOBL SP) Hong Kong BUY 9,670 2.04 47.2 (4.7) (1.4) 14.0 (7.3) (6.0)Olam (OLAM SP) Singapore BUY 4,314 2.58 24.8 (12.5) (15.7) (14.6) (1.9) (17.8)Mewah (MII SP) Singapore BUY 1,030 0.87 na (19.4) (18.7) na na (17.1)Singapore Average (10.5) (13.1) (7.3) (11.1) (13.0)Itochu (8001 JP) Japan BUY 15,657 799.00 106.0 (10.3) (2.3) 7.7 3.0 (2.8)Mitstui (8031 JP) Japan BUY 31,074 1,374.00 185.3 (10.0) 4.7 15.3 (9.2) 2.5 Marubeni (8002 JP) Japan NEUTRAL 12,076 562 106.1 (15.2) (1.4) 19.6 (0.9) (1.6)Mitsubishi (8058 JP) Japan BUY 44,566 2,124 235.5 (10.9) (3.2) 8.6 (9.3) (3.4)Sumitomo (8053 JP) Japan BUY 16,885 1,092 84.0 (15.3) (6.8) (0.2) 4.8 (5.0)Japan traders average (12.4) (1.8) 10.2 (2.3) (2.0)Ruchi Soya (RSI IN) India BUY 665 100.00 3.0 (5.4) (3.6) (25.3) 5.9 (16.9)KS Oils (KSO IN) India BUY 273 31.05 2.3 (9.7) (34.4) (37.9) (54.5) (34.6)China Agri (606 HK) Hong Kong BUY 4,136 7.99 10.3 (3.0) (6.3) (21.7) (23.5) (9.4)ADM (ADM US) United States N.R. 22,280 34.96 225.2 (5.8) 16.4 8.0 19.6 16.2 Bunge (BG US) United States N.R. 9,839 67.00 88.4 (10.0) 8.0 16.6 8.1 2.3 Petra Foods Ltd (PETRA SP) Singapore N.R. 720 1.50 0.2 (6.8) (6.8) 17.2 36.4 (10.7)Graincorp (GNC AU) Australia N.R. 1,465 7.41 10.1 (3.6) 16.1 (2.0) 21.2 12.3 Sri-Trang Agro Industry (STA TB) Thailand NEUTRAL 1,109 26.25 14.3 (6.3) (26.6) 29.3 269.7 (27.1)Kernel Hdg (KER PW) Ukraine N.R. 2,049 80.50 3.2 (3.9) 16.1 19.7 43.8 8.1 Cosan (CSAN3 BZ) Brazil N.R. 6,084 24.95 19.5 (1.3) (2.9) 1.1 6.6 (9.6)Thai Vegetable Oil (TVO TB) Thailand BUY 689 27.25 3.3 3.8 (10.7) 15.0 50.6 (16.2)MIDSTREAM AVERAGE (7.8) (4.8) 2.6 17.8 (7.4)DOWNSTREAM / F&B

China Foods (506 HK) Hong Kong REDUCE 1,743 4.87 2.7 4.1 (4.9) (17.6) (31.0) (1.8)Want Want (151 HK) China BUY 10,721 6.33 11.1 2.8 (5.0) (0.2) 9.0 (7.0)Tingyi (322 HK) China BUY 13,479 18.82 12.8 1.0 (5.6) (6.4) (8.2) (5.4)China Mengniu (2319 HK) Hong Kong BUY 4,478 20.10 14.9 (10.7) (4.3) (16.3) (16.8) (2.4)China Yurun (1068 HK) China BUY 5,164 22.20 25.8 (7.9) (18.2) (23.3) (4.7) (13.1)Indofood Sukses Makmur (INDF IJ) Indonesia N.R. 4,861 4,850.00 6.6 3.2 8.4 (4.9) 19.0 (0.5)GFPT (GFPT TB) Thailand BUY 364 8.80 1.3 7.3 10.7 3.5 71.5 8.6 Charoen Pokphand Foods (CPF TB) Thailand NEUTRAL 6,132 24.70 25.8 12.8 4.2 0.4 90.0 0.0 DOWNSTREAM AVERAGE 1.6 (1.8) (8.1) 16.1 (2.7)

AGRI-INPUTS

Sinofert (297 HK) Hong Kong REDUCE 3,330 3.70 8.2 (19.0) (7.3) (15.1) (15.9) (8.0)United Phosphorus (UNTP IN) India BUY 1,390 136.00 5.8 (6.1) (15.6) (27.4) (12.5) (21.4)China XLX (CXLX SP) China N.R. 299 0.38 0.6 (24.0) (36.7) (34.5) (33.9) (36.1)AGRI INPUTS AVERAGE (16.4) (19.8) (25.7) (20.8) (21.8)

Abs Performance (%)

Note: NR = Not rated, UR = Under review, Pricing as of 18 Mar; Ratings and price targets are as of the date of the most recently published report (http://www.Nomura.com), rather than the date of this document.

