balance · web viewintroduction the balance sheet is one type of financial statement. the...

TRANSCRIPT

BALANCE SHEET

Introduction

The balance sheet is one type of financial statement. The other types are the income statement, the statement of changes in owners’ equity, and the cash flow statement. A balance sheet lists the assets, liabilities, and owners’ equity of an entity at a particular point in time. Assets are probable future economic benefits obtained or controlled as a result of past transactions or events. Liabilities are probable future sacrifices of economic benefits arising from present obligations to transfer assets or provide services in the future as a result of past transactions or events.

The word probable indicates that uncertainties exist with respect to the recognition and measurement of assets and liabilities. This means that the value of a machine is recorded at the price paid even if there is some chance the machine may break down or become obsolete sometime in the near future. This also means that some contingent liabilities are recorded as obligations even if it is not certain that the obligations will be incurred.

The phrase future economic benefits indicates that items on the balance sheet have implications for the future –in particular, about forecasting the future. This means that if assets are determined to have been impaired, they are written down.

The phrase obtained or controlled indicates that even an entity does not legally own a particular item, the entity controls the future benefits from that item, it is recorded as an asset of the entity. This means that in some types of leases, the leased asset is recorded as an asset on the books of the lessee (the renter), even if the title to the asset still belongs to the lessor (the owner).

The phrase past transactions or events indicates that some economic event must already have happened before assets or liabilities can be recognized. This means that signing a purchase order is not enough to record an asset (for the item to be purchased) or a liability (for the price to be paid). The item must actually become the property of the buyer before the asset and the corresponding liability can be recorded.

Classified Balance Sheets and Operating Cycle

Balance sheets are referred to as a classified balance sheet. Assets and liabilities are broadly classified as current or noncurrent. Current means one year from the date of the balance sheet or an operating cycle, whichever is longer.

Current assets are items that are expected to be converted to cash or used in the normal operations of an entity within one year or the operating cycle, whichever is longer. Current liabilities are obligations that are expected to be paid (or satisfied) within one year or the operating cycle, whichever is longer.

Operating cycle is the time it takes for an entity to go from cash and come back to cash after performing its transactions. For example, the operating cycle for a merchandising firm is as follows:

Cash Purchases Inventory Sales Receivables Collections Cash

The three elements given in italics all take time. For example, it may take a few days from the time an item is ordered before it arrives in the store and is ready to be sold. Similarly, it may take some time for an item to be sold, and a few days may elapse from the time it is sold until cash is collected from the customer. The total time to go from cash to cash (that is, the time taken by all the activities as we move from cash to inventory to receivables to cash) is called the operating cycle.

The operating cycle for a manufacturing firm is longer than for a merchandising firm. This is so because the company must first purchase the raw materials and then manufacture the finished goods.

A few industries, such as real estate, specialized farming, or wine-making, have an operating cycle that could be longer than a year. However, for most companies, the operating cycle is less than a year.

Current Assets

Current assets include cash, investments, receivables, inventories, and prepaid assets. In the United States and Canada, cash is listed on the balance sheet first, and the other items are presented in order of liquidity (that is, “nearness to cash” –how quickly an item can be converted to cash). For example, there is only one step in going from accounts receivable to cash –collection from the customer. However, going from inventory to cash involves two steps –first selling the item, and then collecting the cash from the customer. Therefore, accounts receivable are listed ahead of inventory on the balance sheet. Prepaid assets are listed after inventory because they typically may not be convertible to cash but are available for use by the entity.

Companies may purchase stocks or bonds issued by other entities with the intent to sell them in the short term. These investments are called trading securities. Investments are usually listed ahead of receivables because they may be sold immediately and cash can be collected almost immediately, while collecting on a receivable involves more time. (An entity controls the sale of a trading security but it does not entirely control the collection of a receivable. Someone else has to pay the entity.)

There are exceptions, of course. For example, cash that is restricted for noncurrent use (such as to purchase of equipment) is not included in current assets. Land that is held for resale within the next year is classified as a current asset.

Note that differences in the presentation order of the balance sheet items occur in various countries. For example, some countries require the noncurrent assets to be listed first followed by current assets.

Noncurrent Assets

Noncurrent assets include investments; property, plant and equipment; intangible assets; and other assets.

Investments include (1) stocks and bonds of other entities, which management does not intend to sell within the next year, (2) sinking-fund investments, (3) ownership interest in other entities held for the purpose of exerting control, and (4) miscellaneous investments (such as land) not directly related to regular operations of the business.

Property, plant, and equipment (PPE) include land, buildings, machinery, tools, furniture, and vehicles. Land is not depreciated; other PPE assets are shown on the balance sheet at cost less accumulated depreciation.

Intangible assets include items such as goodwill, patents, copyrights, trademarks, franchises, and organizational costs. Such assets are shown at their cost less any amortized amounts. Amortization and depreciation are similar, but the term depreciation is used only for tangible assets (PPE) and the term amortization is used for intangible assets. Another difference is that unlike the accumulated depreciation for tangible assets, there is no accumulated amortization account. Each period when an intangible asset is amortized, the intangible asset account is directly credited (reduced).

