babcock institute discussion paper no. …ageconsearch.umn.edu/bitstream/37660/2/2000-2.en.pdf•...

TRANSCRIPT

BABCOCK INSTITUTE DISCUSSION PAPERNo. 2000-2

THE EVOLUTION OF IRELAND'S KERRYGROUP/PLC—IMPLICATIONS FOR THE U.S. AND

GLOBAL DAIRY-FOOD INDUSTRIES

Jeffrey Wagner, Yane Chandera and W.D. Dobson

The Babcock Institute Renk Agribusiness Institute

The Babcock Institute for International Dairy Research and DevelopmentUniversity of Wisconsin, College of Agricultural and Life Sciences

240 Agriculture Hall, 1450 Linden DriveMadison, Wisconsin 53706-1562

The research presented in this Discussion Paper was supported bythe Babcock Institute for International Dairy Research and Development

and by the Renk Agribusiness Institute, University of Wisconsin-Madison.

The Renk Agribusiness Instituteis a joint program of the

University of Wisconsin-Madison College of Agricultural and Life SciencesUniversity of Wisconsin-Madison School of Business

University of Wisconsin Extension Cooperative Extension Division

The Babcock Institute for International Dairy Research and Developmentis a joint program of the

University of Wisconsin-Madison College of Agricultural and Life SciencesUniversity of Wisconsin-Madison School of Veterinary Medicine

University of Wisconsin Extension Cooperative Extension Division

Funding for the Babcock Institute portion of this study was provided by CSRS USDA SpecialGrant 95-34266-2211

The views expressed in Babcock InstituteDiscussion Papers are those of the authors;

they do not necessarily represent those of theInstitute or of the University.

The Babcock Institute240 Agriculture Hall, 1450 Linden Drive

Madison, WI 53706-1562USA

Phone: 608-265-4169; Fax: 608-262-8852Email: [email protected]: http://babcock.cals.wisc.edu

University of Wisconsin 2000

Table of Contents

Executive Summary. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1Introduction..............................................................................................................................1Core and Supporting Strategies of the Kerry Group/PLC.........................................................1Origins of the Kerry Group/PLC..............................................................................................1Financing Strategies of the Kerry Group/PLC..........................................................................1Kerry Group/PLC' s Acquisitions.............................................................................................2Strategies and Practices that Underpin the Kerry Group/PLC' s Financing, Expansion, and

Diversification Initiatives......................................................................................................2An Analysis of Kerry Group/PLC' s Corporate Strategies.........................................................3Implications of Kerry Group/PLC' s Strategies for U.S. and other Dairy-Food Exporters

and Investors .......................................................................................................................3

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

I . Core and Supporting Strategies of the Kerry Group/PLC. . . . . . . . . . . . . . . . . . . . . . 5

I I . Origins of the Kerry Group/PLC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5The Private Company...............................................................................................................5Formation of Kerry Cooperative...............................................................................................5Growth through Dairy Processing, 1974-78.............................................................................6Management Takes New Directions, 1979-85 ..........................................................................6

III. Financing Strategies of the Kerry Group/PLC. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7Why Did Kerry Cooperative and Other Irish Agricultural Cooperatives Opt to Form PLC' s?....7Kerry Group/PLC' s Stock Prices.............................................................................................9Kerry' s Handling of Potential Conflicts Between Non-Cooperative Stockholders and

Farmer-Members of Kerry Cooperative..............................................................................10

IV. Kerry Group/PLC's Acquisitions and Capital Investments . . . . . . . . . . . . . . . . . . . 1 1Acquisitions ...........................................................................................................................11Capital Investments ................................................................................................................12Financing of Recent Acquisitions ...........................................................................................13

V . Strategies and Practices that Underpin the Kerry Group/PLC's Financing,Expansion and Diversification Initiatives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 4Knowledge is the Forerunner of Strategy ...............................................................................14R&D Expenditures .................................................................................................................15Changes in Personnel Recruitment Practices...........................................................................15Changes in Marketing Practices..............................................................................................15

VI. An Evaluation of Kerry Group/PLC's Corporate Strategies . . . . . . . . . . . . . . . . . . 1 6

VII. Implictions of the Strategies of the Kerry Group/PLC for U.S. and OtherDairy-Food Exporters and Investors. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 8

References. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 0

Appendix. Kerry Group/PLC's Capital Investments, 1995-98. . . . . . . . . . . . . . . . . . . . 2 2

Tables and Figures

Table 1. Partial List of Kerry Group/PLC's Acquisitions, 1995-99................................11

Figure 1. Initial Ownership of Kerry Group/PLC....................................................... 7

Figure 2. Kerry Group/PLC's Share Prices, Earnings, and Dividends, 1995-2000 (U.S.$)...... 9

Figure 3. The Collis-Montgomery Triangle of Corporate Strategy...................................16

Babcock Institute Discussion Paper No. 2000-2 1

THE EVOLUTION OF IRELAND'S KERRY GROUP/PLC—IMPLICATIONS FORTHE U.S. AND GLOBAL DAIRY-FOOD INDUSTRIES

Jeffrey Wagner, Yane Chandera and W.D. Dobson*

Executive Summary

Introduction• Headquartered in Tralee, County Kerry Ireland, the Kerry Group/PLC (Public Limited

Company) is a diversified food ingredients and consumer foods company with 1998 salesof U.S.$2.6 billion.

• The firm grew from a small dairy cooperative in the early 1970s to a multinational firm thathas operations in Ireland, the UK, the U.S., continental Europe, Canada, Mexico, Brazil,Argentina, Chile, New Zealand, Australia, and Malaysia.

• As the firm evolved into a world leader in food ingredients, the sales of Irish-based dairyproducts declined to about 11% of the firm's overall revenues.

• This Discussion Paper describes how the firm developed core strategies, adjustedeffectively to the economic and policy environment that surfaced in the 1970s and 1980s,and found innovative ways to finance growth. The paper also analyzes Kerry's strategiesand discusses implications of the firm's strategies for U.S. and other dairy-food exportersand investors.

Core and Supporting Strategies of the Kerry Group/PLC• The Kerry Group/PLC's core strategy is to diversify and grow the business emphasizing

differentiated (value-added) food ingredients and consumer food products.• Kerry's implementation of this overall strategy has produced a strong emphasis on food

ingredients as noted in the firm's divisional sales figures for 1998: Kerry Ingredients (63%of 1998 sales), Kerry Foods (34% of 1998 sales), and Kerry Agribusiness (3% of 1998sales).

Origins of the Kerry Group/PLC• The roots of the Kerry Group/PLC date back to a private company formed in 1972.• Kerry Cooperative Creameries Ltd. began its legal existence in January 1974.• A brucellosis eradication program reduced Kerry Cooperative's milk supply by about 20%

in the early 1970s. This caused the Kerry Cooperative's management and board ofdirectors to realize that if the firm was to grow it needed to reduce the reliance oncommodity dairy products and diversify into differentiated (value-added) products.

• Kerry Cooperative's diversification program began in 1979-80 when the cooperativebought 19 Irish firms that sold branded food products.

Financing Strategies of the Kerry Group/PLC• In June 1986, Kerry Cooperative exchanged its assets for majority shareholding in a PLC,

mainly to obtain capital for growth.

* Jeffrey Wagner is an MBA in Agribusiness student and Project Assistant at the University of

Wisconsin-Madison (UW-Madison). Yane Chandera is a former MBA in Agribusiness student andformer Project Assistant at the UW-Madison. W.D. Dobson is Professor of Agricultural & AppliedEconomics, Co-Director of the Babcock Institute, and Director of the Renk Agribusiness Institute atthe UW-Madison. This Discussion Paper is a joint product of the Babcock Institute and RenkAgribusiness Institute.

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

2 Babcock Institute Discussion Paper No. 2000-2

• In October 1986, shares of the Kerry Group/PLC were offered to the public andsubsequently listed on the Dublin and London stock exchanges.

• Kerry Group/PLC's shares initially traded for about 52 Irish pence (about U.S.$0.70 pershare) when the firm's shares were first issued in 1986. In 1999, the shares traded mostlyin the U.S.$11.00 to U.S.$12.50 range. The Price/Earnings ratios for Kerry Group stockin 1999 were approximately twice those for Irish dairy cooperative/PLCs, Golden Vale andGlanbia.

• In 1996, Kerry Cooperative reduced its holdings in Kerry Group/PLC below the 51%level. This action allowed the Kerry Group/PLC to float additional shares to obtain neededfunds for expansion capital and increase the liquidity of trading in the Kerry Group'sshares.

• Kerry Cooperative and Kerry Group/PLC have effectively handled the conflicts betweenfarmers and non-farmer shareholders that sometimes arise when an agricultural cooperativeconverts to a PLC.

