balance sheet classifications

DESCRIPTION

Balance Sheet Classifications. Current liabilities: Long-term liabilities:. Due within one year of the balance sheet date. Due beyond one year. LO1. Long-Term Liabilities. Bonds payable Notes payable Leases Deferred taxes. Bonds. Borrower. Investor. Long-term borrowing arrangement - PowerPoint PPT PresentationTRANSCRIPT

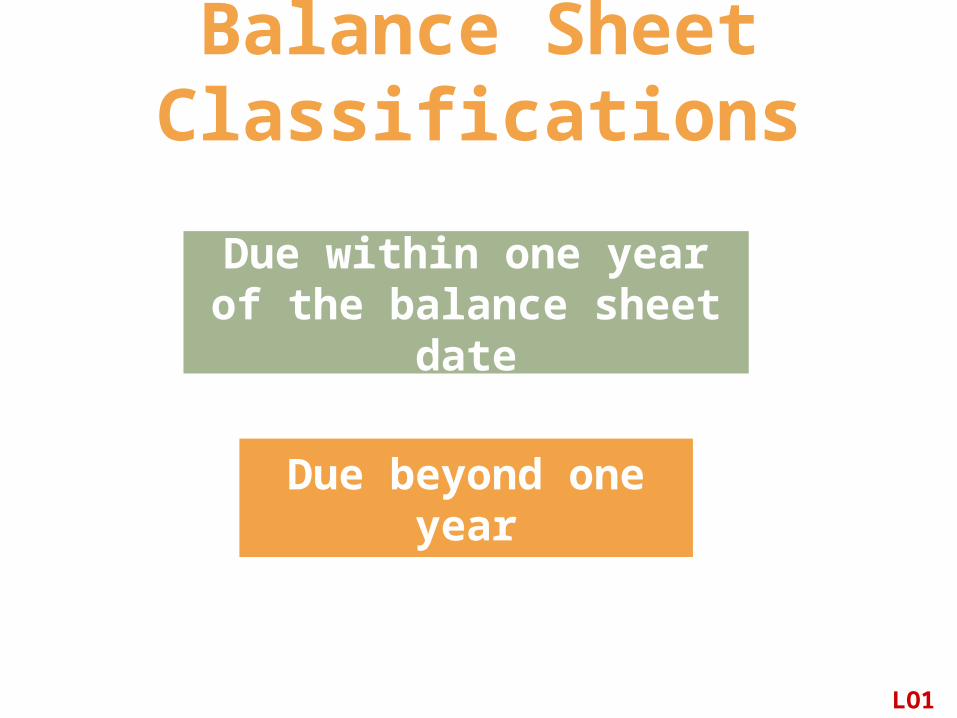

Balance Sheet ClassificationsCurrent liabilities:

Long-term liabilities:

Due within one year of the balance sheet date

Due beyond one year

LO1

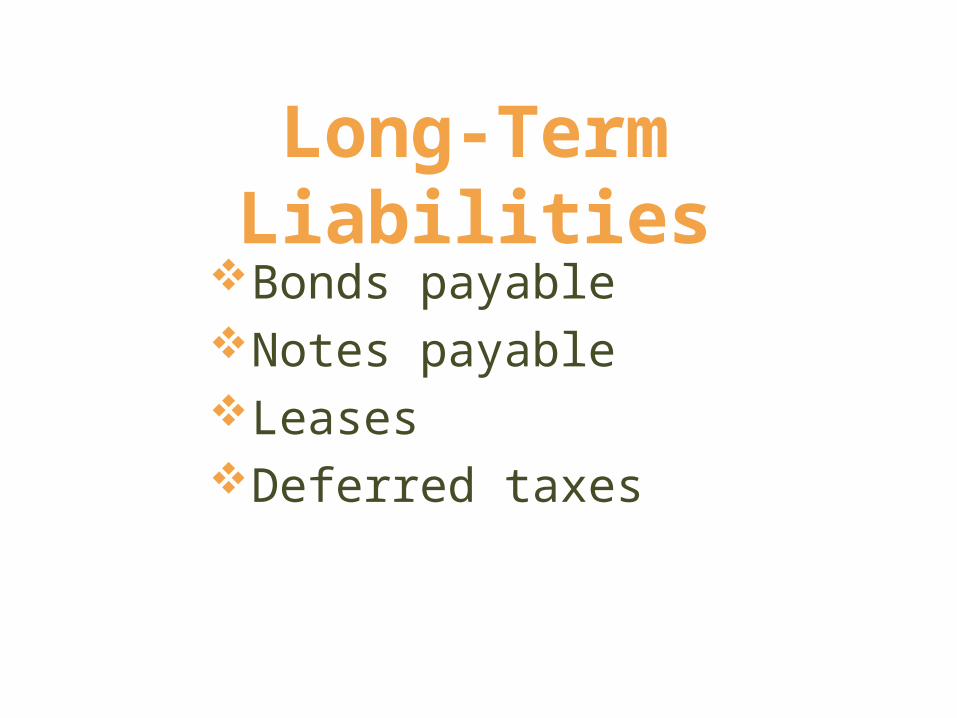

Long-Term LiabilitiesBonds payableNotes payableLeasesDeferred taxes

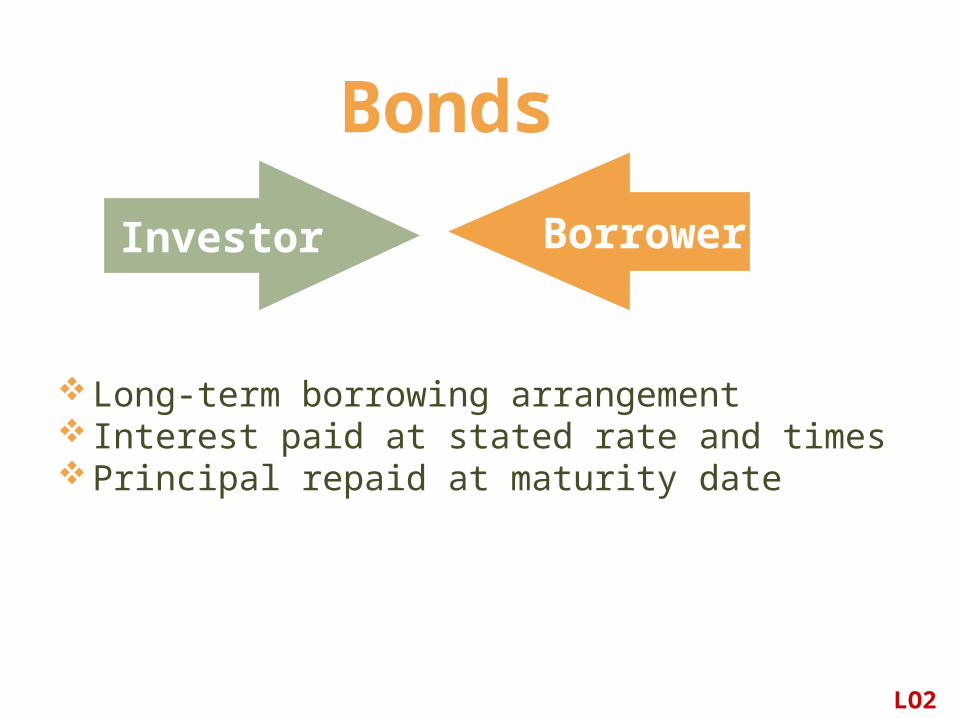

Bonds

Long-term borrowing arrangement Interest paid at stated rate and timesPrincipal repaid at maturity date

