australian pharmaceutical industries limited - · pdf fileaustralian pharmaceutical industries...

TRANSCRIPT

Australian Pharmaceutical Industries Limited

for the year ended 31 August 2015

ANNUAL REPORT 2015

Australian Pharmaceutical Industries Limited Annual Report 2015

API IS ONE OF THE LEADING SERVICE PROVIDERS TO THE PHARMACY INDUSTRY IN AUSTRALIA

The Directors present their report together with the financial report of Australian Pharmaceutical Industries Limited (‘the Company’) and of the consolidated entity, being the Company and its controlled entities, for the year ended 31 August 2015 and the Auditor’s report thereon.

Contents1 Chairman’s and CEO’s Report6 Priceline Sisterhood Foundation8 Directors’ Report29 Lead Auditor’s Independence

Declaration30 Income Statement31 Statement of Comprehensive

Income32 Statement of Financial Position33 Statement of Cash Flows34 Statement of Changes in Equity35 Notes to the Financial

Statements79 Directors’ Declaration80 Independent Auditor’s Report 82 Shareholder Information85 Corporate Directory

Our VisionEnriching life as the most inspirational choice for health, beauty & well being

1. This statement should be read in conjunction with the underlying earnings reconciliation included in the Appendix 4E and full year results presentations lodged with the ASX.

We are pleased to present to shareholders the Company’s annual report for the financial year ended 31 August 2015.

During the past year the Company has continued to successfully execute its operational strategy which has improved returns for shareholders. The continued growth of the Priceline Pharmacy network, sustained performance from Pharmacy Distribution and an improved contribution from New Zealand operations were the key drivers behind the financial results.

The financial highlights for the 2015 financial year included:

– Net profit after tax of $43.1 million, up 37.6% on the underlying1 NPAT for the prior year;

– Earnings before interest and tax was $74 million, an increase of 13.7% on the 2014 underlying1 EBIT;

– Return on capital employed up to 13.5% from 11.9% in 2014;

– Cash generated from operations was up $11.9 million on the prior year to $101.8 million;

– Net debt reduced to $70.8 million, a $28.4 million reduction on the prior year; and

– Fully franked dividends paid to shareholders were up 28.6% for the year to 4.5 cents per share.

The Company’s ability to achieve these results given the challenging retail and pharmacy environment is a testament to the strategic positioning the business now has. The strategy of generating growth through the expansion of Priceline Pharmacy along with sustainable earnings and cashflow from Pharmacy Distribution remains relevant and in place for the foreseeable future.

Competition in the broader retail market has remained intense, with consumer sentiment mixed during the period. New entrants into the domestic health and beauty retail market added to the competitive nature of the operating environment. These factors heightened the need to remain relevant and closely connected with customers to remain top of mind as a shopping destination.

Regulatory reforms through the Pharmaceutical Benefits Scheme (PBS) continued the price deflation on pharmaceuticals, however during the year the Sixth Community Pharmacy Agreement (6th CPA) was signed by the Pharmacy Guild and the Australian Government.

CHAIRMAN’S & CEO’S REPORT

Peter R Robinson Chairman (left)

Stephen P Roche Managing Director and Chief Executive Officer (right)

37.6%

API Underlying1

NPAT

Annual Report 2015 Australian Pharmaceutical Industries Limited

1

2

Australian Pharmaceutical Industries Limited Annual Report 2015

CHAIRMAN’S & CEO’S REPORTCONTINUED

This provided the sector with more confidence and remuneration certainty through until 2020. As part of the 6th CPA, the Community Service Obligation payments to pharmaceutical wholesalers were also continued however there has been no increase nor indexation applied to these payments. This means that as price deflation continues through the supply chain, and volumes continue to increase, wholesalers such as API will be required to look at ongoing reductions in trading terms to manage operational margins. In addition further changes to our distribution model may be required to maintain our strategic position during the course of the 6th CPA.

Operational performancePriceline Pharmacy continued its sales momentum from 2014 recording excellent comparable store sales that were up 4.5% on the prior year, total sales up 10.4% and an increase in transactions by 7.7%. This growth was achieved without compromising profitability in stores with margins maintained in line with the prior year. Franchise partners continued to find the brand an attractive and sustainable proposition with store numbers increasing by 30 to 420 in total.

The Sister Club loyalty program grew by 900,000 members to 5.6 million, entrenched as the largest health and beauty loyalty program in Australia and one of the largest programs across all industries. Customers engaged with the brand across all forms of media with online store visitations up to 10 million page views per month and social media followers at record numbers.

The brand continued to record excellent market growth in its key categories; colour cosmetics grew at 12.6%, skincare at 21.9%, medicinal health at 23.6% and vitamins at 17.8%. These categories are the heartland for Priceline Pharmacy and a focus on new launches, exclusive products, range extensions and great value ensured customer satisfaction.

The presence of the brand was amplified through broader marketing initiatives which in 2015 included; taking the naming rights for the Priceline Pharmacy Kooyong Classic, becoming the principal sponsors for the Adelaide Thunderbirds netball team, and sponsoring the Melbourne Fashion Festival. New TV brand advertising, continued disruptive marketing tactical campaigns and promoting innovative services from pharmacists and beauty advisors kept awareness and consideration of the brand consistently high among our target audience.

13.7%

API Underlying1

EBIT

22.0%

Net Financing

Costs

Annual Report 2015 Australian Pharmaceutical Industries Limited

3

The brand was again recognised by peak industry organisations; claiming the runner up position in the Australian Retailers’ Association Retailer of the Year Award, complementing the win from 2014. This year Priceline Pharmacy was also recognised as a finalist in the Franchise Council of Australia’s Franchisor of the Year Awards.

In Pharmacy Distribution sales growth excluding the impact of the PBS reforms was 6.5%, and in line with the prior year. Gross profit was also held steady in the business through the prudent management of trading terms. There were considerable challenges when major customer groups were acquired by competitors at the commencement of the financial year. Management held many of these accounts and also acquired new business that largely offset the losses from the major groups.

The new business primarily came from independent non-branded pharmacies, which were attracted to API with the range of services offered by the Company. The Club Premium program offers a selection of retail services and it grew by more than 60 pharmacies to 750 during 2015. Combined with the Pharmacist Advice and Soul Pattinson brands and the ongoing generic pharmacy alliance with Alphapharm it provides API-aligned pharmacies with scope for choices that will best suit their local environment.

In the New Zealand operations a restructure in 2014 resulted in a markedly improved performance in 2015 with segment earnings before interest and tax up from $970,000 to $2.84 million. The results were attributable to improved cost management and increased sales from its core product range. It made an important contribution to the Australian business through the provision of private label and exclusive products and is expected to continue to do so in future years.

Group summaryAPI was able to manage its cost base efficiently with our cost of doing business marginally improved from 2014. A major contributor was the supply chain function where we continued to extract efficiencies and reduced overall costs while increasing units delivered for the second year in a row.

The Company has implemented a number of measures to improve its safety for staff and customers, and while further improvement is required we have been pleased with major changes in areas such as the distribution centres where the lost time injury frequency rate dropped by 46% this year.

CHAIRMAN’S & CEO’S REPORTCONTINUED

28.6%

Dividends

4

Australian Pharmaceutical Industries Limited Annual Report 2015

The strong operational performance has enabled the company to improve its financial position with average net debt falling by 21.2% in 2015.

Lower average net debt, lower financing costs, improved cash generation and improved earnings has led to improved returns for shareholders. Since the 2013 financial year, return on equity has grown from 4.09% to 8.62% and return on capital employed has risen from 8.34% to 13.45%.

The Company achieved these results while it implemented an enterprise-wide reporting system as part of our oneERP project. This $45 million investment will deliver approximately $7 million in savings in each financial year. Management was able to implement this project without any material disruption to business performance. We are confident that it will prove to be a successful long term initiative for API to make the Company more efficient and competitive.

This completes a substantial period of investment for the Company which has included upgrading the supply chain and distribution centres and also investing in the repositioning of Priceline Pharmacy. The business is already demonstrating that these investments are delivering benefits to shareholders and management focus will be on extracting further upside.

Corporate Social ResponsibilityThe Company’s Corporate Social Responsibility program, the Priceline Sisterhood Foundation has been able to continue the support of five key charities during the year; Alzheimer’s Australia, Australian Cervical Cancer Foundation, Look Good Feel Better, Children First Foundation, and Perinatal Anxiety and Depression Association. These charities cover some of the primary health concerns of women such as mental health and cancer.

