auditing- nature and basic conceptscaclubindia.s3.amazonaws.com/cdn/forum/files/70126_1175975...the...

TRANSCRIPT

Rathore Institute CA. Nitin Gupta

1

Chapter-1 Auditing- Nature and Basic Concepts

Auditing – Meaning

The word “Auditing” has been derived from Latin word “audire” which means “to

hear”.

Audit is an independent examination of financial information of any entity whether

profit making or not irrespective of its size & legal structure, when such an audit is

conducted with a view to express an opinion thereon.

The audit is not confined to financial audit alone. It may be extended to other areas

also such as management audit, operational audit, internal audit and environmental

audit etc.

The audit is conducted for a stated purpose, for example, the financial audit may be

conducted to ascertain whether they present a true and fair view of the financial

position and the operating result of the enterprise.

Every audit has to be based on some evidence.

The audit findings have to be communicated to those who have appointed the auditor.

For example, in case of a company the audit report is made to the shareholders.

Auditing – Features

1- Examinations of books & statements

The Preparation of financial statements is the responsibility of management of entity. The audit of financial statement does not relieve the management of its liability. Auditor's opinion is on financial statements. General purpose financial statement includes:

Statement of Profit & Loss: Which indicates profits earned or loss incurred during a particular financial year. Balance sheet: Which shows position of assets & liabilities at a particular date. Cash flow & fund flow Statement: Which shows movement of cash/funds during a particular financial year. (However these are not prepared by all entities).

Notes to accounts: Disclosures or explanatory notes.

Rathore Institute CA. Nitin Gupta

2

2- On the basis of proper evidence An audit examination is to be made on the basis of evidential documents such as

invoices, money receipts, and other records, including information and explanations supplied by authorized representatives of the client.

It is the duty of the auditor to carefully assess and evaluate every piece of evidence relevant for his examination.

3- By a properly qualified person In India, audit is to be conducted by a professional having good accounting & auditing

background. A chartered accountant having certificate of practice is eligible to conduct audit. 4- In a Systematic &Independent manner Audit has to be conducted in a proper way. Auditor should be completely objective (unbiased) in his approach. He should not be influenced by the client.

5- Entity His client can be any entity whatever is the legal form i.e., it proprietorship, partnership

trust or company etc. The entity may be profit oriented or a charitable one (For Example- Trust, Section 25

Companies)

6- Opinion His opinion is on 'true &fair view' of financial statements. For this, it is necessary that

(i) Financial statement have been prepared using acceptable policies which are consistently applied

(ii) Financial statements have" been prepared as per regulations, & (iii) There is appropriate disclosure of all material items.

Concept of True & Fair [May 2005 8 Marks, Nov 2012 6 Marks] What Constitutes "true and fair", however, has not been defined in any legislation. The concept of true and fair is a fundamental concept in auditing. The phrase “true and fair" in the auditor's report signifies his opinion as to whether the

state of affairs and the results are truly and fairly represented in the accounts under audit.

Section 211(5) of the Companies Act provides that the accounts of a company shall be deemed as not disclosing a true and fair view, if they do not disclose any matters are required to be disclosed by virtue of provisions of Schedule VI of that Act, virtue of a notification or an order of the Central Government modifying the disclosure requirements.

It is a matter of an auditor’s judgment in the particular circumstances of a case. An auditor has to see:

Rathore Institute CA. Nitin Gupta

3

That the assets are neither undervalued nor overvalued, No material assets are omitted; The charge, if any, on assets are disclosed The liabilities are not under or overvalued and the same are properly classified. Material liabilities should not be omitted The statement of profit and loss discloses all the matters required to be disclosed by

Part II of Schedule VI and the balance sheet has been prepared in accordance with Part I of Schedule VI;

Accounting policies have been followed consistently. All unusual, exceptional or non-recurring items have been disclosed separately.

(Extra ordinary items)

Independent Audit [RTP, Nov 89, May 92, May 93, Nov 91, May 97, May 01, May 07, May 05, May 08, Nov 09,May 10, May 2012 5-8 Marks] The need for auditor independence is provided in Standard on auditing. The Companies Act, 1956 also contains specific provision to ensure auditor’s

independence. As per The chartered Accountants Act, 1949 as amended by The Chartered Accountants

(Amendment) Act, 2006, independence of auditor is required. Independence means that the judgment of a person is not subordinate to wishes of

another person. It requires that he should not act under any influence. If auditor maintains high degree of independence, credibility of financial statements is

enhanced. Independent audit report will be accepted and respected by all the stakeholders. Advantage of Independent Audit

It safeguards the financial interest of persons not associated with the management like shareholders.

It acts as a moral check on the employees from committing fraud.

It is helpful in setting tax liability.

It ensures maintenance of adequate books and records, statutory registers etc.

Audited financial statements are the basis for determining amount receivable or payable in certain circumstances.

Aspects to be covered in Audit The principal aspects to be covered in an audit concerning the final statements of accounts are as follows 1) Accounting and Internal Control System The auditor should obtain an understanding of the accounting and the internal control

system operating in the enterprise. Such an understanding will enable the auditor to ascertain the degree to which reliance can be placed on the information obtained during the audit.

Rathore Institute CA. Nitin Gupta

4

The auditor should review the system from time to time to ascertain its adequacy and comprehensiveness.

2) Examination of books, records etc. The auditor should check the arithmetical accuracy, authenticity and the validity of

transactions entered in to the books of accounts. He should ensure that the entries in the books of accounts are adequately supported by

underlying papers, documents, and other audit evidences.

3) Compliance with the Generally Accepted Accounting Standards and Applicable Statutory Regulation The financial statements should be prepared in accordance with the requirements of

applicable laws and should comply with the relevant accounting standards, guidance notes issued by the ICAI etc.

4) Reporting Once the audit is carried out, the audit findings need to be communicated to the

appropriate person/body. An audit report states that the opinion of the auditor as to the true and fair view of the

financial position and operating results of the enterprise.

Objective of Audit The objective of an audit may be classified into two categories (a) Primary Objective and (b) Secondary Objective.

Primary Objective (As per SA 200 Revised) Audit is conducted to express an opinion on financial statements. Thus primary

objective is Reporting. The auditor reports whether financial statements represent true and fair view. True and fair view can be examined by considering whether:

(a) Financial statements have been prepared using consistent & acceptable accounting policy.

