automotive global sales and production...

TRANSCRIPT

© 2016 IHS Markit. All Rights Reserved.© 2016 IHS Markit. All Rights Reserved.

Global Sales and Production RedefinedAUTOMOTIVE

Mark Fulthorpe, Director Light Vehicle Production, +44 203 159 3474, [email protected]

19 October 2016 | Tokyo

© 2016 IHS Markit

Contents Global outlook for vehicle production Fundamental changes in a fast moving world

The new mobility Emerging trends

Flexible production New platform dynamics

Summary

2

Presentation Name / Month 2016

© 2016 IHS Markit 3

ProductWhich products will be

strategic to future growth?

VolumeWhere should you expand your production footprint?

ManufacturingIndustrial trends shaping the

automotive industry

RANGE FLEXIBILTY

INDUSTRIAL FLEXIBILTY

MARKETFLEXIBILTY

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

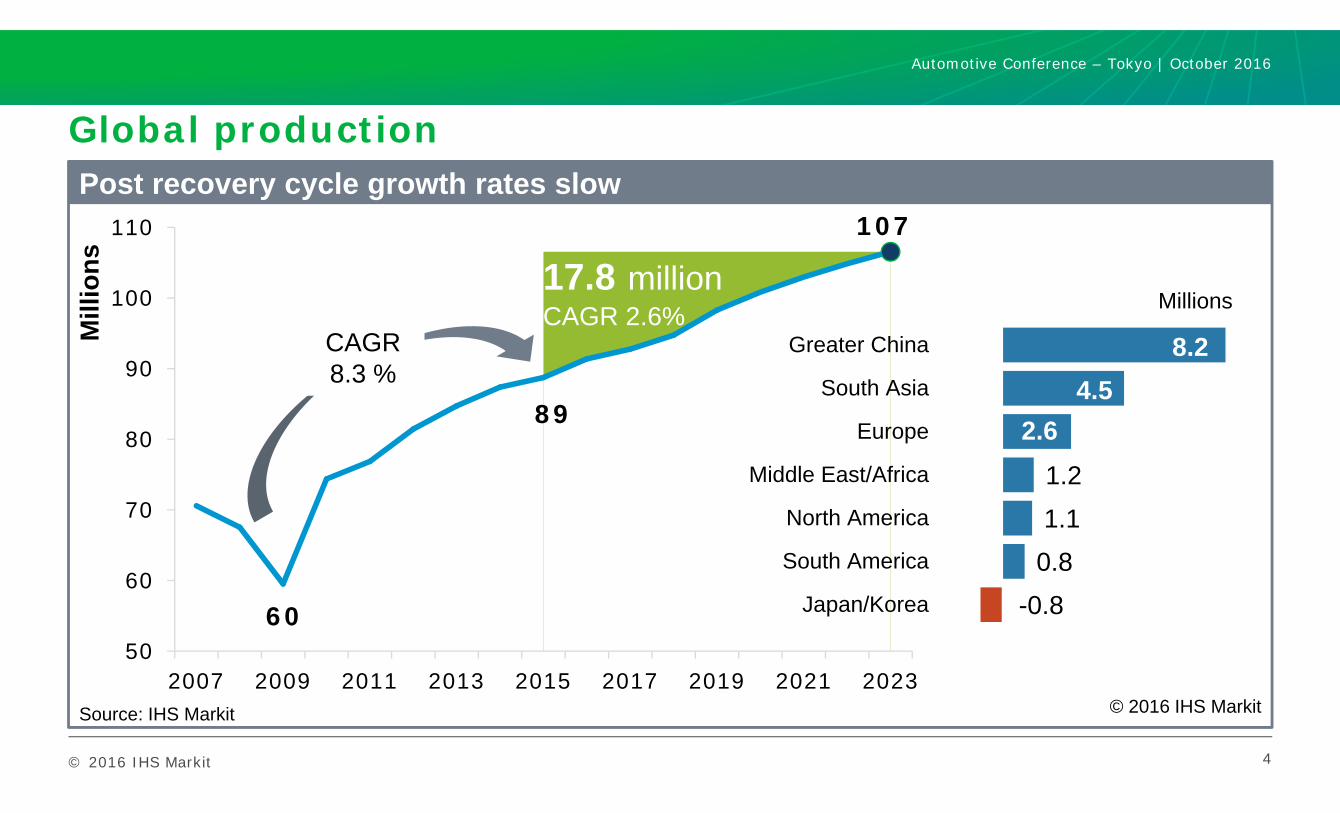

Global production

4

60

89

107

50

60

70

80

90

100

110

2007 2009 2011 2013 2015 2017 2019 2021 2023

Mill

ions 17.8 millionCAGR 2.6%

8.24.5

2.61.21.1

0.8-0.8

Greater China

South Asia

Europe

Middle East/Africa

North America

South America

Japan/Korea

Millions

Post recovery cycle growth rates slow

© 2016 IHS MarkitSource: IHS Markit

Automotive Conference – Tokyo | October 2016

CAGR8.3 %

© 2016 IHS Markit 5

China

0

5

10

15

20

25

30

35

2007 2009 2011 2013 2015 2017 2019 2021 2023

Mill

ions

• Economic pressures slow growth rates to ‘new normal’ levels

• Government intervention to support no less than 6.5% GDP

• Latest 5-Year Plan will boost infrastructure, NEVs and sharing economy

• Second child and regional planning to balance long term outlook

• Urbanization to accommodate cleaning of manufacturing and lower carbon development

Automotive Conference – Tokyo | October 2016

Growth moderates as pressures build; focus on technology

© 2016 IHS Markit.Source: IHS Markit

© 2016 IHS Markit 6

Brazil, Russia, India and ASEAN

0

1

2

3

4

5

6

7

8

2007 2009 2011 2013 2015 2017 2019 2021 2023

Mill

ions

• Brazil and Russia face prolonged recessions; signs of hitting the floor only just emerging

• Failure to diversify into exports during expansion years limits ability to offset domestic weakness

• India realising potential after political impasse; infrastructure investments to pay off

• ASEAN has slowed but exports have helped and AEC could provide stimulus and bolster existing regional hubs

Automotive Conference – Tokyo | October 2016

Reset the map; Brazil and Russia lose momentum

© 2016 IHS MarkitSource: IHS Markit

© 2016 IHS Markit

0

2

4

6

8

10

12

14

2007 2009 2011 2013 2015 2017 2019 2021 2023

Mill

ions

7

North America

• Strong recovery cycle in US sees post-crisis restructuring pay off, greater capacity discipline, platform alignment and renewed focus on exports