2015 was the first full year of operation as an independent foundation and the Company was able to make the most contributions to the Priceline Sisterhood Foundation since the program commenced. At the end of August 2015 the company had raised $1.4 million, thanks to the efforts of staff, Priceline and Priceline Pharmacy stores, suppliers and consumers.

Since the end of the financial year another $600,000 has been raised as a result of the first national Priceline Sisterhood Foundation event in September 2015, taking the total funds raised since 2011 to more than $2 million.

Importantly all funds raised go directly to the charity partners to assist in developing their services to all Australians. This is an initiative that everyone associated with API can take pride in.

Board of directorsDuring the year Dr Michael Wooldridge retired from the Board and we thank him for his contribution over nearly 9 years as a Non-executive director.

Another Non-executive director Mr Ken Gunderson-Briggs was appointed Senior Independent Director and has also replaced Dr Wooldridge on the Remuneration Committee.

The Board is pleased the performance of API has continued to improve, showing strong operational execution of the strategy which is delivering sustainable results. The improved financial position at the end of 2015 will give the Board opportunities to look at options for growth, however the major focus in the short term is ensuring that shareholders see further improvement on the existing assets.

Finally, on behalf of all directors, we would like to thank all API’s staff for their contribution that has delivered the improvements for all shareholders.

Peter R Robinson Chairman

Stephen P Roche Managing Director and Chief Executive Officer

Annual Report 2015 Australian Pharmaceutical Industries Limited

5

The Priceline Sisterhood was initially formed in 2011 with its purpose being to give back to the community and,

specifically, to provide support to women and their families.

Charity partners were selected that covered a range of causes that were close to the hearts of women; coming from the results of a national survey that had more than

25,000 female respondents.

In 2014 the Priceline Sisterhood Foundation Limited was established to allow for tax deductible donations. The

foundation has an independent Board of Directors and the patron of the Foundation is Ita Buttrose. More than $2 million

has been raised since inception and all funds raised go directly to our charity partners.

The Priceline Sisterhood Foundation todayThe Foundation has a desire to help more Australian

women and their families by supporting those who are affected by conditions such as cancer and mental health.

The Foundation also wants to increase the awareness of the work the charities are undertaking which can lead

to greater understanding, better treatment and, in some cases, prevention.

In reality there is only one degree of separation for many Australians who know people affected by these conditions and the Foundation is working to support all those affected

either directly or indirectly.

More information about the Priceline Sisterhood Foundation can be found at https://www.priceline.com.au/sisterhood

6

Australian Pharmaceutical Industries Limited Annual Report 2015

MORE THAN

$2,000,000RAISED SO FAR

Who does the Foundation help?The charity partners help thousands of Australians every day. This is what the causes are about and a snapshot of who they help:

Alzheimer’s Australia provides a wide range of information, support, counselling, training and education to people with dementia, their families and carers as well as to professionals working in the dementia field. They advocate for the needs of Australians living with all types of dementia and they are committed to achieving a dementia-friendly Australia where people with dementia are respected, supported, empowered and engaged in community life .

– 342,800 Australians are living with dementia today1

– Every 6 minutes a new person is diagnosed with dementia1

The Australian Cervical Cancer Foundation has a mission to minimise the incidence and burden of cervical cancer and related women’s health issues: to assist women, their families, and communities by developing and implementing practical and appropriate programs, and by partnering with like-minded governments, organisations, and individuals to achieve health outcomes which reduce marginalisation and contribute to developing stronger communities. They provide life-saving HPV cervical cancer vaccine for women in developing countries, and promote awareness and prevention of cervical cancer.

– Cervical cancer is the 5th most common cancer in Australian women aged 15-442

– Around the world 300,000 women die every year from cervical cancer2

Children First Foundation has a mission to transform the lives of children by giving hope, exceptional care and pathways to a brighter future. Their work ensures that both Australian and overseas children have access to medical care and treatment which are otherwise inaccessible for them.

– Transforming the lives of children who suffer conditions that can’t be treated in their country of birth with life changing or life-saving treatments and rehabilitation3

– Supporting Australian chronically ill or disabled children whose families can’t meet the gap payments that are required for equipment or services that are only partially funded3

PANDA (Perinatal Anxiety and Depression Association) is committed to a community where perinatal depression and anxiety are recognised and the impact on women, men and their families are minimised through acknowledgement, support and education. PANDA provides telephone counselling support services, raises awareness and develops and shares its knowledge with consumers and other health organisations.

– Up to 1 in 10 women in Australia experience antenatal depression with the same number estimated to experience anxiety4

– Up to 1 in 20 men in Australia experience antenatal depression4

Look Good Feel Better is a free community service program dedicated to helping Australians living with cancer cope with the appearance-related side effects caused by cancer treatment. Women, men and teens participate in a practical workshop which covers skincare, make-up and head-wear demonstrations leaving them empowered to face their cancer treatment with confidence. By addressing hair loss and changes to the skin with the use of skin care, makeup, hats, turbans and wigs, they help to restore patients’ appearance and self-image.

– More than 118,000 people have participated in workshops run by volunteers dedicated to teaching cancer patients how to manage the appearance-related side effects of any form of cancer5

– Annually more than 8,500 women participate in approximately 1,000 workshops held to assist their appearance and associated emotional wellbeing5

Our charity partners are:

1. Source: https://fightdementia.org.au2. Source: https://accf.org.au3. Source: http://childrenfirstfoundation.org.au4. Source: http://lgfb.org.au5. Source: http://www.panda.org.au

Further information on the charity partners and the services they provide is available from:

– Alzheimer’s Australia https://fightdementia.org.au

– Australian Cervical Cancer Foundation https://accf.org.au

– Children First Foundation http://childrenfirstfoundation.org.au

– Look Good Feel Better Foundation http://lgfb.org.au

– Perinatal Anxiety and Depression Australia http://www.panda.org.au

7

Annual Report 2015 Australian Pharmaceutical Industries Limited

8

Australian Pharmaceutical Industries Limited Annual Report 2015

DIRECTORS’ REPORT

DIRECTORSThe Directors of the Company at any time during or since the end of the financial year are:

Mr Peter R Robinson, BCom, FAICDChairman.Non-executive director.Director since 5 May 2000.Appointed Chairman 8 July 2003.

Mr Robinson has held both executive and non-executive directorships for over 30 years. Mr Robinson also during this time has had extensive general management and chief executive officer experience in the pharmaceutical industry.

Other current listed company directorships:

– Clover Corporation Limited – TPI Enterprises Ltd (listed ASX 10 August 2015)

Former listed company directorships in the past three years:

– Washington H Soul Pattinson and Company Limited (appointed 1984, resigned 31 March 2015)

– New Hope Corporation Limited (appointed August 1997, resigned 31 March 2015)

– Exco Resources Limited (appointed November 2012, company de-listed January 2013)

Mr Robert D Millner, FAICDNon-executive director.Director since 5 May 2000.Appointed member of the Remuneration Committee on 2 October 2007.Appointed member of the Nomination Committee on 15 August 2012.

Mr Millner has had extensive management and public company experience across a number of industries.

Other current listed company directorships:

– Brickworks Limited – BKI Investment Company Limited – Milton Corporation Limited – New Hope Corporation Limited – TPG Telecom Ltd – Washington H Soul Pattinson and Company Limited

Former listed company directorships in the past three years:

– Exco Resources Limited (appointed November 2012, company de-listed January 2013)

From left to right:Peter R RobinsonRobert D MillnerE Carol HolleyStephen P RocheLee AusburnGerard J MastersKenneth W Gunderson-Briggs

Annual Report 2015 Australian Pharmaceutical Industries Limited

9

Ms E Carol Holley, BA, FCA, FAICDIndependent non-executive director.Director since 19 December 2006.Appointed Chair of the Audit and Risk Committee on 19 December 2006.

Ms Holley is a non-executive director of Defence Housing Australia and Chair of its subsidiary Defence Housing Australia Investment Management Limited.

Ms Holley is also chair of the Audit and Risk Committees of Land and Housing Corporation, Service NSW, The Parliament of NSW and National Health Funding Body and a member of the committees of the NSW Police Force and NSW Mental Health Commission.

Mr Stephen P Roche, BBus, FAICDExecutive director.Managing Director and Chief Executive Officer since 14 August 2006.

Mr Roche joined API in March 2005. Previously he was Group General Manager, Health Services for Mayne Group Limited with responsibility for pharmacy distribution, pathology and other business units. Previous roles included Chief Operating Officer, Healthcare Services for FH Faulding & Co and a number of management roles at CSR.

