australian fisheries statistics - department of the ... · iii foreword australian fisheries...

TRANSCRIPT

Australian Bureau of Agricultural and Resource Economics – Bureau of Rural Sciences

Australian Government

fisheries statistics

August 2010

2009

Australian

© ABARE–BRS and FRDC 2010

This work is copyright. The Copyright Act 1968 permits fair dealing for study, research, news reporting, criticism or review. Selected passages, tables or diagrams may be reproduced for such purposes provided acknowledgment of the source is included. Major extracts or the entire document may not be reproduced by any process without the written permission of the Executive Director, ABARE–BRS.

The Australian Government acting through Australian Bureau of Agricultural and Resource Economics – Bureau of Rural Sciences has exercised due care and skill in the preparation and compilation of the information and data set out in this publication. Notwithstanding, the Australian Bureau of Agricultural and Resource Economics – Bureau of Rural Sciences, its employees and advisers disclaim all liability, including liability for negligence, for any loss, damage, injury, expense or cost incurred by any person as a result of accessing, using or relying upon any of the information or data set out in this publication to the maximum extent permitted by law.

ISSN 1037-6879

ABARE–BRS 2010, Australian fisheries statistics 2009, Canberra, August.

Australian Bureau of Agricultural and Resource Economics – Bureau of Rural Sciences Postal address GPO Box 1563 Canberra ACT 2601 Australia Switchboard +61 2 6272 2010 Facsimile +61 2 6272 2001 Email [email protected] Web abare-brs.gov.au

ABARE–BRS project 3298

Fisheries Research and Development Corporation PO Box 222 Deakin West ACT 2000 Telephone +61 2 6285 0400 Facsimile +61 0 6285 4421 Internet www.frdc.com.au

On 1 July 2010, the Australian Bureau of Agricultural and Resource Economics (ABARE) and the Bureau of Rural Sciences (BRS) merged to form ABARE–BRS.

Acknowledgments Thuy Pham prepared this report. The assistance of officers from state fisheries departments and the Australian Fisheries Management Authority, researchers and various industry representatives is gratefully acknowledged. The Australian Bureau of Statistics supplied the trade data.

Funding for this report was provided by the Fisheries Research and Development Corporation and the Australian Government Department of Agriculture, Fisheries and Forestry.

Note to the readersThe data is accurate at the time of publication but updates may subsequently be available on state websites until they can be incorporated into the following year’s publication. A wider data set is available on request.

iii

Foreword Australian fisheries statistics is an annual report that has been in publication since 1991. It provides annual updates of fisheries production and trade data and serves as an important source of information for the fishing and aquaculture industry, fisheries managers, policymakers and researchers. The estimates of the gross value of production provided in the report are used for a range of purposes; for example, to determine Commonwealth, state and territory fisheries research funding arrangements each year.

The current report contains data on the volume and value of production from state and Commonwealth commercial fisheries, and on the volume and value of Australian fisheries trade, by destination, source and product. Profiles of Commonwealth and state commercial fisheries and state aquaculture for 2008 and 2009 are also provided. These cover selected species, fishing methods and number of licence holders. Additional information is also provided on the recreational fishing sector and the indigenous fishing sector. The amount of information included in the report regarding these two sectors is expected to increase in future reports.

Australian fisheries statistics is part of a suite of ABARE–BRS publications that provide a comprehensive account of historical trends in, and the outlook for, Australian fisheries. Australian commodity statistics provides a historical series of production and trade statistics for fisheries and a range of other commodities. Australian commodities includes forecasts for major fisheries commodities, which are updated each quarter. Detailed analysis of the economic performance of selected fisheries is provided in the annual Australian fisheries survey report. An assessment of the economic performance of all fisheries managed by the Australian Fisheries Management Authority is provided in Fishery status reports.

Phillip Glyde Executive Director August 2010

iviv

Inquiries Inquiries regarding Commonwealth and state information should be directed to the respective coordinators of fisheries statistics shown below.

New South Wales Laurie Derwent (Wild sector) NSW Fisheries Ph: (02) 9527 8568 Fax: (02) 9527 8409

Janine Sakker (Aquaculture) NSW Fisheries Ph: (02) 4916 3847 Fax: (02) 4982 1107 Victoria Mark Taylor and Paula Baker Victorian Department of Primary Industries Ph: (03) 5561 9964

Queensland Lew Williams (Wild sector) Fisheries Queensland, Department of Employment Economic Development and Innovation (DEEDI) Ph: (07) 3224 2550 Fax: (07) 3224 2805

Ross Lobegeiger and Max Wingfield (Aquaculture) Fisheries Queensland, Department of Employment Economic Development and Innovation (DEEDI) Ph: (07) 3400 2040 Fax: (07) 3408 3535

Western Australia Eva Lai and Mark Cliff Western Australian Department of Fisheries Ph: (08) 9203 0111 Fax: (08) 9203 0199

South Australia Angelo Tsolos (Wild sector) South Australian Research and Development Institute (SARDI) Ph: (08) 8207 5414 Fax: (08) 8207 5415

vv

In quir ie s

Natalie Prior (Aquaculture) Department of Primary Industries and Resources South Australia (PIRSA) Ph: (08) 8226 2258 Fax: (08) 8226 0330

Tasmania Denise Garcia Marine Resources Division Department of Primary Industries, Parks, Water and Environment, Tasmania Ph: (03) 6233 6723 Fax: (03) 6233 3198

Northern Territory Maree Apostoles NT Fisheries Department of Resources (DoR) Ph: (08) 8999 2305 Fax: (08) 8999 2057

Commonwealth Thim Skousen and Selvy Coundjidapadam Australian Fisheries Management Authority (AFMA) Ph: (02) 6225 5350 Fax: (02) 6225 5500

Mal Heath (Licensing) Australian Fisheries Management Authority (AFMA) Ph: (02) 6225 5421

vi

Definitions and explanations

Aquaculture production is the live weight quantity of product produced and marketed by aquaculturists.

Aquaculture value is the assessed value received by aquaculturists on the basis of an ‘at farm-gate’ equivalent, for product marketed.

Export quantity data are supplied by the Australian Bureau of Statistics on the basis of the net product weight exported.

Export value data are supplied by the Australian Bureau of Statistics on the basis of free on board value.

Import quantity data are supplied by the Australian Bureau of Statistics on the basis of the net product weight imported.

Import value data are supplied by the Australian Bureau of Statistics on the basis of product cost. The value excludes insurance and freight costs in delivering the commodity to Australia from the port of origin but may include inland freight and insurance costs incurred in delivering the commodity to the port of origin.

Production quantity is a measure of the quantity of fish product landed by fishery, usually on the basis of catch records.

Production value is the assessed value at the point of landing for the quantity produced and excludes transport and marketing costs.

Products consist of fisheries products marketed for human consumption plus non-edible fisheries products.

Real terms/real prices are historical or future prices adjusted to reflect changes to the purchasing power of money (most commonly measured by the consumer price index).

Re-imports (included in merchandise imports statistics) are goods originally exported, which are subsequently imported in either the same condition in which they were exported, or after undergoing repair or minor operations which leave them essentially unchanged. Minor operations include blending, packaging, bottling, cleaning and sorting.

vii

D e f ini tio ns a n d e x p l a n a tio ns

‘Reals’ and rounding—‘Real’ 2008–09 dollars or ‘real terms’ refer to the conversion of nominal dollar values to take account of inflation. Comparison from year to year is expressed in nominal terms unless stated otherwise. Small discrepancies in totals are generally caused by the rounding components. A dash (-) is used to denote a nil or negligible amount.

Seafood is any fish or other aquatic plant or animal intended for human consumption; it excludes non-edible fisheries products.

Southern bluefin tuna sold from aquaculture farms in South Australia is reported at its market value. However, the input value of those tuna is also included as a production output from the Commonwealth’s Southern Bluefin Tuna Fishery. To avoid double counting, the input value is netted out of Australian totals.

Abbreviations and symbols

kg kilogram

t tonne

kt kilotonne

$ dollar (Australian)

$’000 thousand dollars (Australian)

$m million dollars (Australian)

$b billion dollars (Australian)

fob free on board

AFZ Australian Fishing Zone

na not available

nei not elsewhere included

w wild catch

a aquaculture

viii

ContentsProduction 1

Fast facts 1Production by species 2Production by jurisdiction 7Production by sector 16

Trade 19

Fast facts 19Exports and imports 20Exports by commodity 21Exports by destination 23Exports by state 24Imports by commodity 25Imports by source 27

Employment 29

Fast facts 29

Recreational and charter fishing 32

Indigenous fishing 34

Profile of Australian fisheries 39

References 48

1

Production

Fast facts

In 2008–09• The total volume of Australian fisheries production fell by 2800 tonnes to 238 000 tonnes. • The gross value of Australian fisheries production remained relatively stable compared with

2007–08, increasing by $4.9 million to $2.2 billion. • Tasmania accounted for the largest share of gross value of production (23 per cent),

followed by South Australia (21 per cent) and Western Australia (17 per cent). Commonwealth fisheries accounted for 14 per cent of gross value of production.

