autos & auto parts - jefferies · pdf filemkt. cap price cons. current eps estimates...

TRANSCRIPT

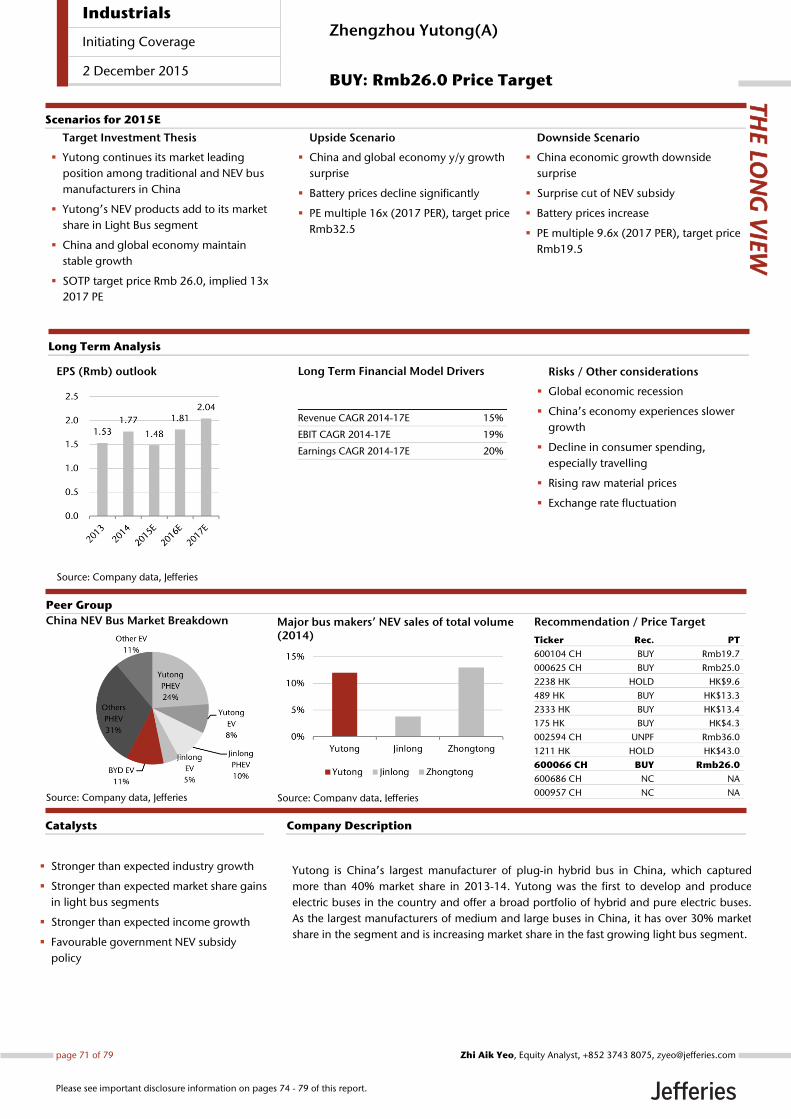

Mkt. Cap Price Cons. Current EPS Estimates Valuation (P/E)Company Name Ticker (MM) Rating Price Target Next FY 2015 2016 2017 2016 2017 BYD Company Limited 1211 HK HK$105,477.6 HOLD HK$42.60 HK$43.00 RMB1.20 RMB0.40 RMB0.72 RMB0.85 59.2x 50.1xBYD Company Limited 002594 CH RMB156,706.0 UNPF RMB63.29 RMB36.00 RMB1.62 RMB0.40 RMB0.72 RMB0.85 87.9x 74.5xZhengzhou Yutong Bus 600066 CH RMB48,109.4 BUY RMB21.71 RMB26.00 RMB1.96 RMB1.48 RMB1.81 RMB2.04 12.0x 10.6x

Initiating Coverage

China | Industrials | Autos & Auto Parts 2 December 2015

Autos & Auto PartsChina NEV Champions Face-Off; InitiateYutong at Buy, BYD at Hold

EQU

ITY R

ESEARC

H C

HIN

A

List of technical abbreviations

NEV: New energy vehicle

PV: Passenger vehicle or car

CV: Commercial vehicle

PHEV: Plug-in hybrid electric vehicle

BEV: Pure electric vehicle

FCV: Fuel cell vehicle

CNG: Compressed natural gas

LNG: Liquefied natural gas

BMS: Battery management system

LFP: Lithium iron phosphate

LMO: Lithium manganese oxide

NCM: Nickel manganese cobalt oxide

NCA: Nickel cobalt aluminum oxide

Zhi Aik Yeo *Equity Analyst

+852 3743 8075 [email protected] Fong, CFA *

Equity Analyst+852 3743 8074 [email protected]

Yoanna Wang *Equity Associate

+852 3743 8776 [email protected] Nan *Equity Associate

+852 3743 8746 [email protected] Yu *

Equity Analyst+852 3743 8047 [email protected]

Johnson Leung *Equity Analyst

+852 3743 8055 [email protected]

* Jefferies Hong Kong Limited

Key Takeaway

A comparative study of Yutong vs. BYD leads us to prefer the former for itshealthier fundamentals, stable growth and reasonable valuation. For BYD, webelieve excessive expectations are priced in, and risks are emerging. We initiateYutong at Buy and BYD – H/A at Hold/Underperform.

NEV bus champion vs. NEV car champion. From Star Wars vs. Star Trek to Pacquiaovs. Mayweather, from Alibaba vs. Tencent to Katy Perry vs. Taylor Swift, everyone loves astory of great rivalry. Even though BYD and Yutong may only overlap in pure electric busesfor now, we have no doubt their paths will increasingly criss-cross. Yutong currently leadsin NEV buses while BYD has the pole position in NEV cars. Not only are these the defaultleaders in China's NEVs, investors often choose between them for an industry proxy. For thisreason, we conducted a comparative study of the two Chinese NEV leaders, and our analysisleads us to conclude Yutong is a better investment choice.

Prefer Yutong for stable growth. Yutong will continue to benefit from replacementdemand and government-backed rise in NEV bus penetration. Stable dividend payout, at4% yield in FY15, will sweeten the deal. We think the market had over-penalized Yutongfor impact of a subsidy cut in FY16/17. No doubt an adjustment of subsidy requirementwould be harsher on NEV buses vs. cars, but we expect NEV buses to better cushion thereduction. Local governments, who are key customers of NEV buses, are less price sensitivethan average consumers; moreover they are bounded by the NEV purchase target of 30%.Also, our calculation on the economics of NEV buses suggests the breakeven vs. diesel buswill be extended by merely ~1.5 years in FY17 upon subsidy cut. Thus from a customerperspective, it still makes economic sense to purchase an NEV bus despite the cut.

BYD is second-best. BYD lacks Yutong's financial soundness, as it is inferior in ROE,FCF yield, cash conversion, gearing and margins. Not to mention its profit included largecontributions of government grants and R&D capitalization. Meanwhile, the market haspriced in excessive expectations for the next 2 years. We are 29-35% below consensus. Ourconcerns lie firstly with volume, as the company faces: i) limited customer base as buyersmainly originate from license restricted cities ii) cannibalization between car models, as seenfrom Qin's recent lacklustre performance iii) authorities tackling the issue of consumers notusing electric mode despite buying PHEV iv) car subsidy cuts mainly affecting PHEV relativeto BEV v) intensifying competition. Meanwhile on margins, subsidy cuts in the short termand preoccupation with LFP batteries may curtail room for margin expansion. And ability toachieve long term cost reduction on battery relies on upcoming A-share placement.

Positive oil view and battery cost decline to spur adoption. We believe theindustry’s explosive growth and strong potential are well understood. Hence in this reportwe have selectively touched on the economics of NEV car/bus in China, outlook for thedecline in battery cost, challenges in consumer adoption and government policies drivingit. Importantly, we would highlight our China Oil & Gas team’s contrarian positive view onoil price, which would spur mass NEV adoption longer term.

Recommendation & Valuation. Based on SOTP valuation for both companies (and usingDCF to cross-check), we initiate Yutong (600066 CH) at Buy with TP of Rmb26.0, while weinitiate BYD - H/A shares (1211 HK, 002594 CH) at Hold /Underperform with TP of HK$43.0/Rmb36.0. At their respective TPs, Yutong represents 13x FY17 PER, while BYD is at 42x.

Jefferies does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that Jefferies may have aconflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investmentdecision. Please see analyst certifications, important disclosure information, and information regarding the status of non-US analysts on pages 74 to 79 ofthis report.

Table of Contents

I. Executive Summary Executive Summary…………………………………………………………………..………… 3

II. Comparative Study of BYD vs. Yutong A comparison of their businesses and operations……………………………………. 5

Market Share

PV and Bus Market

Future Competition

Subsidy Adjustment Impact

Business Model

Technology Roadmap & Risk

Segment Breakdown

Volume & Volume Growth

Revenue & Revenue Growth

Gross Margin

Return on Equity

Working Capital

Net Gearing

Free Cash Flow

Government Grants

Capacity Utilization

Research & Development

Shareholding Structure

III. Sector Outlook An overview of the market and its development………………………….……….… 21

PV EV Adoption No Easy Task

Government Paving the Road for EVs

The Cost of Batteries Coming Down

Tesla and the GigaFactory raising the bar

IV. Company Pages Zhengzhou Yutong Bus (600066 CH) initiate at Buy …..……………………..… 34

Company Background

Management and Shareholders

Earnings Estimates

Valuation & Risks

BYD –H (1211 HK) initiate at HOLD……………………………………………….…… 41

Company Background

Management and Shareholders

Earnings Estimates

Valuation & Risks

BYD –A (002594 CH) initiate at Underperform.......................................... 50