Investor Borrower

LO2

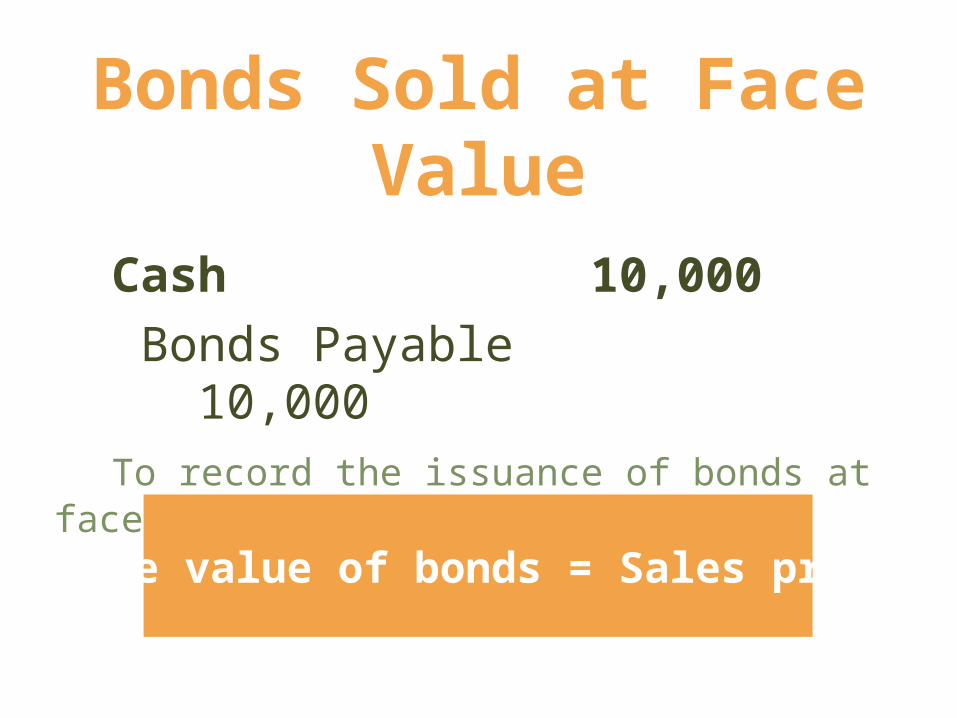

Bonds Sold at Face Value

Cash 10,000 Bonds Payable 10,000

To record the issuance of bonds at face value.

Face value of bonds = Sales price

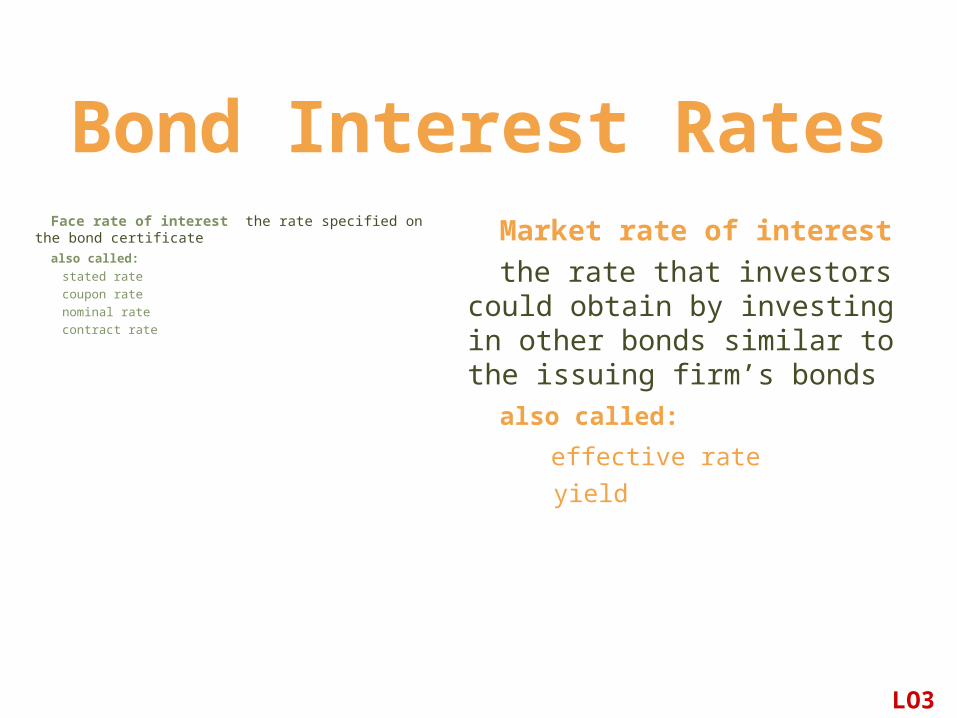

Bond Interest Rates Face rate of interest the rate specified on the bond certificate also called: stated rate coupon rate nominal rate contract rate

Market rate of interest the rate that investors could

obtain by investing in other bonds similar to the issuing firm’s bonds

also called:

effective rate yield

LO3

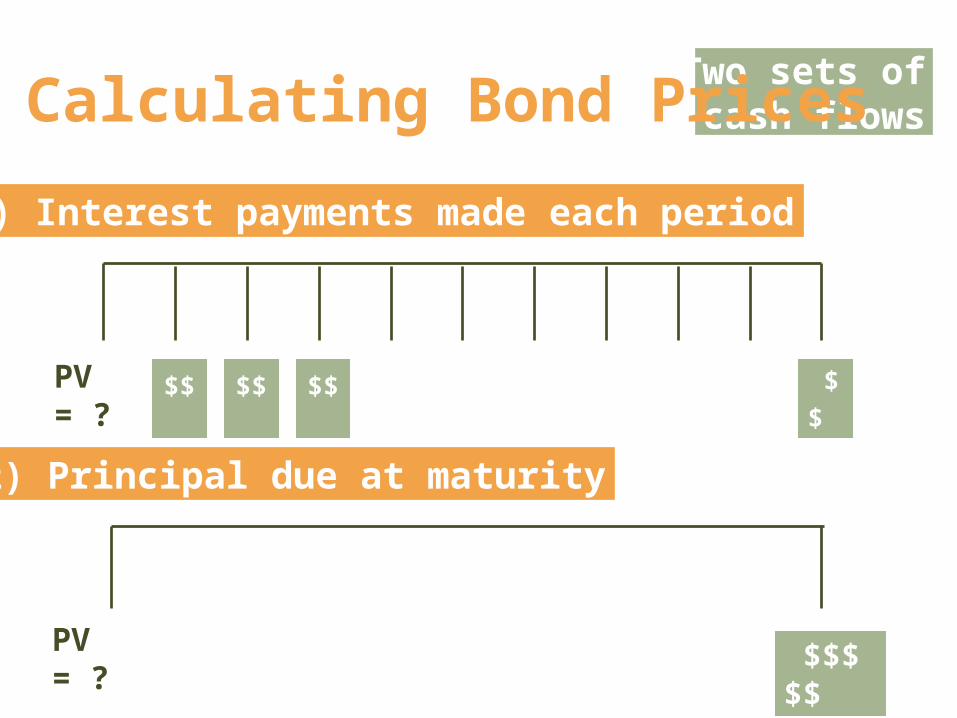

Two sets of cash flows

PV = ?

Calculating Bond Prices

$$

(2) Principal due at maturity

PV = ? $$$$$

(1) Interest payments made each period

etc. $$ $$ $$

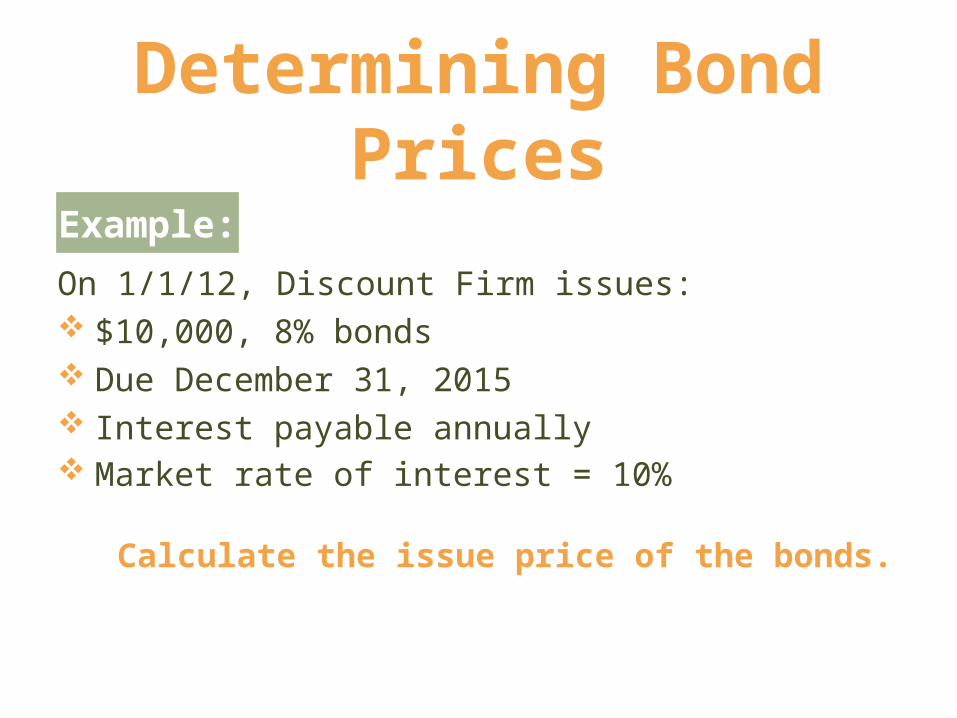

Determining Bond Prices

On 1/1/12, Discount Firm issues: $10,000, 8% bonds Due December 31, 2015 Interest payable annually Market rate of interest = 10%

Calculate the issue price of the bonds.

