b regulation (ec) no 2423/2001 of the european · pdf filem1 regulation (ec) ... m5 regulation...

TRANSCRIPT

This document is meant purely as a documentation tool and the institutions do not assume any liability for its contents

►B REGULATION (EC) No 2423/2001 OF THE EUROPEAN CENTRAL BANK

of 22 November 2001

concerning the consolidated balance sheet of the monetary financial institutions sector

(ECB/2001/13)

(OJ L 333, 17.12.2001, p. 1)

Amended by:

Official Journal

No page date

►M1 Regulation (EC) No 993/2002 of the European Central Bank of 6 June2002

L 151 11 11.6.2002

►M2 Regulation (EC) No 2174/2002 of the European Central Bank of 21November 2002

L 330 29 6.12.2002

►M3 Regulation (EC) No 1746/2003 of the European Central Bank of 18September 2003

L 250 17 2.10.2003

►M4 Regulation (EC) No 2181/2004 of the European Central Bank of 16December 2004

L 371 42 18.12.2004

►M5 Regulation (EC) No 4/2007 of the European Central Bank of 14December 2006

L 2 3 5.1.2007

►M6 Regulation (EC) No 1489/2007 of the European Central Bank of 29November 2007

L 330 20 15.12.2007

Corrected by:

►C1 Corrigendum, OJ L 57, 27.2.2002, p. 34 (2423/2001)

►C2 Corrigendum, OJ L 347, 20.12.2002, p. 60 (2147/2002)

2001R2423— EN— 04.01.2008 — 006.001— 1

REGULATION (EC) No 2423/2001 OF THE EUROPEANCENTRAL BANK

of 22 November 2001

concerning the consolidated balance sheet of the monetary financialinstitutions sector

(ECB/2001/13)

THE GOVERNING COUNCIL OF THE EUROPEAN CENTRAL BANK,

Having regard to Council Regulation (EC) No 2533/98 of 23 November1998 concerning the collection of statistical information by theEuropean Central Bank (1), and in particular to Article 5(1) andArticle 6(4) thereof,

Having regard to Council Regulation (EC) No 2531/98 of 23 November1998 concerning the application of minimum reserves by the EuropeanCentral Bank (2), and in particular to Article 6(4) thereof,

Whereas:

(1) Regulation (EC) No 2819/98 of the European Central Bank of 1December 1998 concerning the consolidated balance sheet of themonetary financial institutions sector (ECB/1998/16) (3) hasalready been amended by Regulation (EC) No 1921/2000(ECB/2000/8) (4); now that new substantial amendments arebeing made to the said Regulation, it is desirable that theprovisions in question should be recast by bringing themtogether in a single text with this Regulation.

(2) The European System of Central Banks (ESCB) requires, for thefulfilment of its tasks, the production of the consolidated balancesheet of the monetary financial institutions (MFI) sector. Theprincipal purpose thereof is to provide the European CentralBank (ECB) with a comprehensive statistical picture ofmonetary developments in the participating Member States,which are viewed as one economic territory. These statisticscover the aggregate financial assets and liabilities, in terms ofstocks, high quality flows for loans and also improved flowsfor holdings of securities.

(3) The ECB shall, in accordance with the provisions of the Treatyestablishing the European Community (hereinafter referred to asthe ‘Treaty’) and under the conditions laid down in the Statute ofthe European System of Central Banks and of the EuropeanCentral Bank (hereinafter referred to as the ‘Statute’), make regu-lations to the extent necessary to implement the tasks of theESCB as defined in the Statute and in some cases laid down inthe provisions adopted by the Council referred to in Article 107(6) of the Treaty.

(4) Article 5.1 of the Statute requires the ECB, assisted by thenational central banks (NCBs), to collect the necessary statisticalinformation either from the competent national authorities ordirectly from economic agents in order to undertake the tasksof the ESCB. Article 5.2 of the Statute stipulates that theNCBs shall carry out, to the extent possible, the tasksdescribed in Article 5.1.

▼B

2001R2423— EN— 04.01.2008 — 006.001— 2

(1) OJ L 318, 27.11.1998, p. 8.(2) OJ L 318, 27.11.1998, p. 1.(3) OJ L 356, 30.12.1998, p. 7.(4) OJ L 229, 9.9.2000, p. 34.

(5) It may be necessary, and may reduce the reporting burden, forNCBs to collect from the actual reporting population thestatistical information necessary to fulfil the statisticalrequirements of the ECB as part of a broader statisticalreporting framework which the NCBs establish under their ownresponsibility in accordance with Community or national law orestablished practice and which serves other statistical purposes,provided that the fulfilment of the statistical requirements of theECB is not jeopardised. In order to foster transparency, it isappropriate, in these cases, to inform the reporting agents thatdata are collected to fulfil other statistical purposes. In specificcases, the ECB may rely on statistical information collected forsuch purposes to fulfil its requirements.

(6) Article 3 of Regulation (EC) No 2533/98 requires the ECB tospecify the actual reporting population within the limits of thereference reporting population and entitles it to fully or partlyexempt specific classes of reporting agents from its statisticalreporting requirements. Article 6(4) provides that the ECB mayadopt regulations specifying the conditions under which the rightto verify or to carry out the compulsory collection of statisticalinformation may be exercised.

(7) Article 5 of Regulation (EC) No 2531/98 empowers the ECB toadopt regulations or decisions in order to exempt institutions fromthe minimum reserve requirements, to specify modalities toexclude or deduct liabilities owed to any other institution fromthe reserve basis and to establish differing reserve ratios forspecific categories of liabilities. Under Article 6, the ECB hasthe right to collect from institutions the information necessary forthe application of minimum reserves and the right to verify theaccuracy and quality of the information which institutions provideto demonstrate compliance with the minimum reserverequirements. It is desirable, in order to reduce the overallreporting burden, for the statistical information regarding themonthly balance sheet to be used, in addition, for the regularcalculation of the reserve base of the credit institutions subjectto the ESCB's minimum reserve system.

(8) Article 4 of Regulation (EC) No 2533/98 provides for MemberStates to organise themselves in the field of statistics and tocooperate fully with the ESCB in order to ensure fulfilment ofthe obligations arising from Article 5 of the Statute.

(9) While it is recognised that regulations adopted by the ECB underArticle 34.1 of the Statute do not confer any rights or impose anyobligations on non-participating Member States, Article 5 of theStatute applies to both participating and non-participatingMember States. Regulation (EC) No 2533/98 recalls thatArticle 5 of the Statute, together with Article 5 of the Treaty,implies an obligation to design and implement at national levelall the measures that the non-participating Member Statesconsider appropriate in order to carry out the collection of thestatistical information needed to fulfil the ECB's statisticalreporting requirements and timely preparations in the field ofstatistics in order for them to become participating MemberStates.

(10) In order to facilitate the liquidity management of the ECB and ofcredit institutions, reserve requirements should be confirmed atthe latest on the first day of the maintenance period; the needmay exceptionally arise for credit institutions to report revisionsto the reserve base or to reserve requirements which have beenconfirmed; the procedures for confirmation or acknowledgementof reserve requirements are without prejudice to the obligation forreporting agents always to report correct statistical informationand to revise incorrect statistical information they may havealready reported.

▼B

2001R2423— EN— 04.01.2008 — 006.001— 3

(11) The determination of specific procedures for mergers anddivisions involving credit institutions is necessary in order toclarify the obligations of these institutions in respect of reserverequirements; the definitions of mergers and divisions laid downin this Regulation are based on definitions already existing insecondary Community legislation relating to public limitedliability companies. These definitions have been adapted to thepurposes of this Regulation; these procedures are withoutprejudice to the possibility of holding minimum reservesthrough an intermediary.

(12) The monetary statistics of the ECB are derived from MFI balancesheet statistics collected in accordance with Regulation (EC) No2819/98 (ECB/1998/16) which was prepared during the secondstage of economic and monetary union and so were considered tobe only the minimum set of data required for monetary policypurposes. Moreover, the Regulation only covered the collectionof balance sheet stocks and not the reporting of revaluationadjustment data required to compile flow statistics for coun-terparts of the broad monetary aggregate M3, from which thegrowth rates are derived. Taking into account the limitations ofthese sets of data, it was necessary to enhance the MFI balancesheet statistics.

(13) It is necessary to expand the monthly requirements to provide amonthly breakdown of deposit liabilities by subsector and furtherby maturity/currency and of loans by subsector/maturity andpurpose as these breakdowns are considered essential formonetary policy purposes. This includes the integration of datapreviously collected only on a quarterly basis.

(14) It is necessary to derive stock and flow statistics for the monetaryaggregates and counterparts in a timely manner. From the conso-lidated balance sheet in terms of stocks, flow statistics are derivedusing additional statistical information relating to exchange ratechanges, other changes in the value of securities and the write-offs/write-downs of loans and other adjustments such as reclassi-fications.

(15) It is necessary to ensure the availability of appropriatelyharmonised and high quality data on write-offs/write-downs onloans by addressing a requirement to the statistical reportingagents. There is also a need to collect data on price revaluationsof securities.

(16) The separate balance sheet category ‘money market paper’ isremoved and merged with the data category ‘debt securitiesissued’ on the liability side. Instruments classified in thiscategory are entered under ‘debt securities issued’ and allocatedaccording to their original maturity. A corresponding reallocationhas been taken also on the asset side of the MFI balance sheet.

(17) The definition of deposits should take into account the use ofbalances representing prepaid amounts in the context of electronicmoney,

HAS ADOPTED THIS REGULATION:

Article 1

Definitions

For the purpose of this Regulation, the terms ‘reporting agents’, ‘parti-cipating Member State’, ‘resident’ and ‘residing’ shall have the samemeaning as defined in Article 1 of Regulation (EC) No 2533/98.

▼B

2001R2423— EN— 04.01.2008 — 006.001— 4

For the purposes of this Regulation, the terms ‘electronic money insti-tution’ and ’electronic money’ shall have the same meaning as inArticle 1(3) of Directive 2000/46/EC of the European Parliament andof the Council of 18 September 2000 on the taking up, pursuit of andprudential supervision of the business of electronic money institutions(1).