Source: Nomura estimates for companies under coverage, Thai covered company estimates provided by Capital Nomura Securities, Bloomberg estimates for others.

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 21

Exhibit 23. Valuation: P/E vs EPS CAGR (2010-12F)

IOI

KLK

Golden Agri

Indofood

Astra Agro

London Sumatra

Univanich Palm Oil

Chaoda Modern Agri

Wilmar

Noble

Olam

Mewah

Itochu

Mitstui

Marubeni

Mitsubishi Sumitomo

Ruchi Soya

KS Oils

China Agri

Thai Vegetable Oil

China Foods

Want Want

Tingyi

China Mengniu

China Yurun

GFPT

Charoen Pokphand Foods

Sinofert

United Phosphorus

China XLX

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

0.0 5.0 10.0 15.0 20.0 25.0 30.0

P/E (CY11F)

EP

S C

AG

R (

CY

10-

12F

)

Source: Bloomberg, Nomura estimates. Estimates for Thai Vegetable Oil and Khon Kaen Sugar provided by Capital Nomura Securities

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 22

Exhibit 24. Valuation: P/BV (CY11F) vs ROE (CY11F)

China XLX

United Phosphorus Sinofert

Charoen Pokphand FoodsGFPT

China Yurun

China Mengniu

China Foods

Thai Vegetable Oil

Sri-Trang Agro Industry

China Agri

KS Oils Ruchi Soya

Sumitomo

Mitsubishi

Marubeni

Mitstui Itochu

Mewah Olam Noble

Wilmar

Chaoda Modern Agri

Lamsoon

Khon Kaen Sugar

Univanich Palm Oil

London Sumatra

Indofood

Golden Agri

KLK IOI

Sime Darby

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0

P/B (CY11F)

RoE

(C

Y11

F)

Source: Bloomberg, Nomura estimates. Estimates for Khon Kaen Sugar and Thai Vegetable Oil provided by Capital Nomura Securities

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 23

Exhibit 25. Valuation: EV/EBITDA vs EBITDA CAGR (2010-12F)

Sime Darby

IOI

KLK Golden Agri

Indofood

Astra Agro

London Sumatra

Univanich Palm Oil

Khon Kaen Sugar

Lamsoon

Chaoda Modern Agri

Wilmar

Noble

Olam

Mewah

Itochu

Mitstui Marubeni

Mitsubishi

Sumitomo

Ruchi Soya KS Oils

China Agri

Sri-Trang Agro Industry

Thai Vegetable Oil

China Foods

Want Want

Tingyi

China Mengniu

China Yurun

GFPT Charoen Pokphand Foods

Sinofert

United Phosphorus

China XLX

0.0

10.0

20.0

30.0

40.0

50.0

60.0

0.0 5.0 10.0 15.0 20.0 25.0 30.0 35.0 40.0

EV/EBITDA (CY11F)

EB

ITD

A C

AG

R (

CY

10-1

2F)

Source: Bloomberg, Nomura estimates. Estimates for Khon Kaen Sugar provided by Capital Nomura Securities

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 24

P/E charts

Valuation charts

Exhibit 26. Wilmar — forward P/E

0

1

2

3

4

5

6

7

8

9

10

Jan-

07

Ap

r-07

Jul-0

7

Oct

-07

Jan-

08

Ap

r-08

Jul-0

8

Oct

-08

Jan-

09

Ap

r-09

Jul-0

9

Oct

-09

Jan-

10

Ap

r-10

Jul-1

0

Oct

-10

Jan-

11

(S$)

25x

20x

15x

10x

5x

Source: Bloomberg

Exhibit 27. Noble — forward P/E

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Jan

-07

Ap

r-07

Jul-0

7

Oct

-07

Jan

-08

Ap

r-08

Jul-0

8

Oct

-08

Jan

-09

Ap

r-09

Jul-0

9

Oct

-09

Jan

-10

Ap

r-10

Jul-1

0

Oct

-10

Jan

-11

(S$)

