asia quarterly - mizuho bankasia quarterly –- q1/q2 2020 1 - executive summary us: the...

TRANSCRIPT

Asia Quarterly ― Q1-Q2 2020: Blindsided ―

9th April 2020 Mizuho Bank, Ltd.

Asia and Oceania Treasury Department

Vishnu Varathan

Head, Economics & Strategy

Lavanya Venkateswaran

Market Economist

Zhu Huani

Market Economist

A weary global economy just beginning to heave a sigh of relief from US-China trade

conflict de-escalation (“Phase-1” deal) has been blindsided by the COVID-19 pandemic.

Unprecedented in every way, global policy-makers do not have the luxury of pulling punches

with – often having to swing blindly at –this invisible, and little understood adversary that has

hijacked economic activity and upended social interactions/norms as we know it.

Attacking in waves, the economic side-effects are grim. The social distancing that is required to

control an unmitigated spread, and resultant seizure in activity inflicts a jarring revenue shock

to businesses; impacting adversely from both the supply- and demand-side.

The challenge for policy-makers all over is to short-circuit the nefarious (liquidity-credit)

spiral from a liquidity/cash-flow seizure (from revenue shocks) to a credit crunch that

cascades into a solvency crisis; and eventually job losses, which is far harder to reverse.

The deluge of liquidity/credit facilities, complementing steep rate cuts, alongside

unprecedented fiscal bazookas enhance policy transmission. But may still fall short of

preventing a global recession. The hope is that policy efforts will help blunt the depth and

duration of the recession. But for now we fly blind.

Asia Quarterly – Q1/Q2 2020

- 1 -

Executive Summary

US: The “corona-crisis” (COVID-19 pandemic) blindsided, triggering

unprecedented largesse to mitigate recession risks. Fiscal stimulus north of 10% of

GDP, ZIRP, “QE infinity” and liquidity/credit kitchen sink are all fair game.

EZ: Fears of a deep recession in Europe has tamed German fiscal hawks and ramped

up ECB stimulus led by QE (APP, PEPP); with self-imposed country limits discarded.

Japan: The pandemic has postponed Tokyo Olympics to summer 2021, and jolted

the Abe government into a 20% of GDP fiscal fillip along with expanded QQE. .

China: With Wuhan as the epi-centre, a brutal seizure in economic activity started

in China, and may result in an unprecedented economic contraction in H1; but with

China pulling all stops, scope for a turnaround later in 2020 remains.

To be clear, even as China resumes activity in Q2, Europe and US locking down

will inevitably frustrate any chance of (even a fleeting) V-shaped recovery. Most

worrying are being blindsided by of second-round infections.

India’s initial relief of being spared infection has proven illusory. Containing the

spread while the correct policy priority will extract an economic toll, exacerbating pre-

existing economic pain associated with banking impediments and confidence shortfall.

Indonesia’s adoption of unprecedented fiscal measures along with monetary

policy support is justified by the scale of the COVID-19 outbreak.

Weakness in South Korea’s domestic sector is inevitable despite the absence of

country-wide lockdown. Challenging external environment on top of slowing

domestic demand due to lockdowns is set to drag Vietnam’s growth to a multi-

year low.

Singapore: 12% of GDP fiscal boost will relieve pain but not prevent a downturn

as travel, supply-chain, financial channels conspire. Malaysia’s economy will be

hit by the triple blow of the pandemic, volatile commodity prices and political

uncertainty.

Growth in Thailand is dragged down by sharp slowdown in tourism activities and

tepid domestic demand due to restrictive lockdown measures. Philippines’ pain

will be exacerbated by the lockdown of the Luzon island.

Australia: The RBA pulling all stops with YCC should help cushion the economic

slide. But commodity- and China channels will tend to amplify shocks; and a

weak AUD may have somewhat diminished efficacy as a shock absorber.

AXJ: Despite rock bottom UST yields and unrestrained QE, a weak USD is not a

given. Risk aversion will tend to keep FX markets volatile, amid a tendency for

capital outflows and AXJ slippage; as USD remains the ultimate refuge.

Asia Quarterly – Q1/Q2 2020

- 2 -

AT A GLANCE

Yearly Economic Forecasts

GDP YoY CPI C/A (% GDP) GDP YoY CPI C/A (% GDP) GDP YoY CPI C/A (% GDP) GDP YoY CPI C/A (% GDP)

United States 2.9 2.5 -2.4 2.3 1.8 -2.3 -1.2 1.1 -2.6 2.2 2.1 -2.5

Eurozone 1.9 1.8 3.1 1.2 1.1 2.7 -3.3 0.4 2.8 1.9 1.5 3.0

Japan 0.3 1.0 3.5 0.7 0.5 3.4 -1.4 0.3 3.6 1.4 0.6 3.1

ASIA (ex-Japan) 6.2 2.6 0.4 4.2 1.9 1.2 1.6 1.3 1.9 4.3 2.1 2.1

ASEAN-6 5.1 2.7 1.4 4.5 2.0 1.8 1.3 2.1 1.2 4.7 2.4 1.4

China 6.6 2.1 0.2 6.2 2.9 1.2 2.4 1.6 2.6 6.3 2.9 2.1

India 7.3 3.9 -2.4 5.3 (4.7) 3.7 (4.7) -0.9 3.2 (3.4) 3.6 (2.6) -0.6 5.4 (5.7) 3.5 (3.7) 1.4

Korea 2.7 1.6 4.7 2.0 0.4 3.0 0.7 0.9 3.4 2.9 1.3 3.6

Singapore 3.2 0.4 17.2 0.7 0.5 17.0 -2.8 -0.9 18.8 3.9 1.3 17.6

Malaysia 4.7 1.0 2.1 4.3 0.7 3.3 0.7 1.3 1.8 4.1 1.5 3.4

Indonesia 5.2 3.2 -2.9 5.0 2.8 -2.7 2.0 2.9 -2.9 4.7 3.0 -2.5

Thailand 4.1 1.1 7.4 2.4 0.7 6.8 -1.3 0.1 4.3 3.5 1.1 5.5

Philippines 6.2 5.2 -2.7 5.9 2.5 -0.1 2.5 2.4 1.4 6.0 3.0 -1.1

Vietnam 7.1 3.8 2.9 7.0 2.8 3.0 4.2 4.7 1.7 6.9 3.4 2.5

Australia 2.8 1.9 -2.1 1.7 1.6 0.7 0.7 0.8 0.4 2.4 1.9 -1.1

Note: Asia (ex Japan) includes China, India, South Korea, Singapore, Hong Kong, Taiwan, Malaysia, Indonesia, Thailand, Philippines, Vietnam

The forecasts in this table do not account for severe trade protectionism outcomes.

2018 2019 20212020Country

Quarterly Outlook – Growth and Consumer Inflation

Growth Forecasts GDP Growth Forecasts

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

China -4.2 2.1 4.0 6.2 11.2 6.8 5.5 3.4 6.2 2.4 6.3

India 3.7 2.3 2.8 3.8 4.6 6.0 6.0 5.7 5.3 (4.9) 3.2 (3.4) 5.4 (5.7)

Korea 0.3 0.1 1.0 1.2 3.1 3.1 2.7 2.7 2.0 0.7 2.9

Singapore -2.2 -5.7 -3.9 0.8 3.4 7.1 4.1 1.2 0.7 -2.8 3.9

Malaysia 0.3 -0.4 1.2 1.6 3.9 4.2 4.3 4.3 4.3 0.7 4.1

Indonesia 3.9 1.0 1.5 1.6 3.3 4.9 5.0 5.5 5.0 2.0 4.7

Thailand -2.7 -4.0 0.3 1.3 3.3 4.2 3.3 3.0 2.4 -1.3 3.5

Philippines 3.8 0.7 1.5 4.1 5.6 6.9 6.3 5.4 5.9 2.5 6.0

Vietnam 3.8 3.0 4.4 5.5 7.1 7.0 6.7 6.6 7.0 4.2 6.9

Australia 0.9 -1.2 1.4 1.8 2.4 3.2 1.9 2.1 1.7 0.7 2.4

2021 2019

(FY19/20)

2020

(FY20/21)

2021

(FY21/22)Country

2020

Consumer Inflation forecasts Inflation Forecast

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

China 1.8 2.6 2.9 4.3 3.9 1.3 1.1 0.3 1.0 3.4 3.5 3.5 2.9 1.6 2.9

India 2.5 3.1 3.5 5.8 6.5 2.7 3.0 2.5 2.4 4.3 3.8 3.6 3.7 (4.7) 3.6 (2.6) 3.5 (3.7)

Korea 0.5 0.7 0.0 0.3 1.2 0.6 0.9 1.0 1.0 1.4 1.3 1.5 0.4 0.9 1.3

Singapore 0.5 0.7 0.4 0.6 0.1 -1.7 -1.2 -0.7 0.2 1.8 1.8 1.4 0.5 -0.9 1.3

Malaysia -0.3 0.6 1.3 1.0 1.5 1.4 1.2 1.2 1.5 1.5 1.5 1.7 0.7 1.3 1.5

Indonesia 2.7 2.9 3.0 2.7 2.9 3.0 2.8 2.8 2.9 3.0 3.1 3.1 2.8 2.9 3.0

Thailand 0.7 1.1 0.6 0.4 0.4 -0.6 0.1 0.5 0.9 1.6 1.1 0.9 0.7 0.1 1.1

Philippines 3.8 3.0 1.7 1.5 2.7 2.1 2.3 2.6 2.8 2.9 3.1 3.1 2.5 2.4 3.0

Vietnam 2.6 2.7 2.2 3.7 5.6 5.0 4.7 3.5 2.8 3.2 3.4 4.0 2.8 4.7 3.4

Australia 1.3 1.6 1.7 1.8 0.6 0.4 1.0 1.2 1.6 1.8 1.9 2.1 1.6 0.8 1.9

2021

(FY21/22)

2019 2019

(FY19/20)Country

2020 2020

(FY20/21)

2021

Asia Quarterly – Q1/Q2 2020

- 3 -

Central Bank Policy Outlook Central Bank Policy Outlook

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

US Fed 1.50-1.75% 0.00-0.25% 0.00-0.25% 0.00-0.25% 0.00-0.25% 0.00-0.25% 0.00-0.25% 0.00-0.25% 0.00-0.25%

