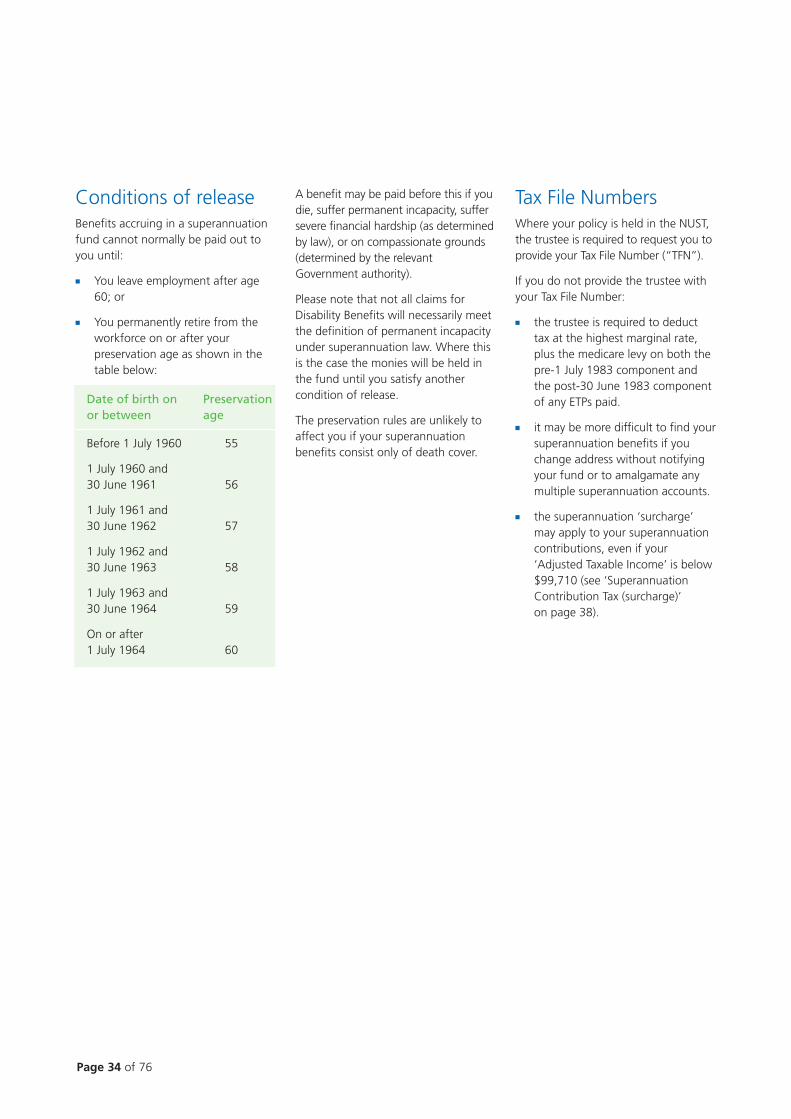

aviva protectionfirst range product disclosure...

TRANSCRIPT

Aviva Protectionfirst Range

Product Disclosure StatementDate of issue 27 September 2004

To acquire the Aviva Protectionfirst products you must complete the application form contained in this Product Disclosure Statement

Page

Protection to suit you 1

How the Aviva Protectionfirst product range works:

Aviva Protection – Life 3

Aviva Protection – Recovery Money 8

Aviva Protection – Flexible Recovery Money 13

Aviva Protection – Stand Alone Recovery Money 16

Aviva Protection – Income Gold & Income Excell (Agreed Value & Indemnity) 18

Aviva Protection – Income Business Expenses 28

Additional Features – all products 31

Holding your policy in your superannuation fund 33

Charges 35

Premiums 35

Policy fees 36

Government taxes and charges 37

Taxation 38

Complaints 40

Other important information 41

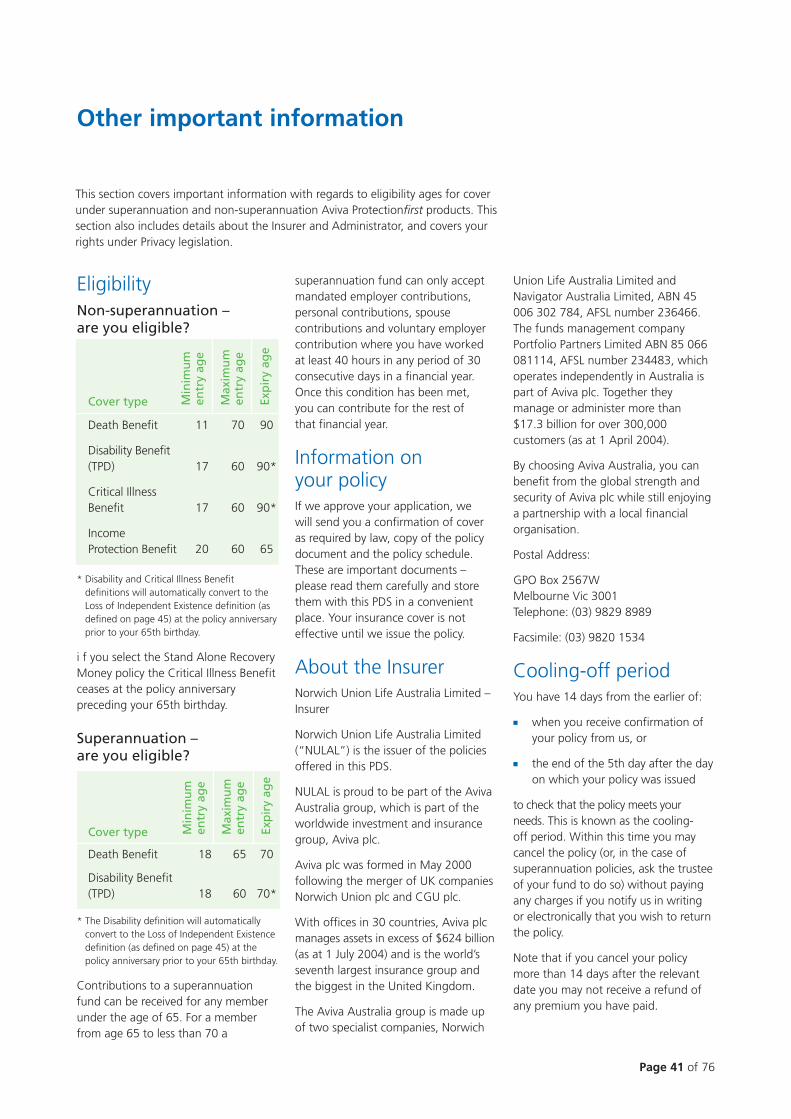

Eligibility 41

About the Insurer 41

Cooling-off Period 41

Privacy statement 42

Medical Definitions 44

How do I get started? 48

Direct Debit Service Agreement 49

Application Form 53

Application for Binding Nominations – NUST 75

This Product Disclosure Statement (“PDS”) covers two separate financial products: life insurance and superannuation.

The life insurance product is called the Aviva Protectionfirst Range and is issued by Norwich Union Life Australia Limited(“NULAL”, “the Administrator”, “our”, “we”, or “us”) ABN 34 006 783 295 Australian Financial Services Licence Number(“AFSL number”) 241686. The superannuation product is called the Norwich Union Superannuation Trust (“NUST”) and is issued by NULIS Nominees (Australia) Limited (“NULIS” or “the Trustee”) ABN 80 008 515 633 AFSL number 236465.Both products are administered by NULAL.

NULAL and NULIS are part of the Aviva Australia group which is ultimately owned by Aviva plc (“Aviva”), the world’sseventh largest insurance and investment company.

The information given in this document is of a general nature only and has been prepared without takinginto account your individual investment objectives, financial situation or particular investment needs. This PDS is not a statement of advice.

Contents

Page 1 of 76

Protection to suit you

With Aviva Protectionfirst, you have peace of mind in knowing you andyour family will be financially secure, should unforeseen situations arise.

If you are unable to work because of injury or illness, Aviva Protection –

Income can pay you a percentage of your regular income. Our Life and Recovery Money policies pay alump sum benefit.

The following table provides an overviewof the products and benefits we offer.

Dea

th B

enef

it

Bu

sin

ess

Pro

tect

ion

Op

tio

n

Ind

exat

ion

(C

PI L

inki

ng

)

Dis

abili

ty (

TPD

) B

enef

it O

pti

on

Eco

no

mis

er O

pti

on

Futu

re In

sura

bili

ty

Gu

aran

teed

Ren

ewab

le

Inte

rim

Acc

iden

t In

sura

nce

Leve

l Pre

miu

m

Dis

abili

ty B

uy

Bac

k O

pti

on

Step

ped

Pre

miu

ms

Sup

eran

nu

atio

n O

pti

on

Term

inal

Illn

ess

Ad

van

ce

Up

gra

de

Gu

aran

tee

Wai

ver

of

Prem

ium

Cri

tica

l Illn

ess

Ben

efit

Cri

tica

l Illn

ess

Bu

y B

ack

Op

tio

n

Cri

tica

l Illn

ess

Rei

nst

atem

ent

Op

tio

n

Futu

re In

sura

bili

ty C

riti

cal I

llnes

s

Aviva Protection – Life

B O B OC B B B B B O B B B B O N N N N

Aviva Protection – Recovery Money

B O B OC B B B B B O B N B B O OC O O B

Aviva Protection – Flexible Recovery Money

N N B OC B N B B B O B N N B O OC O O B

Aviva Protection – Stand AloneRecovery Money

N N B N B N B B B N B N N B N OC N O B

Policies providing a lump sum benefit

B = Benefit included in basic price O = Option at additional cost, benefit ceases at policy anniversary preceding age 65 OC = Option

at additional cost, definition changes to Loss of Independent Existence at policy anniversary preceding age 65 N = Not available

Strong historyAviva Protectionfirst is underwritten byNULAL, which is part of the Aviva plcgroup, one of the first insuranceorganisations in the world to protect personal wealth. NorwichUnion Society for the Insurance ofHouses, Stock and Merchandise fromFire was founded in 1797, at a time inthe United Kingdom when cities werebuilt largely of wood and the threat offire was uppermost in people’s minds.Over 200 years, the business hasgrown to be the world’s seventhlargest insurance group.

