augusto iglesias p. primamérica consultores november, 2003 the impact of mandatory pension funds...

Post on 20-Dec-2015

213 views

TRANSCRIPT

Augusto Iglesias P.Augusto Iglesias P.PrimAmérica ConsultoresPrimAmérica Consultores

November, 2003November, 2003www.primamerica.clwww.primamerica.cl

The impact of mandatory pension funds on The impact of mandatory pension funds on corporate governance: the L.A. experiencecorporate governance: the L.A. experience

* Presented at the World Bank Conference on “Contractual Savings: Supervisory and Regulatory Issues in * Presented at the World Bank Conference on “Contractual Savings: Supervisory and Regulatory Issues in Private Pensions and Life Insurance” (Washington D.C., November 3 –7, 2003).Private Pensions and Life Insurance” (Washington D.C., November 3 –7, 2003).

PrimAméricaConsultores

I. Preliminary remarksI. Preliminary remarks

Since the early eighties, as a consequence of radical Since the early eighties, as a consequence of radical reforms to the social security system, mandatory pension reforms to the social security system, mandatory pension funds have become important players in the capital funds have become important players in the capital markets of many L.A. countries.markets of many L.A. countries.

What has been the impact of mandatory pension funds What has been the impact of mandatory pension funds on corporate governance in these countries?on corporate governance in these countries?

Pension Reform in Latin AmericaPension Reform in Latin America

CountryCountry Year of Year of ReformReform

Pension Fund Pension Fund (MMUS$)(MMUS$)

Dec 2002Dec 2002

ArgentinaArgentina 19941994 11.40911.409

BoliviaBolivia 19971997 1.1441.144

ColombiaColombia 19951995 5.4825.482

ChileChile 19811981 35.41235.412

Costa RicaCosta Rica 20002000 136136

El Salvador (1)El Salvador (1) 19981998 1.0181.018

MexicoMexico 19971997 31.74831.748

PeruPeru 19931993 4.5274.527

UruguayUruguay 19951995 893893

TotalTotal 91.76991.769

(1) Pension Fund 31.09.2002(1) Pension Fund 31.09.2002

Source: FIAP.Source: FIAP.

PrimAméricaConsultores

PrimAméricaConsultores II. The impact of pension funds on II. The impact of pension funds on

corporate governance: the theorycorporate governance: the theory

Pension funds can have a positive influence on Pension funds can have a positive influence on corporate governance through many different corporate governance through many different channels. Among these the most important are:channels. Among these the most important are: Monitoring:Monitoring: Pension funds hold both equity and debt issued Pension funds hold both equity and debt issued

by corporations. They should monitor these firms activities to by corporations. They should monitor these firms activities to minimize the risk of actions by the management (or minimize the risk of actions by the management (or controlling shareholder) against the interest of bondholders controlling shareholder) against the interest of bondholders and shareholders (or minority shareholders). Monitoring can and shareholders (or minority shareholders). Monitoring can be done trough “internal” and “external” channels:be done trough “internal” and “external” channels:

Internal: Appointment of board members; participation in Internal: Appointment of board members; participation in shareholders meetings and bondholders meetings.shareholders meetings and bondholders meetings.

External: Greater scrutiny of corporations and higher standards External: Greater scrutiny of corporations and higher standards of information for firms where pension funds invest.of information for firms where pension funds invest.

Continue

PrimAméricaConsultores II. The impact of pension funds on II. The impact of pension funds on

corporate governance: the theorycorporate governance: the theory

Better regulationsBetter regulations: The development of pension funds can have : The development of pension funds can have an effect on the design of capital market regulations. In turn, an effect on the design of capital market regulations. In turn, better regulations should have a positive impact on corporate better regulations should have a positive impact on corporate governance:governance:

Mandatory pension funds are created by law and they are Mandatory pension funds are created by law and they are part of the social security system. Therefore, there are some part of the social security system. Therefore, there are some implicit – and explicit – state guarantees over the results of implicit – and explicit – state guarantees over the results of the system. Eventually, capital market regulations will need the system. Eventually, capital market regulations will need to be reformed with the purpose of reducing the cost of these to be reformed with the purpose of reducing the cost of these guarantees. These changes in regulations will benefit not guarantees. These changes in regulations will benefit not only pension funds, but also small investors and minority only pension funds, but also small investors and minority shareholders.shareholders.