Company Background

Management and Shareholders

Earnings Estimates

Valuation & Risks

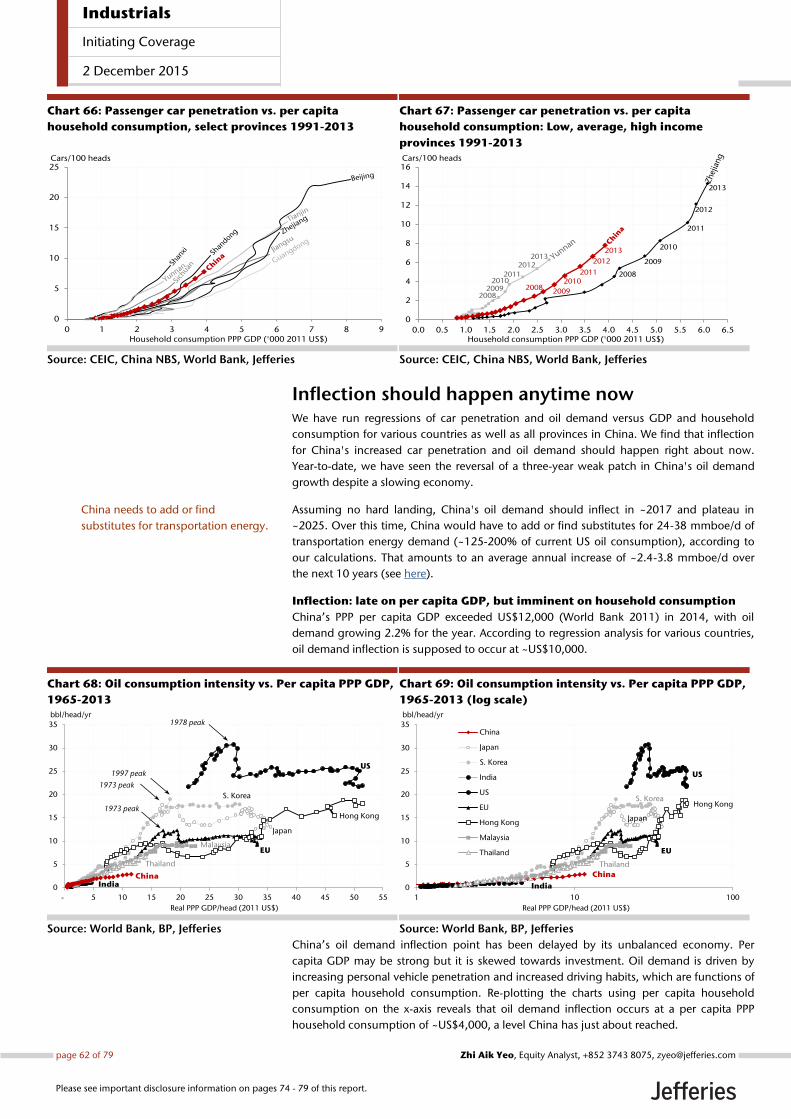

V. Appendix On the Cusp of a Car Culture………………………………………………..…………… 59

Inflection Should Happen Anytime Now

Lowering Vehicle Emissions

Battery Basics

Electric Vehicle Basics

Industrials

Initiating Coverage

2 December 2015

page 2 of 79 , Equity Analyst, +852 3743 8075, [email protected] Aik Yeo

Please see important disclosure information on pages 74 - 79 of this report.

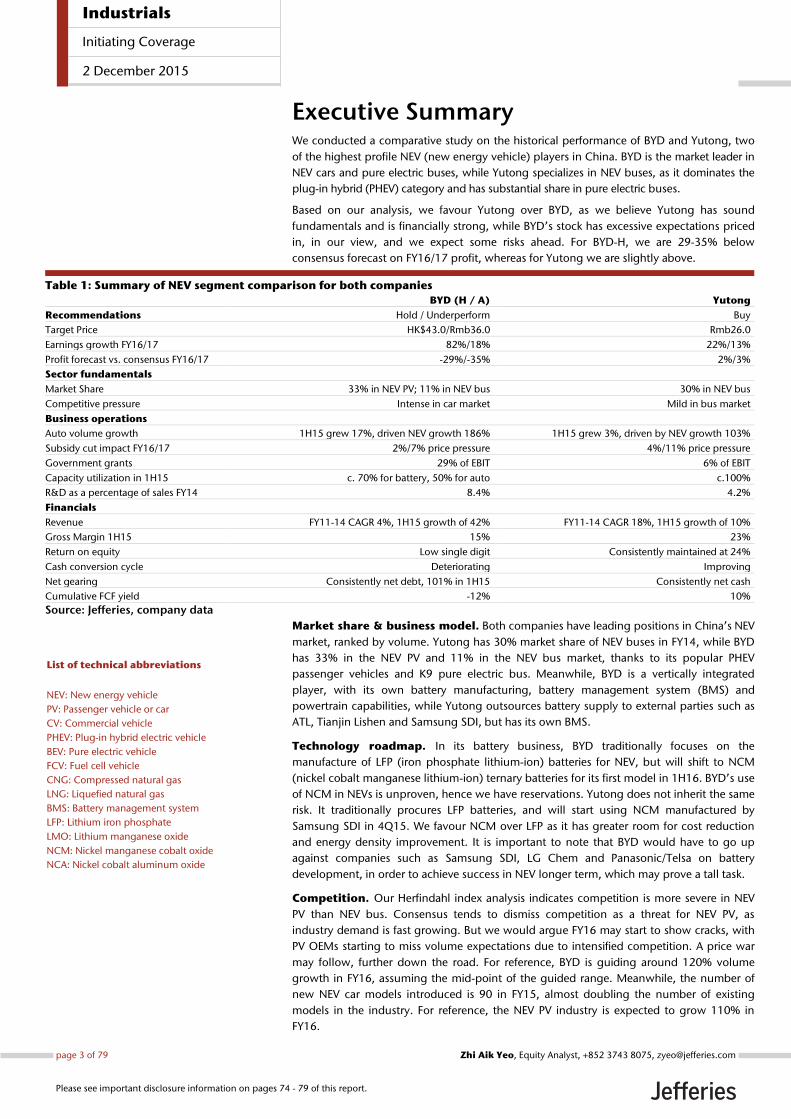

Executive Summary We conducted a comparative study on the historical performance of BYD and Yutong, two

of the highest profile NEV (new energy vehicle) players in China. BYD is the market leader in

NEV cars and pure electric buses, while Yutong specializes in NEV buses, as it dominates the

plug-in hybrid (PHEV) category and has substantial share in pure electric buses.

Based on our analysis, we favour Yutong over BYD, as we believe Yutong has sound

fundamentals and is financially strong, while BYD’s stock has excessive expectations priced

in, in our view, and we expect some risks ahead. For BYD-H, we are 29-35% below

consensus forecast on FY16/17 profit, whereas for Yutong we are slightly above.

Table 1: Summary of NEV segment comparison for both companies

BYD (H / A) Yutong

Recommendations Hold / Underperform Buy

Target Price HK$43.0/Rmb36.0 Rmb26.0

Earnings growth FY16/17 82%/18% 22%/13%

Profit forecast vs. consensus FY16/17 -29%/-35% 2%/3%

Sector fundamentals

Market Share 33% in NEV PV; 11% in NEV bus 30% in NEV bus

Competitive pressure Intense in car market Mild in bus market

Business operations

Auto volume growth 1H15 grew 17%, driven NEV growth 186% 1H15 grew 3%, driven by NEV growth 103%

Subsidy cut impact FY16/17 2%/7% price pressure 4%/11% price pressure

Government grants 29% of EBIT 6% of EBIT

Capacity utilization in 1H15 c. 70% for battery, 50% for auto c.100%

R&D as a percentage of sales FY14 8.4% 4.2%

Financials

Revenue FY11-14 CAGR 4%, 1H15 growth of 42% FY11-14 CAGR 18%, 1H15 growth of 10%

Gross Margin 1H15 15% 23%

Return on equity Low single digit Consistently maintained at 24%

Cash conversion cycle Deteriorating Improving

Net gearing Consistently net debt, 101% in 1H15 Consistently net cash

Cumulative FCF yield -12% 10%

Source: Jefferies, company data

Market share & business model. Both companies have leading positions in China’s NEV

market, ranked by volume. Yutong has 30% market share of NEV buses in FY14, while BYD

has 33% in the NEV PV and 11% in the NEV bus market, thanks to its popular PHEV

passenger vehicles and K9 pure electric bus. Meanwhile, BYD is a vertically integrated

player, with its own battery manufacturing, battery management system (BMS) and

powertrain capabilities, while Yutong outsources battery supply to external parties such as

ATL, Tianjin Lishen and Samsung SDI, but has its own BMS.

Technology roadmap. In its battery business, BYD traditionally focuses on the

manufacture of LFP (iron phosphate lithium-ion) batteries for NEV, but will shift to NCM

(nickel cobalt manganese lithium-ion) ternary batteries for its first model in 1H16. BYD’s use

of NCM in NEVs is unproven, hence we have reservations. Yutong does not inherit the same

risk. It traditionally procures LFP batteries, and will start using NCM manufactured by

Samsung SDI in 4Q15. We favour NCM over LFP as it has greater room for cost reduction

and energy density improvement. It is important to note that BYD would have to go up

against companies such as Samsung SDI, LG Chem and Panasonic/Telsa on battery

development, in order to achieve success in NEV longer term, which may prove a tall task.

Competition. Our Herfindahl index analysis indicates competition is more severe in NEV

PV than NEV bus. Consensus tends to dismiss competition as a threat for NEV PV, as

industry demand is fast growing. But we would argue FY16 may start to show cracks, with

PV OEMs starting to miss volume expectations due to intensified competition. A price war

may follow, further down the road. For reference, BYD is guiding around 120% volume

growth in FY16, assuming the mid-point of the guided range. Meanwhile, the number of

new NEV car models introduced is 90 in FY15, almost doubling the number of existing

models in the industry. For reference, the NEV PV industry is expected to grow 110% in

FY16.

List of technical abbreviations

NEV: New energy vehicle

PV: Passenger vehicle or car

CV: Commercial vehicle

PHEV: Plug-in hybrid electric vehicle

BEV: Pure electric vehicle

FCV: Fuel cell vehicle

CNG: Compressed natural gas

LNG: Liquefied natural gas

BMS: Battery management system

LFP: Lithium iron phosphate

LMO: Lithium manganese oxide

NCM: Nickel manganese cobalt oxide

NCA: Nickel cobalt aluminum oxide

Industrials

Initiating Coverage

2 December 2015

page 3 of 79 , Equity Analyst, +852 3743 8075, [email protected] Aik Yeo

Please see important disclosure information on pages 74 - 79 of this report.

Subsidy cut. The bus sector faces a more stringent subsidy requirement in 2016

compared to PV, as the bus subsidy no longer depends only on size but also on range and

energy efficiency. A PV subsidy cut, though more subtle, will mainly affect PHEVs where

BYD strength lies. On the other hand, we expect Yutong to withstand the drop in subsidy

better than BYD as its customers are mainly local governments or corporates who are less

price sensitive than average consumers. This would essentially mean passing on some of

the subsidy cut to customers. And based on our analysis, an FY17 subsidy cut merely

extends the pay-back period of NEV buses by around 1.5 more years, from 0.5 years in

FY15. Thus it still makes economic sense to purchase an NEV bus.

Volume & revenue. BYD should see a bigger ramp in volume and revenue growth in

FY16/17 as it is heavily exposed to the under-penetrated NEV PV segment. NEV PV sales

penetration was merely 0.6% in 1H15 vs. 6.8% for NEV bus. Unsurprisingly, its profit

growth will also be superior to Yutong, according to our forecasts.

Despite the strong volume growth expected, we believe BYD would have a problem

meeting volume guidance of 120-150k units in FY16. This is due to i) limited customer base

as buyers mainly originate from license restricted cities – Shenzhen & Shanghai alone

accounted for more than 70% of volume ii) cannibalization of volume despite strong

product introductions, as seen from the recent lacklustre performance of the PHEV Qin

sedan after the introduction of Tang (PHEV SUV) iii) authorities may tackle the issue of

consumers not using electric mode despite buying a PHEV iv) preferential policy towards

BEV (battery electric vehicle), as opposed to PHEV v) intensifying competition.

Meanwhile, Yutong does not face such a problem, as we believe sales penetration of NEV

bus can grow steadily due to i) requirement that 30% of government new vehicle

purchases should be NEV ii) replacement demand from retirement of yellow label vehicles

iii) still generous cash subsidy for NEV bus purchases, despite a subsidy cut in FY16/17 iv)

extensive build-out of charging facilities.

