automotive light vehicle production global highlights - … · automotive light vehicle production...

TRANSCRIPT

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved.

Automotive Light Vehicle Production Global highlights

July 1st 2016 Justin Cox, Head of European Production, LMC Automotive

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 2

Outline

Macro

Global highlights: China, Europe, Russia, Brazil, N America

Capacity ‘Health Check’

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 3

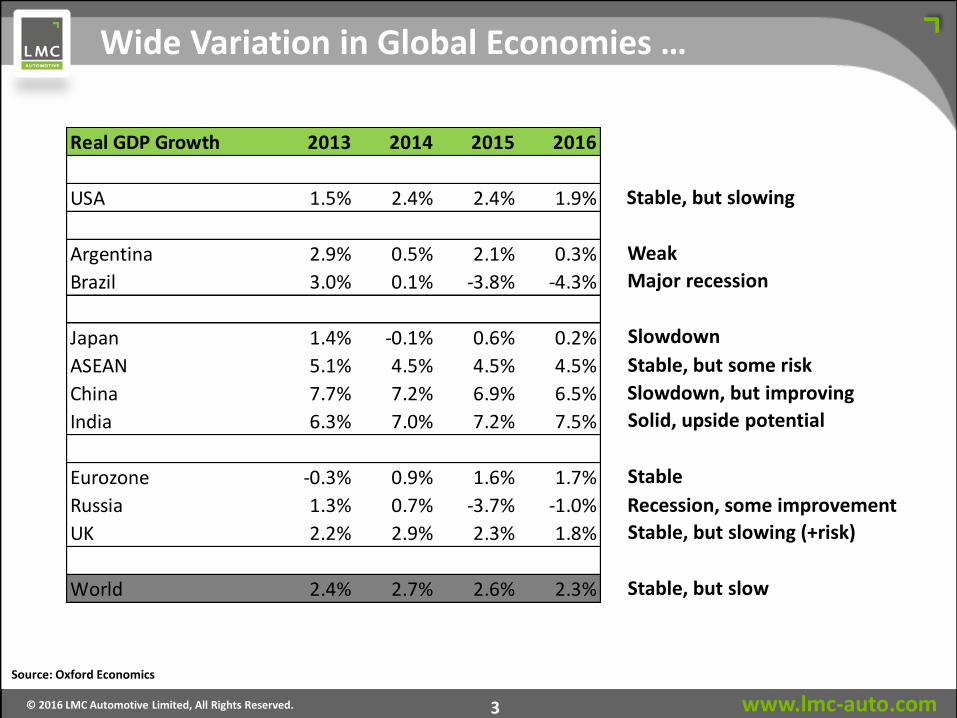

Wide Variation in Global Economies …

Real GDP Growth 2013 2014 2015 2016

USA 1.5% 2.4% 2.4% 1.9%

Argentina 2.9% 0.5% 2.1% 0.3%

Brazil 3.0% 0.1% -3.8% -4.3%

Japan 1.4% -0.1% 0.6% 0.2%

ASEAN 5.1% 4.5% 4.5% 4.5%

China 7.7% 7.2% 6.9% 6.5%

India 6.3% 7.0% 7.2% 7.5%

Eurozone -0.3% 0.9% 1.6% 1.7%

Russia 1.3% 0.7% -3.7% -1.0%

UK 2.2% 2.9% 2.3% 1.8%

World 2.4% 2.7% 2.6% 2.3%

Stable, but slowing

Major recession

Slowdown

Stable, but some risk

Slowdown, but improving

Solid, upside potential

Stable

Recession, some improvement

Stable, but slowing (+risk)

Stable, but slow

Source: Oxford Economics

Weak

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 4

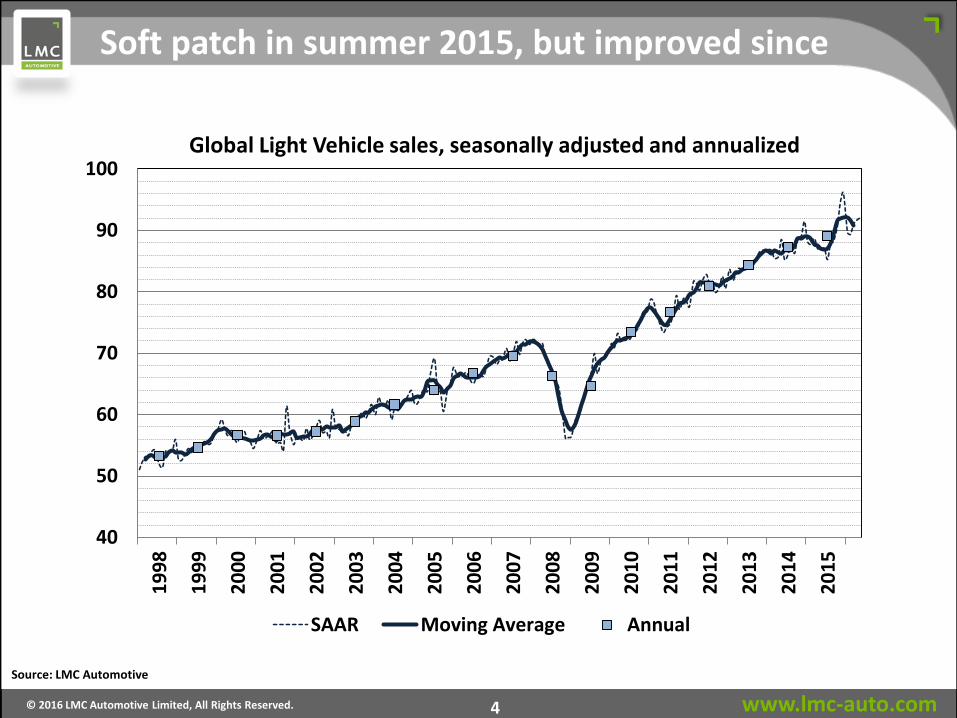

Global Light Vehicle sales, seasonally adjusted and annualized

Source: LMC Automotive

Soft patch in summer 2015, but improved since

40

50

60

70

80

90

1001

99

8

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

SAAR Moving Average Annual

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 5

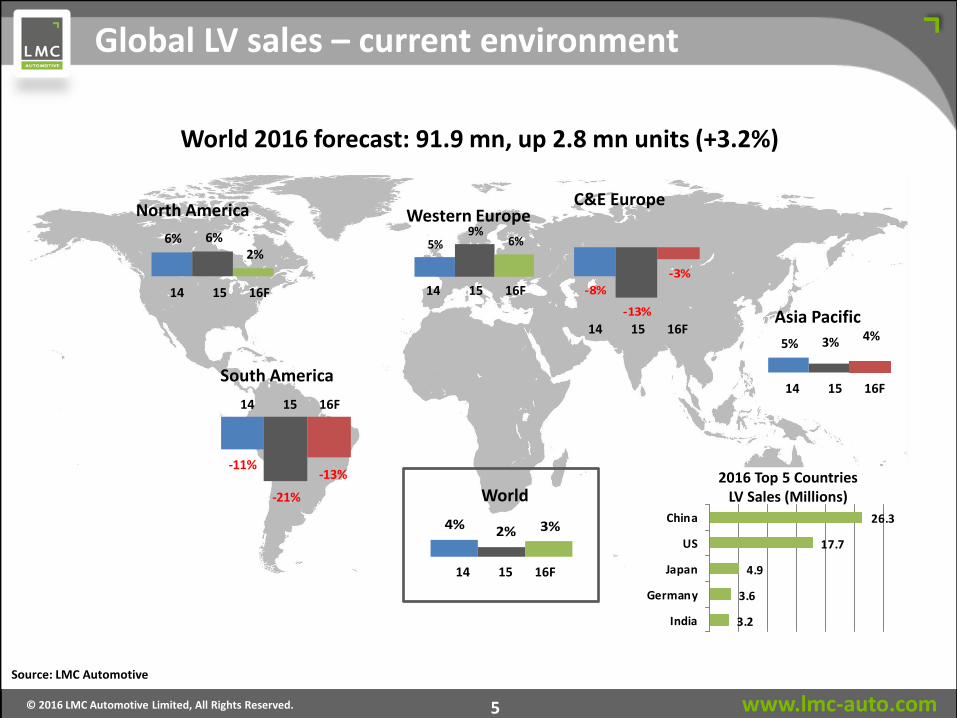

26.3

17.7

4.9

3.6

3.2

China

US

Japan

Germany

India

World 2016 forecast: 91.9 mn, up 2.8 mn units (+3.2%)

