asia corporate treasury

TRANSCRIPT

Sponsored by:

WednesdaySept. 10, 2014www.bloombergbriefs.com

CHINA CURRENCY: Yuan deposits inSouth Korea increase; HongKong-Shanghai equity link to boost yuan;Deutsche Bank authorized for yuanclearing; yuan now seventh-most tradedcurrency. Page 3.

ON THE RECORD: Q&A with DavidBlair, independent treasury consultant,about the issues facing treasurersglobally and in Asia. Page 7.

HEDGE ACCOUNTING: Changes inIFRS 9 are seen as a big improvementover IAS 39 in terms of what qualifies as"hedgeable." Page 9.

INDUSTRY FOCUS: This monthfeatures a look at the communicationsindustry's working capital and free cashflow ratios, plus Asia lending and bondissuance. Page 10.

QUOTED

"Blocking Russia from the SWIFTsystem would be a seriousescalation in sanctions and wouldmost certainly result in equallytough retaliatory actions byRussia. An exclusion fromSWIFT would not block majortrade deals but would causeproblems in cross-border bankingand that would disrupt tradeflows.”

— Chris Weafer, a senior partner at

Moscow-based consulting firm Macro Advisory.

Page 2.

INSIDE THIS ISSUE

DATA POINT OF THE MONTH

Asia syndicated lending year to datethrough August:

Versus $293.6 billion for the same periodlast year, according to Bloomberg data.

$375.7 billion

Yen, Euro May Have Further to Fall as Volatility ReturnsBY MARIKO ISHIKAWA, RACHEL EVANS, DAVID GOODMAN AND ANDREA WONG

The yen and euro seem poised to weaken further as foreign exchange volatilityincreases from all-time lows, making it more expensive for corporates to hedge theircurrency exposures.

The Bank of Japan and European Central Bank’s unprecedented easing policies sentthe yen to the weakest level since October 2008 in the first week of September, while theeuro capped its longest losing streak since its 1999 debut and was trading at its lowestsince mid-2013.

Stimulus measures from global central banks are emboldening traders to raise betsagainst the yen to the highest level since January. The difference in the number ofwagers by hedge funds and other large speculators on a decline in the yen, comparedwith those on a gain, increased to 117,308 contracts in the week through Sept. 2,according to U.S. Commodity Futures Trading Commission data. That’s the largestnet-short position in the futures market since the period ended Jan. 14.

Meanwhile, the decision by ECB President on Sept. 4 to push theMario Draghi deposit rate further below zero and expand the money supply by purchasingasset-backed securities is also helping stoke foreign exchange volatility. JPMorgan'sGlobal FX Volatility Index has bounced up 25 percent from an all-time low on July 3.Increased volatility generally makes currency hedging more expensive.

Record-low rates in the euro area will probably encourage traders to borrow in theregion and invest the proceeds in economies with higher-yielding assets. “The biggest takeaway is they want to bring the balance sheet back to 2012 level,”said , head of global rates and currencies in David Woo New York at Bank of America

.’s Merrill Lynch unit. The Fed’s assets total is $4.42 trillion, widening the differenceCorpwith the ECB’s balance sheet to a record $1.8 trillion. The Bank of Japan finished itsmeeting on Sept. 4 by maintaining its record debt purchases of 60 trillion yen ($570billion) to 70 trillion yen a year.

“The euro and the yen are both very attractive as funding currencies, and the dollarhas really dropped out of that category,” said , a director and head ofDaniel Katziveforeign-exchange strategy, North America, at in New York.BNP Paribas SA

TRANSACTION BANKING

FX Volatility Increases as the Euro and Yen Dive

Sept. 10, 2014 Bloomberg Brief Asia Corporate Treasury 2

TRANSACTION BANKING

Swift Justice: One Way to Make Putin HowlBY CAROL MATLACK, BLOOMBERG NEWS, AND JENNY JOHNSON, BNA

The West’s ultimate weapon against Russian President could be aVladimir Putin little-known organization housed in a neoclassical building on a wooded campus in aBrussels suburb: the ,Society for Worldwide Interbank Financial Telecommunicationor SWIFT.

Britain is pressing the European Union, whose laws govern the cooperative, to barRussian banks from using SWIFT. Being frozen out could wreak havoc with Russiantrade and investment. In an informal survey published on Sept. 2 by a Russianbanking-industry website, banki.ru, representatives of several banks said loss of accessto SWIFT would severely disrupt their business. “According to the Russian association ofSWIFT, the number of users in the Russian Federation ranks 22nd in the world involume of traffic sent,” the notice said. Russian companies are wary of the possibility ofbeing cut off from SWIFT, despite the moves toward alternatives, according to

, a member of the Board of Directors at , a Russian financialAlexander Gentsis Diasoftsoftware company.

The Russian Ministry of Finance announced on Aug. 27 that it has prepared legislationtogether with the central bank on the creation of a Russian alternative. The legislationwill move forward once the central bank is technologically ready to process payments,the ministry said, according to news reports posted to its website. The Russian Union ofIndustrialists and Entrepreneurs, a business group with close ties to the Kremlin,announced Sept. 4 that it has sent the central bank its plan for an alternative to theSWIFT interbank payments system.

Building a system would take time and big banks outside Russia might hesitate to joinfor fear of reprisals from the U.S. and the EU — or even from SWIFT itself, since thecooperative’s bylaws forbid members from participating in activities that could harm it.

If Russia were locked out of SWIFT, it could find other ways to move moneyinternationally. The leading trade group for Russian banks says that its members couldtransfer funds by other means, including secure Internet and fax connections. “It is muchless convenient and much more costly for all sides of the process, but it is a realsolution,” says , an official at the .Serge Penkin Association of Russian Banks

Back-channel arrangements couldn’t replace “the security and the volume that SWIFTprovides” for Russia’s $2 trillion economy, says , a senior research fellowRichard Reidwho studies finance and regulation at the University of Dundee in Scotland.