Kerry Group/PLC's Acquisitions• The financing capacity gained by Kerry, in part by the move to cooperative/PLC status,

allowed the firm to accelerate its overseas acquisitions.• Kerry Group/PLC opened its first overseas food ingredients plant in Jackson, Wisconsin in

1987 and in 1988 acquired Beatreme Food Ingredients, another U.S. firm.• Kerry Group/PLC acquired DCA in 1994 from Allied Domecq for U.S.$402 million.• By 1995, Kerry Group/PLC had made about 43 acquisitions, which had caused the firm to

double in size in each of the previous five-year periods.• Most of Kerry's recent acquisitions have been for food ingredients firms, which typically

generate high profit margins. The corporation's capital investments have provided theinfrastructure (e.g., technology, R&D and distribution systems) needed by the rapidlygrowing firm.

• In 1998, 26% of the firm's sales and 38% of the firm's operating profits were obtainedfrom the Americas.

• While Kerry's early acquisitions were made in part with capital raised in the share market,the bulk of the Kerry Group/PLC's acquisitions—especially those made before KerryCooperative relinquished majority control in 1996—were made with debt.

Strategies and Practices that Underpin the Kerry Group/PLC's Financing,Expansion, and Diversification Initiatives

• Knowledge is the forerunner of strategy . Mr. Denis Brosnan, the Kerry Group/PLC'slong-time Managing Director, contends that to make sound strategic decisions the firm mustknow which sector it is in or wants to be in, the strengths and weaknesses of competitors,the nature of the marketplace, how consumer demands are changing and, for aninternational business, which decisions can be made locally and which must be reserved forthe corporate office.

• R&D expenditures must increase . According to Brosnan, the food ingredients sector issomewhere between food engineering and pharmaceutical application; 2.5% to 3.0% of theKerry Group's turnover will continue to be spent on R&D because of its importance.

• Personnel and marketing practices must evolve . Practices relating to these two functionschanged markedly as Kerry evolved from a dairy cooperative into a food ingredients andconsumer foods company. Kerry stopped exporting through the Irish Dairy Board in about1990.

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

Babcock Institute Discussion Paper No. 2000-1 3

An Analysis of Kerry Group/PLC's Corporate Strategies• The Collis-Montgomery "Triangle of Corporate Strategy" was used to evaluate Kerry's

corporate strategies.• The firm appears to have a well-articulated vision, internally consistent strategies, strategies

that fit well with the external environment, and good risk management capabilities.• It is unclear whether the firm's value creation processes—achieved in part by frequent

acquisitions of high profit margin food ingredient companies—will be sustainable over thelong-term.

• Kerry acquisitions have been, by most accounts, remarkably successful. However, mergerand acquisition studies suggest that most firms should not expect to earn economic rents onassets purchased in the market. The Kerry Group/PLC may confront this reality in futureacquisitions.

Implications of Kerry Group/PLC's Strategies for U.S. and other Dairy-FoodExporters and Investors

• Certain ideas flow from Kerry's strategies that have implications for U.S. and other dairy-food exporters and investors.

• Ability to relate a company to its environment is important.• Continuity in top management is important.• Knowledge is a key forerunner to strategy.• Early mover advantages are important.• Latin America and Asia are growth markets for dairy and other food products.• A firm's infrastructure must change substantially when it evolves as much as Kerry

Group/PLC.• Kerry Cooperative's conversion to a cooperative/PLC was a necessary but not sufficient

condition for success.• Acquisitions possess inherent drawbacks.• The Kerry Group/PLC model will not be easily replicated.

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

4 Babcock Institute Discussion Paper No. 2000-2

THE EVOLUTION OF IRELAND'S KERRY GROUP/PLC—IMPLICATIONS FORTHE U.S. AND GLOBAL DAIRY-FOOD INDUSTRIES

Jeffrey Wagner, Yane Chandera and W.D. Dobson

Introduction

Headquartered in Tralee, County Kerry Ireland, the Kerry Group/PLC (public limitedcompany) is a diversified food ingredients and consumer foods company, which had sales ofU.S.$2.6 billion and 12,378 employees in 1998 [13,31]. The firm has operations in Ireland, theUK, the U.S., continental Europe, Canada, Mexico, Brazil, New Zealand, Australia, and Malaysia[31]. It produces and markets specialty food ingredients, food coatings, bakery mixes, fruitpreparations, flavorings, and proteins and manufactures consumer food products in the dairy,beef, pork, poultry, savory and convenience product sectors.

The firm's sales and net income for 1998 and the average yearly increases in these twofinancial items during 1994-98 appear below [31]:

Sales Net Income(Millions U.S. Dollars)

1998 $2,578.34 $111.101994-98 Growth Rate 14.51% 20.93%

Kerry Group/PLC's three main divisions and the percentage of the firm's revenues generatedby each division in 1998 are noted below [9]:

Division % of 1998 RevenuesKerry Ingredients 63Kerry Foods 34Kerry Agribusiness 3

Food Ingredients produced by Kerry Group/PLC include cheese powders, mozzarella cheeseproducts for restaurant chains, doughnut mixes, other batter mixes, bread crumbs, specialtyproteins for nutritional diets, flavorings for snack foods, and clouding agents. In recent years, thefirm has acquired a substantial presence in the particulates technology business—e.g., small piecesof fruit, nuts, cheese, and chocolate that are used in processed foods such as breakfast cereals,nutritional bars, and premium ice creams.

Kerry Foods brands (which are well known in Ireland, the UK, and other parts of Europe)include Wall's, Mattesson's, Richmond, Denny, Lawson's, Miller's, Golden Bridge, Homepride,Ballyfree, Kerrymaid, Low Low, Dawn (fluid milk and juices), and Kerry Spring (water). TheKerry Group's Foods Division also does private label work for other firms.

Kerry Agribusiness sells animal feeds and fertilizers, operates creameries, and provideslivestock artificial insemination services, trucking services, and on-farm technical services.

Kerry Group/PLC traces its beginnings to 1972 when it began operations as a relatively smallprivate firm that evolved into a small dairy cooperative in 1974.

Kerry Group/PLC is frequently described by analysts as a successful international foodingredients and consumer food products firm that grew rapidly—mainly by acquiring othercompanies—during the late 1980s and 1990s. Information on how the Kerry Group/PLC arrivedat its present position should be useful to U.S. and other firms with interests in exporting andforeign direct investment in global dairy-food businesses. In particular, it should be useful for

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

Babcock Institute Discussion Paper No. 2000-1 5

dairy-food exporters and investors to see how the firm developed core, consistent strategies,adjusted effectively to changes in the economic and policy environment that surfaced in the 1970sand 1980s, and found innovative ways to finance growth of the business. These points areconsidered in the paper, together with an analysis of Kerry's strategies and a discussion ofimplications of the firm's strategies for dairy-food exporters and investors in the U.S. and othercountries.

I . Core and Supporting Strategies of the Kerry Group/PLC

The Kerry Group/PLC's core strategy is to diversify and grow the business emphasizingdifferentiated (value-added) food ingredients and consumer food products [2]. This core strategyhas been supported and complemented by the other strategies and practices that:

• Converted the business from a dairy cooperative to a cooperative/PLC to raise expansioncapital.

• Facilitated growth of the firm both by acquisitions (mostly outside of Ireland) andexpanding existing businesses.

• Involved large Research and Development (R&D) expenditures to support expansion of thefood ingredients business and consumer food product businesses.

• Implemented personnel policies and marketing practices that supported the firm's growthand diversification strategies.

I I . Origins of the Kerry Group/PLC

Michael Porter of Harvard's Business School contends that "The essence of formulatingcompetitive strategy is relating a company to its environment" [28, p. 3]. The Kerry Group/PLCdeveloped strategies that dealt effectively with the economic and policy environment facing the firmin the 1970s and 1980s. It is useful to briefly examine the firm's early history to see the milieufrom which the firm's strategies emerged.

The Private Company

The roots of the Kerry Group/PLC date back to a private company formed in 1972. Theprivate company in question was created when three shareholders—(a) the state-owned DairyDisposal Company, (b) a federation of eight small farmer cooperatives in County Kerry Ireland,and (c) the Erie Casein Company in the U.S.—invested 150,000 Irish pounds to finance a caseinplant that would manufacture casein for export to the U.S. Ownership of the casein manufacturingfirm, known as North Kerry Milk Products Ltd. (NKMP), was split as follows [12]:

• Dairy Disposal Company 42.5%

• Federation of eight farmer cooperatives 42.5%

• Erie Casein Company 15.0%

Formation of Kerry Cooperative

When Ireland joined the then European Economic Community (EEC) in 1973, many smalldairy firms and cooperatives merged to compete with the larger milk companies in the EEC. KerryCooperative Creameries Ltd. was formed when milk producers in County Kerry contributed capitalto acquire the state-owned Dairy Disposal Company and its 42.5% stake in the private NKMP. Inaddition, six of the eight independent farmer cooperatives (part owners of the other 42.5% ofNKMP) merged and the private company created became a subsidiary of the newly formed KerryCooperative Creameries Ltd. Kerry Cooperative Creameries Ltd. began its legal existence in

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

6 Babcock Institute Discussion Paper No. 2000-2

January 1774. The smallest of Ireland's six major agricultural cooperatives, the KerryCooperative, had sales of 23 million Irish pounds (about U.S.$50 million) in 1974.