6% 6%2%

5%9%

6%

-8%

-13%

-3%

-11%

-21%

-13%

5% 3% 4%

North America

Asia Pacific

C&E Europe Western Europe

South America

14 15 16F

4% 2% 3%

World

Global LV sales – current environment

2016 Top 5 Countries LV Sales (Millions)

14 15 16F

14 15 16F

14 15 16F

14 15 16F

14 15 16F

Source: LMC Automotive

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 6

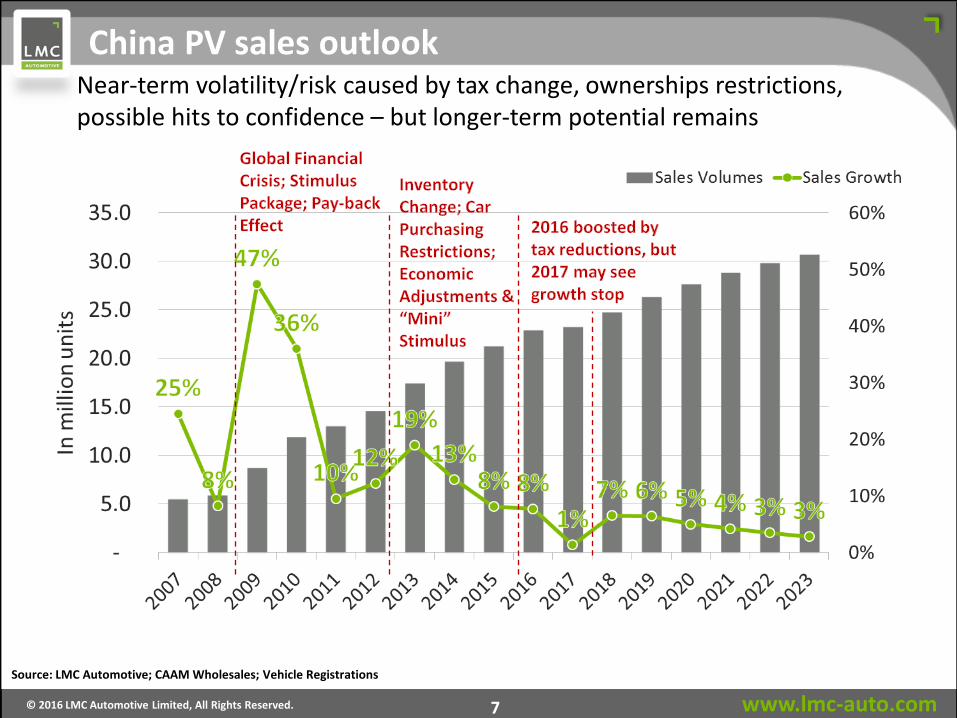

Source: LMC Automotive; CAAM Wholesales; Vehicle Registrations

Financial crisis

Stimulus package

Payback effect

China Light Vehicle sales SAAR

Shrinking Minibus segment; Light Truck/Pickup – affected by China-4 emission standards

Stimulation by the tax cut

Locally made PV sales growth was on a downswing in mid-2015, but we now see a rebound stimulated by the positive impact from the tax change. (Sourcing from CAAM, sales of vehicles fitted with engines of 1.6 liters or less reached 14.5 mn units, a rise of 10.4% in 2015, accounting for around 70% share of total Passenger Vehicle sales.)

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 7

China PV sales outlook Near-term volatility/risk caused by tax change, ownerships restrictions, possible hits to confidence – but longer-term potential remains

Source: LMC Automotive; CAAM Wholesales; Vehicle Registrations

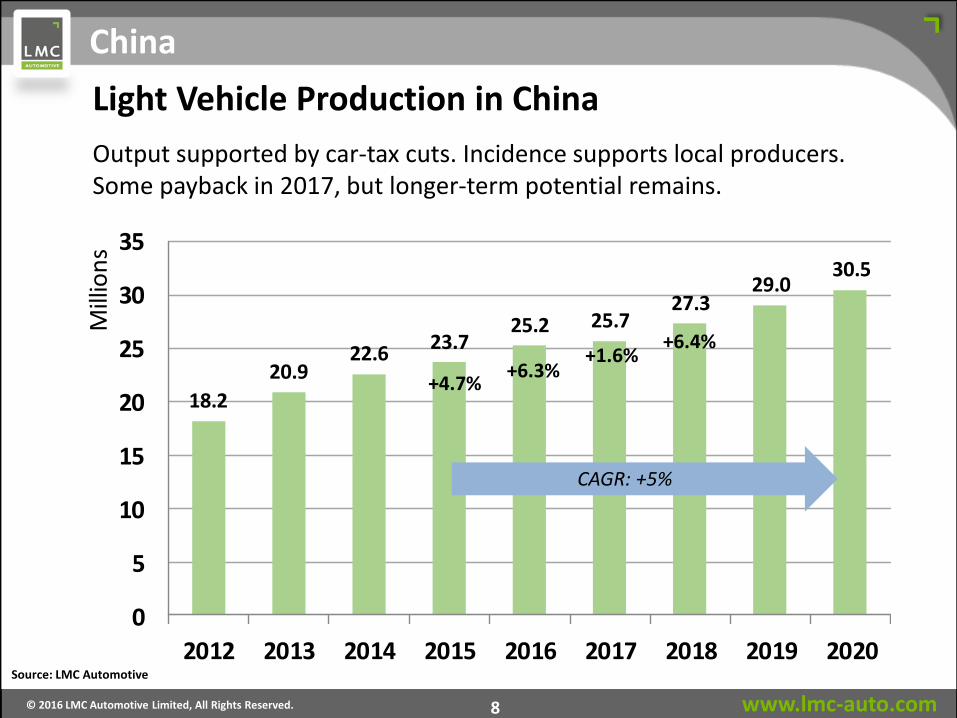

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 8

Light Vehicle Production in China

18.2

20.922.6

23.725.2 25.7

27.329.0

30.5

0

5

10

15

20

25

30

35

2012 2013 2014 2015 2016 2017 2018 2019 2020

Mill

ion

s

+4.7%

Output supported by car-tax cuts. Incidence supports local producers. Some payback in 2017, but longer-term potential remains.

