asian development bank rrp:ind 29694 – national hydroelectric power corporation npc – nuclear...

TRANSCRIPT

ASIAN DEVELOPMENT BANK RRP:IND 29694

REPORT AND RECOMMENDATION

OF THE

PRESIDENT

TO THE

BOARD OF DIRECTORS

ON

PROPOSED LOANS

AND

TECHNICAL ASSISTANCE GRANTS

TO

INDIA

FOR THE

GUJARAT POWER SECTOR DEVELOPMENT PROGRAM

November 2000

CURRENCY EQUIVALENTS(as of 14 November 2000)

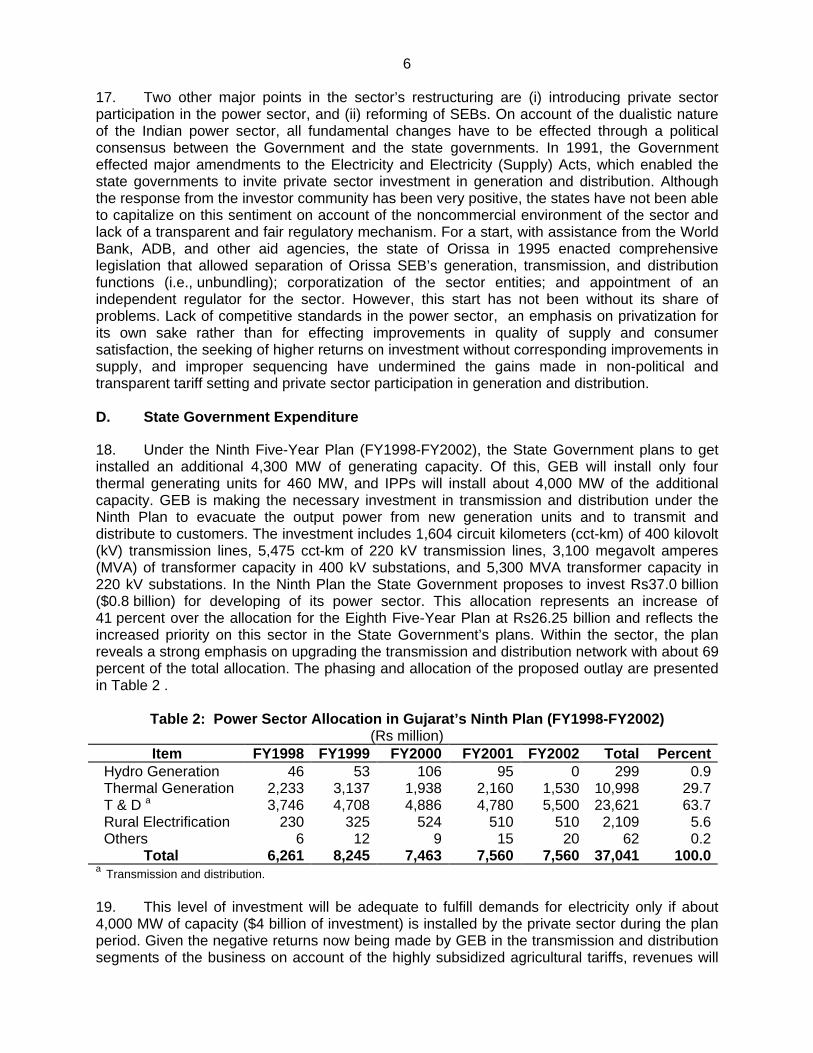

Currency Unit – Rupee/s (Re/Rs)Re1.00 = $0.0215

$1.00 = Rs46.60

ABBREVIATIONS

ADB – Asian Development BankAECO – Ahmedabad Electricity Company LimitedCII – Confederation of Indian IndustryCIDA – Canadian International Development AgencyDFID – Department for International DevelopmentECCF – Electricity Consumers' Coordination ForumEIRR – economic internal rate of returnED – Electricity DepartmentFIRR – financial internal rate of returnGEB – Gujarat Electricity BoardGERC – Gujarat Electricity Regulatory CommissionGETCL – Gujarat Energy Transmission Company LimitedGOG – Government of GujaratGSECL – Gujarat State Electricity Company LimitedHT – high tensionIPP – independent power producerJBIC – Japan Bank for International CooperationKfW – Kreditanstalt für WiederaufbauLT – low tensionNDC – National Development CouncilNHPC – National Hydroelectric Power CorporationNPC – Nuclear Power CorporationNTPC – National Thermal Power CorporationOCR – ordinary capital resourcesPFC – Power Finance CorporationSEB – State Electricity BoardSECO – Surat Electricity Company LimitedSIEE – Summary of initial environmental examinationTA – technical assistanceUSAID – United States Agency for International Development

WEIGHTS AND MEASURES

MW (megawatt) – 1,000 kWkVA (kilovolt-ampere) – 1,000 VAkV (kilovolt) – 1,000 voltskW (kilowatt) – 1,000 WMVA (megavolt-ampere) – 1,000,000 VAW (watt) – unit of active powerha (hectare) – unit of areakWh (kilowatt-hour) – unit of energykm (kilometer) – unit of lengthcct-km (circuit kilometer) – unit of transmission line lengthVA (volt-ampere) – unit of power/capacity

NOTE(S)

(i) The fiscal year (FY) of the Government of India, the Government of Gujarat andthe Gujarat Electricity Board ends on 31 March. FY before a calendar yeardenotes the year in which the fiscal year ends, e.g., FY2002 begins on 1 April2001 and ends on 31 March 2002.

(ii) In this report, "$" refers to US dollars.

