automotive electronics & semiconductor market...

TRANSCRIPT

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.© 2016 IHS Markit. All Rights Reserved.

Automotive Electronics &

Semiconductor Market Trends

LIDARs and sensor fusion ECUs advancing ADAS

architectures towards automated driving

The Annual Tokyo SOI Workshop, 2017

Akhilesh Kona, Senior Analyst, Automotive Electronics and Semiconductors

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Agenda

• Automotive electronics and semiconductor market trends

• ADAS architectures towards automated driving

• Current state of ADAS sensor architectures

• Key technologies enabling next-gen ADAS architectures

• Market Outlook & Key Takeaway

2

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

MARITIME& TRADE

ENGINEERING & PRODUCT DESIGN

AEROSPACE,DEFENSE &SECURITY

CHEMICAL

DIGITAL & WEB SOLUTIONS

ECONOMICS &COUNTRY RISKENERGY

FINANCIALMARKETS DATA

& SERVICES

AUTOMOTIVE

OPERATIONAL RISK& REGULATORY

COMPLIANCE

Addressing strategic

challenges with

interconnected

capabilities

We deliver on the promise of

The New Intelligence

IHS Markit provides leaders

from multiple industries with

the perspective and insights

they need to make the best

choices and stay ahead of

their competition.

TECHNOLOGY,MEDIA &TELECOM

© 2016 IHS Markit. All Rights Reserved.

Offices in 34 countries

IHS Markit colleagues

12,000+ 130+

© 2016 IHS Markit. All Rights Reserved.

Automotive market trends

4

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

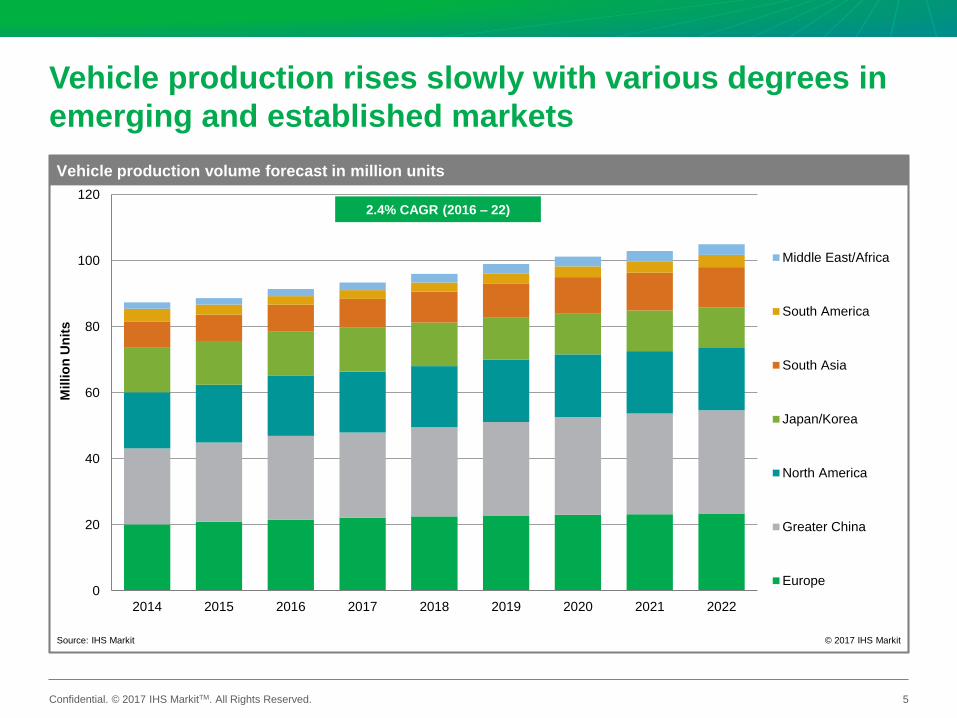

Vehicle production rises slowly with various degrees in

emerging and established markets

0

20

40

60

80

100

120

2014 2015 2016 2017 2018 2019 2020 2021 2022

Chart Title

Middle East/Africa

South America

South Asia

Japan/Korea

North America

Greater China

Europe

Vehicle production volume forecast in million units

© 2017 IHS Markit

Millio

n U

nit

s

Source: IHS Markit

5

2.4% CAGR (2016 – 22)

