asian clearing union annual report 2008 - acu-home annual... · asian clearing union annual report...

TRANSCRIPT

Asian Clearing Union

ANNUAL REPORT 2008

Submitted to:The 38th Meeting of the ACU Board of Directors

held at Central Bank of Sri LankaColombo, Sri LankaJune 16-17, 2009

ACU

1974

II

ANNUAL REPORT 2008

Board of Directors at the 37th ACU Meeting

June 17-18, 2008Nay Pyi Taw, Myanmar

Board of Directors at the 37th ACU Meeting

III

ANNUAL REPORT 2008

Participants at the 37th Meeting of the ACU Board of Directors

June 17-18, 2008Nay Pyi Taw, Myanmar

Participants at the 37th Meeting

IV

ANNUAL REPORT 2008

Board of Directors

Salehuddin AhmedGovernor,

Bangladesh Bank

Daw TenzinGovernor,

Royal Monetary

Authority of Bhutan

D. Subbarao*Governor,

Reserve Bank of India

* From 05.09.2008

Mahmoud Bahmani*Governor,

Central Bank of I.R. of Iran

* From 13.10.2008

Than NyeinGovernor,

Central Bank of Myanmar

Krishna Bahadur ManandharActing Governor,

Nepal Rastra Bank

Shamshad AkhtarGovernor,

State Bank of Pakistan

Ajith Nivard CabraalGovernor,

Central Bank of Sri Lanka

Board of Directors

V

ANNUAL REPORT 2008

Alternate Directors

Ziaul Hasan SiddiquiDeputy Governor,

Bangladesh Bank

Dechen TsheringDeputy Managing

Director,

Royal Monetary

Authority of Bhutan

Meena HemchandraChief General

Manager,

Reserve Bank of India

Reza RaeiVice Governor,

Central Bank of I.R. of Iran

Maung Maung WinDeputy Governor,

Central Bank of Myanmar

Ram Jee RegmiExecutive Director,

Foreign Exchange

Management Dept.,

Nepal Rastra Bank

Yaseen AnwarDeputy Governor,

Corporate Services,

State Bank of Pakistan

J P Mampitiya*Director,

Payments &

Settlements Dept.,

Central Bank of Sri Lanka

* From 18.08.2008

Alternate Directors

VI

ANNUAL REPORT 2008

Offi cers-in-Charge

Md. Belayet HossainGeneral Manager,

Forex Reserve and

Treasury Management

Dept.,

Bangladesh Bank

P. K. Nayak*Deputy General

Manager, DEIO

Reserve Bank of India

* From 29.12.2008

Rinzin LhamuHead Banking Division,

Royal Monetary

Authority of Bhutan

Reza NadaliDirector,

International Dept.,

Central Bank of I.R. of Iran

Maung MaungDirector,

Accounts Dept.,

Central Bank of Myanmar

Shashi Dhar AryalAssistant Director,

Foreign Exchange

Management Dept.,

Nepal Rastra Bank

Muhammad Habib KhanDirector,

Finance Dept.,

State Bank of Pakistan

R. B. Weerasinghe*Deputy Director,

Payments and

Settlements Dept.,

Central Bank of Sri Lanka

* From 02.09.2008

Offi cers-in-Charge

VII

ANNUAL REPORT 2008

Contents

Administrative Organization, 2008................................................................................. 1

Board of Directors, 2008................................................................................................ 2

Offi cers-in-Charge, 2008 ............................................................................................... 3

Letter of Transmittal to the Board of Directors ............................................................... 4

Global Economic Prospects and Challenges ................................................................ 5

Economic Highlights of ACU Member Countries ......................................................... 15

Country Performance .................................................................................................. 26

Bangladesh.................................................................................................................. 26

Bhutan ......................................................................................................................... 39

India ............................................................................................................................. 46

Iran .............................................................................................................................. 59

Myanmar...................................................................................................................... 75

Nepal ........................................................................................................................... 81

Pakistan ....................................................................................................................... 89

Sri Lanka ................................................................................................................... 105

Auditor’s Report .......................................................................................................... 116

ACU Operations ......................................................................................................... 117

Clearing Operations.................................................................................................... 117

Credit Positions .......................................................................................................... 118

Debit Positions............................................................................................................ 118

Net Credit/Debit Positions .......................................................................................... 119

Interest Received/Paid ............................................................................................... 119

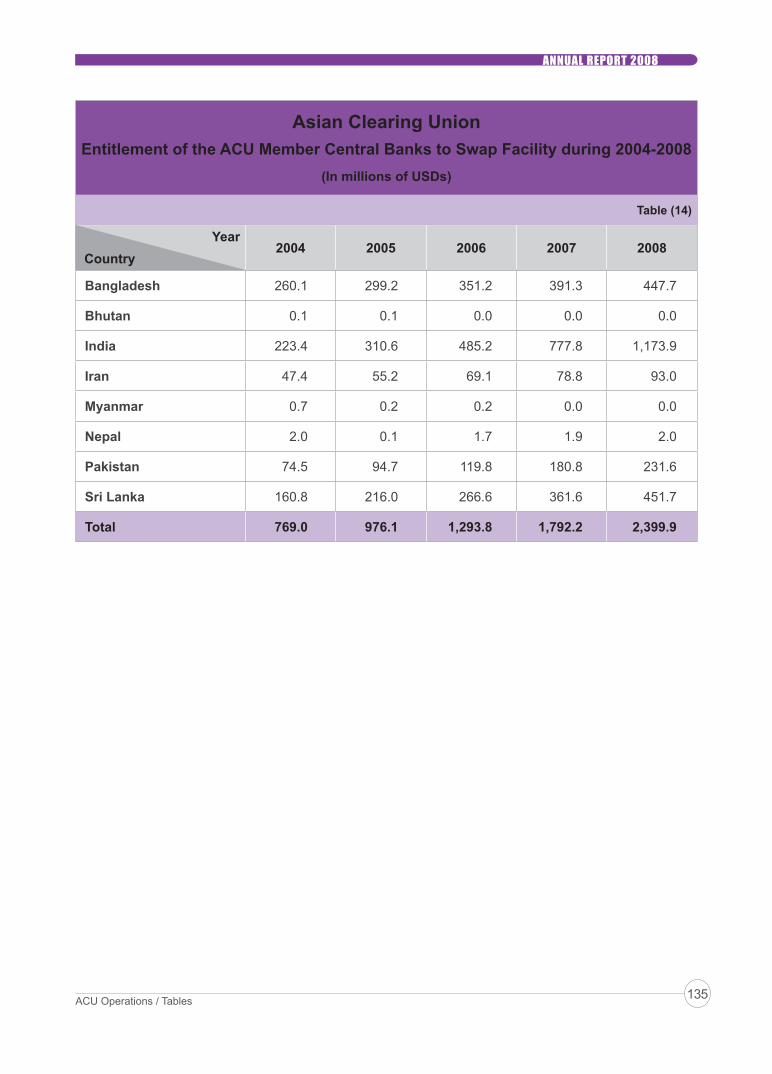

Swap Facility .............................................................................................................. 119

Measures and Achievements ..................................................................................... 120

Tables ......................................................................................................................... 122

Acronyms and Abbreviations ...................................................................................... 142

Contents

1

ANNUAL REPORT 2008

Asian Clearing Union

Administrative Organization, 2008

Mr. Than NyeinChairman of the Board,Governor,Central Bank of Myanmar

Mrs. Lida Borhan-AzadSecretary General

Secretariat Offi ceAddress: No. 207/1, Pasdaran Ave., P.O. Box 15875/7177Tehran, Islamic Republic of IranPhone: (+98 21) 22842076, 22854509Fax: (+98 21) 22847677Telex: (088 21) 3120, 6868Swift: BMJIIRTHACUE-mail: [email protected]: www.asianclearingunion.org

Agent BankCentral Bank of Islamic Republic of Iran

Administrative Organization, 2008

2

ANNUAL REPORT 2008

Asian Clearing Union

Board of Directors, 2008Bangladesh Bank Dr. Salehuddin Ahmed Governor, (Director) Mr. Ziaul Hasan Siddiqui Deputy Governor, (Alternate)

Royal Monetary Authority of Bhutan Mr. Daw Tenzin Governor, (Director) Mr. Dechen Tshering Deputy Managing Director, (Alternate)

Reserve Bank of India D. Subbarao* Governor, (Director) * From 05.09.2008

Mrs. Meena Hemchandra Chief General Manager, (Alternate)

Central Bank of Islamic Republic of Iran Dr. Mahmoud Bahmani* Governor, (Director) * From 13.10.2008

Dr. Reza Raei Vice Governor, (Alternate)

Central Bank of Myanmar Mr. Than Nyein Governor, (Director) Mr. Maung Maung Win Deputy Governor, (Alternate)

Nepal Rastra Bank Mr. Krishna Bahadur Manandhar Acting Governor, (Director) Mr. Ram Jee Regmi Executive Director, (Alternate)

State Bank of Pakistan Dr. Shamshad Akhtar Governor, (Director) Mr. Yaseen Anwar Deputy Governor, (Alternate)

Central Bank of Sri Lanka Mr. Ajith Nivard Cabraal Governor, (Director) Mrs. J P Mampitiya* Director, Payments and Settlements Dept., (Alternate) * From 18.08.2008

Board of Directors, 2008

3

ANNUAL REPORT 2008

Asian Clearing Union

Offi cers-in-Charge, 2008Bangladesh Bank Mr. Md. Belayet Hossain General Manager, Forex Reserve and Treasury Management Dept.

Royal Monetary Authority of Bhutan Mrs. Rinzin Lhamu Head Banking Division

Reserve Bank of India Mr. P. K. Nayak* Deputy General Manager, DEIO * From 29.12.2008

Central Bank of Islamic Republic of Iran Mr. Reza Nadali Director, International Dept.

Central Bank of Myanmar Mr. Maung Maung Director, Accounts Dept.

Nepal Rastra Bank Mr. Shashi Dhar Aryal Assistant Director, Foreign Exchange Management Dept.

State Bank of Pakistan Mr. Muhammad Habib Khan Director, Finance Dept.

Central Bank of Sri Lanka Mrs. R. B. Weerasinghe* Deputy Director, Payments and Settlements Dept. * From 02.09.2008

Offi cers-in-Charge, 2008

4

ANNUAL REPORT 2008

Letter of Transmittal to the Board of Directors

Letter of Transmittal to the Board of Directors

June 16, 2009

The Honorable Ajith Nivard CabraalChairman of the Board,Governor,Central Bank of Sri Lanka,Colombo, Sri Lanka

Dear Mr. Chairman,

I have the honor to present to the Board of Directors, the Annual Report of the Asian Clearing Union (ACU) for the year 2008, duly signed by me, in accordance withChapter III, Article VIII, Section 3(c) of the Agreement Establishing the Asian Clearing Union.