CONTENTS

Page

Loan and Project Summary i

I. THE PROPOSAL 1

II. INTRODUCTION 1

III. THE SECTOR 1

A. Macroeconomic Context 1

B. Sector Description and Recent Performance 2

C. Constraint and Issues 4

D. State Government Expenditure 6

E. The State Government’s Objectives and Strategy 7

F. External Assistance to the Sector 7

G. ADB’s Country and Sector Strategy 8

IV. THE SECTOR DEVELOPMENT PROGRAM 10

A. Rationale 10

B. Objectives and Scope 10

C. Policy Framework and Actions 11

D. The Investment Project 14

E. Environmental and Social Measures 15

V. THE LOANS

A. The Program Loan 16

B. The Project Loan 19

C. The Executing Agency 20

VI. THE TECHNICAL ASSISTANCE 24

VII. BENEFITS AND RISKS 28

A. Expected Impacts 28

B. Risks and Safeguards 31

VIII. ASSURANCES 32

A. Prior Actions by the State Government and GEB 32

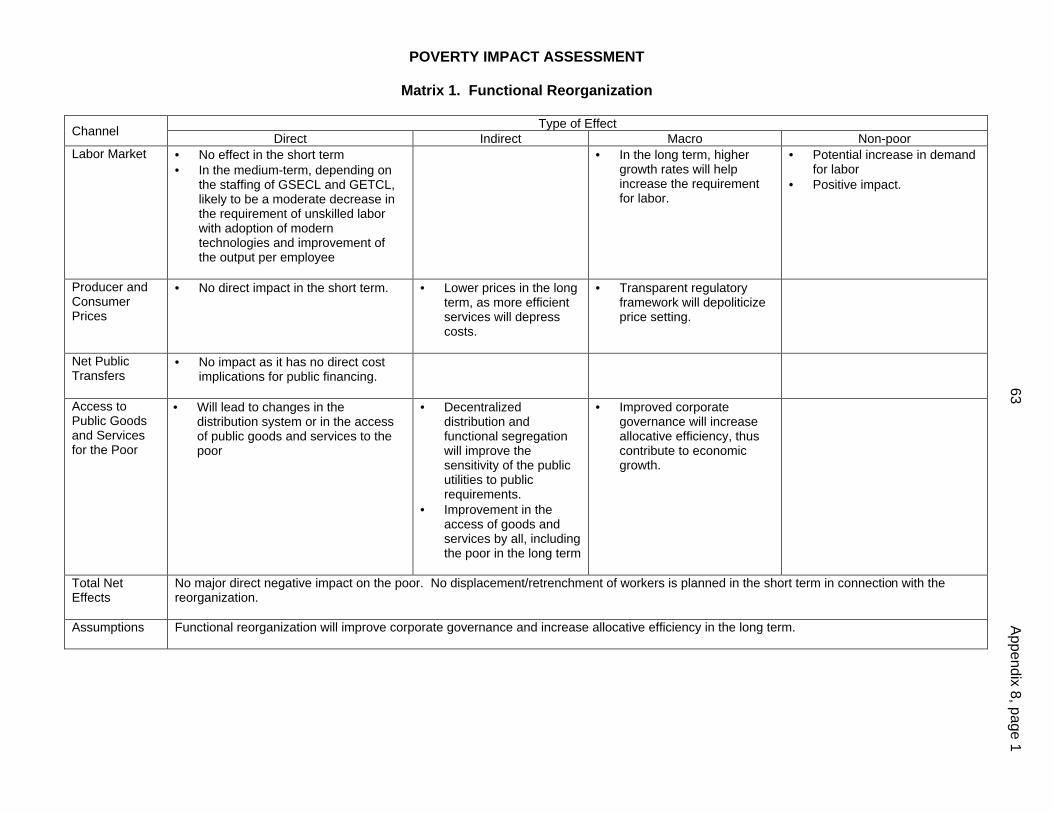

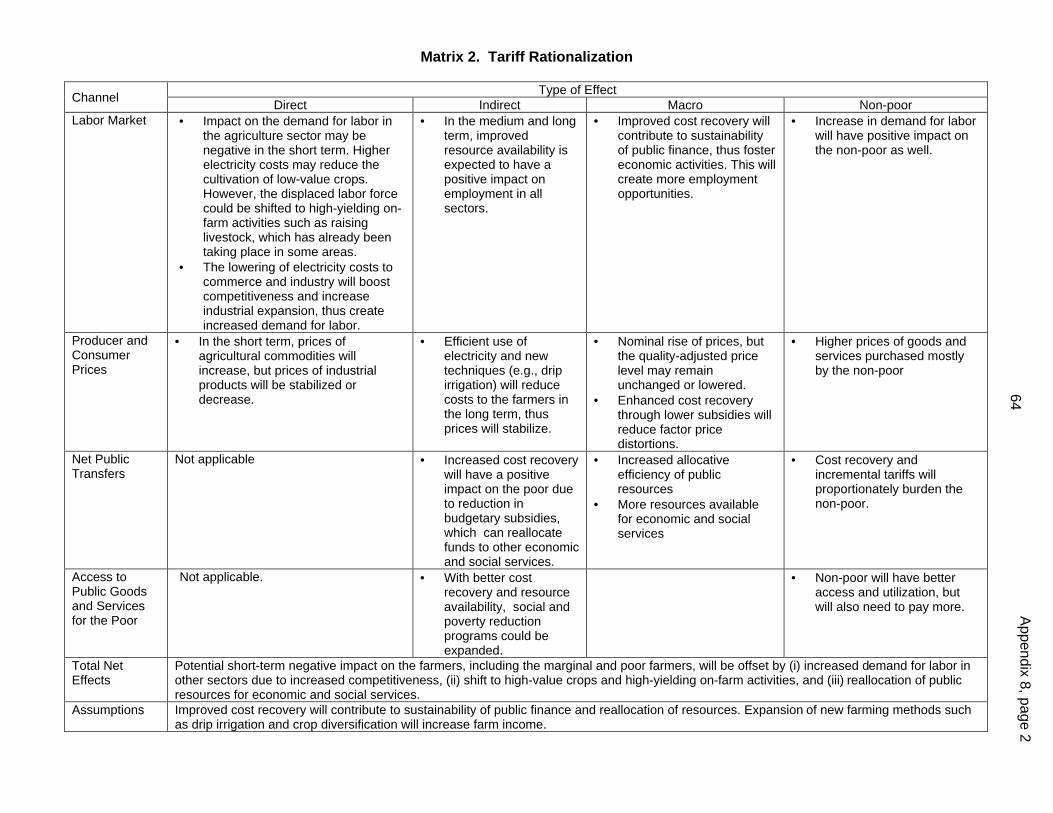

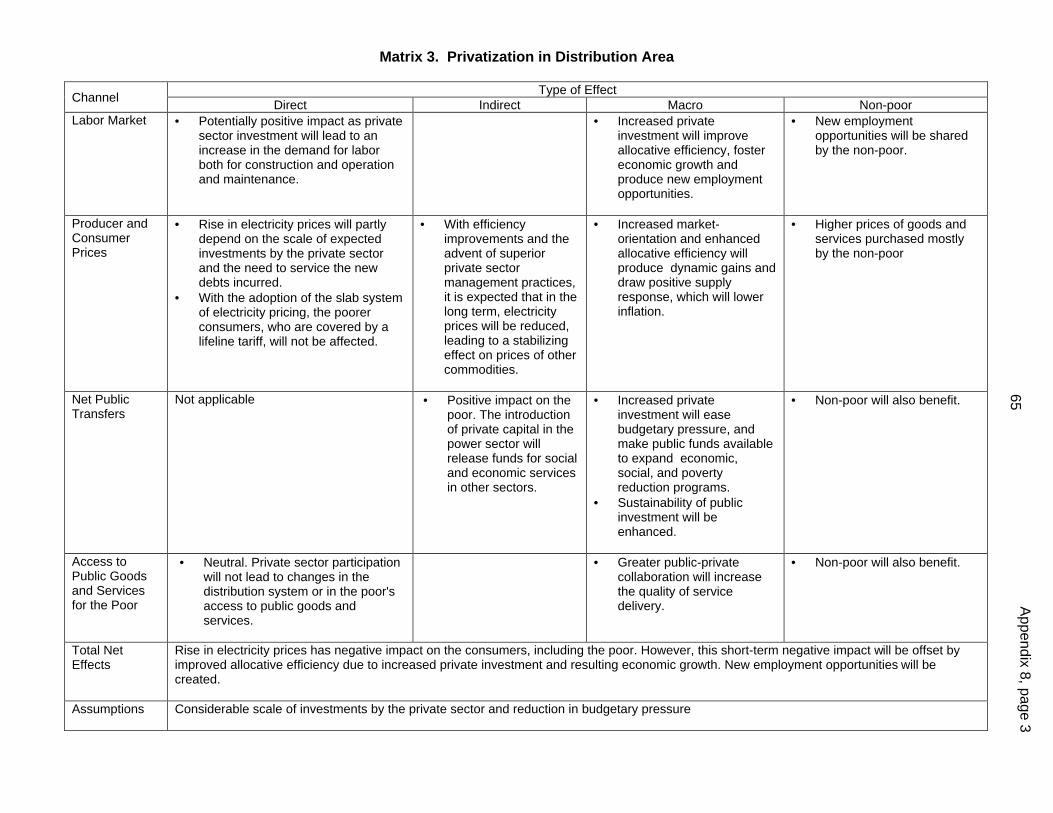

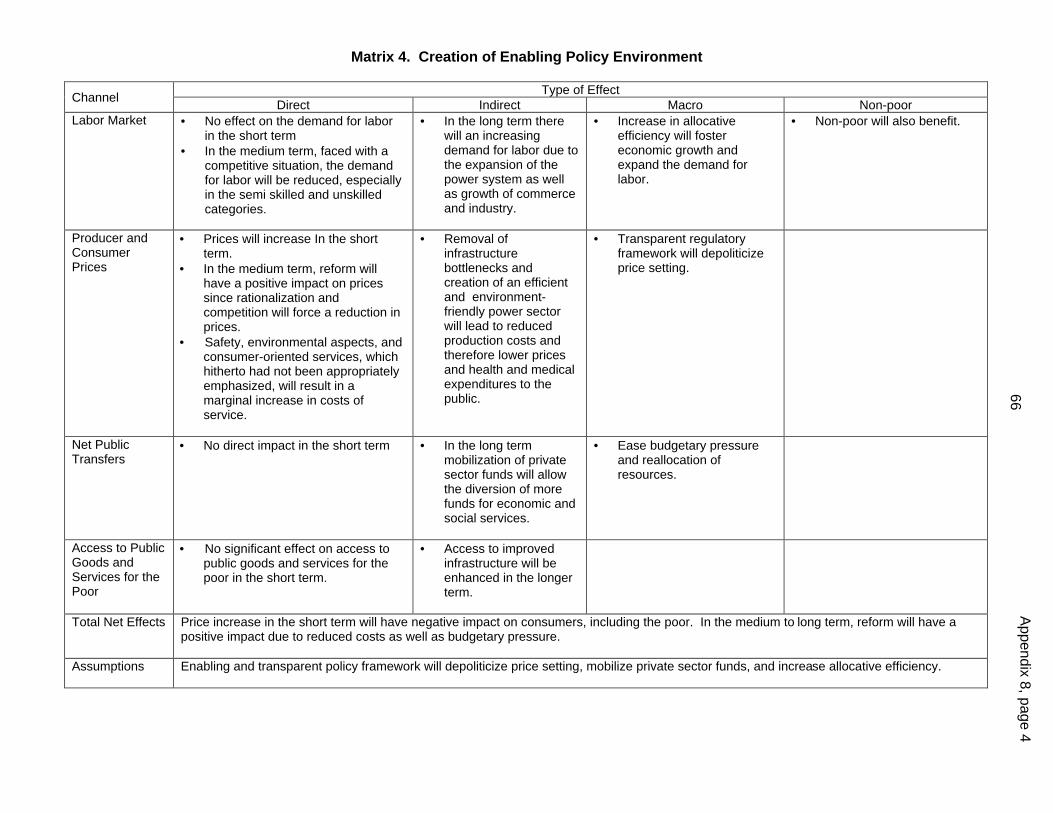

B. Covenants 33

IX. RECOMMENDATION 35

APPENDIXES 36

LOAN AND PROGRAM SUMMARY

Borrower India

The Proposal Two loans totaling $350 million from the Asian Development Bank's(ADB's) ordinary capital resources (OCR) to support the GujaratPower Sector Development Program.

Rationale The Sector Development Program facilitates restructuring of thepower sector in Gujarat, reduces the operating costs throughimproved operating efficiencies and governance, raises additionalrevenues and, over the longer term, eliminates the need fortransfers from the state government budget. It facilitates expansionof power supplies using private generating capacity, andconservation of water and electricity. It will support economicgrowth in the state, particularly in the industry sector. It will alsoallow a shift in state government expenditures from the powersector to its other responsibilities, for example, in the education andhealth sectors. This combination of higher economic growth andshift in public expenditure will contribute to reducing poverty.

Given the present constraints on the power sector in Gujarat-politicized tariff setting and lack of a transparent competitivebusiness environment-, there is a need to change fundamentalpolicies and business practices to improve sector efficiencies.Investments on their own, without changes in policy, will not yieldresults. Therefore, a mixed-modality sector development program,which seeks to correct policies as well as support projectinvestments, is considered the best instrument for supporting aninitiative for restructuring the power sector.

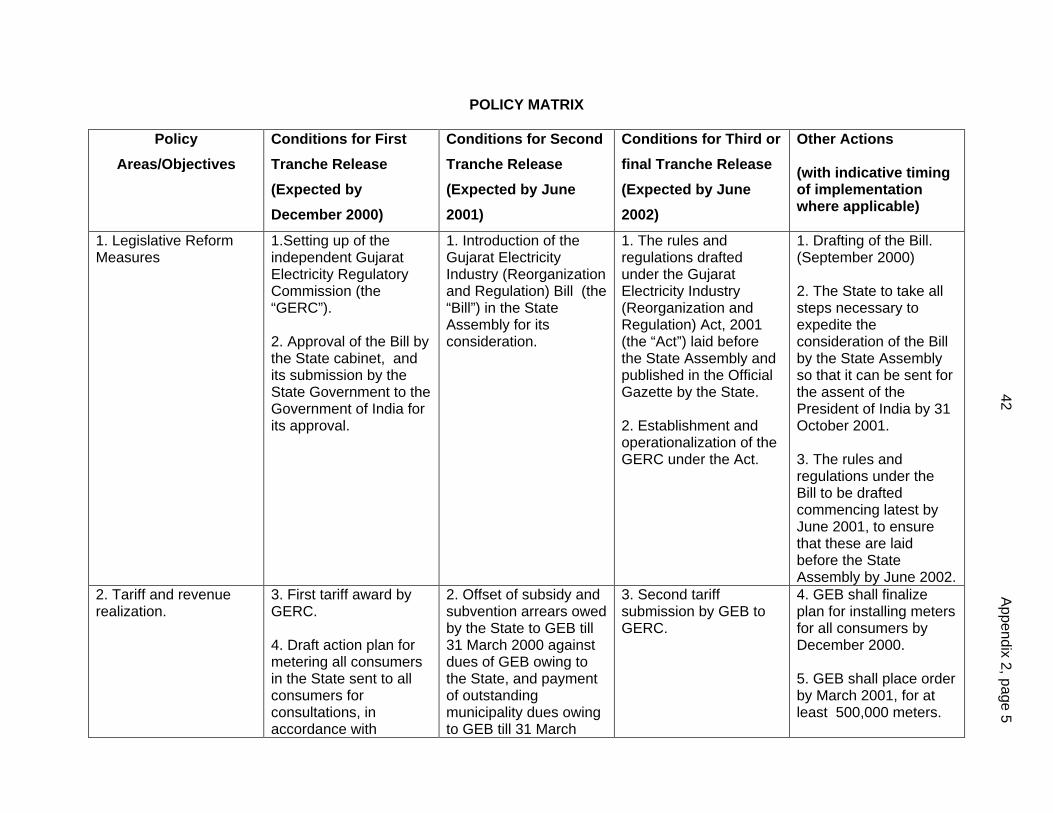

Classification Economic growth

The Sector Development Program

Objectives and Scope The immediate objectives of the Sector Development Program areto (i) establish independent tariff setting and regulation; (ii) rationalizethe imposition of tariffs, duties, and imposts in the sector to maintainequity among consumer categories; (iii) change managementpractices and enhance efficiency in the power sector by introducingcompetition and commercialization; and (iv) improve conservation ofwater and electricity on a pilot basis through improved irrigationsystems.

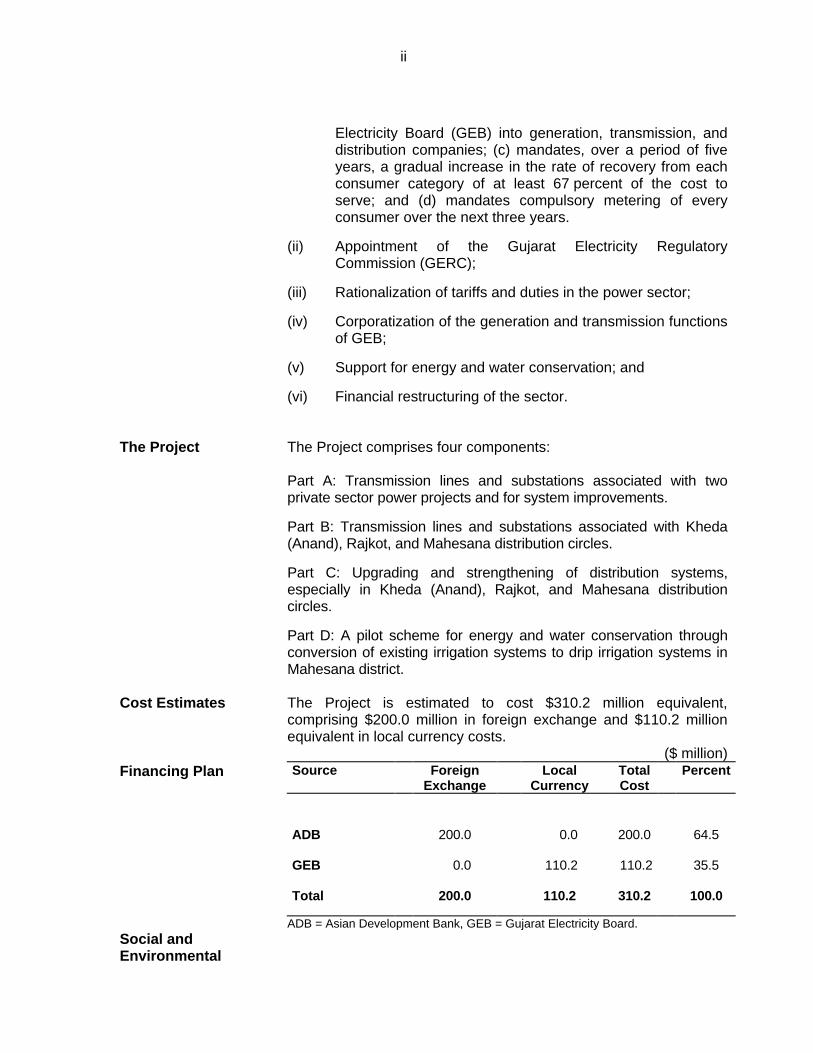

Policy Frameworkand Actions (i) Enactment of a comprehensive Gujarat Electricity Industry

(Reorganization and Regulation) Bill 2000 (the Bill) that(a) enables the creation of a statutory, independentregulatory authority for licensing, tariff setting, and disputeresolution; (b) enables functional segregation of the Gujarat

ii

Electricity Board (GEB) into generation, transmission, anddistribution companies; (c) mandates, over a period of fiveyears, a gradual increase in the rate of recovery from eachconsumer category of at least 67 percent of the cost toserve; and (d) mandates compulsory metering of everyconsumer over the next three years.

(ii) Appointment of the Gujarat Electricity RegulatoryCommission (GERC);

(iii) Rationalization of tariffs and duties in the power sector;

(iv) Corporatization of the generation and transmission functionsof GEB;

(v) Support for energy and water conservation; and

(vi) Financial restructuring of the sector.

