audit workbook

TRANSCRIPT

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 1/42

P a g e | 1

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

W orkbook A dvanced A udit ing and Professional E thics

(CA – F inal)

Compiled by: Pankaj Garg

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 2/42

P a g e | 2

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

Must Read - Preface to Workbook

This workbook contains topics which are not covered in main notes but important to study as questions on these

concepts are regularly asked in the exams. Such Topics are Guidance Notes, Accounting Standards,

Companies (AS) Rules, 2006, Schedule VI etc.

As these topics, in itself are very much detailed and the part of IPCC – Account / Final – Financial Reporting, only the

portion that is relevant for Auditing paper is covered here.

Most of the practical illustrations covered in these notes are taken from “Chartered Accountant” Journal, RTP,

Suggested answers, Practice Manuals and Compiler.

On analysis of past year question papers, it can be concluded that around one question covering 16-20 marks is

from the areas mentioned above and generally that question is compulsory one.

I hope that readers will be satisfied with the contents of these notes. Still, there always remains scope for improvement.

I will be grateful to the readers for their valuable feedback for improvement of these notes.

Wishing every success to the readers.

CA. Pankaj Garg

e-mail: [email protected]

B est of L uck… … … … … .

Schedule of Upcoming Batches

IPCC - Audit F2F 31-May TT 10.30 a.m. - 01.30 p.m. SmartteachCA, IMA - ITO, New Delhi

F2F 31-May TT 05.30 p.m. - 08.30 p.m. SmartteachCA , Pitampura, New delhi

Satellite 21-May SS 10.30 a.m. - 01.30 p.m. ETEN Centers - Across India

IPCC - Law F2F 30-May MWF 10.30 a.m. - 01.30 p.m. SmartteachCA , Pitampura, New delhiFinal - Audit F2F 30-May MWF 05.30 p.m. - 08.30 p.m. SmartteachCA , IMA - ITO, New Delhi

Satellite 28-May SS 02.00 p.m. - 05.00 p.m. ETEN Centers - Across India

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 3/42

P a g e | 3

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

CONTENTS

S. No. Name of Topic Page No. No. of

Illustrations/Questions

Preface 02

Contents 03

1 Guidance Notes 04 – 07 7

2 Questions on Standards on Auditing 08 – 13 36

3 AS and Companies (AS) Rules 14 – 30 40

4 Company Audit and Schedule VI 31 – 35 13

5 Additional Illustrations / Questions

Professional Ethics 36 – 36 3

Bank audit 37 – 38 3

Tax Audit 39 – 40 4

Misc. 41 - 42 4

Total Illustrations/Questions 110

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 4/42

P a g e | 4

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

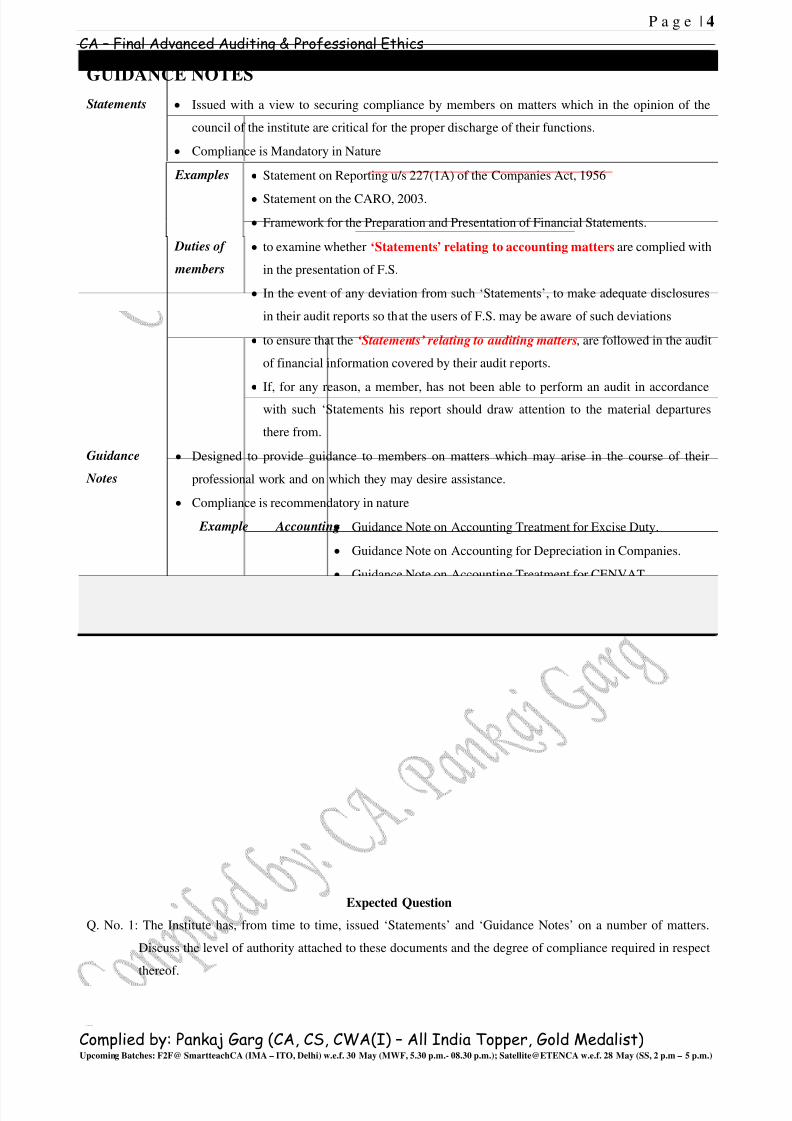

GUIDANCE NOTES

Statements Issued with a view to securing compliance by members on matters which in the opinion of the

council of the institute are critical for the proper discharge of their functions.

Compliance is Mandatory in Nature

Examples Statement on Reporting u/s 227(1A) of the Companies Act, 1956

Statement on the CARO, 2003.

Framework for the Preparation and Presentation of Financial Statements.

Duties of

members

to examine whether ‘Statements’ relating to accounting matters are complied with

in the presentation of F.S.

In the event of any deviation from such ‘Statements’, to make adequate disclosures

in their audit reports so that the users of F.S. may be aware of such deviations

to ensure that the ‘Statements’ relating to auditing matters, are followed in the audit

of financial information covered by their audit reports.

If, for any reason, a member, has not been able to perform an audit in accordancewith such ‘Statements his report should draw attention to the material departures

there from.

Guidance

Notes

Designed to provide guidance to members on matters which may arise in the course of their

professional work and on which they may desire assistance.

Compliance is recommendatory in nature

Example Accounting Guidance Note on Accounting Treatment for Excise Duty.

Guidance Note on Accounting for Depreciation in Companies.

Guidance Note on Accounting Treatment for CENVAT.

Guidance Note on Accounting for Corporate Dividend Tax

Auditing Guidance Note on Independence of Auditors.

Guidance Note on Audit of Fixed Assets.

Guidance Note on Audit u/s 44AB of the Income -tax Act.

Guidance Note on Audit of Abridged Financial Statements.

Duties of

member

Accounting Examine whether the recommendations in a guidance note relating

to an accounting matter have been followed or not.

If the same have not been followed, consider whether keeping in

view the circumstances of the case, a disclosure in his report is

necessary.

Auditing Follow recommendations in a guidance note except where he is

satisfied that in the circumstances of the case, it may not be

necessary to do so.

Expected Question

Q. No. 1: The Institute has, from time to time, issued ‘Statements’ and ‘Guidance Notes’ on a number of matters.

Discuss the level of authority attached to these documents and the degree of compliance required in respect

thereof.

