atip n-12 final information transfer(1)-1

TRANSCRIPT

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 1/164

JjJLt ? [ ^^-r n- )4

As Minister of Healthy Living, Youth and Seniors I am please to reply to the email you sent on July 7 ,h t o

Minister Oswald, regarding taxation of unhealthy food as a health promotion strategy.

You are absolutely co rrect in identifying chronic disease as a major challenge for public he alth, and the

burden it creates for both i l l individuals and for the health care system.

In recent years there have been numerous reports and studies which have made recommendations on

obesity and chronic disease prev ention strategies, and many o f these have suggested a tax o n

'unh ealth y' foo ds, such as a ' junk food tax', a 'fat tax', or tax on sugar-swe etened beverages. The u ti l ity

of such strategies is sti l l the su bject of research and debate . W hile it is clear tha t they could provide a

way of raising considerable revenue, which might be directed to prevention and health promotion, it is

much less clear that they would have any meaningful impact on consumer behaviour, food

consumption, and thus public health. My department has examined this issue in the past and continues

to m on itor ne w resea rch. I wo uld refer you to a summ ary of the issues involved in an article w ritte n by

one of my staff in 2006 [attac hed] as we ll as a more recent overview of the sugar-sweetened beverages

issue. We continue to monitor this issue and should more convincing evidence emerge, we would

certainly revisit the policy options.

Thank you for your interest in this topic

JR

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 2/164

THE

Summary Overview

Over the past few years there has been increasinginterest in nutrition advocacy circles and in the popularpress about the idea of a so-called "fat tax", "junk food

tax" or "snack tax". In this review I will address severalbasic issues connected to small taxes on food includingtheir intended purpose, how they work, pros and cons andimplications for dietetic practice.

Background

The concept of a small tax on selected food products isrooted in two big ideas. Firstly, strong scientific evidencethat l inks diet to chronic disease, together with, concernsover the increasing prevalence of obesity has fuelled callsfor strategies to reduce intakes of dietary fat, sugar, salt

and overall food energy (1). Secondly, as food costs areimportant factors in consumer food choice, it is thought tobe possible to change eating behaviour through theapplication of economic levers. The two ideas intersect inthe fact that energy dense foods are amongst the leastcostly of foods (2).

In 1994, Dr. Kelly Brownell of Yale University suggestedtaxing unhealthy foods, a proposal that was quicklylabelled "the Twinkie Tax" and ridiculed by opponents (3).Since then several types of small taxes on food havebeen proposed, the most common of which are styled:"Junk food tax"; "Fat tax"; and "Snack Tax". An alternativeeconomic strategy, the application of subsidies to healthyfood choices, is beyond the scope of this discussion (4).

Defini t ions

The terms "junk food tax", "fat tax", or "snack tax", lackcommon clear definitions. "Junk food" is more of aconceptual category than it is a nutritional one, althoughthe term is widely used as shorthand to refer to some or

©2006 Dietitians of Canada. All rights reserved.

May be reproduced for educational purposes.

Taxing Food

all of high fat or sugar snack foods, fast foods,, soft drinkand candy (5). "Fat tax" embrac es a variety of schemes ttax foods based on their total fat content, or specificalthe saturated fat or trans-fat component. For exampMarshall suggests that products could be taxed if theraised cholesterol concentrations but be exempted if th"ratio of polyunsaturates to saturates (and trans fatacids) were more favourable" (6). Targeting foods fotaxation based on their fat {or indeed, other nutriencontent provides a clearer nutritional criterion than that ojunk-food / non junk food. "Snack food", like "junk food", a more ambiguous concept. For examp le, Health Canadrefers to snack foods "like potato chips and pretzels" bualso to the concept of healthy nutritious snacks from thfood groups (7), while examples from Industry 1 Canada owhat are considered as snack food include cheese curlspopcorn, corn chips and potato chips (8).

Why a tax?

Advocates identify two potential positive outcomes odifferentiated food taxes. The first is the potential foprompting changes in individual eating behaviour that arconsistent with current nutritional advice on healthy eatinand that will contribute to changes in populatioconsumption patterns leading to reduced levels of obesitand chronic disease. This rationale is generally favoureby public health groups and consumer health lobbies anis often proposed as part of a broader comprehensivhealth promotion/public health strategy, citing thexperience of cigarette taxation as a component of comprehensive tobacco control strategy (9). The seconoutcome is revenue generation that could be'directed tsupport nutritional health promotion programs. For thireason, some critics who doubt the likeliness of the firsoutcome nevertheless support such taxes.

Dietitians of Canada

Les dietetistes du Canada

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 3/164

THE INSIDE STORY

Opt ions fo r t ax in te rven t ion

Taxes on food may be applied at the retail level in the

form of general or targeted sales taxes. In Canada, foodis already differentially taxed through the Goods andServices Tax (GST) and Provincial Sales Tax (PST).Foods and beverages subject to GST are listed byCanada Customs (10). There is, arguably, a high degreeof congruency between what is in this list and what wouldbe likely to be on a "junk food" or "snack food" tax list. Anumber of states from the United States of America haveat different times experimented with levying special taxeson soft drinks and specific snack foods or have excludedthese products from tax exemptions given to foodproducts (11).

There are also options for levying taxes at different

stages in the food system. Approaches tried in the U.S.include:

> Manufacturers tax - payable on production volume (e.g.soft drinks or syrups) or as a percentage of salesrevenue, andWholesalers and distributors tax - payable on amountof product sold.

In several jurisdictions these types of taxes weresubsequently repealed due to industry lobbying andthreats to commercial development (12).

on total fat, saturated fat or sugar could have an impacton consumption of fats, sugars and overall calories forsome groups, although with no "particularly advantageous

effects" for the socio-demographic groups amongst whichobesity and unhealthy diets are of the most concern (14).The authors suggest that combining economicinstruments with public information campaigns may be afruitful avenue for further ex ploration. A U.S. stifdy thatattempted to simulate the effects of a fat tax on dairyproducts concluded that a 10% tax on fat content had littleimpact on the quantity of dairy products consumed by anygroup, though there was an overall predicted 1.4%reduction of average total fat intake (15), Otherresearchers have proposed combining taxation of lesshealthy options with'subsidies for healthier alternativessuch as fruits and vegetables, as a potentially moreeffective strategy in improving diet quality and healthoutcomes (16).

Food taxes would almost certainly raise revenues. TheUSDA analysis cited above estimated that a 1%: tax onpotato chips translates into twenty seven million dollars ofrevenue that could be spent on education programs.Governments are often reluctant to allocate specificrevenue streams to specific purposes. A :notableexception is VicHe alth - a very successful Australianhealth promotion foundation supported through tobaccotaxes (17). More often,, monies go into general revenuesfrom where they are reallocated according to changingneeds and government priorit ies.

Would junk food taxes be ef fect ive?

While there have been few attempts to demonstrate theactual impact of such taxes with real world examples,several recent economic modelling studies haveattempted to gauge the likely impact of such taxes, takinginto account factors such as current levels ofconsumption, price elasticity and substitution strategies. AUnited States Department of Agriculture (USDA) modelsuggests that "small" taxes on snack foods would beineffective in changing patterns of consumption and wouldhave litt le impact on diet quality or heath outcomes (13).Even a 20% tax on salty snack foods would result in onlya 4-6 ounce reduction in annual per capita consumption.

Moreover, as the authors point out, there is no guaranteethat any consumption changes prompted by such taxeswould be nutritionally bene ficial.

An analysis carried out for the Danish Food and ResourceEconomics Institute indicated that differential taxes based

It should be noted that food taxe s are regressive in nature

since they disproportionately affect lower incomepopulations where a higher percentage of income is spenton food. Modelling the distributional effect of hypotheticaltaxes on saturated fat, monounsaturated fat, sodium andcholesterol using data from the National Food Survey, arecent United Kingdom analysis showed that the poorest2% of people wo uld pay 0.7% of total income on a fat tax,while the richest group w ould pay only 0.1 % of totalincome (18).

Implementat ion issues

If the idea of a "junk food", "snack food" or "fat tax" gainedpolit ical and public support, there would be at least twokinds of implem entation challenge s to address. The first isin deciding wh at to tax. It is diff icult to link specific foods tospecific health impacts so the idea of tax on specific foodand beverage products runs counter to the message thatit is overall dietary intake that matters. There wou^ld haveto be broad agree men t on the pa rt of policy makers,

©2006 Dietit ians of Canada. All rights reserved.May be reproduced for educational purposes.

Dietit ians of Canada

Les diet&tistes du Canada

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 4/164

e

practitioners and industry on what constitutes "junk-food"

or "snack food" and therefore is taxable.

The second challenge recognises the complexity ofadministering a differential retail tax. Given that newproducts are constantly appearing on the market, and thatmanufacturers may change product specifications, acontinual monitoring, evaluation and classification systemwould be required. Retailers would need to adopt newtechnologies and/or accounting systems to charge thetax, and tax remittance and collection systems wouldhave to be developed. Restaurants would be faced withan even more complex task. It may be that tax levies atthe manufacturer or distributor level would be relativelyeasier to administer and would underline the idea that

healthier choices are an industry as well as consumerresponsibil ity. In either case, both producers andconsumers would likely bear a share of the costs.