Example:

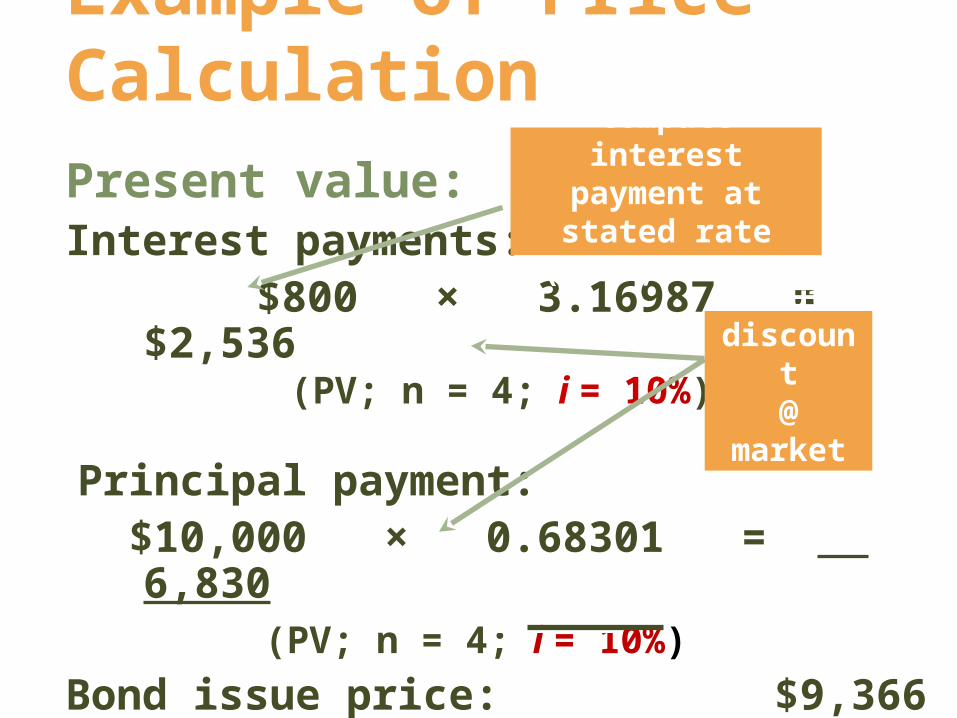

Present value:Interest payments: $800 × 3.16987 = $2,536

(PV; n = 4; i = 10%)

Principal payment: $10,000 × 0.68301 = 6,830

(PV; n = 4; i = 10%)Bond issue price: $9,366

Example of Price Calculation

…butdiscount

@ market rate

Compute interestpayment at stated

rate (i.e., 8%)...

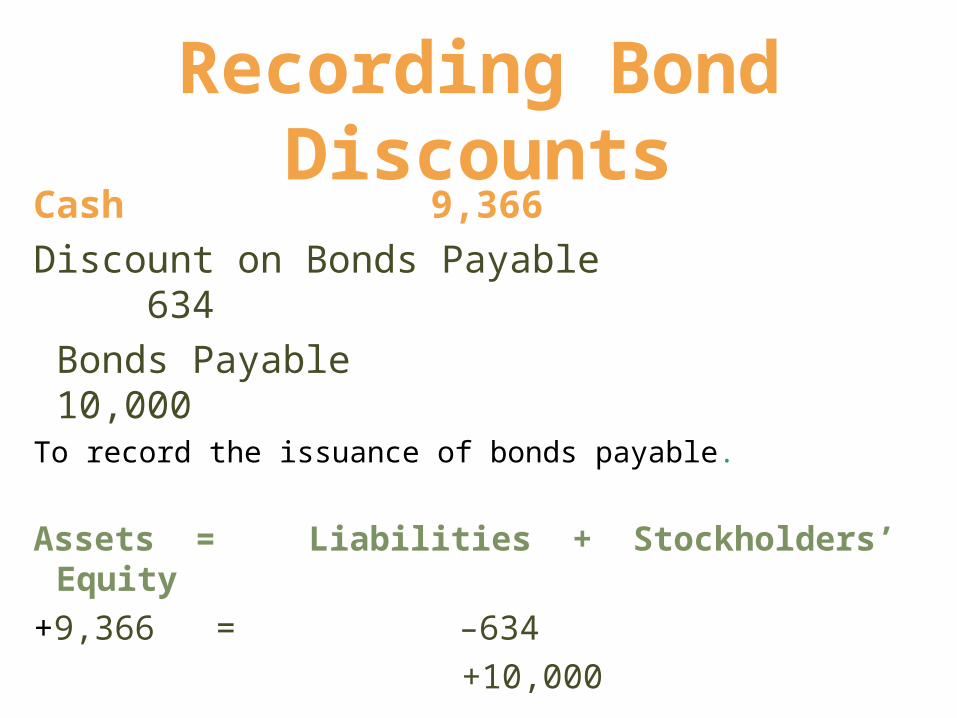

Recording Bond DiscountsCash 9,366Discount on Bonds Payable 634

Bonds Payable 10,000To record the issuance of bonds payable.

Assets = Liabilities + Stockholders’ Equity+9,366 = –634

+10,000 LO4

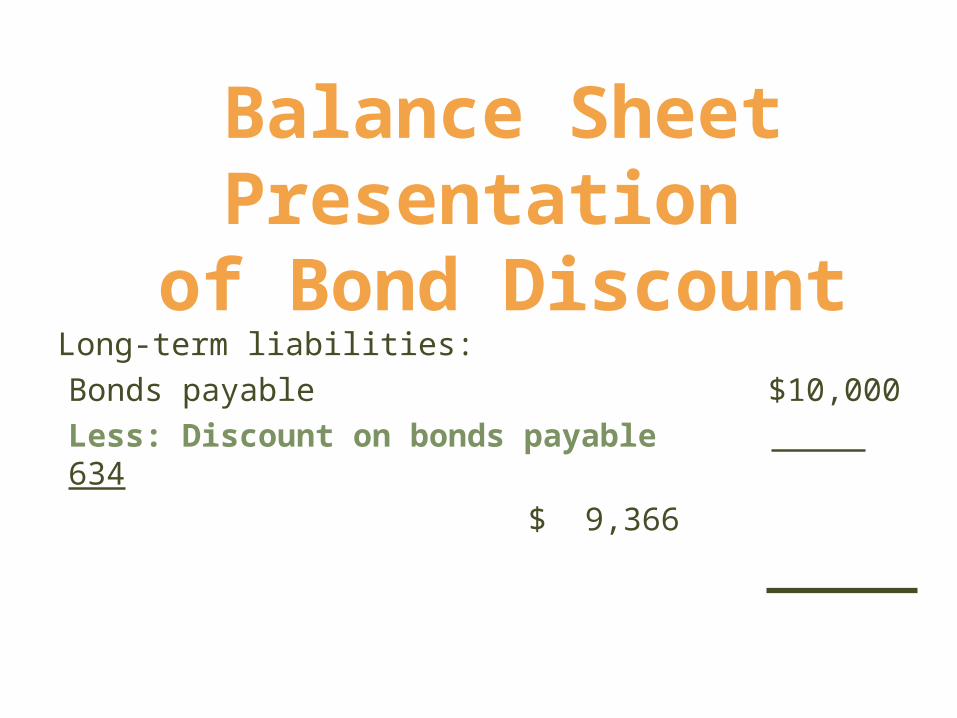

Balance Sheet Presentation of Bond Discount

Long-term liabilities:Bonds payable $10,000Less: Discount on bonds payable 634

$ 9,366

Determining Bond PricesAssume Premium Firm sells the same $10,000, 8% bonds when the market rate on similar bonds is 6%.