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

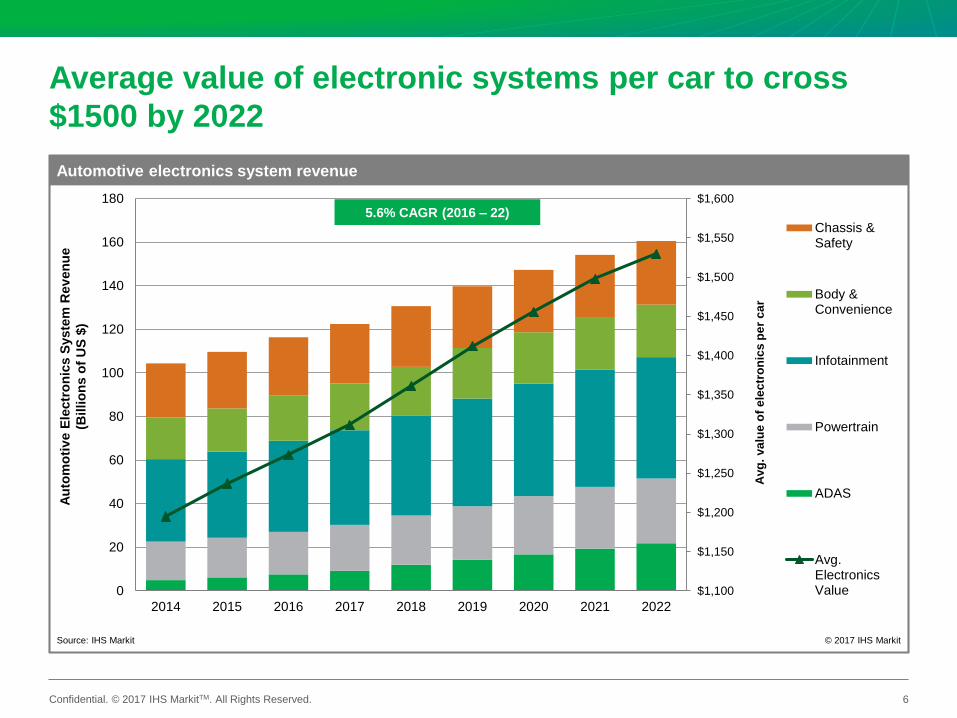

Average value of electronic systems per car to cross

$1500 by 2022

$1,100

$1,150

$1,200

$1,250

$1,300

$1,350

$1,400

$1,450

$1,500

$1,550

$1,600

0

20

40

60

80

100

120

140

160

180

2014 2015 2016 2017 2018 2019 2020 2021 2022

Avg

. va

lue

of

ele

ctr

on

ics

pe

r c

ar

Chart Title

Chassis &Safety

Body &Convenience

Infotainment

Powertrain

ADAS

Avg.ElectronicsValue

Automotive electronics system revenue

© 2017 IHS Markit

Au

tom

oti

ve E

lectr

on

ics S

yste

m R

ev

en

ue

(Billio

ns o

f U

S $

)

Source: IHS Markit

6

5.6% CAGR (2016 – 22)

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

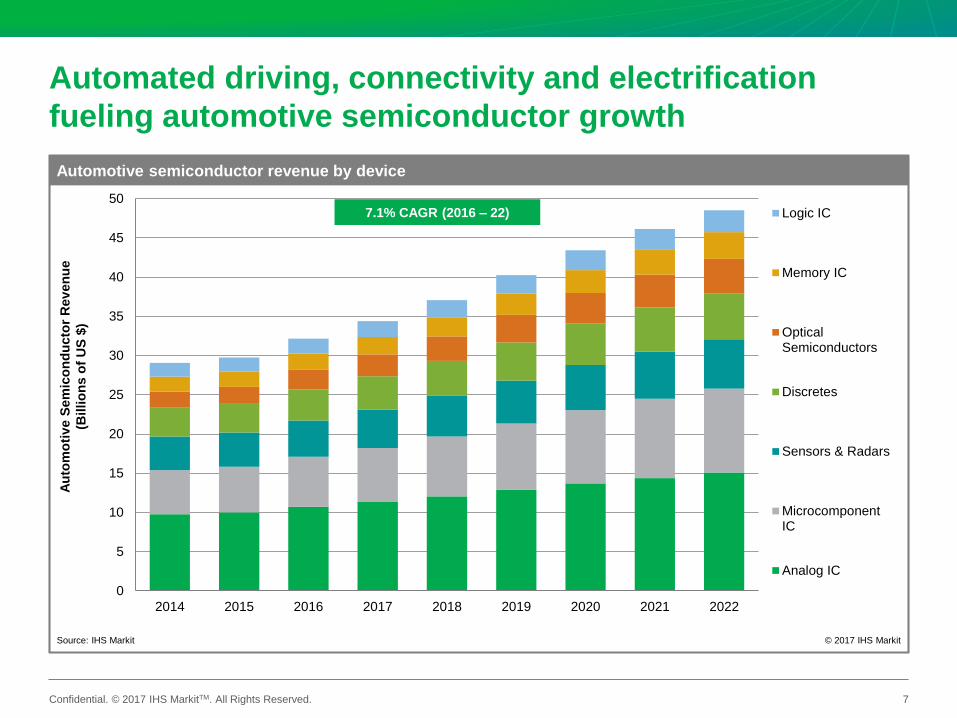

Automated driving, connectivity and electrification

fueling automotive semiconductor growth

0

5

10

15

20

25

30

35

40

45

50

2014 2015 2016 2017 2018 2019 2020 2021 2022

Chart Title

Logic IC

Memory IC

OpticalSemiconductors

Discretes

Sensors & Radars

MicrocomponentIC

Analog IC

Automotive semiconductor revenue by device

© 2017 IHS Markit

Au

tom

oti

ve S

em

ico

nd

ucto

r R

ev

en

ue

(Billio

ns o

f U

S $

)

Source: IHS Markit

7

7.1% CAGR (2016 – 22)

© 2016 IHS Markit. All Rights Reserved.