Other assets include items that cannot be included in any of the other noncurrent asset categories. The most important item in this category is deferred tax assets, which arise when future tax benefits are expected. When some items have been included as expenses in the income statement for financial reporting purposes but have not yet been included as expenses for tax reporting purposes, deferred tax assets may arise. This happens because such expense items can be included in calculating taxable income in future tax years and thus can reduce future taxes. Such items, therefore give future economic benefits and hence are categorized as assets.

Liabilities

As noted earlier, current liabilities are obligations that are expected to be paid (or otherwise satisfied) within one year or operating cycle, whichever is longer. Current

liabilities are recorded at their face value (that is, the full amount expected to be paid in the future).

The major types of current liabilities are accounts payable, short-term borrowings, accrued expenses, and unearned revenue. In addition, any part of a long-term liability that must be repaid within the next year (or operating cycle) is included in the current liabilities section.

Liabilities that must be paid next year (or within the next operating cycle) are excluded from current liabilities (and classified as noncurrent) if they are (1) expected to be refinanced through another long-term issue or (2) retired out of noncurrent assets.

Noncurrent liabilities are obligations expected to be paid (or satisfied) beyond the next year or operating cycle. They include long-term notes, bonds, mortgages, and lease obligations. Noncurrent liabilities are generally recorded at their discounted present value.

Note that we earlier discussed deferred tax assets. In some other circumstances, the differences between financial statement reporting and income tax reporting (which are legitimate and required or permitted by tax laws) give rise to situations in which an expense may be claimed at present value for tax reporting purposes but can be deducted in the financial statements only in the future. In such situations, a deferred tax liability arises because future taxable income (and future taxes) is higher than the future net income reported for financial statement purposes. This deferred tax liability could be current, noncurrent, or a mixture of both. Unlike other noncurrent liabilities, deferred tax liabilities that are classified as noncurrent are recorded at the face value without any present value discounting.

Owners’ Equity

The owners’ equity section of a business varies depending on the type of business enterprise. Sole proprietorships are businesses owned by a single person, and the owners’ equity for such a business is represented by a single account. Partnerships involve two or more owners, and a separate capital account is established for each partner. The major disadvantage of sole proprietorships and partnerships is that the owners are subject to unlimited liability, not only to their investment in the business.

A corporation is different from a proprietorship or a partnership in many ways. The most important difference is that the business is a separate legal entity from the owners. Hence, the owners have limited personal liability. However, one important disadvantage of corporations is that they are subject to double taxation. The corporation is first taxed on its profits, and the stockholders must pay tax on the dividends they receive.

Owners’ equity (also referred to as stockholders’ equity) includes contributed capital and retained earnings. Contributed capital represents the amounts invested by the stockholders and equals the total of the Capital Stock and Additional Paid-in Capital accounts in the balance sheet.

There may be two types of contributed capital accounts: common stock and preferred stock. Preferred stockholders are usually paid a fixed amount of dividends each year and have preference over common stockholders in recovering their investments if the company is liquidated. However, preferred stockholders usually do not have voting rights in managing the company.

Retained earnings refers to net income that has not been given back to the stockholders; that is, it is retained in the business. Retained earnings is increased by the amount of net income, and is reduced by the amount of dividends. If a company has had losses for a few years, retained earnings may be a negative number (a deficit).

The capital stock account on the balance sheet typically provides information about the following: the number of shares authorized to be issued, the number of shares actually issued, and the number of shares outstanding. Note that the number of shares outstanding equals the number of shares issued less the number of shares bought back by the company. Treasury stock represents shares bought back by the company; its value is deducted from stockholders’ equity. (Thus, if a company buys another company’s stock, the company reports it as an asset; however, if a company buys back its own stock it reports this stock as a contra-equity item.)

Other items appear in the stockholders’ equity section. Two of the more common ones are (1) unrealized gains and losses on certain types of securities and (2) foreign currency translation adjustments.