▼B

Article 2

Actual reporting population

1. The actual reporting population shall consist of the MFIs residentin the territory of the participating Member States. For statisticalpurposes, MFIs comprise resident credit institutions as defined inCommunity law, and all other resident financial institutions whosebusiness is to receive deposits and/or close substitutes for depositsfrom entities other than MFIs, and, for their own account (at least ineconomic terms), to grant credits and/or make investments in securities.

2. National central banks may grant derogations to small MFIs,provided that the MFIs which contribute to the monthly consolidatedbalance sheet account for at least 95 % of the total MFI balance sheet interms of stocks, in each participating Member State. NCBs shall checkthe fulfilment of this condition in good time in order to grant orwithdraw, if necessary, any derogation with effect from the start ofeach year.

▼M23. For the purposes of Annex I(1)(III)(vi), the actual reporting popu-lation shall also consist of other financial intermediaries exceptinsurance corporations and pension funds (hereinafter referred to as‘OFIs’), as set out in Article 2(2)(a) of Regulation (EC) No 2533/98.NCBs may grant derogations to those entities provided that the requiredstatistical information is collected from other available sources inaccordance with Annex I(1)(III)(vi). NCBs shall check the fulfilmentof this condition in good time in order to grant or withdraw, ifnecessary, any derogation with effect from the start of each year inagreement with the ECB. For the purposes of this Regulation, NCBsmay establish and maintain a list of reporting OFIs in accordance withthe principles set out in Annex I(1)(III)(vi).

▼M64. Without prejudice to Directive 2006/48/EC of the EuropeanParliament and of the Council of 14 June 2006 relating to the takingup and pursuit of the business of credit institutions (recast) (2) andArticle 2 of Regulation (EC) No 1745/2003 of the European CentralBank of 12 September 2003 on the application of minimum reserves(ECB/2003/9) (3), NCBs may, subject to the conditions specified inparagraphs 2 to 4 of Annex III, grant derogations to individual elec-tronic money institutions. The NCBs shall check the fulfilment of theconditions laid down in paragraph 2 of Annex III in good time in orderto grant or withdraw, if necessary, any derogation. Any NCB that grantssuch a derogation shall inform the ECB thereof.

▼B

Article 3

List of MFIs for statistical purposes

1. In accordance with the classification principles set out in Part 1(I)of Annex I, the ECB shall establish and maintain a list of MFIs forstatistical purposes, taking into account the requirements in respect of

▼M6

2001R2423— EN— 04.01.2008 — 006.001— 5

(1) OJ L 275, 27.10.2000, p. 39.(2) OJ L 177, 30.6.2006, p. 1.(3) OJ L 250, 2.10.2003, p. 10.

frequency and timeliness which arise from its use in the context of theESCB's minimum reserve system. The competence to establish andmaintain the list of MFIs for statistical purposes pertains to theExecutive Board of the ECB.

2. The list of MFIs for statistical purposes and its updates shall bemade accessible by NCBs and the ECB to the institutions concerned inan appropriate way, including by electronic means, via the Internet or, atthe request of the reporting agents concerned, in paper form.

3. The list of MFIs for statistical purposes shall be for informationonly. However, in the event that the latest accessible version of the listin accordance with paragraph 2 is incorrect, the ECB shall not imposesanctions on any entity which did not properly fulfil its reportingrequirements to the extent that it relied in good faith on the incorrectlist.

Article 4

Statistical reporting requirements

1. For the purposes of the regular production of the consolidatedbalance sheet of the MFI sector, in terms of stocks and flows, theactual reporting population shall report monthly statistical informationrelating to its end-of-month balance sheet and monthly flow adjustmentsin respect of write-offs/write-downs of loans and price revaluations inrespect of security holdings during the reporting period, to the NCB ofthe Member State in which the MFI is resident. Further details oncertain items of the balance sheet shall be reported quarterly, in termsof stocks.

2. The required statistical information is specified in Annex I to thisRegulation. ►M3 With reference to paragraphs 6a and 7a of Part 1,Section IV of Annex I, each NCB shall assess if data in respect of cellsmarked ►M5 with the ‘#’ or ‘*’ symbol, ◄ in Tables 3 and 4 of Part2 of Annex I, are insignificant, and shall inform the reporting agentswhen it does not require their reporting. ◄

3. The required statistical information shall be reported in accordancewith the minimum standards for transmission, accuracy, conceptualcompliance and revisions as set out in Annex IV to this Regulation.

4. The NCBs shall define and implement the reporting arrangementsto be followed by the actual reporting population in accordance withnational characteristics. The NCBs shall ensure that these reportingarrangements provide the statistical information required and allowaccurate checking of compliance with the minimum standards for trans-mission, accuracy, conceptual compliance and revisions as referred to inArticle 4(3).

5. The derogations referred to in Article 2(2) shall have the effect ofreducing the statistical reporting requirements of MFIs as follows:

— the credit institutions to which such derogations apply shall besubject to the reduced reporting requirements as set out in AnnexII to this Regulation,

— those small MFIs that are not credit institutions shall be subject tothe reduced reporting requirements as set out in Annex III to thisRegulation.

Small MFIs may choose not to make use of the derogations and to fulfilthe full reporting requirements instead.

6. Without prejudice to the derogation in Article 2(2), NCBs maygrant a derogation in respect of the reporting of revaluation adjustmentsto money market funds (MMFs), removing from the MMFs anyrequirement to report the revaluation adjustment.

▼B

2001R2423— EN— 04.01.2008 — 006.001— 6

7. NCBs may grant a derogation in respect of the frequency and thetimeliness of the reporting of price revaluations of securities and requirethese data on a quarterly basis and with the same timeliness as for stockdata reported on a quarterly basis, subject to compliance with thefollowing requirements:

— reporting agents shall provide the NCBs with the relevant infor-mation on valuation practices, including quantitative indications onthe percentage of their holdings of these instruments subject todifferent valuation methods,

— where a substantial price revaluation has occurred, NCBs shall beentitled to request reporting agents to provide additional informationrelating to the month in which the development took place.

8. In the event of a merger, a division or any other reorganisationthat might affect the fulfilment of its statistical obligations, the reportingagent involved shall inform the relevant NCB, once the intention toimplement such operation has become public and in due time beforethe merger, the division or the reorganisation takes effect, of theprocedures that are planned to fulfil the statistical reporting requirementsset out in this Regulation.

Article 5

Use of the reported statistical information for the purposes ofRegulation (EC) No 2818/98 (ECB/1998/15)

1. The statistical information reported by credit institutions inaccordance with this Regulation shall be used by each credit institutionto calculate its reserve base in accordance with Regulation (EC) No2818/98 of the European Central Bank of 1 December 1998 on theapplication of minimum reserves (ECB/1998/15) (1), as amended byRegulation (EC) No 1921/2000 (ECB/2000/8). In particular, eachcredit institution shall use this information to verify the fulfilment ofits reserve requirement over the maintenance period.

▼M3__________

▼B3. Specific and transitional provisions for the purposes of the appli-cation of the ESCB's minimum reserve system are set out in Annex II tothis Regulation. The specific provisions of this Annex shall prevail overprovisions laid down in Regulation (EC) No 2818/98 (ECB/1998/15).

Article 6

Verification and compulsory collection

The right to verify or to collect compulsorily the information whichreporting agents shall provide in compliance with the statisticalreporting requirements set out in this Regulation shall be exercised bythe NCBs, without prejudice to the right of the ECB to exercise theserights itself. This right shall be exercised in particular when an insti-tution included in the actual reporting population does not fulfil theminimum standards for transmission, accuracy, conceptual complianceand revisions as set out in Annex IV to this Regulation.

▼B

2001R2423— EN— 04.01.2008 — 006.001— 7

(1) OJ L 356, 30.12.1998, p. 1.

Article 7

Transitional provisions

Transitional provisions for application of parts to this Regulation arelaid down in Annex V to this Regulation.

Article 8

Repeal

▼M11. Regulation (EC) No 2819/98 (ECB/1998/16) shall be repealed on1 January 2003.

▼B2. References made to the repealed Regulation shall be construed asbeing made to this Regulation.

▼M1

Article 9

This Regulation shall enter into force on 1 January 2003.

▼B

2001R2423— EN— 04.01.2008 — 006.001— 8

ANNEX I

STATISTICAL REPORTING REQUIREMENTS AND CLASSIFICATIONPRINCIPLES

PART 1

Monetary financial institutions and statistical reporting requirements

Introduction

The requirement is to produce on a regular basis a properly articulated conso-lidated balance sheet of the money-creating financial intermediaries for the parti-cipating Member States, seen as one economic territory, in terms of stocks andflows, based on a complete and homogeneous monetary sector and reportingpopulation.

The statistical system for the participating Member States covering the conso-lidated balance sheet of the monetary financial institution (MFI) sector thereforecomprises the two following main elements:

— a list of MFIs for statistical purposes, and

— a specification of the statistical information reported by these MFIs atmonthly and quarterly frequency.

▼M2For the purpose of obtaining complete information on the MFIs' balance sheets, itis necessary to impose certain reporting requirements on other financial interme-diaries except insurance corporations and pension funds (hereinafter referred to as‘OFIs’), when acting in the context of financial activities involving MMF shares/units.

This statistical information is collected by the national central banks (NCBs)from the MFIs and from OFIs, within the limits set out in Section I(6),according to national arrangements relying on the harmonised definitions andclassifications set out in this Annex.

▼BI. Monetary financial institutions

1. The European Central Bank (ECB) establishes and updates on a regular basisthe list of MFIs for statistical purposes in accordance with the classificationprinciples outlined below. One important aspect is financial innovation,which itself is affected by the development of the single market and themove to economic and monetary union, both of which affect the character-istics of financial instruments and induce financial institutions to change thefocus of their business. Procedures for monitoring and continuous checkingensure that the list of MFIs remains up to date, accurate, and as homogeneousas possible and sufficiently stable for statistical purposes. The list of MFIs forstatistical purposes includes an entry on whether or not institutions are legallysubject to the European System of Central Banks (ESCB) minimum reservesystem.