Ms Lee Ausburn, MPharm, BPharm, DipHospPharm, GAICDIndependent non-executive director.Director since 7 October 2008.Appointed member of the Audit and Risk Committee on 7 October 2008.

Appointed member of the Nomination Committee on 15 August 2012 and appointed Chair on 8 April 2015.

Ms Ausburn is a pharmacist with experience in retail and hospital pharmacy and in academia. She had a long career in the pharmaceutical industry with Merck Sharp and Dohme (Australia) Pty Ltd and was previously Vice President, Asia, for Merck and Co Inc with responsibility for the company’s operations across Asia.

Ms Ausburn is also President, Pharmacy Faculty Foundation, University of Sydney and is a former board member of the Clinical Excellence Commission and Agency for Clinical Innovation, NSW Health.

Other current listed company directorships:

– NIB Holdings Limited – Somnomed Limited

Mr Gerard J MastersIndependent non-executive director.Director since 7 September 2010.Appointed member of the Nomination Committee on 15 August 2012.Appointed member and Chair of the Remuneration Committee on 30 January 2014.

Mr Masters has had extensive experience in retailing. Until his resignation in early 2006, he spent more than 33 years with the Coles Myer Group. This included a 10 year period as Managing Director of Bi Lo, Coles and then the total Supermarkets Group which was Coles Myer’s largest and most profitable business. His most recent role, until his resignation in 2009, was as the Managing Director and CEO of The Reject Shop Limited.

Mr Kenneth W Gunderson-Briggs, BBus, FCA, MAICDSenior Independent non-executive director.Director since 6 May 2014.Appointed member of the Audit and Risk Committee on 6 May 2014.Appointed member of the Remuneration Committee on 8 April 2015.Appointed Senior Independent Director on 2 September 2015.

Mr Gunderson-Briggs is a chartered accountant, registered company auditor and public company director, with broad experience in the finance and retail franchise sectors.

Mr Gunderson-Briggs has been Chairman of Glenaeon Rudolf Steiner School Limited since 2013, having been a director on the Board since 2009.

Other current listed company directorships:

– Harvey Norman Holdings Limited

The Hon Dr Michael R Wooldridge, BSc, MBBS, MBA, LLDIndependent non-executive director.Director since 1 February 2006. Resigned 31 December 2014.Appointed member of the Remuneration Committee on 2 October 2007. Resigned 31 December 2014.Appointed Lead Independent Director on 2 December 2008. Resigned 31 December 2014.Appointed Chair of the Nomination Committee on 15 August 2012. Resigned 31 December 2014.

Former listed company directorships in the past three years:

– Vision Eye Institute Ltd (resigned 30 January 2015)

COMPANY SECRETARYMr Peter Sanguinetti has been Company Secretary and General Counsel since November 2007. Mr Sanguinetti BJuris, LLB, MAICD has extensive experience and was previously Company Secretary and General Counsel of Kodak (Australasia) Pty Ltd for 9 years, responsible for legal and company secretarial activities for the Kodak group across Asia. Mr Sanguinetti was also a non-executive director of HPAL Limited from January 2005 to November 2007. On 2 June 2009, Ms Genevieve Ryan was appointed an Alternate Company Secretary. Ms Ryan BSc (Hons), LLB (Hons) is a qualified lawyer and supports the Company Secretary.

10

Australian Pharmaceutical Industries Limited Annual Report 2015

DIRECTORS’ MEETINGSThe number of Directors’ meetings (including meetings of committees of Directors) and number of meetings attended by each of the Directors of the Company during the period were:

Board Audit and Risk Remuneration Nomination

Director**Number

attendedNumber

Held*Number

attendedNumber

held*Number

attendedNumber

held*Number

attendedNumber

held*

Mr P R Robinson*** 13 14 – – – – – –

Mr R D Millner 13 14 – – 2 2 1 1

Dr M R Wooldridge+ 4 4 – – 1 1 1 1

Ms E C Holley 13 14 5 5 – – – –

Mr S P Roche*** 14 14 – – – – – –

Ms L Ausburn 12 14 5 5 – – – 1

Mr G J Masters 14 14 – – 2 2 1 1

Mr K W Gunderson-Briggs 14 14 5 5 1 1 – –

* Number of meetings held during the time the director held office or was a member of the committee during the period.** All Directors who are not members of Committees are invited to attend Committee Meetings.*** Mr Robinson and Mr Roche attended all Committee meetings by invitation. + Dr Wooldridge retired as a Director and from all Committee positions on 31 December 2014.

OPERATING AND FINANCIAL REVIEWAs required by Section 299A(1) of the Corporations Act, and in accordance with ASIC Regulatory Guide 247 Effective Disclosure in an Operating and Financial Review (RG247) issued in March 2013, the Board is required to include in the Directors’ Report an Operating and Financial Review (OFR) which includes information that shareholders would reasonably require to make an informed assessment of the consolidated entity’s operations, financial position and business strategies, and prospects for future years. The OFR complements and supports the financial report.

Financial PerformanceFor the year ended 31 August 2015 the Company reported a net profit after tax of $43.1 million following strong contributions from its Retail and Pharmacy Segments along with productivity gains across the Supply Chain network. The Company’s reported revenue increased to $3.5 billion with a backdrop of underlying Pharmacy sales growth, along with strong Priceline like for like growth of 4.5% and a store network increase of 30 stores.

The Retail segment recorded sales growth of 16.0% to $872.1 million. The Retail business reported segment gross profit of $218 million being an increase of 10.6% on the previous year. The Sister Club program continued to grow with over 5.6 million members.

The Pharmacy distribution segment reported sales of $2.4 billion being in line with the previous year, notwithstanding the impact of PBS price reforms. The underlying sales adjusting for PBS reforms throughout the year was an increase of 6.5%.

The Company’s New Zealand business reported an increase in earnings to $2.8 million, an increase from $1.0 million in the prior year. This result is attributable to the increase in contract and export sales combined with improved margins across several product categories.

The Company’s associate investment (CH2 Holdings Pty Ltd) reported an operating loss of $0.4m for the year.

Capital expenditure for the year was $30.6 million with the significant part of this investment being the final implementation of the SAP ERP system.

The Company’s operating cash flow improved 24.7% to $80.1 million on the back of stronger working capital management and lower financing costs across the year.

Financial PositionThe Company’s net debt reduced to $70.8 million which reflects a $28.4 million reduction on the prior year. The Company is currently operating comfortably within the Group’s facility limits and associated banking covenants.

In line with the strong operational performance the Company has declared a fully franked final dividend of 2.5 cents per share, bringing the full year dividend to 4.5 cents per share fully franked, an increase of 28.6% on the prior year dividend of 3.5 cents.

DIRECTORS’ REPORTcontinued

Annual Report 2015 Australian Pharmaceutical Industries Limited

11

Business Strategies and Prospects for Future Financial YearsDuring the year the Board undertook a review of its short and long term strategies. This review was performed to ensure that its strategies remained relevant and adaptable to the dynamic regulatory and economic environment that the Company operates in, and which may affect the future financial performance and position of the Company.

The strategic issues that the company needs to address in order to achieve its vision are, by their very nature, long term issues and remain unchanged.

The strategic review analysed a range of internal and external environmental elements which validated the range of identifiable strategic goals and supporting initiatives across all business units and functions. The overall business strategies relevant to the Company’s future financial position and performance include:

– Leveraging our health and beauty competitive advantage

– Market insights driving the customer preferred retail proposition

– Providing a compelling business model for partners – An integrated business driving superior value – Optimised capital investment – A safer place to work every day – Excellence in leadership, learning and recognition

These strategic goals and supporting initiatives are all focused on the Company achieving its vision of ‘Enriching life as the most inspirational choice for health, beauty and wellbeing’

By applying the strategic goals to the Company’s business plans, there will be a continued emphasis on capitalising on the Company’s strengths in the health and beauty retail market and to optimise its strong national community pharmacy wholesale distribution business. This means the Company intends to;

– Continue to promote the Priceline Pharmacy Franchise proposition and grow the store network. Priceline Pharmacy is seen as a compelling proposition for pharmacists who wish to offset the impact of PBS reform, leverage business, pharmacy and retail expertise, and drive further growth from integrated dispensary and retail programs;

– Transition from Company owned Priceline stores to Franchise owned Priceline Pharmacies;

– Build loyalty and increase engagement of the Priceline Sister Club loyalty program, and generally promote increased customer engagement including through the Priceline website and social media channels;

– Grow the Club Premium independent pharmacy buying group program;

– Expand the Company’s Health and Beauty Retail Brand portfolio and offers, supported by an integrated marketing communication strategy;

– Ensure the benefits, delivery and process improvements arising from the OneERP Project implementation;

– Optimise the value of our business portfolio through investment, divestment and acquisition;

– Build on the Company’s merchandising strategy by sourcing pharmaceutical and health and beauty products that focus on superior delivery performance, exclusive product offerings and private brand products, and ranging products that are relevant to everyday needs and deliver value for money enhanced health outcomes;

– Maintain earnings margins within Pharmacy Distribution during a period of ongoing government PBS reforms in the Pharmacy sector;

– Embed our values and behaviours by continuing to develop Personal, Team, Business and Community Leadership capability;

– Continue to invest in supply chain and information technology platforms to drive efficient and cost effective operating cost structures;

– Drive safety leadership throughout the business.