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 5/42

P a g e | 5

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

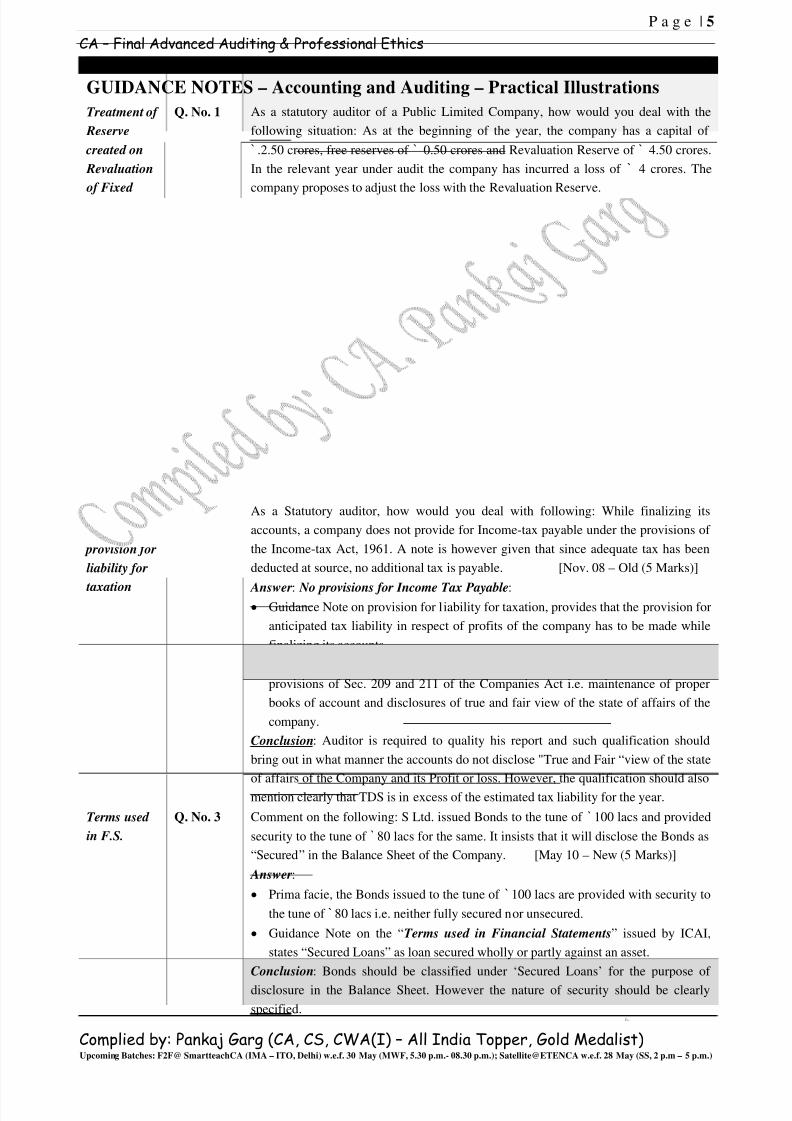

GUIDANCE NOTES – Accounting and Auditing – Practical Illustrations

Treatment of

Reserve

created on

Revaluation

of Fixed

Assets

Q. No. 1 As a statutory auditor of a Public Limited Company, how would you deal with the

following situation: As at the beginning of the year, the company has a capital of

` .2.50 crores, free reserves of ` 0.50 crores and Revaluation Reserve of ` 4.50 crores.

In the relevant year under audit the company has incurred a loss of ` 4 crores. The

company proposes to adjust the loss with the Revaluation Reserve.

Answer: Adjustment of Loss against Revaluation Reserve:

Relevant Provisions: Guidance Note on “Treatment of Reserve created on Revaluation

of Fixed Assets” states that where the value of fixed assets is written up in the books of

account of a company, the corresponding credit appearing as revaluation reserve does

not represent a realised gain and is, therefore, not available for distribution as dividend.

Therefore any accumulated losses / depreciation (including arrears) should not be

adjusted against revaluation reserve since this would amount to setting off actual losses

against unrealized gains.

Conclusion: The auditor should explain to the management that accumulated losses

cannot be adjusted against the revaluation reserve created on revaluation of the fixed

assets. In case the company in question does so, the balance sheet of the company will

not reflect a true and fair view of the state of affairs of the company, keeping in view

the magnitude of the amounts involved, i.e., accumulated losses amount to ` 4 crores

and share capital and reserves amount to ` 3 crores (excluding revaluation reserve).

If the management does not agree with the opinion of the auditor, the auditor may even

issue an adverse report.

Guidance

Note on

provision for

liability for

taxation

Q. No. 2 As a Statutory auditor, how would you deal with following: While finalizing its

accounts, a company does not provide for Income-tax payable under the provisions of

the Income-tax Act, 1961. A note is however given that since adequate tax has been

deducted at source, no additional tax is payable. [Nov. 08 – Old (5 Marks)]

Answer: No provisions for Income Tax Payable: Guidance Note on provision for liability for taxation, provides that the provision for

anticipated tax liability in respect of profits of the company has to be made while

finalizing its accounts.

According to it, non-provision for taxation would amount to contravention of the

provisions of Sec. 209 and 211 of the Companies Act i.e. maintenance of proper

books of account and disclosures of true and fair view of the state of affairs of the

company.

Conclusion: Auditor is required to quality his report and such qualification should

bring out in what manner the accounts do not disclose "True and Fair “view of the state

of affairs of the Company and its Profit or loss. However, the qualification should also

mention clearly that TDS is in excess of the estimated tax liability for the year.

Terms used

in F.S.

Q. No. 3 Comment on the following: S Ltd. issued Bonds to the tune of ` 100 lacs and provided

security to the tune of ` 80 lacs for the same. It insists that it will disclose the Bonds as

“Secured” in the Balance Sheet of the Company. [May 10 – New (5 Marks)]

Answer:

Prima facie, the Bonds issued to the tune of ` 100 lacs are provided with security to

the tune of ` 80 lacs i.e. neither fully secured nor unsecured.

Guidance Note on the “Terms used in Financial Statements” issued by ICAI,

states “Secured Loans” as loan secured wholly or partly against an asset.

Conclusion: Bonds should be classified under ‘Secured Loans’ for the purpose of

disclosure in the Balance Sheet. However the nature of security should be clearly

specified.

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 6/42

P a g e | 6

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

Accounting

for Credit

available in

respect of

MAT under

the IT Act

1961

Q. No. 4 As a Statutory Auditor, how would you deal with the following: For the year ended

31st March, 2011, a company has paid Minimum Alternative tax under section 115 JB

of the Income Tax Act, 1961. The company wants to disclose the same as an ‘Asset’

since the company is eligible to claim credit for the same. [Nov. 09 – New (5 Marks)]

Answer: Disclosure of MAT paid as an Asset:

As per Guidance Note on “Accounting for Credit available in respect of MAT

under the IT Act 1961”, although MAT credit is not a deferred tax asset under AS22 , yet it give rise to expected future economic benefit in the form of adjustment of

future income tax liability arising within the specified period.

The Framework for the Preparation and Presentation of Financial Statements,

issued by the ICAI, defines the term ‘asset’ as follows: “ An asset is a resource

controlled by the enterprise as a result of past events from which future economic

benefits are expected to flow to the enterprise.”

MAT paid in a year in respect of which the credit is allowed during the specified

period under the Income Tax Act is a resource controlled by the company as a

result of past event, namely the payment of MAT.

MAT credit has expected future economic benefits in the form of its adjustmentagainst the discharge of the normal tax liability if the same arises during the

specified period. Accordingly, MAT credit is an asset.

Conclusion: If the auditor is satisfied that the probability of the company to claim the

said credit is high, it could recognize the same as an asset. In Balance sheet it should be

shown under the head “Loans & Advances” as “MAT credit entitlement”.

Revised

Accounts of

Companies

Before

Circulation to

Shareholders

Q. No. 5 Comment on the following: The statutory audit of Fortune Limited for the year ended

on 31.03.2009 was completed and auditor also submitted his report with the audited

Financial Statements to the management of the company. Thereafter, the management

of the company approached the auditor to revise certain items in the Financial

Statements. [Nov. 09 – New (5 Marks)]Or

A company wants to amend its accounts after the completion of the audit and adoption

of the Accounts by the Board, but before circulation to the shareholders. It requires its

statutory auditor to report on the amended accounts. State the steps the statutory audit

should adopt in such a situation.