2. Thus, in accordance with the definition set out in Article 2(1) of this Regu-lation, the MFI sector comprises, in addition to central banks, two broadgroups of resident financial institutions. These are credit institutions asdefined in Community law (‘an undertaking whose business is to receivedeposits or other repayable funds from the public (1) and to grant creditsfor its own account; or an electronic money institution within the meaningof Directive 2000/46/EC of the European Parliament and of the Council of 18September 2000 on the taking up, pursuit and prudential supervision of thebusiness of electronic money institutions’) (OJ L 275, 27.10.2000, p. 39) (2)and other MFIs, i.e. other resident financial institutions which fulfil the MFIdefinition, irrespective of the nature of their business. The degree of substi-tutability between the instruments issued by the latter and the deposits placedwith credit institutions determines their classification, provided that they meetthe MFI definition in other respects.

▼B

2001R2423— EN— 04.01.2008 — 006.001— 9

(1) Including the proceeds arising from the sale of bank bonds to the public.(2) Article 1 of Directive 2000/12/EC of the European Parliament and the Council of 20

March 2000 relating to the taking up and pursuit of the business of credit institutions (OJL 126, 26.5.2000, p. 1), as amended by Directive 2000/28/EC (OJ L 275, 27.10.2000,p. 37), and as it may be amended from time to time.

3. It is noted that Directive 2000/12/EC partially excludes some entities from itsapplication. These exempted entities shall fall under the application of thisRegulation, provided that they meet the MFI definition.

4. Substitutability for deposits in relation to financial instruments issued byfinancial intermediaries other than credit institutions is determined by theirliquidity, combining characteristics of transferability, convertibility, certaintyand marketability, and having regard, where appropriate, to their term ofissue.

►M6 These criteria for the substitutability of deposits are also applied todetermine whether liabilities should be classified as deposits, unless there is aseparate category for such liabilities. ◄

5. ►M6 For the purposes both of determining substitutability of deposits inaccordance with the previous paragraph and classifying liabilities asdeposits: ◄

— transferability refers to the possibility of mobilising funds placed in afinancial instrument by using payment facilities, such as cheques, transferorders, direct debits or similar means,

— convertibility refers to the possibility and the cost of converting financialinstruments into currency or transferable deposits; the loss of fiscaladvantages in such conversion may be considered to be a kind ofpenalty that reduces the degree of liquidity,

— certainty means knowing precisely in advance the capital value of afinancial instrument in terms of national currency, and

— securities quoted and traded regularly on an organised market areconsidered to be marketable. For shares in open-end collective investmentundertakings, there is no market in the usual sense. Nevertheless,investors know the daily quotation of the shares and can withdrawfunds at this price.

6. In the case of collective investment undertakings (CIUs), money market funds(MMFs) fulfil the agreed conditions for liquidity and are therefore included inthe MFI sector. MMFs are defined as those CIUs of which the units are, interms of liquidity, close substitutes for deposits and which primarily invest inmoney market instruments and/or in MMF shares/units and/or in other trans-ferable debt instruments with a residual maturity of up to and including oneyear, and/or in bank deposits, and/or which pursue a rate of return thatapproaches the interest rates of money market instruments. The criteriaapplied in order to identify MMFs shall be derived from the publicprospectus as well as fund rules, instruments of incorporation, establishedstatutes or by-laws, subscription documents or investment contracts,marketing documents, or any other statement with similar effects, of theCIUs. ►M2 The MMF itself or the persons legally representing it ensuresthe provision of any information required to meet the statistical reportingrequirements of MMFs. Where necessary for practical reasons, the datamay be effectively submitted by any of the entities that act in the contextof financial activities involving MMF shares/units, such as depositories. ◄

7. For the purpose of defining MMFs in paragraph 6:

— CIUs shall mean undertakings the sole object of which is the collectiveinvestment of capital raised from the public and the units of which are, atthe request of the holders, repurchased or redeemed directly or indirectlyout of the undertaking's assets. Such undertakings may be constitutedaccording to law, either under the law of contract (as common fundsmanaged by management companies), or trust law (as unit trusts) orunder a statute (as investment companies),

— bank deposits shall mean cash deposits made with credit institutions,repayable on demand or upon prior notice of up to three months, or atagreed maturities of up to two years, inclusive of sums paid to creditinstitutions in respect of a transfer of securities under repurchaseoperations or securities loans,

— close substitutability for deposits in terms of liquidity shall mean theability of units of CIUs, under normal market circumstances, to berepurchased, redeemed or transferred, at the request of the holder,where the liquidity of the units is comparable to the liquidity of deposits,

— primarily shall be deemed to be at least 85 % of the investment portfolio,

▼B

2001R2423— EN — 04.01.2008 — 006.001— 10

— money market instruments shall mean those classes of transferable debtinstruments which are normally traded on the money market (for example,certificates of deposit, commercial paper and banker's acceptances,treasury and local authority bills) because of the following features:

(i) liquidity, where they can be repurchased, redeemed or sold at limitedcost, in terms of low fees and narrow bid/offer spread, and with veryshort settlement delay; and

(ii) market depth, where they are traded on a market which is able toabsorb a large volume of transactions, with such trading of largeamounts having a limited impact on their price; and

(iii) certainty in value, where their value can be accurately determined atany time or at least once a month; and

(iv) low interest risk, where they have a residual maturity of up to andincluding one year, or regular yield adjustments in line with moneymarket conditions at least every 12 months; and

(v) low credit risk, where such instruments are either:

— admitted to an official listing on a stock exchange or traded onother regulated markets which operate regularly, are recognisedand are open to the public, or

— issued under regulations aimed at protecting investors andsavings, or

— issued by:

— a central, regional or local authority, a central bank of aMember State, the European Union, the ECB, the EuropeanInvestment Bank, a non-Member State or, if the latter is afederal State, by one of the members making up thefederation, or by a public international body to which oneor more Member States belong,

or

— an establishment subject to prudential supervision, inaccordance with criteria defined by Community law or byan establishment which is subject to and complies withprudential rules considered by the competent authorities tobe at least as stringent as those laid down by Communitylaw, or guaranteed by any such establishment,

or

— an undertaking the securities of which have been admitted toan official listing on a stock exchange or are traded on otherregulated markets which operate regularly, are recognised andare open to the public.

8. In the European System of Accounts (ESA 95), financial institutions clas-sified as MFIs are categorised in two subsectors, namely central banks(S.121) (1) and other MFIs (S.122).

▼M29. For the purposes of this Regulation:

— ‘MMF registered shares/units’ shall mean MMF shares/units in respect ofwhich, in accordance with national legislation, a record is kept identifyingthe holders of its shares/units, including information on the residency ofthe holder,

— ‘MMF bearer shares/units’ shall mean MMF shares/units in respect ofwhich, in accordance with national legislation, a record is not kept iden-tifying the holders of its shares/units, or in respect of which a record iskept which does not contain information on the residency of the holder.

▼M4II. Accounting rules

Unless otherwise provided for in this Regulation, the accounting rules followedby MFIs for the purposes of reporting under this Regulation are those laid downin the national transposition of Council Directive 86/635/EEC of 8 December1986 on the annual accounts and consolidated accounts of banks and other

▼B

2001R2423— EN— 04.01.2008 — 006.001 — 11

(1) This and subsequent references are to sectors and subsectors in the ESA 95.

financial institutions (1) , as well as in any other international standardsapplicable. Without prejudice to accounting practices and netting arrangementsprevailing in Member States, all financial assets and liabilities are reported on agross basis for statistical purposes.

▼BIII. The consolidated balance sheet on a monthly basis: stocks

Objective

1. The objective is to supply monthly data on the business of MFIs in termsof stocks. Data are supplied in sufficient detail in order to provide the ECBwith a comprehensive statistical picture of monetary developments in theparticipating Member States seen as one economic territory and to allowflexibility in the calculation of monetary aggregates and counterpartscovering this territory. Moreover, the monthly individual stock datareported by the credit institutions subject to the ESCB minimum reservessystem are used for the calculation of the reserve base of the said creditinstitutions in accordance with Regulation (EC) No 2818/98 of theEuropean Central Bank of 1 December 1998 on the application ofminimum reserves (ECB/1998/15) (2), as amended by Regulation (EC)No 1921/2000 (ECB/2000/8) (3). The monthly reporting requirements inrespect of the stocks are shown in Table 1 below. Cells with thinborders (4) are reported solely by credit institutions subject to reserverequirements (for full details, see Annex II); this reporting is mandatoryexcept for the reporting of deposits redeemable at notice over two yearswhich remains voluntary until further notice. A detailed definition ofinstruments is presented in Part 3 of this Annex.