Review Question–1

1. An example of a current asset is _______.

2. An example of a noncurrent asset is _______.

3. Salaries payable is a ______.

4. Bonds payable is a ______.

5. Double taxation is a disadvantage of a _______.

6. Unlimited liability is a feature of a _______.

Answers:1. accounts receivable 2. machinery 3. current liability

4. noncurrent asset 5. corporation 6. partnership

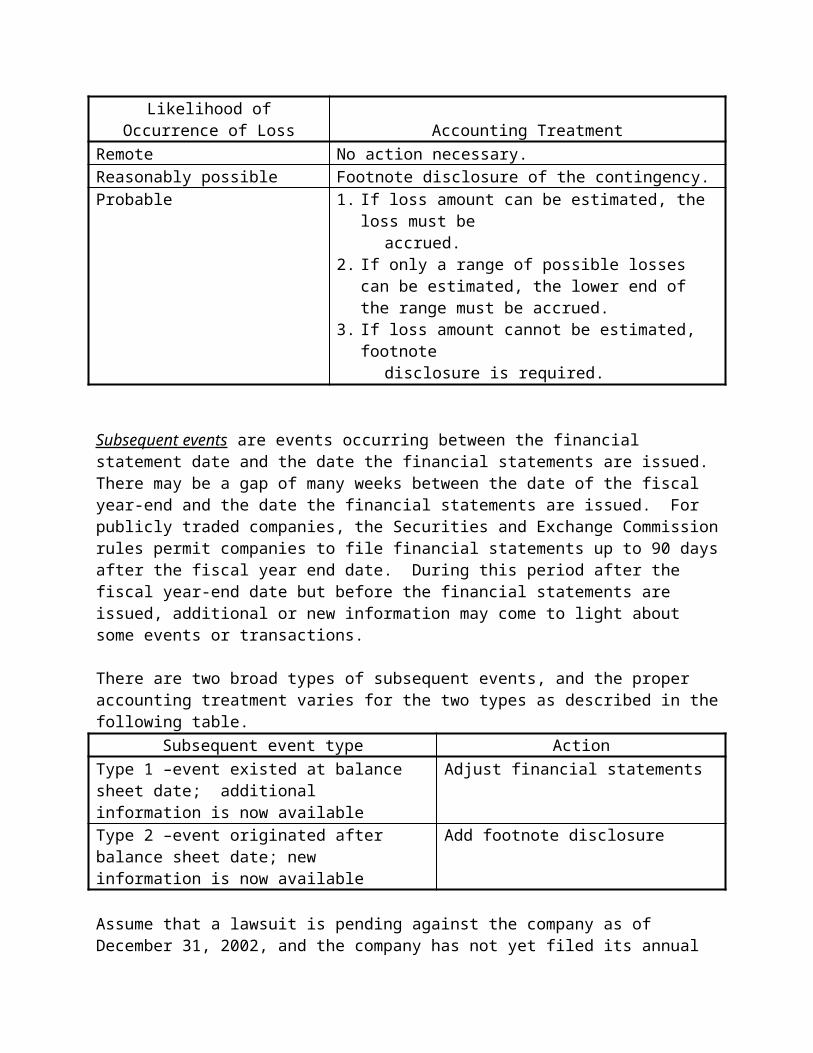

Footnotes, Contingencies, and Subsequent Events

Financial statements include detailed footnotes, that typically follow the presentation of basic financial statements (income statement, balance sheet, statement of changes in owners’ equity, and cash flow statement). The footnotes provide detailed information about accounting policies, some estimates used by management, and a variety of issues including contingencies and appropriate subsequent events.

Contingencies are events that have an uncertain outcome. Thus, a contingent event may or may not occur. The two broad types of contingencies are gain contingencies and loss contingencies.

Accounting for gain contingencies is simple. Following the conservatism principle, they are not recorded in the financial statements.

Accounting for loss contingencies is somewhat more complex. The proper accounting treatment depends on (1) the likelihood that the loss will occur, and (2) whether the amount of loss can be estimated. The following table gives the proper accounting treatment for different situations:

Likelihood of Occurrence of Loss Accounting Treatment

Remote No action necessary.Reasonably possible Footnote disclosure of the contingency.Probable 1. If loss amount can be estimated, the loss must be

accrued.2. If only a range of possible losses can be

estimated, the lower end of the range must be accrued.

3. If loss amount cannot be estimated, footnote disclosure is required.

Subsequent events are events occurring between the financial statement date and the date the financial statements are issued. There may be a gap of many weeks between the date of the fiscal year-end and the date the financial statements are issued. For publicly traded companies, the Securities and Exchange Commission rules permit companies to file financial statements up to 90 days after the fiscal year end date. During this period after the fiscal year-end date but before the financial statements are issued, additional or new information may come to light about some events or transactions.

There are two broad types of subsequent events, and the proper accounting treatment varies for the two types as described in the following table.

Subsequent event type ActionType 1 –event existed at balance sheet date; additional information is now available

Adjust financial statements

Type 2 –event originated after balance sheet date; new information is now available

Add footnote disclosure

Assume that a lawsuit is pending against the company as of December 31, 2002, and the company has not yet filed its annual financial statements at the end of February 2003. On February 15, 2003, the company settled the lawsuit by paying $5 million to the plaintiff. This is a type 1 subsequent event because the lawsuit existed as of the fiscal year-end, and now information about the outcome is available. So a loss of $5 million related to the lawsuit must be recorded for the fiscal year ending 1December 31, 2002 (if the amount has not previously been accrued).

Assume that a fire in a warehouse destroyed goods worth $2 million on January 20, 2003. This is a type 2 subsequent event because the event was not pending as of the fiscal year end (December 31, 2002). This event therefore will be disclosed in a footnote to the financial statements.

Financial Analysis Based on Balance Sheet Information

The information presented in the balance sheet can be used in a variety of ways to perform financial analysis. Horizontal analysis refers to comparisons of various accounts or percentages over time. For example, comparisons of inventory amounts over two or more years is an example of horizontal analysis. Vertical analysis refers to comparisons of different items that are expressed as a percent of a base. For example, expressing different balance sheet items as a percentage of total assets and comparing these percentages is an example of vertical analysis.

