banca mondială - date despre românia

TRANSCRIPT

7/27/2019 Banca mondială - Date despre România

http://slidepdf.com/reader/full/banca-mondiala-date-despre-romania 1/37

April 2013

World Bank Group ‐ Romania Partnership

Program Snapshot

7/27/2019 Banca mondială - Date despre România

http://slidepdf.com/reader/full/banca-mondiala-date-despre-romania 2/37

2

RECENT ECONOMIC DEVELOPMENTS

Growth and External Performance

Romania is starting a tentative recovery from theglobal financial crisis, but future growth remains vulnerable to external factors, notably the weather. The Romanian economy contracted by a cumulative 8

percent during 2009 and 2010, as a result of the financialcrisis. The implementation in 2011 of a bold package of macro-stabilization and structural measures, supported by a multilateral program with the International Monetary Fund (IMF), the European Commission (EC), and the World Bank, began to yield results, and Romaniaexperienced a modest economic recovery of 2.2 percent inthat year, led by exports and a good agricultural harvest.However, Romania remained vulnerable to exogenousshocks. Growth was around zero in 2012, as a result of three factors: (i) an extreme winter at the start of the year, which hit consumption and industrial output, (ii)

protracted economic turmoil in the Eurozone, whichresulted in flat exports in 2012, and (iii) a drought, whichhit the agricultural sector. The latter alone shaved anestimated one percentage point from growth during 2012.

Despite poor growth performance, macroeconomicmanagement has been solid. Following depreciationpressures resulting from political turmoil, the exchangerate has rebounded since the December 2012 elections. The increased political stability has also encouraged areturn of nonresident capital. In addition, Romaniansovereign debt will shortly be included in Barclay’s and JPMorgan’s emerging market indexes. This has helped tobring down credit default swap (CDS) spreads on five-yearbonds to under 200 basis points during January 2013.Public debt reached a moderate 38 percent of GDP(complying to Maastricht criteria) at the end of 2012.

Inflation picked up during the latter half of 2012,reaching nearly 6 percent by January 2013 — significantly above the 2.5 ± 1 percent target—partly as aresult of exchange rate depreciation and partly due toincreases in administered gas and electricity tariffs. Thepolicy rate has remained constant since April 2012, but theNational Bank of Romania (NBR) has intervened with the

aim of reducing short-term exchange rate fluctuations. The crisis led to a sharp curtailment of the currentaccount deficit, which narrowed from 11.6 percent of GDP in 2008 to around 4.5 percent in 2012. The fiscalbalance fell from 4.1 percent of GDP in 2011 to 2.5percent in 2012 on the back of tight control of spending, which fell in real terms for the second consecutive year.Despite the lack of growth, unemployment remained low compared to many European countries and actually fellfrom 7.5 percent in December 2011 to 6.5 percent in

December 2012 (using standardized Eurostatmethodology). This is likely to have been helped partly bya more flexible Labor Code introduced in 2011.

Economic activity is expected to pick up only slightlyin 2013 and to remain relatively subdued over themedium term. GDP growth is expected to reach 1.2percent in 2013, with around half of the pick-up comingfrom a rebound in the agricultural sector. Weak externademand from the rest of the European Union (EU)(accounting for 70 percent of Romanian exports) reducedconsumer and business confidence and continued the lowinflows of capital, which will limit growth in other sectors Absorption of EU funds (just 12 percent of the 2007–13available envelope was drawn by the end of 2012) isexpected to continue the pick-up begun during 2012helping to boost growth. An increase in growth to above2.5 percent over the medium term will require increasedinfrastructure and private investment, including from agradual improvement in the absorption of EU Structura

and Cohesion Funds. Private sector investment can beattracted, notably in the energy, manufacturing, and ITsectors, if structural reforms continue to improve theRomanian investment climate.

The economic outlook entails significant downsiderisks, particularly in the short run. A deep or protractedrecession in the Eurozone will undermine Romania’sgrowth prospects, and a financial crisis would have a majornegative impact on its exports, currency, and bankingsectors, leading to significant financing difficulties. Theongoing precautionary programs with the IMF, the EC

and the World Bank (the €1 billion Development PolicyLoan [DPL] deferred drawdown option [DDO] program)partly mitigates some of these risks. The precautionaryprogram with the IMF and the EC will expire in April2013, but the Government is likely to request a successortwo-year program with the IMF.

Fiscal Performance

Romania has embarked on a significant fiscaadjustment since 2009 and the Government wasdetermined to exercise continued expenditurerestraint in 2012 and in the preparation of the 2013

budget. The general government deficit (EuropeanSystem of Accounts [ESA] terms) was brought down from9 percent of GDP in 2009 to 5.2 percent in 2011, andreached its targeted 3 percent of GDP in 2012, ascommitted under the EU Excessive Deficit Procedure(EDP). This was achieved through strict expenditurecontainment, including cuts in public sector wages andpensions, and the adoption of revenue-enhancingmeasures, particularly an increase in the value added tax(VAT) from 19 to 24 percent in 2010. The dynamics of the

7/27/2019 Banca mondială - Date despre România

http://slidepdf.com/reader/full/banca-mondiala-date-despre-romania 3/37

3

structural fiscal balance (cash basis) illustrate the boldnessof the fiscal adjustment package pursued by theGovernment; it declined from 7.5 percent of GDP in 2008to an anticipated 0.9 percent in 2012. The fiscal deficit ona cash basis was 2.5 percent of GDP in 2012, slightly above target due to a downward revision of nominal GDPand the delayed receipt of EU funds after irregularities by the Romanian authorities being discovered. The fiscalconsolidation is planned to continue in 2013 with thebudget targeting a cash deficit of 2.1 percent of GDP (2.4percent in ESA terms), despite cuts in nominal GDP.Under the EU Fiscal Compact, Romania has set amedium-term objective of 0.7 percent of GDP for thestructural fiscal deficit.

Financial Sector

Despite increasing strains, the Romanian bankingsector maintains significant buffers to deal with pressures and mitigate risks. Driven by the weak economic environment, depreciation of the leu, andlimited possibility of the banks to write them off, due tocurrent legislation and banks’ own lack of appetite,nonperforming loans (NPLs) increased to 18 percent by

the end of 2012, from 14 percent at end-2011. However,the capitalization of the banking sector remained strong at14.7 percent at end-June 2012, albeit with differencesbetween banks, reflecting continued shareholder supportand retained earnings. All banks except one have a capitalratio above the regulatory minimum of 10 percent. Greek banks continue to exhibit capital buffers exceeding thesystem average, owing to capital injections from parentbanks. The introduction of International Financial

Reporting Standards (IFRS) provisioning in early 2012 hasgone smoothly, and the maintenance of a prudential filterand proactive bank supervision has ensured that a prudenprovisioning regime remains in place.

The authorities have introduced several regulatoryand legislative changes that aim to safeguard financiastability and strengthen crisis managementarrangements and contingency planning. The NBRadopted measures in 2011 to restrict foreign currencylending to unhedged household borrowers; it has alsocontinued to closely oversee bank practices to avoid ever-greening to ensure that IFRS loan-loss provisioning andcollateral valuations, as well as the assessment of the credirisk of restructured loans, remain prudent and in line withgood international practices. In June 2012, the fiscal code was amended to ensure a neutral tax treatment of bankreceivables sold to Romanian firms in order to enablebanks to improve their balance sheet management. In January 2012, amendments to the bank resolution

legislation were adopted that introduced bridge bank andother resolution powers for dealing with failing banks. TheNBR, Deposit Guarantee Fund (DGF), and Ministry ofPublic Finance continue to coordinate the implementationof operational preparedness plans.

Structural Reform Agenda

The crisis prompted long-needed reforms. Thefinancial difficulties gave rise to a series of reforms, withsupport from international financial institutions (IFIs), inhealth, education, the financial sector, public financiamanagement (such as treasury and debt managementmacro forecasting capacity, strategic prioritization in the

Table 1. Key Economic Indicators Sources: IMF, MoPF, INS, Staff estimates

2010 2011 2012 2013

Annual Annual Est. Proj.

Real growth, % -1.1 2.2 0.2 1.2

Real growth excl. agriculture, % -0.6 1.7 1.3 0.5

Fiscal balance (% GDP) /1 -6.3 -4.1 -2.5 -2.1

Structural fiscal balance (% GDP) /1 -6.4 -4.1 -2.4 -2.0

Real growth of public spending (% change) -1.5 -4.1 -3.8 -1.0

Public sector debt (% of GDP) /1 30.5 34.7 38.1 38.7

EU funds absorption (% allocations) 3.7 5.6 11.5 16.0

Current Account Balance (% GDP) -4.4 -4.5 -3.6 -3.6

Imports of G&S (% GDP) 41.1 45.4 41.1* 41.1

Exports of G&S (% GDP) 35.4 40.0 37.8* 37.8

Unemployment (%, eop) 7.1 7.5 6.5 6.5

Inflation (%, eop) 8.1 3.2 5.0 3.0

*As of October 2012; . 1/ On a cash basis. Methodology currently being revised; 2/ Maastrict criteria using revised GDP, excluding NBR’s

debt.