References:

1) Shields, M. (2005) Overweight Canadian children aadolescents, Nutrition: Findings from the CanadCommunity Health Survey. Statistics Canahttp://www.statcan.ca/enalish/research/82-620-MiE/2005001/articles/child/cobesitv,htm

2) Drewnowski, A. (2003) Fat and Sugar: An EconoAnalysis. Journal of Nutrition, 133S, 838S-840S.

3) .Brownell, K.D. (1994) Get Slim With Higher TaxNew York Times, Op-Ed., Dec. 15th.

4) Jeffery, R.W., French, S.A., Raether, C. and Bax

J.E. (1994) An Environmental Intervention Increase Fruit and Salad Purchases in :a CafetePreventive Medicine, 23, 6: 788-92.

Impl icat ions for d ie te t ic pract ice

While economic incentives and disincentives are apotential addition to the array of public policy instrumentsavailable to encourage healthy eating, there is as yet noclear cut empirical evidence on which to judge the meritsof junk food or similar taxes. The Institute of Medicineconcludes that there is insufficient evidence to

recommend either for or against taxing these foods, whilea recent Canadian think-tank on addressing obesityconcluded that the relationship between economicpolicies such as the role of tax incentives anddisincentives and their influence on eating behaviours ispoorly understood and requires further research (19).

5) CDC School Health Policies and Programs Stu(2000) Fact Sheet: on Foods and Beverages Sooutside of School Meal ProgramhttD://www.cdc.Qov/HealthvYouth/shoDs/factsheetsdf/outside food.odf

6) Marshall, T. (2000) Exploring a fiscal food policy: tof diet and ischaemic heart disease. British Medical 320:301-04.

7) Health Canada (1997). Canada's Food Guide - FocChildren 6-72 years - Background for Educators andCommunicators. Minister of Public Works and GoveServices Canada. Cat. H39-308/1-1997e

8) htto://slrateais.ic.oc.ca/canadian Industry statistics/DE/cis311919defe.html

It would be useful to develop more robust definitions ofterms such as "Junk Food" and "Snack Food" as a m eansto defining exactly what foods would be targeted and why.

Continuing media discourse about food tax proposalsdoes provide an opportunity for dietitians to engage thepublic in discussions about the importance of healthy

eating and the role of public policy in supporting healthychoices.

9) Institute o f Medicine (2005) Food Marketing to ChildYouth: Threat or Opportunity? The National AcademPress, Washington D.C.

10 ) http://www.era-arc.gc.ca/E/oub/gm/4-3/4-3r-e.html

11) Lohman, J.S. (2002) Taxes on Junk Food.httD://www.coa.ct.oov/2002/olrdata/fin/rot/2002-R-10

12 ) Jacobson, M.F. and Brownwell, K.D. (2000) SmallSoft Drinks and Snack Foods to Promote Health, AmJournal of Public Health. 90 (6) 854-7.

Written by Paul Fieldhouse, PhD and reviewed by KimRaine, PhD, RD and Carmen Connolly.

13 ) Kuchler, F.; Tegene, A. , Harris, M. (2005) TaxingFoods: Manipulating Diet Quality or Financing InfoPrograms?. Review of Agricultural Economics, 27 (

©2006 Dietitians of'Canada, All rights reserved.May be reproduced for educational purposes. Dietitians of CanadaLes dietet/stes du Canada

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 5/164

THE INSIDE STORY

14) Sme d, S., Jensen, J.D., and Denver, S, (2005)

Differentiated Food Taxes as a Tool in Health and NutritionPolicy. Food and Resou rce Econom ics Institute,Frederiksberg.

15) Chouinard, H.H., Davis, D.E. LaFrance J.T. and Perloff,J.M. (2005) The Effects of a Fat Tax on Dairy Products.Working Paper 1007, Department of Agricultural andResource Economics and Policy. U. California.

16) Cash, S.B., Sunding, D.L. and Zilberman, D. (2005) FatTaxes and Thin Subsidies: Prices, Diet, and HealthOutcom es, Ada Aqriculturae Scandinav ica Se ction c: 2, 3-4: 167-174.

17) htto://www.vichealth.vic.aov.au/Content.asox?tooiclD=3

18) Caraher, M. and Cowbum, G. (2005) Taxing Food:Implications for Public Health Nutrition. Public HealthNutrition. 8 (8): 1242-9.

19) Heart & Stroke Foundation of Canada (2005) AddressingObesity in Canada: A Think Tank on Selected R esearchPriorities. Oct 6-7, Ottawa.http://ww2.heartandstroke.ca/Paae . asp?PaoelD-1613&ContentlD=2016a&ContentTvoelD=1

©2006 Die t i t ians o f Canada. A l l r igh ts reserved.May be reproduced fo r educat iona l purposes.

Dietitians of Canada

Les dietetistes du C anada

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 6/164

References

Ahmed, H. M. (2009). Obesity, fast food manufacture, and regulation: Revisiting opportunities for

reform. Food and Drug Law Journal, (54(3), 565-75.

Andrey eva, T., C haloupka , F. J., & Brovmell, K. D. (2011). Estim ating the potential of taxes on

sugar-sweetened beverages to reduce consumption and generate revenue. Preventive

Medicine, 52(6), 413-416. doi:10.l016/j.ypmed.2011.03.013

Andreyeva, T., Long, M. W., & Brownell, K. D. (2010). The impact of food prices on

consum ption: A system atic review of research on the price elasticity of dema nd for food.

American Journal of Public Health, 100(21 216-222. doi: 10.2105/AJPH.2008,151415

Braillon, A. (2012). Taxing "sin drinks": From economy to sugar con trol. Preventive Medicine,

54(3-4), 283-2 83.

Braun, J. L., & Heal, B. A. A. (2004). Obesity: Implications for health care society. Health Policy and

Economics, 2(1), 29-32.

Brow nell, K. D., Farley, T., W illett, W. C , Popkin, B. M., Chaloup ka, F. J., Thomps on, J. W., &

Ludwig, D. S. (2009). The pu blic health and econom ic benefits of taxing sugar-sw eetened

beverages. New E ngland Journal of Medicine, 361(16), 1599-1605.

doi: 10.1056/NEJMhpr0905723

Brownell, K. D., &. Frieden, T. R. (2009). Ounces of prevention—the public policy case for taxes

on sugared beverages. New E ngland Journal of Medicine, 360(18), 1805-1808.

doi:10.1056/NEJMp0902392

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 7/164

Brownell, K. D., & Ludwig, D. S. (2009, October 6). The soda-tax solution. Los Angeles Times, p. A23.

Buhler, S.> & Raine, K.. (2010). Reducing consumption of sugar-sweetened beverages: Does taxation have

a role?. Practice-Based Evidence in Nutrition, December 2010, 1-9.

BySes, 1. (2005, June 4) . 'Fat tax' on thin ice with researcher. The St. Albert Gazette, pp. 11-12.

California Center for Public Health Advocacy. (2002). Nutrition and Physical A ctivity for Children and

Adolescents. Davis, California: Author.

Caraher, M., 8c Coveney, J. (2004). Public health nutrition and food policy. P ublic Health

Nutrition, 7(5), 591-598.

Caraher, M , & Co wbu rn, G. (200 5). Taxin g food: Implications for pub lic health nutrition.

Public H ealth Nutrition, 5(8), 1242-1249.

Cash, S. B., Goddard, E. W., & Lerohl, M. (2006). Canadian health and food: The links between

policy, consumers, and industry. C anadian Journal of Agricultural Economics, 54(4), 605-

629. doi:httD://www.blackwellpublishing.comyiournal.asp?ref-0008--3976

CAS H, S. B., SUN DING, D. L., & ZIL BER MA N, D. (2005). Fat taxes and thin subsidies:

Prices, diet, and health outcomes. Acta Agricuiturae Scandinavica: Section C, Food

Economics, 2(3), 167-174.

Cawley, J. (2004). An economic framework for understanding physical activity and eating

behaviors. American Journal of Preventive M edicine, 27, 117-125.

doi:10.10l6/j.amepre.2004.06.012

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 8/164

References

Ahmed, H. M. (2009). Obesity, fast food manufacture, and regulation: Revisiting opportunities for

reform. Food an d Drug Law Journal, 64(3), 565-75.

Andreyev a, T., Chaloupk a, F. J., & Brow nell, K. D. (2011). Estimating the potential of taxes on

sugar-sweetened beverages to reduce consumption and generate revenue. Preventive

Medicine, 52(6), 413-416. doi:10.1016/j.ypmed.2011.03.013

Andreyeva, T ., Long, M . W., & Brownell, K. D. (2010). The im pact of food p rices on

consum ption: A system atic review of research on the price elasticity of dem and for food.;

American Journal of Public Health, 100(2), 216-222. doi:10.2105/AJPH.2008.151415

Braillon, A. (2012). Taxing "sin drinks": From economy to sugar control. Preventive Medicine,

54(3-4), 283-283.

Braun, J. L., & Heal, B. A. A. (2004). Obesity: Implications for health care society. Health Policy and

Economics, 2(1), 29-32.

Brown ell, K. D., Farley, T., Willett, W. C , Popkin, B. M., Chaloupka, F. J., Thomp son, J. W., &

Ludw ig, D. S. (2009). The public health and economic benefits o f taxing sugar-sweetened

beverages. New England Journal of Medicine, 361(16), 1599-1605.

doi: 10.1056/NEJMhpr0905723

Brownell, K. D., & Frieden, T. R. (2009). Ounces of prevention-the public policy case for taxes

on sugared beverages. New England Journal of Medicine, 360(1$), 1805-1808.

doi:l0.1056/NEJMp0902392

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 9/164

Brownell, K . D., & Ludwig, D. S. (2009, October 6). The soda-tax solution. Los Angeles Times, p. A23.

