august 2018 investor relations - mtu.de · (v2500, cfm56, cf34, ge90) • strong presence in asia 4...

TRANSCRIPT

MTU Aero Engines AGCompany Presentation

August 2018 – Investor Relations

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

Contents

1. Company Overview

2. Commercial OEM Business

3. Military OEM Business

4. Commercial MRO Business

5. Financials & Outlook

6. Digitization @ MTU

7. Corporate Responsibility

8. Appendix

2

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

Contents

1. Company Overview

2. Commercial OEM Business

3. Military OEM Business

4. Commercial MRO Business

5. Financials & Outlook

6. Digitization @ MTU

7. Corporate Responsibility

8. Appendix

3

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

• Risk and revenue sharing partner

with major OEMs

• Focus on Low-Pressure Turbines,

High-Pressure Compressors and

Turbine Center Frames

• Approx. 30% of active aircraft with

MTU participation

• Capability to develop and

manufacture entire engines

• R&D is typically customer financed

• MTU has high shares in key

European military programs

• World's largest independent engine

MRO provider (Maintenance, Repair

and Overhaul)

• Exposure to highest growth engines

(V2500, CFM56, CF34, GE90)

• Strong presence in Asia

4

Commercial Business Military Business Commercial MRO

MTU is Built on Three Pillars

Sales* € 1,282 m (32 %) € 445 m (11 %) € 2,285m (57 %)

OEMBusiness MRO

EBIT margin* 22.1 % 8.5 %

MTU Group* Sales: € 3,889 m / EBIT margin: 14.8 %

* FY 2017 – Key financials restated acc. to IFRS 15

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

Attractive market

• Airframers‘ order books equal 8-9 years of production

• Current passenger traffic growth of ~7% above historical levels of 5%

Strong market position

• Business jet revenues to triple over the next 10 years driven by new PW800

• GTF engines dominate future regional jet market by 90%

• Narrowbodies: V2500 key driver of aftermarket, GTF strengthens footprint by higher

market and MTU program share

• Participation in all new GE widebody programs leads to a balanced engine portfolio

• Commercial MRO: Exceptional growth achieved by extensive service and engine

portfolio

• MTU is a pure aero engine player with high exposure to the aftermarket

High visibility

• Mid to long term new engine production plans well known

• Fleet in service and regulatory requirements give high predictability in the aftermarket

• High barriers to entry

5

Key Investment Highlights

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

Contents

1. Company Overview

2. Commercial OEM Business

3. Military OEM Business

4. Commercial MRO Business

5. Financials & Outlook

6. Digitization @ MTU

7. Corporate Responsibility

8. Appendix

6

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

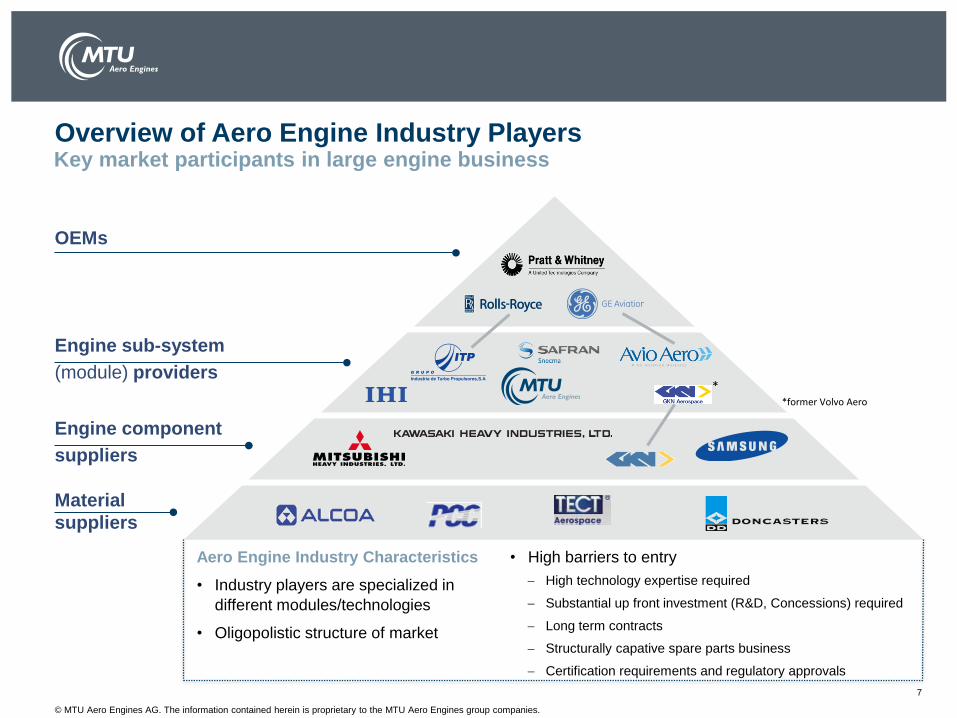

7

Key market participants in large engine business

Overview of Aero Engine Industry Players

Material

suppliers

Engine component

suppliers

Engine sub-system

(module) providers

OEMs

Aero Engine Industry Characteristics

• Industry players are specialized in

different modules/technologies

• Oligopolistic structure of market

**former Volvo Aero

• High barriers to entry

High technology expertise required

Substantial up front investment (R&D, Concessions) required

Long term contracts

Structurally capative spare parts business

Certification requirements and regulatory approvals

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

8

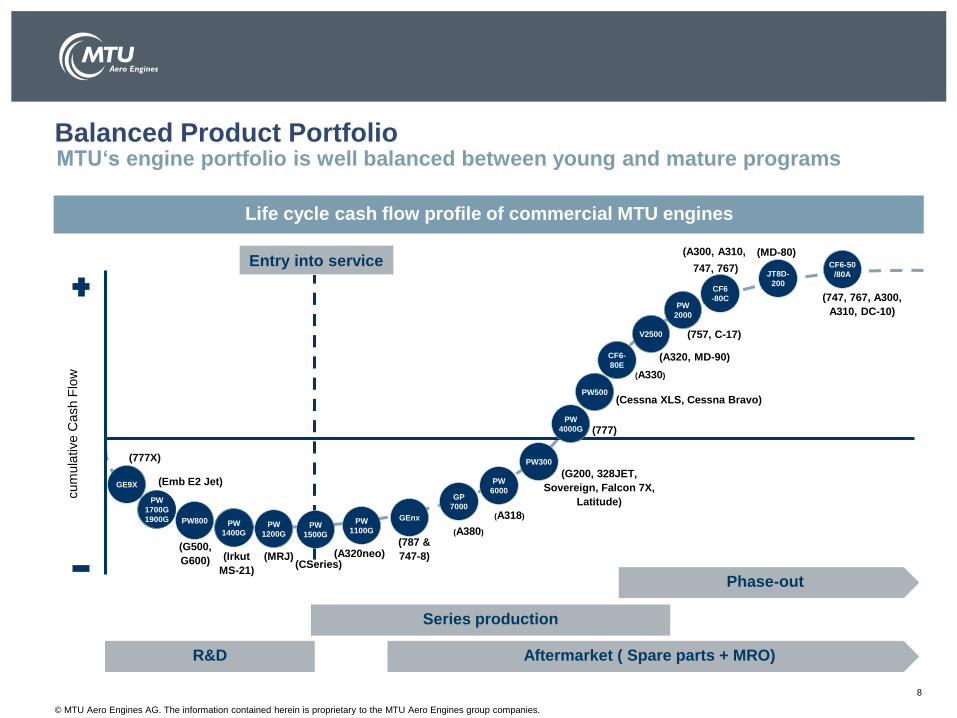

MTU‘s engine portfolio is well balanced between young and mature programsBalanced Product Portfolio

R&D

Series production

Phase-out

Aftermarket ( Spare parts + MRO)

cum

ula

tive C

ash F

low

GP

7000

(A380)

PW

6000

(A318)

PW300

(G200, 328JET,

Sovereign, Falcon 7X,

Latitude)

PW500(Cessna XLS, Cessna Bravo)

CF6-50

/80A

CF6

-80C

(A300, A310,

747, 767)JT8D-

200

(MD-80)

(747, 767, A300,

A310, DC-10)

CF6-

80E

(A330)

PW

1200G

(MRJ)

GEnx

(787 &

747-8)

Entry into service

PW

1100G

(A320neo)

PW

1400G

(Emb E2 Jet)

PW

1700G

1900G

(Irkut

MS-21)

(777X)

V2500

(A320, MD-90)

(757, C-17)

PW800

(G500,

G600)

PW

1500G

(CSeries)

GE9X

PW

4000G (777)

PW

2000

Life cycle cash flow profile of commercial MTU engines

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

9

MTU’s Continuous Growth is Supported by all Market Segments

0

20

40

60

80

100

120

140

2016 2018 2020 2022 2024 2026

OEM market volume ($bn)

CAGR Aircraft

Segment*

Mid single digit Widebody (50-120 klb)

Mid single digit Narrowbody (20-50 klb)

High single digit Regional jet (13-24 klb)

High single digit Business jet (3-16 klb)

CAGR 2016-2026

Total market Mid to high single digit

MTU projects outperformance of market growth in 3 out of 4 segments.