Current state of ADAS

architectures

8

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

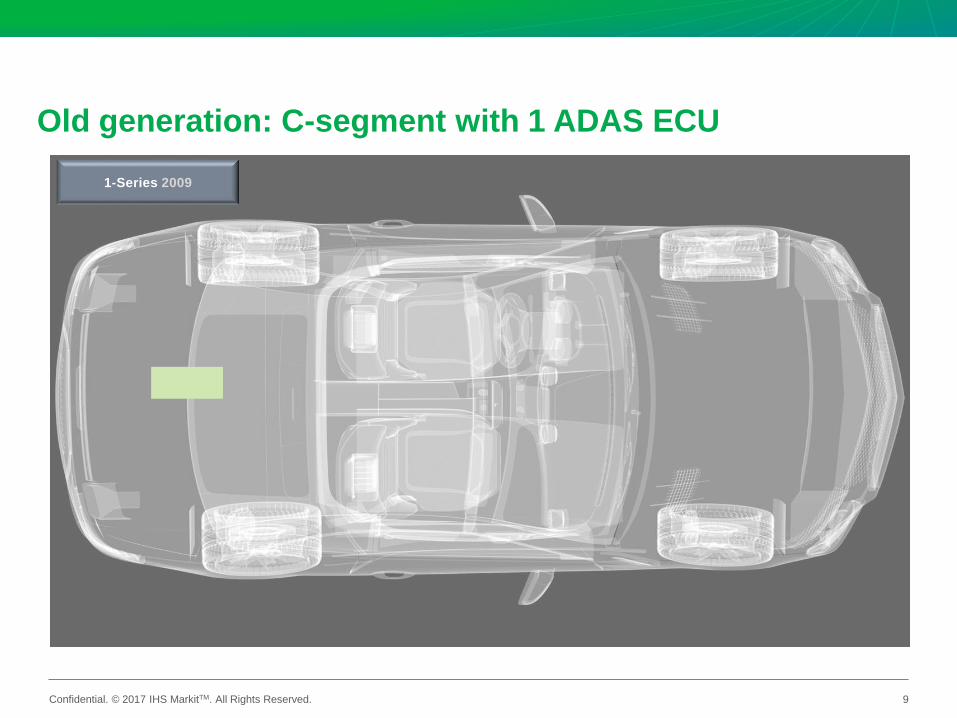

Old generation: C-segment with 1 ADAS ECU

1-Series 2009

9

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

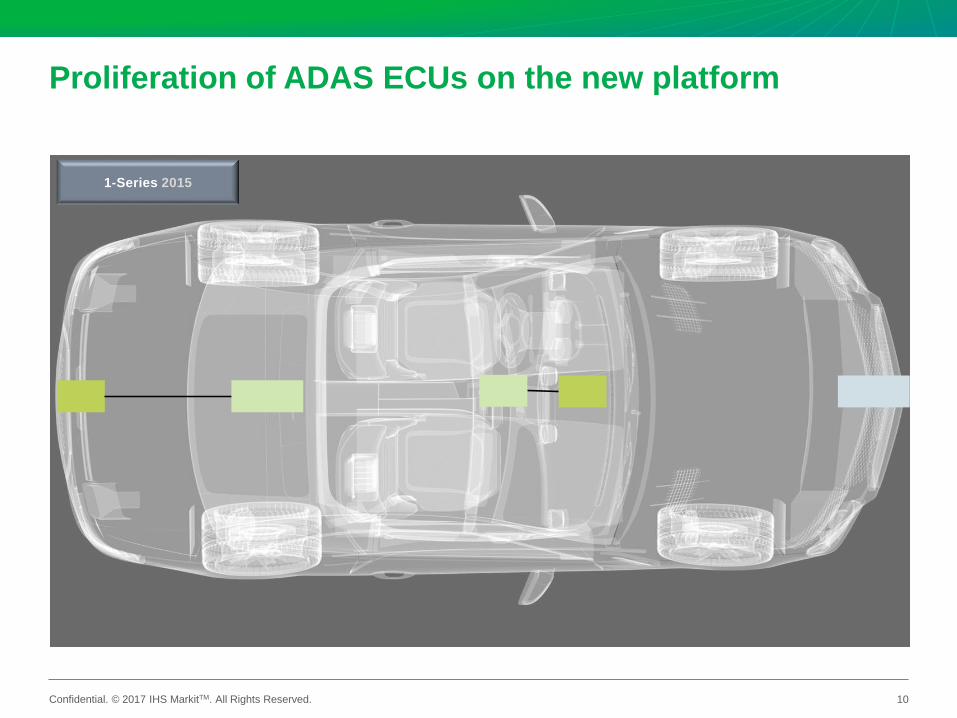

Proliferation of ADAS ECUs on the new platform

10

1-Series 2015

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

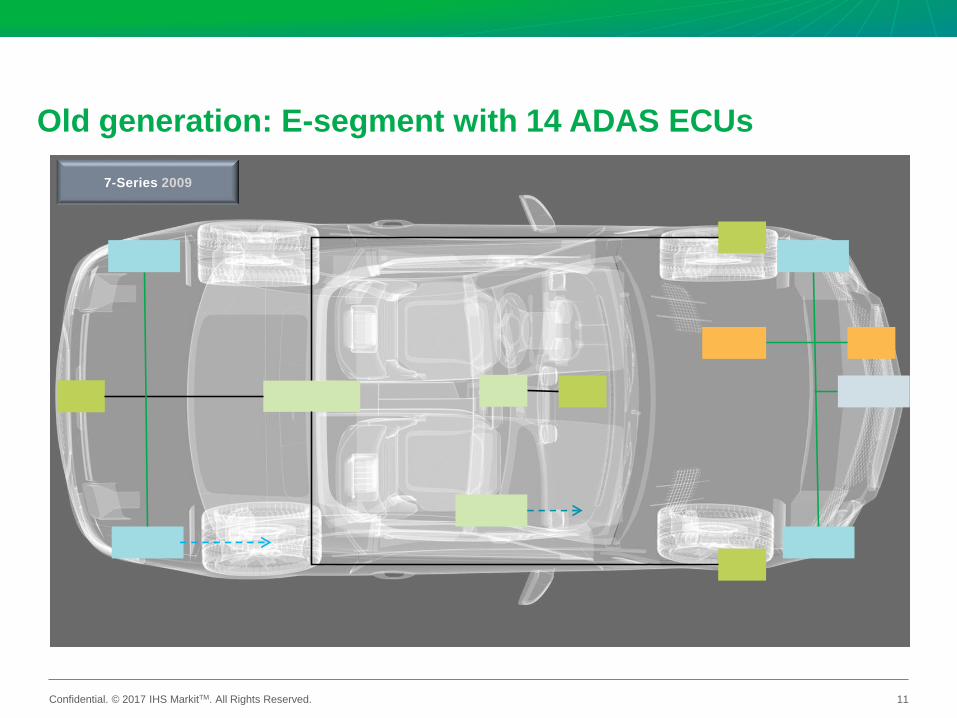

Old generation: E-segment with 14 ADAS ECUs

11

7-Series 2009

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