PrimAméricaConsultores II. The impact of pension funds on II. The impact of pension funds on

corporate governance: the theorycorporate governance: the theory

Capital market development:Capital market development: The accumulation of pension The accumulation of pension funds should have a positive impact on the size of capital funds should have a positive impact on the size of capital markets (total market intermediation). In turn, the increase markets (total market intermediation). In turn, the increase in trading volumes can have positive indirect effects on in trading volumes can have positive indirect effects on corporate governance since:corporate governance since:

There are economies of scale in the process of placing debt There are economies of scale in the process of placing debt and equity. So, as the volume of trading increases, the cost of and equity. So, as the volume of trading increases, the cost of market financing for companies decrease.market financing for companies decrease.

Increased liquidity allows investors to use the “exit” mechanism Increased liquidity allows investors to use the “exit” mechanism (or “voting with their feet”) as a way to protect themselves in (or “voting with their feet”) as a way to protect themselves in case of firms performing below expectations.case of firms performing below expectations.

There are economies of scale in the process of collecting and There are economies of scale in the process of collecting and processing information about companies.processing information about companies.

PrimAméricaConsultores

III. Evidence from L.A.III. Evidence from L.A.

The economic significance of pension funds The economic significance of pension funds (measured as PF/GDP) has been growing but, with (measured as PF/GDP) has been growing but, with the single exception of Chile, is still low compared the single exception of Chile, is still low compared with most OECD countries (simple average: 31,7%)with most OECD countries (simple average: 31,7%)

Pension funds investment in shares and private debt Pension funds investment in shares and private debt (excluded debt issued by financial intermediaries) are (excluded debt issued by financial intermediaries) are very low in many L.A. countries, both as a very low in many L.A. countries, both as a percentage of their total investments and as a percentage of their total investments and as a percentage of total market capitalizationpercentage of total market capitalization

Continue

Pension funds as a share of GDPPension funds as a share of GDP

PrimAméricaConsultores

19971997 19981998 19991999 20002000 20012001 20022002

ArgentinaArgentina 2.9%2.9% 3.4%3.4% 5.4%5.4% 7.0%7.0% 7.9%7.9%

BoliviaBolivia 2,1%2,1% 4.1%4.1% 7.4%7.4% 10.0%10.0% 12.4%12.4% 15.5%15.5%

ColombiaColombia 1.3%1.3% 1.9%1.9% 3.0%3.0% 4.2%4.2% 5.3%5.3% 7.3%7.3%

ChileChile 46.0%46.0% 39.6%39.6% 51.2%51.2% 53.9%53.9% 52.7%52.7% 51.9%51.9%

Costa RicaCosta Rica 2.2%2.2% 3.3%3.3% 4.2%4.2%

El SalvadorEl Salvador 0.5%0.5% 2.2%2.2% 4.3%4.3% 5.6%5.6% 7.4%7.4%

MexicoMexico 3.6%3.6% 4.6%4.6% 6.3%6.3% 7.8%7.8%

PeruPeru 2.6%2.6% 3.3%3.3% 4.9%4.9% 5.2%5.2% 6.6%6.6% 7.1%7.1%

UruguayUruguay 0.8%0.8% 1.5%1.5% 2.6%2.6% 3.9%3.9% 6.0%6.0%

Source: Palacios (2003) Source: Palacios (2003)

