audit responsibilities and objectives chapter (6)

TRANSCRIPT

Audit Responsibilities and Objectives

Chapter (6)

1. The objective of conducting an audit of financial statements.

• The objective of the audit of financial statements by the independent auditor is the expression of an opinion on the fairness with which the financial statements present financial position, results of operations and cash flows in conformity (accordance) with GAAP.

P.Dr. Gamal Khatab

Steps to develop audit objectives

• Understand objectives and responsibilities for the audit.

• Divide financial statements into cycles.• Know management assertions about financial

statements• Know general audit objectives for classes of

transactions, accounts, and disclosures.• Know specific audit objectives for classes of

transactions, accounts, and disclosures.

2. Management's responsibilities in preparing financial statement:

• Management is responsible for:a) Adopting and apply sound accounting policies.b) Maintaining an adequate internal control

structure.c) Making fair presentations of financial statements.• Management annual report must include those

three responsibilities.

P.Dr. Gamal Khatab

• Management responsibility for the integrity and fairness of the presentation (assertions) in the F. S. carries with it the privilege of determining which presentations and disclosures it considers necessarily.

• If management insists on F. S. disclosure that the auditor finds unacceptable, the auditor can either issue an adverse or qualified opinion or withdraw from the engagement.

The auditor’s responsibilities

• The auditor’s responsibility for detecting material misstatements in the F. S.

• When the auditor also reports on the effectiveness of the internal control over financial reporting, the auditor is also responsible for identifying material weakness in internal control over financial reporting.

The auditor's responsibilities• The auditor responsibilities to verify financial

statements and discover material errors; Irregularities and illegal acts

a) Auditors are responsible for designing and completing an audit as a professional in order to provide reasonable assurance of detecting material misstatements in financial statements. but he can not guarantee or insure that management representations are absolutely correct.

P.Dr. Gamal Khatab

b) Audit is performed with professional method to guarantee high level of audit performance.

c) The auditor should not begin the audit assuming that management is dishonest, but the possibility of dishonesty must be considered (professional skepticism).

P.Dr. Gamal Khatab

The auditor responsibility:• The auditor is responsible for obtaining reasonable

assurance that material misstatements in the F.S are detected, whether those misstatements are due to errors or fraud.

• An audit must be designed to provide reasonable assurance of detecting material misstatements in the F.S further the audit must be planned and performed with an attitude of professional skepticism in all aspects of the engagement. Because there is an attempt of concealment of fraud, material misstatements due to fraud are usually more difficult to uncover (detect) than errors.

P.Dr. Gamal Khatab

• Auditors. Therefore, have less responsibility to detect irregularities than errors. The auditors best defense when material misstatements (either errors or fraud) are not uncovered in the audit, is that the audit was conducted in accordance with GAAS.

P.Dr. Gamal Khatab

Material versus immaterial misstatements

• Misstatements are: errors, misappropriation (theft) of assets, and fraud in F.S.

• Misstatement is considered material when it influences F.S users’ decisions.

• It is costly and probably impossible for auditors to have responsibility for finding all errors and fraud. So auditors are concerned with material misstatement.

P.Dr. Gamal Khatab

Reasonable Assurance

• Assurance is a measure of the level of certainty that the auditor has obtained at the completion of the audit.

• Since auditor is not an issuer of correctness of F.S. he provides a reasonable assurance about fair presentation of F.S. not an absolute assurance.

P.Dr. Gamal Khatab

The concept of reasonable assurance:

• It indicates that the auditor is not an insurer or guarantee of the correctness of the financial statement. The auditor's best defense when material misstatements are not uncovered in the audit. Is that audit was conducted in accordance with GAAS.

P.Dr. Gamal Khatab

• The auditor is reasonable for reasonable but not absolute assurance for several reasons:

a) Most audit evidence results from a sample of population.

b) Accounting presentation contain complex estimate which inherently involve uncertainty and can be affected by future events.

c) Fraudulently prepared financial statements are often extremely difficult if not impossible for the auditor to detect especially when there is collusion among management.

P.Dr. Gamal Khatab

Error versus fraud

a- An error is an unintentional misstatement of the financial statements.- Error in balance sheet (Ex) quantity of inventory is not prices.- Errors in income statement (Ex) sales invoice mistakes.- Accounting errors (Ex) accounting errors-typed of

errors by inefficient accountant such as posting in wrong side of accounting (Easy to detect).

- The auditor can detect most cases.