The EU is not rushing to wield SWIFT as a sanctions weapon. The subject wasn’tdiscussed during an Aug. 29-30 summit meeting of EU leaders in Brussels. Germany isworried that a SWIFT ban would create huge costs on both sides, according to a personfamiliar with the EU discussions. “Blocking Russia from the SWIFT system would be avery serious escalation,” says of Moscow-based consulting firm Christopher Weafer

, “and would most certainly result in equally tough retaliatory actions.”Macro-AdvisoryThe EU’s trade with Russia totaled $390 billion in 2013. EU exports to Russia fell 14percent during the first five months of this year as the Ukraine conflict flared.

BY ADI NARAYAN Uber Technologies Inc., maker of the

ride-hailing application that has disruptedtaxi networks around the world, may facea setback in India after the central bankclosed a loophole that let it provide asimpler payment system compared withlocal rivals.

All transactions involving credit cardsissued in India for goods or services inthe country must have an additionalauthentication system at each point ofsale, the Reserve Bank of India said in astatement on Aug. 22. Evasion of theserules by some companies has led to anoutflow of foreign exchange, the RBI said.

Uber, which landed a $17 billionvaluation in its last round of funding,would have to change its app to add anadditional level of authentication or adopta different model to comply with theserules. That would put its cardmanagement on par with local rivalsincluding and Mega Cabs Ltd. Meru Cab

, that have claimed Uber’s trademarkCo.ride-payment system violates Indianforeign-exchange laws, according to areport in the Economic Times daily.

Customers using credit cards to pay fortaxis hailed through local companies,must enter the security code or aone-time-password delivered by textmessage for each transaction, Siddartha

, chief executive officer of Meru,Pahwawhich runs a fleet of about 10,000 radiotaxis in the country, said. Uber’s systemviolates that rule, he said.

Uber’s Asia spokeswoman Evelyn Taydidn't immediately reply to an e-mail.

Uber May Be Blocked inIndia as RBI Tightens Rules

IN BRIEF

PTT Exploration and Production,a subsidiary of , thePTT pclstate-owned oil and gas business, hasbecome the first private Thai companyto get a treasury center license. Thefirst stage of the license coversforeign currency liquidity managementand the company will use the Bank ofThailand’s Automated Cash Pooling, itsaid in an e-mailed statement.

— Tony Jordan

DBS Bank has named John as the head of its GlobalLaurens

Transaction Services. He will replace , who will relocate to theTom McCabe

U.S. to head DBS’s franchise therefrom Oct. 1, the bank said on Sept. 1in an e-mailed statement. Laurenswas HSBC’s Asia-Pacific head ofglobal payments and cashmanagement.

— Sanat Vallikappen

Deutsche Bank has named Peter, formerly head ofMassion

Transaction Banking for Japan atStandard Chartered, as head ofGlobal Transaction Banking, TradeFinance and Cash ManagementCorporates for Deutsche Bank inJapan, according to an e-mailedstatement. The appointment waseffective Sept 1.

— Gearoid Reidy

CHINA CURRENCY

Sept. 10, 2014 Bloomberg Brief Asia Corporate Treasury 3

CHINA CURRENCY

Bank of China Eyes Yuan Deposits in South KoreaBY JIYEUN LEE plans to hire more staff in South Korea and expects yuan depositsBank of China Ltd. in the country to triple to a record $20 billion in 2014 as the two nations start directtrading of their currencies.

The number of employees at the local branch of China’s fourth-largest bank by marketvalue may rise to 160 from 135 by year-end as risk management as well as trading inforeign exchange and derivatives expand, , the lender’s Korea ExecutiveHuang DeOfficer, said in an interview in Seoul.

South Korea’s central bank reported that savings in the Chinese currency rose to anall-time high of $16.19 billion in July, compared with the equivalent of $6.67 billion at theend of 2013. The governments of the two Asian countries agreed on July 3 to make theircurrencies mutually exchangeable in Seoul and conclude free-trade talks by the end ofthis year.

“Despite the jump in yuan deposits here, it’s still at an early stage of development assavings are mostly by financial institutions,” Huang said in his office. “Free tradeagreements can increase yuan usage by South Korean corporates, and consumers canalso be attracted by the higher yields.”

China is South Korea’s biggest trading partner, with shipments amounting to $229billion in 2013, figures from the trade ministry show.

Investors should buy the yuan against the won as the use of Chinese currency in thetwo nations’ bilateral trade surges, according to , head of markets strategyChristy Tanfor Asia at . CNY/KRW will advance to 179 by year-end,National Australia Bankimplying appreciation of more than 7 percent from 167 now, according to Tan. Thatcompares to a forecast for 166 in a Bloomberg survey of strategists.

– Yanping Li and Masaki Kondo

A test program linking the Shanghaishare market with Hong Kong's wentsmoothly, Hong Kong Exchanges

said on Aug. 24.and Clearing Ltd.The mutual market access program,called Hong Kong-Shanghai StockConnect, is due to start within sixmonths of its announcement in Aprilby China's Premier . Li Keqiang “TheHong Kong-Shanghai Stock Connecthas drawn investment demand for theyuan as it signals further opening ofChina’s financial markets,” said Banny Lam, Hong Kong-basedco-head of research at AgriculturalBank of China InternationalSecurities Ltd.

– Fioni Li

Deutsche Bank signed amemorandum of understanding withthe on Aug. 28 for theBank of China clearing and settlement of offshoreyuan in Frankfurt, ,Lothar MeenenDeutsche Bank’s head of tradefinance and cash managementcorporates for Germany said in aninterview. The move aims to increaseliquidity between China and Germany,and support a yuan hub in Frankfurt.Deutsche Bank is the first Germanbank to sign a MoU with the BOC.Clearing contracts with other banksare prepared and ready to beapproved in the coming weeks, saidBernd Meist, who heads BOC’sFrankfurt operations.

– Weixin Zha

The Chinese yuan accounted for1.57 percent of global payments inJuly, up from 1.55 percent in June,according to the Society forWorldwide Interbank Financial

(SWIFT).TelecommunicationsEurope accounted for 10 percent ofyuan payments worldwide by value,and the U.K. ranked first in the regionfor yuan transactions.

