aurigene discovery technologies - london business school

TRANSCRIPT

1

Aurigene Discovery Technologies

_____________________________________________________________________

Abstract Describes the contract R&D venture of Dr. Reddy’s Labs, a major Indian pharmaceutical firm. Hailed as “the new IT” in India, the biotechnology industry has generated much excitement about its potential for generating foreign exchange as well as employment opportunities. The case profiles the state of the Indian biotechnology industry in 2002, and focuses on an attempt to replicate the successful IT off-shore services model to biotechnology. Discussion issues pertain to the offshore services model in R&D, corporate venturing issues, and the strategic challenges of building high technology firms in the developing world. Subjects Covered: R&D outsourcing, Corporate ventures, Biotechnology

_____________________________________________________________________

© London Business School, August 2003. This case was written by Niraj Gelli (MBA ’03) & Chakrapani Tummalapalli (MBA ’03) of the Indian School of Business under the supervision of Prof. Phanish Puranam of the London Business School. It is meant to be used as a basis for classroom discussion, and does not aim to illustrate adept or inept handling of administrative situations, or purport to be a source of primary data. The Aditya V. Birla Center at LBS is acknowledged for funding.

l

LBS referenceCS-03 -14

2

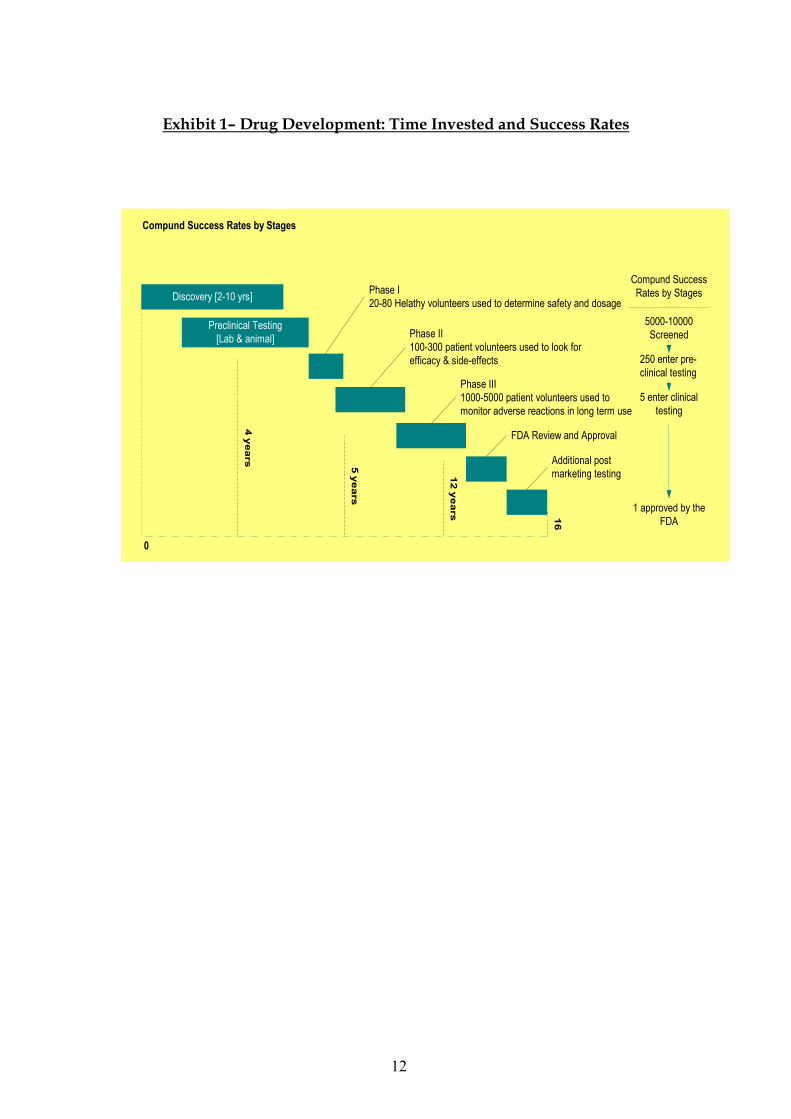

Aurigene Discovery Technologies In early 2003, Dr. Norton Peet (CEO) and Dr. Swaminathan “Swami” Subramaniam (COO) of Aurigene Discovery Technologies were going to make a presentation to the board of Dr. Reddy’s Laboratories (DRL). DRL was one of India’s leading pharmaceutical firms and had already invested $10 million in Aurigene, which was structured as a wholly-owned subsidiary of DRL. Aurigene was to provide fee-based R&D services to global pharmaceutical companies in drug discovery–related research such as protein expression and purification, structure analysis, and drug design. In the ’90s, Indian software firms had achieved spectacular successes by adopting a business model that linked the low-cost, high-quality technical manpower in India to profitable opportunities in the developed world. R&D outsourcing was considered by many to be the next major opportunity for India’s technical workforce. In 2002, there were already several firms in India that provided R&D services in areas like hardware development, chip design, consumer and automotive electronics, and bio-informatics.1 Many argued that the life sciences provided opportunities for the success of a similar business model, as the country had an inexpensive talent pool of highly qualified scientists. Aurigene was among a handful of business ventures across the country that hoped to succeed on a contract R&D model in biotechnology. Swami was going to seek an additional $10 million in funding from DRL, and the presentation he would make would certainly influence the decision. Swami wondered how he could make a persuasive case for additional funding. The Global Pharmaceutical Industry in 20022 With a pipeline of more than 1,000 drugs under development worldwide, the pharmaceutical industry played an ever-increasing role in combating disease. In 2002, the industry had over 98 new medicines in development for AIDS; over 400 for cancer; and over 120 for heart disease and stroke. The US market accounted for 53% of the total global pharmaceutical sales of $320 billion. Of this, nearly $40 billion worth of drugs were estimated to go off-patent in the US market by 2005. In the past, scientists relied on both tedium and serendipity to find candidate compounds that might work against a disease, but technological advances had enabled researchers to custom-design medicines. The hit-or-miss hunt for medicines in soil samples and natural substances that could be active against disease had been superseded by fundamentally new approaches such as genomics and proteomics, and analytical techniques like high throughput screening. The pharmaceutical industry could broadly be divided into prescription drugs, generics, and bulk drugs. Creating and marketing a new prescription drug was a long, expensive, and risky process. Exhibit 1 shows the various steps involved in new drug discovery and development. On average, it took 10 to 15 years to develop a new drug. Most drugs did not survive the rigorous development process—one estimate