Growth through Dairy Processing, 1974-78

During 1974-80, Kerry Cooperative Creameries Ltd. acquired or merged with the Killarney,Limerick, and Ballinahina Dairies and witnessed an increase in its milk supply from 67 million to87 million gallons (+30%). The cooperative recorded satisfactory profits through its milkprocessing activities. But in 1979-80, as a result of an unusually wet summer and the workings ofa brucellosis eradication scheme, the cooperative lost 20% of its milk supply. In 1986, Mr. DenisBrosnan, Managing Director of Kerry Group/PLC or its predecessor firms from 1972 to thepresent, described the impact of the brucellosis eradication program, which led to the slaughter ofthousands of dairy cattle in Kerry Cooperative's milk supply area, as follows [29]:

It was either going to be a disaster or a blessing. Our cow population was immediately cutby 20% but we still had the same overheads. We were forced to reorganize.

It became clear to Kerry Cooperative's management and board of directors that if theorganization was to grow and develop, it needed to reduce its reliance on commodity dairyproducts and diversify into more differentiated (value-added) products. Thus, the firm introducedthe concept of corporate planning and corporate strategy into its management systems and culture[30]. This, in turn, led the organization to agree to a five-year corporate plan that emphasizedR&D, diversification, and overseas growth.

Kerry Cooperative's management and board of directors began efforts to diversify into valueadded products before the EEC adopted milk production quotas in 1984. Thus, the wisdom of thefirm's decision to emphasize overseas investment, as well as production and marketing ofdifferentiated food ingredients and food products, was validated when the EEC decided to imposemilk production-limiting quotas. In 1995, Brosnan explained Kerry's continued lack of interest inexpanding investment in Ireland's milk business, as follows [19]:

If anybody could point out the advantage of merging with or taking over another Irishcompany, then we would do so. I do not see any advantage, we would simply be buying intoa milk business which is heavily regulated by the EU and which is very cyclical.

Management Takes New Directions, 1979-85

Brosnan reported how the new directions first began to materialize as follows[30]:

We started in 1979-80 to get away from dependence on milk, and began buyingcompanies in Ireland—19 altogether. We specifically bought the top brands that wereavailable, and that put us firmly in the food business. We got into ingredients when wedecided to follow our casein to the U.S.

Structures were put in place during 1980-85 to help Kerry Cooperative Creameries, Ltd.become an international food business. Management recognized that the Kerry Cooperative's milkprotein was being used in sophisticated food products. It was also apparent to management thatgreater value could be generated by supplying specialty food ingredients to the convenience foodindustry rather than sell the firm's dairy products as dairy commodities. Accordingly, Kerrybought Erie Casein's interest in NKMP, acquiring full ownership in a large food ingredient base inthe U.S. In 1983, Kerry Cooperative established U.S. and UK headquarters offices in Chicagoand London, respectively.

The Erie Casein acquisition marked the beginning of Kerry Cooperative's major efforts toserve overseas markets. The firm secured the funds required to purchase overseas companiespartly from equity capital obtained by converting the organization to a cooperative/PLC in 1986.

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

Babcock Institute Discussion Paper No. 2000-1 7

III. Financing Strategies of the Kerry Group/PLC

While Kerry Group/PLC has used complex debt, equity, and cash financing practices in recentyears, the firm made a pioneering move in equity financing in 1986 that warrants attention. InJune of 1986, Kerry Cooperative Creameries, Ltd. exchanged its assets for majority shareholdingin a public limited company, mainly to obtain capital for growth. Other Irish cooperatives (thenAvonmore Foods, Waterford Foods, and Golden Vale Cooperative) followed suit shortlythereafter.

Jacobson and O'Leary described Kerry Cooperative's initial share offering in these terms [7,p. 131]:

A total of 150 million shares represented the ownership of Kerry Group PLC. Sixtymillion of the shares were identified as A ordinary shares and were owned by individualinvestors and other investment groups. The other 90 million shares were owned by KerryCooperative Creameries Ltd. The 6,000 shareholders in Kerry Cooperative indirectly ownedthe 90 million B ordinary shares in Kerry Group PLC.

Figure 1. Initial Ownership of Kerry Group/PLC *

60 MillionA Ordinary Shares

- individual investors, etc.

90 MillionB Ordinary Shares

- all owned by KerryCo-op Creamery, Ltd.

KERRY GROUP PLC150 Million Shares

* Source: Jacobson and O'Leary [7].

Kerry Cooperative, Ltd. owned the ordinary B shares of the newly formed Kerry Group/PLC(Figure 1). Rules of the PLC stipulated that the Cooperative was required to retain a controllinginterest (at least 51%) of the new company. In October 1986, the A shares of Kerry Group/PLCwere offered to the public and subsequently listed on the Dublin and London stock exchanges.

Fifteen of the 20 directors for Kerry Group/PLC were farmer-directors of Kerry Cooperative,Ltd. The other five directors were executives of the new PLC firm.

Why Did Kerry Cooperative and Other Irish Agricultural Cooperatives Opt toForm PLC's?

In the mid-1980s, it was unusual for agricultural cooperatives to become cooperative/PLCs.Why did Kerry Cooperative and other Irish agricultural cooperatives take this step?

Prior to the mid-1980s, farmer members of Irish agricultural cooperatives said that theyrequired three things from investments in their organizations [7, p. 52]:

• Capital growth.

• Reasonable dividends.

• Tradability.

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

8 Babcock Institute Discussion Paper No. 2000-2

In Ireland during this period, the PLC mechanism held promise for addressing these matterswhile existing cooperative financing models did not.

The failure of the existing cooperative financing models to address these needs has complexorigins. But, the management and operating practices of Irish agricultural cooperatives exhibitedcharacteristics during this period that encouraged the formation of PLC's, including those notedbelow:

• The ownership structure of the cooperatives had a high proportion of inactive shareholders.In some cooperatives, a substantial number of farmer patrons were not members.

• Equity redemption polices among dairy cooperatives were almost nonexistent.

• There were problems with capital and/or share valuation.

The last two items are perhaps the most important. Prior to the mid-1980s, Irish agriculturalcooperatives had pursued financing practices that discouraged farmers from providing expansioncapital to the organizations. In particular, many Irish agricultural cooperatives retained profitsgenerated from operations in the form of unallocated reserves.

This contrasts with the U.S. situation where frequently a large percentage of the profits of anagricultural cooperative are allocated to individual members on the books of the cooperative andsome minimum amount of profits is paid out to members in cash each year. (U.S. agriculturalcooperatives are legally obligated to pay out at least 20% of net earnings in cash each year.) Therecord of U.S. cooperatives in handling reserves certainly does not satisfy all farmers. However,many U.S. cooperatives operate revolving funds under which profits are (a) revolved back tomembers using 8 to 15 year revolving period arrangements, and (b) revolve back to the farmermember or his/her heirs the allocated reserves when the farmer leaves the cooperative, retires ordies. These practices give value to farmers' claims on the cooperatives allocated reserves.

In the mid-1980s, many Irish agricultural cooperatives had on their books sizeableaccumulations of retained earnings in the form of unallocated reserves. Farmer members heldshares in the Irish cooperatives, which they felt gave them claims to the cooperatives’ unallocatedreserves and other assets. But, farmer members correctly perceived that there was little chance thatunallocated reserves would be paid to them. Thus, their shares had little value but implicitlyrepresented valuable assets if they could cash them in.

While some farmer members received dividends on allocated reserves, these reserves typicallywere such a small percentage of the total reserves of the cooperatives that the payments wereminimal. Jacobson and O'Leary report, for example, that in 1988 allocated reserves accounted foran average of only about 7% of the reserves of 15 Irish dairy cooperatives studied [7, p. 32].

The presence of unallocated reserves also made a few cooperatives targets for takeover byprivate firms. Thus, in January 1988, the shareholders of Bailieboro Cooperative Agricultural andDairy Society Ltd. voted by more than two to one to accept an offer for their shares from theGoodman/Food Industries Group, a public limited company [7, pp. 16-17]. These shareholdershad found a way to obtain cash for the potentially valuable shares. One other cooperative followedsuit.

A number of Irish agricultural cooperatives opted for the PLC model rather than adopt a U.S.-type system of allocating more reserves to members and dealing with other financing problemsaffecting the cooperatives. This choice stemmed partly from the cooperatives' needs to expand thescale of processing operations. For several Irish cooperatives, this expansion would have requiredmore capital than could have been raised even with a U.S. style management and financing systemfor the cooperatives. In part this was because many Irish farmers who needed capital to expand orupgrade their own operations were not in a position to make large capital contributions to thecooperatives.

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

Babcock Institute Discussion Paper No. 2000-1 9

It was against this backdrop that Kerry Cooperative's initiative to form a cooperative PLC toraise needed expansion capital received a cordial reception.