The Project The Project comprises four components:

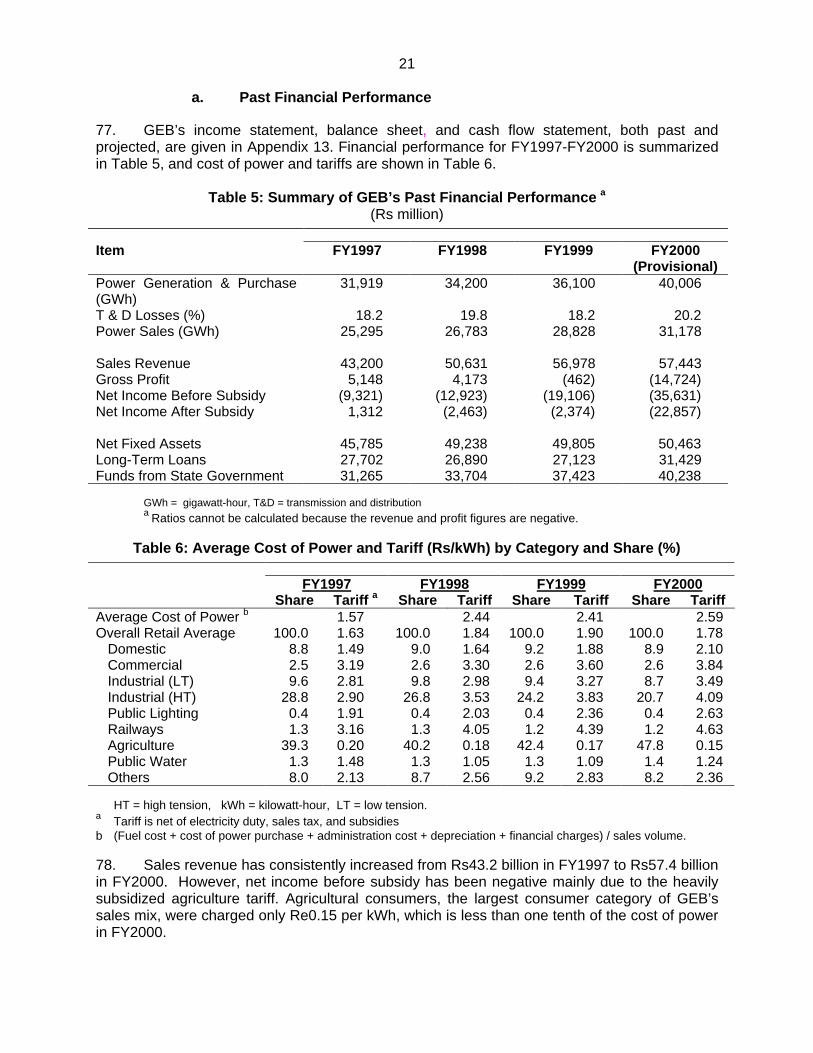

Part A: Transmission lines and substations associated with twoprivate sector power projects and for system improvements.

Part B: Transmission lines and substations associated with Kheda(Anand), Rajkot, and Mahesana distribution circles.

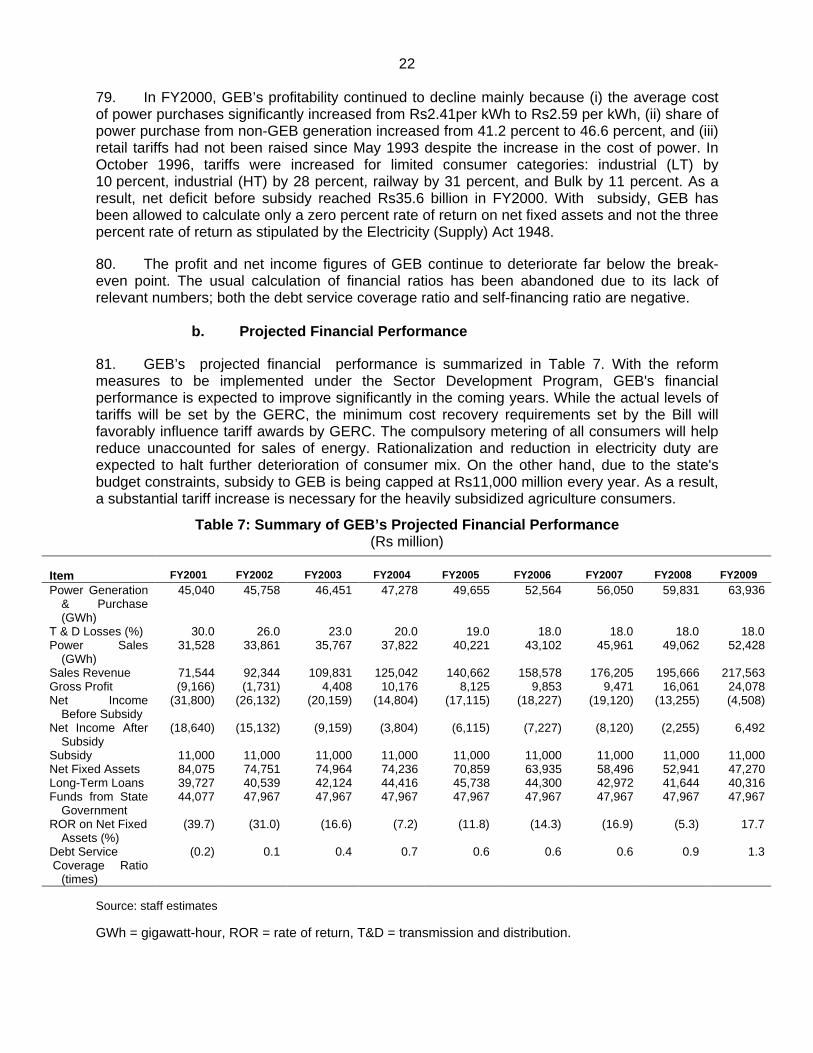

Part C: Upgrading and strengthening of distribution systems,especially in Kheda (Anand), Rajkot, and Mahesana distributioncircles.

Part D: A pilot scheme for energy and water conservation throughconversion of existing irrigation systems to drip irrigation systems inMahesana district.

Cost Estimates The Project is estimated to cost $310.2 million equivalent,comprising $200.0 million in foreign exchange and $110.2 millionequivalent in local currency costs.

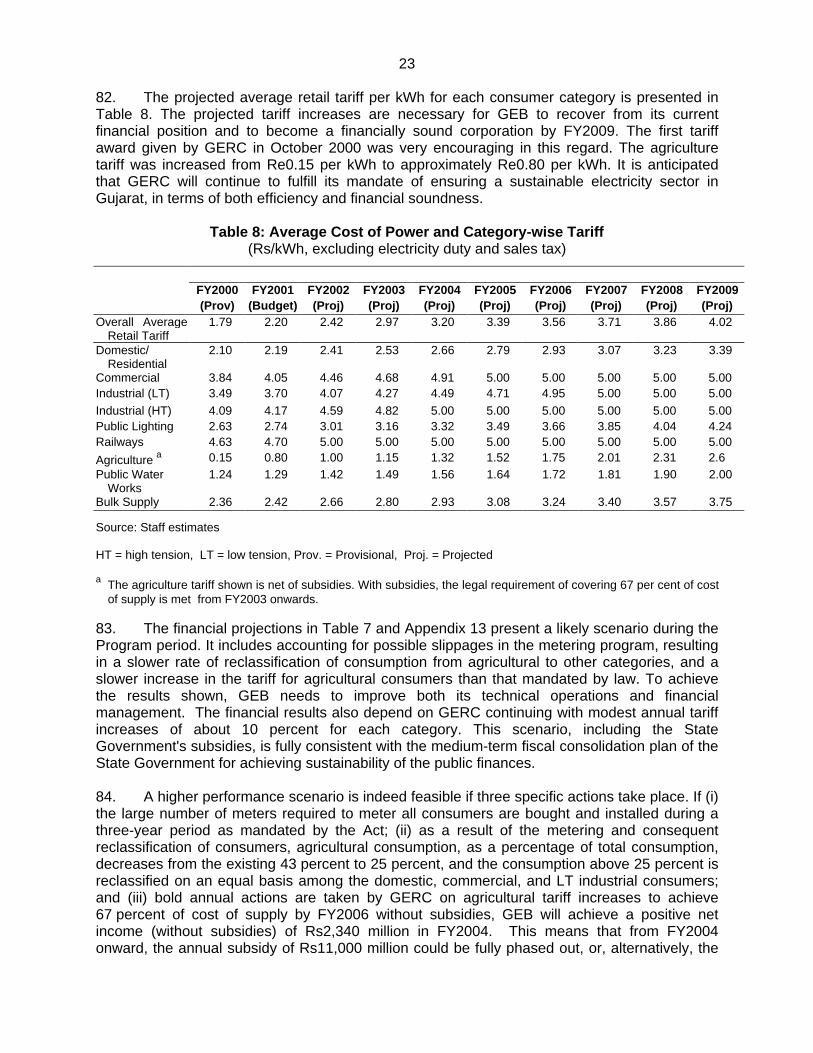

($ million)Financing Plan Source Foreign

ExchangeLocal

CurrencyTotalCost

Percent

ADB 200.0 0.0 200.0 64.5

GEB 0.0 110.2 110.2 35.5

Total 200.0 110.2 310.2 100.0

ADB = Asian Development Bank, GEB = Gujarat Electricity Board.Social andEnvironmental

iii

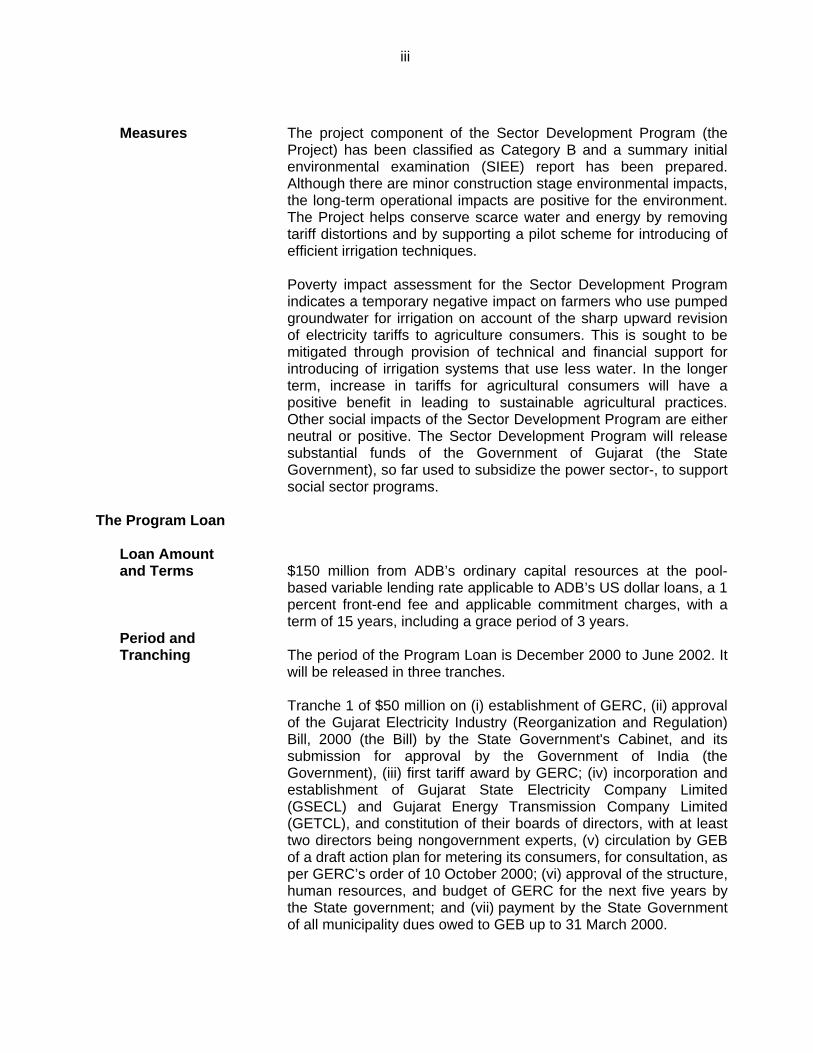

Measures The project component of the Sector Development Program (theProject) has been classified as Category B and a summary initialenvironmental examination (SIEE) report has been prepared.Although there are minor construction stage environmental impacts,the long-term operational impacts are positive for the environment.The Project helps conserve scarce water and energy by removingtariff distortions and by supporting a pilot scheme for introducing ofefficient irrigation techniques.

Poverty impact assessment for the Sector Development Programindicates a temporary negative impact on farmers who use pumpedgroundwater for irrigation on account of the sharp upward revisionof electricity tariffs to agriculture consumers. This is sought to bemitigated through provision of technical and financial support forintroducing of irrigation systems that use less water. In the longerterm, increase in tariffs for agricultural consumers will have apositive benefit in leading to sustainable agricultural practices.Other social impacts of the Sector Development Program are eitherneutral or positive. The Sector Development Program will releasesubstantial funds of the Government of Gujarat (the StateGovernment), so far used to subsidize the power sector-, to supportsocial sector programs.

The Program Loan

Loan Amountand Terms $150 million from ADB’s ordinary capital resources at the pool-

based variable lending rate applicable to ADB’s US dollar loans, a 1percent front-end fee and applicable commitment charges, with aterm of 15 years, including a grace period of 3 years.

Period andTranching The period of the Program Loan is December 2000 to June 2002. It

will be released in three tranches.