Gross margin. Yutong has a much higher margin than BYD on auto business, as BYD

remains unprofitable for conventional vehicles. Comparatively, Yutong maintains industry-

high profitability in conventional buses and even more so in NEV buses. Going forward, we

expect BYD’s GPM to pick up from 15.8% (FY15) to 16.5% (FY17). Meanwhile, Yutong

should see GPM expand from 24.6% (FY15) to 25.4% (FY17). We are more positive than

consensus on Yutong’s GPM expansion, whereas we are more negative than consensus on

BYD, due to the above-mentioned volume concerns. Note, Yutong has a track record of

improving its GPM yearly since 2010. Also, we would expect Yutong to capitalize on the

cheaper cost of NCM battery procurement in FY17, whereas BYD battery cost reduction

would be hampered by predominant use of LFP and customization cost of new BMS. Also,

BYD’s ability to achieve long term cost reduction on battery manufacturing relies on

upcoming A-share placement, which contains risk as borrowing options are limited.

Financials. Unsurprisingly, BYD’s ROE was a mere 2% in FY14 (due to various unprofitable

segments) vs. Yutong at a high 24%. This was due to Yutong enjoying much better NPM

and asset turnover. Meanwhile Yutong had a steadily improving cash conversion cycle vs.

BYD, which had seen deterioration. And Yutong enjoys a healthy FCF yield of 10% vs. BYD

at -12%. Importantly, BYD is highly geared at 103%, while Yutong has a strong net cash

position. This is partially the reason BYD is relying on an Rmb15bn A-share placement, for

capacity expansion and pay-back of debt. Also interesting to note, in 1H15, 26% of BYD’s

EBIT comes from government grants vs. 6% for Yutong. And if we were to strip off the

government grant, BYD would make 0.5% NPM in 1H15.

Recommendation & Valuation. Based on SOTP valuation for both companies (and

using DCF to cross-check), we initiate Yutong (600066 CH) at Buy with TP of Rmb26.0,

while we initiate BYD - H/A (1211 HK, 002594 CH) at Hold / Underperform with TP of

HKD43.0/Rmb36.0. At their respective TPs, Yutong represents 13x FY17 PER, while BYD is at

42x. Risks are consumer adoption of NEV PV taking off faster than expected, and subsidy cut

having a bigger impact on NEV bus demand than we anticipated.

Industrials

Initiating Coverage

2 December 2015

page 4 of 79 , Equity Analyst, +852 3743 8075, [email protected] Aik Yeo

Please see important disclosure information on pages 74 - 79 of this report.

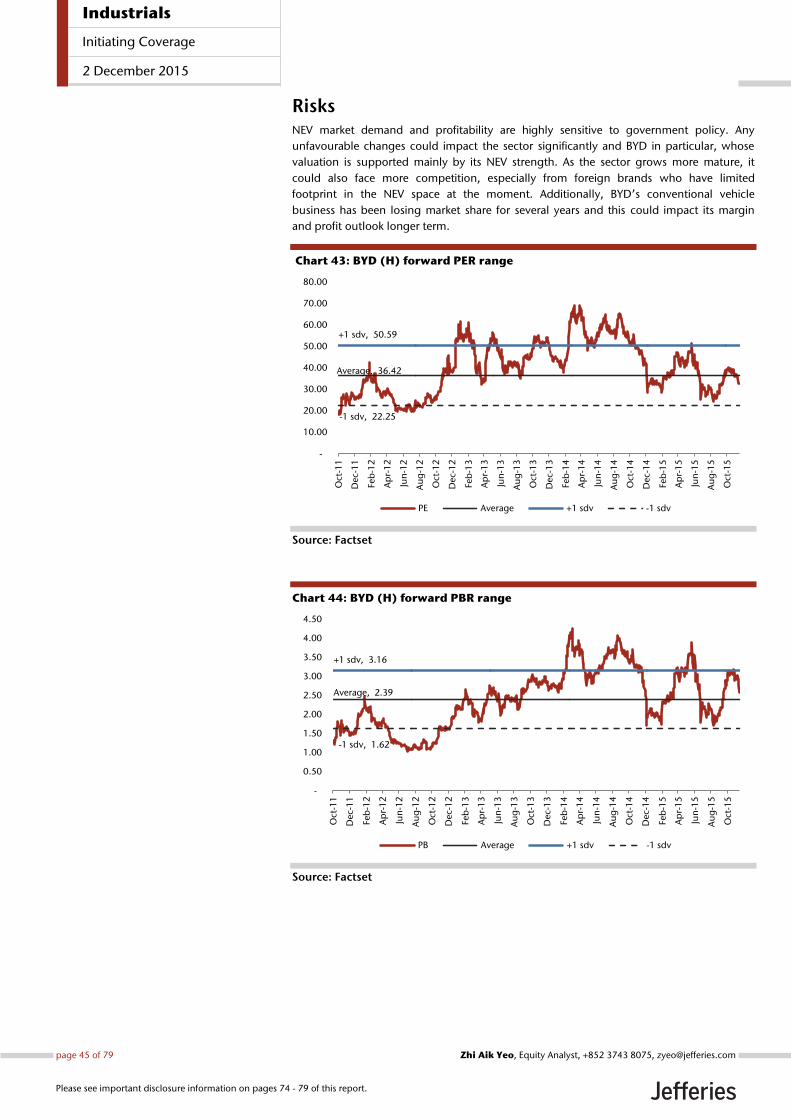

Comparative Study of BYD vs. Yutong BYD is China’s market leader in the sale of NEV passenger vehicles (PV) and pure electric

buses, while Yutong is the market leader in NEV buses because it dominates the plug-in

hybrid (PHEV) category and is actively expanding pure electric offerings. Hence BYD is

commonly seen as having both NEV car and bus exposure, while Yutong is a NEV bus play.

Both companies are pioneers in the Chinese NEV market and we believe for both

companies, the performance of their NEV businesses are the key share price drivers, as seen

from historical trading. In the following pages, do a comparative study of both companies,

particularly on their NEV segments, to determine who has a stronger business proposition.

Below is a summary of the comparison.

Table 2: Summary of NEV segment comparison for both companies

BYD (H / A) Yutong

Recommendations Hold / Underperform Buy

Target Price HK$43.0/Rmb36.0 Rmb26.0

Upside / downside 0%/-43% 19%

Earnings growth FY16/17 82%/18% 22%/13%

Profit forecast vs. consensus FY16/17 -29%/-35% 2%/3%

Sector fundamentals

Market Share 33% in NEV PV; 11% in NEV bus 30% in NEV bus

Competitive pressure Intense Mild

Business operations

Auto volume growth 1H15 grew 17%, driven NEV growth 186% 1H15 grew 3%, driven by NEV growth 103%

Business model Vertically integrated, in-house battery, BMS Outsourced battery to ATL, Samsung SDI

Products NEV & conventional vehicle, batteries,

handset & electronic components

PHEV and EV bus;

conventional bus

Subsidy cut impact FY16/17 2%/7% price pressure 4%/11% price pressure

Government grants 29% of EBIT 6% of EBIT

Capacity utilization in 1H15 c. 70% for battery, 50% for auto c.100%

R&D as a percentage of sales FY14 8.4% 4.2%

Financials

Revenue FY11-14 CAGR 4%, 1H15 growth of 42% FY11-14 CAGR 18%, 1H15 growth of 10%

Gross Margin 1H15 15% 23%

Return on equity Low single digit Maintained at 24% consistently

Cash conversion cycle Deteriorating Improving

Net gearing Consistently net debt, 101% in 1H15 Consistently net cash

Cumulative FCF yield -12% 10%

Source: Jefferies, company data

Market Share BYD has a blended 28% of the China NEV market in FY14, and almost 30% share in 1H15.

This NEV market share is shared between the PV and bus segments, at 33% and 13% share

respectively (please refer to pie charts below).

BYD leads in the PHEV segment of PV, and has a front running position in pure electric

buses. BYD has quickly grown its market share in the PHEV sub-segment, due to the

popularity of its PHEV Qin sedan, and more recently the Tang (PHEV SUV).

More importantly, we believe Shenzhen’s restriction quota, introduced at year-end 14, was

a key factor of BYD strength this year. The policy stipulates that Shenzhen would have

100,000 units quota yearly, 20,000 of that for NEV, while 80,000 for conventional. The

20,000 NEV quota is entirely on lottery, while the 80,000 is half on lottery and half on

bidding. After the policy implementation, Shenzhen residents found it much easier to

purchase a NEV instead of a conventional car.

On the back of the restriction quota, and due to BYD being based in Shenzhen, we expect

the city to account for at least 35% of BYD’s NEV volume in FY15, the other big market

being Shanghai. But the quota is not going to grow, and we believe that will cap BYD’s

volume growth and consequently market share.

Market share in 1H15 had been

boosted by Shenzhen restriction

quota introduced in year-end 14

BYD has pole position in NEV PV and

exposure in pure electric bus.

Industrials

Initiating Coverage

2 December 2015

page 5 of 79 , Equity Analyst, +852 3743 8075, [email protected] Aik Yeo

Please see important disclosure information on pages 74 - 79 of this report.

Chart 1: China NEV PV Market Share by OEM in FY14, total

volume ~52,000 units

Source: Jefferies, CPCA

Chart 2: China New Energy Bus Market Share by OEM in

FY14, total volume ~ 23,000 units

Source: Jefferies, CAAM

Meanwhile, Yutong has seen a slight market share loss in 1H15. As the largest NEV bus

manufacturer in China, Yutong achieved 32% market share in 2014, and near 30% in 1H15,

having significant exposure to both PHEV and EV bus segments. The market share loss in

1H15 was due to relative weak growth on 6-8 meters pure electric buses, as smaller players

gained share on the back of a generous subsidy for this particular category.

Yutong sold NEV buses in more than 30 cities across China, which contributed to its leading

NEV market share in China. Notably, Yutong is one of the few NEV bus manufacturers that

has broken free of local protectionism and penetrated Chinese regions outside of its home

market.

In FY14, Yutong sold over 72% of its NEV buses to cities outside of its home region. This is

the highest proportion amongst the top 8 players. There are peers that sell a higher

proportion of NEV buses outside their home regions, but these are much smaller players.

PV and Bus Markets Between the NEV passenger vehicle and bus markets, the former had shown stronger

growth in recent times. In 1H15, NEV PV grew over 320% vs. NEV bus growth of 78%. This,

we believe is due to the lesser penetration of NEV PV of merely 0.6% as a proportion of PV

sales in China. Comparatively, NEV bus penetration was at 6.8% in 1H15.

OEMs that witnessed the strong growth to date do not want to be left out in the race. That

explains the aggressive NEV product pipelines of PV OEMs in the coming months. Other

than the aggressive introduction of new models, anecdotal evidence suggests NEV PV

consumers mainly come from license restricted cities, which limits the size of the captive

audience i.e. market. These 2 factors are causing competition to intensify and should get

more severe in the coming years.

