balance of payments manual - imf

TRANSCRIPT

BALANCE OF

PAYMENTS

M ANUAL

I N T E R N AT I O N A L M O N E T A R Y F U N D

iv

Contents

Foreword ix

Preface xi

CONCEPTUAL FRAMEWORK

I. Introduction 3

Purposes of the Balance of Payments Manual 3Changes from the Fourth Edition 3Uses of Balance of Payments and International Investment Position Data 4Structure of the Manual 5

II. Conceptual Framework of the Balance of Payments and International Investment Position 6

Definitions 6Principles and Concepts 6Double-entry System 6Concepts of Economic Territory, Residence, and Center of Economic Interest 7Principles for Valuation and Time of Recording 7Concept and Types of Transactions 8Changes Other Than Transactions 9

III. Balance of Payments and National Accounts 10

Introduction 10Relationship Between the SNA and Principles Underlying the Balance of Payments 10Classification 11Integrated Economic Accounts 11

IV. Resident Units of an Economy 20

Concept and Definition of Residence 20Economic Territory of a Country 20Center of Economic Interest 20Resident Institutional Units 21Residence of Households and Individuals 21Residence of Enterprises 22Residence of Nonprofit Institutions 24General Government 24Regional Central Banks 25

V. Valuation of Transactions and of Stocks of Assets and Liabilities 26

Concept of Market Price 26Transactions and Market Price 26Valuing Transactions in the Absence of Market Price 26Market Price Equivalents 26Affiliated Enterprises 27Noncommercial Transactions 28Financial Items 28Valuation of Stocks of Assets and Liabilities 28

VI. Time of Recording 30

Principle of Timing 30Application to Goods 30Exceptions to the Change of Ownership Principle 31Applications to Other Transactions 31Other Timing Adjustments 32

VII. Unit of Account and Conversion 33

Unit of Account 33Conversion Principles and Practices 33Multiple Official Exchange Rates and Conversion 34Black or Parallel Market Rates 34

STRUCTURE AND CLASSIFICATION

VIII. Classification and Standard Components of the Balance of Payments 37

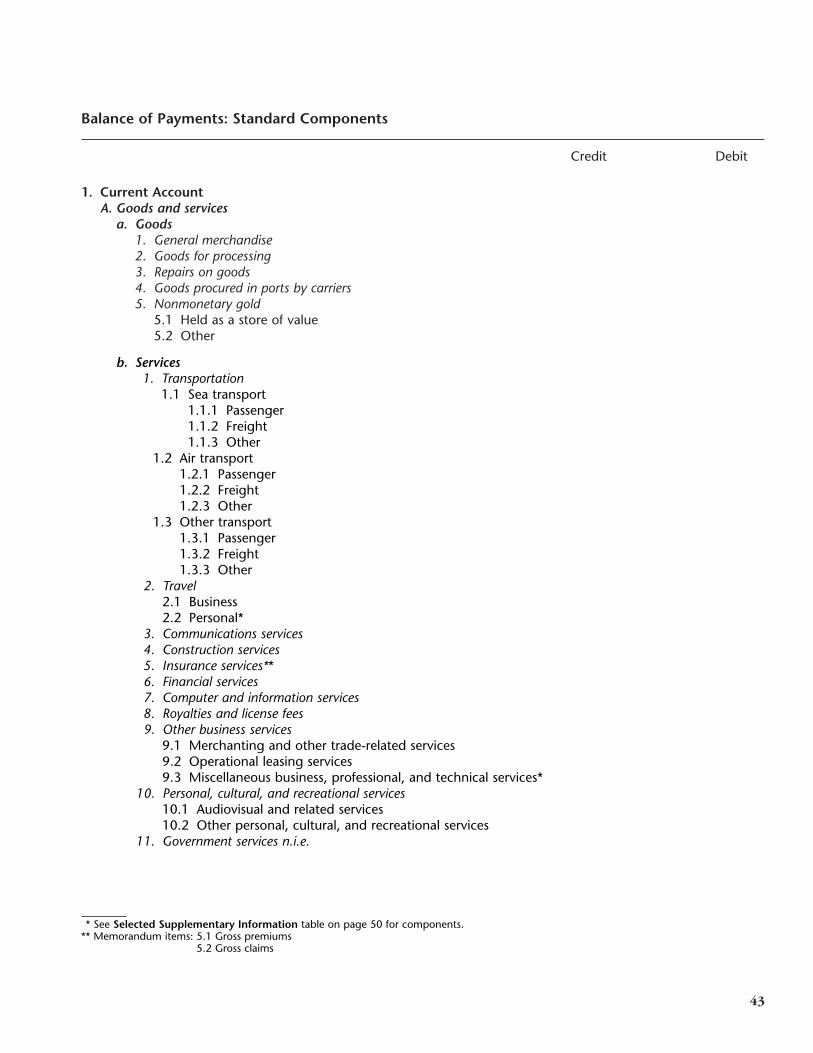

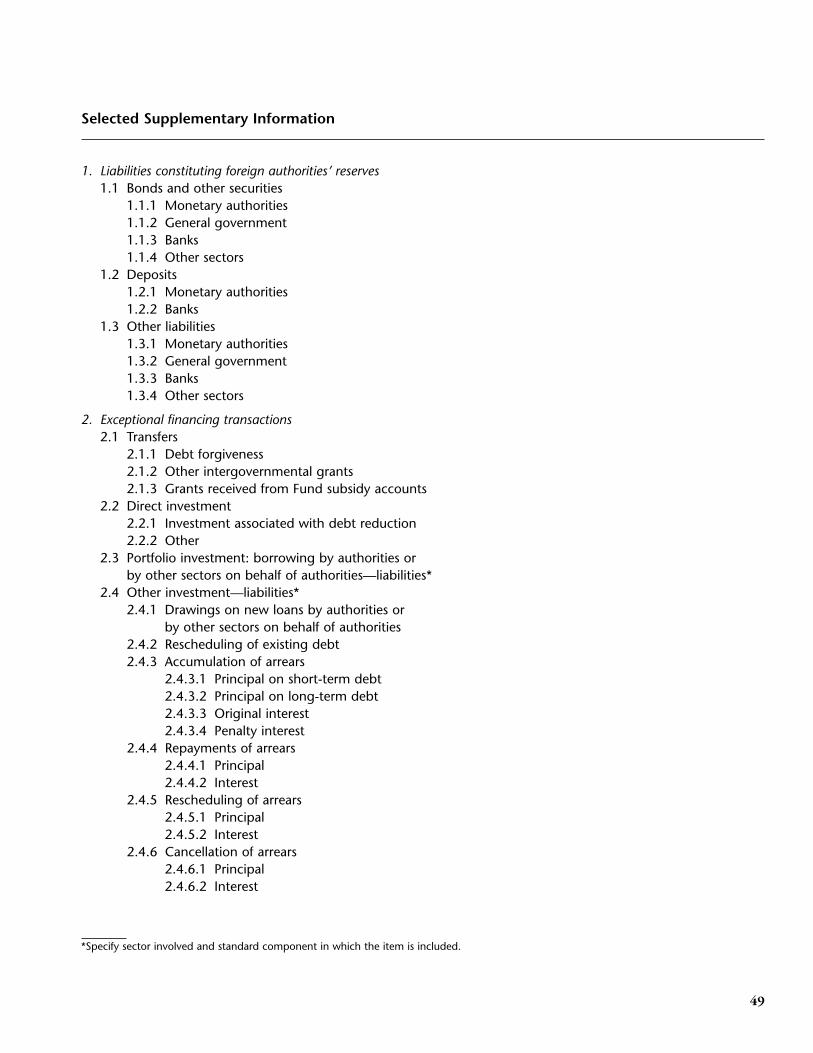

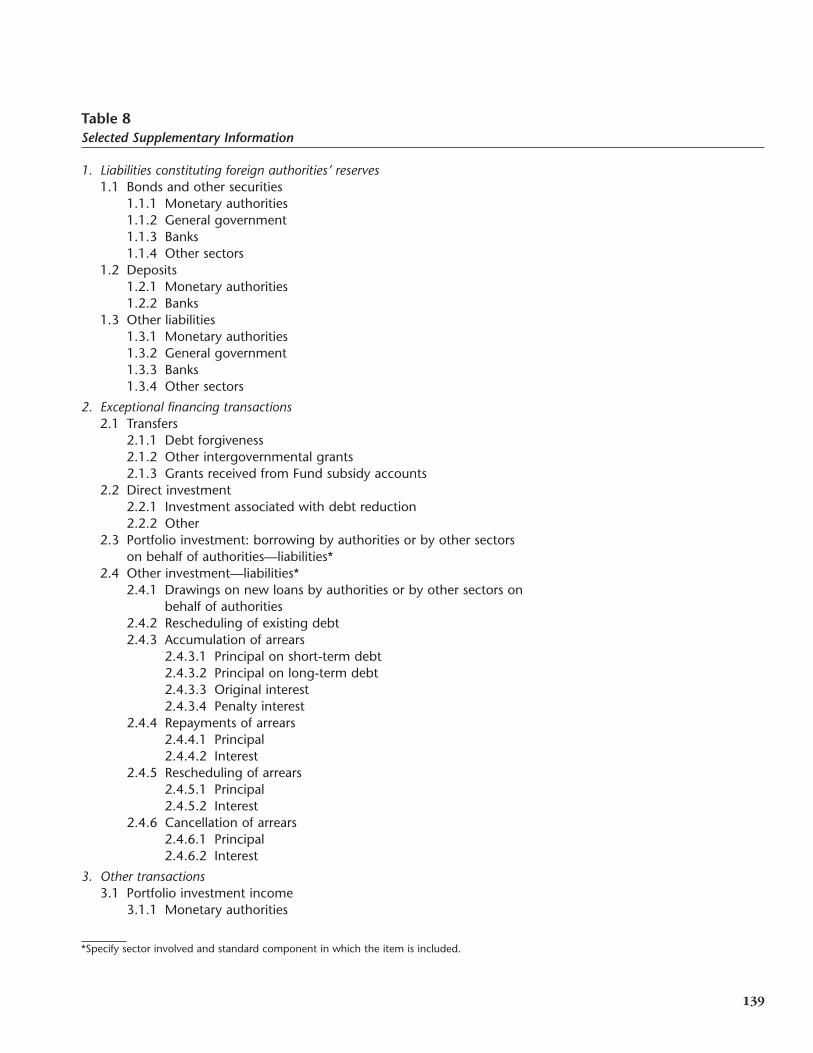

Structure and Classification 37Standard Components 37Net Errors and Omissions 38Major Classifications 38Detailed Classifications 38Balance of Payments: Standard Components Table 43Selected Supplementary Information Table 49

IX. Structure and Characteristics of the Current Account 51

Characteristics and Classification 51Gross Recording, Valuation, and Time of Recording 52

X. Goods 54

Coverage and Principles 54Definitions 54Change of Ownership 55Goods Classified Under Other Categories 57Special Types of Goods 57Time of Recording 58Valuation 58

CONTENTS

v

XI. Transportation 61

Definition and Coverage 61Passenger Services 61Freight Services and Conventions for Recording 61Rentals of Transportation Equipment with Crew 62Supporting and Auxiliary Services 62

