auto trader consumer survey report 2010

TRANSCRIPT

Consumer Feedback on Key Questions

Facing the Industry

Tim Peake

Commercial DirectorCommercial Director29th September 2010

• Auto Trader collected key questions / concerns from dealers at the beginning of September 2010

• These questions were analysed and the top 15 were incorporated into a survey

• The survey was placed on the Auto Trader Website

• 5,000 consumers responded to the survey between 15th September to 25th September 2010

• The following slides summarise the answers from these consumers

Summary

Research Audit &

Repository Update

Slide 2

• The following slides summarise the answers from these consumers

• The report is intended to help dealers understand how the market may change based on current consumer

sentiment. It will hopefully drive some useful debates within your dealership.

• If you have any further questions or would like further detail / discussions on some of the possible implications

this report outlines, please contact Tim Peake:

• Email; [email protected]

• Phone: 01189 239 103

Consumers confidence is stronger now than 12 months

700,000 more consumers seeking to change their car (based

on Auto Trader 10m unique users)

1.7 million

consumers

950,000

consumers

September 2009 September 2010

800,000

consumers

2.4 million

consumers

Research Audit &

Repository Update

Slide 3

7 million

consumers

6.4 million

consumers

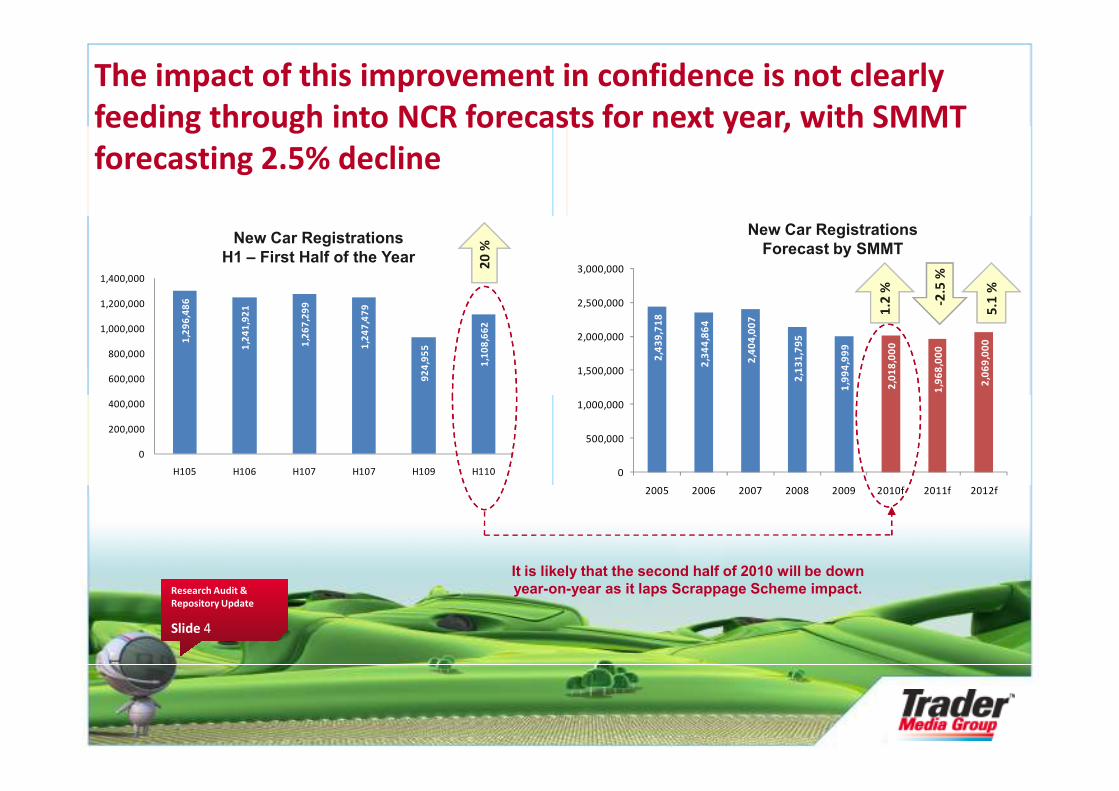

The impact of this improvement in confidence is not clearly

feeding through into NCR forecasts for next year, with SMMT

forecasting 2.5% decline1

,29

6,4

86

1,2

41

,92

1

1,2

67

,29

9

1,2

47

,47

9

92

4,9

55

1,1

08

,66

2

600,000

800,000

1,000,000

1,200,000

1,400,000

New Car Registrations

H1 – First Half of the Year

2,4

39

,71

8

2,3

44

,86

4

2,4

04

,00

7

2,1

31

,79

5

1,9

94

,99

9