In terms of competition, the NEV bus market is less competitive vs. NEV PV. Based on the

Herfindahl index, which measures the level of competition within a sector, NEV PV is at 19%

vs. the Bus market 23% (Chart 4). The lower the percentage, the more competitive it is.

BYD, 33%

Chery, 18% Kandi, 15%

Zotye, 13%

BAIC, 10%

SAIC, 5% Others, 5%

Yutong PHEV

24%

Yutong EV

8%

Jinlong PHEV

10%

Jinlong EV

5%

BYD EV

11%

Others PHEV

31%

Other EV

11%

Yutong has leading market share in

NEV buses. The company also leads

in share of vehicles that are sold

outside its home region.

NEV car market will see stronger

growth than NEV bus due to smaller

base & lesser penetration.

But NEV PV market is more

competitive as OEMs are all gunning

for that growth

Industrials

Initiating Coverage

2 December 2015

page 6 of 79 , Equity Analyst, +852 3743 8075, [email protected] Aik Yeo

Please see important disclosure information on pages 74 - 79 of this report.

Chart 3: Herfindahl Index (HHI) for PV and Bus markets

in 2014, PV is more competitive

Source: Jefferies, CAAM

Chart 4: Herfindahl Index (HHI) for NEV PV and NEV Bus

markets in 2014, NEV PV is more competitive

Source: Jefferies, CAAM

It is a similar story for the broader sector as a whole (Chart 3) i.e. PV market vs. Bus market.

This is hardly surprising, as even though the bus market still has many players i.e. 43 in

2014, market share is concentrated in the hands of a few big OEMs, including Yutong. On a

relative basis, PV market share is more evenly spread across the 66 players in FY14.

The market concentration ratio is very high in the bus market, which supports it being less

competitive. The combined market share of the Top 3 companies is above 41% in the

overall bus market in FY14 and has been relatively stable over the past two years. To add,

the top 5 players accounted for 54% of the market, and top 10 accounted for 75%. And

referring to the chart below, we can see that even for the different sub segments i.e. large,

medium, light bus market, the concentration among the top players remains very high.

Chart 5: Top 3 players’ market share in various bus segments - concentration is

very high

Source: Jefferies, CAAM, Company data

Future Competition The above analysis on competition is done on history, whereas if we try looking ahead into

the future, we will find PV NEV competition getting more intense. In FY15, 90 new NEV PV

models have been or would be launched locally (excluding imported models). The total

number of models will almost double from around 93 in FY14 to 183 by end-15. PHEV

models have seen significantly less competition historically, but number of car model

launches has also increased 91% from 11 (FY14) to 21 (FY15).

4.9%

10.4%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

PV Bus

18.8%

22.8%

0%

5%

10%

15%

20%

25%

NEV PV NEV Bus

40% 41%

56% 54%

44%

48%

55% 52%

0%

10%

20%

30%

40%

50%

60%

Total 2013 Total 2014 Large bus

2013

Large bus

2014

Medium

Bus 2013

Medium

Bus 2014

Light Bus

2013

Light Bus

2014

NEV bus market is not as competitive

as market share is dominated by a

few players…

…and it’s a similar story for the

overall bus market.

New NEV model introductions are

aggressive, expect competition to

intensify

Industrials

Initiating Coverage

2 December 2015

page 7 of 79 , Equity Analyst, +852 3743 8075, [email protected] Aik Yeo

Please see important disclosure information on pages 74 - 79 of this report.

Chart 6: Number of new NEV car models launched every year - big jump in 2015

Source: Jefferies, CAAM, Company data

However, we believe the competition in NEV PV market has yet to see its peak. In 2014, top

10 selling NEVs were manufactured by domestic brands (the 10th being a localized version

of Nissan Leaf), and together they account for 78% market share.

This contrasts with the conventional car market, where domestic brands commanded 32%

share in 2014, vs. 68% for JVs. What this means is many foreign brands have yet to step into

the market, and we see that happening over the next couple of years. Beijing Hyundai may

launch Sonata PHEV in 2016 and we expect brands like VW, GM, Ford and PSA to join the

fight in 2017. PHEV will likely to be a focus of the JVs to address the mass market segment.

Below, we illustrate the competition that BYD e6, Qin and Tang are up against currently, by

showing comparisons with other popular NEV PV models. Compared to Geely Emgrand EV

and BAIC EV200, BYD e6 is not competitive on pricing. And even though Qin & Tang still

hold an edge over the PHEV segment for now, we are afraid it might be affected by

government’s policy/ subsidy preference for BEV.

Chart 7: Comparison of key PHEV and BEV car models in China – BYD will maintain edge in PHEV for now

Source: Jefferies, company data, Wikimedia Commons

16 23

41

80

5

6

2

10

0

10

20

30

40

50

60

70

80

90

100

2012 2013 2014 2015

EV PHEV

Model e6 Geely Emgrand EV BAIC EV200 Model S Qin Tang Roewe 550 Plug-ine6先行者 帝豪EV精英型 EV200 轻秀版 85D 4dr All-wheel Drive 2015 秦双冠版 新旗舰型 2015款 2.0T 四驱豪华型 荣威550 PLUG-IN豪华版

OEM BYD Geely BAIC Tesla BYD BYD SAIC

MSRP (Rmb) 330,000 239,800 226,900 816,800 209,800 251,300 248,800

Subsidy (2015) 110,000 110,000 90,000 60,000 60,000 60,000

Post-subsidy Price 220,000 129,800 136,900 149,800 191,300 188,800

Type BEV BEV BEV BEV PHEV PHEV PHEV

0-100km/h accelerations (sec) 12 9.9 13 4.2 (0-60mph) 5.9 4.9 9.5

Top Speed (km/h) 140 140 125 250 (155mph) 185 180 200

Battery LFP NCM NCM NCA LFP LFP LFP

Battery Capacity (Kwh) 82 45 30 85 13 18.4 12

Electric Range (KM) 400 253 200 435 70 80 60

Battery Density 150wh/kg 81wh/kg

Weight (KG) 2283 1570 1290 2188 1720 2220 N/a

Estimated Home Charging Time 10 hrs 14hrs 9 hrs 12 hrs 8 hrs 10hrs 8hrs

Dimensions (mm)

Length 4,560 4,631 4,025 4,976 4,740 4,815 4,648

Width 1,822 1,789 1,720 1,963 1,770 1,855 1,827

Height 1,630 1,495 1,503 1,435 1,480 1,720 1,479

Wheelbase 2,830 2,650 2,500 2,959 2,670 2,720 2,705

Fuel consumption (L/100km) 0 0 0 0 1.6 2.4 1.6

Engine 1.5T 2.0T 1.5L

Warranty 6 years/150,000km 4 years/100,000km 5 years/100,000km 8 years 6 years/150,000km 6 years/150,000km 5 years/100,000km

Comparisons with the conventional

car market indicate that JV brands

have yet to step in to compete, and

it will just get more competitive in

the next few years

Industrials

Initiating Coverage

2 December 2015

page 8 of 79 , Equity Analyst, +852 3743 8075, [email protected] Aik Yeo

Please see important disclosure information on pages 74 - 79 of this report.

Subsidy Adjustment Impact In terms of the subsidy adjustments happening in FY16/17, we believe the pricing pressure

on Yutong will be larger than BYD, as more stringent requirements are introduced for

buses. In Table 3 below, we carried out an analysis to estimate by how much vehicle prices

need to be reduced in FY16/17, given changing subsidies, assuming customers pay the

same price as FY15. Yutong will have to cut as much as 11% in 2016 and another 7-12% in

2017, while the impact for BYD is mostly in single digits.

However in reality, it depends on the bargaining power of the OEMs over the customers.

We believe consumers of NEV cars would be more price sensitive vs. local governments’

purchase of NEV buses, as they are bounded by purchase targets. It is mandated that 30%

of annual vehicle purchase must come from NEVs. Therefore we are of the view that the

eventual impact of subsidy cut will be well cushioned by Yutong.

We are forecasting overall ASP changes by 6%/-2% for Yutong vs. -8%/-2% for BYD in

FY16/17, respectively. This forecast takes into consideration factors such as EOS, ability to

adjust product mix and bargaining power over customers.

Table 3: Subsidy impact on model pricing – bus will see generally bigger

decline in subsidy vs. car models

BYD Major Models 2016 2017

K9 (12m Bus) -4% -10%

Tang (PHEV) -1% -5%

Qin (PHEV) -1% -6%

E6 (EV) 1% -7%

Yutong Major Models 2016 2017

E7 (7m) -11% -12%

E12 (12m) 0% -11%

14m PHEV (14m) 0% -7%

Source: Jefferies estimates, company data

Business Model One basic difference between the NEV businesses of both companies: BYD is a vertically

integrated NEV manufacturer, while Yutong outsources battery supply to Tianjin Lishen and

Amperex Technology Limited (ATL), mainly LFP batteries.

ATL, which started out as the main supplier for Apple in small batteries, is now trying to

enter the large battery segment and is significantly behind market leaders such as Samsung

SDI, Panasonic/Tesla and LG Chem, in our view. And Korean competitor Samsung SDI will

be contributing ternary (NCM) lithium ion batteries to Yutong starting from 4Q15.

On the other hand, BYD is the one of the most integrated OEMs globally, thanks to its

Chairman’s long-standing focus on technology and the company's history of pursuing

vertical integration. Chairman Wang has a technical background, with a bachelor’s degree

majoring in metallurgy physical chemistry.

BYD supplies its own in-house cells for its NEVs, but it is also engaged in assembling battery

packs and even designing battery management systems (BMS) and electric motor

controllers. We thus see BYD’s integrated model could help the company gain an

advantage in NEV manufacturing at the infancy stages of the industry, as it would enjoy:

Consistency in battery standards

Easier integration with own EVs

Guaranteed supply availability

Cost savings synergies with battery manufacturing

In Table 3, we calculated the impact

on selling prices in FY16/17 if

customers still pay the same, as a

result of the subsidy cut. Buses seem

more impacted than cars.

But in reality, the impact on prices

and margins depends on other

factors as well, such as bargaining

power over customers, ability to

adjust product mix and EOS.

BYD is a vertically integrated player,

while Yutong outsources battery

manufacturing.

BYD’s advantage of vertical

integration may only stand during

the early stages of industry

development and in battery supply

shortage situations.

We expect Yutong to withstand the

subsidy reduction better despite

potentially experiencing a bigger %

subsidy cut vs. BYD

Industrials

Initiating Coverage

2 December 2015

page 9 of 79 , Equity Analyst, +852 3743 8075, [email protected] Aik Yeo

Please see important disclosure information on pages 74 - 79 of this report.

More importantly, batteries are in shortage in China currently, based on our channel

checks. This gives the company an edge in having the security of an in-house battery

supply, at a time when the industry is taking off. At present, Chinese automakers pay a

hefty Rmb2,000/kwh (USD315/kwh) for battery packs. This, in our view, is due to the

explosive growth of NEV demand in China, and specifically the increasing prevalence of

NEV buses, which necessitates heavy battery usage.

However, we expect 2H16 will be the time when supply-demand will balance, due to

aggressive battery capacity expansion in China, and 2017 will potentially see oversupply.