XII. Travel 64

Nature of Travel Services 64Definition 64Types of Travel 64Goods and Services Covered 65

XIII. Other Services 66

Coverage 66Definitions 66

XIV. Income 70

Coverage 70Definition and Classification 70Time of Recording of Investment Income 72Measurement and Recording of Direct Investment Earnings 72Stock Dividends, Bonus Shares, and Liquidating Dividends 73

XV. Current Transfers 74

Definition and Coverage 74Distinction Between Current and Capital Transfers 74Classification 75Valuation and Timing 76

XVI. Structure and Characteristics of the Capital and Financial Account 77

Coverage 77Capital Account 77Financial Account 78Liabilities Constituting Foreign Authorities’ Reserves 82Valuation and Timing 82

XVII. Capital Transfers and Acquisition or Disposal of Nonproduced, Nonfinancial Assets 83

Coverage 83Capital Transfers 83Classification 83Acquisition or Disposal of Nonproduced, Nonfinancial Assets 84

CONTENTS

vi

XVIII. Direct Investment 86

Concept and Characteristics 86Direct Investment Enterprises 86Direct Investors 87Direct Investment Capital 87Extent of Net Recording 88Valuation of Flows and Stocks 89Other Special Cases of Direct Investment Enterprises 89Selected Supplementary Information 89

XIX. Portfolio Investment 91

Coverage 91Classification and Definitions 91Selected Recording Issues 92Valuation 94

XX. Other Investment 95

Coverage 95Classification 95Definitions and Recording 95

XXI. Reserve Assets 97

Concept and Coverage 97Identification of Reserve Assets 97Exclusion of Valuation Changes and Other Adjustments 99Classification 99Valuation 100Interpretation of Changes in Reserve Assets 100

XXII. Supplementary Financial Account Information 101

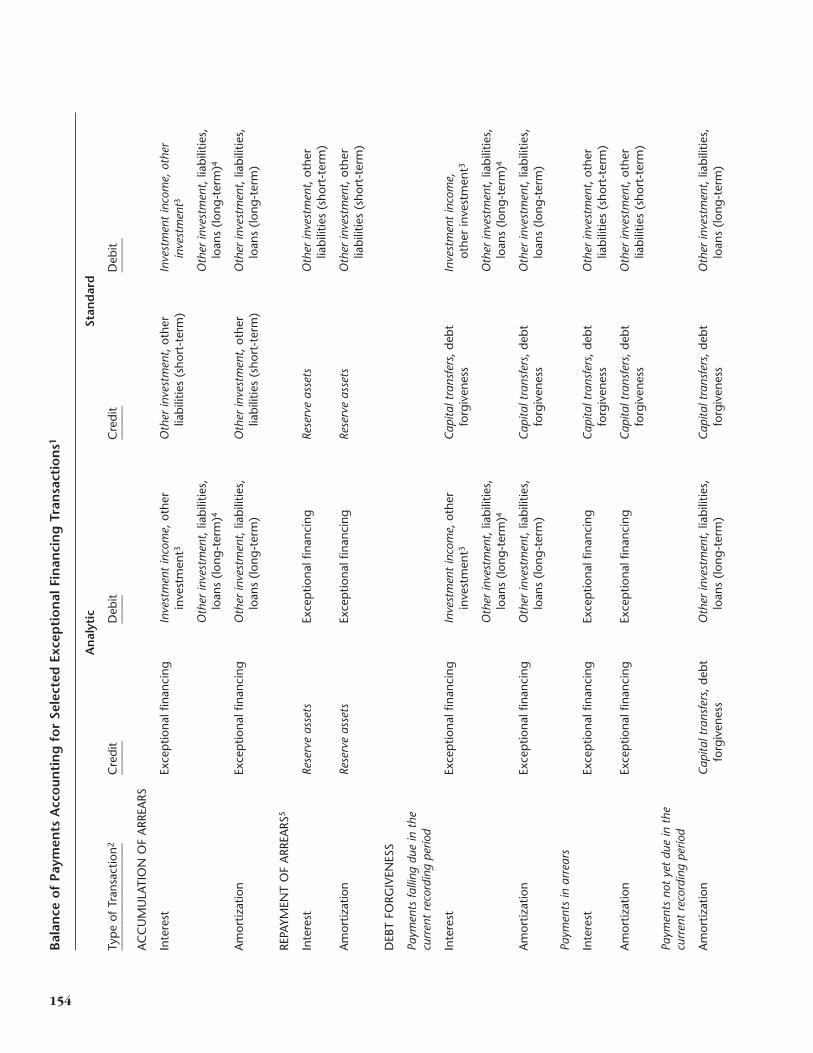

Coverage 101Liabilities Constituting Foreign Authorities’ Reserves 101Exceptional Financing and the Balance of Payments 102Balance of Payments Accounting for Selected Exceptional Financing Transactions 102Foreign Sources of Financing 103

XXIII. International Investment Position 104

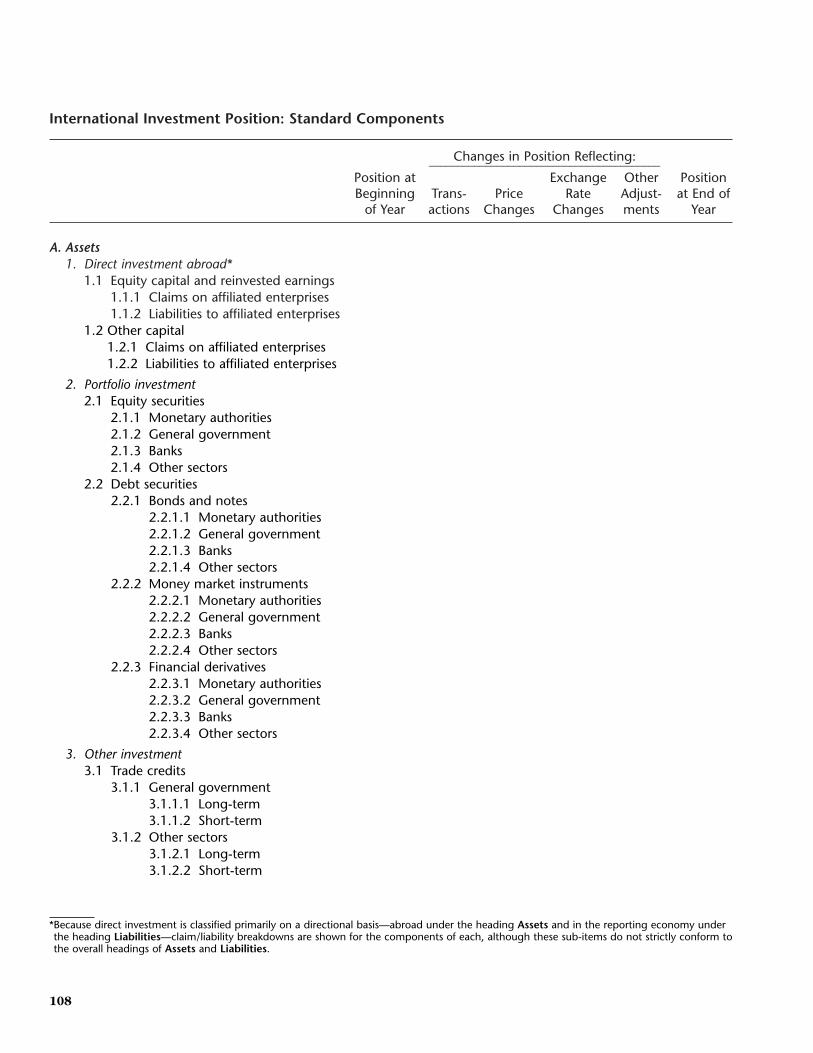

Concept and Coverage 104Classification 104Valuation of Components 105Relationship of the International Investment Position to External Debt 106Investment Income, Rates of Return, and the International Investment Position 106International Investment Position: Standard Components Table 108

CONTENTS

vii

REGIONAL ALLOCATION

XXIV. Regional Statements 115

Regional Allocation Principles 115Problems and Limitations 116Analytical Implications 117Selection of Regions 117

APPENDICES

I. Relationship of the Rest of the World Account to the Balance of Payments Accounts and the International Investment Position 121

II. A Note on Sectors 145

III. Balance of Payments Classification of International Services and the Central Product Classification 146

IV. Accounting for Exceptional Financing Transactions 150

V. Selected Issues in Balance of Payments Analysis 158

INDEX

CONTENTS

viii

Foreword

Measurement of the external positions of membercountries has been a central feature of InternationalMonetary Fund operations since inception. Suchmeasurement is conducted in the dual context of Fundresponsibility for surveillance of countries’ economicpolicies and provision of financial assistance in supportof adjustment measures to correct balance of paymentsdisequilibria. Consequently, the Fund has a compellinginterest in developing and promulgating appropriateinternational guidelines for the compilation of soundand timely balance of payments statistics. Suchguidelines, which have evolved to meet changingcircumstances, have been embodied in successiveeditions of the Balance of Payments Manual (theManual) since the first edition was published in 1948.Because of the important relationship between externaland domestic economic developments, timely, reliable,and comprehensive balance of payments statisticsbased on an appropriate and analytically orientedmethodology are an indispensable tool for economicanalysis and policy making. Indeed, with the growinginterdependence of the world’s economies, the needfor such statistics—which reflects in part the underlyingmovement towards greater liberalization and integrationof markets—has increased over time.

I am particularly pleased to introduce the fifth editionof the Manual, which addresses the many importantchanges and innovations that have occurred ininternational transactions since the fourth edition waspublished in 1977. The fifth edition of the Manual alsoaddresses, for the first time, the important area ofinternational investment position statistics. In addition,concepts in the Manual have been harmonized, asclosely as possible, with those of the revised System ofNational Accounts 1993 and with the Fund’smethodologies pertaining to money and banking andgovernment finance statistics.

The revised Manual has been prepared by the Fund’sStatistics Department in close consultation with balanceof payments experts in member countries andinternational and regional organizations (including theStatistical Office of the European Communities, theOrganisation for Economic Cooperation andDevelopment, the United Nations, and the WorldBank). The process underlying the revision of theManual demonstrates the spirit of internationalcollaboration and cooperation, and I would like tothank all of the national and international expertsinvolved for their invaluable assistance. In this regard, Iam particularly grateful to Mr. Pierre Esteva, chairmanof the Fund’s Working Party on the StatisticalDiscrepancy in World Current Account Balances, and toBaron Jean Godeaux, chairman of the Working Party onthe Measurement of International Capital Flows. Theirassessments of the effects of the unprecedentedchanges in the conduct of international transactionscontributed significantly to the revision of the structureand classification of the international accounts.

I would like to commend the Manual to compilersand users around the world and to urge membercountries to adopt the conceptual guidelines of the fifthedition as the basis for compiling balance of paymentsand international investment position statistics and forreporting this information to the Fund.

Michel CamdessusManaging Director

International Monetary Fund

W-X?7@1?