• The gross value of aquaculture production (including southern bluefin tuna wild catch input to the South Australian tuna farming sector) decreased by 1 per cent ($9.1 million) to $861 million, and accounted for 39 per cent of the gross value of Australian fisheries production. The volume of aquaculture production was 69 600 tonnes, accounting for 29 per cent of total Australian fisheries production.

• Thevalueoffarmedsalmonidsroseby7percentto$323millionin2008–09.Farmedsalmonids continues to be the largest aquaculture species produced in Australia, accounting for 37 per cent of the total value of Australian aquaculture production and 15 per cent of the total value of fisheries production.

• The gross value of production for the wild catch sector increased by 1 per cent, to $1.4 billion. The volume of production decreased by 5 per cent (8500 tonnes) to 173 100 tonnes.

Since 1999–2000• The total annual volume of fisheries production has increased by 15 000 tonnes (7 per cent),

while the annual real gross value of production has fallen by $0.9 billion (30 per cent).• The increase in production volume has been driven predominantly by growth in the

production of Australian sardines and salmonids. • The driving factor behind the fall in production value has been the decline in the value of

rock lobster, prawns, abalone and tuna. The combined value of these four species has fallen by $0.8 billion (in real terms) over this period.

Top five, by volume in 2008–09

(wild catch and aquaculture—tables 2 and 17)

Australian sardine 31 500 tonnes

Salmonids 29 700 tonnes

Prawns 23 900 tonnes

Oysters 14 100 tonnes

Tuna 13 700 tonnes

Top five, by value in 2008–09

(wild catch and aquaculture—tables 2 and 17)

Rock lobster $404 million

Salmonids $323 million

Prawns $289 million

Abalone $188 million

Tuna $187 million

2

Pro du c tio n

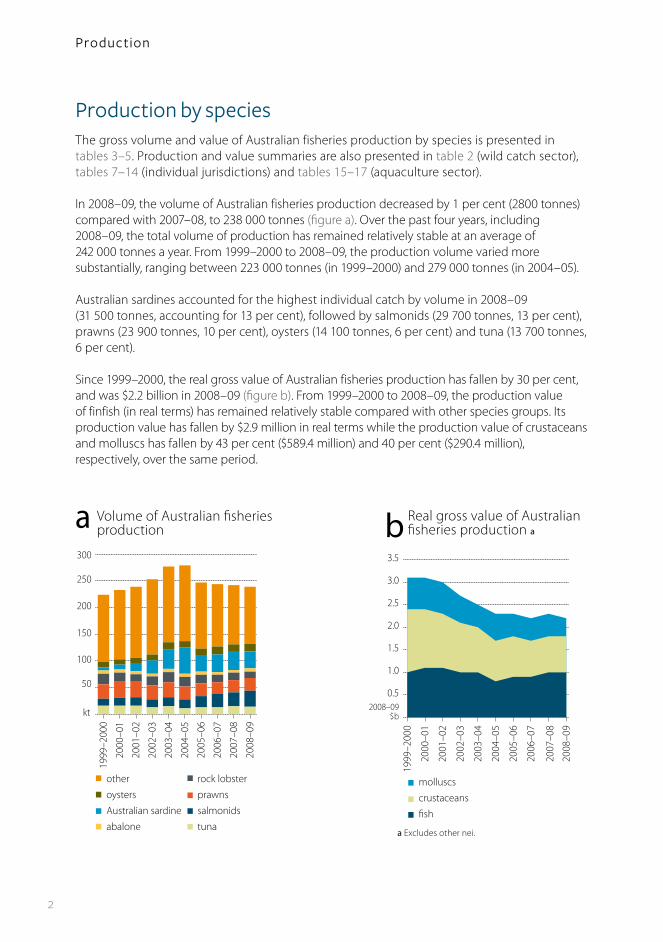

Production by speciesThe gross volume and value of Australian fisheries production by species is presented in tables 3–5. Production and value summaries are also presented in table 2 (wild catch sector), tables 7–14 (individual jurisdictions) and tables 15–17 (aquaculture sector).

In 2008–09, the volume of Australian fisheries production decreased by 1 per cent (2800 tonnes) compared with 2007–08, to 238 000 tonnes (figure a). Over the past four years, including 2008–09, the total volume of production has remained relatively stable at an average of 242 000 tonnes a year. From 1999–2000 to 2008–09, the production volume varied more substantially, ranging between 223 000 tonnes (in 1999–2000) and 279 000 tonnes (in 2004–05).

Australian sardines accounted for the highest individual catch by volume in 2008–09 (31 500 tonnes, accounting for 13 per cent), followed by salmonids (29 700 tonnes, 13 per cent), prawns (23 900 tonnes, 10 per cent), oysters (14 100 tonnes, 6 per cent) and tuna (13 700 tonnes, 6 per cent).

Since 1999–2000, the real gross value of Australian fisheries production has fallen by 30 per cent, and was $2.2 billion in 2008–09 (figure b). From 1999–2000 to 2008–09, the production value of finfish (in real terms) has remained relatively stable compared with other species groups. Its production value has fallen by $2.9 million in real terms while the production value of crustaceans and molluscs has fallen by 43 per cent ($589.4 million) and 40 per cent ($290.4 million), respectively, over the same period.

Volume of Australian fisheriesproduction

other

oysters

Australian sardine

abalone

rock lobster

prawns

salmonids

tuna

100

kt

50

150

200

300

250

a

2008

–09

2007

–08

2006

–07

2005

–06

2004

–05

2003

–04

2002

–03

2001

–02

2000

–01

1999

–200

0

Real gross value of Australianfisheries production ab

molluscs

crustaceans

fish

2008

–09

2007

–08

2006

–07

2005

–06

2004

–05

2003

–04

2002

–03

2001

–02

2000

–01

1999

–200

0

a Excludes other nei.

2008–09$b

0.5

1.0

1.5

2.0

2.5

3.0

3.5

3

Pro du c tio n

At the individual species level, the decline in real value was largely driven by decreases in the value of rock lobster, prawns, abalone and tuna (figure c). The combined value of these species has fallen by 44 per cent ($838.5 million) in real terms over the period.

The declining values of these key species have been driven by falls in unit prices, with the exception of rock lobster (figure d). Since the production of these species is export-oriented, prices are strongly influenced by exchange rate movements. The strength of the Australian dollar against the currencies of major trading partners, particularly the United States and Japan, has reduced the competitiveness of Australian fisheries exports in recent years (box 1). Prices for lobster have been increasing since 2003–04 despite exchange rate movements, owing to increased demand for lobster on international markets and lower supply from key suppliers.

The product composition of the gross value of production of Australian fisheries in 2008–09 has not altered substantially relative to 2007–08. In 2008–09, rock lobster remained Australia’s highest valued production species, at $404 million. It accounted for 18 per cent of the gross value of fisheries production. This was followed by salmonids ($323 million, 15 per cent), prawns ($289 million, 13 per cent), abalone ($188 million, 8 per cent) and tuna ($187 million, 8 per cent) (figure e).

Real value of Australianfisheries production, by key species

rock lobster

prawns

tuna

abalone

salmonids

Australian sardine

2008–09$m

c

100

200

300

400

500

600

700

800

2008

–09

2007

–08

2006

–07

2005

–06

2004

–05

2003

–04

2002

–03

2001

–02

2000

–01

1999

–200

0

Real unit prices for key species

abalone

rock lobster

tuna

2008–09$/kg

d

prawns

salmonids

10

20

30

40

50

60

70

2008

–09

2007

–08

2006

–07

2005

–06

2004

–05

2003

–04

2002

–03

2001

–02

2000

–01

1999

–200

0

4

Pro du c tio n

Value of Australian fisheries production, by producte

2008–09

2007–08

tuna salmonids

barramundisharks

prawnsrock lobster

crabsabalonescallops

edible oysterspearl oysters

$m 200100 300 400 500

box 1 Exchange rates and unit value

As a small producer and exporter of fisheries products, prices received by Australian producers are generally set on world markets in foreign currencies. Other things being equal, a depreciating Australian dollar results in producers receiving a higher export price in Australian dollar terms, while an appreciating Australian dollar results in a lower export price.

The strong appreciation of the Australian dollar between 2001 and 2008 simultaneously made exports less competitive and imports more attractive to domestic consumers. From 2001–02, the Australian dollar appreciated against the US dollar and the Japanese yen, causing Australian export prices to fall. From 2001–02 to 2007–08, the Australian dollar appreciated by 71 per cent against the US dollar and 50 per cent against the Japanese yen (figure f ). However, a depreciation of the Australian dollar against these currencies in 2009—24 per cent against the Japanese yen and 16 per cent against the US dollar—increased Australian export unit values in the 2008–09 financial year.