The Company expects to sustain improvements in earnings performance through the implementation of its core strategies and supporting initiatives. This outlook is subject to no material change in consumer or customer demand, a stable economic climate and no unforseen adjustments to either the regulatory environment or the Pharmaceutical Benefits Scheme.

Specific details about the Company’s business strategies and prospects that could give rise to likely material detriment to the Company, for example, information that is commercially sensitive, confidential or could give a third party a commercial advantage has not been included in this Annual Report. Other than the information set out in this document, information about other likely developments in the Company’s operations in future financial years has not been included.

12

Australian Pharmaceutical Industries Limited Annual Report 2015

MATERIAL BUSINESS RISKSThe Company continues to be influenced by a number of general economic and business conditions including levels of consumer spending, interest and exchange rates and government regulatory policies. The Company has a distinctive positioning in the Community Pharmacy wholesaling sector in Australia as well as being well positioned in the mass market Health and Beauty retail sector.

Despite its strengths in these sectors the Company faces challenges including:

– Ongoing government reforms to the PBS in the Pharmacy sector; and

– Macro-economic factors contributing to volatile retail sales and increasing cost pressures in key areas such as labour.

As part of the Company’s risk management process, the risk profile of the Company is reviewed by Management with the assistance of the Risk and Internal Audit team at least annually. The results of this review are provided to the Audit and Risk Committee for its consideration and recommendation to the API Board.

The Company’s risk management process is integrated with its strategic planning process and involves identifying the risk universe and documenting those factors that contribute to the inherent risk environment. Inherent risk is determined by combining likelihood and consequences assessments determined in the absence of any controls within the business.

The effectiveness of current controls in place to manage the identified risks is then assessed to determine residual risk. Where residual risk is deemed to be greater than the business risk appetite, risk treatment plans are developed and specific personnel assigned responsibility for the management of those risks. The status of risk treatment plans is monitored and reported to the Audit and Risk Committee at regular intervals.

The most recent update was in July 2015 against a backdrop of continued PBS reforms, challenging Retail trading conditions and the Company’s decision to update its Information Technology platforms as it transitioned to a one enterprise approach.

The following is a summary of the contemporary risks facing the Company as assessed by the recent update of the Company’s risk profile:

– Structural reforms within the Australian Community Pharmacy sector.

This relates to the risk of continued Government PBS reforms. The Company monitors the changes to PBS medicines and responds with a combination of reduced discounts to Pharmacy customers and operational

adjustments. The Company also closely monitors costs associated with the Community Service Obligation (CSO).

– Execution of Retail Pharmacy strategy with associated growth of Priceline Pharmacy stores.

There is a risk that the expansion of the Company’s Priceline Pharmacy franchise network is unsuccessful or the expected growth in the next five years is slower than expected. Existing key business processes and responses to mitigate this risk include dedicated Retail Pharmacy Business Development teams, the inclusion of landlords, banks and industry accountants in pharmacist familiarisation and recruitment forums. Tracking measures to monitor growth rates are reported to the Managing Director and the Board on a monthly basis.

– One Enterprise Restructure and Information systems upgrade.

In 2011 the Company undertook a restructure of its Australian business and has transitioned from a multiple Business Unit structure to One Enterprise functional structure. This transition included an upgrade of the Company’s enterprise management information platforms in the latter part of the 2015 financial year.

As this successful initiative progresses through stabilisation and the expected benefits accrue, the next challenge the Company faces is to further optimise these platforms and realise even greater potential. To mitigate the risk of not meeting timelines or expectations, project governance measures, including a Management Steering Committee and Business Optimisation Team, have been established to guide this optimisation process.

– Financial Risk and Long Term Customer Loans.The Company’s activities expose it to a number of financial risks including customer payment defaults, financial guarantees to banks supporting certain Pharmacy customers being called, and general retail trading conditions. The Company adopts a financial risk management program which seeks to minimise potential adverse impacts on the financial performance of the Company. The Company has undrawn funding lines throughout the year to manage any unforeseen financial risks.

REMUNERATION REPORT – AUDITEDThe API Board is committed to transparent disclosure of its remuneration strategy and this report details the processes used in remuneration decisions and their outcomes for Key Management Personnel (KMP) for the 2015 financial year. This report is prepared in accordance with Section 300A of the Corporations Act 2001 (as amended) for the Company and its subsidiaries.

DIRECTORS’ REPORTcontinued

Annual Report 2015 Australian Pharmaceutical Industries Limited

13

In the previous financial year, the Board engaged Guerdon Associates as its independent external remuneration consultant to undertake a review of Executive Remuneration and Executive Incentive Plans (excluding the Managing Director and Chief Executive Officer). Given the relatively recent outcome of this review, the Board did not consider it was necessary to re-engage Guerdon Associates to perform a similar remuneration review in the 2015 financial year. The Board is committed to seeking independent review of the Company’s remuneration structure as required from time to time to ensure its remuneration practices remain consistent with peer market practices. For this purpose, it is intended that Guerdon Associates will provide advice to the Board as required.

With respect to Executive STIP and LTIP Incentive Plans, a review was conducted during the 2015 financial year to ensure those Plans continued to meet market practices. As a consequence of this review, the Board approved changes to the respective plans as summarised below:

1. Short Term Incentive Plan (STIP) for the 2014/2015 award and thereafter – The number of performance rights issued will no

longer be increased by 10% as compensation for forgone dividends. Instead, a cash payment will be made at the time of vesting of the performance rights based on the Company’s actual dividend paid during the 12 month vesting period.

2. Long Term Incentive Plan (LTIP) for the 2015/2016 award and thereafter – The number of performance right entitlements

will no longer be increased by 10% as compensation for forgone dividends, and no other compensation will be payable for forgone dividends.

More details regarding the changes to STIP and LTIP arrangements can be found in Section 2 of the Remuneration Report.

Key Management Personnel Key Management Personnel (KMP) have the authority and responsibility for planning, directing and controlling the activities of the consolidated entity, and comprise:

1. Non-executive Directors;2. Managing Director and Chief Executive Officer;3. Chief Financial Officer; and 4. Group General Manager Business Development and

Operations.

Following a review during the 2015 financial year, it is not considered other Executives of the Company are within the scope of KMP having regard to the definition in AASB 124 and the definitions of “chief executive function” and “chief financial officer function” as set out in Section 295A (4) and (6) Corporations Act 2001.

Non-executive director KMP Peter Robinson Chairman

Lee Ausburn Director

Carol Holley Director

Gerard Masters Director

Robert Millner Director

Michael Wooldridge Director (ceased 31 December 2014)

Kenneth Gunderson-Briggs Director

Executive KMP Stephen Roche Managing Director and Chief

Executive Officer

Graeme Fallet Chief Financial Officer (separated 19 December 2014)

Peter Mendo Chief Financial Officer (appointed interim Chief Financial Officer 21 January 2015, appointed Chief Financial Officer 1 September 2015)

Richard Vincent Group General Manager Business Development and Operations

This report has been audited by the Company’s Auditor, KPMG as required by Section 308(3C) of the Corporations Act 2001.

The Remuneration Committee is governed by its Charter (available on www.api.net.au) which was developed in line with ASX Corporate Governance Principles and Recommendations. The Charter specifies the purpose, authority, membership and activities of the Remuneration Committee, and the Charter is annually reviewed by the Committee to ensure it remains consistent with regulatory requirements.

Membership of the Committee consists of Non-executive directors. During 2014-2015 members of the Committee were Mr Gerard Masters (Chairman), Dr Michael Wooldridge and Mr Robert Millner. Dr Wooldridge retired from the Committee and the Board on December 31, 2014, and Mr Kenneth Gunderson-Briggs was appointed to the committee on April 8, 2015.