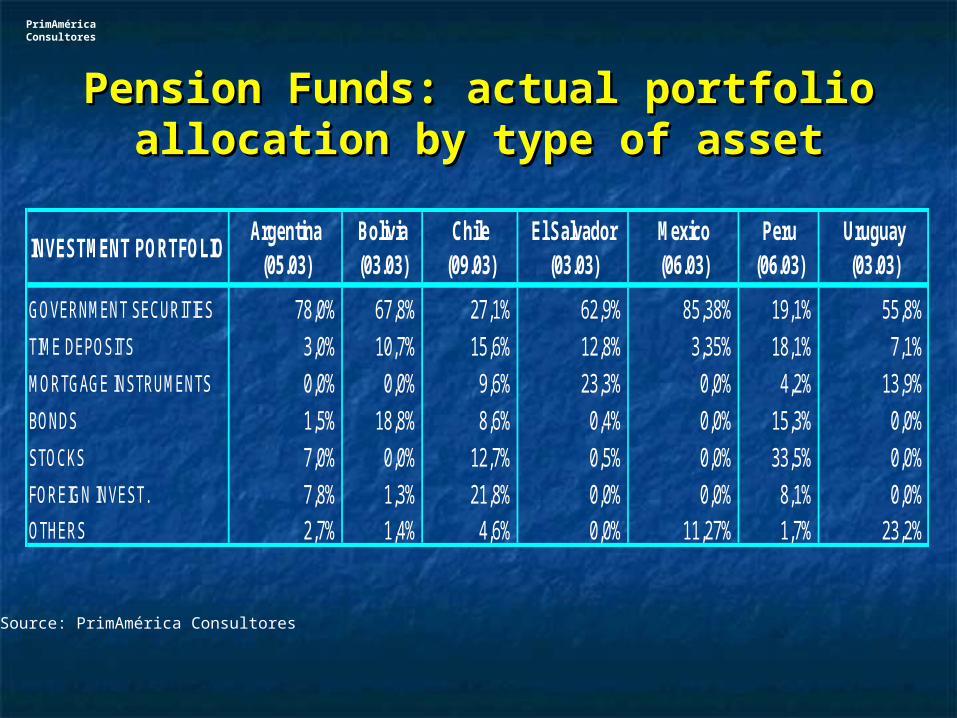

Pension Funds: actual portfolio Pension Funds: actual portfolio allocation by type of assetallocation by type of asset

PrimAméricaConsultores

GOVERNMENT SECURITIES 78,0% 67,8% 27,1% 62,9% 85,38% 19,1% 55,8%

TIME DEPOSITS 3,0% 10,7% 15,6% 12,8% 3,35% 18,1% 7,1%

MORTGAGE INSTRUMENTS 0,0% 0,0% 9,6% 23,3% 0,0% 4,2% 13,9%

BONDS 1,5% 18,8% 8,6% 0,4% 0,0% 15,3% 0,0%

STOCKS 7,0% 0,0% 12,7% 0,5% 0,0% 33,5% 0,0%

FOREIGN INVEST. 7,8% 1,3% 21,8% 0,0% 0,0% 8,1% 0,0%OTHERS 2,7% 1,4% 4,6% 0,0% 11,27% 1,7% 23,2%

INVESTMENT PORTFOLIOEl Salvador

(03.03)Mexico (06.03)

Peru (06.03)

Uruguay (03.03)

Argentina (05.03)

Bolivia (03.03)

Chile (09.03)

Source: PrimAmérica Consultores

Pension Funds in Capital MarketsPension Funds in Capital Markets(December 2002)(December 2002)

PrimAméricaConsultores

(3)=(1)/(2) MMUS$ (6)=(4)/(5)(1) (2) (4) (5)

Argentina 940 126.949 0,7% 198 n/a n/aChile (*) 5.781 47.430 12,2% 3.239 7.459 43,42%Mexico - n/a 0,0% 2,0 12.997,1 0,02%Peru 1.561 12.593 12,4% 645 14.747 4,37%

Source: PrimAmérica Consultores

(*) Pension Funds investment as of sep.2003

Total marketCountry

Pension Funds investment in shares

MMUS$

Total market MMUS$

Pension Funds investment in corporate bonds MMUS$

PrimAméricaConsultores

III. Evidence from L.A.III. Evidence from L.A.

So, at least from this perspective, it seems that in the LA So, at least from this perspective, it seems that in the LA region the impact of pension reform on corporate region the impact of pension reform on corporate governance could not have been substantial.governance could not have been substantial.

However, in most of these countries pension fund However, in most of these countries pension fund accumulation is a rather new phenomena. What has accumulation is a rather new phenomena. What has happened in the country -Chile- where pension funds do happened in the country -Chile- where pension funds do have a larger economic significance?have a larger economic significance?

Continue

PrimAméricaConsultores

III. Evidence from L.A.III. Evidence from L.A.

Circumstantial evidence from Chile shows that:Circumstantial evidence from Chile shows that: Pension funds participation in capital markets is significative.Pension funds participation in capital markets is significative.