Source: LMC Automotive

+6.3% +1.6%

China

CAGR: +5%

+6.4%

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 9

European LV exports growth to China

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

2013: +4% 2014: -3% 2015: -19% 2012: +30%

Source: LMC Automotive

2016ytQ3: +13%

Europe’s exposure

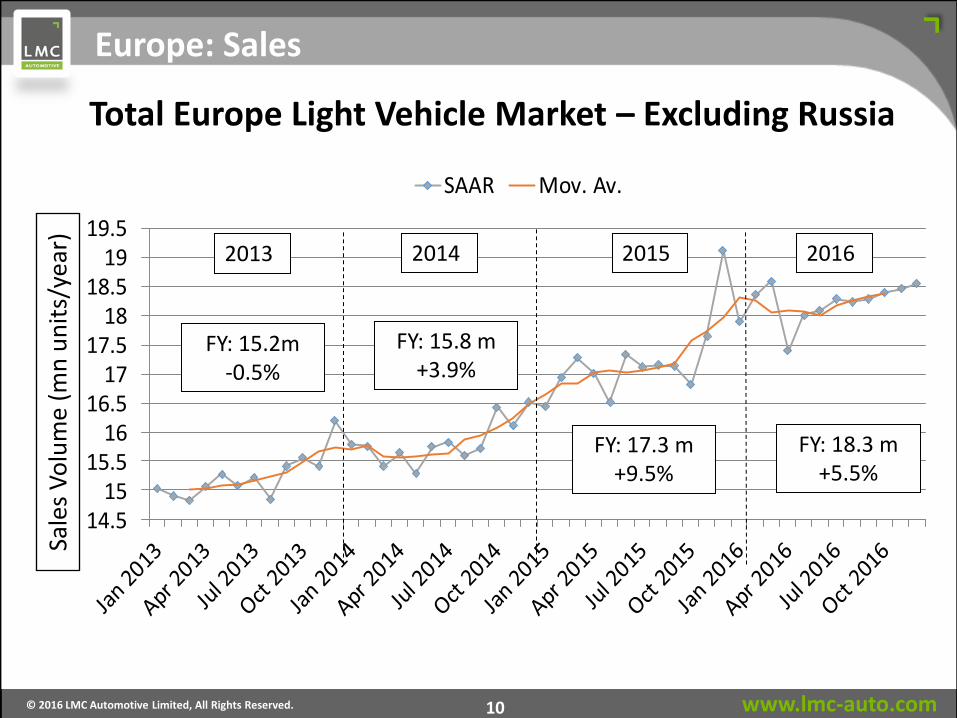

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 10

14.515

15.516

16.517

17.518

18.519

19.5

SAAR Mov. Av.

Sale

s V

olu

me

(mn

un

its/

year

)

2013 2014 2015

Europe: Sales

2016

FY: 15.2m -0.5%

FY: 15.8 m +3.9%

FY: 17.3 m +9.5%

FY: 18.3 m +5.5%

Total Europe Light Vehicle Market – Excluding Russia

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 11

-15%

-10%

-5%

0%

5%

10%

15%

2012 Q1

2012 Q2

2012 Q3

2012 Q4

2013 Q1

2013 Q2

2013 Q3

2013 Q4

2014 Q1

2014 Q2

2014 Q3

2014 Q4

2015 Q1

2015 Q2

2015 Q3

2015 Q4

2016 Q1

2016 Q2

2016 Q3

2016 Q4

European LV Production Growth (excluding Russia)

2013: 17.5m +1%

2014: 18.3m +5%

2015: 19.6m +7%

2012: 17.3m -7%

Source: LMC Automotive

2016: 20.3m +3.5%

Europe: Production

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 12

- Q1 2016: stock reduction following bumper sales pace in Europe

- Despite emissions scandal, VW Group stock levels are lean

- No ‘Red Flags’ yet

European Vehicle Inventory Assessment Overview Group Level

2015 (Q4) 2016 (Q1) 2015 (Q4) 2016 (Q1) Benchmark

BMW Group 390 400 54 48 53

Daimler Group 377 369 60 51 54

Fiat Chrysler Automobiles 265 306 60 60 61

Ford 310 341 56 59 56

Opel AG 208 221 57 60 65

PSA Group 386 411 50 51 62

Renault-Nissan 645 679 62 55 64

Tata Group (JLR) 111 114 49 53 56

Volkswagen Group 1,044 1,043 50 49 53

EUROPE 4,261 4,398 55 53 58

Days SupplyInventory Holding (000s)

End-of-Period Inventory Measure

Europe: Stocks

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 13

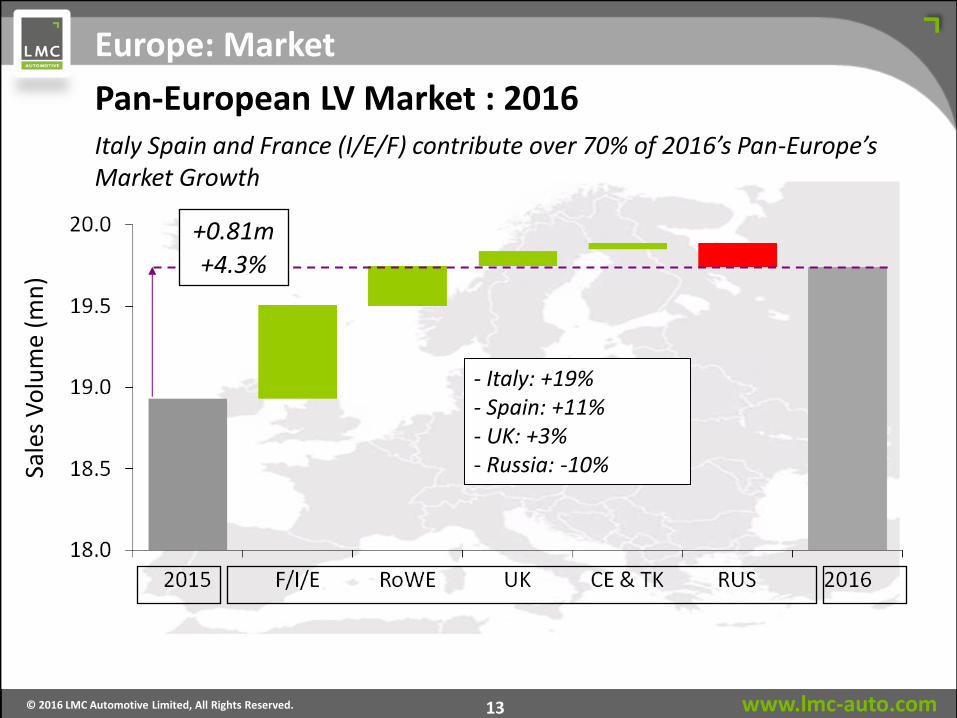

Italy Spain and France (I/E/F) contribute over 70% of 2016’s Pan-Europe’s Market Growth

Sale

s V

olu

me

(mn

)

+0.81m

+4.3%

- Italy: +19% - Spain: +11% - UK: +3% - Russia: -10%

Pan-European LV Market : 2016

Europe: Market

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 14

FY: 2.5 mn -10%

FY: 2.8 mn -3%

Sale

s V

olu

me

(mn

un

its/

year

)