?J@@5?g?)X?W&@@h?@1?7@@@1?f?@@@5?@(MW@?fJ(Y@H? @((Y?75?e?W.Y?@ ?C(YJ@H?eW.Y?J5 @@H?

?@e75f7He7H @5J@e@?e?J5??J@? @H7@e@@e?7H??@@?heW& @?@@?J@HeJ@f@?h?W&@L? ?J@?

?J@5?@@?e75e?75?hW&Y@@? W&@L?7@He@??J@He?@H?h75?@ 7@@1?@@??75?W&@?e?@h?J@H?@)K ?J(M?@J@@??@e7<fJ@h?75??@@@@? W&H??3L? ?O2@@@@?g7@5??@)X@?f7@h?@H??@@@H? ?W&5e?N)X ?O2@@0M??@H?g@@H??@@@5?f@5h?@fW@ O&(Yf@)X? ?O2@@0M?f?@h@@e?@@@H?f@?hJ@e?W&@W26X O2@0Y?f?I/K ?@?@@0M?h?@h@@e?@@5g@@h75e?7@@@@@)K?heO2(MheV46K O2@@@@?@ J@h@@e?@(Yf?J@Hh3Ue?@@@(MI'@@@@@@@6?2@@@0Y?hfI4@6K? O2@@@@0M 75h@5e?(Y?f?@@LhN1e?@@0Y??V+?40?@?4@0?@M? ?I4@6T-T&K ?O-KO)T2@@@@0M 3Uh(Yhe?N@1hJ@e?@M? I+R4@@@@@@@@@@@@@@@@@@@0R4@@0M S1h

?J@@h@@L? *@h?'@@hN@)?@? V'h?V4@h?3@@5?

?V40Y?

O@K??'@@@@@@@@@?@??V4@0M

ix

Preface

The fifth edition of the Balance of Payments Manual(the Manual) continues the series of international standards that have been issued by the InternationalMonetary Fund (IMF) for providing guidance to membercountries in the compilation of balance of payments andrelated data on the international investment position.

Since the fourth edition of the Manual was publishedin 1977, important changes have occurred in the man-ner in which international transactions are conducted.These changes are, in particular, a result of the liberal-ization of financial markets, innovations in the creationand packaging of financial instruments, and newapproaches to the restructuring of external debt. Inaddition, there has been unprecedented growth in thevolume of international trade in services. All thesedevelopments have necessitated changes in the treat-ment and classification of such transactions within thestructure of the balance of payments accounts. Further-more, since publication of the fourth edition, experiencewith application of that edition has brought to light anumber of instances in which guidelines could usefullybe augmented and recommendations clarified. Anadditional impetus to the preparation of the fifth editionof the Manual was the work undertaken to revise thesystem of economic and financial statistics encompassedin the System of National Accounts 1993 (SNA). Therewas the need to achieve, to the maximum extentpossible, harmonization between the two systems andwith IMF statistical systems pertaining to money andbanking statistics and government finance statistics.

The fifth edition of the Manual provides internationalguidelines for the compilation of data for an articulatedset of international accounts encompassing the measure-ment of external transactions (balance of payments), onthe one hand, and the stock of external financial assetsand liabilities (the international investment position) onthe other. This edition of the Manual provides explicitlinks between the outstanding stock of external financialassets and liabilities and corresponding changes thatoccur, during specified periods, in these external finan-cial instruments. The changes reflect transactions,valuation changes, and other adjustments in the relevantfinancial instruments. The delineation of an articulatedset of international accounts represents a major shift in

orientation from the fourth to the fifth edition. The fifthedition also differs from its predecessor in other impor-tant respects. First, the current account of the balance ofpayments is redefined to exclude capital transfers,which are included in an expanded and renamed capitaland financial account. This change provides for agreater degree of harmonization and integration withthe SNA in terms of the underlying concepts and theidentification of major aggregates. Second, within thecurrent account, clear distinctions are made amonggoods, services, income, and current transfers. As areflection of the heightened analytical and policyinterest in data on international trade in services(particularly in the context of the General Agreement onTariffs and Trade negotiations on services) considerabledisaggregation is introduced in the classification ofinternational services transactions.

The classification of the financial account follows ahierarchical structure for functional categories, asset orliability distinctions, instrument specification, sectoriza-tion, and the distinction between long- and short-terminstruments. In addition, the classifications underlyingthe income components of the current and financialaccounts and the international investment position areclosely aligned to enhance analytic potential.

Despite the extensive revision of the Manual, IMFrecommendations for balance of payments compilationmaintain a high degree of continuity. Thus, compilerswho have been producing statistics that conformreasonably well to the standards established in previouseditions should not experience great difficulty in adapt-ing procedures for data collection or in reportingaccording to the recommendations of the fifth edition.The basic concepts and principles in the Manual remaingenerally valid and any necessary adjustments may bereadily effected within a largely unchanged theoreticalframework.

The fifth edition of the Manual was produced by theIMF Statistics Department—primarily through the workof a consultant, Mr. Jack Bame (formerly the associatedirector for international economics at the Bureau ofEconomic Analysis, U.S. Department of Commerce), andthrough close consultation with national compilers of

xi

PREFACE

balance of payments statistics and experts frominterested international and regional organizations. Thereports of the IMF working parties on the StatisticalDiscrepancy in World Current Account Balances and onthe Measurement of International Capital Flows alsocontributed to the development of the Manual. Inaddition, an advisory group of IMF staff providedassistance in articulating IMF operational and analyticneeds in the area of balance of payments statistics. Themembers of the group were Mr. Bruce Smith, senioradvisor in the Southeast Asia and Pacific Department;Mr. Peter Clark, assistant director in the ResearchDepartment; and Mr. Michael Kuhn, division chief in thePolicy Development and Review Department. Theproject was supervised by Mr. Mahinder S. Gill, assistantdirector for the Balance of Payments and External DebtDivision in the IMF Statistics Department. Most of theoriginal drafting was done by Mr. Bame. He also wasresponsible for subsequent redrafting undertaken toreflect comments received from national compilers andconcerned international and regional organizations andto incorporate conclusions that were reached at themeeting of balance of payments experts held at IMFheadquarters in March 1992. Through comments onearlier drafts or through drafting of selected chaptersand appendices, staff of the Balance of Payments andExternal Debt Division made specific contributions: Mr.Gill (Chapter 3 and Appendix 1), Mr. Jan Bové and Mrs.Florencia Frantischek (Appendix 4), and Mr. AbulSiddique (Appendix 3). Mr. Clark of the ResearchDepartment made a particularly valuable contribution bypreparing Appendix V, which addresses selected issuesin balance of payments analysis. Ms. Nancy Basham,Statistics Department, edited and coordinated printproduction and Ms. Suzanna Persaud, administrativestaff of the Balance of Payments and External DebtDivision, typed the various drafts and the final versionof the Manual.

The IMF benefitted immensely from the contributionsand comments made by experts who participated in theMarch 1992 meeting of balance of payments experts.Their deliberations culminated in a set of conclusionsthat, coupled with further consultation through corre-spondence, formed the basis for redrafting and finalizingthe fifth edition. The IMF staff wishes to acknowledge,with thanks, indebtedness to the following experts in

xii

national balance of payments offices and to represen-tatives from regional and international organizations whoparticipated in the meeting and contributed to thepreparation of the Manual.

Australia Ms. Barbara DunlopBrazil Ms. Maria Oliveira NabaoCanada Ms. Lucie LalibertéChile Mrs. Teresa Cornejo BlackChina Ms. Wang LingfenFrance Mr. Jacques Cuny

Dr. Marc AuboinGermany Dr. Rudolf SeilerHungary Mrs. P. HorvathIran Mrs. Mehrangiz TavassoliItaly Dr. Antonello BiagioliJapan Mr. Shinichi Yoshikuni

Mr. Takashi KoriKenya Mr. Pius P. KallaaLibya Mr. Ali Ramadan ShnebeshMexico Mr. Jorge CarrilesNetherlands, The Dr. Marius van NieuwkerkSaudi Arabia Mr. Mohammed Al-Hakami

Mr. Mohanna Al-MohannaSweden Mr. Gunnar BlombergUnited Kingdom Mr. John E. Kidgell

Mr. Bruce BuckinghamUnited States Dr. J. Steven LandefeldZaire Ms. Nkobafily Marie

Marthe LebugheEUROSTAT Mr. J. C. RomanOECD Mr. Erwin VeilUN Mr. Jan van TongerenWorld Bank Datuk Ramesh Chander

John B. McLenaghanDirector, Statistics DepartmentInternational Monetary Fund

@? O2@6X?W2@@@@1?7@(M?@@?

?J@(Y??@@?W&@He?@@?7@5?e?@@?

?J@(Y?e?@@??7@Hf?@@?J@5?fJ@@?7@H?f7@5?@5g@@H?

?J@Hf?J@@he@@@6X??7@?f?7@5g?@@?@@@@1??@@?f?@@Hg?@@?e@@@??@5?fJ@@?hf@@5?J@H?f7@5?e@@g?J@@H?7@g@@H?e@@g?7@5@@f?J@5hfJ@@H@@f?7@Hhf7@@?@@fJ@@?he?J@@5? ?W2@hf@@f7@5?he?7@(Y? W&@5hf@@f@@H?heJ@(Y ?W&@(Yhf@@e?J@5he?W&@H? ?W-X W&@(Y?hf@@e?7@Hhe?7@5 W&@1 ?W&@(Yhg@@e?@@?heJ@@H 7@@5 W&@(Y?hg@@?@@@5?h?W&@@= ?J@@(Y ?O&@(Y@@?N@@H?hW&@@>@@@ ?7@@H? ?W2@@(Y?3@e@5he7@@S@@@@heO2@@ J@@5 W&@@(YN@@@@Hh?J@@@(MW@@hW2@@@@ 7@@H ?W&@@0Y??@@@@?hW&@@0YW&@5g?W&@@@@@@@6X ?J@@5? O&@@

@(?3@@5?g?W&@(Me7@@HgW&@@@@@@@@@) W&@@H? W2@@@@?C(Ye@@H?gW&@(Y??J@@5?g7@@@@@0M?@@H 7@@5he?O2@@@@? ?W&@@(M?@@H??7@@L?g7@@HeW&@(Y?O26Xe3@@@(MeJ@@?heO2@@@? ?J@@@Hhe@@@@@@@?gO2@@6XeW&@@(Y@@eJ@@@1?f?J@@5?e7@@HW2@@@1e?@@(Y??W&@5?hO2@@@@@? O&@@@?he@@@@@@@@@@@@@@@@@@@)KO&@@(Y?