Answer: Revision of F.S.:

As per the Guidance Note on Revised Accounts of Companies Before Circulation to

Shareholders, Mngt. can revise its accounts after adoption on which report has been

issued by the Auditors, but before circulation to the shareholders.

In the instant case, the statutory auditor should ascertain whether the original auditreport along with audited accounts has been circulated to the share-holders.

If not, he can issue a revised report on the amended F.S. subject to following:

(i) Revised accounts must be re-approved by the Board of Directors of the company.

(ii) Ask the company to return all the original copies of the earlier audit report along

with the audited accounts.

(iii) The fact of revision of F.S. with reasons should be incorporated in the Directors’

Report. If it is neither included nor found adequately disclosed in the Director’s

Report, auditor should include the fact with figures and reasons in his revised

audit report to the shareholders.

(iv) Mention specifically that it is a revised audit report.

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 7/42

P a g e | 7

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

Audit of

Payment of

Dividend

Q. No. 6 State your views as an auditor on the following: During the year under audit Z Ltd.

credited to the P & L Account, the entire profit of ` 20 lakhs on the sale of land not

required for its use. You are informed that the directors would like to propose dividend

out of the above profit.

Answer: Payment of dividend out of Capital profits:

Profit of Rs. 20 lakhs on the sale of land is a capital profit. It represents the excess of

sale value over the original cost of the asset, i.e capital profits.

As per Guidance Note on “ Audit of payment of Dividend” the capital profits can be

distributed by a company only if all the following conditions are fulfilled:

1. The articles of association should permit distribution of capital profits.

2. The capital profit which is sought to be distributed should have actually been

realised.

3. The capital profit should remain after a proper valuation has been fairl y taken of

the whole of the assets and liabilities.

Conclusion: The profit arise on sale of land is realized in cash and hence subject to

satisfaction of other conditions can be distributed as dividend. distributable.

Accounting

for

Derivatives

Q. No. 7 As an auditor, how would you deal with the following: XY Ltd. had entered into

derivative transactions in foreign currency which were based on probable export

orders. As at the year end on 31st March, 2011, the mark-to-market (MTM) loss on the

said derivatives was ` 250 lakhs. The company contends that since the MTM loss is

notional and likely to be recouped in the next year, the same need not be provided for.

[Nov. 09 – Old (5 Marks)]

Answer: Derivative transactions (MTM) Loss:

As per ICAI announcement on “ Accounting for Derivatives” the entity is required to

provide for losses in respect of all outstanding derivative contracts at the balance sheet

date by marking them to market, keeping in view the principle of prudence as

enunciated in AS 1 “Disclosure of Accounting Policies”.

Conclusion: In the given case, XY Ltd. should provide for mark to-market (MTM)

losses amounting ` 250 Lakhs. Auditors, should consider for making appropriate

disclosures in their reports if the aforesaid accounting treatment and disclosures are not

made by the company.

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 8/42

P a g e | 8

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

STANDARDS ON AUDITING AND RELATED SERVICES

SA 210 Q. No. 1 What is an audit engagement letter? What are the principal contents of audit engagement

letters?

SA 230 Q. No. 2 As an auditor, how would you deal with the following: The statutory auditor of the Holding

Company demands for the working papers of the auditors of the subsidiary company, of

which you are the auditor. [Nov. 09 – Old (4 Marks)] Answer: Demand of working papers:

As per SA 230, “Audit Documentation” working papers are the property of the auditor.

The auditor may, at his discretion, make portion of or extracts of his working papers

available to his client.

SA 600 “Using the Work of Another Auditors” also states that an auditor should respect

the confidentiality of information acquired during the course of his audit work and

should not disclose such information unless there is a legal or professional duty to

disclose.

As per ICAI Guidelines, statutory auditor of an enterprise do not have right of access to

the audit working papers of the branch auditor. An auditor can rely on the work of another auditor, without having any right of access to the audit working papers of other

auditor.

Conclusion: Statutory auditor of Holding company can not have access to audit working

papers of the subsidiary company’s auditor. He can however, ask the auditor to answer

certain questions about the manner in which the audit is conducted and certain other

clarifications regarding audit.

SA 240 Q. No. 3 As a Statutory Auditor, how would you deal with the following cases: In the books of

accounts of M/s OPQ Ltd. huge differences are noticed between the control accounts and

subsidiary records. The Chief Accountant informs that this is common due to huge volume

of business done by the company during the year.

Answer: Difference between Control Accounts and Subsidiary Records:

The huge differences found between control accounts and subsidiary records in the

books of M/s OPQ Ltd. indicate that there may be material misstatements requiring

detailed examination by the auditor to ascertain the cause.

The contention of Chief Accountant cannot be accepted simply because the company

has done huge volume of business. Such a phenomenon indicates that recording of

transactions is not being done properly or the accounting system fails to capture all

transactions in time.

Having regard to all these circumstances, it appears from the facts of the case that these

differences indicate the possibility of some kind of material misstatements.

According to SA 240 “The Auditors responsibilities relating to Fraud in an audit of

F.S.” , when the auditor comes across such circumstances indicating the possible

misstatements resulting from entity’s procedure, the auditor shall evaluate whether such

a misstatement is indicative of fraud.

In this case, the circumstances indicate the possibility of material misstatements (that

might be due to fraud) and accordingly, the auditor must investigate further to consider

effect on F.S.

Q. No. 4 Explain briefly duties and responsibilities of an auditor in case of material misstatement

resulting from Management Fraud. [Nov. 09 – New (6 Marks)]

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 9/42

P a g e | 9

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

SA - 240 Q. No. 5 Comment on the following: While conducting statutory Audit of ABC Ltd., you come

across IOUs amounting to Rs. 2 crores as against a cash balance shown in books of ` 2.10

crores. You also observe that despite similar high balances throughout the year, small

amounts of ` 50,000 are withdrawn from the bank to meet day-to-day expenses.

[May 09 – New (5 Marks)]

Answer:

According to SA 240 “The Auditors responsibilities relating to Fraud in an audit of

F.S.” , when the auditor comes across such circumstances indicating the possible

misstatements resulting from entity’s procedure, the auditor shall evaluate whether such a

misstatement is indicative of fraud.

In this case, the circumstances indicate the possibility of fraud and accordingly, the auditor

must investigate further to consider effect on F.S.

The Guidance Note on Audit of Cash and Bank balances also mentions that if the entity is

maintaining an unduly large balance of cash, auditor should carry out surprise verification

of cash more frequently to ascertain whether it agrees. If cash in hand is not in agreement

with the book balance, he should seek explanations and if the same are not satisfactory, he

should state this fact appropriately in his Audit Report.

SA 250 Q. No. 6 State briefly the Communication/Reporting requirements as per SA 250 on Non-Compliance in an audit of F.S.:

(i) To the management

(ii) To the users of the auditor's report on the financial statements.

(iii) To the regulatory and enforcement authorities. [May 09 – Old (8 Marks)]

SA 315 Q. No. 7 What are the points to be considered while evaluating the “Knowledge of the Business” in

the conduct of an audit? [May 09 – New (8 Marks)]

SA 500 Q. No. 8 Write short note on: Assessing the reliability of Audit Evidence. [May 09 – Old (4 Marks)]

Q. No. 9 As a Statutory Auditor, how would you deal with the following case: M/s LNK’s group

gratuity scheme’s valuation by actuary shows wide variation compared to the previous

year’s figures. Answer: Using the work of Management Expert as an audit evidence:

SA 500 (Revised), “Audit Evidence” states that the auditor has to evaluate the work of

management expert, say, actuary, before adopting the same.

This becomes more crucial since M/s LNK’s group gratuity scheme’s valuation by

actuary shows wide variation compared to previous year figures. There is no doubt that

appropriateness, reasonableness of assumptions and methods used are the

responsibility of the expert, but the auditor has to determine whether they are

reasonable based on the auditor’s knowledge of the client’s business and result of his

audit procedures.