2,0

18

,00

0

1,9

68

,00

0

2,0

69

,00

0

1,500,000

2,000,000

2,500,000

3,000,000

New Car Registrations

Forecast by SMMT

20

%

1.2

%

-2.5

%

5.1

%

Research Audit &

Repository Update

Slide 4

0

200,000

400,000

H105 H106 H107 H107 H109 H110 0

500,000

1,000,000

2005 2006 2007 2008 2009 2010f 2011f 2012f

It is likely that the second half of 2010 will be down

year-on-year as it laps Scrappage Scheme impact.

This may be partly explained by Consumers being confused

about the impact of changes in VAT

“Will the VAT increase in January 2011 affect your decision to buy a new/used car?”

Research Audit &

Repository Update

Slide 5

VAT confusion is leading to consumers bringing forward

their purchase

“How will the VAT increase affect your decision to buy a new/used car?”¹ (September 2010)

Planning to buy new car Planning to buy used car

Research Audit &

Repository Update

Slide 6

VAT created a pull forward in demand in the German market when they increased

VAT. VAT increased in Jan 2007, demand in Q4 2006 increased and subsequently

NCR in the following year declined

25%

35%

45%

175,000

275,000

375,000

German New Car Registrations SIS Impact

January 2007 VAT Increase

Impact

January 2007 VAT Increase in Germany (from 16% to 19%) created a dip in purchases post the tax increase day (Q1 down by 10% YoY, Q2

and Q3 -6% and Q4 -13% YoY).

Research Audit &

Repository Update

Slide 7

Source: ACEA (equivalent SMMT in Europe)

-25%

-15%

-5%

5%

15%

-225,000

-125,000

-25,000

75,000

175,000

Jan

-06

Ma

r-0

6

Ma

y-0

6

Jul-

06

Se

p-0

6

No

v-0

6

Jan

-07

Ma

r-0

7

Ma

y-0

7

Jul-

07

Se

p-0

7

No

v-0

7

Jan

-08

Ma

r-0

8

Ma

y-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Ma

r-0

9

Ma

y-0

9

Jul-

09

Se

p-0

9

No

v-0

9

New Car Registrations YoY %

What are the 3 most important criteria when deciding to purchase?

