atm indonesia’s less cash -...

TRANSCRIPT

1

ATM

Description Things To Do Supported By

Melakukan support terhadap Direct Marketing dengan bekerja sama oleh pihak merchant lokal atau menambah potensi channel lokal bagi setiap ATM sesuai lokasinya

1. Menilai potensi merchant dengan melihat beberapa faktor seperti customer merchant, jumlah outlet, jumlah transaksi, dan brand equity serta dilengkapi dengan informasi mekanisme penukaran point.

2. Mengirimkan analisa potensi merchant ke EBMD untuk proses approval 3. Setelah approval di dapatkan, maka dilakukan PKS dengan merchant 4. Development sistem penukaran point merchant dan uji coba sistem 5. Melakukan review setelah merchant berhasil live di sistem direct marketing secara berkala

dengan menganalisa penukaran pointnya

Memberikan referensi terkait lokasi yang representatif untuk dijadikan tempat disediakannya ATM, bila ada penyebaran mesin ATM baru.

1. Membuat analisa SWOT serta analisa biaya yang timbul untuk lokasi penempatan ATM apabila ada ATM yang di relokasi atau ada penambahan ATM baru

2. Berkoordinasi dengan cabang dan memaparkan hasil analisa SWOT untuk mendapatkan approval

3. Mengirimkan analisa hasil SWOT ke EBMD untuk proses approval atau rekomendasi atas lokasi penempatan ATM

4. Proses pengajuan yang sudah mendapatkan approval dari kantor pusat, EBMD area berkoordinasi dengan cabang untuk proses kelengkapan administrasi dan memastikan proses pemasangan ATM telah sesuai dengan prosedur

Indonesia’s Less Cash Market Transformation Adrian Gunadi, Managing Director Retail Banking Openway 2015

2

BANK MUAMALAT:

Corporate Profile

BANK MUAMALAT: Building In-Roads to

Less Cash Society

INDONESIA: Burgeoning

Demographics

5

Agenda

1 2 4 BANK

MUAMALAT: Groundbreaking to

Branchless Banking

LANDSCAPE: Growing Less Cash

Society 3

Wonderful Indonesia: A Place of Cultural Heritage, World’s Famous Cullinary and Explore the Diversity of Indonesian Forest..it’s more than BALI

3

A Place of Cultural Heritage

Traditional Dances: Indonesia has unique, various and famous traditional dances Kecak & Saman Dance Traditional Music Instruments: Indonesia has unique traditional music instruments Angklung & Sasando

World’s Famous Cullinary Rendang & Nasi Goreng is two of most popular food in Indonesia and Rank #1 & #2 based on polls from CNN World's 50 best foods

A Place of Cultural Heritage Batik: UNESCO name Batik, Indonesia's traditional process of dying cloth through wax resist methods, as an intangible cultural heritage. Collonial Heritages: Collonial structures in Indonesia from Dutch Colonization era Fatahillah Museum & Lawang Sewu

Explore the Diversity of Indonesian Natural Forrest Forest Adventure: Indonesian forrest adventure Protected wildlife: Orang Utan Endemic Flower: Anggrek

BANK MUAMALAT: Corporate Profile 1

4

5

Bank Muamalat– Indonesia’s 1st Islamic Bank

– Assets Rp62.3 tn or USD 4.8 bio(a)

– Financing Rp43.0 tn or USD 3.3 bio (a)

– Customer deposits Rp51.0 tn or USD 3.9 bio (a)

– Customer Base 4 mio

– Market Share 30% market share in Shariah (a)

– Size #17 local bank in Indonesia(b)

Major banking

presence

Diversified

business mix (b)

– 83 branches across Indonesia

– 461 outlets(c) and 2,000 ATMs

– Access to 4,141 Post Office outlets and 4,000 kiosk

– Presence ranges from high density cities to remote

areas

Nationwide

distribution

network

– Indonesia’s first Shariah bank

– 2014 Best Islamic Retail Bank – Islamic Finance News

– 2014 Best Islamic Bank Indonesia – Global Finance

– Shareholding : Islamic Development Bank (33%) ;