7/27/2019 Banca mondială - Date despre România

http://slidepdf.com/reader/full/banca-mondiala-date-despre-romania 4/37

4

budget process), public administration, social insurance,and social assistance. Some of these reforms addressshort-term responses to the crisis, while others areanchored in a coherent longer-term strategy. Structuralreform priorities in 2011–12 included public finance,energy, and health.

The Fiscal Compact requires Romania to takemeasures that ensure its public financial managementframework meets the binding standards imposed bythe Treaty on Stability, Coordination and Governancein the Economic Monetary Union. This is not an easy task, and in the coming years, the Government will need tofocus on adopting good practices in revenue andexpenditure management. This will consolidatemacroeconomic stability, allow a better alignment of thebudget formulation and execution procedures with thedevelopment priorities of the country and the publicpolicy framework, and result in a more efficient allocationof public resources. National fiscal planning should adopt

a multiannual perspective, so as to attain the medium-termobjective of balance across the general government, with astructural deficit limit of up to 1 percent of the GDP. Thenumerical fiscal rules assumed under the medium-termfiscal framework for 2012–15 should also promotecompliance with the Treaty reference values for deficit anddebt.

The poor performance of the energy sector(dominated by state-owned enterprises, or SOEs)carries significant risks for Romania’s fiscal stability,energy security, and economic growth. The SOEs’

poor financial performance affects Romania’s fiscalsustainability. The largest SOEs are in energy and gas, where they represent 53 percent of all economic activity;transport and storage (34 percent); and mining andquarrying (27 percent). Despite some moderation during the precrisis period, arrears accumulation remains anendemic phenomenon at the level of the state-owned orstate-controlled enterprises. The state is the sole owner of the transmission grids for gas and electricity, all majorelectricity generators, three out of eight electricity distributors, all gas storage, and the hard coal and lignitemines. Electricity and gas markets are regulated: half of the market is supply-demand driven, while the other half isregulated: some consumers purchase energy at pricesregulated by the Romanian Energy Regulatory Authority (ANRE), and power or gas producers are required tosupply the energy at those regulated prices.

There are risks to fiscal stability due to losses of potential revenue and arrears, risks to energy securityand economic growth caused by interruptions insupply, and risks to fair competition from thedistortion of competition in the downstream markets.

To address these problems, the Government has initiatedmeasures to improve the governance of energy SOEsenhance competition, and attract the private capital neededto boost competitiveness in the sector. The Government’s2012–14 program includes enhanced governance andcontracting practices; appropriate legislative and regulatorymeasures to improve competition to attract privateinvestment and align the energy sector with the EU’senergy acquis ; improved heating services and containmenof household heating and municipal budget costsincreased private sector participation in the financing andmanagement of the energy sector; and updated tax androyalty regulations for the oil and gas sector.

Romania spends less than 5 percent of GDP onhealth care, compared to a European average of 6.5 percent and an EU average of 8.7 percent. Access tohealth care in Romania is skewed towards wealthier groups Almost half of the poor do not seek care when requiredcompared to around 20 percent of those in the top

income quintile. Of the public funds allocated for healthcare, much is wasted on inefficient and unnecessaryservices or treatments. Moreover, the current health caresystem is heavily biased towards inpatient hospital care The lack of an appropriate Health Technology Assessmenfor new drugs and medical devices has produced a healthcare system that is also biased towards high-costtechnology.

Taken as a whole, the reforms aim to contain risingcosts and improve the quality of services delivered The Government’s medium-term reform program in

health promotes cost-effective outpatient and primary careservices instead of costly in-patient services, introducescopayments, rationalizes hospital infrastructure, regulatesthe introduction of new drugs and technologies, andreviews the basic benefit package reimbursed by the publichealth insurance system.

RECENT SECTORAL DEVELOPMENTS

Sustainable Development

(i) Agriculture

Agriculture plays an important role in Romaniabecause of the size of the rural population andbecause it is a significant source of employmentmaking it central to Romania’s European integrationand social cohesion goals. Romania has one of the besresource endowments in Europe and was once widelyconsidered a breadbasket for Europe, but the sectorremains underdeveloped. Despite the highest proportionof rural population (45 percent) in the EU, Romania hathe highest incidence of rural poverty (over 70 percent)

7/27/2019 Banca mondială - Date despre România

http://slidepdf.com/reader/full/banca-mondiala-date-despre-romania 5/37

5

the largest gap in living and social standards between ruraland urban areas, and one of the lowest rates of agriculturalcompetitiveness. Although almost 30 percent of employment is in agriculture (compared to some 2 percentin the EU15 and 3–14 percent in the EU8), Romaniaimports an increasing amount of its food needs.

Average yields are half those in the EU27. Less thanoptimal production factors lead to low average yields inRomanian farming, at only half those in the EU27 formost field crops and livestock. Even at this low productivity level, agriculture’s share in the country’s totalgross value added is 7 percent, compared to 1.7 percent inthe EU27. Agricultural production in Romania is also vulnerable to natural calamities and the country’s currentinability to effectively prevent and contain animal diseases.

Transforming agriculture and ensuring the deliveryof public goods to rural areas are therefore critical forRomania. Despite EU financial support, the considerable

agricultural potential remains insufficiently tapped. Additional national actions are thus vital for Romania’sability to both benefit from EU membership and addresskey sectoral shortcomings.

Removing constraints to competitiveness is a key priority. Important issues include addressing land tenuresecurity and high transaction costs in the land market,creating off-farm employment to absorb surplus labor inagriculture, rethinking pension benefits and social security,addressing deficiencies in administration, improving thequality of services provided to beneficiaries of the EU

Common Agriculture Policy, and enhancing the capacity tomonitor and enforce food safety and quality standards.Improvement of the quality of life in rural space is anoverarching goal that involves the development andmodernization of rural infrastructure.

The Bank is supporting agricultural sector and ruraldevelopment through three ongoing projects: the Modernizing Agricultural Knowledge and Information Systems (MAKIS) Project to improve the competitiveness of farmersand agro-processors through enhanced advisory servicesto modernize agricultural research and improve foodsafety, in line with EU requirements; and the Complementing EU Support for Agricultural Restructuring (CESAR) Project tosupport the implementation of land tenure and titling reform, thus enabling better absorption of EU funds. TheIrrigation Rehabilitation and Reform (IRR) Project to support anincrease in agricultural productivity and sector reformclosed at end-FY12.

To further develop the sector, immediate actionshould include: (i) developing a sector strategy focusedon improving the access of local producers to domestic

and external markets; (ii) initiating the programmingprocess for the National Rural Development Program for2014–20; (iii) improving the Ministry of Agriculture andRural Development (MARD) by streamlining its decisionmaking and honing its targeting of the national programsand (iv) continuing to scale up the government’s programof property title registration of land assets in rural areas toimprove the security of property rights and thefunctioning of rural land markets.

(ii) Environment

Romania is below the EU average and has yet to takeadvantage of the €4.5 million EU Structural Funds forEnvironmental Protection and Climate Change. Inlight of its commitments to achieve the EU 20/20/20energy-climate change package and the EU’s Low CarbonRoadmap to build a competitive low-carbon Europe by2050, Romania needs to: (i) thoroughly analyze theopportunities, options, and related costs over the medium

and long term to meet these commitments; (ii) prepare acomprehensive program for funding climate change andgreen growth under the next programming period for EUfinancing (2014–20); (iii) improve climate changemitigation by enhancing inter-ministerial cooperation; (iv)adapt to the economic risks of climate change bypreparing and implementing an adaptation strategy; (v)streamline the environmental permitting process; and (vi)invest in green growth with a view to developing acomparative advantage in this nascent industry. Another ofRomania’s key commitments is to comply with EU waterdirectives, which will also be a major focus of the next EUCohesion Funds programming period.

The Bank has one ongoing project, Integrated NutrienPollution Control , which supports the environmental sectorin Romania through investments in nutrient-vulnerablezones. This will assist Romania in meeting the EU NitrateDirective by financing its animal waste managemeninfrastructure, and also provide institutional support to theMinistry of Environment.

At the request of the Government, the Bank in June2011 completed a Functional Review of theenvironment, water, and forestry sectors. This resulted

in a significant number of recommendations, spanningstrategy formulation, priority setting and human resourcemanagement, regulatory effectiveness, sustainable forestmanagement, and absorption of EU Structural Funds.

(iii) Infrastructure

A considerable share of the Bank’s assistance program was previously directed toward therehabilitation of Romania’s infrastructure. While mosBank financing went to investment in and equipment for

7/27/2019 Banca mondială - Date despre România

http://slidepdf.com/reader/full/banca-mondiala-date-despre-romania 6/37

6

rehabilitation and expansion, loans typically also included atechnical assistance (TA) component for improving thepolicy-making capacity of the ministry in charge and fordeveloping plans to improve the efficiency of the sectors.Often the Bank’s rationale for involvement was to facilitatesector restructuring to promote competition and privatesector investment by involvement in the rehabilitation of the railway, petroleum, telecommunications, and powersupply sectors, as well as the electricity market.