– James Regan

IN BRIEF

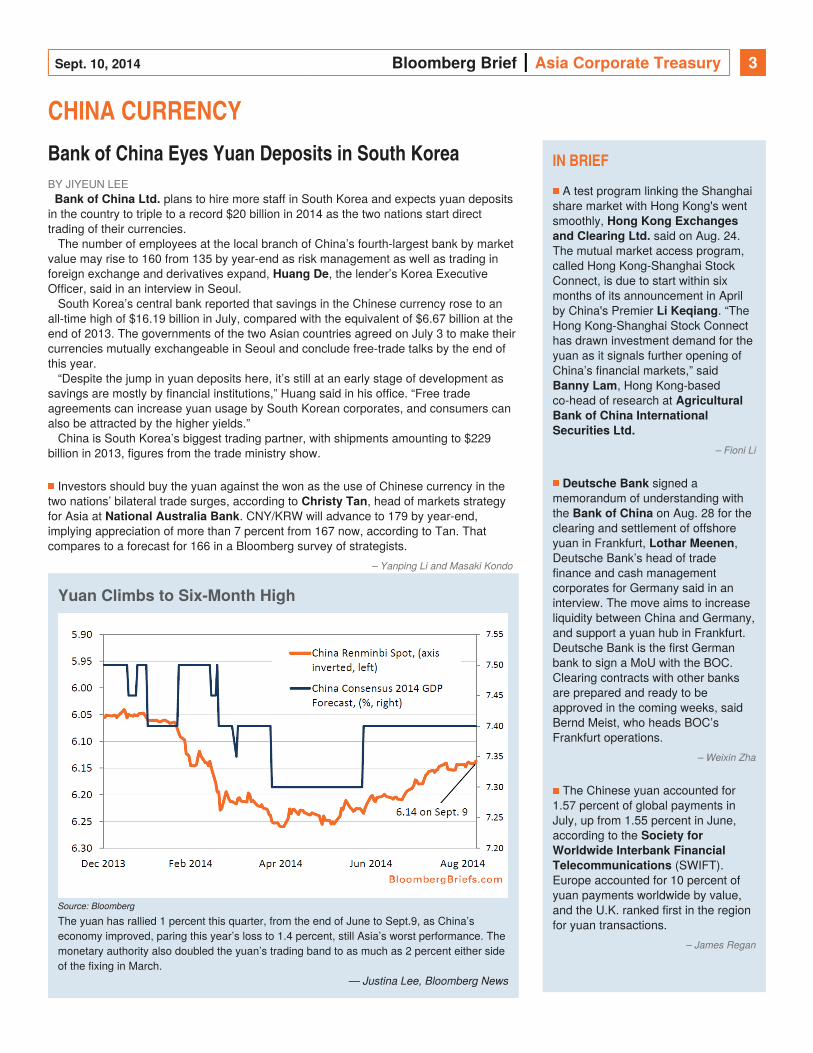

Yuan Climbs to Six-Month High

Source: Bloomberg

The yuan has rallied 1 percent this quarter, from the end of June to Sept.9, as China’seconomy improved, paring this year’s loss to 1.4 percent, still Asia’s worst performance. Themonetary authority also doubled the yuan’s trading band to as much as 2 percent either sideof the fixing in March.

— Justina Lee, Bloomberg News

Sept. 10, 2014 Bloomberg Brief Asia Corporate Treasury 4

SPONSORED CONTENT

China & the International RMB: A New Normal BY SANDIP PATIL, REGIONAL HEAD, GLOBAL LIQUIDITY AND INVESTMENTS, ASIA PACIFIC, TREASURY AND TRADE SOLUTIONS, CITI

China’s leading position on the world economic

stage is now universally acknowledged, and

companies of all sizes and industries are

positioning China at the heart of their growth

strategy. As China becomes increasingly

integrated into global networks, RMB’s role as a

world currency, not only for international trade

but as a treasury, capital and reserve currency is

becoming more strategic. Some companies are

already recognizing that the emergence of a

new world currency will change the way they

conduct their business in China and are

embracing new opportunities to use RMB to

support their business strategy there. However, despite China’s pivotal

position in international trade, a large proportion of corporations have yet to

make the shift and leverage the opportunities to use RMB and include it in

their currency mix, despite the potential benefits of doing so.

Not ‘If’, But ‘When’

Treasurers doing business in China are no longer talking about ‘if’ they will

use RMB, but rather ‘when.' Furthermore, competitors are increasingly taking

advantage of the opportunities that RMB offers, so companies should be

acting sooner rather than later. In March 2014, RMB became the seventh

ranked global payments currency by volume ( ) and is alreadysource: SWIFT

the second currency globally for trade finance after USD at 9 percent of flows,

an achievement considering its zero starting point just a few years ago.

For those that have not yet embarked on their RMB journey, or are at the early

stages, how should they go about it? The logical starting point for most

corporations is to use RMB to settle cross-border trade, whether inbound,

outbound or a combination, an opportunity that has existed since 2009. The

advantages of doing so are well-documented, and include better commercial

conditions (as counterparties’ FX risk is eliminated), greater flexibility in

managing cash, liquidity and risk within China and access to a wider

community of buyers and/ or sellers. Documentation is less onerous when

using RMB rather than foreign currencies, accelerating the business process.

Payment terms can also be more attractive: up to 210 days when using RMB,

compared with 90 days in foreign currency, resulting in obvious working

capital benefits.

Connecting China

Many treasurers are less concerned about settling trade in RMB however,

than how they will manage the resulting surplus or deficit, including managing

funding gaps across legal entities, both within China and cross-border. This

has been a challenging issue in the past, but connecting China within a

regional or global liquidity structure can now bring considerable advantages

for cash-generative businesses and there are now a variety of opportunities to

do so. For example, cross-border on behalf structures, payments netting and

lending/ sweeping are now feasible, and banks such as Citi are experienced in

supporting customers in these techniques. One issue that companies

operating in China need to consider is the disconnect between the RMB

onshore (CNY) and offshore (CNH) markets. For companies with surplus

cash, the onshore market is more liquid and deposit rates are higher. In

contrast, for net borrowers in RMB, offshore borrowing may be cheaper. The

difficulty is that many companies have cash surpluses or deficits at different

times, so our customers rely on Citi as a global bank to advise on the most

appropriate liquidity solution.