2013 2014 2015

Total Russian Light Vehicle Market

- Government support but… - Weak consumption environment

FY: 1.6 mn -36%

2016

FY: 1.4 mn -10%

Russia: Sales

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 15

-40%

-30%

-20%

-10%

0%

10%

20%

30%

2012 Q1

2012 Q2

2012 Q3

2012 Q4

2013 Q1

2013 Q2

2013 Q3

2013 Q4

2014 Q1

2014 Q2

2014 Q3

2014 Q4

2015 Q1

2015 Q2

2015 Q3

2015 Q4

2016 Q1

2016 Q2

2016 Q3

2016 Q4

Russian LV Production Growth

2013: 2.08m -2.5%

2014: 1.82m -12%

2015: 1.3m -28%

2012: 2.13m +13%

Source: LMC Automotive

2016: 1.2m -6%

Russia: Production

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 16

0.0

0.5

1.0

1.5

2.0

2.5

2012 2013 2014 2015 2016 2017 2018 2019 2020

Mill

ion

s

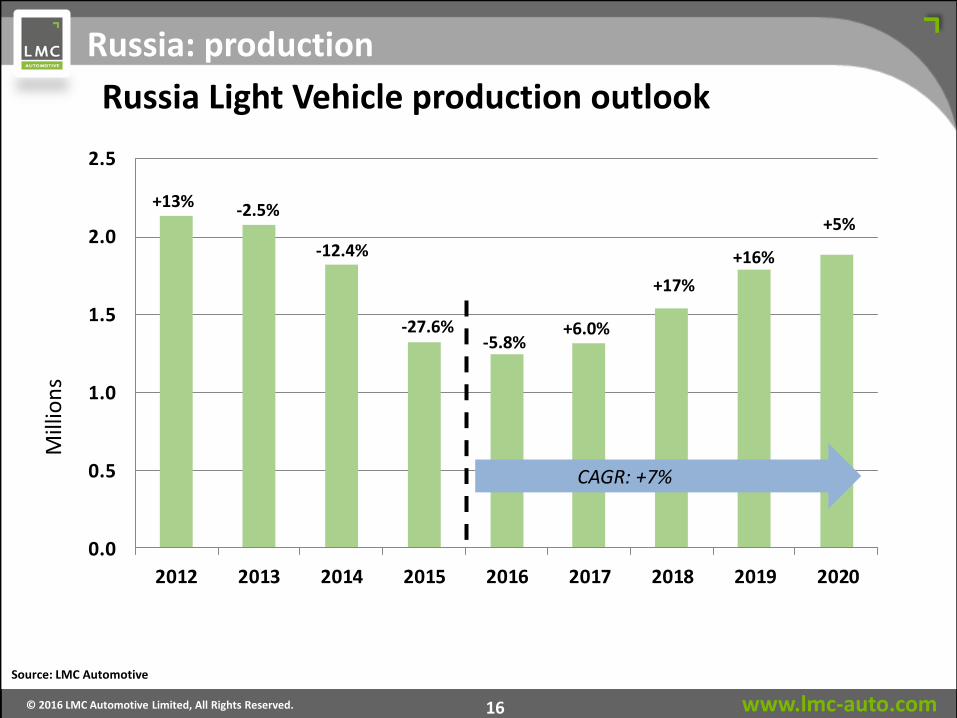

+13% -2.5%

-12.4%

-27.6% -5.8%

+6.0%

+17%

+16%

+5%

Russia Light Vehicle production outlook

CAGR: +7%

Source: LMC Automotive

Russia: production

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 17

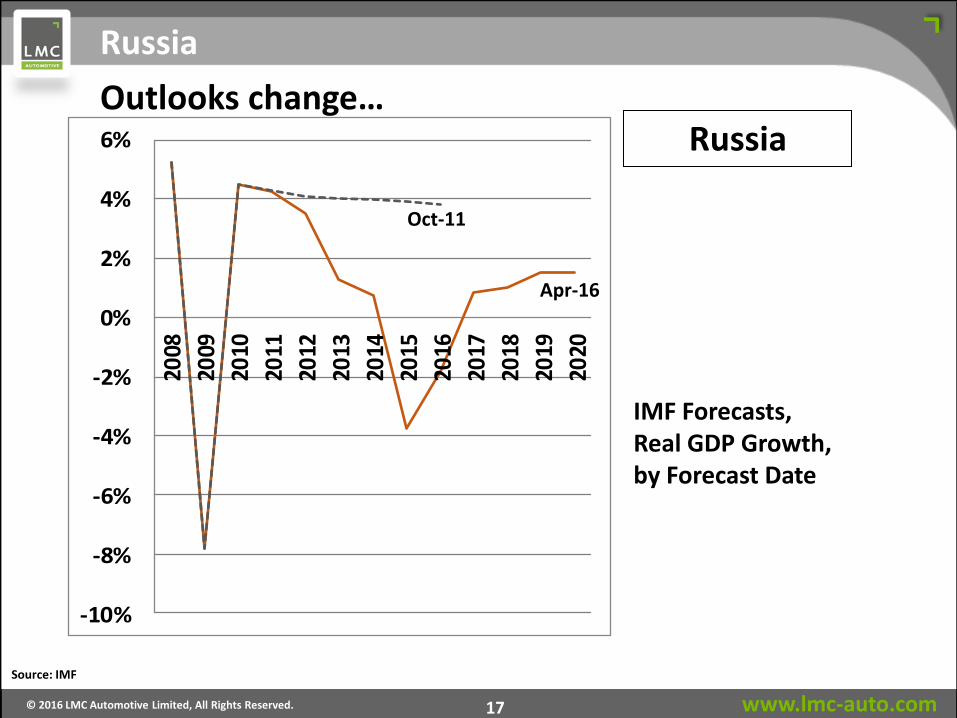

Russia

Source: IMF

IMF Forecasts, Real GDP Growth, by Forecast Date

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Russia

Oct-11

Apr-16

Outlooks change…

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 18

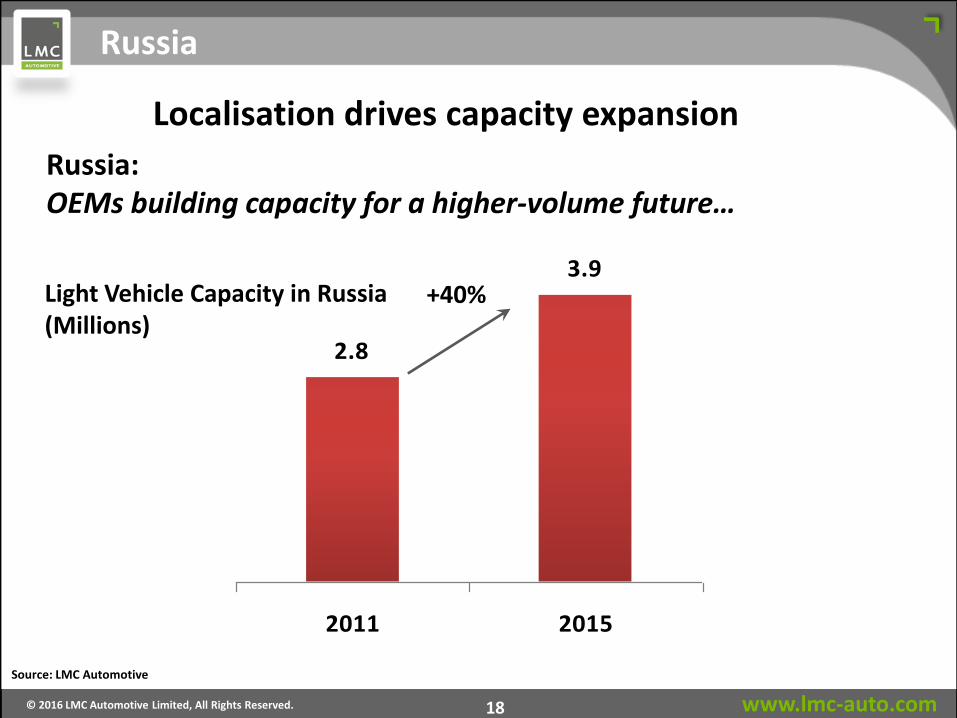

2.8

3.9

2011 2015

Russia

Source: LMC Automotive

Light Vehicle Capacity in Russia (Millions)