(b) Financial statements comply with relevant rules & regulation and (c) Financial statements contain disclosure of all material matters.

Secondary Objective [Nov 2004, 8 Marks]

Rathore Institute CA. Nitin Gupta

5

Secondary objective is detection of misstatement in financial statements. These misstatements may be fraud and errors. SA 240 (Revised) on “The Auditor’s Responsibility to consider Fraud and Error in an

Audit of Financial Statements.” issued by the ICAI defines the term fraud and error and lays the auditor’s responsibility as regard fraud and error.

As per SA-240 primary responsibility of prevention, detection & correction misstatement is that of management.

Auditor may not reveal all misstatement, but if auditor performs his work in accordance with basic principles governing an audit, he cannot be held liable for misstatement in financial statements of client.

The term fraud refers to an intentional act by one or more individuals among management, those charge with governance, employees or third parties, involving the use of deception to obtain an unjust or illegal advantage.

The term error refers to an unintentional misstatement in the financial statements. Auditor should enquire with management regarding assessment and procedure to

identify fraud. Auditor should enquire with those Charged with Governance regarding supervision

by them and their knowledge of fraud. If Auditor finds misstatement as fraud, then auditor should consider the reliability of

written representation and communication at appropriate level on timely basis. If Many Material Frauds as found, then consider whether to continue or not. If auditor

continues he will consider the matter in Audit Report, if auditor does not continue then after discussing with Those Charged with Governance, he will withdraw and communicate the reason to appointing authority, incoming auditor and regulatory authority.

Errors may be classified as follows

As per accounting aspects: Errors of omission- It occurs when a transaction is not recorded in the books of account, either wholly or partially. Full omission does not affect the trial balance but partial omission does. Errors of Commission- It may be committed either at the stage of recording a transaction in the books of original entry or while posting it to the ledger. Errors in totaling and balancing accounts or in carrying forward totals to the trial balance are also called errors of commission. These types of errors may or may not affect the trial balance. [May 2001, 5 Marks] Errors of principle- An error of principle occurs when the generally accepted principles of accounting are not observed while recording any transaction in the books of account. These type of errors do not affect the trial balance. Compensating errors- when there are two or more errors, but they compensate the effect of each other. These problems do not affect the trial balance.

Rathore Institute CA. Nitin Gupta

6

As per nature

Self revealing errors: The existence of these errors becomes apparent during compilation of accounts. A few illustrations of such errors are given hereunder, showing how they become apparent

1 Omission to post a part of a journal entry to the ledger

Trial Balance is thrown out of agreement

2

A failure to record in the cash book paid into or withdrawn from the bank

Bank reconciliation statement will show up error

3

A mistake in recording amount received from X in the account of Y

Statement of account parties will reveal the mistake

Non Self revealing error: The existence of these errors is not revealed automatically by routine accounting procedures. These can be revealed by detailed analysis and normal audit procedures. Example- Revenue expenditure is charged as capital expenditure. Unintentional errors- These are unintentional mistake. Example- Wages paid to X; a casual labourer has not been recorded in the books of account. Intentional errors- These are intentional mistakes / fraud. Example- Fictitious purchases of Rs. 10,000 have been recorded by cashier to misappropriate cash. Procedural errors- These are the errors in the implementation of procedures or frauds. Example- Payment of a purchase invoice without sufficient purchase documents.

Basic Principles Governing an Audit [Nov 2000, Nov 2002, Nov 2003, Nov 2006, 10 Marks, May 2013-8 Marks]

Followings are the basic principles that govern the auditor’s responsibilities whenever an audit is carried out:

1- Integrity, Objectivity, Independency

Auditor should be straightforward, honest and sincere in his professional work. He should be fair and must not be biased. He should maintain impartiality. He should be free of any interest

2- Confidentiality

He should maintain confidentiality of information acquired during his work. He should not disclose any such information to a third party without specific

permission of client or legal or professional duty to disclose.

Rathore Institute CA. Nitin Gupta

7

3- Skills and competence

He should perform work with due professional care. Audit should be performed by persons having adequate training, experience and

competence.

4- Work performed by others

The auditor can delegate work to assistants or use work performed by other auditors and experts.

But he will continue to be responsible for his opinion on financial information. The Auditor is entitled to rely on work performed by others, provided

He exercises adequate skills and care and there is nothing to doubt.

5- Documentation

He should document matters relating to the audit (maintain working papers). Working papers are maintained to demonstrate that the audit was carried out in

Accordance with the basic principles.

6- Planning

He should plan his work to conduct audit in effective and timely manner. Plans should be based on knowledge of the clients business. Plans should be further developed and revised during audit if circumstance requires so.

7- Audit Evidence Auditor should obtain sufficient and appropriate audit evidence by performing

compliance and substantive procedures. Evidences enable the auditor to draw reasonable conclusion. Compliance procedures mean the tests designed to obtain reasonable assurance that

internal controls have been properly designed & operating effectively throughout the year.

Substantive Procedures are performed to obtain evidence as to the completeness, accuracy and validity of data produced by the accounting system.

8- Internal controls

Internal control system ensures that the accounting system is adequate and that all the accounting information has been duly recorded.

The auditor should understand the accounting system and related internal controls adopted by the management.

He should study and evaluate internal controls system to determine the nature, timing and extent of other audit procedures.

Rathore Institute CA. Nitin Gupta

8

9- Audit conclusion and Reporting

The auditor should review and assess the conclusions drawn from the audit evidences

obtained through performance of procedures. The audit report should contain clear written expression of opinion on the financial

statements. His report is on whether:

The financial information has been prepared using acceptable accounting policies which have been consistently applied; The financial information complies with relevant regulation and statutory requirements; and There is adequate disclosure of all material matters.

The report should be as per legal requirement. When other than opinion is given, the audit report should state the reasons thereof.