4.35% 4.35%

-- 4.05% 3.80% 3.65% 3.60% 3.60% 3.60% 3.60% 3.60%

India RBI 5.15% 4.40% 3.90% 3.90% 3.90% 3.90% 3.90% 4.15% 4.15%

Korea BoK 1.25% 0.75% 0.50% 0.50% 0.50% 0.50% 0.50% 0.75% 0.75%

Singapore MAS*

Slightly reduce

S$NEER slope (~0.5%

pa)

Malaysia BNM 3.00% 2.50% 2.00% 1.75% 1.75% 1.75% 1.75% 1.75% 1.75%

Indonesia BI^ 5.00% 4.50% 3.75% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25%

Thailand BoT 1.25% 0.75% 0.50% 0.50% 0.50% 0.50% 0.50% 0.75% 0.75%

Philippines BSP** 4.00% 3.25% 2.50% 2.50% 2.50% 2.50% 2.50% 2.50% 2.50%

Vietnam SBV 6.00% 5.00% 4.50% 4.50% 4.50% 4.50% 4.50% 5.00% 5.50%

Australia RBA 0.75% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25% 0.25%

Central

BankEnd 2019

Status Quo

China

20212020

"Slightly Steepen" (~0.5%

per annum)

PBoC

Country

^ PBoC instituted the loan prime rate (LPR), which sets a floor on commercial interest rates. This replaces the 1-yr Lending rate

* The MAS conducts monetary policy via FX. Specifically it adopts a trade-weighted SGD appreciation at "modest and gradual" (estimated to be 2% per

BI shifted to the 7 Day repurchase rate as the benchmark rate in August 2016. This by default constituted 125 bps reduction from the last policy rate

** BSP instituted an interest rate corridor policy in June 2016. The new effective policy rate is the overnight reverse repurchase rate.

Flatten S$NEER & Re-

Centre to Prevailing

S$NEER (~40-70bps lower) Status Quo

FX Outlook .

Jun 20 Sep 20 Dec 20 Mar 21 Jun 21

USD/JPY 106 105 104 103 102

EUR/USD 1.12 1.13 1.14 1.14 1.15

USD/CNY 7.06 6.98 7.04 6.96 6.88

USD/INR 74.2 73.2 73.8 72.2 71.0

USD/KRW 1210 1190 1200 1170 1160

USD/SGD 1.40 1.38 1.40 1.38 1.37

USD/IDR 16250 16100 16200 16100 16000

USD/MYR 4.30 4.28 4.34 4.30 4.25

USD/PHP 50.5 50.2 51.0 50.7 50.5

USD/THB 32.5 31.8 32.0 31.6 31.2

USD/VND 23360 23200 23300 23200 23160

AUD/USD 0.63 0.67 0.64 0.67 0.69

Market Watch

-40

-35

-30

-25

-20

-15

-10

-5

0Equities YTD Returns (%)

YTD (% in USD) YTD (% in lcl ccy)*As of 7 Apr 20

-10

0

10

20

30

40

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1M 1Y 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10Y

bp

s

% US Treasury Yield Curve

Forward rate changes (RHS) Treasury Yields

Forward 1Y Rates (implied)

-16

-14

-12

-10

-8

-6

-4

-2

0

2FX YTD returns (%)

YTD spot w/ carry (%) YTD spot (%)*As of 7 Apr 20 Sources: Refinitiv, Mizuho Bank

-150-125-100

-75-50-25

0255075

100125

10Y Yield YTD Changes (bps)

Change bps (10y)*As of 7 Apr 20

Asia Quarterly – Q1/Q2 2020

- 4 -

Table of Contents 1. Global Overview --------------------------------------------

5

Blindsided

2. Asia Outlook -------------------------------------------------

7

Dismal

3. China --------------------------------------------------------

8

Epi-Centres & After-Shocks

4. India ---------------------------------------------------------

10

Unwell Even Before the Virus

5. South Korea-------------------------------------------------- 12

Challenging external environment

6. Singapore ---------------------------------------------------

14

3D-Recession

7. Malaysia -----------------------------------------------------

16

Pandemic, poor commodity prices and political pressures

8. Indonesia ----------------------------------------------------

18

Bracing for impact from the COVID-19 outbreak

9. Thailand -----------------------------------------------------

20

Hard-hit tourism drags growth into contraction

10. Philippines ---------------------------------------------------

22

Lockdown to knock down growth

11. Vietnam -----------------------------------------------------

24

Growth may slow to sub-5%

12. Australia ----------------------------------------------------- 26

Compromised

Asia Quarterly – Q1/Q2 2020

- 5 -

Global Overview: Blind-sided

Growth: Blindsided by the “corona crisis”, a global

recession is all but guaranteed. COVID-19 outbreak

erupting into a full-blown global pandemic threatens

unprecedented “revenue shocks”. Urgent attempts to

“flatten the curve” (travel bans, lockdowns, social

distancing etc.) so as not to overwhelm strained hospital

capacity are vital; but entail exorbitant economic cost.

Revenue shocks exacerbated by supply-chain disruptions

risk a credit crisis; feeding into, and off, financial market

shocks. All of which are set to come in waves as dictated

by COVID-19 proliferation. Enter oil shock, and global

activity/capex are rendered even more dismal. And any

recovery in late-2020 will likely be fragile and drawn out.

0

1000

2000

3000

4000

5000

6000

7000

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Jan

-16

Jan

-17

Jan

-18

Jan

-19

Jan

-20

US Weekly Jobless Claims Spike to an Unpercedented 6.65mn vs. 2016-2019 average of

236K!

Risks: The most obvious risk is associated with lagged

response in in some countries blinded by false choices

between containment and growth disproportionately

deepen and prolong the waves of epidemic impact, and

consequent economic pain and societal suffering.

Second, despite unparalleled policy backstop, revenue

shocks escalating from cash-flow/earnings stress to a

credit crunch could unleash cross-default risks. And oil

in particular could turn out to be a nefarious catalyst of

such a contagious cash-credit-default spiral. Finally, a

resumption of US-China tensions post US elections is a

non-negligible risk even if virus risks fade quickly.

20

30

40

50

60

70

80

90100

200

300

400

500

600

700

800

900

1,000

Dec-14 Jul-15 Feb-16 Sep-16 Apr-17 Nov-17 Jun-18 Jan-19 Aug-19 Mar-20

Oil's Plunge triggers a Blow-out in US HY (10Y) Yield Spreads reveal potentially devastating crunch Credit Markets if Risk Re-pricing Leads to Domino Effect of

Cross-Default Fears!

US High-Yield (HY) Spread (LHS, bps, inverted) Brent Crude Prices (RHS, US$bbl)

Depth and Speed of; i) blowout in US High

and Yield (HY) spreads (over UST yields)

as well as; ii) plunge in Oil; far more

brutal than in 2015-2016 .HY Spreads blow out to >1,000bps at the worst point, easing back to 800-900bps.

Sources: Bloomberg, Mizuho Bank

Policy: The bazookas have been brought out; and the

closest thing to unconditional monetary stimulus is on

display. From slashed rates to; unprecedented (in some

cases unlimited) liquidity provision to; credit facilities

(tuned to smaller, more vulnerable firms/industries) to;

asset purchases (QE-type or YCC-type) to fire-up risk

appetite via portfolio channels. An unprecedented scale of

global fiscal stimulus, in some cases north of 10% of

GDP, is leveraging on monetary largesse to pre-empt cash-

flow chokes turning into a solvency crisis and job losses.

These measures remain scalable as deflationary B/S

shock risks dominate policy priorities. There is no free

lunch though and risk of asset market distortions mounts.

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

3.2

3.4

3.6

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

3.2

3.4

3.6

Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18 Jan-19 Jul-19 Jan-20

UST yields have slumped to record lows (10Y sub-0.5% & 30Y slump to ~0.8%; but off lows now); revealing potent mix of safe-haven demand, Oil's Collapse & Fed

Slash Rates to effectiveky zero; triggering a sharp UST yield drop.

US 5Y5Y Inflation Swap (% LHS, 5dma)

10Y UST Yield (%, RHS 5dma)

Trump wins US Presidential elections.

Dis-inflationary spillover from "Brexit".

Fed's emphatic tightening cycle with quarterly hikes of 25bp amid QT

When a "Patient" Fed followed through in March 2019 with neutral "Dot Plot" Shift, yields started correcting down rapidly, culminating Dovish Fed pressures since mid-2019!

Sources: Bloomberg, Mizuho Bank

COVID-19 risks, Oil's Collapse &

"Coordinated Stimulus" Hopes!10Y Yields Free-fall to lows below 0.5%!

Asset Markets: Being brutally plunged into a bear

market in March perhaps motivated an exceptionally

strong policy response that justifiably incorporated risks of

a crash leading to an otherwise avoidable depression. Yes,

an imminent crash was averted. But uncertainty

prevails unchecked despite signs of recovery in asset

markets – specifically whether this is a bona fide bullish

turn or merely a dead cat bounce. The difficulty in

determining which is due to unprecedented monetary

largesse setting a bear-trap on a timer (of unknown

duration). But For now, caution rules and cash may still

reign King at times of stress; which markets remain

vulnerable to until rate of new cases start falling at least.

-57.3

-32.5 -30.2 -28.3 -26.9 -26.7 -26.1 -24.5-23.3

-21.5 -21.3 -20.8-19.6 -19.6 -17.9

-9.5

-69.5

-44.7-41.2

-38.1 -39.8-36.5 -38.3

-34.4-37.1

-33.9 -31.3 -29.5 -28.1

-35.7

-28.7

-14.6

(80)

(70)

(60)

(50)

(40)

(30)

(20)

(10)

0

No Holds Barred Central Bank action & fiscal response backstop, but stilll short of pulling

markets out of bear territory! (vs. recent peak; as of NY close, 7th Apr 2020)

Sources: Bloomberg, CEIC, Mizuho Bank

Correction

Bear Market

US equities' drop into a Bear Market alongside Oil's Collapse is building on market fears.