Boubyan Bank & National Bank Kuwait (30%); Sedco

Investments (25%); Public (12%)

Leading

Indonesian

Shariah bank with

strong brand

(a) As of December 2014

(b) Excluding joint venture and foreign banks in 2014 total 131 banks

(c) Includes branches, sub-branches, and cash offices. Excludes mobile branches

Key financial ratios

1

2

3

4

Business mix (Q2-2014)

Company highlights

Corporate:

Rp19.7tn (46%)

– Commercial – Upper SME

Retail: Rp

23.3tn (54%)

– Lower SME – Consumer – Microfinance

2011 2012 2013 2014

Tier 1 ratio 9.00% 7.00% 11.74% 11.51%

Capital adequacy ratio 12.00% 11.60% 17.27% 16.31%

Net Income Margin (BI) 5.00% 4.60% 4.64% 4.82%

Financing-to-customer deposits ratio 83.90% 94.20% 99.99% 96.78%

Financing-to-funding ratio 117.30% 78.90% 86.19% 85.77%

NPF ratio (gross) 2.60% 2.10% 1.35% 3.30%

Return on equity 20.79% 29.16% 32.87% 20.96%

Return on assets (BI) 1.52% 1.54% 1.37% 1.53%

Funding mix

Corporate

44%

Retail

56%

Financing mix

Commercial 23%

Upper SME 20%

FI 3%

Lower SME 19%

Consumer 35%

Corporate

46%

Retail

54%

Customer

deposits

84%

CASA 31%

Time deposits 50%

Deposits from other banks

13%

Fund borrowing

2%

Sukuk 4%

81

%

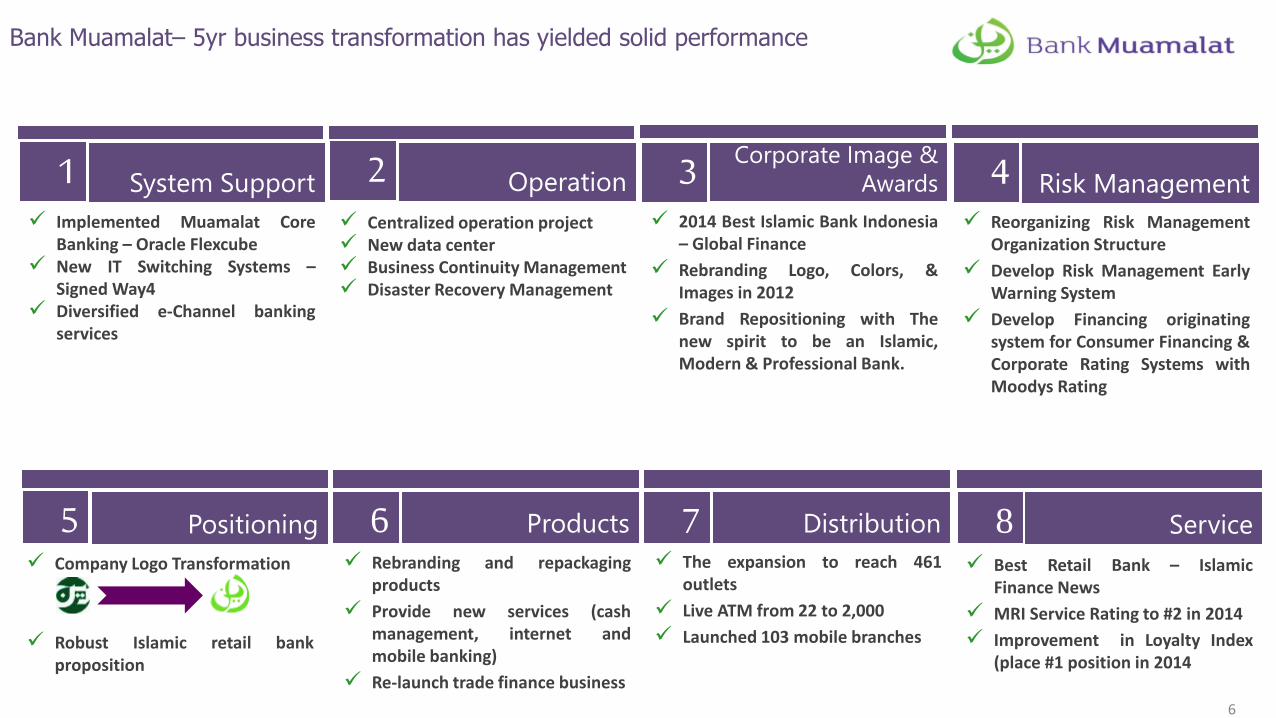

System Support Operation Corporate Image &

Awards Risk Management

2014 Best Islamic Bank Indonesia – Global Finance

Rebranding Logo, Colors, & Images in 2012

Brand Repositioning with The new spirit to be an Islamic, Modern & Professional Bank.

1 2 3 4 Implemented Muamalat Core

Banking – Oracle Flexcube New IT Switching Systems –

Signed Way4 Diversified e-Channel banking

services

Centralized operation project New data center Business Continuity Management Disaster Recovery Management

Reorganizing Risk Management Organization Structure

Develop Risk Management Early Warning System

Develop Financing originating system for Consumer Financing & Corporate Rating Systems with Moodys Rating

Positioning Products Distribution Service 5 6 7 8 Best Retail Bank – Islamic

Finance News

MRI Service Rating to #2 in 2014

Improvement in Loyalty Index (place #1 position in 2014

The expansion to reach 461 outlets

Live ATM from 22 to 2,000

Launched 103 mobile branches

Rebranding and repackaging products