Quality of Auditor [Nov 2004, 4 Marks]

a) Integrity Auditor should be honest, sincere and straightforward while performing his professional duties.

b) Communication Skill During the conduct of audit, he has to interact with various officers and staff of organization & third parties, thus he requires good oral & written communication abilities.

c) Confidentiality He should not disclose confidential information acquired during conduct of his professional duties to any third party except when permitted by client or required by law.

d) Independence He should not be subordinates his judgment to the will of others. He should conduct the audit in unbiased way.

e) Knowledge He should have general knowledge of client’s business and economic trends etc. He must continuously update his knowledge to conduct audit effectively.

f) Logical Skills He must be able to analyse & interpret problem so that he can accordingly deal with the same.

g) Judgment He should be capable to taking firm judgments as to which items are to be checked and what should be the sample size.

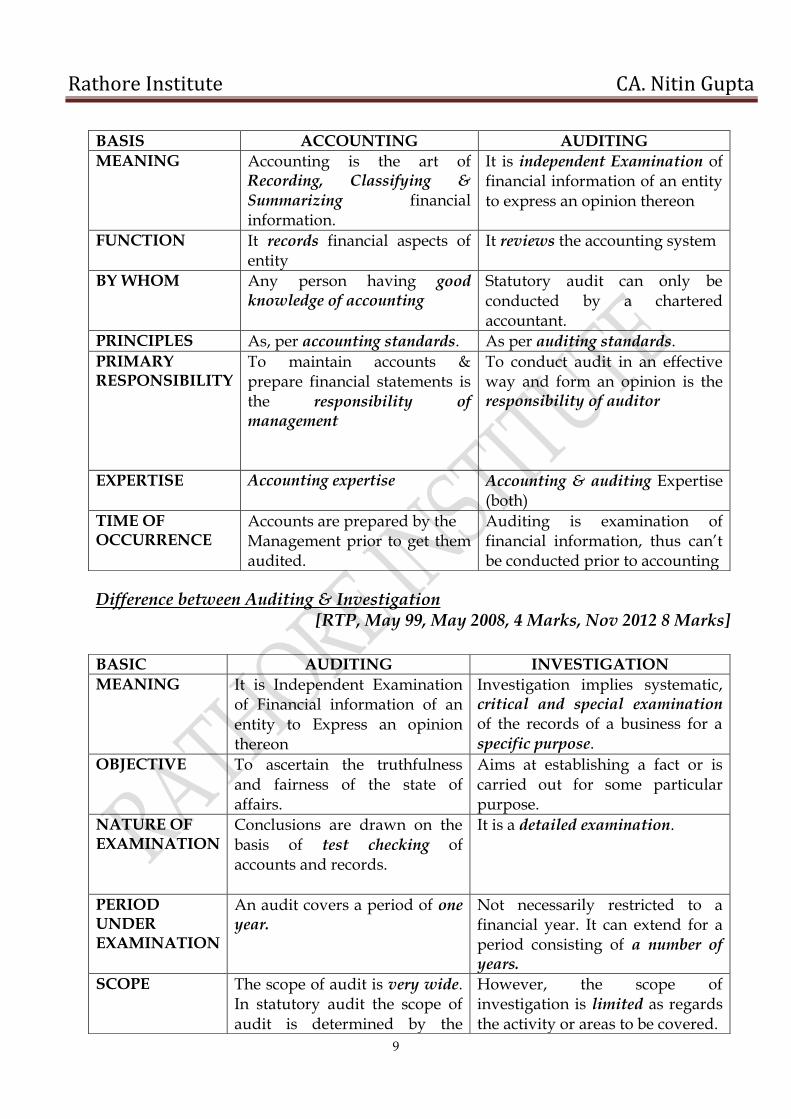

Difference between Accounting & Auditing [May 99]

Rathore Institute CA. Nitin Gupta

9

Difference between Auditing & Investigation [RTP, May 99, May 2008, 4 Marks, Nov 2012 8 Marks]

BASIS ACCOUNTING AUDITING

MEANING Accounting is the art of Recording, Classifying & Summarizing financial information.

It is independent Examination of financial information of an entity to express an opinion thereon

FUNCTION It records financial aspects of entity

It reviews the accounting system

BY WHOM Any person having good knowledge of accounting

Statutory audit can only be conducted by a chartered accountant.

PRINCIPLES As, per accounting standards. As per auditing standards.

PRIMARY RESPONSIBILITY

To maintain accounts & prepare financial statements is the responsibility of management

To conduct audit in an effective way and form an opinion is the responsibility of auditor

EXPERTISE Accounting expertise Accounting & auditing Expertise (both)

TIME OF OCCURRENCE

Accounts are prepared by the Management prior to get them audited.

Auditing is examination of financial information, thus can’t be conducted prior to accounting

BASIC AUDITING INVESTIGATION

MEANING It is Independent Examination of Financial information of an entity to Express an opinion thereon

Investigation implies systematic, critical and special examination of the records of a business for a specific purpose.

OBJECTIVE To ascertain the truthfulness and fairness of the state of affairs.

Aims at establishing a fact or is carried out for some particular purpose.

NATURE OF EXAMINATION

Conclusions are drawn on the basis of test checking of accounts and records.

It is a detailed examination.

PERIOD UNDER EXAMINATION

An audit covers a period of one year.

Not necessarily restricted to a financial year. It can extend for a period consisting of a number of years.

SCOPE The scope of audit is very wide. In statutory audit the scope of audit is determined by the

However, the scope of investigation is limited as regards the activity or areas to be covered.

Rathore Institute CA. Nitin Gupta

10

Inherent Limitations of Audit (As per SA 200 Revised) [Nov 1998, Nov 2001, May 2003 Nov 2005, 4-8 Marks] Meaning The limitations which cannot be overcome irrespective of the nature and extent of a procedures. Followings are the inherent limitation: I. Involvement of judgement

Auditor’s work involves exercise of judgment, for example, in deciding the extent of audit procedures and in assessing the reasonableness of the judgment and estimates made by the management in preparing the financial statements. The judgement by auditor may not always be correct.

II. Nature of evidences

1. The evidences obtained by the auditor are persuasive rather than conclusive and they cannot ensure the auditor in a certain way.

2. Because of these factors, the auditor can only express an opinion and absolute certainty in auditing is rarely attainable.

3. There is also likelihood that some material misstatements of the financial information resulting from fraud or error, if either exists, may not be detected.