Fed's "big guns" attempt at assuaging markets has significantly trapped bears. It may have ironically spooked. Either way, Big Guns do not equate to silver bullets.

Shanghai Composite's Peak-to-Trough will be 25-26% if 2018 (pre US-China trade conflict highs are used)

0

10

20

30

40

50

60

70

80

90(32)

(28)

(24)

(20)

(16)

(12)

(8)

(4)

0

4

8

21-Jan 26-Jan 31-Jan 5-Feb 10-Feb 15-Feb 20-Feb 25-Feb 1-Mar 6-Mar 11-Mar 16-Mar 21-Mar 26-Mar 31-Mar 5-Apr 10-Apr

Equities not fully retracing losses despite "big bang" policy backstops, suggests lingering safe-haven bias; at least until "Peak COVID". But beware volatility & unevenness across

safe-assets. (Start 21-Jan-2020 | LHS: % Chg Cumulative | RHS: VIX)

Dow (% Chg since 21st Jan; Inverted Scale) VIX (RHS) Sources: Bloomberg, Mizuho Bank

Rising VIX, indicating higher volatility and "fear" in the markets.

Falling Dow Jones Equity Index (Dow).

Dow plunges >30% from 12th Feb peak to 12th March (partial recovery since)

Asia Quarterly – Q1/Q2 2020

- 6 -

EUR/USD Outlook: The current state of Eurozone

somewhat looks like a reminiscent of the European

sovereign debt crisis as countries disagree over

Covid-19 rescue plan and the issuance of

coronabond. The fate of the currency to some extent

depends on response in the coming months including

ECB’s outright monetary transactions (OMTs) and

European Stability Mechanism (ESM). Given its

-0.50% interest rate, a strong surge in demand for

EUR is unlikely in near future as investors continue

to flock to safe-haven greenback. Going forward,

given Eurozone’s large current account surplus, the

currency may see mild gains should the greenback

pulls back from an elevated level.

(6)

(4)

(2)

0

2

4

6

8

10

(6)

(4)

(2)

0

2

4

6

8

10

21-Jan 31-Jan 10-Feb 20-Feb 1-Mar 11-Mar 21-Mar 31-Mar 10-Apr

Gold (surge) is Most Buoyant on Debasement Bets; JPY has slipped partly on policy largesse led by ~20% of GDP fiscal boost; EUR

underperforms on ECB's "Whatever it Takes" Stance Takes Over.(% Chg Cumulative; from 21-Jan-2020)

JPYEURGold

Sources: Refinitiv, BIS, Mizuho Bank

USD/JPY Outlook: While these are uncertain times

and the general trend has been of USD strength, we

expect Japan's status as the world's largest external

creditor with an economy in deflation to continue to

support a modest appreciation bias for the currency

in the coming quarters. We expect the pair to remain

within the 100-110 range as fundamental factors

including the change nature of Japan's external credit

(from marketable securities to FDI) prevents a short-

term, large scale sell-off of the currency while

narrowing global interest rate differentials to peer

economies prevents a significant appreciation. 0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

60

70

80

90

100

110

120

130

140

150

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20

UST-JGB spread sollapse on the Fed's abrupt shift to ZIRP & QE Innifity may up latent USD/JPY Volatility.

USD/JPY

UST-JGB 10Y

Sources: CEIC, , Mizuho Bank

Oil (Brent): The collision of adverse demand

shocks from widening and deepening COVID-19

profusion (and expected impact) with price-war

induced supply outburst following failed OPEC+

talks was the perfect storm that decimated near-70%

of oil’s value down to ~$20; and conditions remain

precarious in April. As oil storage capacity gets

stretched, the risks of prices plunging to $10. Only

an awkward Saudi-US-Russia truce that relegates

strategic geo-political priorities, including OPEC+’s

shadow war with Shale, may turn things around

rapidly in the near-term. Otherwise, a more jagged

path in oil gradually back to $45-55 could take the

rest of the year and for COVID to peak.

13.0MBpd

11.3MBpd

9.8 MBpd

4.0MBpd

3

4

5

6

7

8

9

10

11

12

13

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20

MB

pd

Clash of the Titans: Surge in US Crude Output not being liable to Output Cuts (unlike OPEC+) is s sticking point for OPEC+ (Saudi & Russia); Saudi ups optput to >12MBpD.

(MBpd)

US Russia Saudi Combined Iran-Venezuala-Libya

0

10

20

30

40

50

60

70

80

900

5

10

15

20

25

30

35

40

45

50

Dec-14 Jun-15 Dec-15 Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Dec-18 Jun-19 Dec-19

Dirty Tanker-to-Brent Ratio - a barometer of cost side pressures as crude prices plunge - spiking to post-2004 highs reflects unsustainably low crude.

Dirty Tanker to Brent Ratio (10D Avg)

Brent 10D Avg, RHS, Inverted Scale)Sources: Bloomberg, Mizuho Bank

Sources: Bloomberg, Mizuho Bank

Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Fed Rate^ (%) 0.00-0.25 0.00-0.25 0.00-0.25 0.00-0.25 0.00-0.25 0.00-0.25

ECB Rate^ (%) -0.50 -0.50 -0.50 -0.50 -0.50 -0.50

BoJ Rate (%) -0.10 -0.10 -0.10 -0.10 -0.10 -0.10

EUR/USD* 1.10 1.12 1.13 1.14 1.14 1.15

1.16 - 1.15 1.08 - 1.14 1.08 - 1.14 1.10 - 1.15 1.10 – 1.16 1.10 – 1.16

USD/JPY* 108 106 105 104 103 102

101 – 112 105-111 104 - 110 102 - 108 100 - 108 100 -108

Brent Crude (US$/bbl)

22.8 32.6 44.5 53.2 46.5 56.8

21.6-71.5 15.5-36.5 23.5-56.0 38.0-62.5 41.0-66.8 40.0-72.5

Note: Values in black are historical whereas those in blue represent forecasts.

* Point forecast is for end-period. Q1 2020 ranges are from Bloomberg and only indicative.

^ Fed rates refer to the Fed Funds Target rate; ECB rates refer to the Deposit facility rate.

Asia Quarterly – Q1/Q2 2020

- 7 -

Asia Outlook: Dismal

Output: It will be a dismal first half for Asia, with

most economies set to slow substantially, if not slump

into outright contraction; i) devastated by external

headwinds as collapse of travel/tourism conspires with

supply-chain disruptions; ii) dented further as

domestic demand is depressed by social distancing

and other containment efforts, and; iii) hammered by

jarring financial/commodity market shocks. And to

be sure, the depth of oil’s plunge is a negative shock

across Asia – and not just for oil producers or refiners

– given its nefarious credit and asset market ripples

against a backdrop of demand weakness. Even a

tentative and fragile recovery in late 2020 will require

that US-China tensions do not resurface.

-210

-180

-150

-120

-90

-60

-30

0

30

-12.0

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

China India Korea Singapore Malaysia Indonesia Thailand Philippines Vietnam Australia

2020 "COVID-19 Gap": Growth shortfall as a % of ex-COVID near-term growth potential, reveal Thailand & Singapore as far more impacted (in relative terms) than China.

Q1 (%-pts chg, LHS) Q2 Q3 Q4 Full year 2020 (shortfall as % ex-COVID "Potential"; RHS)

Inflation: There will be three nuances of inflation that

is worth noting. First, the food-fuel divergence in cost-

push factors. While oil’s collapse will prove

pervasively dis-inflationary, supply-disruptions could

drive up price of consumables that disproportionately

inflict pain; food being a case in point. Second,

regardless of patches of severe cost-push, demand

shortfall will be deep and “sticky”; and this will

crucially allow policy setting to remain accommodative

for far longer than in usual cycles. Finally, if B/S

shocks persist, cost-demand squeeze may undermine

confidence regardless of inflation expectations.

(100)

(50)

0

50

100

150

200

20

25

30

35

40

45

50

55

60

65

70

75

80

85

Jan 18 Apr 18 Jul 18 Oct 18 Jan 19 Apr 19 Jul 19 Oct 19 Jan 20 Apr 20 Jul 20 Oct 20 Jan 21

Oil Price & Inflation Outlook: Oil prices in the $20 to $60 range will be highly dis-inflationary to somewhat neutral all the way till Feb 2021.

Spot Brent Price

Inflationary Effects of Oil (% YoY; RHS)

Projected Oil Inflation at $20 Brent

Projected Oil Inflation at $40 Brent

Projected Oil Inflation at $60 Brent Sources: Bloomberg, Mizuho Bank

Policy: A rash of rate cuts to record lows, in some

cases well below the GFC lows, amongst most EM

Asia central banks may have room to run. Especially

as oil price plunge alongside severe revenue shocks push

policy calculus to uncharted dovish territory. But

increasingly, unconventional monetary policy tools

dominate. Led by; i) more unrestrained liquidity

provisions, beyond reserve RRR cuts and OMO ramp-up,

to allow for relaxed collateral requirements as well as; ii)

asset purchases to avail liquidity and reduce credit stress.

Lowering borrowing costs to support fiscal stimulus is

also on the menu, but heavily qualified lest it is mistaken

for debt monetization.

4.40%

4.25%

0.75%

2.50%

3.25%

0.75% 0.25%

5.00%

0.125%

4.75%

4.25%

1.25%2.00%

3.00%

1.25%1.25%

7.00%

0.125%

0.25%0.50% 0.50%

2.00%

3.25%

3.75%4.65%

4.00%

0.125%

0

1

2

3

4

5

6

7

8

0

1

2

3

4

5

6

7

8

RBA (AU) BoT (TH) BoK (KR) BNM (MY) BSP* (PH) BI (ID) RBI (IN) SBV* (VN) Fed (US)

Led by the Fed's rate slashes to post-GFC ZIRP, most EM Asia central bank policy raters are now back at, or below all-time lows. But eroding Spreads (vs.) up risks of capital outflow volatility; with

RBI & BI particularly vulnerable.