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

• Installed base of more than 7,600 engines

• 10 business jet applications in operation

• Successful market introduction of Cessna Latitude

• Dassault Falcon 8X in development

• Program share of 15%

• Exclusive engine for future Gulfstreams and future

Dassault Business Jet

• MTU will be responsible for the LPT, the first four

stages of the HPC and will participate in the MRO

• EIS expected in 2018 (G500), 2019 (G600) and 2022

(Dassault)

10

PW300 / PW500 PW800

Business Jet Market

MTU’s turnover in the segment will triple within 10 years

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

• Program share of 15%

• Exclusive engine for MRJ with seats

up to 92 passengers

• First flight in Nov 2015

• EIS expected in 2021

• Program share of 17%

• Exclusive engine for the Bombardier

CSeries

• EIS in July 2016 with launch

customer Swiss International

Airlines

• Program share of 15-17%

• Exlusive engine for Embraer‘s 2nd

Gen E-jets

• Embraer is current market leader

with large customer base

• First flight of E190-E2 with

PW1900G in May 2016

• EIS in 2018-2020

11

PW1200G (MRJ) PW1500G (CSeries) PW1700G/1900G (E2-Jets)

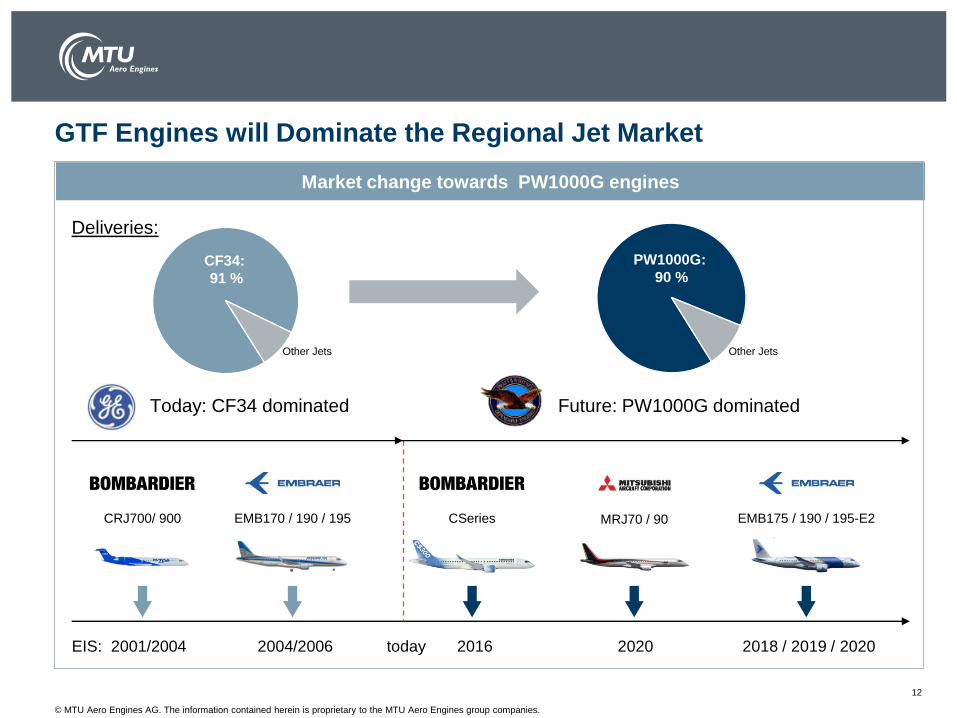

Regional Jet Market

MTU and its partners will dominate the future regional jet market with more than

3,000 engines already ordered or optioned

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

12

GTF Engines will Dominate the Regional Jet Market

Market change towards PW1000G engines

Other JetsOther Jets

EIS: 2001/2004 2004/2006 today 2016 2020 2018 / 2019 / 2020

EMB175 / 190 / 195-E2MRJ70 / 90CSeries

Today: CF34 dominated Future: PW1000G dominated

CF34:

91 %

PW1000G:

90 %

EMB170 / 190 / 195CRJ700/ 900

Deliveries:

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

• ~ 6,500 engines flying

• Most important program w.r.t. revenue contribution

• Strong growth of spare parts sales until mid of next

decade

• #1 MRO provider - capability in 3 locations

• Market share in NB segment ~24%

• Program share increase in 2012 from 11% to 16%

• Strong order book

• 16% improved fuel efficiency

• Designed for lower maintenance cost

• ~50% market share on A320neo family expected

• Increase in Market share in NB segment (~30%)

• Program share of 18%

• EIS 2016

13

V2500 PW1100G-JM

Narrowbody Market

Excellent narrowbody market position leads to continuous OEM & MRO growth

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

• Market share of ~ 50% on the A380

• In production since 2007

• ~ 500 engines in service

• Production peak in 2015

• Market share of 60% on 787,

exclusive on 747-8

• In production since 2011

• ~ 1000 engines in service

• Market expectation of 4,400 engines

• MTU is partner of the GE-MRO

network

• Exp. MRO revenue 3 bn€

• Revenue potential 4 bn€

• 950 orders and options

• Entry into service expected in 2020

• Exclusive engine for Boeing 777X

• MTU will be partner of GE-MRO

network

14

GP7000 GEnx GE9X

Widebody Market

Strong partnership with GE Aviation in the widebody market

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

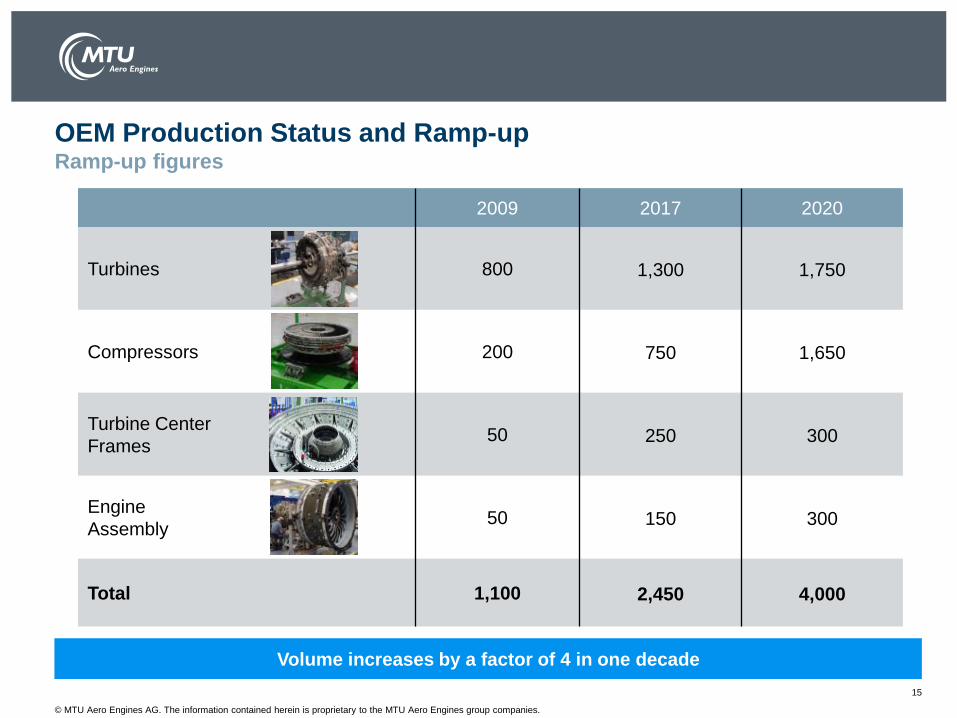

15

OEM Production Status and Ramp-upRamp-up figures

Volume increases by a factor of 4 in one decade

2009 2017 2020

Turbines 800 1,300 1,750

Compressors 200 750 1,650

Turbine Center

Frames50 250 300

Engine

Assembly50 150 300

Total 1,100 2,450 4,000

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

MTU AE Munich

• Sophisticated parts and production

processes

• Automation

• Development of new production

technologies

• Know How to support all MTU sites

and suppliers

MTU AE Polska

• Adopting established parts and

production lines from Munich

• Improvement of ‘mid tech’ parts and

production processes

• Module assembly improved with know

how transferred from automotive

industry

Supplier

• Raw parts

• Finished parts as second source

• ‘Low tech’ parts from low cost countries

16

High Tech Mid-Low Tech Raw Material, Mid-Low Tech

Strategic Setup Production and Supply Chain

• Keeping and improving MTU’s high tech knowledge in Munich

• MTU Polska as prime source for ‘mid tech’ parts – supplier as second source

• Dual Source

• Development of advanced manufacturing technology at MTU Munich

Risk Mitigation

The supply chain is based on 2 MTU manufacturing sites and a worldwide network of suppliers