Kerry Group/PLC's Stock Prices

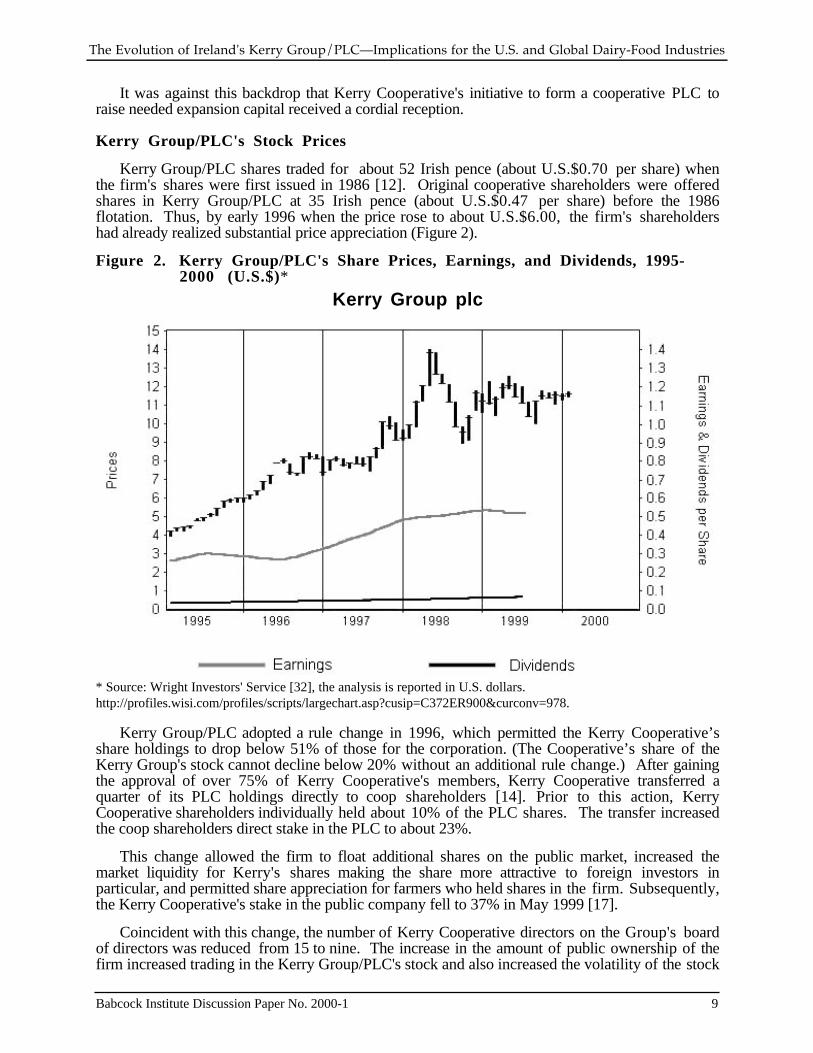

Kerry Group/PLC shares traded for about 52 Irish pence (about U.S.$0.70 per share) whenthe firm's shares were first issued in 1986 [12]. Original cooperative shareholders were offeredshares in Kerry Group/PLC at 35 Irish pence (about U.S.$0.47 per share) before the 1986flotation. Thus, by early 1996 when the price rose to about U.S.$6.00, the firm's shareholdershad already realized substantial price appreciation (Figure 2).

Figure 2. Kerry Group/PLC's Share Prices, Earnings, and Dividends, 1995-2000 (U.S.$)*

Kerry Group plc

* Source: Wright Investors' Service [32], the analysis is reported in U.S. dollars.http://profiles.wisi.com/profiles/scripts/largechart.asp?cusip=C372ER900&curconv=978.

Kerry Group/PLC adopted a rule change in 1996, which permitted the Kerry Cooperative’sshare holdings to drop below 51% of those for the corporation. (The Cooperative’s share of theKerry Group's stock cannot decline below 20% without an additional rule change.) After gainingthe approval of over 75% of Kerry Cooperative's members, Kerry Cooperative transferred aquarter of its PLC holdings directly to coop shareholders [14]. Prior to this action, KerryCooperative shareholders individually held about 10% of the PLC shares. The transfer increasedthe coop shareholders direct stake in the PLC to about 23%.

This change allowed the firm to float additional shares on the public market, increased themarket liquidity for Kerry's shares making the share more attractive to foreign investors inparticular, and permitted share appreciation for farmers who held shares in the firm. Subsequently,the Kerry Cooperative's stake in the public company fell to 37% in May 1999 [17].

Coincident with this change, the number of Kerry Cooperative directors on the Group's boardof directors was reduced from 15 to nine. The increase in the amount of public ownership of thefirm increased trading in the Kerry Group/PLC's stock and also increased the volatility of the stock

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

10 Babcock Institute Discussion Paper No. 2000-2

price (Figure 2). In 1998 the Kerry Group/PLC's stock traded for several months in theU.S.$11.00 to U.S.$14.00 range before leveling off to trade in the U.S.$11.00 to U.S.$12.50range during much of 1999.

The stock of Kerry Group/PLC in 1999 traded at approximately double the P/E ratio of Irishdairy companies Golden Vale and Glanbia (merged Avonmore/Waterford organization) [17].Kerry's higher P/E ratios presumably reflect the impact of many developments, including Kerry'sdecision to emphasize food ingredients.

Kerry's Handling of Potential Conflicts Between Non-Cooperative Stockholdersand Farmer-Members of Kerry Cooperative

When a farmer cooperative converts to a cooperative/PLC, it sometimes creates conflictsbetween farmer-members of the cooperative and non-cooperative shareholders in the PLC.

In part the conflict arises over issues of control. Kerry appears to have resolved this issuesuccessfully. Kerry Cooperative, Inc. still held 37% of the stock of the Kerry Group/PLC andplaced nine members on the board of directors for the Kerry Group after the 1996 action. Thisappeared to satisfy farmer-members of the cooperative that they retained appropriate amounts ofcontrol over Kerry Group/PLC. In addition, in 1996 after Kerry Cooperative's holdings in KerryGroup were reduced, the Kerry Group/PLC gave Kerry Cooperative the option to buy the KerryGroup/PLC's Agribusiness Division between the years 2001 and 2020 [26]. The purchase couldbe made to ensure that the Agribusiness Division's farm inputs and services would continue to beavailable to members of the Cooperative. If the Cooperative elects to buy the Kerry Group'sAgribusiness Division, it likely will finance the purchase with stock held in the Kerry Group/PLC.

Conflicts can also arise between milk suppliers and non-farmer shareholders in a PLC. Forexample, farmer-members supplying milk to a dairy cooperative/PLC often prefer to receive highmilk prices rather than capital appreciation or elevated stock dividends. Non-farmer shareholdersin the organization, on the other hand, typically prefer management activities that emphasize stockappreciation and/or large stock dividends.

This potential source of conflict appears not to have been a problem for Kerry. Members ofKerry Cooperative have benefited both as milk suppliers and stockholders. They have realizedstock appreciation and have received stock dividends and competitive milk prices. Hugh Friel,Deputy Managing Director of Kerry/PLC, reported that "milk prices are not an issue" for Kerry[6]. Presumably this means that Kerry generates enough profit to pay competitive milk pricesthrough efficient and profitable milk processing and marketing operations. Moreover, the firmcould, if it chose to do so, cross subsidize milk producers with profits generated by other parts ofthe firm.

Particularly before the 1996 action, which reduced Kerry Cooperative's holdings of KerryGroup/PLC below 51%, non-farmer shareholders sought additional shares in the thinly-tradedKerry Group stock, presumably because they thought it represented an attractive investment. Thehigh P/E ratios enjoyed by Kerry compared to other Irish cooperative/PLC firms in 1999 suggeststhat it is still regarded as a relatively attractive investment.

Thus, the firm's successes, the 35%+ shareholdings retained by Kerry Cooperative, and theagreement to give Kerry Cooperative an option to buy the Group's Agribusiness Division appear tohave eliminated most potential sources of conflict among Kerry Cooperative, the Kerry Group'sfarmer shareholders and other shareholder groups.

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

Babcock Institute Discussion Paper No. 2000-1 11

IV. Kerry Group/PLC's Acquisitions and Capital Investments

Acquisitions

The financing capacity gained in part by the move to cooperative/PLC status enabled the KerryGroup to accelerate the firm's acquisitions—especially overseas. Kerry Group/PLC opened itsfirst overseas food ingredients manufacturing plant in Jackson, Wisconsin in 1987 and in 1988acquired Beatreme Food Ingredients, a division of Beatrice Corporation [12, p. 3]. Kerry officialsdescribed Beatreme Food Ingredients, which was acquired for U.S.$130 million, as the "premierspecialty food ingredient supplier in the U.S. market" [12, p.3].

The Kerry Group in 1993 acquired Malcolm Foods of St. George, Ontario and ResearchFoods in Toronto, Ontario, Canada.