Human Development

(i) Health

Romania has made notable improvements in thehealth of its population, but challenges remain andadditional efforts are required. Many basic healthindicators have shown improvements. Reductions in infantand maternal mortality have been remarkable: the infantmortality rate fell from 43.5 per 1,000 infants in 1970 to

21.7 in 1995 and 11.6 in 2008. Correspondingly, there wereimprovements in life expectancy at birth during the sameperiod (from 68.5 years in 1970 to 73.4 in 2008). That said,notable challenges remain. For example, life expectancy atbirth is five years below EU averages, and maternal andinfant mortality is among the EU’s highest, with highmortality rates more concentrated in low- income ruralareas.

Romania has historically committed a relatively low share of national wealth to health care. The publicfraction of health care spending has increased from 2.9 to3.7 percent of GDP, but still remains well below other EUcountries. Coverage has also increased, but the quality andresults of the health care system are still far behind EUstandards. The generous basic package of health servicescan no longer be covered by the health insurance system ina sustainable manner. Moreover, the sector is plagued withproblems, including a lack of investment, leading todeteriorating health facilities, a disgruntled workforce, andpublic dissatisfaction with the health system.

Romania’s health infrastructure still suffers fromfragmentation, inefficiency, and poor regulation. Thecurrent facilities providers in primary health care are

characterized by small private businesses, abundant low-,mid-, and high-level hospitals, and few facilities forspecialized outpatient services/secondary ambulatory care(diagnosis and treatment). Bank projects include Health Services Rehabilitation , Programmatic Adjustment Loans (APL 1and 2), and Health Sector Reform projects. Also, severalelements of health sector reforms were implementedunder the framework of budget-support loans such as the APLs and DPL series .

New reforms should build on those alreadycompleted. These include hospital rationalizationstreamlined provider payment mechanisms, and therecently approved copayment law. New efforts can beeffective by: (i) reducing arrears, eliminating waste by usinggeneric drugs, and bringing additional resources into thesystem through reviewing the legal framework for hospitaaccreditation in connection with the quality of providedservices and through the claw-back tax; (ii) reviewing thebenefits package; (iii) implementing transparenmechanisms for new technology and new drugs ( HealthTechnology Assessment ); and (iv) developing a legal basis forintroducing private health insurance.

The Bank will further support the health sector. TheBank is preparing a future operation for the health sectorthat aims to enhance the service delivery systemstrengthen financing and payment methods, and improvegovernance in the health system.

(ii) Education

One of Romania’s key priorities continues to beupgrading the skills of its population to meet Europe2020 targets. The economic crisis has exposed the weaknesses of the economy, and in particular, the lack ofcompetitiveness due partly to the level of skills. A highlyskilled workforce depends on an education system that canproduce graduates with the right skills and quality. Thechallenge is to bring the level of achievement ofRomanian children in key subjects to the levels currentlyfound in most European countries. To this end, Romanianeeds to better align the content of education in schools

with the requirements of a knowledge-based economyimprove the quality of the teaching and learning processand increase the system’s efficiency.

The system has been strengthened in a number of ways over past decades, although there is a significantunfinished agenda in the provision of educationComprehensive reforms were initiated in the 1990s with World Bank and other donor support.

In 2009–10, Development Policy Loans (DPL) 1 and 2 promoted key reforms on per capita financing to

increase the system’s efficiency and effectiveness. Animportant contribution to advance the country’s socialinclusion agenda is currently provided under the EarlyChildhood Education component of the Social Inclusion Project These recent efforts include the development of newcurriculum and application guidelines for inclusive earlychildhood education, associated teacher training, and theongoing rehabilitation and construction of kindergartensin communities with a significant Roma populationSubstantial Bank assistance is also ongoing through the

7/27/2019 Banca mondială - Date despre România

http://slidepdf.com/reader/full/banca-mondiala-date-despre-romania 7/37

7

ICT in Schools component of the Knowledge Economy Project . This is aimed at improving primary and lower secondary education through the integration of information andcommunications technology (ICT) in teaching-learning practices at the classroom level, thereby improving students’ skills and knowledge.

At the tertiary level, TA was provided to introduce astudent loan scheme in Romania, which is expected tobe implemented in the future. The Functional Review on the Pre-university Education Sector and the Functional Review of the Higher Education Sector , undertaken in 2010 and 2011,supported the education program by providing detailedrecommendations for the improvement of the sector’sperformance, which were reflected in specific action plansfrom the Ministry of Education. Selected activities areexpected to be further implemented with the help of the World Bank.

The Government has moved forcefully in advancing

the reform agenda. A new National Education Law hasbeen in force since early 2011 promoting changes in virtually all important education areas: new educationcycles and a focus on early childhood education; a shift tocompetence-based curricula; new systems for professionaldevelopment; evaluation and assessment efforts;preuniversity financing in the decentralization context;classification of universities; a new approach to university management; a focus on lifelong learning; and so on. Inorder to meet the ambitious targets of the Europe 2020strategy, one of Romania’s key priorities will continue tobe upgrading the population’s skills. To this end, the

education sector should focus on: (i) tackling implementation challenges related to the comprehensive National Education Law , with particular attention to aligning education services at the preuniversity and tertiary levels tolabor market requirements; (ii) increasing the capacity of the Ministry of Education to focus on its core business,and enhancing operational efficiency and accountability within the system; and (iii) using the schools network andteaching force more efficiently.

(iii) Poverty and Social Protection

Poverty declined in 2009 due to a generous increase in

social protection and pension spending. Romania’spoverty rate declined dramatically, from 36 percent in 2000to 5.7 percent in 2008. In 2009, poverty declined further to4.4 percent, due to increased social protection andinsurance spending. However, despite large strides, thepoverty rate in Romania is still among the highest in theEU.

In 2010, social issues were very present on the publicagenda for crisis, postcrisis, and other unrelated

reasons. These include (i) persistently high unemploymenlevels despite the decline from over 8.3 percent in early2010 to around 7 percent currently; (ii) the unfavorableclimatic conditions that affected rural populations; (iii) theincrease in inflation, which reduced real incomes acrossthe board; (iv) the massive cuts in the compensation ofpublic sector employees, who lost not only 25 percent inbasic salaries, but also numerous other benefits; and (v) thecuts in untargeted social transfers.

The impact of the cuts in untargeted social transfersand public sector wages is mitigated by severafactors. First, the incidence of poverty among publicservants is very low, as there is a minimum wage floor of600 lei per month. Second, the social assistance programsthat have been reduced are those with a low targetingperformance affecting mostly middle- and upper-incomehouseholds. Key measures have included reducing thechild care allowance by 15 percent, revising the eligibilityrules for family allowances, and removing the package

( trusou ) and allowance for newborn babies. However, thebudget of the income-tested program has been protected.

Before 2010, the Bank’s overall objective in socia protection and poverty alleviation focused onstrengthening the capacity of labor offices to provideemployment services; strengthening the Ministry of Laborand Social Protection to monitor and evaluate employmenand social protection programs; retraining the labor forcereforming the pension system; improving the targeting ofsocial assistance; and promoting community-drivendevelopment.

Significant progress is visible in social protectionincluding through support from the Bank-financed Employment and Social Protection and Social Sector Developmenprojects. A National Agency for Employment was createdin 1998, comprising a network of offices with countrywidereach, and is operating effectively. Progress was also madetoward pension reform that further led to the introductionof private pension funds.

The public pension system has improvedconsiderably. A new pension law was adopted in 2001 which promoted a gradual increase in the retirement ageand introduced a new point-value benefit formula basedon contributions. As a result, the burden of the publicpension system on public finances was reduced (at leasuntil 2007, when the process started to reverse). Beginningin January 2011, the public pension system was reformedagain, in order to improve its medium- and long-termfinancial sustainability.

At the same time, the Romania Antipoverty and SociaInclusion Commission has improved the ability to

7/27/2019 Banca mondială - Date despre România

http://slidepdf.com/reader/full/banca-mondiala-date-despre-romania 8/37

8

evaluate poverty status. The Child Welfare project (1998)actively promoted community-based approaches assustainable and cost-effective alternatives toinstitutionalized child welfare. The most tangible result wasthe large reduction in the number of children in state-runinstitutions.

Over the short term, the key challenge is to rein insocial protection spending by focusing on needs-based social assistance programs. Over the mediumterm, a key objective is to improve labor marketparticipation and earnings while reducing dependence onsocial transfers. Although the recently adopted Social Assistance Framework Law creates the foundation for astreamlined, less costly social assistance system thatstimulates work and human capital accumulation, furtherresults would require that secondary legislation andregulations be developed based on careful analyses; servicedelivery systems be strengthened; activation policiesdeveloped and implemented; and error and fraud reduced.

The Bank is currently working with the Ministry of Labor, Family and Social Protection to support socialassistance reforms in Romania. The Social Assistance System Modernization Project provides the vehicle for WorldBank support to the Government’s new social assistancelaw. The project rewards operational results specified in aseries of 20 disbursement-linked indicators (as opposed tofinancing project inputs), and covers a wide range of reforms to improve the overall performance of Romania’ssocial assistance system. There are four key areas of reform: (i) strengthening performance management to

ensure that monitoring reports are produced frequently and used by the ministry to inform decision making; (ii)improving equity to ensure that the share of socialassistance funds going to the poorest quintile is increased;(iii) enhancing administrative efficiency to reduce theadministrative and client participation costs of means-tested programs; and (iv) reducing error and fraud toreduce leakage from the system and increase the public’strust.