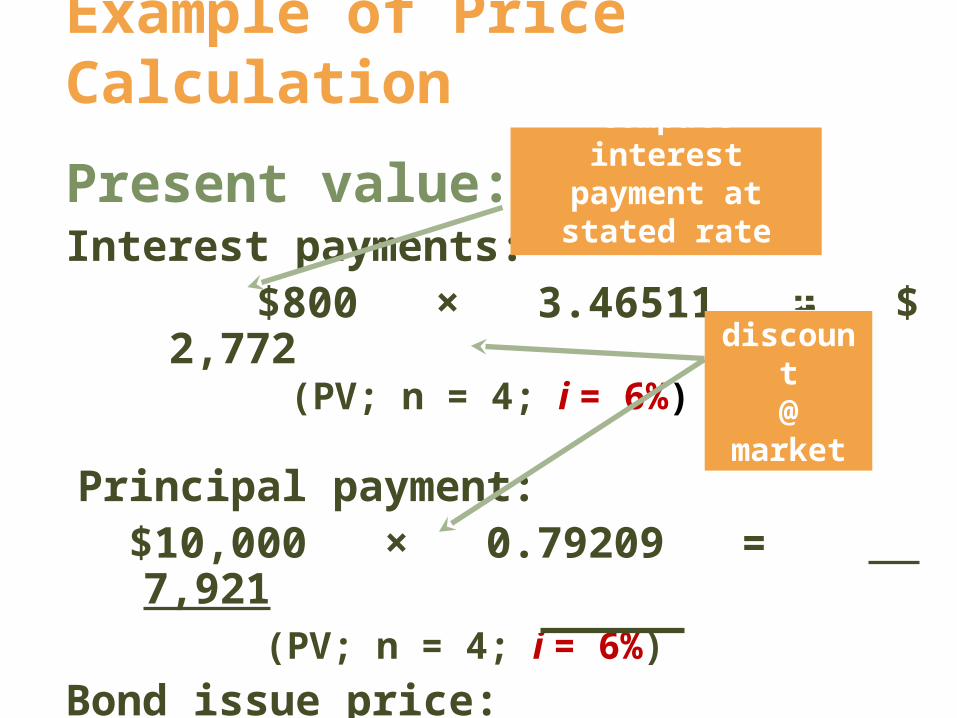

Present value:Interest payments: $800 × 3.46511 = $ 2,772

(PV; n = 4; i = 6%)

Principal payment: $10,000 × 0.79209 = 7,921

(PV; n = 4; i = 6%)Bond issue price: $10,693

Example of Price Calculation

…butdiscount

@ market rate

Compute interestpayment at stated

rate (i.e., 8%)...

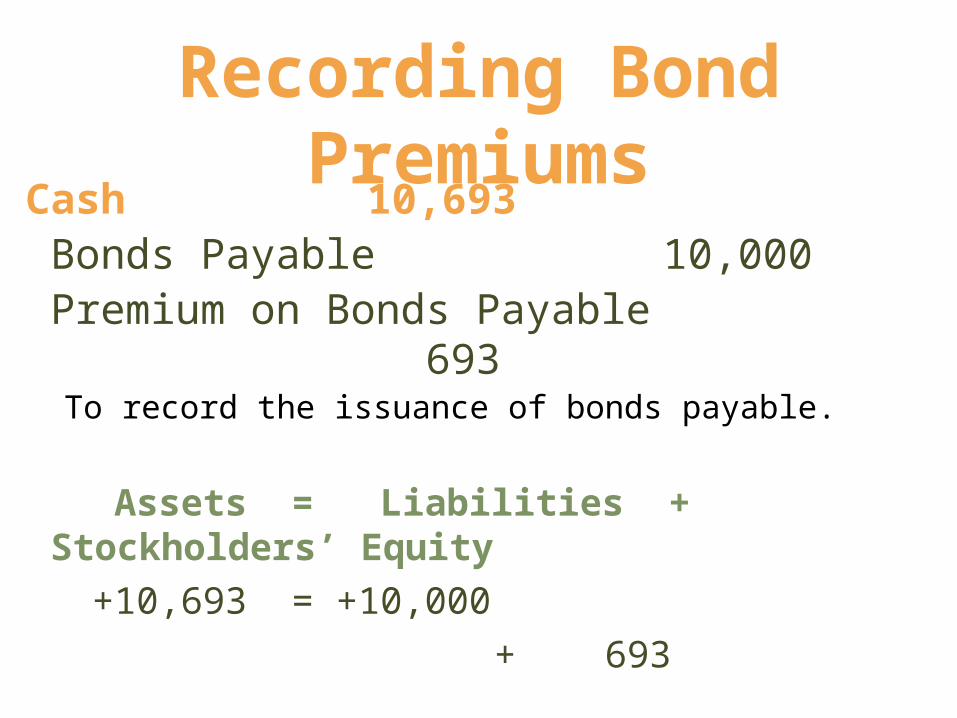

Recording Bond PremiumsCash 10,693

Bonds Payable 10,000Premium on Bonds Payable 693

To record the issuance of bonds payable.