+40%

Russia: OEMs building capacity for a higher-volume future…

Russia Localisation drives capacity expansion

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 19

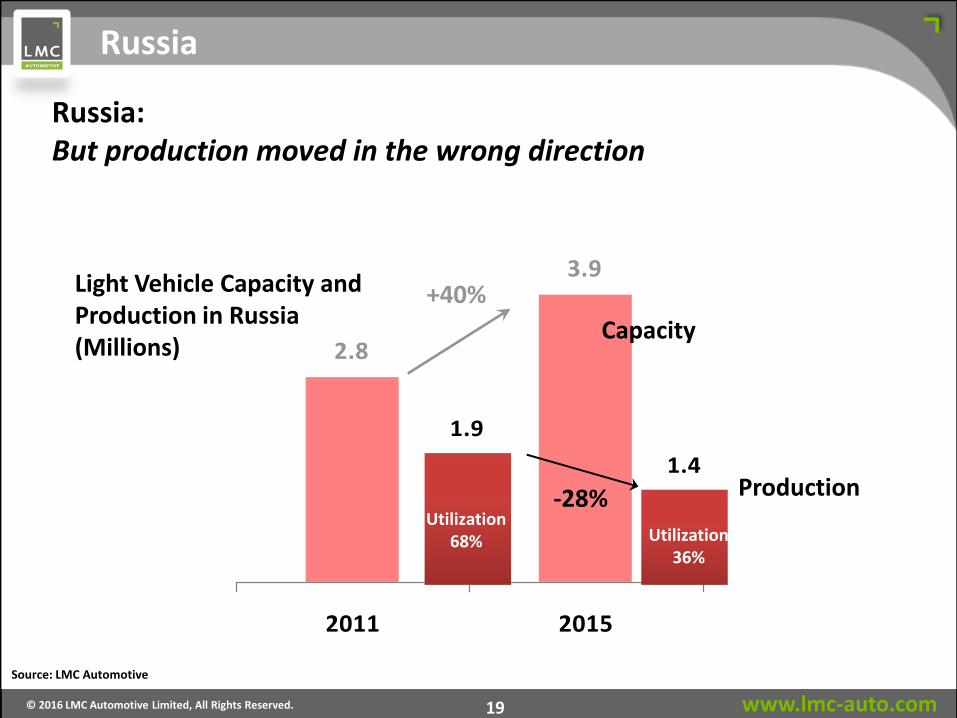

2.8

3.9

2011 2015

1.9

1.4

2011 2015

Source: LMC Automotive

Light Vehicle Capacity and Production in Russia (Millions)

+40%

-28% Utilization

68% Utilization 36%

Capacity

Production

Russia: But production moved in the wrong direction

Russia

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 20

Europe: Long-term utilisation development

Source: LMC Automotive

Europe: Uitlisation

16.719.2 20.5 19.4 19.5 20.1 21.0 21.5 22.2 22.9 23.4 23.7 24.2 24.5 24.9

10.1 10.0 9.96.7 6.16.36.97.3

7.58.9 8.28.68.7

9.5

12.2

0

5

10

15

20

25

30

35

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Mill

ion

s

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Utilisatio

n R

ate

Production Excess Capacity Utilisation

• Utilisation expected to reach ‘industry profitable’ level in 2018 • Plant closures politically sensitive – some ‘trimming’ • Minor capacity expansion • Utilisation improves as output rises to meet demand growth • Wide spectrum of utilisation rates at OEMs

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 21

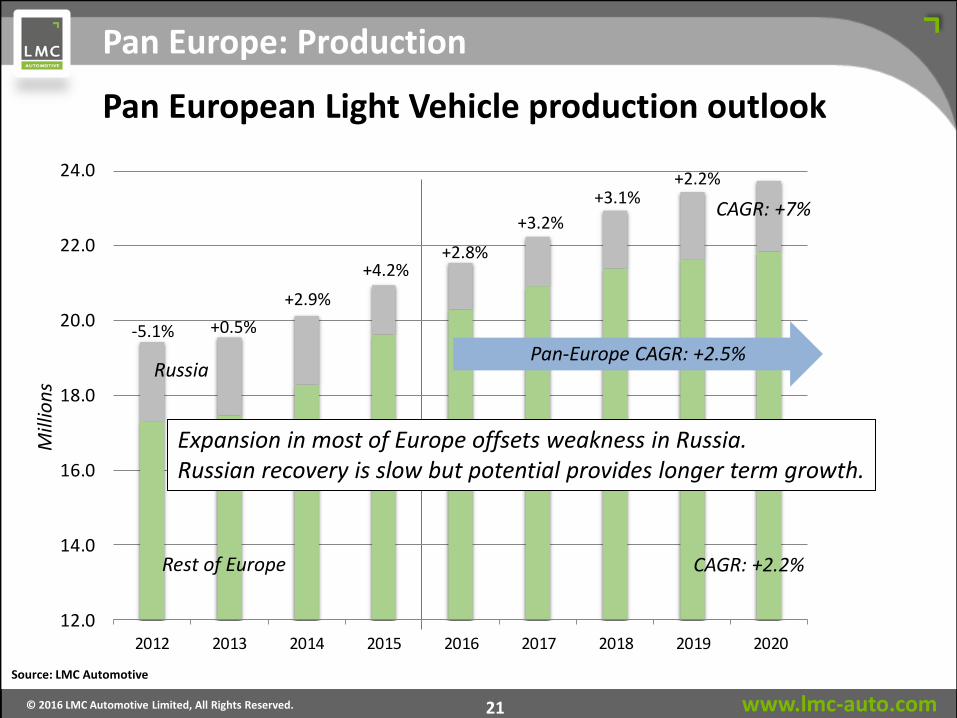

12.0

14.0

16.0

18.0

20.0

22.0

24.0

2012 2013 2014 2015 2016 2017 2018 2019 2020

Mill

ion

sM

illio

ns

-5.1% +0.5%

+2.9%

+4.2% +2.8%

+3.2%

+3.1%

Pan European Light Vehicle production outlook

Pan-Europe CAGR: +2.5%

Expansion in most of Europe offsets weakness in Russia. Russian recovery is slow but potential provides longer term growth.