Financial strength By choosing Aviva Protectionfirst youbenefit from the financial strength and experience of Aviva plc. Aviva plc group has over $624 billionof assets under management and 30million customers worldwide as at 1July 2004 .

Page 2 of 76

Protection to suit you continued

Policies providing income replacement

Aviva Protection – Income Gold

O B B B B O B O B B O B B B B B B B B B N

Aviva Protection – Income Excell

O B N B N O B O B N N B B B N N N B N B N

Aviva Protection – Income Business Expenses

N B N B N N B N B N N B B N N N N B N B B

B = Benefit included in basic price O = Option at additional cost N = Not available

You can combine products to create your own personal package of cover.

Note: more detailed descriptions of the products’ benefits, risks, and charges are covered in the following sections.

Two reasons to protect your wealth with Aviva Protectionfirst

Acc

iden

t B

enef

it O

pti

on

Au

tom

atic

CPI

Lin

kin

g B

enef

it

Cri

tica

l Co

nd

itio

ns

Ben

efit

Dea

th B

enef

it

Emer

gen

cy T

rave

l Ben

efit

Gu

aran

teed

Insu

rab

ility

Op

tio

n

Gu

aran

teed

Yea

rly

Ren

ewab

le

Incr

easi

ng

Cla

im B

enef

it

Inte

rim

Acc

iden

t B

enef

it

Nu

rsin

g C

are

Ben

efit

Plat

inu

m B

enef

it

Leve

l & S

tep

ped

Pre

miu

ms

Rec

urr

ent

Cla

im B

enef

it

Sch

edu

led

Inju

ry B

enef

it

Spo

use

Acc

om

mo

dat

ion

Ben

efit

Reh

abili

tati

on

Ben

efit

Reh

abili

tati

on

Inco

me

Ben

efit

Tota

l & P

arti

al D

isab

ility

Ben

efit

Un

emp

loym

ent

Wai

ver

Wai

ver

of

Prem

ium

Ben

efit

Ext

ensi

on

Page 3 of 76

Aviva Protection – Life

Aviva Protection – Life provides death cover. You can choose to includeoptional disability cover, for an additional premium. If you die or (ifdisability cover is added) are disabled during the term of the policy, youor your beneficiaries will receive a pre-determined lump sum.

These policies are ‘guaranteedrenewable’. This means that providedyou pay the premiums you can renewyour cover each year until the policyexpiry date without having to providefurther medical evidence.

When you apply for the policy, youchoose the amount of the lump sumbenefit payable under the policy. Thislump sum benefit is called the ‘SumInsured’. If you choose to add disabilitycover to your policy, you can choose adifferent Sum Insured for your DeathBenefit and your Disability Benefit.

Your policy can be held in one of twoways. You can hold the policy yourself,or arrange for the trustee of acomplying superannuation fund to holdthe policy, with you as the life insured.

1. Ordinary policy

You hold the policy directly. You candetermine to whom the benefits arepaid, by completing the form on page65. Otherwise, benefits are paid to youor your estate.

2. Superannuation policy

Your policy may instead be held by thetrustee of a complying superannuationfund. Holding your policy through asuperannuation fund affects the taxtreatment of premiums and benefitpayments. You should discuss whetherthis structure is appropriate for youwith your financial adviser.

If you choose this structure, we canarrange for your policy to be heldthrough the Norwich UnionSuperannuation Trust (“NUST”), or you can instruct us to issue thepolicy to the trustee of anothercomplying superannuation fund ofyour choice.

For details in respect of holding yourpolicy through the NUST or anothercomplying superannuation fund, refer to page 33.

The benefitsPayment of benefitsIf you die, are diagnosed as beingterminally ill, or (if the disability cover isadded) are Totally and PermanentlyDisabled, the Sum Insured will be paidon the basis explained below. If thepolicy is held as an ordinary policy theSum Insured is paid to you, as directedby you in your application, or to yourestate. If the policy is held in acomplying superannuation fund, theSum Insured is paid to the trustee ofthe superannuation fund. The paymentof benefits is subject to the exclusionsexplained on page 7.

Dea

th B

enef

it

Bu

sin

ess

Pro

tect

ion

Op

tio

n

Ind

exat

ion

(C

PI L

inki

ng

)

Dis

abili

ty (

TPD

) B

enef

it O

pti

on

Eco

no

mis

er O

pti

on

Futu

re In

sura

bili

ty

Gu

aran

teed

Ren

ewab

le

Inte

rim

Acc

iden

t In

sura

nce

Leve

l Pre

miu

m

Dis

abili

ty B

uy

Bac

k O

pti

on

Step

ped

Pre

miu

ms

Sup

eran

nu

atio

n O

pti

on

Term

inal

Illn

ess

Ad

van

ce

Up

gra

de

Gu

aran

tee

Wai

ver

of

Prem

ium

Aviva Protection – Life

B O B OC B B B B B O B B B B O

Aviva Protection – Life: a snapshot of what this cover includes

B = Benefit included in basic price O = Option at additional cost, benefit ceases at policy anniversary preceding age 65 OC = Option

at additional cost, definition changes to Loss of Independent Existence at policy anniversary preceding age 65

Page 4 of 76

Death Benefit (standard)If you die the agreed Sum Insured willbe paid.

Terminal Illness Benefit(standard)Under this benefit where you arediagnosed as being terminally ill andlikely to die within twelve (12) months,the Sum Insured will be paid out earlywith the agreement of the policyowner as a Terminal Illness Benefit. A medical practitioner nominated by us will need to provide specifiedinformation about the nature of yourillness or injury.

The maximum amount payable underthe Terminal Illness Benefit, includingall other amounts payable by us, is$2,000,000 (or such other amount asadvised by us from time to time). If thedeath Sum Insured under the policy isgreater than $2,000,000, then theunpaid balance of the death SumInsured is payable on your death(provided the corresponding premiumshave been paid). If a Disability Benefitis attached, the amount of SumInsured provided by this benefit will bereduced by the amount paid.

If the cover is held through asuperannuation fund, the availability ofthe Terminal Illness Benefit is subject tothe superannuation legislationregarding the release of benefits ongrounds of permanent incapacity. Thisusually means a person has stoppedworking, and is unlikely to ever workagain. The taxation position may beless favourable than deferring paymentuntil it is payable as a death benefit(see page 39 for further information).

Disability Benefit (optional at additional cost)By taking this option, your policy isextended to include disability cover. If you become Totally and PermanentlyDisabled (as defined below), thedisability Sum Insured will be paid toyou as a lump sum.

Once a Disability Benefit is paid, thedeath cover ceases unless your deathSum Insured exceeds your DisabilityBenefit. Where it does, the excessdeath cover continues upon paymentof the corresponding premium.

Definition up to policyanniversary preceding age 65.

The definition of total and permanentDisability changes at the policypreceding age 65.

When you apply for your policy, youcan choose whether you want the ‘anyoccupation’ or ‘own occupation’ testof Total and Permanent Disability toapply. That choice affects the level ofyour premium, and you should discussit with your financial adviser.

The own occupation test is onlyavailable to certain occupations.

If you choose the ‘any occupation’ test, Total and Permanent Disabilitymeans either:

(a) you have suffered total andirrecoverable loss of the:- sight of both eyes, or- use of two limbs, or- sight of one eye and the use of

one whole hand, or one wholefoot, or

(b) you have been unable to performyour own occupation for a periodof at least three months due tobodily injury or illness and are sodisabled that you are unlikely toever be able to perform your ownoccupation or other occupation forwhich you are suited by education,training or experience.

If you choose the ‘own occupation’test, Total and Permanent Disabilitymeans either:

(a) you have suffered total andirrecoverable loss of the:- sight of both eyes, or- use of two limbs, or

- sight of one eye and the use of onewhole hand, or one whole foot, or

(b) you have been absent fromemployment through injury or illnessfor an uninterrupted period of threemonths and, have becomeincapacitated to such an extent as torender you unlikely ever to be ableto engage in your own occupation.

Your ‘own occupation’ for thispurpose is your occupation at thetime of proposing for this policy,unless you have been in yourcurrent occupation for a consecutiveperiod of at least 18 months at thetime of making a claim.

The above definition of Total andPermanent Disability applies until thepolicy anniversary preceding age 65.

Home duties

If your occupation immediately prior to the commencement of Total andPermanent Disablement can bedescribed as “Home Duties”, then“Total and Permanent Disablement”means that you have, for anuninterrupted period of three months,been under medical supervision withcomplete inability to perform themajority of normal domestic duties,and are unlikely ever to recover.

Occupations of specialised nature

For the purposes of the ownoccupation definition if youroccupation is classified as a SpecialistSurgeon, then part (b) of the definitionabove will be replaced by “you havebeen absent from employmentthrough injury or illness for anuninterrupted period of six monthsand, have become incapacitated tosuch an extent as to render youunlikely ever to be able to engage inyour own occupation”.

Aviva Protection – Life continued

Page 5 of 76

Definition after policy anniversarypreceding age 65

At the policy anniversary preceding your65th birthday the above definition ofTotal and Permanent Disability shallcease to apply. Instead Total andPermanent Disability shall mean Loss ofIndependent Existence as defined onpage 45. This definition shall applyirrespective of your occupation andwhether you have selected the ‘anyoccupation’ or ‘own occupation’ test.