A number of ratios are used in financial analysis. Financial ratios express the relationships between various financial statement items, and are useful in examining a company’s performance.

LIQUIDITY refers to the ability of a company to pay its obligations in the short term. Liquidity is measured using the following ratios:

Current ratio = Current assets/Current liabilitiesQuick ratio = Quick assets/Current liabilities

Current assets and current liabilities were discussed earlier. Quick assets are current assets excluding inventory and prepaid items. Thus, quick assets include cash, short-term investments, and accounts receivable. The ratio is sometimes called the acid test ratio.

In general, a company with a high current ratio and a high quick ratio is considered safe because there is a high likelihood that it will be able to pay its obligations in the short term. A very low current ratio or quick ratio indicates that the company may have difficulty paying its obligations in the short term, which could lead to bankruptcy. The current ratio and the quick ratio may be particularly relevant for short-term creditors, such as suppliers considering selling on credit or a bank examining an application for a short-term loan.

Another measure of liquidity is working capital, which is defined as current assets minus current liabilities.

SOLVENCY refers to the long-term viability of a company, and its ability to meet its obligations. Solvency (or leverage) is usually measured as follows:

Debt ratio = Total liabilities/Total assetsIn general, a low debt ratio indicates a strong company. The higher the debt ratio, the greater is the likelihood that the company may have difficulty repaying all its obligations on time.

Asset turnover measures a company’s efficiency in using its assets to generate sales revenue. It is measured as follows:

Asset turnover = Sales/Total assetsHigh values of asset turnover indicate that the company is using its assets efficiently in generating sales revenue.

Profitability ratios compare the relationship between net income and balance sheet measures such as total assets and stockholders’ equity. Profitability is measured as follows:

Return on assets (ROA) = Net income/Total assetsReturn on equity (ROE) = Net income/Stockholders’ equity

Miscellaneous Issues

The data presented in the balance sheet have some limitations. One limitation occurs because many of the noncurrent assets presented in the balance sheet may not reflect current values. For example, assume that a company bought a building in downtown New York 30 years ago. If the building is being depreciated on a straight-line basis over an estimated useful life of 40 years, the building appears on the balance sheet for a fraction of the original cost but today may be worth many times the original cost.

One way to overcome the problem with historical cost data is to use market values for various assets and liabilities (referred to as mark-to-market). However, this leaves too much room for managerial judgments and manipulation of accounting numbers.

A second limitation related to the balance sheet data is that many of the items involve judgments and estimates. For example, in calculating the book value of buildings and

machinery, estimates about useful lives must be made. In arriving at the net accounts receivable number, judgments about bad debts must be made. These judgments are necessarily subjective, which means that the reported numbers could be different depending on the accountant making the decisions.

A third limitation of the balance sheet is that many items that are of value to the business are not included. For example, a company may have a loyal workforce and an excellent reputation in the community. These are valuable “assets” to have, but they are not reported on the balance sheet.

Review Questions –2

1. If a loss contingency is judged to be reasonably possible, then _____ is required.

2. If a loss contingency is judged to be probable and estimable, then ____ is required.

3. A measure of liquidity is the ______.

4. A measure of solvency (leverage) is the ______.

5. Financial statements must be adjusted for a _____ subsequent event.

6. Footnote disclosure is adequate for a _____ subsequent event.

Answers:1. footnote disclosure 2. accrual 3. current ratio4. debt ratio 5. type 1 6. type 2

Glossary

Contingencies are events that have an uncertain outcome.

Current assets are items that are expected to be converted to cash or used in the normal operations of an entity within one year or the operating cycle, whichever is longer.

Corporations are separate legal entities from their owners and therefore offer the owners limited liability. A disadvantage of this form is double taxation.

Current liabilities are obligations that are expected to be paid (or satisfied) within one year or the operating cycle, whichever is longer.

Current ratio equals current assets divided by current liabilities.

Horizontal analysis refers to comparisons of various accounts or percentages over time.

Liquidity refers to the ability of a company to pay its obligations in the short term.

Operating cycle is the time it takes an entity to go from cash and come back to cash after performing its transactions.

Partnerships are businesses that involve two or more owners.

Property, plant, and equipment include land, buildings, machinery, tools, furniture, and vehicles.

Quick ratio equals quick assets divided by current liabilities.

Sole proprietorships are businesses owned by a single person, and the owners’ equity for such a business is represented by a single account.

Trading securities are stocks or bonds issued by other entities and are purchased with the intent to sell them in the short term.

Treasury stock represents shares bought back by the company.

Type 1 subsequent event refers to the situation when an event exists at balance sheet date and additional information about the event becomes available before the financial statements are prepared.

Type 2 subsequent event refers to the situation when the event originates after balance sheet date but before the financial statements are prepared.

Vertical analysis refers to comparisons of different items that are expressed as a percentage of a base.

Working capital equals current assets less current liabilities.