Requirements

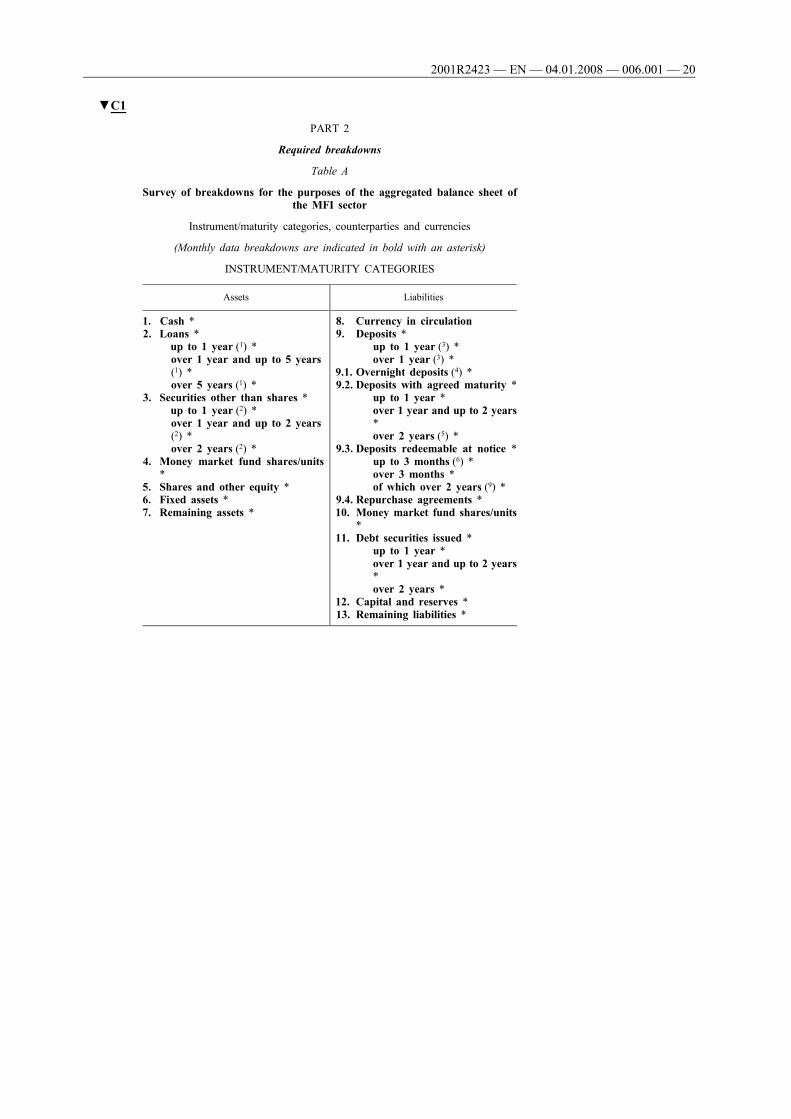

2. The ECB compiles the monetary aggregates for the territory of the parti-cipating Member States as amounts outstanding (stocks). The money stockincludes notes and coins in circulation and other monetary liabilities(deposits and other financial instruments which are close substitutes fordeposits) of MFIs. The counterparts to the money stock comprise allother items in the MFI balance sheet. The ECB also compiles flowsderived from the stocks and from other data, including data reported byMFIs (see section V below).

3. The ECB requires the statistical information to be broken down in terms ofinstrument/maturity categories, currencies and counterparties. Since separaterequirements apply to liabilities and assets, the two sides of the MFIbalance sheet are considered in turn. They are shown in Table A, in Part2 of this Annex.

(i) I n s t r u m e n t a n d m a t u r i t y c a t e g o r i e s

(a) Liabilities

4. The compilation of monetary aggregates covering the participating MemberStates requires relevant instrument categories. These are currency in circu-lation, deposit liabilities, MMF shares/units issued, debt securities issued,capital and reserves and remaining liabilities. In order to separate monetaryand non-monetary liabilities, deposit liabilities are also broken down intoovernight deposits, deposits with agreed maturity, deposits redeemable atnotice and repurchase agreements (repos).

5. Original maturity cut-offs provide a substitute for instrument detail wherefinancial instruments are not fully comparable between markets. The cut-offpoints for the maturity bands (or for periods of notice) are: for depositswith agreed maturity, at one-year and two-years' maturity at issue; and fordeposits redeemable at notice, at three-months' notice and at two-years'notice. Repos are not broken down by maturity as these are usually veryshort-term instruments (usually less than three-months' maturity at issue).Debt securities issued by MFIs are broken down at one year and two years.No maturity breakdown is required for shares/units issued by MMFs.

▼M4

2001R2423— EN — 04.01.2008 — 006.001— 12

(1) OJ L 372, 31.12.1986, p. 1.(2) OJ L 356, 30.12.1998, p. 1.(3) OJ L 229, 9.9.2000, p. 34.(4) Credit institutions may report positions vis-à-vis ‘MFIs other than credit institutions

subject to minimum reserves, ECB and NCBs’ rather than vis-à-vis ‘MFIs’ and ‘creditinstitutions subject to minimum reserves, ECB and NCBs’, provided that no loss of detailis implied and no bold printed positions are affected.

(b) Assets

6. MFI holdings of assets are broken down into cash, loans, securities otherthan shares, MMF shares/units, shares and other equity, fixed assets andremaining assets. A maturity breakdown by original maturity (at one yearand five year maturity bands) is required for MFI loans to residents (otherthan MFIs and general government) of the participating Member States bysubsector and further for MFI loans to households by purpose. A maturitybreakdown is also required for MFI holdings of debt securities issued byother MFIs located in the participating Member States. These holdings mustbe broken down into one and two year maturity bands to enable the inter-MFI holdings of this instrument to be netted off in the calculation of themonetary aggregates.

(ii) C u r r e n c i e s

7. The ECB shall have the option of defining monetary aggregates in such away as to include balances denominated in all currencies combined or ineuro alone. Balances in euro are therefore identified separately in thereporting scheme in respect of those balance sheet items that may beused in the compilation of monetary aggregates.

(iii) C o u n t e r p a r t i e s

8. The compilation of monetary aggregates and counterparts covering theparticipating Member States requires the identification of those counter-parties located in the territory of the participating Member States thatform the money-holding sector. Counterparties located in the domesticterritory and in the other participating Member States are identified sepa-rately and treated in exactly the same way in all statistical breakdowns.There is no requirement for a geographical breakdown of counterpartieslocated outside the territory of the participating Member States in monthlydata.

9. Counterparties located in the territory of the participating Member Statesare identified according to their domestic sector or institutional classifi-cation in accordance with the list of MFIs for statistical purposes and theguidance for the statistical classification of customers provided in the ECB'sMoney and Banking Statistics Sector Manual (‘Guidance for the statisticalclassification of customers’), which follows classification principles that areconsistent with the ESA 95 as far as possible. In order to allow for theidentification of a money-holding sector of the participating Member States,non-MFI counterparties are divided into general government (S.13), withcentral government (S.1311) identified separately in total deposit liabilities,and other resident sectors. In order to calculate a monthly sector disaggre-gation of the monetary aggregates and credit counterpart, other residentsectors are further broken down by the following subsectors: otherfinancial intermediaries + financial auxiliaries (S.123 + S.124), insurancecorporations and pension funds (S.125), non-financial corporations (S.11)and households + non-profit institutions serving households (S.14 + S.15).With respect to total deposit liabilities and the deposit categories ‘depositsover two years agreed maturity’, ‘deposits redeemable at notice over twoyears’ and ‘repos’, an additional distinction is made between credit insti-tutions, other MFI counterparties and central government for the purposesof the ESCB's minimum reserve system.

(iv) P u r p o s e o f l o a n s

10. Loans to households (including non-profit institutions serving households)are broken down by type of loan (consumer credit; lending for housepurchase; other). A detailed definition of consumer and housing loans iscontained in Part 3 of this Annex, within ‘Detailed description ofinstrument categories of the monthly aggregated balance sheet of theMFI sector’, under category 2: ‘Loans’.

(v) C r o s s - r e l a t i n g i n s t r u m e n t a n d m a t u r i t y c a t e g o r i e sw i t h c u r r e n c i e s a n d c o u n t e r p a r t i e s

11. The compilation of monetary statistics covering the participating MemberStates and the data needed for the calculation of the reserve base of creditinstitutions subject to the ESCB's minimum reserve system necessitatescertain cross-relationships being made in the balance sheet betweeninstrument/maturity/currency and counterparties and, in addition, for loansto households, a further breakdown by purpose.

12. The data requirements are most detailed where the counterparties are part ofthe money-holding sector. Statistical information on deposit liabilities by

▼B

2001R2423— EN — 04.01.2008 — 006.001— 13

subsector and maturity classified further by currency is necessary to permita closer analysis of the developments of the foreign currency componentsincluded in M3. In particular, a currency analysis of these componentsfacilitates investigations concerning the degree of substitutability betweenforeign currency and euro denominated components of M3. Breakdowns ofthe positions vis-à-vis other MFIs are identified only in so far as this isnecessary to allow for netting of inter-MFI balances or to calculate thereserve base.

13. Positions vis-à-vis the rest of the world are required for ‘deposits over twoyears agreed maturity’, ‘deposits redeemable at notice over two years’ and‘repos’ in order to calculate the reserve base subject to the positive reserveratio and for total deposit liabilities in order to compile the external coun-terparts. In addition, for balance of payments (b.o.p.) and financial accountspurposes, deposit liabilities and loans vis-à-vis the rest of the world arebroken down at one year original maturity.

▼M2(vi) R e s i d e n c y o f t h e h o l d e r s o f MM F s h a r e s / u n i t s

13a. Reporting agents report, on a monthly basis, as a minimum data on theresidency of the holders of MMF shares/units issued by MFIs of the parti-cipating Member States according to a domestic/other participating MemberStates/rest of the world breakdown. This will enable NCBs to provide theECB with data on the residency of the holders of this instrument and allowthe exclusion of holdings of non-residents of the participating MemberStates for the purposes of the compilation of monetary aggregates.

13b. In accordance with Article 4(4), NCBs may require data on additionalbreakdowns not covered in the requirements of this Regulation, includingbreakdowns by counterparty sector, currency or maturity.

13c. As regards registered shares/units, issuing MMFs or the persons legallyrepresenting them or the entities referred to in Annex I(1)(I)(6) reportdata on the residency breakdown of the holders of their shares/unitsissued in the monthly balance sheet.

13d. As regards bearer shares/units, reporting agents report data on the residencybreakdown of the holders of MMF shares/units according to the approachdecided by the relevant NCB in agreement with the ECB. This requirementis limited to one or a combination of the following options, to be adoptedhaving regard to the organisation of the relevant markets and the nationallegal arrangements in the Member State(s) in question. This will be peri-odically monitored by the NCB and the ECB.

(a) Issuing MMFs

Issuing MMFs or the persons legally representing them or the entitiesreferred to in Annex I(1)(I)(6) report data on the residency breakdown ofthe holders of their shares/units issued. If an issuing MMF is not in aposition to identify directly the residency of the holder, it reports therelevant data on the basis of available information. Such information maycome from the agent distributing the shares/units or from any other entityinvolved in the issuance, buy-back or transfer of the shares/units.