Reduction of benefits forpayments under FlexibleRecovery Money policies

Where this policy is written inconjunction with an Aviva Protection –Flexible Recovery Money:

� The amount of the Death Benefitpayable on death or terminal illnessunder this policy will automaticallybe reduced by the amount ofbenefits actually paid under theFlexible Recovery Money policy.

� The amount of the Disability Benefitunder this policy will be reduced bythe amount by which the CriticalIllness Benefit paid under the FlexibleRecovery Money policy exceeds theDisability Sum Insured under theFlexible Recovery Money policy.

For example if you select the followingpolicies

� Life with $1,000,000 death SumInsured and $850,000 disabilitySum Insured

� Flexible Recovery Money with$250,000 critical illness SumInsured and $150,000 disabilitySum Insured

then after a claim under the FlexibleRecovery Money policy for $250,000the cover under the Life policy will be reduced to $750,000 death Sum Insured and $750,000 disability Sum Insured.

Any remaining benefit under the AvivaProtection – Life, if applicable, willcontinue upon payment of theappropriate premium.

The featuresAviva Protection – Life has variousstandard and optional features,described below. These features helpyou manage the cost of your premiumsand the level of cover over time.

Economiser (standard)The cost of your insurance cover willnormally change each year. WithEconomiser, however you can freezethe premium at any time after your30th birthday, enabling you to controlthe cost of your insurance.

1. At any time after your 30thbirthday you can request theoption to be applied.

2. Applying the Economiser means:

(a) Indexation (as defined on page 31) ceases; and

(b) except at policy anniversarieswhen benefits automaticallyreduce or cease for otherreasons, or premium loadingscease, the Sum Insured will beautomatically reduced ininverse proportion to theincrease in premium rates thatwould have occurred had thisreduction not been made.

This has the effect of ‘freezing’the premium, including inrelation to changes in thepremium scale, or crossingbelow size adjustment bands,as defined on page 35.

3. You may cancel the Economiser at any time by notice in writing.Indexation, if applicable, is thenreinstated.

Future Insurability (standard)When significant events happen in life,you can increase your death and/or

disability Sum Insured without havingto provide further medical evidence.

The death and/or disability SumInsured may be increased when:

� You marry.

� You have a child or legally adopt one.

� You take out a mortgage to buyyour first home.

� You receive an increase in annualsalary of at least 10%.

You must apply for this increase within30 days of the first renewal datefollowing the defined event. We willrequire proof of the defined event.

You may only increase your deathand/or disability Sum Insured onceunder this feature in any twelve (12)month period. You may increase yourSum Insured by 25% or $75,000 or 5times the salary increase (if applicable),whichever is lowest. The maximumtotal amount you can increase yourdeath and/or disability Sum Insuredunder this feature over the life of thepolicy is the lesser of:

� The amount of death and/ordisability Sum Insured under yourpolicy excluding CPI increases andincreases effected under thisfeature; and

� $1,000,000.

The feature cannot be exercised if atthe time of your request:

� You are older than 50 years of age

� You have previously been acceptedby us with special conditionsaffecting the premium rates

� The premiums are being waivedunder the Waiver of PremiumOption, or

� You are currently entitled to makea claim for a Terminal Illness orCritical Illness Benefit under apolicy you currently hold with us.

Page 6 of 76

Aviva Protection – Life continued

Any increase in the disability SumInsured as a result of exercising thisoption cannot result in the disabilitySum Insured exceeding the death SumInsured.

The option to increase the disabilitycover only applies where the initialdisability Sum Insured is $1,500,000 orless.

Disability Buy Back Option(optional at additional cost)

This option can be exercised twelve(12) months after the Disability Benefithas been paid. It enables purchase ofdeath cover from us, renewable to age90, at a time when you have almostcertainly become uninsurable. Thisoption provides disability sufferers witha second level of protection and peaceof mind.

For a period of thirty (30) days fromthe first anniversary of the payment ofthe Disability Benefit, we will accept aproposal provided:

(a) the Sum Insured does not exceedthe Disability Benefit paid; and

(b) premiums will be charged at theappropriate rate for the thenattained age based on the thencurrent published term insurancerates; and

(c) any original exclusions or specialconditions will be maintained.

The option does not apply afterpayment of a Terminal Illness Benefit.

This option ceases at the policyanniversary preceding age 65.

Waiver of Premium Option(optional at additional cost)This option provides for futurepremiums to be waived while you areTotally Disabled for an extended period.

If you are Totally Disabled for at leastthree continuous months then, whileTotal Disability continues, subsequent

premiums falling due are waived up to the policy anniversary prior to your65th birthday. Premiums for increases orpolicies effected as a result of BusinessProtection Option or the Buy-BackOption are not subject to this option.

For the purposes of the Waiver of Premium Option, you will beconsidered Totally Disabled if we aresatisfied that:

(a) you have suffered total andirrecoverable loss of the:

� sight of both eyes, or

� use of two limbs, or

� sight of one eye and use of onewhole hand, or one whole foot,or

(b) you have been unable to performyour own occupation (or otheroccupation for which you aresuited by education training orexperience) for a period of at leastthree (3) months due to bodilyinjury or illness.

Where you are wholly engaged in fulltime unpaid domestic duties at the dateof the event causing Total Disability,then the occupation for which you aresuited by education, training orexperience is be taken to include unpaiddomestic duties. In this case you mustbe disabled to such an extent that youare confined to your place of principalresidence unless assisted.

Business Protection Option(optional at additional cost)The Business Protection Optionprovides you with a right to apply foran annual increase in your death and(if applicable) disability Sum Insuredwithout having to supply furthermedical evidence. The BusinessProtection Option may be used for thefollowing purposes:

� Business succession planning

� Loan guarantor insurance

� Key person insurance

You will need to tell us in writing thepurpose for which you want theBusiness Protection Option and provideus with a valuation from a qualifiedaccountant or valuer of your businessor key person, or evidence of thecontractual guarantees, as the casemay be, together with any otherfinancial evidence that will satisfy usthat the value of your financial interestis at least equal to the increasedamount of cover. Any increase in theSum Insured is subject to our approval.

The death Sum Insured may beincreased subject to the followingmaximums:

� For business succession planningpurposes – three times the SumInsured when this option was firstpurchased or $10 million –whichever is less.

� For loan guarantor or key personpurposes – three times the SumInsured when this option was firstpurchased or $5 million –whichever is less.

You may increase the disability SumInsured to three times the Sum Insuredwhen this option was first purchasedor $2 million – whichever is less.However, the Sum Insured may not beincreased to an amount in excess ofyour death cover under the policy.

You can exercise the right to apply forthe increase within 30 days either sideof your policy’s renewal date up to thepolicy anniversary preceding your 65th birthday.

If the right to apply for an increase isnot exercised on three consecutivepolicy renewals from the later of:

� the date the option was purchased,or

� the date of any previous election toexercise the right for an increase,

Page 7 of 76

then the option will be automaticallycancelled, unless you can demonstratethat the financial evidence relating toyour business and the purposeidentified by you, in respect of thatperiod, did not support an increase inthe Sum Insured.

The maximum age at which the option can be purchased is age 60next birthday.

This feature is not available forsuperannuation policies.

Additional Features The following additional features areexplained on page 31:

Indexation of benefitUpgrade guarantee24 hour world wide coverInterim Accident Cover

Level of coverMinimumsThere is no minimum Sum Insuredrequirement. However minimumpremium and premium loadings doapply, refer to pages 35 and 36.

MaximumsDeath Sum Insured: There are no maximum limits in respect of death cover.

Disability Sum Insured: A maximumdisability Sum Insured of $2,500,000applies.

While there is no maximum death Sum Insured for policies effected undersuperannuation arrangements, youshould note that lump sum benefitsare subject to higher taxation ifReasonable Benefit Limits (RBL) areexceeded (see page 39).

ExclusionsThere are certain exclusions that apply to your policy. Exclusions arecircumstances in which we are notrequired to pay the benefits under the policy.

The Death Benefit is not payable ifyour death was caused by suicidewithin thirteen (13) months ofcommencement or reinstatement ofthe policy. If your death was caused bysuicide within 13 months of anincrease then the increase in the SumInsured is not payable.

Neither the Disability Benefit nor theWaiver of Premium Option will bepayable in the event of attemptedsuicide, self-inflicted illness or injury orparticipation in insurrection.

Where we agree to replace an existingpolicy from another insurer, thethirteen (13) month exclusion forsuicide will not apply where the SumInsured under the policy being replacedis greater than or equal to the SumInsured under this policy, and thepolicy being replaced has been in forcefor at least twelve (12) months.

Page 8 of 76

Aviva Protection – Recovery Money

Aviva Protection – Recovery Money provides death cover, with part or allof the benefit payable early if you are diagnosed with one of the criticalillnesses covered by the policy. You may choose to include optionaldisability cover for an additional premium.

Aviva Protection – Recovery Money is a bundled death and critical illnesscontract with the option to purchasedisability cover.

One policy is issued covering all threeevents. Consequently there is onepolicy owner for all three components.

Being a bundled contract the pricingreflects the overlap of risks betweenthe three covers and the fact that aclaim for a critical illness or disabilitywill reduce the death cover SumInsured. The administration andestablishment costs are also shared.

This policy is ‘guaranteed renewable’.This means that provided you pay thepremiums you can renew your covereach year until the policy expiry datewithout having to provide furthermedical evidence.

When you apply for the policy, youchoose the amount of the lump sumbenefit payable under the policy. Thislump sum benefit is called the ‘SumInsured’. You can choose differentlevels of Sum Insured for the death,critical illness and disability parts of the policy.

The Critical Illness Benefit will only bepaid on correct diagnosis of any one of the listed critical illnesses. Paymentof Critical Illness Benefit is based upon the precise definitions shown in the‘Medical Definitions’ sectioncommencing on page 44.