Demonstration Problem 1Kallis Company

The post-closing account balances of Kallis Company as of December 31, 2002 follow. Prepare a classified balance sheet and calculate the current ratio, quick ratio, and debt ratio as of that date.

Accounts receivable 55,000Accounts payable 40,000Land 34,000Buildings 130,000Machinery 108,000Bad debt expense 8,000Salaries expense 75,000Bonds payable 92,000Cash 25,000Accumulated depreciation – building 35,000Accumulated depreciation – machinery 16,000Depreciation expense – building 10,000Depreciation expense – machinery 4,000Other operating expenses 55,000Treasury stock 10,000Salaries payable 18,000Cost of goods sold 230,000Goodwill 15,000Patents 4,000Common stock 35,000Sales revenue 450,000Inventory 64,000Allowance for doubtful accounts 2,000Retained earnings ?

Solution to Demonstration Problem–Kallis Company

First, prepare the asset and liabilities sections of the balance sheet.Assets = Liabilities + Owners’ equity$382,000 = $150,000 + Owners’ equityHence, owners’ equity is $232,000.

Owners’ equity = Common stock + Retained earnings - Treasury stock$232,000 = $35,000 + Retained earnings - $10,000.Hence, retained earnings is $207,000.

ASSETSCash $25,000Accounts receivable $55,000 less allowance for doubtful accounts (2,000) 53,000Inventory 64,000 $142,000

Property, Plant, and EquipmentLand 34,000Buildings 130,000 less accumulated depreciation (35,000) 95,000

Machinery 108,000 less accumulated depreciation (16,000) 92,000 221,000

Intangible assetsPatents 4,000Goodwill 15,000 19,000TOTAL ASSETS $382,000

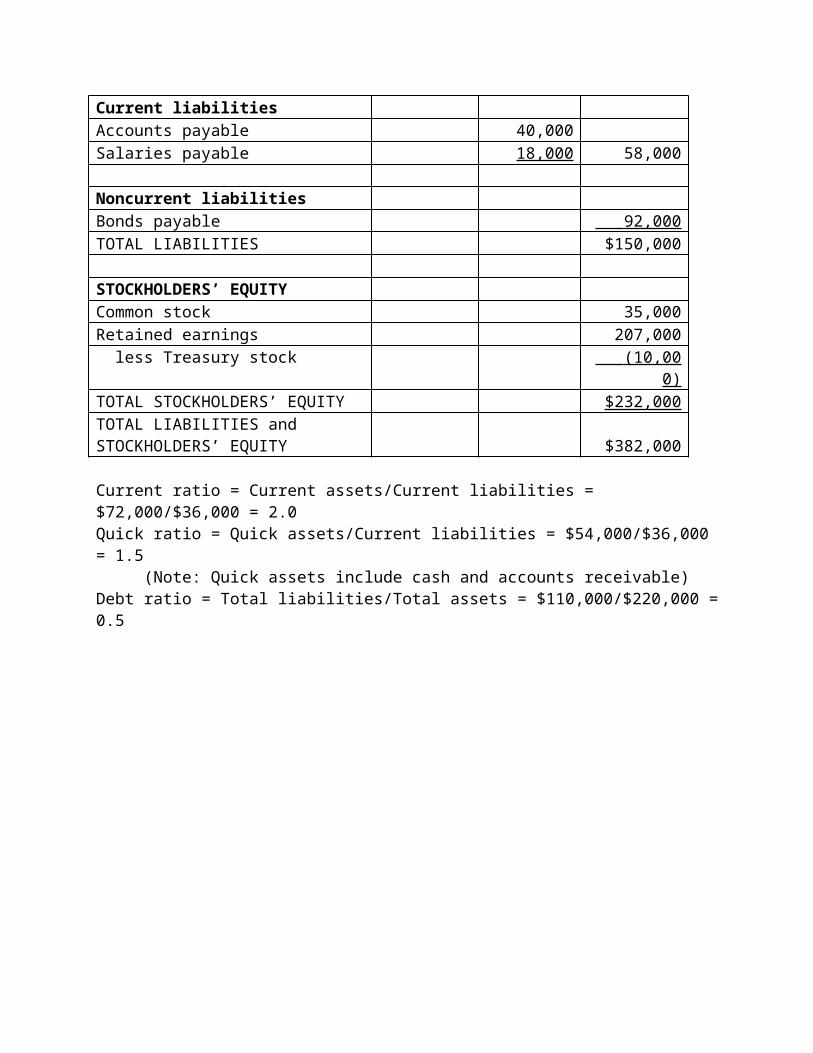

LIABILITIESCurrent liabilitiesAccounts payable 40,000Salaries payable 18,000 58,000

Noncurrent liabilitiesBonds payable 92,000 TOTAL LIABILITIES $150,000

STOCKHOLDERS’ EQUITYCommon stock 35,000Retained earnings 207,000 less Treasury stock (10,000)

TOTAL STOCKHOLDERS’ EQUITY $232,000TOTAL LIABILITIES and STOCKHOLDERS’ EQUITY $382,000

Current ratio = Current assets/Current liabilities = $72,000/$36,000 = 2.0Quick ratio = Quick assets/Current liabilities = $54,000/$36,000 = 1.5

(Note: Quick assets include cash and accounts receivable)Debt ratio = Total liabilities/Total assets = $110,000/$220,000 = 0.5

Demonstration Problem 2Simon Company

The balances in some accounts of Simon Company include the following:Accounts receivable 20,000Accounts payable 20,000Land 12,000Buildings less accumulated depreciation 20,000Machinery less accumulated depreciation 35,500Bonds payable 17,000Cash 10,000Salaries payable 5,000Common stock 10,000Inventory 22,500Retained earnings ?