7@@@@?fW&@(Y??J@@@T&@@@@5e7@(Ye?7@@H?gW2@@@@(M ?W2@@@@@@@6XfO2@@@@@@@@@@@@@@@@@@0?'@@@@@0Y@@g?W&@(YeW&@@>@@@X@@H?J@(Y?eJ@@5g?W&@@@@0Y?g?O2@6X ?O2@6XfO&@@@@@@@@@)KO2@@@@@@@@@0?4@@@0?40M?eN@@@(M

?)X?e?J@@gW&@@H??W&@@V@@@>@@5?W&(Ye?W&@(YgW&@@@0M?f?O2@@@@@@)gO2@@@? O2@@@@@)KO2@@@@@@@@@@@@@@@@@@0M? ?@@0Y?J@)?eW&@5f?W&@@5e?7@@@@@(R@@@HW&@H?e?7@@H?f?W&@@@gO2@@@@@@@@@Ye?O2@@@@@@?heO2@@@@@@@@@@@@@@@@@@@?@@@@@@@@0M

?W&<f7@(Yf?7@@(Ye?@@@@@(YJ@@@T&@5fJ@@5gO&@@@@e?O2@@@@@0M?I'@@@@@@@@@@@@@@?f?O2@@@@@@@@@@@@@@@@@0Y@@@@5?@@0MW&5?e?J@@H?fJ@@(Y?eJ@@@@(Y?7@@V@@(Yf7@(YfO2@@@@@@@@@@@@@0M?fV4@@@@0Me?I'@@@@@@@@@@@@@0Mg?I@Me?J@@@(Y?7@H?e?7@5f?W&@@He?W&@@@(Y?J@@@@@@H?e?J@@H?eO2@@@@?I4@@@@@0M V4@@@@@@@0M? ?7@@@H

?J@@fJ@@HfW&@@5?e?7@@@(Y?W&@@@@@5f?7@5?@@@@@@@@@L? ?@@@5?W&<?f7@5?e?W&@@(Y?e?@@@(Ye7@@?@@(Yf?@@H?@@@@@@@@@1? ?@@@H?

?W&5f?J@@H?e?7@@(Yf?@@0Y??J@@@@@(Y?f?@@??@@@@@@@@@@? J@@@?7@Hf?7@5fJ@@@H?he?7@@@@(Yg?@@??@@@@0M?@@5? 7@@5?@5?fJ@@Hf7@@5hf?@@@@(Y?g?3@@@@@0M?e@@Y? ?J@@(YJ(Y?f7@5?f@@0Yhf?@@@0Yh?V4@@0M?f@@@@ ?7@@H?

?W&Hf?J@@H? @@@5 ?@ ?@@@?7@?fW&@5 @@0Y ?@@@J@5?f7@(Y7@H?e?J@@H?

?J@5fW&@5?7@He?W&@@HJ@5?e?7@@5?7@H?eJ@@(Y?

?J@@e?W&@(Y?7@5eW&@(Y??@@He7@@H?@@??J@@5??@@?O&@(Y??@@@@@(Y?@@@@(Y??@@@0Y

B A L A N C E O F P A Y M E N T S

C O N C E P T U A L F R A M E W O R K

Purposes of the Balance of Payments Manual

1. Like editions issued in 1948, 1950, 1961, and 1977,this 1993 edition of the Balance of Payments Manual(the Manual) serves as an international standard for theconceptual framework underlying balance of paymentsstatistics. The Manual also functions as a guide formember countries submitting regular balance ofpayments reports to the International Monetary Fund(the IMF or the Fund). In preparing this fifth edition,the IMF made every effort to ascertain the needs and toreflect the viewpoints of national compilers and varioususers of balance of payments statistics and internationalinvestment position data.

2. The primary purposes of the Manual are (i) to provide standards for concepts, definitions,classifications, and conventions and (ii) to facilitate thesystematic national and international collection, organi-zation, and comparability of balance of payments andinternational investment position statistics. A companionvolume, the Balance of Payments Compilation Guide(the Guide), provides practical guidance to nationalcompilers on the collection, presentation, andsystematization of external statistics. The Guide isparticularly useful for countries in which statisticalsystems are in the early stages of development or intransition.

Changes from the Fourth Edition

3. The scope and orientation of this Manual differfrom those of the fourth edition in a number ofrespects. One important change is the expansion of theconceptual framework to encompass balance ofpayments flows (transactions) and stocks of externalfinancial assets and liabilities (the internationalinvestment position). A clear distinction is madebetween (i) transactions and (ii) other changes in theaccounts—valuation, reclassification, and otheradjustments. Transactions or other changes may resultin changes in stocks, but only transactions are reflectedin balance of payments accounts. For example, in thefifth edition, the allocation or cancellation of specialdrawing rights (SDRs) and the monetization ordemonetization of gold (each with counterpart entry)

are not included among transactions in the balance ofpayments accounts but as adjustment items affectingthe international investment position.

4. Additionally, linkage of the international investmentposition and balance of payments accounts to the restof the world account in the System of NationalAccounts (SNA) is strengthened and harmonized to themaximum extent possible. Cases in point are identicaltreatments, in the two systems, of residence, valuation,timing, and reinvested earnings on direct investment.Also, to increase harmonization with the SNA, adistinction between current and capital transfers isintroduced in the Manual. As a result of the change,the former balance of payments capital account isredesignated as the capital and financial account.These and other changes reflect the efforts ofinternational experts and coordinating groups, includingnational accountants and balance of paymentscompilers. Their efforts also serve to integrate thebalance or payments more effectively with other IMFstatistical systems such as money and banking,government finance, and international banking.

5. There are also changes in the treatments ofinternational services, income, and certain financialtransactions. First, in contrast to the fourth edition, thefifth edition makes a clear distinction in the currentaccount between international transactions in servicesand transactions in income. In the fourth edition, laborand nonfinancial property income were groupedtogether with services other than shipment, travel, andtransportation, and investment income was coveredseparately. In the fifth edition, the two maincomponents of income flows between residents andnonresidents—compensation of employees andinvestment income—are separately identified as compo-nents of the current account. This treatmentharmonizes with the concept of income presented inthe System of National Accounts 1993 (SNA) andstrengthens the links between the balance of paymentsincome account and financial account and betweenbalance of payments flows and the stocks of assets andliabilities comprising the international investmentposition. Second, the component list of transactions inservices is expanded to reflect the growing importance

3

I. Introduction

of services and the contributions of various inter-national fora to the development of a codified list thatsatisfies the requirements and provides links betweenseparate statistical systems.

6. In the fifth edition, coverage of financial flows andstocks is significantly expanded and restructured. Themodification reflects, first, an orientation towardscompatibility with other IMF statistical systems and theSNA and, second, widespread alterations in the natureand composition of international financial transactionssince publication of the fourth edition in 1977. Thesechanges include the emergence of financial innovations,new instruments, and transactors that are partlyassociated with a trend towards increased asset securi-tization. Such developments tend, in many instances, toblur the distinction between long- and short-termmaturities and to make it more difficult to identifyresident/nonresident transactions, especially when suchtransactions involve a number of currencies and avariety of actual and contingent financial instruments orarrangements. Together with the easing or abolition ofexchange controls in many countries and the progres-sive deregulation of national financial markets, thesedevelopments create new challenges and problems forcompilers and data users. Further complications arise asa result of external debt problems experienced by anumber of countries (e.g., accounting for arrears, debtforgiveness or debt reduction schemes, and associatedinnovative financial arrangements). Partly in responseto such developments, classification of the financialaccount is re-oriented. To cover new financialinstruments, coverage of nonequity portfolio investmentis broadened to include long- and short-term securities,and supplementary classifications covering exceptionalfinancing transactions (with selected arrears-relatedentries for balance of payments accounts) and otheritems of analytical interest are introduced.

Uses of Balance of Payments and InternationalInvestment Position Data

7. Balance of payments and international investmentposition data are most important, of course, for nationaland international policy formulation. External aspects(such as payments imbalances and inward and outwardforeign investment) play a leading role in economicand other policy decisions in the increasingly inter-dependent world economy. Such data are also used foranalytical studies; that is, to determine the causes ofpayments imbalances and the necessity for implement-ing adjustment measures; relationships betweenmerchandise trade and direct investment; aspects of

international trade in services; international bankingflows and stocks; asset securitization and principalmarket developments; external debt problems, incomepayments, and growth; and links between exchangerates and current account and financial account flows.In addition, external data are utilized extensively, alongwith other variables, for balance of paymentsprojections and the relationship of these projections tochanges in countries’ stocks of external assets andliabilities. Finally, balance of payments andinternational investment position data constitute anindispensable link in the compilation of data forvarious components of the national accounts (e.g.,production accounts, income accounts, capital andfinancial accounts, and the related measurement ofnational wealth).

8. Previous brief references to changes in coverage,classification, and orientation do not represent an all-inclusive list of differences between the fourth andfifth editions of the Manual. Other modifications in thetreatment of specific components will be evident—andthoroughly covered—in appropriate chapters. In directinvestment, for example, changes are effected in criteriafor flows between affiliated banks (and related stockpositions) and in the distinction between long- andshort-term intercompany transactions. Aspects ofregional presentation, covered in an appendix in thefourth edition, comprise a chapter in this Manual toreflect growing international interest in this area. Toaddress the expanded conceptual framework thatencompasses stocks of external assets and liabilities,the fifth edition presents a new chapter on theinternational investment position and a full expositionof the classification, components, and links to balanceof payments accounts and balance sheet aspects of theSNA.

9. In contrast to a rather central position in the fourthedition, the discussion of selected issues in balance ofpayments analysis is presented in Appendix 5 of thefifth edition. Such issues and the nature and limitationsof various presentations can be better understood afterthe concepts, structure, and classification of standardcomponents have been covered. A thorough treatmentof analytic material requires more extensive coveragethan would be appropriate in this Manual. Therefore,only selected issues are highlighted to help identifycauses of payments imbalances, to determine financingrequirements, and to focus on appropriate adjustmentmeasures.

10. Although there are significant differences betweenthe fourth and fifth editions of the Manual, the latter

CONCEPTUAL FRAMEWORK

4

preserves the continuity of the data collection frameworkand IMF reports. Every effort has been made todelineate principles and concepts clearly; to relate theseappropriately to practical considerations and limitations;and to establish conventions that may be applied, whendata sources allow, within a consistent framework.Because the development of statistical systems varies,standard components and classification schemespresented in the Manual may be excessively detailed formany IMF member countries and inadequately detailedfor others. The framework provides flexibility in this

respect. The former group may provide limited data onselected components—and subsequently add to these, ifpossible—and the latter group may be encouraged toprovide supplementary data.

Structure of the Manual

11. Part one of the Manual covers the conceptualframework of international accounts. Part two dealswith the structure and classification of accounts, andpart three is concerned with regional allocation.

CHAPTER I

5

Definitions

12. Part one of this Manual deals with the conceptualframework of balance of payments accounts and theinternational investment position. Part one covers theframework’s relationship to national accounts; toconcepts of residence, valuation, and time of recording;and to the unit of account and conversion.

13. The balance of payments is a statistical statementthat systematically summarizes, for a specific timeperiod, the economic transactions of an economy withthe rest of the world. Transactions, for the most partbetween residents and nonresidents,1 consist of thoseinvolving goods, services, and income; those involvingfinancial claims on, and liabilities to, the rest of theworld; and those (such as gifts) classified as transfers,which involve offsetting entries to balance—in anaccounting sense—one-sided transactions. (Seeparagraph 28.)2 A transaction itself is defined as aneconomic flow that reflects the creation, transformation,exchange, transfer, or extinction of economic value andinvolves changes in ownership of goods and/orfinancial assets, the provision of services, or theprovision of labor and capital.