Yours sincerely,

Lida Borhan-Azad Secretary General, ACU

5Global Economic Prospects and Challenges

ANNUAL REPORT 2008

Global Economic Prospects and Challenges1

An overviewThe global economy experienced 3.2 percent growth in 2008; however it is projected to decline by 1.3 percent in 2009 which depicts a sever recession. The trend is expected to recover moderately in 2010, by 1.9 percent growth. The fi nancial crisis and economic slowdown has adversely affected the global economy.

The advanced economies experienced an unprecedented decline in real gross domestic product (GDP) in 2008, and output is anticipated to fall remarkably over the fi rst quarter of 2009. The United States (US) has severely been affected by fi nancial pressures and the continued slump in the housing market. In the Euro area, growth fell to 0.9 percent in 2008. Japan’s economy declined over the year as output growth dropped sharply by 0.6 percent. The output growth in emerging and developing economies fell to 6.1 percent in 2008 mainly due to trade and fi nancial stress. Western Europe and advanced Asia too have suffered from intensifi ed fi nancial strains and the slowdown in global trade.

In tandem with the rapid falling of global activity, infl ation pressures have become less strong. Commodity prices declined, adversely affecting income of the Middle Eastern and Commonwealth of Independent States (CIS) economies, as well as many other commodity exporters in Latin America and Africa. Consequently, in the advanced economies, 12-month headline infl ation declined below 1.0 percent in February 2009, while core infl ation remained around 1.5-2.0 percent, with the exception of Japan. Infl ation in some emerging economies has experienced a moderate pace.

Although efforts have been taken to stabilize fi nancial markets and contain the downturn in output, confi dence in fi nancial markets is still low which dampens the prospects for an early economic recovery.

Total expected write-downs on global exposures are projected around USD 4.0 trillion, of which two-thirds will fall on banks. In advanced economies, banks

1 This summary report is based on World Economic Outlook (WEO-April 2009), International Monetary Fund.

6 Global Economic Prospects and Challenges

ANNUAL REPORT 2008

face with funding strains due to limited access to credit. Many non-fi nancial corporations are unable to obtain working capital, and some have diffi culty to raise longer-term debt.

The issuance of new securities have almost stopped, bond spreads have increased, equity prices have declined, and exchange markets have come under sever pressure. There is a tendency for risk aversion and desire to move funds to mature markets with the increasing provision of guarantees.

The fi nancial crisis has had an impact on the world’s major currencies. Since September 2008, the US dollar, euro, and yen have all strengthened in real effective terms. The Chinese renminbi and currencies pegged to the US dollar (including those in the Middle East) have also appreciated. Most other emerging economy currencies have weakened remarkably, despite the use of international reserves.

Global Prospects and ChallengesThe stabilization of fi nancial market is expected to take longer than previously projected, even with hard efforts taken by policymakers. Therefore, fi nancial pressures in the mature markets are anticipated to continue until well into

2010. However, fi nancial sector will improve slowly due to clarity on bad assets, injections of public capital, lower counterparty risks and market volatility, and restore more liquid market conditions.

In the advanced economies, credit to the private sector is projected to fall in both 2009 and 2010. The emerging and developing economies are anticipated to have limited access to external fi nancing in both years.

From the point of macro-economic policy support, interest rates are projected to decline or remain near the zero bound in the major advanced economies, while central banks continue to explore ways to ease credit conditions. In both advanced and emerging economies, fi scal defi cits are expected to increase severely, as governments implement fi scal stimulus plans in G20 countries amounting to 2.0 percent of GDP in 2009 and 1.5 percent of GDP in 2010. It is expected that commodity prices move around current levels in 2009 and increase moderately in 2010. In spite of policy actions, and anticipating a moderate recovery from the second quarter onward, global activity is expected to fall by 1.3 percent in 2009. This would show by far the deepest post-World War II recession.

Furthermore, the economic slowdown is global, as output per capita is expected

7Global Economic Prospects and Challenges

ANNUAL REPORT 2008

to fall in most countries, and growth in almost all countries has declined remarkably from rates seen in 2003-07.

Overall, the current outlook is uncertain, and downside risks pertinent to insuffi cient policy action, limited public support for policy action, rising corporate and household defaults, greater losses across fi nancial balance sheets, and new systemic events that complicate the task of restoring credibility have raised concerns.

Even once the crisis is over; there will be a diffi cult transition period, with output growth noticeably below rates observed in the recent past.

Regional Economic OutlookThe United States and Canada

The fi nancial crisis has made the US to face with a severe recession. Despite the Federal Reserve’s (Fed) policy actions, credit is costly or diffi cult to access for many households and fi rms. Furthermore, households are being suffered by remarkable losses and increased uncertainty about job security which all made the slump in consumer confi dence. These, in turn, have reduced consumption; the household saving rate has escalated, to over 4.0 percent in

February 2009.

Although fi nancial markets have stabilized slightly, but they remain under sever pressure. In inter-bank markets, spreads continue to exceed normal levels.

Equity markets are 40.0 percent lower than their peaks, as economic outlooks have deteriorated and fi nancial stocks have been hit by large losses and uncertainty about solvency.

The US dollar has strengthened remarkably which refl ects tendency toward government bonds as other economies have become more deeply involved in the crisis.

Real GDP reduced by 6.3 percent in the fourth quarter of 2008, and it is estimated to fall further in the fi rst quarter of 2009.

Employment has continued its downward trend as 5.1 million jobs have been lost since December 2007, causing the unemployment rate to reach 8.5 percent in March. Fed eased monetary policy by cutting policy rates to around zero, however credit market deteriorations are weakening the effectiveness of rate cuts.

The GDP is now estimated to decline by 2.8 percent in 2009. The economy is anticipated to start recovering by the middle of 2010. The growth in 2010 is

8 Global Economic Prospects and Challenges

ANNUAL REPORT 2008

projected to be zero percent.

In 2008, infl ation increased to 3.8 percent, but it is expected to decline sharply in 2009.

Tax rebates caused consumption to rise slightly in the middle of 2008, but their effects have now disappeared. A much larger discretionary stimulus package combines further tax relief with federal assistance to states, which is anticipated to provide a 2.0 percent of GDP stimulus in 2009 and 1.8 percent in 2010. The federal budget defi cit is expected to be about 10.0 percent of GDP in 2010.

In 2008, current account defi cit declined to 4.7 percent of GDP, but further decline is anticipated in the next year.

The Canadian economy has also contracted in 2008, growing by only 0.5 percent compared to 2.7 percent a year ago. The real GDP is expected to drop sharply in 2009. Consumer prices grew by 2.4 percent in 2008, but it is projected to decline next year. Unemployment is estimated to continue its upward trend in 2009, reaching to 8.4 percent. Current account surplus dropped to 0.6 percent of GDP in 2008.

Europe

In most of advanced Europe, economic activity had declined before September 2008 due to increasing oil prices.

Financial systems deteriorated, policy actions were slow to react, confi dence, and global trade fell sharply.

The real economy contracted in 2008, owing to deterioration in funding markets. Financial policies were implemented, but insuffi cient to reinforce their cross-country effectiveness.

Equity prices declined severely, and business investment has been reduced. Furthermore, residential investment has declined in countries with housing booms such as Ireland, Spain, and the United Kingdom (UK). Despite the large fall in oil prices, consumption decreased toward the end of 2008.

Unemployment rates in the advanced economies are expected to exceed 10.0 percent in late 2009 and escalate further in 2010.

In 2008, the growth of real GDP dropped to 0.9 and 0.7 percent in euro area economies and the UK, respectively. The growth is expected to fall by more than 4.0 percent in 2009. The recession is anticipated to be deep in Ireland, Iceland, and the UK. Economic activity has also fallen drastically in many emerging European countries, owing to their heavy reliance on various capital infl ows. With deteriorated Western export markets and increased risk-aversion attitude during fall 2008, the outlook for local exports, growth, and

9Global Economic Prospects and Challenges

ANNUAL REPORT 2008

government revenues worsened severely, causing sovereign spreads to climb from 50.0-100.0 basis points (bps) to 150.0-900.0 bps. As a result, output growth in the emerging economies is expected to decline by about 3.7 percent in 2009 and recover to 0.8 percent in 2010.

Infl ation pressures are declining fast, and risks for sustained defl ation are rising in advanced economies due to the fall in oil prices and demand. In 2010, infl ation is forecast to be between 0.5 and 1.5 percent in most advanced economies. Monetary policy has been eased. The Bank of England has cut policy rates successively from 5.7 percent in 2007 to 0.5 percent in 2009. The European Central Bank (ECB) to respond to infl ation pressure raised rates in July 2008 to 4.2 percent but then lowered rates on its main refi nancing operations to 1.2 percent.

In emerging Europe, infl ation rates are also expected to fall remarkably, from 8.0 percent in 2008 to 4.2 percent in 2010. Exchange rates have depreciated in emerging economies with fl oating currencies.

The UK defi cit is expected to reach 11.0 percent of GDP in 2010.

Asia

Since September 2008, the crisis has drastically affected economies in

Asia. Japan’s economy declined at a 12.0 percent (annualized) rate in the fourth quarter. The newly industrialized economies including Hong Kong SAR, Korea, Singapore, and Taiwan Province of China contracted at rates between 10.0 to 25.0 percent, and south-east Asian emerging economies have also been hit dramatically. These falls were mainly due to the slump in demand for consumer durable goods and capital goods in (non-Asian) advanced economies and the global fi nancial crisis. China and India have been affected by deterioration in the export sector, but their economies have continued to grow, owing to smaller share of trade in their economy and policy actions.

Exports and industrial production have fallen quickly.

Equity and bond prices have dropped, sovereign and corporate spreads have escalated, and inter-bank spreads have increased. Currencies have depreciated in most of the region’s emerging economies (except the yen). The renminbi has remained unchanged relative to the US dollar.

Emerging Asia is expected to continue to grow, led by China and India. Despite contraction in exports, the current account surplus for Asia is forecast to remain unchanged at about 4.7 percent of GDP. Real GDP is expected to fall by

10 Global Economic Prospects and Challenges

ANNUAL REPORT 2008

about 6.0 percent in 2009. The output growth in Japan is estimated to decline by 6.2 percent in 2009. A mild defl ation is projected to persist during 2009 and 2010.

The output growth in China is expected to fall to about 6.5 percent in 2009 compared to 13.0 percent in 2007.

Association of Southeast Asian Nations (ASEAN) economies are being severely damaged by the effects of lower global demand and harder credit conditions. For ASEAN, the output growth is projected to decrease from 6.3 percent in 2007 to zero percent in 2009.

The growth in India is projected to drop severely from 9.3 percent in 2007 to 4.5 percent in 2009. This fall is mainly due to lower investment, refl ecting fi nancing constraints and a turn in the domestic credit cycle.

