auditing - maastricht...

TRANSCRIPT

Technology & Innovation Management Technology & Innovation Managemen

International

Executive Master of Auditing

AUDITING

COURSE MANUAL

Cohort 2014

IEMA2014

All rights reserved. No part of this publication may be reproduced or utilized in any

form or by any means, electronic or mechanical, including photocopying, recording

or by any information storage or retrieval system, without prior written permission

from the copyright owner, or, as the cases may be, the publishers, beyond the

exceptions provided by the Copyright Law.

2

Technology & Innovation Management Technology & Innovation Managemen

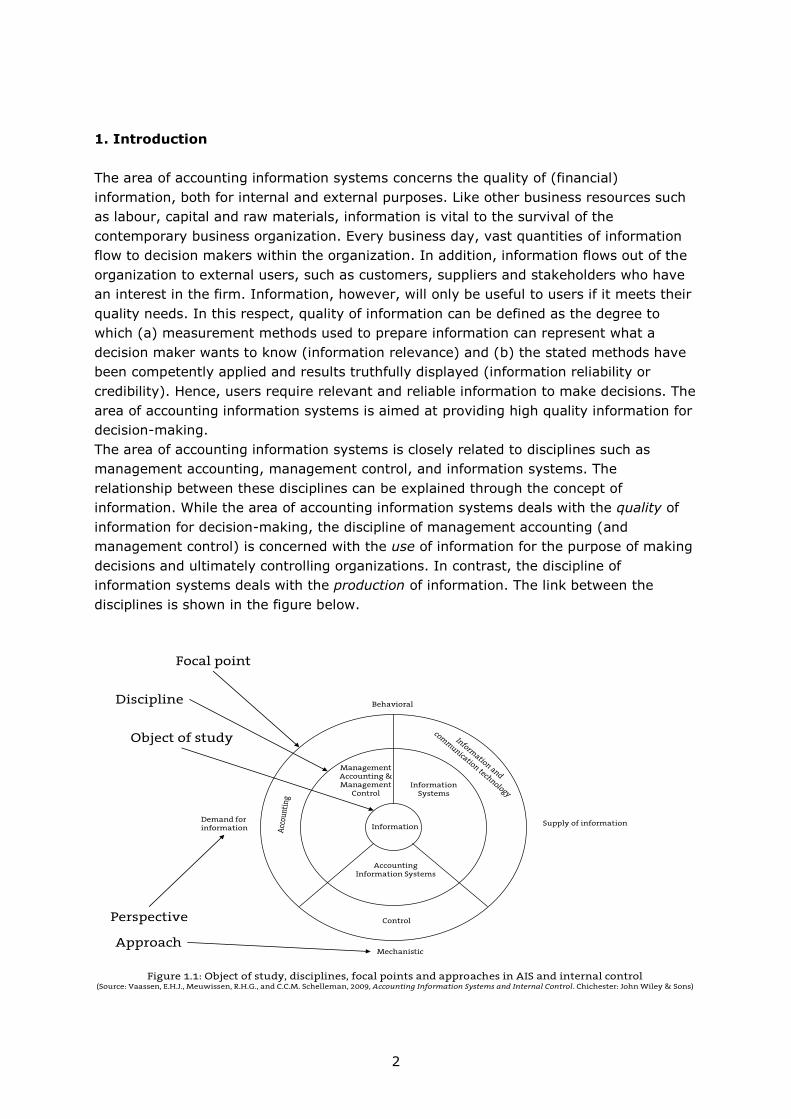

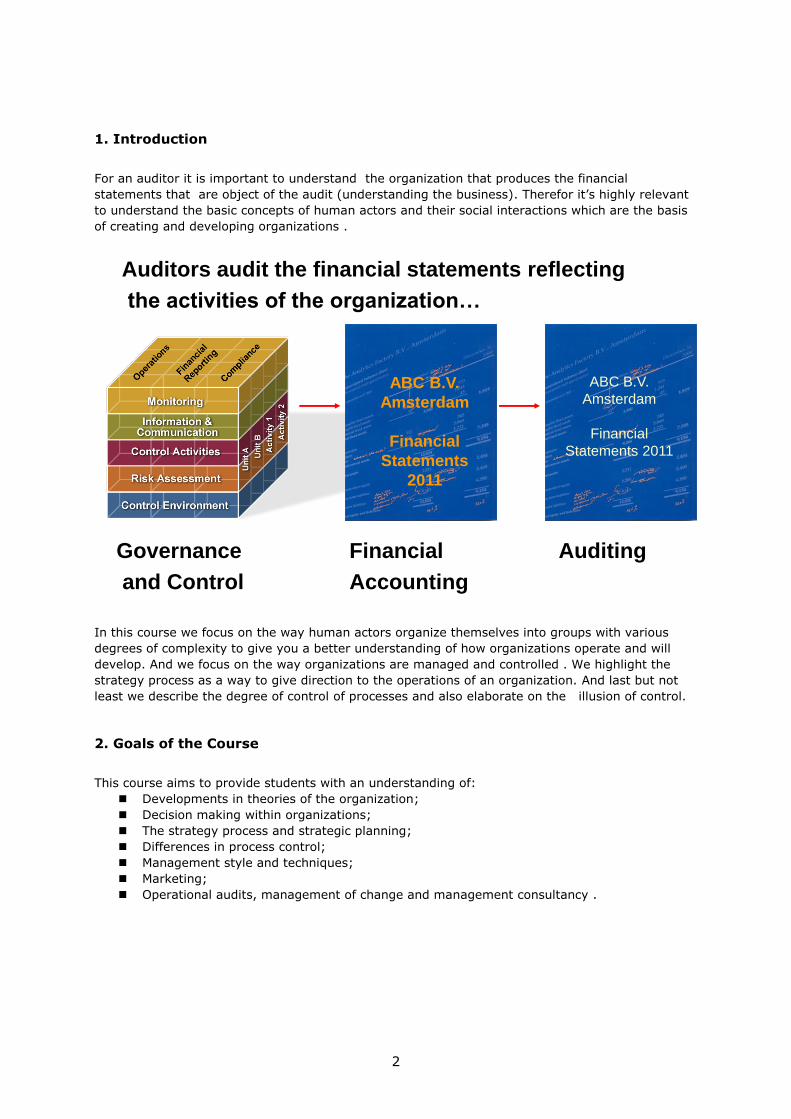

1. Introduction

In today’s information economy, characterized by a rapidly expanding amount of

information available to decision makers, high-quality information has become even more

important to make informed decisions. Hence, there is a need or demand for independent

professionals providing assurance on key financial and non-financial information. Auditing

and assurance services fulfil this role by ensuring the reliability, credibility and relevance

of business information. The high-profile corporate failures in the years 2000 and the

more recent financial crisis made once more clear how critical the role of reliable

information is.

The audit of financial statements is one type of assurance service where the objective is

to provide an opinion about the fairness of the reported financial position and results

based on GAAP, like IFRS or US GAAP, which are used as benchmark criteria. The audit

process consists of a number of audit phases and is greatly dependent on the nature of

the entity’s business. A good understanding of the client’s business model is therefore of

utmost importance for the auditor. The end product of the audit is the audit report, in

which the auditor’s findings are communicated to the users of the financial statements.

While the focus of this course is on financial statement auditing, attention will also be

given to other types of auditing and assurance services, which should be distinguished

from non-assurance services. The IAASB (International Auditing and Assurance

Standards Board) defines an assurance engagement as: “an engagement in which a

practitioner expresses a conclusion designed to enhance the degree of confidence of the

intended users other than the responsible party about the outcome of the evaluation or

measurement of a subject matter against criteria”. The subject matter of assurance

services can take many forms, like for example assurance on the effectiveness of internal

control, performance on human rights, or sustainability performance.

2. Goals of the Course

The objectives of this course are twofold. First, students should obtain a solid knowledge

of the literature on auditing. To that end, both a textbook and academic articles on the

subject of the course will be covered. The literature of this course emphasizes three

aspects of auditing: (1) Conducting an audit is a judgmental process, i.e. auditing is not

“just applying the standard procedures”; (2) Conducting an audit requires a good

understanding of clients, especially their strategy and risks and the client’s internal

control has a strong influence on the audit and (3) conducting an audit is focused in the

public interest, applying appropriate ethics and values, using adequate level of

professional scepticism.

The second objective of this course is that students should obtain skills that are

important in an auditing environment. To train students’ practical skills, cases on various

auditing aspects will be discussed. More specifically, the purposes of these cases are to

further develop students’: (1) problem solving skills in auditing settings; (2) experience

3

Technology & Innovation Management Technology & Innovation Managemen

in using and interpreting data in decision contexts in which they are commonly used; and

(3) report-writing and oral presentation skills.

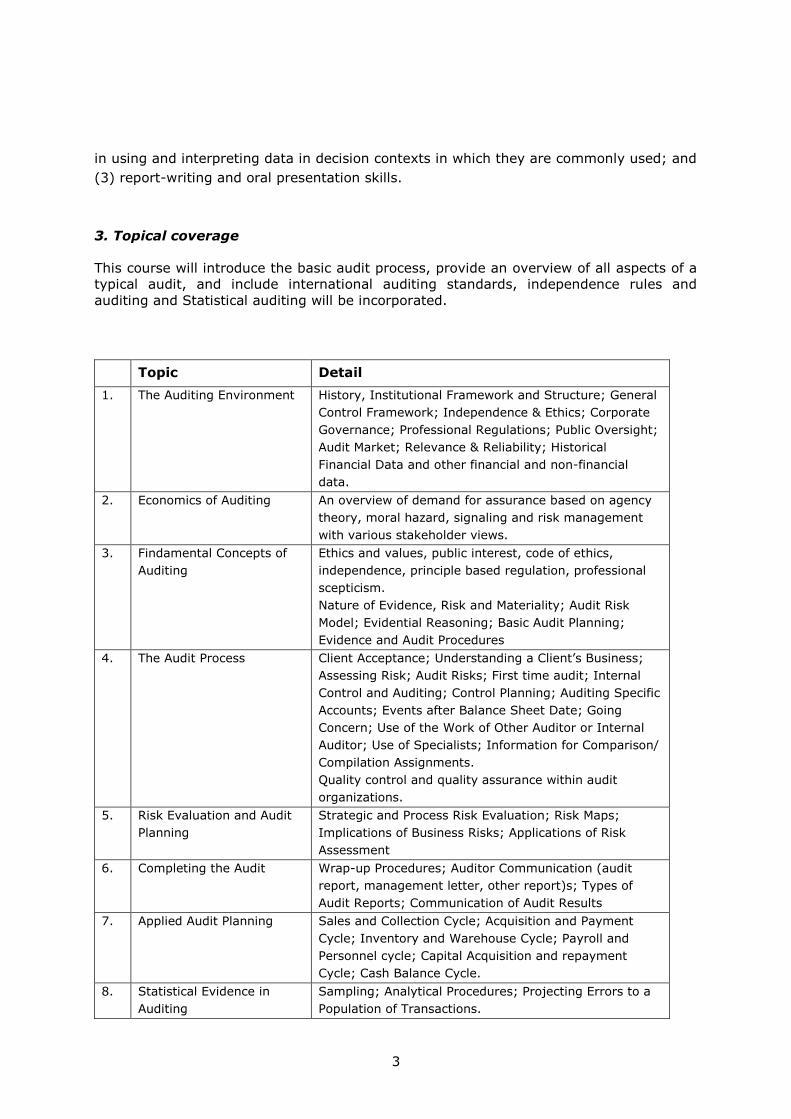

3. Topical coverage

This course will introduce the basic audit process, provide an overview of all aspects of a

typical audit, and include international auditing standards, independence rules and

auditing and Statistical auditing will be incorporated.