Source: LMC Automotive

+2.2%

CAGR: +7%

Russia

Rest of Europe CAGR: +2.2%

Pan Europe: Production

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 22

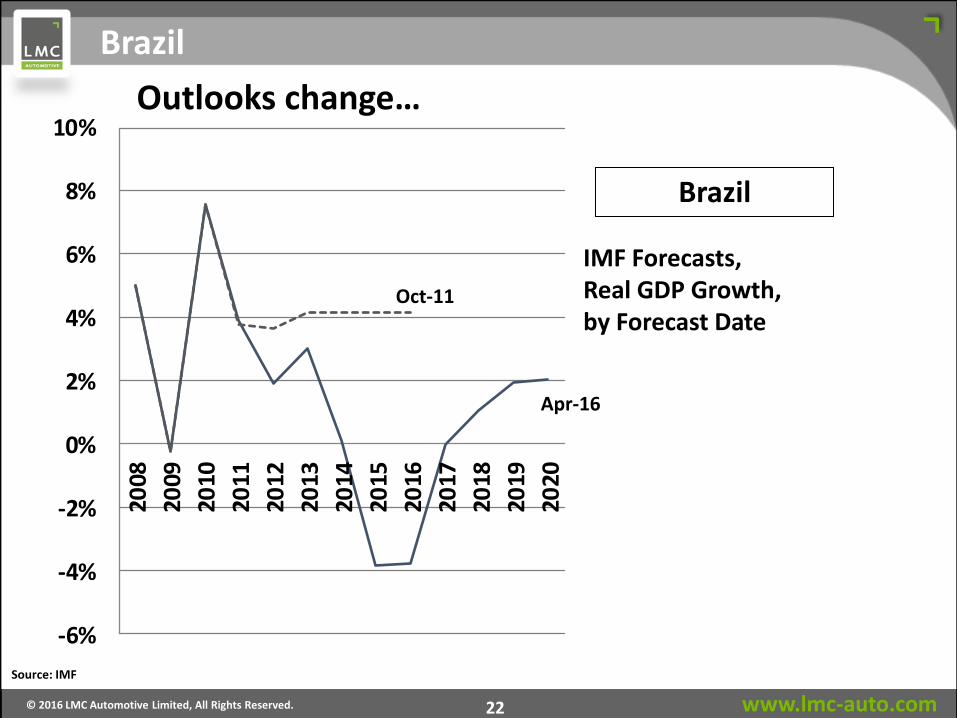

Brazil

Source: IMF

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%20

08

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

IMF Forecasts, Real GDP Growth, by Forecast Date

Brazil

Oct-11

Apr-16

Outlooks change…

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 23

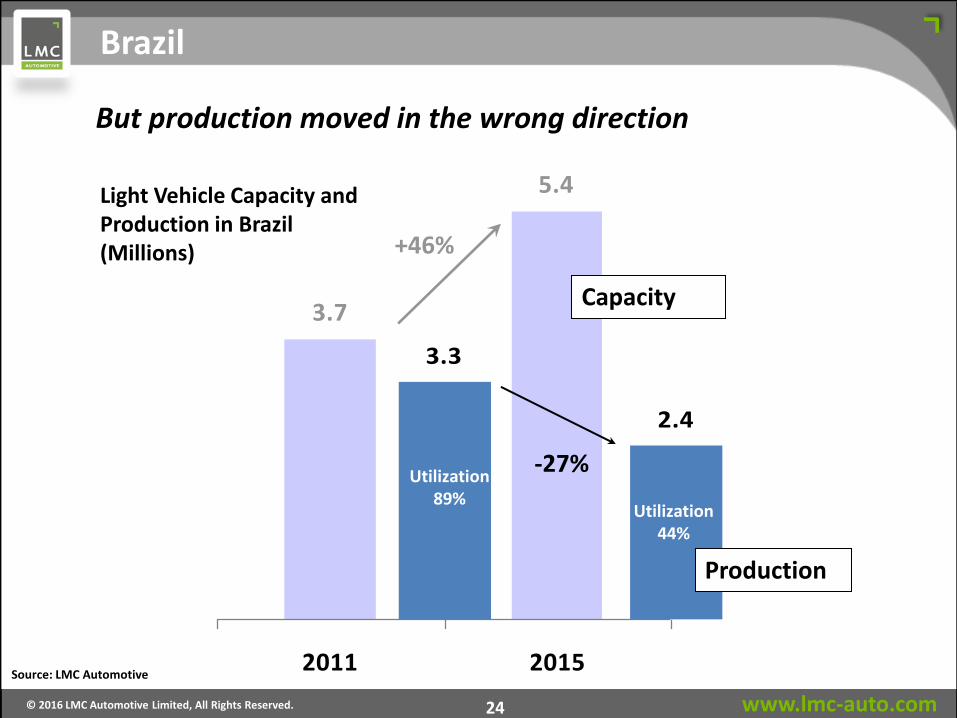

3.7

5.4

2011 2015

Brazil

Source: LMC Automotive

Light Vehicle Capacity in Brazil (Millions) +46%

OEMs building capacity for a higher-volume future…

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 24

3.7

5.4

2011 2015

3.3

2.4

2011 2015

Brazil

Source: LMC Automotive

Light Vehicle Capacity and Production in Brazil (Millions) +46%

Utilization 89%

Utilization 44%

-27%

But production moved in the wrong direction

Capacity

Production

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 25

Investment curtailed but not stopped

2015 2016 2017

Daimler Iracemápolis, Q1 2016 $600 million

Land Rover Itatiaia, Q3 2016 $375 million

Volkswagen & Audi São José dos Pinhais, Q3 2015 $470 million

Fiat Goiana, Q3 2015 $1.8 billion

Fiat Cordoba, Q3 2017 $500 million

JAC Motors Camaçari, Q2 2017 $400 million

Volare Sao Mateus, Q2 2016 $180 million

Honda Itirapina, Q2 2017 $450 million

Chery Jacareí, Q3 2016 $400 million

On track to be

completed in 2016

JAC is facing several difficulties,

future of the plant is uncertain,

date is speculative.

Recently announced

investment to the plant.

Plant opening has been delayed

due to bleak economic

environment in Brazil.

Toyota Sorocaba, Q3 2016 $100 million – expansion for new Etios

Source: LMC Automotive

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 26

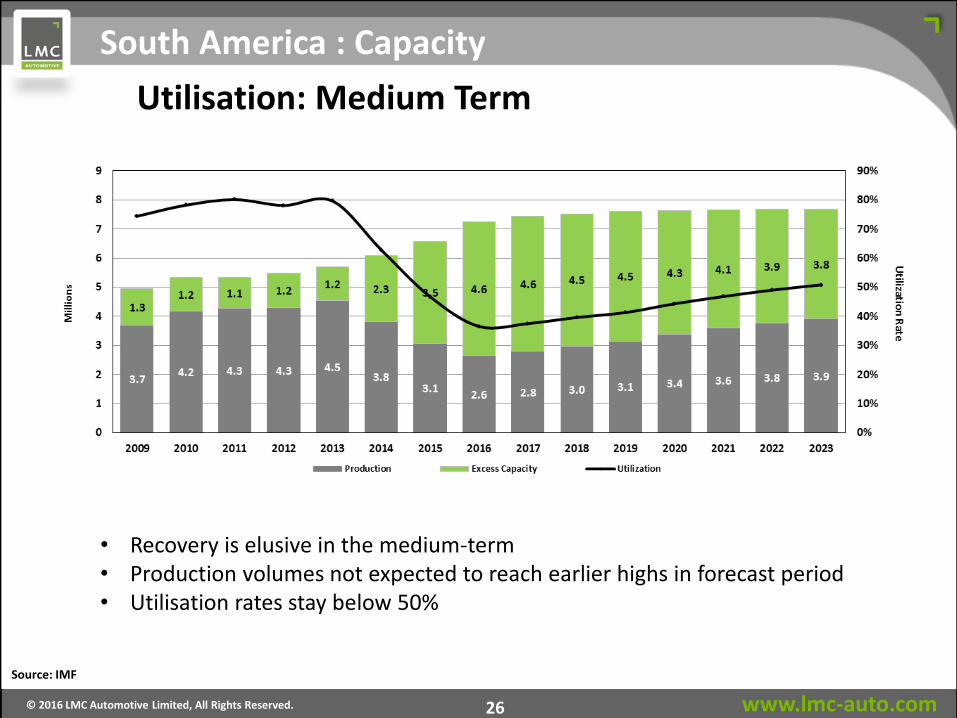

South America : Capacity

Source: IMF

Utilisation: Medium Term

• Recovery is elusive in the medium-term • Production volumes not expected to reach earlier highs in forecast period • Utilisation rates stay below 50%

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 27

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2012 2013 2014 2015 2016 2017 2018 2019 2020