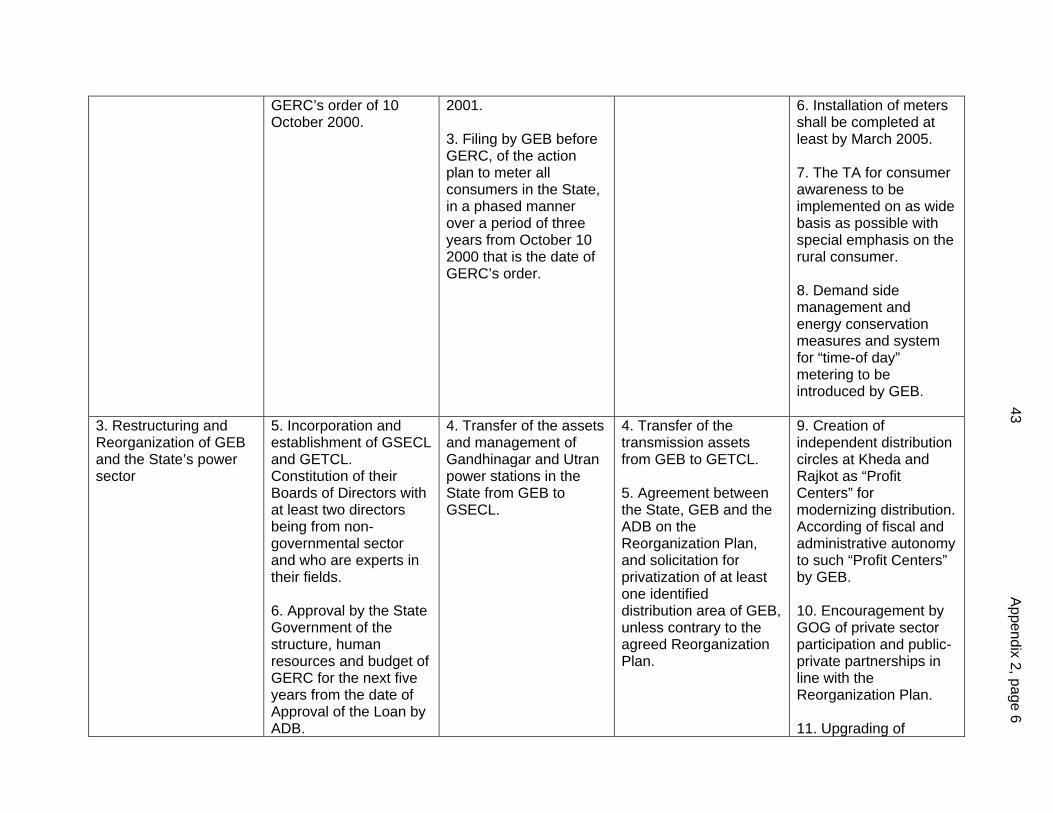

Tranche 1 of $50 million on (i) establishment of GERC, (ii) approvalof the Gujarat Electricity Industry (Reorganization and Regulation)Bill, 2000 (the Bill) by the State Government's Cabinet, and itssubmission for approval by the Government of India (theGovernment), (iii) first tariff award by GERC; (iv) incorporation andestablishment of Gujarat State Electricity Company Limited(GSECL) and Gujarat Energy Transmission Company Limited(GETCL), and constitution of their boards of directors, with at leasttwo directors being nongovernment experts, (v) circulation by GEBof a draft action plan for metering its consumers, for consultation, asper GERC’s order of 10 October 2000; (vi) approval of the structure,human resources, and budget of GERC for the next five years bythe State government; and (vii) payment by the State Governmentof all municipality dues owed to GEB up to 31 March 2000.

iv

Tranche 2 of $50 million on (i) transfer of Gandhinagar and Utranpower stations from GEB to GSECL; (ii) offset of subsidy andsubvention arrears owed by the State Government's to GEB until 31March 2000, and payment of outstanding municipality dues by theState Government's to GEB till 31 March 2001; (iii) introduction ofthe Bill in the Gujarat State Assembly for its consideration; and (iv)rationalization and reduction of electricity duty in the StateGovernment's budget for FY2002, in an amount not less thanRs1,500 million; and (v) Filing by GEB with GERC, of an action planto meter all consumers in the state within a period of three yearsfrom 10 October 2000.

Tranche 3 of $50 million on (i) transfer of transmission assets fromGEB to GETCL; (ii) agreement between the State Government,GEB, and ADB on the Reorganization Plan for GEB developedunder ADB’s proposed technical assistance (TA); (iii) readiness tosolicit offers to privatize at least one identified distribution area ofGEB, unless contrary to the agreed Reorganization Plan; (iv) therules and regulations under the Bill as enacted (the Act) laid beforethe Gujarat State Assembly and published in the Official Gazette;(v) second tariff submission by GEB to GERC; and(vi) establishment and operationalization of GERC under the Act.

Executing Agencies The Executing Agencies will be the Finance Department and theEnergy and Petrochemicals Department of the State Government.

Procurement The proceeds of the Program Loan will finance the foreignexchange costs (excluding local taxes and duties) of eligible items,produced in and procured from ADB’s member countries.

Counterpart Funds Counterpart funds to be generated by the Program Loan will betransferred from the Government to the State Government underthe normal arrangements for the transfer of external assistance andwill be treated as an “additionality” to the Government transfersallocated annually to the State Government. The State Governmentwill use Counterpart funds in accordance with arrangementssatisfactory to ADB, to support the financial restructuring of GEBand adjustment costs associated with the Sector DevelopmentProgram, including (i) reduction of GEB's accounts payable of GEBto power producers, suppliers of fuel and transport; (ii) retirement ofexpensive commercial debt, (iii) payment of outstanding municipaldues; (iv) rationalization of electricity duty; and (v) reduction ofindependent power producer tariffs through buyout of debt.

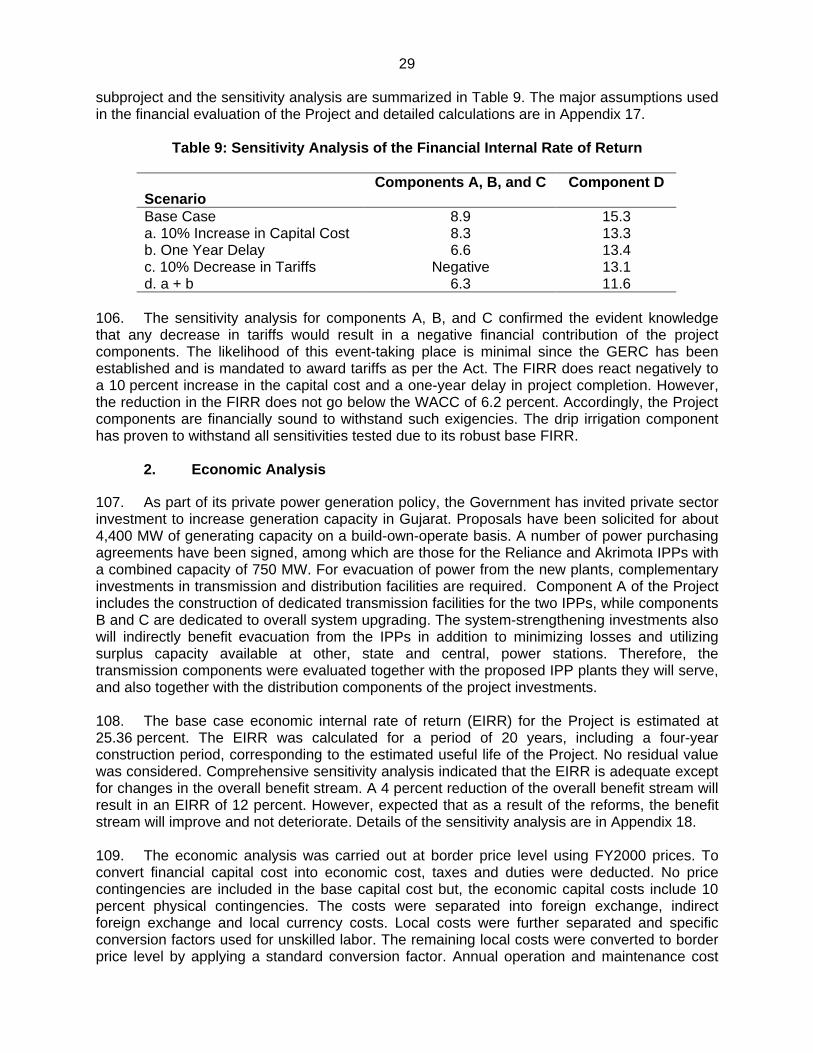

The Project Loan

Loan Amountand Terms $200 million from ADB’s ordinary capital resources at the pool-

based variable lending rate applicable to ADB’s US dollar loans, a 1percent front-end fee and applicable commitment charges, with aterm of 20 years, including a grace period of 5 years. The borrower

v

will be the Government. The loan proceeds will be transferred bythe Government to the State Government under its normalarrangements for transfer of such external assistance. Theproceeds of the loan will be treated as “additional” to theGovernment’s normal transfers to the State Government. The StateGovernment will relend the loan proceeds to GEB, under asubsidiary loan agreement, at an interest rate of 12 percent with aterm of 20 years, including a grace period of 5 years. TheGovernment will bear the foreign exchange risk.

Implementation Arrangements and Executing Agency The Project will be executed by GEB, and its successor entities with

the prior approval of ADB. GEB is a statutory organization createdunder the Indian Electricity (Supply) Act, 1948. It is managed by aboard appointed by the State Government. Successor entities will becompanies registered under the Companies’ Act of 1956.

Procurement and Consulting Services Goods and services financed by GEB will be procured in accordance

with ADB’s Guidelines for Procurement. To accelerate projectimplementation, ADB has allowed advance procurement action. Forimplementing of Part D of the Project, GEB will, under its ownfinancing, appoint a suitable consultant for design, procurement, andproject supervision. Retroactive financing has not been allowed.

Time Frame The Project will be implemented from January 2001 to December2004. Disbursement under the Project Loan will continue until June2005.

Technical Assistance Three TAs are included in the Sector Development Program. Theseare (i) Preparation of a Reorganization Plan for GEB, for $600,000;(ii) Consumer Awareness and Participation in Power SectorReforms, for $50,000; and (iii) Support to GERC, for $450,000.A fourth TA for supporting GEB's Kheda (Anand) and Rajkotdistribution circles has been proposed for funding by bilateralcofinanciers.

Risks and Safeguards The major risks of the Sector Development Program are (i) failure toestablish the regulatory authority, (ii) lack of support of the StateGovernment for politically unattractive decisions of the regulatoryauthority such as raising of electricity tariffs for agricultureconsumers, and (iii) operational inadequacies. These have beenmitigated through (i) approvals by the State Government for theBill establishing the regulatory authority; (ii) GERC’s first tariffaward; and (iii) changing and strengthening organizational andmanagement structures and practices, and effective follow-upmechanisms.

I. THE PROPOSAL

1. I submit for your approval the following Report and Recommendation on proposedassistance to India for the Gujarat Power Sector Development Program, that includes(i) a program loan, and (ii) a project loan. The Report also describes proposed technicalassistance for (i) development of a reorganization plan for the Gujarat Electricity Board (GEB)(ii) consumer awareness and participation in Gujarat's power sector reforms, and (iii) support tothe Gujarat Electricity Regulatory Commission (GERC). If the proposed loans are approved bythe Board, I, acting under the authority delegated to me by the Board, shall approve thetechnical assistance.

II. INTRODUCTION

2. In 1996, the Asian Development Bank (ADB) revised its operational strategy for Indiaand decided to direct a portion of its assistance to the states. This change reflected the factsthat (i) a geographical focus, together with the ongoing selective sectoral focus, would enableADB to maximize its developmental impact on the states concerned, and through thedemonstrational impact of its operations, on other states; (ii) state-level economic reforms,which have been lagging behind initiatives taken by the Government of India, need support andincentives; and (iii) the states have considerable autonomy and have major legislative,administrative, and fiscal responsibilities in many economic and social sectors. Key elements ofthe strategy include (i) reducing the states’ fiscal deficits, (ii) reforming and restructuring publicsector enterprises to improve their operating efficiencies, and (iii) supporting reforms in keyinfrastructure sectors with a view to increasing private investment. Gujarat was the first statechosen for this type of holistic support and the first loan was made by ADB in December 1996.1

The Sector Development Program is an integral part of this assistance and is included in theIndia Country Assistance Plan for 2000. Preparatory to the Sector Development Program, ADBapproved five supporting technical assistance (TA) grants amounting to $1.98 million, forstudies.2 Preappraisal was conducted during 3-24 September 1997. Thereafter, there was abreak in processing which was resumed in May 2000. Appraisal was conducted in four stagesduring July through October 2000. 3

III. THE SECTOR

A. Macroeconomic Context

3. Gujarat is one of the most industrialized states in India and has the fourth highest percapita income in the country. The state's per capita income in real terms increased fromRs11,936 ($257) in FY1995 to RS13,709 ($295) in FY1999, compared with the FY1999national-level per capita real income of Rs11,878 ($255).4 Gujarat also has the third highest per

1 Loan 1506-IND: Gujarat Public Sector Resource Management Program, for $250 million, approved on

18 December 1996.2 The studies include (i) preparation of a power system master plan, (ii) preparation of a framework for electricity

tariffs, (iii) review of electricity legislation and regulations, (iv) financial support to Gujarat Electricity Board (GEB)for formation of two independent distribution profit centers, and (v) solicitation for private sector implementation ofthe Chhara Project.

3 The Missions comprised S. Chander, Senior Project Engineer, IWEN (mission leader); K. Gerhaeusser, SeniorPrograms Officer, PW2; B. Karunaratne, Senior Project Engineer, IWEN; E. Ouano, Senior Environment Specialist,ENVD; P. Pattison, Senior Project Implementation Officer, INRM; R. Stroem, Senior Financial Specialist, IWEN;Y. Uehara, Senior Social Development Specialist, PWOD; D. Graczyk, Project Economist, IWEN; M. Hamano,Project Engineer, IWEN; and V.S. Rekha, Counsel, OGC.