US dollar – Australian dollar and Japanese yen – Australian dollar exchange rates

US$/A$

¥/A$ (right axis)

f

0.00.10.20.30.40.50.60.70.80.91.0

2030405060708090100110120

2008–09

2007–08

2006–07

2005–06

2004–05

2003–04

2002–03

2001–02

2000–01

1999–2000

5

Pro du c tio n

Rock lobsterKey jurisdictions: Western Australia (wild catch (w)), South Australia (w) and Tasmania (w)In 2008–09, the value of rock lobster production decreased by 3 per cent ($11.8 million) to $403.8 million, following a 16 per cent decrease in the volume of rock lobster production. Rock lobsters are caught mainly in Western Australia, South Australia and Tasmania.

In 2008–09, rock lobster production decreased considerably by 2200 tonnes to 11 700 tonnes as a result of falling production volume in all states, with the exception of New South Wales. This decline was mainly attributable to the significant decreases in production in Western Australia and South Australia, which account for approximately 80 per cent of total Australian rock lobster production. Rock lobster production from these two states combined fell by 16 per cent (1900 tonnes) between 2007–08 and 2008–09.

Historically, western rock lobster accounted for a greater share (about two-thirds on average) of the total value of Australian rock lobster production. However, in recent years, the relative share of western rock lobster in value terms has declined compared with southern rock lobster. In 2008–09, the value of the two species was roughly equal mainly because of a 31 per cent increase in average unit value for southern rock lobster and a 15 per cent fall in western rock lobster catch. Between 2007–08 and 2008–09, Western rock lobster catch fell by 15 per cent (1400 tonnes). Accordingly, production of southern rock lobster and western rock lobster contributed $191.3 million and $191.6 million, respectively, to the total value of Australian rock lobster production.

The majority of rock lobster production is exported. Therefore, the beach price of rock lobster is highly dependent on the exchange rate between the Australian dollar and the US dollar. After falling considerably in 2007–08, rock lobster prices improved in 2008–09, increasing by 15 per cent following a 16 per cent depreciation of the Australian dollar against the US dollar (figure d). Most of the increase in prices occurred in Victoria, South Australia and Western Australia.

SalmonidsKey jurisdictions: Tasmania (aquaculture (a))Since the start of salmon farming in 1998, salmonids production has increased significantly, with most of this growth occurring from 2002–03 to 2006–07. Salmonids have become a key species of Australian fisheries production.

Over 95 per cent of Australia’s salmonids production occurs in Tasmania. The remainder of salmonids production occurs in New South Wales and Victoria. In 2008–09, Tasmania produced 28 700 tonnes of salmonids, while New South Wales and Victoria combined produced a total of 1000 tonnes.

The value of salmonids production rose by 7 per cent ($20.2 million) in 2008–09 to $322.6 million. This increase was mainly driven by a 4300 tonne increase in Tasmanian salmonids production, with Tasmania’s total production accounting for $315.6 million or 98 per cent of the total value.

6

Pro du c tio n

Tasmanian producers supply most of their salmonids to the domestic market. A key factor contributing to the rapid growth in recent years has been a strong focus on marketing salmon to Australian consumers. Additionally, the sector’s strong growth has been supported by research and development, which has allowed the sector to adopt improved feeding techniques and apply better disease control measures.

PrawnsKey jurisdictions: Queensland (w, a), Commonwealth Northern and Torres Strait prawn fisheries (w), Western Australia (w) and South Australia (w)In 2008–09, the gross value of Australian prawn production rose by 6 per cent ($17 million) to $289.3 million, following a 5 per cent increase in the volume of production to 23 900 tonnes. Driving this was a 29 per cent increase in the production volume of aquaculture prawns (mostly in Queensland) to 4000 tonnes, valued at $56.8 million. This value was $12.6 million higher than the previous year. Production of wild caught prawns was relatively stable, rising by 1 per cent to 20 000 tonnes. The value of wild caught prawn production rose by $4.3 million to $232.4 million.

Increases in aquaculture prawn production have largely offset decreases in wild caught prawn fisheries, particularly in the Commonwealth Northern Prawn Fishery (NPF) and the Torres Strait Prawn Fishery (TSPF). In 2008–09, prawn production in the NPF fell by 5 per cent (400 tonnes) to 6500 tonnes. In value terms, NPF production fell by 1 per cent ($0.6 million) to $73 million. Meanwhile, prawn production in the TSPF fell by 29 per cent (300 tonnes) to 700 tonnes, with the value of production decreasing by 38 per cent ($4 million) to $6.1 million.

AbaloneKey jurisdictions: Tasmania (w, a), Victoria (w, a) and South Australia (w, a)In 2008–09, the volume of abalone production increased by 5 per cent, from 5300 tonnes in 2007–08 to 5600 tonnes, with increases occurring in both wild catch and aquaculture production. In contrast, the value of abalone production stayed relatively constant, decreasing by $0.2 million to $188.4 million. This resulted from a $6 million decrease in the value of wild caught abalone being partially offset by a $5.7 million increase in the value of aquaculture production.

Most of the increase in abalone production occurred in Tasmania, which increased by 23 per cent in volume terms and accounted for 55 per cent of Australia’s total volume of abalone production in 2008–09.

A large proportion of abalone is exported, mostly to Hong Kong, China and Japan. Therefore, exchange rate movements have a significant effect on abalone export quantities, which in turn affect domestic and export prices. From 2000–01 to 2008–09, following the appreciation of the Australian dollar, abalone average unit prices fell by 45 per cent in real terms. As a result, the total value of production in real terms decreased by 46 per cent ($159.7 million) over the same period.

7

Pro du c tio n

TunaKey jurisdictions: South Australia (a) and Commonwealth Southern Bluefin Tuna Fishery and Eastern Tuna and Billfish Fishery (w)In 2008–09, the value of tuna production fell by 11 per cent ($22.9 million) to $187.1 million (excludes southern bluefin tuna wild catch input to the South Australian tuna farming sector) (figure g). This was the result of a 6 per cent decrease in production volume. The driver of the fall in production volume was a 10 per cent decrease in the volume of aquaculture southern bluefin tuna production, with the aquaculture sector producing 8800 tonnes in 2008–09. This was valued at $157.8 million, 16 per cent ($29 million) lower than in 2007–08.

The wild catch sector accounts for a smaller share of the total value of tuna production, making up 39 per cent of the total value in 2008–09. However, its value increased by 9 per cent ($6.2 million) in 2008–09 to $73.7 million. This was mainly the result of a 30 per cent increase in the production volume of yellowfin tuna which caused its production value to increase by 87 per cent ($6.7 million) to $14.3 million. The value of albacore tuna production also rose by $1.8 million, following a 44 per cent increase in prices and a 10 per cent increase in its production volume. These increases offset a decrease in the value of bigeye tuna production, which fell by $2.8 million to $8.5 million.

A large proportion of Australia’s tuna production is exported, mostly to the Japanese sashimi market. Therefore, prices are highly dependent on the exchange rate between the Australian dollar and the Japanese yen. A depreciation of the Australian dollar in 2008–09 resulted in higher prices for most tuna species.

Production by jurisdictionThe gross volume and value of Australian fisheries production by jurisdiction and location of catch is given in tables 3–6. Production and value summaries for each jurisdiction are given in tables 7–14.

In 2008–09, Tasmania had the largest gross value of production ($522.2 million), accounting for 23 per cent of total fisheries production, followed by South Australia ($465.5 million, 21 per cent) and Western Australia ($393.6 million, 17 per cent) (figure h).

By location of catch—where Commonwealth catch is distributed to the states according to where it was caught—Western Australia, Tasmania and South Australia accounted for 66 per cent of Australia’s gross value of production.

Real value of Australiantuna productiong

yellowfin

big eye

southern bluefin (Commonwealth)

southern bluefin (aquaculture)

100

200

300

400

500

2008–09$m

2008

–09

2007

–08

2006

–07

2005

–06

2004

–05

2003

–04

2002

–03

2001

–02

2000

–01

1999

–200

0

8

Pro du c tio n

In recent years, there has been a substantial shift in the contribution of individual state fishery production to total Australian fisheries production (figure i). Tasmania’s share of Australian fisheries gross value of production has increased significantly from 11 per cent in 1999–2000 to 23 per cent in 2008–09. South Australia’s share of the gross value of production has also increased considerably from 17 per cent to 21 per cent over this period. This reflects the strong growth in aquaculture production in these states during this time. In contrast, Western Australia’s share has declined from 31 per cent to 17 per cent over the same period, reflecting declines in both wild caught and aquaculture production. The share of Commonwealth fisheries production also fell from 17 per cent to 14 per cent in real value terms over the same period.

New South Wales table 7

Key species: oysters (a), prawn (w), sea mullet (w) and rock lobster (w)In 2008–09, the gross value of New South Wales fisheries production was $141.7 million, of which the wild catch sector accounted for $93 million or 66 per cent. The aquaculture sector, which was valued at $48.7 million, accounted for 34 per cent. Compared with 2007–08, the gross value of fisheries production rose by 4 per cent ($4.8 million) in 2008–09, following a 4 per cent increase in average unit values. In contrast, the total volume of fisheries production fell by 1 per cent (180 tonnes) to 21 000 tonnes in 2008–09.