The Kerry Group/PLC initially developed its European food ingredients business in the dairy,confectionery and convenience food sector from the Listowel plant in Ireland and the Wadersloh

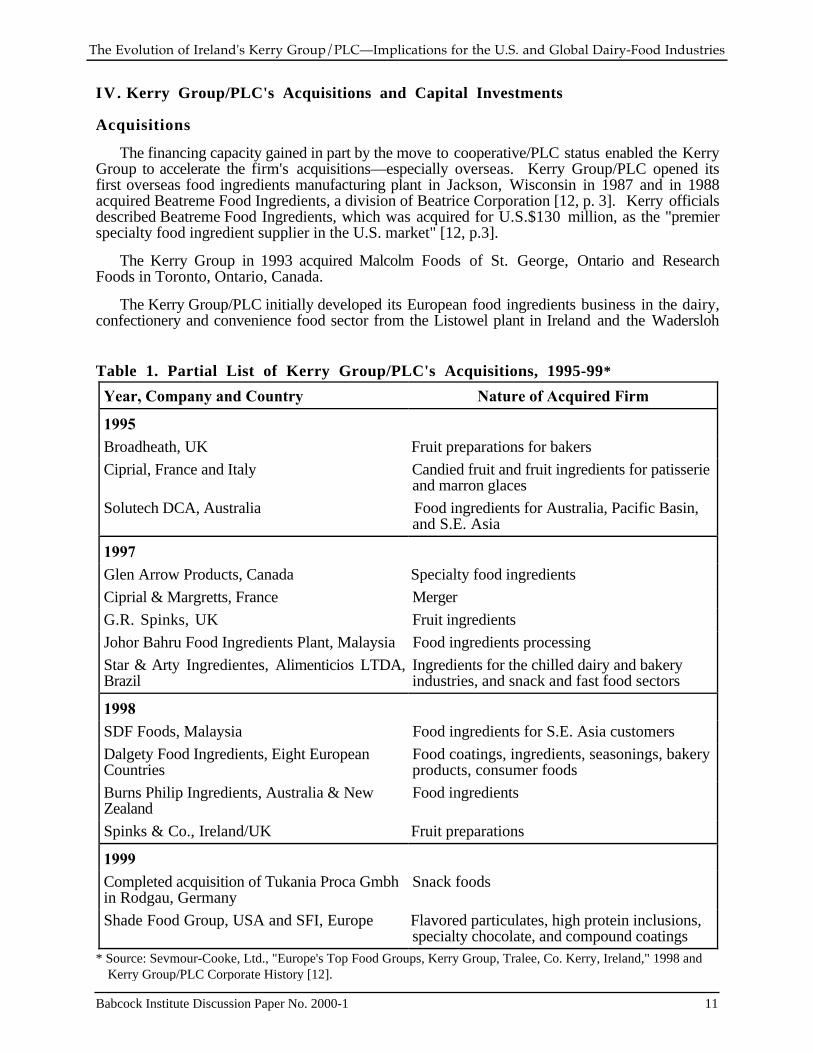

Table 1. Partial List of Kerry Group/PLC's Acquisitions, 1995-99*

Year, Company and Country Nature of Acquired Firm

1995Broadheath, UK Fruit preparations for bakers

Ciprial, France and Italy Candied fruit and fruit ingredients for patisserieand marron glaces

Solutech DCA, Australia Food ingredients for Australia, Pacific Basin,and S.E. Asia

1997Glen Arrow Products, Canada Specialty food ingredients

Ciprial & Margretts, France Merger

G.R. Spinks, UK Fruit ingredients

Johor Bahru Food Ingredients Plant, Malaysia Food ingredients processing

Star & Arty Ingredientes, Alimenticios LTDA,Brazil

Ingredients for the chilled dairy and bakeryindustries, and snack and fast food sectors

1998SDF Foods, Malaysia Food ingredients for S.E. Asia customers

Dalgety Food Ingredients, Eight EuropeanCountries

Food coatings, ingredients, seasonings, bakeryproducts, consumer foods

Burns Philip Ingredients, Australia & NewZealand

Food ingredients

Spinks & Co., Ireland/UK Fruit preparations

1999Completed acquisition of Tukania Proca Gmbhin Rodgau, Germany

Snack foods

Shade Food Group, USA and SFI, Europe Flavored particulates, high protein inclusions,specialty chocolate, and compound coatings

* Source: Sevmour-Cooke, Ltd., "Europe's Top Food Groups, Kerry Group, Tralee, Co. Kerry, Ireland," 1998 andKerry Group/PLC Corporate History [12].

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

12 Babcock Institute Discussion Paper No. 2000-2

plant in Germany [12, p. 3]. Later, through the acquisition of Eastleigh Flavors and Tingles Ltd.in 1993, the Kerry Group became a leading supplier to the UK and Continental Europe snack foodand food processing industries [12, p. 4].

Kerry Group/PLC acquired DCA in 1994 from Allied Domecq, PLC for U.S.$402 million.The acquisition was financed with loans from three Irish Banks plus a share issue. At the time ofthe acquisition, DCA had operations in five countries with two-thirds of the value residing in theU.S. B. McGrath, Markets Editor for The Irish Times , described the acquisition as follows [15]:

DCA brings the group into cereal based ingredients and the fruit flavor markets andcomplements Kerry's existing strengths in dairy-based ingredients. Like the existing Kerrybusiness, DCA has operations in five countries and specializes in the manufacture of foodingredients for the baking, food processing, and food service industries.

This DCA deal made Kerry Group/PLC a world leader in the food ingredients business.

By 1995, Kerry Group/PLC had made about 43 acquisitions, which allowed the firm to doublein size in each of the previous five-year periods [30]. Table 1 shows recent acquisitions togetherwith the geographic areas and products emphasized.

While the acquisitions in Table 1 do not comprise an exhaustive list, the table does show thenature of the Kerry Group/PLC's recent acquisitions—many have been in the food ingredientsbusiness. They also show the firm is establishing the foundation for further expansion into LatinAmerica and South Asia—growth markets for food businesses. Kerry reports that the expansioninto Latin America enables the firm to supply fast food businesses that are expanding rapidly inthese growth markets.

Brosnan provided insights on the firm's acquisition strategies in a 1995 interview. His viewson the Beatreme acquisition, investments in Eastern Europe, and investments in North America aresummarized below [30]:

(Beatreme) In 1983, we began tracking Beatrice Foods Specialties, which eventuallybecame Beatreme. We tried to buy it from '83 to '88. So we were in closest when it was putup for sale…At the time of purchase, we were about the same size. Kerry paid U.S.$135million for Beatreme back in 1988. Many thought it was way too much. But we had adifferent view and followed our judgment.

(Investments in Eastern Europe) In purchasing DCA, we acquired an operation in Poland.We've looked at Eastern Europe quite a lot. Our view is that it's going to take longer thanearlier thought for Eastern Europe to advance. So far, we've decided to stay out, but keep itunder review 'til about the year 2000. Like everyone else, we looked at Poland, Hungary andCzechoslovakia when the barriers came down a few years ago, but decided to wait. There's alot of money to be made, but it depends on the time frame. Although it will cost a bit moreto go in later, we'll wait until we're closer to those countries becoming part of the EU.

(Investments in North America) Kerry has major investments in Mexico and Canada.We've often said that if we were as wise in 1973 when Ireland joined the EC, we could haveperhaps made a lot more money earlier. Joining the EC gave Ireland a much largermarketplace. NAFTA will bring huge opportunities on the North American continent, andwe'll be investing further in all countries. It's good for North America.

Capital Investments

The firm's capital investments during 1995-1998 appear in Appendix Table 1. The pattern isdifferent from that of the acquisitions. The investments were directed substantially toward buildingnew warehouses, distribution centers, technical centers, and research centers. Among otherthings, these expenditures establish the infrastructure to support the functioning of the expandedfirm. Capital expenditures also were made to upgrade, and expand ready meals processing plants,upgrade and expand meat and poultry processing capacity, and fruit preparation. Capitalexpenditures were distributed geographically across a host of countries including the U.S., France,the UK, Ireland, Canada, Poland, and the Asia Pacific region.

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

Babcock Institute Discussion Paper No. 2000-1 13

Kerry made capital investments in Poland in 1998 (Appendix Table 1). The firm invested 2.0million Irish pounds in fruit preparation facilities at its plant in Kielce, Poland to serve markets inCentral and Eastern Europe [9, p. 13]. Apparently Kerry's management concluded that Polandwas sufficiently promising that it warranted the additional investment despite the firm's reluctanceto expand its presence in Eastern Europe.

Kerry Group/PLC's current configuration of course was not entirely determined byacquisitions and capital investment. Divestitures—while not numerous—also have shaped thecompany. Kerry's first acquisition in the U.S.—an imitation cheese company—was later sold[30]. In 1995, the firm sold its Irish beef processing operations in Rathdowney, Waterford, andClones. In 1996, the DCA headquarters in New York and the Fenton, Missouri offices of thecoatings division were closed and administration transferred to Beloit, Wisconsin. In 1998,following the acquisition of Dalgety's food ingredients division, eight Spillers mills and FlemingHowden were sold to Tompkins, PLC.

Kerry Group/PLC's acquisitions and divestitures contributed to the following pattern of salesand operating profits in 1998 [9]:

Geographic Area % of Sales % of Operating Profit

Ireland 26.7 18.6

Rest of Europe 43.9 41.6

Americas 26.3 38.5

Rest of the World 3.1 1.3

Total 100.0 100.0

As noted earlier, the Kerry Ingredients division accounted for 63% of the firm's sales in 1998.The firm's acquisitions of large firms and—especially ingredients firms—promise to be thehallmark of Kerry's future acquisitions. Brosnan commented as follows on these points[30]:

…we seldom buy small companies any longer. We're growing internationally iningredients, and in Europe we're growing in consumer foods…. I think the percentages (ratioof food ingredients to consumer foods) will have to change as food ingredients on aninternational basis give us more scope than food products in Northern Europe. But we'revery good at both.