Having the right car at the right price is key to winning new

business

Research Audit &

Repository Update

Slide 8

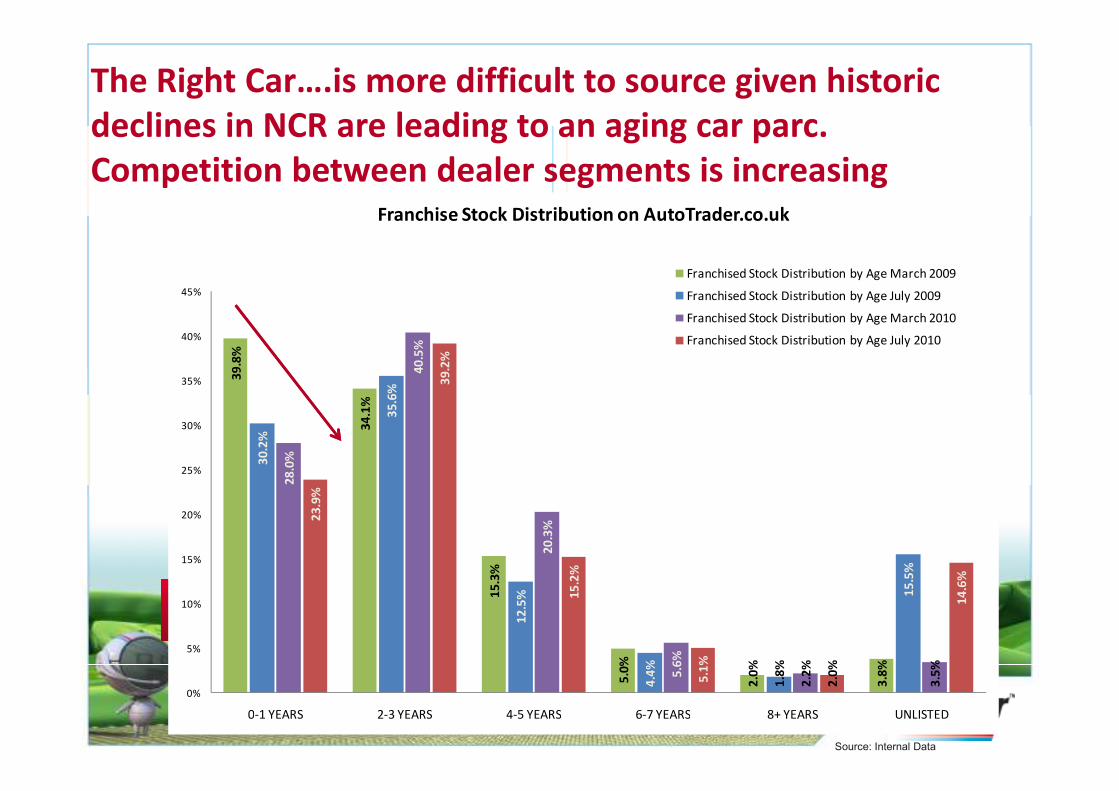

The Right Car….is more difficult to source given historic

declines in NCR are leading to an aging car parc.

Competition between dealer segments is increasing

39

.8%

35

.6%

40

.5%

39

.2%

35%

40%

45%

Franchise Stock Distribution on AutoTrader.co.uk

Franchised Stock Distribution by Age March 2009

Franchised Stock Distribution by Age July 2009

Franchised Stock Distribution by Age March 2010

Franchised Stock Distribution by Age July 2010

Research Audit &

Repository Update

Slide 9

Source: Internal Data

34

.1%

15

.3%

5.0

%

2.0

%

3.8

%

30

.2%

35

.6%

12

.5%

4.4

%

1.8

%

15

.5%

28

.0%

20

.3%

5.6

%

2.2

%

3.5

%

23

.9%

15

.2%

5.1

%

2.0

%

14

.6%

0%

5%

10%

15%

20%

25%

30%

0-1 YEARS 2-3 YEARS 4-5 YEARS 6-7 YEARS 8+ YEARS UNLISTED

The Right Price…..majority of consumers are not prepared

to pay a premium for buying from a franchise dealer

Are you prepared to pay a premium from buying

from a franchise dealer?