As offshore RMB centres in Singapore, London and Taipei develop, in addition

to Hong Kong, liquidity pools are gradually deepening and the range of

available liquidity and risk management instruments is growing. Pretty soon,

treasurers should be able to manage CNH in the same way as any other

international currency which eases the way that business is conducted with

China. At Citi, we have standardized RMB rates across trading centres, and

established a cohesive network of RMB business managers to help our

customers reduce the cost of doing business in China, support effective

trading relationships and manage currency and liquidity risk effectively.

Taking a consistent approach

Just as managing RMB liquidity both domestically and cross- border is

becoming easier, opportunities to set up efficient

Continued on next page...

Manage RMB liquidity in the offshore market — evaluating either investment or funding options

Ensure controls in encapsulating on cross border sweeping without adversely affecting working capital management in China

Cross border controls in China are not yet fully relaxed, and therefore having controls in place in ensuring compliance

Review risk management of different yield curves

While pricing can be more volatile than onshore, depending on market liquidity, CNH borrowing is becoming increasingly compelling as liquidity in other

markets continues to be constrained and investor appetite for CNH continues strongly.

Top tips on embarking on the RMB journey

Sept. 10, 2014 Bloomberg Brief Asia Corporate Treasury 5

Continued from previous page...

SPONSORED CONTENT

cash management processes are also increasing. Through free trade zones,

companies can now centralize payments processing through an SSC or

payments factory using on-behalf structures and perform payments netting,

enabling companies to centralize and streamline payments in a way that is

more or less consistent with other regions than in the past.

There still remain some challenges; for example, regulatory conditions exist in

settling transactions and processes are less automated than when using

established cross-border trading currencies such as USD, but significant

progress is being made.

Approaching the final stage

As developments in cross-border trade and liquidity increase, the final step in

the RMB becoming the default currency for multinationals doing business in

China is its development as a capital currency. With cross border controls still

in place, onshore and offshore markets cannot converge, and with restrictions

on foreign direct investment, RMB is still in a nascent stage of becoming a risk

and capital currency. While there are changes underway, allowing transfers of

RMB between China and offshore centers have certain conditions. As the

obstacles to RMB becoming a capital currency reduce, we are likely to see

substantial growth in the number of corporations, banks and governments

including holding RMB as a reserve currency. This will cement its importance

as a world currency.

An experiment in free trade

The journey towards liberalization has accelerated recently with the launch of

the China (Shanghai) Pilot Free Trade Zone (SFTZ) in September 2013.

Although its scope is currently limited, several pilot programs will be expanded

nationwide. (Further details are expected.)

The SFTZ covers nearly 29 square kilometers and aims to stimulate trade and

investment, accelerate functional, administrative and regulatory transformation

and provide experience and insights into the opportunities and challenges of a

free economy. As a relatively new venture, there remain some issues requiring

clarification and not every organization is eligible, nor would necessarily

benefit from opening an entity in the SFTZ; yet, for select companies, the

advantages could be material. Significantly, the SFTZ represents a major step

towards liberalization in China and could prove a catalyst for wider RMB

capital account convertibility, interest rate liberalization and RMB

internationalization.

Act now, adjust later

Even if economic growth in China experiences periodic slowdowns, which is

inevitable as the economy matures, China will undoubtedly continue to

strengthen its position as a dominant global trading partner. As the journey

towards RMB liberalization progresses, RMB is becoming a strategic global

currency both for doing business in China and more widely. For example,

there will increasingly be demand to settle trade transactions in RMB between

counterparties that do not use USD as their base currency. While the benefits

will differ by organization, ultimately it will be better to learn the game now

rather than be beaten later. Citi works with customers to phase their RMB

adoption in a way that is appropriate to their business and that facilitates,

rather than interrupts, their strategic ambitions in China. There will

undoubtedly need to be adjustments and revisions in companies’ RMB

strategy over time, particularly as regulatory revisions offer new opportunities,

but adopting RMB is critical to cementing a company’s competitive position

both within China and potentially globally. This is inevitable and this is the time

to experiment with the internationalizing RMB and China.