And over the longer term, we adopt a cautious view on whether BYD battery technology

and cost can compete with international competitors such as LG Chem, Panasonic / Tesla

and Samsung SDI. In the sections below, we will highlight the risks BYD faces in battery

technology development.

Technology Roadmap For EV power, lithium-ion batteries have so far been the preferred choice, however they can

be sub-divided into several types of chemical configuration, with varied cost, energy

efficiency, density, safety and durability. The main ones in the market are:

Iron phosphate lithium-ion (LFP)

Manganese lithium-ion (LMO)

Nickel cobalt manganese lithium-ion (NCM)

Nickel cobalt aluminum lithium-ion (NCA)

There is an obvious trade-off between energy density and safety: the higher the energy

density, the higher the chance of fire accidents. Thus far, BYD had focused on LFP, which is

believed to be the safest material, as the core battery chemistry for existing NEVs.

However, LFP batteries have limitations in other aspects, especially energy density, which

gets translated to higher costs for the same power. On the other hand, ternary battery (NCA

or NCM), which are more prone to fire accidents, are weaker on safety but more effective in

energy density. Tesla is a big proponent of the ternary NCA batteries, which it heavily

utilizes in its car models. The market seems to be gravitating towards ternary battery, after

learning how to minimize the probability of fire accidents by improving the BMS.

BYD has said it already has capability in ternary battery, in particular NCM, apart from the

LFP. While it has made 3bn units of ternary batteries for mobile phones, it hasn’t used

ternary cells in NEVs yet, due to fears of fire accidents. This constitutes our key reservation,

as the integration remains unproven. According to the company, going forward BYD will

increasingly use LFP batteries in trucks and buses and NCM batteries in light NEVs and in

particular, small-sized SUVs.

Even though Yutong doesn’t manufacturer NEV batteries, it too focuses on use of LFP for

most of its existing products, mainly through procurement from external parties. Yutong

predominantly procures LFP batteries from companies such as ATL and Tianjin Lishen, but

will shift towards NCM batteries from Samsung SDI starting in 4Q15. Yutong expects

greater cost savings from ternary in longer term because:

Energy density is higher, hence raw material need is lower

Production cost is lower per unit energy

However ternary battery will have more security concerns, hence it requires higher

standards of electrical control technology and BMS, in which Yutong currently leads, in the

NEV bus industry. Because of better compatible infrastructure and scale, management sees

greater cost saving synergies vs. peers.

But longer term, BYD would have to

go up against the global battery

giants to have an edge in NEV, which

may prove a tall task.

Lithium ion battery is the preferred

choice of EV power, but there are

different variations of this battery

type, with different pros and cons

BYD focuses on LFP traditionally, but

wants to gradually switch to NCM

BYD use of NCM is unproven as yet

Yutong will start procuring NCM in

4Q15, has traditionally used LFP

NCM is superior to LFP in energy

density and production cost, and

importantly it provides greater room

for cost savings ahead

Industrials

Initiating Coverage

2 December 2015

page 10 of 79 , Equity Analyst, +852 3743 8075, [email protected] Aik Yeo

Please see important disclosure information on pages 74 - 79 of this report.

The introduction of NCM battery will not entail any change to the plant layout or

production process, according to Yutong. And the company will only need to lift safety

standards in the storage facilities to prevent fire accidents.

Technology Risk Despite prevalent media coverage and strong growth of late, the EV industry is still at its

early stages of development given the immaturity of battery technologies. EV battery is still

evolving, and its future technology track remains unclear. It is unknown which chemical

configuration will emerge as the winner for EV battery over the longer term.

Furthermore, it is not clear whether plug-in hybrids (PHEV) or pure electric NEVs will be the

ultimate solution for clean mobility. Fuel cell vehicle (FCV) technologies are advancing fast,

as seen in the Japanese market, and it is prompting consideration as the technology of

choice for future vehicles, given higher energy efficiency and better convenience of use vs.

electric vehicles.

For BYD, the technology risk is to put most eggs into LFP technology for NEVs, only

considering a diversification to NCM recently. NCM should have greater room for cost

reduction and increase in energy density vs. LFP longer term. Even though the company

did state that NCM battery is not new to them, as they have been using ternary battery in

mobile phones, we are not sure the experience is replicable to cars. Moreover, the BMS

would have to be reconfigured to match the NCM batteries, which would come in the form

of additional costs.

However, we do recognize that BYD should be a bigger beneficiary in the short term vs.

Yutong if the demand for battery overtakes supply. This is what we are seeing in the

Chinese market currently. if BYD can hedge its technology risk appropriately, the vehicles

should benefit from vertical integration in the longer run, given more seamless integration

with batteries and ability to respond to market demand quicker vs. peers that outsource.

Yutong on the other hand, does not inherit such a technology risk, as it procures battery

from external parties, including Samsung SDI, Tianjin Lishen and ATL. We see this as the

more conservative move since the risk of aligning with the wrong technology can be costly,

even with the Chinese government’s backing of electric vehicles.

Referring to our industry section on page 28, battery manufacturing cost should continue

to decline over the longer term, and competition among the battery makers should

intensify, along with the huge capacity buildout plans. Thus Yutong would benefit as

battery makers pass on the cost savings eventually.

Segmental Breakdown BYD as a company derives a much bigger portion of its revenue from businesses outside of

autos, and at times it is seen as a conglomerate instead of an auto OEM. This is the key

reason why SOTP valuation is common used and relevant for the company. Apart from core

auto business, it has a handset component/assembly arm, solar, battery and majority

holdings in BYD Electronics (285 HK, NC).

BYD’s auto business includes both conventional and NEV segments, the latter of which is

one of the most vertically integrated vs. industry peers. It has in-house battery cell

production, assembly of battery packs and even design of battery management systems

(BMS) and electric motor controllers. BYD’s NEV revenue accounted for 35% of Auto

segment revenue or 19% of total revenue in 2014.

This business model contrasts with Yutong, which specializes in the bus space of the auto

sector, and derives most of its revenue and profit in large and medium-sized buses. In FY14,

Yutong derived 22% if its bus sales revenue from NEV buses, in particular large NEV buses.

Battery technology is still evolving

Clean mobility technology track is

undecided too

We have reservations over BYD’s

competitiveness in NCM, and it

would come at the extra cost of a

new BMS that fits

With batteries in shortage in China,

BYD has an advantage, due to the

uncertainty of battery supply

Yutong does not inherit the same

technology risk, as it sources

batteries

Long term battery cost will continue

declining on the back of EOS and

capacity buildout and that would

erode BYD’s advantage

Both companies derive the biggest

portion of their revenue and profit

from auto manufacturing.

BYD’s NEV revenue was 19% in FY14

Yutong’s NEV revenue was 22% in

FY14

Industrials

Initiating Coverage

2 December 2015

page 11 of 79 , Equity Analyst, +852 3743 8075, [email protected] Aik Yeo

Please see important disclosure information on pages 74 - 79 of this report.

Chart 8: BYD revenue by segment

Source: Jefferies, company data

Chart 9: BYD operating profit by segment

Source: Jefferies, company data

In 1H15, BYD had 56% of revenue coming from ‘autos and related products’, and 37%

from ‘mobile handset components’, with ‘rechargeable batteries and photovoltaic’

accounting for the remainder 7%. This compares with Yutong deriving 92% of revenue

from bus sales, and only 8% from transportation services and other businesses.

BYD derives an even bigger portion of its profitability from the auto segment, with 70% of

its gross profit from the segment. Mobile handsets and rechargeable batteries contribute

around 29% and 4%, respectively. For Yutong, it’s a relatively similar picture on the profit

front vs. revenue, where Yutong derives more than 90% from bus sales.

Chart 10: Yutong revenue by segment

Source: Jefferies, company data, Before 2013, all bus combined

Chart 11: Yutong gross profit by segment

Source: Jefferies, company data Before 2013, all bus combined

Volume & Volume Growth BYD total volume growth in FY14 was down 21% y/y due to sharp drop in conventional

vehicles volume. The conventional vehicle segment was down 25% to 352,200 units. Other

than F3 and S6 which saw growth, all other models experienced significant falls in volume

y/y.

In contrast to the weak showing of the conventional vehicle segment, NEV volume spiked

8.8x to 20,807 units in the same period, albeit off a small base. This was mainly driven by i)

new product launch of Qin in late-2013, which saw a strong volume ramp-up in FY14 ii)

strong policy support from the Chinese government.

10% 10% 11% 10% 9%

44% 42% 39% 39% 44%

46% 48% 51% 51% 47%

0%

20%

40%

60%

80%

100%

120%

2010A 2011A 2012A 2013A 2014A

Automobiles and related products

Mobile handset components and assembly service

Rechargeable batteries and photovoltaic business

45% 37% 33%

54% 62%

48% 67% 79%

40% 33%

-20%

0%

20%

40%

60%

80%

100%

120%

2010A 2011A 2012A 2013A 2014A

Automobiles and related products

Mobile handset components and assembly service

Rechargeable batteries and photovoltaic business

Large Bus

62%Large Bus

60%

Medium Bus

29%Medium bus

28%

Light bus

4%Light bus

5%

Total Bus

96%

Total Bus

95%

Total Bus

95%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014

Large Medium Light Bus Service Other

Large Bus

64%Large Bus

62%

Medium Bus

27%Medium Bus

26%

Total Bus

97%Total Bus

96%Total Bus

94%

Light bus

4%Light bus

5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014

Large Medium Bus Light Service Other

We do not have clarity, but we

believe BYD’s NEV contribution to

profit is bigger than Yutong’s as

conventional car business is losing

money

BYD’s NEV volume growth in FY14

was 880%

BYD’s total volume growth was

down 21% in FY14

Industrials

Initiating Coverage

2 December 2015

page 12 of 79 , Equity Analyst, +852 3743 8075, [email protected] Aik Yeo

Please see important disclosure information on pages 74 - 79 of this report.

Table 4: Historical volume performance: BYD delivered 186% NEV volume

growth in 1H15 (units)

BYD 2013 2014 y/y 1H2015 y/y

NEV 2,120 20,807 881% 21,645 186%

E6 1,544 3,560 131% 2,900 108%

Qin 142 14,747 10285% 16,477 208%

Tang 412

Bus 434 2,500 476% 1,856 127%

Others

Non-NEV 471,880 352,193 -25% 188,355 9%

F3 84,364 110,296 31% 76,438 62%

L3 99,450 54,531 -45% 7,709 -73%

Speed 101,152 65,312 -35% 28,710 -27%

S6 93,168 98,720 6% 12,927 -75%

S7 - 6,938 58,586

Others 93,746 16,396 -83% 3,985 -27%

Source: Jefferies, company data

Again, in 1H15, BYD’s NEV volume grew a staggering 1.9x to reach 21,645 units. The

growth rate was weaker than industry NEV growth of 240% y/y but still very strong, driven

by Tang’s (launched in May) incremental volume, and Qin’s rapid volume ramp. More

specifically, industry EV segment grew 293% while PHEV grew 205% in the same period.