4 Data in real terms are in FY1994 constant prices.

2

capita consumption of electricity in the country.5 It has experienced rapid growth in thedevelopment of its economy over the last five years, since India started liberalizing economiccontrols in 1991. However, this growth is now constrained by infrastructural bottlenecks, theprimary one being lack of electricity. GEB, which is the state’s primary executing agency in thesector, is unable to raise resources for investments due to the recurring financial deficits- ithighly suffers on account of the state’s policy of supplying electricity to agricultural consumers atextremely subsidized levels. The Government of Gujarat (the State Government) has initiatedan ambitious policy of inviting private sector participation in the power sector, but this policy isencountering difficulties because the sector revenues at current levels are insufficient to servicethe large inflow of capital that is required. The State Government is making strong efforts tomaintain fiscal discipline in its overall finances, but is constrained by its payables to GEB onelectricity subsidies to agricultural consumers which have escalated to about 20 percent of itstotal revenues. This adversely affects resource availability for other important areas ofinfrastructure as well as for social services thus causing the state to lag behind insocioeconomic indicators compared with other economically advanced states in India. Thus, acomprehensive restructuring of the power sector is essential to the state’s overall economic andsocial development.

B. Sector Description and Recent Performance

1. Organization

4. India consists of 28 states and 7 union territories with a total population of over 1 billion.Its power sector is the third largest in Asia, after that of the People’s Republic of China andJapan. Installed generation capacity grew from about 2,000 megawatts (MW) in 1950 to about98,000 MW as of 31 March 2000, with an additional 12,000 MW of captive generation capacity.More than 77 million electricity consumers and about 86 percent of villages have beenelectrified. However, the annual per capita consumption was only about 360 kilowatt-hours(kWh) in FY2000, which is lower than the consumption levels of many other developingcountries.

5. The organization of the power sector is determined by India’s federal structure. TheGovernment’s Ministry of Power provides overall guidance to the sector, mainly through theCentral Electricity Authority, and owns the central power sector utilities such as the NationalThermal Power Corporation (NTPC), the National Hydroelectric Power Corporation (NHPC), theNuclear Power Corporation (NPC), and the Powergrid Corporation of India (Powergrid), andfinancing institutions such as the Power Finance Corporation (PFC) and the Rural ElectrificationCorporation. State governments control the rest of the sector through 20 state electricity boards(SEBs) and 12 electricity departments (EDs). These SEBs and EDs provide distribution facilitiesand set retail tariffs. Power generation and transmission are split between the central powersector agencies and SEBs. The central agencies own and operate 32 percent of the country’stotal generation, while SEBs and EDs have 64 percent of the total. In addition, five privateutilities in urban agglomerations have a share of 4 percent in power generation.

6. As a result of India’s federal structure, all major issues affecting the power sector requireconcurrent action by the Government and state governments. Although the structure gives theGovernment a say in the affairs of the power sectors of the states, this shared responsibilitylimits its ability to influence the power sector policies of state governments, especially withrespect to retail tariffs.

5 Per capita consumption of 650 kilowatt-hours (kWh) per annum in FY2000 compared with the national average of

360 kWh per annum.

3

2. State Electricity Boards

7. Prior to the reorganization of the power sectors in the states of Orissa (1996), Haryana(1998), Andhra Pradesh (1999), Karnataka (1999), and Uttar Pradesh (2000), the power sectorin every major state was organized through its SEB. Even today, other than in these states,SEBs still control the operations of the sector. The Electricity Act of 1910 and the Electricity(Supply) Act of 1948 with their several amendments provide the legal basis for the sector’sfunctioning and utilities’ operation. These acts allow considerable managerial and financialautonomy to the SEBs, but this autonomy is often nominal as most state governments useSEBs to pursue noncommercial objectives, particularly to provide low-priced or free electricity tothe agriculture sector. Initially, this cross-subsidization was done to provide low-cost inputs foragriculture to stimulate food production and was very successful. However, that stage is nowwell past but the practice has continued largely to attract political support. State governmentsalso tend to interfere with SEBs' day-to-day operations, thus complicating the task of SEBmanagement. These interventions have led to the SEBs’ deteriorating financial health, whichhas become the central problem of India’s power sector.

8. Several years of negative internal cash generation has impoverished SEBs, impeded theconstruction of new power facilities, and restricted the funds available for maintenance andrehabilitation of existing assets, making it impossible to close the demand-supply gap. Chronicpower shortages and poor-quality power supply continue to plague the economy in almost allparts of the country. If not remedied, the unavailability of sufficient power will be the single mostimportant constraint to economic development in the coming years and will thwart efforts toattract domestic and foreign investment.

9. A reform of the power sector at the state level is urgently needed to reduce the need forsubsidies and public spending on the sector. As a result of the state governments' interferencein SEB operation and subsidies to agricultural customers, sector losses in FY1999 reachedRs63.3 billion ($1.4 billion), but were reduced to Rs45.0 billion ($1.0 billion) by subsidies fromstate governments. Power sector reform will significantly reduce claims on the country’s fiscalresources and allow additional spending on other priority sectors such as health and education,which are essential for poverty reduction.

3. Central Power Utilities

10. Until 1972, SEBs were almost solely responsible for power generation and transmissionwithin their states, but were unable to meet the rapidly increasing demand for electricity. Toimprove the efficiency of generation, three central sector agencies - NTPC, NHPC and NPC-,were established in 1975 to generate bulk power for sale to SEBs. In 1989, Powergrid wasestablished as a transmission and dispatch company by amalgamating the transmission anddispatch assets of all central power sector agencies. In addition to these wholly ownedcompanies, the Government also has shares in special-purpose generating companies such asthe Bhakra-Beas Management Board, the Damodar Valley Corporation, the Tehri PowerCorporation, the Nathpa-Jhakhri Power Corporation, the North-East Electric Power Corporation,and the Neyveli Lignite Corporation.

11. The central agencies - NTPC, NHPC, and Powergrid - are seriously affected by the poorfinancial health of most SEBs, as was evidenced several times in the past when excessiveaccounts receivable from the SEBs seriously impaired the central agencies’ financial liquidity.To resolve this problem, NTPC has, in addition to restricting supply and obtaining Government

4

appropriation to settle debts of SEBs, resorted to taking over the generation facilities of SEBs insettlement of accounts receivable.6

4. The Gujarat Power Sector

12. The power sector in Gujarat comprises GEB, the Ahmedabad Electricity Company(AECO) and the Surat Electricity Company (SECO), two private sector generationand distribution licensees in the cities of Ahmedabad and Surat, respectively. Recently, about3,000 MW capacity of captive generation and of independent power producers (IPPs) has beensanctioned. The state has experienced an increase in demand for electricity of about 9 percentper annum over the last five years. This rate of growth is expected to continue inthe foreseeable future since the state has been attracting a large share of the overseas anddomestic investments made in India following the liberalization of the Indian economy in 1991.The key indicators for Gujarat’s power sector are given in Appendix 1. In FY2000 the shares ofthe various utilities in power sector operations were as given in Table 1 below.

Table 1: Comparison of Electric Power Utilities in Gujarat in FY2000

Utility Generation Share Distribution ShareMW GWh % GWh %

GEB a 4,534 23,177 53.54 29,135 85.5AECO 510 3,393 7.84 3,173 9.3SECO 0 0 0.0 1,769 5.2Central Utilities 1,532 10,058 23.24 0 0IPPs 1,785 6,658 15.38 0 0

Total 8,361 43,286 100.0 34,077 100.0

AECO = Ahmedabad Electric Company, GWh = gigawatt-hours, GEB = Gujarat Electricity Board,IPP = independent power producer, SECO = Surat Electricity Company, MW = megawatts,

a GEB owns and operates the transmission network in the state.

C. Constraints and Issues

13. During FY1999, load shedding was experienced ranging between 50 MW and 1,450 MWon 362 days of the year. Gujarat is facing an anticipated shortfall of about 7,000 MW ofgenerating capacity over the next decade and has invited private sector proposals fordeveloping over 4,000 MW of capacity over the next five years. However, the actualization ofthis investment will be constrained by the inflow of revenues into the sector and the perceptionby domestic and international investors of an efficient and impartial regulatory system. TheState Government, therefore, wishes to amend the existing legislation and regulations with aview to enacting a new law that would address the concerns of the investors as well as createa business environment conducive to improving the sector’s (i) operational efficiencies,(ii) financial viability, and (iii) service to its consumers. It proposes to do this through (i) greatercompetition at all levels of the sector wherever practicable; (ii) corporatization andcommercialization of existing sector entities; (iii) private sector participation in the generationand distribution segments; (iv) viable tariffs that enable costs to be recovered and reasonableprofits to be made; (v) an independent regulator; and (vi) transparent, reasonable, direct, and

6 As part of the agreement to make NTPC the Executing Agency for Loan 907-IND: Unchahar Thermal Power

Project, for $160.0 million, approved on 29 September 1988,ADB, the Government of India, the Government ofUttar Pradesh, and NTPC agreed to transfer the title to the 420-MW stage I to NTPC. NTPC has since taken overthe Talcher Thermal Power Station from Orissa SEB, and the Tanda Thermal Power Station from Uttar PradeshSEB.

5

quantified subsidies to vulnerable sections of consumers. In 1995, GOG revised its power policyto incorporate these principles.

14. Subsidized electricity tariffs for agricultural consumers represent a key issue that has tobe addressed in reforming sector. In line with the practice in other states in India with largeagricultural production, the State Government has been providing the agriculture sector withsubsidized electricity. The rationale was that prices of agricultural outputs are controlled and thatinexpensive inputs are required to compensate for these price controls and provide an incentive toincrease agricultural production, so that India can be self-sufficient in food. This argument hasdistorted the pricing of electricity in Gujarat to such an extent that the electricity tariffs for theindustrial and commercial sectors are higher than the long-run marginal cost of power supply,while the tariff for about 0.5 million agricultural consumers, prior to October 2000, wasRs350 ($7.50) per horsepower of load connected per year,7 which in FY2000 led to a revenuerealization of only Re0.15 per kWh ($0.003 per kWh).

15. Based on the cost of new generation, each incremental kWh of agricultural consumptionrequires a subsidy of at least Rs2.00 per kWh ($0.04 per kWh) for generation plus an additionalRe1.00 per kWh ($0.02 per kWh) for transmission and distribution. This situation has resulted in(i) GEB not having resources to finance its expansion to meet unserved demand; (ii) agriculturalconsumers not receiving a signal that electricity is a scarce resource and, accordingly, notconserving it; (iii) other consumer groups, particularly industrial consumers, paying high tariffs thatimpair their competitiveness and consequently establishing their own generation facilities, erodingGEB's consumer mix; and (iv) GEB being unable, without subsidies from the State Government,to earn a return on its investments as prescribed by law. The provision of heavily subsidizedelectricity to agriculture consumers has boosted its share of consumption from 16.7 percent of allelectricity sold in the state in FY1971 to 43.0 percent in FY2000. The loss incurred by GEB on thisaccount is estimated at Rs14.0 billion ($0.3 billion) during FY2000.

16. As a result of efforts made by the National Development Council (NDC)8, a high-levelcommittee on power was constituted in June 1993. In its report submitted in October 1994,the committee recommended (i) organizational reforms at the state level: commercialization, andunbundling of generation, transmission, and distribution of the SEBs; (ii) organizational reforms atregional and national levels to strengthen the role of the central sector agencies, freeing themfrom government control, allowing them to implement new projects on a joint-venture basis withthe private sector, and ultimately reducing Government's equity in them to not more than26 percent; (iii) large-scale involvement of the private sector in generation and distribution, withthe sponsors selected through transparent and competitive bidding procedures; (iv) depoliticizingelectricity tariff setting by creating a national tariff board for regulating bulk tariffs at the nationallevel and regional tariff boards for regulating bulk and retail tariffs for both public and privateutilities at the state level; and (v) progressive phasing out of subsidies to agricultural consumers,with a minimum tariff of not less than 50 percent of the average cost of supply to be introduced inthe first phase.9 These recommendations had been renewed in the meetings of NDC in Octoberand December 1996 and a document titled Common Minimum National Action Plan for Powerwas published by the Government based on the last meeting. However, not much progress hasbeen achieved in these reform areas to date.

7 GEB does not meter its agricultural consumers; hence, tariff is based on connected load.8 NDC is India's highest political body. It is chaired by the Prime Minister and comprises the Chief Ministers of all the

states in India.9 In the previous reports and conclusions of the conferences of power ministers, reference was made to a minimum

agricultural tariff of Rs0.50 per kWh ($0.011 per kWh). The general call for such a minimum tariff has become largelya political issue because the figure of Rs0.50 per kWh has no logical basis other than it is higher than the current tariff.To date, only seven states have increased the electricity tariff for agricultural consumers to this level.

6

17. Two other major points in the sector’s restructuring are (i) introducing private sectorparticipation in the power sector, and (ii) reforming of SEBs. On account of the dualistic natureof the Indian power sector, all fundamental changes have to be effected through a politicalconsensus between the Government and the state governments. In 1991, the Governmenteffected major amendments to the Electricity and Electricity (Supply) Acts, which enabled thestate governments to invite private sector investment in generation and distribution. Althoughthe response from the investor community has been very positive, the states have not been ableto capitalize on this sentiment on account of the noncommercial environment of the sector andlack of a transparent and fair regulatory mechanism. For a start, with assistance from the WorldBank, ADB, and other aid agencies, the state of Orissa in 1995 enacted comprehensivelegislation that allowed separation of Orissa SEB’s generation, transmission, and distributionfunctions (i.e., unbundling); corporatization of the sector entities; and appointment of anindependent regulator for the sector. However, this start has not been without its share ofproblems. Lack of competitive standards in the power sector, an emphasis on privatization forits own sake rather than for effecting improvements in quality of supply and consumersatisfaction, the seeking of higher returns on investment without corresponding improvements insupply, and improper sequencing have undermined the gains made in non-political andtransparent tariff setting and private sector participation in generation and distribution.

