bangko sentral ng pilipinas’ (bsp) - oecd.org rcgonzaga_oecd... · oecd-bsp asian seminar on...

TRANSCRIPT

OECD-BSP Asian Seminar on Financial Inclusion

11 September 2012 • Mactan, Cebu

Bangko Sentral ng

Pilipinas’ (BSP)

Financial Learning

Campaign (FLC)

Ruth C. Gonzaga

Department of Economic Statistics

2

Outline

1. Trends on global and overseas Filipino

remittances

2. BSP’s initiatives on advocacies for overseas

Filipinos and remittances

1

Trends on Global and Overseas Filipino Remittances

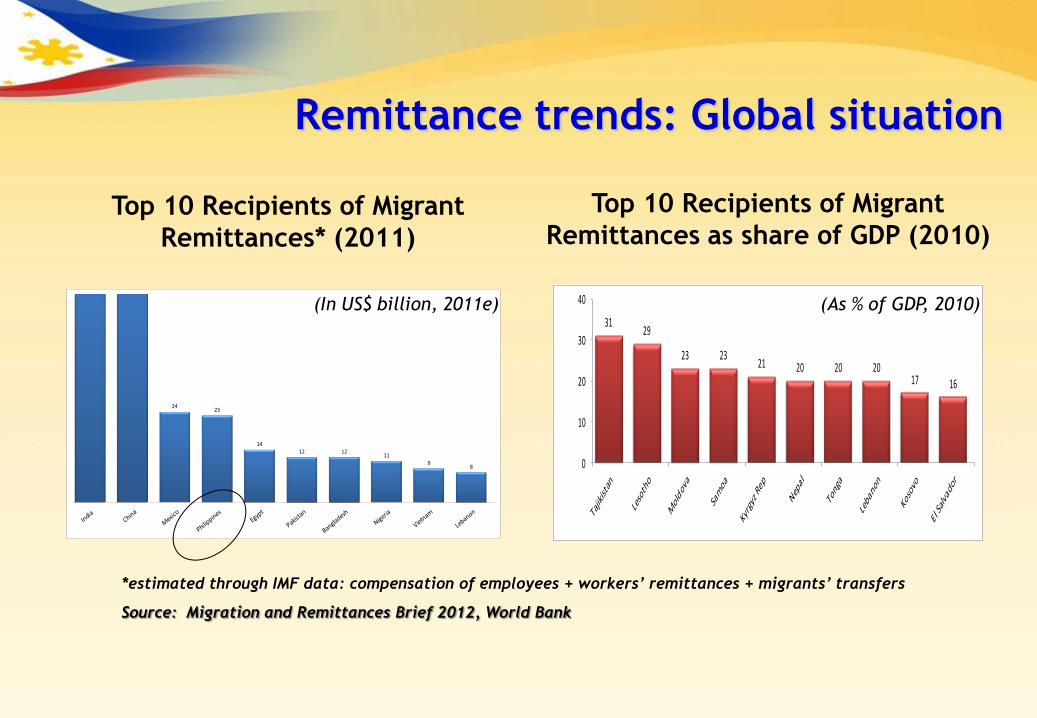

Remittance trends: Global situation

2423

1412 12

119

8

*estimated through IMF data: compensation of employees + workers’ remittances + migrants’ transfers

Source: Migration and Remittances Brief 2012, World Bank

Top 10 Recipients of Migrant

Remittances* (2011)

(In US$ billion, 2011e)

Top 10 Recipients of Migrant

Remittances as share of GDP (2010)

3129

23 2321 20 20 20

17 16

0

10

20

30

40 (As % of GDP, 2010)

Overseas Filipinos’ remittances provide cushion against external shocks

-30

-20

-10

0

10

20

30

40

0

5

10

15

20

25

80 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 J-Jun 11

J-Jun 12 p/

Remittances (RHS) Growth Rate (LHS)

Cash Remittances

1980 – June 2012 (in billion US$) Cash Remittances by source

Asia14%

Americas*53%

Oceania1%

Europe16%

Middle East15%

Africa0%

Others0%

Jan-Jun 2012

* Americas include Canada, USA, Commonwealth of

Northern Marianas Island, and Guam

Source: Bangko Sentral ng Pilipinas (BSP)