P.Dr. Gamal Khatab

b- Fraud : (Irregularities)• Is an intentional misstatement of the financial

statements.• Irregularities: may be the result of either

employee fraud (theft of asset) Ex: A clerk makes theft of cash and not recode in cash register. Or management fraud (fraudulent financial reporting). Ex: Over statement of sales near year end to increase net income auditor cannot detect or uncover all cases.

P.Dr. Gamal Khatab

The differences among “Errors”, “Fraud”, “illegal acts”

P.Dr. Gamal Khatab

Error Fraud Illegal actsAn unintentional misstatement of the financial statements.Example: mistake when footing the columns in the sales journal.

An intentional misstatement of the financial statements.

Violation of laws or government regulations other than fraud.Example: dumping of toxic waste in violations of the federal environmental protection laws.

Professional skepticism• It consists of two primary components a

questioning mind and a critical assessment of audit evidence.

• The auditor should not assume that Management is dishonest but the possibility of dishonesty must be considered.

P.Dr. Gamal Khatab

Characteristics of Skepticism1. Questioning mindset – a disposition to inquiry with some sense

of doubt.2. Suspension of judgment – without holding judgment until

appropriate evidence is obtained.3. Search for Knowledge – a desire to investigate beyond the

obvious, with a desire to corroborate.4. Interpersonal understanding – recognition that people’s

motivations and perceptions can lead them to provide biased or misleading information

5. Autonomy – the self-direction, moral independence, and conviction to decide for oneself, rather than accepting the claims of others.

6. Self-esteem – the self-confidence to resist persuasion and to challenge assumptions or conclusions.

P.Dr. Gamal Khatab

Auditor’s responsibilities for detecting material errors

• Auditors spend a great portion of their time planning and performing audits to detect unintentional mistakes made by management and employees, auditors find a variety of errors resulting from such things as mistakes in calculations, omissions, misunderstanding and misapplication of accounting standards, and incorrect summarizations and descriptions.

P.Dr. Gamal Khatab

Auditor’s responsibilities for detecting material fraud

• Auditing standards make no distinction between the auditor’s responsibilities for searching for errors and fraud. In either case, the auditor must obtain reasonable assurance about whether the statements are free of material misstatements the standards also recognize that fraud is after more difficult detect because management or the employees perpetrating the fraud attempt to conceal the fraud.

P.Dr. Gamal Khatab

The actions on auditor should take when the auditor discovers an illegal act

P.Dr. Gamal Khatab

The auditor should first consider the effects of the illegal act on the financial statements, including the adequacy of disclosures, if the auditor concludes that disclosures are inadequate, the audit report should be modified accordingly, the auditor should also consider the effect of the illegal act on its relationship with management, and management’s trustworthiness, next the client’s audit committee of others of equivalent authority should be informed of the illegal act, if the client does not deal with the illegal act in a satisfactory manner, the auditor should consider withdrawing from the engagement. Finally, if the client is publicly held, the auditor may need to report the matter to the SEC.

Misappropriation of assets versus fraudulent F. reporting

• Misappropriation: Is a theft of assets by employees ordinarily occurs either because of inadequate (ICs) or a violation of existing controls.

• The best way to prevent employee fraud is through adequate (ICs) that function effectively.

• Many times employed fraud is relatively small in dollar amounts and will have no effect on the fair presentation of F.S. there are also cases of large employee fraud that result in bankruptcy to the company.

P.Dr. Gamal Khatab

Fraudulent F. reporting (Management Fraud)

• Is the intentional misstatement of financial information by management of a theft of assets by management

• Management fraud is inherently difficult to uncover because it is possible for one or more members of management to override internal control. Irregularities may include misstatements of F.S. and theft of assets. In many cases the amounts are extremely large and may affect the fair presentation of F.S. Also, in many cases, it is difficult to detect management fraud.

P.Dr. Gamal Khatab

Management Fraud • is difficult to uncover because of the intended deception and

efforts to make them hard to uncover by overriding internal control instructions, omission of fraudulent transactions or recorded amounts.

• To uncover management fraud, this need more cost, client cannot accept.

Examples:• Optimistic estimates of revenues net income to raise shares price.• Consider some current expenses as capital expenses or types of

assets.• Old inventory prices are the same as new inventory.• Decrease depreciation rates or percentage of allowance of

doubtful debts.

Illegal Acts• Are violations of laws or government regulation other than

irregularities such as violation of federal tax law (direct effect illegal acts) and violation of the federal environment protection laws (indirect effect of illegal acts).