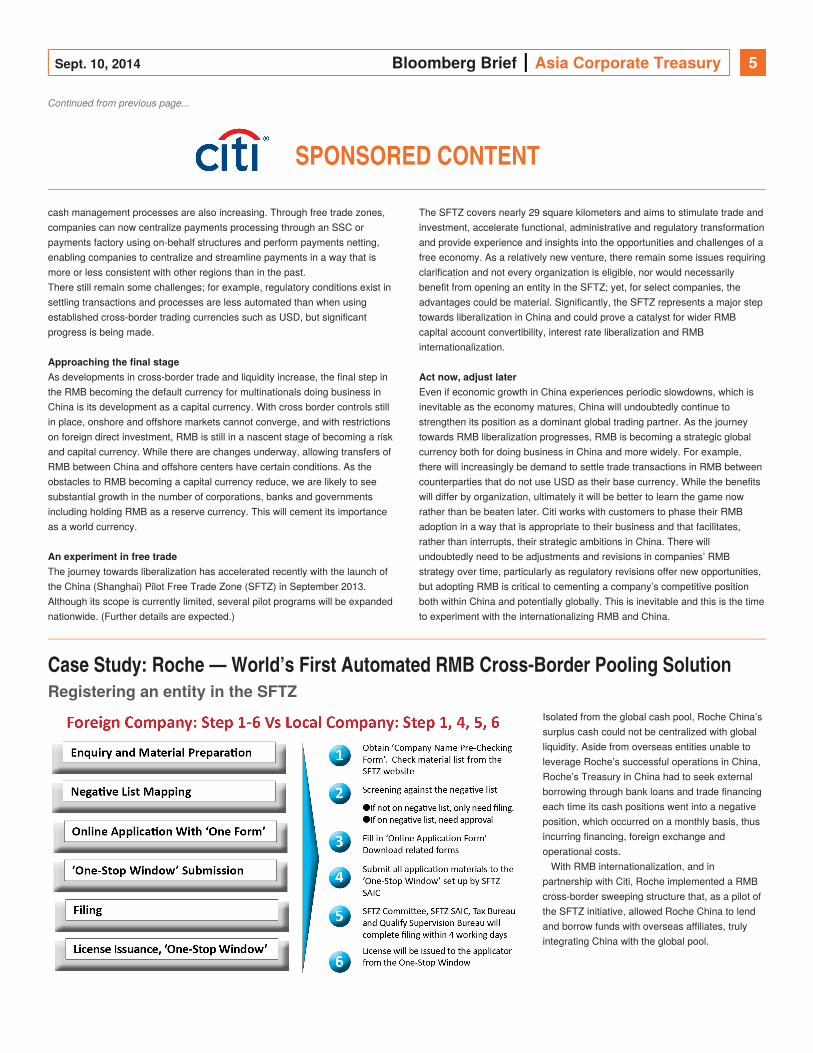

— Case Study: Roche World’s First Automated RMB Cross-Border Pooling Solution

Isolated from the global cash pool, Roche China’s

surplus cash could not be centralized with global

liquidity. Aside from overseas entities unable to

leverage Roche’s successful operations in China,

Roche’s Treasury in China had to seek external

borrowing through bank loans and trade financing

each time its cash positions went into a negative

position, which occurred on a monthly basis, thus

incurring financing, foreign exchange and

operational costs.

With RMB internationalization, and in

partnership with Citi, Roche implemented a RMB

cross-border sweeping structure that, as a pilot of

the SFTZ initiative, allowed Roche China to lend

and borrow funds with overseas affiliates, truly

integrating China with the global pool.

YIELD CURVES

Registering an entity in the SFTZ

Sept. 10, 2014 Bloomberg Brief Asia Corporate Treasury 6

YIELD CURVES

Asia Interest Rates Show TighteningInterest rates in Asia show a slight tightening bias, implying an

average rise of 0.29 percent during the next one year. This termpremium seems appropriate to economic fundamentals as theaverage implied global move (which includes Europe), one yearout, is 0.18 percent.

Chinese rates markets are re-normalizing. One-year ratesonshore have been relatively steady at about 3.6 percent, whileimplied one-year offshore rates have risen to 2.4 percent from 1percent in April. These markets are likely to converge as QFIIquotas are relaxed.

— Yoon Chang, Application Specialist, Emerging Markets Interest Rates and

Foreign Exchange, Bloomberg

USD

JPY CNY

SGD AUD

* Current vs. six months ago for SWAP, investment grade and high yield rates. Current as of Sept. 4, 12:00 EDT.

Q&A

Sept. 10, 2014 Bloomberg Brief Asia Corporate Treasury 7

Q&A

Regulatory Reforms Spur Centralization of Corporate Treasury Functions

David Blair spoke to Bloomberg Brief editor

Justine Bornstein about treasury issues global and

local. Blair stared his career with Price

Waterhouse and later ran treasury departments at

ABB, Nokia and Huawei. He talks about how

macro issues and regulations affect treasurers,

and where Asia is leading the way.

Q. What are the main macro issuesfacing corporate treasurers thesedays? A. Number one has to be post-GFCregulatory change. Regulators are tryingto create a safe banking system. Safeseems to mean holding sovereign debtand possibly housing. This leavesbusinesses starved for funding, hence themassive build-up of cash on corporatebalance sheets and the pervasive movefrom bank funding to bond issuance.

Dodd-Frank and EMIR introducecomplications into important hedgingprograms. The requirement to registertrades is a hassle exacerbated bydivergent regulatory regimes. If MNCshave to collateralize trades, this willintroduce potentially disastrous cash flowvolatility — one airline calculated that itsfuel hedging program would havebankrupted it multiple times whenback-testing the impact of margin calls.

Treasurers are responding to theserisks with an increased emphasis on cashvisibility and forecasting. That andincreasing regulatory burdens are drivingmore centralization — of data andoperational processes, if not decisionmaking — aided by the ease of accessbrought by cloud computing and surgingcomputing resources. Thesedevelopments aid treasurers in their goalof containing risk and reducing costs.

Q: Are there any issues that affectcorporate treasurers in Asia, inparticular?

Treasurers in Asia deal with globalA. issues as well. We can add some twists.Last year’s "taper tantrum" (whenBernanke tried to taper quantitative

easing) wreaked havoc on manyemerging markets. Fortunately, this wasshort lived. It showed that these marketsare vulnerable to G3 policy changes,which heightens uncertainty both in termsof access to funds and in terms of risk.

When Asian treasurers used to talkabout regulations, they meant exchangecontrols, customs and tax in developingmarkets. At a time when those kinds ofregulations are steadily improving — thebest example is China opening up crossborder CNY for companies — Asiantreasurers are now facing a regulatorytsunami from western authorities.

This is accelerating, albeit slowly, theroll out of treasury management systemsand effective cash management in theregion. Asian treasurers are playing catchup with their western peers.

Q: You’ve mentioned that the regulatory environment is not astightly monitored on some levels asthe U.S. and Europe. Examples?A: In terms of DF and EMIR, you can saythey have not yet arrived in Asia. Localregulators are drafting derivativeregulations, and these efforts look likely toincrease complexity. But most derivativereporters in Asia are local treasuries ofwestern MNCs.

So, broadly, yes, derivative regulationhas not hit Asia. We are all scrutinizingthe clouds on the horizon to determinewhether it will be a shower or a typhoon.

Q: In some areas, however, there ismore regulation. What special issues

does that raise for corporates doingbusiness in Asia?

Several Asian countries haveA: exchange controls and non-convertiblecurrencies. This, together with tax issues,

causes a lot of trapped cash in Asia.Asian treasurers have long experiencewith these problems, and they areincreasingly well managed.

It does mean that it can be hard to fundAsian operations when you need localcurrency. Another sub-optimization iscaused by restrictions on intercompanyfunding. India’s new companies act (sofar) seems to have made intercompanyfunding almost impossible. In that case,Asian treasurers can see countries whereone subsidiary has to borrow from localbanks while another subsidiary has todeposit with local banks. Good for banks,very bad for corporates.

Q: Are there any areas where Asia is out front?