1 Product majors shifting more R&D work to India; The Hindu, Business Line, June 19, 2002 2 Section adapted from Pharmaceutical Research and Manufacturers of America, 2002 Industry Profile, PhRMA, Washington, DC, 2002

3

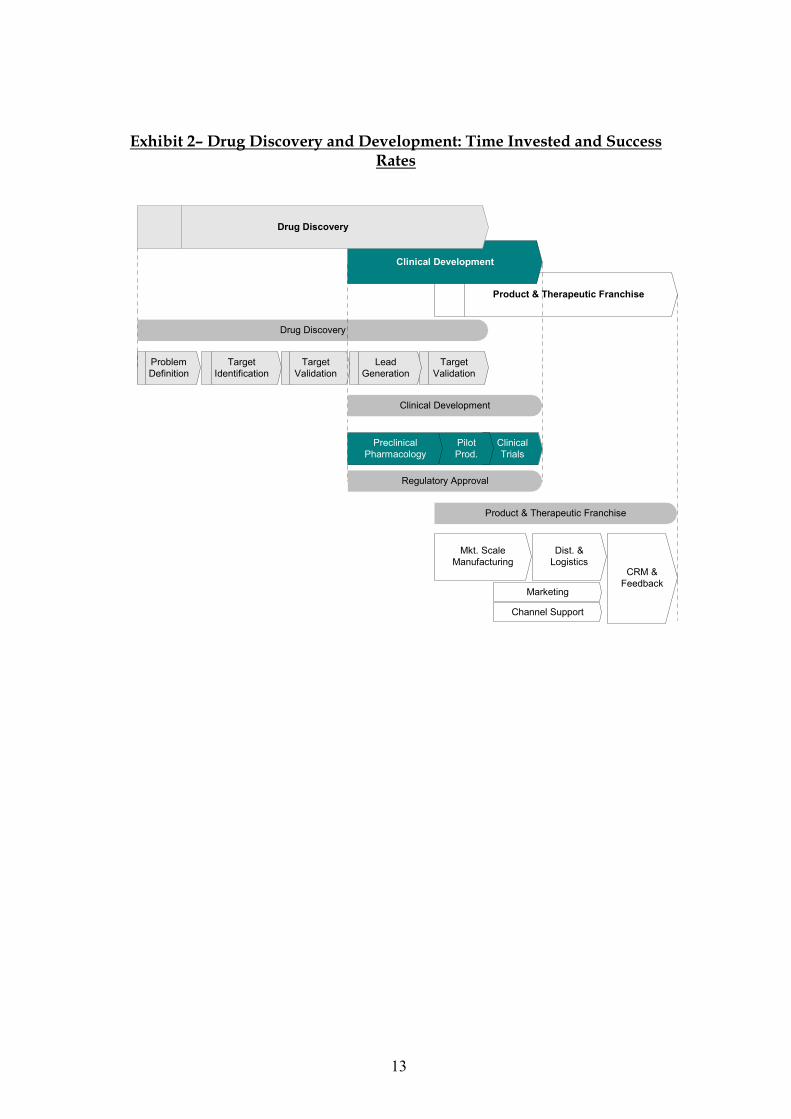

suggested that in the late ’90s, only 20 in 5,000 compounds that were screened finally entered pre-clinical testing, and only one out of five drugs that entered clinical trials was approved for use. By the end of the decade, declining R&D productivity and lengthening drug development timelines had begun to put some pressure on the margins of leading pharmaceutical firms. The ’90s were also marked by the ever-increasing importance of biotechnology in drug discovery. Biotechnology is the science and set of techniques for using living organisms like bacteria, yeast, fungi, plants, and animal cells to produce substances or to perform a commercial purpose.3 Biotechnology was a $50 billion global industry in 2001, with a collective market capitalization estimated at over $200 billion; nearly 5,000 firms worldwide engaged in biotechnology research and product development. The majority of these were concentrated in the US and Europe. In the late 1990s, biotechnology companies were entering into alliances with pharmaceutical partners in unprecedented numbers. Between 1990 and 1998, the top 20 pharmaceutical companies had invested approximately $21 billion in collaborations with biotechnology companies, and between 1996 and 2000 the number of alliances had increased to an average of 616 a year. These collaborations offered biotechnology companies access to resources that they often lacked, such as regulatory expertise and manufacturing and marketing capabilities. In return, pharmaceutical companies gained access to emerging technologies, proprietary products, and the bright minds behind them. Exhibit 2 shows the application of biotechnology to various stages in drug discovery and development. This collaborative approach had proved successful, resulting in biotechnology product sales of $39 billion and a growing pipeline of new products4. In 2002, the pipeline of prescription drugs derived from biotechnology was growing faster than the traditional pharmaceutical pipeline. Pharmaceutical firms outsourced more and more of their R&D budgets -- some estimated that as much as 25% of the discovery-stage R&D budgets of large pharmaceutical firms found its way into small biotechnology firms through various research partnership agreements. It was also estimated that in 2002, 14 of the 55 blockbuster drugs marketed by the ten largest pharmaceutical companies had been in-licensed from biotechnology companies, and their revenues from in-licensed drugs as a proportion of their total revenues had increased from 24% in 1992 to about 40% in 2002. 5 Clinical trials were also becoming increasingly expensive, as volunteers were becoming harder to find in the developed economies of the US and Western Europe. As with R&D productivity, large pharmaceutical firms had dealt with increasing clinical trial costs by beginning to outsource the trials to specialist clinical research organizations (CROs). The development stage R&D outsourcing market had grown relatively sluggishly, from $5.4 billion in 1997 to $9.3 billion in 2001, though some experts predicted that it would grow to $36.0 billion by 2010. In 2001, pharmaceutical