The higher profit margins on ingredients are likely to push the firm to emphasize foodingredients. Curran, an analyst who investigated Kerry Group/PLC's operations, reported that"The food business can yield margins of about 7%, but when a company invests in the technologyto mass produce ingredients such as cheese powder, or coatings for fried products, margins canincrease to over 12%" [5]. It is not clear whether the spread between the margins on ingredientsand consumer food products is as large as the five percentage point difference mentioned byCurran. But it is likely that food ingredients will remain more profitable for Kerry than consumerfood products in the highly competitive European and North American consumer food productmarkets.

Kerry's push toward the ingredients business has been accompanied by a sharp reduction inrevenues from Irish milk sales. After the DCA acquisition in 1994, the dairying business based inIreland formed only about 11% of Kerry's total sales [15].

Financing of Recent Acquisitions

While some of the Kerry Group/PLC's early acquisitions were made substantially with equityfunds, McGrath reports that the firm has funded the “vast bulk of its 800 million Irish pounds ofacquisitions of the past 10 years (1988 to 1998) through debt” [22]. McGrath described the

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

14 Babcock Institute Discussion Paper No. 2000-2

financial impact of Kerry's acquisition of the Dalgety food ingredients business in 1998 as follows[22]:

When this deal is completed, Kerry will have total debt of around 660 million Irishpounds on shareholders funds of just 120 million pounds. This represents a debt/equity levelof over 500%—an astronomical level of debt for a company the size of Kerry….Increasingly, analysts are ignoring gearing (debt load) when assessing companies afterheavily leveraged acquisitions like Kerry's purchase of the Dalgety food ingredients business.Interest cover and cash flow generation are used as more accurate gauges of a company'sability to meet its debt obligations…. Kerry will be able to reduce the 660 million net debtfigure to 590 million pounds by the end of 1998 and reduce it substantially further insucceeding years.

Why the heavy emphasis on debt use to finance acquisitions? Part of the reason lies in theconstraint that until 1996 required Kerry Cooperative to maintain a 51% controlling interest in thePLC. McGrath notes that Kerry apparently has not had to walk away from any acquisitionsbecause of money. However, Brosnan and Friel noted that in the case of the U.S.$402 millionspent on DCA, Kerry would have preferred to use more than 25 million Irish pounds of equityfunding and would have done so if it had not been for the 51% rule [20].

V . Strategies and Practices that Underpin the Kerry Group/PLC's Financing,Expansion and Diversification Initiatives

The Kerry Group/PLC's financing, expansion, and diversification initiatives during the past 25years have required major changes in infrastructure and methods of operation. Those relating toknowledge generation, personnel practices, R&D, and marketing practices are discussed brieflybelow.

Knowledge is the Forerunner of Strategy

Brosnan's comments indicate that the firm's major acquisitions, capital investment decisions,and divestitures were preceded by substantial analysis. In 1995, he described guidelines that haveshaped the firm's product line and the geographic location of the firm's production and marketingactivities, as follow [3]:

• Know which sector you are in or want to be in.

• Know your competitors.

• Know the marketplace.

• Know or anticipate the rapidly changing demands of consumers of your product.

• Know in an international business which decisions can be made by decentralized (local)management and which decisions must be reserved for the corporate office.

Brosnan summarized the importance of these points, saying that knowledge is the forerunnerof strategy. How important knowledge is to the firm's strategies is suggested by comments madeby Kerry officials in connection with the Beatreme and DCA acquisitions.

Recall that Kerry had accumulated knowledge about Beatreme (or its predecessor organization)from about 1983 until the 1988 purchase date. In 1988, some financial analysts argued that Kerrypaid too much for Beatreme. Kerry rejected this reasoning partly because it had followedBeatreme's progress for about five years and had thoroughly assessed the value of the firm. As itturned out, the large profit margins generated by Beatreme helped Kerry manage, and pay downrapidly, a significant part of the potentially burdensome debt load taken on by Kerry for the DCApurchase in 1994.

Kerry's preparations for submitting the bid for DCA provide additional insights about theamount of effort put into knowledge generation. In assembling the bid for DCA, Kerry

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

Babcock Institute Discussion Paper No. 2000-1 15

Group/PLC put in four months of work involving up to 40 people in the final stages of the effort,working on the due diligence and financing arrangements. This allowed Kerry to develop a bidpackage that permitted it to acquire DCA despite strong competition from the British foods group,Dalgety. However, Kerry purchased DCA before all important information was known. Inconceding this point, Brosnan told his bankers that it "would take all of 1995 to fully understandDCA and where it will fit in with our existing businesses [24]."

R&D Expenditures

As the firm evolved heavily into the food ingredients business, the importance of expandingR&D quickly became apparent. Thus, Kerry Cooperative set up an in-house R&D program in theearly 1980s, opting not to rely on the R&D provided by a national government agency.

Brosnan's views on the importance of investments in technology and R&D are revealed in partby a 1995 interview [5]:

The ingredients sector is somewhere between food engineering and pharmaceuticalapplication. It requires companies to invest heavily in technology, as well as research anddevelopment…Continuing with the development of new products in an industry wheretechnology and innovation are so important requires a significant expenditure on researchand development…2.5% to 3.0% of turnover will continue to be spent on R&D because of itsimportance.

In another 1995 interview, Brosnan commented as follows about the importance of R&D [30]:

You must plan for the long-term. Kerry would be millions of dollars more profitable if itdownsized R&D tomorrow morning. We spend heavily in our venture group which is tryingto create the technology of the future. Since we are a technology company, R&D is part ofour strategy. Shareholders have seen Kerry stock outperform the market, so they are veryhappy. Of course, we're also open to short-term ideas that can boost profits overnight.

Changes in Personnel Recruitment Practices

As Kerry Group/PLC has evolved into an international food ingredients and consumer foodproducts company, its personnel needs have changed. The firm's emphasis on technologydevelopment and R&D necessitated recruitment of larger numbers of employees with food science,engineering, and technology backgrounds. The firm's acquisitions also necessitated havingsubstantial in-house capabilities in finance.

The firm's global expansion has placed a premium on diversity and language capabilities.Brosnan commented on this point as follows [30]:

We find differences in American and European thinking, particularly relating tolanguage. We now recruit people out of college who speak two languages plus their nativelanguage. In the Kerry organization, managers are from different backgrounds, nationalities,cultures and have different language skills. It's very important when you to go a newcontinent to have a mix.

Changes in Marketing Practices

Like those relating to personnel, the firm's marketing practices of necessity changed as itmoved away from being a dairy cooperative increasingly into food ingredients and consumerfoods. Part of the difference relates to the need to work closely with final customers for foodingredients and consumer foods.

Hugh Friel, Deputy Managing Director of Kerry Group/PLC, said that the changing nature ofthe firm forced Kerry to stop exporting through the Irish Dairy Board (IDB) in about 1990 [6].Kerry needed to be in position to work with final customers to explain the technical characteristicsof the products and applications of the products. Kerry also wished to be positioned to offer price

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

16 Babcock Institute Discussion Paper No. 2000-2

concessions when necessary to final customers. It is difficult to explain technical characteristics ormake needed price concessions if sales are made through an intermediary such as the IDB.

VI. An Evaluation of Kerry Group/PLC's Corporate Strategies

As noted earlier, the Kerry Group/PLC's corporate strategy is to diversify and grow thebusiness emphasizing differentiated (value-added) food ingredients and consumer food products.This core strategy is supported by a number of other strategies and practices, notably one thatemphasizes growth by acquisition.