Topic Detail

1. The Auditing Environment History, Institutional Framework and Structure; General

Control Framework; Independence & Ethics; Corporate

Governance; Professional Regulations; Public Oversight;

Audit Market; Relevance & Reliability; Historical

Financial Data and other financial and non-financial

data.

2. Economics of Auditing An overview of demand for assurance based on agency

theory, moral hazard, signaling and risk management

with various stakeholder views.

3. Findamental Concepts of

Auditing

Ethics and values, public interest, code of ethics,

independence, principle based regulation, professional

scepticism.

Nature of Evidence, Risk and Materiality; Audit Risk

Model; Evidential Reasoning; Basic Audit Planning;

Evidence and Audit Procedures

4. The Audit Process Client Acceptance; Understanding a Client’s Business;

Assessing Risk; Audit Risks; First time audit; Internal

Control and Auditing; Control Planning; Auditing Specific

Accounts; Events after Balance Sheet Date; Going

Concern; Use of the Work of Other Auditor or Internal

Auditor; Use of Specialists; Information for Comparison/

Compilation Assignments.

Quality control and quality assurance within audit

organizations.

5. Risk Evaluation and Audit

Planning

Strategic and Process Risk Evaluation; Risk Maps;

Implications of Business Risks; Applications of Risk

Assessment

6. Completing the Audit Wrap-up Procedures; Auditor Communication (audit

report, management letter, other report)s; Types of

Audit Reports; Communication of Audit Results

7. Applied Audit Planning Sales and Collection Cycle; Acquisition and Payment

Cycle; Inventory and Warehouse Cycle; Payroll and

Personnel cycle; Capital Acquisition and repayment

Cycle; Cash Balance Cycle.

8. Statistical Evidence in

Auditing

Sampling; Analytical Procedures; Projecting Errors to a

Population of Transactions.

4

Technology & Innovation Management Technology & Innovation Managemen

9. Computer-assisted Audit

Testing and IT

IT Control: Introduction and Trends; Positioning of EDP

in the field of Auditing; Assurance Function of the EDP-

auditor; Cooperation of Auditor and IT auditor; IT-

values and Controls; General Controls; Application

Controls; ICT impact and alignment; CAATS & IT

Governance; XBRL and the Consequences for the

Auditor/ EDP-auditor; Use of File Analysis; Actual

Developments on the Area of Assurance Providing.

10. Organizations and the

Audit

Typology of Organizations and Audit; Governmental

Audit; Audit of Non Profit Organizations; Audit of

Financial Institutions; Audit of SME’s.

11. Assurance Services Fundamentals of Assurance Services; Subject Matter;

General Assurance Standards; Levels of Assurance;

Applications.

12. Forensic Auditing Fraud and Misappropriation of Assets; Requirements for

Basic Audit; Extended Fraud Procedures; Reporting

Responsibilities; Legal Implications and Process.

4. Examination of the Course

The Auditing exam consists of a written examination and an oral examination. The

written examination consists of a university exam (one exam of three hours) and a

national exam (three exams of three hours each). The oral examination is an oral exam

of one hour.

Students receive separate grades for the written and oral examination. A scale from 1-10

is applicable.

In order to pass the written examination you have to pass:

- The university exam with a minimum grade of 6,0

- The national exam, consists of 3 exams. In order to pass the national exam there

need to be obtained at least 17 points out of 30 points. At least 2 exams need to

be passed with a minimum grade of 6 points and the lowest grade should be at

least a minimum grade of 5 points.

If these rules deviate from the requirements from the “Landelijke redactiecommissie

Financial Auditing” or from “Commissie Eindtermen Accountantsopleiding (CEA)” their

requirements are valid.

In order to pass the oral exam a minimum grade of 6 points is required. Admission to the

oral exam is allowed after passing the Auditing university exam and after having

submitted the national auditing exam (not necessarily passed).

The written exams take place in May 2016 (university exam) and in July 2016 (national

exam). The oral exam takes place in Fall 2016.

5

Technology & Innovation Management Technology & Innovation Managemen

See the Education and Examination Regulations 2014-2015 for more detailed information

on the examination and examination rules.

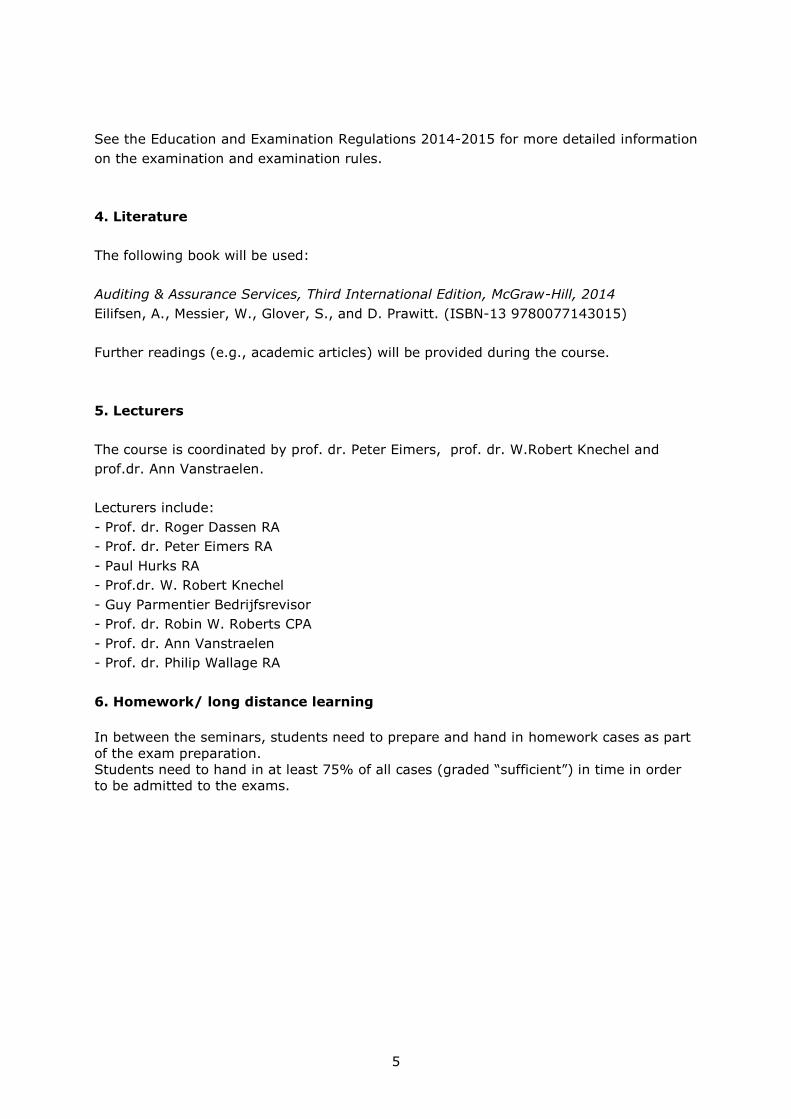

4. Literature

The following book will be used:

Auditing & Assurance Services, Third International Edition, McGraw-Hill, 2014

Eilifsen, A., Messier, W., Glover, S., and D. Prawitt. (ISBN-13 9780077143015)

Further readings (e.g., academic articles) will be provided during the course.

5. Lecturers

The course is coordinated by prof. dr. Peter Eimers, prof. dr. W.Robert Knechel and

prof.dr. Ann Vanstraelen.

Lecturers include:

- Prof. dr. Roger Dassen RA

- Prof. dr. Peter Eimers RA

- Paul Hurks RA

- Prof.dr. W. Robert Knechel

- Guy Parmentier Bedrijfsrevisor

- Prof. dr. Robin W. Roberts CPA

- Prof. dr. Ann Vanstraelen

- Prof. dr. Philip Wallage RA

6. Homework/ long distance learning

In between the seminars, students need to prepare and hand in homework cases as part

of the exam preparation.

Students need to hand in at least 75% of all cases (graded “sufficient”) in time in order

to be admitted to the exams.

6

Technology & Innovation Management Technology & Innovation Managemen

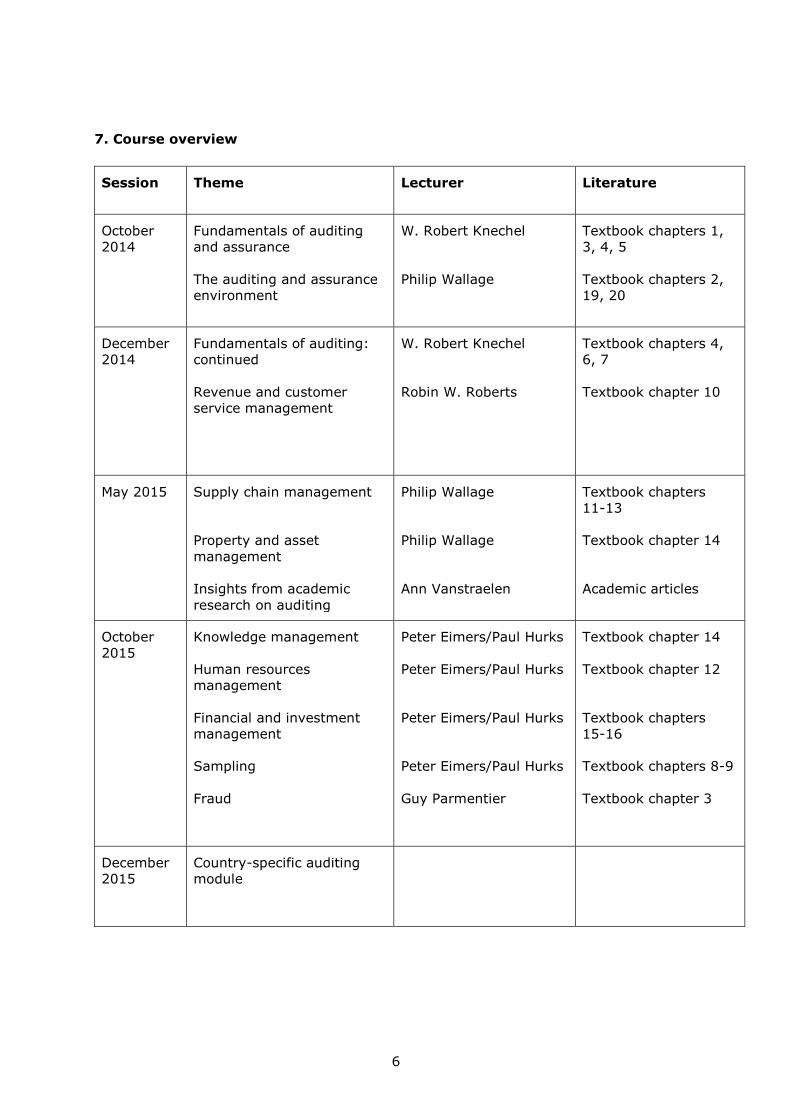

7. Course overview

Session Theme Lecturer

Literature

October

2014

Fundamentals of auditing

and assurance

The auditing and assurance

environment

W. Robert Knechel

Philip Wallage

Textbook chapters 1,

3, 4, 5

Textbook chapters 2,

19, 20

December

2014

Fundamentals of auditing:

continued

Revenue and customer

service management

W. Robert Knechel

Robin W. Roberts

Textbook chapters 4,

6, 7

Textbook chapter 10

May 2015

Supply chain management

Property and asset

management

Insights from academic

research on auditing

Philip Wallage

Philip Wallage

Ann Vanstraelen

Textbook chapters

11-13

Textbook chapter 14

Academic articles

October

2015

Knowledge management

Human resources

management

Financial and investment

management

Sampling

Fraud

Peter Eimers/Paul Hurks

Peter Eimers/Paul Hurks

Peter Eimers/Paul Hurks

Peter Eimers/Paul Hurks

Guy Parmentier

Textbook chapter 14

Textbook chapter 12

Textbook chapters

15-16

Textbook chapters 8-9

Textbook chapter 3

December

2015

Country-specific auditing

module

7

Technology & Innovation Management Technology & Innovation Managemen

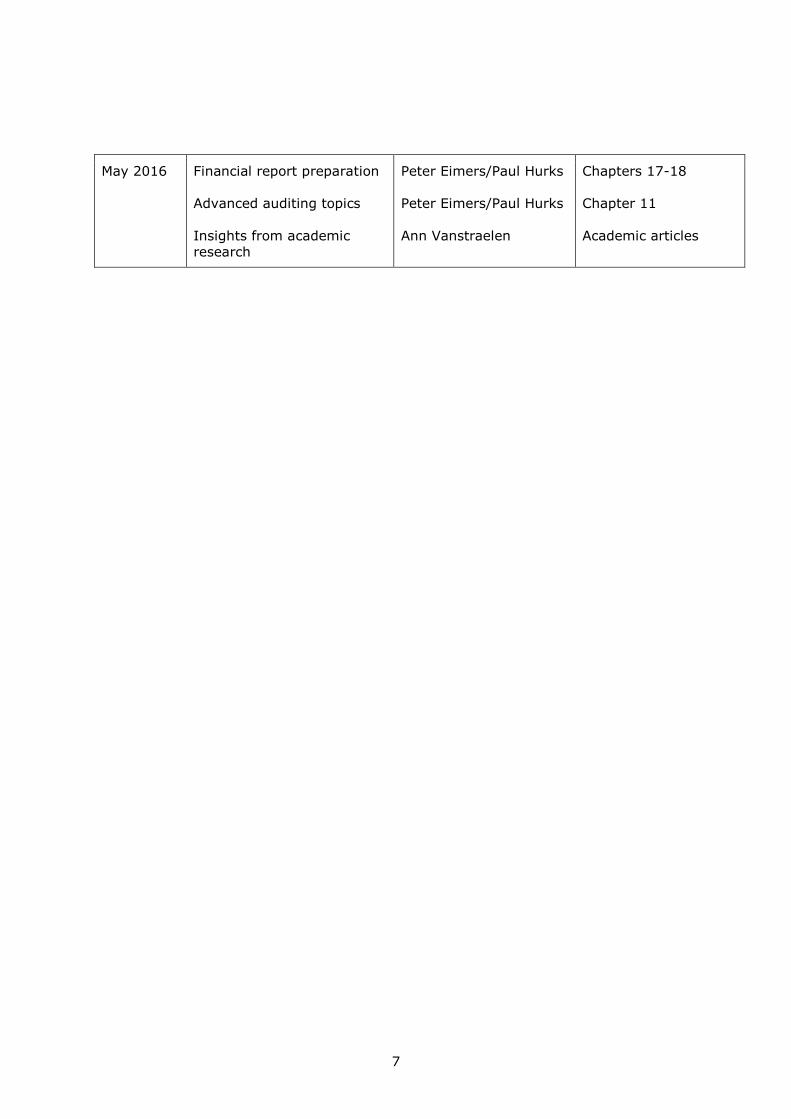

May 2016

Financial report preparation

Advanced auditing topics

Insights from academic

research

Peter Eimers/Paul Hurks

Peter Eimers/Paul Hurks

Ann Vanstraelen

Chapters 17-18

Chapter 11

Academic articles

Technology & Innovation Management Technology & Innovation Managemen

International

Executive Master of Auditing

Corporate Governance

COURSE MANUAL

Cohort 2014

IEMA2014

All rights reserved. No part of this publication may be reproduced or utilized in any form or

by any means, electronic or mechanical, including photocopying, recording or by any

information storage or retrieval system, without prior written permission from the copyright owner, or, as the cases may be, the publishers, beyond the exceptions provided by the Copyright Law.

2

Technology & Innovation Management Technology & Innovation Managemen

1. Introduction

Corporate Governance is the process and structure used to direct and manage the business and

affairs of the corporations with the objective of enhancing shareholder value, which includes

ensuring the financial viability of the business

In this course we focus on the (internal) auditor’s view on Corporate Governance in understanding

major causes of scandals. We will apply Enterprise Risk Management and major elements of

Internal Control of Financial Reporting which are major focus area’s for an auditor to

prevent/discover possible governance issues. We also focus on (un)ethical behavior in a corporate

environment.

2. Goals of the Course

The objectives of this course are twofold. First, students should obtain a solid knowledge of the

academic literature on Corporate governance. To that end, two textbooks will be covered. The

second objective of this course is for students to obtain skills that are important in designing, using

and evaluating the Corporate Governance of an organization. To train student’s skills, cases on

various aspects will be discussed.

This course aims to provide students with an understanding of:

The importance, meaning and inter-relations between Corporate Governance, Internal

Control and Risk Management;

An understanding of the roles and responsibilities of the various stakeholders in a private

or public organization; Role of the (internal)auditor and audit committee.

The content of the vital Corporate Governance codes and the substantial similarities and

differences between various codes;

The way in which risk management can be embedded into the internal control structure of

the organization ;

The importance of proper information systems in the implementation of an internal control

system;

An understanding of the limitations of Corporate Governance codes with respect to

ensuring “proper” management. Sustainability reporting.

3. Lectures and material

Lectures:

The theory will be covered during the lectures. Students are encouraged to ask questions and

participate actively to discuss the topic at hand. There will be 16-20 hours of lectures. Several

cases will be discussed. The lectures will be given by prof. dr. Oscar van Leeuwen.

Students need to prepare the literature and case as requested on the schedule It’s very important

to prepare the cases to improve the quality of interaction in the course. Articles and cases will be

uploaded on blackboard. Besides this you need two books (see below). We use the edition of the

book as presented in the course. You can’t use older editions because the corporate governance

codes changes on a regular basis.

3

Technology & Innovation Management Technology & Innovation Managemen

Material:

The books to be studied are:

- Corporate Governance, Internal Control and Risk Management, 2nd edition,

by R.J. Streng ISBN 978-9-081545815

(please find a PDF from this book on Blackboard!)

- Corporate governance, Principles and Issues, by D. Nordberg, 2011

ISBN 978-1-847873330

The overall set-up of the program can be depicted as follows:

3. Internal Control over Financial Reporting

1. Introduction and definitions

The Key role of Information Systems

Directors, Shareholders and Auditors: Roles and

Responsibilities

2. Business Ethics and Corporate Governance

4. Enterprise Risk management

Sarban

es-Oxley

The D

utch

CG

Co

de 2

00

9

The U

K C

G C

od

e

Oth

er Co

des

4

Technology & Innovation Management Technology & Innovation Managemen

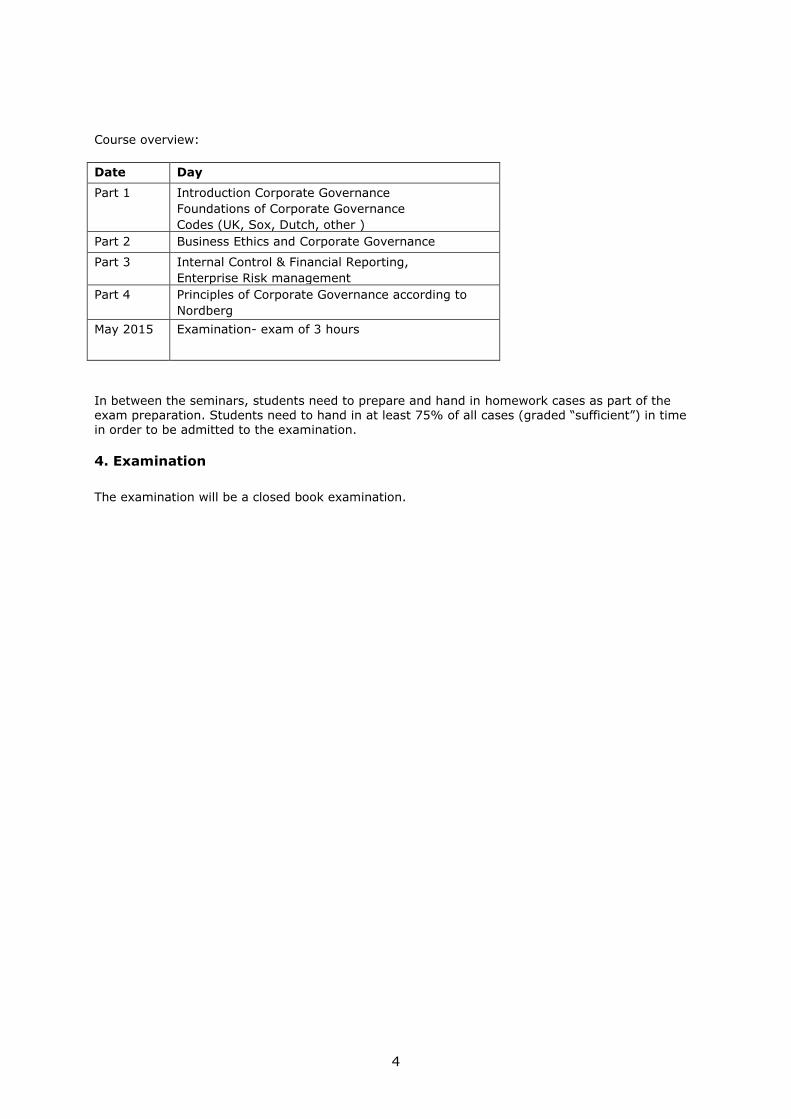

Course overview:

Date Day

Part 1 Introduction Corporate Governance

Foundations of Corporate Governance

Codes (UK, Sox, Dutch, other )

Part 2 Business Ethics and Corporate Governance

Part 3 Internal Control & Financial Reporting,

Enterprise Risk management

Part 4 Principles of Corporate Governance according to

Nordberg

May 2015 Examination- exam of 3 hours

In between the seminars, students need to prepare and hand in homework cases as part of the exam preparation. Students need to hand in at least 75% of all cases (graded “sufficient”) in time in order to be admitted to the examination.