Asian central banks are upgradingA: clearing systems extensively – largelyleapfrogging developed markets.ISO20022 based clearing systems arerolling out all over the region. (And yes itdoes handle non-Roman character sets.)Immediate or near real time low valuepayments are becoming more commonthan in the west.

This is benefiting corporates as well.There has been a substantial move fromchecks to electronic payments; in valueterms the majority is already there. Onebank has even set up a team to helpclient paper-to-electronic (P2E)transitions, calling vendors to get theirbanking details and making sure theseare correctly recorded in ERPs,persuading customers to payelectronically, and so on.

Intra-regional trade in Asia has becomebigger than global trade. Asian corporatesand banks were the first to use SWIFT’sTSU and BPO solutions. Supply-chainfinance is very active here.

Age: 53 Singapore GenevaBased in: Hometown: Degrees: BA Hons, FCCA, MCTFavorite recent movie: "Cloud Atlas"Recommended book: Self Comes to Mind (Antonio Damasio)Best recent vacation: Diving with manta rays in Lembonganwith my kidsFavorite sports team: Ashtanga Yoga Research Institute,Mysore

SYNDICATED LENDING

Sept. 10, 2014 Bloomberg Brief Asia Corporate Treasury 8

SYNDICATED LENDING

Deal Flow Slows As Deal Size Grows in AugustSyndicated loan volume in the

Asia-Pacific region outside Japandropped 46 percent to $16.7 billion inAugust compared with the same period ayear earlier as deal-flow slows, accordingto data compiled by Bloomberg.

Average deal size in the region was$341 million in August, Bloomberg datashow. That compared with $329 million inthe same period of last year. Alibaba

Group Holding Ltd., which is expected toraise as much as $20 billion in its U.S.IPO, completed the biggest loan in theregion this month with a $3 billionrevolver, the data show.

Average interest margins charged forU.S. dollar-denominated loans shrank to230 basis points at the end of August,compared with 266 basis points at theend of 2013, the data show.

Leading the league tables year to dateis State Bank of India with a 9.8 percentmarket share, followed by ANZ at 6.7percent and HSBC at 5 percent. Bank ofChina is next with a 4.8 percent marketshare while National Australia Bank takesthe fifth spot with 4.5 percent.

Asia-Pacific ex-Japan 2014YTD MLA Ranking

RANKING BANKSMARKET

SHARE (%)

1 State Bank of India 0.098

2 ANZ Banking Group 0.067

3 HSBC Bank PLC 0.05

4 Bank of China 0.048

5National Australia BankLtd

0.045

6Commonwealth BankAustralia

0.042

7 Westpac Banking 0.041

8Sumitomo MitsuiFinancial Group Inc

0.034

9Standard CharteredBank

0.032

10 Mitsubishi UFJ Financial 0.029

Deal Type Comparison

USD Bln in2014

2014%

2013%

DomesticCurrency

$174.68 57.2% 56.8%

RefinancePurpose

$102.83 33.7% 42.1%

Club Deals $98.21 32.1% 29.4%

All data from the Bloomberg Asia-Pacific

Syndicated Loans team

Top Deals in 2014 YTD by Country

COUNTRY BORROWER DATE AMOUNT (Mln)

Australia Roy Hill Iron Ore Project Mar-14 USD 7,600

China Cnooc Jun-14 USD 1,500

Hong Kong Hongkong Electric Jan-14 HKD 37,000

India Abg Shipyard Mar-14 INR 160,408

Indonesia Trans Retail Mar-14 USD 1,275

Korea Youngchun-Sangju Highway Jun-14 KRW 1,430,000

Malaysia Sapurakencana Tmc Mar-14 USD 5,500

Singapore Oversea Chinese Banking Mar-14 HKD 38,712

Taiwan Chunghwa Picture Tubes May-14 TWD 22,800

Thailand Cp All Mar-14 THB 81,900

Philippines Pagbilao Expansion Project May-14 PHP 33,309

HEDGE ACCOUNTING BY EVA DE LEON, BLOOMBERG CORPORATE TREASURY SPECIALIST

Asia-Pac Ex Japan Syndicated Loans Volume

Sept. 10, 2014 Bloomberg Brief Asia Corporate Treasury 9

HEDGE ACCOUNTING BY EVA DE LEON, BLOOMBERG CORPORATE TREASURY SPECIALIST

Closing the Gap Between Risk Management and Hedge AccountingAfter five years and more than 1,000

comment letters from stakeholders, IFRS9 is now complete. The new FinancialInstruments Accounting Standard is amajor overhaul of its predecessor, IAS 39,often viewed as too stringent and notaligned to risk management.

In June, Patricia McConnell, a boardmember of the International AccountingStandards Board, wrote: “The new hedgeaccounting model more closely alignsaccounting for hedging activities with acompany’s risk management strategies,and provides improved information aboutthose strategies.”

Under IAS 39 rules, certain hedgingstrategies considered as true economichedges did not qualify for hedgeaccounting. There were inconsistenciesor biases with the qualifying criteria forcertain "hedgeable" risks. For example, itrestricted hedging the components of anon-financial item while allowing it forfinancial items — significant forcorporates that hedge their commodityexposure.

In addition, certain strategies areprecluded as IAS 39 does not allow aderivative to form part of the underlying

hedge item. A company could issue afixed-rate foreign currency (FCY) bondand correspondingly enter into afixed-floating cross currency interest rateswap (CCIRS), converting it to functionalcurrency. This is designated a fair valuehedge. The company could then decide tolock in the interest rate by entering into afloating-fixed interest rate swap (IRS),converting the interest rate exposure to afixed rate. IAS 39 doesn't allow combining

the FCY bond and the CCIRS trade as anunderlying floating rateexposure, so the second derivative (floating-fixed IRS) cannot be designatedas a hedge and must be accounted for inearnings.

Restrictions on designating the full fairvalue of purchased options (only theintrinsic value applied) for hedgeaccounting purposes dissuaded a numberof corporates from using option-basedstrategies.

IFRS 9 has addressed these and otherlimitations and is seen as a significantlessening of the gap between hedgeaccounting and risk managementpractices. The new standard broadenedthe scope on eligible hedged items, so

more types of strategies can qualify forhedge accounting. For example,component hedging is now possible, somanufacturing companies and airlinescan hedge their commodity risk exposure.