D. State Government Expenditure

18. Under the Ninth Five-Year Plan (FY1998-FY2002), the State Government plans to getinstalled an additional 4,300 MW of generating capacity. Of this, GEB will install only fourthermal generating units for 460 MW, and IPPs will install about 4,000 MW of the additionalcapacity. GEB is making the necessary investment in transmission and distribution under theNinth Plan to evacuate the output power from new generation units and to transmit anddistribute to customers. The investment includes 1,604 circuit kilometers (cct-km) of 400 kilovolt(kV) transmission lines, 5,475 cct-km of 220 kV transmission lines, 3,100 megavolt amperes(MVA) of transformer capacity in 400 kV substations, and 5,300 MVA transformer capacity in220 kV substations. In the Ninth Plan the State Government proposes to invest Rs37.0 billion($0.8 billion) for developing of its power sector. This allocation represents an increase of41 percent over the allocation for the Eighth Five-Year Plan at Rs26.25 billion and reflects theincreased priority on this sector in the State Government’s plans. Within the sector, the planreveals a strong emphasis on upgrading the transmission and distribution network with about 69percent of the total allocation. The phasing and allocation of the proposed outlay are presentedin Table 2 .

Table 2: Power Sector Allocation in Gujarat’s Ninth Plan (FY1998-FY2002)(Rs million)

Item FY1998 FY1999 FY2000 FY2001 FY2002 Total Percent Hydro Generation 46 53 106 95 0 299 0.9 Thermal Generation 2,233 3,137 1,938 2,160 1,530 10,998 29.7 T & D a 3,746 4,708 4,886 4,780 5,500 23,621 63.7 Rural Electrification 230 325 524 510 510 2,109 5.6 Others 6 12 9 15 20 62 0.2

Total 6,261 8,245 7,463 7,560 7,560 37,041 100.0a Transmission and distribution.

19. This level of investment will be adequate to fulfill demands for electricity only if about4,000 MW of capacity ($4 billion of investment) is installed by the private sector during the planperiod. Given the negative returns now being made by GEB in the transmission and distributionsegments of the business on account of the highly subsidized agricultural tariffs, revenues will

7

not be sufficient to service this additional investment, irrespective of whether the distributionsystem is privatized or not. Thus, the key to the sustainability of operations in the sectorinvolves changing the business environment and rationalizing tariffs.

E. The State Government’s Objectives and Strategy

20. The State Government aims to create a business environment that would be conduciveto improving the sector’s (i) operating efficiencies, (ii) financial viability, (iii) service to itsconsumers, and (iv) conservation of electricity. It proposes to do this by (i) encouraging andfacilitating private sector participation in power generation and distribution and fostering atransparent and competitive environment with equal opportunities for the public and privatesectors; (ii) optimizing the operations of the power utilities; (iii) tariffs based on commercialprinciples that enable costs to be recovered and reasonable returns to be made on investments;(iv) independent regulation and tariff setting backed up by statutory provisions; and(v) transparent, reasonable, direct and quantified subsidies to targeted sections of consumers.The State Government wishes to comprehensively amend the existing legislation, regulations,and tariffs on the subject to bring into effect the above principles. It issued a comprehensivepower policy document in December 1995 followed by a Letter of Intent to ADB in March 1996.After detailed discussions with ADB as part of the policy dialogue associated with the SectorDevelopment Program, the State Government submitted its development policy letter (Appendix2), which includes a policy matrix.

F. External Assistance to the Sector

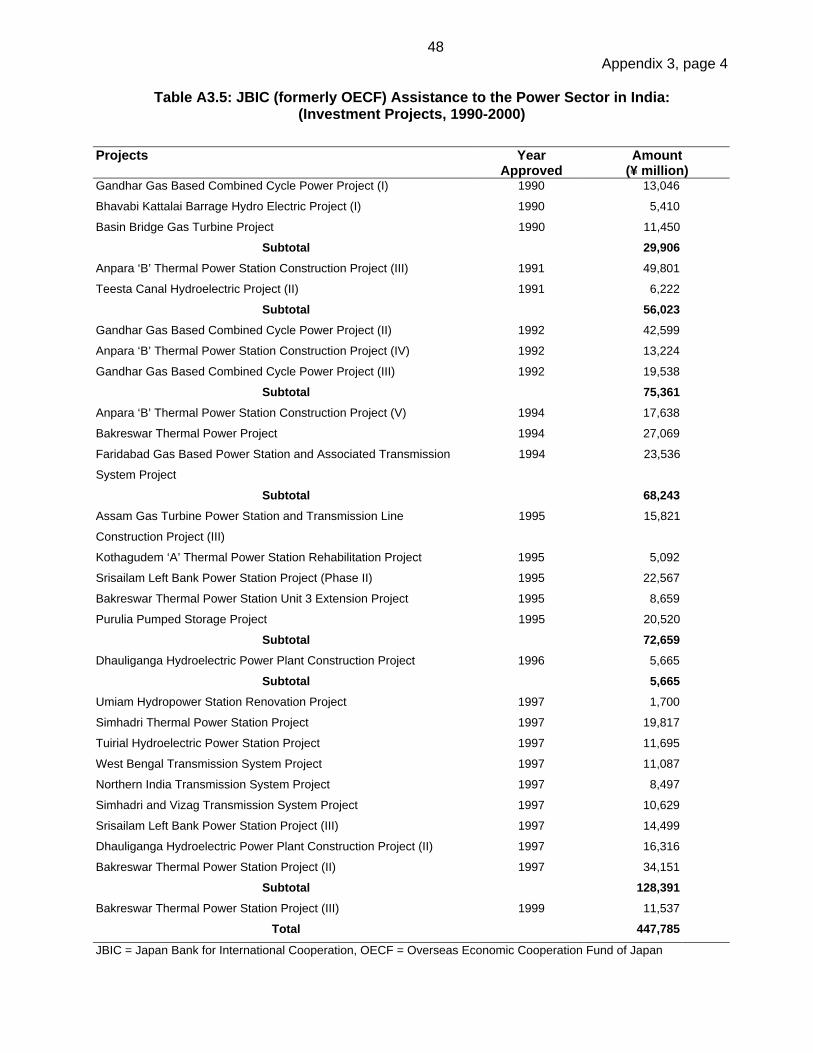

21. The power sector has received a major portion of India's external assistance. Of ADB’stotal Government-guaranteed lending to India amounting to $7.968 billion as of 31 October2000, seven loans for $1.505 billion (19 percent) had been approved for the power sector. Thefirst four projects were for power generation; the three most recent have been sector loans tosupport improvements in the efficiency of SEBs and development of the national transmissiongrid. In addition, ADB's private sector group (PSG) has approved three loans and investmentstotaling $79.8 million for one captive transmission and two generation projects 10. Powersubprojects have also been considered for financing under ADB's private sector infrastructurefacility11 and the Infrastructure Development Finance Company12. ADB also approved$12.2 million for 18 TAs, mainly advisory, at both the national and state levels. The TAs havefocused on environmental and pollution control issues related to power generation, bulktransmission tariffs, improving least-cost system planning, tariff studies at the retail level,improvement of technical and commercial operations, power sector restructuring, andestablishment of an independent regulatory authority. Previous ADB assistance to the powersector in India is listed in Appendix 3.

22. The major funding source to the sector is the World Bank group. NTPC, the WorldBank's largest client worldwide, has been a major beneficiary of this assistance. The WorldBank has supported power generation, transmission, and distribution projects, includingassistance directed to SEBs. ADB coordinates with the World Bank on the geographical

10 Loan 7058/1036-IND: CESC Limited, for $17.8 million, approved on 4 October 1990; Loan 7082/1142-IND: CESC

Limited II, for $32.0 million, approved on 13 December 1991; and Loan 7130/1499-IND: Balagarh Power CompanyLimited, for $15 million in equity and a loan of $25 million, approved on 5 December 1996.

11 Loan 1480-IND: Private Sector Facility: Industrial Credit and Investment Corporation of India Ltd.; 1481-IND:Private Sector Infrastructure Facility: Industrial Finance Corp. of India Ltd.; 1482-IND: Private Sector InfrastructureFacility: SCICI Ltd.; for a total of $300 million, approved on 7 November 1996.

12 Investment 7138-IND: Infrastructure Development Finance Company, for $30 million equity investment, approvedon 14 October 1997. The loan amount was subsequently reduced to $15.463 million due to greater than expectedsubscription from the investors.

8

demarcation of state-level operations, as well as to ensure overall complementarity of actions atboth the central and state levels. ADB and the World Bank have concurrent ongoing operationsfor different projects with three organizations: PFC, Powergrid, and NTPC. Other majoragencies funding the sector are the Japan Bank for International Cooperation (JBIC),Kreditanstalt für Wiederaufbau (KfW, for the Government of Germany), the Department forInternational Development of the United Kingdom (UK) (DFID), the Canadian InternationalDevelopment Agency (CIDA), and the United States Agency for International Development(USAID). Although the combined assistance of all aid agencies constitutes only about 8-10percent of the total investments in the sector, several key policy initiatives have been catalyzedas a result of this assistance. Major external assistance provided to the power sector by otheraid agencies is also listed in Appendix 3.

23. The World Bank is supporting power sector reforms in the states of Andhra Pradesh,Haryana, Orissa, Rajasthan, and Uttar Pradesh. In Andhra Pradesh and Uttar Pradesh, powersector reform is viewed as part of overall reform of state finances as is being supported by ADBin Gujarat and Madhya Pradesh.

24. JBIC is supporting the expansion of public sector generation, transmission, anddistribution including rural electrification. It has no geographic preferences.

25. DFID’s exclusive objective in providing assistance is poverty reduction. It is financingstudies for restructuring the power sector in Andhra Pradesh, Haryana, and Orissa. It has noplans to participate in financing hardware other than in renewable energy systems. It hasoffered to cooperate with ADB in funding studies for power sector restructuring in MadhyaPradesh and West Bengal and to assist these states in other areas also, such as the socialinfrastructure sectors.

26. USAID has extensively supported and continues to support policy aspects of privatesector participation. It has supported studies for state sector reforms through PFC, and throughprovision of grant assistance for energy management, conservation, and training. It is workingwith ADB and PFC for studies in Assam, Punjab, and West Bengal.

27. CIDA has assisted Kerala in conducting extensive studies for restructuring its powersector, and is working with ADB in conducting such studies in Madhya Pradesh, and with theWorld Bank in Andhra Pradesh. ADB is following up on CIDA's work in Kerala through its policydialogue and preparations for a possible loan project.

28. The broad policy content of the Sector Development Program has been discussed withall the aid agencies that have supported activities associated with sector reforms at the centraland state levels. All agencies have expressed general support for it.

G. ADB’s Country and Sector Strategy

1. Lessons Learned

29. The operations of ADB and other aid agencies in the power sector in India havegenerally been successful from a project point of view; i.e., the projects concerned have beencompleted, although with implementation delays, and performed to the desired technical levels.However, except for the ongoing loans to Powergrid13, these projects were not designed tochange the business environment, and sector performance has continued to deteriorate,

13 Loan 1405-IND: Power Transmission (Sector) Project, for $275 million, approved on 16 November 1995 and

Loan 1764-IND: Power Transmission Improvement (Sector) Project, for $250 million, approved on 6 October 2000.

9

although the operations of the project components, taken individually, were satisfactory. Thiswas primarily on account of (i) politicized tariff setting; (ii) rapid growth of the demand forelectricity, making conventional investment strategies unworkable; (iii) government rules andregulations and control of the SEBs that inhibited speedy decision making; and (iv) thenoncommercial setup of the sector that did not generate the market for alternative players tostep in to bridge the gap between supply and demand.

30. In the past, ADB extended assistance to discrete power projects in various states as wellas to the central power sector agencies. Although the policy enabled ADB to support manyprojects, it spread ADB's resources too thinly, with the result that it could not achieve its desiredgoal of policy reforms with its power sector borrowers. In most states, the power sector was thelargest recipient of state resources in terms of both subsidies and capital investments, and itwas realized that macro management of the state's finances needed to be improved for thesuccessful turnaround of the power sector. Therefore, ADB is now assisting selected states forpower sector reforms only in the context of a holistic change in their macroeconomicmanagement.

2. Operational Strategy

31. ADB’s operational strategy in India is to support efforts to achieve higher sustainableeconomic growth to promote employment and reduce poverty. Its contribution to higher growthfocuses on improving the supply side efficiency of the economy, especially by reducingbottlenecks in key infrastructure sectors. Emphasis is on improving the policy, institutional, andregulatory framework so as to enhance the efficiency of public sector operations and toencourage private investment. Improving resource mobilization to finance the necessaryinvestments is a key component of ADB’s assistance, and includes support for developing offinancial and capital markets as well as for improving internal resource mobilization in the sectoragencies and enhancing their creditworthiness. High priority is also given to assisting projectsthat contribute to environmental improvement.