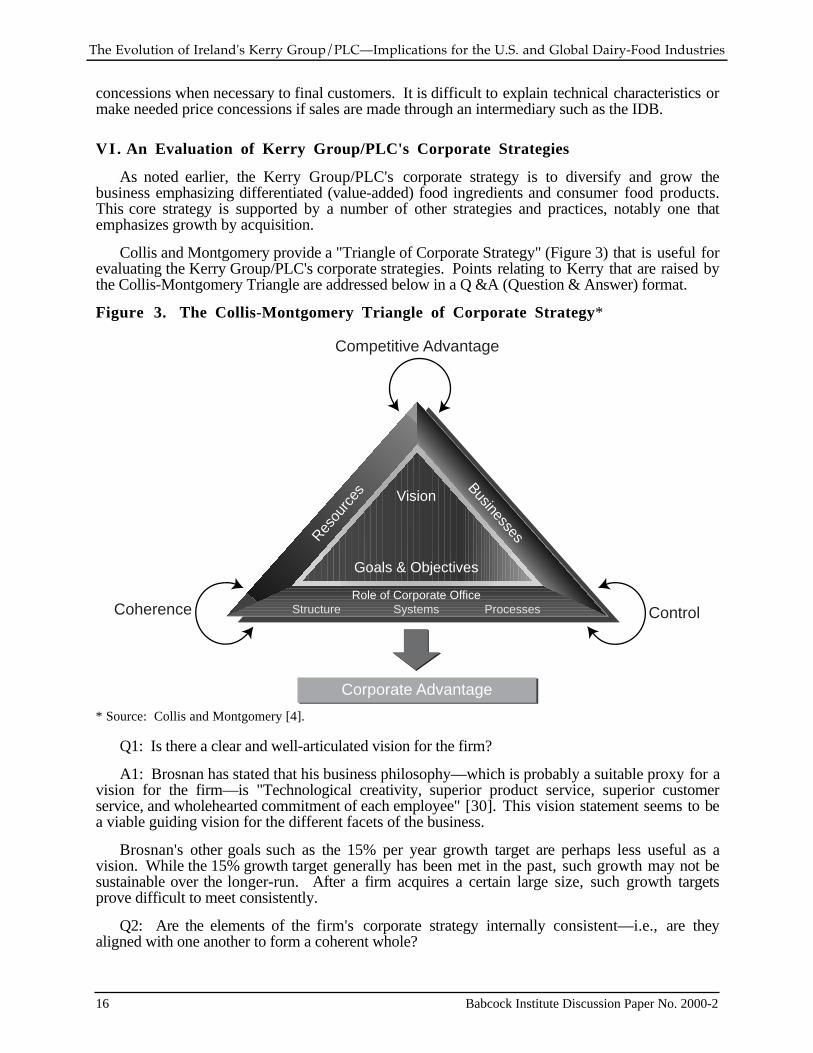

Collis and Montgomery provide a "Triangle of Corporate Strategy" (Figure 3) that is useful forevaluating the Kerry Group/PLC's corporate strategies. Points relating to Kerry that are raised bythe Collis-Montgomery Triangle are addressed below in a Q &A (Question & Answer) format.

Figure 3. The Collis-Montgomery Triangle of Corporate Strategy*

Corporate Advantage

Vision

Competitive Advantage

ControlCoherence

Vision

Goals & Objectives

Role of Corporate OfficeSystems ProcessesStructure

Resou

rces

Businesses

* Source: Collis and Montgomery [4].

Q1: Is there a clear and well-articulated vision for the firm?

A1: Brosnan has stated that his business philosophy—which is probably a suitable proxy for avision for the firm—is "Technological creativity, superior product service, superior customerservice, and wholehearted commitment of each employee" [30]. This vision statement seems to bea viable guiding vision for the different facets of the business.

Brosnan's other goals such as the 15% per year growth target are perhaps less useful as avision. While the 15% growth target generally has been met in the past, such growth may not besustainable over the longer-run. After a firm acquires a certain large size, such growth targetsprove difficult to meet consistently.

Q2: Are the elements of the firm's corporate strategy internally consistent—i.e., are theyaligned with one another to form a coherent whole?

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

Babcock Institute Discussion Paper No. 2000-1 17

A2: This is difficult to assess meaningfully with available information. Certainly the two maindivisions of the firm—food ingredients and consumer food products—are closely related. It isfeasible for the firm to implement strategies and practices that allow the divisions to produceeconomies of scope and complementarities. However, it is unclear whether technologies used toadvantage in one division or location are quickly adopted where appropriate in others. This isdoubtful given the short time between major acquisitions of food ingredient firms by Kerry.However, it is clear that officers of the firm recognize the need for internally consistent strategies.

Q3: Does the firm's strategy fit with the external environment?

A3: The point of this question is that "firms should never forget to assess the underlyingattractiveness of the external environment (industries) in which they compete. No matter howeffective the corporate strategy, if the firm's businesses are tough to make money in, the financialresults of the strategy are likely to be poor" [4, pp. 174-175].

Kerry appears to have developed strategies that address this question exceedingly well. Thefirm recognized early that it was advantageous to de-emphasize businesses that were affected byweather, diseases and EEC (now EU) milk quotas. Kerry has also recognized that foodingredients businesses carry substantially higher profit margins than either the consumer foodsbusiness or the agribusiness functions. Hence, the firm's acquisitions during the late 1980s and1990s focused heavily on ingredient firms. Finally, Kerry’s divestitures—e.g., Spillermills—have purged components of acquired firms that generated low margins or failed tocomplement other aspects of the divisions.

Q4: Is the strategy too risky? Specifically, is the organization being asked to do too much intoo short a time?

A4: Brosnan and other senior managers of Kerry Group/PLC appear to be advocates of"stretch" targets. Collis and Montgomery point out that striking an appropriate balance betweensetting challenging targets and overextending an organization is a difficult task [4, p. 175].

Kerry's managers recognize that firm's employees need time to assimilate major newacquisitions. Moreover, Brosnan and other senior managers didn't make new acquisitions untilafter existing segments of the firm had generated profits needed to pay down debt on previousacquisitions to manageable levels. However, Kerry's new acquisitions during the 1990's certainlywere not made at a leisurely pace. Excessive attention was not paid to these constraints.

Q5: Does the strategy produce value creation that is sustainable?

A5: Kerry's value creation appears to be consistent with ideas advanced by Drucker, Prahaladand Hamel, and other business strategists who claim that the essence of strategy lies in creatingtomorrow's competitive advantages faster than competitors mimic the ones you possess today.Kerry creates competitive advantage partly by being an early mover in acquiring high profit marginfood ingredients businesses. The firm probably can continue to find attractive food ingredientsfirms to acquire for a few more years, but it is difficult to imagine that these acquisitions cancontinue indefinitely. This means that, at some point, the firm will need to squeeze more profitsout of existing businesses or begin to acquire another group of high profit businesses. Valuecreation in the latter areas may be more difficult to achieve than selecting desirable food ingredientscompanies to acquire.

Q6: Are there consistencies between the firm's (a) resources and businesses, (b) businessesand corporate structures, systems and processes, and (c) resources and corporate structures,systems and processes? These points are potentially important for reasons of competitiveadvantage, control and coherence.

A6: Certain aspects of this question are addressed above and need no further discussion.However, Q6 does raise questions about the fit between the acquired firms and Kerry and the long-term profitability of the acquisitions.

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

18 Babcock Institute Discussion Paper No. 2000-2

Collis and Montgomery point out that the benefits and drawbacks associated with acquisitionsinclude those noted below [4, p. 90]:

Benefits Drawbacks

Speed Cost of acquisition

Access to complementary assets Unnecessary adjunct businesses

Removal of potential competitor Organizational clashes may impede integration

Upgrade corporate resources Major commitment

Several of these points have been mentioned in previous sections. Speed of growth was afactor in several of the acquisitions. The Dalgety acquisition resulted in "acquiring an acquirer"which had snapped up food ingredients businesses in Europe prior to the acquisition by Kerry.Thus the Dalgety acquisition eliminated a competitor for high profit margin ingredients business inEurope. Kerry's acquisitions in North America gave the firm access to valuable corporateresources in the form of customer bases on the North American continent.

Among the drawbacks, the cost of acquisition is perhaps most important and worthy of specialcomment. As noted previously, analysts questioned whether Kerry had paid too much for bothBeatreme and DCA. Such questions are raised for the following reasons noted by Collis andMontgomery [4, p. 91]:

When making an acquisition, managers often lose sight of the fact that acquisitions arepurchased in a market—the market for corporate control—that functions reasonably well.Importantly, the going price for a firm reflects not only the value of the firm as a stand aloneconcern, but also incorporates the incremental value the market feels the assets would have toa host of potential acquirers. Unless the winning bidder can use the assets in an unusual way,and create value that other bidders could not, it should not expect to earn economic rents onassets it purchases in the market…value created in most mergers is captured by theshareholders of the acquired firms.

Kerry recognizes these points. Moreover, it is possible that Kerry can use the acquiredresources in unusual ways. Certainly complementarities between the Kerry's dairy ingredientsbusinesses and the cereal-based and fruit-based ingredients businesses acquired in the 1990s mightmake some of those later acquisitions more valuable to Kerry than to competing bidders.Moreover, Kerry did thoroughly analyze the potential profitability of the acquisitions beforemaking them under its "knowledge is the forerunner to strategy" operating procedure. It also mustbe conceded that Kerry's acquisitions in the ingredients business appear to be profitable or at leastnot a problem for the firm.

Nonetheless, the "cost of acquisition" drawback will face Kerry in the future. This is not atrivial point. Some of Kerry's future acquisitions could fit the description of the typicalacquisition, which earns no economic rent for the purchaser.

VII. Implications of the Strategies of the Kerry Group/PLC for U.S. and OtherDairy-Food Exporters and Investors

Certain ideas flow from Kerry's strategies and practices that have implications for U.S. andother dairy-food exporters and investors:

1) Ability to relate a company to its environment is important . Faced with difficult conditionsin the 1970s and mid-1980s, the firm exhibited a noteworthy ability to recognizeopportunities for diversification into value-added products. The firm recognized early thatits basic options were to "diversify or merge." If the firm had chosen to merge rather thandiversify, it probably would now be a small part of one of Ireland's larger dairy companiesrather than a multi-billion dollar multinational firm.