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

17

MTU Commercial OE: Outlook 2017 to 2027 (in m€)Growth secured by strong order books and better diversification

Today (2017 E) Future (2027 E)

• ~ 3/4 of Com OE revenues is generated by

PW1100G, V2500 and GEnx

• Transition of V2500 to PW1100G in 2017-2018

• V2500 peak installed base in 2018

• GEnx stable production

Wide-

body

Narrow-

body

• PW1000G engine family key revenue driver in

future; GTF engine production >1000 by 2020

• EIS of next gen RJ starts from 2016 to 2020

• GEnx and GE9x main revenue driver of widebody

segment

• PW800 driver in business jet segment

CAGR

Wide-

body

Business Jets Others

Narrow-

body

Regional

Jet

Business JetsOthers

Regional Jets

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

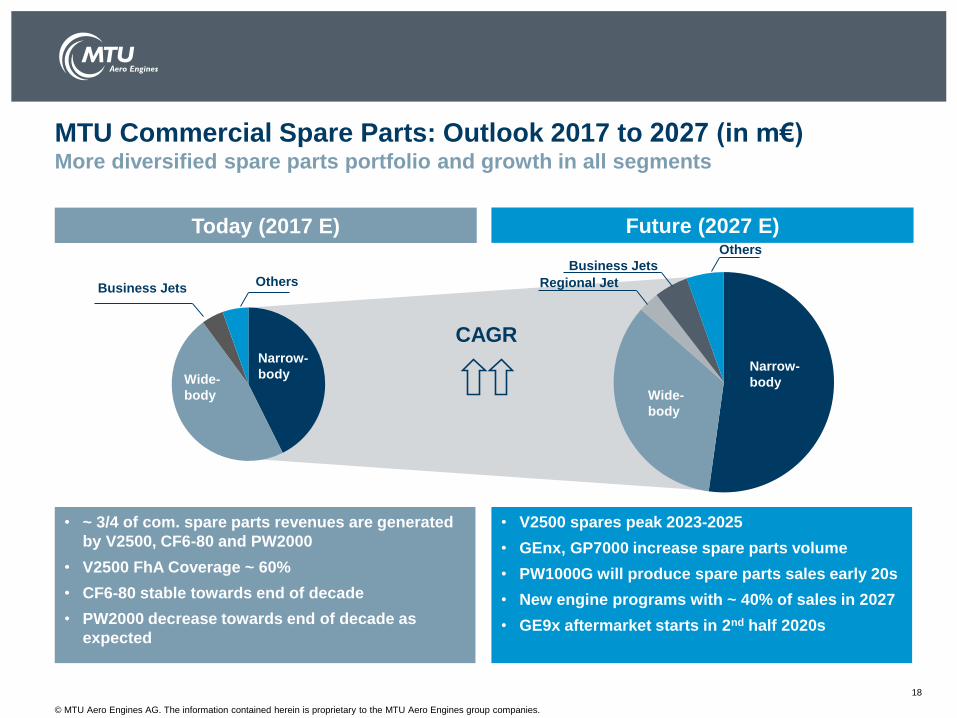

18

MTU Commercial Spare Parts: Outlook 2017 to 2027 (in m€)More diversified spare parts portfolio and growth in all segments

Today (2017 E) Future (2027 E)