Direct – Effect illegal Acts• Certain violations of laws and regulations have a direct

financial effect on specific account balances in the financial statements. For example, a violation of federal tax laws directly affects income tax expense and income taxes payable. The auditor's responsibilities for these direct-effect illegal acts is the same as for errors and fraud.

P.Dr. Gamal Khatab

On each audit, therefore, the auditor will normally evaluate whether or not there is evidence available to indicate material violations of federal or state tax laws.

Indirect effect Illegal Acts• Most illegal acts affect the financial

statements only indirectly. Ex: environmental laws such as decreasing pollution.

P.Dr. Gamal Khatab

Auditor responsibility for illegal acts

• There are three levels of responsibility that the auditor has for finding and reporting illegal acts.

1- There is no reason to believe that there is illegal acts:• Auditor must accumulate evidence to determine that

is no reason for illegal acts. a) Meetings with client’s attorney. b) No laws or regulation violated before. 2- The auditor believed that there is reason to believe there is direct or indirect effect of illegal acts.

P.Dr. Gamal Khatab

Ex: Payment to consultants or government officials.Action to be taken: a) Inquires to management. b) Consult legal counsel or specialist. c ) Accumulate evidence to determine illegal acts.3- Actions when auditor knows of illegal acts:• Consider direct effects on F.S and adequacy of disclosure.• Find cases such as: loosing clients-loosing key employees.• Modification of audit report.• Communication with audit committees and management.• Knowledge about illegal acts to be satisfied.• Withdraw from engagement.• Notify authorities.

P.Dr. Gamal Khatab

Why the auditor obtains assurance by auditing classes of transactions and

ending balances in accounts?

• Audits are performed by dividing the financial statements into smaller segments of components. Each segment is audited separately but not completely independently. After the audit of each segment is completed, including interrelationship with other segments, the results are combined. A conclusion can then be reached about the financial statements taken as a whole.

P.Dr. Gamal Khatab

SETTING AUDIT OBJECTIVES• Auditors conduct audits by performing audit tests of the

transactions making up ending balances and also by performing audit tests of the ending balances themselves.

P.Dr. Gamal Khatab

Beg. Balance $1000Sales $10000

11000End. Balance $2000

Cash Receipts $5000Sales returns $1000Allowance debtsChange – off 3000

11000

Dr AR CR

• Assertion: In general is, as explicit or implicit statement made by one party for use by another party.

• Management Assertion: are implied or expressed representations by management about classes of transactions and the related accounts in the F.S.

• Management assertions are directly related to GAAP. These assertions are part of the criteria that management uses to record and disclose accounting information in financial statements.

P.Dr. Gamal Khatab

Management Assertions:

AICPA auditing standards Classify assertions into 3 categories 1. Assertions about classes of transactions and

events for the period under audit (five assertions).

2. Assertions about account balances at period end (four assertions).

3. Assertions about presentation and disclosure (four assertions).

P.Dr. Gamal Khatab

P.Dr. Gamal Khatab

Assertion Category The Concept

1- Occurrence. Concern whether recorded transactions included in the F.S. actually occurred during the accounting period.

2- Completeness State the all transactions and accounts that should be presented in the F.S. are in fact included.

1- Assertions about classes of transactions and events

3- Accuracy This assertion addresses whether transactions have been recorded at correct amounts.

4- Classification The classification assertion addresses whether transactions are recorded in the appropriate accounts.

5- Cutoff This assertion addresses whether transactions are recorded in the proper accounting period.

P.Dr. Gamal Khatab

2- Assertions about Account Balances

Assertion Category The Concept1- Existence Deal with whether assets, obligations and

equity included in the B.S. actually existed on the B.S. date.

2- Completeness State that all transactions and accounts that should be presented in the F.S. are included.

P.Dr. Gamal Khatab

3- Valuation and allocation These assertions deal with whether assets, liabilities, equity, revenues, and expense accounts have been included in the F.S. at appropriate amounts.

4- Rights and obligations Deal with whether assets are the rights of the entity and obligations of the entity at a given date.