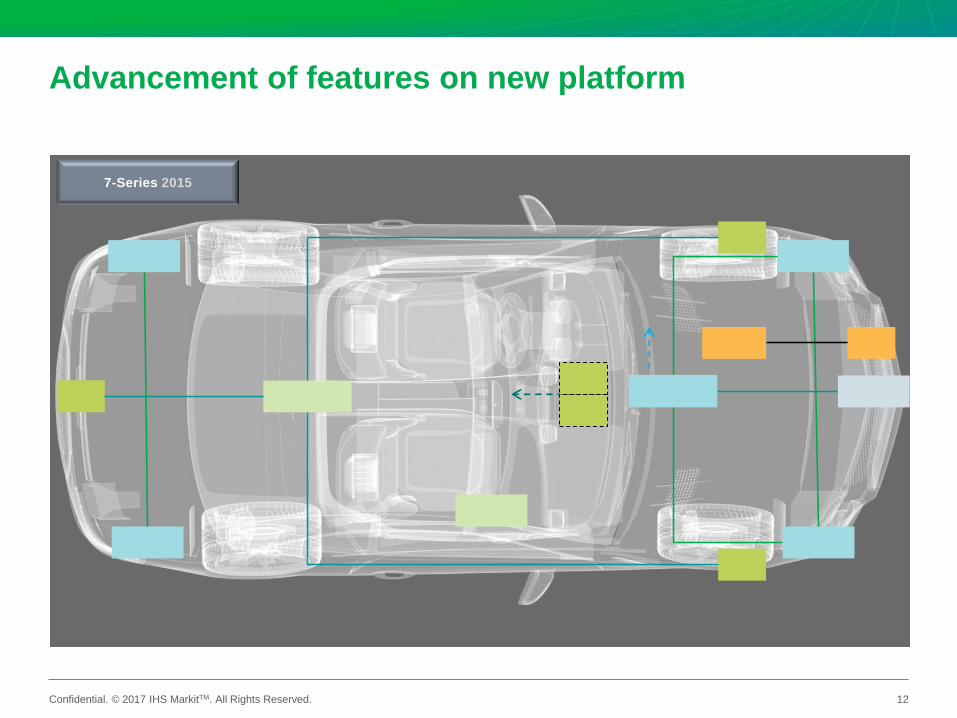

Advancement of features on new platform

12

7-Series 2015

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

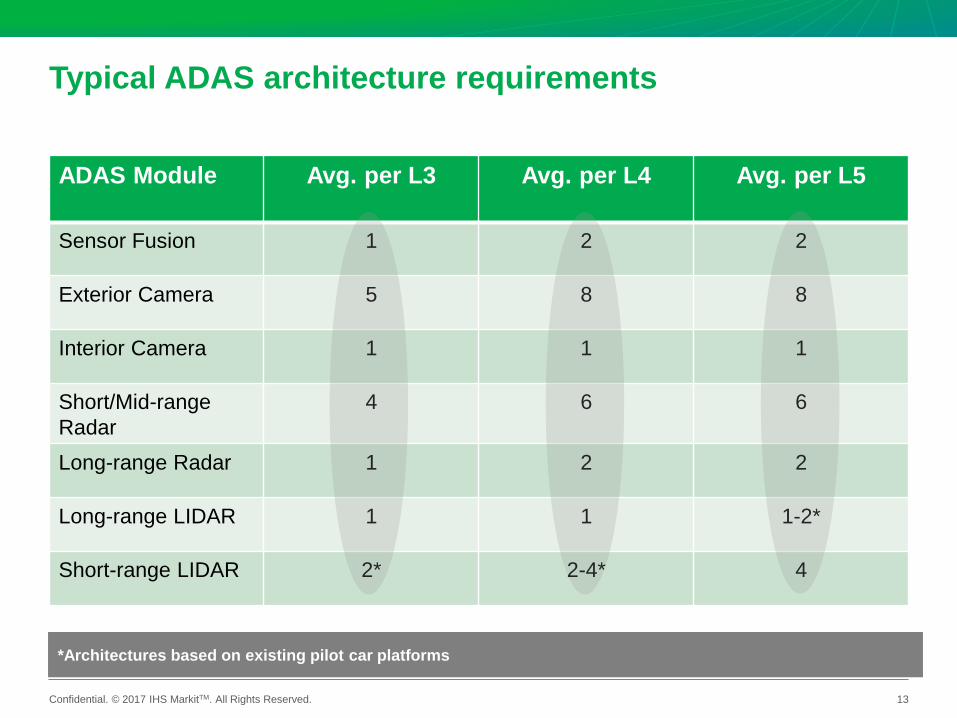

Typical ADAS architecture requirements

ADAS Module Avg. per L3 Avg. per L4 Avg. per L5

Sensor Fusion 1 2 2

Exterior Camera 5 8 8

Interior Camera 1 1 1

Short/Mid-range

Radar

4 6 6

Long-range Radar 1 2 2

Long-range LIDAR 1 1 1-2*

Short-range LIDAR 2* 2-4* 4

13

*Architectures based on existing pilot car platforms

© 2016 IHS Markit. All Rights Reserved.