4. Examination

The examination will be a closed book examination.

1

International

Executive Master of Auditing

COMPANY LAW

COURSE MANUAL

Cohort 2014

IEMA2015

All rights reserved. No part of this publication may be reproduced or utilized in any

form or by any means, electronic or mechanical, including photocopying, recording or

by any information storage or retrieval system, without prior written permission from

the copyright owner, or, as the cases may be, the publishers, beyond the exceptions

provided by the Copyright Law.

2

INTRODUCTION

This course is dedicated to company law from a Dutch perspective. During the course various

aspects of company law will be discussed and where possible placed within a European context.

The focus is on the way in which commercial organizations can be legally structured. We will

start with the different types of business organizations and the division of power and liabilities

within these organizations. From there on we will move to the functioning of private and public

limited liability companies. Issues such as minimum capital requirements, incorporation, the

division of power within the company`s internal structure and company take overs will be

discussed.

Next to company law, parts of the course will furthermore be dedicated to principles Dutch

property and insolvency law.

GOAL AND AIM OF THE COURSE

Through this course participants will acquire in-depth knowledge of Dutch company law and the

relevant Dutch as well as European legal structure in which companies have to operate. Through

the interactive sessions the participants will gain insights into the various types of business

structures and the way in which these business structures can be legally structured and

incorporated. The internal organization, representation, duties, powers and liabilities of those

involved in the business structure as well as the position of employees will be discussed.

The goal is to create awareness of legal considerations that must be taken into account in most

business organizations. Through a didactical approach based on cases and current issues

participants will become acquainted with the functioning and role of company law in relation to

the incorporation, internal division of power and the responsibilities of a company’s main

decision makers.

Additionally, participant will gain knowledge of the basic principles of Dutch insolvency and

property law.

TEACHING METHOD

The teaching method is based on interactive sessions consisting partly of lectures and partly of in

class discussions and solving case studies. Part of the teaching material to be used during the

sessions is incorporated in this manual (see below) other parts will be distributed during class.

3

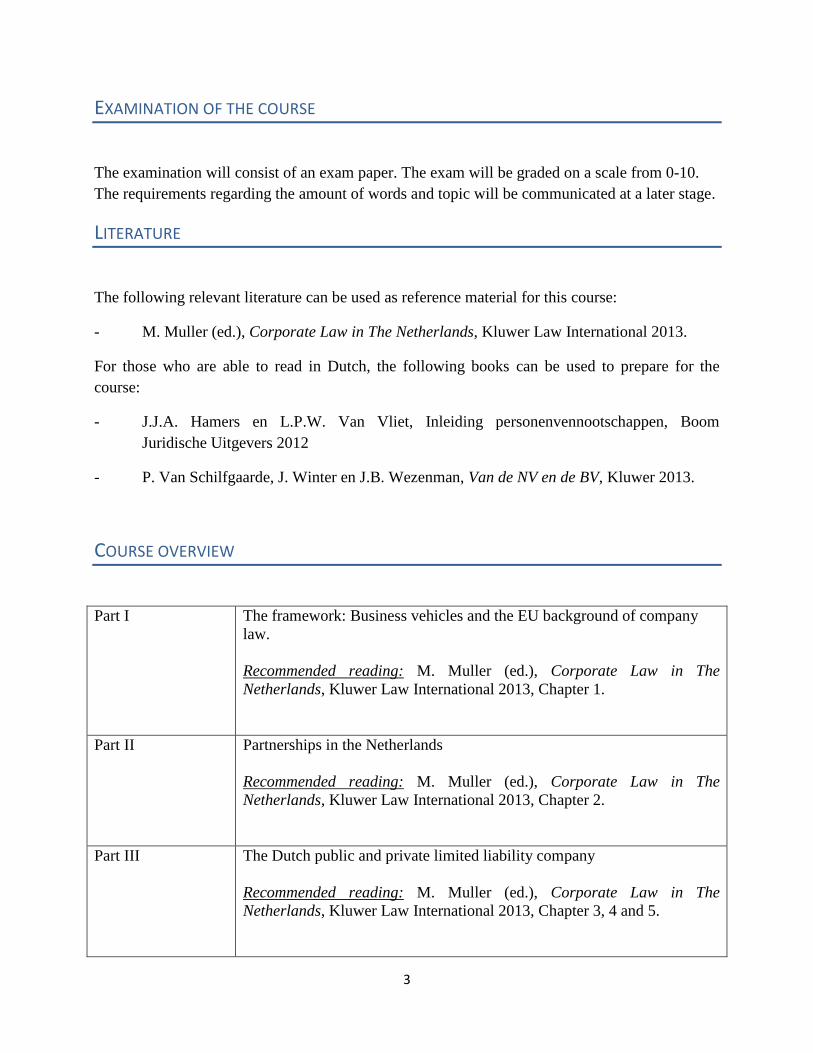

EXAMINATION OF THE COURSE

The examination will consist of an exam paper. The exam will be graded on a scale from 0-10.

The requirements regarding the amount of words and topic will be communicated at a later stage.

LITERATURE

The following relevant literature can be used as reference material for this course:

- M. Muller (ed.), Corporate Law in The Netherlands, Kluwer Law International 2013.

For those who are able to read in Dutch, the following books can be used to prepare for the

course:

- J.J.A. Hamers en L.P.W. Van Vliet, Inleiding personenvennootschappen, Boom

Juridische Uitgevers 2012

- P. Van Schilfgaarde, J. Winter en J.B. Wezenman, Van de NV en de BV, Kluwer 2013.

COURSE OVERVIEW

Part I The framework: Business vehicles and the EU background of company

law.

Recommended reading: M. Muller (ed.), Corporate Law in The

Netherlands, Kluwer Law International 2013, Chapter 1.

Part II Partnerships in the Netherlands

Recommended reading: M. Muller (ed.), Corporate Law in The

Netherlands, Kluwer Law International 2013, Chapter 2.

Part III The Dutch public and private limited liability company

Recommended reading: M. Muller (ed.), Corporate Law in The

Netherlands, Kluwer Law International 2013, Chapter 3, 4 and 5.

4

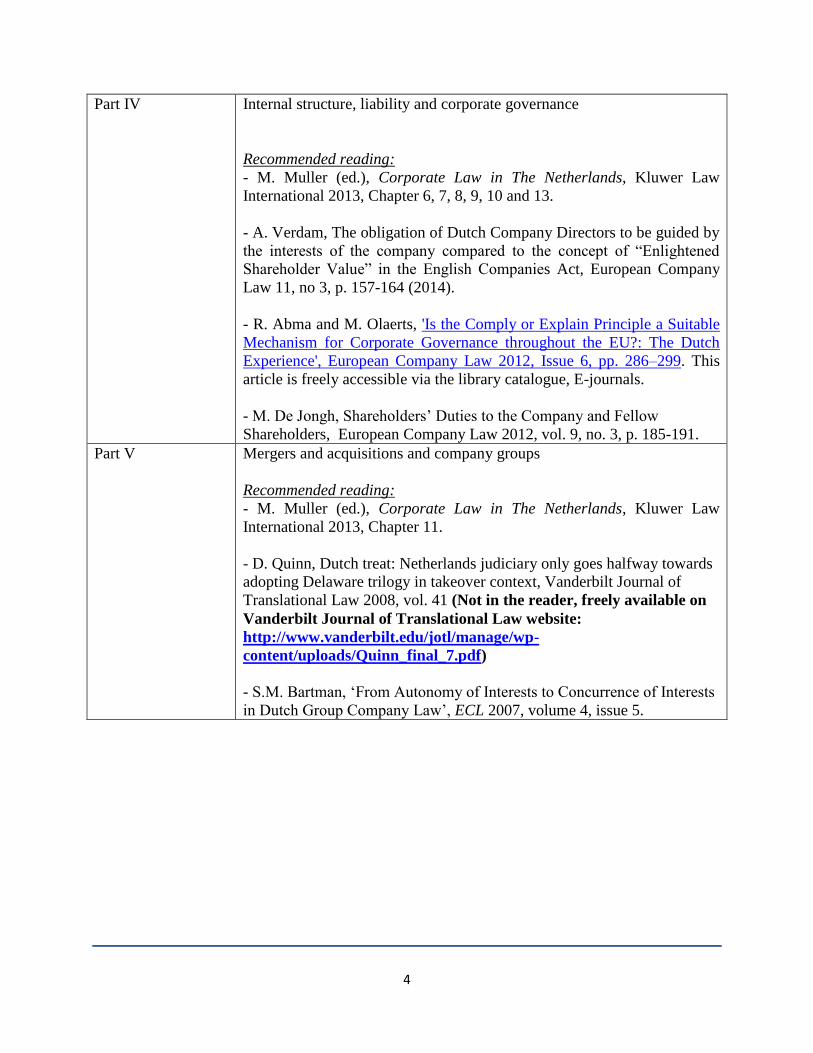

Part IV Internal structure, liability and corporate governance

Recommended reading:

- M. Muller (ed.), Corporate Law in The Netherlands, Kluwer Law

International 2013, Chapter 6, 7, 8, 9, 10 and 13.

- A. Verdam, The obligation of Dutch Company Directors to be guided by

the interests of the company compared to the concept of “Enlightened

Shareholder Value” in the English Companies Act, European Company

Law 11, no 3, p. 157-164 (2014).

- R. Abma and M. Olaerts, 'Is the Comply or Explain Principle a Suitable

Mechanism for Corporate Governance throughout the EU?: The Dutch

Experience', European Company Law 2012, Issue 6, pp. 286–299. This

article is freely accessible via the library catalogue, E-journals.