In Japan, the central bank has reduced rates to almost zero. In China, the central bank has cut interest rates and reserve requirements and loosened credit ceilings. In India, the policy rate and reserve requirements have been reduced. Other central banks in the region (in Cambodia, Korea, Malaysia, the Philippines, Singapore, and Thailand) have also reduced policy rates or decreased reserve requirements.

In Japan, the defi cit is expected to be

around 10.0 percent of GDP in 2009 and net debt to exceed 100.0 percent of GDP.

Latin America and the Caribbean (LAC)

As a result of the global fi nancial strains, LAC suffered from increasing borrowing costs and declining capital infl ows. The slump in commodity prices is hitting large economies in the region (Argentina, Brazil, Chile, Mexico, and Venezuela) which are among the world’s major exporters of primary products. In addition, the economic slowdown in advanced economies-particularly the US, the region’s largest trading partner-is reducing external demand and lowering revenues from exports, tourism, and remittances.

The global fi nancial crisis spread quickly to LAC markets after the middle of September 2008. Local equity markets have been damaged severely, with the largest losses (about 25.0 percent) in Argentina.

Domestic currencies have depreciated, particularly in Brazil and Mexico, which are large commodity-exporting countries with fl exible exchange rate regimes.

Financial markets have differentiated between borrowers, as the fi nancing cost has climbed for some countries (for example, Argentina, Ecuador, and Venezuela) but remains relatively low

11Global Economic Prospects and Challenges

ANNUAL REPORT 2008

for other countries with sound positions and larger policy buffers including Brazil, Chile, Colombia, Mexico, and Peru.

Real GDP is projected to fall by 1.5 percent in 2009. Domestic demand would decline by about 2.2 percent in 2009.

For the region, infl ation is expected to fall from 8.0 percent in 2008 to about 6.5 percent in 2009.

The region’s current account defi cit is forecast to increase to slightly more than 2.0 percent in 2009, owing to negative terms-of-trade effects.

Africa

Relatively mild fi nancial connections with advanced economies have not been a buffer for African economies against the global fi nancial crisis. The contraction of external growth, which is declining demand for African exports and reducing workers’ remittances, drastically hit the continent. The sever slump in commodity prices is also buffeting the resource-rich countries in the region. In addition, the global credit constraints is limiting foreign direct investment (FDI) and reversing portfolio fl ows, especially to emerging and frontier markets (Ghana, Kenya, Nigeria, South Africa, and Tunisia). These deteriorations led to a sharp fall in economic activity. For the region, the growth of output is estimated to drop from 5.2 in 2008 to 2.0 percent in 2009. The slowdown has

greatest impact on oil-exporting countries (Angola, and Equatorial Guinea), as well as on emerging and frontier markets (Botswana, Mauritius, and South Africa).

The economic downturn and the fall in food and fuel prices will curtail infl ation pressures. For the region, infl ation is expected to decline slowly from 10.1 percent in 2008 to 9.0 percent in 2009.

Fiscal and external balances are forecast to worsen remarkably. The overall fi scal position of the region is expected to fall by about 5.7 percent, to a defi cit of 4.5 percent of GDP in 2009.

For the region, the current account balance is also expected to deteriorate, from a surplus of 1.0 percent of GDP in 2008 to a defi cit of 6.5 percent of GDP in the following year. The fi nancing of external defi cits is forecast to remain diffi cult in some of emerging and frontier markets (Ghana, Nigeria, South Africa, and Tanzania), owing to the global credit constraints.

The South African Reserve Bank has reduced its policy rates by a cumulative 200.0 bps since early December.

Middle East

The global fi nancial crisis has affected the Middle East. The substantial slump in the oil price is damaging the region severely. The Middle Eastern countries

12 Global Economic Prospects and Challenges

ANNUAL REPORT 2008

are being affected adversely by the tight external fi nancing conditions and reversal of capital infl ows, refl ecting intense pressure on local property and equity markets. The domestic liquidity conditions have worsened, credit spreads have climbed for a number of fi rms, fi nancial system distresses have emerged in some countries, and sovereign wealth funds have faced with losses from external investments. Moreover, the sharp fall in external demand is reducing export growth, workers’ remittances, and tourism revenues particularly in Egypt, Jordan, and Lebanon.

Despite expansionary policies set to reduce the adverse effect of global fi nancial crisis, the economic activity is projected to deteriorate. The growth of output in the region is forecast to fall from 5.9 percent in 2008 to 2.5 percent a year later. The downturn is projected to be the same for oil and non-oil producing countries, even though the effective factors are quite different. The most sever turndown is anticipated in the United Arab Emirates (UAE). This fall is due to the exit of external funds; refl ecting a substantial decline in liquidity, property and equity prices; and intense pressure in the banking system. In contrast, Qatar is expected to grow by 18.0 percent in 2009 compared to 16.5 percent in the previous year. This growth is forecast to be as a result of substantial increase

in production of natural gas. Lebanon is also expected to experience the sharp slowdown because of external liquidity constraints and the slump in remittances.

Infl ation pressures in the region are estimated to decline sharply due to fall in commodity prices, rents, and economic activity (15.6 percent in 2008 compared to 11.0 percent in the following year).

For the region, the current account balance is forecast to experience a mild defi cit of about 0.6 percent of GDP in 2009.

Fiscal balances in oil-producing countries worsen dramatically due mainly to the slump in revenue.

In the region, central banks have taken sound policy actions such as injecting liquidity and reducing policy rates. In this regard, countries with pegged exchange rate regimes (Bahrain, Kuwait, Libya, Oman, Qatar, Saudi Arabia, Syrian Arab Republic, and UAE) have benefi ted from the expansionary monetary policy in the US.

The fi nancial sector is under pressure throughout the region, as credit exposure of banks elevates due to deterioration of property and stock markets and external liquidity constraints.

13Global Economic Prospects and Challenges

ANNUAL REPORT 2008

Commonwealth of Independent States

In comparison to the other regions of the global economy, the CIS countries are expected to face with the highest deterioration in economic activity in the near future. The effective factors behind the slowdown include diffi cult access to external funding, lower external demand, and the severe drop in commodity prices. In addition, households began to substitute domestic-currency-denominated assets with foreign-currency-denominated assets. Russia, Kazakhstan, Belarus, and Ukraine were severely damaged, with the fi rst two countries reducing foreign currency reserves markedly to lessen the impact of the shock on the exchange rate.

The growth prospects for the commodity exporters (Russia, Kazakhstan, Ukraine, and Turkmenistan) deteriorated. For the area, the current account balance is forecast to be about 0.1 percent of GDP in 2009 compared to 5.0 percent of GDP a year ago. The current account surpluses of energy exporter economies are expected to hit substantially, owing to the slump in commodity prices. However,

for energy importers, external defi cits are forecast to decline due to fi nancing constraints.

In the region, the output growth is estimated to contract by 5.1 percent in 2009 compared to 5.5 percent expansion in the previous year.

For the region as a whole, infl ation is expected to fall to 12.6 percent in 2009 compared to 15.6 percent in the preceding year.

Russia has let ruble to depreciate markedly and has increased interest rates, while Kazakhstan has opted for 18.0 percent devaluation. Other countries (Ukraine and Belarus) observed substantial depreciations of currency early in the crisis. The sharp depreciation of currency increases the effective debt burden on non-fi nancial fi rms that have borrowed in foreign currency.

The region enjoyed current account surplus of 5.0 percent of GDP in 2008, however the current account is projected to fall drastically to 0.1 percent of GDP a year later.

14 Global Economic Prospects and Challenges

ANNUAL REPORT 2008

World Economic Outlook (Percent change, unless otherwise noted)

Year 2007 2008Projections

2009 2010World Output 5.2 3.2 -1.3 1.9Advanced Economies 2.7 0.9 -3.8 0.0

United States 2.0 1.1 -2.8 0.0Euro area 2.7 0.9 -4.2 -0.4Japan 2.4 -0.6 -6.2 0.5United Kingdom 3.0 0.7 -4.1 -0.4Canada 2.7 0.5 -2.5 1.2Others 4.7 1.6 -4.1 0.6

Emerging and developing economies 8.3 6.1 1.6 4.0Africa 6.2 5.2 2.0 3.9Central and Eastern Europe 5.4 2.9 -3.7 0.8Commonwealth of Independent States 8.6 5.5 -5.1 1.2Developing Asia 10.6 7.7 4.8 6.1Middle East 6.3 5.9 2.5 3.5Western Hemisphere 5.7 4.2 -1.5 1.6

European Union 3.1 1.1 -4.0 -0.3World trade volume (goods and services) 7.2 3.3 -11.0 0.6Imports

Advanced economies 4.7 0.4 -12.1 0.4Emerging and developing economies 14.0 10.9 -8.8 0.6

ExportsAdvanced economies 6.1 1.8 -13.5 0.5Emerging and developing economies 9.5 6.0 -6.4 1.2

Commodity prices (USD)Oil 10.7 36.4 -46.4 20.2Non-fuel (average based on world commodity export weights) 14.1 7.5 -27.9 4.4Consumer prices

Advanced economies 2.2 3.4 -0.2 0.3Emerging and developing economies 6.4 9.3 5.7 4.7

London inter-bank offered rate (percent)On US dollar deposits 5.3 3.0 1.5 1.4On Euro deposits 4.3 4.6 1.6 2.0On Japanese yen deposits 0.9 1.0 1.0 0.5Source: World Economic Outlook, IMF, April 2009, Page 10

Source: World Economic Outlook, IMF, April 2009, Pages xv-xx, 1-17, and 63-95

Item

Economic Highlights of ACU Member Countries 15

ANNUAL REPORT 2008

BangladeshReal Gross Domestic Product (GDP) recorded a strong growth of 6.2 percent in 2007/08, marginally lower than 6.4 percent in 2006/07. The growth performance was underpinned by growth of 6.9 percent in industry sector, 6.7 percent in services sector and 3.6 percent in agriculture sector.

Domestic Savings-GDP ratio reduced marginally to 20.1 percent in 2007/08 from 20.4 percent in 2006/07. Investment-GDP ratio also decreased to 24.2 percent in 2007/08 from 24.5 percent in 2006/07.

Bangladesh Bank pursued growth supportive and prudent monetary policy stance during 2007/08.

Broad money (M2) growth was 17.6 percent during 2007/08, which was higher than 17.0 percent growth in 2006/07 and 16.0 percent growth targeted for 2007/08. The higher growth in M2 than programmed was mainly due to higher growth in net foreign assets.

Economic Highlights of ACUMember Countries

Revenue collection in 2007/08 increased by 22.3 percent over 2006/07.

A substantial growth of knitwear products (21.5 percent) and woven garments (10.9 percent) continued to support the high export growth of 15.7 percent in 2007/08.