The Bank carried out a Functional Review of theMinistry of Labor, Family and Social Protection toprovide advice regarding the administrative functioning of the ministry, including in such areas as: structure,personnel, budgeting, and organization.

Public Sector Reform

(i) Reform of Public Administration

Functional Reviews of public administration inRomania were completed in June 2011. The FunctionalReviews (FRs) were operational, and managerial

assessments of 12 ministries, agencies, and other publicbodies were conducted by the Bank in two stages startingin March 2010. The reviews were agreed to in amemorandum of understanding (MoU) signed in June2009 between the Government of Romania and the ECand were financed out of EU Structural Funds. The Bank was requested to support the modernization of publicadministration. The aim of the FRs was to provide thebasis for a series of action plans, in light of theGovernment’s intention to use the reports in developingits medium-term reform agenda. The process will result inthe strengthened effectiveness and efficiency of publicadministration.

(ii) Governance/Institutional Development

Institutional development has gradually become acentral element of the Bank’s assistance strategy. Likeother countries in Eastern Europe after the fall ofcommunism, Romania lacked the basic institutions needed

to support the transition to a market economy: anappropriate legal and regulatory framework, a separationof regulatory and commercial interests, and a financiasystem that could operate on a commercial basis toenforce a hard budget constraint on borrowers. Unlikesome of its neighbors, Romania during its communisperiod had hardly experimented with even limited policy orinstitutional reforms to separate commercial andregulatory functions or to promote private sector activity.

Despite the lack of basic institutions 20 years agoRomania had made considerable progress in developinginstitutions compatible with a market economy since that

time. However, the country continued to lag behind otherCentral and Eastern European countries in policy reformand institutional development, until the prospect of EUmembership became a driving force for reform andmodernization.

The challenges regarding EU funds absorptionrequire the further strengthening of capacityRomania’s performance in EU Structural Funds Absorption is the lowest among the 10 new EU memberstates, both in terms of contracted and disbursed grants The absorption rate of Structural Funds by the end of

January 2013 was 14.92 percent of the total fundsavailable. Several strategic measures were implemented toproduce an increase in the absorption rate, one of which was the establishment of the former Ministry of European Affairs (now Ministry of European Funds). The mosrecent audits and evaluations have revealed a series ofinstitutional and procedural bottlenecks that translate intoa critical need to strengthen the country’s capacity toincrease EU funds absorption. To address the problemsthe Government has requested assistance from IFIs, of

7/27/2019 Banca mondială - Date despre România

http://slidepdf.com/reader/full/banca-mondiala-date-despre-romania 9/37

9

which the Bank, given its global expertise, has provided thelargest share of support.

Private Sector Development

Positioning Romania to become more competitive ina global market requires a renewed effort to attract

investment and enhance productivity throughinnovation.

Competition: priority actions should aim to reducethe dominant role of the state in the economy (e.g.,transport, energy, communications) and consolidate thecapacity of the Competition Council to enforcecompetition policy.

Business environment: Romania lags behind theEU—and globally—in terms of the number of taxpayments to which small and medium enterprises (SMEs)are subject and the number of procedures and daysinvolved to register property. Globally, the functionsdealing with the investment climate should be consolidated within the Ministry of Economy, Commerce and BusinessEnvironment, which, in turn, should come under greatercentral government coordination, eventually positioned inGovernment’s General Secretariat.

Research, development, and innovation: Apreeminent task is to strengthen the governance of theresearch, development, and innovation system. The firststep could be activating the National Council for Science, Technology and Innovation Policy at the prime minister’slevel, thus ensuring high-level government oversight andenforcement of accountability for performance.

WORLD BANK GROUP PROGRAM

Romania joined the International Bank forReconstruction and Development (IBRD) in 1972, theInternational Finance Corporation (IFC) in 1991, andthe Multilateral Investment Guarantee Agency(MIGA) in 1992. The World Bank has been active inRomania for almost 40 years. Lending was discontinued inthe early 1980s and resumed in 1991. Up through 2012,IBRD has committed US$8.954 billion through 60projects. Bank lending after 1991 was extended in four

main stages: (i) support to the transition of Romania’scommand economy to a market economy, FY91–94; (ii)support to reforms in energy, education, infrastructure,and the land market, FY94–04, and to poverty reduction,reform of the state, and environmental protection, FY97– 04; (iii) support for institution building, governancereform, and EU accession, FY05–10; and (iv) support tosystemic reforms and EU convergence (public finances,public administration, financial sector, judiciary, education,health, social assistance, social security, mobilization of EU

funds) and alleviation of the economic and financial crisisFY11–13. The lending program was complemented byUS$41 million in grant financing.

A change in Government priorities has reshaped theuse of Bank instruments during the last three fisca years. Through FY05–08, policy-based lendingrepresented 11 percent in new Bank approvals, andinvestment operations the remaining 89 percent. ThroughFY10–13, policy-based lending represented 79 percent ofthe new approvals, including a large DDO DPLrepresenting a fiscal buffer to the Government equivalento four months of budget financing. The remaining 21percent represent a results-based operation to supportGovernment reforms in the social assistance sector. Animportant new development of Bank assistance is theincreased emphasis on knowledge sharing via an evolvingpackage of fee-based TA programs that support EUconvergence reforms in public administration.

The ongoing FY13 Bank Portfolio consists of 10lending projects and seven pieces of analytical andadvisory work. The share of investment lending projectsin the portfolio is declining sharply and the Bank programof analytical and advisory (AAA) work is growing. As ofSeptember 2012, the net undisbursed commitment of theactive portfolio was US$2.129 billion, of whichundisbursed specific investment loans (SILs) total US$298million. The portfolio also includes one cofinancingGlobal Environment Facility for nutrients pollutioncontrol, one Prototype Carbon Funds, one Japanese granfor policy making for people with disabilities, and one

Institutional Development Fund (IDF) grant for themonitoring and evaluation (M&E) of policy making. TheBank analytical work program includes a CountryEconomic Memorandum (CEM) shared as a sequence ofthematic Policy Notes on long-run fiscal sustainabilityincreasing the competitiveness of the businesenvironment and reforming the labor markets and theinfrastructure sector for competitive growth; themodernization of public administration (judicial systempublic investment framework, competition); and a CitizensReport Card on social accountability.

The Bank’s support to Romania is focused on threeEU-related cross-sectoral themes.

Theme 1: Policy reforms to reap the benefits of EUmembership and meet the objectives of the Europe2020 strategy.

Supporting ongoing structural reforms and new policy actions in line with the National ReformProgramme (NRP) will be critical for Romania toachieve greater convergence with EU member states

7/27/2019 Banca mondială - Date despre România

http://slidepdf.com/reader/full/banca-mondiala-date-despre-romania 10/37

10

Reforms in health, education, the financial sector, andbudget processes were supported in 2011 via developmentpolicy lending. The 2012 Government Program reconfirmsthat policy reforms in social assistance, health, taxadministration, energy, transport, and SOEs mustcontinue, and these are likely areas for a new budget-support operation that is under preparation. Issues onmacroeconomic stability and building blocks forsustainable growth may be considered. Also, inclusion andparticipation require attention, especially on the significantchallenges to providing opportunities for Roma whileovercoming prejudice and stigma. The set of Policy Notes on Growth and Competitiveness ( CEM ) provides a framework toorient policy dialogue concerning challenges to EUconvergence, and to propel Romania’s growth andcompetitiveness.

Theme 2: Modernization of public institutions toenhance resource allocation and the absorption of EU funds.

As mentioned above, over the past one and one-half years, the Bank has carried out FRs of 12 publicinstitutions in Romania. The reviews are providing operational recommendations on strategic management,organizational structure, sector governance, budgeting, andhuman resources management to help guide structuralreforms. Phase 1 FRs (presented to the Government inOctober 2010) covered Transport, Preuniversity Education, Agriculture and Rural Development, PublicFinance, the Center of Government, and the CompetitionCouncil. Phase 2 FRs (presented to the Government in

March 2011) analyzed Environment and Forestry, Energy and Economy, Health, Labor and Social Protection,Regional Development and Tourism, Higher Education,and Research and Innovation. In December 2010, theGovernment approved the action plans derived from therecommendations of the first phase, part of which theBank may support under the EU-financed Modernization of Romanian Public Administration Program (see below). TheGovernment has also approved the action plans derivedfrom the second phase of the FRs’ recommendations andsubmitted them to the EC.

The Bank engaged with the Government instrengthening administrative capacity through theModernization of Public Administration (MAP),including the promotion of better policy coordination andM&E activities. So far, the Bank has been asked to providetechnical support to the Government to implement itsaction plans derived from the Phase 1 FRs’recommendations, currently 16 projects under a MAPpackage that has provisionally been agreed upon. TheBank has also received a request for similar assistance inthe justice sector (this TA has been signed and

implementation has begun), procurement, and EU fundsabsorption as part of the MAP. The MAP packagesupports several interventions, both on policy reforms andinstitutional capacity building. Government action plansfor the second phase have been approved and the Bank isready to support their implementation upon requestHowever, the key current issue is to finalize the signing ofthe MAP activities in order to start implementation.