Key technologies enabling next-

generation ADAS architectures

14

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

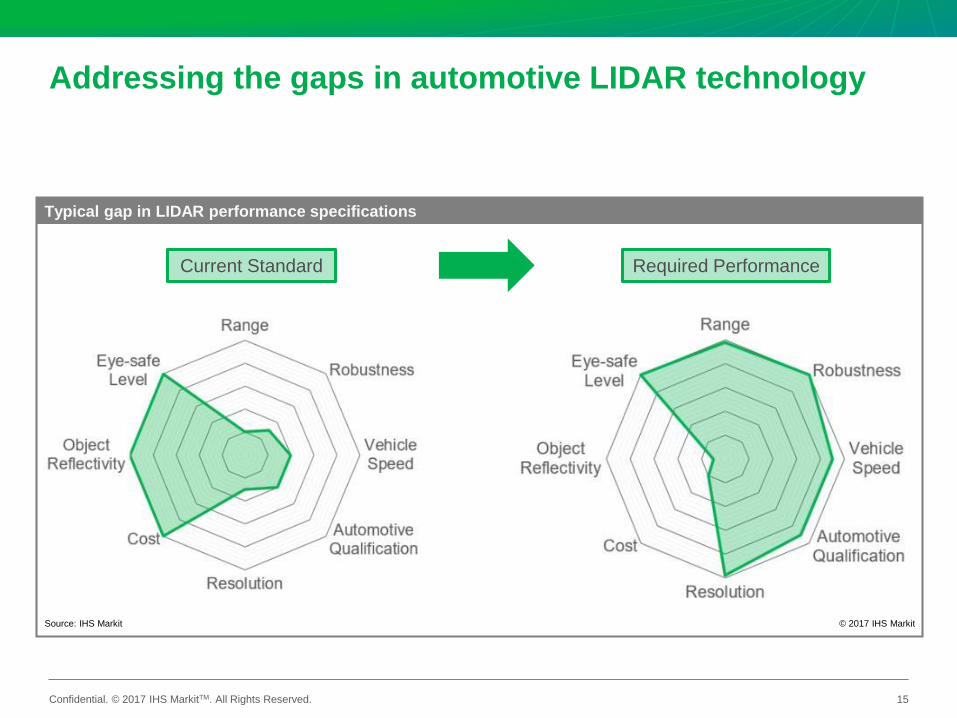

Addressing the gaps in automotive LIDAR technology

Typical gap in LIDAR performance specifications

© 2017 IHS MarkitSource: IHS Markit

15

LIDAR

Current Standard Required Performance

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

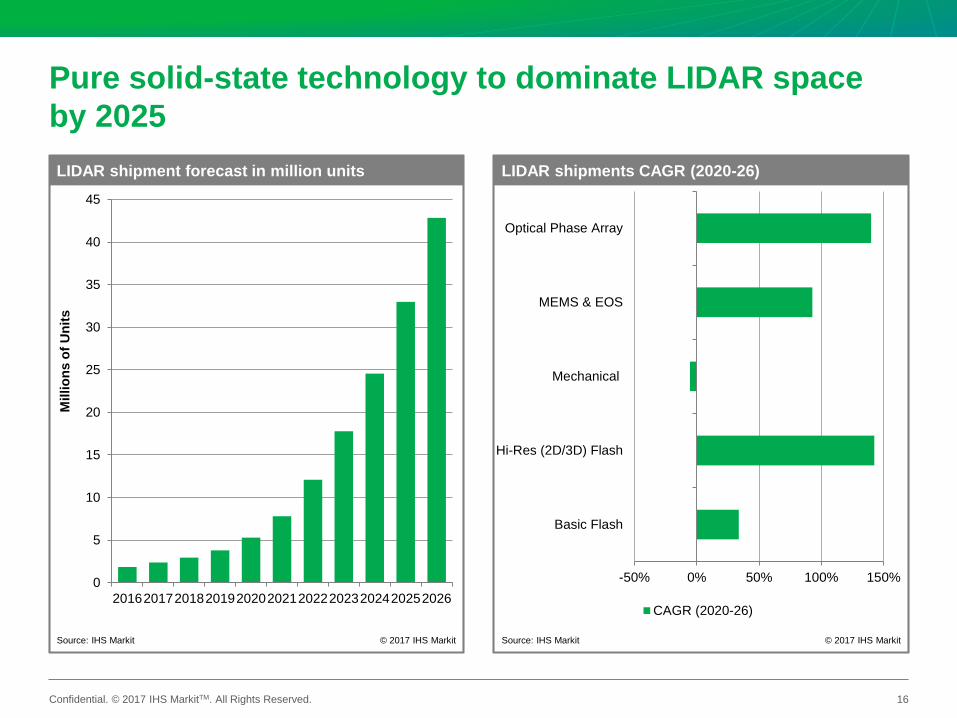

Pure solid-state technology to dominate LIDAR space

by 2025

0

5

10

15

20

25

30

35

40

45