In the present case, the auditor must verify the reasonableness of assumptions made

and methods adopted by the actuary in the evaluation particularly with reference to

factors such as rate of return on investments, retirement age, number and salary of

employees, etc.

Accordingly, the auditor has to satisfy himself whether valuation done by the actuary

can be adopted, otherwise he may report on his findings for wide variation.

Q. No. 10 Comment on the following: Z Ltd. had appointed an outside expert to assess accrued

gratuity liability of the company. Based on the said report, the company provides Rs. 80

lakhs as gratuity in the financial statements. [May 09 – New (4 Marks)]

SA 505 Q. No. 11 Write short note on: Situations where external confirmations can be used.

Q. No. 12 As a Statutory Auditor, how would you deal with the following: The accountant of C Ltd.

has requested you, not to send balance confirmations to a particular group of debtors since

the said balances are under dispute and the matter is pending in the Court.

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 10/42

P a g e | 10

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

SA 510 Q. No. 14 Comment on the following: You have been appointed as the auditor of Good Health Ltd.

for 2010-11 which was audited by CA Trustworthy in 2009-10. As the Auditor of the

company state the steps you would take to ensure that the Closing Balances of 2009-10

have been brought to account in 2010-11 as Opening Balances and the Opening Balances

do not contain misstatements. [Nov. 08 – New (5 Marks)]

Q. No. 15 What are the procedures to be followed by a Statutory Auditor in the audit of opening

balances if the financial statements for the preceding year were audited by another auditor?

[Nov. 09 – Old (8 Marks)]

SA 520 Q. No. 16 As an auditor to what extent you can rely on Analytical Procedures.

SA 530 Q. No. 17 “An auditor while analyzing the errors in a sample need not consider the qualitative aspects

of errors detected.” Comment.

SA 550 Q. No. 18 As a Statutory Auditor, how do you verify the existence of Related Parties and disclosure

of Related Party Transactions? [Nov. 09 – Old (8 Marks)]

Answer: Verification of Existence of related parties and disclosures:

SA 550 (Revised) “Related Parties” requires that during the audit, the auditor shall

remain alert, when inspecting records or documents, for arrangements or otherinformation that may indicate the existence of related party relationships or

transactions that management has not previously identified or disclosed to the auditor.

In particular, the auditor shall inspect the following for indications of the existence of

related party relationships or transactions that management has not previously

identified or disclosed to the auditor:

(a) Bank, legal and third party confirmations obtained during the audit;

(b) Minutes of meetings of shareholders and of TCWG; and

(c) Such other records or documents as the auditor considers necessary.

Records or Documents that auditor may inspect: Entity income tax returns.

Information supplied by the entity to regulatory authorities.

Shareholder registers to identify the entity’s principal shareholders.

Statements of conflicts of interest from management and TCWG.

Records of the entity’s investments and those of its pension plans.

Contracts and agreements with key management or TCWG.

Significant contracts and agreements not in the entity’s ordinary course of business.

Specific invoices and correspondence from the entity’s professional advisors.

Life insurance policies acquired by the entity.

Significant contracts re-negotiated by the entity during the period.

Internal auditors’ reports.

Documents associated with the entity’s filings with a securities regulator (Prospectus).

Examinations of arrangements that may indicate the existence of related party

relationships or transactions:

Participation in unincorporated partnerships with other parties.

Agreements for the provision of services to certain parties under terms and conditions

that are outside the entity’s normal course of business.

Guarantees and guarantor relationships.

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 11/42

P a g e | 11

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

SA 560 Q. No. 19 Briefly explain: Audit procedures on subsequent events. [Nov. 09 – New (4 Marks)]

Q. No. 20 Comment on the following: A Co. Ltd. has not included in the Balance Sheet as on 31-03-

2011 a sum of ` 1.50 crores being amount in the arrears of salaries and wages payable to the

staff for the last 2 years as a result of successful negotiations which were going on during

the last 18 months and concluded on 30-04-2011. The auditor wants to sign the said

Balance Sheet and give the audit report on 31-05-2011. The auditor came to know the

result of the negotiations on 15-05-2011. [Nov. 10 – New (5 Marks)]

Answer: Treatment of subsequent Events:

SA 560 “Subsequent Events” requires that in respect of events occurring between the

date of F.S. and date of the AR, the auditor shall perform audit procedures to obtain

sufficient & appropriate audit evidence to ensure that events which require adjustments

or disclosure in the F.S. have been identified.

If auditor identifies events that require adjustment or disclosure in the F.S., the auditor

should determined whether each such event is appropriately reflected in the F.S.

The auditor shall request the management to provide a “Written Representation” that all

events occurring subsequent to the date of the F.S. and requires adjustment or disclosure

have been adjusted or disclosed.

Conclusion: The facts of the case indicates the event as of adjusting nature as per AS – 4

“Contingencies and Events Occurring after the Balance Sheet date” and requires

adjustment in assets and liabilities, which has not been made by the management. Auditor

should request mngt. to adjust the sum of ` 1.50 crores by making provision for expenses. If

the mngt. does not accept the request the auditor should qualify the AR.

SA 570 Q. No. 21 What are the Financial indications to be considered by an auditor for evolution of the going

Concern assumption? [Nov. 08 – Old (4 Marks)]

Q. No. 22 Comment on the following: A Company's net worth is eroded and creditors are unpaid due

to liquidity constraints. The management represents to the statutory auditor that the

promoter's wife is expected to give an unsecured loan to meet the liquidity constraints and

that negotiations are underway to secure large export orders. [May 09 – New (4 Marks)]

Answer: Appropriateness of Going Concern Assumption:

In this case, it is subjective, but prima-facie a mere expectation of future cash flows from

the promoter’s wife without any firm commitment and the possibility of an export order

being negotiated, may not that be sufficient appropriate audit evidence of mitigating factors

for resolving the going concerns question under SA 570 “Going Concern”.

SA 580 Q. No. 23 What is meant by “Written Representations” and indicate to what extent an auditor can

place reliance on such representations.

Q. No. 24 An auditor of Mohan Ltd. was not able to get the confirmation about the existence and

value of certain machineries. However, the management gave him a certificate to prove the

existence and value of the machinery as appearing in the books of account. The auditor

accepted the same without any further procedure and signed the audit report. Is he right in

his approach?

Answer: Validity of Management Representation:

The physical verification of fixed assets is the primary responsibility of the

management. The auditor, however, is required to examine the verification programme

adopted by the management.

He must satisfy himself about the existence, ownership and valuation of fixed assets.

In the case of Mohan Ltd., the auditor has not been able to verify the existence and

value of some machinery despite the verification procedure followed in routine audit.

He accepted the certificate given to him by the management without making any further

enquiry.

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 12/42

P a g e | 12

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

SA – 580 As per SA 580 “Written Representation” the representations received from management

are recognised as audit evidence, but they do not constitutes Sufficient and

appropriateness.

Auditor is required to seek corroborative audit evidence from other sources inside or

outside the entity, to evaluate whether such representations are reasonable and

consistent with other evidences.

Representation received from Management cannot be a substitute for other audit

evidence that the auditor could reasonably expect to be available.

If the auditor is unable to obtain sufficient appropriate audit evidence that he believes

would be available regarding a matter, which has or may have a material effect on the

financial information, this will constitute a limitation on the scope of his examination

even if he has obtained a representation from management on the matter.

Conclusion: The approach adopted by the auditor is not right.

SA 600 Q. No. 25 “There should be sufficient liaison between a principal auditor and other auditors”. Discuss

the above statement and state in this context the reporting considerations, when the auditor

uses the work performed by other auditor.

SA 610 Q. No. 26 Enumerate, in brief, the important aspects to be evaluated by the external auditor in

determining the efficiency and extent of reliance to be placed on the work and function of

an Internal Auditor.