At least some changes in capital market laws and regulations At least some changes in capital market laws and regulations which improve corporate governance standards are the result of which improve corporate governance standards are the result of pension reform (new rules to control for conflicts of interest; pension reform (new rules to control for conflicts of interest; higher information standards for firms which issue stocks and higher information standards for firms which issue stocks and debt; Audit Committees as part of the Board structure; etc.).debt; Audit Committees as part of the Board structure; etc.).

Pension funds managers do monitor the activities of the firms Pension funds managers do monitor the activities of the firms where they invest (they have been active in shareholders and where they invest (they have been active in shareholders and bondholders meetings; have elected independent board bondholders meetings; have elected independent board members; have initiated legal actions against the management of members; have initiated legal actions against the management of some firms when decisions have been taken that could hurt some firms when decisions have been taken that could hurt minority shareholder interests; etc.).minority shareholder interests; etc.).

Chile: Pension fund (*)Chile: Pension fund (*)significance in capital marketssignificance in capital markets

(MM US$ 2002)(MM US$ 2002)

PrimAméricaConsultores

(*) Include LICO’s Investments(*) Include LICO’s Investments

AssetsAssets 19811981 20022002 GrowthGrowth Pension fundsPension funds(times)(times) in the marketin the market

Public and Central Bank DebtPublic and Central Bank Debt 797797 17.46417.464 21,921,9 75,00%75,00%Mortgage backed securitiesMortgage backed securities 513513 8.4318.431 16,616,6 97,50%97,50%BondsBonds 7171 7.4597.459 104,5104,5 75,00%75,00%SharesShares 5.2355.235 47.43047.430 9,19,1 8,20%8,20%Time depositsTime deposits 4.2084.208 22.16722.167 5,35,3 35,40%35,40%Investment fundsInvestment funds 00 1.1171.117 n/an/a 89,50%89,50%OtherOther 2.7032.703 7.1967.196 2,72,7 37,20%37,20%TotalTotal 13.52713.527 111.264111.264 8,28,2 37,80%37,80%Total intermediation (Debt)Total intermediation (Debt) 4747 66.23866.238 1.424,51.424,5Total intermediation (Shares)Total intermediation (Shares) 7575 3.4393.439 45,945,9

Source: Palma (2003)Source: Palma (2003)

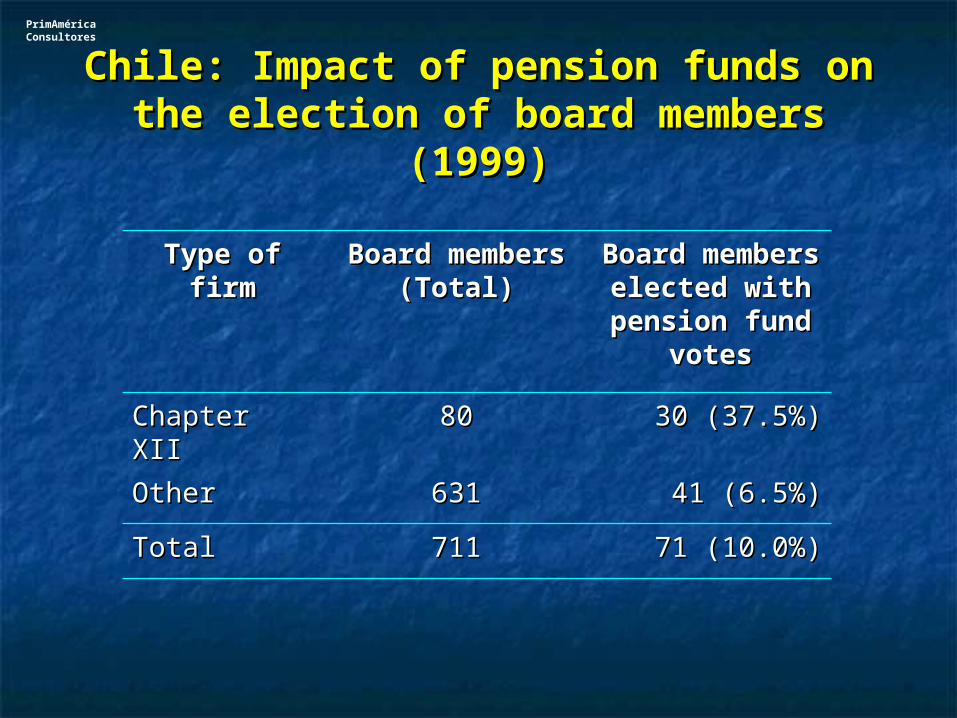

Chile: Impact of pension funds on the Chile: Impact of pension funds on the election of board members (1999)election of board members (1999)