20162017201820192020202120222023202420252026

LIDAR shipment forecast in million units

© 2017 IHS Markit

Millio

ns o

f U

nit

s

Source: IHS Markit

-50% 0% 50% 100% 150%

Basic Flash

Hi-Res (2D/3D) Flash

Mechanical

MEMS & EOS

Optical Phase Array

CAGR (2020-26)

LIDAR shipments CAGR (2020-26)

© 2017 IHS MarkitSource: IHS Markit

16

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

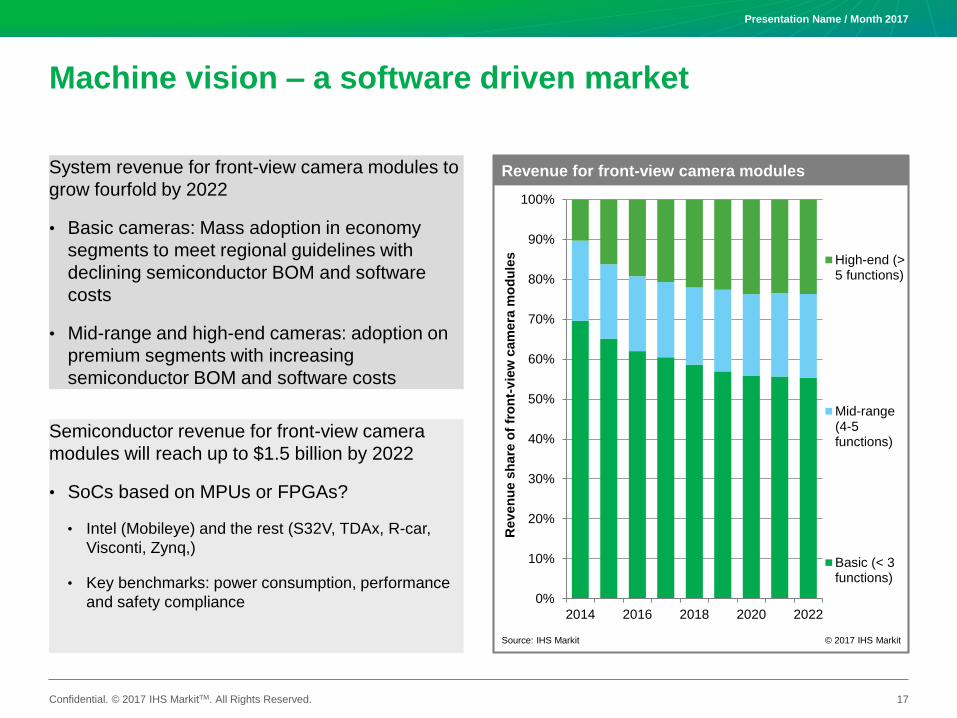

Machine vision – a software driven market

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2014 2016 2018 2020 2022

High-end (>5 functions)