Research Audit &

Repository Update

Slide 10

39%

61%

Yes

No

The Right Price….there are regional differences in terms of

what Consumers are prepared to pay as a premium from a

franchise dealer

Research Audit &

Repository Update

Slide 11

The Right Price…..of the 39% that are prepared to pay a

premium 75% are prepared to pay up to £299 and 25% are

prepared to pay more than £299

An additional

£0 - £99

29%

An

additional

£300 - £500

16%

More than £500

extra

10%

Research Audit &

Repository Update

Slide 12

An additional

£100 - £199

25%

An additional

£200 - £299

21%

16%

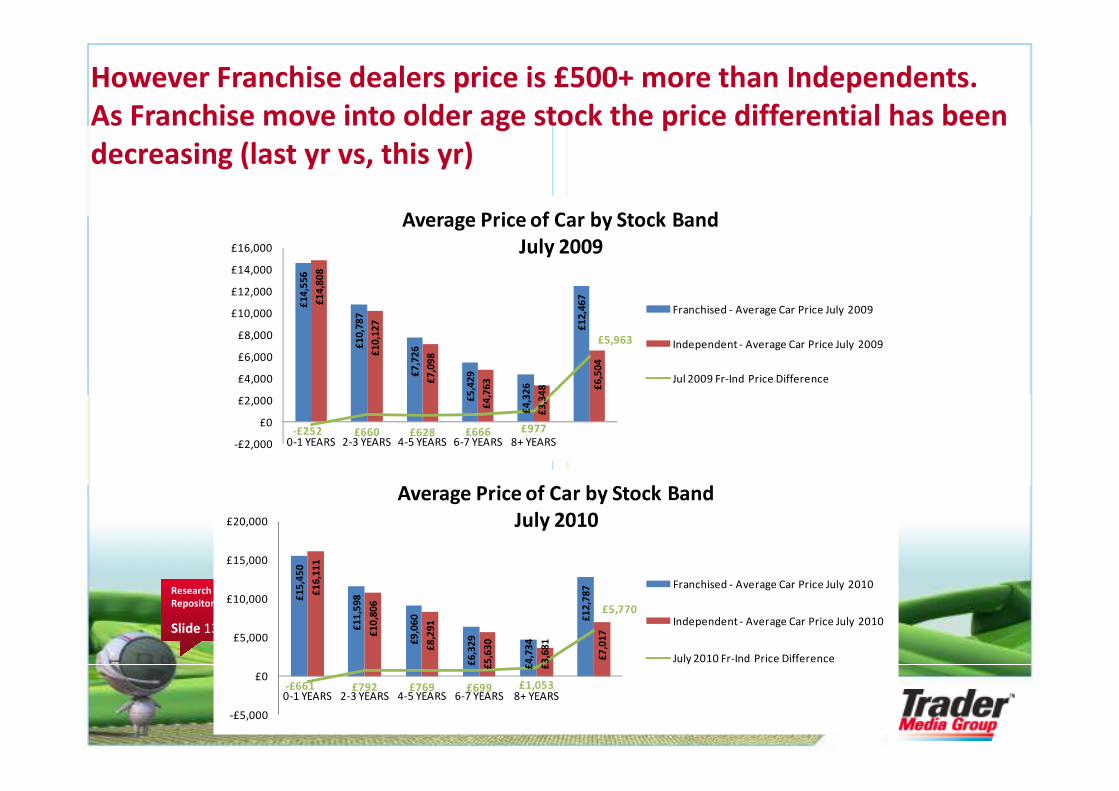

However Franchise dealers price is £500+ more than Independents.

As Franchise move into older age stock the price differential has been

decreasing (last yr vs, this yr)

£1

4,5

56

£1

0,7

87

£7

,72

6

£5

,42

9

£4

,32

6

£1

2,4

67£1

4,8

08

£1

0,1

27

£7

,09

8

£4

,76

3

£3

,34

8 £6

,50

4

£5,963

£2,000

£4,000

£6,000

£8,000

£10,000

£12,000

£14,000

£16,000

Average Price of Car by Stock Band

July 2009

Franchised - Average Car Price July 2009

Independent - Average Car Price July 2009

Jul 2009 Fr-Ind Price Difference

Research Audit &

Repository Update

Slide 13

£5

,42

9

£4

,32

6

£4

,76

3

£3

,34

8

-£252 £660 £628 £666 £977

-£2,000

£0

£2,000

0-1 YEARS 2-3 YEARS 4-5 YEARS 6-7 YEARS 8+ YEARS

£1

5,4

50

£1

1,5

98

£9

,06

0

£6

,32

9

£4

,73

4

£1

2,7

87£1

6,1

11

£1

0,8

06

£8

,29

1

£5

,63

0

£3

,68

1

£7

,01

7

-£661 £792 £769 £699 £1,053

£5,770

-£5,000

£0

£5,000

£10,000

£15,000

£20,000

0-1 YEARS 2-3 YEARS 4-5 YEARS 6-7 YEARS 8+ YEARS

Average Price of Car by Stock Band

July 2010

Franchised - Average Car Price July 2010

Independent - Average Car Price July 2010

July 2010 Fr-Ind Price Difference

Search radius AT.co.uk Consumers who selected a radius when searching

on AT.co.uk (i.e. did not default search to

National)

Furthermore the majority of consumers are searching on a national basis and hence

are exposed to “national prices”. Hence understanding price specifically is key.