• GM, FCA unwind Canada footprint volume moves south

• Mexico set for another phase of investment from D3, Asians and Europeans

• Localization overseas and domestic ceiling will cap growth in this cycle

Automotive Conference – Tokyo | October 2016

Mexico pushes region to new highs but plateau coming soon

© 2016 IHS MarkitSource: IHS Markit

© 2016 IHS Markit 8

Europe

0

1

2

3

4

5

6

7

2007 2009 2011 2013 2015 2017 2019 2021 2023

Mill

ions

• Big 5 western European producers supported by strengthened domestic recovery but Brexit poses risks

• Exports to North America remain robust but China capacity investments will that flow

• Increased movement across the region reflects enhanced flexibility and willingness to change

• Central Europe gains: Daimler Hungary, FCA, GM, Poland, JLR Slovakia, VW Slovakia, Poland

Automotive Conference – Tokyo | October 2016

Flexibility key and Central Europe becomes attractive again

© 2016 IHS MarkitSource: IHS Markit

CentralEurope

© 2016 IHS Markit

Brexit the global risk

9

Automotive Conference – Tokyo | October 2016

Europe -1.0 MnChina -680k

MEA -420k

North America -550k

South America -280k JPN/KOR -150k

South Asia -280k

UK -1.2 MnCumulative adjusted demand 2016 to 2023

© 2016 IHS Markit

Brexit impact on UK production – initial analysisBrexit event UK car market UK auto plantsImpact area Issue Scenario Short term

(1-2 years)Long Term(3+ years)

Short term(1-2 years)

Long term(3+ years)

Macro GDP unwind - - - - - =

Interest rates lower - - - =

Currency £/€ £/$ depreciation - - - - / = + + / =

MarketAccess

Tech regsTrade rules

Keep & copyTrade agreement

==

=-/=

==

-- /=

Labour market Labour laws Lighter = = = +

Skilled migration

Tighter = - / = = -

Bottom line - - - = - / =

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

Brexit exposure UK operations

11

Nissan-Sunderland520,000 units

Current cycle Jun 2021

GM-Ellesmere Port110,000 units

Current cycle Dec 2021

JLR-Halewood180,000 units

Current cycle Mar 2022

Bentley-Crewe13,000 units

Current cycle Jun 2023

Toyota- Derby167,000 units

Current cycle Mar 2019

JLR-Castle Bromwich; Solihull 405,000 units

Current cycle Mar 2023

BMW-Oxford206,000 units

Current cycle Jun 2022

Honda-Swindon144,000 units

Current cycle Jun 2022

BMW-Goodwood4,400 unitsCurrent cycle Dec 2021

GM-Luton 76,000 unitsCurrent cycle Mar 2026

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit 12

Japan/Korea

0

2

4

6

8

10

12

2007 2009 2011 2013 2015 2017 2019 2021 2023

Mill

ions

• Following short term stimulus/disruption in both markets as the result of consumption tax cuts long term return to trend of decline and stagnation.