Buhler, S., & Raine, K. (2010). R educing consumption of sugar-sweetened beverages: Does taxation have;

a role?. Practice-Based Evidence in Nutrition, December 20 JO, 1-9.

Byles, I. (2005, June 4). 'Fat tax' on thin ice with researcher. The St. Albert Gazette, pp. 11-12.

California Center for Public Health Advocacy. (2002). Nutrition and Physical Activity for Children and

Adolescents. Davis, California: Author.

Caraher, M., & Coveney, J. (2004). Public health nutrition and food policy. Public Health

Nutrition, 7(5), 591-598.

Caraher, M., & Cowburn, G. (2005). Taxing food: Implications for public health nutrition.

Public Health Nutrition, 5(8), 1242-1249.

Cash, S. B., Goddard, E. W., & Lerohl, M. (2006). Canadian health and food: The Hnks between

policy, consum ers, and industry. Canadian Journal of Agricultural Economics, 54(4), 605-

629. doi:http://wAvw.blackweIlpublishing.comyiournal.asp?ref= :0008-3976

CA SH, S. B., SUN DING , D. L., & ZILBER MA N, D . (2005). Fat taxes and thin subsidies:

Prices, diet, and health o utcom es. Ada Aghculturae Scandinavica; Section C , Food

Economics, 2(3), 167-174.

Cawley, J. (2004). An economic framework for understanding physical activity and eating

behaviors. American Journal of Preventive Medicine, 27, 117-125.

doi:10.1016/j.amepre.2004.06.012

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 10/164

Centre for Science in the Public Interest. (2005). Testimony of: BillJeffery, LL.B. national coordinator of the

centre for science in the public interest. Pre-budget hearings. Ottawa, Ontario: Author.

Center for Science in the Public Interest. (2009). Taxing sugared beverages would help trim state budget

deficits, consumers' bulging waistlines, and health care costs. Washington, DC; Author.

Chaloupka, F. J., Pow ell, L. M., & Chriqui, J. F. (2011). Sugar-sweetened beverages and obesity

prevention: Policy recommendations. Journal of Policy Analysis an d Management, 30(3),

662-664. doi:http://www 3.mterscience.wilev.com.proxvl.lib.umanitoba.ca/cgi-

bin/ihome/34787

Chaloupka, F . J., Powell, L. M., & Chriqui, J. F. (2011). Sugar-sweetened beverages and obesity:

The potential imp act of public policies. Journal of Policy Analysis and Managem ent, 30(3),

645-655. doi:http://www3.interscience.wiley com.proxvhlib.umanitoba.ca/cgi-

bin/ihorne/34787

Chaufan, C , Hon g, G. H., & Fox, P. (2009). Taxing "sin foods" - obesity prevention and public

health policy. New England Journal of Medicine, 361(24), el 13-el 13.

doi: 10.1056/NEJMopv0909847

Chouinard, H . H., Davis, D . E., LaFrance, J. T., & Perloff, J. M. (2007). Fat taxes: Big money

for small change. Forum for Health Economics and Policy, 10(2)

doi:http://www.bepress.com.proxvl.lib.umanitoba.ca/fhep

Chouinard, H ., Davis, D., L aFrance, J., & Perloff, J. (2005). Th e effects of a fat tax on dairy

products. Unpublished manuscript.

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 11/164

Chriqui, J. F., Eidson, S. S., Bates, H., Kowalczyk, S., & Chaloupka, F. J. (2008). State sales tax

rates for soft drinks and snacks sold through grocery stores and vending machines, 2007.

Journal of Public Hea lth Policy, 29(2), 226-249. doi:10.l057/jphp.2008.9

Chronic Disease Prevention Alliance of Canada. (2011). Extra sugar, extra calories, extra weight, more

chronic disease: The case for a sugar-sweetened beverage tax. Ottawa, Ontario: Author.

Daniells, S. (2007, December 7). Fat tax - proposed again by academia, dismissed by industry. Food

Navigator USA. Retrieved from http://www.foodnavigator.com/Legislation/Fat-tax-proposed-again-b y-

academia-dismissed-by-industry

Dharmasena, S., & Capps, O., J. (2012). Intended and unintended consequences of a proposed

national tax on sugar-sweetened beverages to combat the U.S. obesity problem. Health

Economics, 2/(6), 669-694. doi:10.1002/hec.l738

Duffey, K. 1, Gordon-Larsen, P., Shikany, J. M., Guilkey, D., Jacobs, D., J., & Popkin, B. M.

(2010). Food price and diet and health outcomes: 20 years of the CARD IA study. Archives

of Internal M edicine, 170(5), 420-426. doi:10.1001/archinternmed.2009.545

Edwards, R. D. (2011). Commentary: Soda taxes, obesity, and the shifty behavior of consumers.

Preventive Medicine, 52(6), 417-418. doi:10.1016/j.ypmed.20l 1.04.011

Epstein, L. H., Dearing, K. K., Roba, L. G., & Finkelstein, E. (2010). The influence of taxes and

subsidies on energy purchased in an experimental purchasing study. Psychological Science

(Sage Pub lications Inc.), 2/(3 ), 406-414.

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 12/164

Faith, M. S., Fontaine, K. R., & Baskin, M. L. (2007). Toward the reduction of population

obesity: Macrolevel environmental approaches to the problems of food, eating, and obesity

doi:10.1037/0033-2909.133.2.205

Faulkner, G., Grootendorst, P., Nguyen, V.H., Ferrence, R., Mendelson, R., Donnelly, P., Arbour-

Nicitopoulos, K. (2010). Economic Policy, Obesity and Health; A Scoping Review . Toronto, .

Ontario: Exercise Psychology Unit.

Fieldhouse, P. (2006). Taxing food. Dietitians o f Canada, August 2006. Retrieved from

http://politiquespubliques.inspq.qc.ca/fichier.php/t46/DCTaxingFood.pdf

Fineberg, H. V. (2004). An economic analysis of eating and physical activity behaviors:

Exploring effective strategies to combat obesity doi:10.1016/j.amepre.2004.06.016

Finkelstein, E. A., Zhen, C., Nonnem aker, J., & Todd , J. E. (2010 ). Impact of targeted beverage

taxes on higher- and lower-income households. Archives of Internal Medicine, 170(22),

2028-2034. doi: 10.100l/archinternmed.2010.449

Finkelstein, E., French, S., Variyam, J. N., & Haines, P. S. (2004). Pros and cons of proposed;

interventions to promote healthy eating. American Journal of Preventive Medicine, 27, 163-

171.doi:10.1016/j.amepre.2004.06.017

Fletcher, J. M., Frisvold, D ., & Tefft, N . (2010). Taxing soft drinks and restricting access to

vending machines to curb child obesity. Health Affairs, 29(5), 1059-1066.

doi: 10 .1377/hlthaff.2009.0725

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 13/164

Fletcher^ J. M., Frisvold, D . E., & Tefft, N. (2011). Are soft drink taxes an effective mechanism

for reducing obesity? Journal o f Policy Analysis and Managem ent, 30 (3), 655-662.

doi:http://www 3.interscience.wiley.com.proxvl.lib.uniajiitoba.ca/cgi-bin/jhome/34787

Fletcher, J. M., Frisvold, D. E., & Tefft, N. (2011). The proof is in the pudding: Response to

chaloupka, pow ell, and chriqui. Journal of Policy Analysis a nd Manag ement, 30(2), 664-

665. doi:http://vAvw3.interscience.wilev.com.proxyl.lib.umanitoba.ca/cgi-biii/ihome/34787 :

Fletcher, J. M., Frisvold, D.} & Tefft, N. (2010). Can soft drink taxes reduce population weight?

Contemporary Economic Policy, 25 (1), 23-35. doi:http://www.blackwell-

svnergy.com.proxy l.lib.umanitoba.ca/loi/coep/

Food and Rural Economics Division, Economic Research Service. (2000). Estimation o f Food Demand and

Nutrient Elasticities from Household Survey Data (USDA Publication No. 1887). Washington, DC: U.S.

Government Printing Office.

Forshee, R. A. (2008). Innovative regulatory approaches to reduce sodium consumption: C ould a

cap-and-trade system work? Nutrition Reviews, 66(5). 280-285.

Frank, L. D. (2004). Economic determinants of urban form: Resulting trade-offs between active

and sedentary forms of travel. American Journal of Preventive Medicine, 2 7, 146-153.

doi:10.1016/j.arnepre.2004.06.018

Garson, A., J., & Engelhard, C. L. (2007). Attacking obesity: Lessons from smoking. Journal of

the American College of Cardiology (JACC), 40(16), 1673-1675.