25x

20x

15x

10x

5x

Source: Bloomberg

Exhibit 28. Olam — forward P/E

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Feb

05

Aug

05

Feb

06

Aug

06

Feb

07

Aug

07

Feb

08

Aug

08

Feb

09

Aug

09

Feb

10

Aug

10

Feb

11

(S$)

10x15x

20x

25x

30x

Source: Bloomberg

Exhibit 29. Mewah — forward P/E

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

26-N

ov-1

0

06-D

ec-1

0

16-D

ec-1

0

26-D

ec-1

0

05-J

an-1

1

15-J

an-1

1

25-J

an-1

1

04-F

eb-1

1

14-F

eb-1

1

24-F

eb-1

1

06-M

ar-1

1

16-M

ar-1

1

(S$)

11x

9x

7x

5x

3x

Source: Bloomberg

Exhibit 30. Sime Darby — forward P/E

10

15

20

25

30

35

Nov

-07

Feb

-08

May

-08

Aug

-08

Nov

-08

Feb

-09

May

-09

Aug

-09

Nov

-09

Feb

-10

May

-10

Aug

-10

Nov

-10

Feb

-11

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

P/E (LHS) CPO (RHS)

-1SD = 15.2

(x)

+1SD = 25.0

Average = 20.1

(RM/mT

Source: Bloomberg

Exhibit 31. IOI — forward P/E

0

5

10

15

20

25

30

35

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500PER (LHS)

CPO (RHS)

+1SD=20

Average=15.4

-1SD=10.8

(RM/Mt)

Source: Bloomberg

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

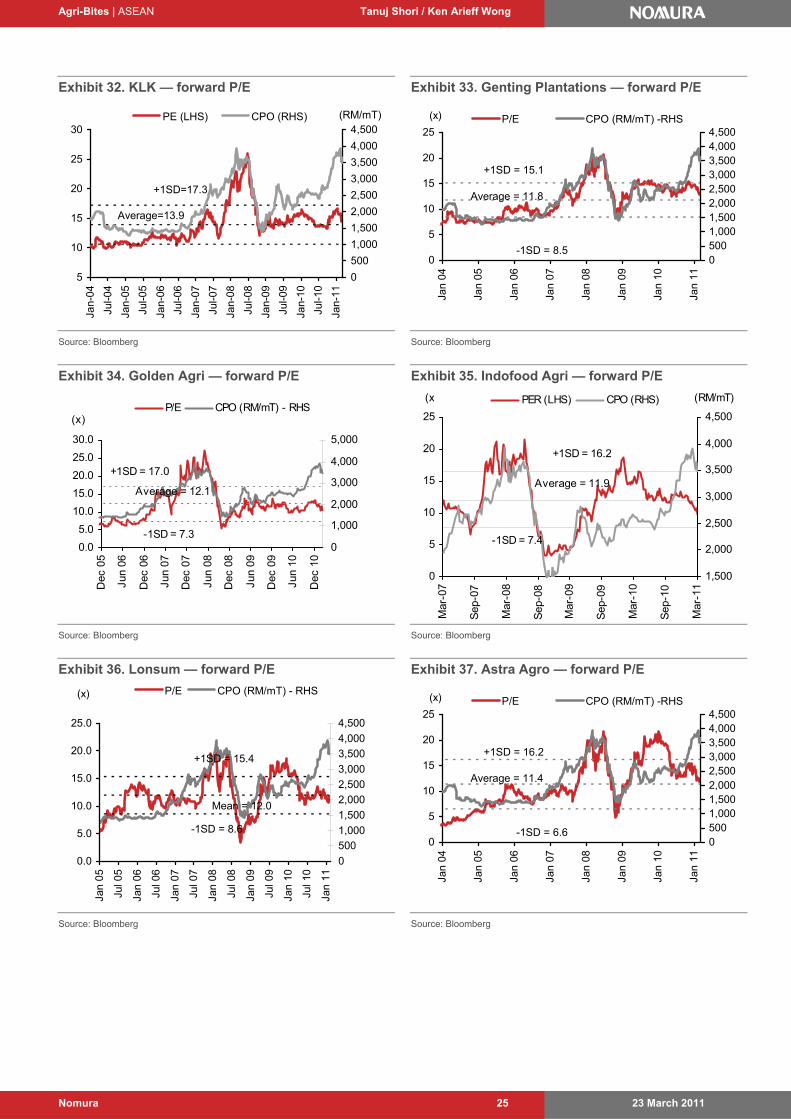

23 March 2011 Nomura 25

Exhibit 32. KLK — forward P/E

5

10

15

20

25

30

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500PE (LHS) CPO (RHS) (RM/mT)