Value of Australian fisheriesproduction, by jurisdiction,2008–09

h

$m

jurisdiction

location of catch

–

100

200

300

400

500

600

other

Commonwealth

NT

Tas

SA

WA

Qld

Vic

NSW

New South Wales 5 New South Wales 6

Victoria 4 Victoria 3

Queensland 12 Queensland 13

Western Australia 31 Western Australia 17

South Australia 17 South Australia 21

Tasmania 11 Tasmania 23

Northern Territory 4 Northern Territory 2

Commonwealth 17 Commonwealth 14

1999–2000 % %2008–09

Shares in gross value of production, by jurisdictioni

9

Pro du c tio n

In 2008–09, the New South Wales wild catch sector produced a total of 15 600 tonnes of seafood, which was a decrease of 2 per cent (370 tonnes) compared with 2007–08. Despite this decline, the value of wild catch production increased by 5 per cent ($4.2 million).

The most valuable wild caught species in New South Wales is prawns. On average, it has accounted for 20 per cent of the total value of wild catch production over the past five years. In 2008–09, the sector harvested about 1800 tonnes of prawns, worth a total of $19.6 million. A large proportion of the catch is typically made up of school prawns. This species accounted for 61 per cent (1100 tonnes) of the total volume of production of wild caught prawns in 2008–09 and king prawns accounted for 35 per cent (634 tonnes). Together, these two prawn species contributed a total of $18.6 million (20 per cent) of the total value of production of the wild catch sector.

The New South Wales wild catch sector also comprised a wide range of finfish species in 2008–09, including mullet (2000 tonnes, valued at $5.5 million), school whiting (1100 tonnes, $3.4 million), bream (259 tonnes, $3.1 million), snapper (289 tonnes, $3 million) and Australian salmon (1400 tonnes, $2.3 million). Declines in the volumes of production for these species resulted in the total volume of finfish production falling by 3 per cent (420 tonnes) to 12 700 tonnes in 2008–09. In contrast, the value of finfish production rose by 8 per cent ($3.9 million) to $51.6 million as a result of a 12 per cent increase in its average unit value.

The New South Wales aquaculture sector produced a total of 5400 tonnes of seafood in 2008–09, which represents an increase of 4 per cent (190 tonnes) compared with 2007–08. This increase was driven mainly by a 5 per cent (235 tonnes) increase in the volume of mollusc production to 4800 tonnes. Oyster production accounted for 99 per cent (4700 tonnes) of this tonnage and was valued at $40 million. Compared with 2007–08, the value of farmed oyster production rose by $1 million (3 per cent). The value of farmed mussels also increased, more than doubling to $0.3 million in 2008–09. The increases in the value of farmed oyster and mussel production partly offset a decline of $0.8 million in the total value of farmed fish and crustacean production. This resulted in the value of aquaculture production rising by 1 per cent ($0.6 million) to $48.7 million.

Other aquaculture species included prawns (164 tonnes, valued at $2.3 million), silver perch (180 tonnes, $1.9 million), barramundi (111 tonnes, $1.3 million) and salmonids (143 tonnes, $1.5 million). These species combined accounted for 11 per cent and 14 per cent of the total volume and value of New South Wales aquaculture production, respectively, in 2008–09.

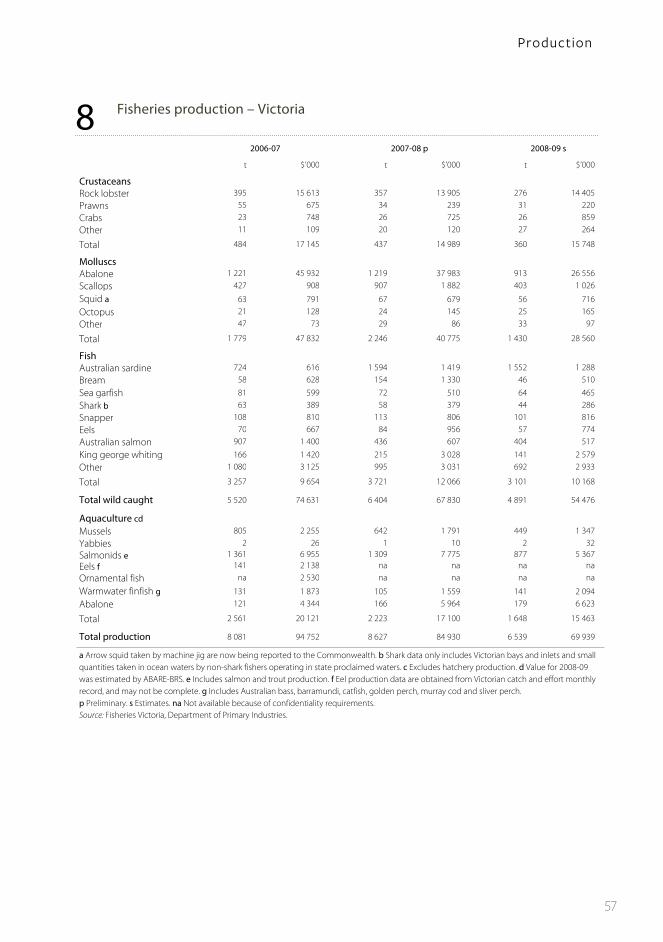

Victoria table 8

Key species: abalone (w), rock lobster (w) and trout (a)In 2008–09, the gross value of Victorian fisheries production was estimated at $69.9 million. The wild catch sector, which was valued at $54.5 million, accounted for 78 per cent of this total value. The aquaculture sector was valued at $15.5 million and accounted for 22 per cent. Compared with 2007–08, the gross value of fisheries production fell by 18 per cent ($15 million) in 2008–09, following a 24 per cent (2100 tonnes) decrease in the total volume of production to 6500 tonnes.

10

Pro du c tio n

Victorian wild catch production fell by 24 per cent (1500 tonnes) to 4900 tonnes in 2008–09. The decrease was mainly driven by decreases in the production volumes of scallops and wild caught abalone. Scallop production declined by 500 tonnes (56 per cent) to 400 tonnes in 2008–09. Wild caught abalone fell by 300 tonnes (25 per cent) to 910 tonnes. Lower total allowable catch settings for abalone and the outbreak of disease in wild abalone stocks in recent years contributed to this fall. A decline in the production of rock lobster (81 tonnes or 23 per cent) also contributed to the overall decline.

The falls in volume also resulted in a 20 per cent fall in the value of the Victorian wild catch sector. A key factor, once again, was wild caught abalone. Its value declined by $11.4 million (30 per cent) between 2007–08 and 2008–09 to $26.6 million. This decline was partly offset by a 4 per cent increase in the value of rock lobster to $14.4 million, which accounted for around 26 per cent of the total value of wild catch production in 2008–09. Other key species in the wild catch sector included King George whiting ($2.6 million, 5 per cent of wild catch production value), Australian sardine ($1.3 million, 2 per cent) and scallops ($1 million, 2 per cent).

The volume of aquaculture production in Victoria decreased by 26 per cent, from 2220 tonnes in 2007–08 to 1650 tonnes in 2008–09. This was largely driven by a 23 per cent decrease in salmonids production. In value terms, aquaculture production decreased by $1.6 million to $15.5 million, mainly the result of falls in the value of salmonids and mussels. The value of salmonids production fell by $1.4 million (20 per cent) to $5.4 million while the value of mussels fell by $0.4 million (25 per cent) to $1.3 million following a 30 per cent decrease in production volume. Contrasting these declines was farmed abalone, which increased in value by $0.7 million (11 per cent) to $6.6 million and in volume by 13 tonnes (8 per cent) to 179 tonnes.

Queensland table 9

Key species: prawns (w, a), coral trout (w), crabs (w) and barramundi (a) The gross value of Queensland fisheries production rose by 7 per cent ($18.9 million) in 2008–09 to $303 million. Wild catch production accounted for $219.2 million, or 72 per cent, of this value. The aquaculture sector made up the remaining $83.9 million, or 28 per cent. In volume terms, total fisheries production in Queensland rose by 5 per cent.

In 2008–09, the Queensland wild catch sector produced a total of 24 900 tonnes of seafood, which was an increase of 3 per cent (740 tonnes) compared with 2007–08. This increase was largely the result of an increase in the volume of prawn production. In 2008–09 the sector harvested about 6300 tonnes of prawns, accounting for 25 per cent of the total volume of Queensland’s wild catch production. This is about 1300 tonnes (25 per cent) more than the previous financial year, with most of the increase being attributed to tiger prawns. In value terms, this increase in prawn production translated to a 26 per cent or $15 million increase (to $72.9 million), with relatively stable unit prices.