Current

Post-GFC low

Mid-2020 Forecast

* using Refinancing Rate as the defacto policy rate for the SBVSources: Bloomberg, Mizuho Bank

-210

-125

-100

-125

-100-75

-175

-150

-225

25 0 25 050

25

125

175

125

-185

-125

-75

-125

-50 -50 -50

25

-100

-250

-200

-150

-100

-50

0

50

100

150

200

-250

-200

-150

-100

-50

0

50

100

150

200

RBI (IN) RBA (AU) BoT (TH) SBV (VN) BoK (KR) BNM (MY) BI (ID) BSP* (PH) Fed (US)

Based on cuts since 2019 (to Feb 2020), RBI has eased most (next to Fed) while BNM has eased the least. Looking through the cycle since mid-2017, BoK, BNM & BSP appear to have room to

cut further; but this ignores overall and more holistic monetary dynam

2019-Feb 2020 Policy Rate Chg

mid-2017 to end-2018 Chg

Net Policy Chg since mid-2017Tightening

Easing

Sources: Bloomberg, Mizuho Bank

FX: Whether the USD will be dented by concerns of

debasement from “QE Infinity” or strengthened by

safe-harbour plays is the puzzle that FX markets will

struggle with. Our best guess? USD dominance will be

favoured in Q2; at least until “peak pandemic” as the

negative tail of the “USD Smile” plays out. And in

the EM Asia FX space, the most vulnerable appear to

be the “twin deficit” currencies such as IDR and INR

given the additional fiscal pressures and monetary that

the COVID crisis unearths. Regardless, despite softer

UST yields, near-term pressures on AXJ are likely to

persist before gradually fading into late-2020. (18)

(15)

(12)

(9)

(6)

(3)

0

3

6

(18)

(15)

(12)

(9)

(6)

(3)

0

3

6

22-Jan 27-Jan 1-Feb 6-Feb 11-Feb 16-Feb 21-Feb 26-Feb 2-Mar 7-Mar 12-Mar 17-Mar 22-Mar 27-Mar 1-Apr 6-Apr 11-Apr

Broad-Based USD Dominance on COVID-19: THB, KRW & AUD worst hit on Wuhan lock-down; SGD stabilizes after sharp S$NEER correction; IDR catch down turns meltdown & MYR slides on politics!

(Cumulative % Chg vs. USD since 22-Jan-2020^)PHP IDR CNH AUD

SGD JPY THB INR

MYR KRW EUR

Sources: Bloomberg, Mizuho Bank

Dismal GDP reveals risks from COVID-19 supply-chain/demand.

Soft GDP and BoT cuts highlight further downside risks to THB as COVID-19 exposure remains a worry.

^22nd Jan was referenced as this allows "mid-Jan "Phase-1"

deal exuberance to fade and is just before the unprecedented

Wuhan lockdown on 23rd Jan.

AUD knock rippling via commodity & RBA

Sharp S$NEER drop inherently limits further SGD under-performance on a trade-weighted basis; and stabilization in COVID-19 cases help to stabilize SGD.

BUT, JPY regains "safe-haven" traction.

IDR MELTS DOWNon doubts of insulation.

Asia Quarterly – Q1/Q2 2020

- 8 -

China: Epi-Centres & After-Shocks

Growth: With Wuhan as the epi-centre of the COVID-19

outbreak, China’s activity seizure (and growth slump) will

lead the global trend. A confluence of lock-down, lunar

New Year holidays and slower than expected resumption of activity set to plunge Q1 GDP into an outright

contraction. The silver lining is that Q2 activity pick-up will

help. But the harsh reality is that China will not be spared

aftershocks from global headwinds. Consequently, growth

is set slump to ~2.4% (from 6.1% last year, which was hit

by US-China trade turbulence). And this is the optimistic

case, incorporating significant fiscal stimulus, unwavering

monetary/credit easing and some pent-up demand in Q4.

Upshot: Growth is likely to be hit be waves of demand

disruption, and so a V-shaped recovery is off the table.

0

2

4

6

8

10

12

14

16

0

2

4

6

8

10

12

14

16COVID's shock waves sends 2020 growth hurling below 3%; Beijing may

forgo a near-6% target focussing on quality of recovery instead.Actual GDP

GDP Target

10

.8

7.8

7.5

7.2

7.0

5.8

5.3

4.4

4.3

3.3

3.3

3.2

3.1

3.1

2.7

2.3

2.1

1.7

1.6

1.4

1.4

1.4

1.1

1.1

0.9

0.9

0.8

0.5

0.2

0.0

0

2

4

6

8

10

12

On a Relative Basis, Guangdong, Zhejiang, Henan, Jinagsu, & Shangdong are worst-hit outside of Hubei; once adjusted for GDP.

(Combined Case-GDP Exposure Impact; % ex-Hubei)

Combined Case-GDP Exposure Impact (% ex-Hubei)Sources: John Hopkins CSSE, Mizuho Bank Calculations

Provinces with Least Impact from COVID-19

Provinces Hardest Hit by COVID-19

Provinces with Significant, But Not the Worst, Hit by COVID-19

Industry: Just as China’s lock-down impacted global

supply-chains in most of Q1, Europe/US tightening on

containment/social distancing will also have negative

feedback to China’s supply-chain and demand. And so,

initial pick-up in primary industries, while emphatic, will

remain sub-par; merely flattered by a low base. Auto

durable/capital goods and trade-related service sectors

are also likely to struggle in the absence of targeted fiscal

stimulus. Admittedly, there may be some pent-up demand

late-2020 accentuated by inventory levels; but only

fleetingly so, and far short of offsetting output lost.

35.7

32.3

29.3

35.5

38.8

27.825

30

35

40

45

50

55

60

65

70

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19 Jan-20

China's Mfg PMIs crash to Record Lows in Feb as the Seizure in Acitivity Eclipses the Slump During GFC (lows in Nov-2008). While March Shows a Big Jump on Activity resumption, adverse Global Pandemic Effcts Could be a Setback All Over again.

PMI-Mfg New Orders Output

Sources: CEIC, Mizuho Bank

GFC lows in Nov 2008 have been broken wit h the COVID shut-downs.

-3.1-pts in the headline

-3.0-pts (-0.3-pts) in terms of New Orders (New Exports Orders)

-7.7-pts for "Output"

Growth dynamics: The conspiracy of demand and

supply shocks slamming into growth at the same time

means that even with exceptional credit push and fiscal

stimulus, growth will flag. To be sure, demand

substitution, on two counts, will help. First, offshore

spending (e.g. outbound tourism) being substituted onshore

will buffer domestic demand. Second, online/delivery

services to may also benefit from a “substitution” boost.

Nonetheless, aggregate demand dent will be hard to fully

compensate for. And this is despite all the stimulus

measures; as the lack of money velocity, rather than

liquidity, stifles.

0

2,000

4,000

6,000

8,000

10,000

12,000

0

40,000

80,000

120,000

160,000

200,000

240,000

280,000

320,000

360,000

400,000

1 6 11 16 21 26 31 36 41 46

Total Cases: Looking for the turning point in Italian/European/ US Cases! While Korea's inflection was "tighter"markets are hoping for China-like Peaking; for exponential case increase in Italy/Europe & US to Slow to a Plateau. But

meanwhile, "lockdown"

China (First Wave, 20th Jan)

Italy (Third Wave, 21st Feb)

US (Third Wave, 21st Feb)

Germany-France-Spain (Third Wave, 21st Feb)

Korea (Second Wave, 14th Feb; RHS)

Days since outbreak accelerated (China: start 20th Jan | Korea start-14th Feb | Italy/Europe/US start: 21st Feb)

Sources: Bloomberg, Mizuho Bank

0

200

400

600

800

1,000

1,200

1,400

0

10,000

20,000

30,000

40,000

50,000

60,000

1 6 11 16 21 26 31 36 41 46

Number of New Cases: Hopes are that Italian/European & US Cases will Slow; consistent with China's Experience of cases peaking in ~4 weeks. But until then activity may be disrupted; and demand may be dented more enduringly.

China (First Wave, 20th Jan)

Italy (Third Wave, 21st Feb)

US (Third Wave, 21st Feb)

Germany-France-Spain (Third Wave, 21st Feb)

Korea (Second Wave, 14th Feb; RHS)

Sources: Bloomberg, Mizuho Bank Days since outbreak accelerated (China: start 20th Jan | Korea start-14th Feb | Italy/Europe/US start: 21st Feb)

Inflation: While pork-flation driven pick-up in CPI was an

issue just a few months back, inflation as a whole is a non-

issue for China. To be sure, spots of cost push inflation –

mainly due to lock downs – in items such as food and

medical supplies are very likely the case. And this might

linger for most of the first half as China gradually resumes

“business as usual”. But collapse in commodity prices, led

by oil, will overwhelming be a dis-inflationary after-shock

in aggregate. Moreover, substitution effects could effectively

dampen cost pressures. Instead, the singe biggest take-away

is that underlying deflationary risks stemming from

revenue shocks and lingering global demand dent far outweigh any sustained cost-side inflationary pressures.

-8

-6

-4

-2

0

2

4

6

8

10

12

-20

-15

-10

-5

0

5

10

15

20

25

30

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18 Jan-19 Jul-19 Jan-20

Producer PPI, a sub-component of PPI, reveals even sharper factory gate dis-inflation; reflecting falling profitability amid loss of pricing power. (% YoY)

Industrial Profits (Smoothed, 6mma)

PPI-Producer

Asia Quarterly – Q1/Q2 2020

- 9 -

Policy: Shock and awe is not the PBoC’s default

playbook. But lack of theatrics should not be mistaken for

a lack of efficacy or tenacity. Instead, the PBoC relies on a

whole range of liquidity and credit tools to augment far

more calibrated rate adjustments. In doing so, achieve

effective, scalable, targeted stimulus, without raising alarm about throwing caution (on mounting credit risks) to

the wind. Specifically; i) an expansion of targeting credit

stimulus to SMEs/worst-hit industries; ii) deeper targeted RRR cuts; iii) ramped-up TLTRO programs; iv) easier

debt/bond rollover LGFVs, SOEs and large corporates. In

concert, these will amplify monetary easing, enhance

transmission and create critical resonance with fiscal

stimulus efforts.

0

5

10

15

20

25

(4)

(2)

0

2

4

6

8

10

06 07 08 09 10 11 12 13 14 15 16 17 18 19 20

Calibrated, albeit Unfettered Easing Bias; favour loosening liquidity; targeted) RRR cuts; credit for SMEs; calibrated, but continuous drip-feed of rate cuts.