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 14/164

Goncalvesova, E. (2011). Is a tax on junk food moving a step closer? European Heart Journal, 32 , 1823-

1831. doi: 10.1093/eurheartj/ehrl 84

Gonzalez-Zapata, L., Alvarez-Dardet, C , Millstone, E., Clem ente-Go mez, V ., Holdsw orth, M.,

Ortiz-Moncada, R. , . . . Horvath, K. Z. (2010). The potential role of taxes and subsidies on

food in the prevention of obesity in europe. Journal of Epidemiology & Community H ealth,

64(Z), 696-704. doi:10.1136/jech.2008.079228

Goodman C, Anise A (2006). What is known a bout the effectiveness of economic instruments to

reduce consumption of foods high in saturated ats and other energy-dense foods for preventing

and treating obesity? Copenhagen, WHO Regional Office for Europe (Health Evidence Network

report; http://www.euro.who.int/document/e88909.pdf, accessed 14 June , 201 2. ,

Harper, T. A., & Mooney, G. (2010). Prevention before profits: a levy on food and alcohol advertising.

The Medical Journal of ustralia, 192(7), 400-402.

Hill, J. O., Sallis, J. F.„ & Peters, J. C. (2004). Econ omic analysis of eating and physical activity:

A next step for research and policy change. American Journal of Preventive Medicine, 27,

111-116. doi:10.1016/j.amepre.2004.06.010

Holt, E. (2010). Romania mulls over fast food tax. Lancet, 375(9720), 1070-1070.

Holt, E. (2011). Hungary to introduce broad range of fat taxes. Lancet, 378(9193), 755-755.:

doi:10.1016/S0140-6736(l 1)61359-7

Jacobson, M. F. (20 09). Soft drinks: Time to tax. Nutrition Action Health Letter, 36(2), 2-2.

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 15/164

Kamerow , D. (2010). The case of the sugar sweetened beverage tax. BM J: British Medical

Journal (Overseas & Retired D octors Edition), 341(7765), 132-132.

Kim, D ., & Kaw achi, I. (2006). Food taxation and pricing strategies to 'T hi n out" the obesity

epidemic. American Journal of Preventive Medicine, 30(5), 430-437.

doi:10.1016/j.amepre.2005.12.007

ICnickman, J. R., & Orleans, C. T. (2004). Integrating economic thinking into research on the

dynamics of obesity: Challenges and opportunities doi:10.1016/j.amepre.2004.06.014

Kuchler, F., Tegene, A ., & H arris, J. M. (2005). Taxing snack foods: Ma nipulating diet quality

or financing information prog rams? R eview of Agricultural Economics, 27(1), 4-20.

doi:http://www.blackwellpublishing.com/iournal.asp?ref==l 058-7195

Kuchler, F., Tegene, A., & Harris, J. M. (2004). Taxing sn ack foods: What to ex pect for diet and tea

revenues, (USDA Publication No. 747-08). Washington, DC: U.S. Government Printing Office.

Laurance, J. (2009). Time for a fat tax? lancet, 373(9675), 1597-1597. doi:10.10l6/S0140-

6736(09)60893-X

Lin, B., Smith, T. A., Lee, J., & Hall, K. D. (2011), Measuring weight outcomes for obesity

intervention strategies: The case of a sugar-sweetened beverage tax. Economics and Human

Biology, 9(4), 329-341.

doi:http://www.elsevier.com/wps/fma7ioumaldescription.cws home/622964/description#de

scription

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 16/164

Lusk, J. L., & Schroeter, C. (2011). When do fat taxes increase consumer welfare? Health Economics, epub

ahead ofprint. DOI: 10.1002/hec.l789

Maddock, J. E. (2010). Soda taxes, obesity, and the perils of complexity. American Journal of

Health Promotion, 25(2), 91-91. doi:10.4278/ajhp.25.2.91

Magnusson, R. S. (2008). What's law got to do with it? part 2; Legal strategies for healthier

nutrition and obesity prevention. Australia & New Zealand Health Policy (ANZ HP), J, 1-17.

doi: 10.1186/1743-8462-5-11

Mann, J. (2004). Cutting the fat: How a fat tax can help fight obesity. Available fromhttp://www.ecologic.org.nz/

Marshall, T. (2000). Exploring a fiscal food policy: The case of diet and ischaem ic heart disease.

BMJ: British Medical Journal (International Edition), 320(1230), 301-304.

doi:10.1136/bmj.320.7230.301

McCoIl, K. (2009). "Fat taxes" and the financial crisis. Lancet, 373(9666), 797-798.

Mytton, O., Gray, A., Rayn er, M., & Rutter, H. (2007).- Could targeted food taxes improv e :

health? Journal of Epidemiology & Community Health, (57(8), 689 -694 .

Mytton, O., Clarke, D,, & Rayner, M. (2012). Taxing unhealthy food and drinks. BMJ: British

Medical Journal (Overseas & Retired D octors Edition), 344(1857), 30-33.

National Policy and Legal Analysis Network to Prevent Childhood Obesity. (2010). Findings for model

sugar-sweetened beverage tax legislation. Oakland, CA: Author.

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 17/164

Nederkoo m, C , H averm ans, R. C , Giesen, J. C. A. H., & Jansen, A. (2011). High tax on high

energy dense foods and its effects on the purchase of calories in a supermarket, an

experiment. Appetite, 5(5(3), 760-7 65. doi: 10 .1016/j.appet.2011.03.002

Nnoaham , K. E., Sacks, G., Rayner, M .. Mytton, O., & Gray, A. (2009). Modelling income

group differences in the health and economic impacts of targeted food taxes and subsidies.

International Journal of Epidemiology, 38(5), 1324-1333. doi:10.1093/ije/dyp214

Pomeranz, J. L. (2012). Advanced policy options to regulate sugar-sweetene d beverages to

support public health. Journal of Public Health Policy, 33(\), 75-88.

doi:10.1057/jphp.2011.46

Powell, L. M,, Chriqui, J., & Chaloupka, F. J. (2009). Associations between state-level soda

taxes and adolescent body m ass index. Journal of Adolescent Health, 45(3), S57-63.

POW ELL, L. M., & CH AL OU PK A, F. J. (2009). Food prices and obesity: Evidence and policy

implications for taxes and subsidies. Milbank Quarterly, 87(1), 229-257.

doi: 10.1111/j. 1468-0009.2009.00554.X

Pratt, M., Macera, C. A., Sallis, J. F., O'Donnell, M., & Frank, L. D. (2004). Economic

interventions to prom ote physical activity: Application of the SLOT H mode l. American

Journal of Preventive Medicine, 27, 136-145. doi:10.1016/j.amepre.2004.06.015

Roehr, B. (2009). US "soda tax" could help tackle obesity, says new director of public health.

BMJ: British Medical Journal (Overseas & Retired Doctors Edition), 339, b3176-b3176.

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 18/164

Roehr, B. (2010). Taxing junk food reduces consumption and improves health outcomes, finds

20 year study. BMJ: British M edical Journal (Overseas & Retired D octors Edition),

340(7146), 557-557.

Rudd Report. (2009, fall). Soft drink taxes: A policy brief. Rudd Center or Food Policy and Obesity.

Retrieved from

http://www.va]eruddcenter.org/resoiirc&s/upload/docs/what/reports/RuddReportSoftDrinkTaxFall2009:pd

f

Rutledge, K., & Raine, K.. (2005). Economic incentives and disincen tives for healthy eating a nd physical

activity; A summary o f evidence. Edmonton, AB: Author?.

Sacks, G., Veerman, J. L.. Mo odic, M., & Swinburn, B. (2011). Traffic-light' nutrition labelling

and 'junk-food' tax: A modelled comparison of cost-effectiveness for obesity prevention.

International Journal of Obesity, 35(1), 1001-1009. doi: 10.103 8/ijo.2010.228

Schroeter, C, Lusk, J., & Tyner, W. (2008). Determining the impact of food price and income

changes on body weight. Journal of Health Economics, 27(\), 45-68.

doi:http://vvvvvv j.elsevier.com/wps/find/iournaldescription.cws home/505560/description#de

scription

Schroeter, C , Lusk, J., & Tyner, W. (2005). Determining the impact of food price and policy changes\on

obesity. Indiana: Purdue University.

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 19/164

Scott-Thomas, C. (2009, September 1). Illinois raises taxes on candy and soft drinks. Food Navigator USA.

Retrieved from http://www.foodnavigator-usa.com/Regulation/IUinois-raises-taxes--on-candy~and--soft-

drinks

Seeman, N., & Luclani.P: (2002). The economics of fat. FraserF'orum.

Shue, B. K. (2009). The price of soft drinks. Journal o f the California Dental Association, 57(11), 757-

758.

Smed, S., Jensen, J. D., & Denver, S. (2005). Differentiated food taxes as a tool in health and nutrition policy.

Food and Resource Economics Institute, volume number, 1-15.

Smed, S., Jensen, J. D., & Denver, S. (2007). Socio-economic characteristics and the effect of

taxation as a health policy instrument. Food Po licy, 32(5-6), 624-639.

doi:httrJ://www.elsevier.com/wps/find/iournaldcscription.cws home/30419/descrimion#desc

ription

Standing Committee on Health. (2006). Evidence HESA Publication No. 019). Ottawa, ON: Canadian

Government Printing Office.

Strnad, J. (2005). Conceptualizing the "fat tax ": The role of food taxes in developed econom ies. Southern

California Law Review, 78, 1221-1326.