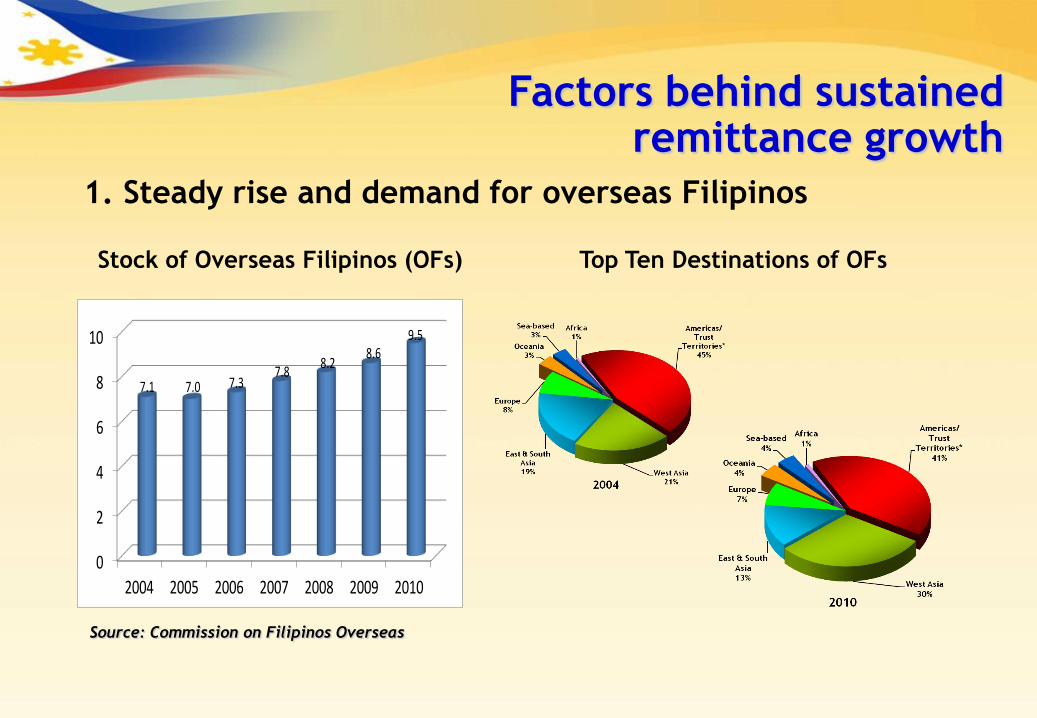

Factors behind sustained remittance growth

Source: Commission on Filipinos Overseas

0

2

4

6

8

10

2004 2005 2006 2007 2008 2009 2010

7.1 7.0 7.37.8

8.28.6

9.5

1. Steady rise and demand for overseas Filipinos

Stock of Overseas Filipinos (OFs) Top Ten Destinations of OFs

No. of Bank Branches, Correspondent

Banks, Remittance Centers and Tie-ups

with OF Remittances

-

1,000

2,000

3,000

4,000

5,000

2007 2008 2009 2010 2011 Mar-2012

1,183

3,015

4,192 4,581 4,723 4,732

Source: Bangko Sentral ng Pilipinas (BSP)

Factors behind sustained remittance growth

2. Expanded, more efficient and accessible financial services

Deposit-taking function (e.g.,

electronic banking)

Servicing of household bills (utilities,

communication)