• ~ 3/4 of com. spare parts revenues are generated

by V2500, CF6-80 and PW2000

• V2500 FhA Coverage ~ 60%

• CF6-80 stable towards end of decade

• PW2000 decrease towards end of decade as

expected

Wide-

body

Narrow-

body

• V2500 spares peak 2023-2025

• GEnx, GP7000 increase spare parts volume

• PW1000G will produce spare parts sales early 20s

• New engine programs with ~ 40% of sales in 2027

• GE9x aftermarket starts in 2nd half 2020s

CAGR

Wide-

body

Business JetsOthers

Narrow-

body

Regional Jet

Business Jets

Others

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

Contents

1. Company Overview

2. Commercial OEM Business

3. Military OEM Business

4. Commercial MRO Business

5. Financials & Outlook

6. Digitization @ MTU

7. Corporate Responsibility

8. Appendix

19

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

• Strong revenue contribution, both

OEM&MRO

• ~ 500 Eurofighter in service

• ~ 1,200 engines delivered

• Production of new engines until

2021

• Strong export potential

• Ramp up successfully achieved

• ~ 200 engines produced

• 174 A400M aircraft on order

• Aircraft well positioned for export

• Power for CH-53K for US marine

corps

• Latest Technology Turboshaft

engine

• First flight October 2015

• Engine could be used for additional

applications

• Strong transatlantic partnership

20

EJ200 TP400-D6 T408

Military Business

Successful new product introduction for the international military market

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

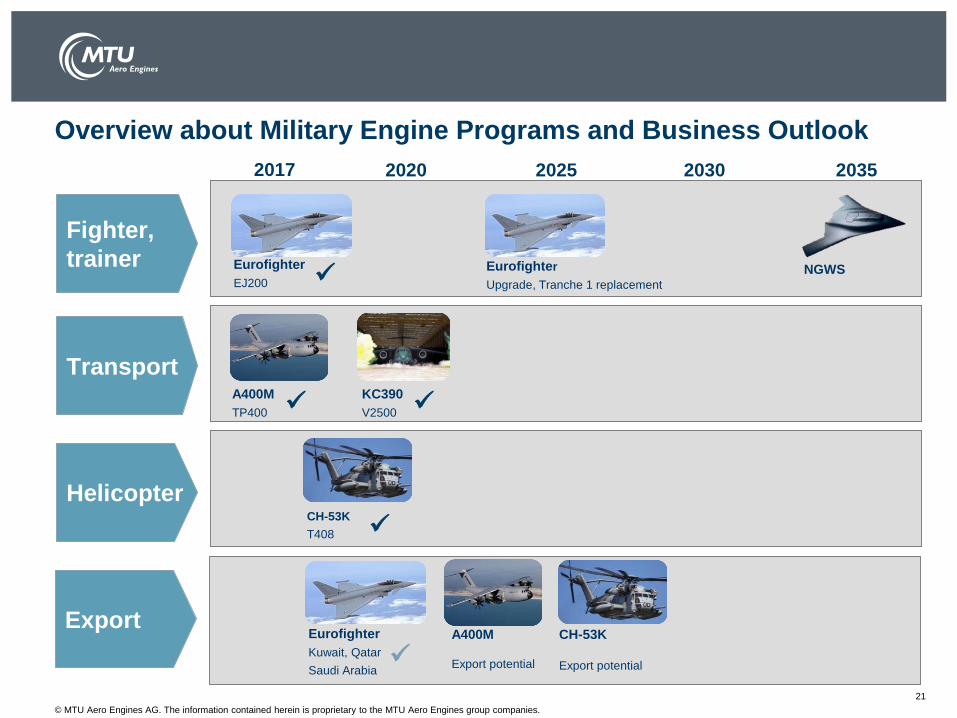

Overview about Military Engine Programs and Business Outlook

21

Fighter,

trainer Eurofighter

EJ200

TransportA400M

TP400

KC390

V2500

HelicopterCH-53K

T408

CH-53K

Export potential

203020252020 20352017

NGWSEurofighter

Upgrade, Tranche 1 replacement

ExportEurofighter

Kuwait, Qatar

Saudi Arabia

A400M

Export potential

12th December 2017 Investor & Analyst Day 2017 - Munich

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

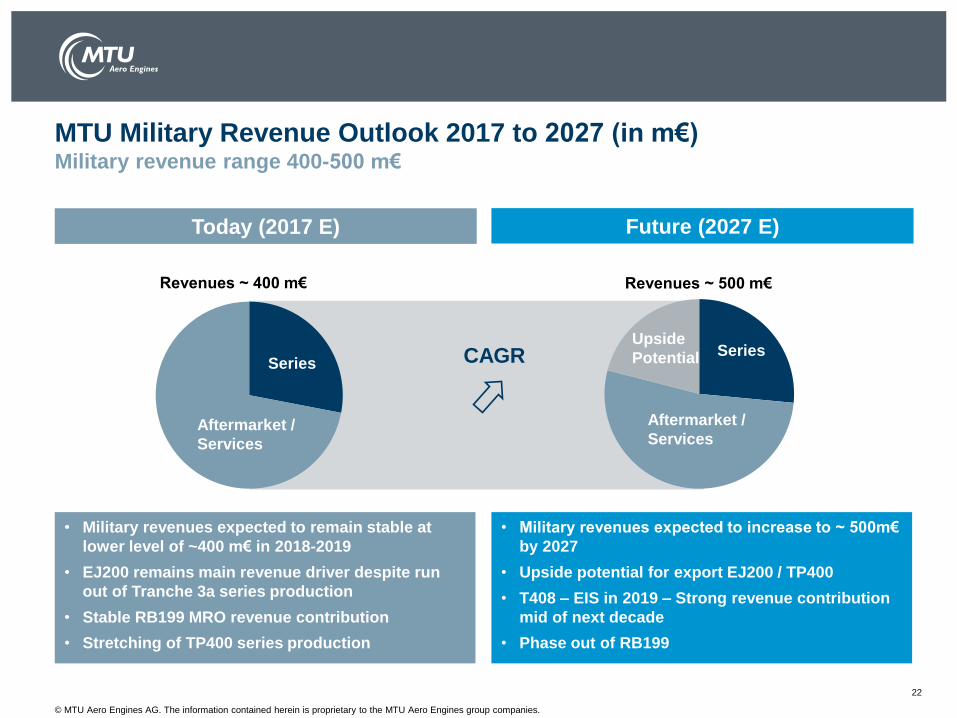

22

MTU Military Revenue Outlook 2017 to 2027 (in m€)Military revenue range 400-500 m€

Today (2017 E) Future (2027 E)

• Military revenues expected to remain stable at

lower level of ~400 m€ in 2018-2019

• EJ200 remains main revenue driver despite run

out of Tranche 3a series production

• Stable RB199 MRO revenue contribution

• Stretching of TP400 series production

Series

Aftermarket /

Services

Series

Aftermarket /

Services

Upside

Potential

• Military revenues expected to increase to ~ 500m€

by 2027

• Upside potential for export EJ200 / TP400

• T408 – EIS in 2019 – Strong revenue contribution

mid of next decade

• Phase out of RB199

CAGR

Revenues ~ 400 m€ Revenues ~ 500 m€

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

Contents

1. Company Overview

2. Commercial OEM Business

3. Military OEM Business

4. Commercial MRO Business

5. Financials & Outlook

6. Digitization@MTU

7. Corporate Responsibility

8. Appendix

23

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

Characteristics:

24

Independent MRO OEM cooperation

MTU’s Diversified Approach Ensures a Broad MRO Market Coverage

• Direct customer contact

• Over 900 customers

• Highly competitive market

• Customized services

• Highly competitive MRO shops due to low labor

cost environment

• OEM is contract holder

• Long term deals with focus on reducing life-cycle

cost

• MTU is OEM network partner

• MRO share is secured at program entry for entire

life

Targets: • Remain #1 provider with focus on customers

• Provide integrated life cycle services

• Develop current and investigate future airline

cooperations

• Provide cost-efficient, industrialized MRO

• Leverage OEM network

Partners: • JV with China Southern

• JV with LH Technik (ASSB)

• OEM

• JV with LH Technik (EME Aero)

• CF34, CF6, CFM56, GE90G, PW2000, V2500,

Parts repair, LM IGTs, Vericor

• GEnx, GP7000, PWC, V2500, PW1000G, GE9XPrograms:

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

25

MTU’s MRO Portfolio is the Basis for Future Growth

0

10

20

30

40

50

60

2015 2017 2019 2021 2023 2025

MRO Market Volume ($bn)

CAGR Market Approach Portfolio

Mid

single

digit

No access as

of today–

High

single

digit

Independent

or Airline

Cooperation

CF34, CFM56,

CF6, GE90G,

PW2000, V2500

High

teensOEM Cooperation

PW1000G, GEnx,

GP7000, V2500…

CAGR 2015-25

Total Market High single digit

MTU-served Low teens

Source: MTU, escalated

MTU has the largest engine MRO portfolio of all providers:

The market MTU serves will grow over-proportionally at low teens level p.a.

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

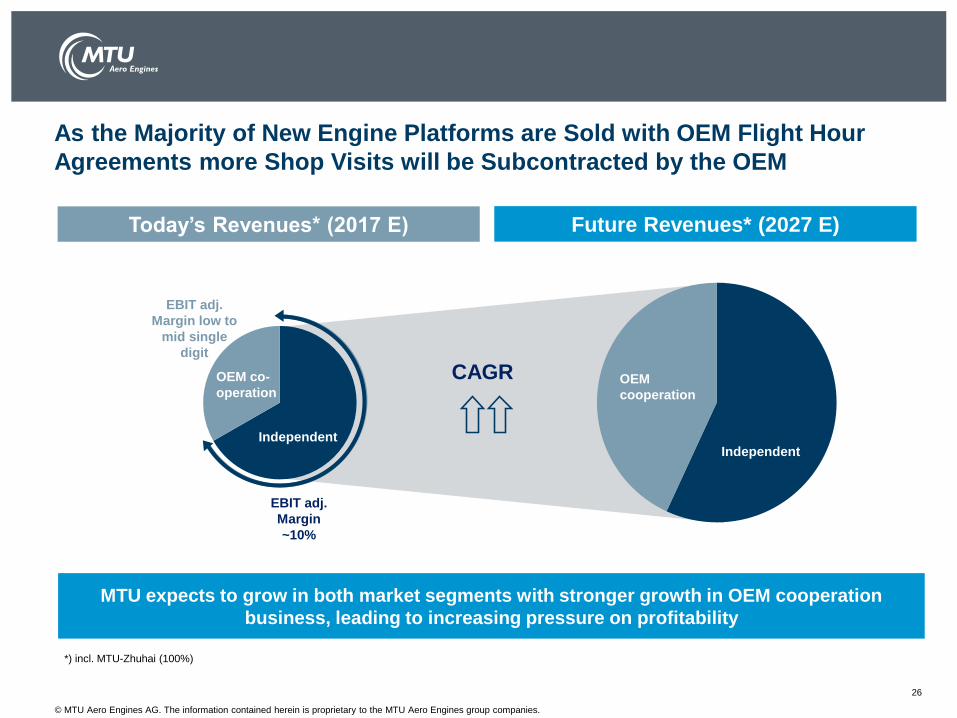

26

As the Majority of New Engine Platforms are Sold with OEM Flight Hour

Agreements more Shop Visits will be Subcontracted by the OEM

Today’s Revenues* (2017 E) Future Revenues* (2027 E)

OEM

cooperation

CAGR

IndependentIndependent

OEM co-

operation

EBIT adj.

Margin

~10%

EBIT adj.

Margin low to

mid single

digit

MTU expects to grow in both market segments with stronger growth in OEM cooperation

business, leading to increasing pressure on profitability

*) incl. MTU-Zhuhai (100%)

OEM co-

operation

Independent

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

27

Expansion of MRO Capacity with Clear Focus on Best Cost Initiated

Capacity needs vs. availability

Total capacity increase

~50%

High cost countries:

short-term increase of

workstaff

Low-cost countries:

doubling of capacity

Low-cost portion to total

capacity increases from

30% to 50%

Efficiency program started

to secure profitable growth

Capacity needs

High cost

locations

Best cost

locations

Long-term growth will be at best-cost sites within the MRO network

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

28

MRO Expansion StrategyMTU Zhuhai: Growing portfolio and customer base requires increase of capacity

Today: no.1 MRO Shop in China and most efficient NB MRO shop world-wide

2018 2020 2022 2024 2026

Max. capacity

Mature engine

platforms

New engine

platforms

MTU Maintenance Zhuhai Ltd.