Assume that the following independent transactions took place. What is the effect of each transaction on (a) the current ratio and (b) the debt ratio? Indicate “I” for increase, “D” for decrease, and “N” for no effect or no change.1. Collected accounts receivable worth $5,000 from a customer.2. Paid $3,000 on an accounts payable.3. Declared and paid dividends of $2,000.4. Issued $10,000 of bonds (payable five years from now).5. Purchased $5,000 of machinery by signing a long-term note payable.

Solution to Demonstration Problem–Simon Company

Before the transactions:Current assets = $10,000 + $20,000 + $22,500 = $52,500Current liabilities = $20,000 + $5,000 = $25,000Total assets = $52,500 (current assets) + $12,000 + $20,000 + $35,500 = $120,000Total liabilities = $25,000 (current liabilities) + $17,000 = $42,000

Current ratio = Current assets/Current liabilities = $52,500/$25,000 = 2.1Debt ratio = Total liabilities/Total assets = $42,000/$120,000 = 0.35

When you have a ratio greater than 1 and add the same number to the numerator and denominator, then the new ratio will be lower than the ratio with which you started. Conversely, when you have a ratio less than 1 and add the same number to the numerator and denominator, the new ratio will be higher than the old ratio with which you started. (Check this out with your own numbers.)

Effect of the following on the current ratio and the debt ratio:1. Collect accounts receivable. This increases cash but decreases accounts

receivable. Thus, current assets and total assets remain the same. Current liabilities and total liabilities are not affected, the current ratio and the debt ratio remain the same.

2. Pay accounts payable. This reduces cash and accounts payable. Thus, current assets, current liabilities, total assets, and total liabilities are all reduced. The current ratio will increase and the debt ratio will decrease.

3. Declare and pay dividends. This reduces cash and retained earnings. Thus, current assets, total assets, and owners’ equity are reduced but current liabilities and total liabilities remain unchanged. The current ratio will decrease and the debt ratio will increase.

4. Issue long-term bonds. This increases cash and long-term liabilities. Thus, current assets, total assets, and total liabilities will increase. The current ratio and debt ratio will increase.

5. Purchase machinery with long-term note payable. This will increase total assets and total liabilities, but current assets and current liabilities will remain unchanged. The current ratio will remain unchanged but the debt ratio will increase.

TransactionEffect on

Current RatioEffect on Debt

Ratio1. Collected on accounts receivable N N2. Paid accounts payable I D3. Declared and pay dividends D I4. Issued long-term bonds I I5. Purchased machinery with long-term notes payable

N I

Practice Problem 1Lara Company

The post-closing account balances of Lara Company as of December 31, 2002 follow. Prepare a classified balance sheet and calculate the current ratio, quick ratio, and debt ratio as of that date.

Accounts receivable 42,000Accounts payable 24,000Land 25,000Buildings 84,000Machinery 57,000Bonds payable 74,000Cash 14,000Accumulated depreciation – building 16,000Accumulated depreciation – machinery 15,000Treasury stock 5,000Salaries payable 12,000Goodwill 10,000Patents 3,000Common stock 20,000Inventory 18,000Allowance for doubtful accounts 2,000Retained earnings 95,000

Solution to Practice Problem–Lara Company

ASSETSCash $14,000Accounts receivable $42,000 less allowance for doubtful accounts (2,000) 40,000Inventory 18,000 $72,000

Property, Plant, and EquipmentLand 25,000Buildings 84,000 less accumulated depreciation (16,000) 68,000

Machinery 57,000 less accumulated depreciation (15,000) 42,000 135,000

Intangible assetsPatents 3,000Goodwill 10,000 13,000TOTAL ASSETS $220,000

LIABILITIESCurrent liabilitiesAccounts payable 24,000Salaries payable 12,000 36,000

Noncurrent liabilitiesBonds payable 74,000 TOTAL LIABILITIES $110,000

STOCKHOLDERS’ EQUITYCommon stock 20,000Retained earnings 95,000 less Treasury stock (5,000) TOTAL STOCKHOLDERS’ EQUITY $110,000TOTAL LIABILITIES and STOCKHOLDERS’ EQUITY $220,000

Current ratio = Current assets/Current liabilities = $72,000/$36,000 = 2.0Quick ratio = Quick assets/Current liabilities = $54,000/$36,000 = 1.5

(Note: Quick assets include cash and accounts receivable)Debt ratio = Total liabilities/Total assets = $110,000/$220,000 = 0.5

Practice Problem 2George Company

The balances in some accounts of George Company follow:Accounts receivable 5,000 Accounts payable 2,500 Land 3,000 Property, plant and equipment (net) 6,000 Bonds payable 5,000 Cash 1,000 Salaries payable 1,500 Common stock 2,000 Inventory 3,000 Retained earnings ?