The overall balance of payments (BOP) position of the country showed a smaller surplus of USD 604.0 million in 2007/08, against a surplus of USD 1,493.0 million in 2006/07, refl ecting reduction of current account surplus and also a substantial decline of surplus on capital and fi nancial account in 2007/08.

Workers’ remittances stood at USD 7,914.8 million in 2007/08 which was 32.4 percent higher than USD 5,978.5 million in 2006/07.

The gross foreign exchange reserves of the country stood at USD 6,149.0 million at the end of June 2008, but declined to USD 5,769.2 million as on February 19, 2009.

Economic Highlights of ACU Member Countries16

ANNUAL REPORT 2008

The foreign exchange market remained almost stable during 2007/08. However, at the end of 2007/08 the nominal Taka-US dollar exchange rate appreciated by 0.4 percent from Taka 68.8 per US dollar at the end of June 2007 to Taka 68.5 per US dollar at the end of June 2008.

Annual average consumer price index (CPI) (base: 1995/96=100) infl ation demonstrated an increase from 7.2 percent in 2006/07 to 9.9 percent in 2007/08. The rising trend in infl ation of 2006/07 as measured by CPI continued throughout 2007/08 due mainly to higher prices of oil and some other imported goods in the international market, disruptions in production and supply caused by repeated fl oods and cyclone.

BhutanIn 2007/08, Bhutan celebrated one hundred years of Monarchy.

The coronation of the fi fth King, Jigme Khesar Namgyel Wangchuck was held in 2007/08.

There was a smooth political transition from a monarchy to a democracy in March 2008.

The Indian Prime Minister, Dr. Manmohan Singh visited Bhutan in 2007/08 and addressed the fi rst session of the newly formed democratic government.

Tamabil port, was opened as the new trade route between Bhutan and Bangladesh.

The real GDP grew by an unprecedented rate of 21.0 percent in 2006/07, an exceptionally high growth due to the full commissioning of the biggest hydropower plant, Tala Hydroelectric Project Authority (THPA).

In line with the general developments in India, the major trading partner, the quarterly CPI reported a higher annual infl ation rate of 8.9 percent in the second quarter of 2008 as compared to 5.9 percent during the same period last year.

Monetary expansion continued to slow with M2 growing at 2.3 percent as compared to 8.6 percent in the previous year while credit to the private sector grew at 36.6 percent as compared to 35.5 percent in 2006/07.

In 2007/08, the substantial fall in exports resulted in a trade defi cit, reversing the surplus that was seen in 2006/07. However, current account and hence the overall balance is estimated to be in surplus due to grant and aid infl ows, resulting in an increase in the country’s gross international reserves by 8.0 percent.

On the exchange rate front, the ngultrum, which is pegged at par to the Indian

Economic Highlights of ACU Member Countries 17

ANNUAL REPORT 2008

Rupee appreciated by 8.7 percent against the US dollar since the last fi nancial year.

IndiaThe advance estimates of the Central Statistical Organisation (CSO) released in February 2009 placed the real GDP growth for 2008/09 at 7.1 percent. In its Annual Policy Statement for the year 2009/10 released in April 2009, the Reserve Bank has projected the GDP growth for 2008/09 in the range of 6.5 to 6.7 percent.

During 2008/09 so far (April-February), industrial growth based on the index of industrial production (IIP), decelerated to 2.8 percent from 8.8 percent in the corresponding period of the previous year.

As per the revised estimates for 2008/09, the gross fi scal defi cit (GFD) and revenue defi cit (RD) stood at 6.0 percent and 4.4 percent of GDP, respectively. As per the Interim Union Budget 2009/10, the GFD and RD are budgeted to decline to 5.5 percent and 4.0 percent of GDP during 2009/10.

During 2008/09, broad Money (M3) increased by 18.4 percent as at the end of March 2009 as compared to 21.2 percent as at the end of March 2008. On a year on year (YoY) basis, growth in reserve money (RM) was lower at 6.4 percent as

at the end of March 2009 as compared to 31.0 percent as at the end of March 2008.

During 2008/09, growth in bank credit moderated during 2008/09 from the strong pace of the previous three years. Aggregate deposits of commercial banks expanded by 19.8 percent as at the end of March 2009 as compared to 22.4 percent a year ago.

Commercial banks’ non-food credit decelerated to 17.5 percent as at the end of March 2009 from 23.0 percent a year ago.

Headline infl ation, as measured by YoY variations in the wholesale price index (WPI), decelerated sharply from its intra-year peak of 12.9 percent on August 2, 2008 to 0.3 percent by March 28, 2009.

During 2008/09, growth in India’s exports decelerated to 3.4 percent from 29.0 percent in 2007/08, while growth in imports was also lower at 14.3 percent as compared to 35.5 percent in 2007/08.

India’s current account defi cit (CAD) widened during 2008/09 (April-December) to USD 36.5 billion in April-December 2008 from USD 15.5 billion in April-December 2007 mainly led by larger trade defi cit on account of higher growth in imports coupled with a slowdown in

Economic Highlights of ACU Member Countries18

ANNUAL REPORT 2008

export growth. Overall, the trade defi cit was higher at USD 105.3 billion during April-December 2008 as compared with USD 69.3 billion in April-December 2007.

The capital account balance moderated during April-December 2008 mainly due to higher gross capital outfl ows coupled with lower gross capital infl ows. While the gross capital infl ows declined toUSD 246.4 billion during April-December 2008 from USD 291.8 billion in April-December 2007, the gross capital outfl ows increased to USD 231.1 billion from USD 209.8 billion during the same period.

Gross inward foreign direct investment (FDI) was USD 31.7 billion during 2008/09 so far (April-February) as compared withUSD 27.6 billion in the corresponding period of the previous year. During 2008/09, foreign institutional investors recorded a net outfl ow of USD 15.0 billion as against net infl ows of USD 20.3 billion a year ago. Refl ecting the tight liquidity conditions in the overseas credit markets and increased cost of borrowings, gross inflows under external commercial borrowings (ECBs) to India moderated sharply during April-December 2008.

India’s total external debt stood atUSD 230.8 billion at the end of December 2008. The increase in external debt stock was essentially due to increase inlong-term debt outstanding by USD 9.4

billion, especially commercial borrowings and bilateral debt, during the third quarter of 2008/09. Short-term debt, however, declined by USD 3.2 billion.

Debt sustainability indicators remained at a comfortable level at the end of December 2008. The debt service ratio was placed at 5.3 percent during the third quarter of 2008/09. The ratio of short-term to total debt was 20.6 percent while the ratio of short-term debt to reserves was 18.5 percent at the end of December 2008. India’s foreign exchange reserves exceeded the external debt by USD 25.1 billion, providing a cover of 110.9 percent to the external debt stock at the end of December 2008.

During the fi nancial year (FY) 2008/09, India’s foreign exchange reserves at USD 252.0 billion declined by USD 57.7 billion from USD 309.7 billion as at the end of March 2008.

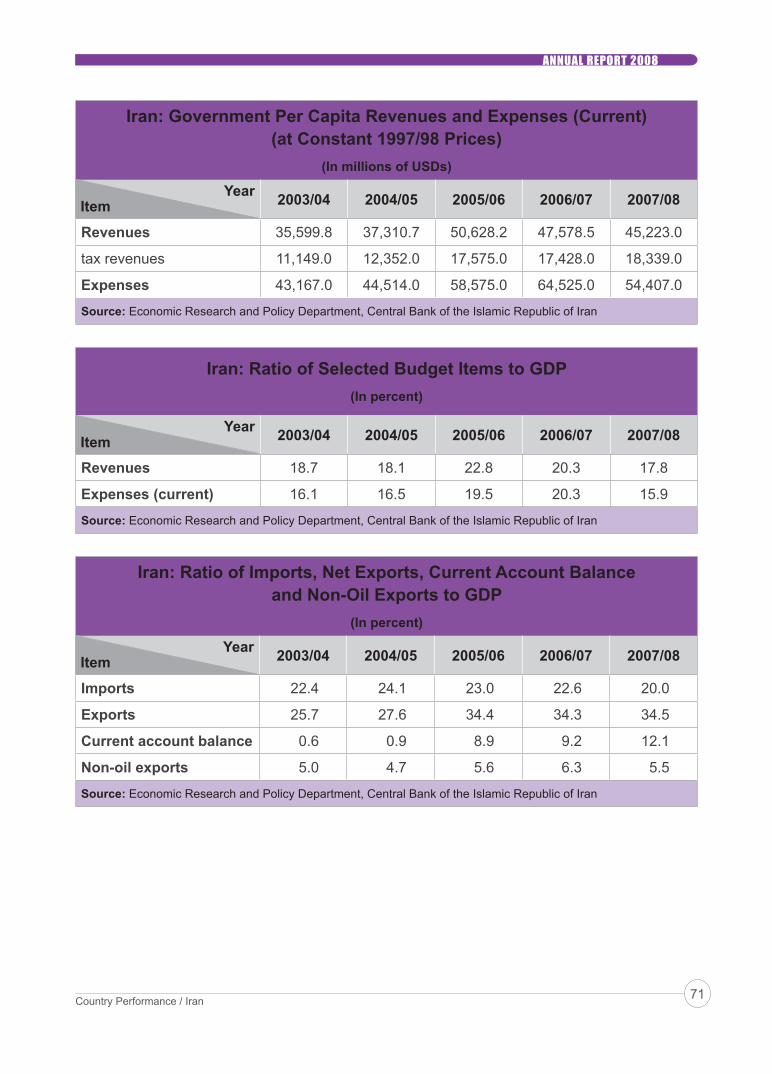

IranDuring 2007/08 (1386), Iranian economy was stable and smooth. Sharp rise in prices and acceleration of infl ation was a foreseeable phenomenon which was realized. In spite of higher infl ation, other major real sector indicators like GDP growth and unemployment rate, did not manifest major changes from medium-term trends.

Economic Highlights of ACU Member Countries 19

ANNUAL REPORT 2008

Based on preliminary estimates, GDP at current prices rose from Rls. 2,038.0 trillion in 2006/07 to Rls. 2,623.0 trillion in 2007/08, showing 28.7 percent growth in nominal terms and 6.9 percent growth in real terms, which indicates 0.7 percentage point increase at constant prices compared with the previous year. Meanwhile, non-oil GDP registered 7.6 percent growth, up by 1.0 percentage point compared with 2006/07.

Iran’s average crude oil production, in adherence to the production quotas set by the Organization of Petroleum Exporting Countries (OPEC), amounted to 4.1 mb/d in 2007/08. Crude oil exports increased by 2.0 percent to 2.5 mb/d; however, exports of oil products plummeted by 25.2 percent to 199.0 thousand b/d compared with the previous year. The average spot price of Iran’s crude oil export grew by 30.9 percent to about USD 78.0.