Assets = Liabilities + Stockholders’ Equity +10,693 = +10,000

+ 693

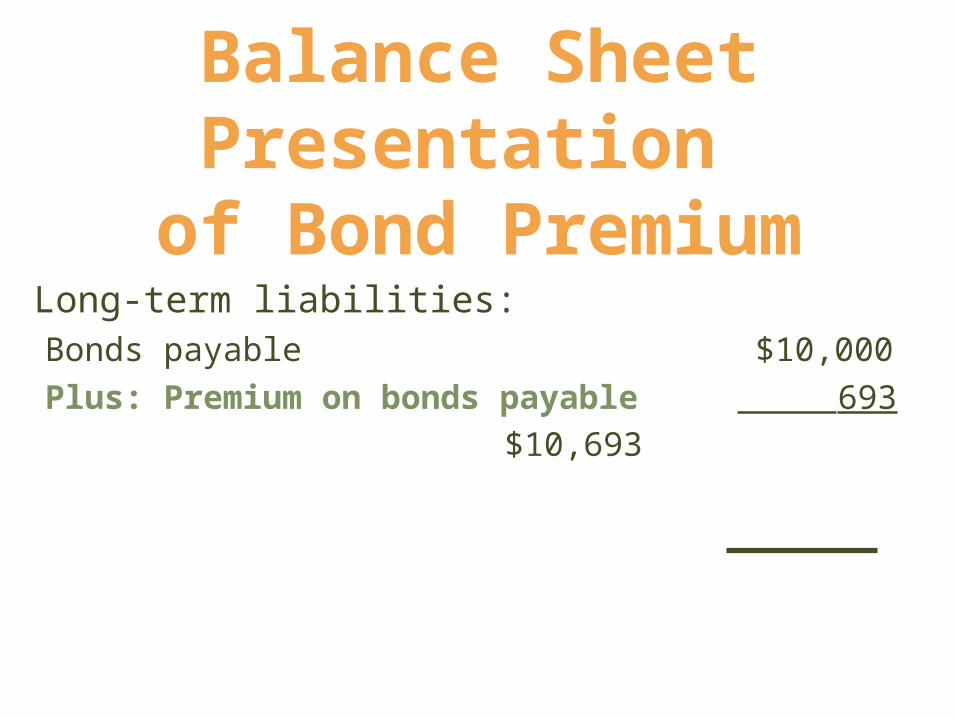

Balance Sheet Presentation of Bond Premium

Long-term liabilities:Bonds payable $10,000Plus: Premium on bonds payable 693

$10,693

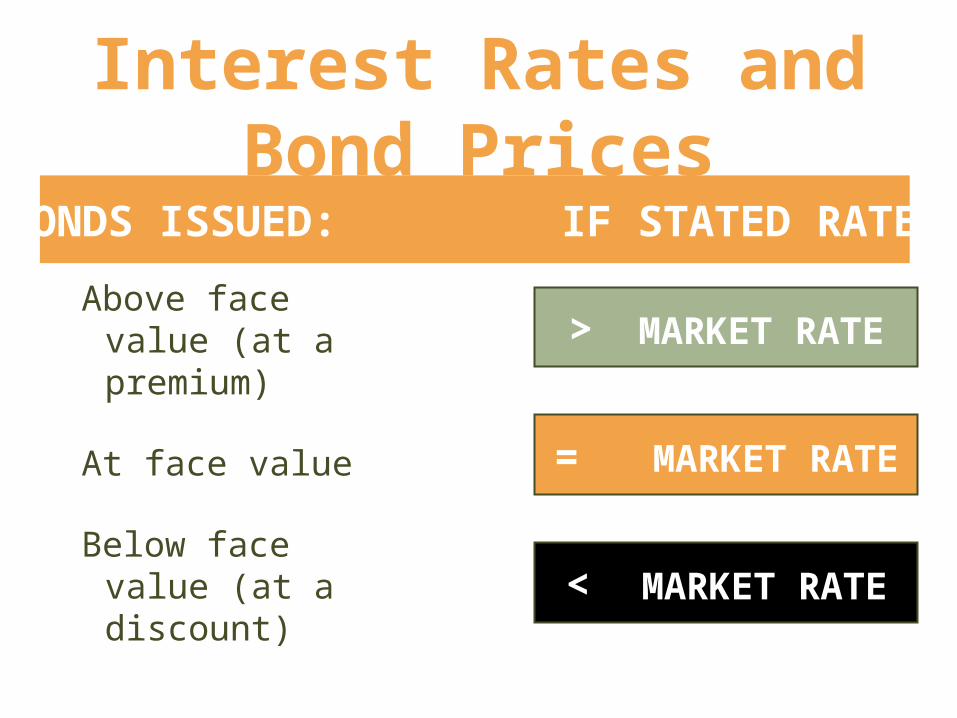

Interest Rates and Bond Prices

Above face value (at a premium)

At face value

Below face value (at a discount)

= MARKET RATE

BONDS ISSUED: IF STATED RATE:

> MARKET RATE

< MARKET RATE

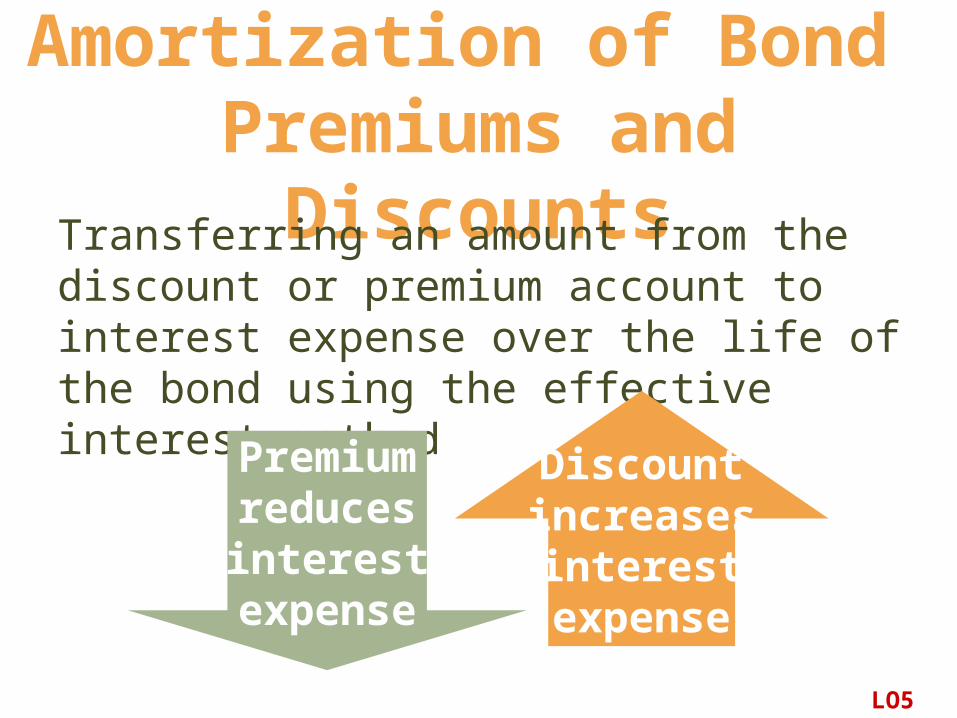

Amortization of Bond Premiums and Discounts

Transferring an amount from the discount or premium account to interest expense over the life of the bond using the effective interest method

Discountincreasesinterestexpense

Premiumreducesinterestexpense

LO5

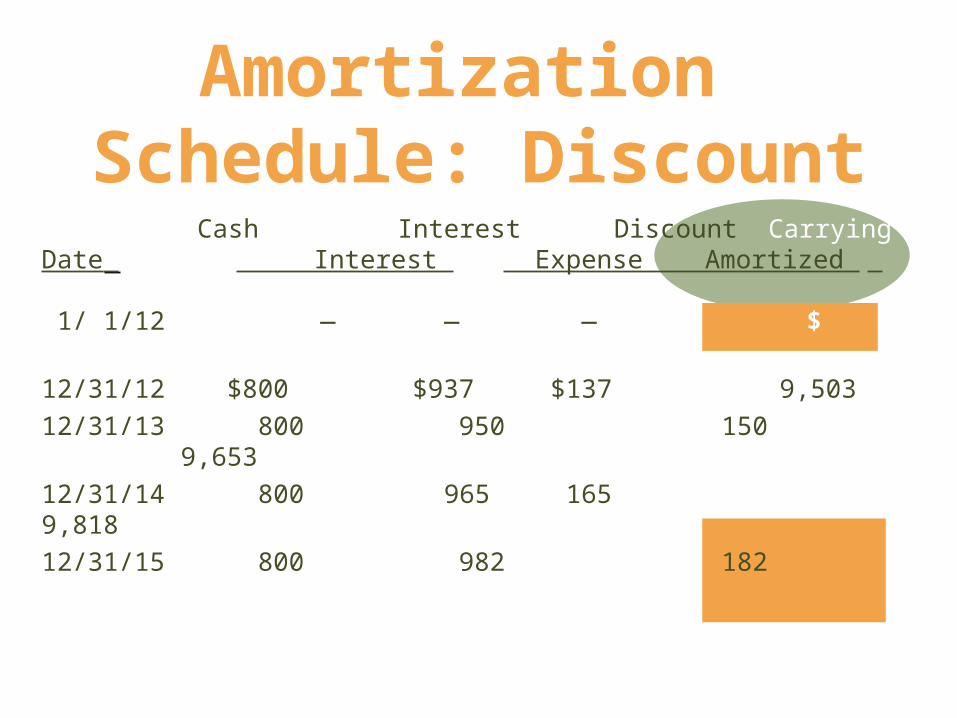

Amortization Schedule: Discount

Cash Interest Discount CarryingDate Interest Expense Amortized Value 1/ 1/12 — — — $ 9,36612/31/12 $800 $937 $137 9,50312/31/13 800 950 150 9,65312/31/14 800 965 165 9,81812/31/15 800 982 182 10,000

(rounded)