32. ADB's strategy for India was revised in 1996 to accommodate an urgent need for aportion of its assistance to be provided in a systematic and comprehensive way at the sub-national or state level. This need reflects the facts that (i) a geographic focus, together with theongoing selective sector focus, enables ADB to maximize its developmental impact both in thestates concerned and, through the demonstrational impact of its operations, in other states aswell; (ii) state-level economic reforms, which have been lagging behind initiatives takenby the Government, need support and incentives; and (iii) the states have considerableautonomy and have major legislative, administrative, and fiscal responsibilities in manyeconomic and social sectors. Key elements of the subnational assistance include (i) improvingthe states' public resources management, (ii) reforming and restructuring public sectorenterprises to improve operating efficiencies, and (iii) supporting reforms in key infrastructuresectors with a view to increasing private investment. Gujarat was the first state chosen for thistype of holistic support and the first loan was granted by ADB in December 1996 (footnote 1).Madhya Pradesh was the second focal state and its loan was accorded in December 199914.

33. Reflecting ADB’s overall country strategy for India, and in recognition of the dualisticstructure of India's power sector, ADB's strategy for the sector, which has been pursued incoordination with the World Bank, intends to operate at two levels. At the central level,assistance to central power sector companies such as Powergrid (footnote 13) and PFC15 aims

14 Loan 1717-IND: Madhya Pradesh Public Resource Management Program, for $250 million, approved on

14 December 1999.15 Loan No. 1161-IND: Power Efficiency (Sector) Project, for $250 million, approved on 26 March 1992. The loan

account was closed on 18 December 1998.

10

to support their commercialization and use them as agents to leverage reform in their clientSEBs. Through Powergrid, ADB also seeks, at the central level, to implement nationwide powersector reforms by establishing of model cases in tariff structures, competitive pool operations,regulating power supply to delinquent SEBs, and investments based on commercial viability ofprojects. At the state level, ADB is building up the reform process from the grassroots byconsidering assistance only for states that demonstrate the political will to substantiallyrestructure and commercialize their power sectors, and by assisting them to actualize thereforms. Gujarat, Madhya Pradesh and Kerala have been identified for ADB’s holistic support.Improvements in the power sector will increase the fiscal space of the state governments andincrease their ability to allocate more resources for poverty reduction and socioeconomicdevelopment.

IV. THE SECTOR DEVELOPMENT PROGRAM

A. Rationale

34. A comprehensive program of reform-oriented studies has been initiated through ADB'stechnical assistance.16 As a subset of the total reforms and GEB’s proposed investments in theNinth Plan period (FY1998-FY2002), the Sector Development Program seeks to further the keyobjectives of the reform process that will mobilize greater resources for the power sector to enablerealization of, and a possible increase in, the total investment. It includes support and incentivesfor restructuring the power sector as program assistance, and support for actual investments forevacuation and distribution of power from proposed private sector IPP generation projects as wellas in hitherto relatively neglected areas of metering, energy end-use management, and systemloss reduction.

35. The Program has been designed to reduce GEB’s operating costs, raise additionalrevenues and progressively eliminate the need for transfers from the State Government'sbudget, allow the expansion of power supplies using private generating capacity, and improvethe environmental consequences of power use. It will support economic growth in the state,particularly in industry, and sustain production in agriculture. It will also shift the focus of theState Government's expenditures from power supply to other responsibilities, for example, in theeducation and health sectors.

36. The Sector Development Program seeks to establish a business environment in thepower sector that promotes efficiency and growth and to support critical investments required tobuild up on the new environment that is created. Since both facets of development are importantfor the success of the reforms, the sector development assistance modality has beenconsidered.

B. Objectives and Scope

37. The immediate objectives of the Sector Development Program are to provide support andincentives to the State Government and GEB for (i) sector reform activities such as independenttariff setting, tariff rationalization, and functional segregation of GEB’s activities; (ii) establishingtransmission systems linked with IPP generation projects; (iii) modernizing and upgradingdistribution systems, especially those in the Anand, Rajkot, and Mahesana distribution circles; and(iv) water and electricity conservation measures. The entire exercise is geared to improve the

16 The studies include (i) preparation of a power system master plan; (ii) preparation of a framework for electricity

tariffs; (iii) review of electricity legislation and regulations; (iv) financial support to GEB for formation of twoindependent distribution profit centers; and (v) solicitation for private sector implementation of the Chhara Project.

11

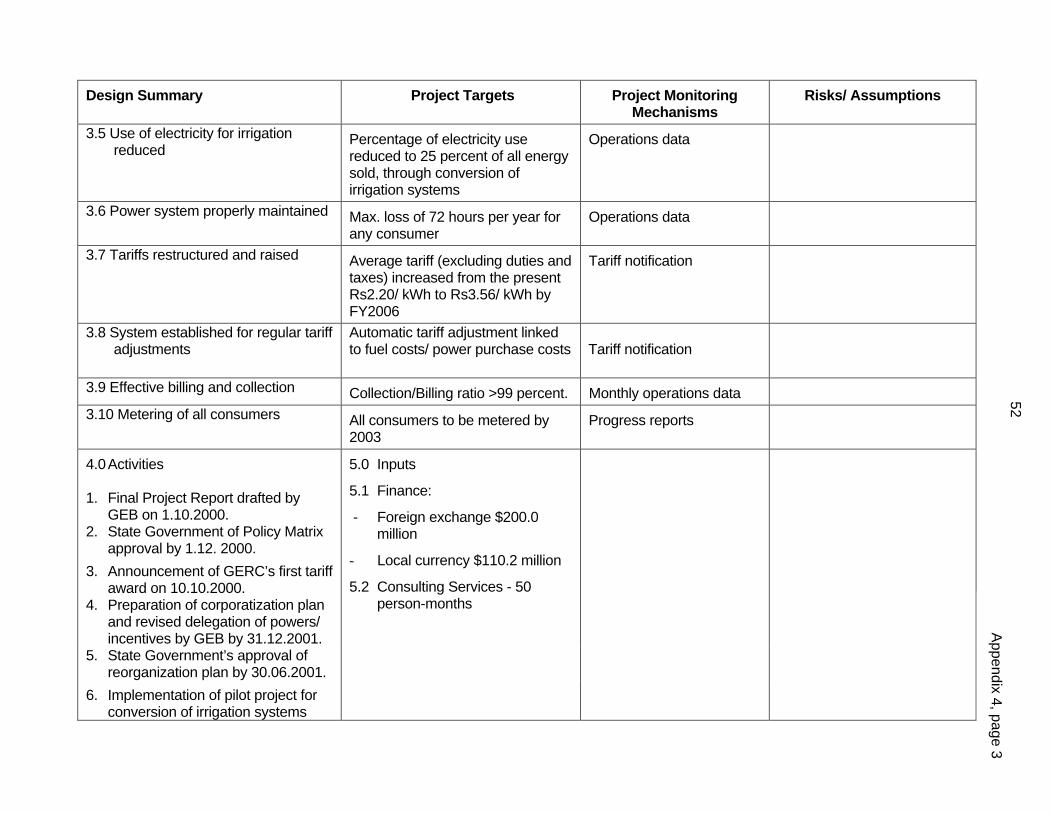

power sector’s financial and economic viability over the next five years to ensure sustained growthof the sector. Appendix 4 shows the Sector Development Program framework. TA for reorganizingof GEB, consultation with electricity consumers, and supporting the Gujarat Electricity RegulatoryCommission (GERC) are part of the Sector Development Program.

C. Policy Framework and Actions

38. The Sector Development Program will assist Gujarat in effecting matching reforms to takeadvantage of the 1991 policy of the Government. To make its interventions more policy orientedand focused, it concentrates assistance in the power sector to a state that is undertaking reformsin its macro finances and has agreed to restructure its power sector and includes comprehensive,albeit gradual approach to restructuring the sector allowing for development of (i) successororganizations to GEB, (ii) a commercial culture, (iii) consumer benefits in terms of quality ofsupply, and (iv) rationalized tariffs and duties.

39. ADB has been conducting policy dialogue on the Sector Development Program at threelevels; (i) with the Government on countrywide changes that need to be done to prepare anenabling framework for sector reforms; (ii) with the State Government for the policy aspects ofthe reforms in the state; and (iii) with GEB for the Project and organizational aspects of thereforms. The issues discussed are as follows.

1. Metering

40. At present, agriculture and socially disadvantaged consumers are provided electricitywithout meters on the premise that the revenues realized from them do not justify the costsincurred in installing meters and using them. However, this practice has led to a sharp increase inconsumption from such connections, a large part of which is theft of electricity. A recent surveyindicates that over 43 percent of GEB's sales is through unmetered supply. Hence, installation ofmeters on all consumer connections is a priority for GEB.

2. Private Sector Participation

41. One of the main objectives of the Sector Development Program is to facilitate privatesector participation in the power sector in Gujarat. It is expected that structured introduction ofsuch participation will (i) provide additional capital, (ii) lead to greater commercialization in thesector, (iii) improve operational efficiencies in the sector, and (iv) provide a competitiveenvironment. Structuring this participation is essential to realize the stated benefits since it isimportant that the profit motive of the private sector be appropriately channeled. Gujarat hashad a long tradition of private sector generation and distribution, but on account of aninadequate business environment, the investments have not been as efficient as they shouldbe. Restructuring requires three key actions: (i) formulation of a least-cost expansion plan thatdovetails investments from both the public and private sectors so as to maximize the overallbenefits of investments; (ii) setting up a tariff regime that does not distort costs and prices sothat market-driven indicators are provided to optimize operations; and (iii) creating a statutoryregulatory authority independent of the State Government that ensures freedom of entry into themarket, transparent procedures, nonpartisan resolution of disputes, and fostering ofcompetition.

3. Electricity Rates to Agricultural Consumers

42. Currently, GEB charges a “per horsepower installed” flat tariff to its agricultural consumers.Since there is no incremental charge based on the actual withdrawal of energy, there is no

12

incentive to conserve electricity. A major social disbenefit caused by this scheme is theindiscriminate use of groundwater by farmers in the relatively dry northern districts of the State togain short-term benefits of higher cropping yields per acre through multicropping and growingwater-intensive cash crops instead of the traditional dry area crops grown earlier. As a result, thewater table has dropped from an estimated 10-12 meters (m) below ground in the 1970s to anaverage of 150-200 m today and is dropping by an estimated 12 m every year. The water nowcontains heavy traces of fluorides and other minerals, and it is feared that in two or three years thewater may turn saline, thereby severely and permanently damaging soil quality and erodingagricultural activity in the area. Lowering of the water table has also increased the consumption ofelectricity per acre of irrigated land since more energy is required each year to pump up the samequantity of water. Hence, for the Sector Development Program, the issues of water conservationand electricity conservation have become inextricably linked. ADB Missions visited severalvillages in Mahesana district in north Gujarat and discussed the issue with about300 representatives of the farming community. The Missions' impression is that (i) many farmersin this district would not mind paying higher rates for electricity provided the quality and reliabilityof power supply improved; and (ii) farmers were hoping that some agency will show themalternative techniques of conserving water while maintaining their current levels of production andincome.

43. The only option available that would fulfill the needs of water and energy conservation,protect the earnings of the farmers and improve the financial viability of the sector is to helpfarmers change the method of irrigation from the present “flood irrigation” technique to “dripirrigation” which has been successfully practiced in dry areas such as Israel and southwest UnitedStates. Some small schemes have also been implemented in Rajasthan and Gujarat withsuccess. The Program, therefore, includes assistance for a pilot scheme for converting ofirrigation systems in Mahesana district.

4. Delegation of Powers to Independent Profit Centers

44. While generation and transmission are activities that are remote from the end users ofelectricity, distribution is closely linked to its consumers. Hence, for improvements to be effected inthis segment, effective delegation of administrative decision-making needs to be made to themanagers that are directly responsible. To make a beginning in this respect, GEB created pilotindependent profit centers at Kheda (Anand circle) and Rajkot. GEB has since delegated thefollowing powers to the superintending engineers (managers) of the centers. The managers ofeach center will be directly accountable for its performance and the manager and the staff will begiven with incentives for good performance.

(i) Procurement. Materials to be procured by GEB headquarters (HQ) will be listed.Except for items on this list, the centers will be allowed to procure all necessarymaterials and sufficient financial powers will be delegated for such procurement.Further, there should be a maximum waiting time for supply of materials by GEB(HQ) to any indent from the centers, even for items on the list of materials to beprocured by GEB (HQ). If GEB (HQ) cannot satisfy the indent in a given time, or incase of an emergency, the centers should be allowed a much higher level ofauthority to effect their own procurement.

(ii) Money Transfers. Based on the approved budget for the year, the centers willwithhold the required funds from their collections, instead of the present practice ofsending in all money collected to GEB (HQ) and then having their funds transferredback. The centers will be debited for all electricity sold to them at 66 kV and alsofor all the materials supplied to them by GEB (HQ). If any non-remunerative work is

13

requested to be undertaken by the centers, GEB (HQ) will pay for the works aswell as the differential revenue loss to the centers for the operation andmaintenance of such schemes.

(iii) Personnel matters. Once GEB (HQ) selects the superintending engineers(managers) of the centers, they will not be transferred or recalled until theycomplete their tenures, except in the gravest of circumstances. Important postingsof officers and staff to the centers will be made by GEB (HQ) only after consultingwith the concerned manager. Further, GEB (HQ) will withdraw from the centers allstaff identified by the managers as redundant, undesirable or inefficient. Themanagers will be provided an annual operations and maintenance budget, whichmay be used for salaries or equipment and facilities. Further, managers will havethe flexibility to reorganize their divisions to extract more efficiencies and may eveninterchange categories of staff.