Aviva Protection – Recovery Money: a snapshot of what this cover includes

Dea

th B

enef

it

Bu

sin

ess

Pro

tect

ion

Op

tio

n

Ind

exat

ion

(C

PI L

inki

ng

)

Dis

abili

ty (

TPD

) B

enef

it O

pti

on

Eco

no

mis

er O

pti

on

Futu

re In

sura

bili

ty

Gu

aran

teed

Ren

ewab

le

Inte

rim

Acc

iden

t In

sura

nce

Leve

l Pre

miu

m

Dis

abili

ty B

uy

Bac

k O

pti

on

Step

ped

Pre

miu

ms

Sup

eran

nu

atio

n O

pti

on

Term

inal

Illn

ess

Ad

van

ce

Up

gra

de

Gu

aran

tee

Wai

ver

of

Prem

ium

Cri

tica

l Illn

ess

Ben

efit

Cri

tica

l Illn

ess

Bu

y B

ack

Op

tio

n

Cri

tica

l Illn

ess

Rei

nst

atem

ent

Op

tio

n

Futu

re In

sura

bili

ty C

riti

cal I

llnes

s

Aviva Protection – Recovery Money

B O B OC B B B B B O B N B B O OC O O B

B = Benefit included in basic price O = Option at additional cost, benefit ceases at policy anniversary preceding age 65 OC = Option

at additional cost, definition changes to Loss of Independent Existence at policy anniversary preceding age 65 N = Not available

DEATH DISABILITY CRITICALILLNESS

Overlapping Risk

One Policy Owner

Bundledpricing

advantages=

Page 9 of 76

The benefitsPayment of BenefitsIf you die, are diagnosed as beingterminally or critically ill, or (if disabilitycover is added) are Totally andPermanently Disabled, the Sum Insuredwill be paid to you, as directed by youin your application, or to your estate.The payment of benefits is subject tothe exclusions explained on page 12.

Payment of one type of benefitautomatically reduces the Sum Insured under the other types by a corresponding amount.

Death Benefit (standard)If you die the agreed Sum Insured willbe paid.

Terminal Illness Benefit(standard)Under this benefit where you arediagnosed as being terminally ill andlikely to die within 12 months, the SumInsured will be paid out early with youragreement. The Critical Illness Benefit,and if attached Disability Benefit, theamount of Sum Insured provided bythese benefits will be reduced by theamount paid. The basis on which theTerminal Illness Benefit is paid underthis policy is the same as under the Lifepolicies, and is explained on page 4.

Critical Illness Benefit(standard)Critical Illness definition before policy anniversarypreceding age 65

If you are correctly diagnosed with one of the following critical illnesses(as defined) at any time up to thepolicy anniversary preceding age 65,we will pay the critical illness SumInsured as a lump sum.

The critical illnesses covered are:

Aplastic AnaemiaBenign Intracranial TumourBlindnessCancerCardiomyopathyChronic Lung DiseaseComaCoronary Artery By-Pass SurgeryCoronary Artery DiseaseDeafnessDementiaEncephalitisHeart AttackHeart SurgeryLiver DiseaseLoss of Independent ExistenceLoss of SpeechMajor BurnsMajor Head TraumaMajor Organ TransplantMedically Acquired HIV InfectionMotor Neurone DiseaseMultiple SclerosisOccupationally Acquired HIV InfectionOpen Heart SurgeryOut of Hospital Cardiac ArrestParalysisParkinson’s DiseasePneumonectomyPrimary Pulmonary HypertensionRenal FailureStroke

The definitions of the critical illnessesare contained in the ‘MedicalDefinitions’ section of this document,commencing on page 44.

For Coronary Artery Disease andMultiple Sclerosis the amount payablemay be limited in the manner set outunder Medical Definitions commencingon page 44.

For Occupationally Acquired HIVInfection and Medically Acquired HIVInfection the Critical Illness Benefit maybe excluded where a Cure becomesavailable as set out under ‘MedicalDefinitions’ commencing on page 44.

Critical Illness definition afterpolicy anniversary precedingage 65

Conversion to Loss of IndependentExistence at age 65.

If you have been covered under theCritical Illness Benefit and there hasnot been a claim on the policy, thenthe Critical Illness Benefit will continuefrom the policy anniversary precedingage 65 until the expiry of the policy.However from the policy anniversarypreceding age 65, the abovedefinitions of critical illness shall ceaseto apply. Instead, the critical illnessSum Insured will be payable if you arecorrectly diagnosed as being subject toa Loss of Independent Existence (asdefined on page 45).

Disability Benefit (optional at additional cost)By taking this option, your policy isextended to include disability cover. If you become Totally and PermanentlyDisabled (as defined on page 4), thedisability Sum Insured will be paid toyou as a lump sum.

Once the Disability Benefit is paid, thedeath cover and critical illness coverboth cease, unless the Sum Insured ineither case exceeds the DisabilityBenefit. Where it does, the excessdeath and critical illness covercontinues upon payment ofcorresponding premiums.

Page 10 of 76

Aviva Protection – Recovery Money continued

Critical facts showing the risk of death andcritical illness for men and women aged 18-64.

27% Breast Cancer $8,509,700

13% Heart Attack $3,984,380

11% Stroke $3,643,925

2% Coronary

Artery Disease $552,365

10% Coronary Artery

Bypass Surgery $3,014,020

4% Other Illnesses $1,335,780

33% Other Cancer $10,655,396

2% stroke

11% cancer

3% heartattack

6% other

1% by-pass

2% death

75% healthy

Trauma & death: risks for females 18-64

3% stroke

10% cancer

9% heartattack

9% other

3% by-pass

5% death

61% healthy

Trauma & death: risks for males 18-64

The facts of life are that many of uswill suffer a major medical condition.

The following graph indicates thelikelihood of an 18-year-old femalesuffering one of the listed majormedical conditions which qualify for a critical illness benefit before shereaches 64.

The probability of death is slim at 2%.However cancer is a major concernwith a one-in-ten chance.

The following graph indicates thelikelihood of an 18-year-old malesuffering one of the listed majormedical conditions which qualify for a critical illness benefit before hereaches 64.

The probability of death is a concern at 5%. However risk of heart attack is higher at 9%. This represents analmost one-in-ten risk.

Source: Fabrizio, E. and Gratton, W. K. – Pricing Dread Disease Insurance: Transactions of the Institute of Actuaries of Australia1994, pages 292-468.

The Institute of Actuaries has consented to the statements attributable to them on this pagebeing included in this PDS in the form and context in which they are included.

Aviva’s claims experience

The above graph provides details of the critical illness claims paid, by NULAL between1 January 2001 and 31 December 2003 (based upon the medical definitions within the relevant NULAL policies).

Page 11 of 76

The featuresEach of the following features isprovided on the terms set out on pages 4 to 6:

Economiser (standard)

Future Insurability (standard)

Waiver of Premium Option (optionalat additional cost)

Business Protection Option (optionalat additional cost)

Disability Buy Back Option (optionalat additional cost)

Note that the Disability Buy BackOption is not available after a CriticalIllness Benefit or Terminal Illness Benefithas been paid under this policy.

Future insurability CriticalIllness (standard)When significant events happen in life,you can increase your critical illnessSum Insured without having to providefurther medical evidence.

The critical illness Sum Insured may beincreased when:

� You marry.

� You have a child or legally adoptone.

� You take out a mortgage to buyyour first home.

� You receive an increase in annualsalary of at least 10%

You must apply for this increase within30 days of the first renewal datefollowing the defined event. We willrequire proof of the defined event.

You may only increase your criticalillness Sum Insured once under thisfeature in any twelve (12) monthperiod. In any twelve (12) monthperiod you may increase your SumInsured by $25,000 or the original Sum Insured, whichever is lower. The maximum total amount you can

increase your critical illness SumInsured under this feature over the lifeof the policy is the lesser of:

� The amount of critical illness SumInsured under your policy excludingCPI increases and increases effectedunder this feature; and

� $1,000,000.

The feature cannot be exercised if atthe time of your request:

� You are older than 50 years of age

� You have previously been acceptedby us with special conditionsaffecting the premium rates

� The premiums are being waivedunder the Waiver of PremiumOption, or

� You are currently entitled to make aclaim for a Terminal Illness orCritical Illness Benefit under a policyyou currently hold with us.

This option is only available where theinitial critical illness Sum Insured is$1,000,000 or less.

In respect of Recovery Money andFlexible Recovery Money the criticalillness Sum Insured cannot exceed theamount of death Sum Insured.

Critical Illness Buy BackOption (optional atadditional cost)One year after a Critical Illness Benefithas been paid, you can purchase anAviva Protection – Life Policy (deathonly) without providing further medicalevidence.

This option can only be exercisedwithin a period of 30 days from thefirst anniversary of the payment of theCritical Illness Benefit. If your policyincludes this option, we will providedeath cover on the following basis:

(a) the death Sum Insured may not exceed the Critical IllnessBenefit paid;

(b) premiums will be charged at theappropriate rate for the thenattained age based on the thencurrent published term insurancerates;

(c) any original exclusions or specialconditions applicable under thispolicy will be maintained.

Where the Critical Illness Buy BackOption is exercised in conjunction with the Critical Illness ReinstatementOption (see below), Indexation (as defined on page 31) will not be available.

This option ceases at the policyanniversary preceding age 65.

Critical Illness ReinstatementOption (optional atadditional cost)One year after a Critical Illness Benefithas been paid, you can reinstate 50%of the critical illness cover withoutproviding further medical evidence.This feature provides critical illnesssufferers with a second level ofprotection and peace of mind.

This option can only be exercisedwithin a period of 30 days from thefirst anniversary of the payment of theCritical Illness Benefit. If your policyincludes this option, we will reinstateyour critical illness cover on thefollowing basis:

(a) the critical illness Sum Insured maynot exceed 50% of the CriticalIllness Benefit paid;

(b) premiums will be charged at theappropriate rate for the thenattained age based on the thencurrent published term insurancerates;

(c) any original exclusions or specialconditions applicable under thispolicy will be maintained.