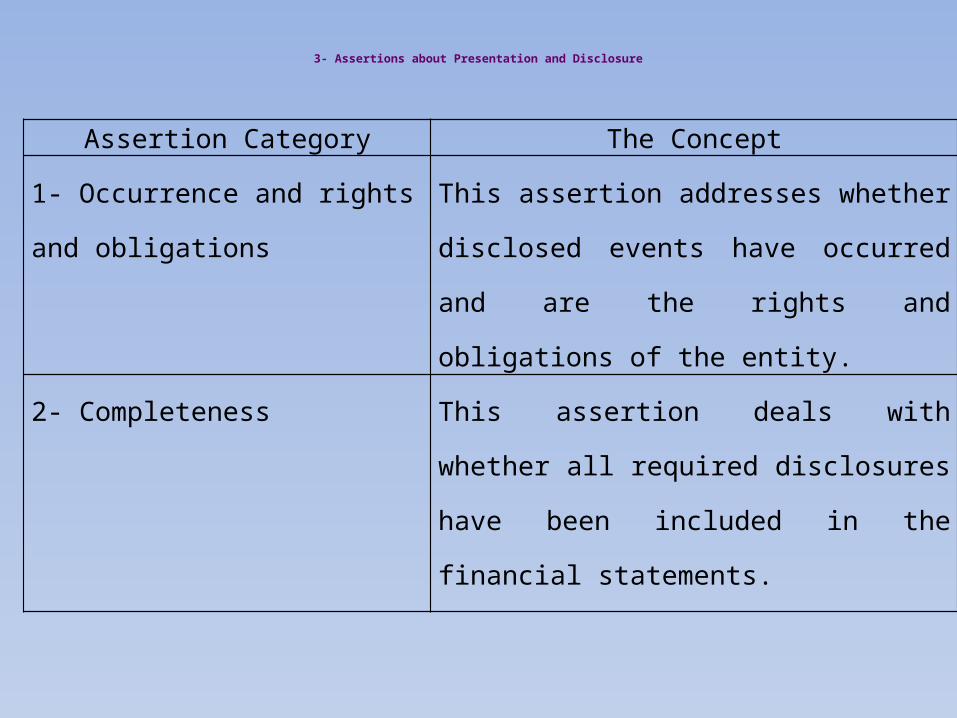

3- Assertions about Presentation and Disclosure

Assertion Category The Concept

1- Occurrence and rights and obligations

This assertion addresses whether disclosed events have occurred and are the rights and obligations of the entity.

2- Completeness This assertion deals with whether all required disclosures have been included in the financial statements.

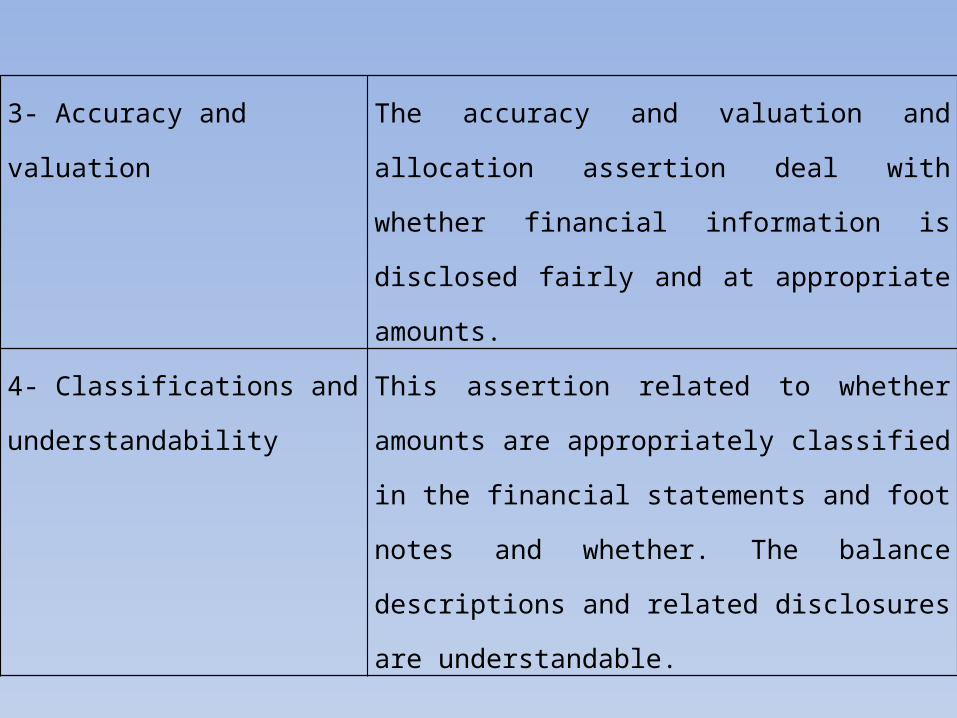

3- Accuracy and valuation The accuracy and valuation and allocation assertion deal with whether financial information is disclosed fairly and at appropriate amounts.