• 50:50 JV with China Southern since 2001

• Current capacity ~300 shop visits after

extension in 2012 (+50%)

• Workforce ~800

• ~50% of visits are from 3rd party airlines

• Growing customer base

• Current portfolio: V2500 and CFM56

• Target to expand to new engine platforms

• Increase capacity by another 50%

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

29

MRO Expansion StrategyEME Aero: New GTF MRO facility

The new shop will have a key role in the GTF MRO network

• Company founded December 2017

• 50:50 joint venture with LHT

• Total investment of €150m

• One product shop: GTF only

• Start of operations in 2020

• Work force max. ~ 800 employees

• Full utilization of capacity in 2028

2018 2020 2022 2024 2026 2028

Max. capacity

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

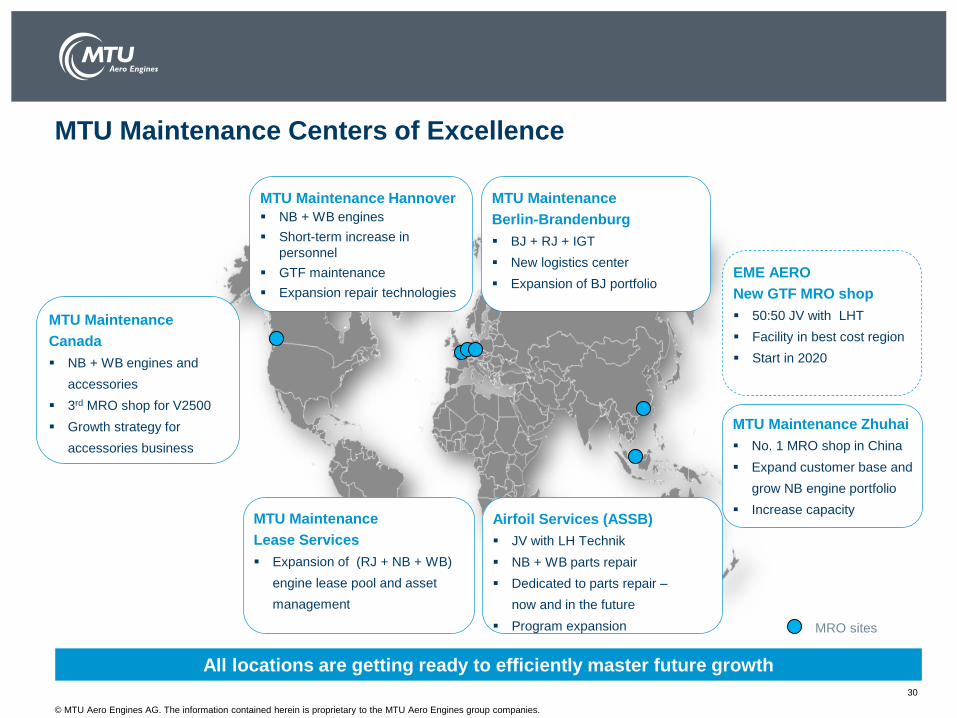

30

MRO sites

MTU Maintenance

Berlin-Brandenburg

BJ + RJ + IGT

New logistics center

Expansion of BJ portfolio

MTU Maintenance Hannover

NB + WB engines

Short-term increase in

personnel

GTF maintenance

Expansion repair technologies

Airfoil Services (ASSB)

JV with LH Technik

NB + WB parts repair

Dedicated to parts repair –

now and in the future

Program expansion

MTU Maintenance Zhuhai

No. 1 MRO shop in China

Expand customer base and

grow NB engine portfolio

Increase capacity

MTU Maintenance

Canada

NB + WB engines and

accessories

3rd MRO shop for V2500

Growth strategy for

accessories business

MTU Maintenance

Lease Services

Expansion of (RJ + NB + WB)

engine lease pool and asset

management

EME AERO

New GTF MRO shop

50:50 JV with LHT

Facility in best cost region

Start in 2020

MTU Maintenance Centers of Excellence

All locations are getting ready to efficiently master future growth

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

Contents

1. Company Overview

2. Commercial OEM Business

3. Military OEM Business

4. Commercial MRO Business

5. Financials & Outlook

6. Digitization @ MTU

7. Corporate Responsibility

8. Appendix

31

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

32

Guidance 2018: Upgrade due to stronger than expected aftermarket

Military: Stable

Commercial OE: Up ~30%

Commercial Spares: Up ~10%

Commercial MRO: Up ~20%

Total Group Sales: ~ 4.2 bn€

Organic Growth: NEW

EBIT adj. ~ 640 m€

* Cash Conversion Rate = Free Cash Flow/Net Income adj.

Net income adj. ~ 450 m€

CCR* ~ 40 - 50%

Stable

Up ~30%

Up mid single digit

Up in the high teens

Moderate progression

Growth in line with EBIT adj

Low to mid double digit

OLD

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

33

Long term outlook 2019-2025 update:

Improved Free Cashflow conversion reconfirmed

Consolidation phase 2019-2025

Net income adj. Steady growth

Working capital

Growing less than revenues+ No consumption of prepayments+ Inventory turns will improve+ More FHAs with preferential Cashflow profile

CF from investing

Will go into decline+ Less payments for intangibles+ Less spendings for capacity build-up (PPE)+ R&D capitalization declines as programs enter into

service

CCR* High double digit %

* Cash Conversion Rate = Free Cash Flow/Net Income adj.

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

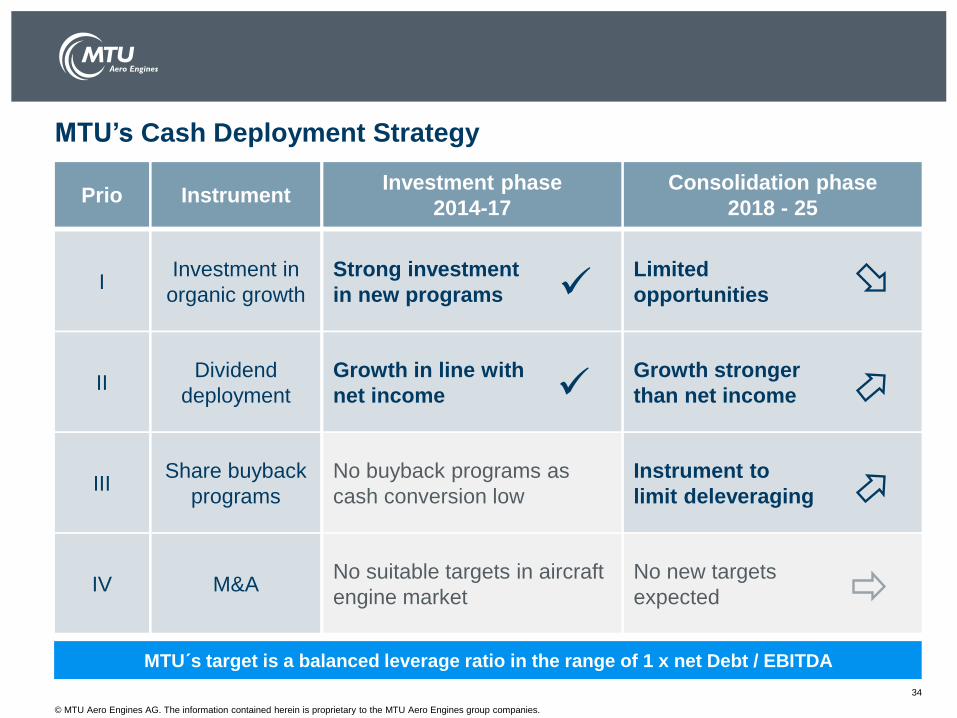

MTU’s Cash Deployment Strategy

34

Share buyback

programs

M&A

Dividend

deployment

Investment in

organic growth

Strong investment

in new programs

Limited

opportunities

Growth in line with

net income

Growth stronger

than net income

No buyback programs as

cash conversion low

Instrument to

limit deleveraging

No suitable targets in aircraft

engine market

I

II

III

IV

PrioInvestment phase

2014-17

Consolidation phase

2018 - 25

No new targets

expected

Instrument

MTU´s target is a balanced leverage ratio in the range of 1 x net Debt / EBITDA

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

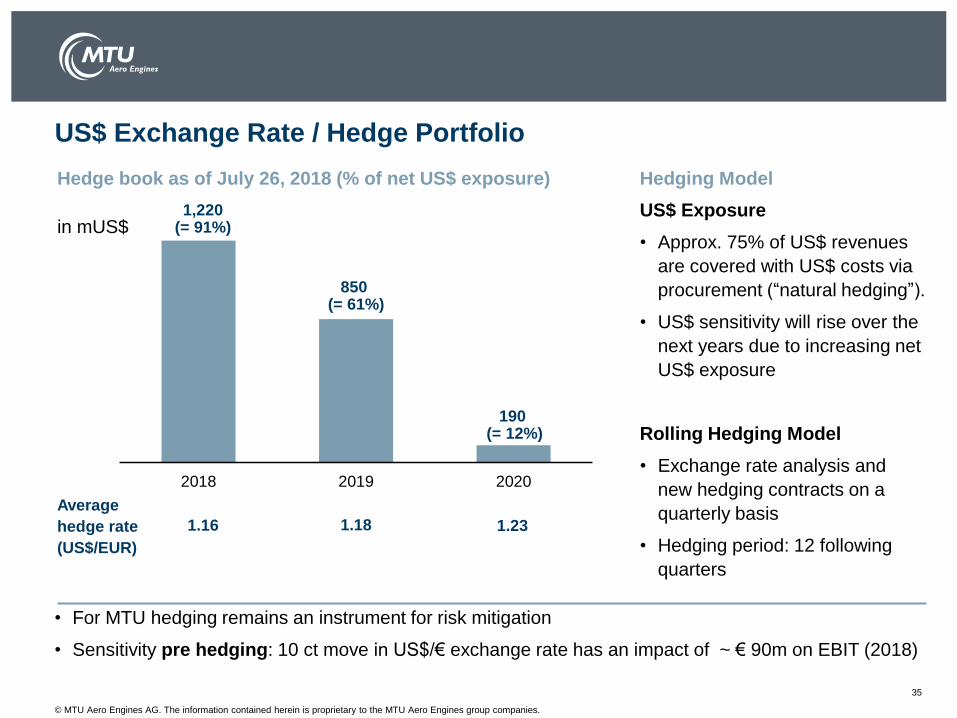

US$ Exchange Rate / Hedge Portfolio

35

Hedging ModelHedge book as of July 26, 2018 (% of net US$ exposure)

in mUS$US$ Exposure

• Approx. 75% of US$ revenues

are covered with US$ costs via

procurement (“natural hedging”).