Direct payment of housing loan

amortizations

Customized services to cover life

insurance, educ. plans, tuition fees

More efficient payments and

settlements system

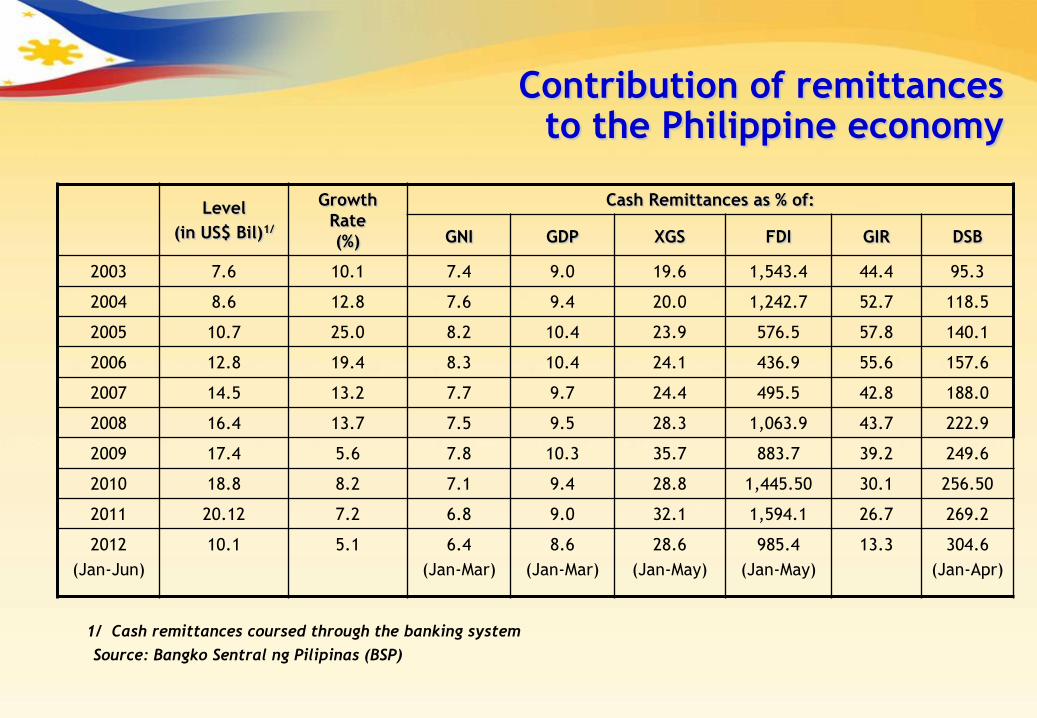

Contribution of remittances to the Philippine economy

Level

(in US$ Bil)1/

Growth

Rate

(%)

Cash Remittances as % of:

GNI GDP XGS FDI GIR DSB

2003 7.6 10.1 7.4 9.0 19.6 1,543.4 44.4 95.3

2004 8.6 12.8 7.6 9.4 20.0 1,242.7 52.7 118.5

2005 10.7 25.0 8.2 10.4 23.9 576.5 57.8 140.1

2006 12.8 19.4 8.3 10.4 24.1 436.9 55.6 157.6

2007 14.5 13.2 7.7 9.7 24.4 495.5 42.8 188.0

2008 16.4 13.7 7.5 9.5 28.3 1,063.9 43.7 222.9

2009 17.4 5.6 7.8 10.3 35.7 883.7 39.2 249.6

2010 18.8 8.2 7.1 9.4 28.8 1,445.50 30.1 256.50

2011 20.12 7.2 6.8 9.0 32.1 1,594.1 26.7 269.2

2012

(Jan-Jun)

10.1 5.1 6.4

(Jan-Mar)

8.6

(Jan-Mar)

28.6

(Jan-May)

985.4

(Jan-May)

13.3 304.6

(Jan-Apr)

1/ Cash remittances coursed through the banking system

Source: Bangko Sentral ng Pilipinas (BSP)