(iv) Priority. GEB will give priority to the centers for all support as well as for reliablepower supplies up to the extent of the electricity paid for by them.

5. Rationalization of Electricity Duty

45. Prior to FY1998, there was a high level of electricity duty on GEB's supplies to hightension (HT) and low tension (LT) industrial consumers (averaging about Re0.50 per kWh)whereas captive generators paid a much lower rate (averaging at about Re0.05 per kWh after aduty-free concession period of 10 years). This put GEB at a disadvantage in retaining its industrialconsumers, especially in the wake of the liberal licensing policies for captive generation adoptedby the state, which provides other benefits such as sales tax waivers on finished products, andhigher depreciation rates. Apart from cross-subsidization in the agriculture sector, the burden ofwhich was principally borne by GEB’s industrial consumers, this was the main factor leading toincreasing captive generation in Gujarat which has reached a sanctioned capacity of 3,100 MWas of 31 March 2000. The State Government has since raised the rate of duty on electricityproduced by captive generators to Re0.2-0.4 per kWh and has agreed to reduce electricity dutyon GEB for its sales to its industrial consumers to make competition fair to GEB.

6. Governance

46. Tariff setting in the power sector in Gujarat has been heavily politicized, with agriculturalconsumers being heavily subsidized. This has led to distortion in consumption and avoidablewastage of both electricity and water. There is an urgent need to depoliticize and rationalizetariffs if the sector's operations are to be viable. Competition in the sector has also beenunstructured and loose as often happens in a near monopoly. Power purchase agreementshave largely been negotiated and there is no competition among similar business segmentswithin the organization. Management of the sector is another key issue. GEB's management[other than its Member (Technical)] comprises political and bureaucratic deputies appointed bythe State Government. Transfers are frequent and there is little attempt at taking long-termperspectives on organizational development and strategies. The solution to these governance-related issues is to (i) reorganize the sector along functional lines; (ii) appoint an independentregulatory commission to set tariffs and structure competition in the sector; and (iii) graduallyreplace appointees of the State Government on the boards of management of the sectorcompanies with experts. As a consequence of this policy dialogue, the State Government(i) established GERC in 1998 under the Central Acts, (ii) agreed to restructure the sectorgenerally along functional lines either, and (iii) agreed to progressively professionalize themanagements of sector entities.

14

D. The Investment Project

1. Project Description

47. The investment project has four components (details are in Appendix 5):

(i) Part A. Transmission lines and substations linked with IPP power projectsand for system improvement.

(ii) Part B. Transmission lines and substations associated with Anand, Rajkotand Mahesana distribution circles.

(iii) Part C. Upgrading and strengthening of distribution systems especially inAnand, Rajkot, and Mahesana distribution circles.

(iv) Part D. A pilot scheme for energy and water conservation by convertingexisting flood irrigation systems to drip irrigation systems in Mahesanadistrict.

2. Cost Estimates and Financing Plan

48. The summary cost estimates of the Project are in Table 3 (details are in Appendix 6).

Table 3: Cost Estimates($ million)

Item Foreign Exchange Local Currency Total Cost

Project ComponentsPart APart BPart CPart D

Subtotal Base Cost (Oct 2000)

72.9 20.0 56.9 7.8157.6

37.813.525.1 2.679.0

110.733.582.010.4236.6

ContingenciesPhysical a

Price b

Subtotal

15.8 9.1 24.9

7.98.015.9

23.717.140.8

Interest During Construction 17.5 15.3 32.8

Total Project Cost 200.0 110.2 310.2

a Computed at 10 percent of base cost.b Computed on the basis of 2.4 percent foreign currency inflation and 6.5 percent local currency inflation.

49. The proposed financing plan for the Project component is summarized in Table 4.

15

Table 4: Financing Plan for Project Component($ million)

Forei gn Exchan ge Local Currency Total Cost Percent

ADB 200.0 - 200.0 64.5

GEB - 110.2 110.2 35.5

TOTAL 200.0 110.2 310.2 100.0

ADB = Asian Development Bank, GEB = Gujarat Electricity Board, - = magnitude zero.

E. Environmental and Social Measures

1. Environment

50. The Sector Development Program has been classified as category B and a summary ofthe initial environmental examination (SIEE) report is given in Appendix 7. Of the various projectcomponents, minor land acquisition and tree cutting are required only for transmission lines andsubstations. The Project has no long-term negative environmental impacts.

51. During Project implementation, GEB will submit to ADB an annual report consisting of(i) monitoring results; and (ii) copies of permits, licenses, and clearances that may be issued bythe Gujarat State Pollution Control Board and other state and national agencies responsible forenforcing of environmental safety regulation and standards. If any project component is cited forviolating laws or standards, the report will include a certification from the relevant agency that thedefect has been corrected or that a time-bound action plan for its correction has been accepted.

52. No significant rehabilitation or resettlement is required for the Project. Specific LandAcquisition and Resettlement Plans (LARPs) to be applied by GEB (or its successor entities) tocompensate those affected by the Project will be drawn up for each component during projectexecution since they can be determined only at the time of actual construction.

2. Social Dimensions

53. The Sector Development Program is designed to promote economic growth by increasingelectricity supply in Gujarat, including the rural areas. It will provide a reliable and quality powersupply, thereby improving industrialization. As a result of faster economic growth due to thegrowth of industry and commerce, employment opportunities are expected to expand, thuscontributing to poverty reduction. Reliable electricity supply will also enhance education, health,and other social infrastructure facilities directly and indirectly. Moreover, since the funds currentlyused to subsidize the power sector will be available for social sector users, the poor will directly bebenefited. Small residential consumers will not be affected since the tariff system incorporates hasa lifetime rate of Rs2.70 per kWh for the first 50 kWh of consumption.

54. During the preparation of the Sector Development Program, GERC held consultationswith the major consumer groups and representatives, including farmers, household heads, andindustrialists. While their views on the tariff structure vary, inefficiency was found to be acommon concern. Transparency in electricity consumption and cross-subsidy provision was amajor concern of industrial and household consumers. There was a strong demand for aplatform to continue the dialogue with GERC/GEB, and the need for educating consumers andtheir raising awareness was suggested. In addition to informing the consumer groups of reform

16

actions and their implications, and seeking feedback from them, consumer education shouldinclude energy conservation and environmental concern.

55. Among the farmers’ groups, water availability is the major concern. It was reported thatthe water table in a village has been dropping an average of 4.5 to 6 m every year and the watertable is now 150-200 m below the ground compared with 60-75 m a decade ago. Farmers areaware of water scarcity and the need for conservation; however, the current per horsepowerinstalled flat tariff gives them little incentive to conserve water. In fact, it drives them toindiscriminate use of groundwater. This causes a vicious cycle of water wastage anddegradation. Sole dependence on the tubewell makes it difficult for farmers to diversify theirfarming. Therefore, the proposed pilot project on drip irrigation will have a positive outcome interms of efficient water use and shift of cultivation to high-value crops.

56. A poverty impact assessment is given in Appendix 8. Tariff increase on agriculturalconsumers may result in a short-term negative impact. However, the impact on the small andmarginal farmers may not be serious, since at present these farmers, who do not own tubewells, buy water from large farmers at a high rate. The richer farmers tend to control watersupply in rural areas, and the small and marginal farmers do not necessarily benefit from thecurrent subsidies. Rationalizing the tariff structure will increase efficiency, and will give endusers water equitable access to water. Overall, the Sector Development Program will have abeneficial impact on the poor.

V. THE LOANS

57. ADB will provide two loans totaling $350 million from its ordinary capital resources(OCR) to the Government, as the Borrower for forwarding to the State Government and GEB (orits successor entities with the prior approval of ADB). The loans will carry interest at the ADB’spool-based variable lending rate for US dollar loans, and will also be subject to a 1 percentfront-end fee, as well as applicable commitment charges in accordance with ADB's policy onOCR loans. The loans are (i) a Program Loan of $150 million with a maturity of 15 yearsincluding a grace period of 3 years, to be disbursed in three equal tranches of $50 million eachupon compliance with policy conditions as specified in paras. 65-67, and (ii) a Project Loan of$200 million with a term of 20 years including a 5-year grace period.

A. The Program Loan

1. Amount, Terms, and Sources of Funds

58. The Program Loan of $150 million will be provided from ADB's OCR resources. Thecounterpart funds to be generated from the loan proceeds will be transferred from theGovernment to the State Government under normal arrangements for the transfer of externalassistance. The funds transferred to the State Government will be treated as “additional” to theGovernment's transfers allocated annually to the State Government. The Government will bearthe foreign exchange risk on the loan.

59. The State Government is expected to incur the following costs of adjustments over thereform period.

(i) Rationalizing of electricity duty is expected to cause a revenue loss of aboutRs1,500 million ($33 million) each year in the next five years for a total of$165 million.

17

(ii) Long-term loans to GEB to retire expensive commercial debt and adjust IPP priceswill be about Rs2,000 million ($43 million).

(iii) Payment of arrears of dues of municipalities and other local bodies until FY2000will cost about Rs700 million ($15 million). It is expected that in FY2001, anadditional $5 million may be required.

(iv) About 700,000 consumer meters will be procured and installed over the next threeyears. While the meters will be procured under the Project, their installation will befinanced by the State Government. At $10 per meter, this works out to $7 million.

60. The total cost of adjustment to be incurred by the State Government over the reformperiod is estimated at $235 million. It is felt that the Program Loan of $150 million is adequate andjustified considering the cost of adjustments incurred by the State Government on account of thereforms and the political costs it will incur during implementation.

2. Executing Agencies

61. The Executing Agencies will be the Finance Department and the Energy andPetrochemicals Department of the State Government.

3. Procurement and Disbursement

62. The proceeds of the Program Loan will be utilized to finance the full foreign exchangecosts (excluding the local duties and taxes) of imports produced in and procured from ADB’smember countries, other than those specified in the list of ineligible items (Appendix 9) andimports financed by other bilateral and multilateral sources. All procurement will be throughnormal commercial practices in case of procurement by the private sector, or prescribedprocedures acceptable to ADB in the case of procurement by the public sector, having dueregard for the principles of economy and efficiency.

4. Counterpart Funds

63. Counterpart funds generated by the Program Loan will be transferred by theGovernment to the State Government and will be used by the State Government underarrangements satisfactory to ADB, to support the financial restructuring of GEB and adjustmentcosts associated with the Sector Development Program, including (i) reduction of the accountspayable of GEB to power producers and suppliers of fuel and transport, (ii) retirement of theexpensive commercial debt of GEB, (iii) payment of outstanding municipal dues,(iv) rationalization of electricity duty, and (v) reduction of IPP tariffs through buyout of debt.

5. Monitoring and Tranching

a. Tranche 1: $50 million

64. The first tranche of $50 million of the Program Loan will be released upon fulfillment ofthe following actions. This release is anticipated in December 2000.

(i) establishment of the GERC;

(ii) approval of the Gujarat Electricity Industry (Reorganization and Regulation) Bill,2000 (the Bill) by the State Government’s Cabinet, and its submission by theState Government to the Government for its approval;

18

(iv) first tariff award by GERC;

(v) incorporation and establishment of Gujarat State Electricity Company Limited(GSECL) and Gujarat Energy Transmission Company Limited (GETCL).Constitution of their boards of directors, with at least two directors being fromnon-governmental sector who are experts in their related fields;

(vi) circulation by GEB of a draft action plan to meter all consumers for consumerconsultation, in accordance with GERC’s order of 10 October 2000;

(vii) approval by the State Government of the structure, human resources, andbudget of GERC for the next five years; and

(viii) payment by the State Government of all municipality dues owed to GEB up to 31March 2000.

b. Tranche 2: $50 million

65. The second tranche of $50 million of the Program Loan will be released upon fulfillmentof the following actions. This release is anticipated in June 2001.

(i) transfer of Gandhinagar and Utran power stations from GEB to GSECL;

(ii) offset of subsidy and subvention arrears owed by the State Government to GEBuntil 31 March 2000, and payment of outstanding municipality dues by the StateGovernment to GEB until 31 March 2001;

(iii) introduction of the Bill in the Gujarat State Assembly for its consideration;

(iv) rationalization and reduction of electricity duty in the State Government’s budgetfor FY2002, in an amount not less than Rs1,500 million; and

(v) filing by GEB before GERC of the action plan to meter all consumers in the state,in a phase manner over a period of three years from 10 October 2000, the dateof GERC' first tariff award.

c. Tranche 3: $50 million

66. The third tranche of $50 million of the Program Loan will be released upon fulfillment ofthe following actions. This release is anticipated in June 2002.

(i) transfer of transmission assets from GEB to GETCL;

(ii) agreement between the State Government, GEB, and ADB on theReorganization Plan for GEB and solicitation for privatization of at least oneidentified distribution area of GEB, unless contrary to the Reorganization plan;

(iii) the rules and regulations under the Bill as enacted (the Act) laid before theGujarat State Assembly and published in the Official Gazette;

(iv) second tariff submission by GEB to GERC; and

19

(vi) establishment and operationalization of GERC under the Act.

B. The Project Loan

1. Amount of Loan, Terms, and Source of Funds