PrimAméricaConsultores

Type of firmType of firm Board members Board members (Total)(Total)

Board members Board members elected with elected with

pension fund pension fund votesvotes

Chapter XIIChapter XII 8080 30 (37.5%)30 (37.5%)

OtherOther 631631 41 (6.5%)41 (6.5%)

TotalTotal 711711 71 (10.0%)71 (10.0%)

PrimAméricaConsultores IV. Determinants of pension funds impact IV. Determinants of pension funds impact

on corporate governanceon corporate governance

L.A. experience shows that the impact of introducing L.A. experience shows that the impact of introducing mandatory pension funds on corporate governance mandatory pension funds on corporate governance should not be taken for granted. Besides the maturity should not be taken for granted. Besides the maturity of the new funded systems, this impact will depend of the new funded systems, this impact will depend on:on:

Capital market conditions prior to pension reform.Capital market conditions prior to pension reform.

Characteristics of pension funds investment Characteristics of pension funds investment regulations.regulations.

Capacity to control for potential conflicts of interest Capacity to control for potential conflicts of interest between pension fund managers and pension fund between pension fund managers and pension fund members.members.

Continue

PrimAméricaConsultores IV. Determinants of pension funds impact IV. Determinants of pension funds impact

on corporate governanceon corporate governance

Capital market conditionsCapital market conditions:: In “iliquid markets”, it’s likely that pension fund managers will In “iliquid markets”, it’s likely that pension fund managers will

have a “bias” in favor of a more active role in shareholders have a “bias” in favor of a more active role in shareholders and bondholders meetings, and that they will try to appoint and bondholders meetings, and that they will try to appoint independent board members.independent board members.

The ownership structure of firms has an influence on the role The ownership structure of firms has an influence on the role of pension funds as shareholders and bondholders. When of pension funds as shareholders and bondholders. When ownership is concentrated, pension fund managers should ownership is concentrated, pension fund managers should monitor potential conflicts of interest between mayority and monitor potential conflicts of interest between mayority and minority shareholders; when ownership is atomized, pension minority shareholders; when ownership is atomized, pension fund managers should monitor potential conflicts of interest fund managers should monitor potential conflicts of interest between the firm managers and its shareholders.between the firm managers and its shareholders.

Continue

PrimAméricaConsultores IV. Determinants of pension funds impact IV. Determinants of pension funds impact

on corporate governanceon corporate governance

Continue

In countries with a well developed capital market (and In countries with a well developed capital market (and in capital markets which are well integrated to in capital markets which are well integrated to international capital markets) the impact of the new international capital markets) the impact of the new pension funds on corporate governance will be pension funds on corporate governance will be relatively small, compared to their impact on a less relatively small, compared to their impact on a less developed (and less integrated) capital market.developed (and less integrated) capital market.

PrimAméricaConsultores IV. Determinants of pension fundsIV. Determinants of pension funds

impact on corporate governance impact on corporate governance

Continue

Pension funds investment regulationsPension funds investment regulations::

Investment limits do shape pension funds Investment limits do shape pension funds portfolios.portfolios.

Other types of investment regulations also have an Other types of investment regulations also have an impact on the way in which pension funds monitor impact on the way in which pension funds monitor the companies where they invest.the companies where they invest.

Portfolio limits by type of asset (2002)Portfolio limits by type of asset (2002)

PrimAméricaConsultores

Country

Central Local Others Cash and Term Bonds Mortage Bonds Equity Mutual Derivates Bonds Equity Mutual Govermment Govermment Deposits Backed Funds Funds