2

BSP Advocacies for Overseas Filipinos

Dual Planks

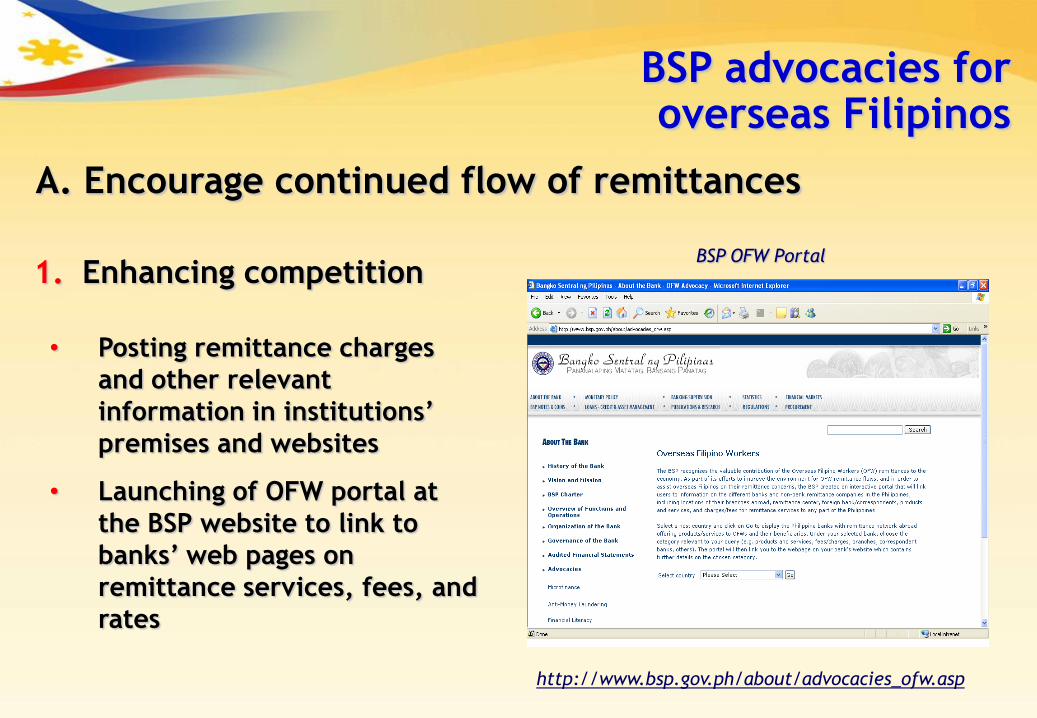

A. Encourage continued flow of remittances

B. Mobilize remittances to fund productive activities

A. Encourage continued flow of remittances

• Posting remittance charges

and other relevant

information in institutions’

premises and websites

• Launching of OFW portal at

the BSP website to link to

banks’ web pages on

remittance services, fees, and

rates

1. Enhancing competition

BSP OFW Portal

http://www.bsp.gov.ph/about/advocacies_ofw.asp

BSP advocacies for overseas Filipinos

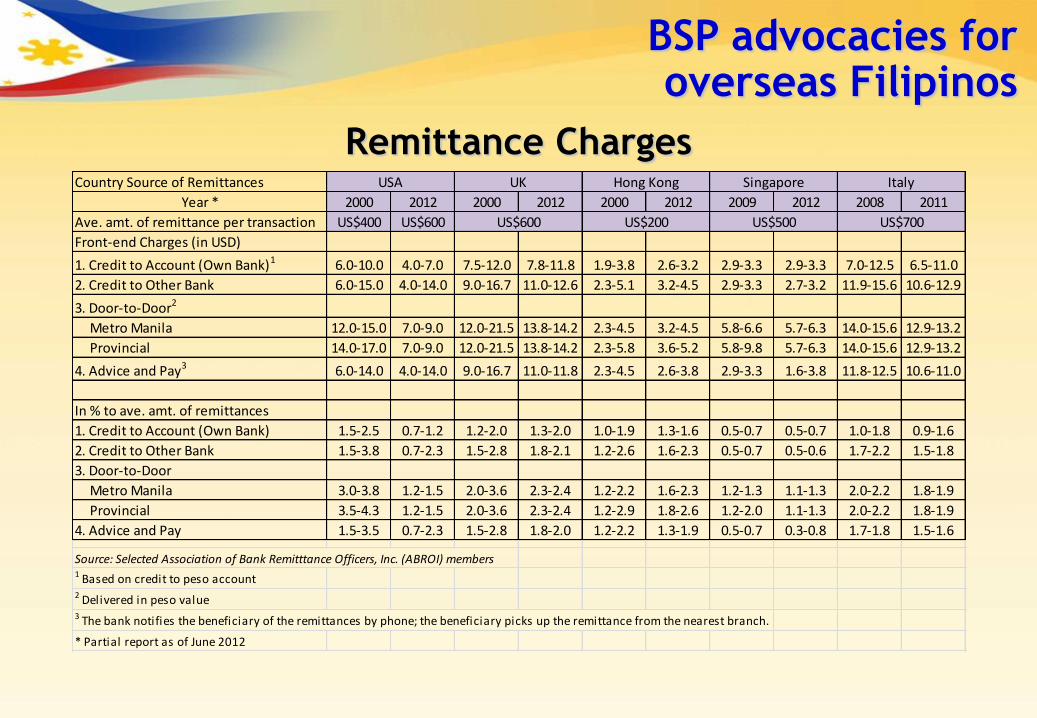

Remittance Charges

BSP advocacies for overseas Filipinos

Country Source of Remittances

Year * 2000 2012 2000 2012 2000 2012 2009 2012 2008 2011

Ave. amt. of remittance per transaction US$400 US$600

Front-end Charges (in USD)