Indexation (as defined on page 31) will not be available.

Page 12 of 76

Aviva Protection – Recovery Money continued

This option cannot be exercised afterCritical Illness Benefits are paid forCoronary Artery Disease, or if Disabilityor Terminal Illness Benefits are paid.

We will pay a claim under thereinstated cover if you suffer from a Critical Illness and

� You have not claimed for the sameCritical Illness.

� You have not claimed for aCardiovascular Related Illness.

� It is not a condition that hasoccurred as a direct or indirectresult of the original Critical Illness event.

� It is not a Stroke (including Paralysisas a result of a CerebrovascularAccident) and the original claim wasfor a Cardiovascular Related Illness.

� The critical event occurs after thecover has been reinstated.

For the purpose of this sectionCardiovascular Related Illness are:

Coronary Artery By-Pass Surgery, Heart Attack, Heart Surgery,cardiomyopathy, Open Heart Surgery,Out of Hospital Cardiac Arrest, Primary Pulmonary Hypertension.

This option ceases at the policyanniversary preceding age 65.

Additional features The following additional features areexplained on page 31:

Indexation of benefitUpgrade guarantee24 hour world wide coverInterim Accident Cover

Level of coverMinimumsA minimum critical illness Sum Insuredof $10,000 applies.

In addition minimum premium andpremium loadings do apply, refer topages 35 and 36.

MaximumsDeath Sum Insured: There are nomaximum limits in respect of deathcover.

Disability Sum Insured: A maximumdisability Sum Insured of $2,500,000applies.

Critical Illness Sum Insured: Themaximum level of critical illness cover is$1,500,000 in aggregate with us andunder any similar policy with any otherinsurer. Additional critical illness coverwill not be issued in excess of thisaggregate limit. The critical illness SumInsured cannot exceed the amount ofdeath Sum Insured.

ExclusionsThere are certain exclusions that apply to your policy. Exclusions arecircumstances in which we are notrequired to pay the benefits under the policy.

The Death Benefit is not payable if yourdeath was caused by suicide withinthirteen (13) months of commencementor reinstatement of the policy. If yourdeath was caused by suicide withinthirteen (13) months of an increase thenthe increase is not payable.

No Critical Illness Benefit will bepayable in the event of self-inflictedillness or injury.

The Critical Illness Benefit will not be payable if it is shown that you donot have the condition which has been diagnosed.

Neither the Disability Benefit nor theWaiver of Premium Option will bepayable in the event of attemptedsuicide, self-inflicted illness or injury orparticipation in insurrection.

No payment will be made for HeartAttack, Cardiomyopathy, Stroke,Benign Intracranial Tumour, Cancer,Heart Surgery, Open Heart Surgery,Coronary Artery By Pass Surgery orCoronary Artery Disease if thecondition is diagnosed, or symptoms

leading to diagnosis become reasonablyapparent, before or within threemonths of the commencement orreinstatement of the policy.

If any of the above conditions isdiagnosed or becomes apparent within three months of an increase in benefits, then the amount of theincrease will not be payable.

Payment will be made for any insured events that are independent of any conditions or symptomsoriginally diagnosed within the threemonth period.

Where this Recovery Money policy is toreplace an existing similar policy fromanother insurer, the three monthexclusion of payments will not applywhere the same medical conditions andprocedures have been covered under thepolicy to be replaced. This will only applyup to the lesser of the Sum Insuredunder the policy being replaced and theSum Insured under this policy. It will alsoonly apply where the life to be insured isthe same under both policies and wherethe policy being replaced has been inforce for at least three months.

In the event of a claim within the firstthree months of this policy, evidence of:

a) the conditions and procedurescovered under the replaced policy;

b) the currency of the replacementpolicy at the Commencement Dateof this policy ; and

c) cancellation of the replaced policyfrom the previous reinsurer,

must be provided by the Policyowner toenable the three month exclusion ofpayments to be waived.

Where we agree to replace an existingpolicy from another insurer, thethirteen (13) month exclusion forsuicide will not apply where the SumInsured under the policy being replacedis greater than or equal to the SumInsured under this policy, and thepolicy being replaced has been in forcefor at least twelve (12) months.

Page 13 of 76

Aviva Protection – Flexible Recovery Money

Aviva Protection – Flexible Recovery Money provides a benefit if you arediagnosed with one of the critical illnesses covered by the policy. It is anancillary policy that can only be held in conjunction with an approvedAviva Protection – Life policy. The Flexible Recovery Money policy and theLife policy are linked. A benefit payable under one policy will reduce thebenefit provided under the other. You may choose to include optionaldisability cover for an additional premium.

Ind

exat

ion

(C

PI L

inki

ng

)

Dis

abili

ty (

TPD

) B

enef

it O

pti

on

Eco

no

mis

er O

pti

on

Gu

aran

teed

Ren

ewab

le

Inte

rim

Acc

iden

t In

sura

nce

Leve

l Pre

miu

m

Dis

abili

ty B

uy

Bac

k o

pti

on

Step

ped

Pre

miu

ms

Up

gra

de

Gu

aran

tee

Wai

ver

of

Prem

ium

Cri

tica

l Illn

ess

Ben

efit

Cri

tica

l Illn

ess

Bu

y B

ack

Op

tio

n

Cri

tica

l Illn

ess

Rei

nst

atem

ent

Op

tio

n

Futu

re In

sura

bili

ty C

riti

cal I

llnes

s

Aviva Protection – Flexible Recovery Money

B OC B B B B O B B O OC O O B

Aviva Protection – Flexible Recovery Money: a snapshot of what this cover includes

B = Benefit included in basic price O = Option at additional cost, benefit ceases at policy anniversary preceding age 65 OC = Option

at additional cost, definition changes to Loss of Independent Existence at policy anniversary preceding age 65

These policies are ‘guaranteedrenewable’. This means that, providedyou pay the premiums you can renewyour cover each year until the policyexpiry date without having to providefurther medical evidence.

When you apply for the policy youchoose the amount of the lump sumbenefit payable under the policy. Thislump sum benefit is called the ‘SumInsured’. You can choose differentlevels of Sum Insured for the criticalillness and disability parts of the policy.

The Critical Illness Benefit will only bepaid on correct diagnosis of any one ofthe listed critical illnesses. Payment ofCritical Illness Benefit is based uponthe precise definitions shown in the‘Medical Definitions’ sectioncommencing on page 44.

For benefits to be payable under thispolicy, an approved Aviva Protection –Life policy must have been in forcethroughout the period insured by thispolicy, with a death Sum Insured atleast equal to the greater of the criticalillness Sum Insured and the aggregateof the disability Sum Insured heldunder this and the associated Lifepolicy.

Aviva Protection – Flexible RecoveryMoney is a policy with the option topurchase disability cover. It is designedto be bundled with the AvivaProtection – Life policy.

The flexibility exists in the innovative waywe allow the critical illness cover to beowned by a different individual or entityfrom the death cover.

Two policies are issued, one for deathand optional disability cover, and onefor critical illness and optionaldisability cover. Each policy can have adifferent owner which can include asuperannuation fund (see page 33).However the policies are priced as ifthey are one combined policy resultingin significant pricing efficiencies.

As the policies are linked, the deathcover must be maintained for thecritical illness cover to remain in force.A claim for critical illness will reducethe death and disability Sum Insured.

DEATH DISABILITY CRITICALILLNESS

Overlapping Risk

Policy Owner 1

Bundledpricing

advantages=

Policy Owner 2

Page 14 of 76

The benefitsCritical Illness Benefit(standard)If a Death Benefit or Terminal IllnessBenefit is paid under the associatedAviva Protection – Life policy, theCritical Illness Benefit payable underthis policy will be reduced by acorresponding amount.

If a Critical Illness Benefit is paid underthis policy, the amount of DeathBenefit, Terminal Illness Benefit and, ifapplicable, Disability Benefit payableunder the Aviva Protection – Life policywill be reduced by a correspondingamount, as explained on page 5.

If a Disability Benefit is paid, theCritical Illness Benefit under this policywill be reduced by the aggregateamounts actually paid under this policyand the associated Aviva Protection –Life policy.

Critical illnesses definitionbefore policy anniversarypreceding age 65

If you are correctly diagnosed with one of the following critical illnesses (as defined) at any time up to policyanniversary preceding age 65, we willpay the Sum Insured as a lump sum.

The critical illnesses covered are:

Aplastic AnaemiaBenign Intracranial TumourBlindnessCancerCardiomyopathyChronic Lung DiseaseComaCoronary Artery By-Pass SurgeryCoronary Artery DiseaseDeafnessDementiaEncephalitisHeart AttackHeart SurgeryLiver DiseaseLoss of Independent ExistenceLoss of Speech

Major BurnsMajor Head TraumaMajor Organ TransplantMedically Acquired HIV InfectionMotor Neurone DiseaseMultiple SclerosisOccupationally Acquired HIV InfectionOpen Heart SurgeryOut of Hospital Cardiac ArrestParalysisParkinson’s DiseasePneumonectomyPrimary Pulmonary HypertensionRenal FailureStroke

The definitions of the critical illnessesare contained in the ‘MedicalDefinitions’ section of this document,commencing on page 44.

For Coronary Artery Disease andMultiple Sclerosis the amount payablemay be limited in the manner set outunder Medical Definitions commencingon page 44.

For Occupationally Acquired HIVInfection and Medically Acquired HIVInfection the Critical Illness Benefit maybe excluded where a Cure becomesavailable as set out under ‘MedicalDefinitions’ commencing on page 44.

Critical illnesses definition afterpolicy anniversary precedingage 65

Conversion to Loss of IndependentExistence at age 65.