BYD also became the largest NEV seller in the world for the first time in May 2015, with

strong volume growth seen in PHEV units. BYD is projected to sell 50,000-60,000 units this

year, up nearly 4x y/y. Next year the company is aiming for 120,000 -150,000 units of NEV

sales, up more than 1x y/y.

The BYD Tang (released in July this year) is selling much faster than anticipated, with

monthly sales already exceeding 5,000 units in Oct 15. Management estimates 2016 sales

at 100,000, but we are not as optimistic. Meanwhile, the volume of conventional autos

grew 9% to 190,000 units in 1H15, on the back of strong S7 SUV performance, which saw

average monthly volume of 9,500 units.

Table 5: Yutong historical volume performance ; Yutong delivered 103% NEV

volume growth in 1H15 (units)

Total 2013 2014 y/y 1H2015 y/y

Total 56,068 61,398 10% 24,079 3%

By Type

NEV 3,897 7,405 90% 3,645 103%

Non-NEV 52,171 53,993 3% 20,434 -5%

By Size

Large 25,584 27,398 7% 9338 -12%

Medium 25,020 25,880 3% 11068 11%

Light 5,464 8,120 49% 3673 31%

Source: Jefferies, company data

Meanwhile for Yutong, total bus volume grew 9.5% in FY14 to 61,400 units – Large (45%),

Medium (42%) and Small (13%). NEV bus growth was up a massive 90% to 7,400 units in

FY14. This was on the back of encouraging regulatory initiatives, subsidy programs and

replacement demand.

In 1H15, total volume was up 3% y/y to 24,100 units: Large (-12%), Medium (11%) and

Small (31%). In terms of NEV, growth accelerated further from FY14’s high growth level to

103% or 3,645 units in 1H15. Large NEV buses are expected to be stronger next year due to

government’s preferential policy for bigger, more efficient modes of transport.

BYD’s NEV volume growth was

186% in 1H15

Tang volume has done well since

launch

BYD became the largest NEV seller

globally in 2015

Yutong NEV grew 90% in FY14,

103% in 1H15

Industrials

Initiating Coverage

2 December 2015

page 13 of 79 , Equity Analyst, +852 3743 8075, [email protected] Aik Yeo

Please see important disclosure information on pages 74 - 79 of this report.

Revenue & Revenue Growth In terms of absolute revenue, BYD is almost 3x the size of Yutong in 1H15. BYD had a top

line of Rmb30.4bn compared to Yutong’s Rmb10.4bn in 1H15. Comparing solely the auto

sales of both companies, BYD’s Rmb17bn worth of revenue was 78% larger than Yutong’s

Rmb9.6bn auto sales. BYD’s lead comes from its dominant positon in NEV passenger

vehicles; conventional passenger vehicles contributed too, albeit not profitable currently.

However, if we go back further in history, Yutong saw stronger revenue growth of 18%

CAGR between FY10-14 vs. a mere 4% for BYD. But in 1H15, the tables turned, as BYD’s y/y

revenue growth accelerated to a staggering 21% vs. 11% at Yutong. This is on the back of

42% y/y spike in auto revenue vs. mere 8% for Yutong in 1H15.

BYD’s 1H15 auto revenue growth accelerated, despite a slowdown in demand growth in

the PV industry (1.4% y/y volume growth).

Table 6: BYD and Yutong: Revenue Comparison (Rmb mn)

2010 2011 2012 2013 2014 1H15 11-14 CAGR

BYD 46,685 46,312 44,381 49,768 55,366 30,435 4%

y/y -1% -4% 12% 11% 21%

BYD Auto 21,550 22,136 22,551 25,291 26,270 16,962 5%

y/y 3% 2% 12% 4% 42%

Yutong 13,479 16,932 19,763 22,198 25,728 10,387 18%

y/y 53% 26% 17% 12% 16% 10%

Yutong Bus 12,917 16,161 18,740 21,010 23,977 9,554 17%

y/y 54% 25% 16% 12% 14% 8%

Source: Jefferies, company data

Referring to the table below, the main source of BYD’s auto revenue acceleration came

from the NEV business, where it was up 1.2x y/y in 1H15 to Rmb5,870mn, which

accounted for 35% of auto segment revenue or 19% of total revenue. In the same period,

NEV volume grew 1.9x, and in particular NEV bus grew 1.3x. Conventional volume grew

merely 9%.

Table 7: BYD historical volume performance; NEV growth was strong but

conventional cars’ growth remained weak despite stimulus (units)

2013 2014 y/y 1H2015 y/y

NEV (including Bus) 2,120 20,807 881% 21,645 186%

Bus 434 2,500 476% 1,856 127%

Conventional car 471,880 352,193 -25% 188,355 9%

Source: Jefferies, company data

Gross Margin For FY14, Yutong achieved higher gross margin of 24.3% vs. BYD’s 13.8%, a gap of

10.5ppt. If we look at the auto businesses alone, gross margin of 24.2% exceeded BYD by a

significant 7.6ppt. It is important to note that Yutong has been improving its gross margins

since 2010.

For 1H15, Yutong achieved higher gross margin of 23.4% vs. BYD 15.0%, a gap of 8.3ppt.

In auto manufacturing, gross margin of 23.0% exceeded BYD by 4.3ppt.

BYD is 3x the size of Yutong in

revenue terms

Yutong saw higher revenue growth

historically, but that changed in

1H15 when BYD overtook it

Unsurprisingly, the NEV segment

was the key contributor to BYD’s

strong revenue growth

Yutong has a clear superior GPM vs.

BYD; Yutong has consistently

improved its GPM since 2010

Industrials

Initiating Coverage

2 December 2015

page 14 of 79 , Equity Analyst, +852 3743 8075, [email protected] Aik Yeo

Please see important disclosure information on pages 74 - 79 of this report.

Yutong’s industry-high gross margin can be explained by economies of scale in both NEV

and conventional buses segments, delivering 25.5% and 23.9%, respectively. While it’s

easy to comprehend that NEV buses benefit from a deep government subsidy that supports

its high profitability, it is also true that Yutong commands a price premium over

competitors on conventional buses, which gives it a high margin vs. peers.

Table 8: Gross Margin Summary – Yutong had been consistently improving

GPM, much superior to BYD

Gross Margin 2010A 2011A 2012A 2013A 2014A 1H15A

BYD 17.7% 14.8% 11.6% 13.1% 13.8% 15.0%

BYD Auto 21.2% 19.0% 14.4% 14.5% 16.6% 18.8%

Yutong 17.3% 18.2% 20.0% 23.1% 24.3% 23.4%

Yutong Bus 17.6% 18.2% 19.8% 22.9% 24.2% 23.0%

Source: Jefferies, company data

Even though Yutong held a substantial lead in FY14 on gross margin, the difference has

narrowed in 1H15, due to the rapid ramp-up of BYD’s PHEV and EV bus sales. Please refer

to Table 4. We believe BYD can deliver higher profitability with scale, lower battery costs

and better product mix in the coming years. The better product mix from moving into NEV

SUVs should award the company a kicker in margins, as Tang’s contribution started only in

2H15.

Return on Equity From a return on equity (ROE) perspective, Yutong is superior to BYD by a long mile.

Referring to the chart below, Yutong achieved 24% and 21% ROE in FY14/FY13,

respectively. This compares with a mere 1.7% and 2.5% for BYD in the same period.

We conducted a DuPont analysis (Table 9 below). Breaking down into its components, BYD

achieved net margin of 0.8% in FY14, along with asset turnover of 59% and leverage of

3.7x. This generated ROE of a mere 1.7%.

This compares with Yutong’s net margin of 10.2% in FY14, coupled with asset turnover of

108% and leverage of 2.2x. This generated an ROE of 24.2%.

We believe a key reason for BYD lagging ROE is due to a much lower margin vs. Yutong. In

terms of net margin, Yutong has a superior lead over BYD, achieving 10.2% in FY14 vs.

BYD’s 0.8%. This is largely due to BYD making losses on conventional autos and solar

business, which dragged on the profitability of NEV business and mobile handset segment.

Chart 12: ROE comparison – Yutong has had consistently higher ROE than BYD

Source: Jefferies, company data

14%

7%

0% 3% 2%

35% 35%

21% 24% 24%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2010A 2011A 2012A 2013A 2014A

BYD Yutong

Yutong’s superior margin is due to

EOS, deep government subsidy,

price premium commanded over

peers

BYD narrowed the gap vs. Yutong in

1H15, as it turned profitable on NEV,

and conventional car business

reduced losses

Yutong is superior in ROE by a mile,

and it has remained so over the past

few years.

Yutong has a strong lead in net

margin and asset turnover, which

contributed to its higher ROE

Industrials

Initiating Coverage

2 December 2015

page 15 of 79 , Equity Analyst, +852 3743 8075, [email protected] Aik Yeo

Please see important disclosure information on pages 74 - 79 of this report.

Table 9: ROE Breakdown – Yutong excels in net margin and asset turnover

2014 Net Margin Asset

Turnover

Asset/Equity DuPont ROE

BYD 1% 59% 3.71 2%

Yutong 10% 108% 2.20 24%

Source: Jefferies, company data

Working Capital The cash conversion cycle is a metric used to gauge the effectiveness of management and

the company’s overall health. The calculation measures how fast a company can convert

cash on hand into inventory and accounts payable, through sales and accounts receivable,

and then back into cash. Hence it indicates the efficiency of the management's ability to

employ short-term assets and liabilities to generate cash for the company.

The result, which be seen clearly from the table below, is that BYD’s cash conversion cycle

had deteriorated from 2012-14 from a negative 63 days to negative 1 day. This compares

with Yutong, which improved from 3 days in 2012 to negative 17 days in 2014.

For BYD, accounts receivable days drastically lengthened in 2014 vs. 2012, which was the

main cause of cash conversion deterioration. Although Yutong had seen a similar trend in

terms of receivable days lengthening, it was more than made up for by the expansion of

payable days. This helped Yutong improve its cash conversion cycle.

Table 10: Working capital calculation – Yutong has a superior cash conversion

cycle vs. BYD

BYD Yutong

Account Receivable Days

2012 82 73

2013 96 83

2014 148 132

Account Payable Days

2012 213 99

2013 213 97

2014 225 171

Inventory Turnover Days

2012 68 29

2013 69 29

2014 76 22

Cash Conversion Cycle

2012 (63) 3

2013 (47) 15

2014 (1) (17)

Source: Jefferies, company data

Net Gearing BYD’s net debt to equity ratio has increased over the years (getting more leveraged) due to

higher capex and unstable earnings. The ratio rose to 103% in 2014, and the company is

planning an equity raise in 2016, to carry out their capacity expansion plan.

For the company to borrow onshore from banks, total liabilities/total assets ratio is also

monitored, with 70% seen as a cap. BYD’s ratio was at 69.3% in 2014 and has not declined

in 1H15. Without replenishing the equity base or increasing asset size, this may pose risks to

their onshore borrowing ability and its liquidity situation.