- M. De Jongh, Shareholders’ Duties to the Company and Fellow

Shareholders, European Company Law 2012, vol. 9, no. 3, p. 185-191.

Part V Mergers and acquisitions and company groups

Recommended reading:

- M. Muller (ed.), Corporate Law in The Netherlands, Kluwer Law

International 2013, Chapter 11.

- D. Quinn, Dutch treat: Netherlands judiciary only goes halfway towards

adopting Delaware trilogy in takeover context, Vanderbilt Journal of

Translational Law 2008, vol. 41 (Not in the reader, freely available on

Vanderbilt Journal of Translational Law website:

http://www.vanderbilt.edu/jotl/manage/wp-

content/uploads/Quinn_final_7.pdf)

- S.M. Bartman, ‘From Autonomy of Interests to Concurrence of Interests

in Dutch Group Company Law’, ECL 2007, volume 4, issue 5.

5

MATERIAL TO BE USED DURING THE SESSIONS

PART II

Case Study

You are a talented engineer and have come up with an innovative technique allowing you to

integrate solar panels into even the smallest devices. You are convinced that this system can

become a hype for the future and you want to develop it further. However, you cannot do this on

your own. First of all, there is your old classmate Peter (who was born in London). You

developed the technique of the solar panels together with him during your years at the University

of Wageningen and the two of you are complementary. You really need his knowledge and skills

to make this business into a success. Secondly, there is the small issue of raising a sufficient

amount of funds. Since you and Peter have just graduated, neither of you has anything to invest

besides brainpower. You talked to your father last week and he is willing to help you out in the

start up phase by investing in the business. This investment may not be enough for the future

once you start selling your products worldwide but it should be enough to get you started.

However, your father is a very dominant man. He has old school ideas about upbringing which he

most probably will also transpose to the running of ‘your business’. He is willing to invest

however, this investment comes with certain conditions. First of all, your father wants to treat his

children equally and he has always dreamed of setting up a family business. Your sister

graduated from the faculty of law three years ago but she still does not have a job. Your father

will only invest if you take her on board as well, not just as a employee but giving her a formal

position so that she can be involved in the business in the long run. You and your sister have had

your differences in the past. However, after the difficult years of puberty these problems seem to

belong to the past and you see some value in taking her on board. After all, she may have some

valuable legal knowledge to help you set up the business. The fact that she graduated in the area

of criminal law does not really help but you are willing to make the most of it. A bigger challenge

is however your brother Ben. Ben is the youngest of the siblings. He took on various studies but

never finished either of them. He mainly enjoyed student life. He is passionate about expensive

sports cars, has a big mouth and is not very responsible with money. Nevertheless, he is a very

social and likable guy and may be an asset in the sales department.

6

PART III

Case study: Pre- incorporation

Edgar Johnston is one of the many victims of the financial crisis and is fired as fashion designer

of Belperry PLC. Although jobless, many former business relations contact Edgar Johnston for

various design assignments. Since business is going great he is thinking of setting up a limited

company under the name “Johnstons Design Ltd”. As of February 2011 Edgar Johnston is

contracting with his business partners on behalf of “Johnstons Design Ltd” yet to be formed.

Edgar Johnston finally finds a spare moment to incorporate his company and on May 15th of the

same year “Johnstons Design Ltd” is registered. Edgar Johnston has full control over his

company and owns 100% of the shares. His girlfriend Anita Rowell becomes sole director of the

company.

One of the suppliers of “Johnstons Design Ltd”, “Buttons and Zippers ltd” has contracted with

“Johnstons Design Ltd” since February 2011. The supplier is still unpaid. “Buttons and Zippers

ltd” asks your advice who he can sue.

7

PART IV

Please note that the two case studies below are a follow up of the case study for part I mentioned

above

Case Study I

You have opted for a public limited liability company. You, Peter, your sister and Ben are all

appointed as directors of the company. However, your sisters’ business talent seems to be

restricted. She is better at law than at making business decisions and turned out not to be the

brightest of entrepreneurs. Therefore, you decide to take precautionary measures by limiting her

power to represent the company. Ben on the other hand needs to be able to conclude contracts in

name and on behalf of the company since he is in charge of the marketing. However, you fear his

car extravaganza may get the better of him and that after a commercial success he may step into

the office of the local car dealer to buy that May Bach he has been dreaming of for years on the

company`s account. In order to prevent this, you curtail his power to represent the company to

contracts not exceeding the value of 5000 euro.

Case Study II

You have eventually decided to incorporate a limited liability company. You and Peter form the

board of directors while your brother and sister are shareholders of the company. You and Peter

of course also own an equal amount of shares. The company has made profits over the past four

years. The majority of the profit has been reinvested and has been used to gradually increase

directors’ salaries. However, Ben is getting anxious. He has his eye on a new car and has already

mentioned on various occasions that in his opinion the time is right to start paying dividends. The

proposal to pay dividend is put on the agenda for the next general meeting.

8

PART V

Voting 'No' on Shareholder Democracy By Michael Kinsley

Google, the Internet search engine company, went public on Thursday, and shares issued at $85

were soon trading at over $100. No one is forced to buy Google shares. People do it voluntarily,

even downright eagerly.

This is so even though what they are buying are so-called Class A shares, which might

more accurately be labelled second-class shares. First-class shares, mischievously called Class B,

are held by the company's two founders and other high executives. In terms of dividends and so

on, the two classes are identical. But Class B shares get 10 votes each, while Class A shares get

only one. This means in effect that the company can raise money, and the founders can get

fabulously rich, by selling stock to the public, but even with a tiny minority of the shares, the

founders will control the company. And the public shareholders can't do anything about it.

Google thus thumbs its nose at one of the major pieties of our day: shareholder

democracy. This has been the high-minded response to Enron and the other corporate-looting

scandals: Shareholders should have more say -- or, more precisely, some say, since now they

basically have none -- about the management of their companies. That way, management couldn't

so easily overpay itself or loot the company in more dramatic ways. The Securities and Exchange

Commission is considering rules to make it easier for large institutional investors, at least, to

challenge management nominees for boards of directors.

It's democracy. Who could be against it? Yet just this week, despite Enron, WorldCom

and all, investors kicked and clawed to put money into a company that, in democratic terms,

might as well be the old Soviet Union. Apparently they don't care. They want to be serfs. Are

they nuts? Financial masochists?

Well, they think they're going to get rich, don't they? And, like the citizens of Singapore,

they would rather be rich than free, at least in this narrow context. They cling to this view despite

studies waved around by shareholder democracy enthusiasts showing that companies with some

fundamental democratic reforms do better than companies without. More important, and unlike

the old Soviet Union, Google will let you leave anytime you want. You just sell your stock.

In their prospectus, Google's founders have some malarkey about how they are doing this

dual-class business to prevent the company from being overly concerned with short-term profits

and enable it to take the longer, ultimately more profitable, view. In other words, they think they

know the shareholders' interests better than the shareholders themselves do. Shareholder

democracy buffs are saying the same thing when they try to pressure, or even require, companies

to make democratic reforms. But unlike Google, you can't free yourself of the SEC by simply

calling your broker.

Another company with dual classes of stock is Berkshire Hathaway Inc., run by the

legendary Warren Buffett. The last thing in the world that even second-class shareholders of

Berkshire want is shareholder democracy. They're buying into Buffett's benign dictatorship, not

into pro-rata shares of the wisdom of any idiot who buys in too. They're delighted to have no say

in the company, as long as they are assured that other shareholders have no say either. That is far

from nuts.

9

Or what about newspaper companies such as The Washington Post, the New York Times

and Dow Jones, which publishes the Wall Street Journal? They have dual classes of stock and are

blunt about the purpose: It is to retain family control. They say that this is to make sure that the

newspaper survives and maintains the highest journalistic standards, even if this means giving up

those last few drops of potential profit. You can believe them, or you can believe it's all about

dynastic vanity. But these companies are being honest that they have goals other than maximizing

profits, and the price of their shares will reflect the extent to which others wish to share in this

enterprise. Why stop them, or even sneer at them?

Democracy is actually a second-best solution. If we're all going to McDonald's, and we all

have to get the same thing, it should be decided by majority vote. But it's even better if we each

can get what we want. And you can be fairly confident that a majority of McDonald's customers

prefer hamburgers, while a majority at Popeye's prefer chicken. You don't have to require a vote.

Advocates of shareholder democracy believe it will lead to companies that care more for

the environment, treat their workers better and so on. Well maybe, maybe not. In a world of

perfect corporate democracy, in which large public companies are required to pursue only those

goals that can be agreed upon by the owners of a majority of the publicly traded shares at any

moment, the most likely result would be companies focused exclusively on maximizing profits.

Requiring shareholder democracy actually stifles it. Why shouldn't shareholder democracy

include the right to decide whether you want shares in a company that practices shareholder

democracy?

Source: Washingtonpost.com, Sunday, August 22, 2004; Page B07

How Capitalist is America?

By: professor Marc Roe

Source: http://www.project-syndicate.org/commentary/how-capitalist-is-america

CAMBRIDGE – If capitalism’s border is with socialism, we know why the world properly sees

the United States as strongly capitalist. State ownership is low, and is viewed as aberrational

when it occurs (such as the government takeovers of General Motors and Chrysler in recent years,

from which officials are rushing to exit). The government intervenes in the economy less than in

most advanced nations, and major social programs like universal health care are not as deeply

embedded in the US as elsewhere.

But these are not the only dimensions to consider in judging how capitalist the US really is.

Consider the extent to which capital – that is, shareholders – rules in large businesses: if a

conflict arises between capital’s goals and those of managers, who wins?

Looked at in this way, America’s capitalism becomes more ambiguous. American law gives more

authority to managers and corporate directors than to shareholders. If shareholders want to tell

directors what to do – say, borrow more money and expand the business, or close off the money-

10

losing factory – well, they just can’t. The law is clear: the corporation’s board of directors, not its

shareholders, runs the business.

Someone naïve in the ways of US corporations might say that these rules are paper-thin, because

shareholders can just elect new directors if the incumbents are recalcitrant. As long as they can

elect the directors, one might think, shareholders rule the firm. That would be plausible if

American corporate ownership were concentrated and powerful, with major shareholders owning,

say, 25% of a company’s stock – a structure common in most other advanced countries, where

families, foundations, or financial institutions more often have that kind of authority inside large

firms.

But that is neither how US firms are owned, nor how US corporate elections work. Ownership in

large American firms is diffuse, with block-holding shareholders scarce, even today. Hedge funds

with big blocks of stock are news, not the norm.