If you have been covered under theCritical Illness Benefit and there hasnot been a claim on the policy, thenthe Critical Illness Benefit will continuefrom the policy anniversary precedingage 65 until the expiry of the policy.However from the policy anniversarypreceding age 65, the abovedefinitions of critical illness shall ceaseto apply. Instead, the critical illnessSum Insured will be payable if you arecorrectly diagnosed as being subject toa Loss of Independent Existence (asdefined on page 45).

Disability Benefit (optional atadditional cost)By taking this option your benefit isextended to include disability cover. If you become Totally and PermanentlyDisabled (as defined on page 4) thedisability Sum Insured will be paid toyou as a lump sum.

The featuresEach of the following features isprovided on the terms set out onpages 5 and 6.

Economiser (standard)

Waiver of Premium Option (optional at additional cost)

Disability Buy Back Option (optional at additional cost)

Each of the following features isprovided on the terms set out on page 11:

Future Insurability Critical Illness(standard)

Critical Illness Buy Back Option(optional at additional cost)

Critical Illness Reinstatement Option(optional at additional cost)

Additional features The following additional features areexplained on page 31:

Indexation of benefitUpgrade guarantee24 hour world wide coverInterim Accident Cover

Level of coverMinimumsA minimum critical illness Sum Insuredof $10,000 applies.

In addition minimum premium andpremium loadings do apply, refer topages 35 and 36.

Aviva Protection – Flexible Recovery Money continued

Page 15 of 76

MaximumsDisability Sum Insured: A maximumDisability Benefit of $2,500,000applies, in aggregate between this andthe Aviva Protection – Life policy. Also,the aggregate of the disability coverheld under this policy and theassociated Aviva Protection – Life policycannot exceed the death Sum Insuredunder the Aviva Protection – Life policy.

Critical Illness Sum Insured: Themaximum level of critical illness cover is$1,500,000 in aggregate with us andunder any similar policy with any otherinsurer. Additional critical illness coverwill not be issued in excess of thisaggregate limit. Further, the criticalillness Sum Insured cannot exceed thedeath Sum Insured under the AvivaProtection – Life policy.

ExclusionsThere are certain exclusions that apply to your policy. Exclusions arecircumstances in which we are notrequired to pay the benefits under the policy.

The Critical Illness Benefit will not bepayable in the event of self-inflictedillness or injury.

The Critical Illness Benefit will not bepayable if it is shown that you do nothave the condition which has beendiagnosed.

Neither the Disability Benefit nor theWaiver of Premium Option will bepayable in the event of attemptedsuicide, self-inflicted illness or injury orparticipation in insurrection.

No payment will be made for HeartAttack, Cardiomyopathy, Stroke,Benign Intracranial Tumour, Cancer,Heart Surgery, Open Heart Surgery,Coronary Artery By Pass Surgery orCoronary Artery Disease if the condition is diagnosed, orsymptoms leading to diagnosis becomereasonably apparent, before or withinthree months of the commencement or

reinstatement of the policy.

If any of the above conditions isdiagnosed or becomes apparent withinthree months of an increase inbenefits, then the amount of theincrease will not be payable.

Payment will be made for any insuredevents that are independent of anyconditions or symptoms originallydiagnosed within the three monthperiod.

Where this Recovery Money policy is toreplace an existing similar policy fromanother insurer, the three monthexclusion of payments will not applywhere the same medical conditions andprocedures have been covered underthe policy to be replaced. This will onlyapply up to the lesser of the SumInsured under the policy being replacedand the Sum Insured under this policy. Itwill also only apply where the life to beinsured is the same under both policiesand where the policy being replaced hasbeen in force for at least three months.

In the event of a claim within the firstthree months of this policy, evidence of:

a) the conditions and procedurescovered under the replaced policy;

b) the currency of the replacementpolicy at the Commencement Dateof this policy ; and

c) cancellation of the replaced policyfrom the previous reinsurer,

must be provided by the Policyowner toenable the three month exclusion ofpayments to be waived.

Page 16 of 76

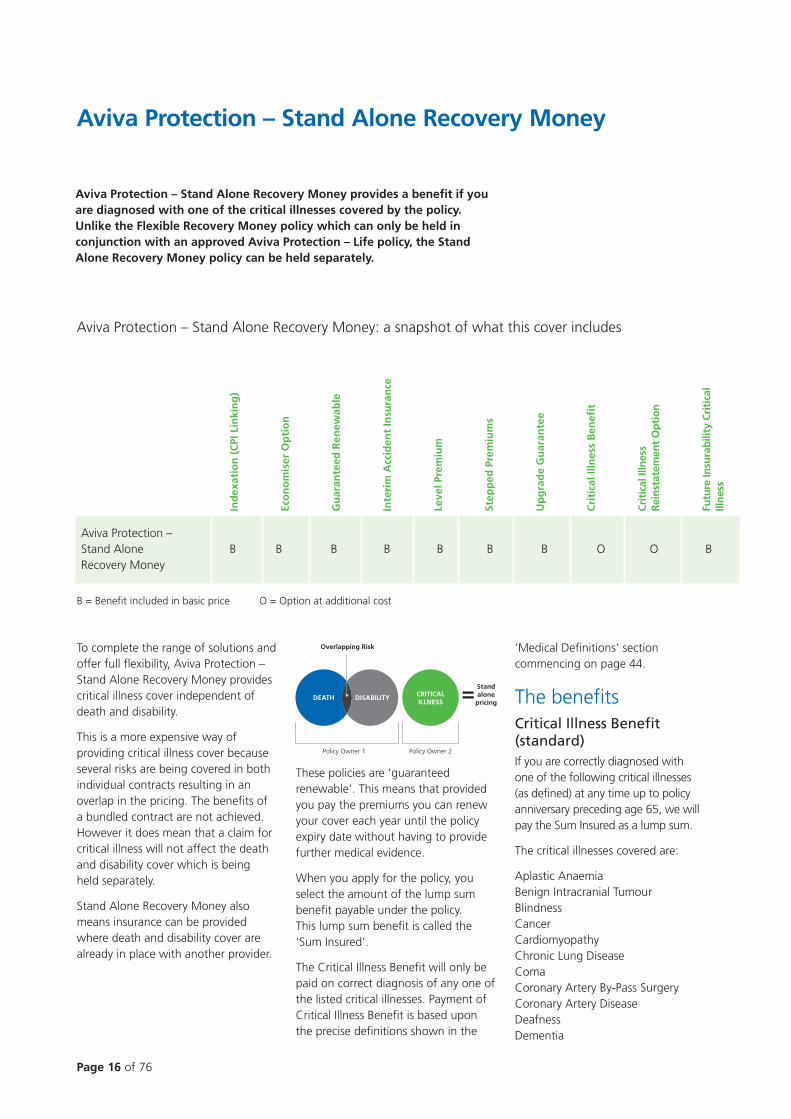

Aviva Protection – Stand Alone Recovery Money

Aviva Protection – Stand Alone Recovery Money provides a benefit if youare diagnosed with one of the critical illnesses covered by the policy. Unlike the Flexible Recovery Money policy which can only be held inconjunction with an approved Aviva Protection – Life policy, the StandAlone Recovery Money policy can be held separately.

Aviva Protection – Stand Alone Recovery Money: a snapshot of what this cover includes

Ind

exat

ion

(C

PI L

inki

ng

)

Eco

no

mis

er O

pti

on

Gu

aran

teed

Ren

ewab

le

Inte

rim

Acc

iden

t In

sura

nce

Leve

l Pre

miu

m

Step

ped

Pre

miu

ms

Up

gra

de

Gu

aran

tee

Cri

tica

l Illn

ess

Ben

efit

Cri

tica

l Illn

ess

Rei

nst

atem

ent

Op

tio

n

Futu

re In

sura

bili

ty C

riti

cal

Illn

ess

Aviva Protection – Stand Alone Recovery Money

B B B B B B B O O B

B = Benefit included in basic price O = Option at additional cost

To complete the range of solutions andoffer full flexibility, Aviva Protection –Stand Alone Recovery Money providescritical illness cover independent ofdeath and disability.

This is a more expensive way ofproviding critical illness cover becauseseveral risks are being covered in bothindividual contracts resulting in anoverlap in the pricing. The benefits of a bundled contract are not achieved.However it does mean that a claim forcritical illness will not affect the deathand disability cover which is being held separately.

Stand Alone Recovery Money alsomeans insurance can be providedwhere death and disability cover arealready in place with another provider.

These policies are ‘guaranteedrenewable’. This means that providedyou pay the premiums you can renewyour cover each year until the policyexpiry date without having to providefurther medical evidence.

When you apply for the policy, youselect the amount of the lump sumbenefit payable under the policy. This lump sum benefit is called the ‘Sum Insured’.

The Critical Illness Benefit will only bepaid on correct diagnosis of any one ofthe listed critical illnesses. Payment ofCritical Illness Benefit is based uponthe precise definitions shown in the

‘Medical Definitions’ sectioncommencing on page 44.

The benefitsCritical Illness Benefit(standard)If you are correctly diagnosed with one of the following critical illnesses (as defined) at any time up to policyanniversary preceding age 65, we willpay the Sum Insured as a lump sum.

The critical illnesses covered are:

Aplastic AnaemiaBenign Intracranial TumourBlindnessCancerCardiomyopathyChronic Lung DiseaseComaCoronary Artery By-Pass SurgeryCoronary Artery DiseaseDeafnessDementia

DEATH DISABILITY

Overlapping Risk

Policy Owner 1

CRITICALILLNESS

Standalone

pricing=

Policy Owner 2

Page 17 of 76

EncephalitisHeart AttackHeart SurgeryLiver DiseaseLoss of Independent ExistenceLoss of SpeechMajor BurnsMajor Head TraumaMajor Organ TransplantMedically Acquired HIV InfectionMotor Neurone DiseaseMultiple SclerosisOccupationally Acquired HIV InfectionOpen Heart SurgeryOut of Hospital Cardiac ArrestParalysisParkinson’s DiseasePneumonectomyPrimary Pulmonary HypertensionRenal FailureStroke

The definitions of the critical illnessesare contained in the ‘MedicalDefinitions’ section of this document,commencing on page 44.