Overall, Queensland’s wild catch production value also increased, by 5 per cent ($10.6 million) to $219.2 million. The increase in wild catch production was attributed to a 10 per cent increase

11

Pro du c tio n

in the production volume and value of barramundi and a 25 per cent increase in the value of Spanish mackerel catches, to $9.8 million in 2008–09. In contrast, the production value of coral trout, which accounted for 16 per cent of wild catch production, fell by 1 per cent to $35.2 million. The production value of lobster (mainly bugs) and scallops also fell considerably, by $4.2 million and $1.1 million, respectively, with falling production volumes and, in the case of lobster, prices. Together, lobster (mainly bugs) and scallops contributed $16.6 million (8 per cent) of the total production value of the Queensland wild catch sector.

Aquaculture production in Queensland rose by 15 per cent (850 tonnes) in 2008–09 to 6500 tonnes. In value terms, production increased by 11 per cent ($8.3 million) to $83.9 million, mainly because of a significant increase in production of prawns, Queensland’s most valuable aquaculture species. A 32 per cent increase in production volume in 2008–09 resulted in the value of aquaculture prawn production increasing by 31 per cent ($13 million) to $54.6 million, making up 65 per cent of the total value of aquaculture production in Queensland in 2008–09. Another key change was a 12 per cent ($2.9 million) decrease in the value of barramundi production from $24.3 million in 2007–08 to $21.4 million in 2008–09. Other key species produced in the Queensland aquaculture sector in 2008–09 included silver perch, jade perch, redclaw and oysters. Together, these species contributed $3.2 million (4 per cent) to the total value of Queensland’s aquaculture sector.

Western Australia table 10

Key species: rock lobster (w), pearls (a) and prawns (w)The gross value of Western Australian fisheries production was $393.6 million in 2008–09. Compared with 2007–08, this represents a fall of 13 per cent ($60.2 million). The total value of fisheries production in Western Australia included $293.4 million of wild catch production (75 per cent of the state’s total fisheries production value) and $100.2 million of aquaculture production (25 per cent), which includes pearl production. The total volume of fisheries production also fell by 13 per cent (3800 tonnes) to 26 300 tonnes.

In volume terms, wild catch production in Western Australia totalled 25 300 tonnes in 2008–09. This followed a decrease of 3800 tonnes or 13 per cent relative to 2007–08. A key component of this catch was approximately 7600 tonnes of rock lobster, 15 per cent (1400 tonnes) lower than the 9000 tonnes caught in 2007–08. Wild caught prawn production also fell, by 11 per cent (300 tonnes) to 2400 tonnes.

The fall in volume in wild catch production was also linked to a decline in value of 11 per cent ($37 million). This was mainly caused by decreases in the value of rock lobster, prawns and scallops as these species accounted for 78 per cent of the total value of Western Australian wild catch production in 2008–09. The value of rock lobster production fell by 12 per cent ($25.9 million) to $191.6 million. Wild caught prawn production fell by 9 per cent ($2.7 million) to $26 million. The value of scallop production fell by 30 per cent ($5.3 million) to $12.5 million given a 30 per cent (1500 tonnes) decrease in production volume. Together, the declines in these three key species resulted in a $34 million decline in value for Western Australian wild catch production between 2007–08 and 2008–09. Other notable changes included a

12

Pro du c tio n

7 per cent ($2.3 million) decrease in the value of finfish species production to $32.6 million in 2008–09. This decline can be predominantly attributed to decreases in the production value of pink snapper, emperor and West Australian dhufish.

Aquaculture production in Western Australia also declined in 2008–09 in value terms, falling by 19 per cent ($23.2 million) to $100.2 million. This fall was mainly the result of a $23 million decrease in the value of pearls, which is the most valuable aquaculture species produced in the state and contributed around 90 per cent ($90 million) of aquaculture production value in 2008–09. The edible seafood component of Western Australia’s aquaculture sector accounted for the remaining 10 per cent of its total aquaculture production value in 2008–09. It fell by $0.2 million between 2007–08 and 2008–09 to $10.2 million. In volume terms, the aquaculture sector produced a total of 1000 tonnes of edible seafood.

Decreases in the value of aquacultured crustaceans and molluscs were offset by an increase in the value of aquaculture fish production of $0.9 million to $5.4 million. Key edible aquaculture species produced in 2008–09 included barramundi (453 tonnes, valued at $4.8 million), mussels (433 tonnes, $1.6 million), marrons (57 tonnes, $1.6 million) and yabbies (40 tonnes, $0.7 million). These species combined accounted for around 97 per cent and 85 per cent of the total volume and value of edible aquaculture seafood production, respectively, in Western Australia in 2008–09.

South Australia table 11

Key species: southern bluefin tuna (a), rock lobster (w), prawns (w), abalone (w) and oysters (a)The gross value of fisheries production in South Australia fell by 1 per cent ($2.6 million) between 2007–08 and 2008–09 to $465.5 million. This occurred with a 3 per cent (2200 tonnes) decrease in production volume. The aquaculture sector accounted for the largest proportion of this value, making up $246.2 million or 53 per cent of the state’s total production value. Wild catch production was valued slightly lower, at $219.3 million, accounting for the remaining 47 per cent of the state’s total fisheries value.

Wild catch production in South Australia fell by 6 per cent (2600 tonnes) in volume terms to 38 200 tonnes. However, in value terms, wild catch production rose by 6 per cent ($13.3 million) between 2007–08 and 2008–09, following increases in the value of crustacean and finfish production by $11.4 million (9 per cent) and $1.8 million (5 per cent), respectively.

The most valuable wild caught species in South Australia is rock lobster. A 46 per cent increase in the average unit price of rock lobster between 2007–08 and 2008–09 resulted in the production value of this species increasing by 14 per cent ($13 million), despite a 22 per cent decline in the volume of rock lobster production. The species accounted for 48 per cent or $104.7 million of the total value of wild catch production in the state in 2008–09.

The increase in rock lobster value contrasts with decreases in the production value of prawns and abalone. These two species accounted for 29 per cent of total production value in the wild catch sector in 2008–09 following a $1.6 million (4 per cent) decrease for prawns and a

13

Pro du c tio n

$1 million (3 per cent) decrease for abalone, relative to 2007–08. These declines in production value were the result of decreases in the production volumes of each species.

Farmed production of southern bluefin tuna makes up the major share of the value of fisheries production in South Australia. The majority of southern bluefin tuna caught in Australia is by Commonwealth-endorsed vessels that catch fish in the Great Australian Bight and tow them to aquaculture farms off Port Lincoln in South Australia for fattening. Almost all of the farmed tuna is exported to Japan. In 2008–09, the value of farmed southern bluefin tuna production fell by 16 per cent ($29 million) to $157.8 million. This followed a 10 per cent decrease in volume and a 6 per cent decrease in the estimated average price paid for southern bluefin tuna. Despite this fall, southern bluefin tuna still accounted for 41 per cent and 64 per cent of South Australian aquaculture production and value, respectively. These declines in southern bluefin tuna production were the main cause of a 6 per cent ($16 million) fall in the total value of aquaculture production in South Australia in 2008–09.

Other key changes in South Australian aquaculture production in 2008–09 included increases in the value of oyster and abalone production, by $2.4 million (8 per cent) and $3 million (58 per cent), respectively. The value of other aquaculture products (mainly fish species) also increased by $14.5 million (52 per cent).

Tasmania table 12

Key species: salmonids (a), abalone (w) and rock lobster (w)In 2008–09, the gross value of Tasmanian fisheries production increased by 7 per cent ($35.2 million) relative to 2007–08, to $522 million. The total volume of production also rose by 13 per cent (4800 tonnes) to reach 40 800 tonnes in 2008–09. In value terms, the wild catch sector accounted for 34 per cent ($176 million) of the state’s total production and the aquaculture sector accounted for the remaining 66 per cent ($346 million).

In volume terms, Tasmania’s wild catch production increased by 5 per cent between 2007–08 and 2008–09 to 7200 tonnes. Wild catch production also rose in value, increasing by 7 per cent ($10.8 million) from $165.6 million in 2007–08 to $176.3 million in 2008–09, driven by increases in the values of production of wild caught abalone and rock lobster. Abalone generally contributes greater than 50 per cent of the total value of wild catch production. In 2008–09, the sector caught 2800 tonnes of abalone, accounting for 39 per cent of the total volume of Tasmanian wild catch production, and the value of abalone production rose by 7 per cent ($5.9 million) to $94.6 million. Rock lobster was the next most valuable wild caught species, accounting for 41 per cent ($72.2 million) of the total value of Tasmanian wild catch production in 2008–09. This followed a 9 per cent increase ($6.2 million) in value compared with 2007–08, given a 1 per cent decrease in catch and an 11 per cent increase in average unit prices. In 2008–09, abalone and rock lobster accounted for 95 per cent ($166.8 million) of the total value of production of the Tasmanian wild catch sector.

Tasmanian aquaculture production increased by 4500 tonnes between 2007–08 and 2008–09 to 33 500 tonnes. A large proportion of Tasmania’s aquaculture production consists of salmonids, which have accounted for, on average, 84 per cent of the total volume and 88 per cent of

14

Pro du c tio n

the total value of Tasmanian aquaculture production over the past 10 years. The volume of salmonids production rose considerably in 2008–09 by 17 per cent (4300 tonnes) to 28 700 tonnes. This was equivalent to 86 per cent of the total volume of aquaculture production in Tasmania. The value of salmonids production also rose, by 8 per cent ($22.5 million) to $315.6 million in 2008–09.