Corporate elections for the directors who run American firms are expensive. Incumbent directors

typically nominate themselves, and the company pays their election expenses (for soliciting votes

from distant and dispersed shareholders, producing voting materials, submitting legal filings, and,

when an election is contested, paying for high-priced US litigation). If a shareholder dislikes, say,

how GM’s directors are running the company (and, in the 1980’s and 1990’s, they were running

it into the ground), she is free to nominate new directors, but she must pay their hefty elections

costs, and should expect that no one, particularly not GM, will ever reimburse her. If she owns

100 shares, or 1,000, or even 100,000, challenging the incumbents is just not worthwhile.

Hence, contested elections are few, incumbents win the few that occur, and they remain in

control. Firms and their managers are subject to competitive markets and other constraints, but

not to shareholder authority.

In lieu of an election that could remove recalcitrant directors, an outside company might try to

buy the firm and all of its stock. But the rules of the US corporate game – heavily influenced by

directors and their lobbying organizations – usually allow directors to spurn outside offers, and

even to block shareholders from selling to the outsider. Directors lacked that power in the early

1980’s, when a wave of such hostile takeovers took place; but by the end of the decade, directors

had the rules changed in their favor, to allow them to reject offers for nearly any reason. It is now

enough to reject the outsider’s price offer (even if no one else would pay more).

American corporate-law reformers have long had their eyes on corporate elections. About a

decade ago, after the Enron and WorldCom scandals, America’s stock-market regulator, the

Securities and Exchange Commission (SEC), considered requiring that companies allow qualified

shareholders to put their director nominees on the company-paid election ballot. The actual

proposal was anodyne, as it would allow only a few directors – not enough to change a board’s

majority – to be nominated, and voted on, at the company’s expense.

Nevertheless, the directors’ lobbying organizations – such as the Business Roundtable and the

Chamber of Commerce (and their lawyers) – attacked the SEC’s initiative. Lobbying was fierce,

and is said to have reached into the White House. Business interests sought to replace SEC

commissioners who wanted the rule, and their lawyers threatened to sue the SEC if it moved

11

forward. It worked: America’s corporate insiders repeatedly pushed the proposal off of the SEC

agenda in the ensuing decade.

Then, in the summer of 2010, after a relevant election and a financial crisis that weakened

incumbents’ credibility, the SEC promulgated election rules that would give qualified

shareholders free access to company-paid election ballots. As soon as it did, the US managerial

establishment sued the SEC, and government officials felt compelled to suspend the new rules

before they ever took effect. The litigation is now in America’s courts.

The lesson is that the US is less capitalist than it is “managerialist.” Managers, not owners, get

the final say in corporate decisions. Perhaps this is good. Even some capital-oriented thinking

says that shareholders are better off if managers make all major decisions. And often the interests

of shareholders and managers are aligned.

But there is considerable evidence that when managers are at odds with shareholders, managerial

discretion in American firms is excessive and weakens companies. Managers of established firms

continue money-losing ventures for too long, pay themselves too much relative to their and the

company’s performance, and too often fail to act aggressively enough to enter new but risky

markets.

When it comes to capitalism vs. socialism, we know which side the US is on. But when it’s

managers vs. capital-owners, the US is managerialist, not capitalist.

Read more at http://www.project-syndicate.org/commentary/how-capitalist-is-

america#HJJDPhJCGr27DGfD.99

12

PART V

KPN

KPN “Poison Pill’s” Slim’s Takeover Bid CAPITAL MARKETS

Source: http://www.internationalfinancemagazine.com/article/KPN-Poison-Pills-Slims-

Takeover-Bid.html

“The soccer rules in Mexico and Netherlands are the same, but taking over a large company

is not soccer. We may have different rules for this here than in Mexico,” said Jacques

Schraven, who heads the foundation.

21st October 2013

Mexican Billionaire Carlos Slim’s effort to take over Dutch Telecom Company, Royal KPN NV, was

foiled by the KPN foundation, set up to safe guard the company’s interests. The foundation moved to

block Carlos Slim’s proposed 7.2 billion – Euros ($ 9.52 billion) offer for the Dutch telecoms group,

ending his ambitions of extending his business interests in Europe. Earlier in August, the Mexican

billionaire had offered to acquire 70 percent of KPN for 2.40 Euros per share, or $ 9.5 billion through

his flagship company, America Movil. Slim’s America Movil already holds 30 percent of KPN, but the

surprise move by the foundation to thwart his efforts underlines the difficulty the tycoon faces in

extending his telecom empire outside Latin America.

Hostile Takeover?

KPN foundation was set up to safe guard key national infrastructure when the former state monopoly

was being privatized, the foundation said it would exercise a right to prevent – what it termed a

hostile takeover bid by America Movil- by issuing new preference shares with voting rights with 49.9

percent of the total shares, to protect other shareholder’s position. “The soccer rules in Mexico and

Netherlands are the same, but taking over a large company is not soccer. We may have different

rules for this here than in Mexico,” said Jacques Schraven, who heads the foundation.

Poison pill- The Dutch Version

The company managed to dodge on what it sees as a takeover-on-the- cheap from one of the

world’s richest men. The hostile approach of America Movil was foiled by the company by a strategy

known as “poison pill” which attempts to thwart hostile takeovers. The companies grant these

13

foundations a call-option to buy preference shares which, if activated, will seize control over the

company for a limited period of time. In the 1980’ and 1990’s many Dutch firms used such defences

to protect themselves against hostile takeovers or activist inventors. The defense is not used

frequently, but experts say it is a measure of last resort that deter investors in ordinary shares and

only buys time to look for alternative strategic options.

“The foundation has intervened in this way in order to safe guard the interests of KPN and its

stakeholders, including share holders, employees, trade unions, customers and Dutch society more

generally. ” it said in a statement. The foundation argued these interests were at risk as America

Movil had not consulted KPN before announcing its intention to make a takeover offer.

With a poison pill, the target company attempts to make its stock less attractive to the potential

acquirer. In this strategy the company may offer a preferred stock option to its share holders that give

special dividends or payments to their holders, the stock option is opened to the share holders when

there is threat of a takeover, the stock is worthless and is used to scare away the bidder who is

attempting to take over the company.

Talks will Resume- KPN Chief

KPN chief executive Eelco Blok said the situation was not yet cut-and-dried, but did not reveal an

asking price which could be considered acceptable by KPN for the takeover bid. America Movil has

not shown any willingness to improve its earlier offer of 2.40 Euros per share, despite several recent

developments including KPN’s agreement to sell its German unit E-Plus to Telefonica and the

acquisition of shares by the foundation. The shareholder foundation which foiled the takeover bid

said that it had “never aimed to block the deal, but to get the two parties to the negotiating table to

come to a merger protocol in a suitable way”.

Hard Pill to Swallow

“It is the first time we have seen Mr.Slim being squeezed” said a telecom analyst; Mr.Slim has

conceded defeat in the 7.2 billion Euros offer ($ 9.8 billion) for the 70 percent stake he didn’t own in

KPN. The Financial times reported that this move could signal an attempt by Mr.Slim to back away

from Europe to focus on Brazil, where the sector could witness significant changes triggered by

Telecom Italia’s mooted sale of its Brazilian unit.

America Movil, whose market dominance is presently facing stiff challenges from regulators in

Mexico and Colombia had offered 2.40 Euros a share for KPN, which has been trading around 2.30

since the offer, were down 8.8 percent to 2.22 Euros, well below the offer promised by Slim’s

America Movil.

14

ABN AMRO

Summary of the Court’s ruling of 13 July 2007 in ABN AMRO

cases

Background information

On 15 May 2007 the Hoge Raad (Supreme Court of The Netherlands) has received three appeals in cassation

against the ruling of the Enterprise Chamber of the Amsterdam Court of Appeal, dated 3 May 2007,

casenumber 451/2007 OK , (published on website rechtspraak.nl, numberBA4395) .

The appealing parties are:

ABN AMRO Holding N.V. and ABN AMRO Bank N.V., “ABN AMRO” (casenumber

R07/102) represented by mr. P.J.M. von Schmidt auf Altenstadt, advocate in The Hague

Bank of America Corporation (casenumber R07/100)

represented by mr. E. Grabandt, mr. S.M. Bartman and mr. J.P. Heering, advocates in The Hague

Barclays PLC (casenumber R07/101)

represented by mr. E. van Staden ten Brink, advocate in The Hague.

The following parties have challenged the appeals:

VEB, P. Schoenfeld Asset Management LLC, J.T.M. de Laat, J.F. van der Steene, J.D. Steneker and

J.A. de Vries, “VEB”

represented by mr. J.W.H. van Wijk, advocate in The Hague.

The Royal Bank of Scotland Group PLC, Fortis N.V., Fortis S.A./N.V. and Banco Santander Central

Hispano S.A., “ the Consortium”,

represented by mr. H.J.A. Knijff, advocate in The Hague.

This lawsuit focuses on the question whether the Board of Directors of ABN AMRO was allowed to sell its US

subsidiary LaSalle without prior approval by the general meeting of shareholders. This sale took place while

the Board of Directors was involved in exclusive negotiations with Barclays regarding a share merger. Before

the sale of LaSalle, a Consortium of three banks (Royal Bank of Scotland, Santander and Fortis) had

announced its intention to acquire the shares in ABN AMRO. The Consortium aims at the acquisition of ABN

AMRO including LaSalle.

VEB has requested the Enterprise Chamber of the Amsterdam Court of Appeal to set up an inquiry into the

policy and the conduct of business of ABN AMRO in relation to the sale of LaSalle. In addition, VEB has

applied for an interim injunction to suspend the sale of LaSalle in order to enable the general shareholders

meeting of ABN AMRO to vote on that transaction. The Enterprise Chamber has granted an interim injunction

to that effect. It is against this injunction that the present appeal in cassation has been lodged.

The judgement of the Enterprise Chamber with regard to the interim injunction

In brief, the Enterprise Chamber has ruled as follows:

1. it has not (yet) been established that the sale of LaSalle was concluded in order to frustrate a

competitive bid of the Consortium;

2. however, in view of the decision by the Board of Directors and of the Supervisory Board to put up for

sale ABN AMRO and find an acquisition candidate, the sale of LaSalle, which cannot be detached from the

15

intended merger of ABN AMRO and Barclays, exceeded the “conduct of business area that is reserved to

the Board of Directors and the Supervisory Board ”;

3. under the circumstances of the case, it would be contrary to the principles of reasonableness and

fairness, laid down in article 2:8 of the Dutch Civil Code (DCC), as well as the principle underlying article

2:107a DCC, if the general meeting of shareholders of ABN AMRO would not be allowed to “express their

views” on the sale of LaSalle;

4. for this reason the sale of LaSalle is suspended until the general meeting of shareholders has

approved the transaction.

The advisory opinion of mr. L. Timmerman, advocate-general at the Supreme Court

The advocate-general was of the opinion that neither the principles of reasonableness and fairness, laid down

in article 2:8 DCC, nor the underlying principle of article 2:107a DCC require the LaSalle transaction being

subject to prior approval by the general meeting of shareholders. For this reason, he recommended the

Supreme Court to set aside the decision of the Enterprise Chamber.