• US$ sensitivity will rise over the

next years due to increasing net

US$ exposure

Rolling Hedging Model

• Exchange rate analysis and

new hedging contracts on a

quarterly basis

• Hedging period: 12 following

quarters

2018 2019 2020

1,220(= 91%)

850(= 61%)

1.16 1.18

Average

hedge rate

(US$/EUR)

• For MTU hedging remains an instrument for risk mitigation

• Sensitivity pre hedging: 10 ct move in US$/€ exchange rate has an impact of ~ € 90m on EBIT (2018)

190(= 12%)

1.23

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

Contents

1. Company Overview

2. Commercial OEM Business

3. Military OEM Business

4. Commercial MRO Business

5. Financials & Outlook

6. Digitization @ MTU

7. Corporate Responsibility

8. Appendix

36

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

37

Impact of Digitization on MTU‘s Business Model

Digitization will not fundamentally alter the business model of MTU in the medium term

but provides with opportunities to improve competitiveness further within the industry

Impacton p

roduct, b

usin

ess

model

(“D

isru

ptive

“)

Impact on cost structure, quality, etc.

(“Evolutionary“)

In B2C industries,

digitization partly leads

to a serious change in

the business model

For companies in B2B

industries, process

improvements are often

the focus of attention

B2C

B2B

ServicesTrade /

Commerce

LogisticsAuto-

mobile

Insurance

Finance/

Banking

Media

Engineering Chemistry

MTU

MRO

MTU

OEM

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

38

Digitization@ MTU Focus on 4 Areas of Activity

Work 4.0

MRO 4.0

Technology 4.0

Production 4.0

Robotic process

automationDigital twin

Unified collaboration

& communicationE-learning

IT security

Virtual engine

Additive

manufacturing

Material &

manufacturing simulation

Optimized material

flow/Logistics 4.0

Intelligent

machine

control

Predictive analyticsPredictive maintenance (ETM)

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

Contents

1. Company Overview

2. Commercial OEM Business

3. Military OEM Business

4. Commercial MRO Business

5. Financials & Outlook

6. Digitization @ MTU

7. Corporate Responsibility

8. Appendix

39

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

• Sustainable business practices

Compliance, corporate governance, risk

management, ratings & rankings

• Environmental protection

MTU climate strategy, environmental

management on the shop floor

• Product responsibility

Eco-efficient engines / Clean Air Engine,

sustainable production and maintenance

procedures, European SRIA standards*

• Responsibility toward employees

Occupational health & safety, work-life balance,

development of young talent

• Commitment to society

Economic cooperation / support of universities

and research institutes, local sponsoring

40

Corporate Responsibility

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

Contents

1. Company Overview

2. Commercial OEM Business

3. Military OEM Business

4. Commercial MRO Business

5. Financials & Outlook

6. Digitization @ MTU

7. Corporate Responsibility

8. Appendix

41

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

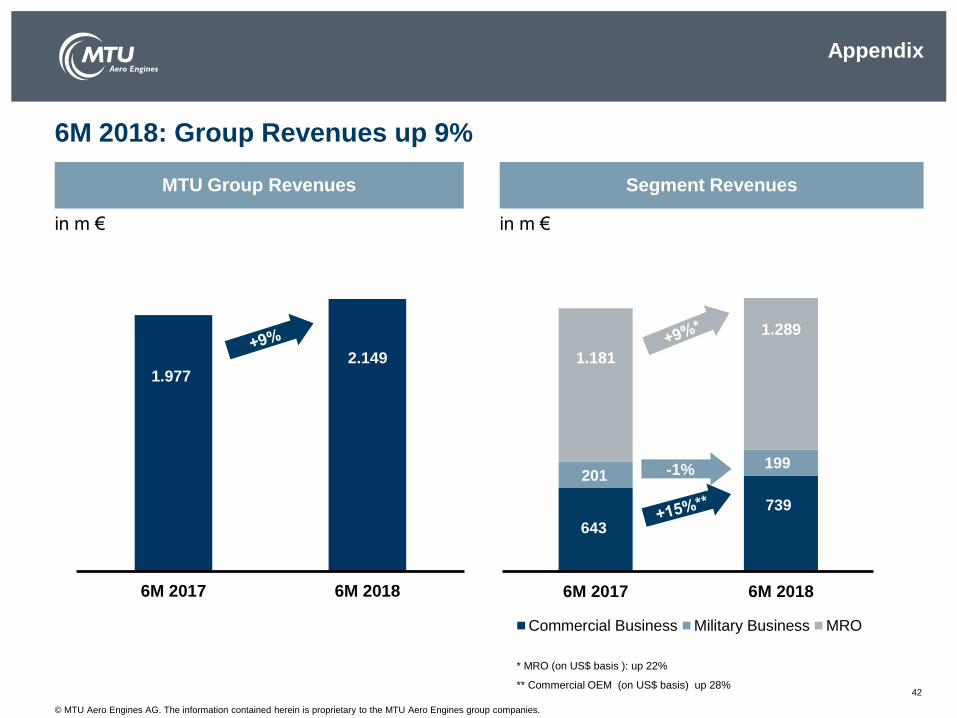

6M 2018: Group Revenues up 9%

42

MTU Group Revenues

in m € in m €

* MRO (on US$ basis ): up 22%

** Commercial OEM (on US$ basis) up 28%

Segment Revenues

1.9772.149

6M 2017 6M 2018

643

739

201199

1.181

1.289

6M 2017 6M 2018

Commercial Business Military Business MRO

-1%

Appendix

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

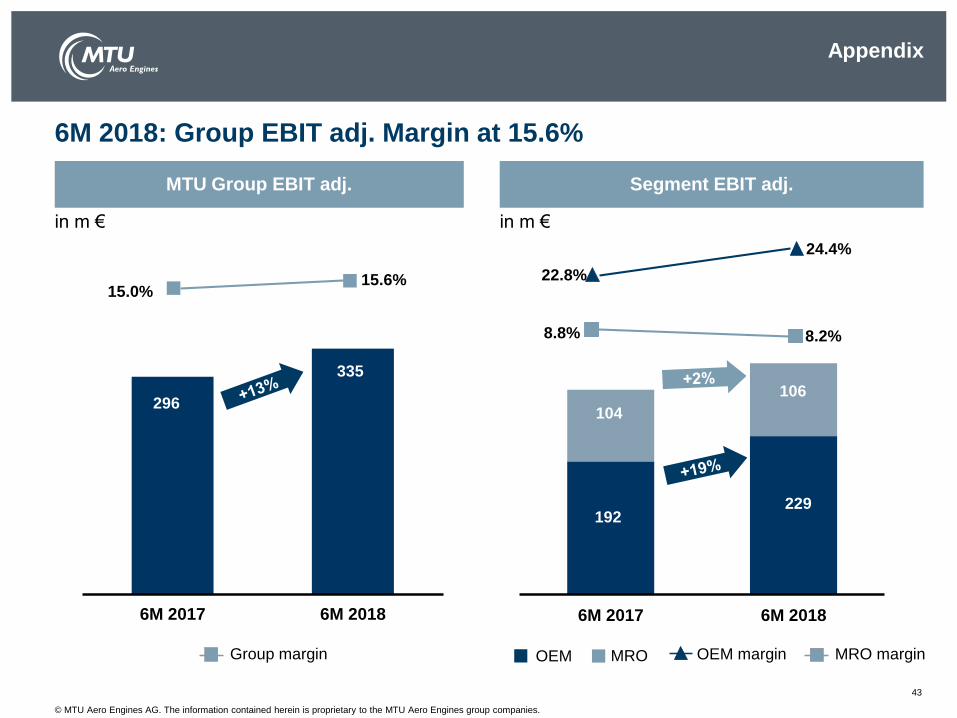

6M 2018: Group EBIT adj. Margin at 15.6%

43

MTU Group EBIT adj. Segment EBIT adj.