Another key Tasmanian aquaculture species is edible oysters. It accounted for around 11 per cent of the state’s aquaculture production volume in 2008–09 and contributed $19.3 million (6 per cent) towards Tasmania’s gross value of production. The remainder of Tasmania’s aquaculture production is composed of mussels (1100 tonnes, valued at $3.1 million) and abalone (230 tonnes, $7.9 million). These two species accounted for 3 per cent of Tasmania’s gross value of fisheries production in 2008–09.

Northern Territory table 13

Key species: gold band snapper (w), crabs (w), barramundi (w, a) and mackerel (w) Fisheries production in the Northern Territory was valued at $54.6 million in 2008–09 following a 2 per cent ($0.9 million) decrease compared with 2007–08. Wild catch production was valued at $33.7 million and accounted for 62 per cent of the Northern Territory’s total production value. The aquaculture sector was valued at $20.9 million and accounted for 38 per cent. Production volume decreased by 7 per cent between 2007–08 and 2008–09.

In 2008–09, the Northern Territory wild catch sector harvested a total of 5600 tonnes of seafood, 400 tonnes (7 per cent) lower than in 2007–08. In contrast, the value of wild catch production remained relatively stable, increasing by $0.8 million (2 per cent) to $33.7 million. This increase was mainly driven by a $3.7 million increase in the value of crab production to $10.2 million. This species accounted for 30 per cent of the total value of wild catch production in the Northern Territory in 2008–09. The increase in crab production value partly offset a decrease in the value of finfish species. Finfish species decreased in value by $2.8 million because of decreases in the volumes of production of gold band snapper and snapper and unit prices of barramundi and sharks. However, sea perch production increased from 9 tonnes in 2007–08 to 1100 tonnes in 2008–09, and from $36 000 in 2007–08 to $4.6 million in 2008–09.

The value of Northern Territory aquaculture production decreased by 7 per cent ($1.7 million) to $20.9 million in 2008–09. Farmed barramundi accounted for 20 per cent ($4.2 million) of this value.

Commonwealth table 14

Key species: prawns, tuna and sharksIn 2008–09, the gross value of production of Commonwealth-managed fisheries increased by 9 per cent ($25 million) to $314 million (figure j). This was despite a 2 per cent decrease in production volume because the average unit value of species caught in Commonwealth fisheries increased by 10 per cent. The reduction in production volume was attributed to decreases in catches in all major Commonwealth fisheries, with the exception of the Commonwealth Trawl Sector of the Southern and Eastern Scalefish and Shark (SESS) Fishery.

15

Pro du c tio n

Despite a slight decline in value, the Northern Prawn Fishery remains the most valuable Commonwealth-managed fishery. The fishery’s gross value of production declined by 1 per cent in 2008–09 to $74 million. This was the result of a 5 per cent fall in catch volume and a 5 per cent increase in average unit values. The fall in production volume was driven by declines in tiger and banana prawn

catches, the two key species in the fishery. The increase in average unit values was driven mainly by a 27 per cent increase in tiger prawn prices, but increases for endeavour prawns (13 per cent) and king prawns (6 per cent) were also a factor. Banana prawn prices remained relatively stable, declining by 1 per cent.

The Commonwealth Trawl Sector of the SESS fishery is the second most valuable Commonwealth-managed fishery. In 2008–09, the sector was valued at $56 million, which was a $9.5 million (21 per cent) increase from 2007–08. This increase was a result of a 19 per cent increase in average unit values and a 2 per cent increase in the volume of production. The volume of production of blue grenadier, tiger flathead and silver warehou continues to dominate production in this sector, accounting for 54 per cent of production volume in

2008–09. These species contributed $30.3 million or 54 per cent of the sector’s total value in 2008–09.

The third most valuable Commonwealth fishery is the Southern Bluefin Tuna Fishery. A 5 per cent increase in the average unit value of tuna caught in the sector was partly a result of a depreciation in the Australian dollar against the Japanese yen in 2008–09. Combined with a 3 per cent decrease in production volume, the fishery’s gross value increased by 2 per cent in 2008–09.

The Bass Strait Central Zone Scallop Fishery reopened in June 2009 after three years of closure following the 2006 ministerial direction to the Australian Fisheries Management Authority to protect Commonwealth fish stocks. The total allowable catch for the 2009 fishing season was set at 2500 tonnes, with fishing occurring in part of the fishery’s area. In June 2009, a total of 594 tonnes was caught, valued at $1.2 million. The remainder of the quota is expected to be filled in the 2009–10 financial year.

Prawns, which were valued at $79 million, remained the most valuable species caught in Commonwealth-

Top five Commonwealth fisheries, by value

Northern Prawn Fishery $74 million

SESS Commonwealth Trawl Sector $56 million

Southern Bluefin Tuna Fishery $45 million

Eastern Tuna and Billfish Fishery $39 million

SESS Gillnet, Hook and Trap sectors $31 million

Real gross value of Commonwealth fisheries production, by species

j

other crustaceans and molluscs

other fish

sharks

prawns

tuna

2008

–09

2007

–08

2006

–07

2005

–06

2004

–05

2003

–04

2002

–03

2001

–02

2000

–01

1999

–200

0

2008–09$m

100

200

400

300

500

600

16

Pro du c tio n

managed fisheries in 2008–09, followed by tuna ($74 million) and sharks ($25 million). Together these species accounted for a total of 57 per cent of the gross value of Commonwealth fisheries production in 2008–09. Other valuable species included flathead ($17.5 million), blue grenadier ($14.8 million), broadbill swordfish ($8.5 million) and ling ($7.8 million). Together, these species accounted for 15 per cent of the Commonwealth fisheries gross value of production.

Production by sectorThe gross volume and value of Australian production, by sector, is given in table 1. Production and value summaries for each sector are given in table 2 (wild catch sector) and tables 15–17 (aquaculture sector).

In 2008–09, the total volume of Australian fisheries production was relatively stable falling by 1 per cent (2800 tonnes) to 238 000 tonnes. This slight fall was caused by lower production in the wild catch sector, where production declined by 5 per cent (8500 tonnes), being partly offset by an increase in production of 8 per cent (5400 tonnes) in the aquaculture sector.

The gross value of Australian fisheries production also remained stable in 2008–09 at $2.2 billion. The gross value of wild catch production rose by 1 per cent to $1.4 billion, while the gross value of aquaculture production fell by 1 per cent to $861 million.

From 1999–2000 to 2008–09, the value of state wild catch production decreased by $691.6 million (39 per cent) in real terms (figure k). The value of aquaculture production decreased to a lesser extent, by $55.4 million (6 per cent), over the same period. The value of Commonwealth fisheries production also declined, by $222.2 million (41 per cent) from $536 million in 1999–2000 to $313.8 million in 2008–09.

Wild catch table 2

Key species: prawns, rock lobster, tuna and abaloneIn 2008–09, the total production volume of the wild catch sector declined by 8500 tonnes (5 per cent) to 173 000 tonnes. Declines in production volumes occurred across all three key species groups: production of fish species declined by 2 per cent, crustaceans by 6 per cent and molluscs by 16 per cent.

Despite a lower production volume, the gross value of wild catch production increased by 1 per cent

Real value of Australian fisheries production, by sector a

k

state wild catch

Commonwealth wild catch

aquaculture

2008

–09

2007

–08

2006

–07

2005

–06

2004

–05

2003

–04

2002

–03

2001

–02

2000

–01

1999

–200

0

2008–09$b

1.0

1.5

0.5

2.5

2.0

3.0

3.5

a Aquaculture total has been adjusted to exclude southern bluefin tuna caught in the Commonwealth Southern Bluefin Tuna Fishery, which is input to farms in South Australia. This avoids double counting.

17

Pro du c tio n

($14.2 million) to $1.4 billion in 2008–09, driven by a 6 per cent increase in the average unit value for product landed by the sector (figure l).

The value of finfish production increased by 7 per cent ($29 million) to $469.6 million following a 9 per cent increase in average unit values. Price increases for high-valued species such as tuna and coral trout were a key driver behind the increase in average unit value.

The value of mollusc production fell by $13.4 million (6 per cent) to $221.1 million between 2007–08 and 2008–09. Falls in the value of wild caught scallops and abalone were key drivers. The value of abalone production fell by $6 million (3 per cent) to $165.7 million as a result of a 6 per cent decrease in its average unit value. The value of scallop production fell by $8 million (24 per cent) because of a 27 per cent decrease in catch volume.