Of the key objectives of the Fourth Five-Year Development Plan (FFYDP) is to reduce unemployment rate to 8.4 percent by the end of the Plan (2009/10). According to the data drawn by the Statistical Center of Iran (SCI) in the “Labor Force Survey”, unemployment rate stood at 10.5 percent in 2007/08, showing 0.8 percentage point decline compared with 2006/07.

Government general revenues amounted to Rls. 298,203.1 billion in the review year, showing 29.0 percent growth

compared with the previous year. Share of tax revenues in total revenues declined from 65.6 percent in 2006/07 to 64.3 percent in the review year. Government tax revenues rose by 26.5 percent toRls. 191,815.3 billion in 2007/08, compared with the previous year.

In the review year, the government expenses rose to Rls. 421,334.1 billion, representing 1.3 percent increase against the previous year. Meanwhile, national expenses declined by 0.9 percent, and provincial expenses grew by 7.9 percent, constituting respectively 72.6 and 27.4 percent of government expenses.

Government paid a total of Rls. 147,715.8 billion for the acquisition of non-fi nancial assets, indicating 1.5 percent growth compared with the year before. Of total payments by the government for the acquisition of non-fi nancial assets, 76.7 percent were in the form of national and 23.3 percent in the form of provincial expenses.

Trade balance posted a surplus ofUSD 40,819.0 million in the review year. This, together with the USD 7,199.0 million defi cit in foreign services balance and the USD 461.0 million surplus in the transfers account, resulted in the USD 34,081.0 million surplus in the current account of BOP. However, non-oil current account ran a defi cit of USD 47,683.0 million, up by 14.6 percent compared with

Economic Highlights of ACU Member Countries20

ANNUAL REPORT 2008

the previous year defi cit of USD 41,609.0 million. This indicates the greater role of oil sector in the external sector of the Iranian economy. Moreover, balance of the Oil Stabilization Fund (OSF) grew by 89.1 percent to USD 38,871.0 million at the end of 2007/08.

Liquidity growth stood at 27.7 percent at the end of 2007/08, indicating 11.7 percentage points reduction against the previous year-end. Among the factors affecting liquidity growth, net foreign and domestic assets of the banking system constituted respectively 3.6 and 24.1 percentage points of liquidity growth.

The Money and Credit Council (MCC) set the minimum lending rate on the facilities extended by public banks for transaction contracts at 12.0 percent for all economic sectors in 2007/08.

Upon reduction of public banks’ lending rates during 2004-08, the minimum expected lending rate of private banks was adjusted in the review year. According to the MCC approval, the minimum expected lending rate on the facilities extended by private banks and credit institutions for transaction contracts was set at 13.0 percent for all economic sectors.

Based on the recommendation of the MCC, the Parliament approved issuance of participation papers by the Central

Bank of Iran (CBI) worth Rls. 40.0 trillion at the provisional profi t rate of 15.5 percent. These papers were tax-exempt with a one-year maturity from the date of issuance.

The recessionary condition in stock market continued in 2007/08. This was largely due to regional uncertainties and certain public policies regarding price administration and short-term boom in real estate market which gravely affected investors’ decision in the stock market.

In 2007/08, the Tehran Stock Exchange Price Index (TEPIX) rose by 2.7 percent, “fi nancial index” 0.5 percent, “industrial index” 2.8 percent, “price and dividend index” 17.6 percent, and “cash dividend index” 14.5 percent. On the other hand, 50 top companies index fell by 19.6 percent. The turnover ratio1 reached 17.1 percent at the end of 2007/08, up from 15.4 percent at the end of 2006/07.

The CPI of goods and services advanced 18.4 percent (base year=2004/05), indicating 6.5 percentage points increase compared with the 11.9 percent growth of the previous year. Among the special groups, the price index of “goods”, with 17.4 percent increase compared with the previous year, accounted for 52.0 percent of the rise in the general index. The main group of “food and beverages”, with 21.7 percent rise compared with the year before, raised the general index by 34.0

1 It is the ratio of trading value to average current value of shares.

Economic Highlights of ACU Member Countries 21

ANNUAL REPORT 2008

percent.

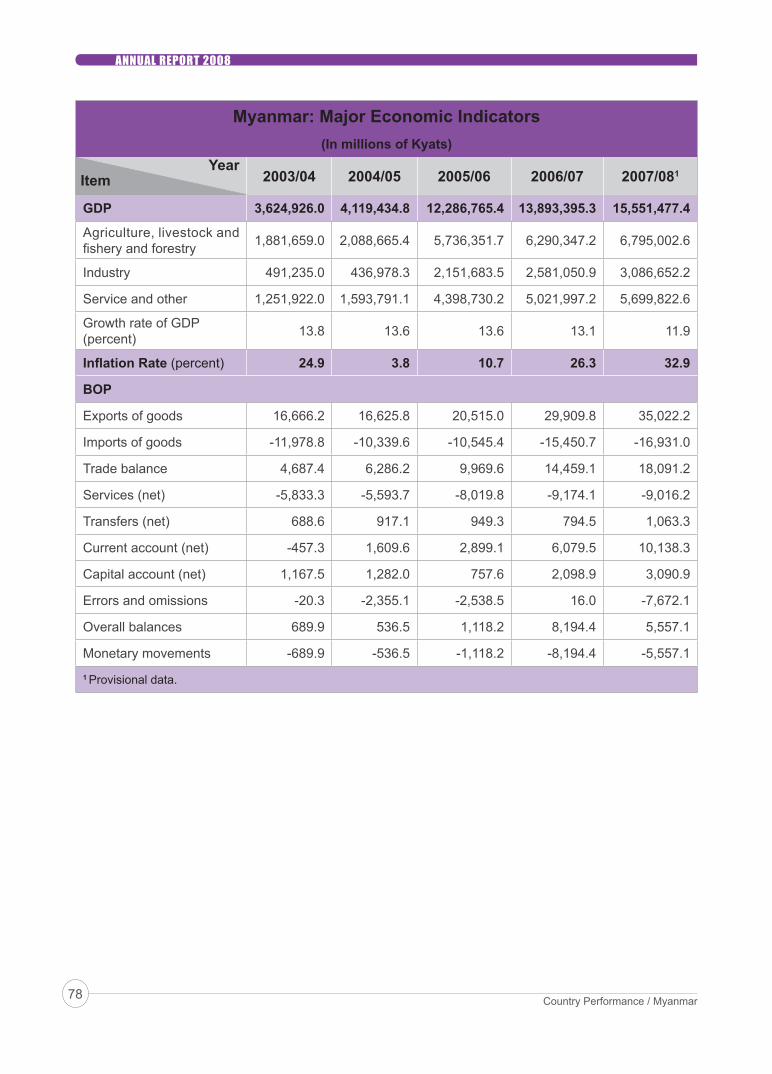

MyanmarThe Government of Myanmar has been formulating and implementing economic short-term plans with a view to achieve balanced economic development in all the economic sectors since the FY 1992/93. The previous three consecutive economic short-term plans; 1992/93 to 1995/96, 1996/97 to 2000/01, 2001/02 to 2004/05, achieved with high growth rates. The fourth fi ve-year economic short-term plan has been formulated from 2006/07 to 2010/11. FY 2007/08 was the second year of the fourth fi ve-year plans and the growth rate of real GDP recorded 11.9 percent. During 2007/08, agriculture, livestock, fi shery and forestry sector are the main contributors to GDP with the share of 44.0 percent, followed by 36.0 percent of the services and other sector and industry sector of 20.0 percent respectively. Looking at the past trend, the share of agriculture, livestock, fi shery and forestry sector in the total GDP indicating 1.0 percent only decreased from the previous year but slightly decreased to 3.0 percent from 2005/06. The share of industry sector in the total GDP has been rising trend. On the other hand, services and other sector decreased to 6.0 percent compared to a year ago. It can be said that the growth refl ected a more diversifi ed and expansion in industry sector.

The Government emphasized the development of the infrastructure sector and encouragement of the private sectors’ economic activities. The government has also focused its expenditure on the provision of essential services building of dams, health and housing. Accordingly, these efforts have caused substantial increase in government expenditures during the recent years. Looking at the revenue side, various tax reform measures have been taken including broadening the tax base, adjusting tax rates and strengthening tax administration and enhancing the State Economic Enterprises’ (SEEs) performance resulted in a substantial increase in revenue. Therefore, the tax revenues have been rising. However, the government revenue has been offset by the increase in government expenditure, especially increase in salaries of government employees in 2006/07. Consequently, the government budget continued to remain in defi cit.

Growth in aggregate bank deposits accelerated to 32.0 percent during 2007/08. Bank credit to commercial sector expanded by 13.0 percent during 2007/08. The banking system remains the main mobilizer of funds in the economy. Monetary policy continues to support economic growth in 2007/08. However, maintaining accommodative monetary stance became more challenging particularly in light of inflationary

Economic Highlights of ACU Member Countries22

ANNUAL REPORT 2008

pressures. The Central Bank of Myanmar has monitored the domestic banks by issuing instructions and using the on-site examination and off-site monitoring.

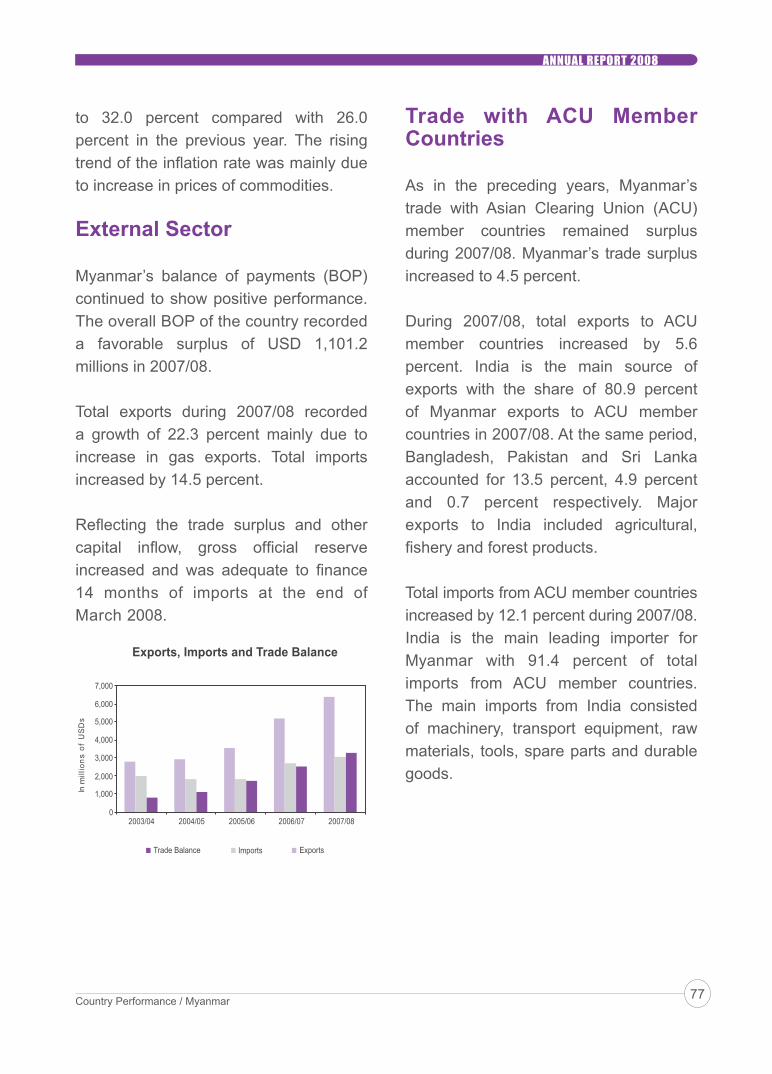

Myanmar’s BOP continued to show positive performance. The overall BOP of the country recorded a favorable surplus of USD 1,101.2 millions in 2007/08. Total exports during 2007/08 recorded a growth of 22.3 percent mainly due to increase in gas exports. Total imports increased by 14.5 percent. Refl ecting the trade surplus and other capital infl ow, gross offi cial reserve increased and was adequated to fi nance 14 months of imports at the end of March 2008. As in the preceding years, Myanmar’s trade with Asian Clearing Union (ACU) member countries remained surplus during 2007/08. Myanmar’s trade surplus increased to 4.5 percent. During 2007/08, total exports to ACU member countries increased by 5.6 percent. Total imports from ACU countries increased by 12.1 percent during 2007/08.