• Japanese OEMs pick up overseas growth hedge to currency movements despite recent support for exports

• Hyundai/Kia pursues expansion; NA and India mix mature and emerging

Automotive Conference – Tokyo | October 2016

Domestic output constrained; overseas expansion dominates

© 2016 IHS MarkitSource: IHS Markit

© 2016 IHS Markit

OEM growth distribution 2015 to 2023

13

Renault/Nissan+2.4Mn

+3.2% p.a. *

Volkswagen+1.8Mn

+2.1% p.a.

11.2+M

Hyundai+1.4Mn

+2% p.a.

Toyota+1.2Mn

+1.4% p.a.

Honda+1.0Mn

+2.6% p.a.General Motors+0.9Mn

+1.3% p.a.

Suzuki+0.6Mn

+2.7% p.a.

Daimler+0.6Mn

+2.6% p.a

PSA+0.6Mn

+2.1% p.a.

FCA+0.4Mn

+1% p.a.

BMW+0.4Mn

+2% p.a.

Ford+0.4Mn

+0.7% p.a.

China

India ASEAN

Mature

Rest of World

Automotive Conference – Tokyo | October 2016

* p.a. = per annum

© 2016 IHS Markit

Contents Global outlook for vehicle sales Fundamental changes in a fast moving world

The new mobility Emerging trends

Flexible production New platform dynamics

Summary

14

Presentation Name / Month 2016

© 2016 IHS Markit

Public Transit VMT

Changes

Economy Oil Prices

Technology

New business models

will materialize

Mobility will be

redefined

Technology and society drive fundamental

change

VMT = Vehicle miles travelled

The future mobility jigsaw is starting to fall into place

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

Future mobility patterns emerging (1/2)

• Rapid increase in expectation of disruption of traditional business models as new personal mobility options emerge and evolve

KPMG Survey* - 82% of execs now say a major business model disruption is ‘extremely likely’ or ‘somewhat likely’ – it was just 12% last year

only 33% think that current OEMs will retain customer relationship – it was 75% last year

IBM survey** suggests by 2025 personal mobility developments could become more important than economic and market trends

66% of consumers say they expect new types of ownership models to be offered

16

Automotive Conference – Tokyo | October 2016

* Source: KPMG Global Automotive Executive Survey 2016

** Source: IBM Automotive 2025: Industry Without Borders 2015

© 2016 IHS Markit

Future mobility patterns emerging (2/2)

• Developed market car cultures have embedded inertia to fast and fundamental change, Emerging market consumers are far more open to new modes

Preference of traditional ownership to a car as a service model: US/Europe ~ 40-50% , Rest of World ~30%, China/India ~20% (KMPG Survey)

IBM survey – EM’s showed 20-25% higher declared interest in ‘mobility solutions’ than Mature markets

Stated ‘interest’ in self driving cars lowest in mature markets , highest in emerging markets (Japan and Brazil are exceptions to both)

• Premium’s chances? Potential impact on premium is equally questioned as it is for low cost manufacturers

“The important image attached to a car seems to lose significant importance in a future dominated by sophisticated mobility services” (KPMG survey ‘editorial’)

17

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit 18

New mobility megatrends converge to a potential ‘Giga-Trend’

New customers Disruptors

Car-Share Ride-Share

Traditional Ownership model (CaaP)

Sharing Economy(CaaS)

Driver is Person

Automated

(CaaRobot)

Autonomous

L5

Gre

ates

t dis

rupt

or

to A

utom

otiv

e In

dust

ry

New Form of mobility

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit 19

New manufacturing required…

Automotive Conference – Tokyo | October 2016

Greater product customisation?

Greater regional diversity?

Brand values re-imagined?

Increasing need to build closer to consumers?

Current scale models too rigid?

Product cadence likely to accelerate further?