1-yr Lending (LHS) *Real interest rates (LHS) CPI (% y/y; LHS)

7-Day Repo (LHS) RRR (RHS) RRR - Small/Med banks (RHS)Sources: CEIC, Mizuho Bank

(30)

(20)

(10)

0

10

20

30

40

50

(30)

(20)

(10)

0

10

20

30

40

50

12 13 14 15 16 17 18 19 20

PBoC's targeted credit push and debt.bond rollover allowance likely tosee resurgent credit dynamics; but likely with overall credit growth to lead "shadow credit".

(Contribution to YoY Credit Growth, 6MAvg, %-pts)

"Shadow Credit" (ex-Bonds & BA)^

Bank Credit

Combined

^ Shadow credit refers to Aggregate Financing less conventional bank loans. And this measure omits bond issuances as well as Bankers' Acceptance (BA).

Sources: CEIC, Mizuho Bank .

External Position: Ironically, economic gloom may

coincide with a significant boost to C/A surplus. For one,

global travel bans in the wake of COVID will significantly

cutback, if not suspend, Chinese tourist dollars ending

up offshore. Second, being the first to recover, China’s

now advantageous position to ship out medical, and

personal protective gear to the rest of the world, over and

above resumption of broader manufacturing and exports

to replenish depleted global inventories. The former

dramatically reducing non-goods deficit while the latter

boosts net goods surplus; both; more than offsetting any

strategic stock-piling. Upshot: C/A surplus increasing by

1.2-1.8%-pts to trend back to ~3% of GDP.

1.3

-0.4

0.1 0.1

2.1

1.8

0.3 0.2

(1.0)

(0.5)

0.0

0.5

1.0

1.5

2.0

2.5

Total Ouward Travel Net Outward Travel Total IP Payments Net IP Payments

China's Net Outward Tourism is to the tune of nearly 2% of GDP. So COVID travel bans should result in 1.5-2.0% reduced C/A tourism outflows;

boosting C/A, all else equal. (% of GDP)

2002 2018

In 2002 more in-bound tourists visisted China than outbound Chinese tourists. Hence tourism boosted China's C/A ~0.4% of GDP then in contrast to the 1.8% of GDP reduction in 2018.

(80)

(40)

0

40

80

120

160

(80)

(40)

0

40

80

120

160

07 08 09 10 11 12 13 14 15 16 17 18 19 20

China: A strong Goods Balance is less likely to be eroded by tourist outflows amid global travel restrictions. This should boost overall C/A position. (US$bn, 4Qma)

Financial A/C Goods Services C/A

FX: However, that is not likely to translate into

resounding CNY strength anytime soon as uncertainty

around the COVID-19 pandemic and recession feats keep

USD premium intact. But equally, CNY will not be on a

free-fall imminently. For one, the PBoC attaches a

significant premium to CNY stability – rightly

recognizing that capital flow stability (which is in turn a

derivative of external liabilities and FX mismatch) far

outweigh misguided notions of mercantilist gains. China

recognizes it cannot grow by cheapening its exports. So

USD/CNY may trade the 6.95-7.25 amid USD-driven

volatility near-term before stabilizing 6.72-6.88 further

out as COVID risks subside.

-2.0

0.0

2.0

4.0

6.0

8.0

10.06.0

6.2

6.4

6.6

6.8

7.0

7.2

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18 Jan-19 Jul-19 Jan-20

CNY Fixing has predominantly been at a premium to previous close; suggesting "counter-cyclical" bias that is supportive of CNY

USD/CNY (LHS, Inverted Scale) CNY Fix Fix Premium* (RHS, % premium of fix over previous close)

Stronger CNY

CNY fix weaker than previous closeFixing biased towards softening CNY

CNY fix stronger than previous close

Fixing biased towards stronger CNY

80

85

90

95

100

105

110

115

120

85

90

95

100

105

110

Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18 Jan-19 Jul-19 Jan-20

Despite COVID-19 shocks, CNY NEER has regained modest traction since US-China "truce" in Sep-2019. USD trend is instead dictating relative CNY shifts! (Index end-2014=100)

CNY NEER

USD (DXY) index (RHS; rebased: Start-2008 = 100)

60 per. Mov. Avg. (CNY NEER)

Paradigm shiftfrom "dirty" USD peg to NEER-based

Coronavirus outbreak, beyond triggering broad-based USD strength (on safe-haven demand), has not materially dented the stability in trade weighted CNY.

Sources: Bloomberg, Mizuho Bank

Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

GDP (% y/y) -4.2% 2.1% 4.0% 6.2% 11.2% 6.8%

CPI (% y/y) 3.9% 1.3% 1.1% 0.3% 1.0% 3.4%

Policy Rate^ (%)

4.05% 3.80% 3.65% 3.60% 3.60% 3.60%

4.35% -- -- -- -- --

USD/CNY* 7.08 7.06 6.98 7.04 6.96 6.88

6.84 – 7.12 6.89 – 7.21 6.87 - 7.10 6.85 – 7.14 6.76 – 7.09 6.71 - 6.99

Note: Values in black are historical whereas those in blue represent forecasts. * Point forecast is for end-period. Q1 2020 ranges are from Bloomberg and only indicative. ^ The 1-yr Loan Prime rate is expected to be adjusted in small 5-10bps calibrations to 3.80%

Asia Quarterly – Q1/Q2 2020

- 10 -

India: Unwell Even Before the Virus Growth: Even before the “corona crisis” adversely

impacted India’s economy, culminating in a lock-down,

the economy was already unwell. Hobbled by fragile

consumer/business confidence and exacerbated by the

credit choke amid banks’, NBFCs’ and corporate B/S

woes, growth was already set to be sub-par. But now,

the depth and duration of pain are now likely to

worsen as revenue/income shocks amplify pre-existing

fragilities. Unprecedented monetary easing (rate cuts,

financing relaxation, 3.2% of GDP liquidity boost, etc)

and INR1.7trln (0.8% of GDP) fiscal stimulus provide

welcome relieve, but no panacea. Slump in growth to

3-4% may risk erring on the optimistic side.

4.3

6.4

7.3

6.5

5.3

8.0

8.7

5.9

7.1

7.6

8.0

7.2

9.1

8.7

9.7

8.6

6.3

5.8 6.5

7.6

8.2

7.1

6.2

5.6

5.7

5.6

5.1

4.7

(2)

0

2

4

6

8

10

12

(2)

0

2

4

6

8

10

12

Mar-13 Sep-13 Mar-14 Sep-14 Mar-15 Sep-15 Mar-16 Sep-16 Mar-17 Sep-17 Mar-18 Sep-18 Mar-19 Sep-19

India Growth: Sharper deceleration in underlying private sector demand, which is even more amplified in private sector domestic demand, reveals deep-seated

issues with domestic confidence predating COVID-19. (Growth YoY %)

GDP

GDP ex-Govt (Private Sector Demand)

GDP ex-Govt & Trade (Private Sector Domestic Demand)

Sources: CEIC, Mizuho Bank

Industry: The lockdown in India, along with external

supply-chain disruptions will inevitably hijack nascent

recovery in the auto sector – one of the few emerging

bright spots. And while significantly lower oil prices is

arguably a much-needed from the cost side of things for

industry, the biggest impediments continue to be

associated with demand deficit. Worryingly, cash

crunch amid COVID-19 may further stifle propensity

for capex/investments as the reflex to conserve more

precautionary cash overtakes; inadvertently retarding a

recovery even more. In short, the virus undermines an

already impaired virtuous investment cycle.

(24)

(20)

(16)

(12)

(8)

(4)

0

4

8

12

16

20

(14)

(12)

(10)

(8)

(6)

(4)

(2)

0

2

4

6

8

10

12

Jun-13 Dec-13 Jun-14 Dec-14 Jun-15 Dec-15 Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Dec-18 Jun-19 Dec-19

India: Slump in capital goods & consumer non-durables suggests chronic confidence deficit; with hopes of a gradual recovery are retarded by COVID.

(3m Avg % y/y)

Ind Pdtn (3m Avg; % YoY) Consumer Durables Capital Goods (RHS)

Sources: CEIC, Mizuho Bank

IP understates the collapse in confidence; which in turn dampens GDP via "multiplier" effects.

(30)

(20)

(10)

0

10

20

30

40

(30)

(20)

(10)

0

10

20

30

40

11 12 13 14 15 16 17 18 19 20

Auto Demand Onshore has collapsed far more sharply suggests confidence shortfall; while external pick-up may be interrupted by COVID crisis.

(3mma % YoY; smoothed for demonetization & GST)

Domestic Vehicles Sales IP - Capital Goods Auto Exports

Growth dynamics: Notions that the RBI pumping

liquidity amounting to ~3.2% of GDP alongside 0.8%

fiscal fillip (even larger fiscal pipeline eyed) will

engineer a decent boost for growth (simplistically ~4%

of GDP) misses a key point. That is, liquidity is

“stock”, but growth requires “flows”. So, unless

business/consumer confidence is restored, a drop in

“money velocity” (flows) may neutralize intended

growth boost from liquidity infusion (stock). Crucially,

banks’ NPAs drag/ NBFC liquidity crisis entailing

cross-default risks, left unresolved, challenge kick-

starting a sustainable recovery. Especially if; i) fiscal

slippage “crowds out” the private sector, and; ii)

disproportional pain on the poorest is not mitigated.

60

62

64

66

68

70

72

74

76

78

80

0

5

10

15

20

25

30

35

07 08 09 10 11 12 13 14 15 16 17 18 19 20

Credit Growth Continues to Falter in a refelction of impediments to both credit demand & supply amid triple (banks, NBFC, corporate) B/S burden.

(3mma % y/y)

Non-food credit (LHS) Deposits (LHS) Loans-to-Deposits Ratio (%; RHS)Sources: Bloomberg, CEIC, Mizuho Bank

621

1,516

896

471

483

657

823

1,054 1,888

2,338

3,455

3,850

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

FY Ending 17-19 Avg FY Ending 20 FY Ending 21

Stretched Non-Tax Revenue Assumptions & Tax Revenues hit by the "corona-crisis" up risks if fiscal slippage ... (INR bn)

Others

Interest

Economic Services

SOE Dividends

RBI Dividends

Non-Tax Revenues (NTR)

NTR - Adjusted Dividends, ex-Telco Fines*

*Normalized RBI dividend growth of 10% per annum from base of FY17-19 levels. And Vodafone fine of INR11trln is assumed to be phased in. So Communication Services revenues (Part of Economic Services) is adjusted down based on 10% growth in spectrum fees from FY19/20.