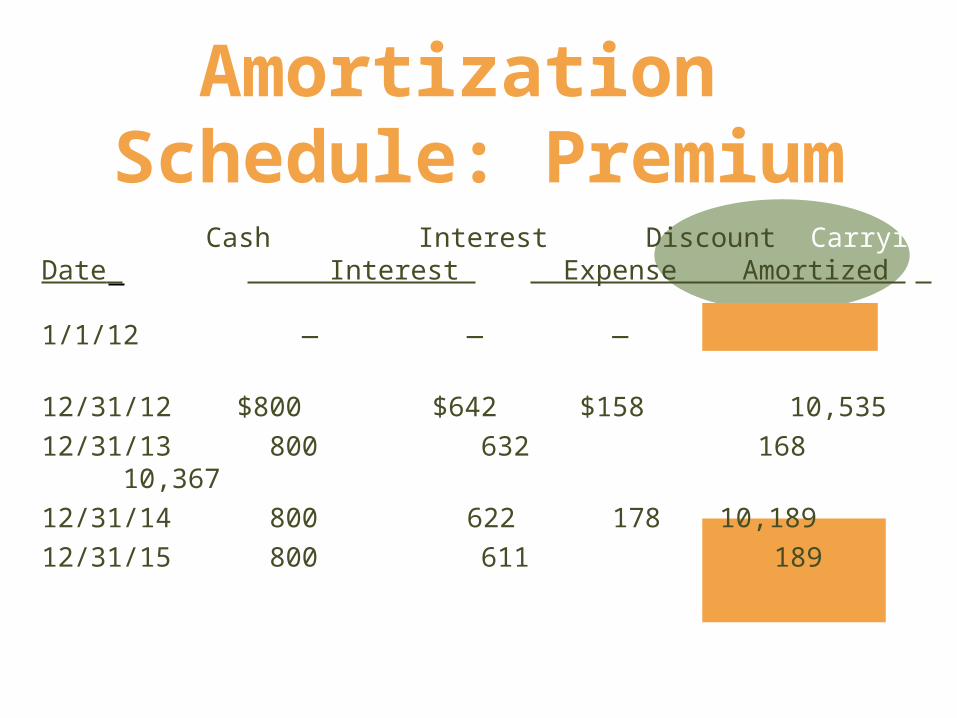

Amortization Schedule: Premium

Cash Interest Discount CarryingDate Interest Expense Amortized Value1/1/12 — — — $10,69312/31/12 $800 $642 $158 10,53512/31/13 800 632 168 10,36712/31/14 800 622 178 10,18912/31/15 800 611 189 10,000

(rounded)

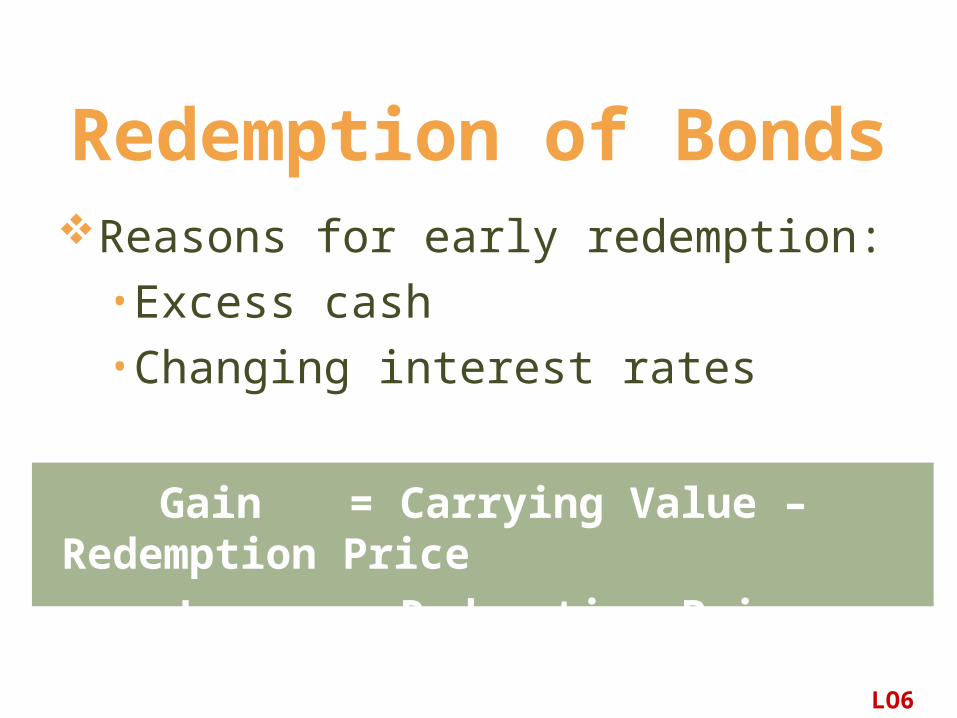

Redemption of BondsReasons for early redemption:

• Excess cash• Changing interest rates

Gain = Carrying Value – Redemption Price Loss = Redemption Price – Carrying Value

LO6

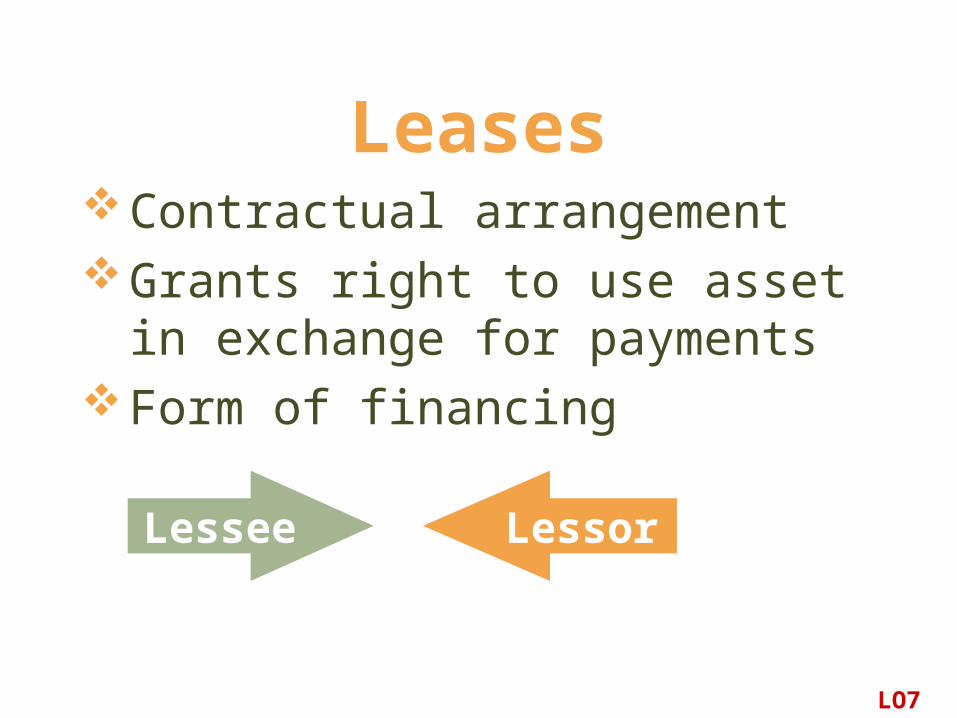

LeasesContractual arrangementGrants right to use asset in exchange

for paymentsForm of financing

Lessee Lessor

LO7

Operating LeasesRecord as rent (lease) expense

each periodDisclose future lease obligations

in financial statement notes

OFFICESPACE

FOR LEASE

Capital Lease Record as asset and corresponding liability

(as if purchased through borrowings)

Depreciate asset over lease term

Separate payments into principal and interest components using the effective interest method

Criteria for Lease Capitalization

Transfers ownership of property

Contains a bargain-purchase option

Term is >75% of property’s life

Present value of payments is >90% of property’s fair market value

Lease meets one or more:

IFRS and LeasesIn U.S., if any of the previous criteria are

present, the lease is considered a capital lease

IFRS considers these criteria as “guidelines” rather than rigid rules

Because of these differences , there is much more flexibility with international standards.