3 Biotechnology Strategies in 1992; HBS; 9-792-082 4 “Value Drivers in Licensing Deals,” Katie Arnold, Anthony Coia, Scott Saywell, Ty Smith, Scott Minick, and Alicia Loffler, Nature Biotechnology, Nov 2002. 5 Pharmaceutical Research and Manufacturers of America, 2002 Industry Profile PhRMA, Washington, DC, 2002

4

firms were outsourcing about 16% of their development budgets. The scope of activities and research that were outsourced to CROs covered pre-clinical studies, clinical studies, regulatory affairs, and filing services. 6 The high-level picture of the stages in drug discovery shown in Exhibit 2 is quite coarse grained; target selection and validation, followed by lead generation and lead optimization, followed by the early clinical candidate selection, could be broken down into several levels that could potentially have 30 to 40 different activities. While the sequence of activities itself was quite “modular” from a technological point of view, there were a few stages which needed to be done together. For example, it would not make sense to do only computational design and not do any medicinal chemistry, as there were significant scope economies and exchange of tacit knowledge across these stages. Instead, as Swami put it, “Access and control of intellectual property were the two reasons why any company would like to be involved in most of the activities. If the activities are split too much, if there are too many hand-overs, then the traceability of who made the invention or who contributed what to the invention is a lot more difficult and complex. Hence the agreement becomes very cumbersome and complex. So typically companies would like to at least do those key processes which make an agreement with another company much more manageable, in terms of identifying who contributed what and how contributions can be evaluated. A key driver behind the fact that companies choose to do a set of activities in-house is their desire to control intellectual property.” The market for generics -- which consisted of drugs that had gone off-patent -- had a different dynamic. In the US, companies filed Abbreviated New Drug Applications (ANDAs) with the Food and Drug Administration (FDA) to seek permission to sell drugs that would go off-patent in the near future. A successful first-time approval for a given product gave a generic manufacturer six months’ exclusive marketing rights in the US, sufficient to earn margins of 30% to 90%. Once the period of exclusivity ended, new competitors would enter rapidly and drive prices down to far less profitable levels. Bulk drugs were essentially a commodity item, with competition based primarily on quality and cost. The Indian Pharmaceutical Industry In the 56 years since India’s independence, the domestic pharmaceutical industry had been shaped primarily by regulation. Initially, multinational companies (MNCs) had a near monopoly on pharmaceuticals. They imported and marketed complete formulations in India, mainly low-cost generics for the masses along with a few highly priced specialty drugs. When the government increased pressure to deter the import of finished products, MNCs set up formulating units in India, and continued importing bulk drugs. In the 1960s, the government laid the foundation for the domestic pharmaceuticals industry by promoting Hindustan Antibiotics Ltd (HAL) and Indian Drugs and Pharmaceuticals Ltd (IDPL), two public-sector companies, for the manufacture of bulk drugs. However, MNCs maintained their lead due to their technical expertise, financial muscle, and ability to move innovations from other

6 Pharmaceutical R&D Outsourcing Strategies: An Analysis of Market Drivers and Resistors to 2010 – Reuters Business Insights