NepalThe performance of Nepalese economy remained satisfactory in 2007/08 compared to that of the previous year. Nepalese economy witnessed a healthy economic growth-the highest in the last four years- in the review period and infl ation stood at a moderate level.

The real GDP at producers’ price

increased by 4.7 percent in 2007/08, compared to that of 2.5 percent in the previous year. The improved performance of agriculture sector coupled with a satisfactory expansion of service sector helped grow the economy to the peak of four years. The annual average consumer price infl ation, however, rose to 7.7 percent in 2007/08 from 6.4 percent in the previous year. The rise in food prices and the price hike in petroleum products were the driving factors for infl ation in 2007/08.

Monetary growth was higher than that of the previous year. For example, M2 rose by 25.2 percent in 2007/08 compared to a growth of 14.0 percent in the previous year. Likewise narrow money (M1) also showed a higher growth of 21.6 percent compared to an increase of 12.2 percent in the previous year. A signifi cant increase in both net foreign assets (NFA) and net domestic assets (NDA) contributed to such a substantial increase in monetary aggregates in the review year.

The Government’s budget on a cash basis recorded a defi cit of Rs. 21.2 billion in 2007/08 compared to the defi cit of Rs. 18.8 billion a year ago. The budget defi cit to GDP ratio remained at 2.6 percent in 2006/07 as in the previous year.

On the external sector front, the merchandise trade defi cit expanded by

Economic Highlights of ACU Member Countries 23

ANNUAL REPORT 2008

22.5 percent. This was on account of higher import growth of 16.1 percent and a lower export growth of 2.4 percent. However, the current account showed a surplus of Rs. 21.7 billion mainly due to the robust growth in external net transfer income. The overall BOP posted a surplus of Rs. 29.7 billion in 2007/08.

Workers’ remittance infl ow recorded an increase of 42.5 percent to Rs. 142.7 billion in 2007/08 compared to an upsurge of 2.5 percent to Rs. 100.0 billion in the previous year. The workers’ remittances to GDP ratio increased to 17.4 percent in 2007/08.

The Nepalese stock market witnessed a major expansion in 2007/08. The YoY Nepal Stock Exchange (NEPSE) index increased by 40.9 percent to 963.4 points in the middle of July 2008. The index was at 684.0 points a year ago. The increased confi dence of investors in the aftermath of political change and a number of corporate actions taken by bank and fi nancial institutions contributed to the upsurge in the NEPSE index.

PakistanThe macroeconomic stresses have visibly eased by November 2008, as the Government entered into a macroeconomic stabilization program to support medium-term reforms under the aegis of the International Monetary Fund

(IMF).

The disbursement of the fi rst tranche under the program meant that any immediate risk of default on external obligations receded, with a substantial improvement in foreign exchange reserve adequacy indicators, and lending strength to the rupee.

At the same time, a sharp decline in international commodity prices is expected to substantially lower the country’s import bill, offering the possibility of a decline in the country’s very large current account defi cit, and lower infl ation.

This supply-side improvement has been reinforced by the reasonably good performance of crops during kharif 2008/09 cropping season. These factors appear to have already halted the persistent uptrend in infl ationary pressures in the economy. Together, they could also help support a very modest improvement in the growth outlook for 2008/09.

There is also substantial progress on containing fi scal imbalances as the Government reduced subsidies, contained growth in other spending and increased revenues. Thus, there is a sharp fall in the fi scal defi cit from 3.4 percent of GDP during the fi rst half of 2007/08 to 1.9 percent of GDP in the fi rst half of 2008/09.

Economic Highlights of ACU Member Countries24

ANNUAL REPORT 2008

While many of the country’s macroeconomic indicators may no longer be worsening, the imbalances are nonetheless still quite large. Resolving them will require disciplined efforts.

The BOP position is still exposed to several risks as exports may be adversely affected due to domestic structural bottlenecks featuring intermittent power and gas supplies and global recession. The latter development may also affect the not only the growth in workers’ remittances, there is also a likelihood of a severe reduction in fi nancial infl ows to emerging market including Pakistan.

On the fi scal side, the risk of missing the tax revenue target has increased in the wake of slowing economic activity.

Currently, the decline in domestic oil prices is not in line with the sharp decline in international oil prices. A regular transfer of the international oil price impact to domestic prices is instrumental in establishing confi dence over Government’s actions. A delayed or no action by the Government after a decline in oil prices not only reduces the direct trickle down impact on domestic prices but also dissuades adjustments in infl ationary expectations.

Though CPI infl ation has eased somewhat its persistence at a high level remains a source of concern. With a

sustained period of high infl ation, there is always a risk and tendency for infl ation to take a chronic form as it becomes entrenched in public’s expectations.

Sri LankaSri Lankan economy demonstrated its resilience by recording a growth of 6.0 percent in 2008 in the midst of unprecedented and unfavorable developments globally and domestically. All the sectors comprised of services, industry, and agriculture contributed favorably towards this growth. During the fi rst part of the year, food and energy crises in the global economy was threatening the macroeconomic imbalances by way of sharply widening trade and current account balances, rising infl ation to the highest ever levels since 1980s and exerting pressures on fi scal balances due to high defense expenditure, cost of reconstruction of the Eastern province and tax exemptions arising from duty waivers in order to minimize the impact of high food and energy prices on domestic cost of living. Towards the latter part of the year, second wave of global fi nancial crisis, which was originated from the sub-prime mortgage issues in the United States (US), turned into a global fi nancial turmoil. This fi nancial turmoil triggered a reversal of capital fl ows from emerging market economies for safety. Sri Lanka also had to cope with its share of sudden withdrawal of foreign capital by

Economic Highlights of ACU Member Countries 25

ANNUAL REPORT 2008

running down almost 50.0 percent of its external offi cial reserves.

Earnings from exports in 2008 totalled USD 8,137.0 million recording a growth of 6.5 percent compared to 2007. Expenditure on imports grew signifi cantly by 24.0 percent as a result of historically high commodity prices. The services account surplus together with the increased worker remittances helped contain the current account defi cit. However, the surplus in the capital and fi nancial account was not suffi cient enough to offset the defi cit in the current account leading to an overall defi cit of USD 1,225.0 million in the BOP by the end of 2008.

The monetary policy of the Central Bank had been tight during the fi rst three quarters in order to contain the higher infl ation resulted from the global food and energy crisis. However, with the escalation of the fi nancial crisis towards the latter part of 2008 the bank had to relax its policy stance in order to enhance the market liquidity and mitigate harmful impacts of domestic fi nancial market.

Prudential regulations and timely action by the Central Bank enabled to maintain fi nancial system stability despite looming threats arising from excessive domestic credit expansion in the past and high interest rates resulting from the tight monetary policy and the collapse of some domestic illegal deposit taking institutions linked to a major fi nancial institution while global fi nancial turmoil cutting off external funding lines to the domestic banking sector.

The fi scal policy strategy of the Government continued to be in the direction enunciated within the overall development strategy of the Government pronounced in the “Ten-Year Horizon Development Framework: 2006-16” (Ten-year Vision). Accordingly, the gradual reduction of the overall budget defi cit to a sustainable level is the thrust of the fi scal policy framework. The medium-term fi scal policy priorities continue towards the fi scal consolidation process by maintaining healthy government revenue and rationalizing recurrent expenditures.

ANNUAL REPORT 2008

26 Country Performance / Bangladesh

BangladeshThe Bangladesh economy showed signs of resilience by maintaining a satisfactory growth momentum in the face of repeated fl oods and cyclone Sidr, and a spike in prices of oil, rice and most commodities in the global market. The government and the Bangladesh Bank (BB) continued to adopt policies in bringing the economy back to its growth momentum. The Government’s growth stimulating and poverty reduction programmes coupled with prudent monetary policies of BB contributed toward a strong real Gross Domestic Product (GDP) growth of 6.2 percent in 2007/08, slightly lower than 6.4 percent of 2006/07. The growth performance was underpinned, on the supply side, by a moderate growth in the agriculture sector and continued strong growth in the industry sector and the services sector, despite two consecutive fl oods and devastating cyclone Sidr and soaring commodity prices in the international market. Economic growth was also aided by the rapid growth in exports and surging remittances. Export earnings recorded a strong growth of

15.7 percent and remittances from non-resident Bangladesh nationals increased substantially by 32.4 percent in 2007/08.

The rising trend in infl ation of 2006/07 as measured by Consumer Price Index (CPI) continued throughout 2007/08 due mainly to higher prices of oil and some other imported goods in the international market, disruptions in production and supply caused by repeated fl oods and cyclone. BB pursued growth supportive and prudent monetary policy stance during 2007/08 to ease the uptrend in infl ationary tendency.

Economic Growth

The 6.2 percent real GDP growth in 2007/08 was propelled mainly by a moderate growth in the agriculture sector and continued strong growth in industry sector, and services sector. Growth rate in agriculture sector achieved a moderate growth of 3.6 percent in 2007/08 against 4.6 percent growth recorded in 2006/07. The deceleration in this sector was

Country Performance

27Country Performance / Bangladesh

ANNUAL REPORT 2008

mainly due to lower growth in crops and horticulture sub-sector. The industry sector attained a growth of 6.9 percent in 2007/08, as against 8.4 percent of 2006/07. The growth rate was led by export-oriented manufacturing and supported by strong growth in mining and quarrying sub-sector. The service sector grew by 6.7 percent in 2007/08, slightly lower than 6.9 percent recorded in 2006/07.

unprecedented rise in commodity prices in the international market particularly of foods and fuel, shortfall in domestic food production and supply due mainly to devastating fl oods and cyclone and higher domestic production cost of essential goods. Annual average CPI (base: 1995/96=100) infl ation increased from 7.2 percent in 2006/07 to 9.9 percent in 2007/08. On a point to point basis the rate of infl ation showed an increase from 9.2 percent in 2006/07 to 10.0 percent in 2007/08.