For Coronary Artery Disease andMultiple Sclerosis the amount payablemay be limited in the manner set outunder Medical Definitions commencingon page 44.

For Occupationally Acquired HIVInfection and Medically Acquired HIVInfection the Critical Illness Benefit maybe excluded where a Cure becomesavailable as set out under ‘MedicalDefinitions’ commencing on page 44.

Death Benefit (standard)If you die within 14 days of thediagnosis of the critical illness, we will pay $5,000 to your estate.

The featuresThe Economiser feature is provided onthe terms as set out on page 5. TheFuture Insurability Critical Illness(standard) and Critical IllnessReinstatement Option (available at anadditional cost) on the terms set outon page 11.

The following additional features areexplained on page 31:

Indexation of benefitUpgrade guarantee24 hour world wide coverInterim Accident Cover

Level of coverMinimums/Maximums A minimum critical illness Sum Insuredof $10,000 applies.

In addition minimum premium andpremium loadings do apply, refer topages 35 and 36.

The maximum Sum Insured is$1,500,000 in aggregate with us and under any similar policy with anyother insurer. Additional critical illnesscover will not be issued in excess ofthis aggregate limit.

ExclusionsThere are certain exclusions that apply to your policy. Exclusions arecircumstances in which we are notrequired to pay the benefits under the policy.

The Critical Illness Benefit will not bepayable in the event of self-inflictedillness or injury.

It will also not be payable if it is shownthat you do not have the conditionwhich has been diagnosed.

We will only pay the Critical Illness Benefitif you live for at least fourteen dayswithout the aid of a life support system,after diagnosis of the Critical Illness.

No payment will be made for HeartAttack, Cardiomyopathy, Stroke,Benign Intracranial Tumour, Cancer,Heart Surgery, Open Heart Surgery,Coronary Artery By Pass Surgery orCoronary Artery Disease if thecondition is diagnosed, or symptomsleading to diagnosis becomereasonably apparent, before or withinthree months of the commencementor reinstatement of the policy.

If any of the above conditions isdiagnosed or becomes apparent withinthree months of an increase inbenefits, then the amount of theincrease will not be payable.

Payment will be made for any insuredevents that are independent of anyconditions or symptoms originallydiagnosed within the three monthperiod.

Where this Recovery Money policy is toreplace an existing similar policy fromanother insurer, the three monthexclusion of payments will not applywhere the same medical conditions andprocedures have been covered under thepolicy to be replaced. This will only applyup to the lesser of the Sum Insuredunder the policy being replaced and theSum Insured under this policy. It will alsoonly apply where the life to be insured isthe same under both policies and wherethe policy being replaced has been inforce for at least three months.

In the event of a claim within the firstthree months of this policy, evidence of:

a) the conditions and procedurescovered under the replaced policy;

b) the currency of the replacementpolicy at the Commencement Dateof this policy ; and

c) cancellation of the replaced policyfrom the previous reinsurer,

must be provided by the Policyowner toenable the three month exclusion ofpayments to be waived.

The Death Benefit is not payable if you commit suicide within thirteenmonths of the commencement orreinstatement of the policy.

Page 18 of 76

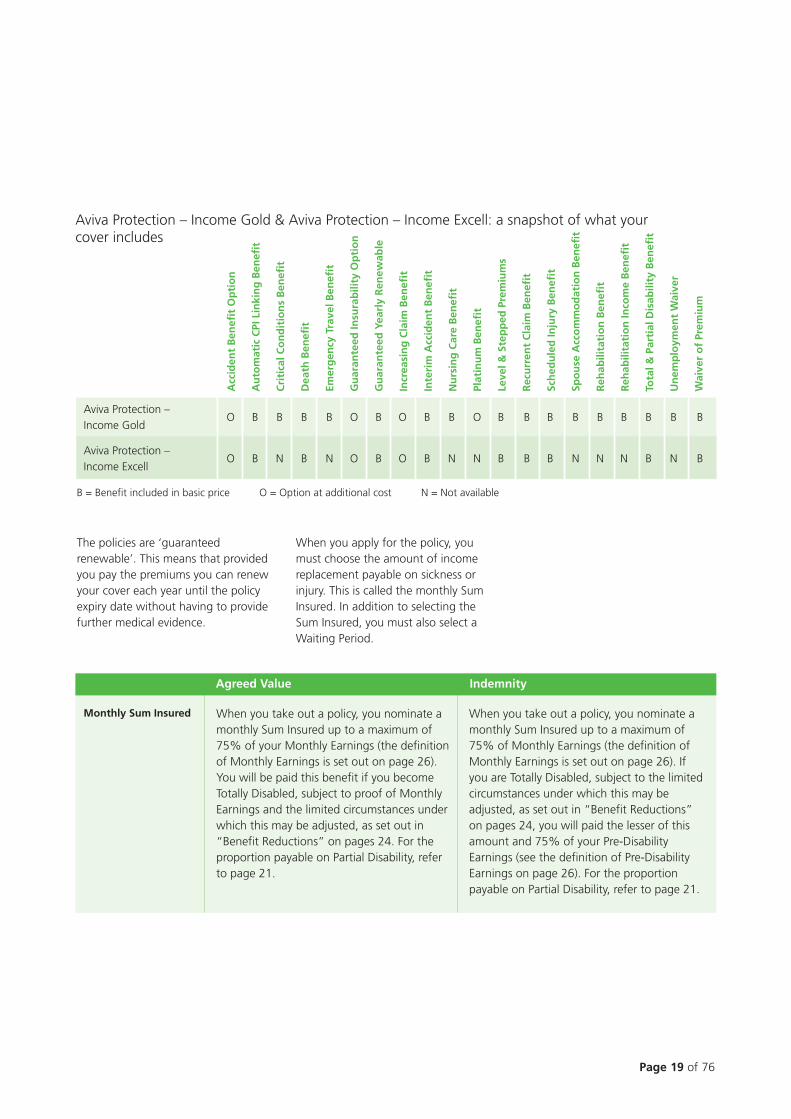

Aviva Protection – Income Gold, and Aviva Protection – Income Excell

Aviva Protection – Income Gold and Aviva Protection – Income Excellprovide income replacement while you are Totally Disabled or PartiallyDisabled and unable to work as a result of either sickness or injury.Payments are made until the end of the chosen benefit period.

The policies have the same basic structure, however Aviva Protection –Income Gold has several additional benefits and features.

Both policies offer you the choice ofagreed value or indemnity cover. Youhave the choice of an agreed monthlySum Insured (agreed value) or a SumInsured limited to the lesser of amonthly value nominated by you, and 75% of your average monthlyearnings for the 12 months precedingthe date of Total Disablement(indemnity). The maximum SumInsured is limited in the mannerdescribed on page 27. The premiumsfor agreed value and indemnity policiesare different and you should discusswith your financial adviser which is themost appropriate for you.

Insuring your greatest assetMany people consider their greatestasset to be their home, contents or insome cases an investment portfolio.The truth is these assets would simplynot exist if the individual did not havea consistent, reliable income.

As well as being necessary for survival,your ability to earn an income is in factyour greatest asset. Just like yourhouse and contents, you shouldconsider insuring this asset against theevent of illness or injury.

Aviva Protection – Income providesmonthly benefit payments to replace a significant portion of your income if you are ill or injured and unable to work.

Flexible solutionsThe Aviva Protectionfirst range ofincome protection solutions allows youto choose your own combination ofcover to meet your personal needs.You select the type of contract yourequire and the options you want atthe same time as having significantcontrol over the premium that you willpay.

By selecting certain options you canlimit the premium you pay, or you canmaximise the benefits you receive bypaying a higher premium.

It is important to discuss your optionswith your financial adviser to makesure you understand the implicationsof your decision.

Aviva Protection – Income Choose Aviva Protection –Income

Agreed ValuePolicy

IndemnityPolicy

Decision 2: Agreed Value Policy or Imdemnity Policy

Protection –Income Gold

Decision 1: Protection – Income Gold or Excell

Agreed ValuePolicy

IndemnityPolicy

Protection –Income Excell

Amount WaitingPeriod

BenefitPeriod

Decision 3: Benefit Amount, Waiting Period and Benefit Period

Amount WaitingPeriod

BenefitPeriod

Amount WaitingPeriod

BenefitPeriod

Amount WaitingPeriod

BenefitPeriod

The Aviva Income Protection decision tree

Page 19 of 76

Aviva Protection – Income Gold & Aviva Protection – Income Excell: a snapshot of what your cover includes

Aviva Protection – Income Gold

O B B B B O B O B B O B B B B B B B B B

Aviva Protection – Income Excell

O B N B N O B O B N N B B B N N N B N B

Acc

iden

t B

enef

it O

pti

on

Au

tom

atic

CPI

Lin

kin

g B

enef

it

Cri

tica

l Co

nd

itio

ns

Ben

efit

Dea

th B

enef

it

Emer

gen

cy T

rave

l Ben

efit

Gu

aran

teed

Insu

rab

ility

Op

tio

n

Gu

aran

teed

Yea

rly

Ren

ewab

le

Incr

easi

ng

Cla

im B

enef

it

Inte

rim

Acc

iden

t B

enef

it

Nu

rsin

g C

are

Ben

efit

Plat

inu

m B

enef

it

Leve

l & S

tep

ped

Pre

miu

ms

Rec

urr

ent

Cla

im B

enef

it

Sch

edu

led

Inju

ry B

enef

it

Spo

use

Acc

om

mo

dat

ion

Ben

efit

Reh

abili

tati

on

Ben

efit

Reh

abili

tati

on

Inco

me

Ben

efit

Tota

l & P

arti

al D

isab

ility

Ben

efit

Un

emp

loym

ent

Wai

ver

Wai

ver

of

Prem

ium

The policies are ‘guaranteedrenewable’. This means that providedyou pay the premiums you can renewyour cover each year until the policyexpiry date without having to providefurther medical evidence.