III. Test checking

1. Auditor uses sampling during performance of audit. 2. It is not possible for him to conduct detailed checking due to time constraints. 3. As he does not check each & every item, it's impossible for him to detect all fraud &

errors. IV. Inherent limitations of internal controls

1. Internal controls suffer from limitation such as collusion among employees or wrong use of authority by management etc.

2. It is clearly evident that there always is some risk of an internal control system failing to operate as designed.

relevant law and in private audit, by the letter of engagement.

CONDUCTED BY

A CA within the meaning of CA Act 1949.

Any person, who need necessarily be a CA.

FINANCIAL ASPECTS

Generally covers financial aspects only

Covers both financial and non financial aspects.

NATURE OF EVIDENCE

Audit is concerned only with prima facie evidence which is sufficient and appropriate

But in an investigation, conclusive evidence is required.

SUBMISSION OF REPORT

The audit report is submitted to the owners of the business.

The investigation report is to be submitted to person (s) on whose behalf it is being conducted.

Rathore Institute CA. Nitin Gupta

11

3. If internal controls are weak, auditor may not be in a position to obtain assurance.

Accounting Concept- Fundamental Accounting Assumption [Nov 2003, May 2007, May 2008, 4 Marks] Meaning- Certain fundamental accounting assumptions underlie the preparation & presentation of financial statements. Their use is assumed. Three fundamental accounting assumptions- Going Concern, Consistency and Accrual. Going Concern: The enterprise is normally viewed as a going concern that is as continuing in operation for the foreseeable future. It is assumed that the enterprise has neither the intention nor the necessity of liquidation. Consistency: It is assumed that accounting policies are consistent from one period to another. Accrual: Revenues and costs are accrued, that is recognized as they are earned or incurred (and not as money is received or paid) and recognized in the financial statements of the periods to which they relate. Disclosure requirement as per AS-1 If the fundamental accounting assumptions, viz., Going concern, Consistency and Accrual are followed in financial statements specific disclosure is not require fundamental accounting assumption is not followed, the fact should be disclosed.

Meaning & Disclosure of Accounting Policies [May 1999, Nov 2002, 4 Marks]

Meaning- It refers to specific accounting principles & methods of applying those principles, adopted by entity in preparation & presentation of financial statements. Examples- The following are example of the areas as given in AS 1, Disclosure of Accounting policies in which different accounting policies may be adopted by different enterprises. [Nov 2007 5 Marks, Nov 2011 6 Marks, Nov 2012 10 Marks] Methods of depreciation ,depletion and Amortization Treatment of expenditure during construction conversion or translation of foreign currency items Valuation of inventories Treatment of goodwill Valuation of investments Treatment of retirement benefits Recognition of profit on long-term contracts Valuation of fixed assets Treatment of contingent liabilities

Rathore Institute CA. Nitin Gupta

12

Requirement of AS-1 regarding disclosure of Accounting Policies- To ensure proper "understanding of financial statements, it is necessary that all

significant accounting policies adopted in the preparation and presentation of financial statements should be disclosed.

Such disclosure should form part of the financial statements. They should be disclosed at one place instead of being scattered over several

statements, schedules & notes and form part of financial statements. Any change in an accounting policy which has a material effect should be disclosed

State True or False with Reason

1) Auditor’s primary responsibility is to detect errors and frauds. False- Auditor’s primary responsibility as per SA 200 is to express an opinion on financial statements.

2) The fundamentals accounting assumptions followed for preparing financial statements should be disclosed. False- It is assumed that fundamental accounting assumptions have been followed while preparing financial statements. In case any one of these has not been followed specific disclosures should be made.

3) The primary responsibility for preparation of financial statement is of the management. True- SA 200 has asserted this.

4) The scope of financial audit extends to all type of entity. True- The scope of audit extends to all entities commercial as well as non commercial.

5) Financial statements include P&L accounting and Balance Sheet but not notes to accounts. False- Financial statements mean whole set of accounts including P&L account, Balance sheet and disclosure i.e. notes to accounts.

6) Auditor needs to be independent True- Independence means that the judgment of a person is not subordinate to wishes of any person. Independent audit enhance credibility of financial statements of client.

7) Auditor does not need communication skills, as he is concerned only with financial information. False – During conduct of audit, he has to interact with various officers and staff of client & third parties, which requires good written & oral communication skills.

8) Auditor must maintain confidentiality subject to certain exceptions. True- Auditor should not disclose any confidential information relating to client. However he can disclose if it is permitted by client or required by law.

9) Documentation is required to be kept by auditor True- Auditor should document matters relating to the audit. Working papers are maintained to demonstrate that the audit was carried out accordance with the basic principles.

10) Sampling is a major inherent limitation of audit.

Rathore Institute CA. Nitin Gupta

13

True- Auditor uses sampling during performance of audit. It is not possible for him to conduct detailed checking due to time constraints and other practical problems. As he does not check each & every items. It is impossible for him to detect all fraud & errors.

11) Auditor is not an insurer. [Nov 2008]

True- The auditor does not insures the interest of users of accounts but only states his opinion after taking all reasonable care and skill that the statement show a true and fair picture.

12) Procedural error arises as a result of transactions having been recorded in a fundamentally in correct manner. [May 2008] False- When transactions are recorded in fundamentally incorrect manner it is known as error of Principle. For e.g. a distinction not being made between capital and revenue income or expenditure.

13) When an auditor identifies a misstatement resulting from fraud, it is his responsibility to communicate it to the regulatory and enforcement authorities apart from those charges with governance. [May 2010] True- According to SA-240 “The auditor Responsibilities Relating to Fraud in an Audit of Financial Statement” an auditor identifies a misstatement resulting from the fraud or error it is his responsibility to communicate the matter with those charged with governance and, in some circumstances, when so required by laws or regulation, to regulatory and enforcement authorities also.

Rathore Institute CA. Nitin Gupta

14

Chapter-2 Core Concept in Auditing

Materiality [Nov 86, Nov 96, May 2007, Nov 2007, 4 Marks, Nov 2009, May 2013]

According to AS-1 Material items are those items, the knowledge of which might influence decisions of the user of financial statements.