Yutong’s cash conversion cycle is

better than BYD’s, which is

important to keep in mind

Yutong has seen an improving cash

cycle over the last 3 years, while BYD

has a deteriorating one

BYD’s net gearing is over 100%, and

it is relying on A-share placement to

carry out its capacity expansion plan

BYD may find it difficult to borrow

from banks

Industrials

Initiating Coverage

2 December 2015

page 16 of 79 , Equity Analyst, +852 3743 8075, [email protected] Aik Yeo

Please see important disclosure information on pages 74 - 79 of this report.

Table 11: Leverage Comparison – BYD is highly geared while Yutong is net cash

2010A 2011A 2012A 2013A 2014A

BYD

Net Debt/Equity 65.4% 69.5% 71.4% 93.6% 103.3%

Total Liability/Total Asset 60.7% 64.1% 65.5% 68.1% 69.3%

Yutong

Net Debt/Equity -36.2% -34.4% -35.5% -42.3% -55.6%

Total Liability/Total Asset 63.4% 57.5% 48.7% 48.9% 54.4%

Source: Jefferies, company data

At the other end of the spectrum, Yutong has managed a very conservative balance sheet.

The company has maintained net cash positions for years and its liability/asset ratio has

stayed within a range of 40-60%. This is the reason why Yutong is able to carry out a

generous dividend policy with pay-out ratio at 57% in FY14. We expect the pay-out ratio to

continue, accruing nearly 4% dividend yield in FY15E. \

Free Cash Flow When free cash flow is positive, it indicates the company is generating more cash than it

uses to run the business and the excess can be reinvested to grow the business. We can use

the free cash flow yield to assess the value of a company. Since this measure uses free cash

flow, the free cash flow yield provides a better measure of the company's performance.

For the period 2011 – 1H15, BYD’s free cash flow was negative, and delivered cumulative

free cash flow yield of -9%. Comparatively, Yutong achieved cumulative positive free cash

flow yield of 9%. With the exception of 2012, all other time periods saw delivered positive

free cash flow.

We believe BYD will still find it difficult to turn FCF-positive until 2017, due to the expected

huge capital outlay in terms of building out capacity. By end 2015, battery capacity will

only reach 8GWH but 14GWH by end FY16. After that the capacity flattens out, and is

expected to gradually head into positive region. Comparatively, Yutong does not have

capacity expansion plans.

Table 12: Free Cash Flow Analysis (mn Rmb)

BYD Yutong

Operating Cash Flow

2010 3,139 1,318

2011 5,985 1,446

2012 5,555 1,372

2013 2,436 2,802

2014 38 3,205

1H15 3,022 1,861

Investing Cash Flow

2010 (12,683) (603)

2011 (8,923) (999)

2012 (4,610) (2,316)

2013 (5,851) (153)

2014 (7,901) (1,714)

1H15 (4,711) (1,999)

Financing Cash Flow

2010 9,183 (645)

2011 4,736 (10)

2012 (1,217) 2,859

2013 4,508 (1,185.57)

2014 7,271 (1,177)

1H15 921 (1,520)

Free Cash Flow

2010 (5,595) 391

Yutong is cash rich, and has a

generous dividend pay-out policy,

which will translate to 4% dividend

yield FY15E

BYD had been consistently running

on negative FCF, while Yutong had

consistently positive FCF except in

2012

BYD will have difficulty turning

positive on FCF due to plans for

huge capital outlay ahead

Industrials

Initiating Coverage

2 December 2015

page 17 of 79 , Equity Analyst, +852 3743 8075, [email protected] Aik Yeo

Please see important disclosure information on pages 74 - 79 of this report.

Table 12: Free Cash Flow Analysis (mn Rmb)

2011 (2,688) 454

2012 (1,451) (524)

2013 (176) 1,636

2014 (4,014) 1,286

1H15 (2,108) 1,220

Cumulative FCF (16,032) 4,464

Market Cap 134,269 46,891

FCF Yield -12% 10%

Source: Jefferies, company data

Government Grants For this part, we are referring to government grants that are awarded to companies for new

energy vehicle R&D and capacity buildout, rather than the subsidies consumers eventually

receive for car purchase. This government grant is commonly found as ‘Other Income’ on a

company’s P&L, and it’s never easy to forecast due to the opaque nature of collection time

and award assessment.

Referring to the charts below, historically Yutong has received significantly less government

grants than BYD, both in absolute terms and as a percentage of operating profit (EBIT). In

FY14 and 1H15, Yutong collected government grants of Rmb157mn and Rmb55mn,

respectively, 20%/17% of what BYD received. In FY14 and 1H15, the Yutong government

grant as a percentage of EBIT was 5%/6% respectively, vs. 86% and 30% at BYD.

This, we believe is a function of BYD making abnormally thin operating margins.

Meanwhile, BYD has done substantially more R&D into NEV passenger vehicles, which

gives it very high government grants. Furthermore, BYD’s vertical integration, which

resulted in huge R&D into battery technology, BMS, and power train, has helped it gain in

this department.

Chart 13: Government grant accounted as income – BYD

has significantly greater grants from government (mn

Rmb)

Source: Jefferies, company data

Chart 14: Government grant as a % of EBIT – BYD has a

significantly larger portion of EBIT from grants (mn Rmb)

Source: Jefferies, company data

Capacity Utilization In terms of capacity utilization, Yutong is superior to BYD, having maintained utilization at

very high levels for the past few years. Despite the rapid growth anticipated in NEV bus,

Yutong does not have any capacity expansion plan in the near term, as it seeks to maintain

its existing 65,000-unit standard capacity. Both conventional and NEV buses can share

production platforms. The last time Yutong increased capacity was in 2012/13 when it

added 30k units capacity (investment was Rmb3.5bn).

0

100

200

300

400

500

600

700

800

2010 2011 2012 2013 2014 1H15

Yutong BYD

2% 5% 7% 11% 5% 6%

13% 19%

135%

59%

86%

29%

0%

20%

40%

60%

80%

100%

120%

140%

2010 2011 2012 2013 2014 1H15

Yutong BYD

Yutong received less government

grants vs. BYD, as it does not

participate in battery manufacturing

Here we refer to government grants

awarded for R&D into NEV and

capacity buildout. It’s different from

government subsidy

Yutong’s capacity utilization is

superior to BYD in both battery

manufacturing and auto assembly

Industrials

Initiating Coverage

2 December 2015

page 18 of 79 , Equity Analyst, +852 3743 8075, [email protected] Aik Yeo

Please see important disclosure information on pages 74 - 79 of this report.

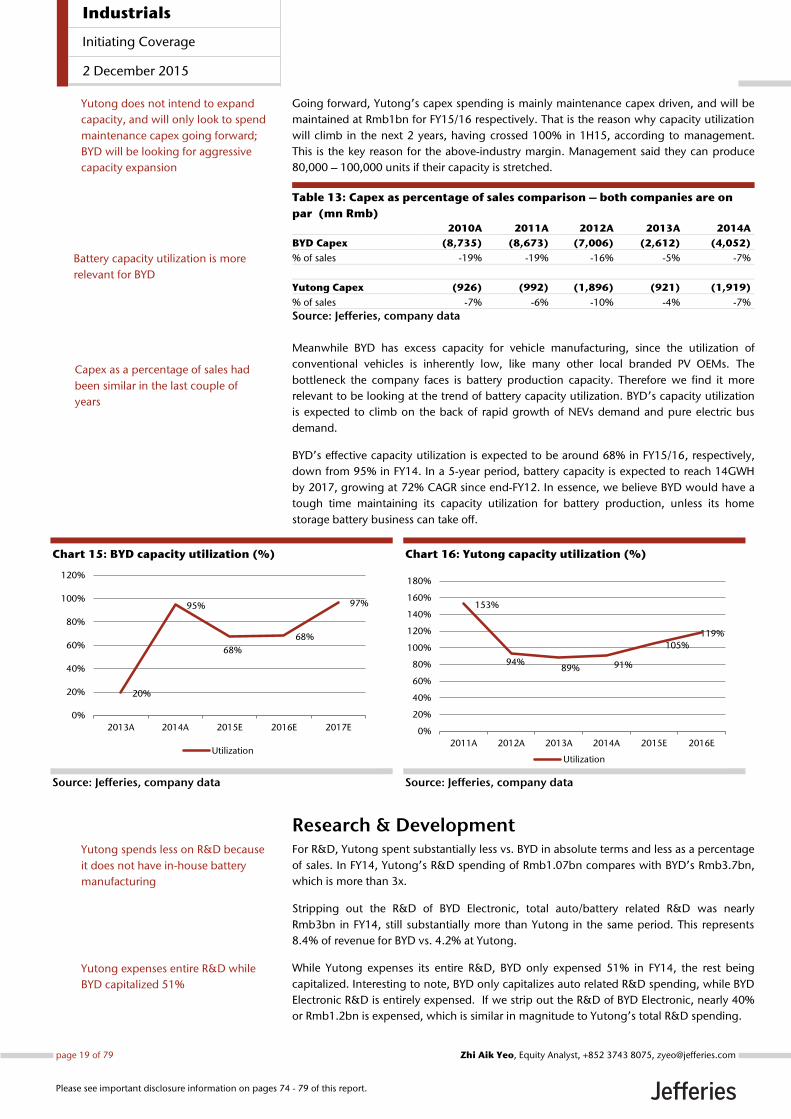

Going forward, Yutong’s capex spending is mainly maintenance capex driven, and will be

maintained at Rmb1bn for FY15/16 respectively. That is the reason why capacity utilization

will climb in the next 2 years, having crossed 100% in 1H15, according to management.

This is the key reason for the above-industry margin. Management said they can produce

80,000 – 100,000 units if their capacity is stretched.

Table 13: Capex as percentage of sales comparison – both companies are on

par (mn Rmb)

2010A 2011A 2012A 2013A 2014A

BYD Capex (8,735) (8,673) (7,006) (2,612) (4,052)

% of sales -19% -19% -16% -5% -7%

Yutong Capex (926) (992) (1,896) (921) (1,919)

% of sales -7% -6% -10% -4% -7%

Source: Jefferies, company data

Meanwhile BYD has excess capacity for vehicle manufacturing, since the utilization of

conventional vehicles is inherently low, like many other local branded PV OEMs. The

bottleneck the company faces is battery production capacity. Therefore we find it more

relevant to be looking at the trend of battery capacity utilization. BYD’s capacity utilization

is expected to climb on the back of rapid growth of NEVs demand and pure electric bus

demand.

BYD’s effective capacity utilization is expected to be around 68% in FY15/16, respectively,

down from 95% in FY14. In a 5-year period, battery capacity is expected to reach 14GWH

by 2017, growing at 72% CAGR since end-FY12. In essence, we believe BYD would have a

tough time maintaining its capacity utilization for battery production, unless its home

storage battery business can take off.

Chart 15: BYD capacity utilization (%)

Source: Jefferies, company data

Chart 16: Yutong capacity utilization (%)

Source: Jefferies, company data

Research & Development For R&D, Yutong spent substantially less vs. BYD in absolute terms and less as a percentage

of sales. In FY14, Yutong’s R&D spending of Rmb1.07bn compares with BYD’s Rmb3.7bn,

which is more than 3x.

Stripping out the R&D of BYD Electronic, total auto/battery related R&D was nearly

Rmb3bn in FY14, still substantially more than Yutong in the same period. This represents

8.4% of revenue for BYD vs. 4.2% at Yutong.