5

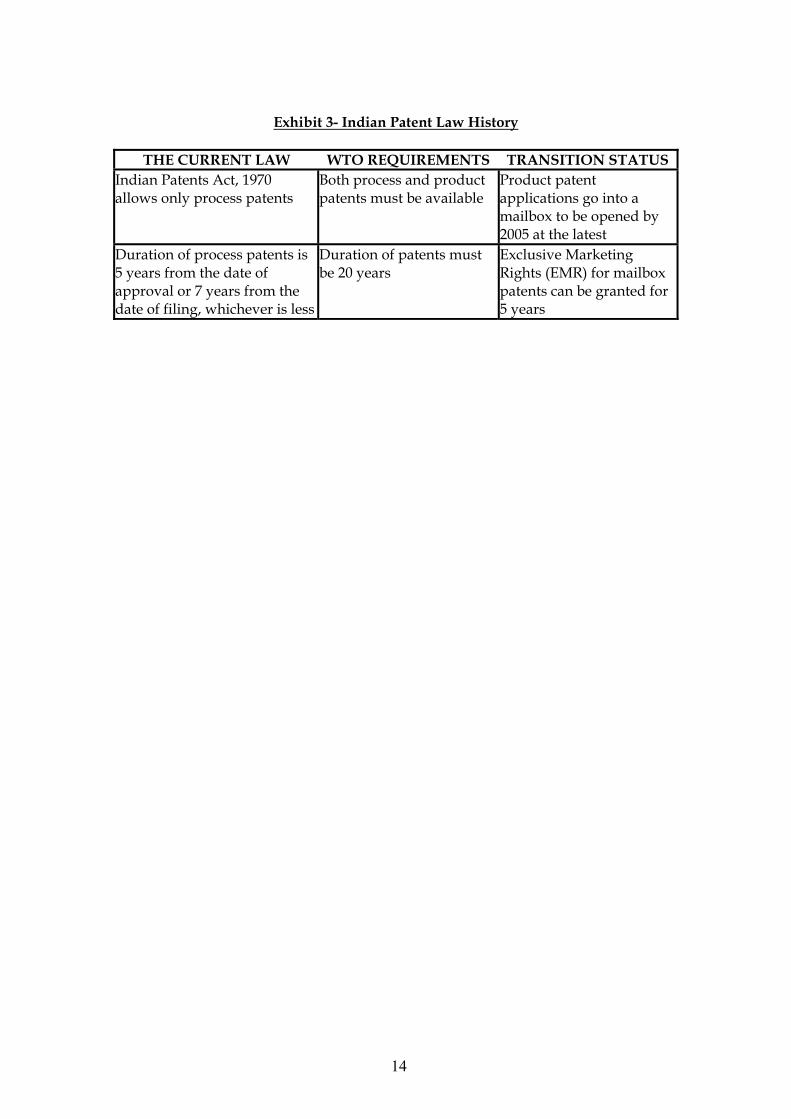

markets into the domestic market. The high cost of basic research, coupled with the sophisticated competencies required and a lack of financing options, deterred private-sector Indian companies from entering the market. This state of affairs changed with the Indian Patent Act of 1970, whereby substances used in foods and pharmaceuticals could no longer be granted product patents. Process patents were granted for a period of five years from the date of grant or seven years from the date of filing, whichever was earlier. Process modifications were far easier to accomplish, and there was a rapid influx of domestic manufacturers. These companies generally started with bulk drugs and gradually progressed into complete formulations. Unlike the MNCs, who were constrained by their parent companies’ product range, local players could branch out to produce almost anything. The lack of product patent royalties dramatically reduced the cost of local manufacture and helped Indian producers to thrive. Shortly thereafter, the Drugs Price Control Order put a ceiling on prices of certain mass-usage formulations. Since selling at such low prices could cause discontent in their home markets, MNCs dramatically curtailed new product launches, giving a further boost to the domestic Indian players. Under the Foreign Exchange Regulations Act in the late ’70s, the MNCs were forced to reduce ownership in their Indian ventures to 40%, or comply with certain export obligations and keep their equity stake at 51%. Many MNCs curtailed the scope of their operations, further strengthening the position of the local pharmaceutical companies. In short, the Indian Patent Act and other laws had awarded the domestic market to the Indian pharmaceutical companies at the expense of MNC drug majors. The Indian pharmaceutical market now consisted of almost 20,000 manufacturers, about 100 of which represented mid-size to large companies holding 20% of the domestic market.7 The total market size was estimated in 1999 at US $7.2 billion -- about 2% of global pharmaceutical revenues. In volume terms, however, it ranked as the world's third largest market. This discrepancy related to the low price of Indian drugs, averaging around 10% of the price of comparable drugs in the US. The industry had grown more than 10% annually for the last 10 years, well above the average industrial growth rate of the Indian GDP. Pharmaceuticals was a net foreign exchange earner for the country, with exports in 1998 amounting to about $1.2 billion. Initially, bulk drug exports were far greater in value than the exports of formulations. Since 1995, however, exports of formulations had overtaken exports of bulk drugs. 8 As part of the WTO agreements, India had agreed to start honoring product patents from 2005 (Exhibit 3). While most believed that this agreement would eventually change the shape of the drug industry in the developing world, some argued that change would be gradual, at best. For one thing, India did not have trained patent examiners to review applications, severely restricting its ability to grant informed patent judgments. Not only must an examiner be fluent in patent law (a subject not taught in Indian universities), he or she must also have deep medicinal chemistry and biological knowledge to grasp the technical nuances of patent approval. Because of

7 Company sources 8 Credit Rating Information Services of India Ltd: CRIS-INFAC Pharmaceutical Industry Annual Review

6

this, no one knew how long it would take before the WTO agreement would come into full force. Biotechnology in India The National Biotechnology Board was established in India in the early ’80s9. This became a full-fledged government department in 1986 and was renamed the Department of Biotechnology (DBT).10 The department functioned as an apex body for a network of government-funded research laboratories and degree-granting institutions throughout the country. The Council for Scientific and Industrial Research (CSIR) was a network of 40 research laboratories across the country. Eleven of these were dedicated to research in biology and biotechnology, and these were generally considered to be at the forefront of research. Though primarily dedicated to industrial applications, some scientists in these institutes were conducting fairly advanced basic research and routinely published their work in international journals and visited leading research labs in the US and Europe. Poor funding conditions in the largely government-owned university departments, and relatively better funding within the CSIR system, had attracted some of the best basic researchers to CSIR. As a result, it became the locus for a large proportion of the basic research in biotechnology in the country, leaving a vacuum in applied research. “We are doing what the universities should be doing,” said one senior scientist in the CSIR system. In 2001, the DBT had created a policy document detailing a fairly ambitious vision for biotechnology in India. The plan called for a focus on genomics and bioinformatics as cutting-edge areas in which Indian scientists could compete effectively, in addition to strengthening traditional biotechnology applications in agriculture. It was estimated that there were about 160 biotechnology companies in India in 2002, engaged in industrial and pharmaceutical biotechnology, with annual revenues of about $150 million.11 By 2002, some established pharmaceutical firms, like DRL, Sun Pharmaceuticals, Nicolas Piramal, and Ranbaxy, had begun investing in biotechnology as they saw the shape of the future in the global pharmaceutical industry. These firms had deep pockets and steady cash flows from their bulk drugs and formulations exports. Some, like DRL, had also achieved considerable success in the lucrative generics market in the US, and most had ambitions of transforming their companies into research-based pharmaceutical firms. Even a non-pharmaceutical company like the diversified Reliance Group had set up a subsidiary, Reliance Life Sciences, that was among the 11 laboratories worldwide to be approved by the National Institutes of Health in the US as a source of embryonic stem cell lines for research. The RP Goenka Group had a similar venture in the offing. Start-up firms like Shanta Biotech and Bharat Biotech, both located in the southern Indian city of Hyderabad, had made the entrepreneurial opportunities in biotechnology widely visible. Bharat Biotech owned the world's second largest