SA 320 is applicable on “Planning and Performing an Audit” Materiality is therefore, an important and relevant consideration for an auditor who

has constantly to judge whether a particular item or transaction is material or not. Judgement of materiality is affected by circumstances and size of the business. Material is a relative term and what may be material in one case may not be material in

another. The concept of materiality recognizes that some matters, either individually or in

aggregate, are important for true and fair presentation of financial information in confirmation with recognized accounting policies and practices. Both the amount and nature i.e. quantity and quality should be considered.

Even insignificant items in terms of quality may also be material in special circumstances.

Sometimes the materiality of an item in term of quantity is described in law itself. For example, schedule VI requires separate disclosures of items of expenditures which are in excess of one percent of revenue from operating activities or Rs. 1,00,000.

Performance Materiality: It means the amount or amounts set by the auditor at less than materiality for the financial statements as a whole to reduce to an appropriately low level the probability that the aggregate of uncorrected and undetected misstatement exceeds materiality for the financial statements as a whole.

There is an inverse relationship between materiality and audit risk. Materiality should be considered by the auditor when: Determining the nature, timing and extent (NTE) of audit procedures. Evaluating the effect of misstatement.

Materiality decided earlier may be revised during the performance of the audit. Auditor should document the following:

Material level considered for financial statement as a whole Performance material considered Any revision made in material level considered earlier.

Audit Evidence [May 2000, Nov 2001, 4 Marks] The information, which may be oral or written obtained for the purpose of audit, is

known as audit evidence. Auditor needs evidences to obtain information for arriving at his judgement.

Rathore Institute CA. Nitin Gupta

15

"The auditor should obtain sufficient & appropriate audit evidence through the performance of compliance and substantive procedures to enable him to draw reasonable conclusion there from on which to base his opinion on the financial information." SA-500

Followings are the factors to determine the sufficient and appropriate [RTP, May 90, May 07, May 09, Nov 2010-6 Marks] Sufficiency refers to the quantum of audit evidence obtained. Appropriateness refers the relevance and reliability of the evidence. The factors that influence the Auditor’s judgement as what is sufficient and appropriate audit evidence are- a) The materiality of the item. b) Type of information available. c) Experience gained during previous audit. d) Trends indicated by accounting ratios and analysis. e) The degree of risk of misstatement

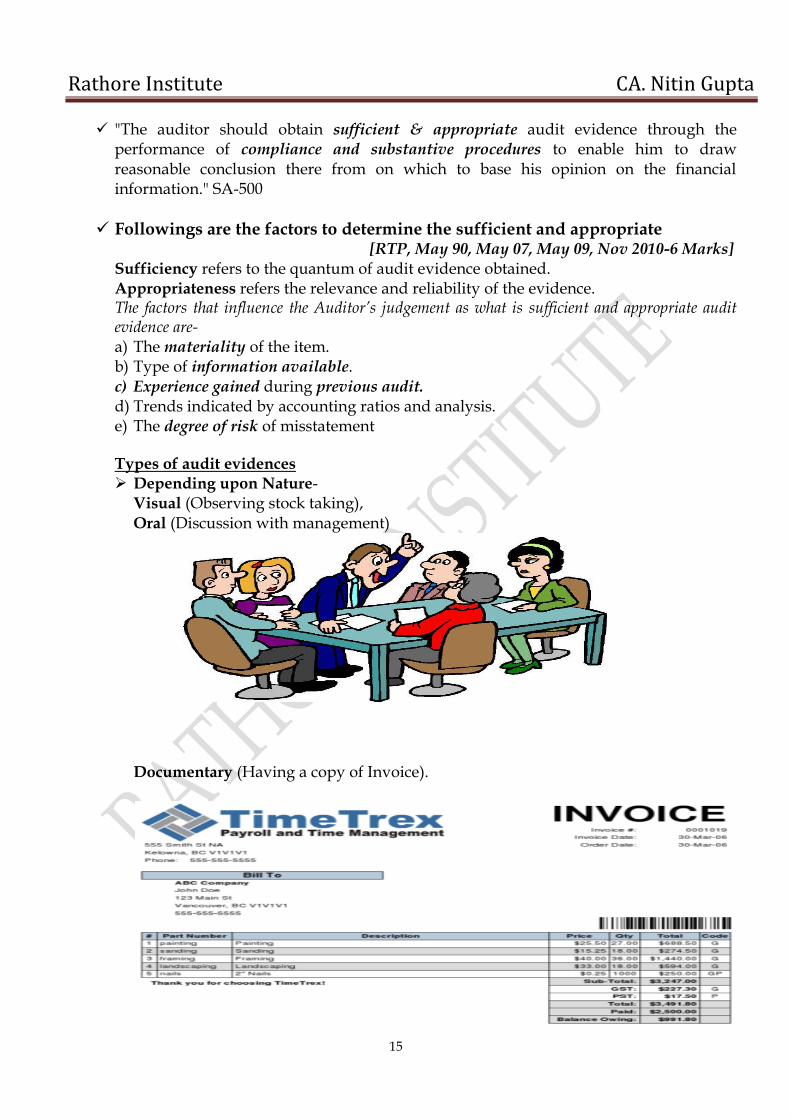

Types of audit evidences Depending upon Nature-

Visual (Observing stock taking), Oral (Discussion with management)

Documentary (Having a copy of Invoice).