Mill

ion

s

-0.5%

+8.5%

-14.2%

-21.3%

-12.7% +5.5%

+7.5% +6% +8%

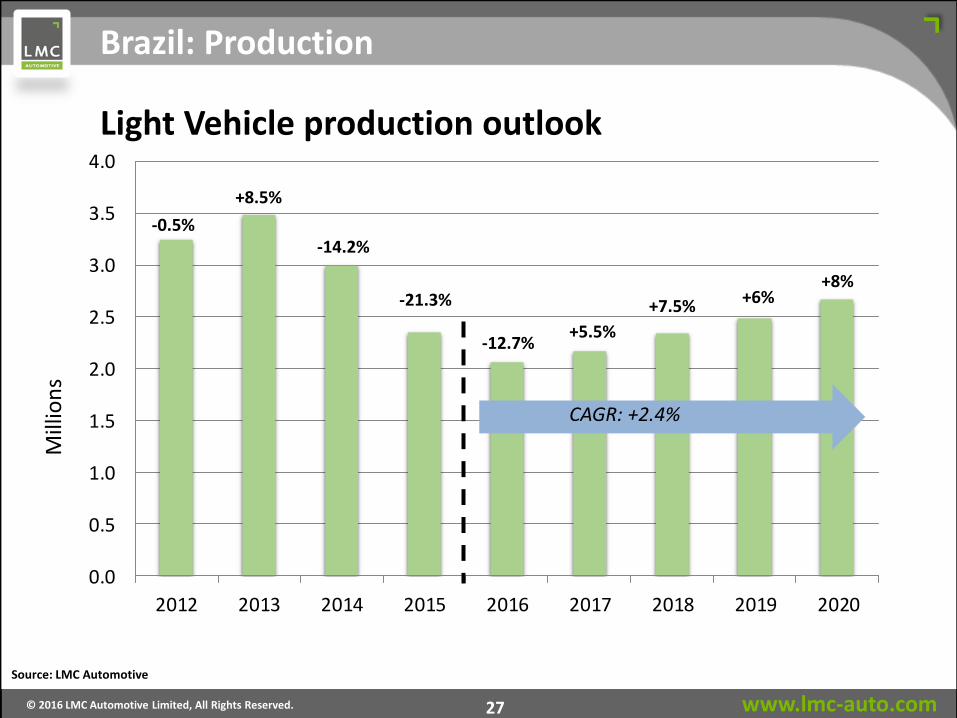

Brazil: Production

CAGR: +2.4%

Source: LMC Automotive

Light Vehicle production outlook

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 28

17.4

12.0

13.0

14.0

15.0

16.0

17.0

18.0

19.0

Mil

lio

ns

US LV sales – monthly selling rate (SAAR) trend

May

Sales pace at beginning of year started off ahead of expectations, but softened through Q1 as Retail sales weakened. May SAAR was steady.

Source: LMC Automotive

Retail sales had been building momentum since the spring of 2015 and accelerated through the autumn with September SAAR >18 mn for total LVs).

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 29

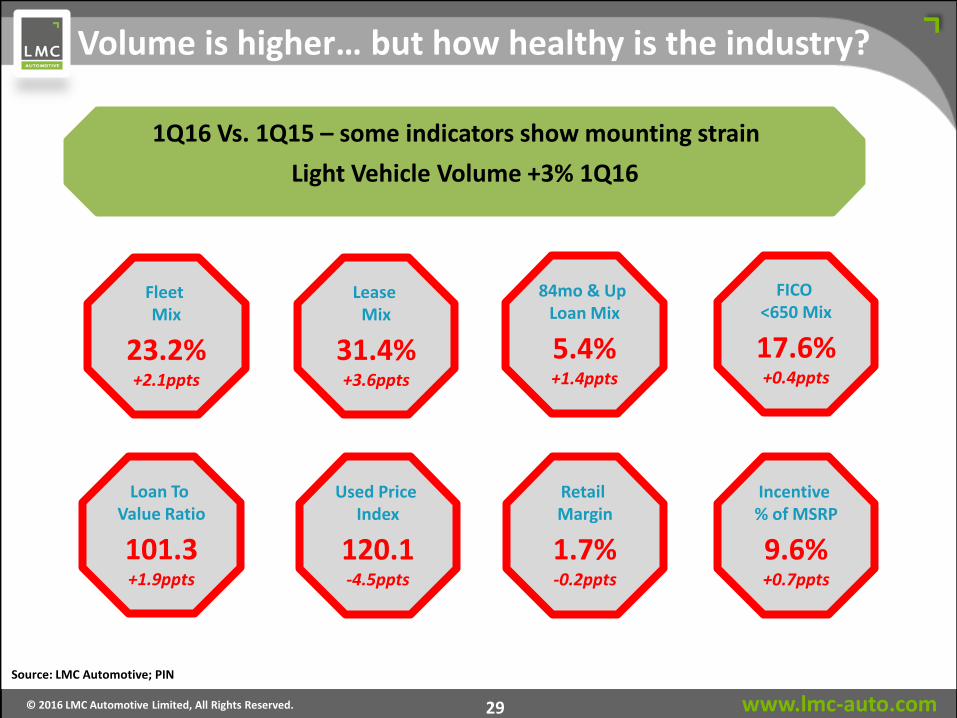

FICO <650 Mix

17.6% +0.4ppts

84mo & Up Loan Mix

5.4% +1.4ppts

Incentive % of MSRP

9.6% +0.7ppts

Retail Margin

1.7% -0.2ppts

Used Price Index

120.1 -4.5ppts

Loan To Value Ratio

101.3 +1.9ppts

Light Vehicle Volume +3% 1Q16

Fleet Mix

23.2% +2.1ppts

Volume is higher… but how healthy is the industry?

1Q16 Vs. 1Q15 – some indicators show mounting strain

Lease Mix

31.4% +3.6ppts

Source: LMC Automotive; PIN

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 30

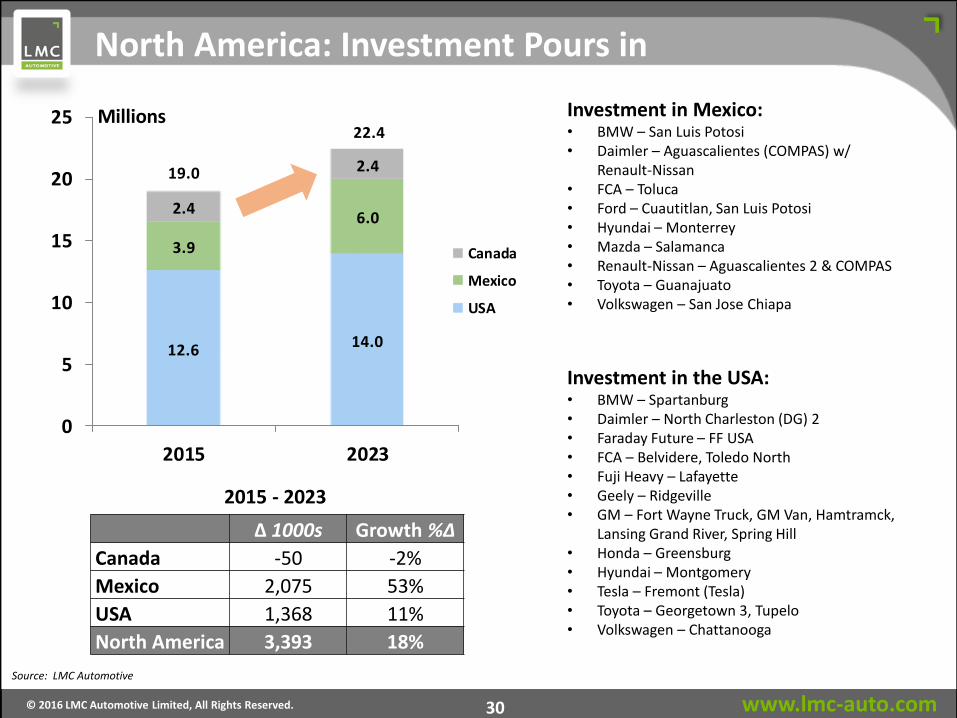

North America: Investment Pours in

2015 - 2023

Investment in Mexico: • BMW – San Luis Potosi • Daimler – Aguascalientes (COMPAS) w/