Provide new services (cash management, internet and mobile banking)

Re-launch trade finance business

Company Logo Transformation

Robust Islamic retail bank proposition

6

Bank Muamalat– 5yr business transformation has yielded solid performance

INDONESIA: Burgeoning Demographics 2

7

8

Indonesia’s unique geographic spread coupled with rising GDP and consumer Spending promotes less cash transactions

0%

10%

20%

30%

40%

50%

60%

70%

2008 2009 2010 2011 2012 2013 2014

Vol Trx % of Total Banked Customers

Withdrawal Purchase Intrabank Transfer Interbank Transfer

0%

10%

20%

30%

40%

50%

60%

70%

80%

2008 2009 2010 2011 2012 2013 2014

Freq Trx % of Total Banked Customers

Withdrawal Purchase Intrabank Transfer Interbank Transfer

Burgeoning Demographics – But challenges remain..

9

100

200

300

400

500

600

700

2008 2009 2010 2011 2012 2013 2014 2015 E

54 57 65 78 93 105 122 146 3 8 14 22

36 36

43

22 26 36

47 55

68 85

125

22 24 27

23 21

20 20

20

149 177

228 259

278

297 309

325

Massive Growth Cellphone Subscribers compare to Bank Cardholders (in million)

ATM Debit Credit Cards E Money Cards Internet User

Fixed Line Subscribers Cell Phone Subscribers

Source : Bank Indonesia; www.redwing/asia.com & compiled from various sources

Burgeoning Demographics – Telcos have higher penetration compared to banks .. only 30% of population have bank accounts

LANDSCAPE: Growing less cash society 3

10

11

Interoperability amongst

Banks-Telco

(inter industry)

(National Payment Gateway)

Regulators Endorsement

1. Standardization

2. Interoperability

3. Push factors

Banks & Telco Collaboration

1. Existing market

2. Emerging market

SUMMARY :Indonesia’s shifting Cash to be Less Cash ? • Key Success Factors on Transforming to be Less Cash Society

Notes : Regulators are not only Central Bank but also regulators of related payment industries Interoperability is also expected to be applied within telco industries Major Banks are still on Focusing to bankable market penetration ( e toll, flazz etc,) while telco (MNO) have easy access to mass market

having a Less Cash society does not necessarily eliminate all cash transactions, it merely encourages people to prefer non-cash transactions