Rathore Institute CA. Nitin Gupta

16

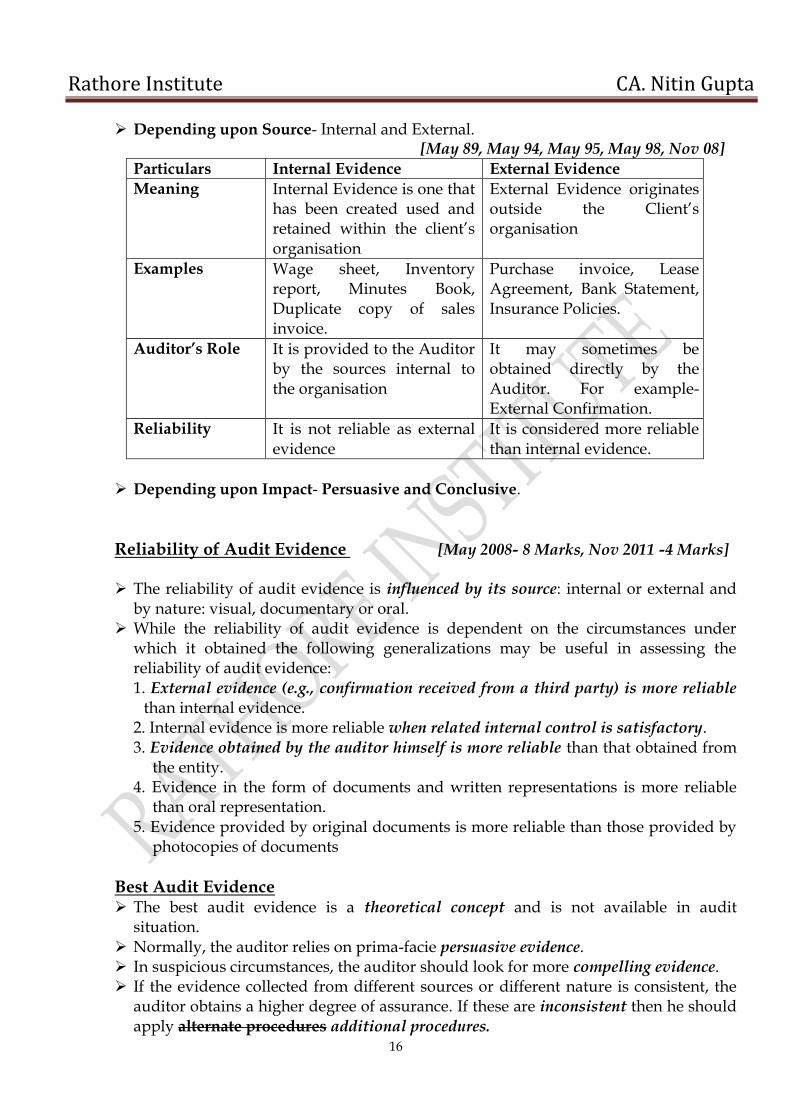

Depending upon Source- Internal and External. [May 89, May 94, May 95, May 98, Nov 08]

Particulars Internal Evidence External Evidence

Meaning Internal Evidence is one that has been created used and retained within the client’s organisation

External Evidence originates outside the Client’s organisation

Examples Wage sheet, Inventory report, Minutes Book, Duplicate copy of sales invoice.

Purchase invoice, Lease Agreement, Bank Statement, Insurance Policies.

Auditor’s Role It is provided to the Auditor by the sources internal to the organisation

It may sometimes be obtained directly by the Auditor. For example- External Confirmation.

Reliability It is not reliable as external evidence

It is considered more reliable than internal evidence.

Depending upon Impact- Persuasive and Conclusive.

Reliability of Audit Evidence [May 2008- 8 Marks, Nov 2011 -4 Marks] The reliability of audit evidence is influenced by its source: internal or external and

by nature: visual, documentary or oral. While the reliability of audit evidence is dependent on the circumstances under

which it obtained the following generalizations may be useful in assessing the reliability of audit evidence: 1. External evidence (e.g., confirmation received from a third party) is more reliable than internal evidence. 2. Internal evidence is more reliable when related internal control is satisfactory. 3. Evidence obtained by the auditor himself is more reliable than that obtained from

the entity. 4. Evidence in the form of documents and written representations is more reliable

than oral representation. 5. Evidence provided by original documents is more reliable than those provided by

photocopies of documents

Best Audit Evidence

The best audit evidence is a theoretical concept and is not available in audit situation.

Normally, the auditor relies on prima-facie persuasive evidence. In suspicious circumstances, the auditor should look for more compelling evidence. If the evidence collected from different sources or different nature is consistent, the

auditor obtains a higher degree of assurance. If these are inconsistent then he should apply alternate procedures additional procedures.

Rathore Institute CA. Nitin Gupta

17

Audit procedures to obtain evidences [May 2008-8 Marks] Compliance Procedure- [May 2013- 2 Marks] Compliance procedures are tests designed to obtain reasonable assurance that those

internal controls on which audit reliance is to be placed are in effect. Compliance tests are conducted in areas governed by the internal control e.g. Purchase, Sales etc.

In obtaining audit evidence from compliance procedures, the auditor is concerned with assertions that the internal control exists, the internal control is operating effectively and the internal control has so operated throughout the period of intended reliance. So the auditor is concerned with the existence, effectiveness and continuity of the control system

Substantive Procedure- [May 2004, May 2007, May 2010, 4 Marks]

Substantive procedures are tests designed to obtain evidence as to the completeness, accuracy and validity of the data produced by accounting system. They are of two types (1) Tests of details of transactions and balances. (2) Analysis of significant ratios and trends including the resulting investigation of

unusual fluctuations and items. (Analytical Review) In obtaining audit evidence from substantive procedures, the auditor is concerned

with following assertions. [Nov 2007, May 2008, Nov 2008, 7 Marks, May 2013]

Existence An asset or liability exists at a given date.

Rights and obligations An asset is a right of the entity and a liability is an obligation of the entity at a given date.

Occurrence A transaction or event took place which pertains to the entity

Completeness There are no unrecorded assets, liabilities or transactions.

Valuation An asset or liability is recorded at an appropriate carrying value.

Measurement A transaction is recorded in the proper amount and revenue expense is allocated to the proper period.

Rathore Institute CA. Nitin Gupta

18

Presentation An item is disclosed, classified and described in accordance with acceptable accounting policies and, when applicable, legal requirement.

Methods (Techniques) to obtain Audit Evidence [Nov 1997, Nov 2001, May 2003, 4 Marks]

One or more of the following methods: Inspection; Observation; Inquiry and confirmation; Computation; and Analytical review.

1-Inspection

Inspection consists of examining records, documents or tangible assets.

Four major categories of documentary evidence which provide different degrees of reliability to the auditor are:

Documentary evidence created and held by the third parties; Documentary evidence created and held by the entity. Documentary evidence created by third parties and held by the entity; and Documentary evidence created by entity and held by third party.

Inspection of tangible assets provides reliable evidence with respect to their existence but not necessarily as to their ownership or value.