Assume that the following independent transactions took place. What is the effect of each transaction on (a) working capital and (b) the debt ratio? Indicate “I” for increase, “D” for decrease, and “N” for no effect or no change.1. Received $500 from a customer as advance for services to be rendered next month.2. Issued stock for $1,000 cash.3. Purchased machinery for $700 by paying cash.4. Declared (but will pay later) dividends of $600.5. Collected accounts receivable worth $800 from a customer.6. Paid $900 on an accounts payable.7. Converted $500 of accounts payable to a long-term note payable.

Solution to Practice Problem–George Company

TransactionEffect on Working Capital

Effect on Debt Ratio

1. Received advance from customer N I2. Issued stock for cash I D3. Purchased machinery by paying cash D N4. Declared dividends D I5. Collected on accounts receivable N N6. Paid accounts payable N D7. Converted accounts payable to long-term note payable I N

Practice Problem 3

1. Which of the following is not a current asset?a. accounts receivableb. inventoryc. landd. cash

2. The usual order of presentation in the balance sheet isa. cash, inventory, accounts receivable.b. cash, accounts receivable, inventory.c. inventory, cash, accounts receivable.d. inventory, accounts receivable, cash.

3. Noncurrent assets include all of the following excepta. land.b. sinking-fund investments.c. ownership interest in other entities held for the purpose of exerting control.d. stocks that were issued by other entities, and that management intends to sell in six months.

4. Treasury stock is reported on the balance sheet asa. an asset.b. a liability.c. a deduction from stockholders’ equity.d. an addition to stockholders’ equity.

5. If a loss contingency is determined to be reasonably possible, the proper accounting treatment is toa. disclose the contingency in a footnote.b. accrue the loss for the minimum expected amount.c. accrue the loss for the maximum expected amount.d. ignore the loss contingency.

6. A fire destroyed a part of the warehouse on January 15, 2003. When preparing the financial statements for the year ended December 31, 2002, this is an example of aa. type 1 contingent event.b. type 2 contingent event.c. type 1 subsequent event.d. type 2 subsequent event.

7. Jones Company’s balance sheet as of December 31, 2002 had the following items: cash, $5,000; accounts receivable, $7,000; inventory, $12,000; land, $20,000; buildings (less accumulated depreciation), $36,000; accounts payable, $6,000; bonds payable (due December 31, 2007) $24,000. The working capital of Jones Company as of December 31, 2002 isa. $50,000.

b. $18,000.c. $20,000.d. $6,000.

8. Biggs Company’s current ratio is 2.5. If the company were to pay off some of its accounts payable, a. the current ratio will decrease and working capital will increase.b. the current ratio will stay the same and working capital will decrease.c. the current ratio will increase and working capital will stay the same.d. the current ratio will decrease and working capital will stay the same.

Homework Problem 1Donald Company

The post-closing account balances of Donald Company as of December 31, 2002, follow. Prepare a classified balance sheet and calculate the current ratio, quick ratio, and debt ratio as of that date.

Accounts receivable 20,000Accounts payable 7,000Land 10,000Buildings 30,000Machinery 42,000Bonds payable 28,000Cash 5,000Accumulated depreciation – building 5,000Accumulated depreciation – machinery 12,000Treasury stock 3,000Salaries payable 5,000Goodwill 3,000Patents 2,000Common stock 10,000Inventory 6,000Allowance for doubtful accounts 1,000Retained earnings 53,000

Solution to Homework Problem–Donald Company

ASSETSCash $5,000Accounts receivable $20,000 less allowance for doubtful accounts (1,000) 19,000Inventory 6,000 $30,000

Property, Plant, and EquipmentLand 10,000Buildings 30,000 less accumulated depreciation (5,000) 25,000

Machinery 42,000 less accumulated depreciation (12,000) 30,000 65,000

Intangible assetsPatents 2,000Goodwill 3,000 5,000 TOTAL ASSETS $100,000

LIABILITIESCurrent liabilitiesAccounts payable 7,000Salaries payable 5,000 12,000

Noncurrent liabilitiesBonds payable 28,000TOTAL LIABILITIES 40,000

STOCKHOLDERS’ EQUITYCommon stock 10,000Retained earnings 53,000 less treasury stock (3,000)TOTAL STOCKHOLDERS’ EQUITY 60,000TOTAL LIABILITIES and STOCKHOLDERS’ EQUITY 100,000

Current ratio = Current assets/Current liabilities = $30,000/$12,000 = 2.5Quick ratio = Quick assets/Current liabilities = $24,000/$12,000 = 2.0

(Note: Quick assets include cash and accounts receivable)Debt ratio = Total liabilities/Total assets = $40,000/$100,000 = 0.4

Homework Problem 2Hayward Company

Hayward Company has current assets of $100,000 and current liabilities of $50,000 before any of the following transactions. For each transaction, indicate the effect on working capital and the current ratio. Indicate “I” for increase, “D” for decrease, and “N” for no change.