Renault-Nissan • FCA – Toluca • Ford – Cuautitlan, San Luis Potosi • Hyundai – Monterrey • Mazda – Salamanca • Renault-Nissan – Aguascalientes 2 & COMPAS • Toyota – Guanajuato • Volkswagen – San Jose Chiapa

Investment in the USA: • BMW – Spartanburg • Daimler – North Charleston (DG) 2 • Faraday Future – FF USA • FCA – Belvidere, Toledo North • Fuji Heavy – Lafayette • Geely – Ridgeville • GM – Fort Wayne Truck, GM Van, Hamtramck,

Lansing Grand River, Spring Hill • Honda – Greensburg • Hyundai – Montgomery • Tesla – Fremont (Tesla) • Toyota – Georgetown 3, Tupelo • Volkswagen – Chattanooga

Source: LMC Automotive

12.6 14.0

3.9

6.02.4

2.419.0

22.4

0

5

10

15

20

25

2015 2023

Canada

Mexico

USA

Millions

Δ 1000s Growth %Δ

Canada -50 -2%

Mexico 2,075 53%

USA 1,368 11%

North America 3,393 18%

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 31

20%

40%

60%

80%

100%

0

4

8

12

16

20

24

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

NA Domestic Asian Domestic Euro Domestic Utilization

North America

Source: LMC Automotive

Change in Share 2014-2020 NA: 54% to 50% AP: 39% to 40% EU: 7% to 10%

Localisation in NA Drives Growth – Alters Mix

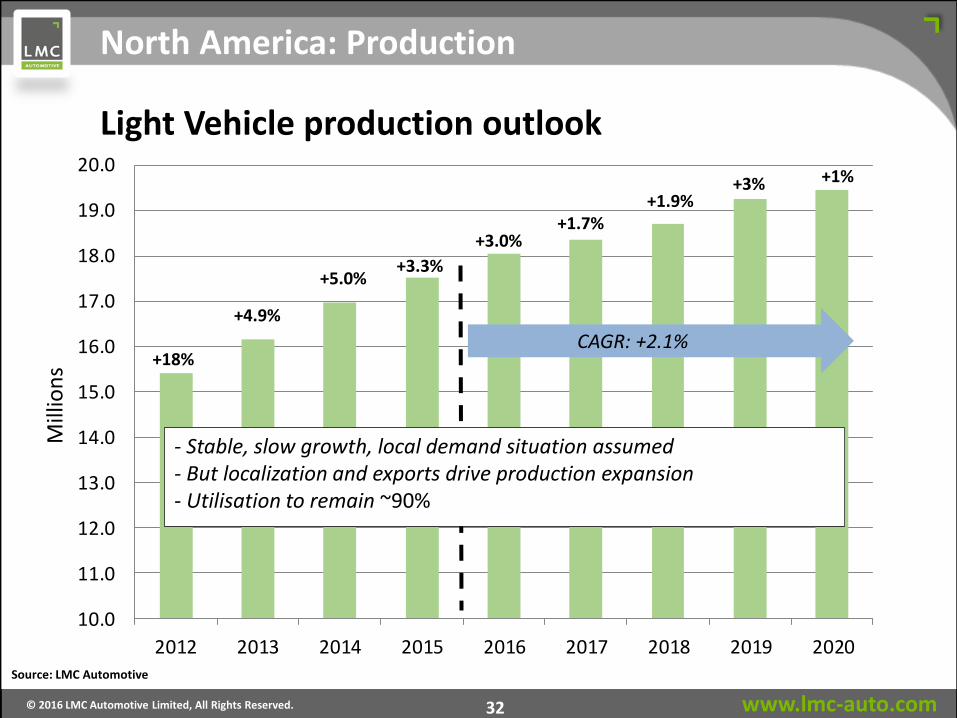

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 32

10.0

11.0

12.0

13.0

14.0

15.0

16.0

17.0

18.0

19.0

20.0

2012 2013 2014 2015 2016 2017 2018 2019 2020

Mill

ion

s +18%

+4.9%

+5.0% +3.3%

+3.0% +1.7%

+1.9% +3% +1%

North America: Production

CAGR: +2.1%

Source: LMC Automotive

Light Vehicle production outlook

- Stable, slow growth, local demand situation assumed - But localization and exports drive production expansion - Utilisation to remain ~90%

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 33

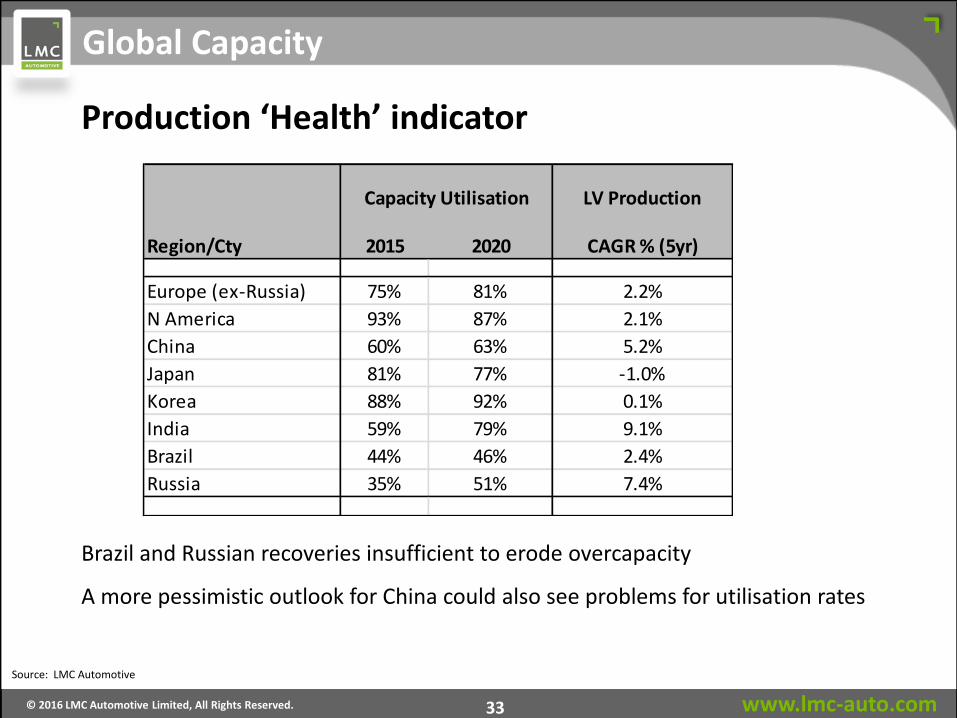

Production ‘Health’ indicator

Global Capacity

Brazil and Russian recoveries insufficient to erode overcapacity

A more pessimistic outlook for China could also see problems for utilisation rates

Source: LMC Automotive

LV Production

Region/Cty 2015 2020 CAGR % (5yr)

Europe (ex-Russia) 75% 81% 2.2%

N America 93% 87% 2.1%

China 60% 63% 5.2%

Japan 81% 77% -1.0%

Korea 88% 92% 0.1%

India 59% 79% 9.1%

Brazil 44% 46% 2.4%

Russia 35% 51% 7.4%

Capacity Utilisation

www.lmc-auto.com © 2016 LMC Automotive Limited, All Rights Reserved. 34

Concluding remarks

• Simultaneous Regional growth remains elusive

• Emerging market stumble, leaving unfulfilled ‘promises’

• Mature markets provide some balance

• Utilisation still remains a problem for some and a potential risk ‘amber’ flag for others

• Global production growth outlook to lean on China. Again.