The Bank has been asked to provide TA forfacilitating the absorption of EU funds. TheGovernment aimed to achieve a 20 percent EU fundsabsorption rate in 2012, which was an ambitious agenda The Plan of Priority Measures for strengthening thecapacity to absorb structural and cohesion funds couldsignificantly reduce barriers to absorption. One of its keycomponents is to identify the 100 top project prioritiesand concentrate counterpart funding and administrativecapacity on these projects. The Government, through itsMinistry of European Affairs and in agreement with the

EC, requested Bank support (on a fee basis with EUfinancing) to implement a series of actions, including ananalysis of policy impediments constraining EU funds. Onthis matter, an MoU between the Government and theBank was signed on January 26, 2012, which coverspriority areas of intervention.

Efforts have also been made to strengthen the centerof government to prioritize, monitor, and proactivelymanage the reform process. A successful reformprogram and medium-term strategy require the center ofgovernment to be strengthened in order to fulfill core

functions: the prioritization and coordination of reforminitiatives that are fully incorporated into the NRP and theGovernment Program, and the monitoring, evaluation, andreporting of their results and impact.

Theme 3: Complement to EU funding.

The availability of Structural Funds makes Bankfinancing a minor instrument for Romania. Howeverthe Bank can complement EU support by financingactivities that are not covered by Structural Funds oralternative instruments. For example, development policylending and results-based operations can supporimproved outcomes and provide additional financing tothe current budget. Subnational activities, access tofinancial markets via guarantees, and areas of nationaresponsibility (i.e., education, health, justice) for whichStructural Funds are not typically allocated could beexplored.

The IFC is investing in Romania on a selective basis The IFC has withdrawn from sectors and business lines where the private sector is ready to take over; however, the

7/27/2019 Banca mondială - Date despre România

http://slidepdf.com/reader/full/banca-mondiala-date-despre-romania 11/37

11

IFC will assist local companies to become competitive inthe domestic market and expand to other countries in theregion, and promote South-South investments. The IFC will continue to support projects of high developmentimpact, such as in infrastructure, frontier regions, andclimate change-related projects.

Additional lending operations were envisaged for thefollowing two years, mainly focusing on budget supportoperations (DPL) and key sectors such as taxadministration and health (see table below). This potentialnew lending is indicative, and actual delivery will dependon the Government’s request, Bank resources, Romania’sperformance, and global economic developments. TheGovernment expressed interest in a new budget supportoperation (DPL) in 2012, with a deferred drawdownoption. This would focus on key reform areas being supported by IFIs, such as tax administration, health,energy, SOEs, transport, corporate governance, and thefinancial sector.

IBRD Lending (US$ M estimates)

Project Commitment

FY2011 ( approved )

DPL2 (disbursed) 300 (US$426)

Social Assist System Mod Project 500 (US$710)

TOTAL €800 (US$1,136)

Project Commitment

FY2012

DPL 3 (disbursed) €400 (US$560)

DPL DDO €1000 (US$1,333)

TOTAL €1400 (US$1,893)

Project Commitment

FY2013 (tentative)

Tax Admin €76 (US$100)

Health €250 (US$344)

TOTAL €326 (US$444)

International Finance Corporation

Since the start of operations in Romania in 1990, IFChas invested a net total of US$1.58 billion in 72 projects, supporting roughly US$3.7 billion ininvestment. IFC’s Committed Portfolio in Romaniastands at US$611 million (US$600 million outstanding). Atpresent, Romania is IFC’s fifth largest country exposure inthe Central and Eastern Europe region after Russia, Turkey Ukraine, and Serbia, accounting for 1.6 percent of

its outstanding global portfolio. Portfolio composition is87 percent debt and loan type quasi-equity, 6 percentequity and quasi-equity, and 7 percent guarantees. There iscurrently one NPL out of a total of 33 projects with 19sponsors, equivalent to about 0.5 percent of outstandingdebt. IFC has played an active crisis response role inRomania. From FY09 to FY12, IFC investedapproximately US$640 million of its own funds andmobilized an additional US$242 million in 21 projects in various sectors. Particular support was provided to thefinancial, renewable energy, and health sectors.

FY12 was a record year for IFC in Romania, withcommitments of US$221.5 million for its own accounin eight projects, and mobilization of US$93 millionCommitments included: (i)trade finance lines withBancpost, Garanti Bank, and Banca Romaneasca, and aUS$32.5 million senior loan to Garanti Bank to provideon-lending to the SME market, with 50 percent of theloan earmarked for women-owned enterprises; (ii) a US$75

million A&B loan package for Cernavoda & Pestera windpower plants and US$16 million equity in TTS, a rivertransport company; (iii) a US$57 million B loan to supportMedlife, a leading private sector provider of health careservices and long-term client of IFC; (iv) a US$67 million A loan to Lidl, a discount grocery chain with stronglinkages to Romanian suppliers; and (v) a €12.5 million Aloan to Agricover Credit IFN, a non-bank financiainstitution, to finance the investment and working capitaneeds of farmers.

FY13 commitments to date total US$51 million in four

projects. US$40 million in three trade finance lines withGaranti Bank, Bancpost, and Banca Romaneasca, and aUS$10.4 million loan (local currency equivalent) to PatriaCredit, the largest microfinance institution in RomaniaProceeds from the loan will be used to finance theexpansion of lending to micro and small entrepreneurs.

IFC is targeting commitments between US$100–200million in FY13. While external vulnerabilities remainelevated, IFC will continue to play a countercyclical rolethrough selective private sector investments. In the realsector, this includes supporting projects that create jobsincrease investment in underserved frontier regionscontribute to the growth and competitiveness of locafirms in sectors such as agribusiness and IT, improveresource efficiency, and increase private sectorparticipation in developing infrastructure and municipautilities. It is anticipated that IFC will invest increasinglyselectively as Romania’s recovery progresses and externa vulnerabilities recede. IFC has also implemented 25 Advisory Services projects in Romania since 1990 in a variety of sectors. IFC currently has no active advisoryprograms in Romania, but is developing a possible public-

7/27/2019 Banca mondială - Date despre România

http://slidepdf.com/reader/full/banca-mondiala-date-despre-romania 12/37

12

private partnership (PPP) advisory project in the healthcare sector.

IFC will continue to play a short-term counter-cyclical role, primarily in the financial sector, while pursuing longer term strategic priorities as describedbelow. There are two predominant short-term strategicpriorities. First, Crisis Response and Recovery. Romanianfinancial institutions and businesses continue to struggle with the fallout from the 2008 crisis, and are faced withnew threats stemming from Western Europe’s debt crisisand a prolonged global economic slowdown. In thiscontext, IFC will continue to support existing banking sector clients as necessary, including through (i) provisionof short-term finance, such as trade finance, to addressimmediate liquidity concerns, (ii) mezzanine and equity investments to strengthen bank capitalization, and (iii)micro, small, and medium enterprise (MSME) finance tosustain funding to the most vulnerable businesses. If thereis demand, IFC may also explore opportunities to invest in

distressed asset platforms to assist banks with NPLresolution. Second, IFC is working with other IFIs on asecond Vienna Initiative which, in the case of market needin Romania and other countries of Central and SouthEastern Europe, would provide additional liquidity forsubsidiaries of Western European banks, and would allow IFIs to play a role in any eventual sectoral consolidation.

Long-Term Strategic Priorities. The overarching long-term objective of the FY09–13 World Bank GroupCountry Partnership Strategy (CPS) for Romania is tosupport Romania’s convergence with the EU through

robust, sustainable, and equitable growth and enhancedcompetitiveness. IFC has a role to play in supporting growth and enhancing economic competitiveness throughselective financing of private sector projects, with anemphasis on helping the country to absorb EU funds inpriority areas like agriculture, health, and infrastructure,plus ongoing financial sector support.

In agriculture, IFC will seek opportunities to work with financial intermediaries to provide financing tofarmers and SMEs in the agriculture sector, which hasbeen largely neglected by commercial banks. Moregenerally, IFC will help develop the country’s competitiveadvantages in the sector through selective investments inprimary production, food and beverage processing, andretail, such as the 2010 investment in the Lidl discountgrocery chain.

In health, in addition to advisory, IFC has made a numberof investments in the private health sector, including three with MedLife, a leading player in the Romanian market.Most recently, IFC mobilized a US$57 million B loan toMedLife to support expansion of its network of hospitals

and clinics into underserved regions. Going forward, IFC will invest selectively, focusing on opportunities to supporsimilar projects outside of the capital. As the markedevelops, opportunities may arise for IFC to invest inhealth insurance.

On infrastructure, IFC is focused on addressingbottlenecks to growth and improving access to marketsgoods, and services through infrastructure investmentsparticularly in the energy sector and in transport andlogistics. In FY11 and FY12, IFC provided over US$135million (including US$36 million in mobilization) todevelop wind power in Romania, and it is seekingadditional investment opportunities in renewable energy toreduce carbon emissions and make progress towardsrenewable energy targets under the EC framework. IFC isalso seeking to invest in subnational infrastructureincluding through PPPs, having supported Romania’s onlysuccessful PPPs to date in the water and health sectors The IBRD has signed an agreement with the Romanian

government to increase EU funds absorption, includingthrough PPPs in the transport sector, an area where IFChas significant global experience and could potentially playa role.