Rathore Institute CA. Nitin Gupta

19

2-Observation

Observation consists of looking at a process a procedure being performed by the others. For example, the auditor may observe the counting of inventories by client

personnel.

3-Inquiry and confirmation [Inquiry- May 2013 4 Marks]

1. Inquiry consists of seeking appropriate information from knowledgeable person

inside or outside the entity. 2. Queries may range from formal written inquires addressed to third parties to

informal oral inquires addressed to persons inside the entity. 3. Responses to inquiries may provide the auditor with information which he did not

previously possess or may provide him with corroborative evidence. (Confirmatory evidence).

4. Confirmation consists of the response to an inquiry to corroborate (Confirm) information in the accounting records. For example, the auditor normally requests confirmation of receivable by direct communication with debtors.

External Confirmation- [Nov 2011, Nov 2012 8 Marks] It means audit evidence obtained as a direct written response to the auditor from a

third party in paper/ electronic/ other form. Auditor should carefully plan & control external confirmation

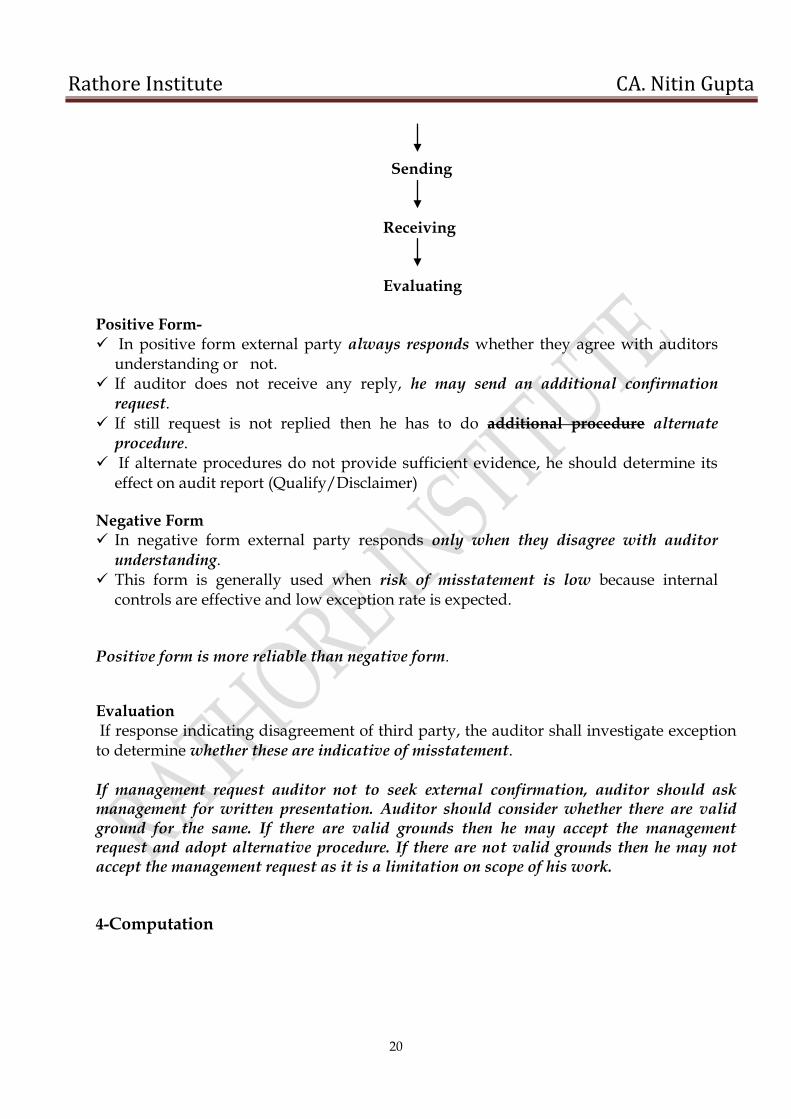

Procedure of external confirmation

Selection(To whom confirmation letter is to be sent)

Design (Positive Form or Negative Form)

Rathore Institute CA. Nitin Gupta

20

Sending Receiving

Evaluating Positive Form- In positive form external party always responds whether they agree with auditors

understanding or not. If auditor does not receive any reply, he may send an additional confirmation

request. If still request is not replied then he has to do additional procedure alternate

procedure. If alternate procedures do not provide sufficient evidence, he should determine its

effect on audit report (Qualify/Disclaimer)

Negative Form In negative form external party responds only when they disagree with auditor

understanding. This form is generally used when risk of misstatement is low because internal

controls are effective and low exception rate is expected.

Positive form is more reliable than negative form.

Evaluation If response indicating disagreement of third party, the auditor shall investigate exception to determine whether these are indicative of misstatement. If management request auditor not to seek external confirmation, auditor should ask management for written presentation. Auditor should consider whether there are valid ground for the same. If there are valid grounds then he may accept the management request and adopt alternative procedure. If there are not valid grounds then he may not accept the management request as it is a limitation on scope of his work.

4-Computation

Rathore Institute CA. Nitin Gupta

21

Computation consists of checking the arithmetical accuracy of source documents, accounting records or of performing independent calculations.

5-Analytical Review (SA-520)

Analytical procedures consist of evaluations of financial information made by a study

of relationship among data. These relationships may be between financial data and between financial and non financial data.

Analytical review may be the followings: - Ratio analysis - Trend analysis - Comparison of actual with budget - Comparison of current year figure with corresponding figure of previous year.

Analytical review consists of studying significant ratios and trends and investigation unusual fluctuation and item.

Auditor may use analytical review at planning stage. The main purpose to use analytical procedures is to determine the nature, timing and

extent of other audit procedures. Its objective is to obtain evidences using substantive procedures. If auditor identifies fluctuation or a significant difference between recorded & expected

values, he shall investigate by inquiring of management and thereafter obtaining evidences to corroborate the same and performing other procedures as necessary in the circumstances

The extent of reliance on the results of analytical procedures will depend on factors like:

Materiality of items involved

- When inventory balances are material analytical reviews alone will not be

sufficient in forming the audit conclusion

Rathore Institute CA. Nitin Gupta

22

- Where certain individual items of income or expenditure are not material,

comparison with previous year data may provide sufficient audit assurance.