14. Closely related to the flow-oriented balance ofpayments framework is the stock-oriented internationalinvestment position. Compiled at a specified date suchas year end, this investment position is a statisticalstatement of (i) the value and composition of the stockof an economy’s financial assets, or the economy’sclaims on the rest of the world, and (ii) the value andcomposition of the stock of an economy’s liabilities tothe rest of the world. In some instances, it may be ofanalytic interest to compute the difference between thetwo sides of the balance sheet. The calculation would

provide a measure of the net position, and the measurewould be equivalent to that portion of an economy’snet worth attributable to, or derived from, itsrelationship with the rest of the world. A change instocks during any defined period can be attributable totransactions (flows); to valuation changes reflectingchanges in exchange rates, prices, etc.; or to otheradjustments (e.g., uncompensated seizures). Bycontrast, balance of payments accounts reflect onlytransactions.

Principles and Concepts

15. The remainder of this chapter deals with theconceptual framework of international accounts; that is,the set of underlying principles and conventions thatensure the systematized and coherent recording ofinternational transactions and stocks of foreign assetsand liabilities. Relevant aspects of these principles,together with practical considerations and limitations,are thoroughly discussed in subsequent chapters.

Double-entry System

16. The basic convention applied in constructing abalance of payments statement is that every recordedtransaction is represented by two entries with equalvalues. One of these entries is designated a credit witha positive arithmetic sign; the other is designated adebit with a negative sign. In principle, the sum of allcredit entries is identical to the sum of all debit entries,and the net balance of all entries in the statement iszero.

17. In practice, however, the accounts frequently donot balance. Data for balance of payments estimatesoften are derived independently from different sources;as a result, there may be a summary net credit or netdebit (i.e., net errors and omissions in the accounts). A separate entry, equal to that amount with the signreversed, is then made to balance the accounts.Because inaccurate or missing estimates may beoffsetting, the size of the net residual cannot be takenas an indicator of the relative accuracy of the balanceof payments statement. Nonetheless, a large, persistent

6

II.Conceptual Framework of the Balance of Payments andInternational Investment Position

1The exceptions to the resident/nonresident basis of the balance of paymentsare the exchange of transferable foreign financial assets between residentsectors and, to a lesser extent, the exchange of transferable foreign financialliabilities between nonresidents. (See paragraph 318.)

2The definitions and classifications of international accounts presented in thisManual are intended to facilitate reporting of data on international transactionsto the Fund. These definitions and classifications do not purport to give effectto, or interpret, various provisions (which pertain to the legal characterization ofofficial action or inaction in relation to such transactions) of the Articles ofAgreement of the International Monetary Fund.

residual that is not reversed should cause concern.Such a residual impedes analysis or interpretation ofestimates and diminishes the credibility of both. A largenet residual may also have implications for interpreta-tion of the investment position statement (See thediscussion in Chapter 23.)

18. Most entries in the balance of payments refer totransactions in which economic values are provided orreceived in exchange for other economic values. Thesevalues consist of real resources (goods, services, andincome) and financial items. Therefore, the offsettingcredit and debit entries called for by the recordingsystem are often the result of equal amounts havingbeen entered for the two items exchanged. When itemsare given away rather than exchanged, or when arecording is one-sided for other reasons, special typesof entries—referred to as transfers—are made as therequired offsets. (The various kinds of entries that maybe made in the balance of payments are discussed inparagraphs 26 through 31.)

19. Under the conventions of the system, a compilingeconomy records credit entries (i) for real resourcesdenoting exports and (ii) for financial items reflectingreductions in an economy’s foreign assets or increasesin an economy’s foreign liabilities. Conversely, acompiling economy records debit entries (i) for realresources denoting imports and (ii) for financial itemsreflecting increases in assets or decreases in liabilities.In other words, for assets—real or financial—a positive figure (credit) represents a decrease inholdings, and a negative figure (debit) represents anincrease. In contrast, for liabilities, a positive figureshows an increase, and a negative figure shows adecrease. Transfers are shown as credits when theentries to which the transfers provide the offsets aredebits and as debits when those entries are credits.

20. The content or coverage of a balance of paymentsstatement depends somewhat on whether transactionsare treated on a gross or on a net basis. The Manualcontains recommendations on which transactionsshould be recorded gross or net. The recommendationsare appropriately reflected in the list of standardcomponents and in suggested supplementarypresentations.

Concepts of Economic Territory, Residence,and Center of Economic Interest

21. Identical concepts of economic territory, residence,and center of economic interest are used in thisManual and in the SNA. Economic territory may not

be identical with boundaries recognized for politicalpurposes. A country’s economic territory consists of ageographic territory administered by a government;within this geographic territory, persons, goods, andcapital circulate freely. For maritime countries,geographic territory includes any islands subject to the same fiscal and monetary authorities as themainland.

22. An institutional unit has a center of economicinterest and is a resident unit of a country when, fromsome location (dwelling, place of production, or otherpremises) within the economic territory of the country,the unit engages and intends to continue engaging(indefinitely or for a finite period) in economicactivities and transactions on a significant scale. (Oneyear or more may be used as a guideline but not as aninflexible rule.)

Principles for Valuation and Time of Recording

23. A uniform basis of valuation for the internationalaccounts (both real resources and financial claims andliabilities) is necessary for compiling, on a consistentbasis, any aggregate of individual transactions and an asset/liability position consistent with suchtransactions. In this Manual, the basis of transactionvaluations is generally actual market prices agreedupon by transactors. (This practice is consistent withthat of the SNA.) Conceptually, all stocks of assets and liabilities are valued at market prices prevailing atthe time to which the international investment positionrelates. A full exposition of valuation principles;recommended practices; limitations; and the valuationof transfers, financial items, and stocks of assets andliabilities appears in Chapter 5. (The expositionincludes cases in which conditions may not allow forthe existence or assumption of market prices.)

24. In the Manual and the SNA, the principle of accrualaccounting governs the time of recording for transac-tions. Therefore, transactions are recorded wheneconomic value is created, transformed, exchanged,transferred, or extinguished. Claims and liabilities arisewhen there is a change in ownership. The change maybe legal or physical (economic). In practice, when achange in ownership is not obvious, the change may beproxied by the time that parties to a transaction recordit in their books or accounts. (The recommended timingand conventions for various balance of paymentsentries, together with exceptions to and departures fromthe change of ownership principle, are covered inChapter 6.)

CHAPTER II

7

Concept and Types of Transactions

25. Broadly speaking, changes in economicrelationships registered by the balance of paymentsstem primarily from dealings between two parties.These parties are, with one exception (see footnote 1),a resident and a nonresident, and all dealings of thiskind are covered in the balance of payments.Recommendations for specific entries are embodied inthe list of standard components (see Chapter 8) and arespelled out in detail from Chapter 9 onward.

26. Despite the connotation, the balance of paymentsis not concerned with payments, as that term isgenerally understood, but with transactions. A numberof international transactions that are of interest in abalance of payments context may not involve thepayment of money, and some are not paid for in anysense. The inclusion of these transactions, in additionto those matched by actual payments, constitutes aprincipal difference between a balance of paymentsstatement and a record of foreign payments.

Exchanges

27. The most numerous and important transactionsfound in the balance of payments may be characterizedas exchanges. A transactor (economic entity) providesan economic value to another transactor and receivesin return an equal value. The economic valuesprovided by one economy to another may becategorized broadly as real resources (goods, services,income) and financial items. The parties that engage inthe exchange are residents of different economies,except in the case of an exchange of foreign financialitems between resident sectors. The provision of afinancial item may involve not only a change in theownership of an existing claim or liability but also thecreation of a new claim or liability or the cancellationof existing ones. Moreover, the terms of a contractpertaining to a financial item (e.g., contractual maturity)may be altered by agreement between the parties. Sucha case is equivalent to fulfillment of the originalcontract and replacement by a contract with differentterms. All exchanges of these kinds are covered in thebalance of payments.

Transfers

28. Transactions involving transfers differ fromexchanges in that one transactor provides an economicvalue to another transactor but does not receive a quidpro quo on which, according to the conventions andrules adopted for the system, economic value is placed.

This absence of value on one side is represented by anentry referred to as a transfer. Such transfers (economicvalue provided and received without a quid pro quo)are shown in the balance of payments. Currenttransfers are included in the current account (seeChapter 15) and capital transfers appear in the capitalaccount. (See Chapter 17.)

Migration

29. Because an economy is defined in terms of theeconomic entities associated with its territory, the scopeof an economy is likely to be affected by changes inentities associated with the economy.

30. Migration occurs when the residence of anindividual changes from one economy to anotherbecause the person moves his or her abode. Certainmovable, tangible assets owned by the migrant are, ineffect, imported into the new economy. The migrant’simmovable assets and certain movable, tangible assetslocated in the old economy become claims of the neweconomy on the old economy. The migrant’s claims on,or liabilities to, residents of an economy other than thenew economy become foreign claims or liabilities ofthe new economy. The migrant’s claims on, or liabilitiesto, residents of the new economy cease to be claimson, or liabilities to, the rest of the world for anyeconomy. The net sum of all these shifts is equal to thenet worth of the migrant, and his or her net worth mustalso be recorded as an offset if the other shifts arerecorded. These entries are made in the balance ofpayments where the offset is conventionally includedwith transfers.

Other imputed transactions

31. In some instances, transactions may be imputedand entries may be made in balance of paymentsaccounts when no actual flows occur. Attribution ofreinvested earnings to foreign direct investors is anexample. The earnings of a foreign subsidiary orbranch include earnings attributable to a directinvestor. The earnings, whether distributed orreinvested in the enterprise, are proportionate to thedirect investor’s equity share in the enterprise.Reinvested earnings are recorded as part of directinvestment income. An offsetting entry with oppositesign is made in the financial account under directinvestment-reinvested earnings to reflect the directinvestor’s increased investment in the foreignsubsidiary or branch. (Reinvested earnings arediscussed in chapters 14 and 18.)

CONCEPTUAL FRAMEWORK

8

Changes Other Than Transactions

Reclassification of claims and liabilities

32. The classification of financial items presented inthis Manual is designed to reveal the motivation ofcreditor or debtor. Financial items are subject toreclassification in accordance with changes inmotivation. A case in point is the distinction betweendirect investment and other types of investment. Forexample, several independent holders of portfolioinvestment (in the form of corporate equities issued bya single enterprise located abroad) may form anassociated group to have a lasting, effective voice inthe management of the enterprise. Their holdings willthen meet the criteria for direct investment, and thechange in the status of the investment could berecorded as a reclassification. Such a reclassificationwould be reflected, at the end of the period duringwhich it occurred, in the international investment

position but not in the balance of payments. Similarly,claims on nonresidents can come under, or be releasedfrom, the control of resident monetary authorities. Insuch cases, there are reclassifications between reserveassets and assets other than reserves.

Valuation changes

33. The values of real resources and financial items areconstantly subject to changes stemming from either orboth of two causes. (i) The price at which transactionsin a certain type of item customarily take place mayundergo alteration in terms of the currency in whichthat price is quoted. (ii) The exchange rate for thecurrency in which the price is quoted may change inrelation to the unit of account that is being used.Valuation changes are not included in the balance ofpayments but are included in the internationalinvestment position.