The value of crustacean production remained relatively stable in 2008–09, falling only marginally by $1.1 million to $710.9 million. Rock lobster production accounted for the major share of the total value of wild caught crustacean production in 2008–09, comprising 57 per

cent. The production volume of this species decreased by 16 per cent (2200 tonnes) to 11 700 tonnes in 2008–09 but the value decreased by only 3 per cent ($11.8 million) to $403.8 million, because of a 15 per cent increase in average unit prices for rock lobster.

Since 1999–2000, the gross value of wild catch production decreased considerably, by 39 per cent ($913.8 million) in real terms. Falls occurred across all major wild caught species over this period. The largest declines occurred for prawns (52 per cent), tuna (49 per cent), rock lobster (45 per cent) and abalone (43 per cent), and were the combined result of declines in unit prices and production volumes.

Real value of Australian wild catch productionl

other

other finfish

rock lobster

prawns

abalone

tuna

2008

–09

2007

–08

2006

–07

2005

–06

2004

–05

2003

–04

2002

–03

2001

–02

2000

–01

1999

–200

0

2008–09$b

1.0

0.5

1.5

2.0

2.5

18

Aquaculture tables 15–17

Key species: prawns, oyster, tuna, salmonidsThe gross value of aquaculture production fell by 1 per cent ($9.1 million) to $861.1 million in 2008–09 (figure m). Considerable decreases in the values of farmed tuna ($29 million or 16 per cent), farmed barramundi ($2.4 million or 7 per cent) and pearl oyster ($24.3 million or 21 per cent) contributed to this decline.

Farmed tuna production consists solely of farmed southern bluefin tuna from South Australia and accounted for 18 per cent of the total value of Australian aquaculture production in 2008–09. The value of farmed tuna production fell by $29 million (16 per cent) between 2007–08 and 2008–09 to $157.8 million because of a 10 per cent fall in production (to 8800 tonnes) and a 6 per cent decline in average unit prices.

The production value of farmed salmonids increased by $20.2 million (7 per cent) between 2007–08 and 2008–09, to $322.6 million. The increase in salmonid value was driven by a 15 per cent (3800 tonnes) increase in production volume. The recent emergence of farmed salmonids as a key species follows several years of rapid growth in Tasmania. Compared with 2003–04, the real value of farmed salmonids production has increased by 98 per cent or $160 million. As a result of this growth, the state’s salmonids production now accounts for more than 95 per cent of Australian salmonids production in both value and volume. It also comprised 37 per cent of the total value of Australian aquaculture production in 2008–09.

Farmed prawns accounted for 7 per cent of the total value of Australian aquaculture production in 2008–09. This species also increased in value by $12.6 million (29 per cent) between 2007–08 and 2008–09 because of a 29 per cent increase in production volume. Most of the increase in farmed prawn production in 2008–09 occurred in Queensland where the volume of farmed prawn production increased by 32 per cent to 3800 tonnes.

Since 1999–2000, the gross value of aquaculture production has declined by 6 per cent ($55.4 million) in real terms, predominantly because of a $164 million decrease in the real value of pearl oyster production. Declines in the value of tuna ($111.8 million) and prawn ($11.6 million) aquaculture production between 1999–2000 and 2008–09 were also key factors. These latter declines in value were driven by declines in unit prices.

Real value of Australian aquaculture productionm

other

pearl oysters

edible oysters

salmonids

tuna

prawns

2008

–09

2007

–08

2006

–07

2005

–06

2004

–05

2003

–04

2002

–03

2001

–02

2000

–01

1999

–200

0

2008–09$m

200

400

600

1000

800

Pro du c tio n

19

Trade Fast facts

ExportsIn 2008–09 • The total value of Australian fisheries exports (edible and non-edible) increased by 14 per

cent ($187.7 million) to $1.5 billion, driven by increases in the export values of both edible and non-edible fisheries products.

• Approximately 75 per cent of export value was derived from edible fishery products such as fish and shellfish. The remainder was comprised of non-edible products, predominantly pearls.

Since 2004–05• The real value of Australian fisheries exports has fallen by 12 per cent ($216.7 million).• The real value of edible fisheries exports has fallen by 18 per cent ($254.5 million), driven by

$10.7 million and $243.8 million declines in the real value of edible fish exports and edible crustacean and mollusc exports, respectively.

• The real value of non-edible fisheries exports has increased by 11 per cent ($37.8 million) with a $36.9 million increase in the real value of pearl exports.

ImportsIn 2008–09 • The total value of Australian imports of fisheries products (edible and non-edible) increased

by 22 per cent ($311.9 million) to $1.7 billion, driven by increases in the import values of both edible and non-edible fisheries products.

• Approximately 75 per cent of import value consisted of edible fishery products. The remainder was comprised of non-edible products, predominantly pearls and fish meal.

Top five exports, by value in 2008–09 (edible and non-edible—tables 18 and 19)

Rock lobster $462 million

Pearls $366 million

Abalone $208 million

Tuna $177 million

Prawns $82 million

Top five export destinations in 2008–09 (edible and non-edible—tables 24 and 25)

Hong Kong, China $726 million

Japan $367 million

United States $87 million

Chinese Taipei $54 million

Singapore $45 million

20

Tr a d e

Since 2004–05• The real value of Australian fisheries imports has increased by 29 per cent ($382.4 million). • The real value of edible fisheries imports has increased by 18 per cent ($196.2 million), driven

by a $204.8 million increase in the real value of edible fish imports.• The real value of non-edible fisheries imports has increased by 77 per cent ($186.1 million),

largely driven by a $155.4 million increase in the real value of pearl imports.

Exports and importsHistorically, Australia has been a net importer of fisheries products in volume terms but a net exporter in value terms. This disparity reflects the composition of Australian fisheries exports compared with imports. Australian fisheries exports are dominated by high value species such as rock lobster, tuna and abalone, while imports largely consist of lower value product such as frozen fish fillets, canned fish and frozen prawns. In recent years, the gap between imports and exports in value terms has closed and in 2007–08 Australia became a net importer of fisheries products in value terms for the first time (figure n). In 2008–09, this trend continued, and Australian imports of fisheries products grew by $311.9 million (22 per cent) while exports of fisheries products also increased but by a lesser amount ($187.7 million or 14 per cent).

In 2008–09, the total value of Australian exports of fisheries products was $1.5 billion. About 75 per cent of this value was derived from exports of edible fisheries products, such as fish, crustaceans and molluscs, which were valued at $1.1 billion. Exports of non-edible fisheries products, such as pearls, fish meals and marine fats and oils, accounted for the remaining 25 per cent ($384 million) of this value.

In real terms, the value of Australian fisheries exports has fallen by 42 per cent ($1.1 billion) since 1999–2000 (figure n). The main factors contributing to this decline were a 27 per cent decrease in the volume of edible exports and falling unit prices for major export species, particularly rock lobster, prawns, tuna and abalone. The decline in unit export prices is the result, in part, of an appreciation in the Australian dollar against both the Japanese yen and US dollar over this period.

In 2008–09, the total value of Australian fisheries imports was $1.7 billion. Since 1999–2000, the value of Australian fisheries imports, in real terms, has risen by 17 per cent ($253.9 million)

Top five imports, by value in 2008–09 (edible and non-edible—table 29)

Canned fish $331 million

Pearls $321 million

Frozen fish fillets $239 million

Canned crustaceans and molluscs $185 million

Fresh, chilled or frozen prawns $135 million

Top five import sources in 2008–09 (edible and non-edible—tables 37 and 38)

Thailand $370 million

New Zealand $218 million

Vietnam $168 million

China $156 million

United States $68 million

21

Tr a d e

(figure n). The main factor contributing to this increase was a 38 per cent increase in the quantity of edible imports (excluding live products), largely reflecting a 35 000 tonne increase in the volume of both canned fish products and canned crustacean and mollusc products.

Exports by commodityThe total export value of fisheries products (edible and non-edible) rose by 14 per cent ($187.7 million) in 2008–09 to $1.5 billion (figure o). This was driven by an 8 per cent ($79.9 million) and 39 per cent ($107.7 million) increase in the value of edible exports and non-edible exports, respectively. The increase in the value of edible exports was driven mainly by a 10 per cent ($70.7 million) increase in the export value of crustaceans and molluscs—predominantly caused by increases in the export values of rock lobsters and prawns—and a 3 per cent ($9.2 million) increase in the export value of fish products. The increase in the value of non-edible exports was because of a 39 per cent ($102.4 million) increase in the export value of pearls.

Rock lobster remained the most valuable export species by value in 2008–09 at $461.7 million, followed by pearls ($366.4 million), abalone ($208.2 million), tuna ($176.8 million) and prawns ($82.2 million) (figure p). These species together accounted for 85 per cent of the Australian total export value of fisheries products in 2008–09.

Edible fisheries productsKey products: rock lobster, abalone, tuna and prawns

Finfish The total export volume of finfish products increased by 15 per cent (3300 tonnes) in 2008–09 to 25 700 tonnes. This followed a 177 per cent increase in whole salmon

product exports, which accounted for 24 per cent of the total export volume of finfish products. In value terms, exports of finfish products rose by a lesser amount of 3 per cent in 2008–09 to $334 million. The smaller increase in value terms was because much of the increase in volume terms came from an increase in the volume of salmon exports, a relatively lower valued finfish product, and there was a decline in the volume of high-valued tuna exports.