Accuracy of prediction

- If the expected results of analytical procedures can be predicted with reasonable

accuracy, such procedure will be more reliable

- For example, the Gross profit percentage over various periods would be consistent

and give more audit reliance than R & D expenditure or Advertisement

expenditure etc.

Nature of risk

- If internal control over sales order processing is weak and hence control risk is

high, more reliance will have to be placed on test of details of transactions and

balances.

If auditor identifies fluctuation or a significant difference between recorded & expected

values, he shall investigate by inquiring of management and thereafter obtaining

evidences to corroborate the same and performing other procedures as necessary in the

circumstances.

Rathore Institute CA. Nitin Gupta

23

State True or False with Reason

1) Evidence should be sufficient and appropriate.

True- Auditor should obtain sufficient & appropriate evidence. Sufficiency refers to

quantum of audit evidence. Appropriateness refers to quality of audit evidences.

2) Auditor should consider consistency of evidence.

True- The audit evidences obtained through different sources or of different nature

should be consistent. If there is inconsistency among different evidences relating to a

single item, auditor should perform additional procedures to resolve inconsistency.

3) Compliance procedure is undertaken to check transaction and balances.

False- Compliance procedure is undertaken to check designing, operating effectiveness

and continuity of internal control system.

4) Substantive procedures are carried out to check data produces by accounting system.

True- Substantive procedures are undertaken to check completeness, accuracy and

validity of data produces by accounting system.

5) Auditor may use analytical review procedure at planning stage.

True The auditor should apply analytical procedures at planning stage for

understanding the business and in identifying areas of potential risk. It uses both

financial and non financial data.

6) Material items are only quantitative in nature.

False- Material items are those which may influence the judgement the judgement of

users of financial statements. It may be quantitative and qualitative as well.

7) There is inverse relation between materiality & audit risk.

True- Generally management / employees do not commit fraud in high value items.

Moreover, as a general practice, auditor checks high value items in detail. Thus it is less

risky that high value fraud and error may not be detected. So high materiality level

leaves audit risk at lower degree.

8) External confirmation means representation from management.

False- It is the process of obtaining and evaluating audit evidences through a direct

communication from a third party in response to a request for information about a

particular item.

9) Reply is required in all cases in positive confirmation request.

True- It asks the respondent to reply the auditor in all cases either by indicating the

respondent’s agreement/ disagreement with the given information or by asking the

respondent to fill in information.

10) Auditor should carefully plan & control external confirmation.

True The auditor should maintain control the process of selecting those to whom a

request will be sent, the preparation and sending of confirmation request and responses

to those requests.

Rathore Institute CA. Nitin Gupta

24

RATHORE INSTITUTE

CA-IPCC GROUP-II

AUDITING & ASSURANCE

IN 22 DAYS

BY

CA. NITIN GUPTA

Batches for Nov 2013

BATCH STARTING FROM DAYS TIMING

1ST BATCH 17 June 2013 MWFS 12 PM – 4 PM

2ND BATCH 20 July Regular 5 PM -9 PM

3RD BATCH 22 August Regular 5 PM-9 PM

4TH BATCH 22 September Regular 5 PM- 9 PM

FEE- Rs. 3,000/-

Combined Fee of IT, SM & Audit- RS. 8,000 Only

Detail of IT & SM Batch

Subject Faculty Batch Timing Fee

SM

P.S. Rathore

1st Batch- 12 June-26June

2nd Batch-12 Aug- 26 Aug

3rd Batch- 16 Sep- 30 Sep

5.30 PM- 9 PM (Laxmi Nagar)

5.30 PM- 9 PM (ITO)

12.00 PM- 4 PM(Laxmi Nagar)

Rs.

5,000

IT CA. Atul Gupta 1st Batch- 27 June-10July 5.30 PM- 9 PM Rs.

Rathore Institute CA. Nitin Gupta

25

2nd Batch-21 Aug- 2 Sep

3rd Batch- 22 Sep- 5 Oct

11.30 AM- 3.30 PM

7.30 AM- 11.30 AM

(All classes in Laxmi Nagar)

3,000

Combined Fee of IT & SM- Rs. 6400/- Only

OUR PAST RESULTS

NAME MARKS NAME MARKS

RICHA SHARMA 76 (ROLL NO 309097)

41ST

RANK

AKSHAY JAIN 62 (ROLL NO-237763)

DHRUV KANT 61 (ROLL NO-232062)

ANISHA 75 (ROLL NO-195101) GAURAV SAXENA 61 (ROLL NO-407917)

MAYANK GOEL 72 (ROLL NO-238011) NEHA MISHRA 60 (ROLL NO-405330)

SIDDARTH KUMAR 70 HIMANSHU GUPTA 60 (Roll No-408570)

JAI PRAKASH SHAH 70 ANUJ AGARWAL 60

HIMANSHU SRIVASTAV 70 (ROLL NO-240963) ANSHU RAI 60

RAJ KUMAR 69 DHEERAJ SHARMA 60

PARTH AGARWAL 68 (ROLL NO-292046) PRADEEP KUMAR 59 (ROLL NO-247528)

TANIKA NARANG 67 (ROLL NO-234348) RISHBH MISHRA 59

ANUPAM SURYA 67 HARSHI GUPTA 57

ANKIT BHATIYA 67 GURPREET SINGH 56(ROLL NO- 238865)

MOHIT SATIJA 67 DEEPAK SHARMA 55 (ROLL NO-226066)

PIYUSH JAIN 67 (ROLL NO-246505) RAJAT SINGHAL 55 (ROLL NO-288201)

NITIKA GUPTA 65 (ROLL NO-246888) RISHBH KAPOOR 53 (ROLL NO-288200)

MUKESH LUMAR 64 (ROLL NO-234028) VAIBHAV JAISWAL 52(ROLL NO- 237480)

AJMER DIN 64 (ROLL NO-229372) AMAN MITTAL 50 (ROLL NO-412814)

PUJA SINE 64 RUCHI JAISWAL 50 (ROLL NO-232255)

ASSURED GOOD MARKS IN MUCH LESS TIME

CONTACT AT

RATHORE INSTITUTE

1/50, LALITA PARK, LAXMI NAGAR, NEW DELHI-110092

PH:-011-43073355, 8527336600