Savings and Investment

Domestic savings-GDP ratio slightly reduced from 20.4 percent of 2006/07 to 20.1 percent in 2007/08 and investment-GDP ratio also decreased from 24.5 percent of 2006/07 to 24.2 percent in 2007/08.

Price Situation

Bangladesh economy witnessed a continued upward infl ationary pressure in 2007/08. The persistent rise in infl ation during 2007/08 was attributed to

Fiscal Developments

In the revised budget, revenue as a percentage of GDP increased to 11.3 in 2007/08 as compared to 10.6 in 2006/07. Expenditure on Annual Development Program (ADP) as percentage of GDP decreased to 4.2 during 2007/08 from 4.6 in 2006/07. To meet the expenditure partially, government borrowings from the banking system was Taka 104.0 billion (1.9 percent of GDP). The rest amount of Taka 95.2 billion (1.8 percent of GDP)

ANNUAL REPORT 2008

28 Country Performance / Bangladesh

of domestic fi nancing of the defi cit was non-bank borrowings mainly consisting of non-cash bond and National Savings Scheme Certifi cate bought and held by the public. The foreign fi nancing component of the budget defi cit was Taka 131.5 billion (2.5 percent of GDP), consisting of foreign grants and loans. The overall budget defi cit (excluding grants) as percentage of GDP, however, stood at Taka 330.7 billion or 6.2 percent of the GDP in 2007/08 which was Taka 173.7 billion or 3.7 percent of the GDP in 2006/07.

Monetary and Credit Situation

BB pursued growth supportive and prudent monetary policy stance to ease the uptrend infl ationary tendency. Broad money (M2) growth was 17.6 percent during 2007/08 which was higher than 17.0 percent growth in 2006/07 and also higher than 16.0 percent growth targeted under the programme for 2007/08. The accelerated growth in broad money than programmed was mainly due to higher growth in net foreign assets although offset slightly by the lower growth in net domestic assets. The growth in net foreign assets stood at 15.1 percent as against projection of 3.4 percent during 2007/08 though notably lower than 49.4 percent growth in 2006/07.

Total domestic credit increased by 21.8 percent during 2007/08, higher than 14.4

percent increase during 2006/07. The private sector credit grew at 24.9 percent notably higher than projected growth of 14.9 percent and the actual growth of 15.0 percent during 2006/07 refl ecting increased economic activities in the real sector. The public sector credit increased by 11.9 percent during 2007/08 compared to projected growth of 26.4 percent and actual growth of 12.4 percent in 2006/07 mainly due to downsizing of ADP, better revenue collection and increased fl ow of foreign fund.

The Cash Reserve Requirement (CRR) for the scheduled banks with the BB remained same at 5.0 percent of their total demand and time liabilities since October 1, 2005. Statutory Liquidity Ratio (SLR) for the scheduled banks, except banks operating under the Islamic Shariah and the specialized banks remained same at 18.0 percent of their total demand and time liabilities, excluding inter bank items since October 1, 2005. The SLR for the Islamic banks remained unchanged at 10.0 percent. The specialized banks continued to remain exempted from maintaining the SLR.

Exchange Rate Developments

The foreign exchange market remained almost stable during 2007/08. During the fi rst quarter of 2007/08, Taka-US dollar exchange rate started with Taka 68.9. Initially there was a modest pressure on

29Country Performance / Bangladesh

ANNUAL REPORT 2008

the exchange rate due to higher demand in the foreign exchange market. With the beginning of second quarter, Taka started to appreciate and in the middle of December it stood at Taka 68.5. During the Third quarter of the year, Taka remained relatively stable with exchange rates ranging within Taka 68.56-68.60. However, at the end of 2007/08, Taka gained slightly and stood at Taka 68.5. The weighted average Taka-US dollar exchange rate came down from Taka 68.8 at the end of June 2007 to Taka 68.5 at the end of June 2008. During the second quarter of 2007/08, BB injected USD 735.5 million to ease the higher import payments related liquidity pressure in the foreign exchange market. At the end of 2007/08 BB purchased USD 202.5 million from the commercial banks for absorbing excess liquidity of the market. However, the nominal Taka-US dollar exchange rate appreciated by 0.4 percent from Taka 68.8 per US dollar at the end of June 2007 to Taka 68.5 per US dollar at the end of June 2008.

Exports (fob)

Export earnings (fob including Export Processing Zone (EPZ)) during 2007/08 increased by 15.7 percent to USD 13,945.0 million as compared to USD 12,053.0 million in the preceding year. A substantial growth of knitwear products (21.5 percent) and woven garments (10.9 percent) continued to support the high

Imports (fob)

Import payments (fob) during 2007/08 stood at USD 19,486.0 million registering a growth of 25.6 percent as compared to USD 15,511.0 million in 2006/07. Increased imports of rice (385.6 percent), fertilizer (77.0 percent), edible oil (72.6 percent), pulses (67.7 percent), milk and cream (65.1 percent) and raw cotton (41.2 percent) contributed in varying degrees to the rise in aggregate imports during 2007/08 over 2006/07.

growth of exports in 2007/08.

ANNUAL REPORT 2008

30 Country Performance / Bangladesh

Workers’ Remittances

Workers’ remittances stood at USD 7,914.8 million in 2007/08 which was 32.4 percent higher than USD 5,978.5 million in 2006/07. The underlying reason for growth of remittances was that BB made vigorous efforts such as expansion of activities of drawing arrangements, review of statements received from foreign banks/exchange houses, close monitoring and supervision of banks, etc. Besides, the concerned scheduled banks had ensured quick delivery of remittances by reducing lead time to the benefi ciaries in Bangladesh, which brought substantial development in the delivery system.

Foreign Exchange Reserves

The gross foreign exchange reserves of the BB continued to grow in the backdrop of steadily increasing export earnings and workers’ remittances and stood at USD 6,149.0 million at the end of June 2008 as against USD 5,077.0 million at the end of June 2007. Foreign exchange reserves stood at USD 5,769.2 million as on February 19, 2009.

Balance of Payments (BOP)

Notwithstanding a hefty 32.4 percent rise in workers’ remittances, the overall BOP position of the country showed a smaller surplus of USD 604.0 million in 2007/08, against a surplus of USD 1,493.0 million

in 2006/07, refl ecting reduction of current account balance surplus from USD 936.0 million in 2006/07 to USD 672.0 million in 2007/08 and substantial decline of surplus on the capital and fi nancial account to USD 145.0 million in 2007/08 from USD 1,252.0 million in 2006/07. The reduction in current account surplus occurred due to widening of the defi cits on the trade, services and income accounts. The defi cit on trade account, income account and service account increased from USD 3,458.0, USD 905.0 and USD 1,255.0 million in 2006/07 to USD 5,541.0, USD 1,005.0 and USD 1,525.0 million in 2007/08.

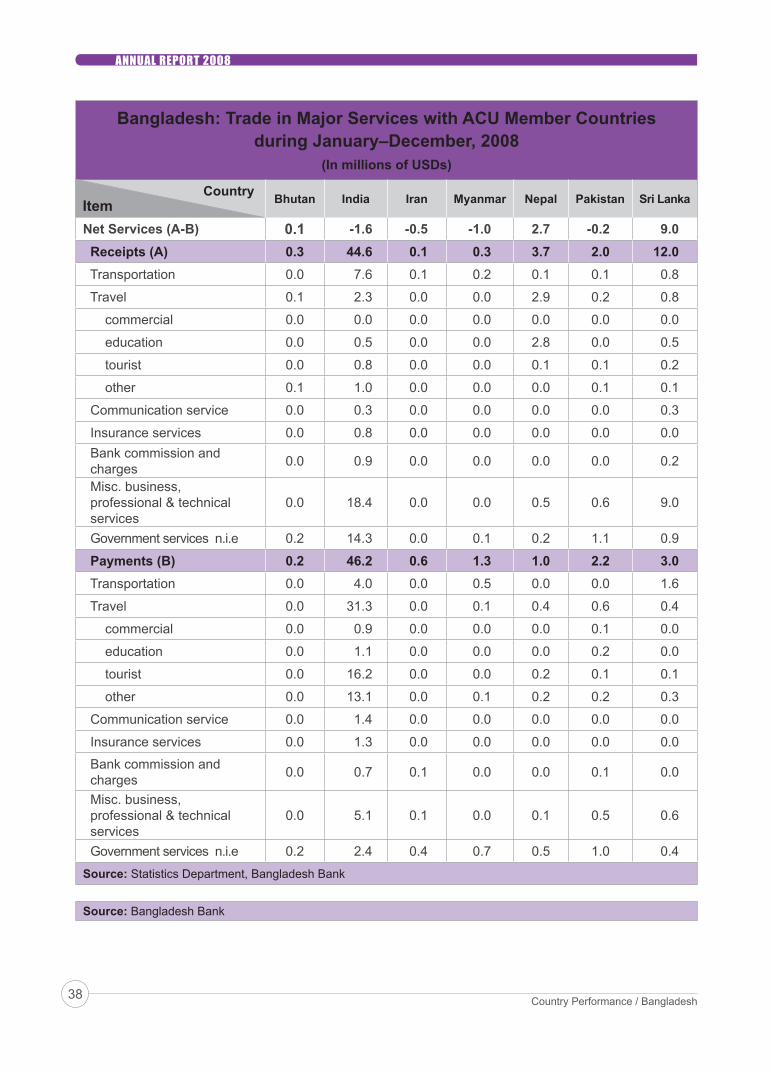

Trade with ACU Member Countries

Total trade (exports + imports) of Bangladesh under Asian Clearing Union (ACU) increased in 2007/08 compared to that in the previous year. As in the preceding years, Bangladesh remained a net debtor in all the six bi-monthly settlements during the year. Export

31Country Performance / Bangladesh

ANNUAL REPORT 2008

1 1 ACUD = 1 USD.

receipts and import payments both increased substantially with the ACU member countries during the year under report. Exports of Bangladesh to the ACU member countries recorded increase of USD 21.51 million or 16.4 percent to USD 153.0 million during 2007/08 from USD 131.5 million in 2006/07. On the other hand, import from the ACU member countries increased substantially by USD 1,436.3 million or 62.4 percent from USD 2,301.1 million in 2006/07 to USD 3,737.3 million in 2007/08. As a result, the net debtor position of Bangladesh increased by USD 1,414.8 million or 65.2 percent to USD 3,584.3 million in 2007/08 compared to USD 2,169.6 million in the preceding year.