Q. No. 27 You are appointed as statutory auditor of X Ltd. X Ltd. has an internal audit system and

reports for the same are given to you. Mention the factors you will consider to ensure that

the said system of internal audit of X Ltd. is commensurate with the size of the company

and nature of its business. [May 09 – New (8 Marks)]

SA 620 Q. No. 28 Briefly explain how an auditor can use the work of an expert.

SA 710 Q. No. 29 Write short note on: Auditor’s responsibilities regarding comparatives.

Q. No. 30 The audit report of P Ltd. for the year 2009-10 contained a qualification regarding nonprovision of doubtful debts. As the statutory auditor of the company for the year 2010-11,

how would you report, if:

(i) The company does not make provision for doubtful debts in 2010-11?

(ii) The company makes adequate provision for doubtful debts in 2010-11?

[June 09 – New (8 Marks)]

Answer:

As per SA 710, when the Audit Report on the prior period intended a qualified opinion and

the said matter is:

(i) Unresolved and results in an modification of the AR regarding current year’s figures,

his report should be modified regarding corresponding figures.(ii) Resolved and properly dealt with in the F.S., the current report need not refer to such

modification.

In the instant Case, if P Ltd. does not make provision for doubtful debts the auditor will

have to modify his report for both current and previous year’s figures.

If however, the provision is made, the auditor need not refer to the earlier years

modification.

SRE

2400

Q. No. 31 The directors of C Ltd. are concerned about the reliability and usefulness of the monthly

financial management information that they receive. As a result, the company’s auditors

have been engaged to review the system and the information it generates, and to report their

conclusions. What an ordinary procedure includes for the review of financial statements?

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 13/42

P a g e | 13

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

SRS

4400

Q. No. 32 What is engagement to perform agreed upon procedures. What are the general principles

governing an agreed upon procedures engagement.

SRS

4410

Q. No. 33 You have been asked by a company to compile financial statements for the purpose of

obtaining loan from a Bank. Draft a report to be given to the Management for the same.

[Nov. 08 – Old (8 Marks)]

Q. No. 34 Draft an illustrative engagement letter for an engagement to compile financial statements of

DEF Ltd. [Nov. 09 – Old (8 Marks)]

Q. No. 35 While compiling the financial statements of a concern, you observed that the input

information supplied by the concern is incomplete, incorrect and few of the Accounting

Standards have not been followed. Describe, in brief, the procedure you will follow in the

above.

Answer: Compilation of Financial Information:

1. As per SA 4410 “Engagements to Compile Financial Information”, an accountant

would normally have to rely upon the management for information to compile the F. S.

in a compilation engagement.

2. If in the course of compilation of financial statements, it is observed that the

information supplied by the entity is incorrect, incomplete or otherwise unsatisfactory,

the accountant should perform following procedures:

Make any enquiries of management to assess the reliability and completeness of

the information provided;

Assess internal controls prevailing in the entity; and

Verify any matters or explanations.

3. The accountant may also request the management to provide additional information.

This may be asked in the form of management representation letter.

4. If the management refuses to provide additional information, the accountant should

withdraw from the engagement, informing the entity of the reasons for such

withdrawal.

5. If one or more ASs are not complied with, the same should be brought to the notice of

the management and if the same is not rectified by the management, the accountant

should include the same in notes to the accounts and the compilation report to the

management.

Q. No. 36 Comment on the following: You are appointed to compile financial statements of Y & Co.

for tax purposes. During the course of work, you learn that the inventory is grossly

understated. On pointing the same, the partners of Y & Co. tell you that since you are not

conducting an audit, the said figures duly certified by the firm should be accepted.

[May 09 – New (5 Marks)]

Answer:

As per SRS 4410 “Engagement to Compile Financial Information “if an accountant

becomes aware of material misstatements, the accountant should persuade the management

to carry out necessary amendments in the F.S. or other compiled financial information. If

such amendments are not made and the F.S. are still considered to be misleading the

accountant should withdraw from the engagement.

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 14/42

P a g e | 14

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

ACCOUNTING STANDARDS

Applicability

of AS

The Preface to the Statements of AS clarifies that the ASs are issued "for use in the presentation of

G.P.F.S. issued to the public by such commercial, industrial or business enterprises, as may be

specified by the Institute from time to time and subject to the attest function of its members.

The term 'G.P.F.S. includes balance sheet, statement of profit and loss and other statements and

explanatory notes which form part thereof, issued for use of shareholders/ members, creditors,employees and public at large".

As far as companies, whether limited or unlimited incorporated under the Companies Act, 1956

are concerned, all such companies are expected to adhere to specified AS in terms of section

211(3A) of the said Act.

The compliance with AS has to be examined by the auditors while auditing general purpose F. S.

which are statutorily required to be audited under any law. Thus, compliance with AS is required

to be examined by an auditor in an audit of F. S. of individuals and non-corporate enterprises (for

example: Partnership firms, Societies, trusts, HUF, AOP) only where the F.S. are statutorily

required to be audited under any law.

The AS are also applicable to commercial, industrial or business activities of even charitable orreligious organisations. Accounting Standards do not apply to those organisations whose entire

activities are not of commercial, industrial or business nature, e.g., an organisation collecting

donations to finance education of poor children. However, even if a very small proportion of the

activities of an entity is commercial, industrial or business in nature, the accounting standards will

apply to all its activities.

Q. No. 1 Comment: The AS issued by the ICAI need to be followed only by limited companies

and not by partnership firms or proprietorships.

Q. No. 2 As an auditor, how would you deal with the following: In the audit of an organization

whose objects are charitable or religious, the organization holds that the Accounting

Standards are not applicable to it since only a very small proportion of its activities are

business in nature. [May 09 – Old (5 Marks)]

Companies

(AS) Rules

2006

Small and

Medium

Size

Company

(i) Whose equity or debt securities are not listed or are not in the process of listing on

any stock exchange, whether in India or outside India;

(ii) Which is not a bank, financial institution or an insurance company;

(iii) Whose turnover (excluding other income) does not exceed ` 50 Cr. in the

immediately preceding accounting year,

(iv) Which does not have borrowings (including public deposits) in excess of ` 10 Cr.

at any time during the immediately preceding accounting year; and

(v) which is not a holding or subsidiary company of a company which is not a small

and medium-sized company.

Explanation: For this purpose, a company shall qualify as a Small and Medium Sized

Company, if the conditions mentioned therein are satisfied as at the end of the relevant

accounting period.

Q. No. 3 Comment whether the following Companies can be classified as a Small and Medium

Sized Company (SMC) as per the Companies (Accounting standards) Rules, 2006:

(i) A Pvt. Ltd., a subsidiary of a multinational company listed on London Stock

Exchange. It has a turnover of ` 12 crores and borrowings of ` 5 crores.

(ii) B Pvt. Ltd. has a turnover of ` 45 crores, other income of ` 7 crores and bank

borrowings of Rs.9 crores.

(iii) C Ltd. has appointed Merchant bankers to prepare a Red-herring prospectus for

the purpose of filing the same with SEBI. [Nov. 08 – Old (12 Marks)]

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 15/42

P a g e | 15

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

Companies

(AS) Rules

2006

Answer: Determination of Small and medium Sized Company:

(i) Since A Pvt. Ltd. is a subsidiary of MNC which is listed, on London Stock

Exchange (and is therefore not a SMC), A Pvt. Ltd. cannot be a SMC. The

turnover and borrowings are not relevant in this case.

(ii) Since B Pvt. Ltd. has a turnover of ` 45 corers and borrowing of ` 9 corers, it will

be classified as SMC. Note: Other incomes are not considered

(iii) Since C Pvt. Ltd. has appointed merchant bankers to prepare a Red Herring

Prospectus for the purpose of filling the same with SEBI, it is in the process of

listing on a Stock Exchange, therefore C Ltd. cannot be classified as a SMC.