1. Purchased merchandise inventory for $28,000 on credit.2. Sold merchandise inventory costing $8,000 for $10,000 cash.3. Sold merchandise inventory costing $6,000 for $7,800 on credit.4. Collected $4,000 of accounts receivable.5. Paid $20,000 of accounts payable.6. Bought a machine costing $8,000 by paying $4,000 cash with a note due in two years for the remainder.7. Converted $5,000 of accounts payable to note payable due 18 months from now.8. Declared and paid dividends of $3,000.

Solution to Homework Problem-Hayward Company

TransactionEffect on Working Capital

Effect on Current Ratio

1. Purchased merchandise inventory for $28,000 on credit. N D

2. Sold merchandise inventory costing $8,000 for $10,000 cash. I I3. Sold merchandise inventory costing $6,000 for $7,800 on credit. I I4. Collected on $4,000 of accounts receivable. N N5. Paid $20,000 of accounts payable. N I6. Bought a machine costing $8,000 by paying $4,000 cash, with a note due in two years for the remainder. D D7. Converted $5,000 of accounts payable to note payable due 18 months from now. I I8. Declared and paid dividends of $3,000. D D

Homework Problem 3

1. Which of the following is a current asset?a. buildingb. inventoryc. landd. machinery

2. Unearned subscription revenue usually appears on the balance sheet as aa. current asset.b. noncurrent asset.c. current liability.d. none of the above.

3. Intangible assets include all of the following excepta. goodwill.b. patents.c. trademarks.d. buildings.

4. The Capital Stock account provides information about all of the following except thea. number of shares authorized.b. number of shares issued.c. number of shares outstanding.d. earnings per share.

5. A certain contingency is deemed to be probable. The proper accounting treatment involvesa. ignoring a gain contingency and accruing a loss contingency.b. accruing a gain contingency and ignoring a loss contingency.c. making a footnote disclosure, regardless of gain or loss contingency.d. making an accrual, regardless of gain or loss contingency.

6. A flood destroyed a part of a factory on January 15, 2003. When preparing the financial statements for the year ended December 31, 2002, the accountant musta. make a footnote disclosure.b. record a loss.c. adjust the financial statements.d. take no action.

7. Patel Company’s balance sheet as of December 31, 2002 had the following items: cash, $6,000; accounts receivable, $8,000; inventory, $14,000; land, $21,000; buildings (less accumulated depreciation), $35,000; accounts payable, $7,000; bonds payable (due December 31, 2007) $14,000. The company’s current ratio as of December 31, 2002, isa. 2.

b. 4.c. 6.d. 12.

8. Barton Company’s current ratio is 2.4. If it were to reclassify some of its current liabilities as noncurrent liabilities, thea. current ratio will decrease and working capital will increase.b. current ratio will stay the same and working capital will decrease.c. current ratio will increase and working capital will increase.d. current ratio will decrease and working capital will stay the same.

Homework Problem 4

1. Which of the following is usually not a current liability?a. bonds payableb. accounts payablec. wages payabled. salaries payable

2. The following types of liabilities are recorded at discounted present value:a. current liabilities but not noncurrent liabilities.b. noncurrent liabilities but not current liabilities.c. both current and noncurrent liabilities.d. neither current nor noncurrent liabilities.

3. Property, plant, and equipment include all of the following excepta. land.b. machineryc. vehicles.d. franchises.

4. Double taxation is a feature ofa. partnerships.b. corporations.c. sole proprietorships.d. partnerships and sole proprietorships.

5. For a loss contingency to be accrued, it must bea. reasonably possible.b. reasonably possible and estimable.c. probable and estimable.d. remote and estimable.

6. A lawsuit was filed against Thomas Company on December 10, 2002, was settled on February 10, 2003. Thomas Company finished preparing its financial statements on March 15, 2003. The lawsuit settlement must bea. disclosed in a footnote in the financial statements for the year ended December 31,

2003.b. disclosed in a footnote in the financial statements for the year ended December 31, 2002.c. accrued in the financial statements for the year ended December 31, 2003.

d. accrued in the financial statements for the year ended December 31, 2002.

7. Read Company’s balance sheet as of December 31, 2002 had the following items: cash, $6,000; accounts receivable, $10,000; inventory, $16,000; land, $32,000; buildings (less accumulated depreciation), $64,000; accounts payable, $8,000; bonds payable (due December 31, 2007) $16,000. The quick ratio of Read Company as of December 31, 2002 isa. 2.

b. 4.c. 8.d. 16.

8. The current ratio for Harper Company is 3.0, and the total current liabilities of the company are $15,000. If the company were to purchase $5,000 of inventory on credit, the current ratio after the purchase will bea. 3.0.b. 4.0.c. 2.5.d. 2.0.