INR950bn of "extraordinary" non tax revenues translates into ~0.3% of GDP revenue boost.

Inflation: The good news is that oil’s collapse is an

accelerant for dis-inflation, helping to offset lingering

cost-push from food. In turn, this should hasten headline

inflation catching down with “core” inflation to 3-4%;

potentially even under-shooting if exceptionally soft oil

prices persist. But the bigger picture of demand-pull

inflation being conspicuously absent is unchanged. And

perversely, cost-push impulses are ultimately deflationary

being defacto income confiscation. The post-COVID

economic climate will probably be one of mainly

contained inflation, looking past spurts of cost push. (2)

0

2

4

6

8

10

12

(2)

0

2

4

6

8

10

12

Mar-13 Sep-13 Mar-14 Sep-14 Mar-15 Sep-15 Mar-16 Sep-16 Mar-17 Sep-17 Mar-18 Sep-18 Mar-19 Sep-19 Mar-20

India CPI: Slump in Oil will be a Catalyst in Hastening inflation as food inflation, led by onions, moderate in any case; broader trend inflation

normalizing to 3.5-4.5% buys RBI some space. (% YoY)

Food Fuel & Light

Clothing Housing

Misc CPI

RBI Policy (Repo) Rate CPI ex-Food, Fuel&Light

Sources: CEIC, Mizuho Bank

^ NBFC: Non-banking financial companies in India, the source of credit surge in the recent past.

Asia Quarterly – Q1/Q2 2020

- 11 -

Policy: RBI rolling out the big guns with 75bps rate cut

(building on a total 135bp cuts in 2019) to a record low

4.40% complemented by a staggering INR6.5trln (3.2% of

GDP) liquidity cannon since Feb (100bps CRR cut to

3.00%, TLTROs, liquidity/credit easing, etc) “improve

liquidity, monetary transmission and credit flows”. But with

inflation likely to be reined in whilst threat of larger

demand shocks looms large, our sense is that the RBI is

inclined to scale up credit/liquidity facilities to provide

targeted and timely relief. Moreover, further headline rate

cuts to ~3.90% by mid-2020 are set to be pushed through

under the auspices of oil’s deflation. Above all, the RBI will

probably dig its heels in on “twist” and some form of YCC

to help anchor long-end bond yields.

-2

-1

0

1

2

3

4

5

6

7

8

-2

-1

0

1

2

3

4

5

6

7

8

Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17 May-17 Sep-17 Jan-18 May-18 Sep-18 Jan-19 May-19 Sep-19 Jan-20

After five cuts of 135bps in 2019 and a 75bp "bazooka cut" this year (to 4.40%); Scope for another 25-50bps facilitated by softer Oil & Growth Slump.

RBI-Fed Spread

Fed (US)

RBI Policy Rate

Real Rate (Policy Rate less Inflation)

Sources: Bloomberg, Mizuho Bank

Cumulative 50bp of rate hikes in 2018.

Five back-to-back cuts of a cumulative 135bp in 2019 and another 75bps in 2020

External Position: Despite India’s reflex to secure food

and other key medical stockpile in reaction to COVID, the

collapse in Oil prices should help to keep C/A (deficit)

under wraps to below 0.5%, rather than escalating to 1.0-

1.5%. Nonetheless, the overall external position may not

benefit much; and could in fact deteriorate. Mainly as

capital outflows mount amid worries of revenue shocks

adversely impacting an economy already straining under

subpar economic conditions, hobbled by financial risks and

political uncertainty. In turn, the circular, adverse

feedback between falling asset prices and rupee

slippage.

20

25

30

35

40

45

50

55

60

65

70

75

80(18)

(16)

(14)

(12)

(10)

(8)

(6)

(4)

(2)

Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17 May-17 Sep-17 Jan-18 May-18 Sep-18 Jan-19 May-19 Sep-19 Jan-20

While global crude prices plunge in Q1 narrower trade deficit (as well as C/A deficit)may be a silver lining. But at these levels of crude price demand shocks outweigh

the price relief. (3mma US$bn)

Trade Deficit

India Crude Oil Basket (US$/bbl, 3mma; RHS)Sources: CEIC; Mizuho Bank

2

4

6

8

10

12

0

1

2

3

4

5

6

06 07 08 09 10 11 12 13 14 15 16 17 18 19 20

India: C/A Deficit is set to be subdued by Oil's Plunge. But while the relief is the real concern is about capital outflows amid risk aversion.

(4Qma, % of GDP)

C/A Deficit (% of GDP)

Trade Deficit (% of GDP; RHS)

FX: Rupee slippage in the 76-78 range remains a

heightened risk near-term. And to be clear, bouts of

interim relief rallies (below 74-75) should not be mistaken

for one-way, sustained rebound in the INR. For one, India

is nowhere near being out of the woods as an initial three-

week lockdown since late-March is likely to be extended.

Crucially, oil prices collapsing so sharply (to $20-30 lows)

is also a net rupee negative insofar that it reflects; i)

demand shocks; ii) sharp capex capitulation, and; iii) wider

high-yield spreads; which overwhelm any C/A advantages

(for rupee) as well as backstop from FX reserves. Fiscal

slippage risks and stretched monetary largesse could also

stifle rupee recovery; even when COVID risks pass. And

so we expect a gradual easing under 72 towards 70 into

2021; rather than a surge to 65-68.

(3)

(2)

(1)

0

1

2

3

(2,000)

(1,500)

(1,000)

(500)

0

500

1,000

1,500

2,000

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18 Jan-19 Jul-19 Jan-20

If the recent slump in SENSEX Persists & Extends, triggering equity out-flows, Rupee could be under renewed pressures.

Smoothed (4wkma, USDmn, LHS) Equity flows

INR % Chg (Wk/Wk, 4wkma, RHS)

Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

GDP (% y/y) 3.7% 2.3% 2.8% 3.8% 4.6% 6.0%

CPI (% y/y) 6.5% 2.7% 3.0% 2.5% 2.4% 4.3%

Policy Rate (%) 4.05% 3.90% 3.90% 3.90% 3.90% 4.15%

USD/INR* 75.3 74.2 73.2 73.8 72.2 71.0

70.7 - 76.4 71.3 - 76.9 71.3 – 75.3 70.5 - 75.5 68.9 - 74.5 68.2 – 73.0

Note: Values in black are historical whereas those in blue represent forecasts. * Point forecast is for end-period. Q1 2020 ranges are from Bloomberg and only indicative.

Asia Quarterly – Q1/Q2 2020

- 12 -

South Korea: Challenging external environment

Growth: Q4 GDP growth picked up marginally to 2.3%

YoY, partly due to base-effect, with government

spending continuing to play a sizeable role. Investment

grew YoY for the first time in seven quarters, again

driven by public investment as government ramped up

civil engineering and specialized construction projects.

Going forward, growth is set to face headwinds imposed

by Covid-19 outbreak in 1H. The nascent recovery in

exports might be dampened due to disruption in supply

chain. Private consumption will also face downward

pressure as people avoid going out. Expansionary fiscal

policy will gain be the main pillar in shoring up growth.

-3

-1

1

3

5

7

2015 2016 2017 2018 2019

Contribution to GDP (%YoY -ppts)Net exports Change in stocks

GFCF Govt spending

Private consumption GDP

Source: CEIC, Mizuho bank

Industry: Trade activities have been holding up

relatively well as of Q1 though the trend of recovery

may see a reversal in coming months due to the

increasing widespread of COVID-19 across the globe.

For one, South Korea’s own confirmed cases have seen

dramatic increase in Mar, which is likely to see disrupted

factory operation due to work-related infections. The

negative impact of delayed resumption of factory

operation in China is also set to show up in full swing as

manufacturers from automobile, mobile phone and

semiconductor sectors ran out of inventory of

intermediate goods.

(20)

(10)

0

10

20

30

2015 2016 2017 2018 2019 2020

Contribution to export growth(3mma, ppts, %)

ChemicalsMachineryEEPassenger CarVesselsCrude materials/fuelsExports, YoY

Source: CEIC, Mizuho Bank

Growth dynamics: The fiscal stimulus launched so far

by the government to combat Covid-19 has been

relatively small at around 0.6% of GDP when other

Asian countries have introduced stimulus as large as

10% of GDP. Though arguably South Korea has

managed to contain the spread in the absence of broad

lockdown measures, consumer based services sector are

still likely to be affected evidenced by slowing growth of

retail sales and plunging consumer confidence. Whilst

the initial extra budget largely focused on boosting

medical equipment, supporting SMEs in the affected

area, the government is drawing up a second

supplementary budget (up to 7.1tn Won) to dispense

cash payments to families in a bid to shore up domestic

demand

YearSize (tln

Won)

% of

GDPFocus Area

2015 11.6 0.7% Address negative effects of the

outbreak of MERS, new spending plans

2016 11.0 0.6%

Support corporate restructuring; create

jobs for laid-off workers in the affected

industries

2017 11.2 0.6%Job creation for the young; boost

economic growth

2018 3.8 0.2%Job creation; help industrial regions

coping with layoffs

2019 6.7 0.4%Address fine dust; support job creation;

boost exports ar SMEs

2020 11.7 0.6% COVID-19 affected areas and firms

Source: Press media, Mizuho Bank

Inflation: Headline inflation rebounded to above 1%,

predominately led by higher fuel prices as last year’s

petroleum prices were lowered due to temporary fuel tax

cut. Given the recent sharp plunge in crude oil prices,

this is likely to temper headline inflation going forward

as oil prices are likely to stay low for some time.