Landscape– Positive support from regulators to accelerate less cash society

12

2. Penetrating the Emerging Market – Banks &Telco Collaboration is required to tap unbanked

1. Telco Technology as Front End Solution

2. Banks function as Settlement & Pooled Fund

3. Banks increasing distribution outlets both conventional and non-conventional

4. Telco & Banks partnership for financial inclusion

5. Interoperability amongst Telco & Banks

1. Deepen on existing customer base -the bankable to increase Less Cash transactions

1. Managing Cost + Revenue = Price

2. Expanding thru established distribution channels: a. Transportation b. Convenience Store etc. 3. Provide transactions for Small ticket purchase such as

parking, tickets thru - E Money

4. Increasing Interoperability = Increasing Access

Landscape– Capturing the opportunity thru targeted business model

BANK MUAMALAT: Building in-roads to less cash

society

4

13

14

- 83 Branches

- 461 Outlets

- 4 Millions Customer

- 2000 ATM

- Direct Marketing

- Avg Trx/Yr 532 Thousand

-Avg Vol/Yr 1,3 Billion

- ± 4.136 Counter

- Visa Debit

- 300.000 Cardholders

- 50.000 users mobile

- ±4.000 Kiosk

- 7 Millions Trx/Year

- Vol 713 billion/Year

- Debit Online

- ±300.000 User Registered

- All Platform (Android, IOS, Blackberry, Windows)

- Live Information (ATM/Branch Location)

Cash In-Cash Out

Market Target

- 435 cooperatives

- 9.000 Alfamart Outlet

- 35.000 XL Tunai Subscriber

- Feature: Deposit, Withdrawal Transfer, Overbook Payment & Purchase

2004

2012

2015 2016-2017

1992 1999

2011

Revamp

2008

• Transaction at anytime, anywhere

• Increase customer accessibility

• Building platform for branchless banking

- Full branchless banking

- Micro Insurance

- Micro Finance

- Remittance & E-Money

Bank Muamalat– Developing payments proposition to capture opportunity .. supported by Way4 since 2010

15

Channel Transaction

Volume Growth*

Fee Base Growth*

Feature Key Metric Other

Internet 251% 391%

- Overbooked & Transfer

- Payment - Purchase

- 103.000 user registered

- 6.700 user active/month**

- OTP Secured

- M-Browser

Mobile Banking (GPRS) 334% 246%

- Overbooked & Transfer

- Payment - Purchase

- 45.000 user registered

- 5.000 user active/month**

Multiplatform

ATM 120% 400%

- Withdrawal - Overbooked &

Transfer - Payment - Purchase

- 2000 ATM (2 Kiosk & 2 Drive Through)

- Join with Malaysia Network

- Direct Marketing

Cash Collecting Payment (PPOB)

1978% 1961 %

- Payment - Purchase

- 4.000 counter registered

- 2.500 counter active/month**

- Flexible Admin Fee

*YoY Growth Q1 2013-2015 **in last 3 years

e-Muamalat

Bank Muamalat– Current e-channel suite

16

Old Mobile Banking Features New Mobile Banking UMB

(USSD Menu Browser)

Balance Inquiry Inquiry Balance Inquiry Balance inquiry

5 last Transaction 10 last Transaction

Account Statement + Account Opening*

Account Statement + Account Opening*

Overbooking Transfer Overbooking Overbooking

Transfer ATM Bersama Transfer ATM Bersama, Prima, SKN

and RTGS Transfer ATM Bersama, Prima, SKN,

RTGS

Telkomsel, Indosat and Telkom

Payment and Purchase Multi Biller (Telco, Utilities and

Insurance)

Multi Biller (Telco, Utilities and Insurance)

Only on old version Blackberry

Operating System Multi Platform (Android, IOS, New

Blackberry and Windows)

Variety Gadget (Smartphone, Tablet, Phablet)

All Gadget (Feature Phone, Smartphone, Tablet, Phablet)