9 India and Its Big Leap Forward In Biotechnology; excerpts from "India Perspectives," August 1997; Sipra Guha Mukherjee 10 http://dbtindia.nic.in/ 11 CII Form Biotech Forum; Business Standard, February 7, 2003

7

hepatitis B manufacturing plant with a capacity of 100 million doses per annum, and the largest contract manufacturing and filling facility in the Asia Pacific region for any biological product. Established in 1996, Bharat Biotech had launched Revac-B in 1998, a vaccine for hepatitis B. Vaccines for hepatitis A, rabies, rotavirus, and malaria were in the pipeline. The founder, Dr. Krishna Ella, was a life scientist who had decided to return to India after several years in the US. Ella strongly believed in the value of keeping abreast with the latest science, and he had committed Bharat Biotech to a range of partnerships with research labs at home and abroad. Shanta Biotech had developed India's first genetically engineered hepatitis B vaccine. Shanta had generics like insulin and streptokinase, as well new vaccines against hepatitis C and hepatitis E in its pipeline. Varaprasad Reddy, an electronics engineer by training, had founded Shanta Biotech. Reddy was also preparing to offer contract R&D services in areas like molecular cloning and antibody development, in addition to leasing out Shanta’s facilities for production. Like Bharat, Shanta had an impressive list of research collaborations with government labs in India and abroad. Both Ella and Reddy were prominent in the business press as examples of technocrats and “bio-entrepreneurs.” Both companies had developed manufacturing infrastructure to meet US FDA standards. The success of the two companies had put serious pressure on hepatitis vaccine sales margins of the Indian subsidiaries of multinational pharmaceutical companies, as the Indian products were substantially cheaper. In a much-publicized deal, Pfizer had signed an agreement with Shanta to market its hepatitis vaccine globally. Bangalore-based Biocon was an industrial biotechnology company that had been among the early entrants into pharmaceutical biotechnology. Biocon and its subsidiaries employed about 700 people and had revenues close to $4 million in 2002. Like Bharat and Shanta, Biocon was privately held; 75% of the company’s equity belonged to founder and CEO Kiran Mazumdar-Shaw and her family. Biocon had begun to have some success with manufacturing generic products for cholesterol reduction in the US market. The company had also succeeded in creating a new platform technology for fermentation. The invention had won a US patent in 2000. Biocon’s subsidiaries, Syngene and Clinigene, were created with the intention of exploiting opportunities in contract R&D. Syngene provided services in the discovery stages, while Clinigene focused on clinical studies. The diversity and density of Indian patient populations was perceived to be a unique advantage for Clinigene to pursue specialized clinical studies. Mazumdar-Shaw was well known to the business press as a spokeswoman for the Indian biotechnology sector, and in 2003, had become the first president of the newly founded Association of Biotechnology-Led Enterprises (ABLE) that would represent the biotechnology sector just as NASSCOM (the National Association of Software and Service Companies) had done for the country’s software industry.12 Dr. Reddy's Laboratories: An Overview Founded in 1984, DRL was a leading Indian pharmaceutical company that developed, manufactured and marketed bulk drugs and formulations at affordable prices. In 2002,