Sturm, R., Powell, L. M., Chriqui, J. F., & Chaloupka, F. J. (2010). Soda taxes, soft drink

consumption, and children's body m ass index. Health Affairs, 29(5), 1052-1058.

doi:10.1377/hlthaff.2009.006l

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 20/164

Sturm, R. (2004). The e conom ics of physical activity; Societal trends and rationales for ,

interventions. American Journal of Preventive Medicine, 27, 126-135.

doi:10.l016/j.amepre.2004.06.013

Sugarman, S. (2009). No more business as usual: Enticing companies to sharply lower the pubjic

health costs of the products they sell. Public Health (Elsevier), 123(3), 275-279.

doi:10.1016/j.puhe.2008.12.020

The Retail Sales Tax Act of Manitoba. (2003). Food and beverages (C.C.S.M. Publication N o. 029).

Winnipeg, Manitoba: Canadian Government Printing Office.

Thow , A. M., Quested, C , Juventin, L., Kun, R., Khan, A. N ., & Sw inbum , B. (2011). Taxing

soft drinks in the pacific; Impleme ntation lessons for improving he alth. Health Promotion

International, 26(\\ 55-64. doi:10.1093/heapro/daq057

Tiffin, R., & Arnoult, M . (2011). The public health impacts of a fat tax. European Journal of.

Clinical Nutrition, 65(4), 427 -433 . doi:10.1038/ejcn.2010.281 ' |

Tiffin, R., & Salois, M. (2012). Inequalities in diet and nutrition. Proceedings of the Nutrition-

Society, 7/(1), 105-111.

Tortolero, S. R., Popha m, K ., & Jacobson, P. D. (2009). Improving information on public health

law best practices for obesity prevention and control. Journal of Law, Medicine & Ethicsl

37(2), 99-109. doi;10.11H/j.l748~720X .2009.00396.x

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 21/164

Vartanian, L. R., Schw artz, M, B ., & Brownell, K. D. (2007). Effects of soft: drink consumption

on nutrition and health: A systematic review and meta-analysis. American Journal of Public

Health, 97(4), 667-675. doi:10.2105/AJPH.2005.083782

W ang, Y., C , Coxsom P ., Shen, Y., Goldm an, L., & Bibbins-Dom ingo, K. (2012). A penny-per-

ounce tax on sugar-sweetened beverages would cut health and cost burde ns of diabetes.

Health Affairs, 31(1), 199-207. doi:10.1377/hlthaff.2011.0410

Waterlander, W. E., Steenhuis, I. H., de Boer, M., Schuit, A. J., & Seidell, J. C. (2012).

Introducing taxes, subsidies or both: The effects of various food pricing strategies in a web-

based supermarket randomized trial. P reventive M edicine, 54(5), 323-330.

Wilson, N. (2007, August 28). The best recipe? Combining food taxes with subsidies on healthy foods

[Review of the article Could targeted food taxes improve health?]. Journal o f Epidemiology Community

Health. Retrieved from http://jech.bmj.eom/content/6l/8/689.abstract

Winkler, J. T. (2010). Tax on sugared drinks, how to raise the prices of unhealthy foods. BMJ:

British Medical Journal (Overseas & R etired Doctors Edition), 341, c4177-c4177.

doi:10.1136/bmj.c4177

Yach, D. (2008). The role of business in addressing the long-term implications of the current food crisis:.

Globalization and Health, 4. doklO.l 186/1744-8603-4-12

Yaniv, G.> Rosin, O., & Tobol, Y. (2009). Junk-food, home cooking, physical activity and

obesity: The effect of the fat tax and the thin subsidy. Journal of Public Econom ics, 93(5-6),

823-830. doi:http://www.elsevier.com/locate/inca/505578/

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 22/164

No author. (2007). Proceedings from the Wingspread Conference Center '07: Potential Policy and Research

Options for Making U.S. Food an d Agricultural Policy Serve Public Health Goals. Racine, Wisconsin.

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 23/164

• At present, 25 states impose small taxes on soda and other beverages with addedsugar.

• A 2009 report/from the Center for Science in the Public Interest, Taxing SugaredBeverages Would Help Trim State Budget Deficits, C onsumers' Bulging W aistlines,and Health Care Costs outlines the health and fiscal benefits of a soda tax,

• President Barack Obam a has lent his support for a soda tax wh ich could benefit

children's health and the nation's wealth. "I actually think it's an idea that we shouldbe exploring. There's no doubt that our kids drink way too much soda."

• A January 2010 CBS New s opinion poll found that 60 % of those surveyed opposeda junk foo d tax.

In ternat ional• Romania will become the first country in the world to introduce a tax on junk food.

The new tax will apply to individuals or organizations that produce, import or processfood with a high content of salt, fats, sugar and additives. The new tax, to beintroduced in March 2 010, will be used for health programs in the coun try. Theministry justified its proposal stating that a significant number of people in Europesuffer from obesity, increasing the risk of diabetes, hypertension a nd premature

death due to u nhealthy food.• Taiwan is considering similar action. The Bureau of Health Promotion is drafting a

bill to levy the special tax on food deeme d unhealthy, such as sugary drinks, candy, .cakes, fast food and alcohol. Revenue from the tax would finance groups promoting |health awareness or subsidize the national health insurance prog ram. If approved itwou ld come into effect next year.

Mi lk Subs id ies• In 2008 a milk subsidy proposal wa s introduced in the NWT legislature, with an

estimated cost of $1.0 - $1,5million per year. This was not successful.• Milk is an eligible product in the Federal Food Mail progra m, wh ich serves some

Manitoba communities. This program has recently been comprehensively reviewed

anplafinaj report is pending.

H ( I ) (b) i t )

• The"N'orthe7hTlealthy Food" Initiative [RRF l] was established as an interdepartmentalgovernment response to the N orthern Food Prices Report, and continues to operateunder the leadership of AN A. HLYS , MH, MA FRI, HCMO an d Conservation are thepartner departm ents. Northern Healthy Food Initiative was given a mand ate to

pursue a limited number of priority items from the report, with a focus on remotecomm unities. The items identified above were not part of the m andate.

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 24/164

ADVISORY NOTE FOR MINISTER OF HEALTHY LIVING, YOUTH & SENIORS

Type: Dec is ion X Discuss ion In form at ion D

In i t ia ted by : Min is ter X DM D ADM Branch

Div is ion /B ranch : Healthy Living & Popu lationsTit le: Junk Food LevyDate: January 27, 2010AIMS Log Number : HLYS 10-00090

H M(0 M

»(0M (0

w(i)U)(\)

Current S ta tus :

Junk Food Tax

Canada

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 25/164

f

C e r q u e i r a , E l i za b e t h ( H L S C A )

From: Fieldhouse, Paul (MHHL)Se nt: March-10-10 2:44 PMTo: Robertson, Mark (MHHL)Su bje ct: FW: Media request: Soda tax/junk food taxAtta ch m en ts: pf taxing food dc currentissues.pdf

Hi Mark - for your considerat ion and forwarding as appropr iate.

. _ comments w ere acc urate : th is is a complex issue th a t has been the su bject of much

and ongoing debate over everything f rom the concept i tsel f to implementat ion to potent ia l outcomes.

Th e de pa rtm ent o f He althy L iv ing, Seniors and Youth [previously H ealth and Hea lthy Liv ing] has

previously undertaken some internal analysis of the issue, and cont inues to monitor developments.

There is a considerable amount of l i terature on th e topic - b oth academ ic and popular commentary -

th a t can be read i ly accessed. [An examp le is attached. Please note this doe s not represent the views of

the department - M ark - I d on't know if you want to include th is or no t. I t is th e Cu rren t Issue s paper

I d id for DC in 20 06 : no dep ar tm ent a f f i l ia t ion is given]

Promo t ion of heal thy e at ing at school has been a major th ru st in th e last few ye ars. The Man itoba

Publ ic Schools Act requires that al l publ ic ly funded schools in Manitoba have a wr i t ten nutr i t ion pol icy.

Governm ent has provided a range of supp orts to schools to help the m achieve th is , such as handbooks,

gu ide l ines, workshops and a to l l - f re e l ine. In fo rm at io n on th is in i t ia t ive can be found at

h t tp :/ /www.qov .mb.ca /hea l thvschoo ls /food inschoo ls / index .h tm l

Government o f Ma nitoba con tr ib ute s funding support fo r school nour ishm ent program s, such asbre ak fas t and snacks, thro ug h th e Chi ld Nu t r i t io n Council o f Mani toba.

The Nor thern Heal thy Food In i t ia t ive is an in terdepar tmenta l in i t ia t ive led by Abor ig ina l and Nor thern

A f f a i r s th at works w i th no r th ern reg iona l par tners to increase access to a f for da b le nu t r i t ious food in

northern and remote communit ies. Projects include gardening, greenhouses, smal l l ivestock product ion,

f re ez er loan pro je cts and school cur r icu lum.

Nutr i t ion programs are also del ivered by RHAs and other heal th agencies and non-government

organisat ions

Dr. Paul FieldhouseNutrition Policy <5 Research AnalystHealthy Living, Youth and Seniors300 Carlton St.Winnipeg, ManitobaCanada R3B 3M9

Phone 2 4 786 735

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 26/164

Fax 204 948 2366

Email [email protected]

i

Confidentiality Notice: This message and any attachment to it are intended for the addressee only and maycontain legally privileged or confidential information. A ny unauthorized us e, disclosure, distribution, orcopying is strictly prohibited. Please notify the sender if you have received this E-mail by mistak e, and p leasedelete it and the attachm ents (and all copies) in a secure manner. Thank you.