+1SD=17.3

Average=13.9

Source: Bloomberg

Exhibit 33. Genting Plantations — forward P/E

0

5

10

15

20

25

Jan

04

Jan

05

Jan

06

Jan

07

Jan

08

Jan

09

Jan

10

Jan

11

05001,0001,5002,0002,5003,0003,5004,0004,500

P/E CPO (RM/mT) -RHS

-1SD = 8.5

(x)

+1SD = 15.1

Average = 11.8

Source: Bloomberg

Exhibit 34. Golden Agri — forward P/E

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Dec

05

Jun

06

Dec

06

Jun

07

Dec

07

Jun

08

Dec

08

Jun

09

Dec

09

Jun

10

Dec

10

0

1,000

2,000

3,000

4,000

5,000

P/E CPO (RM/mT) - RHS

-1SD = 7.3

(x)

+1SD = 17.0

Average = 12.1

Source: Bloomberg

Exhibit 35. Indofood Agri — forward P/E

0

5

10

15

20

25

Mar

-07

Sep

-07

Mar

-08

Sep

-08

Mar

-09

Sep

-09

Mar

-10

Sep

-10

Mar

-11

1,500

2,000

2,500

3,000

3,500

4,000

4,500

PER (LHS) CPO (RHS) (RM/mT)

+1SD = 16.2

Average = 11.9

-1SD = 7.4

(x

Source: Bloomberg

Exhibit 36. Lonsum — forward P/E

0.0

5.0

10.0

15.0

20.0

25.0

Jan

05

Jul 0

5

Jan

06

Jul 0

6

Jan

07

Jul 0

7

Jan

08

Jul 0

8

Jan

09

Jul 0

9

Jan

10

Jul 1

0

Jan

11

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

P/E CPO (RM/mT) - RHS

-1SD = 8.6

(x)

+1SD = 15.4

Mean = 12.0

Source: Bloomberg

Exhibit 37. Astra Agro — forward P/E

0

5

10

15

20

25

Jan

04

Jan

05

Jan

06

Jan

07

Jan

08

Jan

09

Jan

10

Jan

11

05001,0001,5002,0002,5003,0003,5004,0004,500

P/E CPO (RM/mT) -RHS

-1SD = 6.6

(x)

+1SD = 16.2

Average = 11.4

Source: Bloomberg

Agri-Bites | ASEAN Tanuj Shori / Ken Arieff Wong

23 March 2011 Nomura 26

What went up, what went down

The ups and downs In this section, we track valuation changes and price performances of the regional agri-players and key soft commodities. We also keep tabs on consensus expectations on earnings and price performance for the companies under our coverage.

Last month’s commodity price performance: negative Commodity price performance was generally negative over the past month, due to concerns on the Japanese earthquake and tsunami impact and expectations of supply recovery capping prices. Prices of oils such as CPO (-14.1% m-m), refined palm oil (-11.1% m-m), US soybean (-10.6% m-m), US wheat (-26.6% m-m) and rubber (-25.2% m-m) were lower. We witnessed a secular downtick in commodity prices across the board. The S&P GSCI Agri Index was down 12.3% last month.

Exhibit 38. Commodity price performance

Commodity name Current price Unit % chg m-m % chg ytd % chg y-y Description

Vegetable Oils

Malaysia Crude Palm Oil 3,369.5 MYR/metric tonne (14.1) (10.3) 28.2 Malaysian Palm Oil Board Crude Palm Oil fob Spot Price

Refined Palm Oil 1,162.5 USD/Metric Tonne (11.1) (7.0) 44.0 RBD Palm Oil (Fully Refined) FOB Malaysia Spot Price

US Soybean Oil 50.01 USd/pound (9.4) (6.7) 40.9 USDA Crude Soybean Oil Spot Price/Illinois

China Soybean Oil 9,950 CNY/MT (3.9) 1.5 36.3 China No. 4 Soybean Oil Spot Price Dalian