The removal of the bright-line test isgood news; it doesn't fully eliminate theneed to quantify and monitor a company’srisk management activity and itseffectiveness. It introduced the concept ofsetting a ‘hedge ratio’ and an assessmentthat the effect of credit risk does notdominate the change in value. It doesallow companies a more flexible approachon how to assess the effectiveness oftheir hedges, in line with their riskmanagement program. There is still therequirement to prove the credit riskassessment quantitatively in certaincases.

Overall, IFRS 9 provides relief tocorporates on hedge accounting as itcovers more scenarios and allowsaccounting treatment that best reflects theeconomic reality of their risk managementactivities. The changes could drivecorporates to hedge more or broaden thetypes of instruments used.

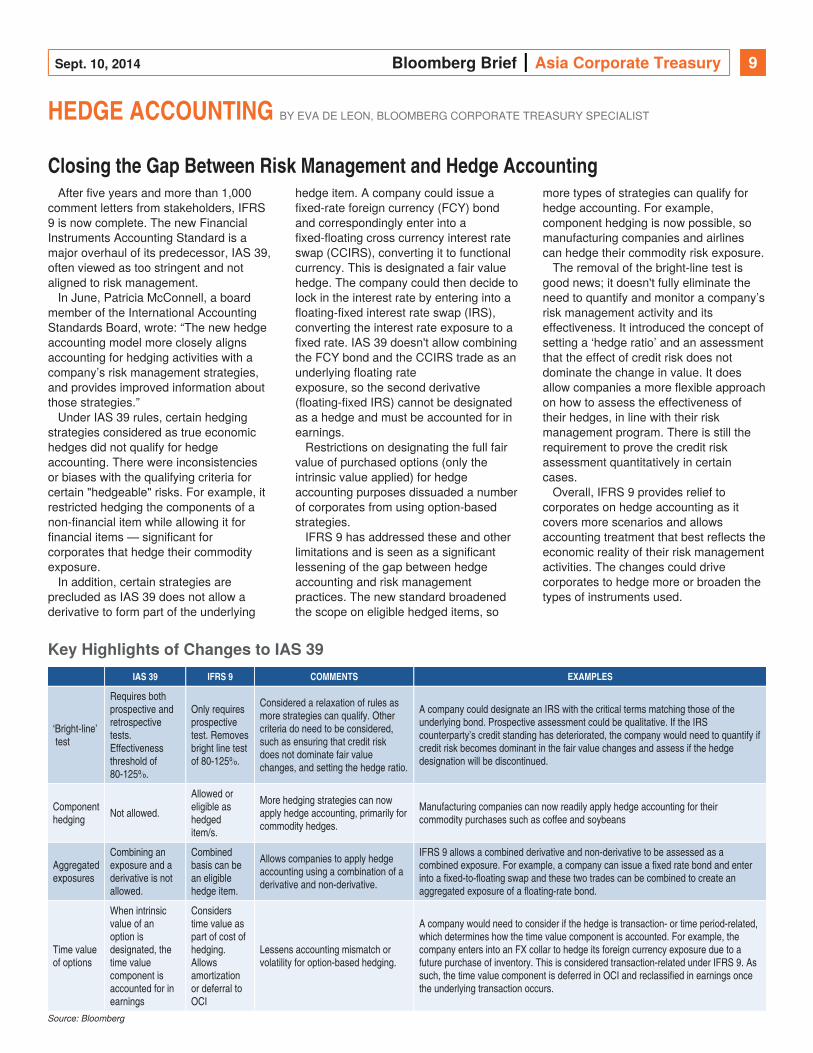

Key Highlights of Changes to IAS 39

IAS 39 IFRS 9 COMMENTS EXAMPLES

‘Bright-line’ test

Requires bothprospective andretrospectivetests.Effectivenessthreshold of80-125%.

Only requiresprospectivetest. Removesbright line testof 80-125%.

Considered a relaxation of rules asmore strategies can qualify. Othercriteria do need to be considered,such as ensuring that credit riskdoes not dominate fair valuechanges, and setting the hedge ratio.

A company could designate an IRS with the critical terms matching those of theunderlying bond. Prospective assessment could be qualitative. If the IRScounterparty’s credit standing has deteriorated, the company would need to quantify ifcredit risk becomes dominant in the fair value changes and assess if the hedgedesignation will be discontinued.

Componenthedging

Not allowed.

Allowed oreligible ashedgeditem/s.

More hedging strategies can nowapply hedge accounting, primarily forcommodity hedges.

Manufacturing companies can now readily apply hedge accounting for theircommodity purchases such as coffee and soybeans

Aggregatedexposures

Combining anexposure and aderivative is notallowed.

Combinedbasis can bean eligiblehedge item.

Allows companies to apply hedgeaccounting using a combination of aderivative and non-derivative.

IFRS 9 allows a combined derivative and non-derivative to be assessed as acombined exposure. For example, a company can issue a fixed rate bond and enterinto a fixed-to-floating swap and these two trades can be combined to create anaggregated exposure of a floating-rate bond.

Time valueof options

When intrinsicvalue of anoption isdesignated, thetime valuecomponent isaccounted for inearnings

Considerstime value aspart of cost ofhedging.Allowsamortizationor deferral toOCI

Lessens accounting mismatch orvolatility for option-based hedging.

A company would need to consider if the hedge is transaction- or time period-related,which determines how the time value component is accounted. For example, thecompany enters into an FX collar to hedge its foreign currency exposure due to afuture purchase of inventory. This is considered transaction-related under IFRS 9. Assuch, the time value component is deferred in OCI and reclassified in earnings oncethe underlying transaction occurs.

Source: Bloomberg

FOCUS: COMMUNICATIONS INDUSTRY WORKING CAPITAL

Sept. 10, 2014 Bloomberg Brief Asia Corporate Treasury 10

FOCUS: COMMUNICATIONS INDUSTRY WORKING CAPITALThe advertising revenue rebound since

2010 has substantially boosted theoperating and free cash flow of mediacompanies, enhancing their liquidities.