The judgment of the Supreme Court

In brief the Supreme Court has ruled as follows:

1. The Enterprise Chamber has considered the sale of LaSalle to Bank of America not to be an unlawful

anti-takeover measure by ABN AMRO Holding. This opinion was upheld in cassation.

2. The Enterprise Chamber rightly held that (a) as a rule the Board of Directors of ABN AMRO was

entitled to sell LaSalle and that (b) article 2:107a, paragraph 1, DCC does not confer to the shareholders

a right of approval with regard to the sale of LaSalle.

3. Contrary to the Enterprise Chamber’s ruling, such a right of approval cannot be assumed in the light

of special circumstances and is not required by the principles of proper corporate governance (article 2:8

and article 2:9 DCC). The Board of Directors shall put the interest of the company and the enterprise

connected therewith first. The fact that the shareholders aim at selling their shares at the highest possible

price involves no obligation for the Board of Directors of ABN AMRO to obtain the shareholders’ approval

of the sale of LaSalle, nor does such an obligation arise from the prevailing views of the law in The

Netherlands.

4. Article 2:107a DCC should not be interpreted broadly nor applied to other cases than exactly those

to which it refers.

5. Now that the sale of LaSalle is definite, the interests of Bank of America and Barclays should be

taken into account. There should not be any unnecessary uncertainty about the carrying out of this

agreement, into which the Board of Directors of ABN AMRO was entitled to enter.

6. The Supreme Court holds that there are no grounds for granting the requested interim injunctions.

It sets aside the judgment of the Enterprise Chamber and dismisses the requested interim injunction.

Consequences of this ruling

7. The Supreme Court’s ruling implies that the appeals by Bank of America, Barclays and ABN AMRO

succeeded, whereas the appeal by VEB failed and its request for an interim injunction to suspend

(pending the approval by the shareholders) the contract of sale regarding LaSalle, was dismissed

irrevocably.

16

SELECTED ARTICLES OF BOOK 2 DUTCH CIVIL CODE

Below you will find a selection of provisions of Dutch company law to

be used during the sessions. Please note that these are not official translations.

Source: http://www.dutchcivillaw.com/civilcodebook022.htm

Article 2:24a Definition of a ‘subsidiary’

- 1. A subsidiary of a legal person is:

a. a legal person in which another legal person or one or more of its subsidiaries, whether or not under

a contract with other persons entitled to vote, is able to exercise, solely or jointly, more than one half

of the voting rights at the General Meeting;

b. a legal person with regard to which another legal person or one or more of its subsidiaries, whether

or not under a contract with other persons entitled to vote, is able to appoint or discharge, solely or

jointly, more than one half of the members of the Board of Directors or the Supervisory Board, even if

all persons entitled to vote would cast their vote.

- 2. With a subsidiary is equated a commercial partnership acting in its own name in which the legal

person or one or more of its subsidiaries participate as a partner who is fully liable towards the

creditors of that commercial partnership for all debts.

- 3. For the purpose of paragraph 1, rights attached to shares shall not be linked to a person who

holds these shares on behalf of someone else. Rights attached to shares shall be linked to the person

on whose behalf these shares are held, if this person has the power to decide how these rights are to

be exercised or if he has the power to acquire these shares.

- 4. For the purpose of paragraph 1, voting rights attached to pledged shares are linked to the pledgee

(holder of the pledge) if he has the power to decide how these rights are to be exercised. If the shares,

however, are encumbered with a pledge as security for a loan which the pledgee has provided in the

ordinary course of his business, then the voting rights shall only be linked to him if he has exercised

them in his own interest.

Article 24b Definition of a ‘group’

A group is an economic unit in which legal persons and commercial partnerships are organizationally

interconnected. Group companies are legal persons and commercial partnerships interconnected to

each other in one group.

Article 2:107a Resolutions that need the approval of the General Meeting

- 1. Resolutions of the Board of Directors leading to changes in the identity or character of the

Corporation or its enterprise must be approved by the General Meeting, among which in any case

17

resolutions for:

a. a transfer of the enterprise or of practically the entire enterprise to a third party;

b. the start or termination by the Corporation or its subsidiary of a long-lasting alliance with another

legal person or of a commercial partnership, or the start or termination by the Corporation or its

subsidiary as fully liable partner in a limited partnership (''commanditaire vennootschap') or general

partnership ('vennootschap onder firma'), always only when the start or termination of such alliance or

partnership is of fundamental importance for the Corporation;

c. the acquisition or disposal of a participating interest in the capital of another legal person to the

value of at least one third of the amount of the assets according to the Corporation's balance sheet

with explanatory notes or, if the Corporation makes use of a consolidated balance sheet, according to

its consolidated balance sheet with explanatory notes, always according to the last adopted annual

accounts of the Corporation.

- 2. The absence of the General Meeting's approval on a resolution as referred to in paragraph 1, does

not affect the authority of representation of the Board of Directors or the Directors.

- 3. When the Open Corporation (’naamloze vennootschap’) has established a Works Council by virtue

of statutory provisions, the request for an approval shall not be presented to the General Meeting than

after the Works Council has been given the opportunity, timely prior to the convening date referred to

in Article 1:114, to determine its point of view on the matter. The Works Council’s point of view is

offered simultaneously with the request for an approval to the General Meeting. The chairman or a

member of the Works Council assigned by him to this end may elucidate the Works Council’s point of

view at the General Meeting. The absence of that point of view does not affect the decision-making

over the request for an approval.

- 4. For the purpose of paragraph 3, by a Works Council is understood also the Works Council of the

enterprise of a subsidiary company, provided that the employees in service of the Open Corporation

(‘naamloze vennootschap’) and the group companies in majority are working within the Netherlands.

When there are more Work Councils than one, the power meant in the present Article is exerted by

these Councils jointly. Where a Central Works Council has been established for the relevant enterprise

or enterprises, the before meant power belongs to that Central Works Council.

Article 2:138 Liability of the Directors in the event of a bankruptcy of the Open Corporation

- 1. In the event of a bankruptcy of the Open Corporation ('naamloze vennootschap'), each Director is

towards the liquidation estate jointly and severally liable for the amount of the debts as far as these

cannot be recovered after the assets of the Corporation have been wound up, if the Board of Directors

has performed its duties clearly improperly and it is likely that this is a major cause of the

Corporation's bankruptcy.

- 2. If the Board of Directors has not complied with its obligations under Article 2:10 or 2:394, then it

shall have performed its duties improperly and it is presumed that this improper performance of duties

is a major cause of the Corporation's bankruptcy. The same applies if the Corporation is a fully liable

partner in a general partnership (vennootschap onder firma) or a limited partnership ('commanditaire

vennootschap') and the obligations of Article 3:15i have not been complied with. An insignificant

omission (default) is, however, not taken into account.

- 3. A Director who proves that the improper performance of duties by the Board of Directors is not

attributable to him and that he has not been negligent in taking measures to avert the consequences

thereof, is not liable.

- 4. The court may reduce the amount for which the Directors are liable if it regards this amount to be

excessive, given the nature and seriousness of the improper performance of duties by the Board of

18

Directors, the other causes of the bankruptcy and the way in which the liquidation estate has been

wound up. The court may furthermore reduce the amount of liability of an individual Director if it

regards this amount to be excessive in view of the time during which that Director has been in office in

the period when the improper performance of duties took place.

- 5. Where the amount of the deficit of the liquidation estate is still unknown, the court may determine,

whether or not under application of paragraph 4, which part of the deficit has to be paid by the

Directors personally, and it may order the preparation of a deficit list in accordance with the provisions

of Title 6 of Book 2 of the Code of Civil Procedure.

- 6. A legal action (claim) against one or more Directors can be filed only on the basis of the present

Article on the ground of an improper performance of duties which took place in the period of three

years preceding the Corporation's bankruptcy. The fact that a Director has been discharged from

liability, does not preclude the filing of a legal action (claim) as meant in the previous sentence.

- 7. For the purpose of the present Article, a person who has actually determined or co-determined the

policy of the Corporation as if he were a Director, is equated with a Director. A legal action (claim) as

meant in the present Article cannot be filed against an administrator appointed by the court.

- 8. The present Article does not affect the possibilities of the liquidator in the bankruptcy of the

Corporation to file a legal action (claim) against a Director on the basis of the agreement between the

Corporation and the Director or on the basis of Article 2:9.

- 9. Where a Director is liable pursuant to the present Article, but he is unable to pay the debt which

has arisen as a consequence thereof, the liquidator in the bankruptcy of the Corporation may, on

behalf of the liquidation estate, nullify by means of an extrajudicial declaration all juridical acts which

have been performed by the Director without any legal obligation to do so, and which have harmed the

recovery rights against his own property, if it is plausible that these juridical acts have been performed

only or mainly with the intention to harm these recovery rights. Article 3:45, paragraph 4 and 5,

applies accordingly.

- 10. Where the liquidation estate of the Corporation is insufficient to file a legal action (claim) on the

basis of the present Article or of Article 2:9 or to make preliminary inquiries as to the possibilities to

file such actions (claims), the liquidator in the bankruptcy of the Corporation may request the Minister

of Justice to provide him the necessary funds by way of an advanced payment. The Minister may set

rules for the assessment of the merits of such request and for the limits within which the request may

be granted. The request must contain the grounds on which it is based, and a reasoned estimate of the

cost and extent of the inquiries. Where the request concerns the start of preliminary inquiries it needs

the approval of the magistrate in bankruptcy ('rechter-commissaris').

Section 2.4.3 The capital of an Open Corporation

Article 2:93 Juridical acts performed in the name of a still to be formed Open Corporation

- 1. It is possible to perform juridical acts in the name of an Open Corporation ('naamloze

vennootschap') which still has to be formed (incorporated); from such juridical acts, however, can only

arise rights and obligations for the Corporation when it has ratified these juridical acts after its

formation (incorporation), either explicitly or tacitly, or when it has become engaged (bound) due to

paragraph 4.

- 2. The persons who have performed a juridical act in the name of a still to be formed Corporation,

are jointly and severally liable for that act until the Corporation has ratified it after its formation

(incorporation), unless the contrary has been stipulated explicitly in respect of that juridical act.

- 3. If the Corporation has ratified the juridical act but fails to perform the obligations which arise from

it, then the persons who have acted in the name of the still to be formed Corporation are jointly and

severally liable for the damage which a third person suffers as a result, if they knew or reasonably

could have known that the Corporation could not comply with these obligations, all without prejudice to

any possible liability of the Directors on account of a ratification. The knowledge that the Corporation

19

could not comply with its obligations, is presumed to be present when the Corporation is declared

bankrupt within one year after its formation (incorporation).