4- Classifications and understandability

This assertion related to whether amounts are appropriately classified in the financial statements and foot notes and whether. The balance descriptions and related disclosures are understandable.

Audit Objectives• Auditor must be sure assertion are correct.• General audit objectives follow from and are closely

related to Management assertions• General audit objective, however, are intended to

provide a frame work to help the auditor accumulates sufficient competent evidence required by the third standard at field work while Management about classes of transactions and the related account in the F.S.

• Audit objectives more useful to auditors than assertions because they are more detailed and more closely related to helping the auditor accumulate sufficient competent evidence.

P.Dr. Gamal Khatab

P.Dr. Gamal Khatab

Objectives are divided into two categories

(A) Transaction – Related Audit objectives

· Which are applicable to every class of transactions but are

stated in broad - terms.

(B) Balances (Specific) – Transaction – Related

Audit objectives

· Which are also applicable to each class of transactions but are stated in

terms to specific tailored to class of transactions. EX: sales transactions.

General Specific

General

Specific

(A) General Transaction – Related Audit Objectives• Transaction – related audit objectives are closely

related to management assertions.• These objectives are used to provide a framework

to help auditor in accumulating competent sufficient evidence.

There are six General Transactions Related Audit Objectives1- Occurrence• It deals with whether amounts included in the F.S should

actually occurred (this objective is the auditor's counterpart to the management assertion of occurrence).

2- Completeness:• Existing transactions are recorded. This objective deals with

whether all transactions that should be included in the journals have actually been included.

• The objective is the counterpart to the management assertion of completeness.

P.Dr. Gamal Khatab

3- Accuracy• Transactions are stated at the correct amounts.• This objective deals with the accuracy of

information for accounting transactions.(Ex): The quantity of goods shipped was different from billed. This objective is related to Management assertion of valuation and allocation.4- Classification• Transactions included in the client's journals are

properly classified. This objective is related to Management assertion of valuation and allocation.

P.Dr. Gamal Khatab

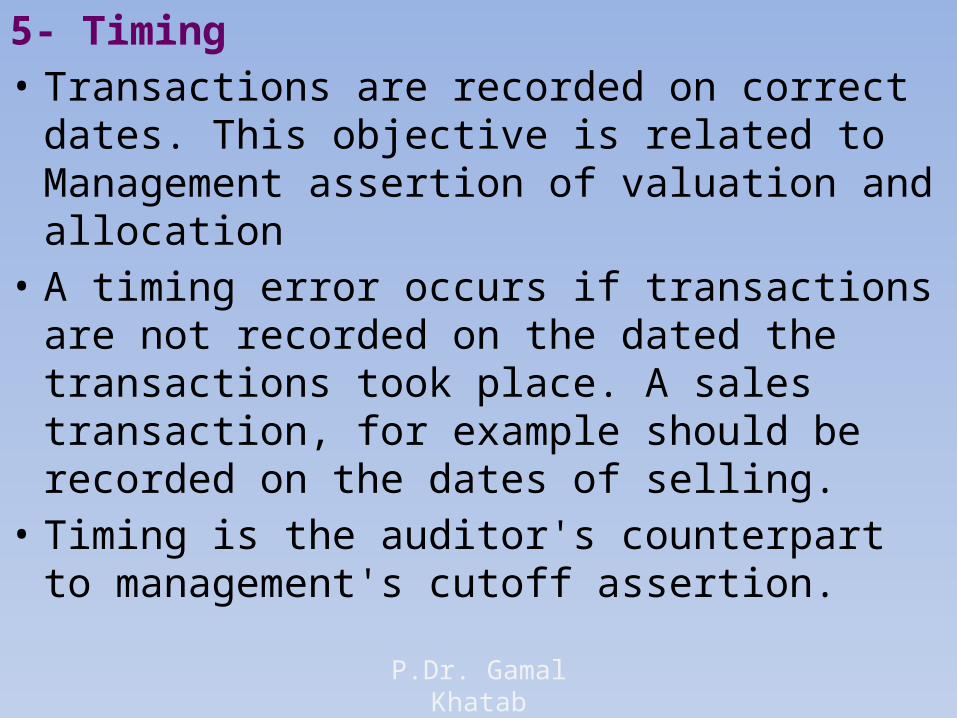

5- Timing• Transactions are recorded on correct dates. This

objective is related to Management assertion of valuation and allocation

• A timing error occurs if transactions are not recorded on the dated the transactions took place. A sales transaction, for example should be recorded on the dates of selling.