1. Credit to Account (Own Bank)1 6.0-10.0 4.0-7.0 7.5-12.0 7.8-11.8 1.9-3.8 2.6-3.2 2.9-3.3 2.9-3.3 7.0-12.5 6.5-11.0

2. Credit to Other Bank 6.0-15.0 4.0-14.0 9.0-16.7 11.0-12.6 2.3-5.1 3.2-4.5 2.9-3.3 2.7-3.2 11.9-15.6 10.6-12.9

3. Door-to-Door2

Metro Manila 12.0-15.0 7.0-9.0 12.0-21.5 13.8-14.2 2.3-4.5 3.2-4.5 5.8-6.6 5.7-6.3 14.0-15.6 12.9-13.2

Provincial 14.0-17.0 7.0-9.0 12.0-21.5 13.8-14.2 2.3-5.8 3.6-5.2 5.8-9.8 5.7-6.3 14.0-15.6 12.9-13.2

4. Advice and Pay3 6.0-14.0 4.0-14.0 9.0-16.7 11.0-11.8 2.3-4.5 2.6-3.8 2.9-3.3 1.6-3.8 11.8-12.5 10.6-11.0

In % to ave. amt. of remittances

1. Credit to Account (Own Bank) 1.5-2.5 0.7-1.2 1.2-2.0 1.3-2.0 1.0-1.9 1.3-1.6 0.5-0.7 0.5-0.7 1.0-1.8 0.9-1.6

2. Credit to Other Bank 1.5-3.8 0.7-2.3 1.5-2.8 1.8-2.1 1.2-2.6 1.6-2.3 0.5-0.7 0.5-0.6 1.7-2.2 1.5-1.8

3. Door-to-Door

Metro Manila 3.0-3.8 1.2-1.5 2.0-3.6 2.3-2.4 1.2-2.2 1.6-2.3 1.2-1.3 1.1-1.3 2.0-2.2 1.8-1.9

Provincial 3.5-4.3 1.2-1.5 2.0-3.6 2.3-2.4 1.2-2.9 1.8-2.6 1.2-2.0 1.1-1.3 2.0-2.2 1.8-1.9

4. Advice and Pay 1.5-3.5 0.7-2.3 1.5-2.8 1.8-2.0 1.2-2.2 1.3-1.9 0.5-0.7 0.3-0.8 1.7-1.8 1.5-1.6

Source: Selected Association of Bank Remitttance Officers, Inc. (ABROI) members1 Based on credit to peso account2 Delivered in peso value3 The bank notifies the beneficiary of the remittances by phone; the beneficiary picks up the remittance from the nearest branch.

* Partial report as of June 2012

USA UK Hong Kong Singapore Italy

US$600 US$200 US$500 US$700

2. Improving channels of remittances

• Interconnection of ATM networks

• Grant of FCDU license to rural and cooperative banks

• Lower remittance fees charged by remittance

companies by 90% for credit-to-other bank transfers

through the BSP PhilPaSS

• Approval of new technologies in remittance transfers

(mobile phones, internet, cash cards)

BSP advocacies for overseas Filipinos

A. Encourage continued flow of remittances

1. Facilitating access to financial services/products

• Simplified regulations on acceptable IDs for financial

transactions to one valid ID issued by official authority

• Granted commercial banks authority to offer investment

products of OFs and their families (hedging instrument, long-

term bonds)

• Promoted market-based lending to micro, small and medium

enterprises (MSMEs)

BSP advocacies for overseas Filipinos

B. Mobilize remittances to fund productive activities

Dec-2004 Dec-2011 % Change Dec-2004 Dec-2011 % Change

Microfinance-

Oriented Banks 336 2,112 529 63,306 370,594 485

Regular Banks

with Microfinance

Operations 2,985 5,097 71 486,672 610,930 26

Total 3,321 7,209 117 549,978 981,524 78

Source: BSP

Amount (in million Php) No. of Borrowers

Microfinance loans and number of borrowers

Financial Learning Campaigns (FLCs)