Furthermore, core inflation is also set to stay tepid too at

around 0.5% given minimal underlying pricing pressure

as growth comes under pressure. As such, we expect

inflation to stay at low-1% in 1H. -1.0

0.0

1.0

2.0

3.0

2016 2017 2018 2019 2020

Contribution to inflation (%YoY, - ppts, 3mma)

Transport Food Core Policy rate CPI - headline

Sources: CEIC, Mizuho Bank

Asia Quarterly – Q1/Q2 2020

- 13 -

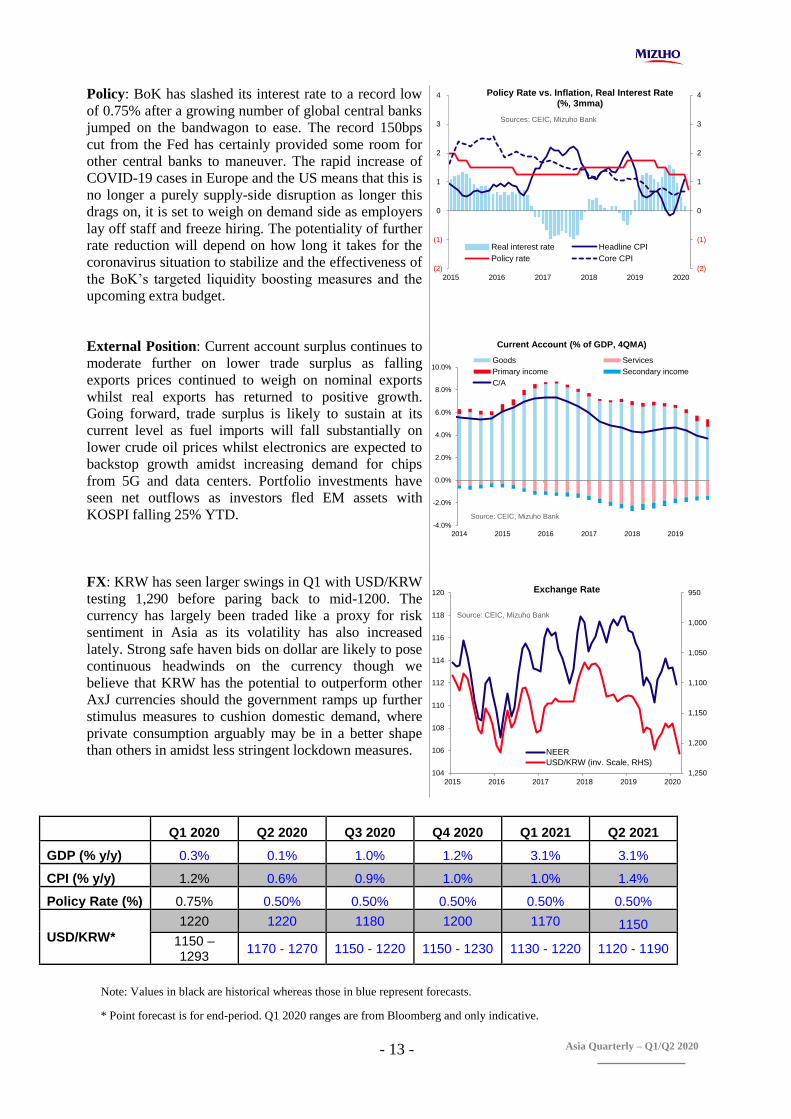

Policy: BoK has slashed its interest rate to a record low

of 0.75% after a growing number of global central banks

jumped on the bandwagon to ease. The record 150bps

cut from the Fed has certainly provided some room for

other central banks to maneuver. The rapid increase of

COVID-19 cases in Europe and the US means that this is

no longer a purely supply-side disruption as longer this

drags on, it is set to weigh on demand side as employers

lay off staff and freeze hiring. The potentiality of further

rate reduction will depend on how long it takes for the

coronavirus situation to stabilize and the effectiveness of

the BoK’s targeted liquidity boosting measures and the

upcoming extra budget.

(2)

(1)

0

1

2

3

4

(2)

(1)

0

1

2

3

4

2015 2016 2017 2018 2019 2020

Policy Rate vs. Inflation, Real Interest Rate (%, 3mma)

Real interest rate Headline CPI

Policy rate Core CPI

Sources: CEIC, Mizuho Bank

External Position: Current account surplus continues to

moderate further on lower trade surplus as falling

exports prices continued to weigh on nominal exports

whilst real exports has returned to positive growth.

Going forward, trade surplus is likely to sustain at its

current level as fuel imports will fall substantially on

lower crude oil prices whilst electronics are expected to

backstop growth amidst increasing demand for chips

from 5G and data centers. Portfolio investments have

seen net outflows as investors fled EM assets with

KOSPI falling 25% YTD.

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2014 2015 2016 2017 2018 2019

Current Account (% of GDP, 4QMA)

Goods Services

Primary income Secondary income

C/A

Source: CEIC, Mizuho Bank

FX: KRW has seen larger swings in Q1 with USD/KRW

testing 1,290 before paring back to mid-1200. The

currency has largely been traded like a proxy for risk

sentiment in Asia as its volatility has also increased

lately. Strong safe haven bids on dollar are likely to pose

continuous headwinds on the currency though we

believe that KRW has the potential to outperform other

AxJ currencies should the government ramps up further

stimulus measures to cushion domestic demand, where

private consumption arguably may be in a better shape

than others in amidst less stringent lockdown measures.

950

1,000

1,050

1,100

1,150

1,200

1,250104

106

108

110

112

114

116

118

120

2015 2016 2017 2018 2019 2020

Exchange Rate

NEER

USD/KRW (inv. Scale, RHS)

Source: CEIC, Mizuho Bank

Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

GDP (% y/y) 0.3% 0.1% 1.0% 1.2% 3.1% 3.1%

CPI (% y/y) 1.2% 0.6% 0.9% 1.0% 1.0% 1.4%

Policy Rate (%) 0.75% 0.50% 0.50% 0.50% 0.50% 0.50%

USD/KRW*

1220 1220 1180 1200 1170 1150

1150 – 1293

1170 - 1270 1150 - 1220 1150 - 1230 1130 - 1220 1120 - 1190

Note: Values in black are historical whereas those in blue represent forecasts. * Point forecast is for end-period. Q1 2020 ranges are from Bloomberg and only indicative.

Asia Quarterly – Q1/Q2 2020

- 14 -

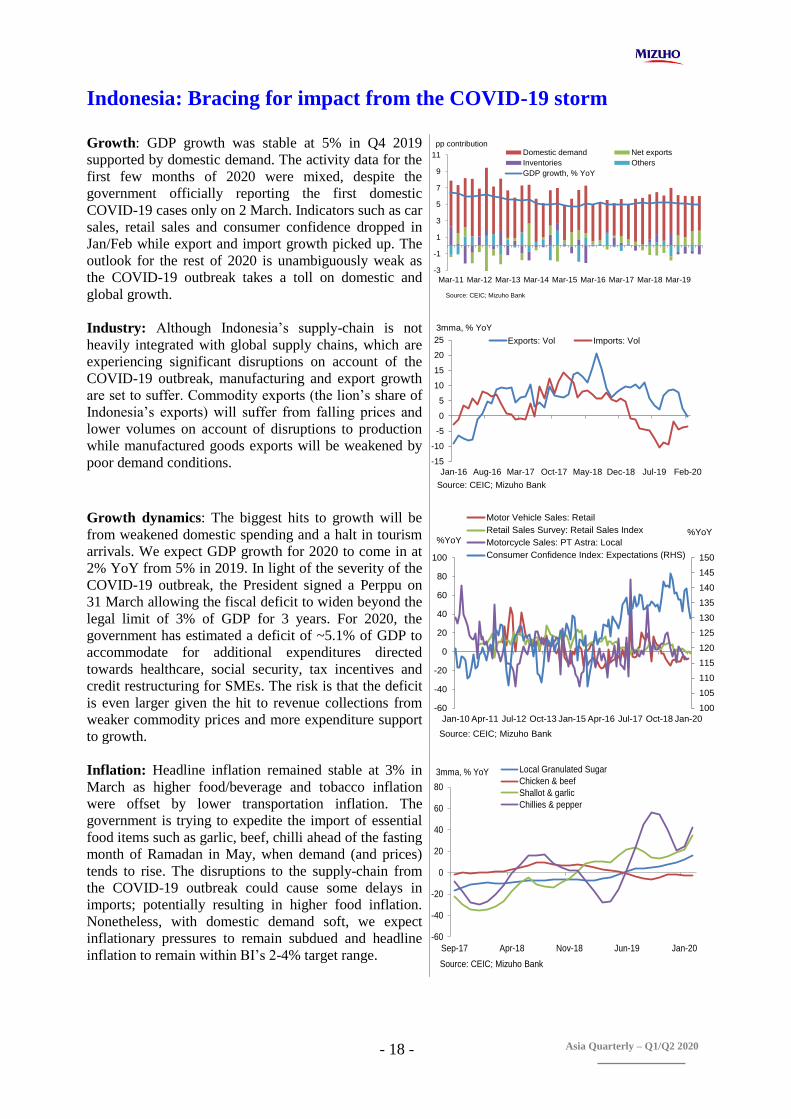

Singapore: 3D-Recession

Growth: A significantly deeper contraction in Q2, after 2.2%

YoY drop in Q1, is all but unavoidable. And a recession is now

no longer a question of “if”, but of depth, duration, and

lasting damage (“3D”) – in terms of jobs and balance sheet

(B/S) shocks. Official GDP forecasts revised down to -4 to -1%

(from …) reveals the small and open economy exposed to

every bump; from COVID-19 travel ban impact on its

regional air hub status /tourist sector; to the supply-chain

disruptions buffeting manufacturing; demand dent from

revenue shocks; social distancing further dampening

activity/demand. All of which are compounded by financial and

oil market dislocations. This “perfect storm”, is set to inflict a

2.8% contraction for 2020; with risks to the downside and a

precarious, fragile recovery into 2021.

7.9

7.4

9.0

3.9

-10.1

-8.5

-8.9

-6.7

-15.0 -10.0 -5.0 0.0 5.0 10.0

AFC (1997-98)

"Dot Com" (2000-01)

GFC (2008-09)

COVID-19 (2019-20)

Crisis Impact on Singapore's Growth: In terms of absolute growth rate shock (drop), AFC was the worst (-10.7%-pts); but relative to baseline

growth ...