12 Information on Bharat Biotech, Shanta Biotech and Biocon India is drawn mostly from secondary sources.

8

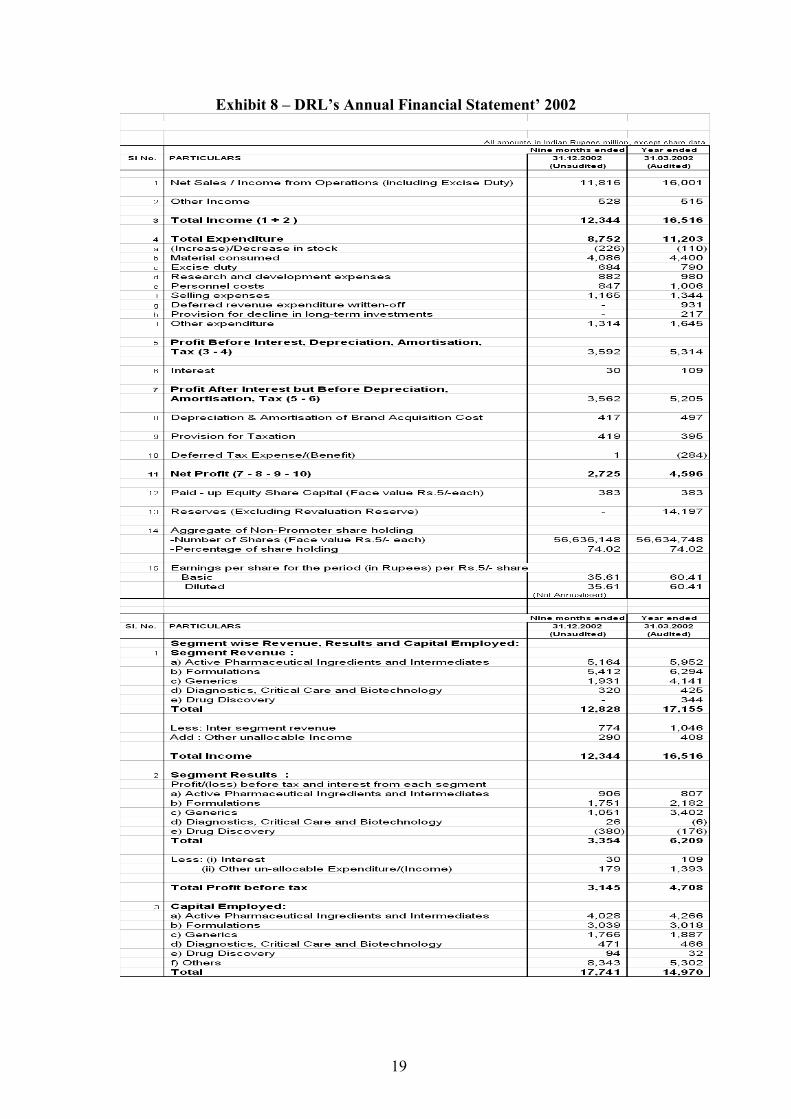

it had revenues of $320 million, mostly from exports to 60 countries (Exhibit 8). The company was named after its founder, Dr. Kallam Anji Reddy. DRL initially began as a supplier of bulk “actives” to Indian drug manufacturers, but soon started exporting to other less-regulated markets. This had the advantage of not requiring manufacturing in FDA-approved facilities, for which certification was very costly and time consuming. In 1993, DRL entered into joint ventures in Russia and the Middle East, creating two formulation units. DRL exported bulk drugs to these formulation units, which then converted them into finished products. Much of DRL’s early success came in unregulated markets, which recognized process patents but not product patents. This enabled the company to reverse-engineer patented drugs from the developed world and sell them royalty-free in India and Russia. By the early ’90s, using the expanded scale and profitability from these unregulated markets, DRL had begun to focus on obtaining FDA approval for its formulations and bulk drug manufacturing plants in the developed economies. This allowed its movement into regulated markets such as the US and Europe. Reddy’s vision was to eventually transform DRL into a “discovery-led global pharmaceutical company.” Reddy had recognized India’s cost advantages early on. In his presidential address to the Indian Pharmaceutical Congress (1992), he said, “Basic research is an arduous task and is said to be expensive. The statistical data from Western countries are frightening. It is estimated to cost anywhere between $100 and $200 million, but it is my considered opinion that in the Indian context such an endeavor may be accomplished within Rs 100 crore [about $30 million at that time] or so. Expenditure of this magnitude is within the reach of some companies in India.” He set up Dr. Reddy’s Foundation (DRF) to be the research arm of DRL in 1992. DRF filed its first US patent in 1996. By 1997, DRL was ready for the next major step. From being a bulk drug supplier to regulated markets like the US and the UK, and a branded formulations supplier in unregulated markets like India and Russia, DRL made the transition into generics. The same year, DRF out-licensed a molecule for clinical trials to Novo Nordisk, a Danish pharmaceutical company. By 2000, DRL had undertaken its first commercial launch of a generic product with market exclusivity in the US, and in 2001, it became the first non-Japanese pharmaceutical company from the Asia-Pacific region to be listed on the New York Stock Exchange. Each of these achievements was path-breaking for the Indian pharmaceutical industry (Exhibit 4 provides a list of significant milestones in DRL’s history). Reddy felt that DRL was making significant progress in moving toward its goal of transforming itself from a bulk drug manufacturer to becoming a research-based discoverer of new chemical entities (NCEs). In five to seven years, he hoped to transform DRL into a global research-driven pharmaceutical company. By 2001, the research arm of the firm, DRF, had managed to create nine NCEs that were improvements on existing drugs in therapeutic areas like pain management, hypertension, and diabetes (Exhibit 5). By the end of the following year, it had managed to obtain close to 40 US patents and had about 215 employees. Instead of committing to investing the enormous resources necessary for clinical trials, it had opted to out-license some of the molecules to larger international players. This was a

9

routine practice at much smaller but similarly cash-constrained biotechnology firms in the West. The licensor would receive milestone payments as the NCE crossed various regulatory and clinical-trial hurdles. DRL posted an income of Rs 34.4 crore (US $7.2 million) from drug discovery activities in 2001-2002. However, by early 2003 the pipeline of nine NCEs had fallen into some disarray as trials were suspended on three of them -- DRF-4848, DRF-3188, and DRF-NPPC. While the first two were in the late pre-clinical stage, DRF-NPPC had recently completed pre-clinical trials. DRF-3188 was to be used in treating cancer, viral infections, and immuno-stimulation. DRF-4848 was an anti-inflammatory, while DRF-NPPC was an insulin sensitizer. Of the nine NCEs listed on the 2002 balance sheet, the company had also out-licensed two anti-diabetic molecules to Novo Nordisk and one insulin sensitizer to Novartis. In July 2002, Novo Nordisk announced its decision to suspend clinical trials on DRF-2725, citing preliminary data from pre-clinical studies, which indicated the development of urine bladder tumors in rats and mice. The company had yet to decide whether to carry out further clinical trials. Soon after, Novartis also announced its decision to discontinue further development of DRF-4158. Setting up Aurigene Discovery Technologies

DRL management saw no reason that the R&D outsourcing opportunities being exploited in other industries (such as software, hardware, and electronics) should not also embrace the life sciences. After toying with the idea of setting up a new division for contract R&D, DRL ultimately chose to float a separate company known as Aurigene Discovery Technologies, with offices in Bangalore and Boston. Swami believed there were good reasons for this decision. First, it would be a difficult proposition for DRL to source business from competing players, as the firm had its own drug discovery practice. This was critical in the Indian context, where there was no provision for product patents in the immediate future. Second, a fast-growing research boutique would necessitate an entrepreneurial culture that could not be offered by a large, organization such as DRL.