Message de confidentialite : Ce m essage et tout document dans cette transmission est destine a la personne oaux personnes a qui il est adresse\ II peut contenir des informations privileg iees ou confidentielles. Touteutilisation, divulgation, distribution ou copie non autorisee est strictement defendue. Si vous n'etes pas ledestinataire de ce cou rriel, veuillez en informer I'expediteur et effacer l'original (et toutes les pieces jointe s) demaniere securitaire. Merci.

2

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 27/164

THE INSIDE STORY

Tax ing Food

Summary Overv iew

Over the past few years there has been increasinginterest in nutrit ion advocacy circles and in the popularpress about the idea of a so-called "fat tax", "junk food

tax" or "snack tax". In this review I will address severalbasic issues connected to small taxes on food includingtheir intended purpose, how they work, pros and cons andimplications for dietetic practice.

Ba c k g r o u n d

The concept of a small tax on selected food products isrooted in two big ideas. Firstly, strong scientif ic evidencethat links diet to chronic disease, together with, concernsover the increasing prevalence of obesity has fuelled callsfor strategies to reduce intakes of dietary fat, sugar, saltand overall food energy (1). Secondly, as food costs areimportant factors in consumer food choice, it is thought tobe possible to change eat ing behaviour through theapplication of economic levers. The two ideas intersect inthe fact that energy dense foods are amongst the leastcostly of foods (2).

In 1994, Dr. Kelly Brownell of Yale University suggestedtaxing unhealthy foods, a proposal that was quicklylabelled "the Twinkie Tax" and ridiculed by opponents (3).Since then several types of small taxes on food havebeen proposed, the most common of which are styled:"Junk food tax"; "Fat tax"; and "Snack Tax". An alternativeeconomic strategy, the applicat ion of subsidies to healthyfood choices, is beyond the scope of this discussion (4).

Def in i t ions

The terms "junk food tax", "fat tax", or "snack tax", lackcommon clear definit ions. "Junk food" is more of aconceptual category than it is a nutrit ional one, althoughthe term is widely used as sh orthand to refer to some or

all of high fat or sugar snack foods, fast foods, soft drinksand candy (5). "Fat tax" embraces a variety of schemes totax foods based on their total fat content, or specificallythe saturated fat or trans-fat component. For exampleMarshall suggests that products could be taxed if theyraised cholesterol concentrations but be exempted if the

"ratio of polyunsaturates to saturates (and trans fattyacids) were more favourab le" (6). Targeting fpods fortaxation bas ed o n their fat (or indeed , other [nutrient)content provides a clearer nutrit ional criterion than that ofjunk-food / non junk food. "Snack food", like "junk-food", isa more ambiguous conce pt. For example, Health Canadarefers to snack foods "like potato chips and pretzels" butalso to the con cept of healthy nutritious snacks jfrom thefood groups (7), while examples from Industry Canada ofwhat are considered as snack food include cheese curls,popcorn, corn chips and potato chips (8).

Why a tax?

Advocates identify two potential positive outcomes ofdifferentiated food taxes. The first is the potential forprompting changes in individual eating behaviour that areconsistent with current nutrit ional advice on healthy eatingand that will contribute to changes in populationconsumption patterns leading to reduced levels of obesityand chronic disease. This rationale is generallyifavouredby public health groups and consumer health lobbies andis often proposed as part of a broader comprehensivehealth promotion/public health strategy, cit ing theexperience of cigarette taxation as a component of acomprehensive tobacco control strategy (9). The secondoutcome is revenue generation that could be directed to

support nutrit ional health promotion programs.' For thisreason, some crit ics who doubt the likeliness of the firstoutcome ne vertheless support such taxes.

©2006 Diet it ians of Canada. All r ights reserved.May be reproduced for educational purposes.

Dietit ians of CanadaLes dietetistes du Canada

1/4

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 28/164

THE INSIDE STORY

Opt ions for tax in tervent ion

Taxes on food may be applied at the retail level in theform of general or targeted sales taxes. In Canada, foodis already differentially taxed through the Goods andServices Tax (GST) and Provincial Sales Tax (PST).Foods and beverages subject to GST are listed byCanada Customs (10). There is, arguably, a high degreeof congruency between what is in this l ist and what wouldbe likely to be on a "junk food" or "snack food" tax list. Anumber of states from the United States of America haveat different times experimented with levying special taxeson soft drinks and specific snack foods or have excludedthese products from tax exemptions given to foodproducts (11).

There are also options for levying taxes at differentstages in the food system. Approaches tried in the U.S.include:

» Manufacturers tax - payable on production volume (e.g.soft drinks or syrups) or as a percentage of salesrevenue, andWholesalers and distributors tax - payable on amountof product sold.

In several jurisdictions these types of taxes weresubsequently repealed due to industry lobbying andthreats to commercial development (12).

on total fat, saturated fat or sugar could have an impact

on consumption of fats, sugars and overall calories forsome groups , although with no "particularly advantageouseffects" for the socio-demographic groups amongst whichobesity and unhealthy diets are of the most concern (14).The authors suggest that combining economicinstruments with public information campaigns may be afruitful aven ue for furthe r exploration . A U.S. study thatattempted to simulate the effects of a fat tax on dairyproducts concluded that a 10% tax on fat content had littleimpact on the quantity of dairy products consumed by anygroup, though there was an overall predicted 1.4%reduction o f average , total fat intake (15). O therresearchers have proposed combining taxation of lesshealthy options with subsidies for healthier alternativessuch as fruits and vegetables, as a potentially more

effective strategy in improving diet quality and healthoutcomes (16).

Food taxes would almost certainly raise revenues. TheUSDA analysis cited above estimated that a 1% tax onpotato chips translates into twenty seven million dollars ofrevenue that could be spent on education programs.Governments are often reluctant to allocate specificrevenue streams to specific purposes. A notableexception is VicHe alth - a very succes sful Australianhealth promotion foundation supported through tobaccotaxes (17). More often, monies go into general revenuesfrom where they are reallocated according to changingneeds and government priorities.

Would junk food taxes be ef fect ive?

While there have been few attempts to demonstrate theactual impact of such taxes with real world examples,several recent economic modelling studies haveattempted to gauge the likely impact of such taxes, takinginto account factors such as current levels ofconsum ption, price elasticity and substitution strategies. AUnited States Department of Agriculture (USDA) modelsuggests that "small" taxes on snack foods would beineffective in changing patterns of consumption and wouldhave little impact on diet quality or heath outcomes (13).Even a 20% tax on salty snack foods would result in onlya 4-6 ounce reduction in annual per capita consumption.Moreover, as the authors point out, there is no guaranteethat any consumption changes prompted by such taxeswould be nutritionally be neficial.

An analysis carried out for the Danish Food and ResourceEconom ics Institute indicated that differential taxes base d

It should be noted that food taxes are regressive in naturesince they disproportionately affect lower incomepopulations where a higher percentage of income is spenton food. Modelling the distributional effect of hypotheticaltaxes on saturated fat, monounsaturated fat, sodium andcholesterol using data from the National Food Survey, arecent United Kingdom analysis showed that the poorest2% of people would pay 0.7% of total income on a fat tax,while the richest group would pay only 0 .1 % of totalincome (18).

Implementat ion issues

if the idea of a "junk food", "snack food" or "fat tax" ga inedpolitical and public support, there would be at least twokinds of implem entation c hallenges to address. The first isin deciding what to tax. It is difficult to link specific foods tospecific health impacts so the idea of tax on specific foodand beverage products runs counter to the message thatit is overall dietary intake that matters. There would haveto be broad agreeme nt on the part of policy m akers,

©2006 Dietitians of Canada. All rights reserved.

May be reproduced for educational purposes.

Dietitians of Canada

Les dietettstes du Canada

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 29/164

ISSUESTHE INSIDE STORY

practitioners and industry on what constitutes "junk-food"

or "snack food" and therefore is taxable.

The second challenge recognises the complexity ofadministering a differential retail tax. Given that newproducts are constantly appearing on the market, and thatmanufacturers may change product specifications, acontinual monitoring, evaluation and classification systemwould be required. Retailers would need to adopt newtechnologies and/or accounting systems to charge thetax, and tax remittance and collection systems wouldhave to be developed. Restaurants would be faced withan even more complex task. It may be that tax levies atthe manufacturer or distributor level would be relativelyeasier to administer and would underline the idea thathealthier choices are an industry as well as consumerresponsibil ity. In either case, both producers andconsumers would likely bear a share of the costs.

References:

1) Shields, M. (2005) Overweight Canadian children andadolescents, Nutrition; Findings from the CanadianCommunity Health Survey. Statistics Canada.http://www.statcan.ca/enQHsh/research/82-620-MIE/2005001/articles/chiid/cobesitv.htm

2) Drewnowski, A. (2003) Fat and Sugar: An EconomicAnalysis. Journal of Nutrition, 133S, 838S-840S.

3) Brownell, K.D. (1994) Get Slim With Higher Taxes"New York Times, Op-Ed., Dec. 15th.

4) Jeffery, R.W ., French, S.A., Raether, C. an d Baxter,

J.E. (1994) An Environmental Intervention toIncrease Fruit and Salad Purchases in a Cafeteria,Preventive Medicine, 23, 6: 788-92.

Impl icat ions for d ie te t ic pract ice

While economic incentives and disincentives are apotential addition to the array of public policy instrumentsavailable to encourage healthy eating, there is as yet noclear cut empirical evidence on which to judge the meritsof junk food or similar taxes. The Institute of Medicineconcludes that there is insufficient evidence torecommend either for or against taxing these foods, while

a recent Canadian think-tank on addressing obesityconcluded that the relationship between economicpolicies such as the role of tax incentives anddisincentives and their influence on eating behaviours ispoorly understood and requires further research (19).