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

Babcock Institute Discussion Paper No. 2000-1 19

2) Continuity of top management is important . Denis Brosnan, Managing Director of theKerry Group/PLC, has served as top manager of the firm or its predecessors since 1972.Moreover, two of the firm's Deputy Managing Directors have been with firm since 1972and a number of Kerry's other top managers have been with the firm since the mid-1970s.This has permitted the firm to pursue consistent strategies over an extended time period. The continuity and trust generated by Brosnan, in particular, has permitted the firm tochange from a position where Kerry Cooperative, Inc. held 51% control to a positionwhere the Cooperative held about 37% of the Group's stock. This change in controlpermitted greater use of equity capital for expansion purposes and helped the firm gainother important advantages.

3) Knowledge is a key f orerunner to strategy . The Kerry Group has made importantacquisitions and other strategic moves only after careful (and sometimes lengthy) analysis.The analysis appears to have converted certain of Kerry's acquisitions from the excessivelyrisky category to the manageable risk category.

4) Early mover advantages are important . The firm has evolved into one of the world'slargest food ingredients firms, partly because of early recognition of the importance ofacquiring Beatreme and DCA. While corporate "stretch" was involved in theseacquisitions, the company probably would now be the poorer if it had not made theacquisitions. The two acquired firms exhibit complementarities and strong profitgenerating capacity.

5) Latin America and Asia are growth m arkets for dairy and other food products . Kerry'sdecision to expand its food ingredients business into Latin America and Asia recognizesthat these markets are growth markets. The firm's ability to serve fast food companies thatare expanding rapidly in these markets should contribute to profits.

6) A firm's infrastructure must change substantially when it evolves as dramatically as KerryGroup/PLC . The firm changed its financing, R&D, personnel recruitment, and marketingpractices to reflect what it has become. Kerry's capital investment decisions were alsomade to support the changing nature of the firm as it evolved from a commodity-orienteddairy cooperative into a global food ingredients and consumer foods company.

7) Kerry's conversion to a coopera tive/PLC was a necessary but not sufficient condition forsuccess . In the business environment of the mid-1980s, Kerry Cooperative's decision toconvert to a cooperative/PLC was a sound strategic move. This move helped Kerry tomake certain early acquisitions. But many of the firm's acquisitions in the late 1980s and1990s were made mostly with debt rather than stock equity. The continuity of topmanagement, the Managing Director's vision, the firm's bold acquisition practices, and thefirm's knowledge of customers, competitors, and markets go further in explaining Kerry'ssuccess than its PLC structure.

8) Acquisitions possess inherent drawbacks . Kerry appears to have made mostly successfulacquisitions to build the firm into a world leader in food ingredients. However, unlessKerry can continue to use acquired assets in an unusually productive way, and create valuethat other bidders cannot, it should not expect to earn economic rents on assets it purchasesin the market. This fact of life will affect Kerry's future acquisitions.

9) The Kerry Group/PLC model will not be easily replicated . Kerry's experience should beof interest to U.S. firms that are contemplating expansion into international dairy-foodmarkets, and to organizations, such as the New Zealand Dairy Board, that are consideringfundamental changes in global marketing practices. However, it is apparent that uniqueconditions in the business environment in the 1970s in Ireland, a complex bundle ofmutually-reinforcing strategies, and early mover advantages (which will make it expensivefor others to gain large positions in international ingredients markets in particular) havecontributed to the Kerry Group PLC's successes. Opportunities to assemble thiscombination of developments and strategies will not occur frequently.

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

20 Babcock Institute Discussion Paper No. 2000-2

REFERENCES

1. Avonmore Waterford Group plc, "Corporate Identity—A New Identity for a NewMillennium," 1999.

2. Brosnan, D., Managing Director, Kerry Group, "Address to Irish Grassland AssociationConference," April 19, 1996.

3. Canniffe, M., "Clear focus the key to success—Researching the competition and analyzingstrengths and weaknesses are essential," The Irish Times , April 28, 1995, Supplement p. 6.

4. Collis, D.J. and C.A. Montgomery, Corporate Strategy—Resources and the Scope of theFirm , Irwin, McGraw-Hill Publishing, 1997.

5. Curran, R., "The right ingredients—Kerry tapping into huge market in U.S. and LatinAmerica," Irish Independent , June 8, 1995, p. 5.

6. Friel, H., Deputy Managing Director, Kerry Group, Interview Conducted by W.D. Dobsonon June 5, 1996 in Tralee, Ireland.

7. Jacobson, R.E. and C. O'Leary, Dairy Co-op Issues in Ireland—with Special Reference toPLC Activities ," Litho Press, Midleton Co., Cork, Ireland, July 1990, 144 pages.

8. Kerry Group plc, Annual Report, 1995.

9. Kerry Group plc, Annual Report, 1998.

10. Kerry Group plc, Building a Global Business, 1998.

11. Kerry Group plc, Interim Report, 1999.

12. Kerry Group/PLC, "Our History—Building an Irish Multinational," Tralee, Ireland, 1998.

13. Lexis-Nexis Academic Universe, "Kerry Group plc," 1999.

14. McGrath, B., "Co-op to cut stake in Kerry Group to 39%," The Irish Times , May 16, 1996,p. 17.

15. McGrath, B., "Dairying becoming less important as Kerry Group expands horizons," TheIrish Times , November 8, 1994, p. 14.

16. McGrath, B., "Kerry's Cash Crop," The Irish Times , May 31, 1996, Supplement p. 18.

17. McGrath, B., "Kerry Group has (pounds) 1bn for right acquisition," The Irish Times , May26, 1999, p. 16.

18. McGrath, B., "Kerry in $80m buy from Swiss," The Irish Times , October 1, 1999, p. 51.

19. McGrath, B., "Kerry targets Argentina and the Far East for expansion," The Irish Times ,June 7, 1995, p. 15.

20. McGrath, B., "Kerry to expand borders to the Far East," The Irish Times , May 31, 1996,Supplement p. 18.

21. McGrath, B., "Kerry to use strong cash flow to cut borrowing," The Irish Times , March 8,1995, p. 14.

22. McGrath, B., "Mega deals create (pounds) 660m debt," The Irish Times , January 27, 1998,p. 18.

23. McGrath, B., "Speed the key as Kerry wins the battle for DCA," The Irish Times ,November 11, 1994, Supplement p. 3.

24. Murdoch, B., "Has Kerry Foods paid too much for DCA?" The Irish Times , December 19,1994, p. 14.

25. O'Kane, P., "Co-op transformed by commonsense approach," The Irish Times , November8, 1994, p. 14.

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

Babcock Institute Discussion Paper No. 2000-1 21

26. O'Keefe, B., "Kerry Co-op members to reduce stake," The Irish Times , July 16, 1996,p. 16.

27. O'Sullivan, J., "Kerry Group pays (pounds) 394m for food ingredients businesses ofDalgety," The Irish Times , January 27, 1998, p. 18.

28. Porter, M.E., Competitive Strategy—Techniques for Analyzing Industries and Competitors ,The Free Press, 1980.

29. Smith, M., "Food Co-operative Set To Float," London Financial Times , July 8, 1986, p. 19.

30. Toops, D., "Taking the high road with Kerry Group's Denis Brosnan—Ireland-basedKerry's managing director talks about how his company got so big," Food Processing ,September 1995, pp. 19-21.

31. Worldscope/Extel Database, "Company Briefs/Company Financials—Kerry Group PLC,"1999.

32. Wright Investors' Service, "Kerry Group plc," 2000http://profiles.wisi.com/profiles/scripts/largechart.asp?cusip=C372ER900&curconv=978.

The Evolution of Ireland's Kerry Group/PLCÑImplications for the U.S. and Global Dairy-Food Industries

22 Babcock Institute Discussion Paper No. 2000-2

Appendix. Kerry Group/PLC's Capital Investments, 1995-98*

Year and Country ofCapital Investment

Nature of Capital Investment

1995UK A new central warehouse and distribution facility was completed at

Hyde.

1996US An investment program for a technical center in Beloit, Wisconsin

was started. Investment was made in Evansville, Indiana foodcoatings plant.

France A fruit research center was established at Apt as part of the Ciprialoperations.

UK Investments were made in the fruit processing sector and in the Hydeand Durham meat and ready meals processing plants.

Ireland The Limerick meat processing facility was upgraded.

1997UK The direct sales division was relocated to new headquarters in

Andover, 50 new vans were secured, and two new distributioncenters were opened in Carlisle and Newbury. A facility was beingdeveloped at Burton on Trent site to handle premium chilled readymeals.

Ireland Limerick site extended for increased production of value-addedchicken products. Forty vehicles were delivered to aid in-housedistribution.

US Culinary unit developed at R&D Center in Beloit, Wisconsin.

Asia Pacific Region Technical center/administrative headquarters built to serve region.

1998UK Completed investment program at Attleborough site to provide

extended facilities for ready-to-cook meats.

Canada Major investment program at Glen Arrow Products followingacquisition.

Poland Investment in fruit preparation facilities.* Source: Sevmour-Cooke Ltd., “Europe’s Tops Food Groups, Kerry Group, Tralee, Co. Kerry, Ireland,” 1998.