• Timing is the auditor's counterpart to management's cutoff assertion.

P.Dr. Gamal Khatab

6- Posting and summarizing• Recorded transactions are properly included in the

master files and are correctly summarized. This objective deals with the accuracy of the transfer of information from recorded.

• Posting and summarizing is a part of the accuracy assertion for classes of transactions.

P.Dr. Gamal Khatab

B- Specific Transaction–Related Audit objectives• After the general-transactions related audit objectives are determined, specific-transactions related audit objectives for each material class of transactions can be developed.Ex: Existence, completeness, accuracy, classification, timing, posting and summarizing of sales transactions specific class of transactions.

P.Dr. Gamal Khatab

Balance – Related Audit Objectives• Resulting also from mgmt.'s assertions and provide a frame work for accumulating sufficient competent evidence about ending balances stated in F.S.

P.Dr. Gamal Khatab

• There are Nine General Balance-Related Audit Objectivesa) Existence: Ex: amounts included actually existed.b) Accuracy: Ex: amounts are stated correctly.c) Presentation and Disclosure: Ex: proper presentation on financial statements.d) Detail Tie-in: Ex: details in account balance agree with related master file.e) Completeness: EX: existing amount s are included.f) Classification: EX: amounts are properly classified.g) Cutoff: Ex: transactions near the balance sheet date are recorded in the proper period.h) Rights and Obligations: Ex: amount included are owned or owed.i) Realizable Value: Ex: assets are stated at the value to be realized.

P.Dr. Gamal Khatab

How audit objectives are met?• The auditor must obtain sufficient competent audit evidence to support all Management assertions in the F.S to express an opinion on the fairness with the F.S present fairly in conformity with GAAP.

• To meet audit objectives, the auditor must follow ''four'' phases (or steps).

P.Dr. Gamal Khatab

To meet audit objectives, the auditor must follow ''four'' phases (or steps).

• Plan and design an audit approach based on risk assessment procedures.

• Perform tests of controls and substantive tests of transactions.

• Perform analytical procedures and tests of details of balance.

• Complete the audit and issue an audit report.

A-Plan & Design an audit approach:-

• Two overriding considerations affect the approach the auditor selects:-

• Sufficient appropriate evidence must be accumulated to meet the auditor’s professional responsibility.

• The cost of accumulating the evidence should be minimized.

• Risk assessment: three key aspects

1- Obtain an understanding of the entity and its environment

• Including knowledge of strategies and processes the auditor should study the client’s business model, perform analytical procedures and make comparisons to competitors.2- Understand internal control and assess control risk

• The auditor identifies internal controls and evaluates their effectiveness, a process called assessing control risk.3- Assess risk of material misstatement:

• The auditor uses the understanding of the client’s industry and business strategies, as well as the effectiveness of controls, to assess the risk misstatements in the financial statements.

• This assessment will then impact the audit plan and the nature, timing, and extent of audit procedures.

B- Perform tests of controls and substantive tests of transactions

• Before auditors can justify reducing planes assessed control risk when internal controls are believed to be effective, they must first test the effectiveness of the controls the procedures for this type of testing are commonly referred to as tests of control.

• Auditors also evaluate the client’s recording of transactions by verifying the monetary amounts of transactions, a process called substantive tests of transactions.

C- Perform Analytical procedures and tests of details of balances involved:-

• Analytical procedures: consist of evaluations of financial information through analysis of plausible relationships among financial and non-financial data.

• Tests details of balances: are specific procedures for each audit objective and for each financial statement.

D- Complete the audit and issue an audit report:-

• After the auditor has completed all procedures for each audit objective and for each financial statement account and related disclosures, it is necessary to combine the information obtained to reach an overall conclusion as to whether the financial statements are fairly presented

The cycle approachIt is a method of dividing the audit such that closely related types of transactions and accounts balance are included in the same cycle.

P.Dr. Gamal Khatab

General ledger account Cycle

SalesAPREAR

InventoryRepairs & maintenance

Sales & collectionAcquisition & payment

Capital acquisition & repaymentSales & collection

Inventory & warehousingAcquisition & payment

Prof. Gamal Khatab