Media companies historically generatepositive working capital as there is very little inventory and the cash turnover cycleis quite short. They have high operatingleverage and minimal capital spending.

Telecom companies have greater working capital needs and more

substantial capital spending relative to other communications sectors.

— Paul Sweeney, U.S. Director of Research,

Media, Entertainment and Internet,

Bloomberg Intelligence

Ranking Breakdowns

The rankings are derived from the largest 980

public and private companies, by market

capitalization, according to the BICS classification

for communications. All company accounts were

converted to IFRS or U.S. GAAP for consistency.

Some companies do not report all data or years.

FOCUS: COMMUNICATIONS INDUSTRY FUNDING (ASIA)

Working Capital/Sales by Sub-Sector

Free Cash Flow/Sales by Sub-Sector

By Number of Companies

By Revenue

By Number of Companies,Region

Sept. 10, 2014 Bloomberg Brief Asia Corporate Treasury 11

FOCUS: COMMUNICATIONS INDUSTRY FUNDING (ASIA)Companies have preferred to access

funds through lending, instead of bond,markets. Japanese corporates were thelargest borrowers, and yen the most usedcurrency. Australia and India corporatesregularly use this market for funding, too.

The 2014 run rate suggests this yearwill see local bond issuance outstripsyndicated lending, driven in large part byChinese corporates' issuance.

Bond issuance tends to be morecommon in countries with larger, liquidbond markets, of which Japan, Australiaand Korea have been the largest.

Lending by Currency

CURRENCYMARKET

SHARE (%)ISSUES

LOANTRANCHESIZE (Mln)

JPY 35.57 69 $62,443

USD 16.28 149 $28,569

INR 13.48 39 $23,658

AUD 10.03 64 $17,602

NZD 4.10 18 $7,191

IDR 3.40 46 $5,964

HKD 3.30 14 $5,800

THB 2.93 17 $5,139

SKW 2.87 65 $5,040

SGD 2.46 6 $4,318

MYR 1.97 12 $3,451

TWD 1.70 21 $2,988

PHP 0.91 35 $1,591

CNR 0.35 11 $621

Source: Bloomberg

Bond Issuance by Currency

CURRENCYMARKET

SHARE (%)ISSUES

AMTOUTSTANDING

(Mln)

JPY 26.19 57 $24,343

USD 24.35 45 $22,627

CNR 12.92 78 $12,004

SKW 10.78 267 $10,015

EUR

8.38 9 $7,788

INR 3.79 40 $3,518

AUD 2.71 9 $2,522

THB 2.20 27 $2,045

MYR 1.89 34 $1,756

TWD 1.31 13 $1,216

PHP 1.20 19 $1,111

IDR 0.96 11 $890

SGD 0.93 4 $863

HKD 0.72 12 $671

Source: Bloomberg

BANK RANKINGS BY SHAN ANWAR, BLOOMBERG CORPORATE TREASURY SPECIALIST

Communications Sector Borrowing by Country

Communications Sector Bond Issuance by Country

N.B. The Communications sector is classified as Cable & Satellite, Entertainment, Media(Non-Cable), Wireless Telecoms Services and Wireline Telecoms Services. Analysis is ofAsia-based corporates, including local companies and local subsidiaries of multinationalcompanies.

Sept. 10, 2014 Bloomberg Brief Asia Corporate Treasury 12

BANK RANKINGS BY SHAN ANWAR, BLOOMBERG CORPORATE TREASURY SPECIALIST

Bloomberg Ranking of Main Corporate Treasury Banks' Financial StrengthBloomberg created an overall score of major players in transaction banking and treasury services based on seven numerical indicators.Credit and liquidity measures each comprise 40 percent of the score. Performance metrics comprise 20 percent. The list is filtered formajor players in transaction banking/corporate treasury services. Each bank is ranked from best to worst. Data is as of Sept. 9, 2014.

Notes:

1) Bloomberg default risk scale: Rates from Investment Grade (IG) to High Yield (HY) based on default probability. See for more information.DRSK<GO>

2) Day 1 CVA Charge: Credit Valuation Adjustment is calculation of a 5-year pay float — receive fixed $100 Mln interest rate swap on Sept. 3, 2014.

3) Excess Tier 1 Capital Ratio: The amount of the Bank's tier 1 capital ratio above the Basel requirement of 6 percent.

Swaps Rule Requires $644 Billion in Collateral, Regulator Says BY SILLA BRUSH AND JESSE HAMILTON

U.S. banks would need $644 billion in collateral to offset risksin swaps traded among themselves, according to an analysis ofrules re-proposed by regulators.

The Office of the Comptroller of the Currency laid out estimatedcosts for companies including JPMorgan Chase & Co., Bank ofAmerica Corp. and Citigroup Inc. to support trades that won’t beguaranteed by clearinghouses.

Under revised rules for non-cleared swaps issued by the OCC,Federal Reserve and Federal Deposit Insurance Corp., bankswould have to finance collateral and hold it in custody accountsthat may be less profitable than other uses. As a result, OCCeconomists estimate the requirement will cost the bankingindustry between $2.9 billion and $6.4 billion annually once therules are fully in place in 2019.

U.S. banks and their clients would need to have about $300billion in initial margin to offset risks in the trades, according toindustry and regulator estimates cited by the Fed.

U.S. and overseas regulators have sought to increaseoversight of the $710 trillion global swaps market since largelyunregulated trades helped fuel the 2008 credit crisis and forced abailout of American International Group Inc. For swaps thatremain non-cleared and traded directly between buyers andsellers, regulators have proposed standards for requiring banksand their clients to exchange collateral to prevent risks frombuilding up in the market.

The nine national banks and six foreign-bank branches affectedby the proposal would face about $659 million in administrativecosts to get the system up and running, and another $149 milliona year to comply with the rule, according to the estimate.

Bloomberg Brief: Asia Corporate TreasuryTed Merz

Newsletter

Executive Editor

Jennifer Rossa

Newsletter

Managing Editor

Justine Bornstein

Brief Editor

jbornstein6@

bloomberg.net

Paul Smith

Brief Editor

Nick Ferris

Newsletter

Business Manager

©2014 Bloomberg LP. All rights reserved.