Customer Touch Point Live Information, Branch/ATM

Location & Advertisement

Support by 3 Major Telco Provider SMS-Banking Replacement

No Internet Connection Needed

New Mobile Banking UI

USSD Mobile Browser UI

Bank Muamalat– Mobile banking platform GPRS & UMB capability to penetrate banked & unbanked

*Target launch Dec 2015

17

• Bank Muamalat ATM Network of 2,000 terminals

– 2,000 ATMs

– 2 Kiosks/ Non Cash ATMs

– 2 Drive Through ATMs

• Features

– Cash Transactions

– Transfer, bill payment

– Virtual account

– Card-less withdrawals

– Implemented loyalty program and direct marketing

features

• Implemented in

– Fixed Location (branches, public areas)

– Mobile Location (mobile branches)

Bank Muamalat– Largest ATM network for Islamic Bank in Indonesia

18

ATM CRM : Bank Muamalat ATM Loyalty & Crossed Selling to Off Us Trx

18

Bank Muamalat was 1st Islamic Bank to launch campaign and yielded significant gains in increasing Off-Us transaction to become 40% of total monthly ATM transactions

Branch Transformation Model ATM Transformation Model

Applied For ANY BANK ATM CARD Transact More, Get More !

USP: 1. 5x Times

Transaction Get Vouchers.

2. Input Name & Cell Phone Get Vouchers.

3. ATM Surprise! Get Your Handset for x Transaction

Bank Muamalat– ATM loyalty campaign increased off-us transaction & awareness

BANK MUAMALAT: Groundbreaking to Branchless

Banking 5

19

20

Service Remarks

Opening Account Yes

Deposit Yes

ATM Yes

EDC Yes

Cash Collecting Payment (PPOB)

Yes

IB & MB Reg Yes

Service Remarks

Opening Account Yes

Deposit Yes

More in depth to gain & serve market and requires mobility with mobile-branch and partnership with large network such as PT POS INDONESIA – with over 4500 outlets

• Getting Closer to Customers • Servicing @ odd hours • Full Service : ATM, Tellers, Pick Up

Money & Cash Collecting of Bill Payment

Bank Muamalat– Branchless banking as the new frontier

21

Muamalat Payment Point Franchise

Muamalat Payment Point • Technology driven solution

for micro segment • Clear parameters • Monitoring systems for

managing Counters with diverse features

Transaction Growth 2013 - 2014

163%

Vol Transaction Growth 2013 - 2014

173%

FBI Growth 2013 - 2014

80%

21

Basic Saving Account

Micro Insurance

Micro Finance Other Financial

Product

Cash In, Cash Out, Overbook & Transfer

LAKU PANDAI

BRANCHLESS BANKING MUAMALAT

Transaction Integrated With E-Wallet (Telco

provider)

Open Reguler Account (CA,SA,TD)

Bank Muamalat– Branchless banking with Muamalat Mobile as technology platform leveraging realtionship with agents

GPRS & UMB Platform

1

Cash Out Transaction

BSA, Micro Finnancing &

Insurance

Remittance & E-Money

Cash In Transaction

22

Phase 2 Phase 1 Phase 3 Phase 4

•BSA (Basic Saving Account)

•Micro Finance

•Micro Insurance

•Transactional Activity

•E-Money

•Remittance

•Overbooking

•Withdrawal

•Deposit

•Payments

•Transfers

Cash In – Cash Out Project

2015 2015 2016 2017

Bank Muamalat– Branchless banking milestones

Target Projections in 5 yrs

NOA – Basic savings account new 4,9 mio new Accounts

VOL – Basic savings account new IDR 1,644 M or eq USD 130 mio

Agents 12.160 Agent

23

• Indonesia’s exponential growth in the consumer market in the next 5 yrs

• Constant innovation of products is critical to stay ahead of the curve

• Growing middle class customer require robust delivery channels and accessibility

• Robust technology infrastructure imperative for sustainable growth

• Organization culture transformation – From Top to Bottom

Front office & Back Office

Key Takeaways

24