Cultivate financial education among Overseas Filipinos

(OFs) and their beneficiaries

Promote savings and investments among OFs/

beneficiaries by informing them of alternative uses of

their remittances, including savings, investments in

financial products and business ventures

2. Raising the level of financial learning of Overseas Filipinos

and their families

BSP advocacies for overseas Filipinos

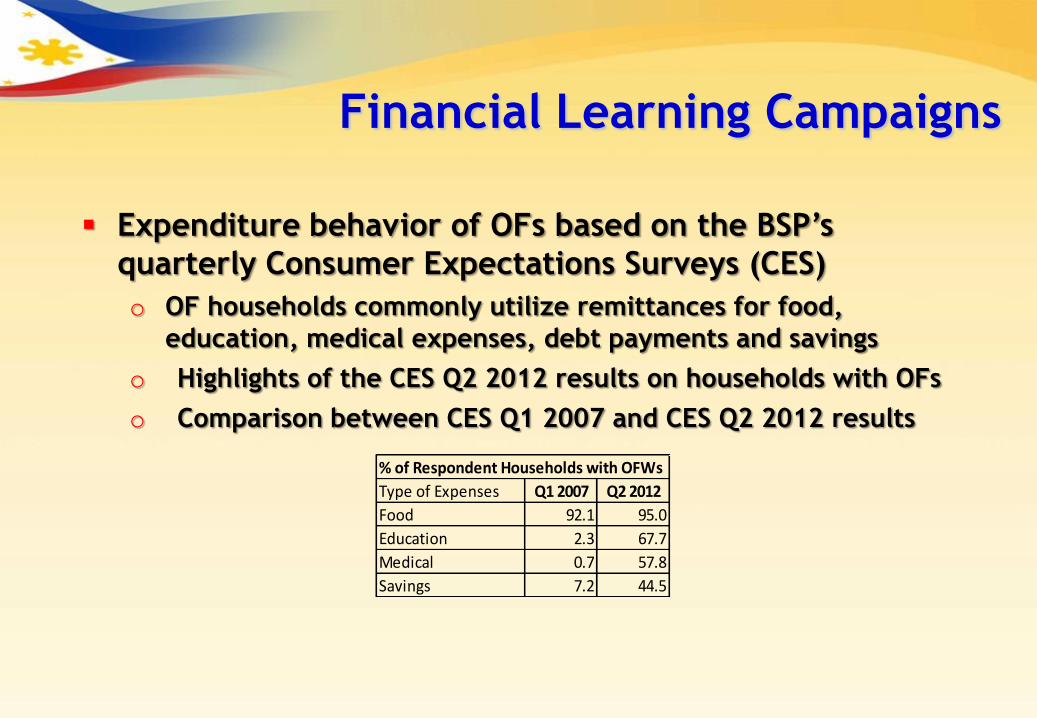

Financial Learning Campaigns

Expenditure behavior of OFs based on the BSP’s

quarterly Consumer Expectations Surveys (CES)