CHAPTER II

9

10

III. Balance of Payments and National Accounts

Introduction

34. Conceptually, balance of payments accounts andrelated data on the international investment positionare closely linked to a broader system of nationalaccounts that provides a comprehensive and systematicframework for the collection and presentation of theeconomic statistics of an economy. The internationalstandard for this framework is the System of NationalAccounts (SNA), which encompasses transactions,other flows, stocks, and other changes affecting thelevel of assets and liabilities from one accountingperiod to another. Linkage of the balance of payments and the SNA is reinforced by the fact that, in almost all countries, balance of payments andinternational investment position data are compiledfirst and subsequently incorporated into nationalaccounts.

35. The SNA is a closed system in that both ends ofevery transaction are recorded; that is, each transactionis shown as a use for one part of the system and as aresource for another part. Stocks of assets affected bytransactions are covered as of the beginnings and endsof appropriate periods. Stocks of assets also areaffected by valuation and other volume changes (suchas uncompensated seizures or destruction of assets)that occur during the period and cause additionaldifferences in stock value.

36. In the SNA, transactors and holders of stocks arethe resident economic entities of a particular economy.For the SNA to be closed, there must be a segment tocapture flows that involve uses or resources fornonresident entities. That segment is known as the restof the world account. The segment for resident entitiesor sectors consists of accounts for production, incomegeneration, primary and secondary distribution ofincome, redistribution of income, consumption, andaccumulation. Since the system is closed, the rest of theworld account is constructed from the perspective ofthe rest of the world rather than that of the compilingeconomy. Consequently, entries in the balance ofpayments and the international investment position arereversed in the presentation of rest of the worldaccounts.

37. In this chapter, the balance of payments and theinternational investment position are described inrelation to the SNA and links between those inter-national accounts and relevant segments of the SNA are discussed.

Relationship Between the SNA and PrinciplesUnderlying the Balance of Payments

38. As the balance of payments and the internationalinvestment position are integral parts of the SNA, thereis virtually complete concordance—between the Manualand the SNA—on such issues as the delineation ofresident units (producers or consumers), valuation oftransactions and the stock of external assets andliabilities, time of recording transactions and stocks,conversion procedures, coverage of internationaltransactions in real resources (goods, services andincome), and transfers (current and capital). There isconcordance, as well, on external financial assets andliabilities and coverage of the international investmentposition.

Resident units

39. The SNA and the Manual identify residentproducers and consumers in identical fashion. Bothinvoke the concepts of economic territory and thecenter of economic interest to identify resident units.(These concepts are elaborated in Chapter 4.)

Valuation

40. In the Manual and the SNA, market price is theprimary concept for valuation of transaction accountsand balance sheet accounts. (The market price conceptis defined and elaborated in Chapter 5.)

Time of recording

41. Balance of payments and national accounts areconstructed, in principle, on an accrual basis. The twosystems employ essentially identical applications of theaccrual basis in specific categories of transactions.(Chapter 6 provides a full discussion on application of

the accrual basis underlying balance of paymentsaccounts.)

Conversion procedures

42. Both systems employ consistent procedures forconverting transactions denominated in a variety ofcurrencies or units of account into the unit of account(usually the domestic currency) adopted for compilingthe balance of payments statement or the nationalaccounts. (See Chapter 7.) There also is concordancebetween the two systems on conversion proceduresused in constructing balance sheet accounts.

Classification

43. It would be convenient, for some purposes, if theclassification of transactions in the balance of paymentsand the rest of the world account of the SNA wereidentical in all respects. Differences are justifiable,however, because the two statements have differentuses. Whereas the classification scheme of the rest ofthe world account maintains the basic, fundamentaldistinction between production flows, income flows,and accumulation flows, that subclassification is oflesser importance in the context of balance ofpayments analysis. Congruence of underlying principlesmakes the balance of payments consistent with the SNAframework and permits the balance of payments to bedescribed in the context of the SNA. This overallcongruence is more important than exact, detailedconcordance between the balance of payments andSNA accounts pertaining to relationships of residentunits with the rest of the world.

44. Before examining the relationship between the SNArest of the world account and the balance of paymentsaccounts and international investment position, readersmay find it useful to consider how the broad elementsof the latter two statements relate to integratedeconomic accounts for the economy as a whole, aswell as to institutional sectors of the economy.

Integrated Economic Accounts

45. Integrated economic accounts (see pages 14–19)in the form of T-accounts provide an overview ofstructural elements of the SNA by depicting variousfacets of economic phenomena (e.g., production,income, consumption, accumulation, and wealth) inthree types of accounts: current accounts, accumulationaccounts, and balance sheets. Details for the totaleconomy and various institutional sectors are presented

separately in these accounts. Resources, stocks ofliabilities, and net worth (and changes thereof) areshown on the right side of the accounts; uses andstocks of assets (and changes thereof) are shown onthe left side in the tabular presentation. However, inthe account for goods and services, the sources ofsupply (resources) from the economy’s output andimports are shown on the left side, and the distributionof that supply (uses such as exports, intermediateconsumption, and final consumption by the economy)is shown on the right side. For each category oftransactions, the sum of the entries on the right side ofthe accounts is equal to the sum of the entries on theleft side. Because the SNA is closed, external flows areportrayed or measured from the perspective of the restof the world to achieve this equality. Thus, for example,payments of compensation to employees (uses) byvarious institutional sectors may exceed receipts(resources) for the household sector because somepayments are made to nonresidents (resources for therest of the world). The inclusion of payments tononresidents on the resources side (for the rest of theworld sector) ensures that both sides of the account areequal.

46. SNA current (transactions) accounts—the first set ofintegrated economic accounts—portray (i) output,intermediate consumption, and value added for eachsector and the total economy, as well as the disposition of domestic production and imports ofgoods and services; (ii) distributive, from the viewpoint of producers, transactions that are directlylinked to the process of production or, alternatively, the composition of value added; (iii) primary incomedistribution showing how gross value added isdistributed to factors of labor, capital, and governmentand, when appropriate, reflects flows to and from therest of the world; (iv) secondary income distribution;(v) income redistribution covering, in principle, current taxes on income, wealth, and other currenttransfers and allowing for the derivation of disposableincome and adjusted disposable income; and (vi) useof income. Saving is a balancing item for alltransactions accounts and provides a link toaccumulation accounts.

47. Accumulation accounts of the SNA show changesin assets and liabilities and net worth (the difference,for any sector or for the total economy, between assetsand liabilities) and follow a presentation similar tobalance sheets. A first group of accounts coverstransactions that would correspond to all changes inassets, liabilities, and net worth if saving and voluntary

CHAPTER III

11

transfers of wealth were the only sources of change innet worth. A second group of accounts relates tochanges—in assets, liabilities, and net worth—that aredue to other factors. The first group of accumulationaccounts contains the capital account and the financialaccount. These two accounts are distinguished to showa balancing item (i.e., net lending/net borrowing)useful for economic analysis. The second group coverschanges—in assets, liabilities, and net worth—that area result of other factors affecting the values andvolume of assets and liabilities. Examples of suchchanges are discoveries or depletion of subsoilresources, natural catastrophes, uncompensatedseizures of assets, etc., and price and exchange ratechanges that affect only the values of assets andliabilities.

48. Flows reflected in the balance of payments affect,in important ways, the total economy’s activitiesassociated with production, generation and distributionof income, consumption, and accumulation activities.For instance, credit and debit entries for goods andservices in balance of payments accounts are equivalentto flows of exports and imports of goods and services.These flows are reflected in the economy’s account forgoods and services and consequently affect themeasurement of gross domestic product (GDP) and itscomposition in terms of final demand components(e.g., final consumption, gross capital formation, etc.).When measured from the final demand side, GDP isequivalent to the sum of entries in the uses column ofthe goods and services account less imports (the firstentry on the resources side of the account) in theintegrated accounts. Flows of exports and imports ofgoods and services are defined, in terms of coverage,in virtually identical fashion in the SNA and theManual.

49. In viewing—for both institutional sectors and thetotal economy—the generation of income, theallocation of primary income, the secondary distributionof income, and the redistribution of income in kind,readers should note that, apart from income flowsgenerated domestically and included in the measure ofgross value added or GDP, there are income flows to orfrom the rest of the world. These flows (in the form ofcompensation of employees; property income; taxes onproduction and imports; current taxes on income,wealth, etc.; and other current transfers) constituteadditional sources of income. These additional sourcesof income are included in the measurement of sectoraland national disposable income and, consequently, insectoral and national saving—the balancing item

between disposable income and final consumption. Interms of the balance of payments, compensation ofemployees and property income flows comprise theincome category, while taxes and other current transfers are identical with the coverage of currenttransfers.

50. Accumulation activity of the total economy anddomestic institutional sectors is portrayed, in the SNA, in the capital and financial accounts. The capitalaccount shows (i) sources of financing accumulation(saving and net capital transfers) on the changes inliabilities side; (ii) the composition of investment (grossor net) which takes into account the consumption offixed capital (capital formation) on the changes in assets side; and (iii) acquisitions less disposals ofnonproduced, nonfinancial assets. Changes in net worth that result from saving and net capital transfersrepresent the sum of sources of financing accumulation.The balancing item between sources of financing andthe sum of net capital formation and net purchases ofnonproduced, nonfinancial assets constitutes netlending/net borrowing for each sector and the nation as a whole. Net capital transfers (capital transfersreceivable less capital transfers payable) for each sector contain both intersectoral flows and transactionswith the rest of the world. Within the total economy,however, intersectoral flows cancel each other so thatthe net flow constitutes transactions relating only to the rest of the world. In the balance of payments, netlending/net borrowing for the total economycorresponds to the sum of the current account balance and the balance on capital account transactions within the capital and financial account.The measure of net lending/net borrowing for the total economy also represents net financial investmentvis-à-vis the rest of the world. In the integratedaccounts, net lending/net borrowing for the totaleconomy is equivalent to amounts shown in columnsfor the rest of the world. However, because the rest of the world columns are viewed from the perspectiveof nonresidents and balance of payments accounts are viewed from that of the compiling economy,changes in assets of the rest of the world representchanges in liabilities of the compiling economy, andvice versa.

51. According to the guidelines for residence (seeChapter 4), transactions in land can only take placebetween resident entities. When a nonresident entity(other than a foreign government or internationalorganization acquiring land for use as an extraterritorialenclave) acquires land in the domestic economy, the

CONCEPTUAL FRAMEWORK

12

acquisition is considered a financial investment(included in net incurrence of liabilities) in a notionalresident enterprise.

52. The financial account of the SNA shows the netacquisition of financial assets and the net incurrence ofliabilities. Transactions in financial assets and liabilitiesfor each institutional sector and the total economyencompass those among domestic sectors and thoserelated to the rest of the world. Consolidated domesticflows cancel each other so that transactions for theeconomy as a whole are (i) accounted for bytransactions vis-à-vis the rest of the world and (ii) equal to flows shown in columns for the rest of the world. In the balance of payments, transactions(from the viewpoint of the compiling economy) in thefinancial account of the capital and financialaccount correspond to entries in columns for thefinancial account of the rest of the world, but changesin assets of the rest of the world represent changes inliabilities for the compiling economy and vice versa.