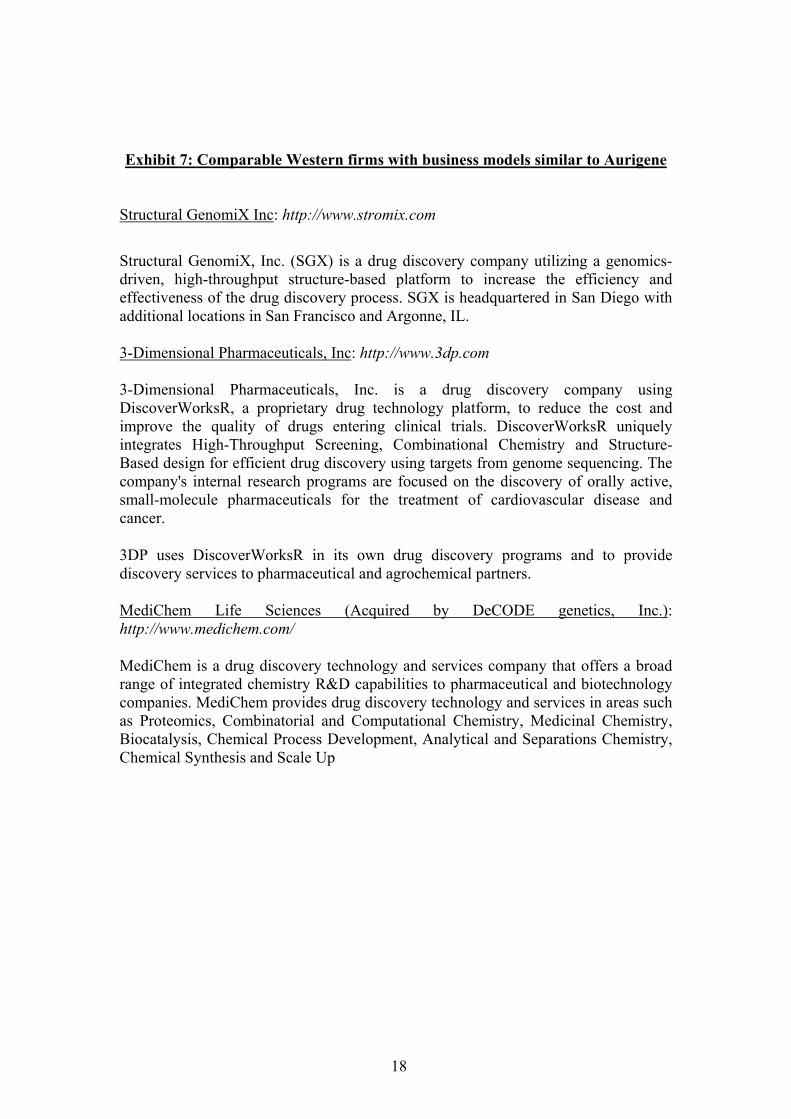

Aurigene was floated as a 100% subsidiary of DRL late in 2001. The mission for Aurigene was to become the preferred partner for drug discovery companies worldwide. Aurigene aimed to provide high-end services by working on complex lead molecules that could ultimately become the subject matter for intellectual property filing. Aurigene aimed to provide comprehensive support for drug discovery through its services in protein expression and purification, structural biology, structure-based drug design, and medicinal chemistry. By working closely with the clients and through a unique mix of talented people and computational and laboratory technologies, the company wanted to offer a comprehensive platform for the rapid and efficient exploitation of genomic data for drug discovery (Exhibit 6). While the idea of contract R&D services in drug discovery was not new, and several firms with similar business models already existed in the West (Exhibit 7), Swami believed that the on-shore/off-shore combination was unique and would allow Aurigene to leverage substantial cost advantages.

10

Peet, Aurigene’s CEO, operated from the firm’s Boston office. Peet had earned his Ph.D. in natural products chemistry from the University of Nebraska and had done his post-doctoral studies at MIT. Swami, the COO, headed the Indian facility in Bangalore. After obtaining his medical degree, a Ph.D. from the University of Pennsylvania, and a stint as a visiting scientist at the National Institutes of Health in the US, Swami had chosen to return to India. G. V. Prasad, the CEO of DRL, was the chairman of Aurigene’s board. Prasad had a B.S. in chemical engineering from Illinois Institute of Technology and an M.S. in industrial administration from Purdue University. Aurigene’s Boston office was mostly staffed with local recruits. The lab spaces at the Bangalore and Boston facilities were 200,000 square feet and 7,200 square feet, respectively. The capacity available at the Bangalore facility was expected to generate powerful scale-based economies. Although small, the Boston center had sufficient R&D activity to prove its capabilities and credibility to US clients. However, many clients preferred to visit the Bangalore laboratory before entering into a major relationship with Aurigene. Based on the availability of resources, some of the research work was initiated in Boston. As Aurigene built out its resources in Bangalore, it hoped to move most of the work off-shore, where the cost advantages would be significant. In cases where the client needed a quick turnaround or overnight results, the Boston lab was a better choice. The Boston center also helped to address a major concern of Aurigene’s potential clients -- the protection of their intellectual property. The US presence bound Aurigene to the local judicial system. Aurigene was exploring a range of payment structures from each of its clients. The agreements differed according to the level of risk-sharing with the clients.

• Up-front Payment: In the early stages, the company expected partial funding for some of the R&D activities. This was followed by a “contingent payment” mechanism at the end of every milestone reached. Aurigene would not have any claim on the intellectual property.

• Pure Outsourcing Method: According to this agreement, Aurigene got paid on a fee basis with no claims on intellectual property.

• Discover & Share: In this method, Aurigene along with the collaborating company jointly conducted research and agreed to share the proceeds of commercialization as per a previously agreed-upon formula. Aurigene was thus exposed to a higher risk in this model. If its research succeeded in identifying or optimizing a lead molecule, Aurigene would share the gains (50% or even more) with the interested party.

The mandate to Aurigene from DRL was to position itself as a service company and become profitable quickly. Hence, in the initial years, Aurigene would seek more up-front and fee-for-service payments and would assume a very small part of the risk. The front-loading of the payments would help the company become revenue positive and profitable much faster.