© 2016 IHS Markit

Contents Global outlook for vehicle production Fundamental changes in a fast moving world

The new mobility Emerging trends

Flexible production New platform dynamics

Summary

20

Presentation Name / Month 2016

© 2016 IHS Markit 21

Reduced purchasing costs and

accelerated development

times

Increased flexibility and product

cadence compared to traditional

floorpan and top hat

Suppliers will need to support

volume and geographic

requirements

OEMs purchasing strategies have

been driving consolidation in the

supplier sector

Global platforms will support 69% of new light vehicle production by 2023

Age of the Mega Platform

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

Age of the Mega Platform

2

4

6

5 5

3

5

3 3 3

7

3

0.0

0.2

0.4

0.6

0.8

1.0

Mill

ions Average volume

per platform2015

Average volumeper platform2023

Number ofplatforms tosupport 80% ofvolume in 2023

22

New architectures drive greater efficiency short term

© 2016 IHS MarkitSource: IHS Markit

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit 23

Does the Volkswagen scandal reveal the next challenges in vehicle production?

“…Mercedes Is About to Unveil an Entire Fleet of Electric Vehicles”

Bloomberg August 2016

“…Electric powertrains will "reinvent the car" says Jaguar design chief”

Autocar April 2016

“…BMW revamps "i" electric car division to focus on self-driving tech”

Reuters June 2016

“…Ford making long-range EV to rival GM, Tesla”Detroit News April 2016

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit 24

New vehicle concepts challenge manufacturing efficiency – importance of flexibility

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit 25

New vehicle usage concepts challenge manufacturing efficiency – importance of flexibility

Personal mobility, short commutes, delivery vehiclesHigh EV penetration

Longer distance, family mobility, outside of city or urban areas, hybridisation still likely to dominate

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

The view from Asia

OEM TargetYear HEV PHEV FCV EV Electrification Strategy

Toyota 2050 ○ ◎ △ ×PHEV is a mainstay, based on the deeply-evolved and widely-spread HEV technology,followed by FCV.

Nissan 2050 △ × ○ ◎Battery EV and range-extender EV aremainstays, followed by the e-Bio Fuel-cellvehicle.

Honda 2050 × ◎ ○ △ PHEV is a mainstay, evolved by the i-MMDhybrid system, followed by FCV (without HEV).

Hyundai 2020 ◎ ○ × △HEV is a mainstay, but the dedicated models willoffer other electrified models such as PHEV andEV.

Definition : ◎=most dependent, ○=dependent, △= less dependent, ×= optional or no development

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

Can modular architectures support greater electrification?

‘Mainstream’ offerings likely to develop concept of complimentary platform structures

27

• It is expected that MQB and MEB will operate hand in hand.

• This “complimentary” platform structure ensures flexibility and planning reliability in either case: BEV boom vs. BEV flop

• Allows OEM to switch or re-balance the production mix of BEV models and more conventional products

MEB (?)“MEB ensures to produce pure electric vehicles, hybrid cars and conventional powertrains, cost efficiently on a single production line! Frank Welsch

Head VW brand R&D, Volkswagen AG

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

Can modular architectures support greater electrification?

28

Needs to be cost efficient! Focused on image and technology, not cost

Automotive Conference – Tokyo | October 2016

© 2016 IHS Markit

Summary

• Extraneous shocks and gathering pace of change forcing genuine re-evaluation of outlook: what will it mean to be in the automotive sector in early 2020s?

• New ownership, operation and usage patterns expected to be a major determining force alongside already identified move to greater fuel efficiency and reduced green house gases

• Customer facing business models changing with balance of power shifting to less ‘core-automotive’ experiences

• Changes will have a tangible effect on manufacturing as OEMs respond to new requirements; greater importance of flexibility over efficiency during transitional steps

• OEM responses will vary challenging existing consensus

29

Automotive Conference – Tokyo | October 2016

IHS MarkitTM COPYRIGHT NOTICE AND DISCLAIMER © 2016 IHS Markit.

No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent of IHS Markit. Content reproduced or redistributed with IHS Markit permission must display IHS Markit legal notices and attributions of authorship. The information contained herein is from sources considered reliable, but its accuracy and completeness are not warranted, nor are the opinions and analyses that are based upon it, and to the extent permitted by law, IHS Markit shall not be liable for any errors or omissions or any loss, damage, or expense incurred by reliance on information or any statement contained herein. In particular, please note that no representation or warranty is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, forecasts, estimates, or assumptions, and, due to various risks and uncertainties, actual events and results may differ materially from forecasts and statements of belief noted herein. This presentation is not to be construed as legal or financial advice, and use of or reliance on any information in this publication is entirely at your own risk. IHS Markit and the IHS Markit logo are trademarks of IHS Markit.

IHS Markit Customer Care:[email protected]: +1 800 IHS CARE (+1 800 447 2273)Europe, Middle East, and Africa: +44 (0) 1344 328 300Asia and the Pacific Rim: +604 291 3600

30

Presentation Name / Month 2016