(b) MFIs and OFIs as custodians of MMF shares/units

As reporting agents, MFIs and OFIs acting as custodians of MMF shares/units report data on the residency breakdown of the holders of shares/unitsissued by resident MMFs and held in custody on behalf of the holder or ofanother intermediary also acting as a custodian. This option is applicable ifthe following conditions are met. First, the custodian distinguishes MMFshares/units kept in custody on behalf of holders from those that are kepton behalf of other custodians. Second, most of the MMF shares/units are inthe custody of domestic resident institutions that are classified as financialintermediaries (MFIs or OFIs).

(c) MFIs and OFIs as reporters of transactions of residents with non-residents involving shares/units of a resident MMF

As reporting agents, MFIs and OFIs acting as reporters of transactions ofresidents with non-residents involving shares/units of a resident MMFreport data on the residency breakdown of the holders of shares/unitsissued by resident MMFs, which they trade on behalf of the holder oranother intermediary also involved in the transaction. This option isapplicable if the following conditions are met. First, the reportingcoverage is comprehensive, i.e. it covers substantially all of the transactions

▼B

2001R2423— EN — 04.01.2008 — 006.001— 14

carried out by the reporting agents. Second, accurate data on purchases andsales with non-residents of the participating Member States are provided.Third, differences between issuing value and redemption value, excludingfees, of the same shares/units are minimal. Fourth, the amount of shares/units held by non-residents of the participating Member States issued byresident MMFs is low. If the reporting agent is not in a position to identifydirectly the residency of the holder, it reports the relevant data on the basisof available information.

13e. If registered shares/units or bearer shares/units are issued for the first timeor if market developments require a change of option or combination ofoptions, NCBs may grant derogations for one year in respect of therequirements set out in paragraphs 13c and d.

▼BTimeliness

14. The ECB receives an aggregated monthly balance sheet covering thepositions of MFIs in each participating Member State by close ofbusiness on the 15th working day following the end of the month towhich the data relate. NCBs decide when they need to receive data fromreporting agents in order to meet this deadline, taking into account therequired timeliness for the ESCB's minimum reserve system.

▼M4Statistical valuation of deposit liabilities and loans

15. Deposit liabilities and loans are reported, for the purposes of this Regu-lation, at the nominal amount outstanding at the end of the month and on agross basis. Nominal amount means the amount of principal that a debtor iscontractually obliged to repay to a creditor.

16. NCBs may allow the reporting of provisioned loans net of provisions andthe reporting of purchased loans at the price agreed at the time of theiracquisition, provided that such reporting practices are applied by allresident reporting agents and are necessary to maintain continuity in thestatistical valuation of loans with the data reported for periods prior toJanuary 2005.

▼BIV. Balance sheet statistics at quarterly frequency (stocks)

Objective

1. Certain data are needed for the further analysis of monetary developmentsand to serve other statistical purposes such as financial accounts andbalance of payments. The objective is to provide further details oncertain items of the balance sheet for these purposes.

Requirements

2. The quarterly breakdowns are provided only in respect of key items of theaggregated balance sheet. Furthermore, the ECB may allow some flexibilityin calculating aggregates where it can be shown from figures collected at ahigher level of aggregation that the data involved are unlikely to besignificant.

(a) S u b s e c t o r a n d m a t u r i t y b r e a k d o w n o f c r e d i t t on o n - M F I s o f t h e p a r t i c i p a t i n g M e m b e r S t a t e s

3. In order to enable the complete subsector and maturity structure of MFIs'overall credit financing (loans and securities) vis-à-vis the money-holdingsector to be monitored, loans to general government other than centralgovernment are to be broken down quarterly at one year and five yearoriginal maturity and holdings of securities issued by general governmentother than central government at one year original maturity, all cross-relatedto a subsector breakdown (state government (S.1312), local government(S.1313) and social security funds (S.1314)). A cross-related breakdownby subsector with a maturity split, up to one year and more than one year,of holdings of securities other than shares issued by residents other thanMFIs and general government is also required. A breakdown of MFIholdings of shares and other equity by subsector is required vis-à-vis thefollowing subsectors: other financial intermediaries + financial auxiliaries(S.123 + S.124), insurance corporations and pension funds (S.125) andnon-financial corporations (S.11).

4. Total amounts of MFI loans and MFI holdings of securities other thanshares vis-à-vis the central government (S.1311) are also required.

▼M2

2001R2423— EN — 04.01.2008 — 006.001— 15

(b) S u b s e c t o r b r e a k d o w n o f M F I d e p o s i t l i a b i l i t i e s t ot h e g e n e r a l g o v e r n m e n t ( o t h e r t h a n c e n t r a lg o v e r n m e n t ) o f t h e p a r t i c i p a t i n g M e m b e r S t a t e s

5. The deposit liability categories vis-à-vis general government other thancentral government in the participating Member States are broken downinto the state government (S.1312), local government (S.1313) and socialsecurity funds (S.1314).

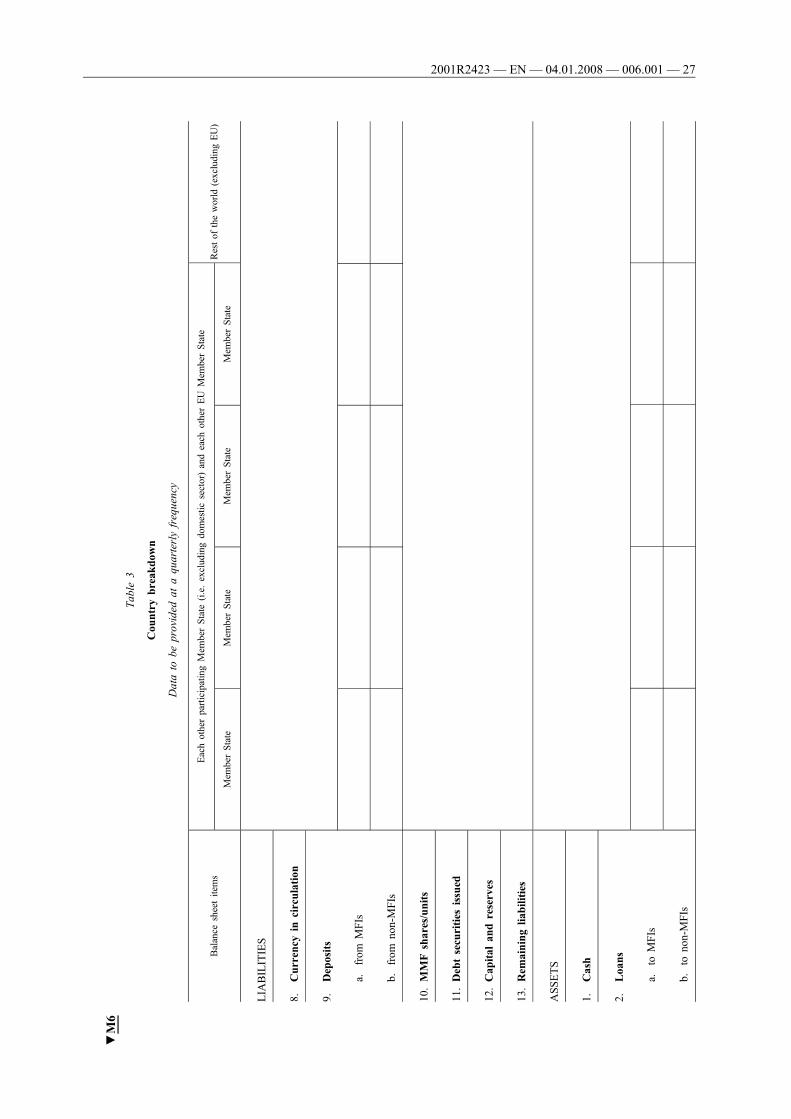

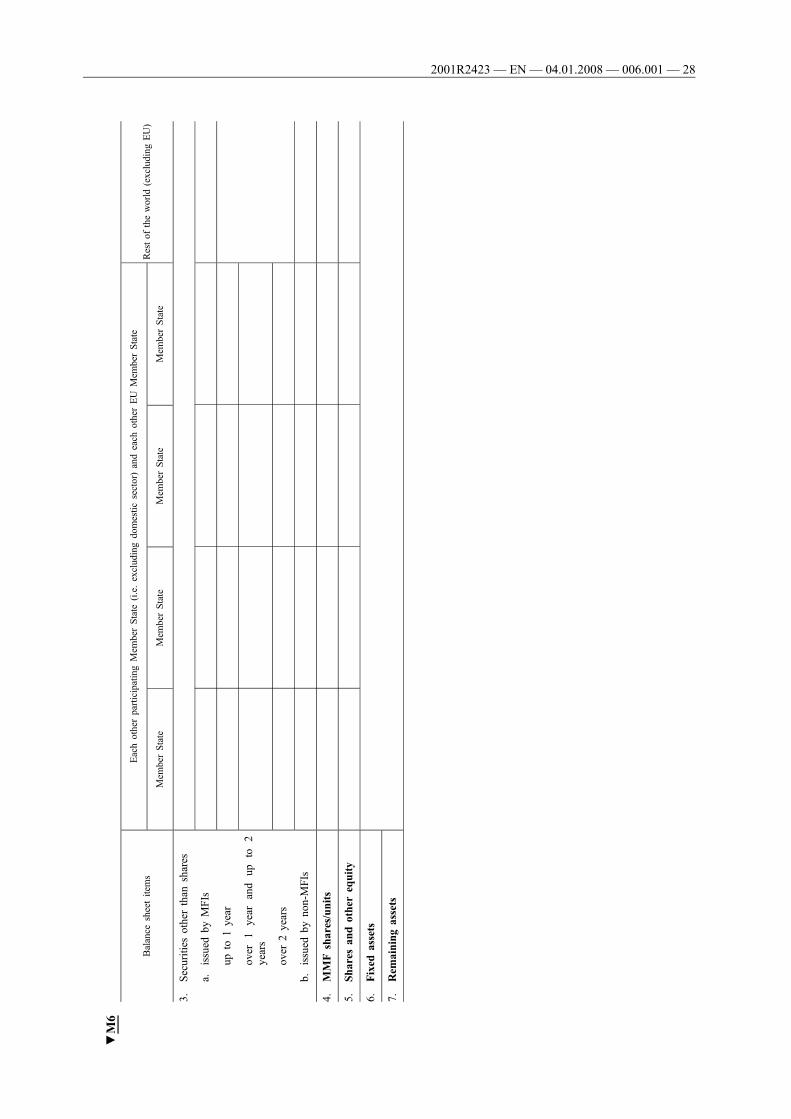

(c) C o u n t r y b r e a k d o w n

6. Counterparties by Member State are identified to analyse further monetarydevelopments and also for the purposes of the transitional requirements andfor data quality checks. In order to provide better information on theholdings of debt securities by issuing country included in the monetaryaggregates, the maturity breakdown is required at one and two yearmaturity bands.