Securities

Argentina 50.0% 30.0% 30.0% 40.0% 60.0% 20.0% 20.0% 2.0% 10.0% 10.0%Bolivia 100.0% 10.0% 50.0% 50.0% 45.0% 40.0% 10.0% 50.0%Chile 50.0% 50.0% 50.0% 70.0% 40.0% 25.0% 25.0% 20.0% 10.0%Colombia 50.0% 20.0% 2.0% 40.0% 40.0% 30.0% 30.0% 5.0% 10.0%Costa Rica 70.0% 5.0% 70.0% 30.0% 20.0%Dom. Rep. 10.0% 60.0% 50.0% 70.0% 30.0%El Salvador 80.0% 15.0% 40.0% 15.0% 50.0% 5.0%Mexico 20.0%Nicaragua 50.0% 50.0% 30.0% 50.0% 10.0% 30.0%Peru 60.0% 30.0% 25.0% 40.0% 40.0% 35.0% 15.0% 5.0% 7.5%Uruguay 60.0% 30.0% 30.0% 20.0% 25.0% 0.0%

GOVERMMENT FOREIGNFINANCIAL INSTITUTIONS CORPORATE

Latin America: regulation on the vote of Latin America: regulation on the vote of pension funds in shareholders meetingspension funds in shareholders meetings

PrimAméricaConsultores

* When their participation exceeds some* When their participation exceeds some** The pension fund industry has adopted a Code for self regulation ** The pension fund industry has adopted a Code for self regulation

Ch

ile

Ch

ile

Arg

enti

na

Arg

enti

na

Co

lom

bia

C

olo

mb

ia

Per

uP

eru

1.1. Are pension funds allowed to participate in shareholders meetings?Are pension funds allowed to participate in shareholders meetings? YesYes YesYes YesYes YesYes

2.2. Are pension funds forced to participate in shareholders meetings?Are pension funds forced to participate in shareholders meetings? Yes *Yes * YesYes Yes *Yes * NoNo

3.3. Election of board members:Election of board members: NRNR

·· Can pensions funds vote in the election of members of the boardCan pensions funds vote in the election of members of the board YesYes YesYes YesYes

·· Board of the pension fund must select the candidate to the boardBoard of the pension fund must select the candidate to the board YesYes YesYes

·· Pension funds must make their vote publicPension funds must make their vote public YesYes NoNo YesYes

·· Is it possible to vote for:Is it possible to vote for: NR ** NR **

-- Candidates related to mayority shareholders?Candidates related to mayority shareholders? NoNo NoNo

-- Candidates related to the pension fund management firm?Candidates related to the pension fund management firm? YesYes NoNo

PrimAméricaConsultores

Controlling pension funds managers:Controlling pension funds managers: Good corporate governance practices within the pension Good corporate governance practices within the pension

funds are needed to avoid the risk of pension fund funds are needed to avoid the risk of pension fund managers acting against the interest of pension fund managers acting against the interest of pension fund members:members:

Limits to use of privileged information.Limits to use of privileged information. Disclosure of information.Disclosure of information. Prohibition to invest in firms where pension fund managers Prohibition to invest in firms where pension fund managers

have an interest.have an interest. Valuation of assets at market prices.Valuation of assets at market prices. Legal separation between pension fund assets from Legal separation between pension fund assets from

pension company assets.pension company assets.

In some countries, there are concerns for the possibility In some countries, there are concerns for the possibility of pension fund companies controlling the firms in which of pension fund companies controlling the firms in which the pension fund invest.the pension fund invest.

IV. Determinants of pension fundsIV. Determinants of pension funds impact on corporate governance impact on corporate governance

PrimAméricaConsultores

V. Final commentsV. Final comments

The accumulation of pension funds which follows the creation of The accumulation of pension funds which follows the creation of a mandatory funded pension program, can have a positive a mandatory funded pension program, can have a positive impact on corporate governance.impact on corporate governance.

However, the magnitude of this impact will be strongly correlated However, the magnitude of this impact will be strongly correlated with: the quality of pension fund investment regulations; the with: the quality of pension fund investment regulations; the characteristics of local capital markets; and with the capacity of characteristics of local capital markets; and with the capacity of the supervisors to control for potential conflicts of interest the supervisors to control for potential conflicts of interest between pension fund managers and pension fund members.between pension fund managers and pension fund members.

Even under the appropriate regulatory framework, pension fund Even under the appropriate regulatory framework, pension fund influence over corporate governance will evolve gradually and influence over corporate governance will evolve gradually and will depend on the portfolio decisions of pension fund managers.will depend on the portfolio decisions of pension fund managers.