in m € in m €

296

335

6M 2017 6M 2018

192229

104

106

6M 2017 6M 2018

24.4%

22.8%

8.2%8.8%

15.0%15.6%

OEM MRO marginMRO OEM marginGroup margin

Appendix

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

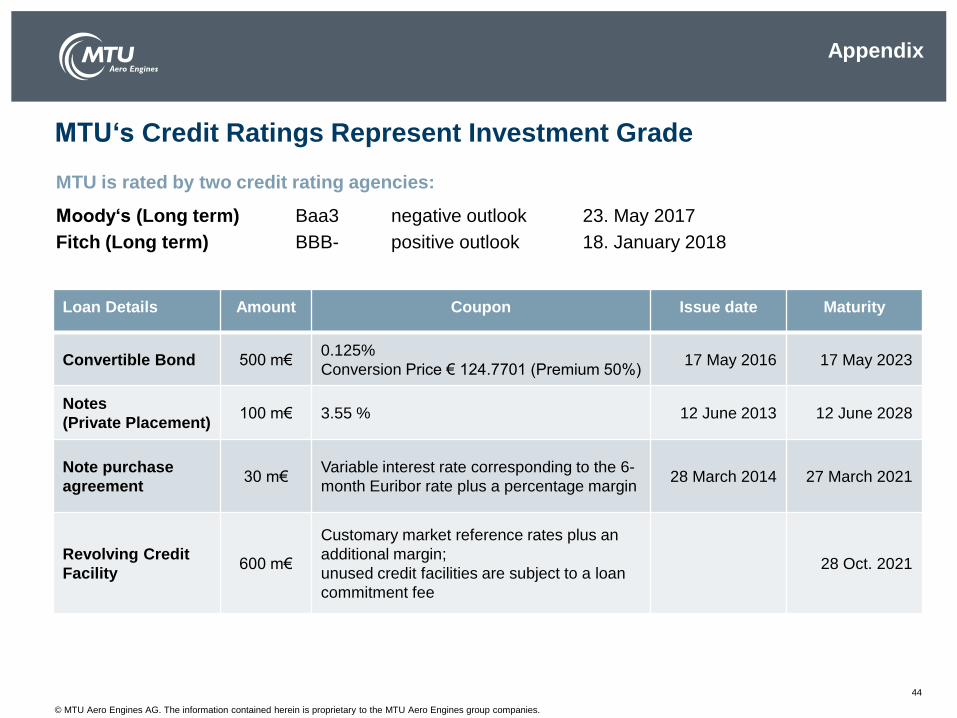

MTU‘s Credit Ratings Represent Investment Grade

44

Loan Details Amount Coupon Issue date Maturity

Convertible Bond 500 m€0.125%

Conversion Price € 124.7701 (Premium 50%)17 May 2016 17 May 2023

Notes

(Private Placement)100 m€ 3.55 % 12 June 2013 12 June 2028

Note purchase

agreement30 m€

Variable interest rate corresponding to the 6-

month Euribor rate plus a percentage margin28 March 2014 27 March 2021

Revolving Credit

Facility600 m€

Customary market reference rates plus an

additional margin;

unused credit facilities are subject to a loan

commitment fee

28 Oct. 2021

MTU is rated by two credit rating agencies:

Moody‘s (Long term) Baa3 negative outlook 23. May 2017

Fitch (Long term) BBB- positive outlook 18. January 2018

Appendix

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

45

Update: Development Milestones of new Engine Programs

With PW1200G and PW1900G two more Geared Turbofan engines were certified in 2017

PW1500G

C-Series

PW1100G

A320neo

PW1200G

MRJ

PW1400G

MS-21

PW1900G

E-Jets 2nd

Gen

PW800

G500 /

G600

GE9X

B 777X

T408

CH-53K

First

engine to

test

Tested in

flying

testbed N/A 2017 N/A

Engine

certifica-

tion 2019 2018*

First flight 2019

Entry into

service 2021 2019 2018 2018 2020 2019

* T408: Certification of whole aircraft system after flight testing

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

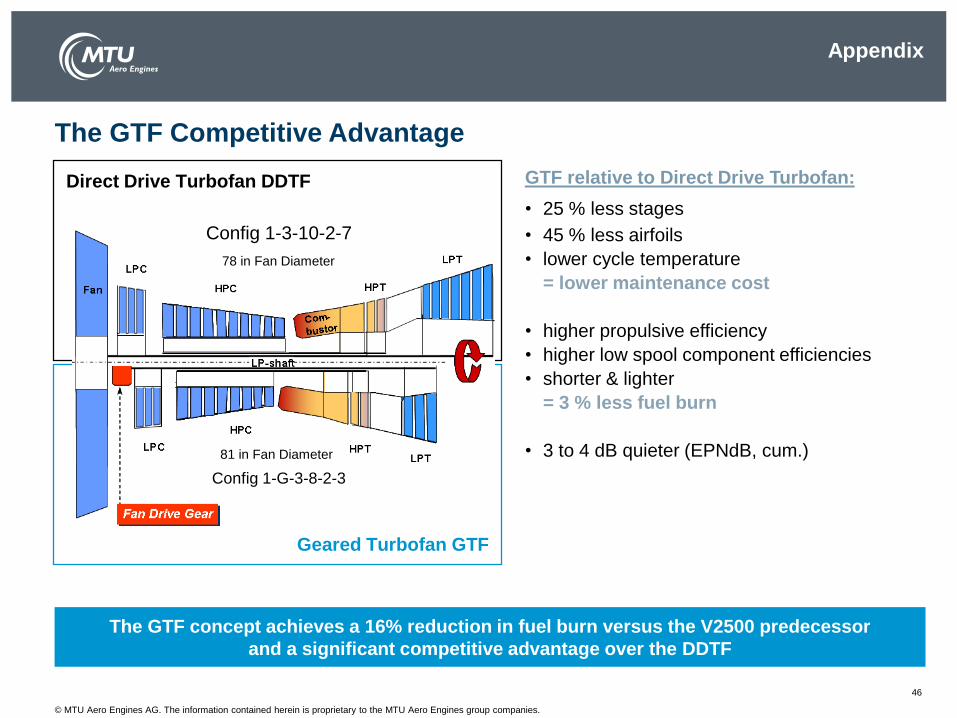

The GTF Competitive Advantage

46

Geared Turbofan GTF

Direct Drive Turbofan DDTF

Config 1-G-3-8-2-3

81 in Fan Diameter

Config 1-3-10-2-7

78 in Fan Diameter

GTF relative to Direct Drive Turbofan:

• 25 % less stages

• 45 % less airfoils

• lower cycle temperature

= lower maintenance cost

• higher propulsive efficiency

• higher low spool component efficiencies

• shorter & lighter

= 3 % less fuel burn

• 3 to 4 dB quieter (EPNdB, cum.)

The GTF concept achieves a 16% reduction in fuel burn versus the V2500 predecessor

and a significant competitive advantage over the DDTF

Appendix

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

Commercial Engine Fleet

47

Aircraft Segment Engine Program Share Aircraft Application

Widebody

(50 – 120 klb)*

GP7000

PW4000G

CF6-80C

Genx

CF6-80E

CF6-50/80A

GE9X

22.5%

12.5%

9.1%

6.6%

n.n.

n.n.

4%

A380

B777

B747-400, B767, Boeing MD-11, A310

B787 Dreamliner, B747-8

A330

DC 10-30, B767, A310

B777X

Narrowbody

(20 – 50 klb)*

PW2000

PW1100G-JM

PW6000

V2500

JT8D-200

21.2%

18%

18%

16%

12.5%

B757, C-17

A320neo

A318

A320 family, Boeing MD-90

Boeing MD-80 range

Regional Jets

(13 – 24 klb)*

PW1500G

PW1700G/1900G

PW1200G

17%

15-17%

15%

Bombardier CSeries

Embraer E-Jet Gen 2

MRJ

Business Jets

(3 – 16 klb)*

PW300

PW500

PW800

25% (PW305/306)

15% (PW307)