When you apply for the policy, youmust choose the amount of incomereplacement payable on sickness orinjury. This is called the monthly SumInsured. In addition to selecting theSum Insured, you must also select aWaiting Period.

B = Benefit included in basic price O = Option at additional cost N = Not available

Monthly Sum Insured When you take out a policy, you nominate amonthly Sum Insured up to a maximum of75% of your Monthly Earnings (the definitionof Monthly Earnings is set out on page 26).You will be paid this benefit if you becomeTotally Disabled, subject to proof of MonthlyEarnings and the limited circumstances underwhich this may be adjusted, as set out in“Benefit Reductions” on pages 24. For theproportion payable on Partial Disability, referto page 21.

When you take out a policy, you nominate amonthly Sum Insured up to a maximum of75% of Monthly Earnings (the definition ofMonthly Earnings is set out on page 26). Ifyou are Totally Disabled, subject to the limitedcircumstances under which this may beadjusted, as set out in “Benefit Reductions”on pages 24, you will paid the lesser of thisamount and 75% of your Pre-DisabilityEarnings (see the definition of Pre-DisabilityEarnings on page 26). For the proportionpayable on Partial Disability, refer to page 21.

Agreed Value Indemnity

Page 20 of 76

Aviva Protection – Income Gold, and Aviva Protection – Income Excell continued

Waiting periodYou must choose a waiting periodwhen taking out your policy. TheWaiting Period is the period you mustwait before benefits become payable.

Your choice of waiting period dependson your choice of benefit period andthe type of premium (ie stepped orlevel). Your financial adviser will be ableto assist you with all these choices.

For stepped premiums if you choose atwo or five year benefit period, youhave the choice of waiting periods of14 days, 30 days, 60 days, 90 days,and 180 days.

If you choose a benefit period to age60, 65 or 70 years you also have thechoice of waiting periods of 365 and730 days. However if you choose a 365days or 730 days waiting period, theCritical Conditions Benefit, SpouseAccommodation Benefit, Nursing CareBenefit, Scheduled Injury Benefit,Emergency Travel Benefit, RehabilitationIncome Benefit are not available.

For level premiums you have the choiceof waiting periods of 14 days, 30 days,60 days and 90 days.

Generally speaking, the longer thewaiting period, the lower the insurancepremium.

The waiting period commences on thedate that you receive advice ofDisability from a medical practitioner. Incircumstances where it can besubstantiated that disability had begunearlier than the date of receiving advicefrom a medical practitioner, the date ofcommencement may be backdated byup to 7 days with medical certification.

If You return to full time gainfulemployment during the Waiting Periodfor five (5) consecutive days or less, the number of days that You weregainfully employed will be added tothe Waiting Period.

If You return to full time gainfulemployment during the Waiting Periodfor more than five (5) consecutive days,the Waiting Period begins again fromthe day after the last day You weregainfully employed.

Benefit periodThe Benefit Period is the maximumperiod of time for which the monthlybenefit is payable, whilst you areTotally or Partially Disabled due toinjury or sickness.

The Benefit Period commences at theend of the applicable waiting period. Itcontinues until the expiry of the BenefitPeriod selected or the policy anniversarypreceding the specified age (whichever occurs first), in accordance withthe following table.

Expiry at policy Benefit anniversaryPeriod: preceding age:

2 years for sickness and injury 65

5 years for sickness and injury 65

To age 60 years for sickness and injury 60

To age 65 years for sickness and injury 65

To age 70 years for sickness and injury 65

The benefit period to age 70 years isonly available to people in certainoccupational classes. Where thebenefit period is to age 70 years, theexpiry date of the policy is the policyanniversary preceding age 65 years.However, the insured is Totally orPartially Disabled at the policyanniversary preceding age 65 thenpayment of benefits will continue tothe policy anniversary preceding age70 years, or until the insured ceases tobe either Totally or Partially Disabled,whichever occurs first.

If the policy is an indemnity policy andyou are receiving benefits as a result ofPartial Disability then the claimpayment will continue for a maximumof two years.

The benefits andfeaturesKey terms used in this section aredefined on pages 25 to 27; please readthose definitions carefully.

Total Disability Benefit(standard)If, solely as a result of Injury orSickness, you are Totally Disabled whileyour policy is in force, we will pay yourmonthly Sum Insured. Payment willstart from the first day after theWaiting Period has elapsed andcontinue while you are Totally Disabledup to the cessation of the BenefitPeriod for any one Injury or Sickness.We will pay one-thirtieth of themonthly Sum Insured for each day ofTotal Disability.

Partial Disability Benefit(standard)If you are Partially Disabled, aproportion of the monthly Sum Insuredwill be paid to you.

For agreed value policies only

If you have an agreed value policy andyou are Partially Disabled for longerthan the Waiting Period, we will assessthe impact of Your Partial Disability onYour earning ability.

We will pay a proportion of theMonthly Benefit to the Policyowner, at the end of the Waiting Period, due to Your Partial Disability only if:

(i) solely because of Your PartialDisability You have been unable togenerate at least 80% of Your Pre-Disability Earnings for theduration of the Waiting Period; or

(ii) Your Partial Disability is due to Youhaving suffered a Deemed Disabilityand at the end of the applicablepayment period for DeemedDisability benefits You are stillPartially Disabled at the end of theWaiting Period.

If You satisfy one of the above criteria,the proportion we will pay will be:

A - B A

where A is Your Pre-Disability Earningsand B is Your Monthly Earnings for themonth in which Partial Disability isclaimed. If, during the first three (3)months of a continuous period ofPartial Disability Your Monthly Earningsare 20% or less of Your Pre-DisabilityEarnings, we will pay the full MonthlyBenefit during those months.

If You are capable of working on apartial basis but You are not working,then we will calculate MonthlyEarnings based on what You couldreasonably be expected to earn if Youwere working. We will base thiscalculation on medical advice (whichwill include the opinion of YourMedical Practitioner).

If You have suffered a DeemedDisability and at the end of theapplicable payment period you arePartially Disabled, the Waiting Periodwill be deemed to have commencedon the date that You suffered theDeemed Disability, as certified by aMedical Practitioner.

We will pay the Partial DisabilityBenefit monthly in arrears. The PartialDisability Benefit will stop at the end ofthe Benefit Period, or when You ceaseto be Partially Disabled or when YourMonthly Earnings equals Your Pre-Disability Earnings, whicheveroccurs first.

For indemnity policies only

If you have an indemnity policy andyou are Partially Disabled for longerthan the Waiting Period, we will assessthe impact of Your Partial Disability onYour earning ability.

We will pay a proportion of theMonthly Claim to the Policyowner, atthe end of the Waiting Period, due toYour Partial Disability only if:

(i) solely because of Your PartialDisability You have been unable togenerate at least 80% of Your Pre-Disability Earnings for theduration of the Waiting Period; or

(ii) Your Partial Disability is due to You having suffered a DeemedDisability and at the end of theapplicable payment period forDeemed Disability benefits You are still Partially Disabled at the end of the Waiting Period.

If you satisfy one of the above criteria,the proportion we will pay will be:

A - BA

where A is your Indexed Pre-DisabilityEarnings and B is your Monthly Earningsfor the month in which Partial Disabilityis claimed. If, during the first three (3)months of a continuous period ofPartial Disability your Monthly Earningsare 20% or less of Your Pre-DisabilityEarnings, we will pay the full MonthlyBenefit, during those months.

If You are capable of working on apartial basis but you are not working,then we will calculate Monthly Earningsbased on what you could reasonably beexpected to earn if you were working.We will base this calculation onmedical advice (which will include theopinion of your Medical Practitioner).

If you have suffered a DeemedDisability and at the end of theapplicable payment period you arePartially Disabled, the Waiting Periodwill be deemed to have commencedon the date that you suffered theDeemed Disability, as certified by aMedical Practitioner.

We will pay the Partial DisabilityBenefit monthly in arrears. The PartialDisability Benefit will stop at the end ofthe Benefit Period, or when you ceaseto be Partially Disabled or when yourMonthly Earnings, equal your Pre-Disability Earnings, whicheveroccurs first.

Page 21 of 76

The Partial Disability Benefit will berestricted to a maximum of two yearsin respect of any one claim, includingbenefits paid under the RecurrentClaim Benefit.

Waiver of Premium(standard)After you have been disabled forlonger than the Waiting Period, we willwaive all premiums payable under yourpolicy for the period you continue toreceive either the Partial or TotalDisability Benefit.

Recurrent Claim Benefit(standard)If your benefit period is to age 60, 65 or 70 and you suffer a Total orPartial Disability within 12 months afterthe end of a Disability claim from thesame or related causes, the WaitingPeriod will not be applied again and allperiods of Disability will be consideredpart of the same benefit period. For allother benefit periods this will applywhere the related disablement occurswithin 6 months.

Scheduled Injury Benefit(standard)If you sustain any of the followinginjuries, we will pay you a ScheduledInjury Benefit equal to your monthlySum Insured even if you are working.The Scheduled Injury Benefit is paidmonthly in advance commencing uponreceipt of the claim form verifying theinjury, and will stop on the earlier ofthe expiry of the Scheduled InjuryBenefit Payment Period, or the last day of the Benefit Period.

Total and PaymentPermanent periodLoss of: (months)

Use of your legs or your legs and arms due to paralysis 60