14

Australian Pharmaceutical Industries Limited Annual Report 2015

The Remuneration Report is in sections as follows:

Section 1 Non-executive Director KMP RemunerationA Policy & Principles

B Remuneration Details (excluding the Chief Executive Officer)

Section 2 Executive KMP Remuneration A Policy & Principles

B Remuneration Structure

C Short Term Incentive Plan (STIP)

D Long Term Incentive Plan (LTIP)

E Summary of KMP Employment Contracts

F KMP Remuneration Details

Section 3 Other matters A Comments on Remuneration Report at the

Company’s most recent AGM

B Appointment of Remuneration Consultant

SECTION 1 NON-EXECUTIVE DIRECTOR KMP REMUNERATION

A. Policy and PrinciplesNon-executive directors’ fees are determined within an aggregate Non-executive directors’ pool limit. An annual total fee pool of $850,000 was approved by shareholders at the 30 January 2014 Annual General Meeting. Total Non-executive directors’ remuneration including board committee fees, non-monetary benefits and superannuation paid at the statutory prescribed rate for the year ended 31 August 2015 was $673,444 which is within the approved annual fee pool. This is a 6.4% increase on the prior year, and attributable to an increase in base board and committee fees following a review of director fees in 2014. Non-executive directors’ remuneration is based on the data provided by independent remuneration consultants, the need to attract and retain appropriately qualified Non-executive directors, fee levels applied in similarly sized companies, and board judgement as to whether any adjustments are appropriate. Non-executive directors do not receive performance related remuneration.

Under the Board’s Retirement Scheme, which was approved by Shareholders at the 1994 AGM, retiring Non-executive directors are paid on a pro-rata basis up to ten (10) years’ service to a maximum of three (3) times the average annual remuneration in the three (3) years preceding retirement. The retirement benefit is capped at $220,000 per Director and applies only to Directors appointed prior to 9 September 2003. The Directors have agreed to freeze this benefit as at 31 August 2009.

Annual Board fees (including superannuation) were structured as follows with effect from March 2014:

RoleAnnual Fee

Structure

Board chairman $170,000

Board member $80,000

Audit and Risk Committee chair $35,000

Audit and Risk Committee member $6,000

Remuneration Committee chair $12,500

Remuneration Committee member $6,000

Nomination Committee chair (no fee)

Nomination Committee member (no fee)

Lead Independent Director $12,500

The Board Chairman does not receive Committee fees.

DIRECTORS’ REPORTcontinued

Annual Report 2015 Australian Pharmaceutical Industries Limited

15

B. RemunerationofDirectors(ExcludingtheChiefExecutiveOfficer)

Short Term

Post

-em

ploy

men

t su

pera

nnua

tion

cont

ribut

ions

Oth

er lo

ng te

rm

Term

inat

ion

paym

ents

Equi

ty V

alue

of r

ight

s gr

ante

d un

der S

TIP

Equi

ty V

alue

of r

ight

s gr

ante

d un

der L

TIP

Tota

l

Prop

ortio

n of

rem

uner

atio

n pe

rform

ance

rela

ted

Valu

e of

righ

ts a

s pr

opor

tion

ofre

mun

eration(%

)

Sala

ry &

Fee

s

Cas

h - S

hort-

term

ince

ntiv

es

Non

-mon

etar

y be

nefit

s

Tota

l

DIRECTORS $ $ $ $ $ $ $ $ $ $ % %

Non-executiveMr P R Robinson31 August 2015 155,606 – 1,261 156,867 14,783 – – – – 171,650 – –

31 August 2014 147,653 – 2,467 150,120 13,723 – – – – 163,843 – –

Mr R D Millner31 August 2015 79,539 – – 79,539 7,478 – – – – 87,017 – –

31 August 2014 67,960 – – 67,960 6,319 – – – – 74,279 – –

DrMRWooldridge(resigned31December2014)31 August 2015 30,053 – – 30,053 2,855 – – – – 32,908 – –

31 August 2014 79,180 – – 79,180 7,362 – – – – 86,542 – –

Ms E C Holley31 August 2015 105,263 – – 105,263 10,000 – – – – 115,263 – –

31 August 2014 92,232 – – 92,232 8,575 – – – – 100,807 – –

Ms L Ausburn31 August 2015 78,719 – – 78,719 7,478 – – – – 86,197 – –

31 August 2014 67,960 – – 67,960 6,319 – – – – 74,279 – –

Mr G Masters31 August 2015 84,668 – – 84,668 8,043 – – – – 92,711 – –

31 August 2014 67,163 – 1,234 68,397 6,254 – – – – 74,651 – –

MrKGunderson-Briggs(appointed6May2014)31 August 2015 80,089 – – 80,089 7,608 – – – – 87,697 – –

31 August 2014 25,345 – – 25,345 2,377 – – – – 27,722 – –

Retirement benefits for Non-executive Directors are included on an accrual basis. The benefits are paid on a pro rata basis up to 10 years’ service to a maximum of three times the average annual remuneration in the three years preceding retirement. The retirement benefit is capped at $220,000 and does not apply to Directors first appointed after 9 September 2003. On 31 August 2009 the Directors agreed to freeze this benefit.

Post employment superannuation contributions are inclusive of the super guarantee increase effective 1 July 2014. The Annual Board fees disclosed on the previous page have not yet been adjusted to reflect this statutory change.

16

Australian Pharmaceutical Industries Limited Annual Report 2015

SECTION 2 EXECUTIVE REMUNERATION INCLUDING THE MANAGING DIRECTOR

A. Policy and PrinciplesAPI’s remuneration strategy is to:

– Offer a remuneration structure that will attract, focus, retain and reward highly capable people;

– Ensure that remuneration decisions are based on a fair and transparent job evaluation process that is linked to comparative market data and the experience of the individual in the position;

– Have a clear and transparent link between performance and remuneration;

– Encourage and integrate risk management within the reward framework; and

– Build employee engagement and align management and shareholder interests through the ownership of Company shares.

Executive remuneration is set with regard to the size and nature of the position with reference to market median benchmarks and the performance of the individual.

Remuneration will incorporate at risk elements to:

– Link Executive reward with the achievement of API’s business objectives and financial performance; and

– Ensure total remuneration is competitive by market standards.

The Remuneration Committee has the role of reviewing and making recommendations to the Board on Executive remuneration at API. The Remuneration Committee may seek independent advice on the appropriateness of remuneration levels given trends in comparable companies. The Remuneration Committee is authorised to seek advice if and when required.

B. Remuneration StructureThe Executive Remuneration Framework as it applies to the Managing Director and Senior Executives comprises:

– Fixed remuneration; and – Performance linked remuneration in the form of a Short

Term Incentive Plan (STIP) and a Long Term Incentive Plan (LTIP).

Fixed RemunerationFixed remuneration is a guaranteed salary level inclusive of any Fringe Benefits Tax (FBT), charges related to employee benefits including motor vehicles and employer contributions to superannuation funds.

Fixed remuneration levels are reviewed annually. Fixed remuneration levels are set in reference to each position’s accountability and the median level for similar jobs in the market. Any adjustment needs to also consider individual segment results and overall performance of the consolidated entity. In addition, external consultants provide analysis and advice to ensure that Executive remuneration is appropriate given market practice.

Performance Linked RemunerationPerformance linked remuneration includes both short term and long term incentives and is designed to reward KMP’s for meeting or exceeding their financial and non-financial objectives. The short term incentive is provided in the form of a cash payment and deferred rights to acquire shares while the long term incentive is provided as deferred rights to acquire shares (“Performance Rights”).

The Group has a policy that prohibits those that are granted share-based payments as part of their remuneration from entering into other arrangements that limit their exposure to losses that would result from share price decreases. Entering into such arrangements has been prohibited by law since 1 July 2011.

C.ShortTermIncentivePlan(STIP)The STIP is an annual at risk incentive plan for Executives and other designated senior employees who are considered to be in business critical roles.

Prior to the start of the Company’s financial year the Remuneration Committee recommends for Board approval the size of the STIP pool which is the maximum amount payable under the STIP. The size of the pool is determined as a percentage of target EBIT for the year. Prior to any payment under the STIP, Company performance must pass an acceptable minimum gateway requirement of Group Net Profit After Tax before associates (NPAT).

At the start of each year the Remuneration Committee sets a ‘scorecard’ of performance conditions for the STIP as follows:

– NPAT; and – Other financial and non-financial measures tailored for

each business segment.

Other performance measures vary by business segment, however each scorecard includes a measure related to Earnings Before Interest and Tax (EBIT), Return on Net Assets (RONA), Return on Capital Employed (ROCE) and, in relation to Supply Chain, overall cost measurement. Multiple measures of performance help diversify risk.