53. The linkage between key aggregates of accounts of the total economy and balance of payments flowscan, by the use of symbols, be summarizedalgebraically within a savings/investment framework.

C = private consumption expenditureG = government consumption expenditure

I = gross domestic investmentS = gross saving

X = exports of goods and servicesM = imports of goods and services

NY = net income from abroadGDP = gross domestic product

GNDY = gross national disposable incomeCAB = current account balance in the balance of

payments

NCT = net current transfersNKT = net capital transfers

NPNNA = net purchases of nonproduced, nonfinancialassets

NFI = net foreign investment or net lending/netborrowing vis-à-vis the rest of the world

Balance of payments flows are italicized in thefollowing equations.

GDP = C + G + I + X–M(X–M = balance on goods and services in the balance of payments)

CAB = X – M + NY+NCTGNDY = C + G + I + CAB

GNDY – C – G = SS = I + CAB

S – I = CABS – I + NKT – NPNNA = CAB + NKT–NPNNA = NFI(NKT – NPNNA = balance on the capital account of the balance ofpayments)

54. Balance sheet accounts for the total economy anddomestic institutional sectors depict the level andcomposition of the stock of assets and liabilities at thebeginnings and ends of appropriate reference periods.

55. The difference between the sum of assets and thesum of liabilities equals the net worth of the economyand the sectors. In the integrated accounts, financialassets and liabilities recorded in columns for the totaleconomy are an aggregation of the financial assets andliabilities of individual sectors; balance sheet accounts of a nation as a whole are not fully consolidated. Ifaccounts were fully consolidated, the financial assetsand liabilities of domestic sectors would cancel eachother, and the economy’s financial assets and liabilitieswould refer to the stock of external assets and liabilities(the international investment position). From thatperspective, the national wealth or net worth of aneconomy consists of its stock of nonfinancial assets plusthe net international investment position (stock ofexternal assets minus stock of external liabilities). TheIIP also may be derived from the integrated accountscolumn for assets and liabilities of the rest of the world.As the IIP viewpoint is that of the compiling economy,the assets of the rest of the world represent liabilities ofthe compiling economy and vice versa.

56. Appendix 1 contains a discussion of the relation-ship of (i) various SNA accounts pertaining to the restof the world to (ii) balance of payments accounts andthe IIP. Because there is concordance between theunderlying principles of the two systems, the focus ofAppendix 1 is on classification issues and ways ofconstructing bridges to derive relevant nationalaccounts flows and stocks from balance of paymentsaccounts and the IIP.

CHAPTER III

13

14

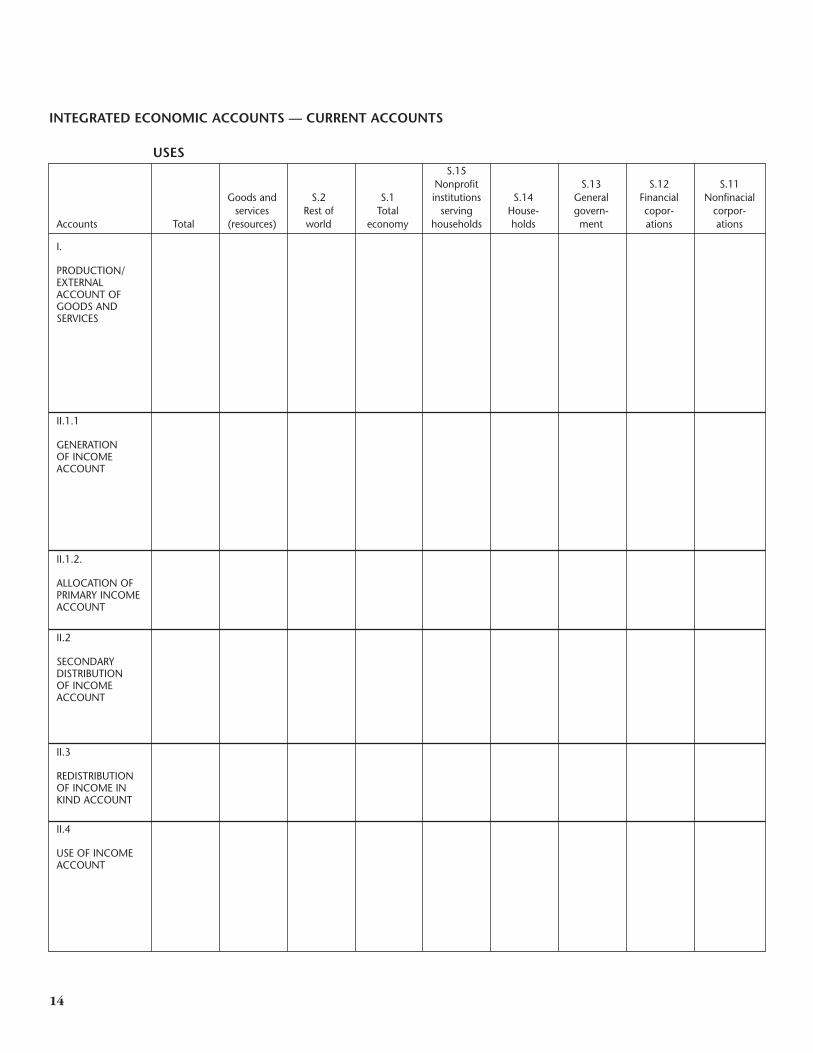

INTEGRATED ECONOMIC ACCOUNTS — CURRENT ACCOUNTS

USESS.15

Nonprofit S.13 S.12 S.11Goods and S.2 S.1 institutions S.14 General Financial Nonfinacial

services Rest of Total serving House- govern- copor- corpor-Accounts Total (resources) world economy households holds ment ations ations

I.

PRODUCTION/EXTERNALACCOUNT OF GOODS AND SERVICES

II.1.1

GENERATIONOF INCOME ACCOUNT

II.1.2.

ALLOCATION OF PRIMARY INCOME ACCOUNT

II.2

SECONDARYDISTRIBUTIONOF INCOMEACCOUNT

II.3

REDISTRIBUTION OF INCOME IN KIND ACCOUNT

II.4

USE OF INCOME ACCOUNT

S.15S.11 S.12 S.13 Nonprofit Goods

Nonfinan- Financial General S.14 institutions S.1 S.2 andcial corpor- corpor- govern- House- serving Total Rest of services

Code Transactions and Balancing Items ations ations ment holds households economy the world (uses) Total Accounts

P.7 Imports of goods and services I.P.6 Exports of goods and servicesP.1 Output PRODUCTION/P.2 Intermediate consumption EXTERNALD.21-D.31 Taxes less subsidies on ACCOUNT OF

products GOODS ANDSERVICES

B.1g/B.1*g Value added, gross/Gross domestic product

K.1 Consumption of fixed capitalB.1n VALUE ADDED, NET/NET

DOMESTIC PRODUCTB.11 EXTERNAL BALANCE OF

GOODS AND SERVICES

D.1 Compensation of employees II.1.1D.2-D.3 Taxes less subsidies on

production and imports GENERATION D.21-D.31 Taxes less subsidies on OF INCOME

products ACCOUNTD.29-D.39 Other taxes less subsidies on

productionB.2g Operating surplus, grossB.3g Mixed income, grossB.2n OPERATING SURPLUS, NETB.3n MIXED INCOME, NET

D.4 Property income II.1.2.

B.5g Balance of primary incomes, ALLOCATION gross/National income, gross OF PRIMARY

B.5n BALANCE OF PRIMARY INCOMES INCOMENET/NATIONAL INCOME, NET ACCOUNT

D.5 Current taxes on income, II.2wealth, etc.

D.61 Social contributions SECONDARYD.62 Social benefits other than DISTRIBUTION

social transfers in kind OF INCOMED.7 Other current transfers ACCOUNT

B.6g Disposable income, grossB.6n DISPOSABLE INCOME, NET

D.63 Social transfers in kind II.3

B.7g Adjusted disposable income, REDISTRIBUTION gross OF INCOME IN

B.7n ADJUSTED DISPOSABLE KIND ACCOUNTINCOME, NET

B.6g Disposable income, gross II.4B.6n DISPOSABLE INCOME, NETP.4 Actual final consumption USE OF INCOMEP.3 Final consumption expenditure ACCOUNTD.8 Adjustment for the change in net

equity of households inpension funds

B.8g Saving, grossB.8n SAVING, NETB.12 CURRENT EXTERNAL BALANCE

15

INTEGRATED ECONOMIC ACCOUNTS — CURRENT ACCOUNTS

RESOURCES

16

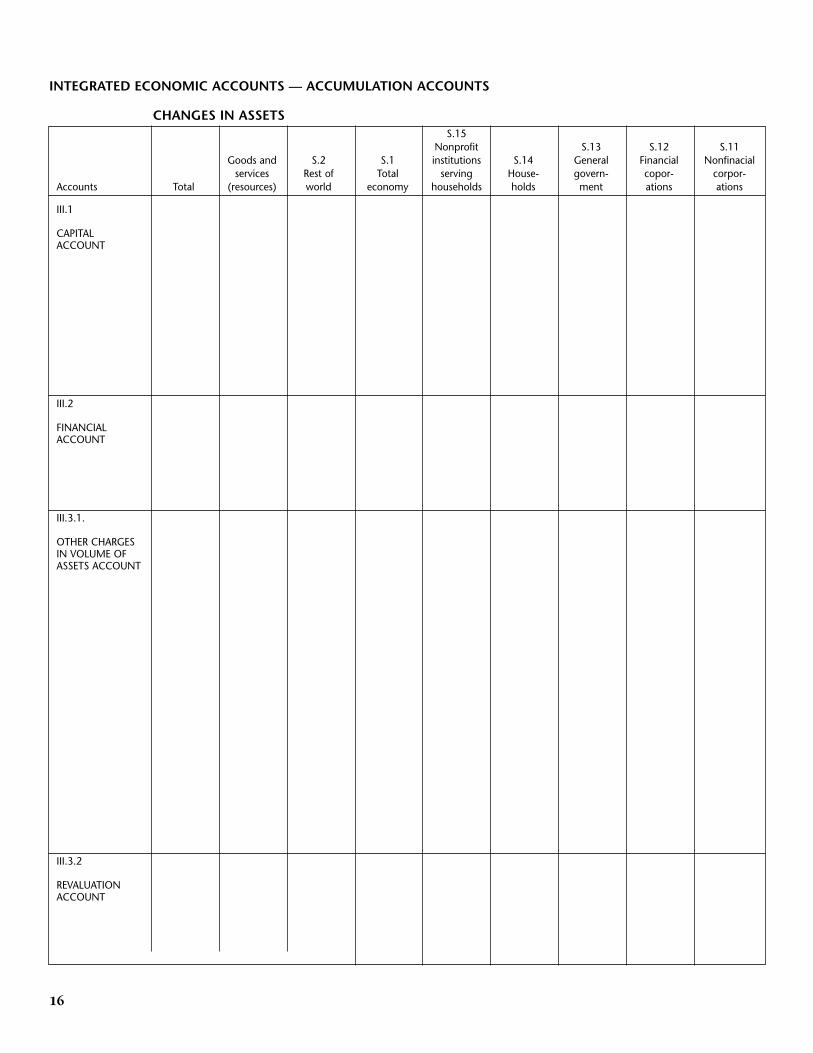

INTEGRATED ECONOMIC ACCOUNTS — ACCUMULATION ACCOUNTS

CHANGES IN ASSETSS.15

Nonprofit S.13 S.12 S.11Goods and S.2 S.1 institutions S.14 General Financial Nonfinacial

services Rest of Total serving House- govern- copor- corpor-Accounts Total (resources) world economy households holds ment ations ations

III.1

CAPITAL ACCOUNT

III.2

FINANCIAL ACCOUNT

III.3.1.