While Yutong expenses its entire R&D, BYD only expensed 51% in FY14, the rest being

capitalized. Interesting to note, BYD only capitalizes auto related R&D spending, while BYD

Electronic R&D is entirely expensed. If we strip out the R&D of BYD Electronic, nearly 40%

or Rmb1.2bn is expensed, which is similar in magnitude to Yutong’s total R&D spending.

20%

95%

68%

68%

97%

0%

20%

40%

60%

80%

100%

120%

2013A 2014A 2015E 2016E 2017E

Utilization

153%

94% 89% 91%

105%

119%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

2011A 2012A 2013A 2014A 2015E 2016E

Utilization

Yutong spends less on R&D because

it does not have in-house battery

manufacturing

Yutong expenses entire R&D while

BYD capitalized 51%

Capex as a percentage of sales had

been similar in the last couple of

years

Yutong does not intend to expand

capacity, and will only look to spend

maintenance capex going forward;

BYD will be looking for aggressive

capacity expansion

Battery capacity utilization is more

relevant for BYD

Industrials

Initiating Coverage

2 December 2015

page 19 of 79 , Equity Analyst, +852 3743 8075, [email protected] Aik Yeo

Please see important disclosure information on pages 74 - 79 of this report.

Shareholding Structure BYD was founded in 1995 by Chairman Wang Chuanfu and listed on the Shenzhen and HK

stock exchanges in 2010/2002, respectively. At present, Mr Wang holds 21% effective stake

in the company, followed by the other co-founder, Mr. Lv Xiangyang with 10% and the

Warren Buffet backed Berkshire Hathaway with 9%. Berkshire’s stake ownership is mainly

through H-shares, while Chairman Wang’s holdings are in A-shares.

Table 14: BYD Major Shareholders

A shares H shares

% of

share capital

Wang Chuanfu 512,623,820 20.70%

Lv Xiangyang 239,228,620 9.66%

Berkshire Hathaway Inc. 225,000,000 9.09%

Youngy Investment 162,681,860 6.57%

Xia Zuoquan 118,977,060 4.81%

*Updated till Sept 15

Source: Jefferies, company data

In 1997, Yutong’s A-shares were issued on the Shanghai Stock Exchange. Currently, Yutong

is majority owned by shareholder Zhengzhou Yutong Group with 37% stake, which is in

turn controlled by the Chairman Mr. Tang Yu Xiang. Other major shareholders include GIC

(1.5%), Lions Bus (4%), Pingan Insurance (2%) and China Road Machinery (2%). And since

the company is eligible for participation through the HK-Shanghai stock connect scheme,

other foreign institutions accounted for 9% through the Hong Kong Stock Clearing body.

Table 15: Yutong Major Shareholders

A shares

% of

share capital

Zhengzhou Yutong Group 823,314,023 37.19%

Hong Kong Clearing 188,255,267 8.50%

Lions Bus (100% owned by Yutong Group) 87,428,292 3.95%

China Securities Finance Corp 65,986,258 2.98%

China Pingan-Orient Securities 46,561,632 2.10%

China Highway Vehicle & Machinery Co Ltd 44,385,192 2.00%

GIC Private Limited 32,946,068 1.49%

*Updated till Sept 15

Source: Jefferies, company data

Chart 17: BYD public shareholding structure

Source: Jefferies, company data

Chart 18: Yutong public shareholding structure

Source: Jefferies, company data

A shares

Listed, 30%

A shares

Unlisted,

33%

H shares

Listed, 37%

A shares

Listed, 86%

A shares

Unlisted,

14%

Wang Chuanfu, Lv Xiangyang and

Berkshire Hathaway are BYD’s

biggest shareholders

For Yutong, it is Yutong Parent

group, Lions Bus, CSFC, Pingan-

Orient Securities

Industrials

Initiating Coverage

2 December 2015

page 20 of 79 , Equity Analyst, +852 3743 8075, [email protected] Aik Yeo

Please see important disclosure information on pages 74 - 79 of this report.

Sector Outlook

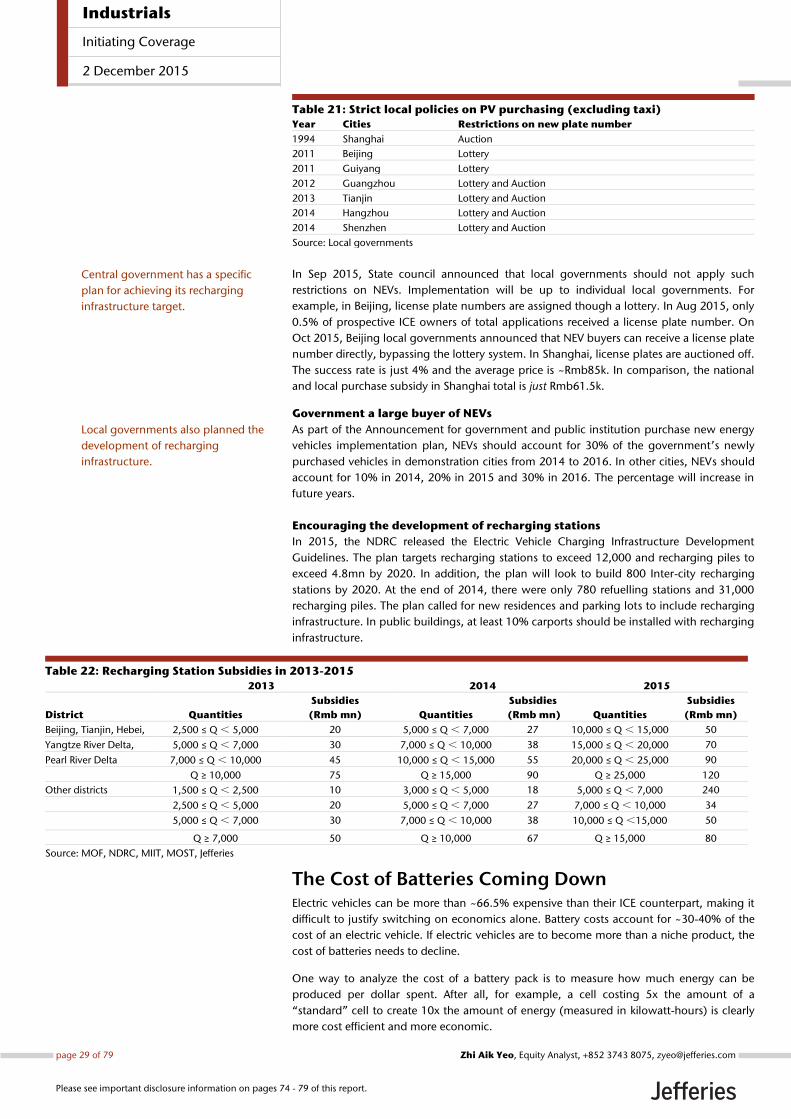

PV EV Adoption No Easy Task Despite China’s policies on EVs, we estimate only ~294,000 electric vehicles are on the road

as at end October. Barring a sudden surge in EV sales, China will likely miss its 2015 target

with regard to both EV installed base and recharging infrastructure. China may yet see its

NEV installed base reach 5m vehicles by 2020.

Chart 19: China likely to fall short of 2015 Targets…

Source: Jefferies

Chart 20: …but could still reach the 2020 target

Source: China Association of Auto Manufacturers, Jefferies

NEV sales have accelerated in 2014, with EV sales growing by 324% YoY to ~75k units. In

2015, we believe NEV sales can grow by 150%+ to more than ~200k units. NEV would still

account for just ~1% of total PV sales in 2015 but we believe NEV sales will continue to

grow.

Chart 21: Electric Vehicles Sales pick up in 2014 and 2015

Source: China Association of Auto Manufacturers, Jefferies estimates

Forecasting 4.8m Electric Passenger Vehicles by 2020

We are forecasting China’s electrical passenger vehicles installed base to reach 4.8m

vehicles, just short of the 5mn mark. By 2020, electrical passenger vehicles sales should

reach 1.3m, accounting for just 4% of annual PV sales.

0% 20% 40% 60% 80% 100%

Charging

Poles

Charging

Stations

Electric

Vehicles 500

2,000

400

294 (59%)

636 (39%)

27 (8%)0

1,000

2,000

3,000

4,000

5,000

6,000

2011 2012 2013 2014 2015E 2016E 2017E 2018E 2019E 2020E

000's

2020 Target

0

50

100

150

200

250

2011 2012 2013 2014 2015E

000's

Battery Electric Vehicles

Plug-in Hybrid Electric Vehicles

Industrials

Initiating Coverage

2 December 2015

page 21 of 79 , Equity Analyst, +852 3743 8075, [email protected] Aik Yeo

Please see important disclosure information on pages 74 - 79 of this report.

Chart 22: Electric Vehicles Sales to Just Miss 2020 Target

Source: China Association of Auto Manufacturers, Jefferies estimates

The Payback Period is Attractive with Subsidies

The fundamental EV economic equation is higher upfront costs in the form of a battery in

exchange for lower fuel costs. The more you drive, the more quickly an EV will pay off the

upfront additional cost. For that reason, EVs are a natural fit for fleet vehicles such as buses.

For individual consumers, those who drive frequently will benefit more quickly from the

savings per “tank” fill-up with an EV. For PHEVs and BEVs, the payback period is 3 and 8

years, respectively.

If we factor in the purchase subsidies and the exemption of plate numbers fees, a BEV

payback period falls to 5 months and a PHEV is actually cheaper than its ICE counterpart. In

the table below we summarize our payback period analysis.

Chart 23: Payback Period Analysis for PV BEVs

Source: Jefferies

Chart 24: Payback Period Analysis for PV PHEVs

Source: Jefferies

In the exhibits below we highlight the sensitivity of the payback period to the price

difference and average km driven per year, and price difference and price of gasoline.

Passenger Vehicles 2014 2015E 2016E 2017E 2018E 2019E 2020E

EV PV Installed base 000's 123 345 811 1,508 2,410 3,493 4,789

YoY % Change % 154.8% 180.4% 135.1% 85.9% 59.8% 44.9% 37.1%

EV as a % of PV Installed Base % 0.1% 0.2% 0.5% 0.8% 1.2% 1.5% 1.9%

EV PV Sales 000's 75 222 466 699 909 1,091 1,309

YoY % Change % 323.8% 196.9% 110.0% 50.0% 30.0% 20.0% 20.0%

EV Sales as a % of PV Sales % 0.4% 1.1% 2.1% 3.0% 3.7% 3.9% 3.9%

EV Scrappage 0 0 0 2 7 8 13

PV Installed base 000's 123,267 141,785 161,863 181,876 203,622 228,299 257,812

YoY % Change % 16.7% 15.0% 14.2% 12.4% 12.0% 12.1% 12.9%

PV Sales 000's 19,700 20,488 22,537 22,987 24,826 28,054 33,665

YoY % Change % 9.9% 4.0% 10.0% 2.0% 8.0% 13.0% 20.0%

Scrappage 000's 2,351 2,713 2,561 2,766 3,088 3,195 3,501