On financial markets, in the banking sector, which islargely dominated by foreign banks (about 90 percent ofbanking assets), IFC’s longer term strategy is to work withlocal banks to strengthen their capacity to provide loans tounderserved sectors such as MSMEs and agribusiness andto promote products such as local currency and renewableand energy-efficiency finance. In FY12, IFC made its first

investment to support lending to women-owned SMEs inRomania and will seek additional opportunities of thistype. IFC is also looking at potential investments in theprivate health insurance and pension industries.

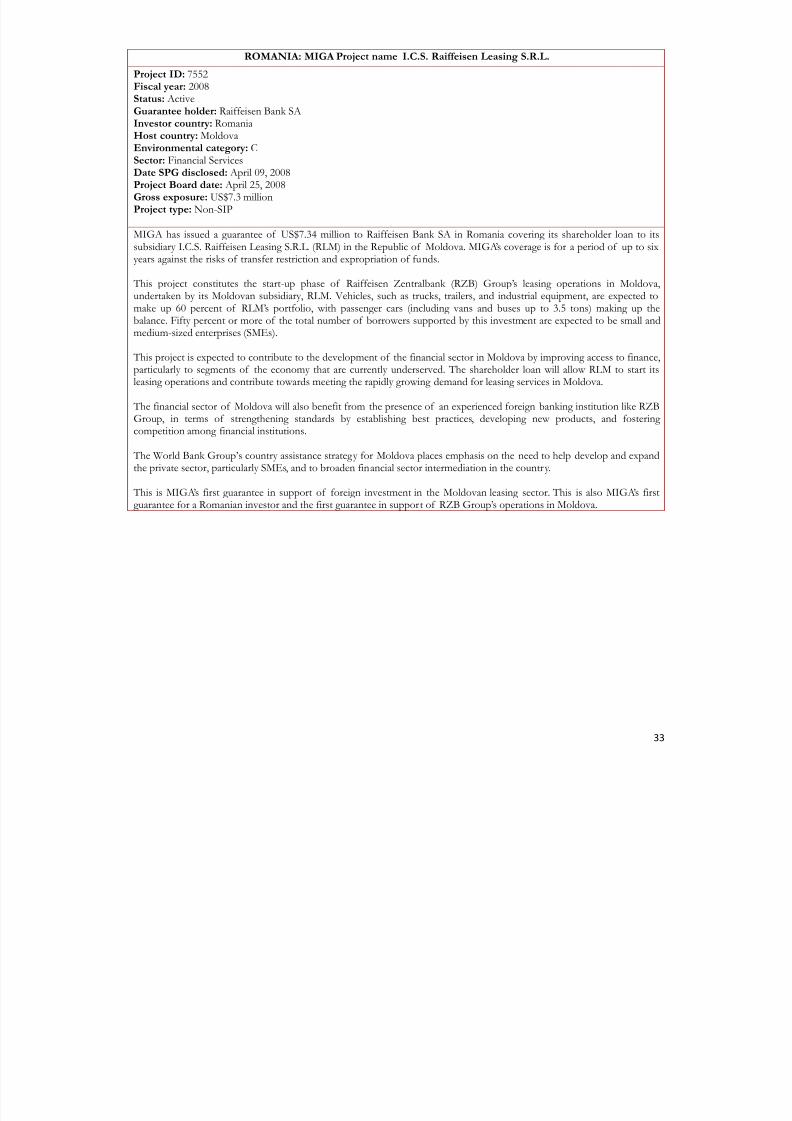

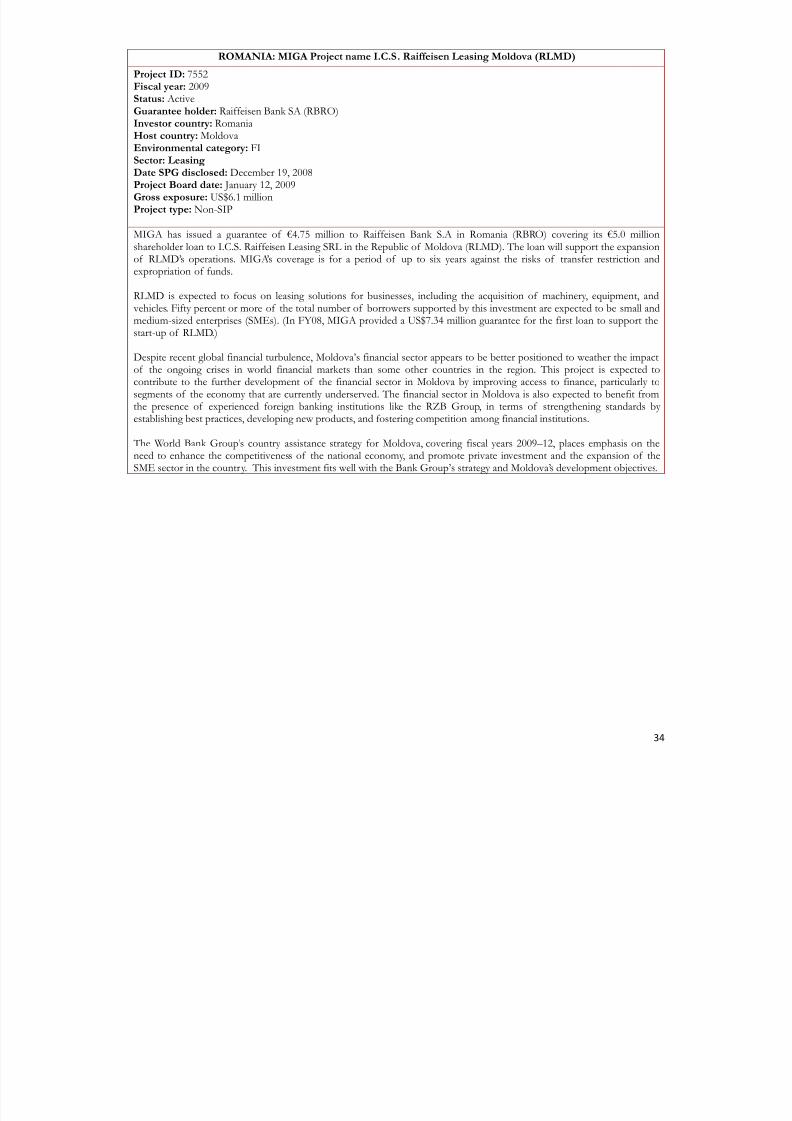

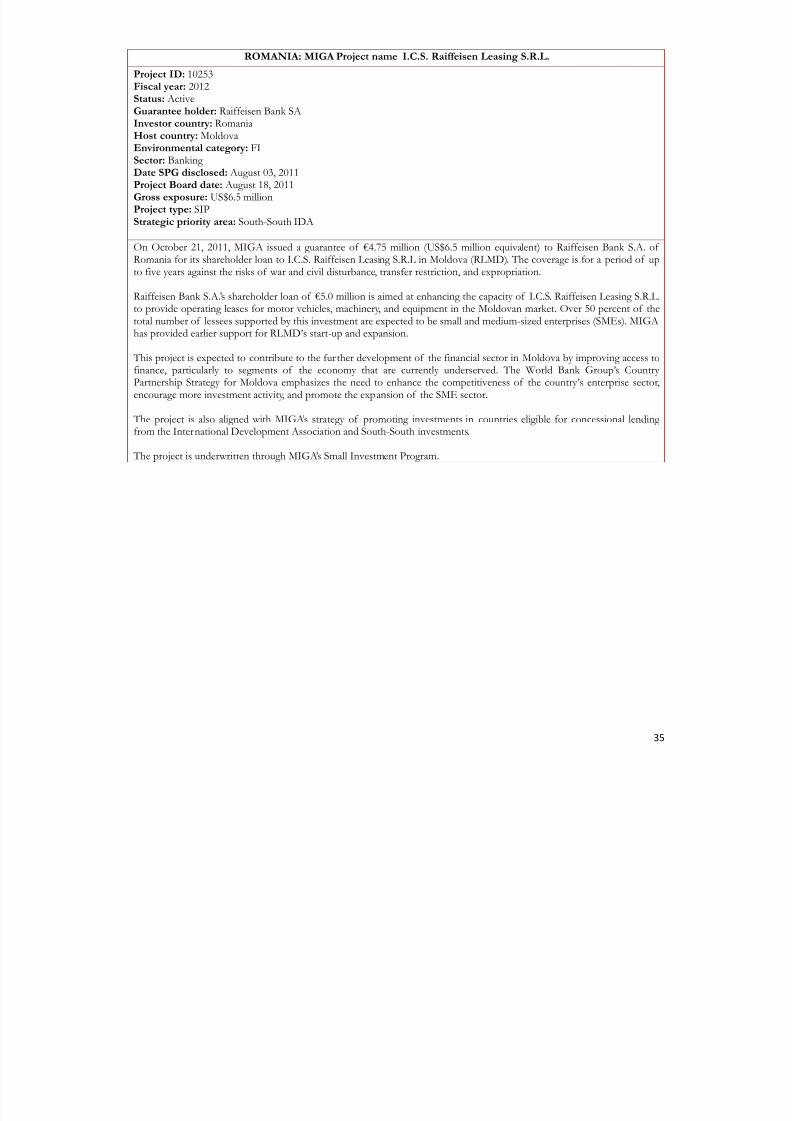

Multilateral Investment Guarantee Agency

MIGA has guaranteed 13 projects in Romania, includingRaiffeisen Zentralbank, Austria’s equity investment inBanca Agricola. It also guaranteed the loansaccommodated by Volksbanken Austria to modernizeColţ ea Clinical Hospital and those provided by Raiffeisen

Bank for enlarging loan operations for SMEs. MIGA’soutstanding guarantee portfolio in Romania consists ofthree contracts in the financial sector. At the end of FY10the agency’s gross exposure in Romania was about US$102million (equivalent to 1.4 percent of MIGA’s grossexposure), while the exposure net of reinsuranceamounted to roughly US$55 million (also equivalent to 1.4percent of MIGA’s net exposure). As an investor countryRomania’s gross exposure is US$9.6 million, representingone project in Moldova’s financial and leasing sector.