Mid-range(4-5functions)

Basic (< 3functions)

Revenue for front-view camera modules

© 2017 IHS Markit

Rev

en

ue s

hare

of

fro

nt-

vie

w c

am

era

mo

du

les

Source: IHS Markit

System revenue for front-view camera modules to

grow fourfold by 2022

• Basic cameras: Mass adoption in economy

segments to meet regional guidelines with

declining semiconductor BOM and software

costs

• Mid-range and high-end cameras: adoption on

premium segments with increasing

semiconductor BOM and software costs

Semiconductor revenue for front-view camera

modules will reach up to $1.5 billion by 2022

• SoCs based on MPUs or FPGAs?

• Intel (Mobileye) and the rest (S32V, TDAx, R-car,

Visconti, Zynq,)

• Key benchmarks: power consumption, performance

and safety compliance

Presentation Name / Month 2017

17

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

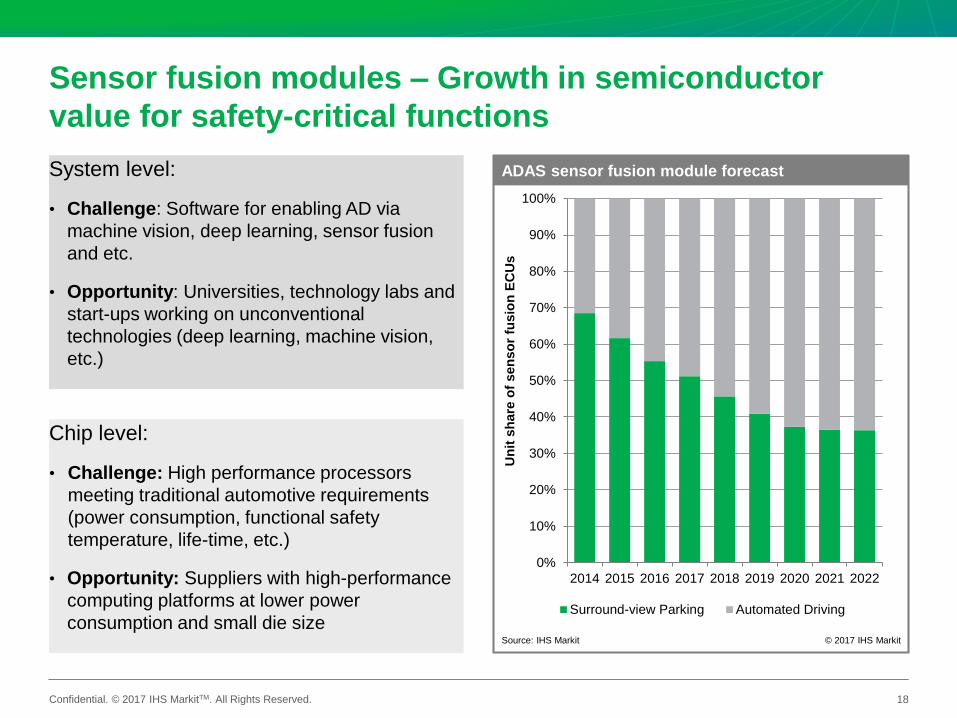

Sensor fusion modules – Growth in semiconductor

value for safety-critical functions

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2014 2015 2016 2017 2018 2019 2020 2021 2022

Surround-view Parking Automated Driving

ADAS sensor fusion module forecast

© 2017 IHS Markit

Un

it s

hare

of

sen

so

r fu

sio

n E

CU

s

Source: IHS Markit

System level:

• Challenge: Software for enabling AD via

machine vision, deep learning, sensor fusion

and etc.

• Opportunity: Universities, technology labs and

start-ups working on unconventional

technologies (deep learning, machine vision,

etc.)

Chip level:

• Challenge: High performance processors

meeting traditional automotive requirements

(power consumption, functional safety

temperature, life-time, etc.)

• Opportunity: Suppliers with high-performance

computing platforms at lower power

consumption and small die size

18

© 2016 IHS Markit. All Rights Reserved.