Furthermore communicating points of differentiation are even more important

given price transparency (e.g. Trust, Reputation, other products / services).

Research Audit &

Repository Update

Slide 14

Price distribution for Ford Focus 1.6 Zetec 5 dr (climate pack) 07 Plate

Pricing tools are going to become even more important. Market

Tracker provides visibility of AT advertised price, CAP retail and CAP

Trade prices and is updated daily (with AT prices)

Research Audit &

Repository Update

Slide 15

An example of innovation in products and services to build trust is Guaranteed

Buy Back. Of the 17% of consumers who were not planning to buy a car in the

next 12 months, 58% could change their mind if a dealer guaranteed to buy back

their car. Hence using products to build Trust can pull in more consumers

“If a dealer guaranteed to buy back your car for an agreed price in the future, would this influence your decision

to purchase?”

287,000

consumers

Research Audit &

Repository Update

Slide 16

721,000

consumers

691,000

consumers

9% of consumers will not visit a dealership, suggesting they buy from Friends,

family or get someone else to conclude the transaction (could also be online

opportunity)

The majority of Consumers visit between 2-3 dealerships when making a

purchase decision

Research Audit &

Repository Update

Slide 17

“What is the most important quality you look for in a dealership?”

Consumers, when choosing a dealership value reputation, trust and knowledgeable

sales staff (enhances trust)

Pushing manufacturer brands would allow Franchise to win in their segment (1-3 yr

old cars), whilst Independents can price competitively in older age vehicles

Research Audit &

Repository Update

Slide 18

Does dealer branding influence which dealership you buy from?

Consumers are agnostic to dealer brands - 65% outlined the dealer brand is

unimportant

Research Audit &

Repository Update

Slide 19

Source: 1. Top 10 Dealer Concerns Survey launched on autotrader.co.uk September 2010

Franchise

• Price premium achievement is more likely if messaging is based on:

• Trust – manufacturer brand vs. dealer brand vs group – be clear on the value of these

• Reputation – consumer user reviews

• Additional Products – buy back for guaranteed price, increases consumer demand and demand that can

be fulfilled via franchise dealers

• Knowledgeable sales staff

• What justifies the premium (warranty, checks, approved used schemes)

• After sales service

Franchise and Independent need to focus on what differentiates

them to win different types of consumers in the next 12 months

Research Audit &

Repository Update

Slide 20

• After sales service

• Consistent brand messages

• Pricing tools critical

• Independent

• Priced competitively, acknowledging national price transparency

• Pricing tools critical

• Trust, knowledgeable sales staff just as important (£425 spent on used cars after purchase to rectify

problems)

• Ageing car parc, similarities in stock profile make the importance of these points of differentiation critical in

the next 12 months

Creating trust through your website

Research Audit &

Repository Update

Slide 21

Communicating trust via online stock

advertising

Research Audit &

Repository Update

Slide 22

Doing the basics well

Research Audit &

Repository Update

Slide 23

“Would you like to be able to order your new car online?”

3.3 million

consumers

6.3 million

33% of consumers are already prepared to order their new car

(used and new) online….that’s potentially 3.3m transactions

Research Audit &

Repository Update

Slide 24Do sales staff seek to close the transaction on the phone

or do they try and encourage the consumer into the show

room?

6.3 million

consumers

There are regional differences, with 38% of consumers in

London and the South East most likely to order a vehicle

online

“Would you like to be able to order your new car online?”