OTHER CHARGES IN VOLUME OF ASSETS ACCOUNT

III.3.2

REVALUATION ACCOUNT

S.15S.11 S.12 S.13 Nonprofit Goods

Nonfinan- Financial General S.14 institutions S.1 S.2 andcial corpor- corpor- govern- House- serving Total Rest of services

Code Transactions and Balancing Items ations ations ment holds households economy the world (uses) Total Accounts

B.8 SAVING, NET III.1B.12 CURRENT EXTERNAL BALANCEP.51 Gross fixed capital formation CAPITALK.1 Consumption of fixed capital (–) ACCOUNTP.52 Changes in inventoriesP.53 Acquisitions less disposals

of valuablesK.2 Acquisitions less disposals of

nonproduced, nonfinancial assetsD.9 Capital transfers, receivableD.9 Capital transfers, payable (-)B.10.1 CHANGES IN NET WORTH DUE TO

SAVING AND CAPITAL TRANSFERS

B.9 NET LENDING (+)/NETBORROWING (–)

F Net acquisition of financial assets III.2F Net incurrence of liabilitiesF.1 Monetary gold and SDRs FINANCIALF.2 Currency and deposits ACCOUNTF.3 Securities other than sharesF.4 LoansF.5 Shares and other equityF.6 Insurance technical reservesF.7 Other accounts receivable/payable

K.3 through Other volume changes, total III.3.1.K.10 andK.12 OTHERK.3 Economic appearance CHANGES IN

of nonproduced assets VOLUMEK.4 Economic appearance OF ASSETS

of produced assets ACCOUNTK.5 Natural growth of non-cultivated

biological resourcesK.6 Economic disappearance of

nonproduced assetsK.7 Catastrophic lossesK.8 Uncompensated seizuresK.9 Other volume changes in

nonfinancial assets n.e.c.K.10 Other volume changes in financial

assets and liabilities n.e.c.K.12 Changes in classifications and

structure

Of whichAN Nonfinancial assetsAn 1 Produced assetsAN 2 Nonproduced assetsAF Financial assets/liabilities

B.10.2 CHANGES IN NET WORTH DUETO OTHER CHANGES IN VOLUME OF ASSETS

K.11 Nominal holding gains/losses III.3.2AN Nonfinancial assetsAN.1 Produced assets REVALUATIONAN.2 Nonproduced assets ACCOUNTAF Financial assets/liabilities

B.10.3 CHANGES IN NET WORTH DUETO NOMINAL HOLDINGGAINS (+)/LOSSES (–)

17

INTEGRATED ECONOMIC ACCOUNTS — ACCUMULATION ACCOUNTS

CHANGES IN LIABILITIES AND NET WORTH

18

INTEGRATED ECONOMIC ACCOUNTS — BALANCE SHEETS

ASSETSS.15

Nonprofit S.13 S.12 S.11Goods and S.2 S.1 institutions S.14 General Financial Nonfinacial

services Rest of Total serving House- govern- copor- corpor-Accounts Total (resources) world economy households holds ment ations ations

IV.1

OPENINGBALANCESHEET

IV.2

CHANGES INBALANCESHEET

IV.3

CLOSINGBALANCESHEET

S.15S.11 S.12 S.13 Nonprofit Goods

Nonfinan- Financial General S.14 institutions S.1 S.2 andcial corpor- corpor- govern- House- serving Total Rest of services

Code Transactions and Balancing Items ations ations ment holds households economy the world (uses) Total Accounts

AN Nonfinancial assets IV.1AN.1 Produced assetsAN.2 Nonproduced assets OPENINGAF Fnancial assets/liabilities BALANCE

SHEETB.90 NET WORTH

Total changes in assets IV.2

AN Nonfinancial assets CHANGES INAN.1 Produced assets BALANCEAN.2 Nonproduced assets SHEETAF Financial assets/liabilities

B.10 CHANGES IN NET WORTH, TOTALB.10.1 SAVING AND CAPITAL TRANSFERSB.10.2 OTHER CHANGES IN VOLUME

OF ASSETSB.10.3 NOMINAL HOLDING GAINS (+)/

LOSSES (–)

AN.1 Nonfinancial assets IV.3AN.2 Produced assetsAF Nonproduced assets CLOSING

Financial assets/liabilities BALANCESHEET

B.90 NET WORTH

19

INTEGRATED ECONOMIC ACCOUNTS — BALANCE SHEETS

LIABILITIES

Concept and Definition of Residence

57. Residence is a particularly important attribute of aninstitutional unit in the balance of payments becausethe identification of transactions between residents andnonresidents underpins the system. Residence is alsoimportant in the SNA because the residency status ofproducers determines the limits of domestic productionand affects the measurement of GDP and manyimportant flows.

58. The concept of residence used in this Manual isidentical to that used in the SNA. The concept is notbased on nationality or legal criteria, although it maybe similar to concepts of residence used for exchangecontrol, tax, and other purposes in many countries. Theconcept of residence is based on a sectoral transactor’scenter of economic interest. Moreover, countryboundaries recognized for political purposes may notalways be appropriate for economic purposes.Therefore, it is necessary to recognize the economicterritory of a country as the relevant geographical areato which the concept of residence is applied. Aninstitutional unit is a resident unit when it has a centerof economic interest in the economic territory of acountry.

Economic Territory of a Country

59. The economic territory of a country consists of thegeographic territory administered by a government;within this territory, persons, goods, and capitalcirculate freely. In a maritime country, economicterritory includes islands that belong to the country andare subject to the same fiscal and monetary authoritiesas the mainland; goods and persons move freely to andfrom the mainland and the islands without any customsor immigration formalities. The economic territory of acountry includes the airspace, territorial waters, andcontinental shelf lying in international waters overwhich the country enjoys exclusive rights and has, orclaims to have, jurisdiction over fishing rights and rightsto fuels or minerals below the sea bed. The economicterritory of a country also includes territorial enclaves inthe rest of the world. These are clearly demarcated landareas (such as embassies, consulates, military bases,

scientific stations, information or immigration offices,aid agencies, etc.) located in other countries and usedby governments that own or rent them for diplomatic,military, scientific, or other purposes with the formalpolitical agreement of governments of countries wherethe land areas are physically located. While goods orpersons may move freely between a country and itsterritorial enclaves located abroad, such goods orpersons become subject to control by governments ofthe countries where the goods or persons are located ifthey move out of the enclaves. In addition, economicterritory includes free zones and bonded warehouses orfactories operated by offshore enterprises undercustoms control. (These are considered part of theeconomic territory of the country in which the freezones, etc. are physically located.)

60. The economic territory of an international organi-zation (see paragraph 88 for characteristics) consists ofterritorial enclave(s) over which the organization hasjurisdiction; these are clearly demarcated land areas orstructures that the international organization owns orrents and uses for organizational purposes formallyagreed upon with the country, or countries, in whichthe enclave(s) are physically located.

61. Therefore, although territorial enclaves used byforeign governments or international organizations maybe physically located within a country’s geographicalboundaries, such enclaves are not included in thecountry’s economic territory.

Center of Economic Interest

62. An institutional unit has a center of economic interestwithin a country when there exists, within the economicterritory of the country, some location, dwelling, place ofproduction, or other premises on which or from whichthe unit engages and intends to continue engaging, eitherindefinitely or over a finite but long period of time, ineconomic activities and transactions on a significant scale.The location need not be fixed so long as it remainswithin the economic territory.

63. In most cases, it is reasonable to assume that aninstitutional unit has a center of economic interest in a

20

IV. Resident Units of an Economy

country if the unit has already engaged in economicactivities and transactions on a significant scale in thecountry for one year or more, or if the unit intends todo so. The conduct of economic activities andtransactions over a period of one year normally impliesa center of interest, but the choice of any specificperiod of time is somewhat arbitrary. The one-yearperiod is suggested only as a guideline and not as aninflexible rule.

64. Ownership of land and structures located within acountry’s economic territory is sufficient qualification forthe owner to have a center of economic interest in thecountry. Land and buildings can only be used forpurposes of production in the country where they arelocated and their owners, in their capacity as owners,are subject to the laws and regulations of that country.However, an owner who is resident in another countrymay not have any economic interest, other thanownership of land or buildings, in the country wherethe land or buildings are located. In that case, theowner is treated as if he has transferred his ownershipto a notional institutional unit that is actually resident inthe country. The notional unit is treated as being ownedand controlled by the nonresident owner—much as aquasi-corporation is owned and controlled by its owner.Rents and rentals paid by the tenants of the land orbuildings are paid to the notional resident unit; in turn,this unit transfers the income to the actual nonresidentowner.

Resident Institutional Units

65. The sectors of an economy are composed of twomain types of institutional units: (i) households andindividuals who make up a household and (ii) legaland social entities, such as corporations and quasi-corporations (e.g., branches of foreign direct investors),nonprofit institutions, and the government of thateconomy. These institutional units must meet certaincriteria to be considered resident units of the economy.

Residence of Households and Individuals

66. A household has a center of economic interestwhen household members maintain, within the country,a dwelling or succession of dwellings treated and usedby members of the household as their principalresidence. All individuals who belong to the samehousehold must be residents of the same country. If amember of an existing household ceases to reside inthe country where his or her household is resident, theindividual ceases to be a member of that household.

67. If a resident household member leaves theeconomic territory and returns to the household after alimited period of time, the individual continues to be aresident even if he or she makes frequent journeysoutside the economic territory. The individual’s centerof economic interest remains in the economy in whichthe household is resident. Treated as residents are

travelers or visitors—individuals who leave aneconomic territory for limited periods of time (lessthan one year) for business or personal purposes(see paragraphs 71, 243, and 244);

workers or employees—individuals who work someor all of the time in economic territories that differfrom those of their resident households. Suchindividuals are

workers who may, because of seasonal demandfor labor, work part of the year in another countryand then return to their households;

border workers who regularly (each day) orsomewhat less regularly (e.g., each week) crossfrontiers to work in neighboring countries;

staff of international organizations who work inthe enclaves of those organizations;

locally recruited staff of foreign embassies,consulates, military bases, etc.;

crews of ships, aircraft, or other mobileequipment operating partly or wholly outside aneconomic territory.