DIRECTORS’ REPORTcontinued

Annual Report 2015 Australian Pharmaceutical Industries Limited

17

Each year, the Board establishes NPAT performance hurdles of which base, target and maximum STIP entitlements will be payable. The current practice is that base equates to budget less 10%, the target equates to budget and the maximum equates to 110% of budget.

After the conclusion of the financial year, the Board assesses performance against Group and Segment Scorecards with 80% of the total maximum percentage based on key financial objectives and 20% based on individual objectives. Prior to any consideration of a STIP payment, the Company must meet a base NPAT performance, usually set as 90% of the target NPAT. The Board has discretion for a STIP payment where achievement is between base and target NPAT levels.

The precise number of performance rights granted will be determined by dividing the value of the deferred component of the STIP award by the volume weighted average closing price of API shares on the ASX in the 10 day period after announcement of full year results.

Offers made for the 2014/2015 STIP award and the 2015/2016 STIP award and thereafter will no longer include an increase in the number of rights granted on account of compensation for forgone dividends during the vesting period. Instead a cash payment will be made based on the Company’s actual dividends paid during the 12 month vesting period. The reason for the change is to ensure the deferred STIP reflects the actual value received by shareholders rather than an estimate.

The deferred component of the STIP award is designed to manage risk by ensuring that decisions taken in the previous 12 months have resulted in sustainable Company benefit. The API Board has the discretion to clawback any unvested rights or unvested cash due to excessive risk taking, material misstatement of financial statements or fraudulent or gross misconduct.

For members of the Executive Leadership Team with STIP performance scorecard measures established after 1 September 2015 and any resulting award, the 50% 12 month deferred component of any STIP award will continue to be paid in performance rights. In addition, participants will be eligible to receive at the time of vesting a cash payment based on the Company’s actual dividend paid during the 12 month vesting period.

On vesting and exercise of a performance right, an employee will be provided with a fully paid ordinary share in API. No amount will be payable for the API shares upon vesting and exercise of the performance right.

More broadly, the Board retains absolute discretion over all awards made under the incentive award plans at API, including the STIP.

Managing Director and Chief Executive OfficerAt base, Mr Roche’s STIP equates to 32.5% of fixed remuneration, at target it equates to 65% of fixed remuneration and if NPAT is at a level that is 110% of budget, the STIP provides for a maximum payment of 100% of fixed remuneration.

Mr Roche’s STIP scorecard is varied by the Board from year to year and is drawn from financial measures such as NPAT (before associates), ROE and ROCE. Non-financial measures may include retail sales growth, Priceline Pharmacy network growth, pharmacy distribution market share and set improvement targets relating to workplace safety.

Other Executive KMPAt base, Executive KMP STIP equates to 10% of fixed remuneration, at target it equates to 20% of fixed remuneration and if NPAT is at a level that is 110% of budget, the STIP provides for a maximum of 40% of fixed remuneration. The Remuneration Committee determines the financial measures for Executive KMP STIP which includes divisional EBIT, ROCE and in the case of Supply Chain, operating costs.

During the 2014-15 financial year, the NPAT result exceeded the NPAT gateway and the Board approved the following Short Term Incentive payments.

In making the Short Term award to the Executive KMP the Board had regard to the following factors:

– Company performance – Meeting the performance criteria set out in the STIP

offer.

18

Australian Pharmaceutical Industries Limited Annual Report 2015

Maximum STIP Opportunity

as a % of Fixed Remuneration

Awarded STIP as a % of Fixed Remuneration

STIP Cash Entitlement

STIP Deferred Equity1

EXECUTIVES % % $ $

Mr S P Roche – Managing Director and CEO31 August 2015 100.0% 100.0% 490,543 490,543*

31 August 2014 100.0% – – –

Mr R Vincent – Group General Manager, Business Development & Operations31 August 2015 40.0% 40.0% 117,452 117,452

31 August 2014 40.0% 20.0% 56,884 56,884

MrGFallet–ChiefFinancialOfficer(separated19December2014)31 August 2015 – – – –

31 August 2014 40.0% 20.0% 47,160 47,160

MrPMendo–ChiefFinancialOfficer(appointed21January2015)^31 August 2015 – – – –

1. 50% of the deferred equity has been recognised in remuneration for the year in accordance with AASB 2 Share Based Payments.* On vesting and exercise of STIP performance rights, the Managing Director will be provided with fully paid ordinary shares purchased on-market.^ Appointed Interim Chief Financial Officer on 21 January 2015. Appointed Chief Financial Officer on 1 September 2015.

D. LongTermIncentivePlan(LTIP)The Remuneration Committee has responsibility for API’s Long Term Incentive Plan (LTIP). The Plan was established during the year ended 30 April 2006. The Remuneration Committee is responsible for awards to be granted under the Plan as well as overseeing administration of the Plan. Part of the administration is the determination of the performance conditions associated with each grant. The LTIP involves the granting of rights to acquire API shares.

Rights are granted to the Managing Director and Chief Executive Officer (which are subject to approval at the following AGM) and to certain executives as soon as practicable after the full year results are announced. This ensures that the allocation of rights reflects the market’s best informed assessment of Company value and share price. The number of Rights granted is derived by calculating a value representing the relevant percentage of a participant’s Fixed Remuneration, and dividing that value by the unit value per Right. This unit value is determined by calculating the 10 day Volume Weighted Average Closing Price of API shares immediately after announcement of full year results.

For LTIP performance scorecard measures established after 1 September 2015, performance rights no longer include additional rights to shares that would otherwise accrue from dividend reinvestment during the three (3) year vesting period. Executives do not receive dividends on unvested shares.

If performance conditions are satisfied, the Rights vest and convert to API shares on a one-for-one basis. If performance conditions are not met, the Rights lapse. Under the LTIP, shares can be purchased on market on behalf of the participant or new shares issued by the Company. If any vesting is satisfied through the achievement of performance criteria, a participant will be provided with shares in API. Performance conditions will be tested only once and any Performance Rights that do not meet the performance conditions will lapse and will not be re-tested. The Company has a policy whereby directors and employees are prohibited from dealing in financial products issued or created over or in respect of securities (e.g. hedges or derivatives) which have the effect of reducing or eliminating the risk associated with any equity incentives that may be offered from time to time.

If the holder of an LTIP entitlement ceases to be employed before the end of the Performance Period for reasons other than redundancy, death, disability or illness, then the Performance Rights will automatically lapse, subject to Board discretion. If the holder of an LTIP entitlement ceases to be employed, before the Performance Period and the date of employment ceasing is on or after the first anniversary date of the Commencement Date, due to redundancy, death, disability or illness, then the number of Performance Rights will be reduced pro-rata to reflect the length of time during the Performance Period the employee was employed.

DIRECTORS’ REPORTcontinued

Annual Report 2015 Australian Pharmaceutical Industries Limited

19

More broadly, the Board retains absolute discretion over all awards made under the incentive award plans at API, including the LTIP. The LTIP is in the form of a grant of ‘rights to shares’ for exceptional performance over a three year period.

For grants made prior to 31 August 2014, the performance condition is based on the actual Return on Equity (ROE) achieved by the consolidated entity during the three (3) year period commencing at the beginning of the performance period when compared to the target ROE set by the Board for the same period (Target ROE). In both cases, ROE is expressed as a percentage created by dividing the net profit after tax for the relevant financial period by total shareholder equity for the relevant financial year. The target ROE is derived from the Corporate Plan for the three (3) years commencing at the beginning of the performance period.

Grants made after 1 September 2014 will include a target measure of 3 year earnings per share (EPS) compound annual growth (CAGR), in addition to the existing ROE measure. Each of the two measures (EPS and ROE) will contribute equally to a LTIP award. If ROE is achieved and EPS is not achieved, or vice versa, then the total available award would be halved. This means 50% of the award is dependent on the ROE metric, and 50% of the award is dependent on the EPS metric. EPS is derived from the Corporate Plan for the three years commencing at the beginning of the performance period. The EPS performance condition compares the actual EPS growth achieved by the API group during a 3 year performance period, against the target amount of EPS growth set by the Board for the same period. The EPS is the basic earnings per share disclosed in the Income Statement of the Financial Statements of API for each financial year during the performance period. The initial benchmark EPS that serves as the basis for calculating EPS growth, and the target EPS may be varied by the Board in its absolute discretion.

Managing Director and Chief Executive OfficerThe LTIP provides for Performance Rights equivalent in value to 60% of Fixed Remuneration.