Research Audit &

Repository Update

Slide 25

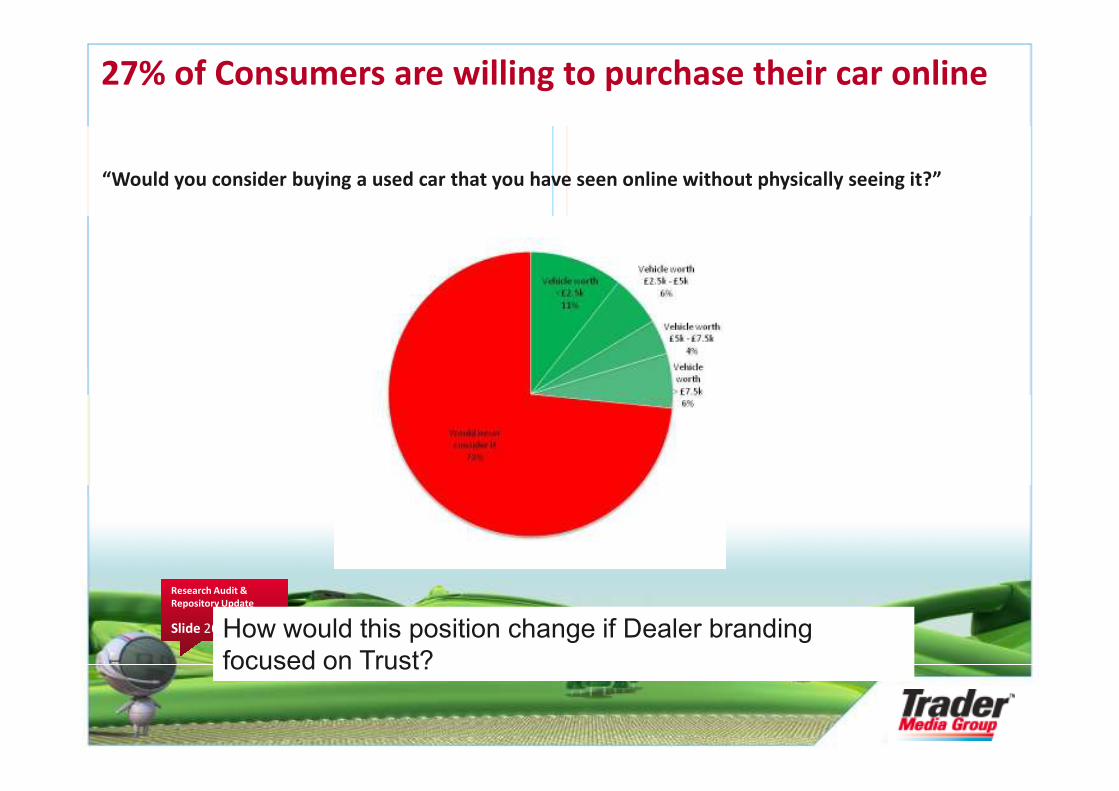

27% of Consumers are willing to purchase their car online

“Would you consider buying a used car that you have seen online without physically seeing it?”

Research Audit &

Repository Update

Slide 26How would this position change if Dealer branding

focused on Trust?

Maximising the opportunity in the next 12

months

There is potentially a large appetite to begin transacting online

The assets required to unlock the opportunity are:Right car, right price (or justification of the right price)

Reputation, Trust , knowledgeable sales staff

Research Audit &

Repository Update

Slide 27

These are the same attributes that consumers value when choosing a

dealership offline

However consumers do not associate these assets with specific dealer brands

Hence the majority are not prepared (or do not necessarily see the benefit) to

pay a premium from a franchise dealer (or pay more from one franchise dealer

than another)

Maximising the opportunity in the next 12

monthsHowever

Trust is built through clear brand messaging (manufacturer brands, groups, dealers - what role

should each play?)

Investment in optimising online advertising is key

Doing the basics well (photos, clear messaging, brand values)

Communicate trust on everything you do - all your advertising

Don’t be afraid of user reviews, consumers are more generous than you think

Research Audit &

Repository Update

Slide 28

Don’t be afraid of user reviews, consumers are more generous than you think

Re-align your thinking on brand

Focus on evolution of products – e.g. guarantee buy-back, builds trust

Fundamentally the market has already changed

The key is to unlock the opportunity by changing the business model to benefit from

the new landscape