Market Outlook & Key takeaway

19

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

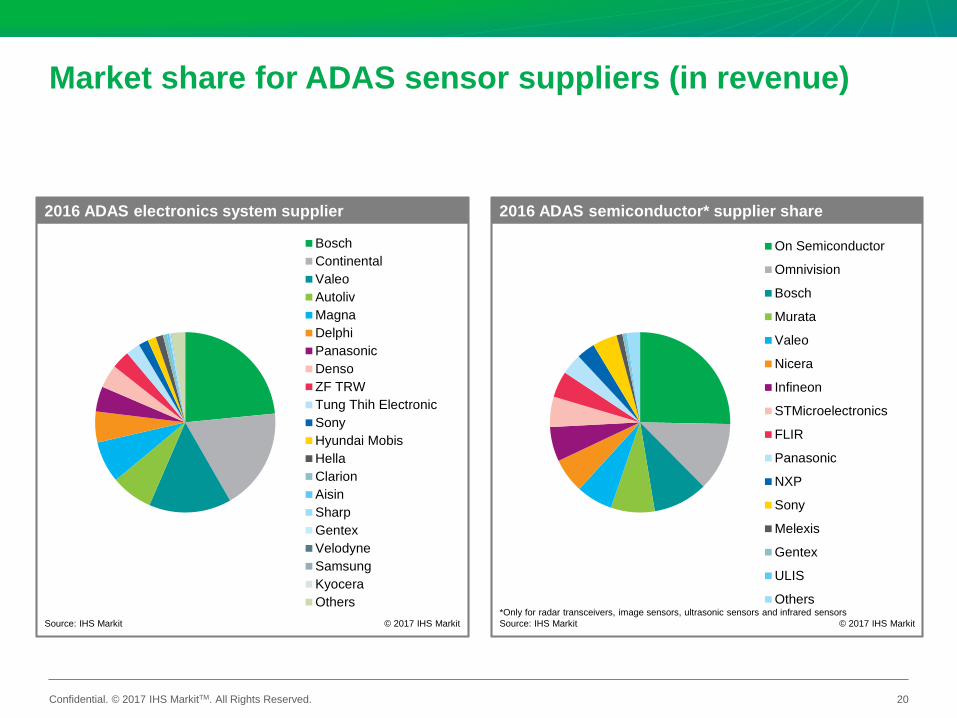

Market share for ADAS sensor suppliers (in revenue)

Bosch

Continental

Valeo

Autoliv

Magna

Delphi

Panasonic

Denso

ZF TRW

Tung Thih Electronic

Sony

Hyundai Mobis

Hella

Clarion

Aisin

Sharp

Gentex

Velodyne

Samsung

Kyocera

Others

2016 ADAS electronics system supplier

© 2017 IHS MarkitSource: IHS Markit

20

On Semiconductor

Omnivision

Bosch

Murata

Valeo

Nicera

Infineon

STMicroelectronics

FLIR

Panasonic

NXP

Sony

Melexis

Gentex

ULIS

Others

2016 ADAS semiconductor* supplier share

© 2017 IHS Markit

*Only for radar transceivers, image sensors, ultrasonic sensors and infrared sensors

Source: IHS Markit

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Key Takeaways

• Economy vehicle segments – proliferation of

sensors and ECUs for compliance (NCAPs,

NHTSA,..).

• Premium vehicle segments – Addition of

LIDARS and high-end sensor fusion modules

for automated driving.

• No compromise on sensor technology for

automated driving – redundancy is a must.

• Functional safety and performance for

autonomy will drive the semiconductor

growth through artificial intelligence and

sensor fusion.

• Consolidation of ECUs to drive high-

performance computing platforms.

21

IHS Markit Customer Care

Americas: +1 800 IHS CARE (+1 800 447 2273)

Europe, Middle East, and Africa: +44 (0) 1344 328 300

Asia and the Pacific Rim: +604 291 3600

Disclaimer

The information contained in this presentation is confidential. Any unauthorized use, disclosure, reproduction, or dissemination, in full or in part, in any media or by any

means, without the prior written permission of IHS Markit Ltd. or any of its affiliates ("IHS Markit") is strictly prohibited. IHS Markit owns all IHS Markit logos and trade names

contained in this presentation that are subject to license. Opinions, statements, estimates, and projections in this presentation (including other media) are solely those of the

individual author(s) at the time of writing and do not necessarily reflect the opinions of IHS Markit. Neither IHS Markit nor the author(s) has any obligation to update this

presentation in the event that any content, opinion, statement, estimate, or projection (collectively, "information") changes or subsequently becomes inaccurate. IHS Markit

makes no warranty, expressed or implied, as to the accuracy, completeness, or timeliness of any information in this presentation, and shall not in any way be liable to any

recipient for any inaccuracies or omissions. Without limiting the foregoing, IHS Markit shall have no liability whatsoever to any recipient, whether in contract, in tort (including

negligence), under warranty, under statute or otherwise, in respect of any loss or damage suffered by any recipient as a result of or in connection with any information

provided, or any course of action determined, by it or any third party, whether or not based on any information provided. The inclusion of a link to an external website by IHS

Markit should not be understood to be an endorsement of that website or the site's owners (or their products/services). IHS Markit is not responsible for either the content or

output of external websites. Copyright © 2017, IHS MarkitTM. All rights reserved and all intellectual property rights are retained by IHS Markit.

Presentation Name / Month 2017

Thank You!