Senior ExecutivesThe LTIP provides for Performance Rights equivalent in value to 25% of Fixed Remuneration.

2012 GrantDuring the 2014-15 financial year the Performance Rights relating to the 2012 grant lapsed as the hurdles set for this grant were not achieved.

2013 GrantAt 10 December 2013, performance rights (the 2013 grant) were granted with a performance period commencing on 1 September 2013 and ending 31 August 2016. Performance rights granted to the Managing Director and Chief Executive Officer were approved by shareholders at the 2014 Annual General Meeting. The performance condition, being API’s return on equity (ROE) for the exercise of performance rights will be assessed at the Remuneration Committee meeting after 31 August 2016, being the end of the performance period.

The ROE performance condition has the effect that:

– if a cumulative ROE of 21.35% is achieved for the three year period ending 31 August 2016, then 50% of the Rights will vest;

– if a cumulative ROE of 25.62% is achieved for the three year period ending 31 August 2016, then 100% of the Rights will vest; and

– if the cumulative ROE is between these two levels, then the number of rights that vest will be calculated on a straight line proportional basis.

2014 GrantAt 16 December 2014, performance rights (the 2014 grant) were granted with a performance period commencing on 1 September 2014 and ending 31 August 2017. Performance rights granted to the Managing Director and Chief Executive Officer were approved by shareholders at the 2015 Annual General Meeting. The performance condition, being API’s return on equity (ROE) and earnings per share (EPS) for the exercise of performance rights will be assessed at the Remuneration Committee meeting after 31 August 2017, being the end of the performance period.

The ROE performance condition has the effect that:

– if a cumulative ROE of 21.38% is achieved for the three year period ending 31 August 2017, then 20% of the Rights subject to the ROE Performance Condition will vest;

– if a cumulative ROE of 34.74% is achieved for the three year period ending 31 August 2017, then 100% of the Rights subject to the ROE Performance Condition will vest; and

– if the cumulative ROE is between these two levels, then the number of rights that vest will be calculated on a straight line proportional basis.

20

Australian Pharmaceutical Industries Limited Annual Report 2015

The EPS Compound Annual Growth Rate (CAGR) performance condition has the effect that:

– if CAGR of 7.5% is achieved for the three year period ending 31 August 2017, then 20% of the Rights subject to the CAGR Performance Condition will vest;

– if a CAGR of 10.0% is achieved for the three year period ending 31 August 2017, then 100% of the Rights subject to the CAGR Performance Condition will vest; and

– if the CAGR is between these two levels, then the number of rights that vest will be calculated on a straight line proportional basis.

E. Employment ContractsThe Company has entered into service contracts with Executive KMP. These contracts outline the components of remuneration paid to them but do not prescribe how remuneration levels are modified from year to year. Remuneration levels are reviewed each year to take into account any change in the scope of the role performed, and any other changes required to meet the principles of the Company’s remuneration policy outlined earlier.

Mr Stephen Roche, the Company’s Managing Director and Chief Executive Officer, has a contract of employment with the Company dated 27 September 2006. The contract continues until the employment is terminated in accordance with the contract. The contract states the following in respect of cessation of his employment:

– Mr Roche may resign from the Company by giving three months written notice;

– The Company may summarily terminate Mr Roche’s employment in specified circumstances with immediate effect and no termination benefits will apply other than accrued entitlements; and

– The Company may terminate Mr Roche’s employment by the giving of twelve months written notice and may make a termination payment in lieu of notice of up to twelve months fixed remuneration.

Mr Roche is subject to a twelve month non-compete restriction after cessation of his employment.

Mr Roche’s service contract has no fixed term.

The employment conditions and remuneration of the KMP are formalised in individual contracts of employment. No fixed terms are specified within these employment contracts and the following termination provisions apply:

KMP Term of Contract Notice Period by Company Notice Period by Employee

Graeme Fallet (separated 19 December 2014)

No fixed duration 6 months 6 months

Peter Mendo^ (appointed 21 January 2015)

No fixed duration 6 months 6 months

Richard Vincent No fixed duration 12 months 3 months

^ Appointed Interim Chief Financial Officer on 21 January 2015 on a fixed rate and fixed term contract that did not include participation in the 2014/15 STIP or 2014 LTIP. Appointed Chief Financial Officer on 1 September 2015. The notice period for the first twelve months of employment is 3 months and 6 months thereafter.

The Company may terminate an employment contract without cause by providing written notice, or making a payment in lieu of the notice period. Each employment contract provides for termination of employment without notice in circumstances sufficient to warrant summary termination. Each employment contract provides for a non-compete restriction of up to twelve (12) months after cessation of employment.

DIRECTORS’ REPORTcontinued

Annual Report 2015 Australian Pharmaceutical Industries Limited

21

F. Remuneration of Executives Including the CEODetails of the nature and amount of each major element of remuneration of each of the Key Management Personnel of the consolidated entity (including the Chief Executive Officer) are:

Short Term

Post

-em

ploy

men

t sup

eran

nuat

ion

cont

ribut

ions

Oth

er lo

ng te

rm (ii

)

Term

inat

ion

paym

ents

Equi

ty V

alue

of r

ight

s gr

ante

d un

der

STIP

Equi

ty V

alue

of r

ight

s gr

ante

d un

der

LTIP

(i)

Tota

l

Prop

ortio

n of

rem

uner

atio

n pe

rform

ance

rela

ted

Valu

e of

righ

ts a

s pr

opor

tion

of

remun

eration(%

)

Sala

ry &

Fee

s

Cas

h-Sh

ort-

term

ince

ntiv

es

Non

-mon

etar

y be

nefit

s

Tota

l

EXECUTIVES $ $ $ $ $ $ $ $ $ $ % %

Mr S P Roche – Managing Director and CEO31 August 2015 954,899 490,453 9,889 1,455,241 18,871 28,611 – 245,227 157,811 1,905,761 46.9 21.1

31 August 2014 910,723 – 15,834 926,557 17,943 22,996 – – 107,494 1,074,990 10.0 10.0

Mr R Vincent – Group General Manager, Business Development & Operations31 August 2015 566,382 117,452 2,535 686,369 18,871 15,037 – 87,168 37,736 845,181 28.7 14.8

31 August 2014 547,855 56,884 2,615 607,354 17,943 13,796 – 28,442 41,216 708,751 17.9 9.8

MrGFallet–ChiefFinancialOfficer(separated19December2014)31 August 2015 140,017 – – 140,017 6,261 – 340,209 (23,580) (112,444) 350,463 (38.8) (38.8)

31 August 2014 451,447 47,160 1,234 499,841 17,943 – – 23,580 34,097 575,461 18.2 10.0

MrPMendo–ChiefFinancialOfficer(appointed21January2015)31 August 2015 363,750 – 1,140 364,890 – – – – – 364,890 – –

(i) The value of performance rights is calculated at grant date using the Black-Scholes Option Pricing model. The value is allocated to each reporting period evenly over the performance period.

(ii) Other long term benefits are the amounts charged against profits for the year for accrued Long Service Leave entitlements.

22

Australian Pharmaceutical Industries Limited Annual Report 2015

SpecificBonusandEquityRemunerationAnalysis–AuditedAnalysis of Performance Rights over Equity Instruments granted as compensationDetails of the vesting profile of performance rights awarded as remuneration to each key management person are detailed below.

Executive Director

Performance Rights granted

Included in Remuneration

% vested in the

period

% forfeited

in the period*^

Financial period in which grant

vestsNumber ValuePerformance

period commences

Mr S P RocheLTIP 957,774 354,375 1 September 2012 (236,250) 0% 100% 31 August 2015

777,088 357,460 1 September 2013 119,153 0% 0% 31 August 2016

993,644 824,725 1 September 2014 274,908 0% 0% 31 August 2017

STIP Deferred Equity^ 490,453 1 September 2014 245,227 0% 0% 31 August 2017

Executive OfficersMr R VincentLTIP 364,562 134,888 1 September 2012 (89,926) 0% 100% 31 August 2015

295,888 136,108 1 September 2013 45,369 0% 0% 31 August 2016

297,444 246,879 1 September 2014 82,293 0% 0% 31 August 2017

STIP Deferred Equity 81,263 56,884 1 September 2013 28,442 0% 0% 31 August 2016

STIP Deferred Equity^ 117,452 1 September 2014 58,726 0% 0% 31 August 2017

Mr G FalletLTIP 303,364 112,245 1 September 2012 (74,830) 0% 100% 31 August 2015

245,309 112,842 1 September 2013 (37,614) 0% 100% 31 August 2016

STIP Deferred Equity 67,371 47,160 1 September 2013 (23,580) 0% 100% 31 August 2016

* The % forfeited in the year represents the reduction from the maximum number of performance rights available to vest due to the performance criteria not being achieved.