o OF households commonly utilize remittances for food,

education, medical expenses, debt payments and savings

o Highlights of the CES Q2 2012 results on households with OFs

o Comparison between CES Q1 2007 and CES Q2 2012 results

% of Respondent Households with OFWs

Type of Expenses Q1 2007 Q2 2012

Food 92.1 95.0

Education 2.3 67.7

Medical 0.7 57.8

Savings 7.2 44.5

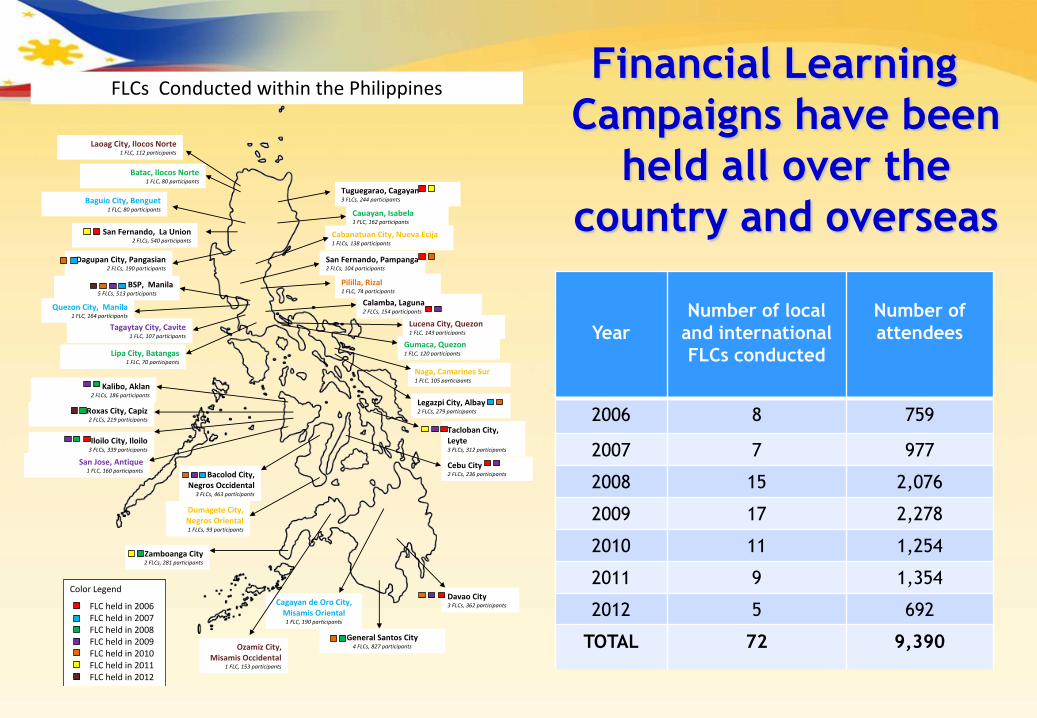

Financial Learning

Campaigns have been

held all over the

country and overseas

Year

Number of local

and international

FLCs conducted

Number of

attendees

2006 8 759

2007 7 977

2008 15 2,076

2009 17 2,278

2010 11 1,254

2011 9 1,354

2012 5 692

TOTAL 72 9,390

Cebu City 2 FLCs, 236 participants

Tuguegarao, Cagayan 3 FLCs, 244 participants

Cauayan, Isabela 1 FLC, 162 participants

Calamba, Laguna 2 FLCs, 154 participants

Gumaca, Quezon 1 FLC, 120 participants

Legazpi City, Albay 2 FLCs, 279 participants

Tacloban City, Leyte 3 FLCs, 312 participants

Davao City 3 FLCs, 362 participants

General Santos City 4 FLCs, 827 participants

Cagayan de Oro City, Misamis Oriental

1 FLC, 190 participants

Zamboanga City 2 FLCs, 281 participants

Bacolod City, Negros Occidental

3 FLCs, 463 participants

San Jose, Antique 1 FLC, 160 participants

Iloilo City, Iloilo 3 FLCs, 339 participants

Roxas City, Capiz 2 FLCs, 219 participants

Kalibo, Aklan 2 FLCs, 186 participants

Lipa City, Batangas 1 FLC, 70 participants

Tagaytay City, Cavite 1 FLC, 107 participants

Quezon City, Manila 1 FLC, 164 participants

BSP, Manila 5 FLCs, 513 participants

San Fernando, Pampanga 2 FLCs, 104 participants

Dagupan City, Pangasian 2 FLCs, 190 participants

San Fernando, La Union 2 FLCs, 540 participants

Baguio City, Benguet 1 FLC, 80 participants

Batac, Ilocos Norte 1 FLC, 80 participants

FLCs Conducted within the Philippines

Color Legend

FLC held in 2006 FLC held in 2007 FLC held in 2008 FLC held in 2009 FLC held in 2010 FLC held in 2011 FLC held in 2012

Pililla, Rizal 1 FLC, 74 participants

Laoag City, Ilocos Norte 1 FLC, 112 participants

Cabanatuan City, Nueva Ecija 1 FLCs, 138 participants

Lucena City, Quezon 1 FLC, 143 participants

Naga, Camarines Sur 1 FLC, 105 participants

Dumagete City, Negros Oriental 1 FLCs, 93 participants

Ozamiz City, Misamis Occidental

1 FLC, 153 participants