25%

15%

Learjet 60, Do328 JET, Gulfstream G200, Hawker

1000, Dessault Falcon 7X, Cessna Sovereign

Cessna Bravo, Cessna Excel

Gulfstream G500, G600

Appendix

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

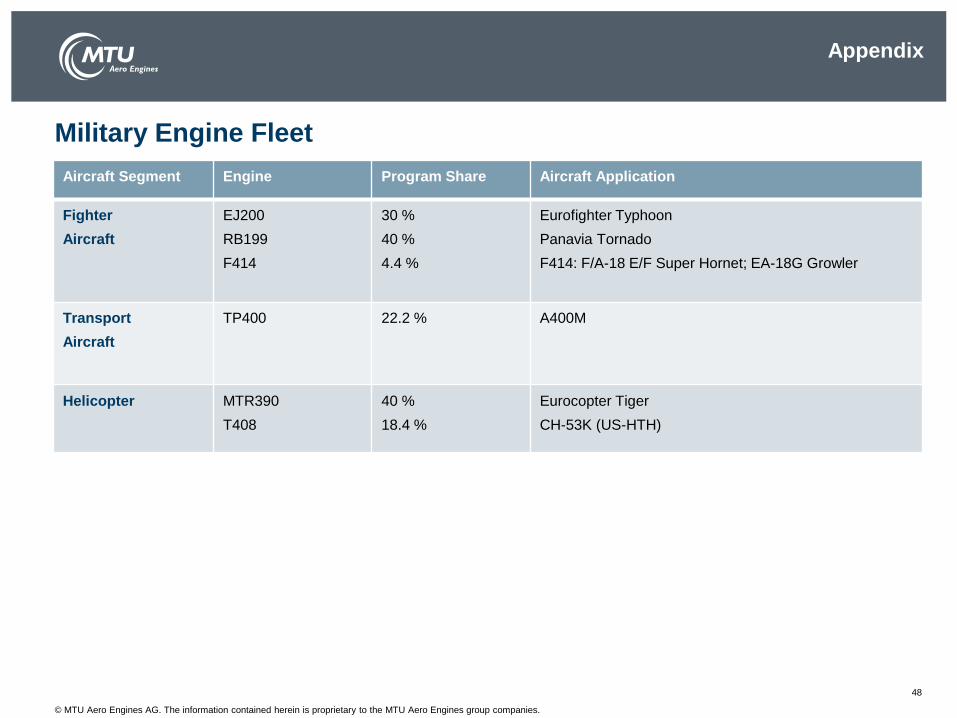

Military Engine Fleet

48

Aircraft Segment Engine Program Share Aircraft Application

Fighter

Aircraft

EJ200

RB199

F414

30 %

40 %

4.4 %

Eurofighter Typhoon

Panavia Tornado

F414: F/A-18 E/F Super Hornet; EA-18G Growler

Transport

Aircraft

TP400 22.2 % A400M

Helicopter MTR390

T408

40 %

18.4 %

Eurocopter Tiger

CH-53K (US-HTH)

Appendix

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

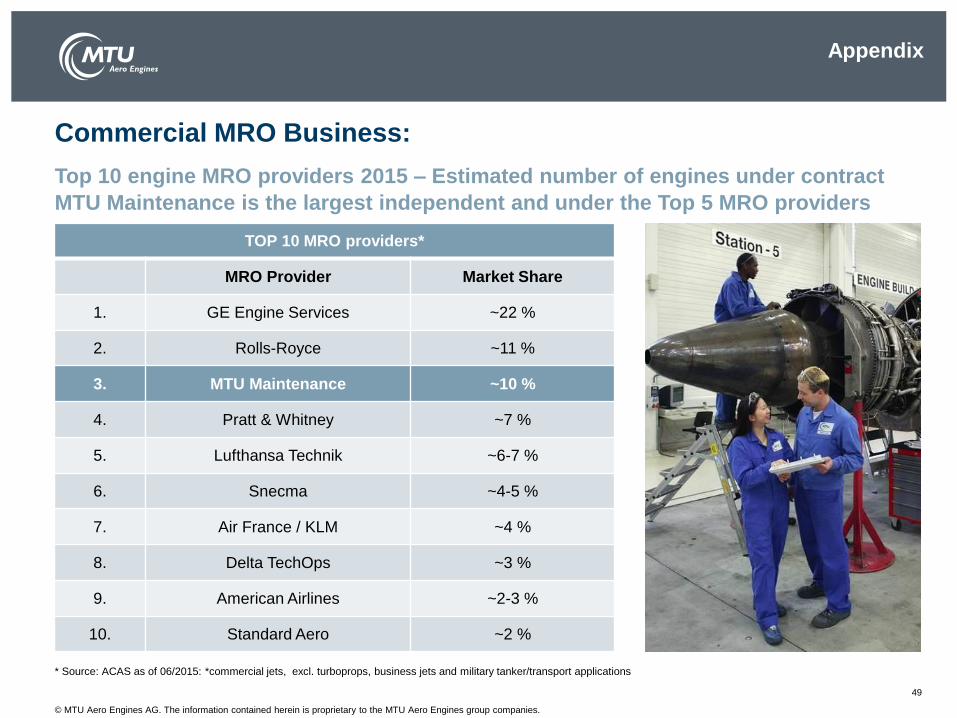

Commercial MRO Business:

49

Top 10 engine MRO providers 2015 – Estimated number of engines under contract

MTU Maintenance is the largest independent and under the Top 5 MRO providers

TOP 10 MRO providers*

MRO Provider Market Share

1. GE Engine Services ~22 %

2. Rolls-Royce ~11 %

3. MTU Maintenance ~10 %

4. Pratt & Whitney ~7 %

5. Lufthansa Technik ~6-7 %

6. Snecma ~4-5 %

7. Air France / KLM ~4 %

8. Delta TechOps ~3 %

9. American Airlines ~2-3 %

10. Standard Aero ~2 %

* Source: ACAS as of 06/2015: *commercial jets, excl. turboprops, business jets and military tanker/transport applications

Appendix

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

Financial Calendar 2018 & IR Contact

50

Michael Röger

Vice President Investor Relations

phone: +49 89 14 89-8473

E-Mail: [email protected]

Claudia Heinle

Senior Manager Investor Relations

phone: +49 89 14 89-3911

E-Mail: [email protected]

2018

February 21, 2018

Conference Call

Full year results 2017

April 11, 2018

Annual General Meeting

for the fiscal year 2017

May 3, 2018

Conference Call

Q1 2018 results

July 26, 2018

Conference Call

Q2 2018 results

October 25, 2018

Conference Call

Q3 2018 results

November 30, 2018

Investor & Analyst Day

Matthias Spies

Senior Manager Investor Relations

phone: +49 89 14 89-4108

E-Mail: [email protected]

Appendix

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

Cautionary Note Regarding Forward-Looking Statements

51

Certain of the statements contained herein may be statements of future expectations and other forward-looking statements that are based on

management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance

or events to differ materially from those expressed or implied in such statements. In addition to statements that are forward-looking by reason of

context, the words “may,” “will,” “should,” “expect,” “plan,” “intend,” “anticipate,” “forecast,” “believe,” “estimate,” “predict,” “potential,” or “continue”

and similar expressions identify forward-looking statements.

Actual results, performance or events may differ materially from those in such statements due to, without limitation, (i) competition from other

companies in MTU’s industry and MTU’s ability to retain or increase its market share, (ii) MTU’s reliance on certain customers for its sales, (iii) risks

related to MTU’s participation in consortia and risk and revenue sharing agreements for new aero engine programs, (iv) the impact of non-compete

provisions included in certain of MTU’s contracts, (v) the impact of a decline in German or other European defense budgets or changes in funding

priorities for military aircraft, (vi) risks associated with government funding, (vii) the impact of significant disruptions in MTU’s supply from key

vendors, (viii) the continued success of MTU’s research and development initiatives, (ix) currency exchange rate fluctuations, (x) changes in tax

legislation, (xi) the impact of any product liability claims, (xii) MTU’s ability to comply with regulations affecting its business and its ability to respond

to changes in the regulatory environment, (xiii) the cyclicality of the airline industry and the current financial difficulties of commercial airlines, (xiv)

our substantial leverage and (xv) general local and global economic conditions. Many of these factors may be more likely to occur, or more

pronounced, as a result of terrorist activities and their consequences.

The company assumes no obligation to update any forward-looking statement.

Any securities referred to herein have not been and will not be registered under the U.S. Securities Act of 1933, as amended (the “Securities Act”),

and may not be offered or sold without registration thereunder or pursuant to an available exemption therefrom. Any public offering of securities of

MTU Aero Engines to be made in the United States would have to be made by means of a prospectus that would be obtainable from MTU Aero

Engines and would contain detailed information about the issuer of the securities and its management, as well as financial statements.

Neither this document nor the information contained herein constitutes an offer to sell or the solicitation of an offer to buy any securities.

These materials do not constitute an offer of securities for sale in the United States; the securities may not be offered or sold in the United States

absent registration or an exemption from registration.

No money, securities or other consideration is being solicited, and, if sent in response to the information contained herein, will not be accepted.

© MTU Aero Engines AG. The information contained herein is proprietary to the MTU Aero Engines group companies.

This document contains proprietary information of the MTU Aero Engines AG group

companies. The document and its contents shall not be copied or disclosed to any third

party or used for any purpose other than that for which it is provided, without the prior

written agreement of MTU Aero Engines AG.

52

Proprietary Notice