5) CDC School Health Policies and Programs Study(2000) Fact Sheet: on Foods and Beverages Soldoutside of School Meal Programs.httD://www.cdc.QOv/HealthvYouth/shDDs/factsheets/D df/outside food.odf

6) Marshall, T. (2000) Exploring a fiscal food policy: the caof diet and t'schaemic heart disease. British Medical Jour320: 301-04.

7) ^Health Canada (1997). Canada's Food Guide - Focus on

Children 6-12 years- Background for Educators andCommunicators. Minister of Public Works and GovernmenServices Canada. Cat. H39-308/1-1997e

8) http://strateqis.ic.gc.ca/canadian industry statisths/cis.nsfDE/cis311919defe.html

It would be useful to develop more robust definitions ofterms such as "Junk Food" and "Snack Food" as a m eansto defining exactly what foods would be targeted and why.

Continuing media discourse about food tax proposalsdoes provide an opportunity for dietitians to engage thepublic in discussions about the importance of healthyeating and the role of public policy in supporting healthy

choices.

9) Institute o f Medicine (2005) Food Marketing to Children aYouth: Threat or Opportunity? The National AcademiesPress, Washington D.C.

10) htto://www. era-arc, oc. ca/E/oub/gm /4-3/4-3r-e.html

11) Lohman, J. S. (2002) Taxes on Junk Food.htto://www.caa.ct.oov/2002/olrdata/fin/rot/2002-R^.100 4.htm

12) Jacobson, M.F. an d Brownwell, K.D. (2000) Small Taxes Soft Drinks and Snack Foods to Promote Health, AmericaJournal of Public Health. 90 (6) 854-7.

Written by Paul Fieldhouse, PhD and reviewed by KimRaine, PhD, RD and Carmen Connolly.

13 ) Kuchler, F. ; Tegene, A. , Ham's, M (2005) Taxing SnacFoods: Manipulating Diet Quality or Financing InformationPrograms?. Review of Agricultural Economics. 27 (1) 4-2

©2006 Dietitians of Canada. All rights reserved.

May be reproduced for educational purposes.

Diet i t ians of Canada

Les d ie t& t is tes du Canada

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 30/164

CURRENT ISSUETHE INSIDE STORY

14) Smed, S., Jensen, J.D., and Denver, S. (2005)Differentiated Food Taxes as a Tool in Health and NutritionPolicy. Food and Resource Economics Institute,Frederiksberg.

15) Chouinard, H.H., Davis, D.E., LaFrance J.T. and Perioff,

J.M. (2005) The Effects of a Fat Tax on Dairy Products.Working Paper 1007, Department of Agricultural andResource Economics and Policy. U. California.

16) Cash, S.B., Sunding, D.L and Zilberman, D. (2005) FatTaxes and Thin Subsidies: Prices, D iet, and HealthOutcomes, Acta Aariculturae Scandinavica Section c; 2, 3-4:167-174.

17) httD://www.vichealth.vic.aov.au/Content.asDX?tQDiclD=3

18) Caraher, M. and Cowburn, G. (2005) Taxing Food:Implications for Public Health Nutrition. Public HealthNutrition, 8 (8): 1242-9.

19) Heart & Stroke Foundation of Canada (2005) AddressingObesity in Canada: A Think Tank on Selected R esearchPriorities. Oct 6-7, Ottawa.htto://ww2.heartandstroke.ca/Page.aso?PaaelD=1613&ContentlD=20169&ContentTvoelD=1

©2 0 0 6 D ie t i t i a n s o f Ca n a d a . A l l r i g h t s r e se r ve d .May be reproduced fo r educat iona l purposes.

Diet i t ians of Canada

Les d ie te tis tes du Canada

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 31/164

Manitoba

Re q u e s t f o r Ba c kg r o u n d e r Co r r e sp o n d e n ce Un it

1074- 300 Carlton Street

Phone: 788-63 56 - Gai l Wiggins

Date: Nov 28 2008 Fax: 947-9314

Minister ia l Log # ; HLIVM08--03650

Cl ient Name:

Context : (background)

v " -J e-mai led the p re m ie r- which was referred to Minister Osw ald, suggest ing a'Lard-Ass Tax' to pay for recruitment of addit ional health care workers. {A response tothis recruitment issue is being prepared separately by Workforce}

. roposes taxing 'unhealthy foods' and removing PST on i tems that encouragegood health and fitness.

Current S ta tus:

The issue of food taxes has been, and cont inues to be, d iscussed by governments andacadem ic rese archers, in Canada and internat ionally , over the past decade .

Most recently in Can ada, food taxes were one of the issues con sidered by the S tandingCommittee on Health of the House of Commons, dur ing an examinat ion of chi ldhoodobesity .

In the department, Dr. Paul Fieldhouse has made a particular study of the issue of junkfood taxes. A recent article is attached for information.

Currently there is only, at best, weak evidence that junk food taxes would be effective inachieving pub l ic health goals of in f luencing food choices. Such taxe s would certa in lyraise revenue - wh ich could potentially be targete d to other healthy eating program s -

and could have a symbolic value. Most studies have considered the impact of tax ratesof up to 30%. I t has been show n, even with smal l taxes, that the effect would beregressive - that is,-there would be a greater economic impact on lower incomeconsumers .

It is well known that the cost of fruits and vegetables is higher per 100kcaloriesthanhigh fat and sugar products, and that high costs of healthy foods is one barrier to

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 32/164

healthier eating. The re is evide nce to suggest that lowering the relative cost of healthierfood choices may be more effective than taxing ' junk foods'.

Providing tax relief or other form s of subsidy on health-prom oting good s and activit ieshas been considered. Current examples of relevant init iatives include the low-costchildren's bike helmet cam paign that the departme nt has sponso red for the last 3 years- providing over 42,00 0 b ike helmets at very low cost and many for no cost, and the$500.00 annual child f itness credit provided by the provincial government, which

matches the federalcredit to support children involved in activity programs.

Caut ionary Notes :

Junk food taxes co ntinues to be a topic of discussion in nutrit ion policy circles in

Recommended Response :

Provide information as above.Enclose copy of attachment if desired.

Prepared by : Dr. Paul FieldhouseTelephone: 786 7350

Please l is t s ta f f who m ust rev iew le t ter before i t goes in for s ignature:

Dr. Paul FieldhouseMr. Mark RobertsonM s. Marie O'Neill

Return to CU by ( leave b lank) :

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 33/164

Does the taxman have a role innutritional health?

Dietitians of Canada

Annual Conference

Vancouver

June 2007

Dr. Paul Fieldhouse

Manitoba Health & Healthy Liv ing

University of Manitoba

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 34/164

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 35/164

Food taxes - a

TWROUCYPODCAST

Br i t i s h Co l u m b i a Se l ec t

S t an d i n g C o m m i t t ee o nHeal th 2006

" Investigate the feasibi l i ty ofnew junk food taxes on non-

nutri t ive foods and beverages"

pirited discourse

• Tax jun k food to fightobes ity: CMA head• Canadian Press

• W edn esda y, March 22, 2006

nzherald .co.nz

Push for tax on junk food salesI2 :00AM Thurs day August 07 ,2003By Martin Johnston

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 36/164

DIFFERENTIATED FOOD TAXES AS A TOOL IX

HEALTH AND XUTRITION POLICY

The Effects of a Fat Tax on Dairy Products

lIiG Oh '} ' " " ^ n - ^* * / ,

"HayleV"HrChotUitafdDavid E. Davis "

Jeffrey T . LaFrancc "JeffievM. Pe-rloff''

Siane Smed* Jorgeai Dejgaavtl .Uewseit niul Sigrid DenverFood and Resource Economics Institute, KVL

Rolighedsvej 25BK-195S Frederiksberg C

E-mail: sjaaifc^foidk, iorge& afoidk

^^W ^" * « i f tS , 0

*f t

< ? *

C&O

T o ,

H,<wtf*

IN L C O N O M I C S O l :

u r r e n t I s s u e s

«*>/'/.,

- > , , ,

* * ./ t o . °

E: culture Information 8 uM n N B 747*08

1-"()(.)U M A K K E I ' S

AUBU' tJWW

" W *»#,* %

Taxing Snack F ood s: Wh at to E xpec t forD ie t and Tax Reve nues

THE INSIDE STORY

An Economic Analysis of Eat ing and Physical Act ivi ty

B e h a v i o r sExploring Effective Smri-e-gle.s to C>>ml>at Obesity

I I . t f t v v V I'iMflx-W. M i l . 1'liLJ

Taxing Food

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 37/164

Economics as ain

choice

Cost is secondbehind taste/quality / freshness

Food expenditureincreases withincome

A v e r a g e w e e k l i y e x p e n d r t u r e p e r p e r s o n o nm e s- 't an ir si nt s a n d f o u r m afc n- f o o d c a t e g o o e s b y

h o u s e h o l d i ri oo rrr ae g i r o u p

A v e r a g e w e e k l y 3

2 0

-15

I O

5

0

L e s s C h a n $ 2 0 , 0 0 0

EO $ 2 G , 0 0 D t o $ 7 9 , 9 9 9$ 6 0 , 0 0 0 o r m o r - e

Restaurants Meatand f ish

Fini te andvegetables

Dai iyp roduc tsand eaas

Bakeryand crthe r

cerealp roduc ts

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 38/164

% income spent onfood inversely relatedto total income

% i n c o m e o n f o o d at h o m e 2 0 0 5

6 0 -;

5 0 ;

4 0 I

3 0

2 0 -

1 0 '-.