11

“DRL has provided the initial impetus for Aurigene, in terms of skills, talent, and funding, and expects Aurigene to run as a stand-alone company and maintain its independence,” remarked DRL CEO Prasad. Swami believed that Aurigene clearly derived some advantages from its lineage. The assured funding commitment from DRL enabled it to take a long-term approach. In addition, it was able to tap into DRL’s expertise and experience to ramp up the operations in less than a year’s time. DRL had also made a conscious effort to commit key human and intellectual resources for the venture to be a success. The objective of the investment in Aurigene was to create value in terms of IP, skills, and R&D infrastructure. What was in it for DRL? According to Prasad, “If it was purely financial return, we would not have invested in Aurigene.” Through Aurigene, DRL would have access to R&D services using the latest tools of drug discovery. Few companies in India had this expertise. Thus, Aurigene would strengthen DRL’s discovery pipeline. Swami did believe that Aurigene faced a challenge in convincing customers that it was independent of DRL, and that any intellectual property developed by Aurigene for its customer would not be accessible to anyone else, including DRL. The two companies had categorically refused to share people, resources, and knowledge between them beyond the start-up stage. The official “no-poaching policy” corroborated this philosophy. Both companies were operatively independent, with interactions taking place only at the board level. However, Aurigene was mandated to make a formal request to the board for any further capital requirements. Prasad agreed that in order for Aurigene to succeed and attract more customers, it had to remain neutral: “If they are not neutral it does not serve the purpose it has been created for.” DRL at best would be a preferred customer with no additional rights or benefits. Future Directions DRL’s initial investment of $10 million had been used up to build the management team and R&D facilities at Boston and Bangalore. Aurigene had come up with a fresh request for additional funds to the tune of $10 million. This amount was intended to be spent on scaling up the facilities and to sustain operations for the next two to three years. With only one hour remaining until the board meeting, Swami wondered how he could make a strong case for the additional funding. He knew that Prasad would be asking him and the Aurigene board some tough questions: Had floating Aurigene as an independent firm been the right decision? How was this model creating value for DRL and its shareholders? Would the long-term payoff be strategic or financial in nature? Was this a good time to bring in outside investors like VCs and other pharmaceutical companies?

12

Exhibit 1– Drug Development: Time Invested and Success Rates

Compund Success Rates by Stages

Discovery [2-10 yrs]

Preclinical Testing[Lab & animal]

Phase I20-80 Helathy volunteers used to determine safety and dosage

Phase II100-300 patient volunteers used to look forefficacy & side-effects

Phase III1000-5000 patient volunteers used tomonitor adverse reactions in long term use

FDA Review and Approval

Additional postmarketing testing

Compund SuccessRates by Stages

5000-10000Screened

250 enter pre-clinical testing

5 enter clinicaltesting

1 approved by theFDA

4 years 5 years

12 years 16

0

13

Exhibit 2– Drug Discovery and Development: Time Invested and Success Rates

Product & Therapeutic Franchise

ClinicalTrials

TargetValidation

ProblemDefinition

TargetIdentification

TargetValidation

LeadGeneration

PilotProd.

PreclinicalPharmacology

Clinical Development

Drug Discovery

Regulatory Approval

Clinical Development

Drug Discovery

CRM &Feedback

Dist. &Logistics

Mkt. ScaleManufacturing

Product & Therapeutic Franchise

Marketing

Channel Support

14

Exhibit 3- Indian Patent Law History

THE CURRENT LAW WTO REQUIREMENTS TRANSITION STATUS

Indian Patents Act, 1970 allows only process patents

Both process and product patents must be available

Product patent applications go into a mailbox to be opened by 2005 at the latest

Duration of process patents is 5 years from the date of approval or 7 years from the date of filing, whichever is less

Duration of patents must be 20 years

Exclusive Marketing Rights (EMR) for mailbox patents can be granted for 5 years

15

Exhibit 4 – DRL’s Progress since Inception

16

Exhibit 5: DRL’s NCE Pipeline

(Source: Company Information)

17

Exhibit 6 – Aurigene’s Business Model

18

Exhibit 7: Comparable Western firms with business models similar to Aurigene

Structural GenomiX Inc: http://www.stromix.com

Structural GenomiX, Inc. (SGX) is a drug discovery company utilizing a genomics-driven, high-throughput structure-based platform to increase the efficiency and effectiveness of the drug discovery process. SGX is headquartered in San Diego with additional locations in San Francisco and Argonne, IL.

3-Dimensional Pharmaceuticals, Inc: http://www.3dp.com 3-Dimensional Pharmaceuticals, Inc. is a drug discovery company using DiscoverWorksR, a proprietary drug technology platform, to reduce the cost and improve the quality of drugs entering clinical trials. DiscoverWorksR uniquely integrates High-Throughput Screening, Combinational Chemistry and Structure-Based design for efficient drug discovery using targets from genome sequencing. The company's internal research programs are focused on the discovery of orally active, small-molecule pharmaceuticals for the treatment of cardiovascular disease and cancer.

3DP uses DiscoverWorksR in its own drug discovery programs and to provide discovery services to pharmaceutical and agrochemical partners.

MediChem Life Sciences (Acquired by DeCODE genetics, Inc.): http://www.medichem.com/

MediChem is a drug discovery technology and services company that offers a broad range of integrated chemistry R&D capabilities to pharmaceutical and biotechnology companies. MediChem provides drug discovery technology and services in areas such as Proteomics, Combinatorial and Computational Chemistry, Medicinal Chemistry, Biocatalysis, Chemical Process Development, Analytical and Separations Chemistry, Chemical Synthesis and Scale Up

19

Exhibit 8 – DRL’s Annual Financial Statement’ 2002