- 4. In the notarial deed of incorporation the founders (incorporators) can only engage (bind) the

Corporation directly to the following juridical acts: the issuance of shares, the acceptance of

contributions paid up on those shares, the appointment of Directors, the appointment of Supervisory

Directors and the performance of juridical acts as meant in Article 2:94, paragraph 1*). If a founder

(incorporator) has observed insufficient diligence in respect thereof, then Articles 2:9 and 2:138 shall

apply accordingly.

Section 2.4.5 The Board of Directors of an Open Corporation and the

supervision of the Board of Directors

Article 2:129 Tasks and powers of the Board of Directors

- 1. Subject to any restrictions under the articles of incorporation, the Board of Directors is charged

with the governance (management) of the Corporation

- 2. The articles of incorporation may provide that a particular Director designated by name or function

(position), may cast more than one vote. One Director may not cast more votes than the other

Directors combined.

- 3. Resolutions of the Board of Directors can only be subjected by or pursuant to the articles of

incorporation to the approval of a body of the Corporation.

- 4. The articles of incorporation may provide that the Board of Directors should behave according to

the instructions of a body of the Corporation on the general policy which is to be pursued on areas set

in the articles of incorporation.

- 5. The Directors shall in the performance of their duties direct their attention to the interests of the

Corporation and of the enterprises connected with it. *)

- 6. A Director does not participate in the deliberations and decision-making if he has a direct or

indirect personal interest therein that is contrary to the interests meant in paragraph 5. If, as a result,

no Board resolution can be passed, the resolution shall be passed by the Supervisory Board. In the

absence of a Supervisory Board, the resolution shall be passed by the General Meeting, unless the

articles of incorporation provide otherwise.*)

- 7. If shares in the Corporation or depository receipts for shares issued in cooperation with the

Corporation are admitted for trade to a regulated market as meant in Article 1:1 of the Financial

Supervision Act , and a Director holds shares in the Corporation or rights have been granted to him to

subscribe on or acquire shares in the capital of the Corporation, then the Corporation shall, if it makes

public (discloses) that it has passed a resolution as meant in Article 2:107, paragraph 1, under (a), (b)

or (c) or that a public bid is announced as referred to in Article 5 of the Decree Public Bids Wft, assess

the value which the shares or rights of the Director had, after closing of the stock exchange, four

weeks prior to the day on which this resolution has passed or a public bid was announced. Four weeks

after that resolution or, if a public bid has been announced, for weeks after the ending of that public

bid, the value of the shares or rights shall be assessed again after closing of the stock exchange. If the

value has increased compared to the earlier assessment, the Director has to pay that increase in value

to the Corporation. The Supervisory Board shall assess the increase in value. Where Article 2:129a is

applied, the Board of Directors shall asses the increase in value, yet without any participation of the

executive Directors in the decision-making. *)

*) In force as of 01-01-2013.

20

Article 2:129a Division between non-executive and executive Directors*)

- 1. The articles of incorporation may specify that the duties of the Directors are divided between one

or more non-executive Directors and one or more executive Directors. The duty to supervise the

performance of duties by the Directors cannot be taken away from a non-executive Director by a

division of duties as meant in the previous sentence. Te chairmanship of the Board of Directors, the

making of proposals for the appointment of a Director and the adoption (assessment) of the

remuneration of the executive Directors may not be assigned to an executive Director. Non-executive

Directors are always natural persons.

- 2. The executive Directors do not participate in the decision-making on the adoption (assessment) of

the remuneration of executive Directors.

- 3. It is allowed to specify by or pursuant to the articles of incorporation that one or more Directors

may decide (pass resolutions) legitimately in regard of subjects belonging to his or their duty. When

such specification is made pursuant to the articles of incorporation, this must be done in writing.

*) In force as of 01-01-2013.

Article 2:130 Power of representation

- 1. The Board of Directors represents the Corporation as far as the law does not provide otherwise.

- 2. Each Director may also individually represent the Corporation. The articles of incorporation may,

however, provide that only one or more of the Directors may represent, next and in addition to the

Board of Directors, the Corporation. The articles of incorporation may provide furthermore that a

Director only has the power to represent the Corporation in cooperation with one or more other

persons.

- 3. The power of representation of the Board of Directors or of the Directors to whom such power is

granted, either individually or jointly with others, is always unrestricted and unconditional, as far as

the law does not provide otherwise. A legally permitted or required restriction or condition regarding

the power of representation can only be invoked by the Corporation.

- 4. The articles of incorporation may also grant other persons than Directors the power to represent

the Corporation.

Book 2 Legal Persons

Title 2.5 Closed Corporations (private limited companies)

Article 2:216 Distribution of profits

- 1. The General Meeting is empowered with the allocation (appropriation) of the profits which have

been determined by adoption of the annual accounts, and with the adoption of the distributions, to the

extent that the equity (total assets and liability) of the Closed Corporation (‘besloten vennootschap’)

exceeds the reserves which have to be maintained by virtue of law or the articles of incorporation. The

articles of incorporation may limit the powers meant in the first sentence or assign these to another

body of the Closed Corporation.

- 2. A resolution (decision) for a distribution has no effect as long as the Board of Directors has not

21

given its approval to it. The Board of Directors shall only deny its approval if it knows or reasonably

ought to foresee that the Closed Corporation (‘besloten vennootschap’), after the distribution, shall no

longer be able to continue the payment of its due and collectable debts.

- 3. If the Closed Corporation (‘besloten vennootschap’), after a distribution, is not able to continue the

payment of its due and collectable debts, then the Directors who knew that result at the moment of

the distribution or who reasonably ought to have foreseen that result at that moment, are joint and

several liable towards the Closed Corporation (‘besloten vennootschap’) for compensation of the deficit

which has arisen on account of the distribution, raised with the statutory interest running as of the day

of distribution. Article 2:248, paragraph 5, applies accordingly. Not liable is the Director who proves

that it is not due to him that the Closed Corporation (‘besloten vennootschap’) has made the

distribution and, in addition, that he has not been negligent in taking measures to avert the

consequences thereof.

The person who acquired the distribution while he knew or reasonably ought to have foreseen that the

Closed Corporation (‘besloten vennootschap’) would no longer be able to continue the payment of its

due and collectable debts after the distribution, is towards the Closed Corporation (‘besloten

vennootschap’) liable for compensation of the deficit which has arisen on account of the distribution, to

at the most the amount or value of the distribution he received, raised with the statutory interest

running as of the day of distribution.

When the Directors have paid the debt-claim by virtue of the first sentence, then the compensation

meant in the third sentence is made to them in proportion to the part that each Director has paid. With

regard to a debt that is imposed pursuant to the first or third sentence, the debtor has no right of

setoff.

- 4. For the purpose of paragraph 3 a Director is equated with a person who has laid down the

corporate policy or has co-participated therein as if he was a Director. The legal claim (right of action)

cannot be filed against an administrator appointed by the court.

- 5. In calculating each distribution, the shares that the Closed Corporation (‘besloten vennootschap’)

holds in its own capital (treasury shares) are not taken into account, unless the articles of

incorporation provide otherwise.

- 6. In calculating the amount which is to be distributed on each share, only the amount of the

obligatory payments on the nominal amount of the shares is taken into account. It is possible to

derogate from the previous sentence in the articles of incorporation or each time with the approval of

all shareholders.

- 7. The articles of incorporation may provide that shares of a certain type (class) or indication do not

or only in a limited way enclose a right of sharing in the profits or reserves of the Closed Corporation

(‘besloten vennootschap’).

- 8. For an arrangement in the articles of incorporation as meant in paragraph 6 or 7, the approval is

required of all holders of shares whose rights are harmed by such amendment of the articles of

incorporation.

- 9. The articles of incorporation may provide that the claim of a shareholder does not become

prescribed after a period of five years, but shall elapse after a longer period of time. Such a provision

in the articles of incorporation shall in that event apply accordingly to the claim of a holder of a

depository receipt against the shareholder of the share for which that depository receipt was issued.

- 10. The articles of incorporation may provide that the profits to which holders of shares of a specific

type (class) are entitled, shall be reserved in full or in part for their benefit.

- 11. Paragraph 3 does not apply to distributions in the form of shares in the capital of the Closed

Corporation (‘besloten vennootschap’), nor to the crediting of not paid up shares.

22

Section 2.5.5 The Board of Directors of a Closed Corporation and the

supervision of the Board of Directors

Article 2:239 Tasks and powers of the Board of Directors

- 1. Subject to any restrictions under the articles of incorporation, the Board of Directors is charged

with the governance (management) of the Corporation

- 2. The articles of incorporation may provide that a particular Director designated by name or function

(position), may cast more than one vote. One Director may not cast more votes than the other

Directors combined.

- 3. Resolutions of the Board of Directors can only be subjected by or pursuant to the articles of

incorporation to the approval of a body of the Corporation.

- 4. The articles of incorporation may provide that the Board of Directors has to behave itself according

to the instructions of another body of the Corporation. The Board of Directors is compelled to follow

the instructions, unless these are in conflict with the interests of the Corporation or of the enterprise

connected with it.

- 5. The Directors shall in the performance of their duties direct their attention to the interests of the

Corporation and of the enterprises connected with it. *)

- 6. A Director does not participate in the deliberations and decision-making if he has a direct or

indirect personal interest therein that is contrary to the interests meant in paragraph 5. If, as a result,

no Board resolution can be passed, the resolution shall be passed by the Supervisory Board. In the

absence of a Supervisory Board, the resolution shall be passed by the General Meeting, unless the

articles of incorporation provide otherwise.*)

*) In force as of 01-01-2013.

Article 2:239a Division between non-executive and executive Directors*)

- 1. The articles of incorporation may specify that the duties of the Directors are divided between one

or more non-executive Directors and one or more executive Directors. The duty to supervise the

performance of duties by the Directors cannot be taken away from a non-executive Director by a

division of duties as meant in the previous sentence. Te chairmanship of the Board of Directors, the

making of proposals for the appointment of a Director and the adoption (assessment) of the

remuneration of the executive Directors may not be assigned to an executive Director. Non-executive

Directors are always natural persons.

- 2. The executive Directors do not participate in the decision-making on the adoption (assessment) of

the remuneration of executive Directors.

- 3. It is allowed to specify by or pursuant to the articles of incorporation that one or more Directors

may decide (pass resolutions) legitimately in regard of subjects belonging to his or their duty. When

such specification is made pursuant to the articles of incorporation, this must be done in writing.

*) In force as of 01-01-2013.

23

Article 2:240 Power of representation

- 1. The Board of Directors represents the Corporation as far as the law does not provide otherwise.

- 2. Each Director may also individually represent the Corporation. The articles of incorporation may,

however, provide that only one or more of the Directors may represent, next and in addition to the

Board of Directors, the Corporation. The articles of incorporation may provide furthermore that a