0 4 -

l"'l: 1

C .2 < ; expenditure

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 39/164

03 m

5 3

oZx03 Q _

" D CDCD Z J

CD- * »

OoQ .

O Tl

S °D O- ! Q .I—H

i =•CD O

C D

(I)

O=r03Z5

CQCD

Percentagechancje =? Q

_j> _ s N J U J 4^ -

o o o o o o

Fresh fruits andvegetables

Total fruits andvegetables

Ce-real andbakeiy

Daiiry

:'Red meats

Poultry

[Sugar and sweets

If at s and oils

SSL Qa. c£

5" 5'

o

to1rooOo

I Soft drinks

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 40/164

dnoj6-9ixioo=ui Aq saue/v A |p i| t© |g •

o p # | 9 u i a A i f i p j p o oj j € | p u » l y i Q *

JB9Uj|jo u pu eiue p pue eoud uosM^eq d!qsuo r|B|9^ .

pueuiep jo A;!0!|SB|3

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 41/164

TypesoJ ecanxSnix

• Taxes• Taxowdits

• Subsidies- Consumer

- Producer

• Pricipfl ilisiteg ies - p

• Coupons/discounts

.o.p.

etc

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 42/164

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 43/164

Taxation & Public Policy

Efficiency in meeting public policy goal

Legal and financial impacts

Economic efficiency

Fairnessimplicity

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 44/164

Rationale for

• Change consumerbehaviour

• Generate revenue

- Use for targeted

programs

• Symbolic / catalytic

taxes on food

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 45/164

Perverse outcomes

• Regressive nature of impact

• No guarantee of 'healthier'alternate choices

• Reduction of revenue

• Competitiveness

• Black markets

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 46/164

Deciding what to tax

• Categories of food commodities- Definitions

- Drawing the line

• Nutrient content

-Which nutr ient /s?

- Both good and bad

- Single food focus

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 47/164

Tax

• Consumer

• Manufacturer

• Distributor

ilicy options

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 48/164

Canada R evenue Agency / Manitoba Finance

GST/HST M emoranda Seriesm**m*

4.3 Bii-stc Groceries January 2007

Thr. memorandum piovide r. de:.iitetl in fc-.mn lien -:n ierc»-»a:ed b.v.ic sioceiy product'. .i% thevielate to (he sow h aari ien.jce'. o>: i.unionized ;a\i\ tax-GST HST> provision* of ihe Excise T.vAcruh.vA.ci).

Hole Tin:, uiHu cuc i i t i i isp la^s ; GVT Hi I MiiucixiKkuM - i j . J ^ w Gi9ee>ia. 4J3i«iNweinbei iS ?- . Due IOIIW uuuib?! of

l ev i v i w. . lie caaagej Ims aoi l>e*u rifle-tuned Tt:v nseiao taud its tacrcpo u'.a; poiiey -.litiaienK ?-?SR tin iuppi'' ctFondttt Chctciaa. P-31S T*\ SM/«.- nf D e-Aifohdtzed WMC. P- 'U C*-Sf //5f JAIAC o/CeiteinI<c C U WJ. lcel-JiiyShtfott. Fiozo: Yoghint Ftoziit Pitikims PtujucK. ?-_-4A/w«i>.f t>/C.-iW iu* v*?ri«<: . P-23H.V« ni; i i t jo'"Oni«. u T p n t f a o i C ofPiep&t(IF<>&i".?-2K

lAp£kciifi&!\JC>i71i*7ttFt0aiic!zC&!i>HQtil} Described o: 'Diettny

Si'ffylentou: ".isid ?-*41 Sfer.ntit; vfQihvi .^hai'tu Si-wA'/Vsw "-"». «« Poispap'n Itji a/ Pr.f: W o/Sc':e-J:i t T! .v iht

£\?i;c T.x\.ic:

l**™-*** r*ta'M&f JT-MW-W in>*-±

BULLETIN NO. 029

issued May 2000

Revised May 2003

THE RETAIL SALES TA X ACT

FOOD AND BEVERAGES

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 49/164

in C

GST on about one-third of food

expendituresper annum

$2bn annually in revenue

GST on soft drinks, snack foods,chocolate, candy etc

GST on some 'healthy' choicesNo GST on some 'unhealthy' choices

No evaluation of impact of GST on foodconsumption

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 50/164

US S tate M an ufa ctu rer / .D is t r ibutor Food Tax

• Arkansas - levy on soft drink syrups, powders and bottledsoft drinks

• Maine - tax on soda proposed - revenue for HealthPromotion Fund [inactive]

• Missouri - 'inspection tax' paid by manufacturers and

distributors of soft drinks

• Rhode Is. - tax on volume of beverage containers sold

• Tennessee - tax on volume of import, manufacture andsales of soft drinks

• Virginia - tax on every wholesa ler or distributor ofcarbonated soft drinks

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 51/164

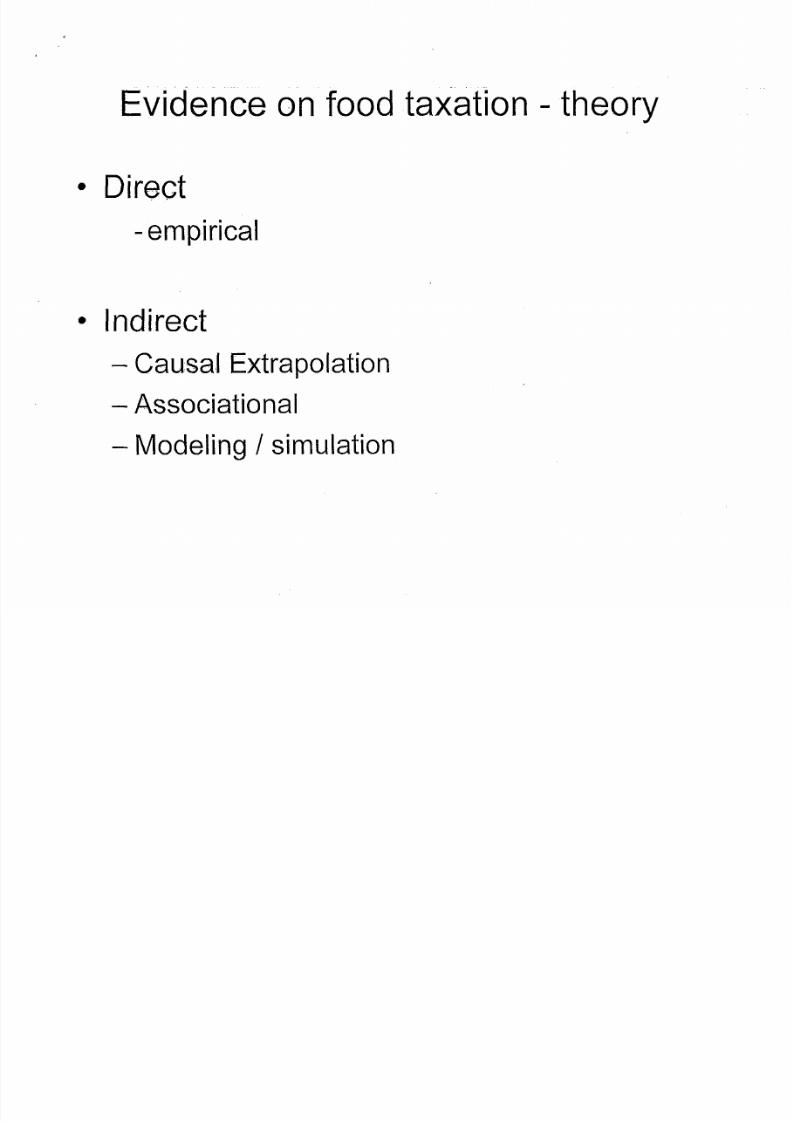

Evidence on food taxation - theory

• Direct-empirical

• Indirect

- Causal Extrapolation

- Associational

- Modeling / simulation

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 52/164

Evidence on food 1

• Direct-empirical

• Indi rect

- Causal Extrapolation

- Associational

- Modeling / simulation

axation - practice

X

x

V x

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 53/164

Conclusions

• Review and reform of GST/PST may be worth exploringfurther

• Combination of taxes and incentives may be better thaneach alone

• Rigorous prospective research is needed to draw firm

conclusions

• Weight of current evidence and commentary suggeststhere are more promising avenues to explore. E.g.subsidies for 'healthy foods'

8/13/2019 ATIP N-12 Final Information Transfer(1)-1

http://slidepdf.com/reader/full/atip-n-12-final-information-transfer1-1 54/164

V 2 ^

A D V I S O R Y N O T E F O R T H E M IN I S T E R O F H E A L T H Y L I V I N G

Di vis ion /B ran ch : Heal thy L iving\Healthy Populat ionsSu bje ct: Fat taxes and junk food taxes

I ssue Sum m ary :So-called 'fat taxes' and 'junk food taxes' have been much discussed in public and professionalarenas. What are the pro's and con's and have such taxes been successful ly implemented inother jurisdictions?