^ The precise number of performance rights awarded will be determined by dividing the value of the deferred component of the STIP award by the volume weighted average closing price of API shares on the ASX in the 10 day period after announcement of full year results.

DIRECTORS’ REPORTcontinued

Annual Report 2015 Australian Pharmaceutical Industries Limited

23

– The LTIP performance rights granted on 22 February 2013 (2012 grant) lapsed on 31 August 2015 without vesting.

– LTIP performance rights were granted on 10 December 2013 with a performance period commencing on 1 September 2013 and ending 31 August 2016 (the 2013 grant). The performance condition for the exercise of performance rights will be assessed shortly after 31 October 2016. The fair value of the performance rights is dependent upon the ROE performance condition for the entire grant and is $0.46 per share.

– LTIP performance rights were granted on 16 December 2014 with a performance period commencing on 1 September 2014 and ending 31 August 2017 (the 2014 grant). The performance conditions for the exercise of performance rights will be assessed shortly after 31 October 2017. The fair value of the performance rights is dependent upon the ROE and EPS performance conditions for the entire grant and is $0.95 per share.

– Performance rights relating to the STIP program commencing on 1 September 2013 and ending 31 August 2015 were granted on 7 October 2014. The performance rights have been valued at $0.77 per share reflecting the volume weighted average closing price of API shares on the ASX in the 10-day period after announcement of full year results. Performance rights will only vest if the Executive remains employed with the Company at the exercise date subject to forfeiture conditions.

– Performance rights relating to the STIP program commencing on 1 September 2014 and ending 31 August 2016 were granted on 7 October 2015. The precise number of performance rights awarded will be determined by dividing the value of the deferred component of the STIP award by the volume weighted average closing price of API shares on the ASX in the 10 day period after announcement of full year results. Performance rights will only vest if the Executive remains employed with the Company at the exercise date subject to forfeiture conditions.

– The performance rights were provided at no cost to the recipient.

Performance Rights Over equity instrumentsThe movement during the reporting period in the number of performance rights over ordinary shares in Australian Pharmaceutical Industries Limited held directly or beneficially, by each key management person, including their related parties, is as follows:

Held at 1 Sept 14

Granted as Compensation* Exercised

Otherchanges**

Held at 31 Aug 15

Vestedduring

the year

Vested andexercisableat 31 Aug 15

DirectorsMr S P Roche 1,734,862 993,644*** – (957,774) 1,770,732 – –

ExecutivesMr R Vincent 749,839 297,444 – (372,688) 674,595 – –

Mr G Fallet 622,782 – – (622,782) – – –

Held at 1 Sept 13

Granted as Compensation* Exercised

Otherchanges**

Held at 31 Aug 14

Vestedduring

the year

Vested andexercisableat 31 Aug 14

DirectorsMr S P Roche 1,768,935 777,088 – (811,161) 1,734,862 – –

ExecutivesMr R Vincent 671,539 385,277 – (306,977) 749,839 – –

Mr G Fallet 559,178 319,418 – (255,814) 622,782 – –

* Total KMP grants of 1,291,088 of rights over new issue shares were equal to 0.3% of common shares outstanding** Other changes represent performance rights that expired or were forfeited during the year as well as adjustments to deferred STIP performance rights

attributable to the difference between the estimated price and final exercise price as determined by the volume weighted average price in the 10 day period after announcement of the full year results.

No options held by key management personnel are vested but not exercisable at 31 August 2014 or 2015.*** Performance rights with respect to the Company’s Long Term Incentive Plan was approved by shareholders at the 2014 Annual General Meeting held

on 29 January 2015.

24

Australian Pharmaceutical Industries Limited Annual Report 2015

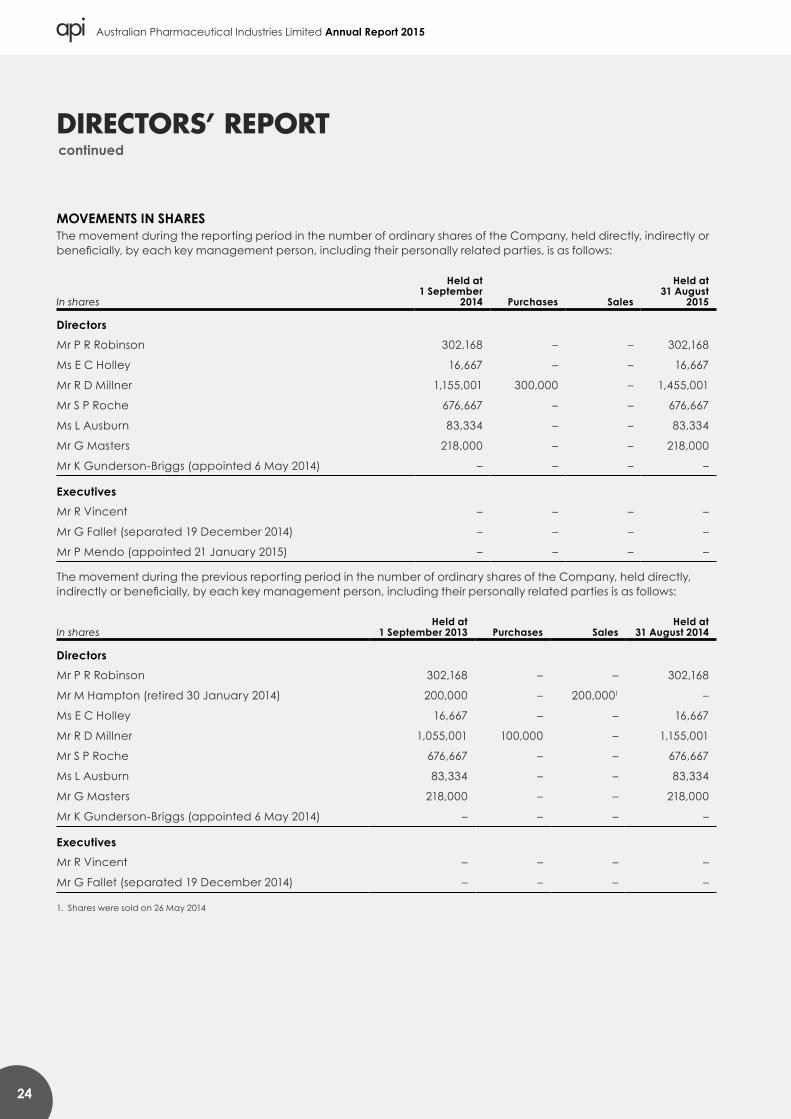

MOVEMENTS IN SHARESThe movement during the reporting period in the number of ordinary shares of the Company, held directly, indirectly or beneficially, by each key management person, including their personally related parties, is as follows:

In shares

Held at 1 September

2014 Purchases Sales

Held at 31 August

2015

DirectorsMr P R Robinson 302,168 – – 302,168

Ms E C Holley 16,667 – – 16,667

Mr R D Millner 1,155,001 300,000 – 1,455,001

Mr S P Roche 676,667 – – 676,667

Ms L Ausburn 83,334 – – 83,334

Mr G Masters 218,000 – – 218,000

Mr K Gunderson-Briggs (appointed 6 May 2014) – – – –

ExecutivesMr R Vincent – – – –

Mr G Fallet (separated 19 December 2014) – – – –

Mr P Mendo (appointed 21 January 2015) – – – –

The movement during the previous reporting period in the number of ordinary shares of the Company, held directly, indirectly or beneficially, by each key management person, including their personally related parties is as follows:

In sharesHeld at

1 September 2013 Purchases SalesHeld at

31 August 2014

DirectorsMr P R Robinson 302,168 – – 302,168

Mr M Hampton (retired 30 January 2014) 200,000 – 200,0001 –

Ms E C Holley 16,667 – – 16,667

Mr R D Millner 1,055,001 100,000 – 1,155,001

Mr S P Roche 676,667 – – 676,667

Ms L Ausburn 83,334 – – 83,334

Mr G Masters 218,000 – – 218,000

Mr K Gunderson-Briggs (appointed 6 May 2014) – – – –

ExecutivesMr R Vincent – – – –

Mr G Fallet (separated 19 December 2014) – – – –

1. Shares were sold on 26 May 2014

DIRECTORS’ REPORTcontinued

Annual Report 2015 Australian Pharmaceutical Industries Limited

25