Q. No. 4 As a Statutory auditor, how would you deal with following: A company which satisfies

the conditions of a Small and Medium sized Company (SMC) as per Companies (AS)

Rules, 2006 has represented that it does not require to give disclosures required by AS-3

“Cash Flow Statements” and AS-18 “Related Party Disclosures” in its F.S.

[Nov. 08 – Old (4 marks)]

Answer: Compliance of AS-3 and AS-18 by SMC :

As per the Companies (AS) Rules, 2006, Compliance of Certain ASs is not mandatory,

but optional.

AS-3, as per the above Rules is not mandatory for SMC. However, AS-18 is required to

be complied with mandatorily.

Conclusion: T company, even if it is a SMC, will have to give disclosures for:

(i) related party relationships, and

(ii) transactions between a reporting enterprise and its related parties.

Q. No. 5 Comment: The management tells you that there is no need for them to follow AS

specified by the ICAI as these are for the auditor to follow.

Answer: Observance of AS:

In terms of Companies (AS) Rules, 2006 prescribed by the C.G. u/s 211(3)(c) of the

Companies Act, 1956, it is mandatory for a Company to follow all the prescribedAS while preparing and presenting its F.S.

If a Company does not follow AS, the auditor is required to give a qualification in

his report in terms of section 227(3) of the Companies Act, 1956.

Infact directors of the companies are also required to give a written statement as

part of Director Responsibility Statement u/s 217 of the Companies Act that all the

AS prescribed has been followed and there are no discrepancies.

Conclusion: The contention of the company is not correct.

Q. No. 6 LMN Pvt. Ltd. is a dealer in government securities. The turnover on account of sale of

securities for the year ended 31st March, 2011 is ` 85 crores whereas the net profit is

` 0.10 Cr. While finalizing the accounts the company did not prepare the Cash FlowStatement. [May 10 – Old (5 Marks)]

Answer: Exemption for applicability of AS – 3, preparing Cash Flow Statement is

available only to Small and Medium Size Companies) preparation of Cash

Flow Statement, as per AS – 3 is now made mandatory in respect of the

following enterprises:

(i) Enterprises whose equity of debt securities are listed on a recognized

Stock Exchange in India and Enterprises that are in the process of issuing

equity or debt securities that will be listed on a recognized Stock

Exchange in India.

(ii) All other Commercial, industrial and business reporting enterprises,whose turnover for the accounting period exceeds Rs. 50 crores.

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 16/42

P a g e | 16

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

In the instant case, LMN Pvt. Ltd. did not prepare the Cash Flow Statement,

even its turn over exceeded Rs. 50 crores. It is not considered as a small and

medium size company as per Companies (AS) Rules, 2006 (AS-3) as

discussed earlier, hereinabove.

Therefore, if LMN Pvt. Ltd. does not prepare cash flow statement it is a

violation of AS-3 and section 211(3C) of the Companies Act, 1956.

The auditor will have to accordingly qualify his report that 211(3C) is not

complied with, the profit & loss account would give a ‘True & Fair View’.

AS-2 Q. No. 7 A company was engaged in the business of buying IMFL (Indian Made Foreign Liquor)

and beer and selling same through retail vending shops and bars run by it. The company

sold beer to some of the customers who consumed them in bars run by it and left the

bottles behind. (Technically, these bottles were the property of the customers.) These

bottles were later on disposed off by the company. Answer the followings:

1. Are these bottles left behind by the customers “assets” of the company?

2. Are they “inventories”?

3. If they are “inventories”, how they should be valued?

4. Can the “bottles” be valued at net realisable value and treated as “income”?

Answer:1. An asset is a resource controlled (not necessarily “owned”) by an enterprise as a

result of past events from which future economic benefits to the enterprise are

expected. In assessing whether an item meets the above definition of “assets”, the

consideration should be given to economic reality and substance and not merely

legal form. Accordingly, the bottles can be considered as “assets” of the company.

2. The stock of empty bottles is “inventory” as the company holds them for sale in the

ordinary course of its business of running the bars.

3. These bottles should be valued at the lower of cost and NRV. However, the cost of

purchase and selling price of beer / IMFL are both inclusive of cost of bottles as beer

/ IMFL cannot be sold without bottles – the primary packing. Practically, the emptybottles do not appear to cost anything to the company (i.e. zero cost), if that be the

case, the bottles should be reflected at nominal value of Re.1.

4. It would not be correct to value the bottles at NRV with credit being given to

“income” as the bottles have not been sold at the balance sheet date.

Q. No. 8 As an auditor state your views on the following: Included under Current Assets of XYZ

Ltd. is inventory aggregating to ` 20 crores. A part of the said inventory manufactured

for export had to be sold earlier at a discounted price offshore due to moisture content

present at the time of delivery. A part of similar inventory is included in `20 crores.

Answer: Valuation of Damaged Inventory:

Auditor is required to examine what part of the inventory is included in the

inventory valued at ` 20 crores.

He will also have to satisfy himself that whether such part left with the company

has also been damaged on account of moisture content.

If required, the auditor may obtain a certificate from an expert about the condition

of the inventory.

Thereafter, it should be verified whether the principle of valuation enunciated in AS

2 “Valuation of Inventories” have been followed. The standard requires that the

inventories should be valued at the lower of cost or NRV.

Conclusion: In the present case the auditor shall satisfy himself whether the balance

inventory lying with the company is carrying the same quality issue. If yes, than value

of inventory will be revised based on its NRV(if lower than cost).

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 17/42

P a g e | 17

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

Q. No. 9 The management tells you that WIP is not valued since it is difficult to know the same

in view of multiple processes involved and in any case opening and closing WIP would

be more or less the same.

Answer: Valuation of WIP: As per AS-2, “Valuation of inventories” inventories

includes any item held in the process of production. This is known as WIP.

Company is required to find out the stage of completion of products and value of the

same. In certain cases, due to nature of the product and the manufacturing process

involved, physical verification of WIP may be impracticable. But in such cases, the

advice of an expert can be taken. The value of such WIP is normally done by taking the

basic raw material cost and adding thereto the proportionate factory overhead cost

incurred up to the stage of completion.

Valuation of WIP is important due to following:

WIP is an item of Manufacturing, Trading & Profit & Loss A/c and also forming

part of current assets, is relevant and can not be ignored. Omitting WIP will result

in under or over statement of profit and current assets.

Part II of Schedule VI to the Companies Act also prescribes that the figures of

opening and closing balances of stock and WIP be disclosed in the profit & loss

account. Part I of the same schedule requires that the mode of valuation of stock be

shown in the Balance Sheet.

Conclusion: The argument of the management that the opening and closing WIP would

be more or less the same is not justified because the cost incurred for raw materials and

overheads would be different and would give different value of opening and closing

WIP. Taking into consideration all the above aspects, management is wrong and if WIP

is not valued or taken into consideration, auditor should qualify his report.

AS - 4 Q. No. 10 During the course of audit of D Co. Ltd. you as an auditor have observed that Inter

corporate deposit of ` 50 lakhs has been over due. The D Co. Ltd. has disclosed this in

the notes to accounts note No. 15 in schedule no. 21 stating that ` 50 lakhs is over due

from XYZ Co. Ltd. and the said company is in the process of liquidation. The

management is taking steps to appoint the liquidator.’ [Nov. 10 – New (5 Marks)]

Answer:

As per AS 4 “Contingencies and Events occurring after the Balance Sheet Date”,

adjustments to assets and liabilities are required for events occurring after the balance

sheet date that provide additional information materially affecting the determination of

the amounts relating to conditions existing at the balance sheet date.

In the instant case, it appears from the note no 15 that the overdue of outstanding inter

corporate deposit may not be realisable in full. The company is in the process of

liquidation, makes it clear that on the balance sheet date, the amount of deposit is not

safe and is not likely to be realised.

Conclusion: As per AS 4 provision for the loss was required in the accounts.

Accordingly, auditor should qualify the Audit Report.