▼M66a. In the event that any country accedes to the EU after 31 December 2007,

reporting agents must thereafter report positions vis-à-vis counterpartiesresident in that new Member State in accordance with Table 3 of Part 2.

If figures collected at a higher level of aggregation show that positions vis-à-vis counterparties resident in any Member State that has not adopted theeuro are insignificant, an NCB may decide not to require reporting inrelation to such Member State. The NCB shall inform its reportingagents of any such decision.

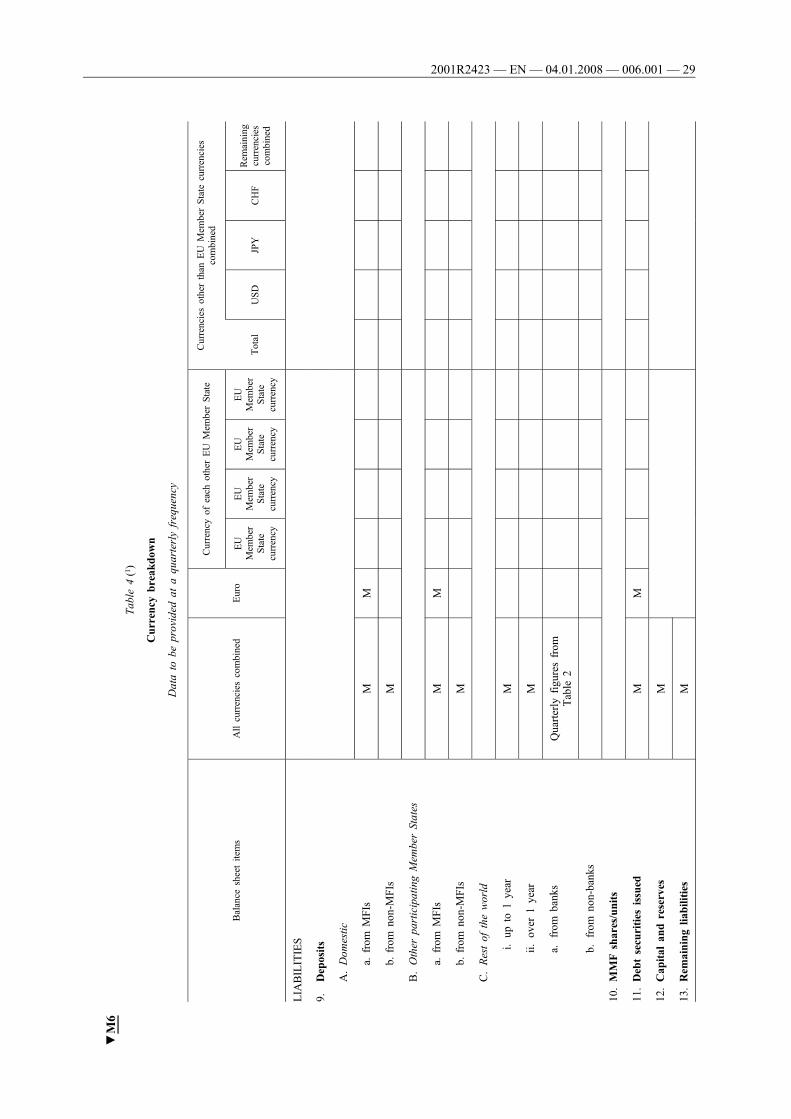

▼B(d) C u r r e n c y b r e a k d o w n

7. The key balance sheet items are broken down into the currencies of thenon-participating Member States and into the major international currencies(the US dollar, the yen and the Swiss franc). These breakdowns arerequired in order to permit the calculation of flow statistics for monetaryaggregates and counterparts adjusted for exchange rate changes where theseaggregates are defined in such a way as to include all currencies combined.For b.o.p. and financial account purposes, the currency breakdown fordeposit liabilities and loans vis-à-vis the rest of the world is providedwith a maturity breakdown at one-year original maturity.

▼M67a. In the event that any Member State adopts the euro after 31 December

2007, reporting agents must thereafter report positions vis-à-vis thecurrency of that new participating Member State in accordance withTable 4 of Part 2.

In such cases, the column in Table 4 of Part 2 corresponding to the formercurrency of the new participating Member State is no longer applicable.

In the event that any country accedes to the EU after 31 December 2007,reporting agents must thereafter report positions vis-à-vis the currency ofthat new Member State in accordance with Table 4 of Part 2.

If figures collected at a higher level of aggregation show that positions vis-à-vis the currency of a Member State that has not adopted the euro areinsignificant, an NCB may decide not to require reporting in relation tosuch Member State. The NCB shall inform its reporting agents of any suchdecision.

▼B(e) S e c t o r b r e a k d o w n s o f p o s i t i o n s w i t h c o u n t e r -

p a r t i e s o u t s i d e t h e p a r t i c i p a t i n g M e m b e r S t a t e s( n o n - p a r t i c i p a t i n g M e m b e r S t a t e s a n d t h e r e s t o ft h e w o r l d )

8. For MFIs' positions vis-à-vis counterparties resident outside the territory ofthe participating Member States, positions with banks (or MFIs in non-participating Member States) and non-banks need to be distinguished; asregards non-banks, a distinction is needed between general government andother resident sectors. The sector classification in accordance with theSNA93 applies where the ESA 95 is not in force.

Timeliness

9. Quarterly statistics are transmitted by NCBs to the ECB by close ofbusiness on the 28th working day following the end of the month to

▼B

2001R2423— EN — 04.01.2008 — 006.001— 16

which they relate. NCBs decide when they need to receive data fromreporting agents in order to meet this deadline.

▼M69a. Where positions in respect of cells corresponding to Member States that

have not adopted the euro are insignificant but NCBs nevertheless collectthem, these may be transmitted by the NCBs to the ECB with a delay of afurther one month from the close of business on the 28th working dayfollowing the end of the quarter to which the positions relate. The NCBsmay decide when they need to receive data from reporting agents in orderto meet this deadline.

▼M4Statistical valuation of deposit liabilities and loans

10. Deposit liabilities and loans are reported according to the rules set out formonthly stocks in paragraphs 15 and 16 of section III.

▼BV. Compilation of flows statistics

Objective

1. In order to compile flow statistics in respect of the monetary aggregates andcounterparts, data on the value of transactions need to be derived in atimely manner from the consolidated balance sheet in terms of stocks,which provides information on outstanding assets and liabilities, and addi-tional statistical information relating to reclassifications, exchange ratechanges, other valuation changes and certain other adjustments such aswrite-offs of loans.

Requirements

2. Financial transactions are identified as the difference between stockpositions at end-month reporting dates, from which the effect of changesthat arise due to influences other than transactions is removed. For thispurpose, the ECB requires statistical information on these influencesrelating to many items of the MFI balance sheet. The information takesthe form of adjustments that cover ‘reclassifications and other adjustments’,exchange rate adjustments and ‘revaluations and loan write-offs/write-downs’. In addition, the ECB requires explanatory information on theadjustments in ‘reclassifications and other adjustments’.

3. The statistical requirement addressed to the actual reporting populationunder this Regulation concerns exclusively the ‘revaluation adjustments’,covering both the write-offs/write-downs of loans and price revaluations inrespect of holdings of securities in the reference period.

4. Reporting agents are subject to a reporting requirement formed by the‘minimum requirements’ identified in Table 1A in Part 2 of this Annex.The ‘minimum requirements’ are considered as the minimum required inorder to compile and estimate adjustments in respect of the full set of datarequired by the ECB. NCBs are permitted to collect additional data notcovered by the ‘minimum requirements’. These additional data may refer tothe breakdowns marked in Table 1A other than the ‘minimumrequirements’.

5. The requirement addressed to the reporting agents does not cover theexchange rate changes and the reclassification adjustment. The ECBcalculates the monthly exchange rate adjustment from currency-by-currency stock data supplied by the reporting agents. These data aresupplied on a quarterly basis in accordance with Table 4 in Part 2 ofthis Annex. The reclassifications mentioned in paragraph 1 are alsoexcluded because these data are collected by the NCBs themselves usingvarious information sources that are already available to the NCBs.

Write-offs / write-downs of loans

6. The adjustment in respect of the write-offs/write-downs is reported in orderto remove from the flows statistics the impact of changes in the value ofloans recorded on the balance sheet that are caused by the application ofwrite-off/write down of loans. It should also reflect the changes inprovisions on loans if an NCB decides that outstanding stocks should berecorded net of provisions. Write-offs/write-downs recognised at the timethe loan is sold or transferred to a third party are also included, whereidentifiable.

▼B

2001R2423— EN — 04.01.2008 — 006.001— 17

(i) I n s t r u m e n t a n d m a t u r i t y c a t e g o r i e s

7. Write-offs/write-downs refer to the asset item ‘loans’. A maturitybreakdown is not required as part of the ‘minimum requirements’. NCBsmay however require reporting agents to submit additional data accordingto the maturity breakdown outlined for the monthly stock data.

(ii) C u r r e n c i e s

8. A breakdown of the ‘revaluation adjustment’ according to the currency(euro/non-euro) of the loans is not included in the ‘minimum requirements’;whereas NCBs may, however, require a currency breakdown.