7/27/2019 Banca mondială - Date despre România

http://slidepdf.com/reader/full/banca-mondiala-date-despre-romania 13/37

12

ROMANIA: DEFFERED DRAWDOWN OPTION DEVELOPMENT POLICY LOAN (DDO DPL)

Approved: December 6, 2012Effective: January 11, 2013Closing: December 31, 2015 Financing in M EUR:

Financier Financing

IBRD Loan $mOr € 1 B equivalent 1,333

World Bank Disbursements, M US Dollars *: T tal Disbursed Undisbursed

IBRD 1,333 0 1,333

* as of March 1, 2013.

Role of the Operation The deferred drawdown option (DDO) Development Policy Loan (DPL) is a fiscal buffer equivalento four months of budget deficit financing and debt rollover. The fiscal buffer was defined in the Government Public DebStrategy 2011–13 and in the Fiscal Budgetary Strategy 2012–14 and is in accordance with the Fiscal Compact ConvergenceProgram for 2013–2015. It serves to protect the economy against unforeseen shocks outside the Government’s control. It alsohelps Romania raise financing on international markets under its Medium-Term Notes program.

Selected Key Expected Development Results:

Public Financial ManagementEnhanced revenue collection with lower administrative costs and corruption

Tax revenue increases by €500 million in 2014

Tax administration costs are reduced to 1.05 percent of tax revenue in 2014 from 1.11 percent in 2011Implementation of the EU Fiscal Convergence Program

General Government budget deficit is below 3 percent of GDP in cash terms as of 2012

Governance reform of state-owned enterprises (SOEs)Improved SOE capacity to generate savings and attract capital

Extra revenue of €70 million from higher sales prices in renegotiated bilateral contracts and avoided loses of roughly €73million

Electricity prices for nonresidential consumers fully deregulated by end-2013 and beyond

Sales in the OPCOM Power Exchange and Transelectrica balancing generation account for a minimum 50 percent of Romania SOE generation in 2014

Fiscal sustainability in the health sector

Rationalize public health spending: Potential savings of €100 million by 2014 from revision of basic health servicespackage

Project contribution to the Country Partnership Strategy (CPS) outcome indicators: The project contributes to meeting Romania’s fiscal sustainability goals defined in the EU Fiscal Compact.Mitigation of social risks via energy subsidies and essential public health services for vulnerable households.

Donor coordination:Continuous dialogue between the Bank and other international financial institutions (IFIs), joint European Commission (EC)-

International Monetary Fund (IMF)-Bank quarterly assessments of the macro framework.

7/27/2019 Banca mondială - Date despre România

http://slidepdf.com/reader/full/banca-mondiala-date-despre-romania 14/37

13

ROMANIA: HEALTH SECTOR REFORM APL 2 PROJECT

Approved: December 16, 2004Effective: June 27, 2005Restructured: February 16, 2011(level 2) Closing: March 15, 2013(R)

Financing in M US Dollars:Financier Financing

IBRD Loan Government of Romania Co-financier: EIB

80 44.77 81.72

Total Project Cost 206.49

World Bank Disbursements, M US Dollars *:

Total Disbursed Undisbursed

IBRD 80 72 8

* as of March 1, 2013. Note: Disbursements may differ from financing due to exchange

rate fluctuations at the time of disbursement. The Health Sector Reform 2 project continues the support provided to the Romanian Government by the World Bank in timplementation of key elements of the program set out in 2000 through the first Health Sector Reform project, also addsupport for the rehabilitation of the maternity and neonatal care units.

Project Objective. The strategic purpose of this program was a healthy Romania, with lower morbidity and fewer prematudeaths, equitable access to health services, and an improved and more efficient health care system. The objectives of tproject were to: a) provide more accessible services of increased quality and improved health outcomes for those requirmaternity and newborn care and emergency medical care, and b) provide support for the preparation of a primary health castrategy.

Key Expected Results and Current Achievements:

Project interventions in the areas of mother and child care and emergency services were targeted at priority areas preventable morbidity and mortality and are expected to contribute to improving the status of various health conditions whRomania lags behind other new EU member countries.

In the area of mother and child care, the project supported the rehabilitation of selected maternity hospitals, tprocurement and delivery of medical equipment for the entire network of maternity clinics, as well as the training medical staff (both doctors and nurses) in order to improve the quality of services delivered. A new referral system wdeveloped, and its implementation is well under way. The maternal mortality rate decreased from 0.24 percent in 20040.14 percent in 2009, while the nationwide neonatal mortality rate has dropped from 2,068 deaths in 2004 to 1,044 deain 2011, which means a decrease of approximately 50 percent.

In the area of emergency health services, the project supported the establishment of: in-take emergency units aintensive care units in the emergency hospitals, as well as the improvement of communications for the integratemergency dispatch centers under the EU unique call number (112). As a result, the response time for emergency servic

decreased for all types of emergencies. The 24-hour death rate among the patients treated in the in-take rooms and thadmitted to the ICU also decreased from 5.78 to 4.16 in 2012, which is a decrease of 28 percent.

A project restructuring was completed in early 2011 to add technical assistance (TA) activities that sustain health secreforms, and the implementation of the National Strategy for Hospitals and Sanitary System Rationalization. The closing da was also extended. In February 2013, the Government requested a new extension of the closing date by nine months, unDecember 31, 2013. The main rationale is that additional time is needed for the completion of the financial impact assessmof the new health reforms. A partial three-month extension may be considered by the Bank. This will also allow a bridging current project implementation with the early preparatory stages of the new health project.

7/27/2019 Banca mondială - Date despre România

http://slidepdf.com/reader/full/banca-mondiala-date-despre-romania 15/37

14

ROMANIA: SOCIAL ASSISTANCE SYSTEM MODERNIZATION

Approved: May 26, 2011Effective: Expected by October 2011Closing: September 30, 2014 Financing in M US Dollars:

Financier Financing

IBRD LoanGovernment of RomaniaCo-financier:

710.400

Total Project Cost 710.4

World Bank Disbursements, M US Dollars: Total Disbursed Undisbursed

IBRD 710.4 192.2 447.8

* as of March 1, 2013.

Project Objective. The project aims to improve the overall performance of Romania’s social assistance system bystrengthening performance management, improving equity and administrative efficiency, and reducing error and fraud.

Key Expected Results and Current Achievements: The project aims to improve the performance of Romania’s social assistance system, with a focus on the Government’s mainprograms for low-income households, the disabled, and families with children. It is organized around four key results areaseach contributing to the project objective:

Strengthened performance management: Romania’s social assistance reform is implemented according to a results-oriented strategy and action plan and is supported by a performance management monitoring and evaluation (M&E)system;

Improved equity: The share of social assistance funds going to the first poorest quintile of the population will increase to45 percent from 37.7 percent at baseline (in 2009);

Improved administrative efficiency: Reduction in administrative and client costs for means-tested programs by 15 percenfrom baseline value; and

Reduced error and fraud: Programs for low-income households, disability benefits, and family policy programs have

strengthened information systems, oversight, and control procedures, including detection of error and fraud, using riskbased investigation, data matching, data quality audits, and consolidated beneficiary registries.

Important progress is being made with the reform and institutional development agenda . Six disbursement-linkedindicators (DLIs) in three results areas: Performance Management, Improved Equity, Reducing Error and Fraud were met(DLI 1: Action Plan; DLI 2: Monitoring Reports; DLI 4: Family Allowance benefits with harmonized means-testing and lowereligibility threshold; DLI 5: Child Raising Benefits using lower replacement income; DLI 13: thematic inspection of fourprograms; DLI 15: guaranteed minimum income paid through the National Agency for Social Benefits. The results from fivof these six DLIs have been sustained since disbursement in FY2012. The main Government priorities ahead are: (i) continueto move toward fewer programs with simpler and standardized application procedures; (ii) improve eligibility criteria formeans-tested programs to achieve both stronger targeting and higher coverage of the poor (e.g., by eliminating the list of assefilters that exclude genuinely poor households from means-tested programs); (iii) support the transition from assistance to work for the one-half million adults in the poorest quintile that benefit from cash assistance but do not work; (iv) promotehousehold investments in the human capital of their children; (v) expand the Social Assistance (SA) Management InformationSystem (MIS) to cover more programs and link to other databases; (vi) improve capacity to use the MIS for decision makingand (vi) increase Social Inspectorate capacity and authority to enforce action where fraud and corruption are found. Work hasbegun on these key elements that will underpin some of the more complex reform efforts, as well as on an accompanyingcommunications strategy. TA support is provided from the Social Inclusion Project. Estimated Disbursement in FY2013 is$100 million (under three DLIs).