Real value of Australian fisheriesexports and imports n

3.0

2.0

2.5

1.5

1.0

0.52008–09

$b

exports

imports

2004

–05

2006

–07

2007

–08

2008

–09

2005

–06

2003

–04

–

2002

–03

2001

–02

2000

–01

1999

–200

0

Real value of Australian fisheries exportso

non-edible

crustaceans and molluscs

fish

2008

–09

2007

–08

2006

–07

2005

–06

2004

–05

2003

–04

2002

–03

2001

–02

2000

–01

1999

–200

0

2008–09$b

1.0

0.5

1.5

2.0

3.0

2.5

22

Tr a d e

Tuna exports (including canned) dominated edible finfish exports, accounting for 53 per cent ($176.8 million) in value terms. Relative to 2007–08, tuna exports fell by 8 per cent (1100 tonnes) in volume terms and 14 per cent ($29.4 million) in value terms in 2008–09. Falls in the export value (29 per cent) and volume (18 per cent) of whole frozen tuna were the main cause of these decreases.

Salmon exports (including canned) accounted for a relatively smaller share of the value of edible finfish exports—13 per cent or $44.1 million. In volume terms, salmon exports account for 25 per cent of edible finfish exports or 6300 tonnes. Exports of salmon products increased significantly in 2008–09, by 128 per cent (3500 tonnes) in volume terms and 126 per cent ($24.6 million) in value terms. The major cause of this increase was a 164 per cent ($25.8 million) rise in the export of fresh or chilled whole salmon, which accounted for 94 per cent of total salmon exports by value in 2008–09.

Exports of other finfish products also increased considerably in 2008–09, rising by $14 million to $113 million, following increases in the export values of live fish and fresh or chilled whole fish (excluding tuna and salmon). The export value of live fish rose by 9 per cent ($3.7 million) to $46.5 million in 2008–09. The export value of fresh or chilled whole fish (excluding tuna and salmon) also increased, by $9 million to reach $21 million in 2008–09. In total, exports of other finfish products accounted for 34 per cent ($113 million) of total edible finfish exports.

Crustaceans and molluscs

In 2008–09, exports of crustaceans and molluscs fell by 2 per cent (390 tonnes) in volume terms. At the same time, the total value of crustacean and mollusc exports rose by 10 per cent ($70.7 million). Crustacean and mollusc exports accounted for 45 per cent and 71 per cent of edible export volume and value, respectively.

The major crustacean and mollusc exports are rock lobsters, prawns, crabs, abalone and scallops. Rock lobster exports accounted for 57 per cent of the total export value of

Value of Australian fisheries exports, by key speciesp

2008–09

2007–08

rock lobster

prawns

abalone

scallops

pearls

tuna

$m 200100 300 400 500

23

Tr a d e

crustaceans and molluscs in 2008–09. Compared with 2007–08, the export value of rock lobsters rose by 15 per cent ($60.8 million) to $461.7 million, strongly driven by a 14 per cent increase in the average export price received for rock lobster. Abalone exports accounted for 26 per cent of the total value of crustacean and mollusc exports. The value of these exports fell by 4 per cent ($9 million) to $208.2 million in 2008–09, largely because of a 7 per cent decrease in its export volume. The value of prawn exports increased significantly in 2008–09, by 20 per cent ($13.6 million) to $82.2 million. This is linked to an increase of 23 per cent in average unit prices for exported prawns between 2007–08 and 2008–09. The total export value of crabs and scallops rose by $6.1 million, also resulting from increases in the unit export value. These two commodities contributed a total of $49.6 million (6 per cent) of the total value of crustacean and mollusc exports.

Non-edible fisheries productsKey products: pearlsThe value of non-edible fisheries product exports rose by 39 per cent ($107.7 million) to $384 million in 2008–09. This increase was largely attributable to a $102.4 million increase in the value of pearl exports. Pearl exports were valued at $366.4 million and were the most valuable non-edible export product, accounting for 95 per cent of the total non-edible export value and 24 per cent of total exports of fisheries products in 2008–09. The remaining 5 per cent of the total export value of non-edible fisheries products included marine fats and oils, fish meal, ornamental fish and other non-edible products.

Exports by destination

Edible fisheries productsMain destinations: Hong Kong, JapanIn 2008–09, Australia’s major seafood export destinations were Hong Kong ($525.3 million), Japan ($302.3 million), the United States ($64.4 million), Chinese Taipei ($53.7 million) and Singapore ($43.7 million) (figure q), which together accounted for 90 per cent of the total value of Australian seafood exports in 2008–09.

Most finfish products were exported to Japan (mainly tuna and salmon), New Zealand (canned fish), Thailand (whiting) and China (whiting). Hong Kong and Japan remained the primary markets for Australia’s exports of crustaceans and molluscs.

In 2008–09, Hong Kong remained Australia’s major export destination for edible fisheries products, accounting for 48 per cent of the total export value of edible fisheries products. Rock lobster and abalone were the main export species, accounting for 61 per cent and 26 per cent of the total value of exports to Hong Kong, respectively. In 2008–09, the export value of rock lobsters increased by 38 per cent ($87.7 million) to $320.4 million; while exports of abalone fell by 3 per cent ($3.7 million) to $135.6 million. Exports of scallops, dried, salted or smoked fish, crabs and prawns accounted for most of the remainder of total edible fish product exports to Hong Kong.

24

Tr a d e

Japan accounted for 28 per cent of the total export value of edible fisheries products in 2008–09. The main edible fisheries products exported were tuna (whole), rock lobster, abalone and prawns, accounting for 92 per cent of the total value of edible exports to Japan. Whole tuna was the most important export species, contributing more than half or $168.4 million of the total export value. Japan is one of Australia’s most important whole tuna export markets and accounted for 96 per cent of Australian exports of whole tuna in value terms.

Other important export destinations in 2008–09 included the United States, Chinese Taipei, Singapore and China. Chinese Taipei and the United States are important export markets for rock lobster and accounted for 12 per cent and 8 per cent, respectively, of the volume of Australia’s rock lobster exports in 2008–09. Singapore and China are key export markets for abalone, with 10 per cent and 16 per cent of the volume of Australian abalone exports in 2008–09, respectively. China also accounted for 13 per cent of the volume of Australian crab exports in the same year.

Non-edible fisheries productsMain destinations: Hong Kong, Japan, United StatesThe key export destinations for Australian non-edible fisheries products in value terms in 2008–09 were Hong Kong ($201 million), Japan ($64.3 million) and the United States ($22.2 million). Together, these countries comprised 75 per cent of non-edible fisheries product exports in value terms. The major product exported to these markets was pearls, accounting for 100 per cent, 98 per cent and 83 per cent of non-edible exports to Hong Kong, Japan and the United States, respectively.

Exports by stateIn 2008–09, South Australia remained the major exporter of edible fisheries products, valued at $330.5 million, followed by Western Australia ($302.2 million), Tasmania ($188.3 million) and Queensland ($179.2 million). Together, these states accounted for 87 per cent of the total value of edible exports. The remaining 13 per cent came from Victoria ($96.1 million), New South Wales ($29.5 million) and the Northern Territory ($0.3 million).

In 2008–09, South Australia exported $169.5 million of fresh, chilled or frozen whole fish, with exports of southern bluefin tuna contributing 93 per cent ($157.5 million) of this value. South Australia also exported a significant amount of rock lobsters in the same year, valued at $113.8 million. Western Australian exports of rock lobster accounted for 54 per cent ($250.8 million) of Australia’s total rock lobster export value in 2008–09. The major export products for Tasmania in 2008–09 were abalone

Australian exports of edible fisheries products (excluding live), by destination

q

800

400

200

600

2008–09$m

1000

JapanHong KongChinese TaipeiUnited StatesSingaporeChina

2004

–05

2006

–07

2007

–08

2008

–09

2005

–06

2003

–04

2002

–03

2001

–02

2000

–01

1999

–200

0

25

Tr a d e

($94.7 million), fresh, chilled or frozen whole fish ($44.9 million) and rock lobster ($44.8 million). For Queensland, the key edible export products were prawns and live fish, together valued at $90 million.

Non-edible exports, predominantly pearls, were dominated by exports from the Northern Territory, which accounted for 62 per cent ($238.6 million) in value terms, and Western Australia, which accounted for 19 per cent ($74.8 million).

Imports by commodityThe total value of Australian fisheries imports rose by 22 per cent ($311.9 million) in 2008–09 to $1.7 billion. Approximately 75 per cent of this value consisted of edible products (valued at

$1.3 billion). Edible imported products in 2008–09 included $824.6 million of finfish (64 per cent of total edible imports) and $458.1 million of crustaceans and molluscs (36 per cent). Non-edible products made up the remaining 25 per cent ($427 million) of imports in value terms and included pearls, fish meal and marine fats and oils (figure r).