(iii) C o u n t e r p a r t i e s

9. The ‘minimum requirements’ include the separate identification of amountswritten-off/written-down, and changes in provisions where loans arereported net of provisions, according to the geographical location of thecounterparties. In addition, counterparties located in the participatingMember States are classified according to their institutional sector, withseparate data for MFIs and ‘other resident sector’ and the latter with afurther breakdown by subsector i.e. other financial intermediaries +financial auxiliaries (S.123 + S.124), insurance corporations and pensionfunds (S.125), non-financial corporations (S.11) and households + non-profit institutions serving households (S.14 + S.15). Furthermore, thehousehold sector is reported with an additional breakdown according tothe purpose of the loan, i.e. consumer credit, lending for house purchaseand other (residual). Total amounts are reported in respect of the loans tothe rest of the world, without any additional breakdown.

(iv) T i m e l i n e s s

10. The ECB shall receive aggregated ‘revaluation adjustments’ in respect ofloan write-offs/write-downs corresponding to the loans granted by thereporting agents in each participating Member State by close of businesson the 15th working day following the end of the month to which the datarelate. NCBs decide when they need to receive data from reporting agentsin order to meet this deadline.

Price revaluation of securities

▼M411. The adjustment in respect of the price revaluation of securities refers to

fluctuations in the valuation of securities that arise because of a change inthe price at which securities are recorded or traded. The adjustmentincludes the changes that occur over time in the value of end-periodbalance sheet stocks because of changes in the reference value at whichsecurities are recorded, i.e. potential gains/losses. It may also containvaluation changes that arise from transactions in securities i.e. realisedgains/losses.

▼B(i) I n s t r u m e n t a n d m a t u r i t y c a t e g o r i e s

(a) Liabilities

▼M412. No minimum reporting requirement is established for the liability side of

the balance sheet. However, if valuation practices applied by reportingagents to debt securities issued result in changes to their end-periodstocks, NCBs are permitted to collect data relating to such changes. Suchdata are reported as ‘other revaluation’ adjustments.

▼B(b) Assets

13. The price revaluation adjustment is collected from MFIs in respect of theitems ‘securities other than shares’ and ‘shares and other equity’. The‘minimum requirements’ refer to ‘securities other than shares’ withoriginal maturity over two years. Nevertheless, NCBs may extend therequirement beyond the ‘minimum requirements’, by requiring thereporting of the same currency and maturity breakdowns as for monthlystock data. In respect of the item ‘shares and other equity’, the ‘minimumrequirements’ refer to total amounts by sector and coincide with therequirement for stock data.

▼B

2001R2423— EN — 04.01.2008 — 006.001— 18

(ii) C u r r e n c i e s

14. A currency breakdown of the price revaluation is not required in ‘minimumrequirements’. NCBs may extend the requirement beyond the ‘minimumrequirements’ in respect of the currency breakdown (euro/non-euro).

(iii) C o u n t e r p a r t i e s

15. In respect of the price revaluation for the item ‘securities other than shares’,the ‘minimum requirements’ refer to the breakdown of the domesticresidents and residents of the other participating Member States bysector, i.e. MFIs, general government and other resident sector. Totalamounts of the adjustment are reported in respect of the rest of theworld. NCBs may extend the requirement to cover the same breakdownas for monthly stock data.

16. In respect of the price revaluation for ‘shares and other equity’, the‘minimum requirements’ refer to the breakdown of the domestic residentsand residents of the other participating Member States by sector i.e. MFIsand other resident sectors, and total amounts of the adjustment are reportedin respect of the rest of the world. In this case, the set of ‘minimumrequirements’ coincides with the set of data reported to the ECB by theNCB.

(iv) T i m e l i n e s s

17. The ECB receives the aggregated revaluation adjustments covering theprice revaluations of securities corresponding to the reporting agents ineach participating Member State by close of business on the 15thworking day following the end of the month to which the data relate.NCBs decide when they need to receive data from reporting agents inorder to meet this deadline.

▼B

2001R2423— EN — 04.01.2008 — 006.001— 19

PART 2

Required breakdowns

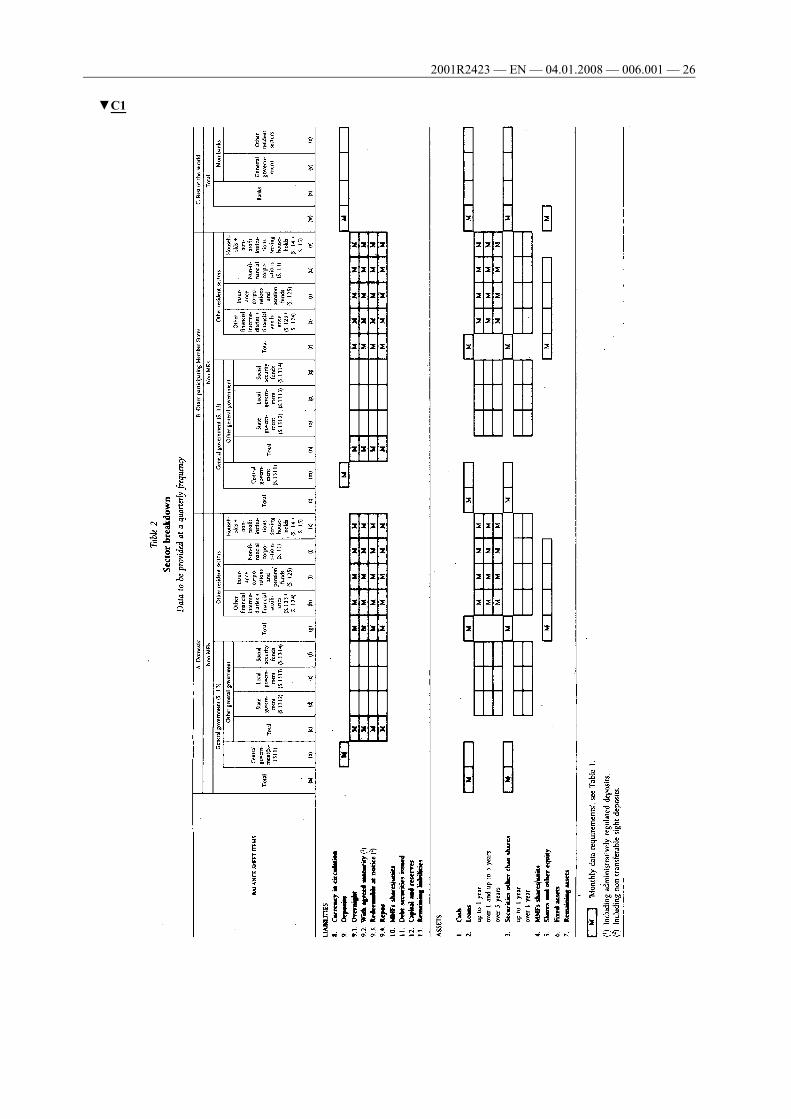

Table A

Survey of breakdowns for the purposes of the aggregated balance sheet ofthe MFI sector

Instrument/maturity categories, counterparties and currencies

(Monthly data breakdowns are indicated in bold with an asterisk)

INSTRUMENT/MATURITY CATEGORIES

Assets Liabilities

1. Cash *2. Loans *

up to 1 year (1) *over 1 year and up to 5 years(1) *over 5 years (1) *

3. Securities other than shares *up to 1 year (2) *over 1 year and up to 2 years(2) *over 2 years (2) *

4. Money market fund shares/units*

5. Shares and other equity *6. Fixed assets *7. Remaining assets *

8. Currency in circulation9. Deposits *

up to 1 year (3) *over 1 year (3) *

9.1. Overnight deposits (4) *9.2. Deposits with agreed maturity *

up to 1 year *over 1 year and up to 2 years*over 2 years (5) *

9.3. Deposits redeemable at notice *up to 3 months (6) *over 3 months *of which over 2 years (9) *

9.4. Repurchase agreements *10. Money market fund shares/units

*11. Debt securities issued *

up to 1 year *over 1 year and up to 2 years*over 2 years *

12. Capital and reserves *13. Remaining liabilities *

▼C1

2001R2423— EN — 04.01.2008 — 006.001— 20

COUNTERPARTIES

Assets Liabilities

A. Domestic residents *MFIs *Non-MFIs *

General government *central governmentstate governmentlocal governmentsocial security funds

Other resident sectors (10) *other financial interme-diaries, etc. (S. 123 + S.124) (7), (10) *insurance corporationsand pension funds (S.125) (10) *non-financialcorporations (S. 11)(10) *households, etc. (S. 14 +S. 15) (8), (10) *

B. Residents of the other partici-pating Member States *

MFIs *Non-MFIs *

General government *central governmentstate governmentlocal governmentsocial security funds

Other resident sectors (10) *other financial interme-diaries, etc. (S. 123 + S.124) (7) (10) *insurance corporationsand pension funds (S.125) (10) *non-financialcorporations (S. 11) (10)*households, etc. (S. 14 +S. 15) (8), (10) *

C. Residents of the rest of the world*

BanksNon-banks

general governmentother resident sectors

D. Not allocated

A. Domestic residents *MFIs *

of which: Credit institutions*

Non-MFIs *General government *

central government *state governmentlocal governmentsocial security funds

Other resident sectors (10) *other financial interme-diaries, etc. (S. 123 + S.124) (7), (10) *insurance corporationsand pension funds (S.125) (10) *non-financialcorporations (S. 11) (10) *households, etc. (S. 14 +S. 15) (8) (10) *

B. Residents of the other partici-pating Member States *MFIs *

of which: Credit institutions*

Non-MFIs *General government *

central government *state governmentlocal governmentsocial security funds

Other resident sectors (10) *other financial interme-diaries, etc. (S. 123 + S.124) (7), (10) *insurance corporationsand pension funds (S.125) (10) *non-financialcorporations (S. 11) (10) *households, etc. (S. 14 +S. 15) (8), (10) *

C. Residents of the rest of the world*BanksNon-banks

general governmentother resident sectors

D. Not allocated

▼C1

2001R2423— EN — 04.01.2008 — 006.001— 21

Currencies

e euro

x Foreign currencies Currencies other than the euro (i.e.other Member State currencies, USD,JPY, CHF, remaining currencies)

(1) Monthly maturity breakdown applicable only to loans to other resident sectors thanMFIs and general government of the participating Member States and the monthlymaturity breakdown at one year, for loans to the rest of the world. Quarterlymaturity breakdowns for loans to general government other than central governmentof the participating Member States.