Project contribution to the Country Partnership Strategy (CPS) outcome indicators. Although not envisaged in theCPS, the project is fully consistent with the objectives and pillars of the strategy. The project is directly linked to pillar 3,Social and Spatial Inclusion, and contributing to channeling a larger share of support to the poorest 20 percent.

7/27/2019 Banca mondială - Date despre România

http://slidepdf.com/reader/full/banca-mondiala-date-despre-romania 16/37

15

ROMANIA: SOCIAL INCLUSION PROJECT (SIP)

Approved: June 13, 2006Effective: March 17, 2007Restructured: Feb 16, 2011 (level 2); March 9, 2011 (level 1)Closing: June 30, 2014(R)Financing in M US Dollars:

Financier Financing IBRD Loan Government of Romania

58.5 15.9

Total Project Cost 74.4

World Bank Disbursements, M US Dollars *: Total Disbursed Undisbursed

IBRD 58.5 30 28.5

* as of March 1, 2013. Note: Disbursements may differ from financing due to exchange rate fluctuations at the time of disbursement.

Social inclusion and poverty reduction measures targeted at disadvantaged groups have long been aimed at contributing toRomania’s social cohesion and integration. Romania and the EC signed a Joint Inclusion Memorandum on June 20, 2005, aimed apreparing the country for full participation in the “open method of coordination” on social inclusion. The memorandumidentified as vulnerable social groups the Roma minority, children at high risk, persons with disabilities, youth over 18 leavingthe state child protection system, and victims of domestic violence.

Project Objective. The overall objective is to improve the living conditions and social inclusion of the most disadvantagedand vulnerable people in Romania by: (i) improving the living conditions and social inclusion of Roma from poor settlementsand (ii) strengthening the administration of social assistance benefits. Key Expected Results and Current Achievements:

42 percent reduction in the gap between targeted settlements and neighboring communities, measured by the living conditions index(target exceeded);

81 percent of poorest Roma settlements targeted by SIP now have access to improved infrastructure (e.g., water, roads) and basic livingconditions, compared with 10 percent before the project;

the increased participation of children from vulnerable groups in targeted communities to early childhood education; compliance with the quality of standards for social services for persons with disabilities; and

an increase in the employment rate for youth aged 18 and older from multifunctional centers.

The project is highly relevant in all respects and progressing. In 130 poor Roma settlements, the living conditions of 81percent of the population were improved as a result of 100 investment subprojects in community infrastructure (sanitation, water supply, roads, and electricity supply). An additional 33 subprojects are under implementation. The construction andrehabilitation of 27 kindergartens in 19 selected Roma communities has improved the access of Roma children to inclusiveearly childhood education, preparing them for school attendance. Persons with disabilities, youth at risk, and victims of domestic violence will benefit from better access to social services via 17 community centers of social interest that are underimplementation. The SIP was restructured in 2011 (reallocation of savings to support further improvement in community infrastructure in Roma settlements and other activities supporting the reforms of the cash benefits transfers) and its closing

date extended to March 2013. The new project subcomponent (3.4) supporting the TA activities for the Social AssistanceModernization Project (SASMP) and Development Policy Loan (DPL) program had a good take-off. The first phase of theupgrade of the National Agency for Social Benefits IT system (software and hardware) has been completed, and theselection of consulting services for several other activities are ongoing. The contracts for the development of a NationalData Base for the persons with disabilities and the SA Communication Campaign have been signed, while the draft contractfor the second phase of the SAFIR upgrade has recently been sent to the Bank for review. Given the time needed for thecompletion of subprojects under Components 1 and 3 and the completion of the TA activities supporting the SASMP, theGovernment requested and the Bank approved a new extension of the project closing date of 17 months, to June 30, 2014.

7/27/2019 Banca mondială - Date despre România

http://slidepdf.com/reader/full/banca-mondiala-date-despre-romania 17/37

16

ROMANIA: INTEGRATED NUTRIENT POLLUTION CONTROL PROJECT

Approved: October 30, 2007Effective: December 8, 2008 Closing: December 31, 2013 Financing in M EUR:

Financier Financing

IBRD Loan

Government of RomaniaBeneficiariesGEF Grant

50

1.15.15.0

Total Project Cost 61.2

World Bank Disbursements, M EUR *: Total Disbursed Undisbursed

IBRD 50 18.4 31.6

* as of March 1, 2013.

Romanian agriculture is dominated by individual and household farms that typically do not take into account environmental impacts Awareness is still low of potential alternatives to comply with the Nitrates Directive, which is required to qualify for farm subsidy paymentin Nitrate Vulnerable Zones (NVZ).Project Objective. The overall development objective of the project is to support the Government of Romania to meet the EU Nitrate

Directive requirements by reducing nutrient discharges into water bodies, promoting behavioral change at the community level, andstrengthening institutional and regulatory capacity. The Integrated Nutrient Pollution Control project cofinancing Global EnvironmenFacility (GEF) has the objective of reducing, over the long term, the discharge of nutrients into water bodies leading to the Danube Riveand Black Sea through integrated land and water management.

Key Expected Results and Current Achievements: The proposed interventions build on the successes of a pilot activity in Calarasi County, and help to implement priority actions identified inthe Black Sea-Danube Strategic Partnership Nutrient Reduction Investment Fund, the Danube River Strategic Action Plan, and the DanubeRiver Basin Pollution Reduction Program supported by the GEF. To date, significant on-the-ground implementation progress includes: (i) construction and delivery of 32 communal and 1,128 householdmanure platforms (in nine Training and Demonstration Sites (TDS) and 17 NVZ communes; (ii) purchase and delivery of 2,462 household waste segregation plastic bins; (iii) procurement and delivery of equipment for animal waste management (including 29 frontal loaders, 35tractors, 70 agricultural trailers, 29 vacuum tankers, and 29 manure spreaders); (iv) tree planting on 87.2 hectares in 10 communes; and (v)completion and delivery of the extension of the Voina Training Center. In addition, stemming from the recent project restructuring(November 2012), all nine planned commune wastewater investments have been contracted and are under construction, and a major public

awareness campaign, critical for helping Romania achieve the EU’s Nitrate Directive’s objectives, is under implementation, putting theproject on course for achieving its development objectives. To finalize all project activities and reach all its developmental objectives, theGovernment, due to insufficient space for needed budget allocation, has requested a 24-month extension of the closing date, currentlyunder consideration by the Bank. The project’s key outcomes include:

At least 80 percent of targeted NVZs showing a 10 percent reduction in nutrient discharge in water bodies.

Around 50 percent of the population in the project area adopting remedial measures to reduce nutrient discharges.

Improved inter-governmental coordination and capacity to assess, monitor, and report on progress with implementation of theEU Nitrates Directive.

The project will also test/demonstrate the feasibility of biogas/energy cogeneration from manure/organic household waste.

Project contribution to the CPS outcome indicators: The project is directly linked to Pillar 2, Growth and Competitivenessof CPS, through its support to EU convergence goals by means of more efficient agriculture, and to meeting EU climate

change targets.Donor coordination: The nitrates reduction investments were identified as an urgent priority by the Ministry ofEnvironment and Climate Change (MECC) and were highlighted in a Memorandum of Understanding between the PrimeMinister, the Ministry of Public Finance, and the Ministry of Environment and Forests (MEF) as a high priority for IBRDfunds. A GEF of US$5.5 million under the Danube Black Sea Strategic Partnership provides incremental support for nutriencontrol measures under the project.

7/27/2019 Banca mondială - Date despre România

http://slidepdf.com/reader/full/banca-mondiala-date-despre-romania 18/37

17

ROMANIA: COMPLEMENTING EU SUPPORT FOR AGRICULTURAL RESTRUCTURING PROJECT

Approved: November 27, 2007Effective: March 9, 2009Restructured: March 9, 2011 (level 2)Closing: June 30, 2013 Financing in M EUR:

Financier Financing

IBRD Loan

Government of Romania

43.4

3.7

Total Project Cost 47.1

World Bank Disbursements, M EUR *: Total Disbursed Undisbursed

IBRD 39 8.6 30.4

* as of March 1, 2013.

Note: Disbursements may differ from financing due to exchange rate fluctuations at the time of disbursement.

Project Objective. The objective of the Complementing EU Support for Agricultural Restructuring (CESAR) Project is tofacilitate market-based farm restructuring by enhancing the ability of farmers, farm family members, and farm workers to

manage their assets and income. Under this overarching objective, the CESAR project helps Romania to complete theproperty title registration of land assets in rural areas in order to improve the security of land property rights and reducetransaction costs on rural land markets. Equally important, the project assists the Romanian government in improving thedelivery of guidance services that enable the agricultural population to more sustainably manage its income and assets andthus contribute to the absorption of available national and EU support programs.

Key Expected Results and Current Achievements:

Project impact will be measured in terms of:

improved property rights security;

enhanced functioning of rural land markets;

more effective provision of socioeconomic guidance services to the agricultural population, enabling it to take informeddecisions about income opportunities and asset transfers and to access national and EU Common Agricultural Policy

(CAP) support programs.