Growth "Shock" (% Pts) Baseline (Avg 2-Y Prior) Growth Rate (% YoY)

-200 -180 -160 -140 -120 -100 -80 -60 -40 -20 0

AFC (1997-98)

"Dot Com" (2000-01)

GFC (2008-09)

COVID-19 (2019-20)

Magnitude of Singapore's Growth Shock (Adjusted for Baseline): COVID-19 Could Have a Far Larger, and Longer-Lasting Imapct (10.7%-pts); but relative to

baseline growth

Growth "Shock" (Proportion of Baseline Growth %)

Industry: So-called “front-line” industries taking the brunt

upfront are travel/tourism/hospitality followed by F&B scene

with spillover to transport. But the buck doesn’t stop there, as

global pandemic negative “contagion” proliferates via supply,

demand and financial channels. Also, tighter containment

efforts, led by stringent social distancing, have rapidly

transmitted “revenue shocks” more widely to retail trade and

across services. Amplifying pain is the Oil’s brutal (~50%)

drop cascading through Singapore’s extensive petrochemical,

O&G services, storage and trading sectors; consistent with a

deeper and longer lasting economic shock if credit stress and

energy sector capex plans pullback sharply.

95

100

105

110

115

120

125

06/2002 09/2002 12/2002 03/2003 06/2003 09/2003 12/2003 03/2004 06/2004 09/2004 12/2004

Singapore SARS Impact: Negative Shocks on GDP peaked after three quarters (Q4 2002 to Q2 2003); restored following2-3 quarters.

(Indexed; Q2 2002=100)

GDP GDP ex-SARS

It took a total of ~6 quarters for GDP to be restored to a hypothetical "sans-SARS" state

20

30

40

50

60

70

80

90

100

102

103

104

105

106

107

108

Oct-14 May-15 Dec-15 Jul-16 Feb-17 Sep-17 Apr-18 Nov-18 Jun-19 Jan-20

Oil's plunge this time was more consistent with a deeper S$NEER step reduction; squaring with the risks of prolonged negative output gap.

S$NEER adjusted for appreciation bias* (LHS; Levels)

Brent Crude Prices (RHS, US$bbl)Sources: Bloomberg, Mizuho Bank

S$NEER is discounted by the policy appreciation bias to "de-trend" and better correlate to Oil prices (assumed to be "stationary".

Growth dynamics: The nature of the “coronavirus crisis” is

such that in the details, there will admittedly be some; demand

creation for tele-commuting solutions, demand substitution to

online/delivery services; demand brought forward from

household/strategic stock-piling. Nevertheless, in aggregate,

private sector demand will undeniably be compromised. And

in recognizing sharp demand shortfall, the government has

unveiled three quick successions if counter-cyclical fiscal

stimulus totaling near-S$60bn (12% of GDP). Fiscal measures

particularly aim to “short-circuit” the fallout from cash/liquidity

seizures from revenue shocks to spiraling into a credit crunch,

degenerating into to a solvency crisis and subsequent job losses.

-9.5%-7.5%

-2.1%

-6.2%

-62.9%

(70)

(60)

(50)

(40)

(30)

(20)

(10)

0

10

20

30 The "Triple Fiscal Boost" anticipated this time, blows away all pervious counter-cyclical fiscal counter-strike seen; ~12% of GDP as "direct" COVID pain relief!

(% of Operating Revenues)

GFC

SARS"Dot Com" Bust

Oil/China "Shock"

Budget Surplus corresponds to fiscal tightening, all else equal.

Budget Deficit corresponds to fiscal stimulus, all else equal.

COVID Response = "Unity" + "Resilience + Solidarity

Inflation: To be sure, inflation drivers are not homogeneous

one; given the juxtaposition of deep dis-inflationary shocks

from of Oil’s dramatic crash, upside pressures from cost-

push that results from supply disruptions; and

administrative price relief (suspension in government fees,

road tax reductions, subsidies for utilities/conservancy etc.).

But in concert, dis-inflationary dynamics, both in amplitude

and durability, are likely to overwhelm. And CPI – both

headline and core – are set to fall close to 1% on the year

in 2020, before recovering gradually; especially given

considerably weaker wage-price mechanics amid softer job

market hampering demand-pull inflation from resurfacing.

(2)

(1)

0

1

2

3

4

5

6

10 11 12 13 14 15 16 17 18 19 20

Headline CPI restoration towards 1% interrupted by Oil shocks (supply-side) & COVID impact (demand-end); Dis-inflation to Persist in 2020,

with headline and Core CPI set to turn Negative.

CPI CPI ex-OOA*

* CePI ex-OOA: CPI ex owner-occupied accommodation imputed rental.

Asia Quarterly – Q1/Q2 2020

- 15 -

Policy: The MAS’ double barelled easing, comprising; i)

S$NEER slope flattening (from ~0.5% to 0% per annum

appreciation rate) and; ii) re-centring the S$NEER mid-point

lower (by an estimated 40-70bps) helps to position monetary

policy for a prolonged slowdown and provide some degree of

instant buffer against the abrupt revenue shocks. While the MAS

remains “vigilant” of more downside risks, the bar is fairly

high for further easing – most likely for another mid-point shift

down (a.k.a. “step depreciation”). As the MAS rightly alluded,

monetary policy merely supports much more fine-tuned

fiscal stimulus – ramped up tremendously to nearly S$60bn

(~12% of GDP). We thus expect the MAS to maintain status

quo at least into H1 2021. And

102

103

104

105

106

107

108

109

110

111

102

103

104

105

106

107

108

109

110

111

Jan-14 May-14 Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17 May-17 Sep-17 Jan-18 May-18 Sep-18 Jan-19 May-19 Sep-19 Jan-20 May-20

MAS "affirms the current ... slightly below the mid-point" S$NEER | Will "adopt zero percent ... rate of appreciation starting at the prevailing level of the S$NEER" | Effectively; i) a re-centring lower by ~40-

70bps and; ii) suspending S$NEER appreciati

NEER

Mid-Point

Sources: MAS, Bloomberg, CEIC , Mizuho Bank

+/- 2% from S$NEER mid-pt

Stronger trade-weighted SGD

Apr '16: Surpriserevocation of appreciation bias (to 0% slope) prompts knee-jerk, but short-lived S$NEER slip.

Oct '16: MAS invokes "neutral ... for extended period" dovish caveat.

Apr '17: MAS surprises by retaining "neutral for extended period" dovish caveat.

Apr '18: MAS restores "slight" S$NEER slope. We estimate ~0.5% per annum

S$NEER rise within "neutral" 0% policy slope was recognised as defacto tightening; supporting longer policy hold.

Sharp S$NEER plunge entails intra-band, defacto easing; exploited amid COVID-19 risks. Diminishes case for urgent, inter-meeting moves.

S$NEER drop effectivelyachieves further easingdespite no additional policy moves.

Oct '18: MAS "slightly" increases S$NEER slope gradient. We estimate to ~1.0% per annum

Apr '19:

MAS Holds. We estimate to ~1.0% per annum

Oct '19: MAS "slightly" reduces S$NEER slope gradient. We estimate to ~0.5% per annum

External: Neither the exceptional C/A strength (~17% of

GDP for 2019) nor the seasonal dip for Q4 (to ~15% of GDP)

deserve attention. Instead, the overall external balance (BOP)

turning negative (exaggerated by exceptionally large financial

outflow in Q2 2019) is worth a closer look – especially if

coordinated global financial market volatility is heightened

(to the point of meltdown risks). That said, Singapore’s quasi

safe-haven status helps to buffer SGD from “safe-

harbour” refuge from risks such as COVID-19 within EM

Asia (re-allocation rather than brutal liquidation). Especially

as the strongly accretive C/A supports stability. (15)

(10)

(5)

0

5

10

15

20

25

30

35

40

(15)

(10)

(5)

0

5

10

15

20

25

30

35

40

07 08 09 10 11 12 13 14 15 16 17 18 19 20

"Margin Squeeze" in the midst of the US-China Trade Conflict appears to have eroded te Goods Balance. But the far Greater

Risk at this Juncture is from Financial Outflows on BOP. (% of GDP, 4Qma)

Goods Services

Income & Others BOP

C/A Sources: Bloomberg, Mizuho Bank

FX: Despite MAS’ “double barrelled” easing, a weaker SGD

or S$NEER is not to be assumed. For one, slope flattening

merely suspends appreciation bias. And while re-centring

lower is “step deprecation” of band, actual S$NEER shift

down predates MAS move. Whereas, MAS’ stance that fiscal

policy will do the heavy-lifting; dispels misguided notions of

unbridled monetary stimulus. Crucially, the MAS refraining

from widening policy bands reveals that excessive SGD

drop is neither helpful nor desirable. In turn, squaring with

S$NEER around mid-band; with USD trend and FX

volatility dictating USD/SGD. Upside risks to USD/SGD are

elevated near-term amid COVID and wider market risks.

Further out sub-1.38 USD/SGD begins to appear.

1.33

1.34

1.35

1.36

1.37

1.38

1.39

1.40

1.41

1.42

1.43

1.44

1.45

1.46

1.47

1.48

1.33

1.34

1.35

1.36

1.37

1.38

1.39

1.40

1.41

1.42

1.43

1.44

1.45

1.46

1.47

1.48

9-Aug-19 3-Sep-19 28-Sep-19 23-Oct-19 17-Nov-19 12-Dec-19 6-Jan-20 31-Jan-20 25-Feb-20 21-Mar-20 15-Apr-20

Implied SGD Trading Band Corresponding to S$NEER Policy Band: SGD closes up gap with mid-point after MAS "affirms" (re-cnetres). Further USD moves more

dependent on USD trends/Fed policy. (based on Mizuho estimates)

SGD (Actual) SGD (Mid Pt)

Sources: Bloomberg, CEIC, Mizuho Bank

Stronger SGD

2019 nCoV related risks hammering CNY and Asia FX correlate to the policy bands shifting down, while earlier MAS easing bets account for actual SGD falls within (relative to) the bands.

Q1 2020 Q2 2020 Q3 2019 Q4 2020 Q1 2021 Q2 2021