(2) Monthly maturity breakdown relates only to holdings of securities issued by MFIslocated in the participating Member States. As quarterly data, holdings of securitiesissued by non-MFIs in the participating Member States are split into ‘up to one year’and ‘over one year’.

(3) Vis-à-vis the rest of the world only.(4) Including suspense balances representing amounts stored on prepaid cards issued in the

name of MFIs and other liabilities resulting from the issuance of electronic money.(5) Including administratively regulated deposits.(6) Including non-transferable sight deposits.(7) Other financial intermediaries (S. 123) + financial auxiliaries (S. 124)(8) Households (S. 14) + non-profit institutions serving households (S. 15).(9) The reporting of the item ‘deposits redeemable at notice over two years’ is voluntary

until further notice.(10) Monthly breakdown by subsector is required for loans and deposits.

▼C1

2001R2423— EN — 04.01.2008 — 006.001— 22

►(1) M2

►(2) C2

▼C1

2001R2423— EN — 04.01.2008 — 006.001— 23

▼C1

2001R2423— EN — 04.01.2008 — 006.001— 24

►(1) M2

▼C1

2001R2423— EN — 04.01.2008 — 006.001— 25

▼C1

2001R2423— EN — 04.01.2008 — 006.001— 26

2001R2423— EN — 04.01.2008 — 006.001— 27

Tab

le3

Cou

ntrybreak

dow

n

Datato

beprovided

ataqu

arterlyfrequency

Balance

sheetitems

EachotherparticipatingMem

berState

(i.e.exclud

ingdo

mestic

sector)andeach

otherEU

Mem

berState

Restof

theworld

(excluding

EU)

Mem

berState

Mem

berState

Mem

berState

Mem

berState

LIA

BILITIES

8.Currency

incirculation

9.Deposits

a.from

MFIs

b.from

non-MFIs

10.MMF

shares/units

11.Debtsecurities

issued

12.Cap

ital

andreserves

13.Rem

aininglia

bilities

ASSETS

1.Cash

2.Loa

ns

a.to

MFIs

b.to

non-MFIs

▼M6

2001R2423— EN — 04.01.2008 — 006.001— 28

Balance

sheetitems

EachotherparticipatingMem

berState

(i.e.exclud

ingdo

mestic

sector)andeach

otherEU

Mem

berState

Restof

theworld

(excluding

EU)

Mem

berState

Mem

berState

Mem

berState

Mem

berState

3.Securities

otherthan

shares

a.issued

byMFIs

upto

1year

over

1year

and

upto

2years

over

2years

b.issued

byno

n-MFIs

4.MMF

shares/units

5.Shares

andother

equity

6.Fixed

assets

7.Rem

ainingassets

▼M6

2001R2423— EN — 04.01.2008 — 006.001— 29

Tab

le4(1)

Currency

break

dow

n

Datato

beprovided

ataqu

arterlyfrequency

Balance

sheetitems

Allcurrencies

combined

Euro

Currencyof

each

otherEU

Mem

berState

Currenciesotherthan

EU

Mem

berState

currencies

combined

EU

Mem

ber

State

currency

EU

Mem

ber

State

currency

EU

Mem

ber

State

currency

EU

Mem

ber

State

currency

Total

USD

JPY

CHF

Rem

aining

currencies

combined

LIA

BILITIES

9.Deposits

A.Dom

estic

a.from

MFIs

MM

b.from

non-MFIs

M

B.Other

participatingMem

berStates

a.from

MFIs

MM

b.from

non-MFIs

M

C.Restof

theworld

i.up

to1year

M

ii.ov

er1year

M

a.from

bank

sQuarterly

figu

resfrom

Table

2

b.from

non-bank

s

10.MMF

shares/units

11.Debtsecurities

issued

MM

12.Cap

ital

andreserves

M

13.Rem

aininglia

bilities

M

▼M6

2001R2423— EN — 04.01.2008 — 006.001— 30

Balance

sheetitems

Allcurrencies

combined

Euro

Currencyof

each

otherEU

Mem

berState

Currenciesotherthan

EU

Mem

berState

currencies

combined

EU

Mem

ber

State

currency

EU

Mem

ber

State

currency

EU

Mem

ber

State

currency

EU

Mem

ber

State

currency

Total

USD

JPY

CHF

Rem

aining

currencies

combined

ASSETS

2.Loa

ns

A.Dom

estic

a.to

MFIs

M

b.to

non-MFIs

MM

B.Other

participatingMem

berStates

a.to

MFIs

M

b.to

non-MFIs

MM

C.Restof

theworld

i.up

to1year

M

ii.ov

er1year

M

a.to

bank

sQuarterly

figu

resfrom

Table

2

b.to

non-bank

s

3.Securities

other

than

shares

A.Dom

estic

a.issued

byMFIs

MM

b.issued

byno

n-MFIs

MM

▼M6

2001R2423— EN — 04.01.2008 — 006.001— 31

Balance

sheetitems

Allcurrencies

combined

Euro

Currencyof

each

otherEU

Mem

berState

Currenciesotherthan

EU

Mem

berState

currencies

combined

EU

Mem

ber

State

currency

EU

Mem

ber

State

currency

EU

Mem

ber

State

currency

EU

Mem

ber

State

currency

Total

USD

JPY

CHF

Rem

aining

currencies

combined

B.Other

participatingMem

berStates

a.issued

byMFIs

MM

b.issued

byno

n-MFIs

MM

C.Restof

theworld

a.issued

bybank

sQuarterly

figu

resfrom

Table

2

b.issued

byno

n-bank

s

4.MMF

shares/units

A.Dom

estic

M

B.Other

participatingMem

berStates

M

C.Restof

theworld

M

5.Shares

andother

equity

M

6.Fixed

assets

M

7.Rem

ainingassets

M

(1)

‘M’means

mon

thly

data

requ

irem

ents

(see

Table

1).

▼M6

▼C1

2001R2423— EN — 04.01.2008 — 006.001— 32

▼C1

2001R2423— EN — 04.01.2008 — 006.001— 33

PART 3

Definitions relating to the consolidated balance sheet to be submitted to theECB - instrument categories of liabilities and assets

General definitions

For the purpose of compiling the consolidated balance sheet of the MFI sectorcovering the participating Member States, the reporting population consists ofMFIs included in the list of MFIs for statistical purposes and resident in theterritory of the participating Member States (1). These are:

— institutions incorporated and located in the territory, including subsidiaries ofparent companies located outside that territory, and

— branches of institutions that have their head office outside that territory.

Subsidiaries are separate incorporated entities in which another entity has amajority or full participation, whereas branches are unincorporated entities(without independent legal status) totally owned by the parent.

MFIs consolidate for statistical purposes the business of all their offices(registered or head office and/or branches) located within the same nationalterritory. No consolidation for statistical purposes is permitted across nationalboundaries.

When a parent company and its subsidiaries are MFIs located in the samenational territory, the parent company is permitted to consolidate in its statisticalreturns the business of these subsidiaries, keeping however the business of creditinstitutions and other MFIs separate, for the purposes of the ESCB minimumreserve system.

If an institution has branches located within the territories of the other partici-pating Member States, the registered or head office located in a given partici-pating Member State shall consider the positions towards all these branches aspositions towards residents in the other participating Member States. Conversely,a branch located in a given participating Member State shall consider thepositions towards the registered or head office or towards other branches ofthe same institution located within the territories of the other participatingMember States as positions towards residents in the other participatingMember States.

If an institution has branches located outside the territory of the participatingMember States, the registered or head office in a given participating MemberState shall consider the positions towards all these branches as positions towardsresidents of the rest of the world. Conversely, a branch located in a givenparticipating Member State shall consider the positions towards the registeredor head office or towards other branches of the same institution located outsidethe participating Member States as positions towards residents of the rest of theworld.

Institutions located in offshore financial centres are treated statistically asresidents of the territories in which the centres are located.

Maturity at issue (original maturity) refers to the fixed period of life of a financialinstrument before which it cannot be redeemed (e.g. debt securities) or beforewhich it can be redeemed only with some kind of penalty (e.g. some types ofdeposits). The period of notice corresponds to the time between the moment theholder gives notice of an intention to redeem the instrument and the date onwhich the holder is allowed to convert it into cash without incurring a penalty.Financial instruments are classified according to the period of notice only whenthere is no agreed maturity.

Definitions of sectors

The ESA 95 provides the standard for sector classification. For the sector classi-fication of non-MFI counterparties located outside the domestic territory, furtherguidance may be found in the ECB's Money and Banking Statistics SectorManual.

Banking institutions located outside the Member States are referred to as ‘banks’rather than as MFIs. Similarly, the term ‘non-MFI’ refers only to the MemberStates; for other countries the term ‘non-banks’ is appropriate. ‘Non-MFIs’comprise the following sectors and sub-sectors:

▼B

2001R2423— EN — 04.01.2008 — 006.001— 34

(1) In the tables of Part 2 of this Annex, the ECB is to be classified as to MFIs resident ofthe country where the ECB is physically located.

— general government: resident units which are principally engaged in theproduction of non-market goods and services, intended for individual andcollective consumption and/or in the redistribution of national income andwealth (the ESA 95, paragraphs 2.68 to 2.70),

— central government: administrative departments of the State and other centralagencies whose competence extends over the whole economic territory,except for the administration of social security funds (the ESA 95,paragraph 2.71),

— state government: separate institutional units exercising some of the functionsof government at a level below that of central government and above that oflocal government, except for the administration of social security funds (theESA 95, paragraph 2.72),

— local authorities: public administration whose competence extends only to alocal part of the economic territory, excluding local agencies of socialsecurity funds (the ESA 95, paragraph 2.73),

— social security funds: central, state and local institutional units whoseprincipal activity is to provide social benefits (the ESA 95, paragraph 2.74).