Q. No. 11 State your views as an auditor on the following: V Ltd. had announced a voluntary

retirement plan for its employees on January 1, 2010. The scheme is scheduled to close

on June 30, 2010. The scheme envisaged an initial lump sum payment of maximum of

Rs. 2 lakhs and monthly payments over the balance period of service of employees

coming under the plan. 200 employees opted for the scheme as on March 31, 2010. The

total lump sum payment for these employees would be Rs. 250 lakhs and the aggregate

of future payments to them would amount to Rs.1,500 lakhs. However, no payment had

been made to the employees under the scheme up to March 31, 2010. Nor the company

made any provision in its accounts towards any liability under the scheme.

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 18/42

P a g e | 18

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

AS - 4 Answer: Event occurring after the B/S Date:

Relevant Provision: As per AS- 4 on 'Contingencies and Events Occurring After the

Balance Sheet Date', assets and liabilities should be adjusted for events occurring after

the balance sheet date that provide additional evidence to assist the estimation of

amounts relating to conditions existing at the balance sheet date or that indicate that the

fundamental accounting assumption of going concern is not appropriate.

Facts of the case: A condition existed on the balance sheet date (31st March, 2010)

regarding the liability towards the Voluntary Retirement Plan since the management

started the scheme in the month of January, 2010 and 200 employees opted for the

scheme as on March 31, 2010.

Conclusion: Since it was probable that future events will confirm that a liability has

been incurred on the balance sheet date and that the amount could be estimated on

reasonable basis, a provision for payments under the scheme would be required to be

made for an appropriate amount for the aforesaid number of employees.

Q. No. 12 Arya Ltd. was under audit for the year ended 31.03.2010. An appeal filed by Arya Ltd.

against the demand of Excise Duty of ` 26 crores was pending before the Supreme

Court for which neither provision was made nor was disclosed in the notes to the

financial statements. On 12th July, 2010, the auditor came to know through paper

reports that the point involved in the appeal of Arya Ltd. was adjudicated by the

Supreme Court in the case of some other assessee, which is in favour of the department

of Excise Duty. The auditor insisted that provisions be made of ` 26 crores in the

financial statements. The Management was of the view that since its own case is still

pending, no provision is called for. It was also of the view that the event does not have

any effect on the financial position of the company on the date of the Balance Sheet. Is

the view of the Management tenable?

Answer: Subsequent Events:

Relevant Provisions:

As per AS- 4 on 'Contingencies and Events Occurring After the Balance Sheet

Date', assets and liabilities should be adjusted for events occurring after the balance

sheet date that provide additional evidence to assist the estimation of amounts

relating to conditions existing at the balance sheet date or that indicate that the

fundamental accounting assumption of going concern is not appropriate.

SA 560 on “Subsequent Events” lays down that the “auditor should consider the

effect of subsequent events on the F.S. and on the auditor’s report”.

Explanation:

The issue involved in the appeal of Arya Ltd. was similar to the point in case of

some other company and since the appeal of that company was decided against that

company and in favour of the Excise Department, it is necessary for Arya Ltd. to

make a provision of Rs. 26 crores.

Conclusion: The view of the management that its own appeal is undecided or that it has

no effect on the financial position as on 31.03.2006 is not at all tenable. Since the

financial position is materially affected, the auditor should express a qualified opinion

or an adverse opinion as may be appropriate.

AS - 5 Q. No. 13 As a statutory auditor, how would you deal when PQ Ltd., as part of overall cost cutting

measure announced voluntary retirement scheme (VRS) to its employees, to reduce the

employee strength. During the first half year ended 30.9.2010 the company paid a

compensation of ` 72 lakhs to those who availed the scheme. The Chief Accountant has

reflected this payment as part of regular salaries and wages paid by the company. Is this

correct?

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 19/42

P a g e | 19

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

AS - 5 Answer: Treatment of Ordinary activity with large amount:

As per AS 5, “Net Profit or Loss for the Period, Prior Period Items and Changes in

Accounting Policies” the payment made to its employees on account of VRS as an

overall cost cutting measure is an ordinary activity.

AS 5 requires that when items of income and expense within profit or loss from

ordinary activities are of such size, nature or incidence that their disclosure is

relevant to explain the performance of the enterprise for the period, the nature and

amount of such items should be disclosed separately.

Though this is not an extraordinary item, but the nature and amount of this

expenses is such that its separate disclosure is required to allow the users to

understand the financial position and performance of the company.

Conclusion: Compensation of ` 72 Lakhs paid towards VRS availed by employees

should be shown separately in the profit and loss account of PQ Ltd.

Q. No. 14 State your views as an auditor on the following: Y Ltd. provided ` 25 lakhs for

inventory obsolescence in 2009-2010. In the subsequent years, it was determined that

50% of such stock was usable. The company wants to adjust the same through prior

period adjustment account as the provision was made in the earlier year.

Answer: Prior Period Adjustment:

As per AS 5 on "Net Profit or Loss for the Period, Prior Period Items and Changes

in Accounting Policies", prior period items are income or expenses which arise in

the current period as a result of errors or omissions in the preparation of the F.S. of

one or more prior periods.

The write-back of provision made in respect of inventories in the earlier year does

not constitute prior period adjustment since it neither constitutes error nor omission.

An estimate may have to be revised if changes occur regarding the circumstances

on which the estimate was based, or as a result of new information, moreexperience or subsequent developments.

The revision of the estimate, by its nature, does not bring the adjustment within the

definitions of an extraordinary item or a prior period item.

Conclusion: Revision of the estimate does not bring the resulting amount of ` 12.5

lakhs within the definition either of a prior period item or of an extraordinary item. The

amount, however, involved is material and requires separate disclosure to understand

the financial position and performance of an enterprise. Accordingly, adjustment in the

value of the inventory through prior period item would not be proper.

AS - 7 Q. No. 15 Comment: B Co. Ltd. is engaged in the business of developing mass scale housing

projects including development of small commercial complexes. The flats/commercialspaces are booked by the public and are allotted by way of allotments letter to each

allottee. Major construction activities pertaining to buildings are undertaken of

flats/commercial spaces is given to allottees by executing legal document. The CEO of

the B Co. says that AS 7 is not applicable to the company. [Nov. 09 – New (5 Marks)]

Answer: Applicability of AS-7 :

AS 7 (Revised) “Accounting for Construction contracts” states that, "This Statement

should be applied in accounting for construction contracts in the F.S. of contractors.

The revised AS 7 is silent about its applicability to construction activities undertaken

by enterprises on their own account and not as contractors.

The matter was considered by Expert Advisory committee of the Institute and theyare of the view that the revised AS 7 is not applicable to such enterprises.

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 20/42

P a g e | 20

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

Conclusion: The activity of developing housing projects on its own account can be

considered as a commercial venture by the company in the nature of production activity

and, therefore, should be construed as such. Accordingly, the flats/commercial spaces

should be identified as inventories in accordance with AS 2 and revenue should be

recognition in accordance with AS 9.

AS - 9 Q. No. 16 A Ltd. prepared an invoice for an export consignment on FOB basis on 30 th March,

2010. The goods were dispatched from the factory on 30th March, 2010 and the Bill of

Lading was made on 3rd April, 2010. A Ltd. had booked the invoice in the Sales

Register for March, 2010. [May 10 – Old (5 Marks)]

Answer: Revenue recognition in case of export sale:

As per AS-9 ‘Revenue Recognition’ revenue involving sale of goods is to be

recognized on transfer of significant risk and reward of ownership to the buyer.

In the instant case, A Ltd. has invoiced the goods and they have left the factory on 30 th

March, 2011. However the same is for export and the bill of landing is dated 3 rd April

2011.

Conclusion: The sale should be therefore, recognized in April 2011. The auditor will

therefore have to qualify his report stating that revenues are overstated to that extent.

Q. No. 17 State your views as an auditor on the following: T Ltd. purchased goods on credit for

` 5 crores for export from ABC Ltd. Upon the export order being cancelled, T Ltd.

decided to sell the same in the domestic market at a discounted price. Accordingly ABC

Ltd was requested to offer a price discount of 25%. ABC Ltd. wants to adjust the sales

figure to the extent of discount requested by T Ltd.