Outlook and Challenges

2007/08 was a challenging and eventful year for Bangladesh on several counts. Over the fi rst half of the fi nancial year, two successive fl oods, devastating cyclone Sidr, domestic infl ation, global market scenarios and the consequent impact of these on investment and business confi dence put the economy under serious test. But the economy bounced back strongly in the second half of the fi nancial year with pro-active measures by the Government along with BB’s timely measures in improving production environment through encouraging unhindered fl ow of credit to productive sectors like agriculture, Small and

Medium Enterprises (SMEs), and other income generating rural activities being the prime targets.

Recently, Bangladesh and all other South Asian countries have been experiencing infl ationary pressures resulting mainly from higher food and energy prices in the international market. Furthermore, in Bangladesh, production losses due to repeated fl oods and cyclone Sidr have added to the infl ationary pressures. Besides, the sustained high global oil prices have heightened pressure on country’s BOP, threatened fi scal and monetary stability alongside adversely affecting the economic activity. Maintaining fi scal discipline by the Government and minimizing the dependence on fi nancing fi scal defi cit from the banking system generate less infl ationary pressure. The Government raised administered prices of oil and revised the oil prices downward following recent decline in global oil prices. It is important to introduce a pricing system providing for automatic adjustment of domestic fuel prices with some mechanisms to protect the farmer and the poor from hardships. Besides, there is a need to reduce dependence on imported petroleum products by maximizing the use of alternative indigenous fuels and enhancing the effi ciency of energy use.

The depth and severity of the recent global fi nancial crisis as well as its impact on Bangladesh economy is still

ANNUAL REPORT 2008

32 Country Performance / Bangladesh

unfolding. However, Bangladesh is relatively insulated from the fi nancial side, but the global growth outlook, especially the growth prospect in the United States (US) and the country’s other major trade partners, has weakened which could create adverse impact on export growth, particularly export growth of ready-made garments (RMGs).

By maintaining macroeconomic stability through prudent fi scal and monetary policy with supportive external sector policy and

progress in advancing structural reforms, against the backdrop of recent natural disasters and food crisis, the near and medium-term macroeconomic prospects of Bangladesh appear favourable. In the updated medium-term macroeconomic framework (MTMF) of Poverty Reduction Strategy Paper (PRSP)1 under the base case scenario, the real GDP growth has been projected to increase gradually to 6.5 percent in 2008/09, 7.0 percent in 2009/10 and 7.2 percent in 2010/11.

1 Source: Moving Ahead-National Strategy for Accelerated Poverty Reduction II (FY2009-11), Planning Commission, Government of the People’s Republic of Bangladesh, October 2008.

33Country Performance / Bangladesh

ANNUAL REPORT 2008

Bangladesh: Major Economic Indicators

Year 2003/04 2004/05 2005/06 2006/07 2007/08

National Income and PricesReal GDP growth (percent) 6.3 6.0 6.6 6.4 6.2

GDP defl ator (percent change) 4.2 5.1 5.2 6.8 8.0

CPI infl ation (annual average) 5.8 6.5 7.2 7.2 9.9

GDP at current market prices (billion Taka) 3,330.0 3,707.0 4,157.0 4,725.0 5,419.0

GDP at current market prices (billion US dollar) 56.5 60.4 62.0 68.4 79.0

Fiscal Sector (percent of GDP)Total revenue 10.6 10.6 10.8 10.6 11.3

Total expenditure 14.8 15.1 14.7 14.3 17.5

Overall budget defi cit (excluding grants) 4.2 4.5 3.9 3.7 6.2

Financing of overall budget defi cit 4.6 4.5 3.3 3.7 6.2

Net domestic fi nancing 2.2 2.1 2.0 2.1 3.7

Bank borrowings 0.8 1.0 1.2 1.4 1.9

Non bank borrowings 1.4 1.1 0.8 0.7 1.8

Net foreign fi nancing 2.4 2.4 1.3 1.6 2.5

Money and Credit (percent change)Private sector 14.2 17.0 18.1 15.0 25.0

Broad money (M2) 13.8 16.7 19.3 17.1 17.6

Balance of Payments (percent change)Exports (fob) 15.9 14.0 21.6 15.8 15.7

Imports (fob) 13.0 20.6 12.1 16.6 25.6

Remittances 10.1 14.1 24.8 24.5 32.4

Gross offi cial reserve (million US dollar) 2,705.0 2,930.0 3,484.0 5,077.0 6,149.0

Gross offi cial reserve (month of imports) 2.8 2.5 2.7 3.3 3.2

Sources: (i) Bangladesh Bank Annual Report 2007/08; (ii) Economic Trends, November 2008, Bangladesh Bank; and (iii) Bangladesh Bank Quarterly, July-September 2008

Item

ANNUAL REPORT 2008

34 Country Performance / Bangladesh

Bangladesh: Total Exports and Imports(In millions of USDs)

Year2003/04 2004/05 2005/06 2006/07 2007/08

Exports (fob, including EPZ)7,521.0 8,573.0 10,412.0 12,053.0 13,945.0

(15.9) (14.0) (21.5) (15.8) (15.7)

Imports (fob, including EPZ)9,840.0 11,870.0 13,301.0 15,511.0 19,486.0

(13.0) (20.6) (12.1) (16.6) (25.6)

Trade Balance -2,319.0 -3,297.0 -2,889.0 -3,458.0 -5,541.0

Note: Figures in the brackets indicate percentage changes over the previous year.

Source: Annual Report 2007/08, Bangladesh Bank

Item

35Country Performance / Bangladesh

ANNUAL REPORT 2008

Bangladesh: Exports to ACU Member Countriesduring January–December, 2008

(In millions of USDs)

Commodity/Country ValueBhutan 0.8

Chemical products 0.1Woven garments 0.1Others 0.6

India 369.1Frozen foods 48.5Agri-products 14.6Chemical products 159.1Leather 7.1Raw jute 16.1Jute goods 50.2Knitwear 1.2Woven garments 8.8Others 63.5

Iran 53.1Jute goods 32.8Others 20.3

Myanmar 7.7Chemical products 5.4Leather 0.0Others 2.3

Nepal 10.8Chemical products 1.5Others 9.3

Pakistan 80.9Agri-products 2.7Tea 11.1Raw jute 54.4Others 12.7

Sri Lanka 21.8Chemical products 13.3Jute goods 1.3Others 7.2Source: Export Promotion Bureau (EPB)

ANNUAL REPORT 2008

36 Country Performance / Bangladesh

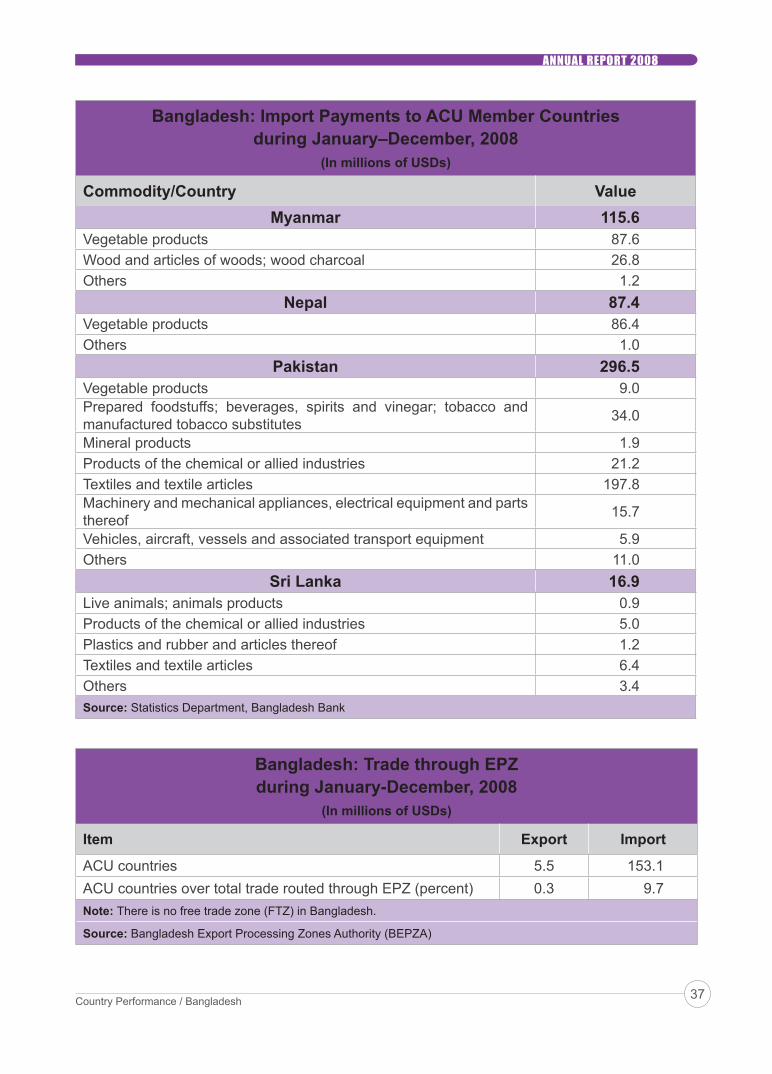

Bangladesh: Import Payments to ACU Member Countriesduring January–December, 2008

(In millions of USDs)

Commodity/Country Value

Bhutan 15.0Vegetable products 8.3Mineral products 5.9Others 0.8

India 3,510.6Live animals; animals products 37.2Edible vegetable certain roots and tubers 147.8Edible fruits and nuts peel of citrus fruits or melons 39.1Coffee, tea, mate and spices 27.3Cereals 669.8Prepared foodstuffs; beverages, spirits and vinegar; tobacco and manufactured tobacco substitutes 393.6

Salt, sulphur, earths and stone, plastering materials 34.9Mineral fuels, mineral oils and products of their distillation, bituminous substances; mineral waxes 76.2

Organic chemicals 98.5Tanning or dyeing extracts 60.5Plastics and rubber and articles thereof 118.7Paper and paperboard and articles thereof 31.2Textile and textile articles thereof 840.5Base Metals and article of base metals 199.6Machinery and mechanical appliances, electrical machinery and equipment and parts thereof 214.8

Vehicles other than railway or tramway, rolling stock, parts and accessories thereof 219.0

Others 301.9

Iran 42.6Vegetable products 17.3Mineral products 17.3Cotton 5.3Others 2.7

37Country Performance / Bangladesh

ANNUAL REPORT 2008

Bangladesh: Import Payments to ACU Member Countriesduring January–December, 2008

(In millions of USDs)

Commodity/Country ValueMyanmar 115.6

Vegetable products 87.6Wood and articles of woods; wood charcoal 26.8Others 1.2