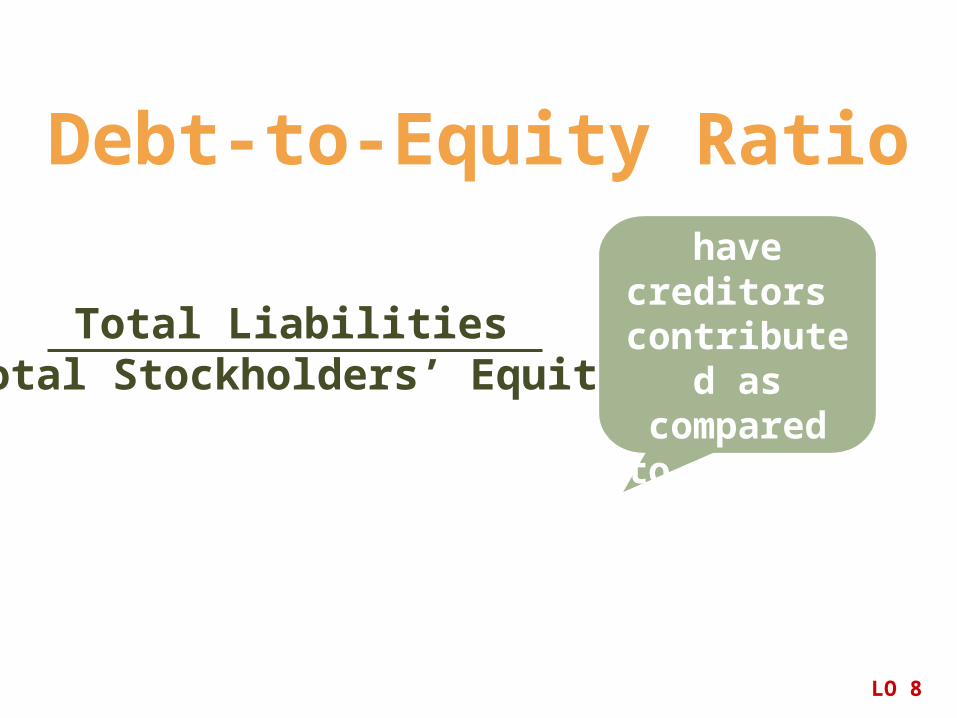

Debt-to-Equity Ratio

Total LiabilitiesTotal Stockholders’ Equity

How much have creditors contributed as compared to

owners?

LO 8

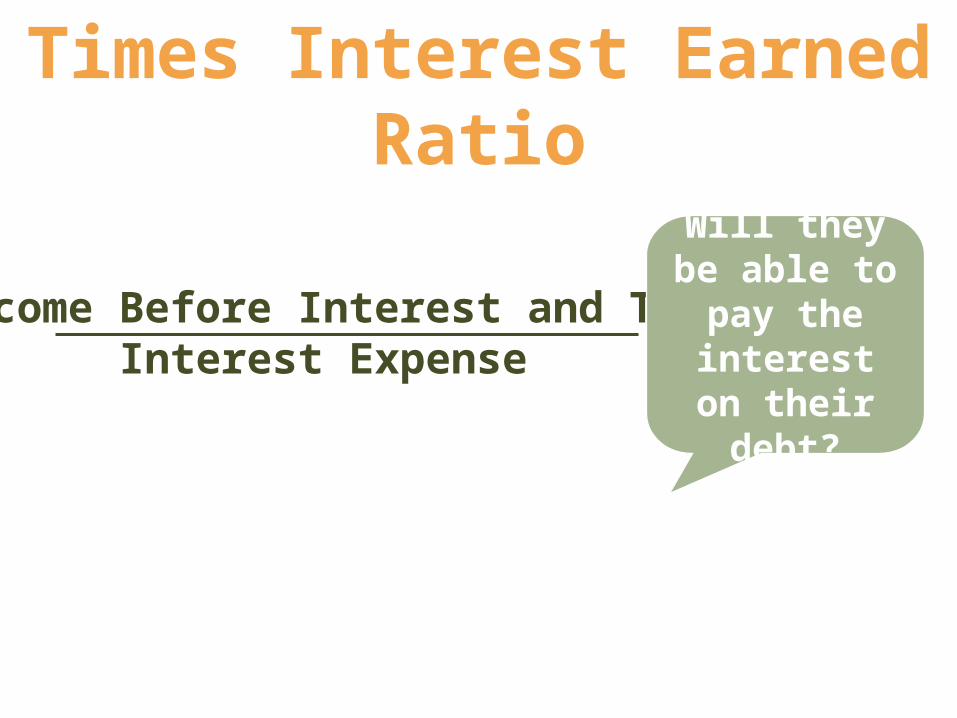

Times Interest Earned Ratio

Income Before Interest and TaxInterest Expense

Will they be able to pay the

interest on their debt?

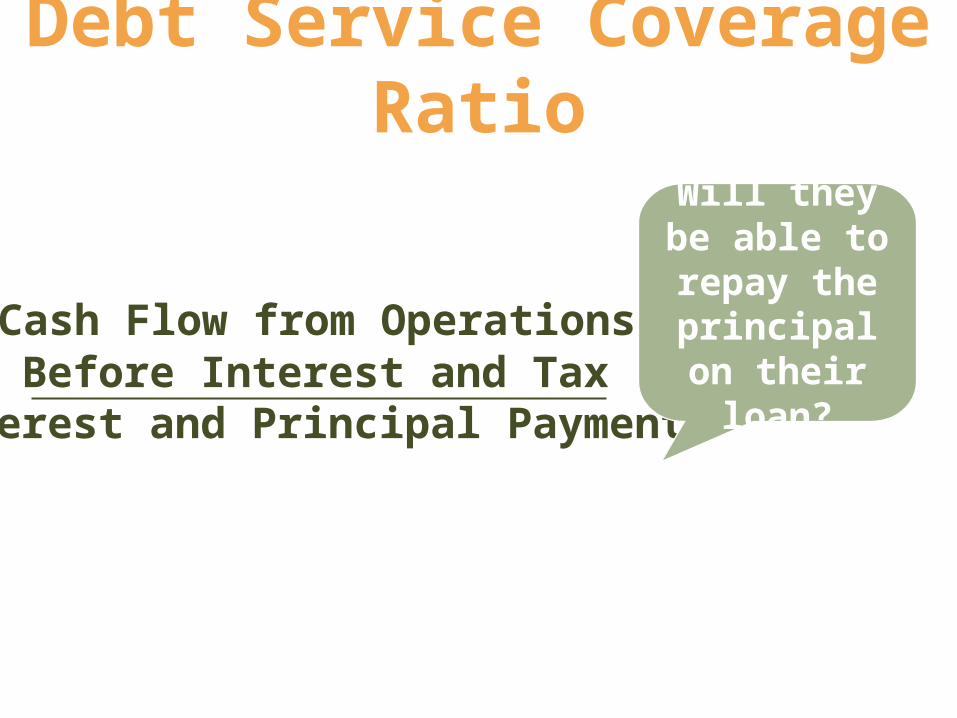

Debt Service Coverage Ratio

Cash Flow from Operations Before Interest and Tax

Interest and Principal Payments

Will they be able to repay the principal

on their loan?

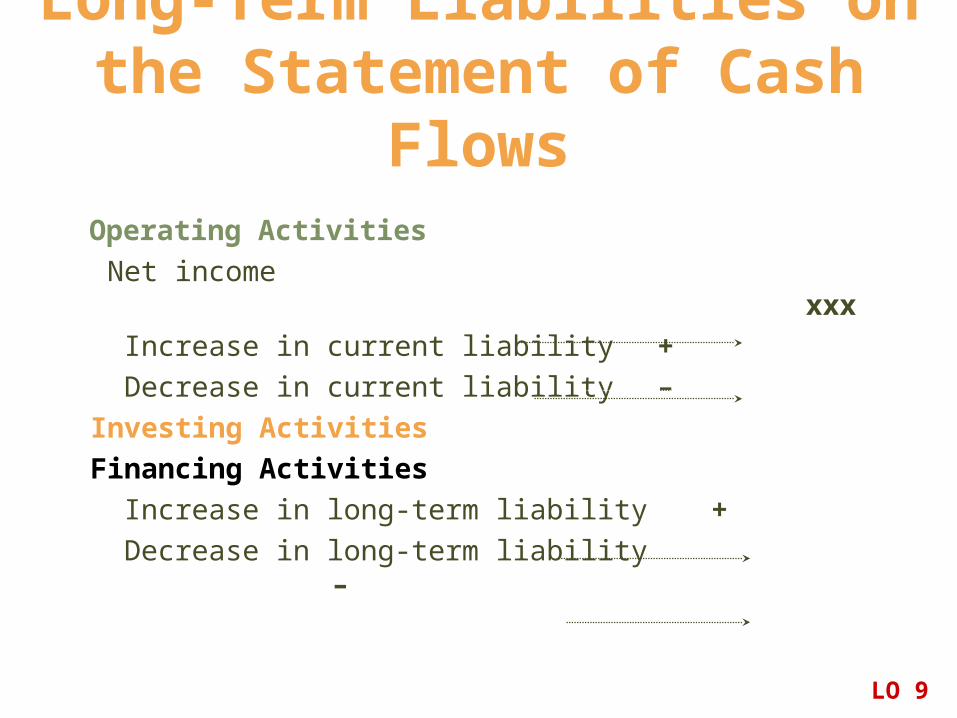

Long-Term Liabilities on the Statement of Cash Flows

Operating Activities Net income xxx Increase in current liability + Decrease in current liability – Investing Activities Financing Activities Increase in long-term liability + Decrease in long-term liability –