Answer: Treatment of discount subsequent o sale:

ABC Ltd. had sold goods on credit worth ` 5 crores to T Ltd. and, therefore, the sale

was complete in all respects. T Ltd' s decision to sell the same in the domestic

market at a discount does not affect the amount booked under sales by ABC Ltd.

The price discount of 25% offered by ABC Ltd. at the request of T Ltd. was not in

the nature of discount given during the ordinary course of trade.

As far as ABC Ltd. is concerned, there appears to be an uncertainty relating to

collectability, which has arisen subsequent to the time of sale.

Therefore, it would be appropriate to make a separate provision to reflect the

uncertainty relating to collectability rather than to adjust the amount of revenue

originally recorded.

Conclusion: Discount should be charged to the P & L A/c separately and not shown as

deduction from the sales figure.

Q. No. 18 Comment: LM Ltd. has 2 divisions L and M. The finished products of division L are

transferred to division M where further processing is carried out before sale to

customers. To achieve transparency and accountability between the divisions, division

L raises an invoice on division M at cost plus normal margins. At the year end the

unrealized profits on inter-division stocks are eliminated. However, the transfers are

recorded at the invoice value as sales and purchases in the respective divisions for the

purpose of preparing the Profit and Loss Account. Suitable disclosures, for this are

given in then ‘Notes to Accounts’.

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 21/42

P a g e | 21

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

AS - 9 Answer: Revenue recognition in case of inter division transfers:

The recognition of inter-divisional transfers as sales is an inappropriate accounting

treatment and is inconsistent with AS 9.

In case of inter-divisional transfers, risks and rewards remain within the enterprise

and also there is no consideration from the point of view of the enterprise as a

whole. Thus, the recognition criteria for revenue recognition has not been fulfilled

in respect of inter-divisional transfers.

Conclusion: In the instant case, LM Ltd cannot recognise inter-division transfers from

L to M as sales and the same will have to be eliminated during finalisation. If not so

done, the statutory auditor will have to qualify his report.

Q. No. 19 As an auditor, state your view on the following: (a) M Ltd. manufactures machinery

used in Steel Plants. It quotes prices in various tenders issued by Steel Plants. As per

terms of contract, full price of machinery is not released by the steel plants, but 10%

thereof is retained and paid after one year if there is satisfactory performance of the

machinery supplied. The company accounts for only 90% of the invoice value as sales

income and the balance amount in the year of receipt to the extent of actual receipts

only.

Answer: Recognition of Revenue:

AS 9 on ‘Revenue Recognition’, states that revenue from sale of goods should be

recognised as and when sale is made if following conditions are satisfied:

Property in the goods has been transferred for a price

all significant risks and rewards of ownership have been transferred, and

seller retains no effective control of the goods associated with ownership and

no significant uncertainty exists regarding the amount of consideration.

In the present case, the goods, as well as the risks and rewards of ownership have been

transferred to the steel plants. The invoice raised by M Ltd. is for the full price, but

10% less is received as the same is kept as ‘Retention Money’.

Conclusion: Under the circumstances, revenue is required to be recognised at the full

invoice price. Depending on the past experience of recovering the balance 10% from

the steel plants, M Ltd. can, make a provision for sales income which is not likely to

realise. In the absence of the above, the auditor will have to qualify his report.

AS - 10 Q. No. 20 Comment: In the notes to accounts of C Co. Ltd. as on 31-03-2011 Note no. 11 states

that ‘Certain machinery items are lying at customs warehouses and company has paid `

900 lakhs up to 30-06-2010 as detention charges, out of which a sum of ` 580 lakhs is

written back during the year 2010-11 based on settlement with the concerned

authorities in respect of a major spares of machinery. For the remaining machinery item

negotiations are pending and a provision of ` 44 lakhs is made. As such total amount of

` 364 lakhs paid/provided on account of detention charges have been capitalized and

included in the fixed assets/capital work in progress. The management is of the view

that these expenses are directly attributable to the acquisition of the related FixedAsset.’ [Nov. 10 – New (5 Marks)]

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 22/42

P a g e | 22

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

AS - 10 Answer: Capitalisation of Detention Charges:

As per AS – 10 “Accounting for Fixed Assets” the cost of an item of fixed assets

comprises its purchase price, including import duties and other non-refundable taxes or

levies and any directly attributable cost of bringing the asset to its working condition

for its intended use; any trade discounts and rebates are deducted in arriving at the

purchase price. Examples of directly attributable costs are:

1. site preparation ;

2. initial delivery and handling costs ;

3. installation cost, such as special foundations for plant ; and

4. professional fees, for example fees of architects and engineers.

Conclusion: Detention charges, being in the nature of penalty levied by Customs for

not removing the articles within specified period from custom port can not be

considered as directly attributable cost.

Treatment done by the company is incorrect. The auditor should qualify the report

appropriately mentioning the effect on Balance sheet and Profit and Loss Account.

Q. No. 21 F Limited includes in the Schedule of Inventory, those items of Fixed Assets whichhave not been in active use and held for disposal, as inventory item.

[May 10 – New (5 Marks)]

Answer: Treatment of assets held for Disposal

AS-10 “Accounting for Fixed Assets” requires that the items of fixed assets that

have been retired from active use and are held for disposal be stated at the lower of

their net book value and NRV and are shown separately in the financial statements.

As per AS-2 “Valuation of Inventories” , “inventories” are assets “held for sale in

the ordinary course of business, in the process of production for such sale; or in the

form of materials or supplies to be consumed in the production process or in the

rendering of service”.

Conclusion: Inclusion of fixed assets, not in active use and held for disposal, as

inventory item in the schedule of inventory is not in line with the requirements of AS-

10 and AS-2. Such fixed assets should be stated at lower of net book value and NRV

and are shown separately in F.S.

Q. No. 22 Comment: An old car of a company having a nominal book value has found a buyer,

who is willing to pay ` 1 lakh for it. The company proposes not to sell the car, but to

neglect its valuation in its accounts at `1 lakh. Should the auditor permit the company

to do so?

Answer: Valuation of Fixed Assets:

Relevant provisions:

The old car formed part of the fixed assets of the company and ordinarily the same

should be valued at actual cost less depreciation written off. The market price of any

of such assets is not relevant for balance sheet valuation of a going concern.

There is no prohibition in law for revaluation of fixed assets. But when all other

assets are presumably shown at historical cost, revaluation only of one motorcar

seems illogical and has the effect of distorting the overall view of the accounts.

AS- 10, “Accounting for Fixed Assets” also clarifies, when a fixed asset is revalued

in F.S., an entire class of assets should be revalued, or the selection of assets for

revaluation should be made on a systematic basis and the basis should be disclosed.

8/4/2019 Audit Workbook

http://slidepdf.com/reader/full/audit-workbook 23/42

P a g e | 23

CA – Final Advanced Auditing & Professional Ethics

Complied by: Pankaj Garg (CA, CS, CWA(I) – All India Topper, Gold Medalist)Upcoming Batches: F2F@ SmartteachCA (IMA – ITO, Delhi) w.e.f. 30 May (MWF, 5.30 p.m.- 08.30 p.m.); Satellite@ETENCA w.e.f. 28 May (SS, 2 p.m – 5 p.m.)

AS - 10 Facts of the case:

In the present case, there is no proper appraisal and a revaluation based on one stray

bid is not proper to establish a proper replacement value of an item of asset.

The willingness of a buyer to pay the particular price is not logical basis to work out

the value of the asset. The company though proposes not to sell the car at Rs. One

lakh yet it has decided to neglect its value in the accounts.

Conclusion: In view of the fact that the company has been taking proper step, the

auditor should permit the company to neglect the valuation of car in the

accounts because it is in accordance with the relevant requirements of the AS.

Q. No. 23 As a statutory auditor of a Public Limited Company, how would you deal with the