LO 9

AppendixAccounting Tools:

Other Liabilities

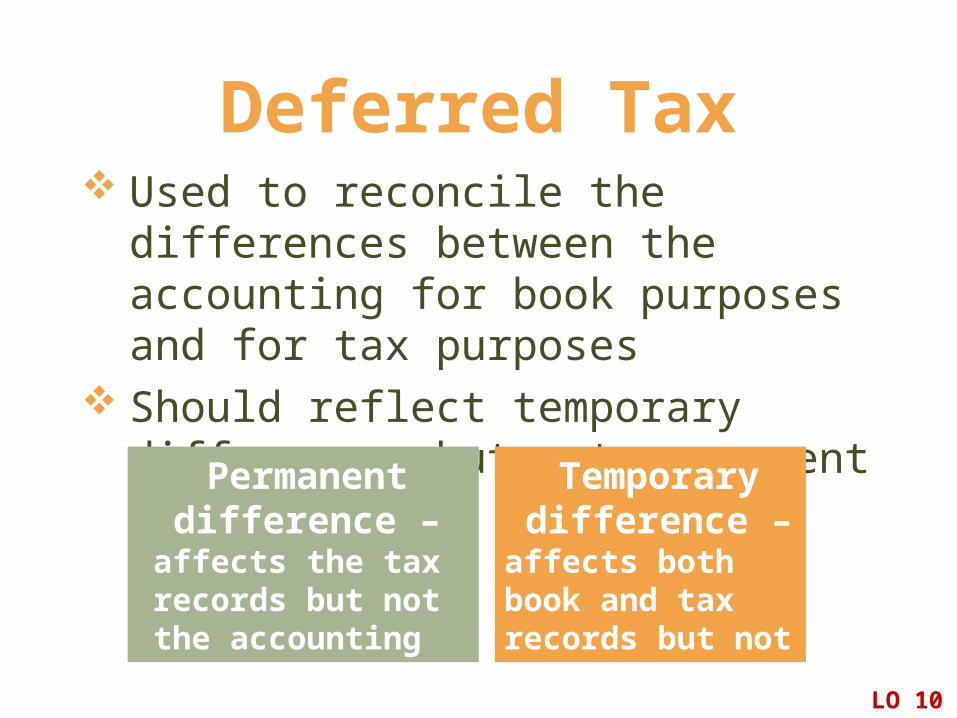

Deferred Tax Used to reconcile the differences between

the accounting for book purposes and for tax purposes

Should reflect temporary differences but not permanent differences

LO 10

Permanent difference –

affects the tax records but not the accounting records, or vice versa

Temporary difference –

affects both book and tax records but not in the same period

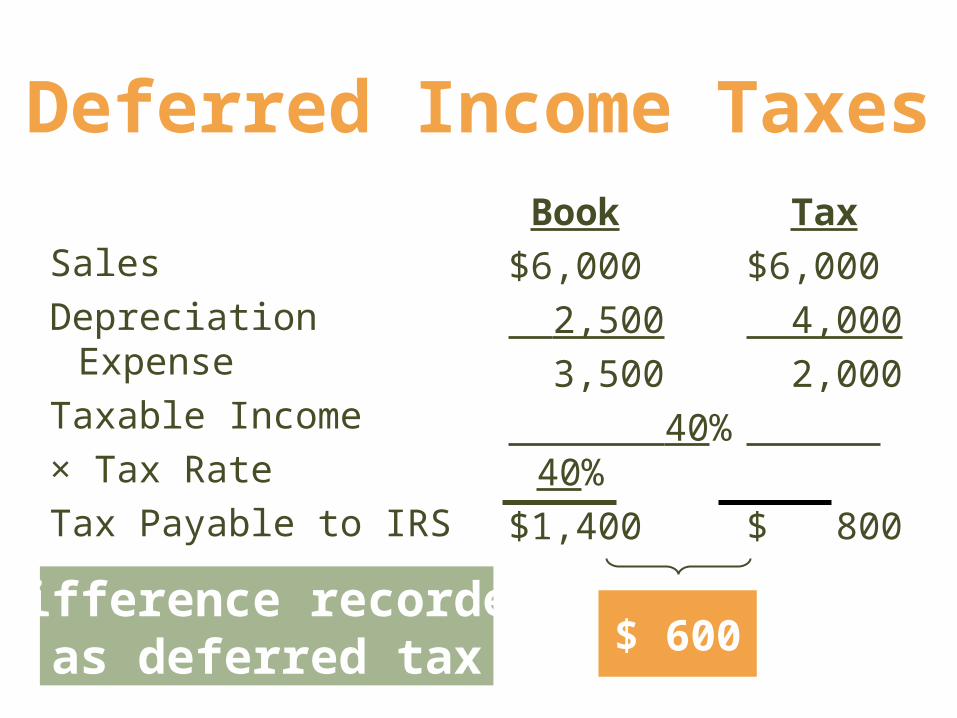

Deferred Income Taxes

SalesDepreciation ExpenseTaxable Income× Tax RateTax Payable to IRS

Book Tax$6,000 $6,000 2,500 4,000 3,500 2,000 40% 40%$1,400 $ 800

$ 600Difference recorded

as deferred tax

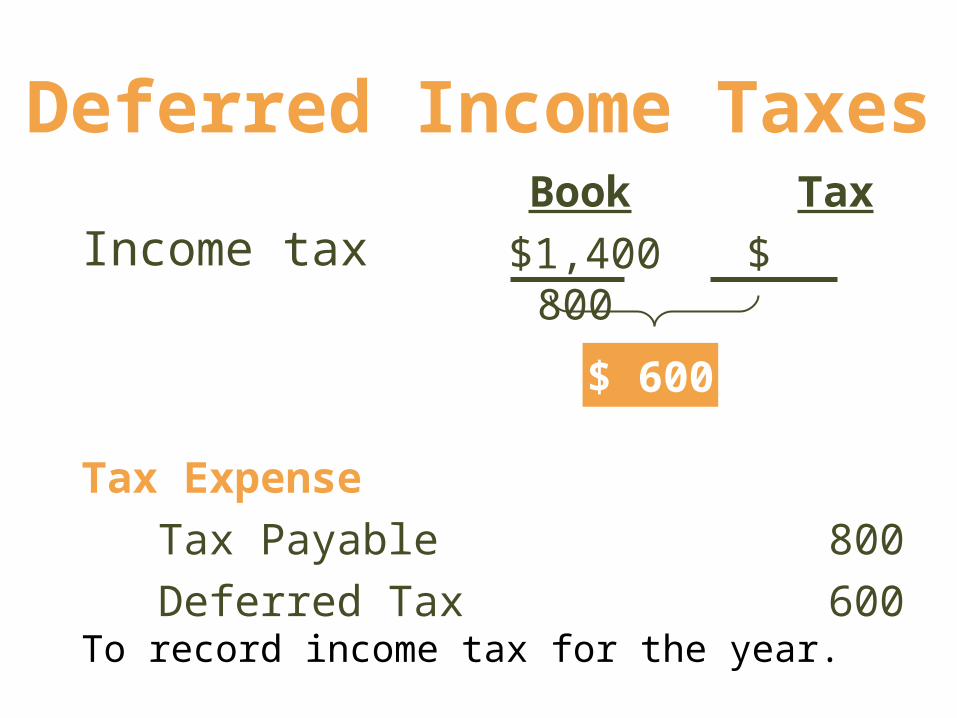

Deferred Income Taxes

Income tax Book Tax$1,400 $ 800

Tax Expense 1,400 Tax Payable 800 Deferred Tax 600To record income tax for the year.

$ 600

End of Chapter 10